seafood exchange united states - global aquaculture … · industry association. ... protein...

TRANSCRIPT

1

Travis Larkin Seafood Exchange United States Travis Larkin is president of Seafood Exchange, a seafood-importing and wholesale company based in Raleigh, North Carolina USA. Previously, he handled shrimp procurement for Darden Restaurants until 1997. Larkin is actively involved in GAA and the National Fisheries Institute, where he currently serves as chairman of its Nominating Committee and previously served on its Executive Committee. He also served as president of the National Shrimp Industry Association.

Closing Remarks Travis Larkin

President, Seafood Exchange Raleigh, North Carolina, USA

GOAL 2013 “Join the Journey”

What have we learned on our journey together this week?

First, that this is a beautiful city

4

Five Major Challenges (+1)

1. Health and Disease Management

2. Feeds

3. Environmental/Social Accountability

4. Investment Capital

5. Market Support

6. Leadership

Examples of Leadership in Our Community

• Responsible Aquaculture Foundation – Initially focused on Africa

• Education • Training • Support

• Seafood Industry Research Foundation (SIRF)

• Seafood Nutrition Partnership

6

Seafood is Essential Nutrition Solution

Ea#ng 8 oz. of seafood a week reduces the risk of dying from

heart disease by

36%

Moms-‐to-‐be that eat 8 to 12 oz. of seafood a week

have

be'er outcome for baby brain and

eye health

Older adults who had the highest

blood levels of the faAy acids found in

fish lived, on average

2.2 years longer

Source: JAMA Source: JAND Source: Annals of Internal Medicine

7

Projected seafood consumption by source through 2050

8

-

20

40

60

80

100

120

140

160

180 19

50

1953

19

56

1959

19

62

1965

19

68

1971

19

74

1977

19

80

1983

19

86

1989

19

92

1995

19

98

2001

20

04

2007

20

10

2013

20

16

2019

20

22

2025

20

28

2031

20

34

2037

20

40

2043

20

46

2049

MM

T

Source: FAO, HighQuest Analysis

Wild Catch Aquaculture

HQP estimate based on linear growth rate (1980-2011) of production for wild catch(1.0%) and aquaculture(8.1%): • 2013 - 2021 at historical growth rate • 2022 - 2031 at 75% of historical growth rate • 2032 - 2041 at 50% of historical growth rate • 2042 - 2050 at 25% of historical growth rate

Insights from Ole-Eirik Lerøy

• By 2030: Additional 40 million MT of aquatic food needed

• We have a great story to tell! – Time for transparency and a straight telling of

our story…Remember doctors and “internet patients.”

– Blue is the new green!

9

World Shrimp Aquaculture by Species: 1991-2015 EMS takes a bite out of supply

0.0

0.6

1.2

1.8

2.4

3.0

3.6

4.2

Million MT

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

P. vannamei P. monodon M. rosenbergii Other

12%

59%

67% 65%

71%

Percentages indicate the share of P. vannamei.

16%

72%

45%

76%

Sources: FAO (2013) for 1991-2011; GOAL (2013) for 2012-2015.

U.S. Shrimp Imports Down Over 15% Since 2011

0

80

160

240

320

400

480

560

640

1997 1999 2001 2003 2005 2007 2009 2011 2013*

Thou

sand

MT

Other

Honduras

Malaysia

Mexico

China

Vietnam

India

Indonesia

Ecuador

Thailand

Source: USDC/NMFS (2013) * Estimate

After peaking in 2010 at 203,000 tons, imports from Thailand declined in 2011 and 2012

and are expected to fall even further in 2013 to around 90,000 tons. Ecuador, Indonesia,

and India are picking up some of the slack. Imports from Mexico have also fallen.

Spanish Shrimp Imports Down 22% since 2011 First a weak economy, now high prices

0

20

40

60

80

100

120

140

160

180

200

1997 1999 2001 2003 2005 2007 2009 2011 2013*

Thou

sand

MT

Others India Honduras Morocco Senegal Thailand Nicaragua China Ecuador Argentina

Source: Eurostat (2013) * Estimate

Reflecting the difficult economic conditions in the country, the Spanish market

contracted substantially in 2012 and is expected to contract even further in 2013 (-20%

relative to 2011). Argentina and Ecuador currently supply around 50% of the market.

Prices Rising Sharply P. monodon vs. P. vannamei (U.S. Wholesale)

Source: Urner Barry (2013)

(2.00)

(1.00)

-‐

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Jan-‐99 Jan-‐00 Jan-‐01 Jan-‐02 Jan-‐03 Jan-‐04 Jan-‐05 Jan-‐06 Jan-‐07 Jan-‐08 Jan-‐09 Jan-‐10 Jan-‐11 Jan-‐12 Jan-‐13

USD/

lb

Farmed, Ecuador White, 26-‐30 Farmed, SE Asian Tiger, 26-‐30 Premium (White minus Tiger)

Wholesale shrimp prices have been rising since 2010 but increased sharply during 2013, reflecting the reduced

availability of imported shrimp in the U.S. market as a result of EMS/AHPNS.

Diseases***Production costs - Feed/Fishmeal

Access to disease-free broodstock***International market prices

Seed stock quality & availabilityProduction costs - Others

Environmental managementFeed quality and availability

Product quality controlProduction costs - Fuel

Access to CreditBanned chemicals / antibiotic use

***International trade barriersMarket coordination

InfrastructureConflicts with other users

Public Relations Management

Not Important Extremely Important

Moderately Important

GOAL 2013 Survey Issues & Challenges in Shrimp Aquaculture

All Countries

Asterisk indicates a Top 3 issue in GOAL 2007 Survey

EMS: “It’s Complicated” - Robins McIntosh

A Perfect Killer??? • It grows extremely fast (competitive). • It is a colonizer (very sticky). • It produces a potent toxin. • Quorum Sensing (coordination of activity).

15

Market Impacts of EMS

1. Trade flow shift from West to East (China a key new net importer)

2. Demand contraction to accelerate in the west

3. Lack of quality information available to the public

16

Thailand's Recovery Scenarios

17

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2010 2011 2012 2013 2014 2015 2016 2017 2018

U recovery

PessimisOc scenario

V recovery

Aquaculture Fish

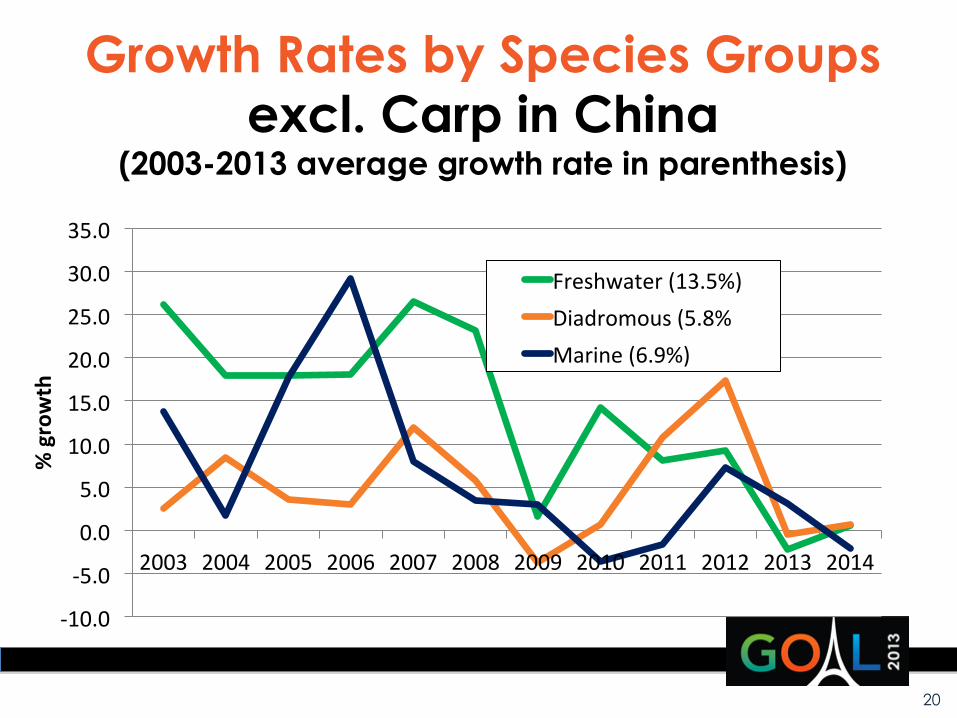

• Production expected stable or down for 2013 and 2014

• Double in a decade? Yes for some species from 2003 to 2013, but slower growth rates now

• Growth trend declining in general

18

Production of Surveyed Species Excl. Carp in China 2002-2014

2.1 2.6 3.1 3.7 4.3 5.5 6.8 6.9 7.8 8.5 9.3 9.1 9.1

1.7 1.7 1.9 1.9 2.0

2.2 2.4 2.3

2.3 2.5

3.0 3.0 3.0

0.2 0.2 0.2

0.3 0.4

0.4 0.4 0.4

0.4 0.4

0.4 0.5 0.4

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill. M

etric

Ton

s

Marine Diadromous Freshwater

19

Growth Rates by Species Groups excl. Carp in China

(2003-2013 average growth rate in parenthesis)

-‐10.0

-‐5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% growth

Freshwater (13.5%) Diadromous (5.8% Marine (6.9%)

20

New Opportunities: Arabian Peninsula

• Ample coastline and superb waters, governments beginning to offer support

• Opportunities for partners with technical expertise and capital to invest

• Jim Greenberg: “Don’t lump all these countries together.”

21

New Opportunities: Africa • Positives: Favorable conditions, thousands of km of

coastline, growing domestic markets

• Constraints: Limited growth capital and lack of political will/systematic approach for aquaculture

• Intl. Finance Corp: Looking for sponsors with “deep experience and strong track record”

22

Feed Sustainability: Where to get protein for feed?

• 70-80% of global supplies of fish meal and fish oil currently used in aqua feeds

• Alternatives to fish protein needed: Soy protein forecast to supply one-half of global aqua feed requirements by 2020

23

Emerging Protein Sources… Time to Get Creative!

Algae

Krill

Insects

2

3

2

4

3

Fish Meal Challenge: Standards Example (from Sustainable Fisheries Partnership):

• Standards established in western countries to suit known production systems may not work elsewhere.

• Asia is the engine room of world aquaculture

production with a huge demand for fish meal. It needs systems that work there.

25

Tropical Asian purse seine catch: 40+ species, including benthic species lured by FADs and/or lights (not all species may go to fish meal). Trawl is even more diverse.

Purse seine catch in Panama

Standards Challenges (cont.) • In this case traceability is very difficult—if not

impossible—and further complicated by species diversity.

• Solution: – Accept that “one size does not fit all” in

standards development. – Diverse stakeholders must work together for

improvements that work for that producer community.

27

Wrapping Up: Today’s Issues

• Carl-Christian Schmidt: “Green Growth and Implications for Fisheries and Aquaculture”

• Health and Nutrition: Seafood Nutrition Partnership

• Retail and Foodservice Panels

28

Health and Nutrition: Addressing Public Health Crisis through Public-Private Partnerships

Seafood Industry

Healthcare Industry

Nonprofits & Foundations

Gov’t Agencies

Corporations Media

Local Communities

29

Doubling Consumption: Seafood Nutrition Partnership

Year 2

A. Provide Seafood Nutrition Education. Strategy: Partner w/ Health Influencers

B. Shape the American Palate. Strategy: Partner w/ Tastemakers

C. Inspire a Healthier America

Feb. Heart Health Month

Feb. Heart Health Month

30

Year 3 Year 1

Feb. Heart Health Month

30

In Summary: We have work to do

1. Health and Disease Management

2. Feeds

3. Environmental/Social Accountability

4. Investment Capital

5. Market Support

6. Leadership

See you in Vietnam for GOAL 2014!

32