seac fall meeting - southeastern actuaries conference · seac fall meeting © 2007 towers perrin 2...

TRANSCRIPT

November 15, 2007

Noel Harewood

© 2007 Towers Perrin

US GAAP Update – What’s New

SEAC Fall Meeting

© 2007 Towers Perrin 2

US GAAP for insurers is changing….

GAAP ClassicIncome statement focusComparability and consistency valued highly

New GAAPBalance sheet focusComparability and consistency decline in significance

© 2007 Towers Perrin 3

So what’s new?

SOP 05-1 – Internal Replacements

SFAS 157 – Fair Value Measurement

SFAS 159 – Fair Value Option

© 2007 Towers Perrin 4

SOP 05-1

Addresses accounting for internal replacementsInternal replacements defined as “modification in product benefits, features, rights or coverages”If contract modifications affect integrated features and the contract is substantially changed— existing DAC is written off— new DAC is set up for the replacement policyIf contract is substantially unchanged, then existing DAC is continued

© 2007 Towers Perrin 5

What is an integrated feature?

Benefit that can ONLY be determined in conjunction with the base policy

E.g., GMxB

Non-integrated features do not affect the base contract directly

E.g., term rider on annuitiesNon-integrated features do not affect the accounting for the base contract

© 2007 Towers Perrin 6

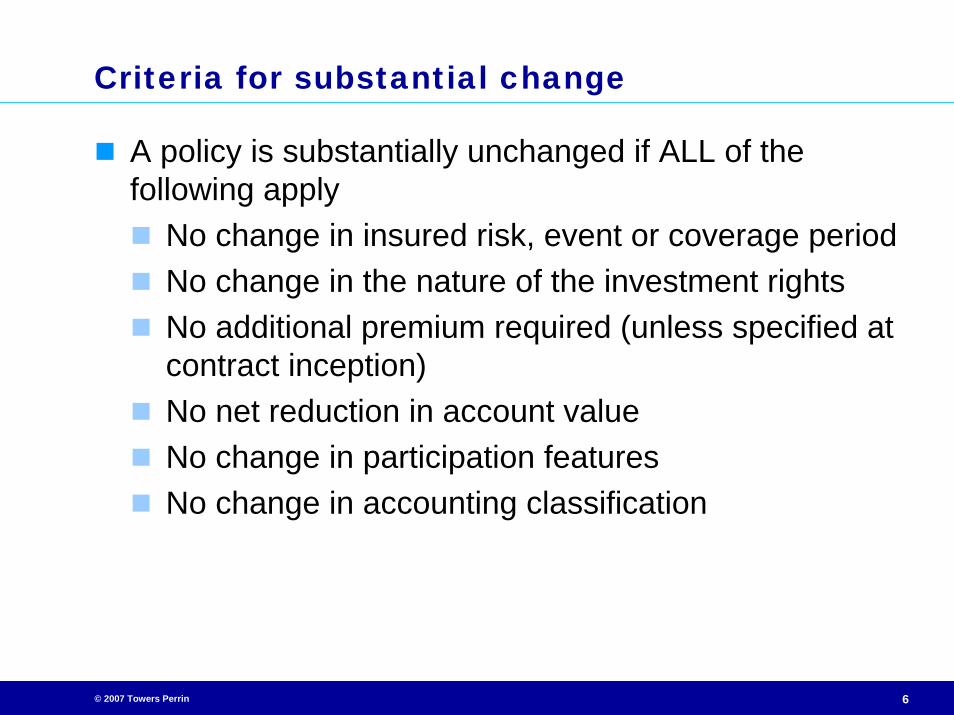

Criteria for substantial change

A policy is substantially unchanged if ALL of the following apply

No change in insured risk, event or coverage periodNo change in the nature of the investment rightsNo additional premium required (unless specified at contract inception)No net reduction in account valueNo change in participation featuresNo change in accounting classification

© 2007 Towers Perrin 7

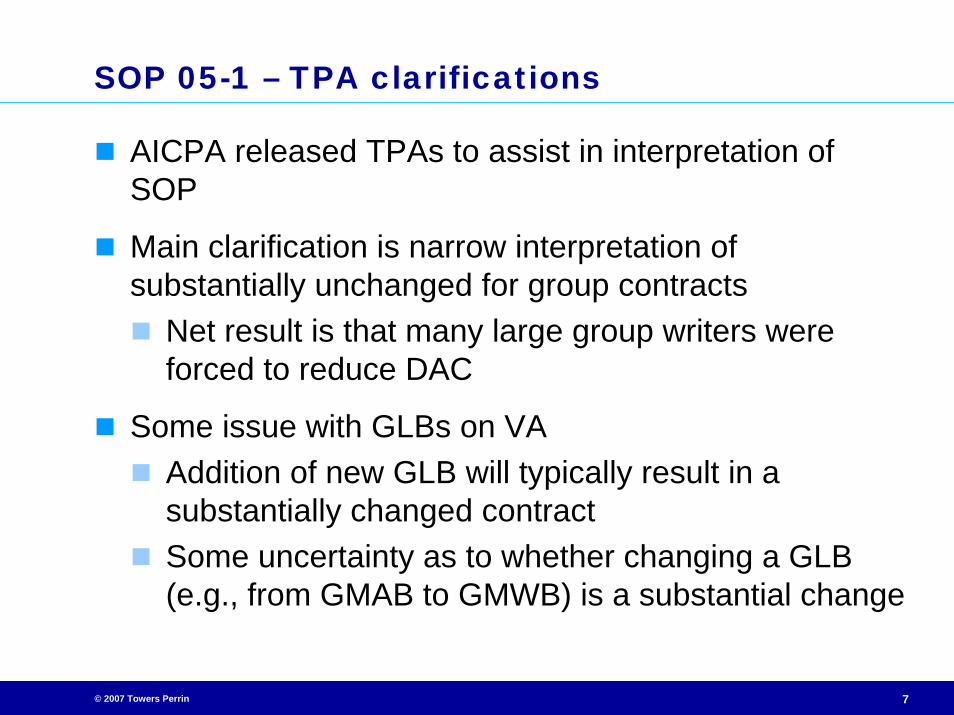

SOP 05-1 – TPA clarifications

AICPA released TPAs to assist in interpretation of SOP

Main clarification is narrow interpretation of substantially unchanged for group contracts

Net result is that many large group writers were forced to reduce DAC

Some issue with GLBs on VAAddition of new GLB will typically result in a substantially changed contractSome uncertainty as to whether changing a GLB (e.g., from GMAB to GMWB) is a substantial change

© 2007 Towers Perrin 8

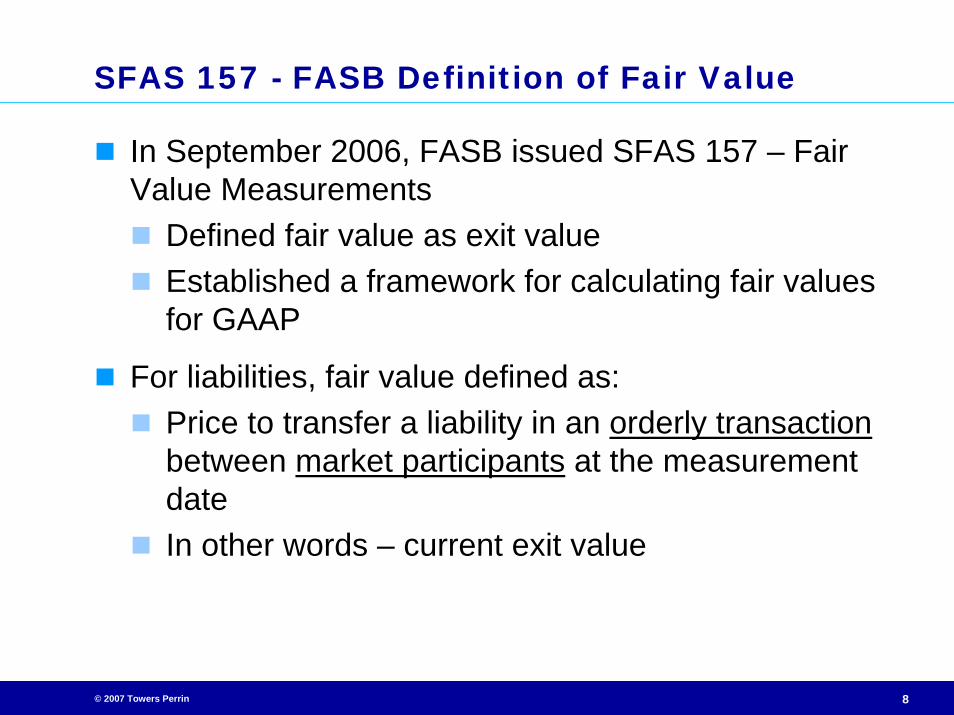

SFAS 157 - FASB Definition of Fair Value

In September 2006, FASB issued SFAS 157 – Fair Value Measurements

Defined fair value as exit valueEstablished a framework for calculating fair values for GAAP

For liabilities, fair value defined as:Price to transfer a liability in an orderly transactionbetween market participants at the measurement dateIn other words – current exit value

© 2007 Towers Perrin 9

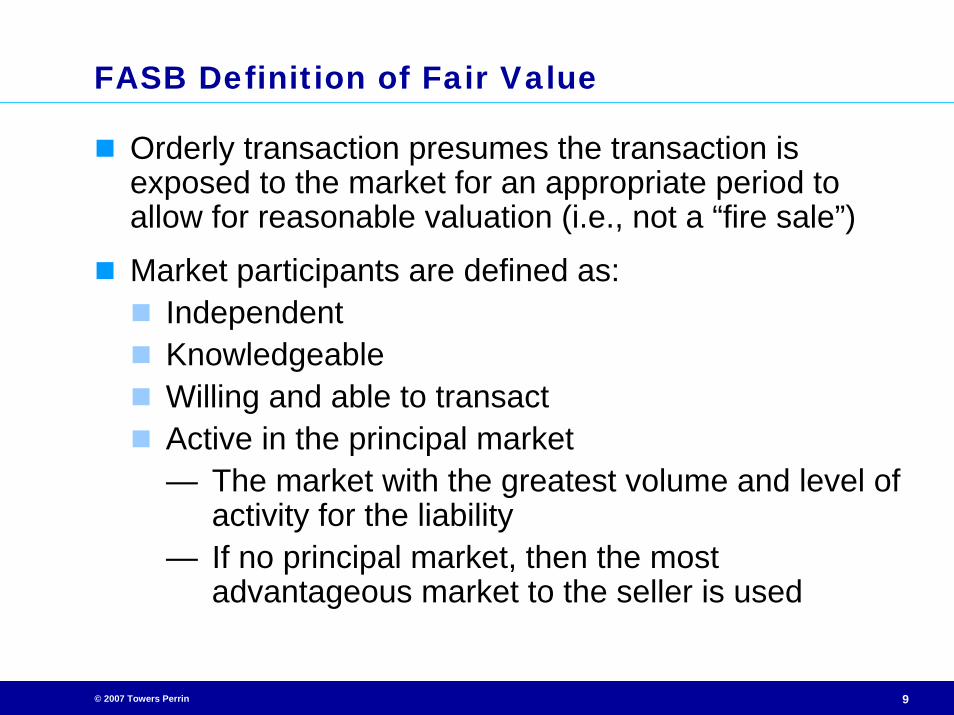

FASB Definition of Fair Value

Orderly transaction presumes the transaction is exposed to the market for an appropriate period to allow for reasonable valuation (i.e., not a “fire sale”)

Market participants are defined as:IndependentKnowledgeableWilling and able to transactActive in the principal market— The market with the greatest volume and level of

activity for the liability— If no principal market, then the most

advantageous market to the seller is used

© 2007 Towers Perrin 10

Fair Value and Convergence

IFRS Phase 2 on insurance accounting requires fair value

Largely similar to SFAS 157 (current exit value)

Solvency II (European capital standard) also based on similar concepts

Norwalk Agreement and others indicate convergence in accounting between North America and Europe is coming

SEC pressure to “speed up” conversion

Fair values likely here to stay

© 2007 Towers Perrin 11

Valuation Techniques

SFAS 157 describes three applicable valuation techniques for calculating fair values

Market approachUses market prices and other relevant market information

Income approachUses discounted cash flows

Cost approachUses current replacement cost

Currently, expectation is that insurance liabilities will be valued using Income approach

© 2007 Towers Perrin 12

Applying the Income Approach

Projected cash flows

Time value of money

Allowance for risk

IFRS Phase 2 Building Blocks

© 2007 Towers Perrin 13

Projected cash flows

Underlying assumptionsShould be “consistent with market”Should consider all available information— Possible to use information outside standard

actuarial sourcesBest estimate?Prudence in assumptions?

Practical considerations indicate continued use of company experience studies for mortality, persistency

Expense assumptions an important consideration

© 2007 Towers Perrin 14

Time value of money

Reflecting the time value of money central to fair value concept

FASB defines US risk-free rate as based on treasury rates

Note that this is not prescribed for other currenciesSome areas (e.g., Europe) show preference for swap curve

© 2007 Towers Perrin 15

Allowance for risk

Under traditional methods (e.g., actuarial appraisals), risk is reflected through an addition to the discount rate

Addition may be based on application of CAPM— Financial theory suggests that this approach may

be overly simplistic

Under financial economics, cash flows adjusted for correlation with market

Risk-adjusted cash flows then discounted at risk-free rates

Overall intent is to reflect “market” compensation for bearing risk

Theory may suggest that only undiversifiable risk requires compensation

© 2007 Towers Perrin 16

Alternative Approaches

Direct MethodCalculate fair value directly by discounting policyholder cash flows

Indirect MethodCalculate fair value of shareholder cash flows (embedded value)Fair value of liabilities is difference between fair value of assets and embedded value

IFRS appears to favor Direct Method explicitly

Girard (2000) and others have shown equivalence of these two approaches

© 2007 Towers Perrin 17

Some technical issues to consider

Risk margins

Allowance for nonperformance

Treatment of options and guarantees

© 2007 Towers Perrin 18

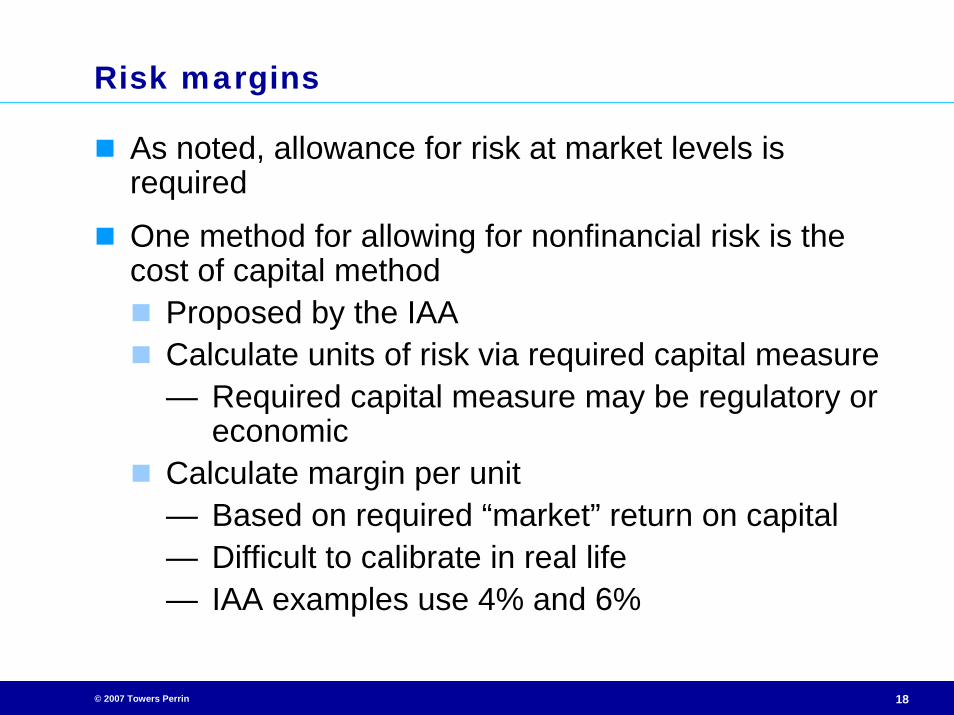

Risk margins

As noted, allowance for risk at market levels is required

One method for allowing for nonfinancial risk is the cost of capital method

Proposed by the IAACalculate units of risk via required capital measure— Required capital measure may be regulatory or

economicCalculate margin per unit— Based on required “market” return on capital— Difficult to calibrate in real life— IAA examples use 4% and 6%

© 2007 Towers Perrin 19

Allowance for nonperformance risk

Nonperformance risk widely held to mean own-credit risk

Requirement is to reflect own-credit risk in liabilityEvaluation of credit risk for company’s specific rating classEvaluation of credit risk within classWill lead to a lower liability

Alternative view is that insurance liabilities are over-collateralized

Implies a higher rating than general debt

© 2007 Towers Perrin 20

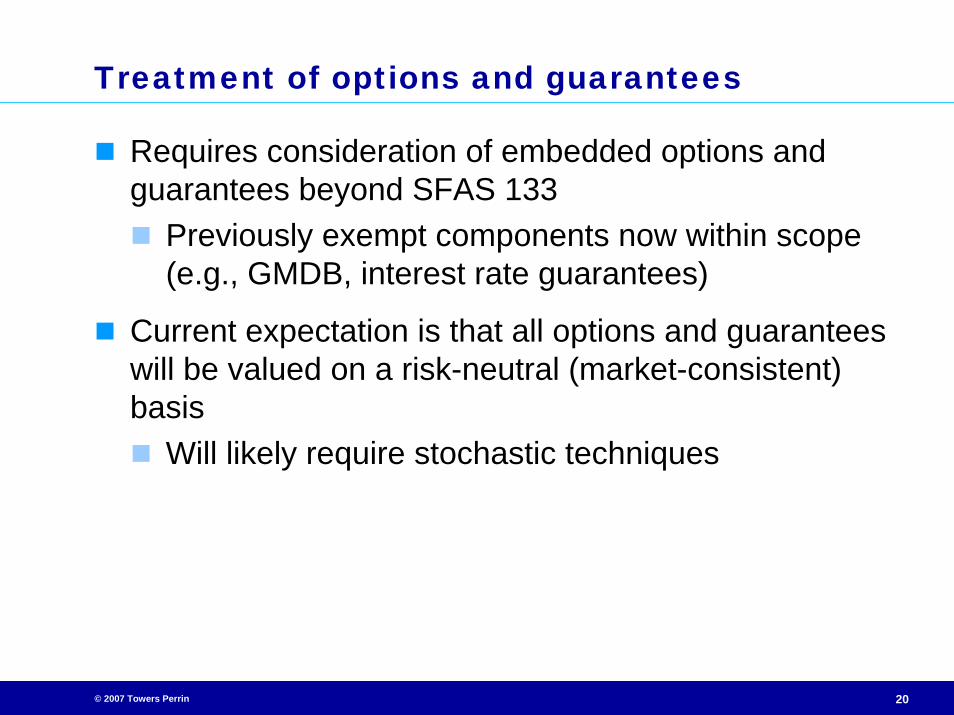

Treatment of options and guarantees

Requires consideration of embedded options and guarantees beyond SFAS 133

Previously exempt components now within scope (e.g., GMDB, interest rate guarantees)

Current expectation is that all options and guarantees will be valued on a risk-neutral (market-consistent) basis

Will likely require stochastic techniques

© 2007 Towers Perrin 21

What does it mean for reporting entities?

Required determinationsUnit of account (most likely block)Principal market— M&A vs Reinsurance vs Capital MarketsValuation technique— Direct vs. IndirectLevel of inputs (for disclosures)— Insurance inputs almost certainly Level 3

© 2007 Towers Perrin 22

SFAS 159 – Fair Value Option

Permits entities to choose to measure most financial instruments at fair value

Optional only, no requirement to change accounting

Establishes disclosure requirements for reporting these fair values in financial statements

© 2007 Towers Perrin 23

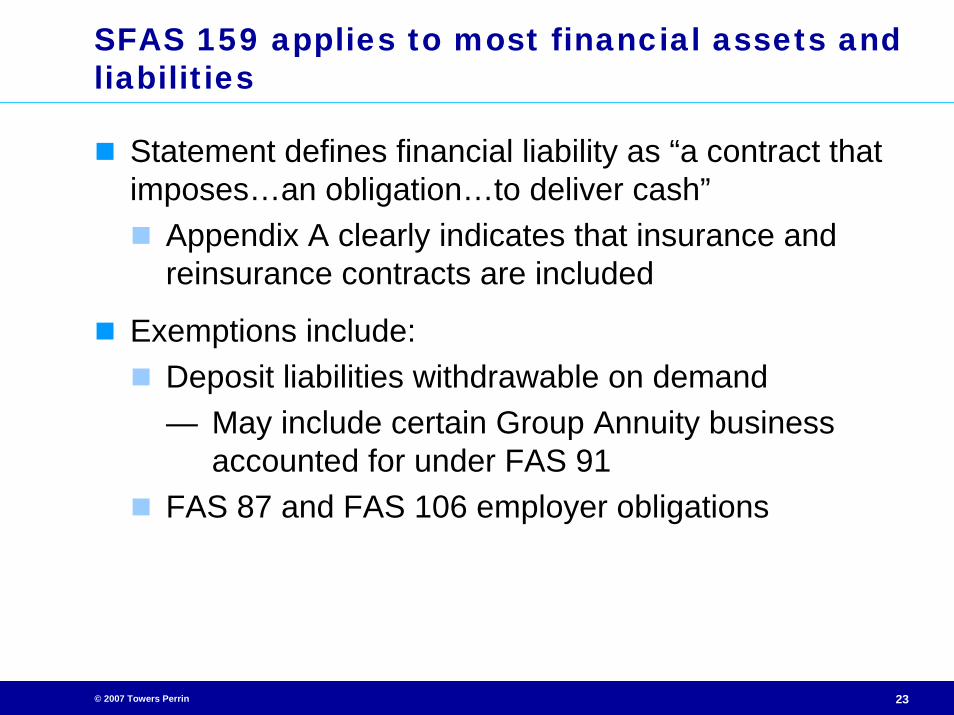

SFAS 159 applies to most financial assets and liabilities

Statement defines financial liability as “a contract that imposes…an obligation…to deliver cash”

Appendix A clearly indicates that insurance and reinsurance contracts are included

Exemptions include:Deposit liabilities withdrawable on demand— May include certain Group Annuity business

accounted for under FAS 91FAS 87 and FAS 106 employer obligations

© 2007 Towers Perrin 24

There is a fair amount of flexibility…

Election is made on a contract-by-contract basisElection will be made on acquisitionElection is irrevocable (except for remeasurementevents, e.g. purchase)One-time opportunity at effective date to revalue inforce business

© 2007 Towers Perrin 25

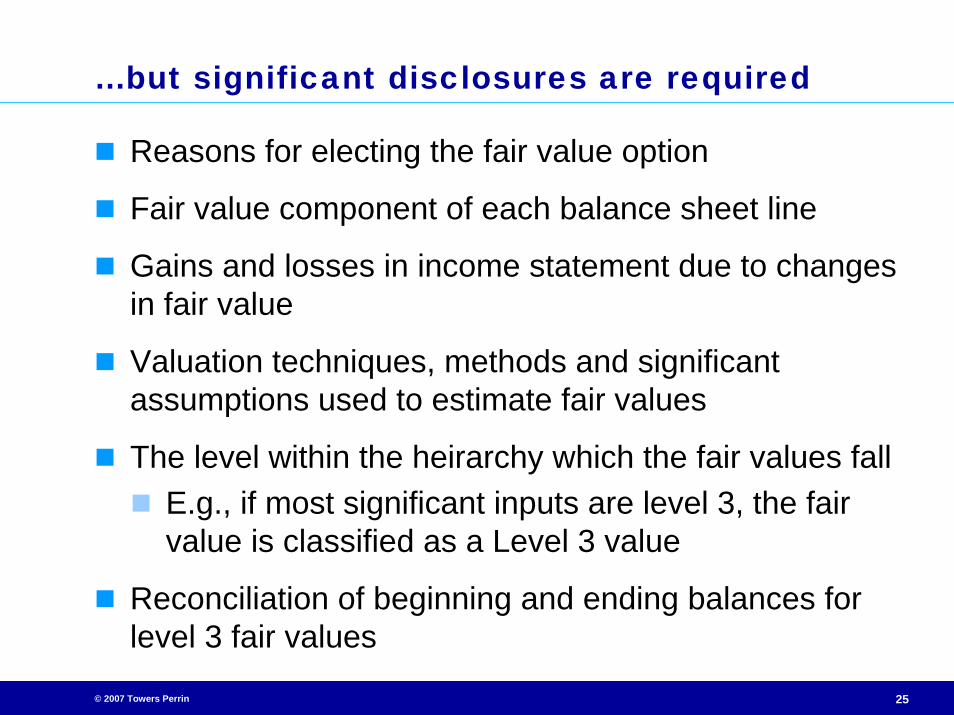

…but significant disclosures are required

Reasons for electing the fair value option

Fair value component of each balance sheet line

Gains and losses in income statement due to changes in fair value

Valuation techniques, methods and significant assumptions used to estimate fair values

The level within the heirarchy which the fair values fallE.g., if most significant inputs are level 3, the fair value is classified as a Level 3 value

Reconciliation of beginning and ending balances for level 3 fair values

© 2007 Towers Perrin 26

Pricing Considerations

What GAAP measures are in use?GAAP profit marginGAAP ROE — both single measure and emergencePV of GAAP profits

Often used as a supplement to statutory pricing

© 2007 Towers Perrin 27

Pricing Considerations

How will these measures look in a Fair Value context?Gain/loss at issueViability of ROE

Analysis of movement in equity will become more meaningful

Similar to embedded value analysis, with focus on VNB-type figure