scotia private poolstm 2012dr.scotiabank.com/ca/en/files/12/11/scotia_private_pools_-_en.pdf ·...

TRANSCRIPT

Scotia Private PoolsTM 2012(formerly The Pinnacle Funds)

Simplified ProspectusNovember 19, 2012Pinnacle Series (formerly Class A) and Series F units (unless otherwise noted) and Series I and Series M(formerly Manager Class) units where noted.

Money Market FundsScotia Private Short Term Income Pool

Bond FundsScotia Private Income Pool (Series I units available)Scotia Private High Yield Income Pool (Series I and Series M units available)Scotia Private American Core-Plus Bond Pool (Series I units available)

Balanced FundScotia Private Strategic Balanced Pool

Canadian Equity FundsScotia Private Canadian Value Pool (Series I units available)Scotia Private Canadian Mid Cap Pool (Series I units available)Scotia Private Canadian Growth Pool (Series I units available)Scotia Private Canadian Small Cap Pool (Series I units available)

Foreign Equity FundsScotia Private U.S. Value Pool (Series I units available)Scotia Private U.S. Large Cap Growth Pool (Series I units available)Scotia Private U.S. Mid Cap Value Pool (Series I and Series M units available)Scotia Private U.S. Mid Cap Growth Pool (Series I and Series M units available)Scotia Private International Equity Pool (Series I units available)Scotia Private International Small to Mid Cap Value Pool (Series I units available)Scotia Private Emerging Markets Pool (Series I and Series M units available)Scotia Private Global Equity Pool (Series I units available)Scotia Private Global Real Estate Pool (Series I units available)

No securities regulatory authority has expressed an opinion about these units. It is an offence to claim otherwise.

The Funds and the units they offer under this simplified prospectus are not registered with the U.S. Securities and ExchangeCommission. Units of the Funds may be offered and sold in the United States only in reliance on exemptions fromregistration.

Table of Contents

INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

FUND SPECIFIC INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

ABOUT THE FUND DESCRIPTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Scotia Private Short Term Income Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

Scotia Private Income Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12

Scotia Private High Yield Income Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

Scotia Private American Core-Plus Bond Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

Scotia Private Strategic Balanced Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

Scotia Private Canadian Value Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

Scotia Private Canadian Mid Cap Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

Scotia Private Canadian Growth Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

Scotia Private Canadian Small Cap Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

Scotia Private U.S. Value Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Scotia Private U.S. Large Cap Growth Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

Scotia Private U.S. Mid Cap Value Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

Scotia Private U.S. Mid Cap Growth Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37

Scotia Private International Equity Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39

Scotia Private International Small to Mid Cap Value Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .41

Scotia Private Emerging Markets Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43

Scotia Private Global Equity Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45

Scotia Private Global Real Estate Pool . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47

WHAT IS A MUTUAL FUND AND WHAT ARE THE RISKS OF INVESTING IN A MUTUALFUND? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49

ORGANIZATION AND MANAGEMENT OF THE FUNDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55

PURCHASES, SWITCHES AND REDEMPTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58

About the Series of Units . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58

How to Buy the Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58

How We Calculate Net Asset Value Per Unit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58

How to Place Orders for the Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .59

How to Switch the Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .59

How to Switch between Series of a Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .59

How to Redeem Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .59

Short-term Trading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60

1

OPTIONAL SERVICES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60

Tax-Deferred Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60

Optimized Portfolios (Pinnacle Series units) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

Custom Portfolios (Pinnacle Series units) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

Automatic Rebalancing (Pinnacle Series units) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

Pre-Authorized Chequing Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

Automatic Withdrawal Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

FEES AND EXPENSES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .62

DEALER COMPENSATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

DEALER COMPENSATION FROM MANAGEMENT FEES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

INCOME TAX CONSIDERATIONS FOR INVESTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

WHAT ARE YOUR LEGAL RIGHTS? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .67

2

IntroductionIn this document,

fund or funds means a mutual fund that is offered for sale under this simplified prospectus;

Manager, SAM, we, us, and our refer to Scotia Asset Management L.P.;

Scotiabank includes The Bank of Nova Scotia (Scotiabank) and its affiliates, including The Bank of NovaScotia Trust Company (Scotiatrust), Scotia Asset Management L.P., Scotia Securities Inc. and Scotia CapitalInc. (including ScotiaMcLeod and Scotia iTRADE, each a division of Scotia Capital Inc.);

ScotiaFunds refers to all of our mutual funds and the series, thereof, which are offered under separatesimplified prospectuses under the ScotiaFunds brand and includes the Scotia mutual funds offered under thissimplified prospectus;

Tax Act means the Income Tax Act (Canada); and

underlying fund refers to a mutual fund (either a ScotiaFund or other mutual fund) in which a fundinvests.

This simplified prospectus contains selected important information to help you make an informedinvestment decision about the Scotia Private Pools and to understand your rights as an investor. It’s dividedinto two parts. The first part, from pages 4 to 48, contains specific information about each of the funds offeredfor sale under this simplified prospectus. The second part, from pages 49 to 67 contains general informationthat applies to all of the funds offered for sale under this simplified prospectus and the risks of investing inmutual funds generally, as well as the names of the firms responsible for the management of the funds.

Additional information about each fund is available in its annual information form, its most recently filedfund facts, its most recently filed annual and interim financial statements and its most recently filed annual andinterim management reports of fund performance. These documents are incorporated by reference into thissimplified prospectus. That means they legally form part of this simplified prospectus just as if they wereprinted in it.

You can get a copy of the funds’ annual information form, financial statements and management reportsof fund performance at no charge by calling 1-800-268-9269 (416-750-3863 in Toronto) for English, or1-800-387-5004 for French, or by asking your mutual fund representative. You’ll also find these documents onour website at www.scotiabank.com/privatepools.com.

These documents and other information about the funds are also available at www.sedar.com.

3

Fund specific informationThe funds are a family of 18 mutual funds. Each fund is associated with an investment portfolio having

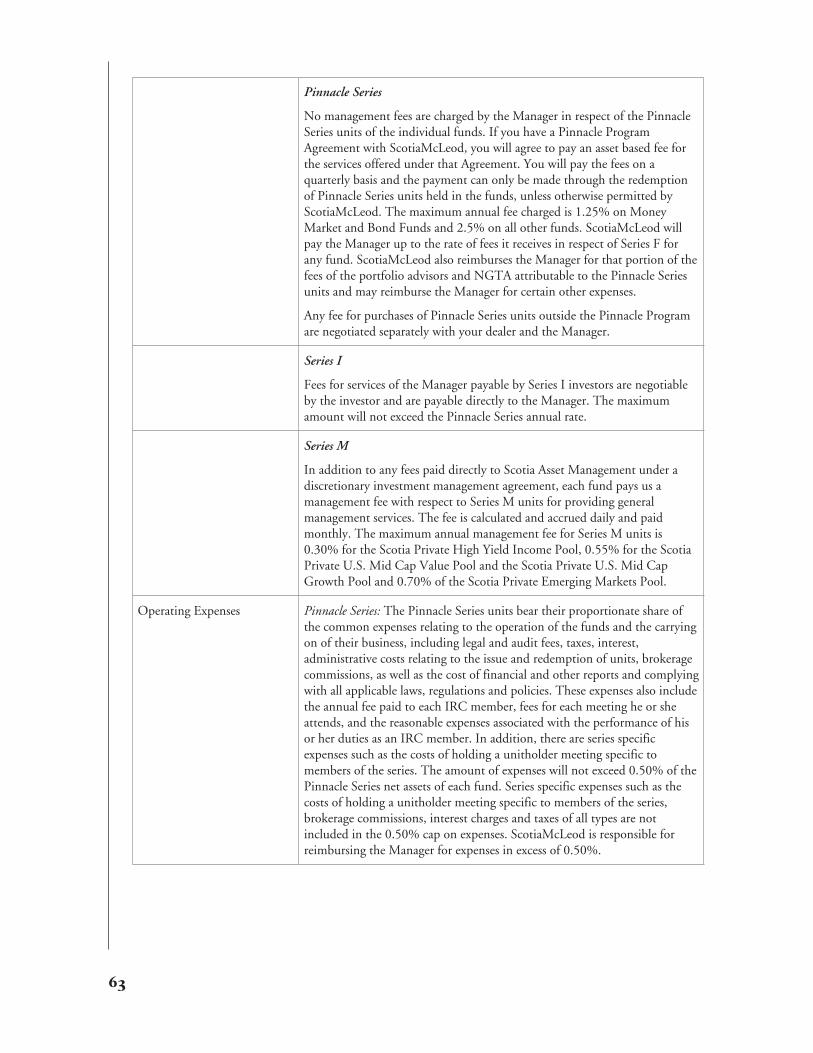

specific investment objectives. Each unit of a series represents an equal, undivided interest in the portion of thefund’s net assets attributable to that series. The funds offered for sale under this simplified prospectus offerPinnacle Series and (except Scotia Private Emerging Markets Pool) Series F units. Some of the funds also offerSeries I and/or Series M units.

The series have different management fees and are intended for different investors. Pinnacle Series unitsare only available to investors who participate in the Pinnacle Program through ScotiaMcLeod advisors or asotherwise permitted by the Manager. Series F units are generally available only to investors who have fee-basedaccounts with their dealer. We may make Series F units available to other investors from time to time. Series Iunits are available only to eligible institutional investors and other qualified investors and are currently onlyavailable through Scotia Asset Management L.P. Series M units are available only to investors who have signeda discretionary investment management agreement with Scotia Asset Management L.P. or Scotiatrust. You’llfind more information about the series under the heading About the Series of Units.

About the fund descriptionsOn the following pages, you will find detailed descriptions of each of the funds to help you make your

investment decisions. Here’s what each section of the fund descriptions tells you.

Fund details

This section gives you some basic information about each fund, such as its start date and its eligibility forregistered plans, including Registered Retirement Savings Plans (RRSPs), Registered Retirement Income Plans(RRIFs), Registered Education Savings Plans (RESPs), Registered Disability Savings Plans (RDSPs), LifeIncome Funds (LIFs), Locked-in Retirement Income Funds (LRIFs), Locked-in Retirement Savings Plans(LRSPs), Prescribed Income Funds (PRIFs) and Tax-Free Savings Accounts (TFSAs).

All of the funds offered under this simplified prospectus are qualified investments under the Income TaxAct (Canada) (“Tax Act”) for registered plans. In certain cases, we may restrict purchases of units of certainfunds by certain registered plans.

What does the fund invest in?

This section tells you the fund’s fundamental investment objectives and the strategies it uses in trying toachieve those objectives. Any change to the fundamental investment objectives must be approved by a majorityof votes cast at a meeting of unitholders.

Portfolio advisor selection and monitoring

The Manager has retained the services of an independent investment consulting firm, NT GlobalAdvisors, Inc. (“NTGA”), a wholly owned subsidiary of Northern Trust Corporation, to assist in the selectionand monitoring of portfolio advisors (the “Portfolio Advisors”). Based on consultation with and research onprospective portfolio advisors, NTGA evaluates and recommends a group of qualified portfolio advisors who,in the opinion of NTGA, are best able to carry out the investment objectives and strategies of the funds.Portfolio Advisors are then chosen by the Manager from this group based on each Portfolio Advisor’sspecialized expertise, performance, consistency, investment philosophy or style, investment disciplines andquality of service. Each Portfolio Advisor is required to operate within the limits of the investment objectives,restrictions and any supplemental guidelines developed from time to time by the Manager.

On an ongoing basis, NTGA will monitor the performance of the Portfolio Advisors and report to us.

About derivatives

Derivatives are investments that derive their value from the price of another investment or fromanticipated movements in interest rates, currency exchange rates or market indexes. Derivatives are usually

4

contracts with another party to buy or sell an asset at a later time and at a set price. Examples ofderivatives are options, forward contracts, futures contracts and swaps.

• Options generally give holders the right, but not the obligation, to buy or sell an asset, such as asecurity or currency, at a set price and a set time. Option holders normally pay the other party a cashpayment, called a premium, for agreeing to give them the option.

• Forward contracts are agreements to buy or sell an asset, such as a security or currency, at a set priceand a set time. The parties have to complete the deal, or sometimes make or receive a cash payment,even if the price has changed by the time the deal closes. Forward contracts are generally not tradedon organized exchanges and are not subject to standardized terms and conditions.

• Futures contracts, like a forward contract, are agreements to buy or sell an asset, such as a security orcurrency, at a set price and a set time. The parties have to complete the deal, or sometimes make orreceive a cash payment, even if the price has changed by the time the deal closes. Futures contractsare normally traded on a registered futures exchange. The exchange usually specifies certainstandardized terms and conditions.

• Swaps are agreements between two or more parties to exchange principal amounts or payments basedon returns on different investments. Swaps are not traded on organized exchanges and are notsubject to standardized terms and conditions.

A fund can use derivatives as long as it uses them in a way that’s consistent with the fund’s investmentobjectives and with Canadian securities regulations. All of the funds may use derivatives to hedge theirinvestments against losses from changes in currency exchange rates, interest rates and stock market prices.Some of the funds may also use derivatives to gain exposure to financial markets or to invest indirectly insecurities or other assets. This can be less expensive than buying securities or assets directly.

When a fund uses derivatives for purposes other than hedging, it holds enough cash or money marketinstruments to fully cover its positions, as required by securities regulations.

Funds that engage in repurchase and reverse repurchase transactions

Some of the funds may enter into repurchase or reverse repurchase agreements to generate additionalincome from securities held in a fund’s portfolio. When a mutual fund agrees to sell a security at one priceand buy it back on a specified later date (usually at a lower price), it is entering into a repurchasetransaction. When a mutual fund agrees to buy a security at one price and sell it back on a specified laterdate (usually at a higher price), it is entering into a reverse repurchase transaction. For a description of thestrategies the funds use to minimize the risks associated with these transactions, see the discussion underRepurchase and reverse repurchase transaction risk.

Funds that lend their securities

Some of the funds may enter into securities lending transactions to generate additional income fromsecurities held in a fund’s portfolio. A mutual fund may lend securities held in its portfolio to qualifiedborrowers who provide adequate collateral. For a description of the strategies the funds use to minimizethe risks associated with these transactions, see the discussion under Securities Lending Risk.

About REITs

A Real Estate Investment Trust (“REIT”) is an entity that buys, manages and sells real estate assets. REITsallow participants to invest in a professionally managed portfolio of real estate properties. REITs qualify aspass-through entities, which are able to distribute the majority of income cash flows to investors withouttaxation at the corporate level (providing that certain conditions are met). As a pass-through entity, whosemain function is to pass profits on to investors, a REIT’s business activities are generally restricted togeneration of property rental income. Another major advantage of a REIT is its liquidity (ease ofliquidation of assets into cash), as compared to traditional private real estate ownership which can bedifficult to liquidate. One reason for the liquid nature of a REIT is that its units are primarily traded on

5

major exchanges, making it easier to buy and sell REIT assets/units than to buy and sell properties inprivate markets. See the discussion under Real Estate Sector Risk and Income trust Risk.

About purchasing debt from related parties

The funds may purchase or sell non-government and government debt securities in the secondary marketfrom, or to, Scotia Capital Inc. or one of our affiliates. The funds may only do so in reliance upon anexemption from the Canadian Securities Administrators and provided that such transactions are done inaccordance with certain conditions.

What are the risks of investing in the fund?

This section tells you the risks of investing in a fund. You’ll find a description of each risk under theheading Specific risks of mutual funds.

This section can help you decide if a fund might be suitable for your portfolio. It’s meant as a generalguide only. For advice about your portfolio, you should consult your mutual fund representative. If you don’thave a mutual fund representative, you can speak with one of our representatives at any Scotiabank branch orby calling a Scotia Securities Inc. or Scotia McLeod office.

Investment Risk Classification Methodology

A risk classification rating is assigned to each fund to provide you with information to help you determinewhether the fund is appropriate for you. Each fund is assigned a risk rating in one of the following categories:low, low to medium, medium, medium to high or high. The investment risk rating for each fund is reviewed atleast annually as well as if there is a material change in a fund’s investment objective or investment strategies.

The methodology used to determine the risk ratings of the fund for purposes of disclosure in thissimplified prospectus is based on a combination of the qualitative aspects of the methodology recommended bythe Fund Risk Classification Task Force of the Investment Fund Institute of Canada and the Manager’squantitative analysis of a Portfolio’s historic volatility. The Manager takes into account other qualitative factorsin making its final determination of each Portfolio’s risk rating. In particular, the standard deviation of eachfund is reviewed. Standard deviation is a common statistic used to measure the volatility of an investment.Portfolios with higher standard deviations are generally classified as being more risky. Qualitative factors takeninto account include key investment policy guidelines which may include but are not limited to regional,sectoral and market capitalization restrictions as well as asset allocation policies.

The Manager recognizes that other types of risk, both measurable and non-measurable, may exist and thathistorical performance may not be indicative of future returns and a fund’s historic volatility may not beindicative of its future volatility.

The methodology that the Manager uses to identify the investment risk level of the funds is available onrequest at no cost by contacting us toll free at 1-800-268-9269 (416-750-3863 in Toronto) for English or1-800-387-5004 for French or by email at [email protected] or by writing to us at the address on the backcover of this simplified prospectus.

Distribution Policy

This section tells you when the fund usually distributes any net income and capital gains, and whereapplicable, return of capital, to unitholders. The funds may also make distributions at other times.

Distributions on units under in registered plans and non-registered accounts are reinvested in additionalunits of the fund, unless you tell your mutual fund representative that you want to receive cash distributions.For information about how distributions are taxed, see Income tax considerations for investors.

Fund expenses indirectly borne by investors

A fund pays its expenses out of its assets. This means investors in a fund indirectly pay for these expensesthrough lower returns. This chart allows you to compare the costs of investing in a fund with the cost of othermutual funds. This chart is for illustrative purposes as required by securities regulators and it shows thecumulative expenses you would have paid over various time periods if you:

• invested $1,000 in the fund; and

• earned a total annual return of 5%, which may be different than the fund’s actual return in any given year.

6

If a fund does not offer Series I or Series F units or did not previously offer Series F, Series I or Series Munits, no fund expenses information is available for that Series. You will find more information about fees andexpenses in Fees and Expenses.

The management expense ratio (“MER”) is based on total expenses for each year shown. It’s expressed as apercentage of daily average net assets during the period. The MER is shown as an annualized rate even if afund’s financial year is less than 12 months. The MER includes all the expenses borne directly by a fund,including interest charges and taxes of most types.

The information in this chart assumes that the fund had the same MER each year as it did in the fund’slast completed financial year. See Fees and Expenses for more information about the costs of investing in thefunds.

7

MONEY MARKET FUND

Scotia Private Short Term Income Pool

This fund has the lowest risk of all the fundsbecause it invests in very high quality short terminstruments. This fund is managed to attempt tomaintain a constant unit value of $10. Interestincome will vary with short term interest rates.

8

Scotia Private Short Term Income PoolFund details

Type of fund Canadian money market fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008

Eligible for registered plans? Yes

Portfolio advisor Scotia Asset Management L.P.Toronto, Ontario

Sub-advisor GCIC Ltd.Toronto, Ontario

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to preserve investment capital while providing interest income andmaintaining liquidity by investing primarily in highly liquid, senior investment grade money marketinstruments (i.e. federal and provincial treasury bills and bonds) and bankers acceptances with a minimumcredit rating of R-1 (low) or A-1 (low).

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund’s investments will have a maximum 180 average term to maturity and a maximum 90 dayaverage term to maturity when calculated on the basis that the term of a floating rate obligation is the periodremaining to the date of the next rate setting. The fund’s investments may also include:

• up to 30% foreign government money market instruments

• other money market investments

The fund aims to maintain a constant unit value of $10 by crediting income and capital gains daily anddistributing them monthly.

The fund can invest up to 30% of its assets in foreign securities. Not less than 95% of the fund’s assetsmust be denominated in Canadian currency.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns may vary with movements in interest rates.

Although the fund intends to maintain a constant unit price of $10, there is no guarantee that the pricewill not go up or down.

See What are the risks of investing in a mutual fund? — Credit Risk, Currency Risk, Foreign InvestmentRisk, Interest Rate Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk and U.S. Withholding Tax Risk.

9

SCOTIA PRIVATE SHORT TERM INCOME POOL

Who should invest in this Fund?

This fund may be suitable for you if:

• you want interest income and liquidity with a high level of safety

• you’re investing for the short term

• you can accept low risk

• you’re aiming to preserve capital

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund credits net income daily and distributes it monthly on the last business day of each month.Distributions on units held in registered plans and non-registered accounts are reinvested in additional units ofthe fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $5.84 $18.42 $32.28 $73.49

Series F $6.97 $21.97 $38.51 $87.67

10

BOND FUNDS

Scotia Private Income PoolScotia Private High Yield Income PoolScotia Private American Core-Plus Bond Pool

The Bond Funds aim to offer the potential forhigher interest income than the Money MarketFund. These funds are more sensitive to changesin interest rates and the credit- worthiness ofissuers.

11

Scotia Private Income PoolFund details

Type of fund Canadian fixed income fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008Series I: since September 8, 2010

Eligible for registered plans? Yes

Portfolio advisor Fiera Capital CorporationToronto, Ontario

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to preserve investment capital while seeking to achieve increasedincome by investing primarily in a portfolio of Canadian government and corporate bonds, preferred shares ofCanadian corporations and loans of supranational organizations.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund’s investments may also include:

• mortgage backed securities, mortgage bonds and mortgages

• term loans

• short term instruments and cash equivalents

Duration may vary by no more than one year from the duration of the DEX Universe Bond Index. ThePortfolio Advisor may actively trade the fund’s investments. This can increase trading costs, which may lowerthe fund’s returns. It also increases the chance that you will receive taxable distributions if you hold the fund ina non-registered account.

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 30% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary inversely with movements in interest rates (i.e. if interest rates rise, returns will decline; ifinterest rates drop, returns will increase).

See What are the risks of investing in a mutual fund? — Asset-Backed and Mortgage-Backed SecuritiesRisk, Credit Risk, Currency Risk, Foreign Investment Risk, Interest Rate Risk, Issuer-specific Risk, Repurchaseand Reverse Repurchase Transaction Risk, Securities Lending Risk, Series Risk, and U.S. Withholding TaxRisk.

12

SCOTIA PRIVATE INCOME POOL

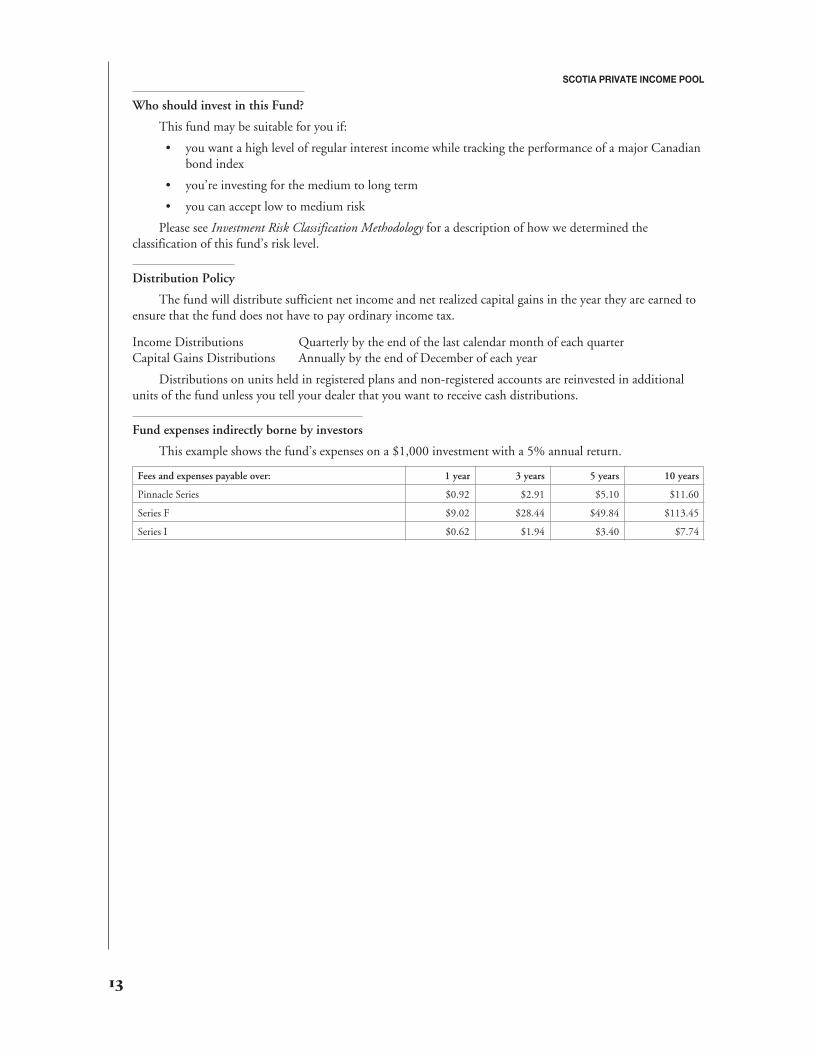

Who should invest in this Fund?

This fund may be suitable for you if:

• you want a high level of regular interest income while tracking the performance of a major Canadianbond index

• you’re investing for the medium to long term

• you can accept low to medium risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Quarterly by the end of the last calendar month of each quarterCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $0.92 $2.91 $5.10 $11.60

Series F $9.02 $28.44 $49.84 $113.45

Series I $0.62 $1.94 $3.40 $7.74

13

Scotia Private High Yield Income PoolFund details

Type of fund High yield fixed income fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008Series I: since September 8, 2010Series M: since September 8, 2010

Eligible for registered plans? Yes

Portfolio advisor Guardian Capital LPToronto, Ontario

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns and to provide income as well ascapital growth by investing primarily in high yield, lower rated Canadian corporate bonds, preferred shares andshort term money market securities.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund’s investments will have an average duration of 7 years and an average credit rating of single B.

The fund’s investments may also include up to 30% high yield, lower rated bonds of U.S. corporations.

The Portfolio Advisor may actively trade the fund’s investments. This can increase trading costs, whichmay lower the fund’s returns. It also increases the chance that you will receive taxable distributions if you holdthe fund in a non-registered account.

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 100% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them startingunder What are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary inversely with movements in interest rates (i.e. if interest rates rise, returns will decline; ifinterest rates drop, returns will increase).

Higher potential for gain and greater risk of loss associated with lower rated securities.

See What are the risks of investing in a mutual fund? — Credit Risk, Currency Risk, Derivatives Risk,Foreign Investment Risk, Interest Rate Risk, Issuer-specific Risk, Liquidity Risk, Repurchase and ReverseRepurchase Transaction Risk, Securities Lending Risk, Series Risk and U.S. Withholding Tax Risk.

As at November 1, 2012, Scotia INNOVA Income Portfolio, Scotia INNOVA Balanced IncomePortfolio, and Scotia INNOVA Balanced Growth Portfolio held approximately 20.0%, 16.4%, and 13.9%,respectively, of the outstanding units of the fund.

14

SCOTIA PRIVATE HIGH YIELD INCOME POOL

Who should invest in this fund?

This fund may be suitable for you if:

• you’re seeking a high level of regular interest income

• you’re contributing to the income portion of a diversified portfolio

• you’re investing for the medium to long term

• you can accept medium risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Quarterly by the end of the last calendar month of each quarterCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $1.44 $4.52 $7.93 $18.05

Series F $9.74 $30.70 $53.81 $122.48

Series I $1.03 $3.23 $5.66 $12.89

Series M $4.00 $12.60 $22.09 $50.28

15

Scotia Private American Core-Plus Bond PoolFund details

Type of fund Global fixed income fund

Date established February 14, 2002

Type of securities Pinnacle Series: since February 14, 2002Series F: since December 22, 2008Series I: since December 22, 2008

Eligible for registered plans? Yes

Portfolio advisor Logan Circle Partners, L.P.Conshohocken, Pennsylvania

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns and to provide income as well ascapital growth by investing primarily in a portfolio of U.S. government and corporate bonds and mortgage passthrough securities. The fund may also invest in the U.S. dollar denominated emerging markets,non-investment grade debt and non-U.S. investment grade sovereign and corporate debt.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund’s investments in bonds will have an average credit rating of at least single A.

Up to 20% of the net asset value of the fund may be invested in U.S. denominated non-investment grade(high yield and emerging market) bonds.

Up to 20% of the net asset value of the fund may be invested in non-U.S. government agency andcorporate bonds.

At least 80% of the net asset value of the fund will consist of investment grade securities. Investments innon-U.S. dollar denominated securities and non-investment grade securities will be made tactically based onthe Portfolio Advisor’s evaluation of spread management using fundamental bottom up research.

The fund’s investments may also include:

• short term instruments and cash equivalents

• U.S. denominated asset backed securities and mortgage backed securities

The Portfolio Advisor may actively trade the fund’s investments. This can increase trading costs, whichmay lower the fund’s returns. It also increases the chance that you will receive taxable distributions if you holdthe fund in a non-registered account.

The fund may use derivatives for foreign currency hedging purposes.

The fund can invest up to 100% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

16

SCOTIA PRIVATE AMERICAN CORE-PLUS BOND POOL

What are the risks of investing in the Fund?

Returns will vary inversely with movements in interest rates (i.e. if interest rates rise, returns will decline; ifinterest rates drop, returns will increase).

Higher potential for gain and greater risk of loss associated with lower rated securities.

See What are the risks of investing in a mutual fund? — Asset-Backed and Mortgage-Backed SecuritiesRisk, Commodity Risk, Credit Risk, Currency Risk, Derivatives Risk, Emerging Markets Risk, ForeignInvestment Risk, Interest Rate Risk, Issuer-specific Risk, Liquidity Risk, Repurchase and Reverse RepurchaseTransaction Risk, Securities Lending Risk, Series Risk and U.S. Withholding Tax Risk.

As at November 1, 2012, Scotia INNOVA Income Portfolio, Scotia INNOVA Balanced IncomePortfolio, and Scotia INNOVA Balanced Growth Portfolio held approximately 28.5%, 25.0% and 22.0%,respectively, of the outstanding units of the fund.

Who should invest in this Fund?

This fund may be suitable for you if:

• you want a high level of regular interest income and U.S. dollar exposure• you’re investing for the medium to long term• you can accept medium risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Quarterly by the end of the last month of each quarterCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $3.18 $10.02 $17.56 $39.97

Series F $10.25 $32.31 $56.64 $128.92

Series I $0.82 $2.59 $4.53 $10.31

17

BALANCED FUND

Scotia Private Strategic Balanced Pool

The fund offers a combination of equity, bondsand money market securities in a singleinvestment. The fund generally has less volatilitythan Equity Funds but more volatility thanIncome Funds.

18

Scotia Private Strategic Balanced PoolFund details

Type of fund Canadian neutral balanced fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008

Eligible for registered plans? Yes

Portfolio advisor Gryphon Investment Counsel Inc.Toronto, Ontario

What does the Fund invest in?

Investment Objectives

This fund’s investment objective is to achieve superior long term returns through a combination of capitalgrowth and income by investing primarily in large capitalization stocks of Canadian corporations andCanadian government bonds. The weighting of the fund’s portfolio will be allocated between asset classeswithin specified ranges: 40%-80% equities; 20%-60% fixed income securities; 0%-30% short term moneymarket securities and cash.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

This fund uses an investment strategy of allocating investments between short term money marketsecurities and cash, fixed income and equity securities. Reallocations between these asset classes tend to becarried out gradually and are fixed within specific ranges. The proportion of assets invested in different classesof securities will vary from time to time based on market conditions, economic outlook and level of interestrates and dividend yields.

The fund may use derivatives for hedging purposes and to provide more effective exposure while reducingtransaction costs.

The fund can invest up to 30% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?

What are the risks of investing in the Fund?

Returns may vary with changes in interest rates and stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Interest Rate Risk, Issuer-specific Risk, Liquidity Risk,Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, Series Risk and U.S.Withholding Tax Risk.

19

SCOTIA PRIVATE STRATEGIC BALANCED POOL

Who should invest in this Fund?

This fund may be suitable for you if:

• you want both interest income and growth through strategic asset allocation among the three majorasset classes

• you’re investing for the medium to long term

• you can accept medium risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Quarterly by the end of the last calendar month of each quarterCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $4.00 $12.60 $22.09 $50.28

Series F $16.20 $51.05 $89.49 $203.70

20

CANADIAN EQUITY FUNDS

Scotia Private Canadian Value PoolScotia Private Canadian Mid Cap PoolScotia Private Canadian Growth PoolScotia Private Canadian Small Cap Pool

The Equity Funds offer the greatest potential forlong term growth. These funds also have higherrisk because the prices of equity securities canchange significantly in a short period of time.

21

Scotia Private Canadian Value PoolFund details

Type of fund Canadian focused equity fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008Series I: since September 8, 2010

Eligible for registered plans? Yes

Portfolio advisor Scheer, Rowlett & AssociatesInvestment Management Ltd.Toronto, Ontario

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns through capital growth byinvesting primarily in securities of Canadian corporations.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund uses a value-oriented investment style to achieve its investment objectives.

The fund’s investments may also include up to 15% cash and cash equivalents.

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 30% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Income Trust Risk, Interest Rate Risk, Issuer-specificRisk, Liquidity Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk and U.S. Withholding Tax Risk.

Who should invest in this Fund?

This fund may be suitable for you if:

• you want a Canadian value holding in a diversified portfolio

• you’re investing for the long term

• you can accept medium risk.

22

SCOTIA PRIVATE CANADIAN VALUE POOL

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Annually by the end of December of each yearCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $2.26 $7.11 $12.46 $28.36

Series F $13.53 $42.65 $74.76 $170.18

Series I $1.23 $3.88 $6.80 $15.47

23

Scotia Private Canadian Mid Cap PoolFund details

Type of fund Canadian focused small/mid capequity fund

Date established February 14, 2002

Type of securities Pinnacle Series: since February 14, 2002Series F: since December 22, 2008Series I: since September 8, 2010

Eligible for registered plans? Yes

Portfolio advisor Connor, Clark & Lunn InvestmentManagement Ltd.Vancouver, British Columbia

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns through capital growth byinvesting primarily in stocks of small and medium capitalization Canadian corporations.

Any changes to the fundamental investment objectives of the fund must be approved by a majority ofvotes cast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund uses a value-oriented investment style to achieve its investment objectives.

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 30% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

Stock prices of small and medium capitalization companies are typically more volatile due to size andshorter trading history.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Income Trust Risk, Interest Rate Risk, Issuer-specificRisk, Liquidity Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk, Small Company Risk and U.S. Withholding Tax Risk.

Who should invest in this Fund?

This fund may be suitable for you if:

• you want a Canadian medium capitalization value holding in a diversified portfolio

• you’re investing for the long term

• you can accept high risk

24

SCOTIA PRIVATE CANADIAN MID CAP POOL

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Annually by the end of December of each yearCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $3.69 $11.63 $20.39 $46.41

Series F $13.43 $42.33 $74.20 $168.89

Series I $1.74 $5.49 $9.63 $21.92

25

Scotia Private Canadian Growth PoolFund details

Type of fund Canadian equity fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008Series I: since September 8, 2010

Eligible for registered plans? Yes

Portfolio advisor Manulife Asset ManagementToronto, Ontario

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns through capital growth byinvesting primarily in stocks of large and medium capitalization Canadian corporations.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund uses a growth-oriented investment style to achieve its investment objectives.

The fund’s investments may also include up to 15% cash and cash equivalents.

The Portfolio Advisor may actively trade the fund’s investments. This can increase trading costs, whichmay lower the fund’s returns. It also increases the chance that you will receive taxable distributions if you holdthe fund in a non-registered account.

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 30% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Income Trust Risk, Interest Rate Risk, Issuer-specificRisk, Liquidity Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk and U.S. Withholding Tax Risk.

As at November 1, 2012, Scotia INNOVA Balanced Growth Portfolio, and Scotia INNOVA GrowthPortfolio held approximately 16.9%, and 14.8%, respectively, of the outstanding units of the fund.

26

SCOTIA PRIVATE CANADIAN GROWTH POOL

Who should invest in this Fund?

This fund may be suitable for you if:

• you want a Canadian growth holding in a diversified portfolio

• you’re investing for the long term

• you can accept medium risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Annually by the end of December of each yearCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $2.15 $6.79 $11.89 $27.07

Series F $13.43 $42.33 $74.20 $168.89

Series I $1.23 $3.88 $6.80 $15.47

27

Scotia Private Canadian Small Cap PoolFund details

Type of fund Canadian small/mid cap equity fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008Series I: since December 22, 2008

Eligible for registered plans? Yes

Portfolio advisor Mawer Investment Management Ltd.Calgary, Alberta

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns through capital growth byinvesting primarily in stocks of small and medium capitalization Canadian corporations.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund uses a growth-oriented investment style that is moderated by price sensitivity (growth at areasonable price) to achieve its investment objectives.

The fund’s investments may also include up to 15% cash and cash equivalents.

The Portfolio Advisor may actively trade the fund’s investments. This can increase trading costs, whichmay lower the fund’s returns. It also increases the chance that you will receive taxable distributions if you holdthe fund in a non-registered account.

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 10% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

Stock prices of small capitalization companies are typically more volatile due to size and shorter tradinghistory.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Income Trust Risk, Interest Rate Risk, Issuer-specificRisk, Liquidity Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk, Small Company Risk and U.S. Withholding Tax Risk.

28

SCOTIA PRIVATE CANADIAN SMALL CAP POOL

As at November 1, 2012, Scotia INNOVA Balanced Growth Portfolio, Scotia INNOVA GrowthPortfolio, and Scotia INNOVA Balanced Income Portfolio held approximately 29.2%, 19.8%, and 12.5%,respectively, of the outstanding units of the fund.

Who should invest in this Fund?

This fund may be suitable for you if:

• you want a Canadian small capitalization growth holding in a diversified portfolio

• you’re investing for the long term

• you can accept high risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Annually by the end of December of each yearCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $3.08 $9.69 $16.99 $38.68

Series F $13.33 $42.01 $73.63 $167.60

Series I $0.92 $2.91 $5.10 $11.60

29

FOREIGN EQUITY FUNDS

Scotia Private U.S. Value PoolScotia Private U.S. Large Cap Growth PoolScotia Private U.S. Mid Cap Value PoolScotia Private U.S. Mid Cap Growth PoolScotia Private International Equity PoolScotia Private International Small to Mid Cap Value PoolScotia Private Emerging Markets PoolScotia Private Global Equity PoolScotia Private Global Real Estate Pool

The Equity Funds offer the greatest potential forlong term growth. These funds also have higherrisk because the prices of equity securities canchange significantly in a short period of time.Foreign Equity Funds usually have more riskthan Canadian Equity Funds because theinvestments may be in countries that have fewerregulations.

30

Scotia Private U.S. Value PoolFund details

Type of fund U.S. equity fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008Series I: since December 22, 2008

Eligible for registered plans? Yes

Portfolio advisor Herndon Capital Management, LLCAtlanta, Georgia

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns through capital growth byinvesting primarily in stocks of large capitalization U.S. corporations.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund uses a value-oriented investment style to achieve its investment objectives.

The fund’s investments may also include:

• up to 15% cash and cash equivalents

• up to 10% non-U.S. securities

The Portfolio Advisor may actively trade the fund’s investments. This can increase trading costs, whichmay lower the fund’s returns. It also increases the chance that you will receive taxable distributions if you holdthe fund in a non-registered account.

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 100% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information on securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Income Trust Risk, Interest Rate Risk, Issuer-specificRisk, Liquidity Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk and U.S. Withholding Tax Risk.

As at November 1, 2012, Scotia INNOVA Balanced Growth Portfolio, Scotia INNOVA BalancedIncome Portfolio, Scotia INNOVA Income Portfolio, and Scotia INNOVA Growth Portfolio heldapproximately 23.5%, 20.1%, 15.3%, and 13.3%, respectively, of the outstanding units of the fund.

31

SCOTIA PRIVATE U.S. VALUE POOL

Who should invest in this Fund?

This fund may be suitable for you if:

• you want long term growth of capital through well established, high quality U.S. companies

• you want a U.S. value holding in a diversified portfolio

• you’re investing for the long term

• you can accept medium to high risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Annually by the end of December of each yearCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $3.69 $11.63 $20.39 $46.41

Series F $13.33 $42.01 $73.63 $167.60

Series I $0.51 $1.62 $2.83 $6.45

32

Scotia Private U.S. Large Cap Growth PoolFund details

Type of fund U.S. equity fund

Date established February 23, 2001

Type of securities Pinnacle Series: since February 23, 2001Series F: since December 22, 2008Series I: since September 8, 2010

Eligible for registered plans? Yes

Portfolio advisor American Century InvestmentManagement, Inc.Kansas City, Missouri

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns through capital growth byinvesting primarily in large capitalization stocks of U.S. corporations.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund uses a growth-oriented investment style to achieve its investment objectives. The fund’sinvestments may also include:

• up to 15% cash and cash equivalents

• up to 10% non-U.S. securities

The Portfolio Advisor may actively trade the fund’s investments. This can increase trading costs, whichmay lower the fund’s returns. It also increases the chance that you will receive taxable distributions if you holdthe fund in a non-registered account.

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 100% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Income Trust Risk, Interest Rate Risk, Issuer-specificRisk, Liquidity Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk, and U.S. Withholding Tax Risk.

33

SCOTIA PRIVATE U.S. LARGE CAP GROWTH POOL

Who should invest in this Fund?

This fund may be suitable for you if:

• you want the growth potential of investing in equity securities of U.S. companies

• you want a U.S. growth holding in a diversified portfolio

• you’re investing for the long term

• you can accept medium to high Risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Annually by the end of December of each yearCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $5.64 $17.77 $31.15 $70.91

Series F $13.22 $41.68 $73.06 $166.31

Series I $1.85 $5.82 $10.19 $23.21

34

Scotia Private U.S. Mid Cap Value PoolFund details

Type of fund U.S. small/mid cap equity fund

Date established February 14, 2002

Type of securities Pinnacle Series: since February 14, 2002Series F: since December 22, 2008Series I: since December 22, 2008Series M: since September 8, 2010

Eligible for registered plans? Yes

Portfolio advisor Cramer Rosenthal McGlynn, LLCNew York, New York

What does the Fund invest in?

Investment Objectives

The fund’s objective is to achieve superior long term returns through capital growth by investing primarilyin stocks of small and medium capitalization companies located in the U.S.

Any change to the fundamental investment objectives of the fund must be approved by the majority ofvotes cast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund uses a value-oriented investment style to achieve its investment objectives.

The fund’s investments may also include:

• up to 15% cash and cash equivalents

• up to 10% non-U.S. equivalent

The fund may use derivatives for foreign currency hedging purposes only.

The fund can invest up to 100% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

Stock prices of small and medium capitalization companies are typically more volatile due to size andshorter trading history.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Income Trust Risk, Interest Rate Risk, Issuer-specificRisk, Liquidity Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk, Small Company Risk and U.S. Withholding Tax Risk.

35

SCOTIA PRIVATE U.S. MID CAP VALUE POOL

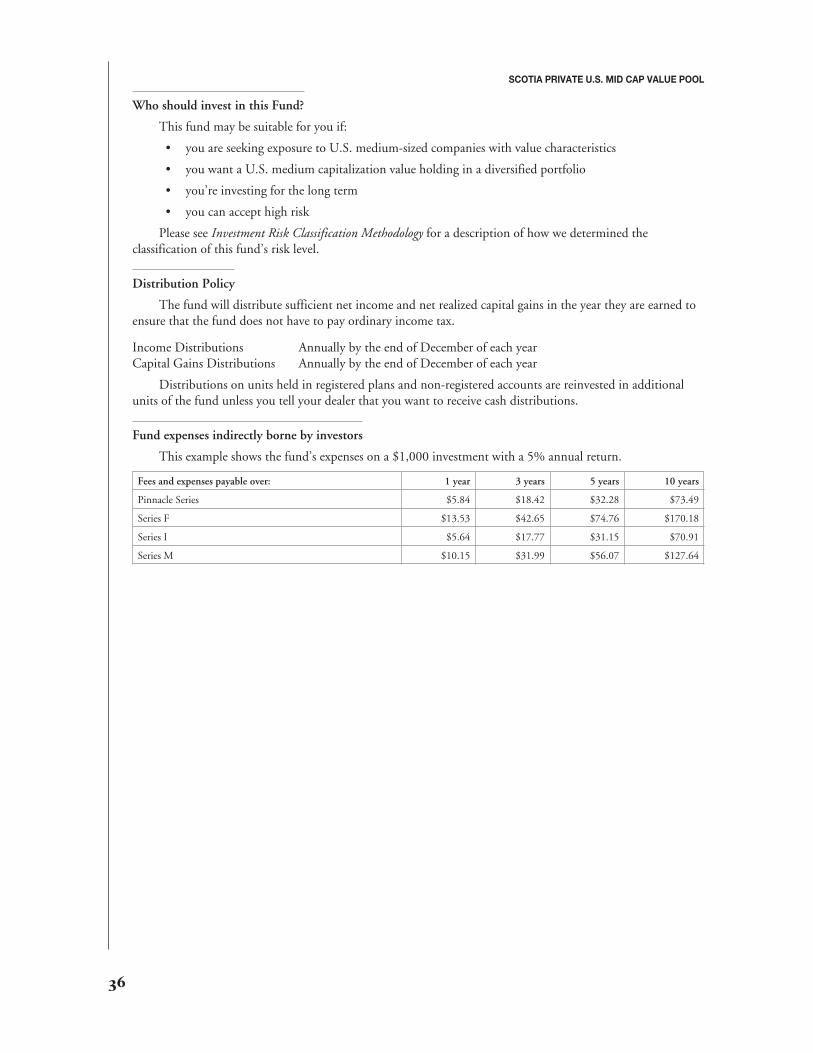

Who should invest in this Fund?

This fund may be suitable for you if:

• you are seeking exposure to U.S. medium-sized companies with value characteristics

• you want a U.S. medium capitalization value holding in a diversified portfolio

• you’re investing for the long term

• you can accept high risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Annually by the end of December of each yearCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $5.84 $18.42 $32.28 $73.49

Series F $13.53 $42.65 $74.76 $170.18

Series I $5.64 $17.77 $31.15 $70.91

Series M $10.15 $31.99 $56.07 $127.64

36

Scotia Private U.S. Mid Cap Growth PoolFund details

Type of fund U.S. small/mid cap equity fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008Series I: since December 22, 2008Series M: since September 8, 2010

Eligible for registered plans? Yes

Portfolio advisor TCW Investment ManagementCompanyLos Angeles, California

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve superior long term returns through capital growth byinvesting primarily in stocks of small and medium capitalization companies traded on U.S. stock exchanges.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies

The fund uses a growth-oriented investment style to achieve its investment objectives.

The fund’s investments may also include up to 15% cash and cash equivalents. The fund may usederivatives for foreign currency hedging purposes only.

The fund can invest up to 100% of its assets in foreign securities.

The fund may participate in securities lending, repurchase and reverse repurchase transactions to achieveits investment objectives and to enhance returns. You’ll find more information about securities lending,repurchase and reverse repurchase transactions and how the fund limits the risks associated with them underWhat are the risks of investing in a mutual fund?.

What are the risks of investing in the Fund?

Returns will vary with changes in stock prices.

Prices of equity securities tend to fluctuate more than those of fixed income securities, resulting in greaterprice fluctuations than would be expected of the money market or bond funds.

Stock prices of small and medium capitalization companies are typically more volatile due to size andshorter trading history.

See What are the risks of investing in a mutual fund? — Commodity Risk, Credit Risk, Currency Risk,Derivatives Risk, Equity Risk, Foreign Investment Risk, Income Trust Risk, Interest Rate Risk, Issuer-specificRisk, Liquidity Risk, Repurchase and Reverse Repurchase Transaction Risk, Securities Lending Risk, SeriesRisk, Small Company Risk and U.S. Withholding Tax Risk.

As at November 1, 2012, Scotia INNOVA Balanced Growth Portfolio, and Scotia INNOVA GrowthPortfolio held approximately 48.2%, and 26.0%, respectively, of the outstanding units of the fund.

37

SCOTIA PRIVATE U.S. MID CAP GROWTH POOL

Who should invest in this Fund?

This fund may be suitable for you if:

• you’re seeking exposure to U.S. medium-sized growth companies

• you want a U.S. medium capitalization growth holding in a diversified portfolio

• you’re investing for the long term

• you can accept high risk

Please see Investment Risk Classification Methodology for a description of how we determined theclassification of this fund’s risk level.

Distribution Policy

The fund will distribute sufficient net income and net realized capital gains in the year they are earned toensure that the fund does not have to pay ordinary income tax.

Income Distributions Annually by the end of December of each yearCapital Gains Distributions Annually by the end of December of each year

Distributions on units held in registered plans and non-registered accounts are reinvested in additionalunits of the fund unless you tell your dealer that you want to receive cash distributions.

Fund expenses indirectly borne by investors

This example shows the fund’s expenses on a $1,000 investment with a 5% annual return.

Fees and expenses payable over: 1 year 3 years 5 years 10 years

Pinnacle Series $6.15 $19.39 $33.98 $77.35

Series F $13.22 $41.68 $73.06 $166.31

Series I $1.23 $3.88 $6.80 $15.47

Series M $7.48 $23.59 $41.35 $94.11

38

Scotia Private International Equity PoolFund details

Type of fund International equity fund

Date established October 6, 1997

Type of securities Pinnacle Series: since October 6, 1997Series F: since December 22, 2008Series I: since December 22, 2008

Eligible for registered plans? Yes

Portfolio advisor Thornburg Investment Management,Inc.Santa Fe, New Mexico

What does the Fund invest in?

Investment Objectives

The fund’s investment objective is to achieve long term returns through capital growth by investingprimarily in large capitalization stocks of companies in Europe, Australia and the Far East.

Any change to the fundamental investment objectives of the fund must be approved by a majority of votescast at a meeting of unitholders called for that purpose.

Investment Strategies