scotia howard weil annual energy conferencefilecache.investorroom.com/mr5ir_anadarko/844...scotia...

TRANSCRIPT

w w w . a n a d a r k o . c o m | N Y S E : A P C

A N A D A R K O P E T R O L E U M C O R P O R A T I O N

JOHN COLGLAZIERSenior Vice President

832 636 2306

JEREMY SMITHDirector

832 636 1544

SHANDELL SZABODirector

832 636 3977

I N V E S T O RR E L A T I O N S

SCOTIA HOWARD WEIL44TH ANNUAL ENERGY CONFERENCE

Al WalkerChairman, President & CEO

March 2016

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C 2

Cautionary LanguageRegarding Forward-Looking Statements and Other Matters

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Anadarko believes that its expectations are based on reasonable assumptions. No assurance, however, can be given that such expectations will prove to have been correct. A number of factors could cause actual results to differ materially from the projections, anticipated results, or other expectations expressed in this presentation, including Anadarko’s ability to realize its expectations regarding performance in this challenging economic environment and meet financial and operating guidance; timely complete and commercially operate the projects and drilling prospects identified in this presentation; reduce its net debt; consummate the transactions described in this presentation and identify and complete additional transactions; achieve further drilling cost reductions and efficiencies; successfully plan, secure necessary government approvals, enter into long-term sales contracts, finance, build, and operate the necessary infrastructure and LNG park in Mozambique; and achieve production expectations on its mega projects. See “Risk Factors” in the company’s 2015 Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and other public filings and press releases. Anadarko undertakes no obligation to publicly update or revise any forward-looking statements.

Please also see our website at www.anadarko.com under “Investor Relations” for reconciliations of the differences between any non-GAAP measure used in this presentation, including the appendix slides, and the most directly comparable GAAP financial measures. Also on our website at www.anadarko.com is a glossary of terms.

Cautionary Note to Investors - The U.S. Securities and Exchange Commission (SEC) permits oil and gas companies, in their filings with the SEC, to disclose only proved, probable and possible reserves that meet the SEC’s definitions for such terms. We may use terms in this presentation, such as “resources,” “net resources,” “net discovered resources,” “recoverable resources,” and similar terms that the SEC’s guidelines strictly prohibit us from including in filings with the SEC. U.S. Investors are urged to consider closely the oil and gas disclosures in our Form 10-K for the year ended December 31, 2015, File No. 001-08968, available from us at www.anadarko.com or by writing to us at: Anadarko Petroleum Corporation, 1201 Lake Robbins Drive, The Woodlands, Texas 77380 Attn: Investor Relations. You can also obtain this form from the SEC by calling 1-800-SEC-0330.

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C

Focus on Enhancing and Preserving ValueReduce Capital Program ~50% YOYReduce DividendsAchieve Additional Cost Savings and Efficiency GainsContinue Active Monetization ProgramReduce Net Debt

3

Successfully Navigating a Volatile Environment

Note: All amounts are approximate

Shenandoah

Colombia

Côte d’Ivoire

Mozambique

$1.5~ 1 Y E A R

$0.51 - 3 Y E A R S

$0.53 + Y E A R S

2 0 1 6 E & P I N V E S T M E N T S ( B i l l i o n s )

Delaware Basin

GOM Appraisals

DJ Basin

GOM Tiebacks

TEN Startup

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C 4

2016 Expectations

~$1.3 Billion Monetized Thru 2/16 $420 Million Soda Ash and Coal Royalties $750 Million WES Transaction $105+ Million East Chalk Divestiture

Additional Monetizations Under Way

2016E 2015

CAPITAL1

(BILLIONS) $2.6 - $2.8 $5.4 ~50%SALES VOLUMES2

(MMBOE) 282 - 286 292 ~3%OIL SALES VOLUMES2

(MBOPD) 308 - 313 312 ~Flat1 Excludes capital expenditures by WES2 Excludes all sales volumes associated with EOR, Bossier, PRB-CBM and East Chalk

GOM$0.7 B

International$0.7 B

Midstream & Other$0.2 B

U.S. Onshore$1.1 B

2016E CAPITAL PROGRAM$2.6 - $2.8 BILLION*

* Excludes capital expenditures by WES

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C 5

Benefits of a Balanced Portfolio~18% Base DeclineLeveraging IDUC InventoryMega Project Contribution Full-Year Lucius Contribution Heidelberg First Oil 1Q16 TEN First Oil Expected 3Q16

$2.0 $2.2 $2.5 $2.9 $2.9 $2.7 ~$1.8

$0.5$1.1 $1.3

$1.8$2.9

$0.1$2.0

$1.6$1.9

$2.1$2.0

$2.4

$0

$4

$8

2010 2011 2012 2013 2014 2015 2016E

E&P

Cap

ital A

lloca

tion

(Bill

ions

)

Advantaged Maintenance Capital Provides Flexibility

Maintenance Capital Short-Cycle Growth Capital Mid- & Long-Cycle Capital

L I Q U I D S M I X ~43% ~56%

Note: Maintenance capital is defined as capital investments necessary to keep current-year sales volumes flat to previous year

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C

Increasing Flexibility 50% YOY Capital Reduction 80% Dividend Reduction Improving Cost Structure

Targeting up to $3 Billion Monetizations ~$1.3 Billion Monetized Thru 2/16

$0.9

$2.5 - $3.0$2.1 - $2.2

$2.0 - $3.0 $2.6 - $2.8

$0.1

$0

$6

YE15 Cash Adj. DCF* Monetizations Capital Investments** Dividends YE16E Cash

Bill

ions

2016: Building Cash & Reducing Net Debt(Excludes Working Capital Changes)

6

Financial Discipline: Investing Within Cash Inflows

* Based on consensus prices as of 3/11/2016: WTI $39.50/Bbl and HH $2.50/Mcf** Excludes capital expenditures by WESNote: See Appendix for non-GAAP definitions

$1.3

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C

Successfully Refinanced Near-Term MaturitiesAmple Liquidity $900+ Million Cash-on-Hand YE15 $3 Billion 5-Year Revolving Credit Facility $2 Billion 364-Day Facility

Substantial Flexibility

7

Maintaining Financial StrengthInvestment-Grade Quality, Investment-Grade Approach

Rating Outlook Last Update

S&P BBB Negative 2016

FITCH BBB Negative 2016

MOODY’S Ba1 Negative 2016

-$3

$15

Bill

ions

Differentiating Capital Allocation & Portfolio Management

Adj. DCF Monetizations TPE Capital DWH/TRX Adj. FCF (Cumulative) Adj. FCF (CumulativeIncluding DWH/TRX)

2011 2012 2013 2014 2015 2016E*

* Based on consensus prices as of 3/11/2016: WTI $39.50/Bbl and HH $2.50/McfNote: See Appendix for non-GAAP definitions and reconciliations

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C

U.S. Onshore: Enhancing & Preserving Value~70% Capital Reduction YOY Decrease Average Rig Count to 5 from 25

Focus on Base ProductionReduce Costs and Improve EfficienciesLeverage 230 IDUCs When Returns Compelling ~170 IDUCs Expected YE16

8

U . S . O N S H O R E N E T S A L E S V O L U M E S * 2 0 1 5 2 0 1 6 E

TOTAL (MBOE/D) 616 596 - 601LIQUIDS (MBBL/D) 283 266 - 270

Delaware Basin~$800 MM

DJ Basin~$1,300 MM

Midstream~$400 MM

Other Onshore~$600 MM

Eagleford$500

Delaware Basin~$500 MM

DJ Basin~$500 MM

Midstream~$100 MM

Other~$100 MM

2016E CAPITAL PROGRAM~$1.2 BILLION

2015 CAPITAL PROGRAM~$3.6 BILLION

* Excludes all sales volumes associated with EOR, Bossier, PRB-CBM and East ChalkNote: See Appendix for non-GAAP definitions

D J B A S I NP L A N N E D A C T I V I T Y

~1 Rig~2 Frac Crews

$6/BOE Development Cost <$15,000/Flowing Barrel

Activation Cost

D E L A W A R E B A S I NP L A N N E D A C T I V I T Y

~4 Rigs~1 Frac Crew

Delineation and Lease Maintenance

2+ BBOE: Doubled Net Resources

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C

$5.1

$4.4

$3.7

$2.7

$0

$3

$6

2013 2014 2015 2016E

Mill

ions

Driving Down Well Costs(4,800’ Short-Lateral Equivalent)

CONSOLIDATED CORE ACREAGEWITH MINERALS-INTEREST UPLIFT

OILLIGHT OIL

5 MILES

~$30

~$25

$0

$20

$40

New Drills IDUCs

WTI

Pric

e ($

/Bbl

)

BTAX PV-10 Breakeven**

9

DJ Basin: World-Class Asset1.5+ BBOE Net Resources ~4,000 Identified Drilling Locations

Leveraging Competitive Advantages Minerals-Interest Ownership Infrastructure in Place IDUC Inventory APC Acreage

APC Mineral Interest

D J B A S I NNet Acres: ~350,000

C O L O R A D O

2 0 1 6 P L A N N E D O P E R A T E D A C T I V I T Y

R I G S W E L L S - S L E F R A C C R E W S Y E 1 6 I D U C S

~1 ~45 ~2 ~60

0

100

200

300

$0

$1

$2

$3N

et S

ales

Vol

umes

(MB

OPD

)

Bill

ions

Differentiating Capital Allocation & Portfolio Management(E&P Only)

EBITDAX Capital MonetizationsAdj. FCF (Cumulative) Net Sales Volumes

2011 2012 2013 2014 2015 2016E*

* Based on consensus prices as of 3/11/2016: WTI $39.50/Bbl and HH $2.50/McfNote: EBITDAX excludes corporate G&A; see Appendix for non-GAAP definitions ** Assumes HH $2.50/Mcf

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C 10

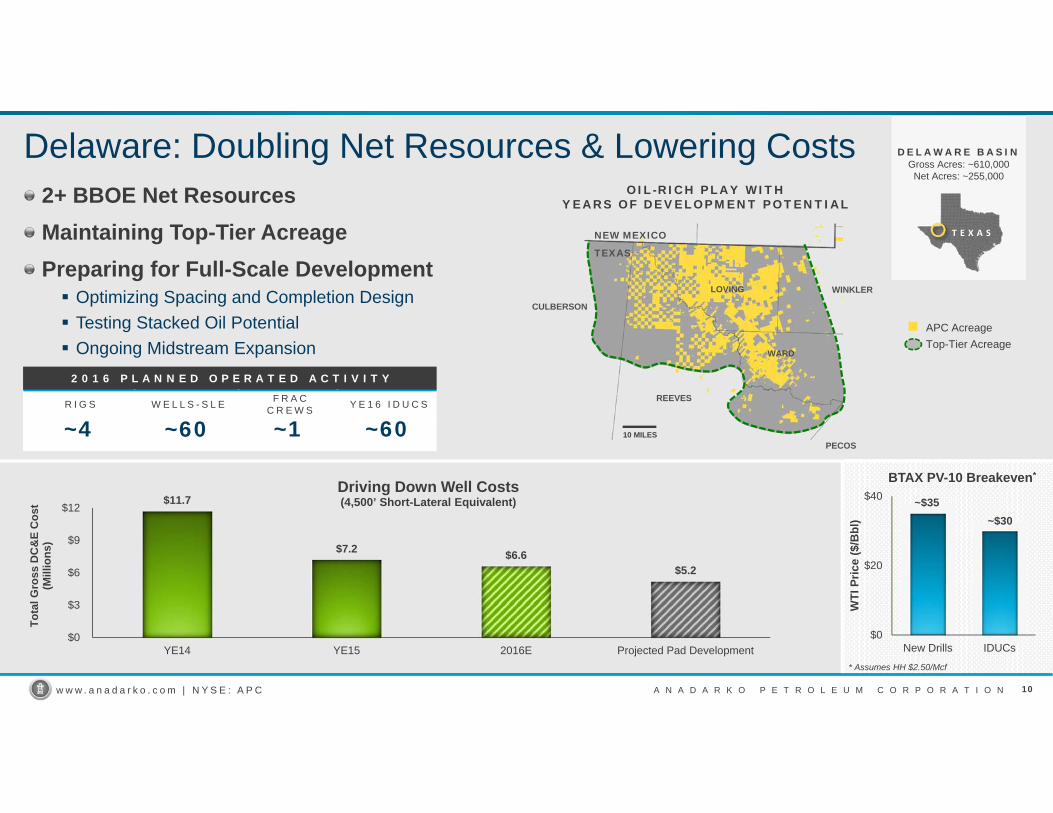

Delaware: Doubling Net Resources & Lowering Costs

T E X A S

DE L AWARE BAS IN Gross Acres: ~610,000

Net Acres: ~255,000

2+ BBOE Net ResourcesMaintaining Top-Tier Acreage Preparing for Full-Scale Development Optimizing Spacing and Completion Design Testing Stacked Oil Potential Ongoing Midstream Expansion

CULBERSON

REEVES

NEW MEXICO

TEXAS

WARD

WINKLER

PECOS

LOVING

OIL-RICH PLAY WITH YEARS OF DEVELOPMENT POTENTIAL

10 MILES

APC AcreageTop-Tier Acreage

~$35~$30

$0

$20

$40

New Drills IDUCs

WTI

Pric

e ($

/Bbl

)

BTAX PV-10 Breakeven*

$11.7

$7.2 $6.6$5.2

$0

$3

$6

$9

$12

YE14 YE15 2016E Projected Pad Development

Tota

l Gro

ss D

C&

E C

ost

(Mill

ions

)

Driving Down Well Costs(4,500’ Short-Lateral Equivalent)

2 0 1 6 P L A N N E D O P E R A T E D A C T I V I T Y

R I G S W E L L S - S L E F R A C C R E W S Y E 1 6 I D U C S

~4 ~60 ~1 ~60

* Assumes HH $2.50/Mcf

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C

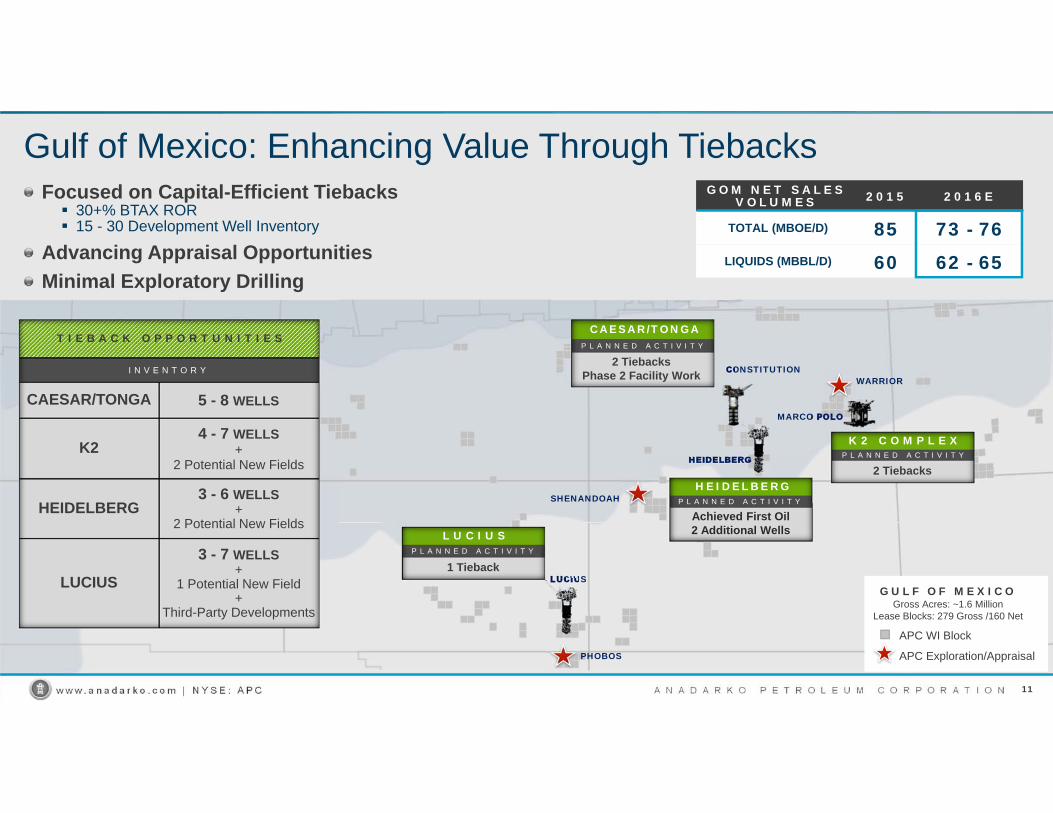

CONSTITUTION

MARCO POLO

LUCIUS

11

Gulf of Mexico: Enhancing Value Through TiebacksFocused on Capital-Efficient Tiebacks 30+% BTAX ROR 15 - 30 Development Well Inventory

Advancing Appraisal OpportunitiesMinimal Exploratory Drilling

HEIDELBERG

L U C I U SP L A N N E D A C T I V I T Y

1 Tieback

HEIDELBERGP L A N N E D A C T I V I T Y

Achieved First Oil2 Additional Wells

K 2 C O M P L E XP L A N N E D A C T I V I T Y

2 Tiebacks

CAESAR/TONGAP L A N N E D A C T I V I T Y

2 TiebacksPhase 2 Facility Work

G U L F O F M E X I C OGross Acres: ~1.6 Million

Lease Blocks: 279 Gross /160 Net

APC WI Block

APC Exploration/Appraisal

G O M N E T S A L E S V O L U M E S 2 0 1 5 2 0 1 6 E

TOTAL (MBOE/D) 85 73 - 76LIQUIDS (MBBL/D) 60 62 - 65

T I E B A C K O P P O R T U N I T I E S

I N V E N T O R Y

CAESAR/TONGA 5 - 8 WELLS

K24 - 7 WELLS

+2 Potential New Fields

HEIDELBERG3 - 6 WELLS

+2 Potential New Fields

LUCIUS

3 - 7 WELLS+

1 Potential New Field+

Third-Party Developments

WARRIOR

PHOBOS

SHENANDOAH

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O N

A F R I C A

Ghana & Algeria: Growing Higher-Margin Oil

Algeria 2+ Billion Barrels Cumulative Gross Production Flat YOY Volumes for <$40 Million Capital

Ghana Jubilee: Flat YOY Volumes for <$50 Million Capital TEN: First Oil Expected 3Q16

APC WI BlockOil FieldGas CondensateAppraisal AreaExport Pipeline

BLOCK 404A

PK0

BLOCK208

10 MILES16 KMS

OURHOUD CPF

HBNS CPF

EL MERK CPF

A L G E R I A

WEST CAPE THREE POINTS

MAHOGANY

TEAK

Jubilee Unit24% WI

20 MILES32 KMS

DEEPWATER TANO

NTOMME

Planned FPSO Location

TWENEBOA

WAWA

ENYENRA

TEN Complex19% WI

G H A N A

12

0

40

80

2011 2012 2013 2014 2015 2016E

MB

bl/d

Algeria Net Sales Volumes

0

20

40

2013 2014 2015 2016E 2017E 2018E

MB

OPD

Ghana Net Sales Volumes

Jubilee TEN

G H A N A &A L G E R I A

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O N

FID WHEN UNCERTAINTY

REMOVED

Mozambique LNG: Working Parallel Processes

APPROVE PLAN OF DEVELOPMENT

SECURE 8+ MMTPA SPAs

ADVANCE TOWARD ~2/3 LEVERAGE

Legal &Contractual Framework

OfftakeAgreements

Project Financing

MINIMAL 2016 CAPITAL REQUIRED

13

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C

2016 International & Deepwater Exploration ActivityG O M

L A N D P O S I T I O N

~1.7 MM Gross Acres2 0 1 6 A C T I V I T Y

PHOBOSAppraisal Well

SHENANDOAHAppraisal Well

WARRIORExploration Well

C O L O M B I AL A N D P O S I T I O N

~16 MM Gross Acres2 0 1 6 A C T I V I T Y

PURPLE ANGEL-1 Exploration Well GRAND COL

3D Seismic Acquisition

14

2 0 1 6 P L A N N E D A C T I V I T Y

C A P I T A L D R I L LT A R G E T N E T D I S C O V E R E D R E S O U R C E S

~$500Million

~8Wells

~250Million

C Ô T E D ’ I V O I R EL A N D P O S I T I O N

~1 MM Gross Acres2 0 1 6 A C T I V I T Y

PAON Appraisal Well

PELICAN Exploration WellROSSIGNOL

Exploration Well

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O N

Net Discovered Resources

~6.5 BBOE

~$14 Billion

Monetized

~5 BBOE ~250 MBOE/d

Resources RetainedNet Production

Exploration: Creating Unmatched Value with Optionality

15

D R I V I N G V A L U EE X P L O R I N G A P P R A I S I N G D E V E L O P I N G

Colombia Côte d’Ivoire GOM (Warrior)

Shenandoah Paon Phobos

Heidelberg TEN Mozambique LNG

~$10 Billion Capital Invested

w w w . a n a d a r k o . c o m | N Y S E : A P C A N A D A R K O P E T R O L E U M C O R P O R A T I O NA N A D A R K O P E T R O L E U M C O R P O R A T I O Nw w w . a n a d a r k o . c o m | N Y S E : A P C 16

Successfully Navigating a Volatile EnvironmentMaintain Financial Discipline and Invest Within Cash InflowsFocus on Value Reduce Capital Spending and Cost StructurePosition U.S. Onshore for the FutureCapitalize on Portfolio Diversification and FlexibilityContinue Active Monetization Program

PRODUCTION

EXPLORATION

EAST AFRICA

WEST AFRICA

GULF OF MEXICO

U.S. ONSHORENORTH AFRICA

ALASKA

COLOMBIA

NEW ZEALAND