school district of cape may point - new jersey district of cape may point cape may point board of...

TRANSCRIPT

SCHOOL DISTRICTOF

CAPE MAY POINT

Cape May Point Board of EducationCape May Point, New Jersey

Comprehensive Annual Financial ReportFor the Fiscal Year Ended June 30, 2012

of the

Comprehensive AnnualFinancial Report

Cape May Point Board of EducationCape May Point, New Jersey

For the Fiscal Year Ended June 30, 2012

Prepared by

Cape May Point Board of EducationFinance Department

CAPE MAY POINT SCHOOL DISTRICT

INTRODUCTORY SECTION

Letter of TransmittalOrganizational ChartRoster of OfficialsConsultants and Advisors

FINANCIAL SECTION

Independent Auditor's Report

K-I Report on Compliance and on Internal Control Over Financial Reporting Basedon an Audit of Financial Statements Performed in Accordance withGovernment Auditing Standards

Required Supplementary Informadon - Part IManagement's Discussion and Analysis

Basic Financial Statements

A. District-wide Financial Statements:

A-IA-2

Statement of Net AssetsStatement of Activities

B. Fund Financial Statements:

Governmental Funds:B-1 Balance SheetB-2 Statement of Revenues, Expenditures, and Changes in Fund BalancesB-3 Reconciliation of the Statement of Revenues, Expenditures, and Changes in

Fund Balances of Governmental Funds to the Statement of Activities

Proprietary Funds:B-4 Statement of Net AssetsB-5 Statement of Revenues, Expenses, and Changes in Fund Net AssetsB-6 Statement of Cash Flows

Fiduciary Funds:B-7 Statement of Fiduciary Net AssetsB-8 Statement of Changes in Fiduciary Net Assets

Notes to the Financial Statements

Page2678

10

12

15

2223

2526

27

N/AN/AN/A

2829

30

Required Supplementary Information - Part II

C. Budgetary Comparison Schedules

C-I Budgetary Comparison Schedule - General FundC-I a Combining Schedule of Revenues, Expenditures and Changes

in Fund Balance - Budget and Actual (if applicable)C-2 Budgetary Comparison Schedule - Special Revenue Fund

43

N/AN/A

Notes to the Required Supplementary InformationC-3 Budget-to-GAAP Reconciliation 45

Other Supplementary Information

D. School Level Schedules N/A

E. Special Revenue Fund N/A

F. Capital Projects Fund N/A

G. Proprietary Fund:

Enterprise Fund N/A

Internal Service Fund N/A

H. Fiduciary Funds:H-I Combining Statement of Fiduciary Net AssetsH-2 Combining Statement of Changes in Fiduciary Net AssetsH-3 Student Activity Agency Fund Schedule of Receipts and DisbursementsH-4 Payroll Agency Fund Schedule of Receipts and Disbursements

4849

N/A50

I. Long-Term Debt: N/A

STATISTICAL SECTION (Unaudited)

J-IJ-2J-3J-4J-5J-6J-7

Net Assets by ComponentChanges in Net Assets, Last Nine Fiscal YearsFund Balances, Governmental Funds, Last Nine Fiscal YearsChanges in Fund Balances, Governmental Funds, Last Eight Fiscal YearsGeneral Fund - Other Local Revenue by Source, Last Ten Fiscal YearsAssessed Value and Actual Value of Taxable Property, Last Ten Fiscal YearsDirect and Overlapping Property Tax Rates, Last Ten Fiscal Years

52535556575859

STATISTICAL SECTION (Unaudited) (Continued)

J-8 Principal Property Tax Payers, Current Year and Nine Years Ago 60J-9 Property Tax Levies and Collections, Last Ten Fiscal Years 61J-I0 Ratios of Outstanding Debt by Type 62i-n Ratios of Net General Bonded Debt Outstanding 63J-12 Ratios of Overlapping Governmental Activities Debt, As of December 31, 2011 64J-13 Legal Debt Margin Information, Last Ten Fiscal Years 65J-14 Demographic and Economic Statistics 66J-15 Principal Employers, Current Year & Nine Years Ago (information not available) N/AJ-16 Full-time Equivalent District Employees by Function/Program, Last Ten Fiscal Years 67J-17 Operating Statistics, Last Six Fiscal Years 68J-18 School Building Information 69J-19 Schedule of Required Maintenance 70J-20 Insurance Schedule 71

SINGLE AUDIT SECTION

K-2 Report on Compliance with Requirements Applicable to Each MajorProgram and on Internal Control Over Compliance in Accordance withOMB Circular A-133 and New Jersey OMB Circular Letter 04-04

Schedule of Expenditures of Federal Awards, Schedule ASchedule of Expenditures of State Financial Assistance, Schedule BNotes to the Schedules of Awards and Financial AssistanceSchedule of Findings and Questioned CostsSummary Schedule of Prior Audit Findings

N/AN/A73747679

K-3K-4K-5K-6K-7

Introductory Section

CAPE MAY POINT BOARD OF EDUCATION- PO Box 143 - Cape May Point, New Jersey 08212 - (609) 884-8485-

September 25, 2012

Honorable President andMembers of the Board of Education

Cape May Point School DistrictCounty of Cape May, New Jersey

Dear Board Members:

The Comprehensive Annual Financial Report (CAFR) of the Cape May Point SchoolDistrict for the fiscal year ended June 30, 2012 is hereby submitted. This CAFR includesthe District's Basic Financial Statements prepared in accordance with GovernmentalAccounting Standards Board Statement 34. Responsibility for both the accuracy of thedata and completeness and fairness of the presentation, including all disclosures, restswith the management of the Board of Education. To the best of our knowledge andbelief, the data presented in this report is accurate in all material respects and is reportedin a manner designed to present fairly the financial position and results of operations ofthe various funds and account groups of the District. All disclosures necessary to enablethe reader to gain an understanding of the District's financial activities have beenincluded.

The Comprehensive Annual Financial Report is presented in four sections: Introductory,Financial, Statistical and Single Audit. The Introductory Section includes this transmittalletter, the District's organizational chart and a list of principal officials. The FinancialSection includes the general-purpose financial statements and schedules, as well as theauditor's report thereon. The Statistical Section includes selected financial anddemographic information, generally presented on a multi-year basis. The District isrequired to undergo an annual single audit in conformity with the provisions of the SingleAudit Act of 1984 and the U.S. Office of Management and Budget Circular A-133,"Audits of States, Local Governments and Non-Profit Organizations," and New JerseyOMS's Circular 04-04, "Single Audit Policy for Recipients of Federal Grant, StateGrants and State Aid." Information related to this single audit, including the auditor'sreport on the internal control structure and compliance with applicable laws andregulations and findings and recommendations, are included in the single audit section ofthis report.

2

1. REPORTING ENTITY AND ITS SERVICES:

Cape May Point School District is an independent reporting entity within the criteriaadopted by the GASB as established by GASB Statement No. 14. All funds and accountgroups of the District are included in this report. The Cape May Point Board ofEducation and its school constitute the District's reporting entity.

The District is a sending district and operates no schools and/or facilities. Students aresent on a tuition basis to Cape May City Elementary School for grades PreK-6 and toLower Cape May Regional School District for grades 7-12. They are sent to the SpecialServices District when appropriate. The District completed the 2011-12 school year withan enrollment of 5 students. The following details the changes in the student enrollmentof the District over the last nine years.

Average Daily EnrollmentFiscal Student PercentYear Enrollment Change

2011-12 5.0 -16.67%2010-11 6.0 20.00%2009-10 5.0 66.67%2008.Q92007.Q82006.Q72005.Q62004.Q52003.Q4

3.04.06.08.0

to.O10.0

-25.00%-33.33%-25.00%-20.00%

0.00%42.86%

2. ECONOMIC CONDITION AND OUTLOOK:

The Borough of Cape May Point is a relatively affluent area. The majority of taxpayersare summer residents. There is minimal expansion and development occurring at presentdue to a weak economy and lack of property available for development.

3. MAJOR INITIATIVES:

The Cape May Point School District relies on its receiving districts for curriculum, schoolmanagement and accomplishments of our students. Board members may attend Boardmeetings of the Cape May City and Lower Cape May Regional districts but have novoting rights at present.

3

4. INTERNAL ACCOUNTING CONTROLS:

Management of the District is responsible for establishing and maintaining an internalcontrol structure designed to ensure that the assets of the District are protected from loss,theft or misuse and to ensure that adequate accounting data are compiled to allow for thepreparation of financial statements in conformity with accounting principles generallyaccepted in the United States of America (GAAP). The internal control structure isdesigned to provide reasonable, but not absolute, assurance that these objectives are met.The concept of reasonable assurance recognizes that: (1) the cost of a control should notexceed the benefits likely to be derived; and (2) the valuation of costs and benefitsrequires estimate and judgments by management.

As a recipient of state financial assistance, the District also is responsible for ensuringthat an adequate internal control structure is in place to ensure compliance withapplicable laws and regulations related to those programs. This internal control structureis also subject to periodic evaluation by the District management.

5. BUDGETARY CONTROLS:

In addition to internal accounting controls, the District maintains budgetary controls. Theobjective of these budgetary controls is to ensure compliance with legal provisionsembodied in the annual appropriated budget approved by the voters of the municipality.Annual appropriated budgets are adopted for the general fund and the special revenuefund. Project-length budgets are approved for the capital improvements accounted for inthe capital projects fund. The final budget amount as amended for the fiscal year isreflected in the financial section.

An encumbrance accounting system is used to record outstanding purchase commitmentson a line item basis. Open encumbrances at year-end are either canceled or are includedas reappropriations of fund balance in the subsequent year. Those amounts to bereappropriated are reported as reservations of fund balance at June 30, 2012.

6. ACCOUNTING SYSTEMS AND REPORTS:

The District's accounting records reflect generally accepted accounting principles, aspromulgated by the Governmental Accounting Standards Board (GASB). Theaccounting system of the District is organized on the basis of funds and account groups.These funds and account groups are explained in "Notes to the Financial Statements,"Note 1.

4

7. CASH MANAGEMENT:

The investment policy of the District is guided in large part by state statute as detailed in"Notes to the Financial Statements," Note 2. The District has adopted a cashmanagement plan that requires it to deposit public funds in public depositories protectedfrom loss under the provisions of the Governmental Unit Deposit Protection Act("GUDPA"). GUDPA was enacted in 1970 to protect governmental units from a loss offunds on deposit with a failed banking institution in New Jersey. The law requiresgovernmental units to deposit public funds only in public depositories located in NewJersey, where the funds are secured in accordance with the Act.

8. RISK MANAGEMENT:

The Board carried various forms of insurance, including but not limited to generalliability and fidelity bonds.

9. OTHER INFORMATION:

State statutes require an annual audit by independent certified public accountants orregistered municipal accountants. The accounting firm of Inverso & Stewart, LLC, wasselected by the Board of Education. In addition to meeting the requirements set forth instate statutes, the audit also was designed to meet the requirements of the Single AuditAct of 1984 and the related OMB Circular A-l33 and New Jersey OMB's Circular 04-04.The auditor's report on the general-purpose financial statements and combining andindividual fund statements and schedules is included in the financial section of thisreport.

Respectfully submitted,

Rose M. MillarBoard Secretary/Business Administrator

5

CAPE MAY POINT BOARD OF EDUCATION

Organizational Chart(UNIT CONTROL)

Board of Education

Board Secretary I· Treasurer

6

CAPE MAY POINT BOARD OF EDUCATIONCAPE MAY POINT, NEW JERSEY

ROSTER OF OFFICIALSJUNE 30, 2012

Members of the Board of EducationTerm

Expires

Alice Gibson - President

Joan Brown - Vice-President

Meredith Scott - Member

2013

2014

2012

Other OfficialsRose Millar, Board Secretary &

School Business Administrator

Francine Springer, Treasurer of School Monies

7

CAPE MAY POINT SCHOOL DISTRICTConsultants and Advisors

Audit Firm

Inverso & Stewart, LLC12000 Lincoln Drive West, Suite 402

Marlton, NJ 08053

Official Depository

Cape Savings Bank225 North Main Street

Cape May Court House, NJ 08210

8

Financial Section

INVERSO & STEWART, LLC

Certified Public AccountantsRegistered Municipal Accountants

12000 Uncoln Drive West. Suite 402Marlton. New Jeney 08653(856) 983-2244Fax (856) 983-6674E-Ma1l: IscpaS@-conc;entrlc;.net

-Member of-American Institute of CP AsNew Jeney Society ofCPAs

INDEPENDENT AUDITOR'S REPORT

The Honorable President and Membersof the Board of Education

Cape May Point School DistrictCounty of Cape MayCape May Point, New Jersey

We have audited the accompanying fmancial statements of the governmental activities, the business-type activities, eachmajor fund and the aggregate remaining fund information of the Cape May Point School District, in the County of CapeMay, State of New Jersey (School District), as of and for the fiscal year ended June 30, 2012, which collectively comprisethe School District's basic financial statements as listed in the table of contents. These financial statements are theresponsibility of the School District's management. Our responsibility is to express opinions on these financial statementsbased on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America; thestandards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller Generalof the United States; and in compliance with audit requirements as prescribed by the Division of Finance, Department ofEducation, State of New Jersey. Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material misstatement. An audit includes consideration ofinternal control over financial reporting as a basis for designing audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on the effectiveness of the School District's internalcontrol over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis,evidence supporting the amounts and disclosures in the fmancial statements. An audit also includes assessing theaccounting principles used and significant estimates made by management, as well as evaluating the overall fmancialstatement presentation. We believe that our audit provides a reasonable basis for our opinions.

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financialposition of the governmental activities, business-type activities, each major fund and the aggregate remaining fundinformation of the Cape May Point School District, in the County of Cape May, State of New Jersey, as of June 30, 2012,and the respective changes in financial position and, where applicable, cash flows thereof for the fiscal year then ended inconformity with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated September 7, 2012 on ourconsideration of the Cape May Point School District, in the County of Cape May, State of New Jersey's internal controlover financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grantagreements and other matters. The purpose of that report is to describe the scope of our testing of internal control overfinancial reporting and compliance and the results of that testing, and not to provide an opinion on the internal controlover financial reporting or on compliance. That report is an integral part of an audit performed in accordance withGovernment Auditing Standards and should be considered in assessing the results of our audit.

10

The accompanying management's discussion and analysis and budgetary comparison information, as listed in the table ofcontents, are not a required part of the basic financial statements but are supplementary information required byaccounting principles generally accepted in the United States of America. We have applied certain limited procedures,which consisted principally of inquiries of management regarding the methods of measurement and presentation of therequired supplementary information. However, we did not audit the information and express no opinion on it.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise theCape May Point School District's basic financial statements. The accompanying Schedule of Expenditures of FederalAwards and State Financial Assistance are presented for purposes of additional analysis as required by U.S. Office ofManagement and Budget Circular A-l33, Audits of States. Local Governments, and Non-Profit Organizations and Stateof New Jersey Circular 04-04-0MB, Single Audit Policy for Recipients of Federal Grants, State Grants and State Aid,and are not a required part of the financial statements. In addition, the introductory section, combining statements andrelated major fund supporting statements and schedules, and statistical section listed in the' table of contents are alsopresented for purposes of additional analysis and are not a required part of the basic financial statements. The Schedulesof Expenditures of Federal Awards and State Financial Assistance, combining statements and related major fundsupporting statements and schedules have been subjected to the auditing procedures applied in the audit of the basicfinancial statements and, in our opinion, are fairly stated in all material respects in relation to the basic fmancialstatements taken as a whole. The introductory and statistical sections have not been subjected to the auditing proceduresapplied in the audit of the basic financial statements, and accordingly, we express no opinion on them.

Respectfully submitted,

INVERSO & STEWART, LLCCertified Public Accountants

!}rpJ-Robert P. InversoCertified Public AccountantRegistered Municipal Accountant

Marlton, New JerseySeptember 7, 2012

11

INVERSO & STEWART, LLC

Certified Public AccountantsRegistered Municipal Accountants

12000 Uncoln Drive West, Suite 402Marlton, New Jersey 08053(856) 983-2244Fax (856) 983-6674E-Mail: [email protected]

-Member of-American Institute of CPAsNew Jersey Society of CPAs

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTINGAND ON COMPLIANCE AND OTHER MATIERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCEWITH GOVERNMENT AUDITING STANDARDS

The Honorable President and Membersof the Board of Education

Cape May Point School DistrictCounty of Cape MayCape May Point. New Jersey

We have audited the financial statements of the governmental activities, the business-type activities, each major fund andthe aggregate remaining fund information of the Cape May Point School District (School District), in the County of CapeMay , State of New Jersey, as of and for the fiscal year ended June 30, 2012, which collectively comprise the SchoolDistrict's basic financial statements and have issued our report thereon dated September 7, 2012. We conducted our auditin accordance with auditing standards generally accepted in the United States of America; the standards applicable tofinancial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; andin compliance with audit requirements as prescribed by the Division of Finance, Department of Education, State of NewJersey.

Internal Control Over Financial Reporting

Management of the Cape May Point School District is responsible for establishing and maintaining effective internalcontrol over financial reporting. In planning and performing our audit, we considered the Cape May Point SchoolDistrict's internal control over fmancial reporting as a basis for designing our auditing procedures for the purpose ofexpressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectivenessof the School District's internal control over financial reporting. Accordingly, we do not express an opinion on theeffectiveness of the School District's internal control over financial reporting.

A deficiency in internal control exists when the design or operation of a control does not allow management oremployees, in the normal course of performing their assigned functions, to prevent, or detect and correct misstatements ona timely basis. A material weakness is a deficiency, or combination of deficiencies, in internal control, such that there is areasonable possibility that a material misstatement of the School District's financial statements will not be prevented, ordetected and corrected on a timely basis.

Our consideration of internal control over financial reporting was for the limited purpose described in the first paragraphof this section and was not designed to identify all deficiencies in internal control over financial reporting that might bedeficiencies, significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control overfmancial reporting that we consider to be material weaknesses, as defined above.

12

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Cape May Point School District's financial statements arefree of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contractsand grant agreements, noncompliance with which could have a direct and material effect on the determination of fmancialstatement amounts. However, providing an opinion on compliance with those provisions was not an objective of ouraudit and, accordingly, we do not express such an opinion. The results of our tests disclosed no instances ofnoncompliance or other matters that are required to be reported under Government Auditing Standards and auditrequirements as prescribed by the Division of Finance, Department of Education, State of New Jersey.

This report is intended solely for the information and use of the management of the School District, the Division ofFinance, Department of Education, State of New Jersey, and federal and state awarding agencies and pass-through entitiesand is not intended to be and should not be used by anyone other than these specified parties.

Respectfully submitted,

INYERSO & STEWART, LLCCertified Public Accountants

Robert P. InversoCertified Public AccountantRegistered Municipal Accountant

Marlton, New JerseySeptember 7,2012

13

Required Supplementary Information - Part I

Management's Discussion and Analysis

Cape May Point School DistrictManagement's Discussion and AnalysisFor the Fiscal Year Ended June 30,2012

As management of the Board of Education of the Cape May Point School District in Cape May NewJersey, we offer readers of the School District's financial statements this narrative overview and analysis ofthe School District for the fiscal year ended June 30, 2012. We encourage readers to consider theinformation presented in conjunction with additional information that we have furnished in our letter oftransmittal, which can be found in the introductory section of this report.

Financial HighUghts

• The assets of the School District exceeded its liabilities at the close of the most recent fiscalyear by $109,153 (net assets).

• Governmental activities have unrestricted net assets of $96,965.

• The total net assets of the School District decreased by $25,807, or a 19.12% decrease fromthe prior fiscal year-end balance.

• Fund balance of the School District's governmental funds decreased by $25,807 resulting inan ending fund balance of $109,153. This decrease is due to the results of operations of thegeneral fund.

Overview of the Basic Financial Statements

This discussion and analysis is intended to serve as an introduction to the School District's basic financialstatements. Comparison to the prior year's activity is provided in this document. The basic fmancialstatements are comprised of three components: 1) District-wide financial statements, 2) Fund financialstatements, and 3) Notes to the basic financial statements. This report also contains other supplementaryinformation in addition to the basic financial statements themselves.

District-wide Financial Statements

The district-wide financial statements are designed to provide the reader with a broad overview of thefinancial activities in a manner similar to a private-sector business. The district-wide financial statementsinclude the statement of net assets and the statement of activities.

The statement of net assets presents information about all of the School District's assets and liabilities. Thedifference between the assets and liabilities is reported as net assets. Over time, changes in net assets mayserve as a useful indicator of whether the financial position of the School District is improving ordeteriorating.

The statement of activities presents information showing how the net assets of the School District changedduring the current fiscal year. Changes in net assets are recorded in the statement of activities when theunderlying event occurs, regardless of the timing of related cash flows. Thus, revenues and expenses arereported in this statement even though the resulting cash flows may be recorded in a future period.

The district-wide fmancial statements distinguish functions of the School District that are supported fromtaxes and intergovernmental revenues (governmental activities). Governmental activities consolidategovernmental funds including the General Fund, Special Revenue Fund, Capital Projects Fund, and DebtService Fund. The District maintains no Business-type activities.

15

Fund Financial Statements

Fund financial statements are designed to demonstrate compliance with finance-related requirements. Afund is a grouping of related accounts that is used to maintain control over resources that have beensegregated for specific objectives. All of the funds of the School District are divided into three categories:governmental funds, proprietary funds andfiduciary funds.

Governmental funds account for essentially the same information reported in the governmental activities ofthe district-wide fmancial statements. However, unlike the district-wide financial statements, thegovernmental fund financial statements focus on near-term financial resources and fund balances. Suchinformation may be useful in evaluating the financing requirements in the near term.

Since the governmental funds and the governmental activities report information using the same functions,it is useful to compare the information presented. Because the focus of each report differs, a reconciliationis provided on the fund financial statements to assist the reader in comparing the near-term requirementswith the long-term needs.

The School District maintains one individual governmental fund. The major fund is the General Fund.

The School District adopts an annual appropriated budget for the General Fund. A budgetary comparisonstatement has been provided to demonstrate compliance with budgetary requirements.

Proprietary funds are used to present the same functions as the business-type activities presented in thedistrict-wide financial statements. The School District maintains no proprietary funds.

Fiduciary funds are used to account for resources held for the benefit of parties outside the government.Fiduciary funds are not reflected in the district-wide financial statements because the resources of thosefunds are not available to support the School District's programs.

Notes to the Basic Financial Statements

The notes to the basic financial statements provide additional information that is essential to a fullunderstanding of the data provided in the basic financial statements.

Other Information

In addition to the basic fmancial statements and accompanying notes, this report also contains othersupplementary information and schedules required by the New Jersey Audit Program, issued by the NewJersey Department of Education.

District-wide Financial Analysis

The assets of the School District are classified as current assets and capital assets. Cash, investments,receivables, inventories and prepaid expenses are current assets. These assets are available to provideresources for the near-term operations of the School District. The majority of the current assets are theresults of the tax levy and state aid collection process.

Current and long-term liabilities are classified based on anticipated liquidation either in the near-term or inthe future. Current liabilities include accounts payable, accrued salaries and benefits, unearned revenues,and current debt obligations. The liquidation of current liabilities is anticipated to be either from currentlyavailable resources, current assets or new resources that become available during fiscal year 2012.

16

Cape May Point School DistrictComparative Summary of Net Assets

As of June 30, 2012 and 2011

Governmental Activities

2012 2011

Assets:Current assets S 109,190 S 135,052

Capital assets

Total assets 109,190 135,052

Liabilities:Current Liabilities 37 92

Noncurrent Liabilities

Total liabilities 37 92

Net assets S 109,153 S 134,960

Net assets consist of:Restricted net assets S 12,188 S 12,188

Unrestricted net assets 96.965 122,772

Net assets S 109,IS3 S I34z96O

Governmental Activities

Governmental activities decreased the net assets of the School District by $25,807 during the current fiscalyear. Key elements of the decrease in net assets for governmental activities are as follows:

• The decrease is due to the results of operations in the General Fund.

17

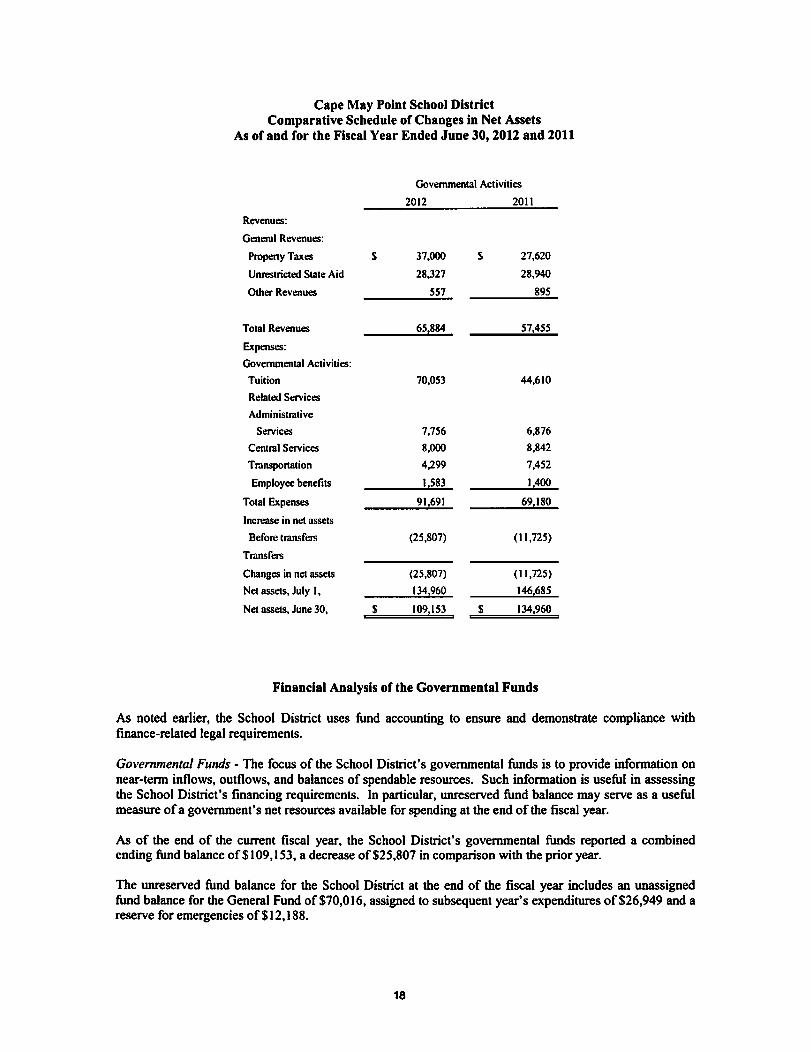

Cape May Point School DistrictComparative Schedule of Changes in Net Assets

As of and for the Fiscal Year Ended June 30t 2012 and 2011

Governmental Activities

2012 2011

Revenues:

General Revenues:

Property Taxes S 37,000 S 27,620

Unrestricted State Aid 28,327 28,940

Other Revenues 557 895

Total Revenues 65884 57.455

Expenses:Governmental Activities:Tuition 70,053 44,610

Related ServicesAdministrative

Services 7,756 6,876

Central Services 8,000 8,842

Transportation 4,299 7,452

Employee benefits 1583 1400

Total Expenses 91691 69180

Increase in net assetsBefore transfers (25,807) (11,725)

Transfers

Changes in net assets (25,807) (11,725)Net assets, July I, 1341960 1461685

Net assets, June 30, S 109,153 S 134.960

Financial Analysis of the Governmental Funds

As noted earlier, the School District uses fund accounting to ensure and demonstrate compliance withfinance-related legal requirements.

Governmental Funds - The focus of the School District's governmental funds is to provide information onnear-term inflows, outflows, and balances of spendable resources. Such information is useful in assessingthe School District's financing requirements. In particular, unreserved fund balance may serve as a usefulmeasure of a government's net resources available for spending at the end of the fiscal year.

As of the end of the current fiscal year, the School District's governmental funds reported a combinedending fund balance of $1 09,153, a decrease of $25,807 in comparison with the prior year.

The unreserved fund balance for the School District at the end of the fiscal year includes an unassignedfund balance for the General Fund of $70,0 16, assigned to subsequent year's expenditures of $26,949 and areserve for emergencies of $12,188.

18

General Fund Budgetary Highlights

At the end of the current fiscal year, unreserved fund balance (budgetary basis) of the general fund was$72,777 and total fund balance (budgetary basis) was $111,914. As a measure of the general fund'sliquidity, it may be useful to compare both unreserved fund balance (budgetary basis) and total fundbalance (budgetary basis) to total general fund expenditures. Actual (budgetary basis) expenditures of theGeneral Fund including other financing uses amounted to $91,691. Unreserved fund balance (budgetarybasis) represents 79.37% of expenditures and total fund balance (budgetary basis) represents 122.06% ofthat same amount.

Capital Assets

The School District does not have any capital assets.

Debt Administration

At June 30, 2012, the District did not have outstanding debt issues.

For the Future

The Cape May Point School District is in good financial condition presently. Cape May Point is aresidential community, with few large ratables; thus the burden is focused on homeowners to share the taxburden. The 2012-2013 Budget reflects an increase in the local tax levy of$740 which represents a slightincrease in the tax rate.

In conclusion, the Cape May Point School District has committed itself to fmancial excellence. The SchoolDistrict plans to continue its sound fiscal management to meet the challenges of the future.

Requests for Information

This fmancial report is designed to provide a general overview of the School District's finances for allthose with an interest in the School District. Questions concerning any of the information provided in thisreport or requests for additional financial information should be addressed to the Cape May Point SchoolDistrict Business Administrator, P.O. Box 143, Cape May Point, NJ 08212.

19

Basic Financial Statements

District-Wide Financial Statements

A-1CAPE MAY POINT SCHOOL DISTRICT

Statement of Net AssetsJune 30, 2012

Governmental Business-TypeActivities Activities Total

ASSETS:Cash and Cash Equivalents $104,500 $104.500Accounts Receivable 4,690 4.690

Total Assets 109,190 109.190

UABIUnES:Other Liabilities 37 37

Total Liabilities 37 37

NET ASSETS:Restricted for:

General Fund 12,188 12.188Unrestricted 96,965 96.965

Total Net Assets $1091153 $109.153

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.22

Pr2

CAPE MAY POINT SCHOOL DISTRICTStatement of AcUvlUes

For the RscaJ Year Ended June 30, 2012

Program RevenuesNet (Expense) Revenue and

Changes In Net Assets

ExpensesCharges for

Services

OperaUng CapitalGrants and Grants and

ContrfbuUons ContrfbuUonsGovernmental

AcUvlUesBusiness-Type

AcUvlUes Total

Governmental Activities:Support SetVices:

TuitionGeneral administrative servicesCentral servicesPupil IlanSpoJtationEmployee benefits

Total Govemmental Activities

Business-Type Activities:

Total Business-Type Activities

Total Primary Govemment

70,053 ($70,053) (70.053)7,756 (7,756) (7.756)8.000 (8,000) (8,000)4,299 (4,299) (4,299)1,583 (1,583) (1,583)

91,691 (91,691) (911691}

$91,691 (91,691)(91,691)

General Revenues:Taxes:

Property taxes, levied for general purposes, netFederal and State aid not restrictedMiscellaneous income

37,000 37,00028,327 28,327

557 557

65,884 65,884(25,807) (25.807)

134,960 134.960$109,153 $109.153

Total general revenues, special items, and transfersChange in Net Assets

Net Assets - July 1Net Assets - June 30

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

Fund Financial Statements

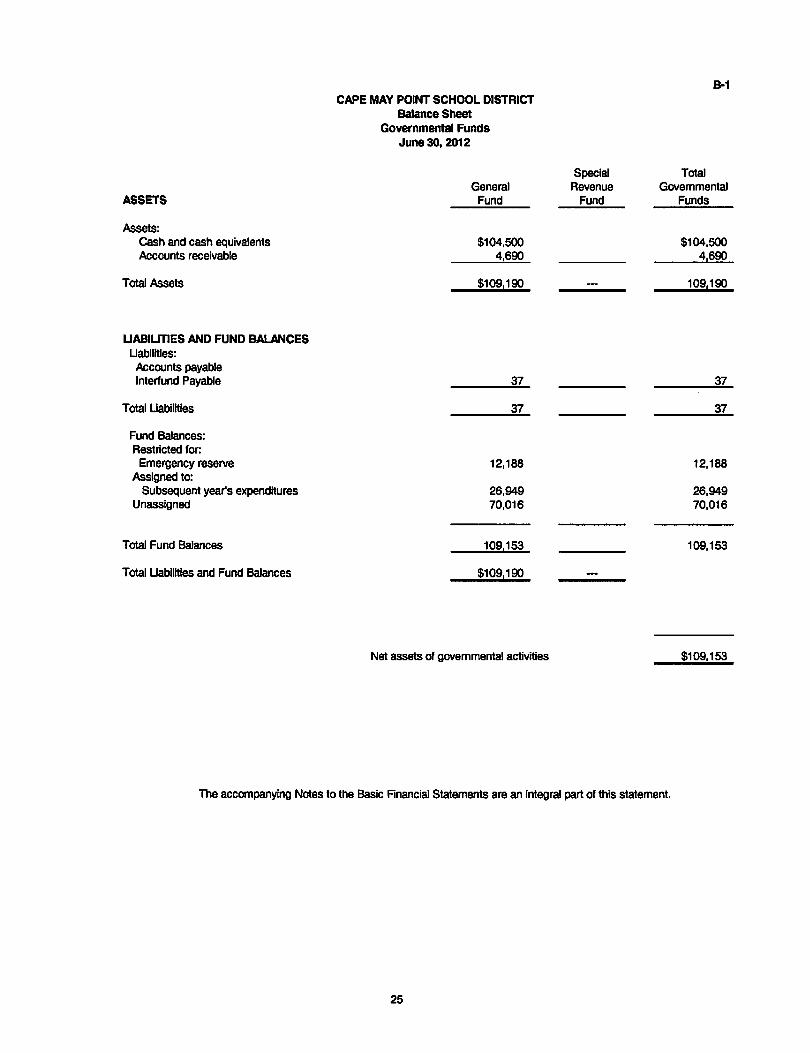

B-1CAPE MAY POINT SCHOOL DISTRICT

Balance SheetGovernmental Funds

June 30,2012

ASSETSGeneral

Fund

SpecialRevenue

Fund

TotalGovemmental

Funds

Assets:Cash and cash equivalentsAccounts receivable

$104,5004,690

$104,5004,690

Total Assets $109,190 109,190

UABlUTIES AND FUND BALANCESUabilities:Accounts payableInterfund Payable 37 37

Total Uabilities 37 37

Fund Balances:Restricted for:

Emergency reserve 12,188 12,188Assigned to:

Subsequent year's expenditures 26,949 26,949Unassigned 70,016 70,016

Total Fund Balances 109,153 109,153

Total Uabilities and Fund Balances $109,190

Net assets of govemmental activities $109,153

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

25

B-2CAPE MAY POINT SCHOOL DISTRICT

Statement of Revenues, Expenditures and Changes In Fund BalancesGovernmental Funds

For the RscaJ Year Ended June 30, 2012

REVENUES:Local sources:

Local tax levyMiscellaneous

Special TotalGeneral Revenue Governmental

Fund Fund Funds

$37,000 $37,000557 557

37,557 37,557

28,327 28,327

65.884 65.884

Total local sources

State sourcesFederal sources

Total Revenues

EXPENDITURES:Current expense:

Support services and undistributed costs:TuiUonStudent and instruction related servicesGeneral administrative servicesCentral servicesPupil transportationUnallocated benefits

70.053 70,053

7,756 7,7568,000 8,0004,299 4,2991.583 1.583

91.691 91.691

(25,807) (25,807)134.960 134.960

$109,153 !109.153

Total Expenditures

Net Change in Fund BalancesFund Balances· July 1

Fund Balances· June 30

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

26

CAPE MAY POINT SCHOOL DISTRICTReconciliation of the Statement of Revenues, expenditures

and Changes In Fund Balances of Governmental Fundsto the Statement of ActIvities

For the Fiscal Year Ended June 30,2012

Total Net Change in Fund Balances - Governmental Funds (from B-2) ($25.807)

Amounts reported for governmental activities in the statement of activities (A-2)are different because:

None

Change In Net Assets of Governmental Activities ($25.807)

The accompanying Notes to the Basic Rnancial Statements are an integral part of this statement.

27

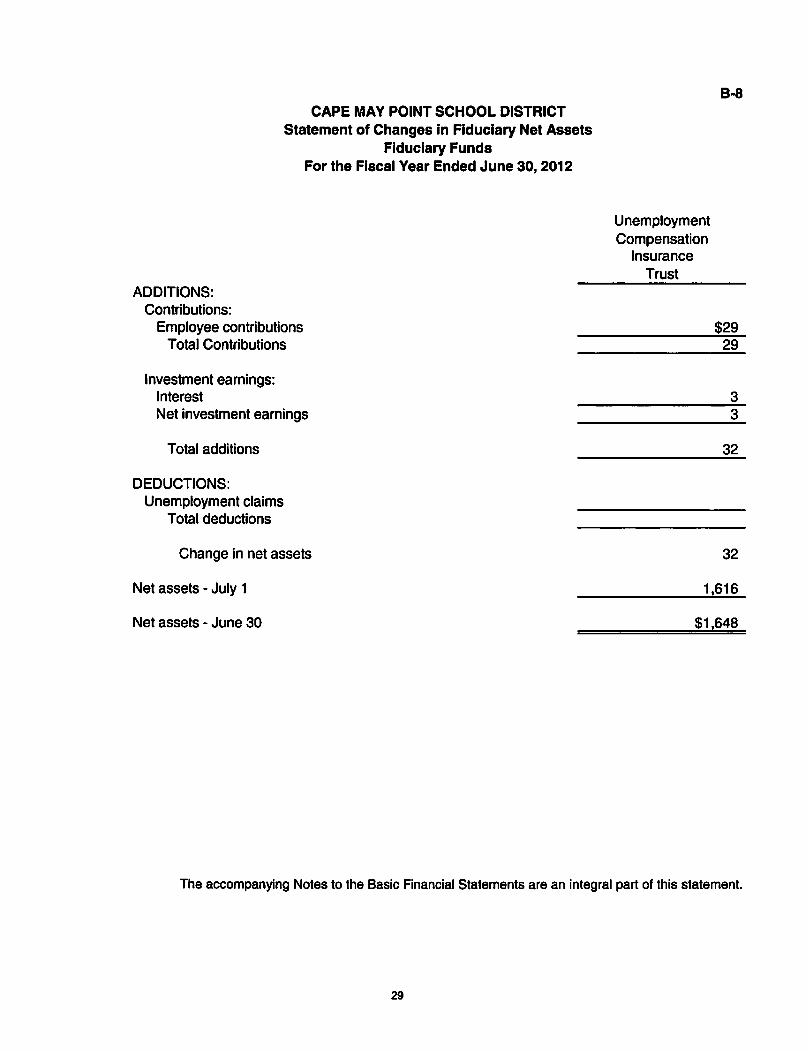

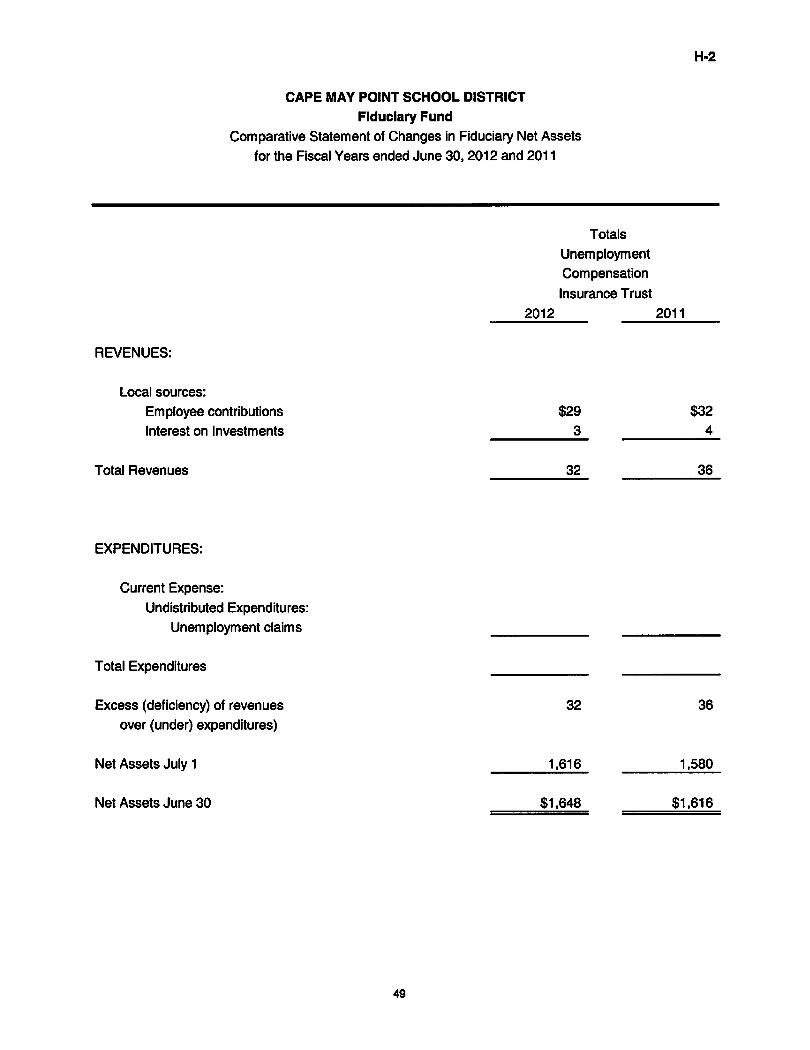

CAPE MAY POINT SCHOOL DISTRICTStatement of Fiduciary Net Assets

Fiduciary FundsJune 30, 2012

UnemploymentCompensation

InsuranceTrust

ASSETS:Cash and cash equivalentsInterfund Receivable

$1,61137

Total assets $1,648

LIABILITIES:Interfund payableDue to student groups

Total liabilities

NET ASSETS:Held in trust for unemployment

claims and other purposes $1,648

9-7

AgencyFund

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

28

8·8CAPE MAY POINT SCHOOL DISTRICT

Statement of Changes in Fiduciary Net AssetsFiduciary Funds

For the Fiscal Year Ended June 30, 2012

UnemploymentCompensation

InsuranceTrust

ADDITIONS:Contributions:

Employee contributionsTotal Contributions

$2929

Investment earnings:InterestNet investment earnings

33

Total additions 32

DEDUCTIONS:Unemployment claims

Total deductions

Change in net assets 32

Net assets - July 1 1,616

Net assets - June 30 $1,648

The accompanying Notes to the Basic Financial Statements are an integral part of this statement.

29

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30, 2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Reporting Entity - The Cape May Point School District (District) is located in Cape May County, New Jersey. It isorganized under the Constitution of the State of New Jersey, and is considered a non-operating school district as allstudents are transported to various other school districts located within the region. Students in grades K through 6 aretransported to the Cape May Point School District and students in grades 7 through 12 are transported to the Lower CapeMay Regional School District. The District is managed under a locally elected Board form of government consisting ofthree members elected to three-year terms. The terms are staggered so that a least one member's term expires each year.The District sends approximately 5 students.

The primary criteria for including activities within the School District's reporting entity, as set forth in Section 2100 of theGovernmental Accounting Standards Board (GASB) Codification of Governmental Accounting and Financial ReportingStandards is the degree of oversight responsibility maintained by the School District. Oversight responsibility includesfinancial interdependency, selection of governing authority, designation of management, ability to significantly influenceoperations and accountability for fiscal matters. The combined financial statements include all funds of the School districtover which the Board exercises operating control. There were no additional entities required to be included in the reportingentity under the criteria as described above. Furthermore, the School District is not includable in any other reporting entityon the basis of such criteria.

Basis of Presentation

The basic fmancial statements of the School District have been prepared in conformity with accounting principles generallyaccepted in the United States of America (GAAP) as applied to governmental units. The Governmental AccountingStandards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financialreporting principles. The School District also applies Financial Accounting Standards Board (FASB) Statements andInterpretations issued on or before November 30, 1989 to its governmental and business-type activities and to itsproprietary funds, provided they do not conflict with or contradict GASB pronouncements. The more significant of theSchool District's accounting policies are described below.

The School District's basic financial statements consists of government-wide statements, including a statement of net assetsand a statement of activities, and fund financial statements, which provide a more detailed level of financial information.

Government-wide Statements - The statement of net assets and the statement of activities display informationabout the School District as a whole. These statements include the financial activities of the primary government,except for fiduciary funds. The statements distinguish between those activities of the School District that aregovernmental and those that are considered business-type activities. The statement of net assets presents thefinancial condition of the governmental and business-type activities of the School District at fiscal year-end. Thestatement of activities presents a comparison between direct expenses and program revenues for each program orfunction of the School District's governmental activities and for the business-type activities of the School District.Direct expenses are those that are specifically associated with a service, program or department and, therefore,clearly identifiable to a particular function. The policy of the School District is to not allocate indirect expenses tofunctions in the statement of activities. Program revenues include charges paid by the recipient of the goods orservices offered by the program, grants and contributions that are restricted to meeting the operational or capitalrequirements of a particular program and interest earned on grants that is required to be used to support a particularprogram. Revenues, which are not classified as program revenues, are presented as general revenues of the SchoolDistrict, with certain limited exceptions. The comparison of direct expenses with program revenues identifies theextent to which each business segment or governmental function is self-fmancing or draws from the generalrevenues of the School District.

30

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30,2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Fund Financial Statements - During the fiscal year, the School District segregates transactions related to certainSchool District functions or activities in separate funds in order to aid financial management and to demonstratelegal compliance. Fund financial statements are designed to present financial information of the School District atthis more detailed level. The focus of governmental and enterprise fund financial statements is on major funds.Each major fund is presented in a single column. The fiduciary fund is reported by type. The School District usesfunds to maintain its financial records during the fiscal year. A fund is defined as a fiscal and accounting entity witha self-balancing set of accounts. There are three categories of funds: governmental, proprietary, and fiduciary.

Governmental Funds - Governmental funds are those through which most governmental functions typically are financed.Governmental fund reporting focuses on the sources, uses and balances of current financial resources. Expendable assetsare assigned to the various governmental funds according to the purposes for which they mayor must be used. Currentliabilities are assigned to the fund from which they will be paid. The difference between governmental fund assets andliabilities is reported as fund balance. The following are the School District's major governmental funds:

General Fund - The general fund is the general operating fund of the School District and is used to account for allfinancial resources except those required to be accounted for in another fund. Included are certain expenditures forvehicles and movable instructional or non-instructional equipment classified in the capital outlay sub-fund.

As required by the New Jersey State Department of Education, the School District includes budgeted capital outlayin this fund. Accounting principles generally accepted in the United States of America as they pertain togovernmental entities state that general fund resources may be used to directly finance capital outlays for long-livedimprovements as long as the resources in such cases are derived exclusively from unrestricted revenues.

Resources for budgeted capital outlay purposes are normally derived from State of New Jersey aid, district taxes andappropriated fund balance. Expenditures are those which result in the acquisition of or additions to capital assets forland, existing buildings, improvements of grounds, construction of buildings, additions to or remodeling of buildingsand the purchase of built-in equipment.

In addition to the capital outlay sub-fund, the School District is accountable for an additional sub-fund, the EducationJobs Fund (''Ed Jobs"), resulting from federal legislation signed into law on August 10,2010. The Ed Jobs programwas created to provide funding assistance to states in order to save or create education jobs for the period from theSeptember 30, 2010 through September 30, 2012. Jobs funded under this program include those that provideeducational and related services for early childhood, elementary, and secondary education. Ed Jobs revenues andexpenditures are recorded in the general fund (fund 18) on a reimbursement basis. As such, revenue is not includedin the fiscal year surplus, and no portion of general fund balance at June 30, 2012 is considered to be attributable toEd Jobs. Ed Jobs expenditures are included as a component of overall general fund expenditures, and are alsoincluded in general fund expenditures for purposes of the excess surplus calculation.

Fiduciary Funds - Fiduciary fund reporting focuses on net assets and changes in net assets. The fiduciary fund category issplit into two classifications: trust funds and agency funds. Agency funds are used to account for assets held by the SchoolDistrict in a trustee capacity or as an agent for individuals, private organizations, other governments, and/or other funds(i.e. payroll and student activities). They are custodial in nature (assets equal liabilities) and do not involve measurementof results of operations. The School District has two fiduciary funds; an unemployment compensation trust fund and apayroll fund.

31

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30, 2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Measurement Focus

Government-wide Financial Statements - The government-wide financial statements are prepared using the economicresources measurement focus. All assets and all liabilities associated with the operation of the School District are includedon the statement of net assets.

Fund Financial Statements - All governmental funds are accounted for using a flow of current financial resourcesmeasurement focus. With this measurement focus, only current assets and current liabilities generally are included on thebalance sheet. The statement of revenues, expenditures and changes in fund balances reports on the sources (i.e. revenuesand other financing sources) and uses (i.e. expenditures and other financing uses) of current financial resources. Thisapproach differs from the manner in which the governmental activities of the government-wide financial statements areprepared. Governmental fund financial statements, therefore, include a reconciliation with brief explanations to betteridentify the relationship between the government-wide statements and the statements for governmental funds.

Like the government-wide statements, all proprietary fund types are accounted for on a flow of economic resourcesmeasurement focus. All assets and all liabilities associated with the operation of these funds are included on the statementof net assets. The statement of changes in fund net assets presents increases (i.e. revenues) and decreases (i.e. expenses) innet total assets. The statement of cash flows provides information about how the School District finances and meets thecash flow needs of its proprietary activities. Fiduciary funds are reported using the economic resources measurementfocus.

Basis of Accounting

Basis of accounting determines when transactions are recorded in the fmancial records and reported on the fmancialstatements. Government-wide financial statements are prepared using the accrual basis of accounting. Governmentalfunds use the modified accrual basis of accounting. Proprietary and fiduciary funds also use the accrual basis ofaccounting. Differences in the accrual and the modified accrual basis of accounting arise in the recognition of revenue, therecording of deferred revenue, and in the presentation of expenses versus expenditures.

Revenues - Exchange and Non-exchange Transactions - Revenue resulting from exchange transactions, in which eachparty gives and receives essentially equal value is recorded on the accrual basis when the exchange takes place. On amodified accrual basis, revenue is recorded in the fiscal year in which the resources are measurable and becomeavailable. "Measurable" means the amount of the transaction can be determined and "available" means that the resourceswill be collected within the current fiscal year or are expected to be collected soon enough thereafter to be used to payliabilities of the current fiscal year. For the School District, available means expected to be received within sixty daysafter fiscal year end.

Non-exchange transactions, in which the School District receives value without directly giving equal value in return,include Ad Valorem (property) taxes, grants, entitlements, and donations. Ad Valorem (property) Taxes are susceptibleto accrual, as under New Jersey State Statute, a municipality is required to remit to its school district the entire balance oftaxes in the amount voted upon or certified, prior to the end of the school year. The School District records the entireapproved tax levy as revenue (accrued) at the start of the fiscal year since the revenue is both measurable and available.The School District is entitled to receive monies under the established payment schedule and the unpaid amount isconsidered to be an "accounts receivable". With the exception of restricted formula aids recorded in the special revenuefund, revenue from grants, entitlements, and donations is recognized in the fiscal year in which all eligibilityrequirements have been satisfied. Eligibility requirements include timing requirements, which specify the fiscal yearwhen the resources are required to be used or the fiscal year when use is first permitted, matching requirements, in whichthe School District must provide local resources to be used for a specified purpose, and expenditure requirements, inwhich the resources are provided to the School District on a reimbursement basis.

Under the modified accrual basis, the following revenue sources are considered to be both measurable and available atfiscal year-end; tuition, grants, fees, and rentals.

32

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30,2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Basis of Accounting (Continued)

Expenses/Expenditures - On the accrual basis of accounting, expenses are recognized at the time they are incurred.The fair value of donated commodities used during the fiscal year is reported in the operating statement as an expense.Unused donated commodities are reported as deferred revenue. The measurement focus of governmental fundaccounting is on decreases in net financial resources (expenditures) rather than expenses. Expenditures are generallyrecognized in the accounting period in which the related fund liability is incurred, if measurable. Allocations of cost,such as depreciation and amortization, are not recognized in governmental funds.

BudgetslBudgetary Control - Annual appropriated budgets are prepared in the spring of each fiscal year for the general,special revenue, and debt service funds. The budgets are submitted to the county office for their approval. Budgets areprepared using the modified accrual basis of accounting. The legal level of budgetary control is established at line itemaccounts within each fund. Line item accounts are defined as the lowest (most specific) level of detail as establishedpursuant to the minimum chart of accounts referenced in N.J.A.C. 6:23A-16.2(f)1. Transfers of appropriations may bemade by School Board resolution at any time during the fiscal year in accordance with N.J.A.C. 6A:23A-13.3.

Formal budgetary integration into the accounting system is employed as a management control device during the fiscalyear. For governmental funds there are no substantial differences between the budgetary basis of accounting andaccounting principles generally accepted in the United States of America with the exception of the legally mandatedrevenue recognition of the one or more June state aid payments for budgetary purposes only and the special revenue fund.Encumbrance accounting is also employed as an extension of formal budgetary integration in the governmental fund types.Unencumbered appropriations lapse at fiscal year end.

The accounting records of the special revenue fund are maintained on the budgetary basis. The budgetary basis differsfrom GAAP in that the budgetary basis recognizes encumbrances as expenditures and also recognizes the related revenues,whereas the GAAP basis does not. Sufficient supplemental records are maintained to allow for the presentation of GAAPbasis financial reports.

The budget, as detailed on Exhibit C-I, Exhibit C-2 and Exhibit 1-3, includes all amendments to the adopted budget, ifany.

Exhibit C-3 presents a reconciliation of the general fund revenues and special revenue fund revenues and expendituresfrom the budgetary basis of accounting as presented in the general fund budgetary comparison schedule and the specialrevenue fund budgetary comparison schedule to the GAAP basis of accounting as presented in the statement of revenues,expenditures and changes in fund balances - governmental funds. Note that the School District does not reportencumbrances outstanding at year end as expenditures in the general fund since the general fund budget follows modifiedaccrual basis with the exception of the revenue recognition policy for the one or more June state aid payments.

Encumbrances - Under encumbrance accounting purchase orders, contracts and other commitments for the expenditure ofresources are recorded to reserve a portion of the applicable appropriation. Encumbrances are a component of fund balanceat fiscal year end as they do not constitute expenditures or liabilities but rather commitments related to unperformedcontracts for goods and services. Open encumbrances in governmental funds, other than the special revenue fund, whichhave not been previously restricted, committed, or assigned, should be included within committed or assigned fundbalance, as appropriate.

Open encumbrances in the special revenue fund, however, for which the School District has received advances of grantawards, are reflected in the balance sheet as deferred revenues at fiscal year end.

The encumbered appropriation authority carries over into the next fiscal year. An entry will be made at the beginning ofthe next fiscal year to increase the appropriation reflected in the certified budget by the outstanding encumbrance amountas of the current fiscal year end.

33

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30, 2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Cash, Cash Equivalents and Investments - Cash and cash equivalents, for all funds, include petty cash, change funds,cash in banks and all highly liquid investments with a maturity of three months or less at the time of purchase and arestated at cost plus accrued interest. Such is the definition of cash and cash equivalents used in the statement of cash flowsfor the proprietary funds. U.S. Treasury and agency obligations and certificates of deposit with maturities of one year orless when purchased are stated at cost. All other investments are stated at fair value.

Jersey school districts are limited as to the types of investments and types of financial institutions they may invest in.N.J.S.A. 18A:20-37 provides a list of permissible investments that may be purchased by New Jersey school districts.

N.J.S.A. 17:9-41 et seq. establishes the requirements for the security of deposits of governmental units. The statuterequires that no governmental unit shall deposit public funds in a public depository unless such funds are secured inaccordance with the Governmental Unit Deposit Protection Act (GUDPA), a multiple financial institution collateral pool.which was enacted in 1970 to protect governmental units from a loss of funds on deposit with a failed banking institutionin New Jersey. Public depositories include State or federally chartered banks, savings banks or associations located in orhaving a branch office in the State of New Jersey, the deposits of which are federally insured. All public depositories mustpledge collateral, having a market value at least equal to five percent of the average daily balance of collected public funds,to secure the deposits of Governmental Units. If a public depository fails, the collateral it has pledged, plus the collateralof all other public depositories, is available to pay the full amount of their deposits to the governmental units.

Tuition Payable - Tuition charges for the fiscal years ended June 30. 2012 and 2011 were based on rates established by thereceiving school district. These rates are subject to change when the actual costs have been determined.

Inventories - Inventories are valued at cost, which approximates market. The costs are determined on a first-in, first-outbasis.

The cost of inventories in governmental fund types is recorded as expenditures when purchased rather than whenconsumed, and is not recorded since any amounts are considered immaterial to the basic financial statements.

Inventories recorded in the government-wide fmancial statements and in the proprietary fund types are recorded asexpenditures when consumed rather than when purchased.

Prepaid Expenses - Prepaid expenses recorded on the government-wide financial statements and in the proprietary fundtypes represent payments made to vendors for services that will benefit periods beyond June 30,2012.

In the governmental fund types, however, payments for prepaid items are fully recognized as an expenditure in the fiscalyear of payment. No asset for the prepayment is created, and no expenditure allocation to future accounting periods isrequired (non-allocation method). This is consistent with the basic governmental concept that only expendable fmancialresources are reported by a specific fund.

Deferred Expenditures - Deferred expenditures are disbursements that are made in one period, but are more accuratelyreflected as an expenditure/expense in the next fiscal period. Unlike prepaid expenses, deferred expenditures are notregularly recurring cost of operations.

Short-Term Interfund Receivables I Payables - Short-term interfund receivables I payables represent amounts that areowed, other than charges for goods or services rendered to I from a particular fund in the School District and that are duewithin one year. These amounts are eliminated in the governmental and business-type columns of the statement of netassets, except for the net residual amounts due between governmental and business-type activities, which are presented asinternal balances.

Capital Assets - The District is a non-operating school district and does not possess any fixed assets required to becapitalized.

34

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30, 2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Compensated Absences - The District does not offer compensated absences (e.g. unused vacation, sick leave) to itsemployees.

Deferred Revenue - Deferred revenue arises when assets are recognized before revenue recognition criteria have beensatisfied.

Accrued Liabilities and Long-Term ObHgations - All payables, accrued liabilities, and long-term obligations arereported on the government-wide financial statements, and all payables, accrued liabilities and long-term obligationspayable from proprietary funds are reported on the proprietary fund financial statements. In general, governmental fundpayables and accrued liabilities that, once incurred, are paid in a timely manner and in full from current financial resourcesare reported as obligations of the funds. However, claims and judgments, compensated absences, special terminationbenefits and contractually required pension contributions that will be paid from governmental funds are reported as aliability in the fund financial statements only to the extent that they are normally expected to be paid with expendableavailable financial resources. Bonds are recognized as a liability on the fund financial statements when due.

Net Assets - Net assets represent the difference between assets and liabilities. Net assets invested in capital assets, net ofrelated debt consists of capital assets, net of accumulated depreciation, reduced by the outstanding balance of anyborrowings used for the acquisition, construction, or improvement of those assets. Net assets are reported as restrictedwhen there are limitations imposed on their use either through the enabling legislation adopted by the School District orthrough external restrictions imposed by creditors, grantors, or laws or regulations of other governments.

It is the School District's policy to apply restricted resources when an expense is incurred for purposes for which bothrestricted and unrestricted net assets are available.

Fund Balance - The School District reports fund balance in classifications that comprise a hierarchy based primarily onthe extent to which the School District is bound to honor constraints on the specific purposes for which amounts in thosefunds can be spent. The School District's classifications, and policies for determining such classifications, are as follows:

Nonspendable - The nonspendable fund balance classification includes amounts that cannot be spent because theyare either not in spendable form or are legally or contractually required to be maintained intact. The "not inspendable form" criteria includes items that are not expected to be converted to cash, such as inventories and prepaidamounts. The School District had no nonspendable fund balance at June 30, 2012.

Restricted - This fund balance classification includes amounts that are restricted to specific purposes. Suchrestrictions, or constraints, are placed on the use of resources either by being (a) externally imposed by creditors,grantors, contributors, or laws or regulations of other governments; or (b) imposed by law through constitutionalprovisions or enabling legislation.

Committed - This fund balance classification includes amounts that can only be used for specific purposes pursuantto constraints imposed by formal action of the School District's highest level of decision making authority, which forthe School District is the Board of Education. Once committed, amounts cannot be used for any other purpose unlessthe Board of Education removes, or changes, the specified use by taking the same type of action imposing thecommitment.

Assigned - This fund balance classification includes amounts that are constrained by the School District's intent to beused for specific purposes, but are neither restricted nor committed. Intent is expressed by either the Board ofEducation or by the Business Administrator, to which the Board of Education has delegated the authority to assignamounts to be used for specific purposes.

35

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30,2012

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Unassigned - This fund balance classification is the residual classification for the General Fund. It represents fundbalance that has not been assigned to other funds and that has not been restricted, committed, or assigned to specificpurposes within the general fund. The general fund is the only fund that reports a positive unassigned fund balanceamount. In other governmental funds, if expenditures incurred for specific purposes exceed the amounts restricted,committed, or assigned to those purposes, it may be necessary to report a negative unassigned fund balance.

When an expenditure is incurred for purposes for which both restricted and unrestricted fund balances are available, it isthe School District's policy to spend restricted fund balances first. Likewise, when an expenditure is incurred for purposesfor which amounts in any of the unrestricted fund balance classifications can be used, it is the policy of the School Districtto spend fund balances, if appropriate, in the following order: committed, assigned, then unassigned.

Interfund Activity - Transfers between governmental and business-type activities on the government-wide statements arereported in the same manner as general revenues. Exchange transactions between funds are reported as revenues in theseller funds and as expenditures/expenses in the purchaser funds. Flows of cash or goods from one fund to another withouta requirement for repayment are reported as interfund transfers. Interfund transfers are reported as other financingsources/uses ingovernmental funds and after non-operating revenues/expenses in proprietary funds. Reimbursements fromfunds responsible for particular expenditures/expenses to the funds that initially paid for them are not presented on thefmancial statements.

Estimates - The preparation of fmancial statements in conformity with accounting principles generally accepted in theUnited State of America requires management to make estimates and assumptions that affect the amounts reported in thefinancial statements and accompanying notes. Actual results may differ from those estimates.

2. CASH AND CASH EQUIVALENTS

Custodial Credit Risk Related to Deposits - Custodial credit risk refers to the risk that, in the event of a bank failure, theSchool District's deposits may not be recovered. Although the School District does not have a formal policy regardingcustodial credit risk, N.J.S.A 17.9-41 et seq. requires that governmental units shall deposit public funds in publicdepositories protected from loss under the provisions of the Governmental Unit Deposit Protection Unit (GUDPA). Underthe Act, the first $250,000.00 of governmental deposits in each insured depository is protected by the Federal DepositInsurance Corporation (FDIC). Public funds owned by the School District in excess of FDIC insured amounts areprotected by GUDPA. Banks that qualify as public depositories under New Jersey statutes hold cash deposits, with bankbalances totaling $106, III at June 30, 2012.

3. ACCOUNTS RECEIVABLES

Accounts receivables at June 30, 2012 consisted of accounts (fees) and intergovernmental grants. All intergovernmentalreceivables are considered collectible in full due to the stable condition of State programs and the current fiscal yearguarantee of federal funds.

Accounts receivable at June 30,2012 for the School District's individual major and fiduciary funds, in the aggregate, are asfollows:

GeneralFund

FiduciaryFunds Total

Tax Levy $ 4,690 $ $ 4..;..1,,6.;;.;;9~0

Total 4,690 4,690

36

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30, 201l

4. PENSION PLANS

Description of Plans - Substantially aU of the School District's employees participate in one of the following pensionplans which have been established by State statute, and are administered by the New Jersey Division of Pensions andBenefits (Division): the Teachers' Pension and Annuity Fund (TPAF), the Public Employees' Retirement System (PERS) orthe Defined Contribution Retirement Program (DCRP). Each plan has a Board of Trustees that is primarily responsible forits administration. The Division issues a publicly available financial report that includes fmancial statements and requiredsupplementary information. That report may be obtained by writing to the State of New Jersey, Division of Pensions andBenefits. P.O. Box 295, Trenton, New Jersey, 08625-0295.

Teachers' Pension and Annuity Fund (TPAF)

The Teachers' Pension and Annuity Fund is a cost-sharing contributory defmed benefit pension plan which was establishedon January I, 1955, under the provisions of N.J.S.A. 18A:66. The TPAF provides retirement, death and disability, andmedical benefits to qualified members. Vesting and benefit provisions are established by N.J.S.A. 18A:66.

The contribution requirements of plan members are determined by State statute. In accordance with Chapter 92 andChapter 103, P.L. 2007, plan members were required to contribute 5.5% of their annual covered salary. Chapter 78 P.L.2011 changed the employee contribution rate as follows: Effective with the first payroll check to be paid on or afterOctober 1,2011 plan members rate will increase to 6.5% with an additional increase of .14% beginning in July 2012 andcontinuing each year until the rate reaches 7.5% in July 2018. The State Treasurer has the right under the current law tomake temporary reductions in rates based on the existence of surplus pension assets in the retirement system; however,statute also requires the return to the normal rate when such surplus pension assets no longer exists.

Under current statute, all employer contributions are made by the State of New Jersey on-behalf of the School District andall other related non-contributing employers. No normal or accrued liability contribution by the School District has beenrequired over the several preceding fiscal years. The District had no employees enrolled in the TP AF for the fiscal yearended June 30, 2012.

Public Employees' Retirement System (PERS)

The Public Employees' Retirement System is a cost-sharing multiple-employer defined benefit pension plan which wasestablished on January I, 1955. The PERS provides retirement, death and disability, and medical benefits to certainqualified members. Vesting and benefit provisions are established byN.J.S.A. 43:15A and 43:3B.

The contribution requirements of plan members are determined by State statute. In accordance with Chapter 92 andChapter 103, P.L. 2007, plan members were required to contribute 5.5% of their annual covered salary. Chapter 78 P.L.20 II changed the employee contribution rate as follows: Effective with the first payroll check to be paid on or afterOctober 1,2011 plan members rate will increase to 6.5% with an additional increase of .14% beginning in July 2012 andcontinuing each year until the rate reaches 7.5% in July 2018. The State Treasurer has the right under the current law tomake temporary reductions in rates based on the existence of surplus pension assets in the retirement system; however,statute also requires the return to the normal rate when such surplus pension assets no longer exists.

The School District is billed annually for its normal contribution plus any accrued liability. The School District'scontributions, equal to the required contribution for each fiscal year, were as follows:

Public Eml!lo}:ee5 Retirement SIstemNon-Contrib

Fiscal Normal Accrued Insurance Total Funded by Paid byXw: Contribution Liability Premium Liability State District

2012 - 0- -0- -0- -0- -0- -0-2011 - 0- -0- -0- -0- -0- -0-2010 -0- -0- -0- -0- -0- -0-

37

Cape May Point School DistrictNotes to Basic Financial Statements

For the Fiscal Year Ended June 30, 2012

4. PENSION PLANS (Continued)

Defined Contribution Retirement Program (DCRP)

The Defmed Contribution Retirement Program is a cost-sharing multiple-employer defined contribution pension planwhich was established on July 1, 2007, under the provisions of Chapter 92, P.L. 2007 and Chapter 103, P.L. 2007(N.J.S.A.43:15C-1 et seq), and expanded under the provisions of Chapter 89, P.L. 2008 and Chapter 1, P.L. 2010. TheDefined Contribution Retirement Program Board oversees the DCRP, which is administered for the Divisions of Pensionsand Benefits by Prudential Financial. The DCRP provides eligible members, and their beneficiaries, with a tax-sheltered,defined contribution retirement benefit, along with life insurance and disability coverage. Vesting and benefit provisionsare established by N.J.S.A. 43: 15C-l et. seq.

The contribution requirements of plan members are determined by State statute. In accordance with Chapter 92, P.L. 2007and Chapter 103, P.L. 2007, plan members are required to contribute 5.5% of their annual covered salary. Chapter 78 P.L.2011 changed the employee contribution rate as follows: Effective with the first payroll check to be paid on or afterOctober 1,2011 plan members rate will increase to 6.5% with an additional increase of .14% beginning in July 2012 andcontinuing each year until the rate reaches 7.5% in July 2018. The State Treasurer has the right under the current law tomake temporary reductions in rates based on the existence of surplus pension assets in the retirement system; however,state statute also requires the return to the normal rate when such surplus pension assets no longer exist. The employeecontributions along with the School District's contribution for each pay period are transmitted to Prudential Financial notlater than the fifth business day after the date on which the employee is paid for that pay period.

There were no School District employees enrolled in the DCRP for the fiscal years ended June 30, 2012, 2011, and 2010

S. POST-RETIREMENT BENEFITS

The School District contributes to the New Jersey State Health Benefits Program (SHBP), a cost-sharing multiple-employer defined benefit post-employment healthcare plan administered by the State of New Jersey Division of Pensionand Benefits. SHBP was established to provide medical, prescription drug, mental health/substance abuse and MedicarePart B reimbursement to retirees and their covered dependents. The State Health Benefits Program Act is found in NewJersey Statutes Annotated, Title 52, Article 17.25 et seq. Rules governing the operation and administration of the programare found in Title 17, Chapter 9 of the New Jersey Administrative Code. The State of New Jersey Division of Pensionissues a publicly available financial report that includes financial statements and required supplementary information forSHBP. That report may be obtained by writing to the Division of Pension and Benefits, PO Box 295, Trenton, NJ 08625-0295.