school district no. 6 (rocky mountain) · the board of education of school district no. 6 (rocky...

TRANSCRIPT

Audited Financial Statements of

School District No. 6 (Rocky Mountain)

June 30, 2016

September 13, 2016 15:56

School District No. 6 (Rocky Mountain)June 30, 2016

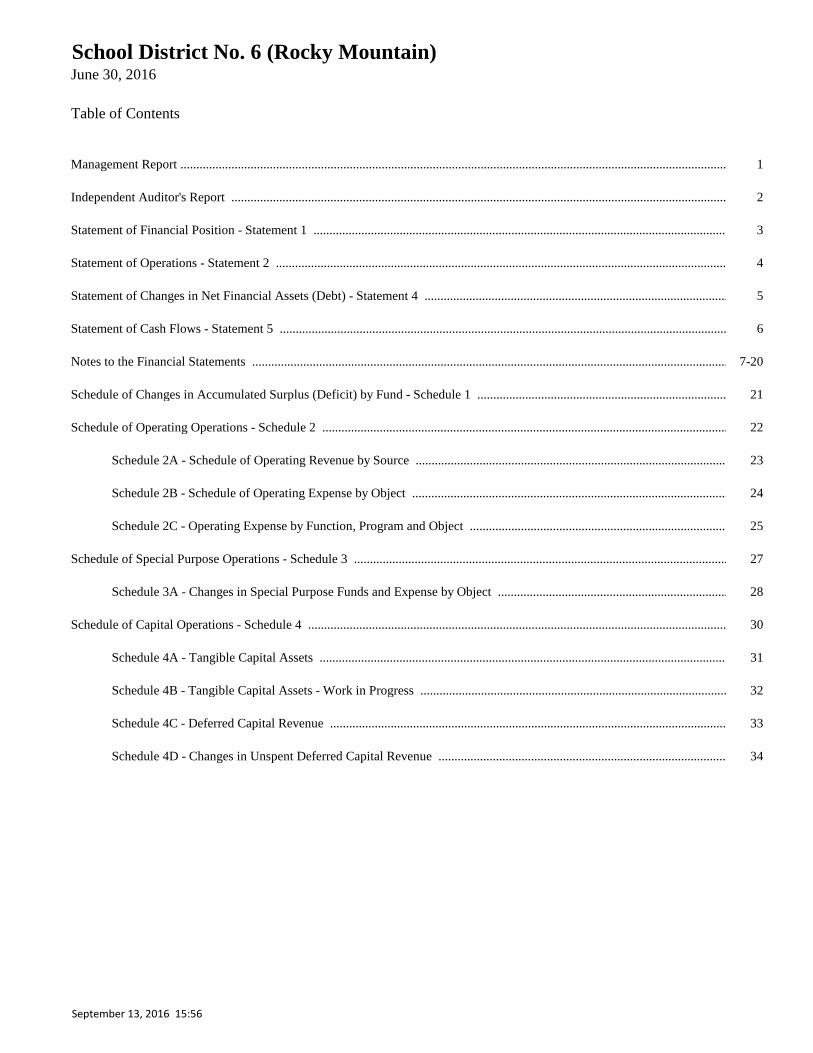

Table of Contents

Management Report ...........................................................................................................................................................................................1

Independent Auditor's Report ...........................................................................................................................................................................................2

Statement of Financial Position - Statement 1 ...........................................................................................................................................................................................3

Statement of Operations - Statement 2 ...........................................................................................................................................................................................4

Statement of Changes in Net Financial Assets (Debt) - Statement 4 ...........................................................................................................................................................................................5

Statement of Cash Flows - Statement 5 ...........................................................................................................................................................................................6

Notes to the Financial Statements ...........................................................................................................................................................................................7-20

Schedule of Changes in Accumulated Surplus (Deficit) by Fund - Schedule 1 ...........................................................................................................................................................................................21

Schedule of Operating Operations - Schedule 2 ...........................................................................................................................................................................................22

Schedule 2A - Schedule of Operating Revenue by Source ...........................................................................................................................................................................................23

Schedule 2B - Schedule of Operating Expense by Object ...........................................................................................................................................................................................24

Schedule 2C - Operating Expense by Function, Program and Object ...........................................................................................................................................................................................25

Schedule of Special Purpose Operations - Schedule 3 ...........................................................................................................................................................................................27

Schedule 3A - Changes in Special Purpose Funds and Expense by Object ...........................................................................................................................................................................................28

Schedule of Capital Operations - Schedule 4 ...........................................................................................................................................................................................30

Schedule 4A - Tangible Capital Assets ..................................................................................................................................................................................31

Schedule 4B - Tangible Capital Assets - Work in Progress ...........................................................................................................................................................................................32

Schedule 4C - Deferred Capital Revenue ...........................................................................................................................................................................................33

Schedule 4D - Changes in Unspent Deferred Capital Revenue ...........................................................................................................................................................................................34

September 13, 2016 15:56

School District No. 6 (Rocky Mountain)

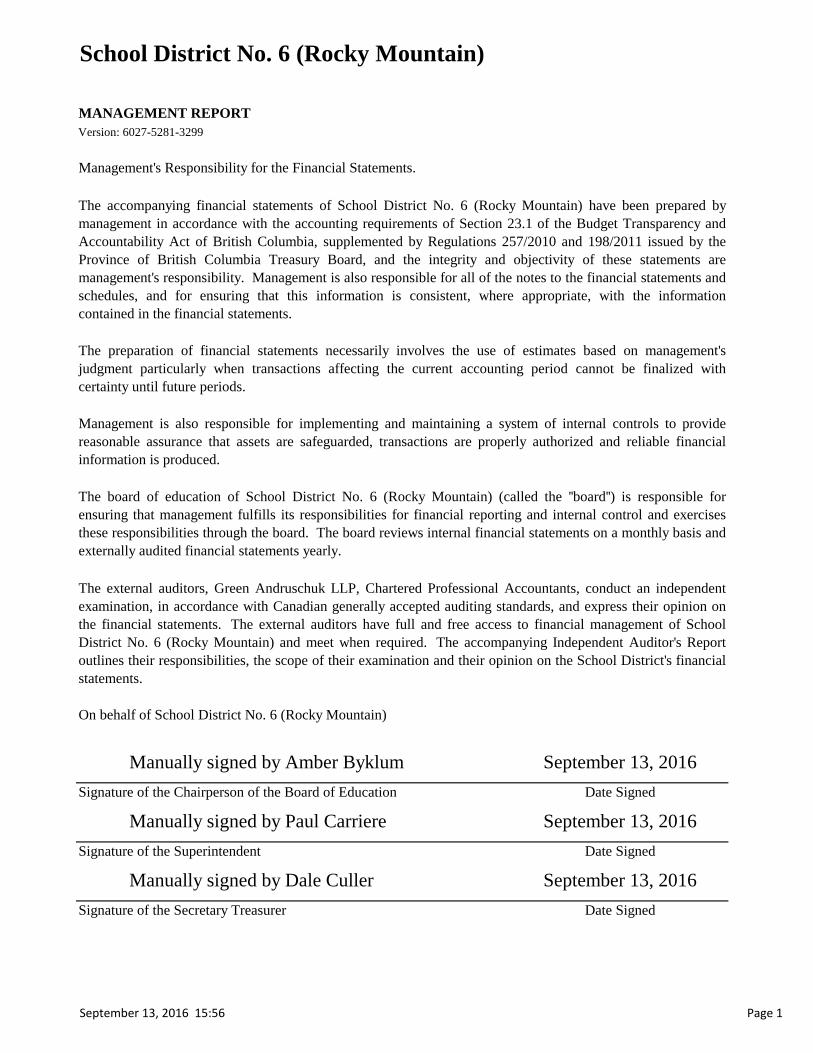

MANAGEMENT REPORT

Management's Responsibility for the Financial Statements.

On behalf of School District No. 6 (Rocky Mountain)

Signature of the Chairperson of the Board of Education

Signature of the Superintendent

Signature of the Secretary Treasurer

Version: 6027-5281-3299

The external auditors, Green Andruschuk LLP, Chartered Professional Accountants, conduct an independent

examination, in accordance with Canadian generally accepted auditing standards, and express their opinion on

the financial statements. The external auditors have full and free access to financial management of School

District No. 6 (Rocky Mountain) and meet when required. The accompanying Independent Auditor's Report

outlines their responsibilities, the scope of their examination and their opinion on the School District's financial

statements.

Date Signed

Date Signed

Date Signed

The accompanying financial statements of School District No. 6 (Rocky Mountain) have been prepared by

management in accordance with the accounting requirements of Section 23.1 of the Budget Transparency and

Accountability Act of British Columbia, supplemented by Regulations 257/2010 and 198/2011 issued by the

Province of British Columbia Treasury Board, and the integrity and objectivity of these statements are

management's responsibility. Management is also responsible for all of the notes to the financial statements and

schedules, and for ensuring that this information is consistent, where appropriate, with the information

contained in the financial statements.

Management is also responsible for implementing and maintaining a system of internal controls to provide

reasonable assurance that assets are safeguarded, transactions are properly authorized and reliable financial

information is produced.

The preparation of financial statements necessarily involves the use of estimates based on management's

judgment particularly when transactions affecting the current accounting period cannot be finalized with

certainty until future periods.

The board of education of School District No. 6 (Rocky Mountain) (called the ''board'') is responsible for

ensuring that management fulfills its responsibilities for financial reporting and internal control and exercises

these responsibilities through the board. The board reviews internal financial statements on a monthly basis and

externally audited financial statements yearly.

Manually signed by Amber Byklum September 13, 2016

Manually signed by Paul Carriere September 13, 2016

Manually signed by Dale Culler September 13, 2016

Page 1 September 13, 2016 15:56

Statement 1

2016 2015

Actual Actual

$ $

Financial Assets

Cash and Cash Equivalents 4,831,169 5,774,731

Accounts Receivable

Due from Province - Ministry of Education 631,791 31,616

Due from LEA/Direct Funding 33,973 56,824

Other (Note 3) 268,755 161,813

Portfolio Investments (Note 4) 3,235,255 3,232,309

Total Financial Assets 9,000,943 9,257,293

Liabilities

Accounts Payable and Accrued Liabilities

Due to Province - Ministry of Education 2,519

Other (Note 5) 2,872,452 2,978,188

Unearned Revenue (Note 6) 948,628 498,649

Deferred Revenue (Note 7) 1,452,048 1,374,608

Deferred Capital Revenue (Note 8) 32,242,417 32,075,774

Employee Future Benefits (Note 9) 662,119 616,438

Capital Lease Obligations (Note 10) 496,785

Total Liabilities 38,674,449 37,546,176

Net Financial Assets (Debt) (29,673,506) (28,288,883)

Non-Financial Assets

Tangible Capital Assets (Note 11) 58,483,176 56,972,465

Restricted Assets (Endowments) (Note 13) 105,873 105,873

Prepaid Expenses 10,501 96,214

Total Non-Financial Assets 58,599,550 57,174,552

Accumulated Surplus (Deficit) 28,926,044 28,885,669

Manually signed by Amber Byklum

Signature of the Chairperson of the Board of Education

Manually signed by Paul Carriere

Signature of the Superintendent

Manually signed by Dale Culler

Signature of the Secretary Treasurer

School District No. 6 (Rocky Mountain)Statement of Financial Position

As at June 30, 2016

Date Signed

Date Signed

Date Signed

Contractual Obligations and Contingencies

Approved by the Board

September 13, 2016

September 13, 2016

September 13, 2016

The accompanying notes are an integral part of these financial statements.Version: 6027-5281-3299

September 13, 2016 15:56 Page 3

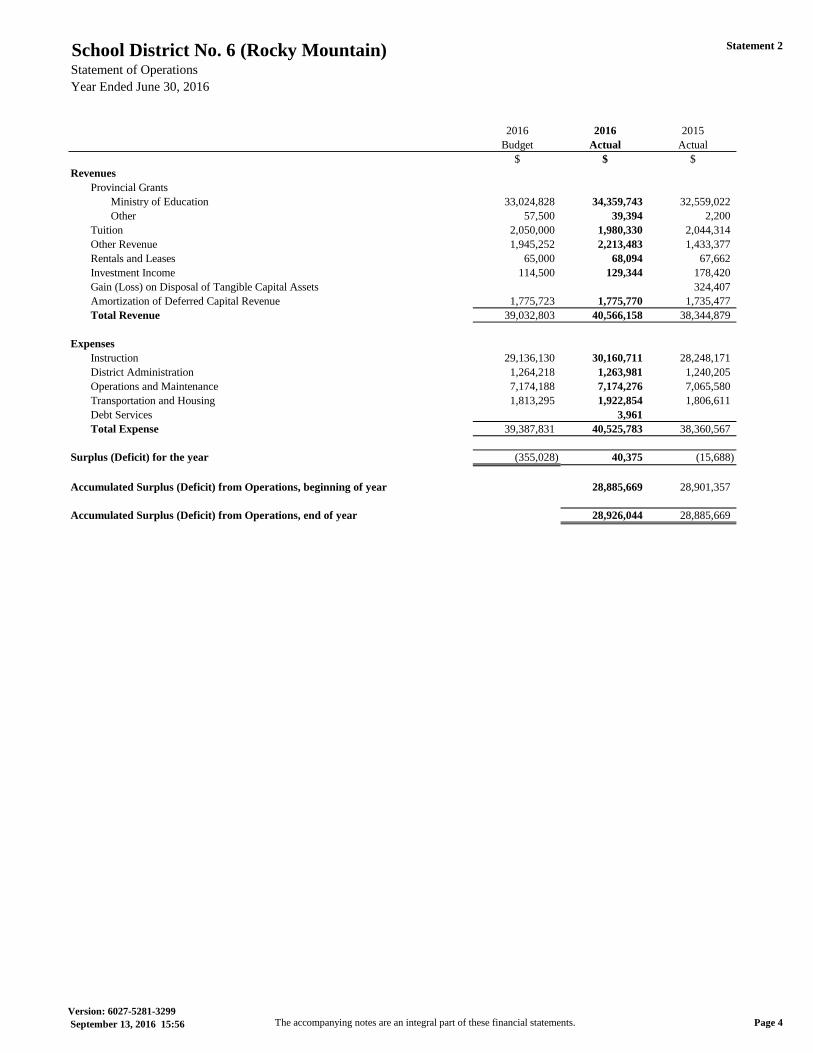

Statement 2

2016 2016 2015

Budget Actual Actual

$ $ $

Revenues

Provincial Grants

Ministry of Education 33,024,828 34,359,743 32,559,022

Other 57,500 39,394 2,200

Tuition 2,050,000 1,980,330 2,044,314

Other Revenue 1,945,252 2,213,483 1,433,377

Rentals and Leases 65,000 68,094 67,662

Investment Income 114,500 129,344 178,420

Gain (Loss) on Disposal of Tangible Capital Assets 324,407

Amortization of Deferred Capital Revenue 1,775,723 1,775,770 1,735,477

Total Revenue 39,032,803 40,566,158 38,344,879

Expenses

Instruction 29,136,130 30,160,711 28,248,171

District Administration 1,264,218 1,263,981 1,240,205

Operations and Maintenance 7,174,188 7,174,276 7,065,580

Transportation and Housing 1,813,295 1,922,854 1,806,611

Debt Services 3,961

Total Expense 39,387,831 40,525,783 38,360,567

Surplus (Deficit) for the year (355,028) 40,375 (15,688)

Accumulated Surplus (Deficit) from Operations, beginning of year 28,885,669 28,901,357

Accumulated Surplus (Deficit) from Operations, end of year 28,926,044 28,885,669

School District No. 6 (Rocky Mountain)Statement of Operations

Year Ended June 30, 2016

The accompanying notes are an integral part of these financial statements.Version: 6027-5281-3299

September 13, 2016 15:56 Page 4

Statement 4

2016 2016 2015

Budget Actual Actual

$ $ $

Surplus (Deficit) for the year (355,028) 40,375 (15,688)

Effect of change in Tangible Capital Assets

Acquisition of Tangible Capital Assets (2,336,770) (4,295,731) (3,404,541)

Amortization of Tangible Capital Assets 2,791,517 2,785,020 2,653,161

Net carrying value of Tangible Capital Assets disposed of 104,023

Total Effect of change in Tangible Capital Assets 454,747 (1,510,711) (647,357)

Acquisition of Prepaid Expenses (10,501) (96,214)

Use of Prepaid Expenses 96,214 94,835

Total Effect of change in Other Non-Financial Assets - 85,713 (1,379)

(Increase) Decrease in Net Financial Assets (Debt),

before Net Remeasurement Gains (Losses) 99,719 (1,384,623) (664,424)

Net Remeasurement Gains (Losses)

(Increase) Decrease in Net Financial Assets (Debt) (1,384,623) (664,424)

Net Financial Assets (Debt), beginning of year (28,288,883) (27,624,459)

Net Financial Assets (Debt), end of year (29,673,506) (28,288,883)

School District No. 6 (Rocky Mountain)Statement of Changes in Net Financial Assets (Debt)

Year Ended June 30, 2016

The accompanying notes are an integral part of these financial statements.Version: 6027-5281-3299

September 13, 2016 15:56 Page 5

Statement 5

2016 2015

Actual Actual

$ $

Operating Transactions

Surplus (Deficit) for the year 40,375 (15,688)

Changes in Non-Cash Working Capital

Decrease (Increase)

Accounts Receivable (684,266) 417,502

Prepaid Expenses 85,713 (1,379)

Increase (Decrease)

Accounts Payable and Accrued Liabilities (108,255) (833,867)

Unearned Revenue 449,979 (1,366)

Deferred Revenue 77,440 168,771

Employee Future Benefits 45,681 26,737

Loss (Gain) on Disposal of Tangible Capital Assets (324,407)

Amortization of Tangible Capital Assets 2,785,020 2,653,161

Amortization of Deferred Capital Revenue (1,775,770) (1,735,477)

Recognition of Deferred Capital Revenue Spent on Sites (102,413)

Total Operating Transactions 915,917 251,574

Capital Transactions

Tangible Capital Assets Purchased (2,993,393) (3,252,028)

Tangible Capital Assets -WIP Purchased (657,421) (152,513)

District Portion of Proceeds on Disposal 352,626

Capital Lease Purchases (644,917)

Total Capital Transactions (4,295,731) (3,051,915)

Financing Transactions

Capital Revenue Received 1,942,413 914,615

Capital Lease Proceeds 644,917

Capital Lease Payments (148,132)

Total Financing Transactions 2,439,198 914,615

Investing Transactions

Proceeds on Disposal of Portfolio Investments 84,690

Investments in Portfolio Investments (2,946)

Total Investing Transactions (2,946) 84,690

Net Increase (Decrease) in Cash and Cash Equivalents (943,562) (1,801,036)

Cash and Cash Equivalents, beginning of year 5,774,731 7,575,767

Cash and Cash Equivalents, end of year 4,831,169 5,774,731

Cash and Cash Equivalents, end of year, is made up of:

Cash 3,695,572 3,663,526

Cash Equivalents 1,135,597 2,111,205

4,831,169 5,774,731

School District No. 6 (Rocky Mountain)Statement of Cash Flows

Year Ended June 30, 2016

The accompanying notes are an integral part of these financial statements.Version: 6027-5281-3299

September 13, 2016 15:56 Page 6

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 7

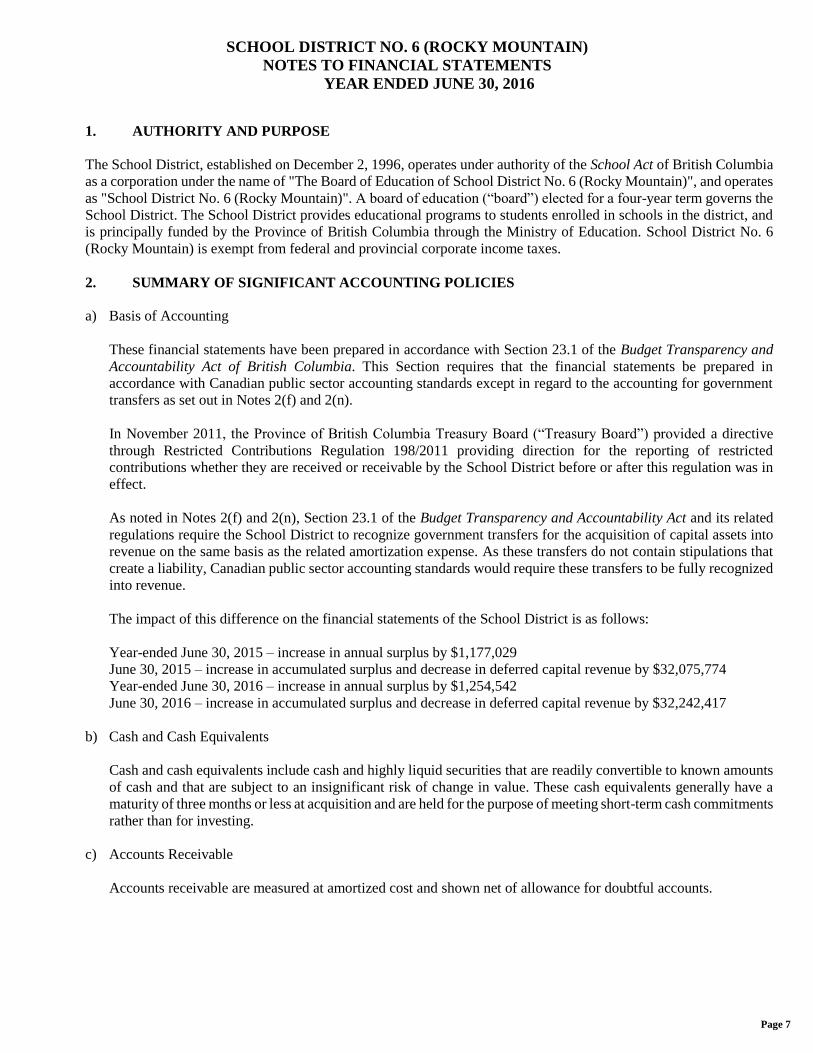

1. AUTHORITY AND PURPOSE

The School District, established on December 2, 1996, operates under authority of the School Act of British Columbia

as a corporation under the name of "The Board of Education of School District No. 6 (Rocky Mountain)", and operates

as "School District No. 6 (Rocky Mountain)". A board of education (“board”) elected for a four-year term governs the

School District. The School District provides educational programs to students enrolled in schools in the district, and

is principally funded by the Province of British Columbia through the Ministry of Education. School District No. 6

(Rocky Mountain) is exempt from federal and provincial corporate income taxes.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a) Basis of Accounting

These financial statements have been prepared in accordance with Section 23.1 of the Budget Transparency and

Accountability Act of British Columbia. This Section requires that the financial statements be prepared in

accordance with Canadian public sector accounting standards except in regard to the accounting for government

transfers as set out in Notes 2(f) and 2(n).

In November 2011, the Province of British Columbia Treasury Board (“Treasury Board”) provided a directive

through Restricted Contributions Regulation 198/2011 providing direction for the reporting of restricted

contributions whether they are received or receivable by the School District before or after this regulation was in

effect.

As noted in Notes 2(f) and 2(n), Section 23.1 of the Budget Transparency and Accountability Act and its related

regulations require the School District to recognize government transfers for the acquisition of capital assets into

revenue on the same basis as the related amortization expense. As these transfers do not contain stipulations that

create a liability, Canadian public sector accounting standards would require these transfers to be fully recognized

into revenue.

The impact of this difference on the financial statements of the School District is as follows:

Year-ended June 30, 2015 – increase in annual surplus by $1,177,029

June 30, 2015 – increase in accumulated surplus and decrease in deferred capital revenue by $32,075,774

Year-ended June 30, 2016 – increase in annual surplus by $1,254,542

June 30, 2016 – increase in accumulated surplus and decrease in deferred capital revenue by $32,242,417

b) Cash and Cash Equivalents

Cash and cash equivalents include cash and highly liquid securities that are readily convertible to known amounts

of cash and that are subject to an insignificant risk of change in value. These cash equivalents generally have a

maturity of three months or less at acquisition and are held for the purpose of meeting short-term cash commitments

rather than for investing.

c) Accounts Receivable

Accounts receivable are measured at amortized cost and shown net of allowance for doubtful accounts.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 8

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

d) Portfolio Investments

The School District has investments in guaranteed investment certificates and term deposits that have a maturity

of greater than three months at the time of acquisition. Guaranteed investment certificates and term deposits not

quoted in an active market are reported at cost.

e) Unearned Revenue

Unearned revenue includes tuition fees received for courses to be delivered in future periods and receipt of

proceeds for services or products to be delivered in a future period. Revenue will be recognized in that future

period when the courses, services, or products are provided.

f) Deferred Revenue and Deferred Capital Revenue

Deferred revenue includes contributions received with stipulations that meet the description of restricted

contributions in the Restricted Contributions Regulation 198/2011 issued by Treasury Board. When restrictions

are met, deferred revenue is recognized as revenue in the fiscal year in a manner consistent with the circumstances

and evidence used to support the initial recognition of the contributions received as a liability as detailed in Note

2(n).

Funding received for the acquisition of depreciable tangible capital assets is recorded as deferred capital revenue

and amortized over the life of the asset acquired as revenue in the statement of operations. This accounting

treatment is not consistent with the requirements of Canadian public sector accounting standards which require

that government transfers be recognized as revenue when approved by the transferor and eligibility criteria have

been met unless the transfer contains a stipulation that creates a liability in which case the transfer is recognized

as revenue over the period that the liability is extinguished. See Note 2(a) for the impact of this policy on these

financial statements.

g) Employee Future Benefits

The School District provides certain post-employment benefits including vested and non-vested benefits for certain

employees pursuant to certain contracts and union agreements. The School District accrues its obligations and

related costs including both vested and non-vested benefits under employee future benefit plans. Benefits include

vested sick leave, accumulating non-vested sick leave, early retirement, retirement/severance, vacation, overtime

and death benefits. The benefits cost is actuarially determined using the projected unit credit method pro-rated on

service and using management’s best estimate of expected salary escalation, termination rates, retirement rates and

mortality. The discount rate used to measure obligations is based on the cost of borrowing. The cumulative

unrecognized actuarial gains and losses are amortized over the expected average remaining service lifetime

(EARSL) of active employees covered under the plan.

The most recent valuation of the obligation was performed at March 31, 2016 and projected to March 31, 2019.

The next valuation will be performed at March 31, 2019 for use at June 30, 2019. For the purposes of determining

the financial position of the plans and the employee future benefit costs, a measurement date of March 31 was

adopted for all periods subsequent to July 1, 2004.

The School District and its employees make contributions to the Teachers’ Pension Plan and Municipal Pension

Plan. The plans are multi-employer plans where assets and obligations are not separated by employer. The costs

are expensed as incurred.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 9

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

h) Asset Retirement Obligations

Liabilities are recognized for statutory, contractual or legal obligations associated with the retirement of tangible

capital assets when those obligations result from the acquisition, construction, development or normal operation

of the assets. The obligations are measured initially at fair value, determined using present value methodology,

and the resulting costs capitalized into the carrying amount of the related tangible capital asset. In subsequent

periods, the liability is adjusted for accretion and any changes in the amount or timing of the underlying future

cash flows. The capitalized asset retirement cost is amortized on the same basis as the related asset and accretion

expense is included in the Statement of Operations.

i) Liability for Contaminated Sites

Contaminated sites are a result of contamination being introduced into air, soil, water or sediment of a chemical,

organic or radioactive material or live organism that exceeds an environmental standard. The liability is recorded

net of any expected recoveries. A liability for remediation of contaminated sites is recognized when a site is not in

productive use and all the following criteria are met:

an environmental standard exists;

contamination exceeds the environmental standard;

the School District:

o is directly responsible; or

o accepts responsibility;

it is expected that future economic benefits will be given up; and

a reasonable estimate of the amount can be made.

The liability is recognized as management’s estimate of the cost of post-remediation including operation,

maintenance and monitoring that are an integral part of the remediation strategy for a contaminated site.

j) Tangible Capital Assets

The following criteria apply:

Tangible capital assets acquired or constructed are recorded at cost which includes amounts that are

directly related to the acquisition, design, construction, development, improvement or betterment of the

assets. Cost also includes overhead directly attributable to construction as well as interest costs that are

directly attributable to the acquisition or construction of the asset.

Donated tangible capital assets are recorded at their fair market value on the date of donation, except in

circumstances where fair value cannot be reasonably determined, which are then recognized at nominal

value. Transfers of capital assets from related parties are recorded at carrying value.

Work in progress is recorded as an acquisition to the applicable asset class at substantial completion.

Tangible capital assets are written down to residual value when conditions indicate they no longer

contribute to the ability of the School District to provide services or when the value of future economic

benefits associated with the sites and buildings are less than their net book value. The write-downs are

accounted for as expenses in the Statement of Operations.

Buildings that are demolished or destroyed are written-off.

Works of art, historic assets and other intangible assets are not recorded as assets in these financial

statements.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 10

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

j) Tangible Capital Assets (continued)

The cost, less residual value, of tangible capital assets (excluding sites), is amortized on a straight-line

basis over the estimated useful life of the asset and commences the year following acquisition. It is

management’s responsibility to determine the appropriate useful lives for tangible capital assets. These

useful lives are reviewed on a regular basis or if significant events initiate the need to revise. Estimated

useful lives are as follows:

Buildings 40 years

Furniture & Equipment 10 years

Vehicles 10 years

Computer Software 5 years

Computer Hardware 5 years

Computer Hardware Under Capital Lease 5 years

k) Capital Leases

Leases that, from the point of view of the lessee, transfer substantially all the benefits and risks incident to

ownership of the property to the School District are considered capital leases. These are accounted for as an asset

and an obligation. Capital lease obligations are recorded at the present value of the minimum lease payments

excluding executor costs, e.g., insurance, maintenance cost, etc. The discount rate used to determine the present

value of the lease payments is the lower of the School District’s rate for incremental borrowing or the interest rate

implicit in the lease.

All other leases are accounted for as operating leases and the related payments are charged to expenses as incurred.

l) Prepaid Expenses

Prepaid insurance, maintenance fees, permits and other costs included as prepaid expenses are stated at acquisition

cost and are charged to expense over the periods expected to benefit from them.

m) Funds and Reserves

Certain amounts, as approved by the board, are set aside in accumulated surplus for future operating and capital

purposes. Transfers to and from funds and reserves are an adjustment to the respective fund when approved (see

Note 14 – Interfund Transfers and Note 18 – Internally Restricted Surplus – Operating Fund).

n) Revenue Recognition

Revenues are recognized in the period in which the transactions or events occurred that gave rise to the revenues.

All revenues are recorded on an accrual basis, except when the accruals cannot be determined with a reasonable

degree of certainty or when their estimation is impracticable.

Contributions received, or where eligibility criteria have been met, are recognized as revenue except where the

contribution meets the criteria for deferral as described below. Eligibility criteria are the criteria that the School

District has to meet in order to receive the contributions including authorization by the transferring government.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 11

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

n) Revenue Recognition (continued)

For contributions subject to a legislative or contractual stipulation or restriction as to their use, revenue is

recognized as follows:

non-capital contributions for specific purposes are recorded as deferred revenue and recognized as revenue

in the year related expenses are incurred;

contributions restricted for site acquisitions are recorded as revenue when the sites are purchased; and

contributions restricted for tangible capital asset acquisitions other than sites are recorded as deferred

capital revenue and amortized over the useful life of the related assets.

Donated tangible capital assets other than sites are recorded at fair market value and amortized over the useful life

of the assets. Donated sites are recorded as revenue at fair market value when received or receivable.

The accounting treatment for restricted contributions is not consistent with the requirements of Canadian public

sector accounting standards which require that government transfers be recognized as revenue when approved by

the transferor and eligibility criteria have been met unless the transfer contains a stipulation that meets the criteria

for liability recognition in which case the transfer is recognized as revenue over the period that the liability is

extinguished. See Note 2(a) for the impact of this policy on these financial statements.

Revenue related to fees or services received in advance of the fee being earned or the service being performed is

deferred and recognized when the fee is earned or service performed.

Investment income is reported in the period earned. When required by the funding party or related Act, investment

income earned on deferred revenue is added to the deferred revenue balance.

o) Expenditures

Expenses are reported on an accrual basis. The cost of all goods consumed and services received during the year

is expensed.

Categories of Salaries

Principals, Vice-Principals, and Directors of Instruction employed under an administrative officer contract

are categorized as Principals and Vice-Principals.

Superintendents, Assistant Superintendents, Secretary-Treasurers, Trustees and other employees excluded

from union contracts are categorized as Other Professionals.

Allocation of Costs

Operating expenses are reported by function, program, and object. Whenever possible, expenditures are

determined by actual identification. Additional costs pertaining to specific instructional programs, such as

special and aboriginal education, are allocated to these programs. All other costs are allocated to related

programs.

Actual salaries of personnel assigned to two or more functions or programs are allocated based on the time

spent in each function and program. School-based clerical salaries are allocated to school administration

and partially to other programs to which they may be assigned. Principals and Vice-Principals salaries are

allocated to school administration and may be partially allocated to other programs to recognize their other

responsibilities.

Employee benefits and allowances are allocated to the same programs, and in the same proportions, as the

individual’s salary.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 12

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(Continued)

o) Expenditures (continued)

Allocation of Costs (continued)

Supplies and services are allocated based on actual program identification.

p) Endowment Contributions

Endowment contributions are reported as revenue on the Statement of Operations when received. Investment

income earned on endowment principal is recorded as deferred revenue if it meets the definition of a liability and

is recognized as revenue in the year related expenses (disbursements) are incurred. If the investment income earned

does not meet the definition of a liability, it is recognized as revenue in the year it is earned. Endowment assets

are reported as restricted non-financial assets on the Statement of Financial Position.

q) Financial Instruments

A contract establishing a financial instrument creates, at its inception, rights and obligations to receive or deliver

economic benefits. The financial assets and liabilities portray these rights and obligations in the financial

statements. The School District recognizes a financial instrument when it becomes a party to a financial instrument

contract.

Financial instruments consist of cash and cash equivalents, accounts receivable, portfolio investments, accounts

payable and accrued liabilities, capital lease obligations and other liabilities.

Except for portfolio investments in equity instruments quoted in an active market that are recorded at fair value,

all financial assets and liabilities are recorded at cost or amortized cost and the associated transaction costs are

added to the carrying value of these investments upon initial recognition. Transaction costs are incremental costs

directly attributable to the acquisition or issue of a financial asset or a financial liability.

Interest and dividends attributable to financial instruments are reported in the Statement of Operations.

All financial assets except derivatives are tested annually for impairment. When financial assets are impaired,

impairment losses are recorded in the statement of operations. A write-down of a portfolio investment to reflect a

loss in value is not reversed for a subsequent increase in value.

For financial instruments measured using amortized cost, the effective interest rate method is used to determine

interest revenue or expense.

r) Measurement Uncertainty

Preparation of financial statements in accordance with the basis of accounting described in Note 2(a) requires

management to make estimates and assumptions that impact reported amounts of assets and liabilities at the date

of the financial statements and revenues and expenses during the reporting periods. Significant areas requiring the

use of management estimates relate to the potential impairment of assets, liabilities for contaminated sites, rates

for amortization and estimated employee future benefits. Actual results could differ from those estimates.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 13

3. ACCOUNTS RECEIVABLE – OTHER RECEIVABLES

2016

2015

Due from Federal Government $ 75,249 $ 79,789

Due from Other School Districts 12,769 4,141

Other 180,737 77,883

$ 268,755 $ 161,813

4. PORTFOLIO INVESTMENTS

2016

2015

Investments in the cost and amortized cost category:

Guaranteed investment certificates $ 157,123 $ 156,116

Term deposits 3,078,132 3,076,193

$ 3,235,255 $ 3,232,309

5. ACCOUNTS PAYABLE AND ACCRUED LIABILITIES - OTHER

2016

2015

Trade payables $ 1,665,008 $ 1,752,045

Salaries and benefits payable 885,010 870,235

Accrued vacation pay 322,434 355,908

$ 2,872,452 $ 2,978,188

6. UNEARNED REVENUE

2016

2015

Balance, beginning of year $ 498,649 $ 500,015

Changes for the year:

Increase:

Tuition fees 948,628 498,649

948,628 498,649

Decrease:

Tuition fees 498,649 500,015

Net changes for the year 449,979 (1,366)

Balance, end of year $ 948,628 $ 498,649

7. DEFERRED REVENUE

Deferred revenue includes unspent grants and contributions received that meet the description of a restricted

contribution in the Restricted Contributions Regulation 198/2011 issued by Treasury Board, i.e., the stipulations

associated with those grants and contributions have not yet been fulfilled. Detailed information about the changes in

deferred revenue is included in Schedule 3A.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 14

8. DEFERRED CAPITAL REVENUE

Deferred capital revenue includes grants and contributions received that are restricted by the contributor for the

acquisition of tangible capital assets that meet the description of a restricted contribution in the Restricted Contributions

Regulation 198/2011 issued by Treasury Board. Once spent, the contributions are amortized into revenue over the life

of the asset acquired. Detailed information about the changes in deferred capital revenue is included in Schedules 4C

and 4D.

9. EMPLOYEE FUTURE BENEFITS

Benefits include vested sick leave, accumulating non-vested sick leave, early retirement, retirement/severance,

vacation, overtime and death benefits. Funding is provided when the benefits are paid and accordingly, there are no

plan assets. Although no plan assets are uniquely identified, the School District has provided for the payment of these

benefits.

2016 2015

Reconciliation of Accrued Benefit Obligation

Accrued Benefit Obligation – April 1 $ 711,210 $ 642,535

Service Cost 52,203 45,714

Interest Cost 16,608 21,616

Benefit Payments (37,767) (48,430)

Actuarial (Gain) Loss (184,284) 49,775

Accrued Benefit Obligation – March 31 $ 557,970 $ 711,210

Reconciliation of Funded Status at End of Fiscal Year

Accrued Benefit Obligation – March 31 $ 557,970 $ 711,210

Market Value of Plan Assets – March 31 0 0

Funded Status – Surplus (Deficit) (557,970) (711,210)

Employer Contributions After Measurement Date 0 3,506

Benefits Expense After Measurement Date (12,574) (17,203)

Unamortized Net Actuarial (Gain) Loss (91,575) 108,469

Accrued Benefit Asset (Liability) – June 30 $ (662,119) $ (616,438)

Reconciliation of Change in Accrued Benefit Liability

Accrued Benefit Liability – July 1 $ 616,438 $ 589,701

Net expense for Fiscal Year 79,942 78,276

Employer Contributions (34,261) (51,539)

Accrued Benefit Liability – June 30 $ 662,119 $ 616,438

Components of Net Benefit Expense

Service Cost $ 48,201 $ 47,337

Interest Cost 15,981 20,364

Amortization of Net Actuarial (Gain)/Loss 15,760 10,575

Net Benefit Expense (Income) $ 79,942 $ 78,276

The significant actuarial assumptions adopted for measuring the School District’s accrued benefit obligations are:

Discount Rate – April 1 2.25% 3.25%

Discount Rate – March 31 2.50% 2.25%

Long Term Salary Growth – April 1 2.50% + seniority 2.50% + seniority

Long Term Salary Growth – March 31 2.50% + seniority 2.50% + seniority

EARSL – March 31 9.8 9.6

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 15

10. CAPITAL LEASE OBLIGATIONS

The School District has entered into capital leases for computer hardware from Macquarie Equipment Finance Ltd.

with implicit interest rates of 0% to 3.30%, expiring September 17, 2019 to May 31, 2021.

Repayments are due as follows:

2017 $ 152,094

2018 152,094

2019 152,094

2020 55,526

Total minimum lease payments $ 511,808

Less amounts representing interest (15,023)

Present value of net minimum capital lease payments $ 496,785

Total interest on leases for the year was $3,961 (2015: $0)

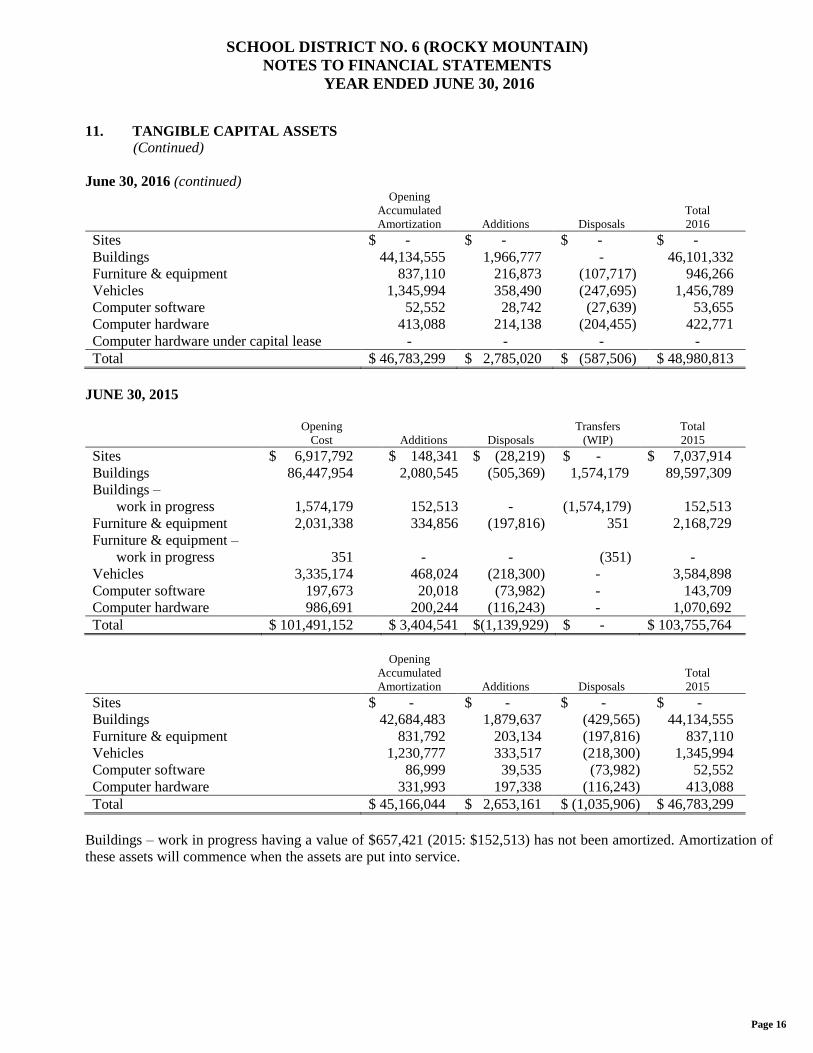

11. TANGIBLE CAPITAL ASSETS

Net Book Value:

Net Book Value

2016

Net Book Value

2015

Sites $ 7,064,902 $ 7,037,914

Buildings 46,082,722 45,462,754

Buildings – work in progress 657,421 152,513

Furniture & equipment 1,222,115 1,331,619

Vehicles 2,007,136 2,238,904

Computer software 99,735 91,157

Computer hardware 704,228 657,604

Computer hardware under capital lease 644,917 -

Total $ 58,483,176 $ 56,972,465

JUNE 30, 2016

Opening

Cost

Additions

Disposals

Transfers

(WIP)

Total

2016

Sites $ 7,037,914 $ 26,988 $ - $ - $ 7,064,902

Buildings 89,597,309 2,434,232 - 152,513 92,184,054

Buildings –

work in progress

152,513

657,421

-

(152,513)

657,421

Furniture & equipment 2,168,729 107,369 (107,717) - 2,168,381

Vehicles 3,584,898 126,722 (247,695) - 3,463,925

Computer software 143,709 37,320 (27,639) - 153,390

Computer hardware 1,070,692 260,762 (204,455) - 1,126,999

Computer hardware –

under capital lease

-

644,917

-

-

644,917

Total $ 103,755,764 $ 4,295,731 $ (587,506) $ - $ 107,463,989

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 16

11. TANGIBLE CAPITAL ASSETS

(Continued)

June 30, 2016 (continued) Opening

Accumulated

Amortization

Additions

Disposals

Total

2016

Sites $ - $ - $ - $ -

Buildings 44,134,555 1,966,777 - 46,101,332

Furniture & equipment 837,110 216,873 (107,717) 946,266

Vehicles 1,345,994 358,490 (247,695) 1,456,789

Computer software 52,552 28,742 (27,639) 53,655

Computer hardware 413,088 214,138 (204,455) 422,771

Computer hardware under capital lease - - - -

Total $ 46,783,299 $ 2,785,020 $ (587,506) $ 48,980,813

JUNE 30, 2015

Opening

Cost

Additions

Disposals

Transfers

(WIP)

Total

2015

Sites $ 6,917,792 $ 148,341 $ (28,219) $ - $ 7,037,914

Buildings 86,447,954 2,080,545 (505,369) 1,574,179 89,597,309

Buildings –

work in progress

1,574,179

152,513

-

(1,574,179)

152,513

Furniture & equipment 2,031,338 334,856 (197,816) 351 2,168,729

Furniture & equipment –

work in progress

351

-

-

(351)

-

Vehicles 3,335,174 468,024 (218,300) - 3,584,898

Computer software 197,673 20,018 (73,982) - 143,709

Computer hardware 986,691 200,244 (116,243) - 1,070,692

Total $ 101,491,152 $ 3,404,541 $(1,139,929) $ - $ 103,755,764

Opening

Accumulated

Amortization

Additions

Disposals

Total

2015

Sites $ - $ - $ - $ -

Buildings 42,684,483 1,879,637 (429,565) 44,134,555

Furniture & equipment 831,792 203,134 (197,816) 837,110

Vehicles 1,230,777 333,517 (218,300) 1,345,994

Computer software 86,999 39,535 (73,982) 52,552

Computer hardware 331,993 197,338 (116,243) 413,088

Total $ 45,166,044 $ 2,653,161 $ (1,035,906) $ 46,783,299

Buildings – work in progress having a value of $657,421 (2015: $152,513) has not been amortized. Amortization of

these assets will commence when the assets are put into service.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 17

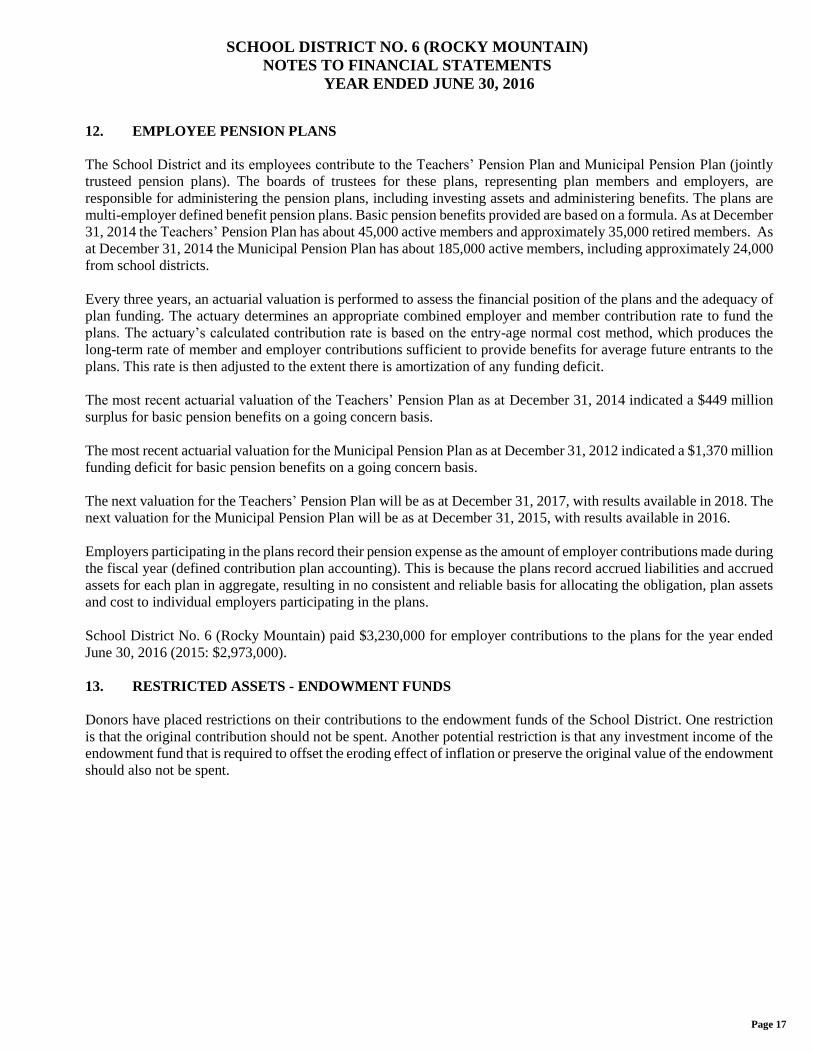

12. EMPLOYEE PENSION PLANS

The School District and its employees contribute to the Teachers’ Pension Plan and Municipal Pension Plan (jointly

trusteed pension plans). The boards of trustees for these plans, representing plan members and employers, are

responsible for administering the pension plans, including investing assets and administering benefits. The plans are

multi-employer defined benefit pension plans. Basic pension benefits provided are based on a formula. As at December

31, 2014 the Teachers’ Pension Plan has about 45,000 active members and approximately 35,000 retired members. As

at December 31, 2014 the Municipal Pension Plan has about 185,000 active members, including approximately 24,000

from school districts.

Every three years, an actuarial valuation is performed to assess the financial position of the plans and the adequacy of

plan funding. The actuary determines an appropriate combined employer and member contribution rate to fund the

plans. The actuary’s calculated contribution rate is based on the entry-age normal cost method, which produces the

long-term rate of member and employer contributions sufficient to provide benefits for average future entrants to the

plans. This rate is then adjusted to the extent there is amortization of any funding deficit.

The most recent actuarial valuation of the Teachers’ Pension Plan as at December 31, 2014 indicated a $449 million

surplus for basic pension benefits on a going concern basis.

The most recent actuarial valuation for the Municipal Pension Plan as at December 31, 2012 indicated a $1,370 million

funding deficit for basic pension benefits on a going concern basis.

The next valuation for the Teachers’ Pension Plan will be as at December 31, 2017, with results available in 2018. The

next valuation for the Municipal Pension Plan will be as at December 31, 2015, with results available in 2016.

Employers participating in the plans record their pension expense as the amount of employer contributions made during

the fiscal year (defined contribution plan accounting). This is because the plans record accrued liabilities and accrued

assets for each plan in aggregate, resulting in no consistent and reliable basis for allocating the obligation, plan assets

and cost to individual employers participating in the plans.

School District No. 6 (Rocky Mountain) paid $3,230,000 for employer contributions to the plans for the year ended

June 30, 2016 (2015: $2,973,000).

13. RESTRICTED ASSETS - ENDOWMENT FUNDS

Donors have placed restrictions on their contributions to the endowment funds of the School District. One restriction

is that the original contribution should not be spent. Another potential restriction is that any investment income of the

endowment fund that is required to offset the eroding effect of inflation or preserve the original value of the endowment

should also not be spent.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 18

13. RESTRICTED ASSETS - ENDOWMENT FUNDS

(Continued)

Name of Endowment

Balance

June 30, 2015

Contributions

June 30, 2016

Balance

June 30, 2016

Tom Sanders Memorial

Scholarship $ 50,000 $ - $ 50,000

J. Alfred and Mollie Laird

Bursaries 22,739 - 22,739

Nathan Emery Memorial

Bursary 11,619 - 11,619

Alicia Raven Memorial

Scholarship 10,645 - 10,645

Other Scholarships and

Bursaries 10,870 - 10,870

Total $ 105,873 $ - $ 105,873

14. INTERFUND TRANSFERS

Interfund transfers between the operating, special purpose and capital funds for the year ended June 30, 2016 were as

follows:

Operating funds transferred to capital funds - $1,631,566

Special purpose funds transferred to capital funds - $105,053

15. RELATED PARTY TRANSACTIONS

The School District is related through common ownership to all Province of British Columbia ministries, agencies,

school districts, health authorities, colleges, universities, and crown corporations. Transactions with these entities,

unless disclosed separately, are considered to be in the normal course of operations and are recorded at the exchange

amount.

16. BUDGET FIGURES

Budget figures included in the financial statements are not audited. They were approved by the board through the

adoption of an annual budget on May 12, 2015.

17. EXPENSE BY OBJECT

2016 2015

Salaries and benefits $ 31,133,275 $ 29,257,240

Services and supplies 6,603,527 6,450,166

Interest 3,961 -

Amortization 2,785,020 2,653,161

$ 40,525,783 $ 38,360,567

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 19

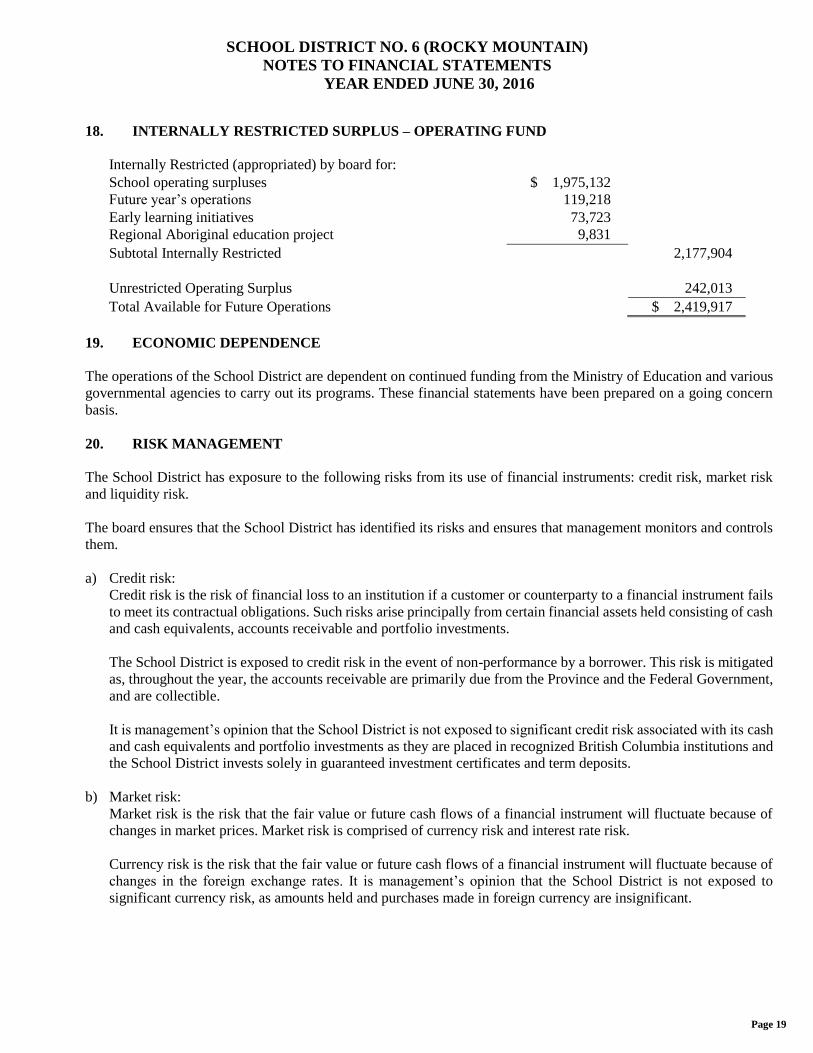

18. INTERNALLY RESTRICTED SURPLUS – OPERATING FUND

Internally Restricted (appropriated) by board for:

School operating surpluses $ 1,975,132

Future year’s operations 119,218

Early learning initiatives 73,723

Regional Aboriginal education project 9,831

Subtotal Internally Restricted 2,177,904

Unrestricted Operating Surplus 242,013

Total Available for Future Operations $ 2,419,917

19. ECONOMIC DEPENDENCE

The operations of the School District are dependent on continued funding from the Ministry of Education and various

governmental agencies to carry out its programs. These financial statements have been prepared on a going concern

basis.

20. RISK MANAGEMENT

The School District has exposure to the following risks from its use of financial instruments: credit risk, market risk

and liquidity risk.

The board ensures that the School District has identified its risks and ensures that management monitors and controls

them.

a) Credit risk:

Credit risk is the risk of financial loss to an institution if a customer or counterparty to a financial instrument fails

to meet its contractual obligations. Such risks arise principally from certain financial assets held consisting of cash

and cash equivalents, accounts receivable and portfolio investments.

The School District is exposed to credit risk in the event of non-performance by a borrower. This risk is mitigated

as, throughout the year, the accounts receivable are primarily due from the Province and the Federal Government,

and are collectible.

It is management’s opinion that the School District is not exposed to significant credit risk associated with its cash

and cash equivalents and portfolio investments as they are placed in recognized British Columbia institutions and

the School District invests solely in guaranteed investment certificates and term deposits.

b) Market risk:

Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of

changes in market prices. Market risk is comprised of currency risk and interest rate risk.

Currency risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of

changes in the foreign exchange rates. It is management’s opinion that the School District is not exposed to

significant currency risk, as amounts held and purchases made in foreign currency are insignificant.

SCHOOL DISTRICT NO. 6 (ROCKY MOUNTAIN)

NOTES TO FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2016

Page 20

20. RISK MANAGEMENT

(Continued)

b) Market risk: (continued)

Interest rate risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because

of changes in the market interest rates. The School District is exposed to interest rate risk through its portfolio

investments. It is management’s opinion that the School District is not exposed to significant interest rate risk as

it invests solely in guaranteed investment certificates and term deposits that have a maturity date of no more than

five years.

c) Liquidity risk:

Liquidity risk is the risk that the School District will not be able to meet its financial obligations as they become

due.

The School District manages liquidity risk by continually monitoring actual and forecasted cash flows from

operations and anticipated investing activities to ensure, as far as possible, that it will always have sufficient

liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable

losses or risking damage to the School District’s reputation.

Risk management and insurance services for all school districts in British Columbia are provided by the Risk

Management Branch of the Ministry of Finance.

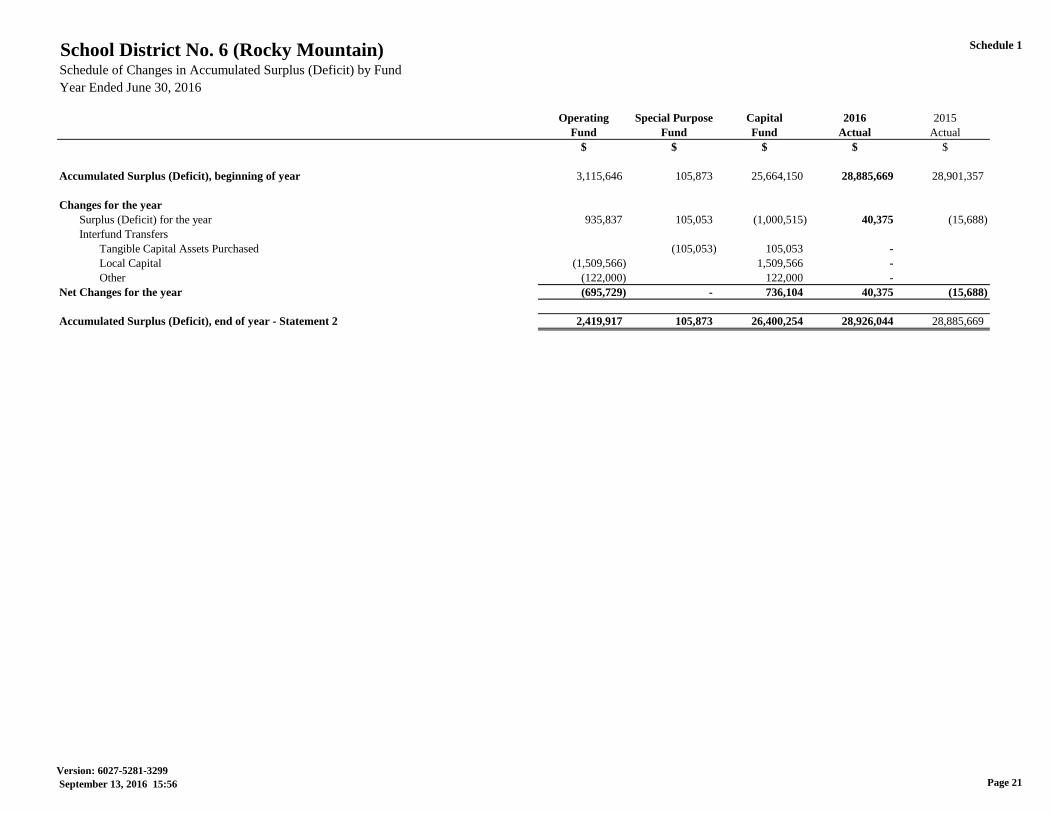

Schedule 1

Operating Special Purpose Capital 2016 2015

Fund Fund Fund Actual Actual

$ $ $ $ $

Accumulated Surplus (Deficit), beginning of year 3,115,646 105,873 25,664,150 28,885,669 28,901,357

Changes for the year

Surplus (Deficit) for the year 935,837 105,053 (1,000,515) 40,375 (15,688)

Interfund Transfers

Tangible Capital Assets Purchased (105,053) 105,053 -

Local Capital (1,509,566) 1,509,566 -

Other (122,000) 122,000 -

Net Changes for the year (695,729) - 736,104 40,375 (15,688)

Accumulated Surplus (Deficit), end of year - Statement 2 2,419,917 105,873 26,400,254 28,926,044 28,885,669

School District No. 6 (Rocky Mountain)Schedule of Changes in Accumulated Surplus (Deficit) by Fund

Year Ended June 30, 2016

Version: 6027-5281-3299

September 13, 2016 15:56 Page 21

Schedule 2

2016 2016 2015

Budget Actual Actual

$ $ $

Revenues

Provincial Grants

Ministry of Education 31,425,714 32,853,770 30,992,594

Other 2,000 2,200

Tuition 2,050,000 1,980,330 2,044,314

Other Revenue 920,341 1,192,990 506,178

Rentals and Leases 65,000 68,094 67,662

Investment Income 100,000 111,710 142,780

Total Revenue 34,561,055 36,208,894 33,755,728

Expenses

Instruction 26,575,872 27,811,010 26,073,165

District Administration 1,256,099 1,257,358 1,239,260

Operations and Maintenance 4,624,137 4,610,339 4,575,412

Transportation and Housing 1,571,829 1,594,350 1,566,836

Total Expense 34,027,937 35,273,057 33,454,673

Operating Surplus (Deficit) for the year 533,118 935,837 301,055

Budgeted Appropriation (Retirement) of Surplus (Deficit) 626,578

Net Transfers (to) from other funds

Local Capital (1,159,696) (1,509,566) (773,472)

Other (122,000)

Total Net Transfers (1,159,696) (1,631,566) (773,472)

Total Operating Surplus (Deficit), for the year - (695,729) (472,417)

Operating Surplus (Deficit), beginning of year 3,115,646 3,588,063

Operating Surplus (Deficit), end of year 2,419,917 3,115,646

Operating Surplus (Deficit), end of year

Internally Restricted 2,177,904 2,733,174

Unrestricted 242,013 382,472

Total Operating Surplus (Deficit), end of year 2,419,917 3,115,646

School District No. 6 (Rocky Mountain)Schedule of Operating Operations

Year Ended June 30, 2016

Version: 6027-5281-3299

September 13, 2016 15:56 Page 22

Schedule 2A

2016 2016 2015

Budget Actual Actual

$ $ $

Provincial Grants - Ministry of Education

Operating Grant, Ministry of Education 31,322,736 32,729,505 31,345,544

AANDC/LEA Recovery (157,845) (176,714) (157,845)

Strike Savings Recovery (1,009,579)

Other Ministry of Education Grants

Labour Settlement Funding 516,058

Pay Equity 207,823 207,823 207,823

Funding for Graduated Adults 1,426 12,736

Economic Stability Dividend 22,922

Carbon Tax Reimbursement 53,000 53,858 53,843

Teacher EHB Plan Grant 16,533

Focus Group Workplan Grant 7,481

Curriculum Implementation Supports 8,300

Skills Training Grant 5,000

Aboriginal Provincial Gathering Grant 900

MyEd SD Academy Travel 750

Total Provincial Grants - Ministry of Education 31,425,714 32,853,770 30,992,594

Provincial Grants - Other 2,000 2,200

Tuition

Offshore Tuition Fees 2,050,000 1,980,330 2,044,314

Total Tuition 2,050,000 1,980,330 2,044,314

Other Revenues

Other School District/Education Authorities 997 17,013

LEA/Direct Funding from First Nations 157,845 175,344 157,845

Miscellaneous

Project Donations 739,696 965,565 314,599

Course Registration Fees 240 8,050

Artists in Education 7,800 7,720 7,800

Other 15,000 43,124 871

Total Other Revenue 920,341 1,192,990 506,178

Rentals and Leases 65,000 68,094 67,662

Investment Income 100,000 111,710 142,780

Total Operating Revenue 34,561,055 36,208,894 33,755,728

School District No. 6 (Rocky Mountain)Schedule of Operating Revenue by Source

Year Ended June 30, 2016

Version: 6027-5281-3299

September 13, 2016 15:56 Page 23

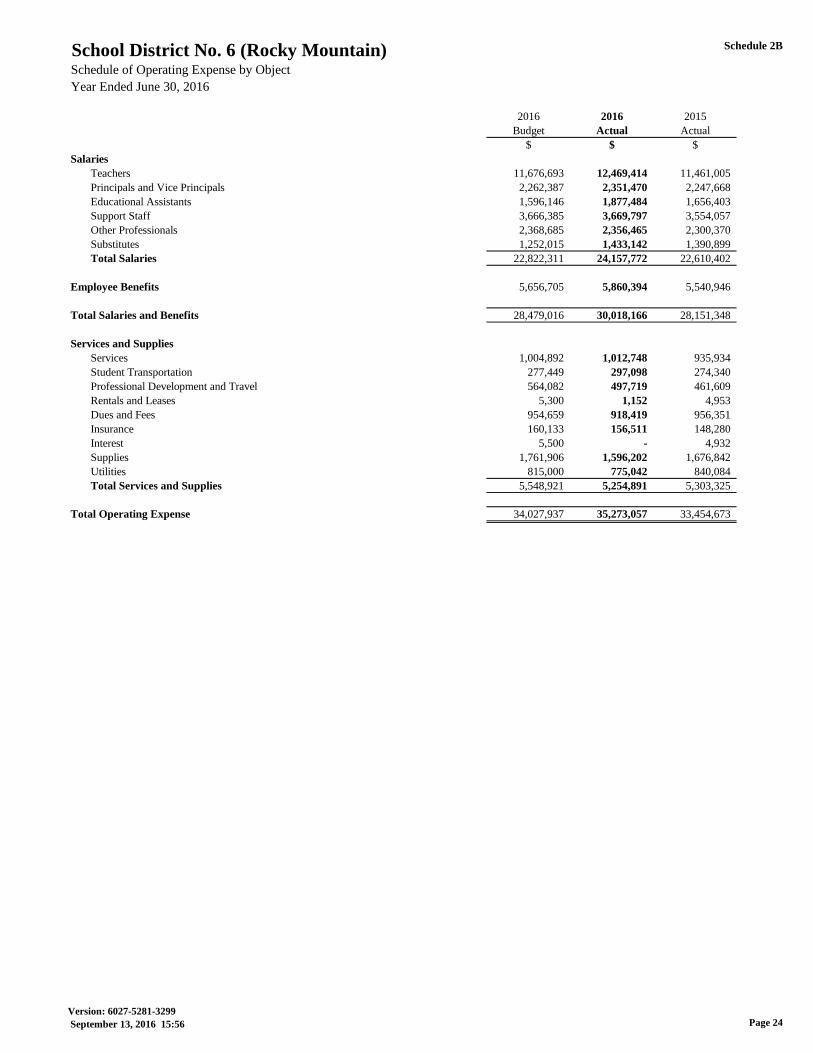

Schedule 2B

2016 2016 2015

Budget Actual Actual

$ $ $

Salaries

Teachers 11,676,693 12,469,414 11,461,005

Principals and Vice Principals 2,262,387 2,351,470 2,247,668

Educational Assistants 1,596,146 1,877,484 1,656,403

Support Staff 3,666,385 3,669,797 3,554,057

Other Professionals 2,368,685 2,356,465 2,300,370

Substitutes 1,252,015 1,433,142 1,390,899

Total Salaries 22,822,311 24,157,772 22,610,402

Employee Benefits 5,656,705 5,860,394 5,540,946

Total Salaries and Benefits 28,479,016 30,018,166 28,151,348

Services and Supplies

Services 1,004,892 1,012,748 935,934

Student Transportation 277,449 297,098 274,340

Professional Development and Travel 564,082 497,719 461,609

Rentals and Leases 5,300 1,152 4,953

Dues and Fees 954,659 918,419 956,351

Insurance 160,133 156,511 148,280

Interest 5,500 - 4,932

Supplies 1,761,906 1,596,202 1,676,842

Utilities 815,000 775,042 840,084

Total Services and Supplies 5,548,921 5,254,891 5,303,325

Total Operating Expense 34,027,937 35,273,057 33,454,673

School District No. 6 (Rocky Mountain)

Year Ended June 30, 2016

Schedule of Operating Expense by Object

Version: 6027-5281-3299

September 13, 2016 15:56 Page 24

Schedule 2CSchool District No. 6 (Rocky Mountain)Operating Expense by Function, Program and Object

Principals and Educational Support Other

Teachers Vice Principals Assistants Staff Professionals Substitutes Total

Salaries Salaries Salaries Salaries Salaries Salaries Salaries

$ $ $ $ $ $ $

1 Instruction

1.02 Regular Instruction 10,799,275 698,954 301,069 524,801 138,494 1,083,708 13,546,301

1.03 Career Programs 10,528 355 10,883

1.07 Library Services 143,782 117,475 128,551 3,891 393,699

1.08 Counselling 322,170 322,170

1.10 Special Education 1,171,557 144,846 1,513,383 16,032 316,377 137,088 3,299,283

1.30 English Language Learning 7,367 16,072 23,439

1.31 Aboriginal Education 63,032 403,481 23,486 489,999

1.41 School Administration 1,348,074 329,850 22,630 1,700,554

1.61 Continuing Education 14,735 14,735

1.62 Offshore Students 5,090 261,649 6,586 273,325

Total Function 1 12,469,414 2,325,421 1,877,484 1,004,324 1,120,001 1,277,744 20,074,388

4 District Administration

4.11 Educational Administration 178,426 178,426

4.40 School District Governance 103,177 103,177

4.41 Business Administration 534,277 534,277

Total Function 4 - - - - 815,880 - 815,880

5 Operations and Maintenance

5.41 Operations and Maintenance Administration 26,049 113,228 2,924 142,201

5.50 Maintenance Operations 1,956,963 146,054 78,811 2,181,828

5.52 Maintenance of Grounds 64,208 11,648 75,856

5.56 Utilities -

Total Function 5 - 26,049 - 2,021,171 259,282 93,383 2,399,885

7 Transportation and Housing

7.41 Transportation and Housing Administration 63,933 11,414 75,347

7.70 Student Transportation 644,302 97,369 50,601 792,272

Total Function 7 - - - 644,302 161,302 62,015 867,619

9 Debt Services

Total Function 9 - - - - - - -

Total Functions 1 - 9 12,469,414 2,351,470 1,877,484 3,669,797 2,356,465 1,433,142 24,157,772

Year Ended June 30, 2016

Page 25Version: 6027-5281-3299

September 13, 2016 15:56

Schedule 2CSchool District No. 6 (Rocky Mountain)Operating Expense by Function, Program and Object

1 Instruction

1.02 Regular Instruction

1.03 Career Programs

1.07 Library Services

1.08 Counselling

1.10 Special Education

1.30 English Language Learning

1.31 Aboriginal Education

1.41 School Administration

1.61 Continuing Education

1.62 Offshore Students

Total Function 1

4 District Administration

4.11 Educational Administration

4.40 School District Governance

4.41 Business Administration

Total Function 4

5 Operations and Maintenance

5.41 Operations and Maintenance Administration

5.50 Maintenance Operations

5.52 Maintenance of Grounds

5.56 Utilities

Total Function 5

7 Transportation and Housing

7.41 Transportation and Housing Administration

7.70 Student Transportation

Total Function 7

9 Debt Services

Total Function 9

Total Functions 1 - 9

Year Ended June 30, 2016

Total Employee Total Salaries Services and 2016 2016 2015

Salaries Benefits and Benefits Supplies Actual Budget Actual

$ $ $ $ $ $ $

13,546,301 3,341,693 16,887,994 1,062,765 17,950,759 16,831,155 16,680,630

10,883 2,768 13,651 30,360 44,011 23,799 23,501

393,699 102,921 496,620 158,135 654,755 637,154 592,974

322,170 83,307 405,477 8,746 414,223 411,262 350,896

3,299,283 848,143 4,147,426 229,148 4,376,574 4,266,833 4,087,284

23,439 5,639 29,078 731 29,809 33,791 29,653

489,999 124,014 614,013 62,086 676,099 636,738 640,746

1,700,554 390,999 2,091,553 129,094 2,220,647 2,249,414 2,213,956

14,735 3,838 18,573 18,573 19,370 17,219

273,325 43,855 317,180 1,108,380 1,425,560 1,466,356 1,436,306

20,074,388 4,947,177 25,021,565 2,789,445 27,811,010 26,575,872 26,073,165

178,426 49,578 228,004 20,549 248,553 235,720 240,747

103,177 1,690 104,867 62,673 167,540 201,153 185,670

534,277 124,775 659,052 182,213 841,265 819,226 812,843

815,880 176,043 991,923 265,435 1,257,358 1,256,099 1,239,260

142,201 31,212 173,413 117,399 290,812 301,424 282,653

2,181,828 487,184 2,669,012 572,818 3,241,830 3,314,577 3,241,458

75,856 15,779 91,635 97,362 188,997 189,460 174,546

- - 888,700 888,700 818,676 876,755

2,399,885 534,175 2,934,060 1,676,279 4,610,339 4,624,137 4,575,412

75,347 15,005 90,352 11,780 102,132 110,450 100,532

792,272 187,994 980,266 511,952 1,492,218 1,461,379 1,466,304

867,619 202,999 1,070,618 523,732 1,594,350 1,571,829 1,566,836

- - - - - - -

24,157,772 5,860,394 30,018,166 5,254,891 35,273,057 34,027,937 33,454,673

Page 26Version: 6027-5281-3299

September 13, 2016 15:56

Schedule 3

2016 2016 2015

Budget Actual Actual

$ $ $

Revenues

Provincial Grants

Ministry of Education 1,599,114 1,505,973 1,464,015

Other 57,500 37,394

Other Revenue 1,024,911 1,020,493 927,199

Investment Income 4,500 4,938 4,915

Total Revenue 2,686,025 2,568,798 2,396,129

Expenses

Instruction 2,560,258 2,349,701 2,175,006

District Administration 8,119 6,623 945

Operations and Maintenance 107,421 76,782

Total Expense 2,568,377 2,463,745 2,252,733

Special Purpose Surplus (Deficit) for the year 117,648 105,053 143,396

Net Transfers (to) from other funds

Tangible Capital Assets Purchased (117,648) (105,053) (143,396)

Total Net Transfers (117,648) (105,053) (143,396)

Total Special Purpose Surplus (Deficit) for the year - - -

Special Purpose Surplus (Deficit), beginning of year 105,873 105,873

Special Purpose Surplus (Deficit), end of year 105,873 105,873

Special Purpose Surplus (Deficit), end of year

Endowment Contributions 105,873 105,873

Total Special Purpose Surplus (Deficit), end of year 105,873 105,873

School District No. 6 (Rocky Mountain)

Year Ended June 30, 2016

Schedule of Special Purpose Operations

Version: 6027-5281-3299

September 13, 2016 15:56 Page 27

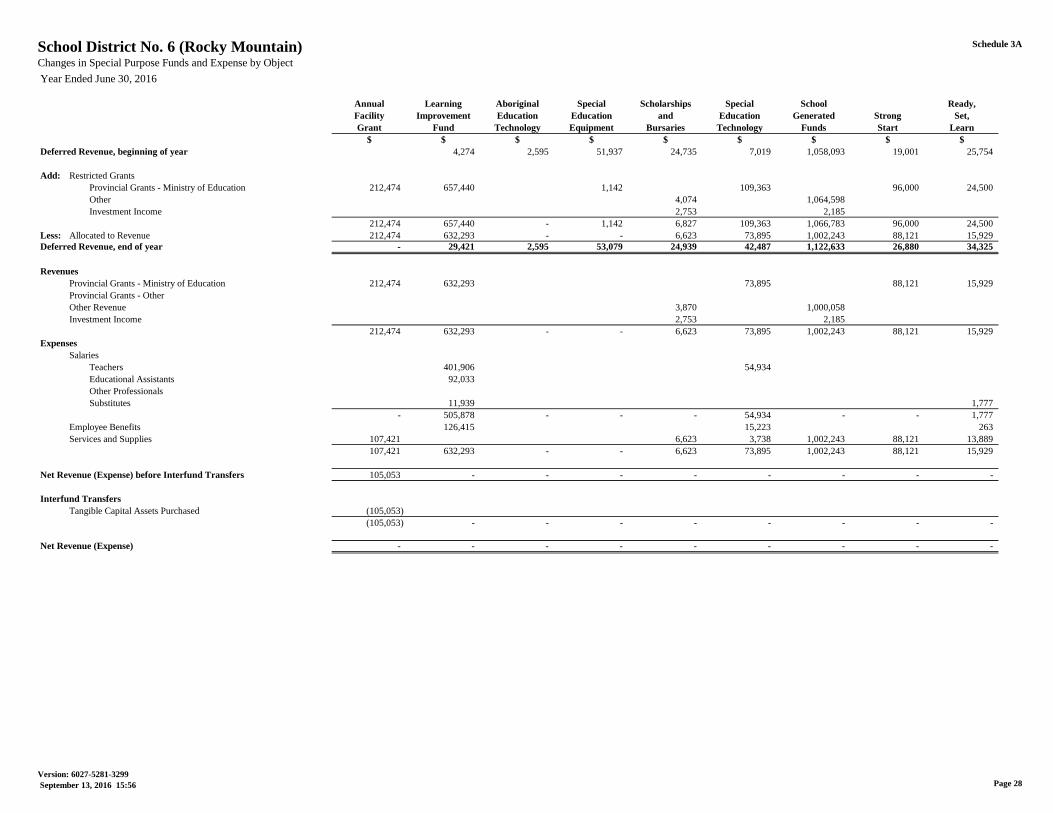

Schedule 3ASchool District No. 6 (Rocky Mountain)Changes in Special Purpose Funds and Expense by Object

Annual Learning Aboriginal Special Scholarships Special School Ready,

Facility Improvement Education Education and Education Generated Strong Set,

Grant Fund Technology Equipment Bursaries Technology Funds Start Learn

$ $ $ $ $ $ $ $ $

Deferred Revenue, beginning of year 4,274 2,595 51,937 24,735 7,019 1,058,093 19,001 25,754

Add: Restricted Grants

Provincial Grants - Ministry of Education 212,474 657,440 1,142 109,363 96,000 24,500

Other 4,074 1,064,598

Investment Income 2,753 2,185

212,474 657,440 - 1,142 6,827 109,363 1,066,783 96,000 24,500

Less: Allocated to Revenue 212,474 632,293 - - 6,623 73,895 1,002,243 88,121 15,929

Deferred Revenue, end of year - 29,421 2,595 53,079 24,939 42,487 1,122,633 26,880 34,325

Revenues

Provincial Grants - Ministry of Education 212,474 632,293 73,895 88,121 15,929

Provincial Grants - Other

Other Revenue 3,870 1,000,058

Investment Income 2,753 2,185

212,474 632,293 - - 6,623 73,895 1,002,243 88,121 15,929

Expenses

Salaries

Teachers 401,906 54,934

Educational Assistants 92,033

Other Professionals

Substitutes 11,939 1,777

- 505,878 - - - 54,934 - - 1,777

Employee Benefits 126,415 15,223 263

Services and Supplies 107,421 6,623 3,738 1,002,243 88,121 13,889

107,421 632,293 - - 6,623 73,895 1,002,243 88,121 15,929

Net Revenue (Expense) before Interfund Transfers 105,053 - - - - - - - -

Interfund Transfers

Tangible Capital Assets Purchased (105,053)

(105,053) - - - - - - - -

Net Revenue (Expense) - - - - - - - - -

Year Ended June 30, 2016

Page 28Version: 6027-5281-3299

September 13, 2016 15:56

Schedule 3ASchool District No. 6 (Rocky Mountain)Changes in Special Purpose Funds and Expense by Object

Deferred Revenue, beginning of year

Add: Restricted Grants

Provincial Grants - Ministry of Education

Other

Investment Income

Less: Allocated to Revenue

Deferred Revenue, end of year

Revenues

Provincial Grants - Ministry of Education

Provincial Grants - Other

Other Revenue

Investment Income

Expenses

Salaries

Teachers

Educational Assistants

Other Professionals

Substitutes

Employee Benefits

Services and Supplies

Net Revenue (Expense) before Interfund Transfers

Interfund Transfers

Tangible Capital Assets Purchased

Net Revenue (Expense)

Year Ended June 30, 2016

Service School

Community- Delivery Reach Out FSA POPFASD Student Based

OLEP LINK Transformation And Up! Testing Project Assistance Prevention TOTAL

$ $ $ $ $ $ $ $ $

32,222 51,206 25,000 14,229 7,468 1,075 50,000 1,374,608

90,786 369,891 8,696 1,570,292

2,336 1,071,008

4,938

90,786 369,891 - 2,336 8,696 - - - 2,646,238

116,406 358,159 - 16,565 8,696 - - 37,394 2,568,798

6,602 62,938 25,000 - - 7,468 1,075 12,606 1,452,048

116,406 358,159 8,696 1,505,973

37,394 37,394

16,565 1,020,493

4,938

116,406 358,159 - 16,565 8,696 - - 37,394 2,568,798

29,470 85,463 571,773

47,293 139,326

149,542 149,542

6,825 8,187 2,353 31,081

36,295 282,298 - - 8,187 - - 2,353 891,722

8,716 72,259 511 223,387

71,395 3,602 16,565 509 34,530 1,348,636

116,406 358,159 - 16,565 8,696 - - 37,394 2,463,745

- - - - - - - - 105,053

(105,053)

- - - - - - - - (105,053)

- - - - - - - - -

Year Ended June 30, 2016

Page 29Version: 6027-5281-3299

September 13, 2016 15:56

Schedule 4

2016 Invested in Tangible Local Fund 2015

Budget Capital Assets Capital Balance Actual

$ $ $ $ $

Revenues

Provincial Grants

Ministry of Education - 102,413

Investment Income 10,000 12,696 12,696 30,725

Gain (Loss) on Disposal of Tangible Capital Assets - 324,407

Amortization of Deferred Capital Revenue 1,775,723 1,775,770 1,775,770 1,735,477

Total Revenue 1,785,723 1,775,770 12,696 1,788,466 2,193,022

Expenses

Amortization of Tangible Capital Assets

Operations and Maintenance 2,550,051 2,456,516 2,456,516 2,413,386

Transportation and Housing 241,466 328,504 328,504 239,775

Debt Services

Capital Lease Interest 3,961 3,961

Total Expense 2,791,517 2,785,020 3,961 2,788,981 2,653,161

Capital Surplus (Deficit) for the year (1,005,794) (1,009,250) 8,735 (1,000,515) (460,139)

Net Transfers (to) from other funds

Tangible Capital Assets Purchased 117,648 105,053 105,053 143,396

Local Capital 1,159,696 1,509,566 1,509,566 773,472

Capital Lease Payment 122,000 122,000

Total Net Transfers 1,277,344 105,053 1,631,566 1,736,619 916,868

Other Adjustments to Fund Balances

Tangible Capital Assets Purchased from Local Capital 1,673,740 (1,673,740) -

Principal Payment

Capital Lease 148,132 (148,132) -

Total Other Adjustments to Fund Balances 1,821,872 (1,821,872) -

Total Capital Surplus (Deficit) for the year 271,550 917,675 (181,571) 736,104 456,729

Capital Surplus (Deficit), beginning of year 24,962,670 701,480 25,664,150 25,207,421

Capital Surplus (Deficit), end of year 25,880,345 519,909 26,400,254 25,664,150

School District No. 6 (Rocky Mountain)Schedule of Capital Operations

Year Ended June 30, 2016

2016 Actual

Version: 6027-5281-3299

September 13, 2016 15:56 Page 30

Schedule 4A

Furniture and Computer Computer

Sites Buildings Equipment Vehicles Software Hardware Total

$ $ $ $ $ $ $

Cost, beginning of year 7,037,914 89,597,309 2,168,729 3,584,898 143,709 1,070,692 103,603,251

Changes for the Year

Increase:

Purchases from:

Deferred Capital Revenue - Bylaw 1,214,600 1,214,600

Special Purpose Funds 26,988 78,065 105,053

Local Capital 1,141,567 107,369 126,722 37,320 260,762 1,673,740

Assests Acquired by Lease 644,917 644,917

Transferred from Work in Progress 152,513 152,513

26,988 2,586,745 107,369 126,722 37,320 905,679 3,790,823

Decrease:

Deemed Disposals 107,717 247,695 27,639 204,455 587,506

- - 107,717 247,695 27,639 204,455 587,506

Cost, end of year 7,064,902 92,184,054 2,168,381 3,463,925 153,390 1,771,916 106,806,568

Work in Progress, end of year 657,421 657,421

Cost and Work in Progress, end of year 7,064,902 92,841,475 2,168,381 3,463,925 153,390 1,771,916 107,463,989

Accumulated Amortization, beginning of year 44,134,555 837,110 1,345,994 52,552 413,088 46,783,299

Changes for the Year

Increase: Amortization for the Year 1,966,777 216,873 358,490 28,742 214,138 2,785,020

Decrease:

Deemed Disposals 107,717 247,695 27,639 204,455 587,506

- 107,717 247,695 27,639 204,455 587,506

Accumulated Amortization, end of year 46,101,332 946,266 1,456,789 53,655 422,771 48,980,813

Tangible Capital Assets - Net 7,064,902 46,740,143 1,222,115 2,007,136 99,735 1,349,145 58,483,176

School District No. 6 (Rocky Mountain)Tangible Capital Assets

Year Ended June 30, 2016

Version: 6027-5281-3299

September 13, 2016 15:56 Page 31

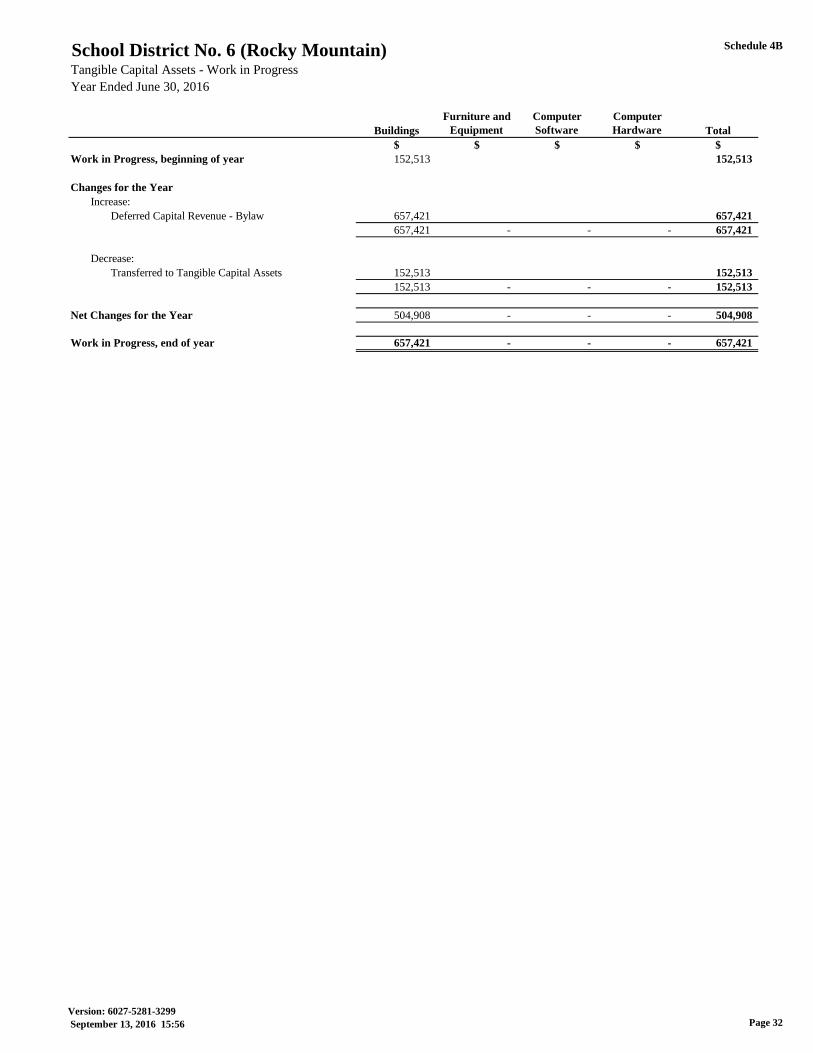

Schedule 4B

Furniture and Computer Computer

Buildings Equipment Software Hardware Total

$ $ $ $ $

Work in Progress, beginning of year 152,513 152,513

Changes for the Year

Increase:

Deferred Capital Revenue - Bylaw 657,421 657,421

657,421 - - - 657,421

Decrease:

Transferred to Tangible Capital Assets 152,513 152,513

152,513 - - - 152,513

Net Changes for the Year 504,908 - - - 504,908

Work in Progress, end of year 657,421 - - - 657,421

School District No. 6 (Rocky Mountain)Tangible Capital Assets - Work in Progress

Year Ended June 30, 2016

Version: 6027-5281-3299

September 13, 2016 15:56 Page 32

Schedule 4C

Bylaw Other Other Total

Capital Provincial Capital Capital

$ $ $ $

Deferred Capital Revenue, beginning of year 30,432,699 1,537,155 31,969,854

Changes for the Year

Increase:

Transferred from Deferred Revenue - Capital Additions 1,214,600 1,214,600

Transferred from Work in Progress 39,942 39,942

1,254,542 - - 1,254,542

Decrease:

Amortization of Deferred Capital Revenue 1,731,862 43,908 1,775,770

1,731,862 43,908 - 1,775,770

Net Changes for the Year (477,320) (43,908) - (521,228)

Deferred Capital Revenue, end of year 29,955,379 1,493,247 - 31,448,626

Work in Progress, beginning of year 39,942 39,942

Changes for the Year

Increase

Transferred from Deferred Revenue - Work in Progress 657,421 657,421

657,421 - - 657,421

Decrease

Transferred to Deferred Capital Revenue 39,942 39,942

39,942 - - 39,942

Net Changes for the Year 617,479 - - 617,479

Work in Progress, end of year 657,421 - - 657,421

Total Deferred Capital Revenue, end of year 30,612,800 1,493,247 - 32,106,047

School District No. 6 (Rocky Mountain)Deferred Capital Revenue

Year Ended June 30, 2016

Version: 6027-5281-3299

September 13, 2016 15:56 Page 33

Schedule 4D

MEd Other

Bylaw Restricted Provincial Land Other

Capital Capital Capital Capital Capital Total

$ $ $ $ $ $

Balance, beginning of year 10,057 55,921 65,978

Changes for the Year

Increase:

Provincial Grants - Ministry of Education 1,921,028 1,921,028

Other 20,000 20,000

Investment Income 1,385 1,385

1,921,028 21,385 - - - 1,942,413

Decrease:

Transferred to DCR - Capital Additions 1,214,600 1,214,600

Transferred to DCR - Work in Progress 657,421 657,421

1,872,021 - - - - 1,872,021

Net Changes for the Year 49,007 21,385 - - - 70,392

Balance, end of year 59,064 77,306 - - - 136,370

School District No. 6 (Rocky Mountain)Changes in Unspent Deferred Capital Revenue

Year Ended June 30, 2016

Version: 6027-5281-3299

September 13, 2016 15:56 Page 34