scheme booklet registered with australian securities and ... · mantra group limited domestique...

TRANSCRIPT

P +61 (0)7 5631 2500 F +61 (0)7 5631 2995 Level 15, 50 Cavill Avenue Surfers Paradise QLD 4217 PO Box 8016 Gold Coast MC QLD 9726 www.mantragroup.com.au Mantra Group Limited ACN 137 639 395 ABN 69 137 639 395

ASX Release

5 April 2018

Scheme Booklet registered with Australian Securities and Investment Commission Mantra Group Limited (ASX:MTR) ("Mantra") is pleased to announce that the Australian Securities and Investments Commission ("ASIC") has registered the Scheme Booklet in relation to the proposed Scheme of Arrangement (“Scheme”), under which all Mantra shares will be acquired by AAPC Limited (a subsidiary of Accor S.A.) ("AccorHotels"). A full copy of the Scheme Booklet, which includes the Independent Expert’s Report and Notice of Scheme Meeting for the Scheme Meeting, is attached to this announcement. Copies of the Scheme Booklet and proxy form will be sent to Mantra shareholders on or around Wednesday, 11 April 2018 (and those shareholders who have previously nominated an electronic means of notification to Mantra's share registry will receive an email where they can download the Scheme Booklet and lodge their proxy online). The Mantra Board continues to unanimously recommend that Mantra shareholders vote in favour of the Scheme at the Scheme Meeting to be held on 18 May 2018. For further information contact: Investors Media

Fiona van Wyk Lauren Thompson Mantra Group Limited Domestique Consulting +61 7 5631 2552 +61 2 9119 3078 [email protected] +61 438 954 729

This is an important document and requires your immediate attention.

You should read this document carefully and in its entirety before deciding whether or not to vote in favour of the resolution to approve the Scheme. If you are in doubt as to what you should do, you should consult your legal, financial or other professional adviser. If, after reading this Scheme Booklet, you have any questions about the Scheme or the number of Mantra Shares you hold or how to vote, please call the Shareholder Information Line on 1300 795 998 (within Australia) or +61 1300 795 998 (outside Australia) Monday to Friday between 8:30am and 5:30pm (Sydney time).

Financial Adviser Legal Advisers

SCHEME BOOKLETMantra Group Limited ACN 137 639 395

For a scheme of arrangement relating to the proposed acquisition of all of the ordinary shares in Mantra Group Limited by AAPC Limited, a subsidiary of Accor S.A., at a cash price of $3.96 per share.

Your Directors unanimously recommend that you vote in favour of the Scheme in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme to be in the best interests of Mantra Shareholders.

VOTE IN FAVOUR

DEFINED TERMSCapitalised terms used in this Scheme Booklet are defined in the Glossary in Section 8 of this Scheme Booklet.

NATURE OF THIS SCHEME BOOKLETThis Scheme Booklet provides Mantra Shareholders with information about the proposed acquisition of Mantra Group by AAPC by way of a scheme of arrangement between Mantra Group and Mantra Shareholders. A copy of the proposed Scheme is set out in Annexure C to this Scheme Booklet.

If you have sold all of your Mantra Shares, please disregard this document.

This Scheme Booklet includes the explanatory statement required to be sent to Mantra Shareholders for the Scheme Meeting in relation to the Scheme under Part 5.1 of the Corporations Act. A copy of the Notice of Scheme Meeting is set out in Annexure B.

You should read this Scheme Booklet carefully and in its entirety before making a decision as to how to vote on the resolution to be considered at the Scheme Meeting. If you are in doubt as to what you should do, you should consult your legal, financial or other professional adviser.

RESPONSIBILITY FOR INFORMATIONExcept as provided below, the information in this Scheme Booklet has been provided by Mantra Group and is the responsibility of Mantra Group. Mantra Group’s directors, officers and advisers do not assume any responsibility for the accuracy or completeness of any such information.

a. AAPC has provided and is responsible for the AAPC Information. Mantra Group and its directors, officers and advisers do not assume any responsibility for the accuracy or completeness of the AAPC Information.

b. The Independent Expert, Grant Thornton, has provided and is responsible for the information contained in the Independent Expert’s Report in Annexure A of this Scheme Booklet. Mantra Group, its directors, officers and advisers do not assume any responsibility for the accuracy or completeness of the information contained in Annexure A except in relation to information given by it to the Independent Expert. The Independent Expert does not assume any responsibility for the accuracy or completeness of the information contained in this Scheme Booklet other than that contained in Annexure A.

Mantra’s Share Registry, Link, has had no involvement in the preparation of any part of this Scheme Booklet other than being named as Mantra’s Share Registry. Link has not authorised or caused the issue of, and expressly disclaims and takes no responsibility for, any part of this Scheme Booklet.

INVESTMENT DECISIONSThe information in this Scheme Booklet does not constitute financial product advice. This Scheme Booklet has been prepared without reference to the investment objectives, financial situation or particular needs of any Mantra Shareholder or any other person. This Scheme Booklet should not be relied on as the sole basis for any investment decision. Independent legal, financial and taxation advice should be sought before making any investment decision in relation to your Mantra Shares.

NOT AN OFFERThis Scheme Booklet does not constitute or contain an offer to Mantra Shareholders or a solicitation of an offer from Mantra Shareholders, in any jurisdiction.

REGULATORY INFORMATIONThis document is the explanatory statement for the scheme of arrangement between Mantra Group and the holders of Mantra Shares as at the Scheme Record Date for the purposes of section 412(1) of the Corporations Act. A copy of the proposed Scheme is included in this Scheme Booklet as Annexure C.

A copy of this Scheme Booklet (including the Independent Expert’s Report) has been lodged with, and registered by, ASIC for the purposes of section 412(6) of the Corporations Act.

ASIC has been requested to provide a statement in accordance with section 411(17)(b) of the Corporations Act stating that it has no objection to the Scheme. If ASIC provides that statement, then it will be produced to the Court at the time of the Court hearing to approve the Scheme.

Neither ASIC nor any of its officers take any responsibility for the contents of this Scheme Booklet.

A copy of this Scheme Booklet has been lodged with ASX. Neither ASX nor any of its officers take any responsibility for the contents of this Scheme Booklet.

IMPORTANT NOTICE ASSOCIATED WITH COURT ORDER UNDER SUBSECTION 411(1) OF THE CORPORATIONS ACTThe fact that under subsection 411(1) of the Corporations Act the Court has

ordered that a meeting be convened and has approved the explanatory statement required to accompany the notice of the meeting does not mean that the Court:

a. has formed any view as to the merits of the proposed Scheme or as to how members should vote; or

b. has prepared, or is responsible for the content of, the explanatory statement.

NOTICE REGARDING SECOND COURT HEARING AND IF A MANTRA SHAREHOLDER WISHES TO OPPOSE THE SCHEMEThe date of the Second Court Hearing to approve the Scheme is Wednesday, 23 May 2018. The hearing will be at 10.15am (Sydney time) at the Federal Court of Australia at Law Courts Building, 184 Phillip Street, Sydney NSW 2000.

Each Mantra Shareholder has the right to appear and be heard at the Second Court Hearing and if desired, oppose the approval of the Scheme at the Second Court Hearing. If you wish to oppose in this manner, you must file and serve on Mantra Group a notice of appearance, in the prescribed form, together with any affidavit on which you wish to rely at the hearing. The notice of appearance and affidavit must be served on Mantra Group at its address for service at least one day before Wednesday, 23 May 2018. The address for service for Mantra Group is:

C/– Baker McKenzieTower One – International Towers SydneyLevel 46, 100 Barangaroo AvenueBarangaroo NSW 2000

Attention: Maria O’Brien

Maria.O’[email protected]

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTSThis Scheme Booklet contains both historical and forward-looking statements.

The forward-looking statements in this Scheme Booklet are not based on historical facts, but rather reflect the current views held only as at the date of this Scheme Booklet concerning future results and events and generally may be identified by the use of forward-looking words or phrases such as “believe”, “aim”, “expect”, “anticipated”, “intending”, “foreseeing”, “likely”, “should”, “planned”, “may”, “estimated”, “potential”, or other similar words and phrases. Similarly, statements that describe objectives, plans, goals or expectations are or may be forward-looking statements.

The statements in this Scheme Booklet about the impact that the Scheme may have

MANTRA GROUP SCHEME BOOKLET

IMPORTANT NOTICES

on the results of Mantra Group’s operations, and the advantages and disadvantages anticipated to result from the Scheme, are also forward-looking statements.

Mantra Group believes that any other forward-looking statements included in Section 3 of this Scheme Booklet have been made on reasonable grounds. Although Mantra Group believes that the views reflected in those forward-looking statements have been made on a reasonable basis, no assurance can be given that such views will prove to have been correct.

AAPC believes that any forward-looking statements included in the AAPC Information in Section 4 of this Scheme Booklet have been made on reasonable grounds. Although AAPC believes that the views reflected in those forward-looking statements have been made on a reasonable basis, no assurance can be given that such views will prove to have been correct.

These forward-looking statements involve known and unknown risks, uncertainties, assumptions and other factors that may cause Mantra Group’s actual results, performance or achievements to differ materially from the anticipated results, performance or achievements expressed, projected or implied by these forward-looking statements. Deviations as to future results, performance and achievements are both normal and to be expected, Mantra Shareholders should note that the historical financial performance of Mantra Group is no assurance of future financial performance of Mantra Group (whether the Scheme is implemented or not). Mantra Shareholders should carefully review all of the information included in this Scheme Booklet. The forward-looking statements included in this Scheme Booklet are made only as of the date of this Scheme Booklet. Neither Mantra Group, AccorHotels Group, nor their respective directors, officers or advisers give any representation, assurance or guarantee to Mantra Shareholders that any forward-looking statements will actually occur or be achieved. Mantra Shareholders are cautioned not to place undue reliance on such forward-looking statements.

Subject to any continuing obligations under law or the ASX Listing Rules, neither Mantra Group or AccorHotels Group give any undertaking to update or revise any forward-looking statements after the date of this Scheme Booklet to reflect any change in expectations in relation to those statements or any change in events, conditions or circumstances on which any such statement is based.

PRIVACY AND PERSONAL INFORMATIONMantra Group may collect personal information to implement the Scheme. The personal information may include the names, contact details and details of holdings of Mantra Shareholders, plus contact details of individuals appointed by Mantra Shareholders as proxies, corporate representatives or attorneys at the Scheme Meeting. The collection of some of this information is required or authorised by the Corporations Act.

Link advises that personal information it holds about you (including your name, address, and details of your financial assets) is collected by Link organisations to administer your investment. Personal information is held on the public register in accordance with Chapter 2C of the Corporations Act. Some or all of your personal information may be disclosed to contracted third parties, or related Link companies in Australia and overseas. Your information may also be disclosed to Australian government agencies, law enforcement agencies and regulators, or as required under other Australian law, contract, and court or tribunal order. For further details about Link’s personal information handling practices, including how you may access and correct your personal information and raise privacy concerns, visit Link’s website at www.linkmarketservices.com.au for a copy of the Link condensed privacy statement, or contact Link by phone on +61 1800 502 355 (free call within Australia) 9.00 am to 5.00 pm (Sydney time) Monday to Friday (excluding public holidays) to request a copy of Link’s complete privacy policy.

The information may be disclosed to print and mail service providers, and to Mantra Group and AccorHotels Group and their related bodies corporate and advisers to the extent necessary to effect the Scheme. If the information outlined above is not collected, Mantra Group may be hindered in, or prevented from, conducting the Scheme Meeting or implementing the Scheme effectively or at all. Mantra Shareholders who appoint an individual as their proxy, corporate representative or attorney to vote at the Scheme Meeting should inform that individual of the matters outlined above.

NOTICE TO PERSONS OUTSIDE AUSTRALIAThe release, publication or distribution of this Scheme Booklet in jurisdictions other than Australia may be restricted by law or

regulation in such other jurisdictions and persons outside of Australia who come into possession of this Scheme Booklet should seek advice on and observe any such restrictions. Any failure to comply with such restrictions may constitute a violation of applicable laws or regulations.

This Scheme Booklet has been prepared in accordance with Australian law and the information contained in this Scheme Booklet may not be the same as that which would have been disclosed if the Scheme Booklet had been prepared in accordance with the laws and regulations outside Australia.

This Scheme Booklet and the Scheme are subject to Australian disclosure requirements, which may be different from the requirements applicable in other jurisdictions. The financial information included in this document is based on financial statements that have been prepared in accordance with Australian equivalents to International Financial Reporting Standards, which may differ from generally accepted accounting principles in other jurisdictions.

This Scheme Booklet and the Scheme do not in any way constitute an offer of securities in any place in which, or to any person to whom, it would not be lawful to make such an offer.

EFFECT OF ROUNDINGA number of figures, amounts, percentages, estimates, calculations of value and fractions in this Scheme Booklet are subject to the effect of rounding. Accordingly, the actual calculation of these figures may differ from the figures set out in this Scheme Booklet.

TIMES AND DATESUnless otherwise stated, all times referred to in this Scheme Booklet are times in Sydney, Australia. All dates following the date of the Scheme Meeting are indicative only and are subject to the Court approval process and the satisfaction or, where applicable, waiver of the conditions precedent to the implementation of the Scheme (see Section 1 of this Scheme Booklet).

CURRENCYThe financial amounts in this Scheme Booklet are expressed in Australian currency unless otherwise stated. A reference to $ and cents is to Australian currency, unless otherwise stated.

DATEThis Scheme Booklet is dated 4 April 2018.

SCHEME BOOKLET MANTRA GROUP 1

KEY DATES 3

CHAIRMAN’S LETTER 4

HOW TO VOTE 8

FREQUENTLY ASKED QUESTIONS 10

1. SUMMARY OF THE SCHEME 16

2. KEY CONSIDERATIONS RELEVANT TO YOUR VOTE 25

3. INFORMATION ON MANTRA GROUP 30

4. AAPC INFORMATION 41

5. RISKS ASSOCIATED WITH MANTRA GROUP 46

6. TAXATION IMPLICATIONS 50

7. ADDITIONAL INFORMATION 54

8. GLOSSARY 59

ANNEXURE A. INDEPENDENT EXPERT’S REPORT 66

ANNEXURE B. NOTICE OF SCHEME MEETING 149

ANNEXURE C. SCHEME OF ARRANGEMENT 153

ANNEXURE D. SCHEME DEED POLL 165

CORPORATE DIRECTORY IBC

2 MANTRA GROUP SCHEME BOOKLET

CONTENTS

SCHEME BOOKLET MANTRA GROUP 3

KEY DATES

EVENT1 TIME/DATE

First Court Date 4 April 2018

Date of this Scheme Booklet 4 April 2018

Scheme Meeting proxies – the last date by which proxy forms for the Scheme Meeting must be received by the Share Registry.

10.00am (Sydney time) on 16 May 2018

Voting Record Date – the date and time for determining who can vote at the Scheme Meeting. 7.00pm (Sydney time) on 16 May 2018

Date of Scheme Meeting – to be held at Tower One – International Towers Sydney, Level 46, 100 Barangaroo Avenue, Sydney NSW 2000.

10.00am (Sydney time) on 18 May 2018

IF THE SCHEME IS APPROVED BY MANTRA SHAREHOLDERS AT THE SCHEME MEETING:

Second Court Date to approve the Scheme 23 May 2018

Effective Date – the date on which the Scheme comes into effect and is binding on Mantra Shareholders. The Court order will be lodged with ASIC and announced on the ASX. Mantra Shares will be suspended from trading at the close of trading on the Effective Date. If the Scheme proceeds, this will be the last day that Mantra Shares will trade on the ASX.

23 May 2018

Special Dividend Record Date 7.00pm (Sydney time) on 25 May 2018

Scheme Record Date – all Mantra Shareholders who hold Mantra Shares on the Scheme Record Date will be entitled to receive the Scheme Consideration.

7.00pm (Sydney time) on 28 May 2018

Special Dividend Payment Date 30 May 2018

Implementation Date – all Scheme Shareholders will be paid the Scheme Consideration to which they are entitled on this date.

31 May 2018

1. All dates following the date of the Scheme Meeting are indicative only and are subject to the Court approval process and the satisfaction or, where applicable, waiver of the conditions precedent to the implementation of the Scheme (see Section 1 of this Scheme Booklet). All dates and times, unless otherwise indicated, refer to the date and time in Sydney, Australia. Any changes to the above timetable will be announced to ASX and notified on Mantra Group’s website at www.mantragroup.com.au.

CHAIRMAN’S LETTER

Dear Mantra Shareholder,

On behalf of the Mantra Board, I am pleased to provide you with this Scheme Booklet, which contains information relating to the proposed acquisition of Mantra Group by AAPC Limited (a subsidiary of Accor S.A.).

On 12 October 2017, Mantra Group announced that it had entered into a binding Scheme Implementation Agreement under which AAPC Limited (a subsidiary of Accor S.A.) agreed to acquire all Mantra Shares under a scheme of arrangement1. Implementation of the Scheme is subject to the satisfaction of customary conditions including obtaining the approval of Mantra Shareholders. All regulatory approvals required in relation to the Scheme (including ACCC and FIRB) have been obtained.

If the Scheme is approved, Mantra Shareholders will receive an aggregate cash payment of $3.96 per Mantra Share, which will comprise:

• a fully franked special dividend of $0.16 per Mantra Share held on the Special Dividend Record Date, payable by Mantra Group; and

• the Scheme Consideration of $3.80 per Mantra Share held on the Scheme Record Date, payable by AAPC.

The Mantra Board believes that the offer from AAPC represents an attractive opportunity for Mantra Shareholders. The Total Cash Consideration of $3.96 represents a cash premium of:

• 22.6% over the previous closing price of Mantra Shares on 6 October 2017, the last trading day prior to confirmation that Mantra Group had received an indicative and non-binding proposal from AAPC2;

• 29.2% over the 30 day VWAP of Mantra Shares up to and including 6 October 20173; and

• 33.1% over the 90 day VWAP of Mantra Shares up to and including 6 October 20174.

The Total Cash Consideration equates to an underlying FY2017 P/E multiple5 of 23.7x and an underlying FY2017 EV/EBITDA multiple of 12.4x, both of which are considered by the Mantra Board to be attractive, when compared to the transaction multiples of comparable companies referenced by the Independent Expert’s Report and the trading multiples of Mantra Shares up to and including 6 October 2017.

For those Mantra Shareholders who are able to realise the full benefit of franking credits, the total value received is $4.03 per Mantra Share, which represents a 31.4% premium to the 30 day volume weighted average price6. Whether you will be able to realise the full benefit of the franking credits will depend on your individual tax circumstances.

DIRECTORS’ RECOMMENDATION

Your Directors unanimously recommend that Mantra Shareholders vote in favour of the Scheme, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme to be in the best interests of Mantra Shareholders.

Subject to the same qualifications, each of your Directors intends to vote, or cause to be voted, all the Mantra Shares held or controlled by them in favour of the Scheme at the Scheme Meeting.

Your Directors, having regard to multiple factors including the dynamics of the industry within which Mantra Group operates and the cash premium available to Mantra Shareholders compared to recent share trading results, believe that the Scheme is in the best interests of Mantra Shareholders for the following reasons:

• the Independent Expert has concluded that the Scheme is fair and reasonable and, therefore, in the best interests of Mantra Shareholders in the absence of a Superior Proposal;

• the Total Cash Consideration, and the premium which it represents, provides an attractive and compelling opportunity for Mantra Shareholders to realise immediate and certain value; and

• as at the date of this Scheme Booklet, a Superior Proposal has not been put forward since the receipt of the proposal from AAPC.

1. A scheme of arrangement is a commonly used legal procedure in Australia to undertake the acquisition of a publicly listed company.

2. Last closing price of $3.23 on 6 October 2017.

3. Volume weighted average price of $3.07 adjusted for the FY2017 final dividend of $0.06 per share.

4. Volume weighted average price of $2.98 adjusted for the FY2017 final dividend of $0.06 per share.

5. Based on NPATA (net profit after tax adjusted to add back expense relating to amortisation of lease rights).

6. Volume weighted average price up to and including 6 October 2017 of $3.07 adjusted for the FY2017 final dividend of $0.06 per share.

4 MANTRA GROUP SCHEME BOOKLET

For more details on the recommendation given by the Mantra Board, please consider Section 2 of this Scheme Booklet.

Although the Board’s unanimous recommendation to Mantra Shareholders is to vote in favour of the Scheme, you may disagree that the Scheme is in your best interests and instead prefer to retain your Mantra Shares. Some of the reasons you may wish to vote against the Scheme would be because you wish to continue to participate in the future financial performance of Mantra Group and maintain your existing investment profile. You may also believe that there is potential for a Superior Proposal to be made in relation to Mantra Group.

INDEPENDENT EXPERT

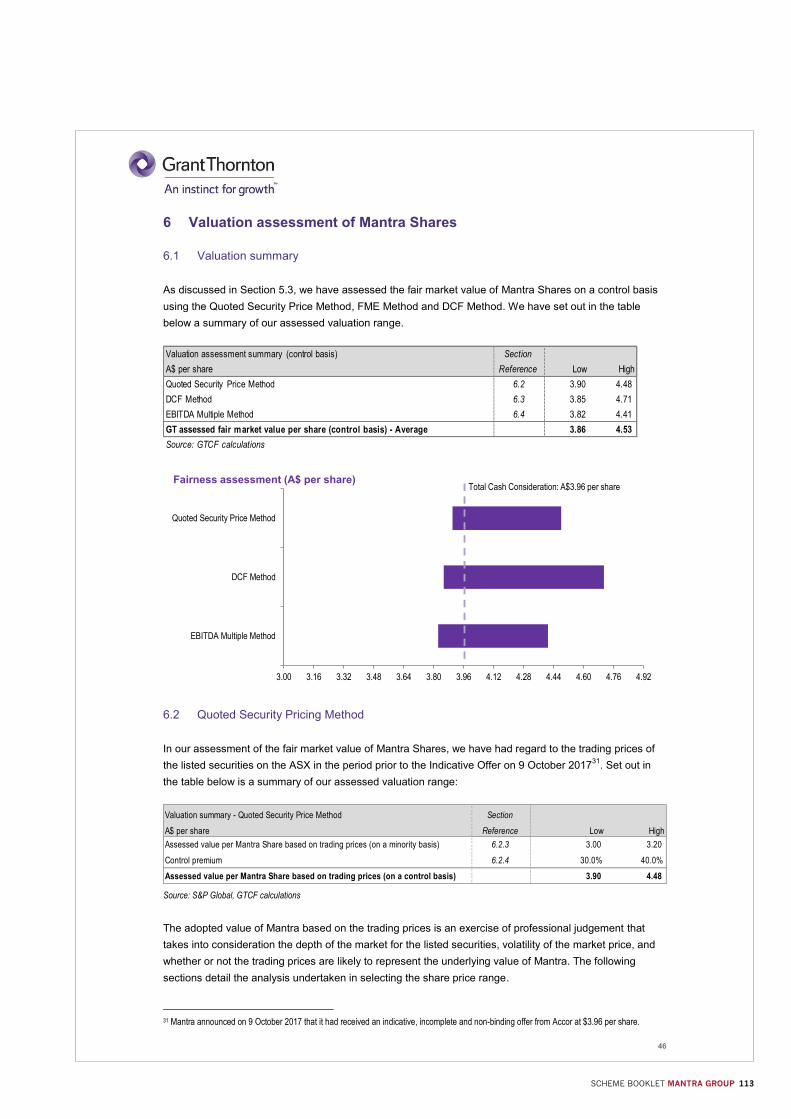

Your Directors appointed Grant Thornton as the Independent Expert to assess the merits of the Scheme. The Independent Expert has concluded that the Total Cash Consideration is fair and reasonable and, therefore, in the best interests of Mantra Shareholders, in the absence of a Superior Proposal.

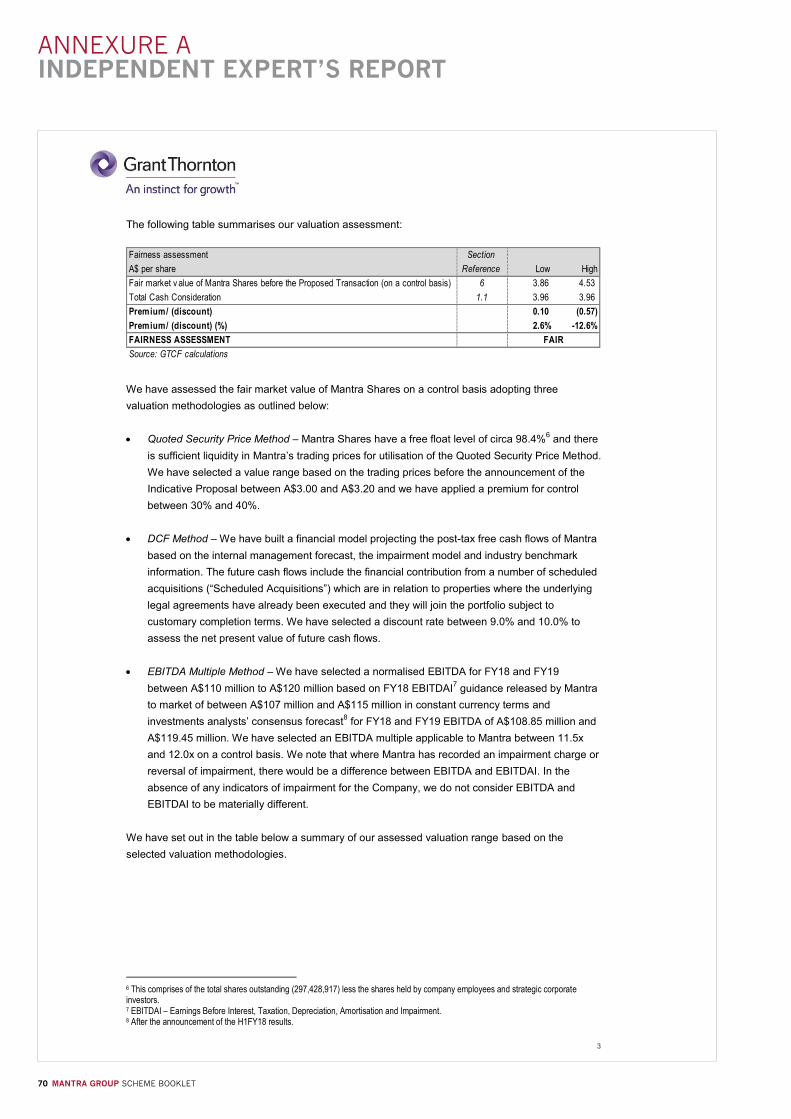

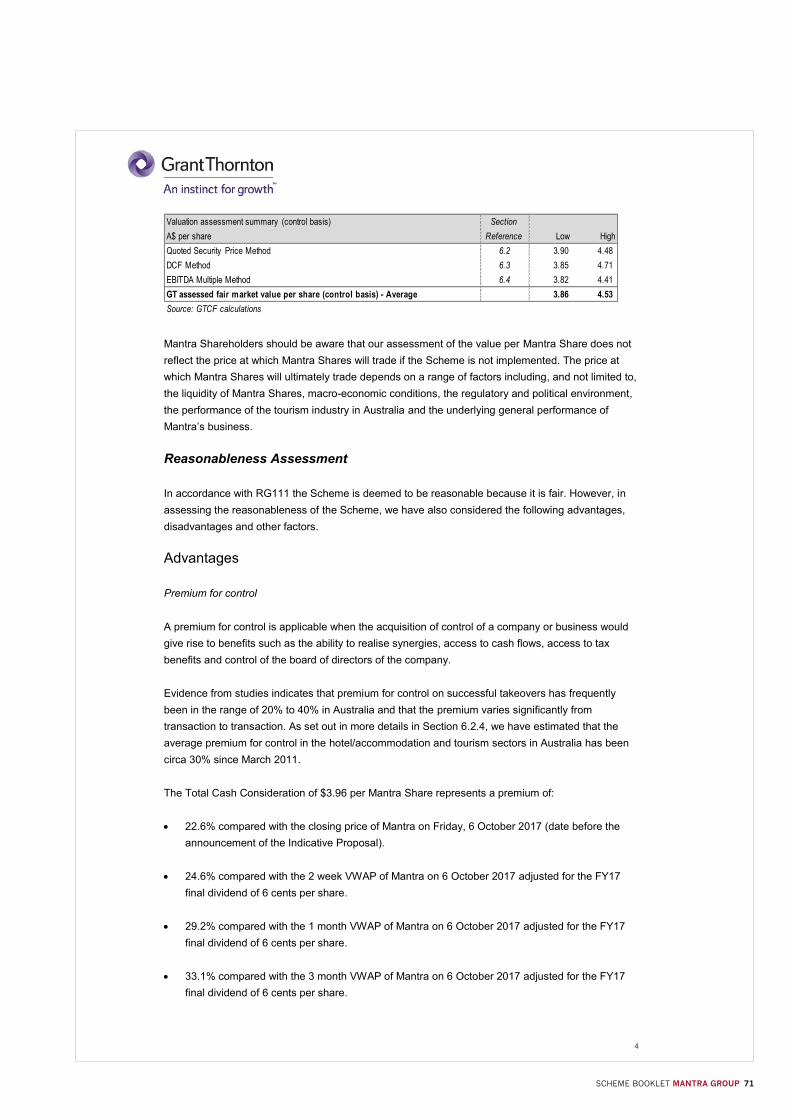

The Independent Expert has assessed the full underlying value of Mantra Group at between $3.86 and $4.53 per Mantra Share. The Total Cash Consideration of $3.96 per Mantra Share is within this range. Moreover, Mantra Group’s intention to pay a fully franked Special Dividend of $0.16 per Mantra Share (as part of the Total Cash Consideration) will deliver additional value of up to $0.07 per Mantra Share for Mantra Shareholders who are able to realise the full benefit of franking credits, reinforcing the Independent Expert’s conclusion.

A complete copy of the Independent Expert’s Report is included in Annexure A of this Scheme Booklet.

HOW TO VOTE

Your vote is important. In order for the Scheme to be implemented, the Scheme Resolution must be approved by the required majorities of Mantra Shareholders at the Scheme Meeting. The Scheme Meeting will be held at 10.00am (Sydney time) on 18 May 2018 at Tower One – International Towers Sydney, Level 46, 100 Barangaroo Avenue, Sydney NSW 2000.

For this reason, your Directors encourage you to vote by attending the Scheme Meeting – if you are unable to attend the Scheme Meeting, the Mantra Directors urge you to complete and return, in the enclosed reply paid envelope, the personalised proxy form that accompanies this Scheme Booklet or lodge your proxy form online at the Mantra Share Registry’s website (www.linkmarketservices.com.au) in accordance with the instructions given on the proxy form.

If you wish for the Scheme to proceed, it is important that you vote in favour of the Scheme.

ADDITIONAL INFORMATION

Your Directors encourage you to read this Scheme Booklet carefully and in its entirety, as it contains important information that will need to be considered before you vote on the Scheme Resolution. Your directors also encourage you to seek independent financial, legal and taxation advice before making any investment decision in relation to your Mantra Shares.

If you require further information or have questions in relation to the Scheme or this Scheme Booklet, please contact the Shareholder Information Line on 1300 795 998 (within Australia) or +61 1300 795 998 (outside Australia) Monday to Friday between 8.30am and 5.30pm (Sydney time).

I would like to thank you for your ongoing support of Mantra Group.

Yours sincerely,

Peter Bush

Chairman of the Board

SCHEME BOOKLET MANTRA GROUP 5

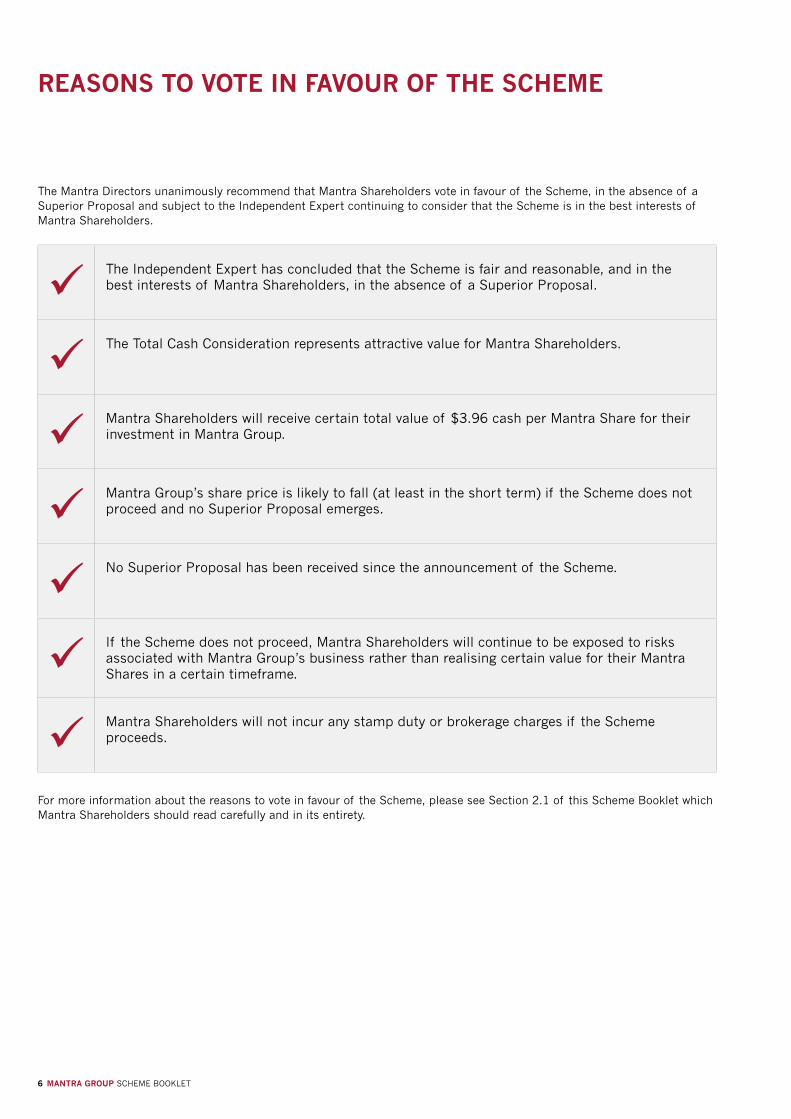

REASONS TO VOTE IN FAVOUR OF THE SCHEME

6 MANTRA GROUP SCHEME BOOKLET

The Mantra Directors unanimously recommend that Mantra Shareholders vote in favour of the Scheme, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider that the Scheme is in the best interests of Mantra Shareholders.

The Independent Expert has concluded that the Scheme is fair and reasonable, and in the best interests of Mantra Shareholders, in the absence of a Superior Proposal.

The Total Cash Consideration represents attractive value for Mantra Shareholders.

Mantra Shareholders will receive certain total value of $3.96 cash per Mantra Share for their investment in Mantra Group.

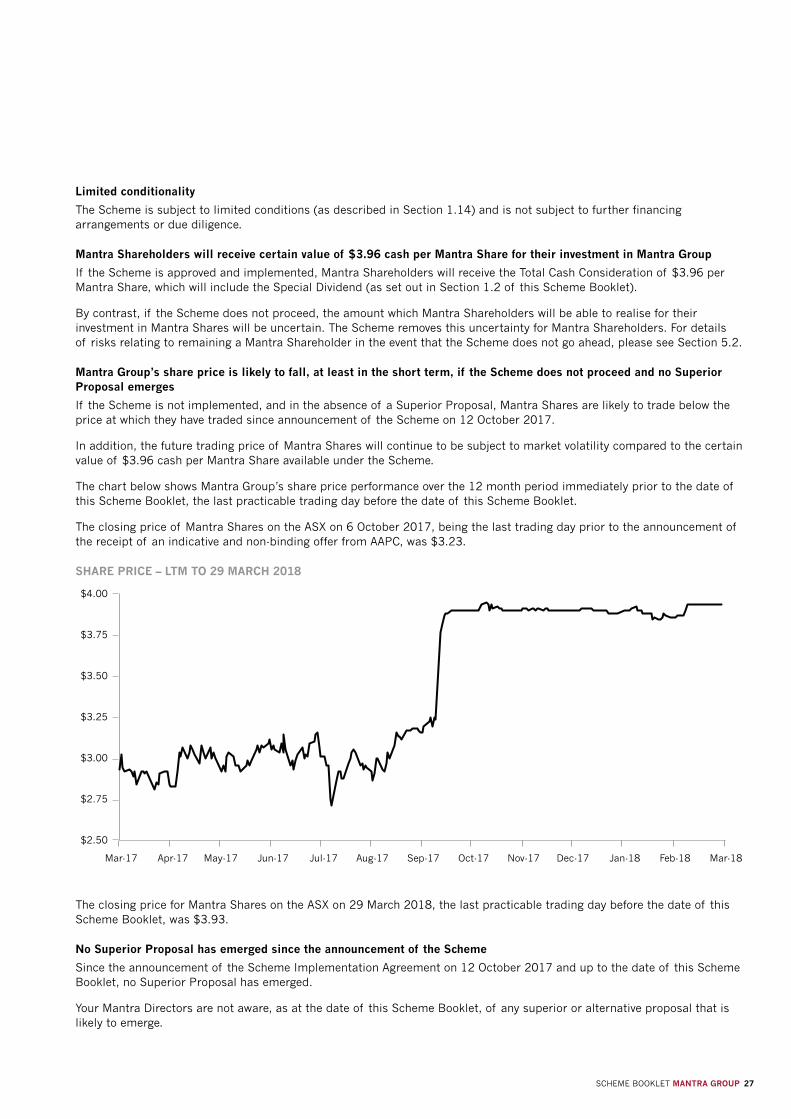

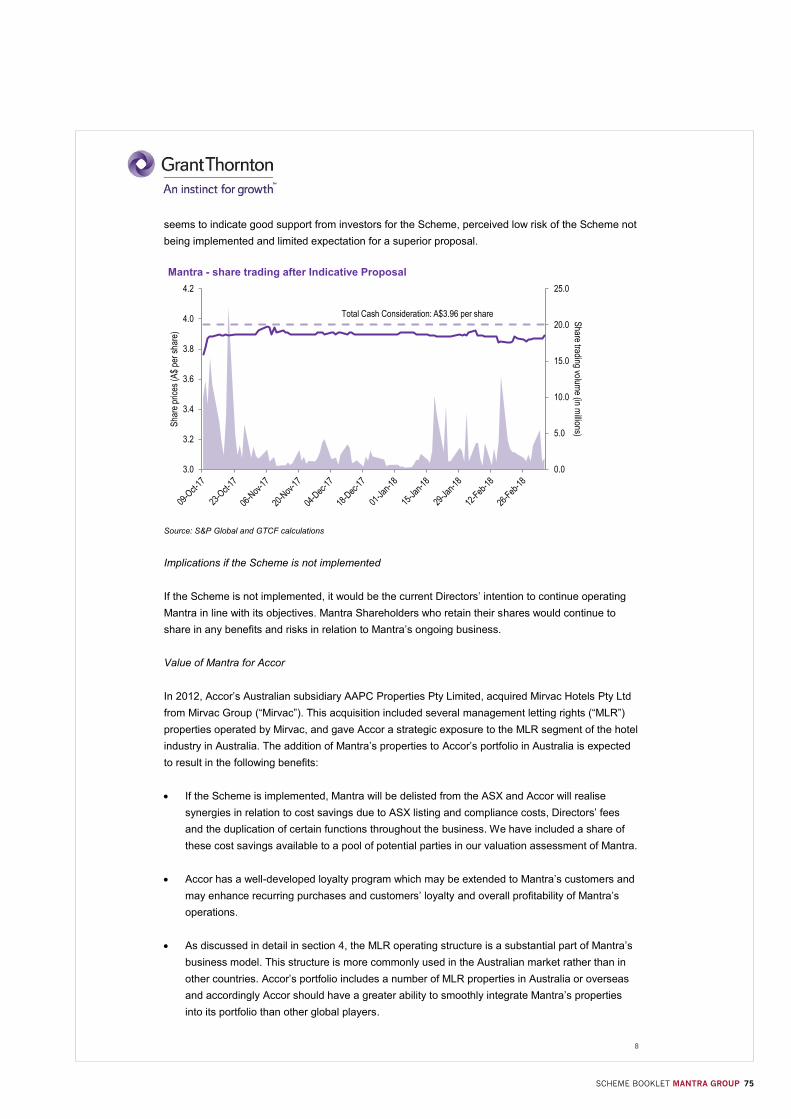

Mantra Group’s share price is likely to fall (at least in the short term) if the Scheme does not proceed and no Superior Proposal emerges.

No Superior Proposal has been received since the announcement of the Scheme.

If the Scheme does not proceed, Mantra Shareholders will continue to be exposed to risks associated with Mantra Group’s business rather than realising certain value for their Mantra Shares in a certain timeframe.

Mantra Shareholders will not incur any stamp duty or brokerage charges if the Scheme proceeds.

For more information about the reasons to vote in favour of the Scheme, please see Section 2.1 of this Scheme Booklet which Mantra Shareholders should read carefully and in its entirety.

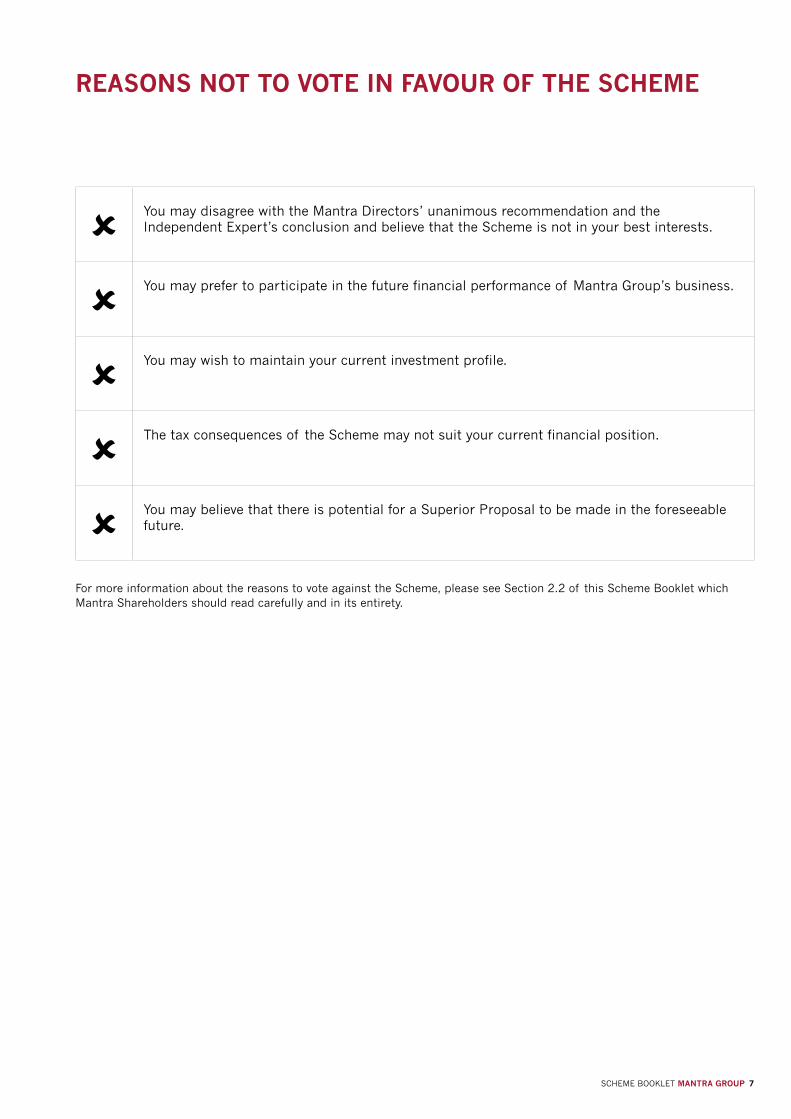

REASONS NOT TO VOTE IN FAVOUR OF THE SCHEME

SCHEME BOOKLET MANTRA GROUP 7

You may disagree with the Mantra Directors’ unanimous recommendation and the Independent Expert’s conclusion and believe that the Scheme is not in your best interests.

You may prefer to participate in the future financial performance of Mantra Group’s business.

You may wish to maintain your current investment profile.

The tax consequences of the Scheme may not suit your current financial position.

You may believe that there is potential for a Superior Proposal to be made in the foreseeable future.

For more information about the reasons to vote against the Scheme, please see Section 2.2 of this Scheme Booklet which Mantra Shareholders should read carefully and in its entirety.

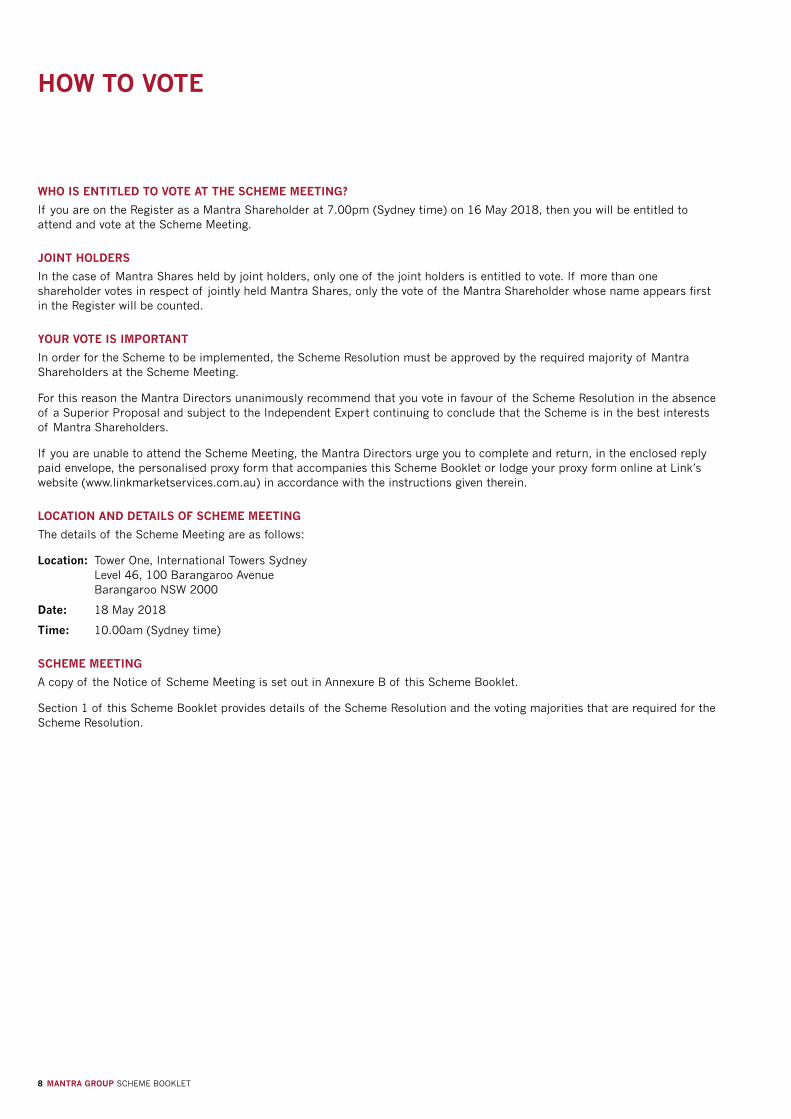

HOW TO VOTE

8 MANTRA GROUP SCHEME BOOKLET

WHO IS ENTITLED TO VOTE AT THE SCHEME MEETING?

If you are on the Register as a Mantra Shareholder at 7.00pm (Sydney time) on 16 May 2018, then you will be entitled to attend and vote at the Scheme Meeting.

JOINT HOLDERS

In the case of Mantra Shares held by joint holders, only one of the joint holders is entitled to vote. If more than one shareholder votes in respect of jointly held Mantra Shares, only the vote of the Mantra Shareholder whose name appears first in the Register will be counted.

YOUR VOTE IS IMPORTANT

In order for the Scheme to be implemented, the Scheme Resolution must be approved by the required majority of Mantra Shareholders at the Scheme Meeting.

For this reason the Mantra Directors unanimously recommend that you vote in favour of the Scheme Resolution in the absence of a Superior Proposal and subject to the Independent Expert continuing to conclude that the Scheme is in the best interests of Mantra Shareholders.

If you are unable to attend the Scheme Meeting, the Mantra Directors urge you to complete and return, in the enclosed reply paid envelope, the personalised proxy form that accompanies this Scheme Booklet or lodge your proxy form online at Link’s website (www.linkmarketservices.com.au) in accordance with the instructions given therein.

LOCATION AND DETAILS OF SCHEME MEETING

The details of the Scheme Meeting are as follows:

Location: Tower One, International Towers Sydney Level 46, 100 Barangaroo Avenue Barangaroo NSW 2000

Date: 18 May 2018

Time: 10.00am (Sydney time)

SCHEME MEETING

A copy of the Notice of Scheme Meeting is set out in Annexure B of this Scheme Booklet.

Section 1 of this Scheme Booklet provides details of the Scheme Resolution and the voting majorities that are required for the Scheme Resolution.

SCHEME BOOKLET MANTRA GROUP 9

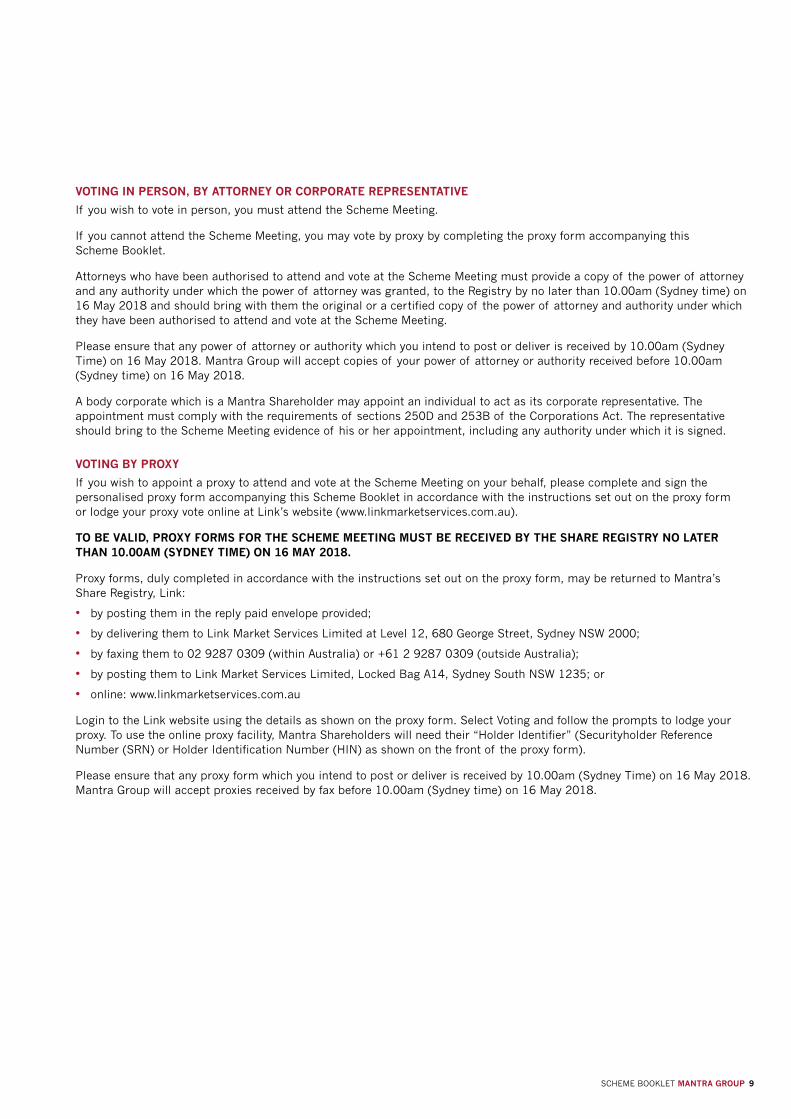

VOTING IN PERSON, BY ATTORNEY OR CORPORATE REPRESENTATIVE

If you wish to vote in person, you must attend the Scheme Meeting.

If you cannot attend the Scheme Meeting, you may vote by proxy by completing the proxy form accompanying this Scheme Booklet.

Attorneys who have been authorised to attend and vote at the Scheme Meeting must provide a copy of the power of attorney and any authority under which the power of attorney was granted, to the Registry by no later than 10.00am (Sydney time) on 16 May 2018 and should bring with them the original or a certified copy of the power of attorney and authority under which they have been authorised to attend and vote at the Scheme Meeting.

Please ensure that any power of attorney or authority which you intend to post or deliver is received by 10.00am (Sydney Time) on 16 May 2018. Mantra Group will accept copies of your power of attorney or authority received before 10.00am (Sydney time) on 16 May 2018.

A body corporate which is a Mantra Shareholder may appoint an individual to act as its corporate representative. The appointment must comply with the requirements of sections 250D and 253B of the Corporations Act. The representative should bring to the Scheme Meeting evidence of his or her appointment, including any authority under which it is signed.

VOTING BY PROXY

If you wish to appoint a proxy to attend and vote at the Scheme Meeting on your behalf, please complete and sign the personalised proxy form accompanying this Scheme Booklet in accordance with the instructions set out on the proxy form or lodge your proxy vote online at Link’s website (www.linkmarketservices.com.au).

TO BE VALID, PROXY FORMS FOR THE SCHEME MEETING MUST BE RECEIVED BY THE SHARE REGISTRY NO LATER THAN 10.00AM (SYDNEY TIME) ON 16 MAY 2018.

Proxy forms, duly completed in accordance with the instructions set out on the proxy form, may be returned to Mantra’s Share Registry, Link:

• by posting them in the reply paid envelope provided;

• by delivering them to Link Market Services Limited at Level 12, 680 George Street, Sydney NSW 2000;

• by faxing them to 02 9287 0309 (within Australia) or +61 2 9287 0309 (outside Australia);

• by posting them to Link Market Services Limited, Locked Bag A14, Sydney South NSW 1235; or

• online: www.linkmarketservices.com.au

Login to the Link website using the details as shown on the proxy form. Select Voting and follow the prompts to lodge your proxy. To use the online proxy facility, Mantra Shareholders will need their “Holder Identifier” (Securityholder Reference Number (SRN) or Holder Identification Number (HIN) as shown on the front of the proxy form).

Please ensure that any proxy form which you intend to post or deliver is received by 10.00am (Sydney Time) on 16 May 2018. Mantra Group will accept proxies received by fax before 10.00am (Sydney time) on 16 May 2018.

FREQUENTLY ASKED QUESTIONS

Question Answer More information

AN OVERVIEW OF THE SCHEME

Why have I received this Scheme Booklet?

You have received this Scheme Booklet because you are a Mantra Shareholder. Mantra Shareholders are being asked to vote on a Scheme under which AAPC would acquire all Mantra Shares for a Total Cash Consideration of $3.96 per Mantra Share, which comprises:

• a fully franked special dividend of $0.16 per Mantra Share held by a Mantra Shareholder on the Special Dividend Record Date, payable by Mantra Group; and

• the Scheme Consideration of $3.80 per Mantra Share held by a Mantra Shareholder on the Scheme Record Date, payable by AAPC.

This Scheme Booklet is intended to assist you in deciding how to vote on the Scheme Resolution which needs to be passed at the Scheme Meeting and, if passed by the required majority, the Scheme will proceed.

N/A

What is the Scheme?

The Scheme is a scheme of arrangement between Mantra Group and Mantra Shareholders. A scheme of arrangement is a statutory procedure which is commonly used in Australia to undertake an acquisition of a publicly listed company.

On 12 October 2017, Mantra Group announced the proposed Scheme to ASX. If the Scheme is approved and implemented, Mantra Shareholders who hold Mantra Shares on both the Scheme Record Date and Special Dividend Record Date will receive Total Cash Consideration of $3.96 cash for each Mantra Share they own.

Section 1 of this Scheme Booklet.

Who is AccorHotels Group?

Accor S.A. is a French company, acting as the holding company of the AccorHotels Group. Its shares are listed on the Euronext Paris Stock Exchange and are included in the CAC 40 index under ISIN code FR0000120404.

AAPC is an Australian public company, incorporated in Australia and ultimately controlled by Accor S.A.

AAPC trades in Australia as AccorHotels, and its business is the management and operation of hotels and resorts in Australia.

AccorHotels Group is a global travel and lifestyle group and digital innovator offering unique experiences in more than 4,200 hotels, resorts and residences around the world. Benefiting from dual expertise as an investor and operator, AccorHotels operates in 99 countries.

Its portfolio includes internationally renowned luxury brands such as Raffles, Sofitel Legend, SO Sofitel, Sofitel, Fairmont, Onefinestay, MGallery by Sofitel, Pullman and Swissôtel; the mid-range boutique hotel brands such as Novotel, Mercure, Mama Shelter and Adagio; and very popular budget brands such as JO&JOE, Ibis, Ibis Styles and Ibis budget, as well as the regional brands such as Grand Mercure, The Sebel and hotelF1.

AccorHotels also provides concierge services through its acquisition of John Paul.

There are currently over 200 hotels and over 27,000 rooms in Australia operating under AccorHotels Group’s brands with hotel businesses either owned or managed by AAPC and its subsidiaries or operated under a franchise arrangement.

For more information on AAPC and AccorHotels Group, please refer to Section 4 of this Scheme Booklet.

Section 4 of this Scheme Booklet.

10 MANTRA GROUP SCHEME BOOKLET

Question Answer More information

How will the Scheme be implemented?

In order for the Scheme to be implemented, all conditions precedent under the Scheme Implementation Agreement must be satisfied or waived (where capable of waiver), including that the Scheme Resolution must be approved by Mantra Shareholders at the Scheme Meeting and the Scheme must be approved by the Court.

Details of this Scheme Resolution and the majorities required to approve the resolution are set out in Section 1 of this Scheme Booklet.

Will I receive any further dividends from Mantra Group?

Subject to the Scheme becoming effective, Mantra Group will pay a fully franked Special Dividend of $0.16 per Mantra Share held by a Mantra Shareholder on the Special Dividend Record Date. The Special Dividend forms part of the Total Cash Consideration of $3.96 per Mantra Share.

Mantra Group has applied to the ATO requesting a class ruling to confirm the key taxation implications of the Scheme and the Special Dividend (Class Ruling). See Section 6 for further information.

No further dividends will be paid if the Scheme is implemented.

Section 6 of this Scheme Booklet.

What is the Special Dividend and will any franking credits attach to the Special Dividend?

The Special Dividend is a dividend that will be paid by Mantra Group if the Scheme becomes Effective.

The Special Dividend will be $0.16 per Mantra Share, fully franked and has a record date of 7.00pm (Sydney Time) on 25 May 2018. It will be paid on the Special Dividend Payment Date of 30 May 2018.

Those Mantra Shareholders who are able to realise the full benefit of franking credits will receive additional value of up to $0.07 per Mantra Share.

Whether a Mantra Shareholder will be able to realise the full benefit of the franking credits, will depend on their personal tax circumstances.

Section 6 of this Scheme Booklet.

What do the Mantra Directors recommend?

The Mantra Directors unanimously recommend that you vote in favour of the Scheme Resolution to approve the Scheme, in the absence of a Superior Proposal and subject to the Independent Expert continuing to conclude that the Scheme is in the best interests of Mantra Shareholders.

Section 1 of this Scheme Booklet.

How are the Mantra Directors intending to vote?

Each of the Mantra Directors intends to vote, or cause to be voted, in favour of the Scheme in respect of all the Mantra Shares they control, in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme to be in the best interests of Mantra Shareholders.

Section 1 of this Scheme Booklet.

What is the Independent Expert’s opinion of the Scheme?

The Independent Expert concluded that the Scheme is in the best interests of Mantra Shareholders, in the absence of a Superior Proposal. The Independent Expert, in arriving at this opinion, assessed whether the Scheme was fair and reasonable to the Mantra Shareholders.

The Independent Expert has estimated the full underlying value of Mantra Group to be in the range of $3.86 to $4.53 per share.

The Mantra Directors recommend that you read the Independent Expert’s Report carefully and in its entirety.

The Independent Expert’s Report is included in Annexure A of this Scheme Booklet.

SCHEME BOOKLET MANTRA GROUP 11

FREQUENTLY ASKED QUESTIONS

Question Answer More information

What will happen if a Superior Proposal emerges?

If Mantra Group receives a Competing Proposal from a third party, there are certain steps that must be taken by Mantra Group in respect of that proposal, including providing AAPC with the opportunity to make a matching or superior proposal.

Since the announcement of the Scheme on 12 October 2017 and up to the date of this Scheme Booklet, no Superior Proposal has been received.

Details of these provisions and other provisions in the Scheme Implementation Agreement are set out in Section 1 of this Scheme Booklet.

What are the risks and benefits associated with an investment in Mantra Group if the Scheme does not become Effective?

If the Scheme does not proceed, and no Superior Proposal is received, then Mantra Group’s share price is likely to fall or trade at a price below the Total Cash Consideration of $3.96 per Mantra Share, at least in the near term.

You will continue to be a Mantra Shareholder and participate in the future financial performance of Mantra Group’s business, and continue to be subject to the specific risks associated with Mantra Group’s business and other general risks.

Sections 2.2 and 5.2 of this Scheme Booklet.

AN OVERVIEW OF THE TOTAL CASH CONSIDERATION

What is the Total Cash Consideration?

If the Scheme becomes effective, Mantra Shareholders will receive a Total Cash Consideration of $3.96 for each Mantra Share they hold, provided they are registered in the Register on both the Scheme Record Date and Special Dividend Record Date.

Section 1.3 of this Scheme Booklet.

What is the premium of the Total Cash Consideration to Mantra Group’s Share price?

The Total Cash Consideration of $3.96 cash per share represents a premium of:

• 22.6% over the previous closing price of Mantra Shares on 6 October 20171, the last trading day prior to confirmation that Mantra Group received an indicative and non-binding proposal from AAPC;

• 29.2% over the 30 day VWAP of Mantra Shares up to and including 6 October 20172; and

• 33.1% over the 90 day VWAP of Mantra Shares up to and including 6 October 20173.

Section 2 of this Scheme Booklet.

How is AAPC funding the Scheme Consideration?

Accor S.A. and AAPC intend to fund the Scheme Consideration using either or both cash and cash equivalent investments on hand (including cash proceeds which may be received from any business or asset sales undertaken by the AccorHotels Group prior to the Implementation Date) or debt facilities.

Accor S.A. has put in place a €900,000,000.00 bridge financing arrangement to fund part or all of the Scheme Consideration, if necessary. In any event, Accor S.A. has in place a €1,800,000,000.00 Multi-Currency Revolving Credit Facility Agreement with undrawn borrowing capacity well in excess of the total Scheme Consideration. The availability of funds under the revolving credit facility is not subject to any conditions to borrowing which are outside the control of Accor S.A. The revolving credit facility is provided by a syndicate of lenders comprising various financial institutions, including Société Générale as Facility Agent, The Bank of Tokyo-Mitsubishi UFJ, Ltd., BNP Paribas, Commerzbank Aktiengesellschaft, Crédit Agricole Corporate and Investment Bank as Coordinators and 18 French and International Bank Institutions as Mandated Lead Arrangers and Bookrunners.

Section 4.6 of this Scheme Booklet.

1. Last closing price of $3.23 on 6 October 2017.

2. Volume weighted average price of $3.07 adjusted for the FY2017 final dividend of $0.06 per share.

3. Volume weighted average price of $2.98 adjusted for the FY2017 final dividend of $0.06 per share.

12 MANTRA GROUP SCHEME BOOKLET

Question Answer More information

Who is entitled to participate in the Scheme?

Persons who hold Mantra Shares on the Scheme Record Date will participate in the Scheme and, if the Scheme is approved and implemented, those persons will receive the Total Cash Consideration of $3.96 cash in respect of each Mantra Share held both on the Special Dividend Record Date and on the Scheme Record Date.

Section 1 of this Scheme Booklet.

When will I be paid?

Payment of the Scheme Consideration is expected to be made on 31 May 2018, and payment of the Special Dividend is expected to be made on 30 May 2018.

Section 1 of this Scheme Booklet.

How will I be paid?

All payments (including the Special Dividend) will be made by direct deposit into your nominated bank account, as advised to the Registry. If you have not nominated a bank account, payments will be made by cheque.

Section 1 of this Scheme Booklet.

What are the tax implications of the Scheme for you?

The tax implications for Scheme Shareholders if the Scheme is approved and implemented will depend on the specific taxation circumstances of each Scheme Shareholder.

General information about the likely Australian tax consequences of the Scheme is set out in Section 6 of this Scheme Booklet. You should not rely on this general information as advice for your own affairs.

For information about your individual financial or taxation circumstances please consult your financial, legal, taxation or other professional adviser.

Section 6 of this Scheme Booklet.

Will I have to pay brokerage or stamp duty?

No, you will not have to pay brokerage or stamp duty if your Mantra Shares are acquired under the Scheme.

Section 6 of this Scheme Booklet.

SCHEME, VOTING AND APPROVALS

Are there any conditions that must be satisfied or waived in order for the Scheme to be implemented?

There are a number of conditions that must either be satisfied or waived (where capable of waiver) in order for the Scheme to be implemented. In summary, as at the date of this Scheme Booklet, the outstanding conditions include:

• approval by Mantra Shareholders of the Scheme at the Scheme Meeting;

• Court approval of the Scheme and a copy of the Court approval is lodged with ASIC;

• no prohibitive orders that have the effect of preventing or materially restricting the Scheme are in effect as at the Second Court Date;

• all necessary and outstanding regulatory consents are obtained or deemed obtained on terms that AAPC considers acceptable before 8:00 am on the Second Court Date;

• no Mantra Prescribed Event having occurred;

• there has been no Mantra Material Adverse Change;

• each of the Mantra Warranties are true and correct;

• each of the AAPC Warranties are true and correct; and

• the Independent Expert does not change or publicly withdraw their opinion that the Scheme is in the best interests of Mantra Shareholders.

In addition, the existing regulatory consents obtained or deemed obtained under the Scheme Implementation Agreement (including in respect of FIRB and ACCC) must not have been withdrawn, cancelled or revoked before 8.00am on the Second Court Date. The NZCC regulatory consent which formed part of the conditions under the Scheme Implementation Agreement was formally waived on 10 November 2017.

The conditions of the Scheme are summarised in further detail in Section 1 of this Scheme Booklet.

Section 1 of this Scheme Booklet.

SCHEME BOOKLET MANTRA GROUP 13

FREQUENTLY ASKED QUESTIONS

Question Answer More information

Are there any conditions that must be satisfied or waived in order for the Scheme to be implemented?continued

Mantra Shareholders should also be aware that the Scheme Implementation Agreement may be terminated in certain circumstances (details of which are summarised in Section 1 of this Scheme Booklet). If the Scheme Implementation Agreement is terminated, the Scheme will not proceed.

As at the date of this Scheme Booklet, the Mantra Directors are not aware of any reason why these conditions should not be satisfied or waived.

Mantra Group intends to announce on ASX the satisfaction (or waiver) of the conditions to the Scheme.

Section 1 of this Scheme Booklet.

What happens if these conditions are not satisfied or the Scheme Implementation Deed is terminated?

If the Scheme conditions are not satisfied or waived or the Scheme Implementation Agreement is terminated then the Scheme will not be implemented and, as set out in Section 1 of this Scheme Booklet:

• you will retain your Mantra Shares and they will not be acquired by AAPC;

• you will not receive the Scheme Consideration or the Special Dividend; and

• Mantra Group will continue to operate as a stand-alone company listed on ASX.

Depending on the reasons for the Scheme not proceeding, Mantra Group may be liable to pay the Reimbursement Fee to AAPC, or AAPC may be required to pay the Reimbursement Fee to Mantra Group. No Reimbursement Fee is payable merely because Mantra Group Shareholders do not approve the Scheme.

Section 1 of this Scheme Booklet.

What happens if the Scheme is approved, all conditions are satisfied and it is implemented?

If the Scheme becomes Effective and you remain a Mantra Shareholder as at the Scheme Record Date for the Scheme, all of your Mantra Shares will be transferred to AAPC under the Scheme, and you will receive the Total Cash Consideration of $3.96 cash for each Mantra Share you hold both the Special Dividend Record Date and the Scheme Record Date, comprising:

• a fully franked special dividend of $0.16 per Mantra Share payable by Mantra on the Special Dividend Payment Date; and

• the Scheme Consideration of $3.80 per Mantra Share payable by AAPC on the Scheme Record Date.

Section 1 of this Scheme Booklet.

Am I entitled to vote at the Scheme Meeting?

If you are registered as a Mantra Shareholder on the Register at 7.00pm (Sydney time) on 16 May 2018, then you will be entitled to attend and vote at the Scheme Meeting.

Details of the Scheme Meeting and voting are on pages 8–9 and 17–19.

How do I vote? Voting at the Scheme Meeting may be in person, by attorney, by proxy or, in the case of a corporation, by corporate representative.

Details of the Scheme Meeting and voting are on pages 8–9 and 17–19.

When and where will the Scheme Meeting be held?

The Scheme Meeting will be held at 10.00am (Sydney time) on 18 May 2018 at Tower One – International Towers Sydney, Level 46, 100 Barangaroo Avenue, Sydney NSW 2000.

Details of the Scheme Meeting and voting are on pages 8–9 and 17–19.

Is voting compulsory?

Voting is not compulsory. However, the Scheme will only be successful if it is approved by the required majorities of Mantra Shareholders and therefore voting is important and Mantra Directors encourage you to vote. If the Scheme is approved, you will be bound by the Scheme whether or not you voted and whether or not you voted in favour of it.

Details of the Scheme Meeting and voting are on pages 8–9 and 17–19.

14 MANTRA GROUP SCHEME BOOKLET

Question Answer More information

What vote is required to approve the Scheme?

For the Scheme to proceed, the Scheme Resolution must be passed by:

• a majority in number (more than 50%) of Mantra Shareholders present in person or by proxy and voting (whether in person or by proxy) on the Scheme Resolution; and

• at least 75% of the votes cast on the Scheme Resolution.

Details of the Scheme Meeting and voting are on pages 8–9 and 17–19.

What happens if I do not vote or if I vote against the Scheme?

If you do not vote, or vote against the Scheme, the Scheme may not be approved at the Scheme Meeting by the required majorities of Mantra Shareholders. If this occurs then the Scheme will not proceed, you will not receive the Total Cash Consideration and you will remain a Mantra Shareholder.

However, if the Scheme is approved by the required majorities and the Scheme is implemented, you will receive the Scheme Consideration for each Mantra Share you hold on the Scheme Record Date whether or not you voted in favour of the Scheme and your Mantra Shares will be transferred to AAPC under the Scheme.

Details of the Scheme Meeting and voting are on pages 8–9 and 17–19.

Can I keep my shares in Mantra Group?

If the Scheme is implemented, your Mantra Shares will be transferred to AAPC. This is so even if you did not vote at all or you voted against the Scheme Resolution at the Scheme Meeting.

Section 1 of this Scheme Booklet

When will the results of the Scheme Meeting be available?

The results of the Scheme Meeting will be available shortly after the conclusion of the Scheme Meeting and will be announced to the ASX. Even if the Scheme Resolution is passed at the Scheme Meeting, the Scheme will only proceed if Court approval of the Scheme is obtained and all of the other conditions precedent are satisfied or waived.

Details of the Scheme Meeting and voting are on pages 8–9 and 17–19.

What do I do if I oppose the Scheme?

If you, as a Mantra Shareholder, oppose the Scheme, you should:

• attend the Scheme Meeting either in person or by proxy and vote against the Scheme Resolution; and/or

• if Mantra Shareholders pass the Scheme Resolution at the Scheme Meeting and you wish to appear and be heard at the Second Court Hearing and if so advised, oppose the approval of the Scheme at the Second Court Hearing, you must lodge a notice of intention to appear at the Second Court Hearing, attend the hearing and indicate opposition to the Scheme.

Details of the Scheme Meeting and voting are on pages 8–9 and 17–19.

Can I sell my Mantra Shares now?

You can sell your Mantra Shares on market at any time before close of trading on ASX on the Effective Date at the then prevailing market price (which may vary from the Scheme Consideration).

Mantra Group intends to apply to ASX for Mantra Shares to be suspended from official quotation on ASX from close of trading on the Effective Date (which is currently expected to be 23 May 2018). You will not be able to sell your Mantra Shares on market after this time. If you sell your Shares before the Special Dividend Record Date, being 7.00pm (Sydney Time) 25 May 2018, then you will not receive the Special Dividend and the additional value of franking credits related to the Special Dividend of up to an additional $0.07 value per Mantra Share that may be available depending on your individual tax circumstances.

N/A

FURTHER INFORMATION

What if I want further information?

If you have any questions about the Scheme or you would like additional copies of this Scheme Booklet, please contact the Shareholder Information Line on 1300 795 998 (within Australia) or +61 1300 795 998 (outside Australia) Monday to Friday between 8.30am and 5.30pm (Sydney time).

For information about your individual financial or taxation circumstances please consult your financial, legal, taxation or other professional adviser.

Section 7 of this Scheme Booklet.

SCHEME BOOKLET MANTRA GROUP 15

SECTION 1SUMMARY OF THE SCHEME

16 MANTRA GROUP SCHEME BOOKLET

1.1 BACKGROUND

On 12 October 2017, Mantra Group announced a proposal for AAPC to acquire 100% of the shares in Mantra Group by way of a scheme of arrangement. The announcement was made immediately after Mantra Group and AAPC signed the Scheme Implementation Agreement containing the key terms and conditions of the proposed transaction.

If the Scheme is approved and implemented, all Mantra Shares will be transferred to AAPC, and Mantra Group will become a wholly-owned subsidiary of AAPC. Following implementation of the Scheme, Mantra Group will apply to be de-listed from ASX.

This Scheme Booklet contains important information that you should consider before voting on the Scheme. The Mantra Directors encourage you to read this Scheme Booklet in its entirety and recommend that you vote in favour of the Scheme, in the absence of a Superior Proposal. A copy of the Scheme is set out in full in Annexure C.

1.2 OVERVIEW OF SCHEME IMPLEMENTATION STEPS AND PAYMENT OF SPECIAL DIVIDEND

The key steps to implement the Scheme are:

1. Mantra Shareholders will have an opportunity to vote to approve the Scheme at the Scheme Meeting.

2. If Mantra Shareholders approve the Scheme, and all conditions to the Scheme (other than Court approval) have been satisfied or waived, Mantra Group will apply to the Court for approval of the Scheme.

3. If the Court approves the Scheme, Mantra Group will lodge with ASIC a copy of the court orders approving the Scheme. The date on which this occurs will be the Effective Date for the Scheme and will be the last day for trading of Mantra Shares on ASX.

4. Subject to the Scheme becoming effective, the Special Dividend will be paid to Mantra Shareholders who hold Mantra Shares on the Special Dividend Record Date.

5. On the Implementation Date, AAPC will acquire all of the Mantra Shares and will provide the Scheme Consideration.

6. After the Scheme becomes Effective, Mantra Group will apply for suspension of trading in Mantra Shares, followed by removal of Mantra Group from the official list of ASX.

1.3 SCHEME CONSIDERATION

If the Scheme is approved and implemented, Mantra Shareholders will receive Total Cash Consideration of $3.96 per Mantra Share, comprising:

• a fully franked Special Dividend of $0.16 in cash per Mantra Share held by a Mantra Shareholder on the Special Dividend Record Date, payable by Mantra; and

• Scheme Consideration of $3.80 in cash per Mantra Share held by a Mantra Shareholder on the Scheme Record Date, payable by AAPC.

Those Mantra Shareholders who are able to realise the full benefit of franking credits will receive up to an additional $0.07 value per Mantra Share. Whether a Mantra Shareholder will be able to realise the full benefit of the franking credits will depend on their individual tax circumstances.

1.4 SCHEME MEETING

On 4 April 2018, the Court ordered that Mantra Group convene the Scheme Meeting in accordance with the Notice of Scheme Meeting and appointed Peter Bush to chair the meeting, with David Gibson as his alternate. The Court order does not constitute an endorsement of, or any other expression of opinion on, the Scheme or this Scheme Booklet.

The purpose of the Scheme Meeting is for Mantra Shareholders to consider whether to approve the Scheme. Mantra Shareholders who are registered on the Register at 7.00pm (Sydney time) on the Voting Record Date are entitled to vote at the Scheme Meeting.

Voting at the Scheme Meeting will be by poll. Instructions on how to attend and vote at the Scheme Meeting (in person or by proxy) are set out on pages 8–9 and in the Notice of Scheme Meeting in Annexure B.

1.5 APPROVALS REQUIRED FROM MANTRA SHAREHOLDERS AND THE COURT

The Scheme will only become Effective if it is approved by:

• the required majorities of Mantra Shareholders at the Scheme Meeting; and

• the Court on the Second Court Date.

SCHEME BOOKLET MANTRA GROUP 17

SECTION 1SUMMARY OF THE SCHEME

The Scheme will be approved if Mantra Shareholders vote in favour of the Scheme Resolution by:

• a majority in number (more than 50%) of Mantra Shareholders present in person or by proxy and voting at the Scheme Meeting (whether in person or by proxy); and

• at least 75% of the total number of votes cast on the Scheme Resolution at the Scheme Meeting by Mantra Shareholders.

The Court has the power to waive the first requirement.

The Corporations Act and the relevant Court rules provide a procedure for Mantra Shareholders to oppose the approval of the Scheme by the Court. If you wish to oppose the approval of the Scheme at the Second Court Hearing you may do so by appearing at the Second Court Hearing and applying to raise any objections you may have at the hearing. You should notify Mantra Group in advance of an intention to object. The date for the Second Court Hearing is currently scheduled to be Wednesday, 23 May 2018. Any change to this date will be announced through the ASX on Mantra Group’s website.

1.6 RECOMMENDATION OF MANTRA DIRECTORS

The Mantra Directors consider that, in the absence of a Superior Proposal, the Scheme is in your best interests as a Mantra Shareholder and unanimously recommend that you vote in favour of the Scheme for the reasons set out in Section 2 of this Scheme Booklet. The Mantra Directors consider that the reasons for Mantra Shareholders to vote in favour of the Scheme outweigh the reasons to vote against the Scheme. As at the date of this Scheme Booklet, no Superior Proposal for Mantra Group has been received.

Each Mantra Director intends to vote in favour of the Scheme in respect of all Mantra Shares controlled or held by, or on behalf of, each of them (including any proxies placed at their discretion) in the absence of a Superior Proposal and subject to the Independent Expert continuing to consider the Scheme to be in the best interests of Mantra Shareholders.

In making their recommendation and determining how to vote on the Scheme, the Mantra Directors have considered the following:

• the reasons for Mantra Shareholders to vote in favour of the Scheme, as set out in Section 2.1;

• the reasons for Mantra Shareholders not to vote in favour the Scheme as set out in Section 2.2;

• the risks associated with the Scheme, as set out in Section 5; and

• the Independent Expert’s Report, which has concluded that the Scheme is fair and reasonable and, therefore, in the best interests of Mantra Shareholders, in the absence of a Superior Proposal, as set out in Annexure A.

Before making your decision in relation to the Scheme, the Mantra Directors encourage you to read this Scheme Booklet in its entirety, having regard to your investment objectives, financial situation, tax position or particular needs. If you have any questions in relation to this Scheme Booklet or the Scheme, you should call the Shareholder Information Line on 1300 795 998 (within Australia) or +61 1300 795 998 (outside Australia) Monday to Friday between 8.30am and 5.30pm (Sydney Time). Alternatively, you should contact your legal, financial or other professional adviser.

The interests of Mantra Directors are disclosed in Section 7.

1.7 INDEPENDENT EXPERT

The Mantra Directors have engaged Grant Thornton as Independent Expert to consider whether the Scheme is in the best interests of Mantra Shareholders and prepare a report with its findings and conclusions.

The Independent Expert has concluded that the Scheme is fair and reasonable, and therefore in the best interests of Mantra Shareholders, in the absence of a Superior Proposal.

The Independent Expert summarised its views on the likely advantages and disadvantages of the Scheme for Mantra Shareholders as follows:

Advantages

• The Total Cash Consideration represents a premium for control of Mantra Group which is unlikely to be available to Mantra Shareholders in the absence of the Scheme or an alternative proposal.

• In the absence of the Scheme or an alternative proposal, all other things being equal, it is likely that Mantra Shares will trade at prices below the Total Cash Consideration.

• Mantra Shareholders will avoid ongoing risks associated with the operations of Mantra Group and receive certain cash for their investment in Mantra Group.

18 MANTRA GROUP SCHEME BOOKLET

• Franking credits are attached to the Special Dividend which could result in additional after tax value for certain categories of Mantra Shareholders.

• Mantra Shareholders will be able to realise their investment in Mantra Group without incurring any brokerage costs.

Disadvantages

• Mantra Shareholders will forgo the opportunity to participate in the potential future upside of Mantra Group.

• There is the potential of a superior offer (although no superior proposal has emerged to date).

• Implementation of the Scheme may crystallise a capital gains tax liability for Mantra Shareholders.

A copy of the Independent Expert’s Report (which sets out further details about the Independent Expert’s conclusions) is set out in Annexure A. Mantra Shareholders are encouraged to read this report in its entirety.

1.8 HOW TO VOTE

If you are registered as a Mantra Shareholder on the Register at 7.00pm (Sydney time) on the Voting Record Date of 16 May 2018, you are entitled to vote at the Scheme Meeting. Mantra Shareholders can vote by:

• attending the Scheme Meeting and voting in person, by attorney or by corporate representative if you are a corporate shareholder; or

• by appointing a proxy to attend and vote on your behalf.

See pages 8–9 of this Scheme Booklet for a summary on how to vote. For detailed information on voting procedure, see the Notice of Scheme Meeting set out in Annexure B.

1.9 WHAT HAPPENS IF THE SCHEME PROCEEDS?

If the Scheme is approved by Mantra Shareholders and by the Court at the Second Court Hearing, all Mantra Shareholders who hold Mantra Shares as at the Scheme Record Date, being Scheme Shareholders, will participate in the Scheme, regardless of their voting decision.

Once the Court approves the Scheme, Mantra Group will lodge with ASIC a copy of the Court orders approving the Scheme. On the date that this lodgement occurs (Effective Date), the Scheme will become Effective.

After the Scheme becomes Effective, a Scheme Shareholder must not dispose of or purport or agree to dispose of, any Scheme Shares or any interest in them after the Scheme Record Date. Mantra Group will disregard any such disposal and any attempt to do so will have no effect.

Mantra Group will notify ASX and apply for Mantra Shares to be suspended from trading from close of trading on the Effective Date. Following the Implementation Date, Mantra Group will apply for termination of the official quotation of Mantra Shares and removal from the official list of ASX.

If approved and implemented, the Scheme will result in:

• each Scheme Shareholder receiving the Total Cash Consideration;

• the transfer of all Mantra Shares to AAPC; and

• Mantra Group being delisted from ASX and becoming a wholly-owned subsidiary of AAPC.

1.10 DETERMINATION OF ENTITLEMENT TO SCHEME CONSIDERATION

For the purposes of establishing who are Scheme Shareholders, dealings in Mantra Shares will only be recognised if:

1. in the case of dealings of the type to be effected by CHESS, the transferee is registered in the Register as the holder of the relevant Mantra Shares on or before the Scheme Record Date; and

2. in all other cases, registrable transmission applications or transfers in respect of those dealings are received on or before the Scheme Record Date at the Mantra Share Registry.

Subject to the Corporations Act, ASX Listing Rules and Mantra Group’s constitution, Mantra Group must register transmission applications or transfers which it receives by the Scheme Record Date. Mantra Group will not accept for registration or recognise for any purpose any transmission application or transfer in respect of Mantra Shares received after the Scheme Record Date.

SCHEME BOOKLET MANTRA GROUP 19

SECTION 1SUMMARY OF THE SCHEME

Mantra Group will, until the Scheme Consideration has been provided and AAPC has been entered in the Register as the holder of all Scheme Shares, maintain the Register on this basis and the Register in this form will solely determine entitlements to the Scheme Consideration.

With effect from the Scheme Record Date:

• all statements of holding in respect of Mantra Shares cease to have effect as documents of title in respect of such Mantra Shares; and

• each entry on the Register will cease to be of any effect other than as evidence of entitlement to Scheme Consideration.

1.11 PAYMENT OF TOTAL CASH CONSIDERATION

If the Scheme becomes Effective, AAPC will acquire all of the Mantra Shares. Mantra Shareholders will receive Total Cash Consideration of $3.96 per Mantra Share, comprising:

• a fully franked Special Dividend of $0.16 in cash per Mantra Share held by a Mantra Shareholder on the Special Dividend Record Date, payable by Mantra Group; and

• Scheme Consideration of $3.80 in cash per Mantra Share held by a Mantra Shareholder on the Scheme Record Date, payable by AAPC.

Payment of the Special Dividend will be made on the Special Dividend Payment Date, currently expected to be 30 May 2018. Payment of the Scheme Consideration will be made on the Implementation Date, currently expected to be 31 May 2018.

For the purposes of paying the Scheme Consideration, AAPC will deposit in cleared funds, by no later than the Business Day before the Implementation Date, an amount equal to the total Scheme Consideration into a trust account operated by Mantra Group to be held on trust for the Scheme Shareholders.

The Special Dividend and the Scheme Consideration will be paid in Australian currency by:

• making a deposit into the nominated Australian bank account of the relevant Mantra Shareholder recorded on the Register as at the Special Dividend Record Date (in the case of the Special Dividend) and the Scheme Record Date (in the case of the Scheme Consideration). If you have not previously notified the Mantra Share Registry of your nominated bank account or would like to change your existing nominated bank account, you should contact the Mantra Share Registry on 1300 554 474 (within Australia) or +61 1300 554 474 (outside Australia) prior to the Special Dividend Record Date; or

• if you have not notified the Mantra Share Registry of your nominated bank account, payment will be made by cheque drawn in your name posted to your address registered with the Mantra Share Registry as at the Scheme Record Date.

If the whereabouts of a Mantra Shareholder are unknown as at the Special Dividend Record Date or Scheme Record Date (as applicable), payments due to Mantra Shareholders will be paid into a separate bank account and held until claimed or applied under laws dealing with unclaimed moneys.

Mantra Group’s current dividend reinvestment plan will be suspended in order for the Special Dividend to be paid entirely in cash. You should carefully read Section 6 of this Scheme Booklet which contains details regarding the taxation treatment of the Special Dividend.

1.12 DEEMED WARRANTIES BY SCHEME SHAREHOLDERS

Under the terms of the Scheme, each Scheme Shareholder is deemed to have warranted to Mantra Group and AAPC that:

• as at the Implementation Date, all of their Scheme Shares (including all rights and entitlements attached to them) transferred to AAPC under the Scheme will, on the date of transfer, be fully paid and free from all mortgages, charges, liens, encumbrances, pledges, security interests and other interests of third parties of any kind (whether legal or otherwise) and restrictions on transfer of any kind; and

• they have full power and capacity to sell and transfer their Scheme Shares (including all rights and entitlements attached to them) to AAPC.

Scheme Shareholders should be aware that, to the extent that this warranty is untrue and their Scheme Shares are not transferred under the Scheme free of third party interests, they may be liable to compensate AAPC for any damage caused to AAPC resulting from such an encumbrance.

20 MANTRA GROUP SCHEME BOOKLET

1.13 WHAT HAPPENS IF THE SCHEME DOES NOT PROCEED?

If the Scheme is not approved at the Scheme Meeting or all of the conditions to the Scheme are not satisfied or waived, the Scheme will not proceed, and:

• Mantra Group will continue to operate as an independent entity listed on ASX;

• Mantra Shareholders will continue to hold their Mantra Shares and share in any benefits and risks of Mantra Group’s ongoing business; and

• Mantra Shareholders will not receive the Total Cash Consideration.

Depending on the reasons why the Scheme does not proceed, Mantra Group may be liable to pay a Reimbursement Fee to AAPC, or AAPC may be liable to pay a Reimbursement Fee to Mantra Group. See Section 1.14(c) for further information on the Reimbursement Fee.

If the Scheme is not implemented, and in absence of a Superior Proposal, Mantra Shares will likely trade below the price at which they have traded since announcement of the Scheme Implementation Agreement on 12 October 2017.

1.14 SCHEME IMPLEMENTATION AGREEMENT

Mantra Group and AAPC have entered into a Scheme Implementation Agreement as announced on 12 October 2017. A copy of the full Scheme Implementation Agreement is available on the ASX website and on Mantra Group’s website.

The Scheme Implementation Agreement sets out the rights and obligations of Mantra Group and AAPC in connection with the Scheme. The key terms of the Scheme Implementation Agreement are summarised below.

a. Conditions Precedent

The Scheme is subject to a number of conditions, some of which have already been satisfied. The conditions which have not yet been satisfied include:

• (Mantra Shareholder approval) the Scheme is approved by Mantra Shareholders at the Scheme Meeting;

• (Court approval) the Court approves the Scheme in accordance with section 411(4)(b) of the Corporations Act;

• (Order lodged with ASIC) a copy of the Court order approving the Scheme is lodged with ASIC as contemplated by section 411(1) of the Corporations Act;

• (No prohibitive orders) no law, statute, ordinance, regulation, rule, temporary restraining order, preliminary or permanent injunction or other judgment, order or decree issued by any Court of competent jurisdiction or Governmental Agency or other legal restraint or prohibition preventing or materially restricting the Scheme is in effect at 8.00am on the Second Court Date;

• (Regulatory Approvals) before 8.00am on the Second Court Date, all regulatory approvals or consents required from any Government Agency to implement the Scheme are obtained (or deemed obtained) on terms which AAPC (acting reasonably) considers acceptable;

• (No Mantra Group Prescribed Event) no Mantra Prescribed Event occurs between (and including) the date of the Scheme Implementation Agreement and 8.00am on the Second Court Date;

• (No Mantra Material Adverse Change) no Mantra Material Adverse Change occurs or otherwise becomes known to AAPC between (and including) the date of the Scheme Implementation Agreement and 8.00am on the Second Court Date;

• (Mantra Warranties) each of the Mantra Warranties being true and correct in all material respects on until 8.00am on the Second Court Date;

• (AAPC Warranties) each of the AAPC Warranties being true and correct in all material respects until 8.00am on the Second Court Date; and

• (Independent Expert’s Report) the Independent Expert does not change or publicly withdraw their opinion that the Scheme is in the best interests of Mantra Shareholders before 8.00am on the Second Court Date.

In addition, the Scheme is conditional on existing regulatory consents obtained or deemed obtained under the Scheme Implementation Agreement not having been withdrawn, cancelled or revoked before 8:00am on the Second Court Date.

If the conditions are not satisfied or waived then the Scheme will not proceed.

SCHEME BOOKLET MANTRA GROUP 21

SECTION 1SUMMARY OF THE SCHEME

As at the date of this Scheme Booklet, each of ACCC and FIRB have provided (and have not withdrawn) their respective approvals for the purposes of the regulatory condition in the Scheme Implementation Agreement. The NZCC approval condition was waived on 10 November 2017.

See the Scheme Implementation Agreement and the Glossary for the meanings of the defined terms in this Section 1.14.

b. Exclusivity Provisions

Mantra Group has agreed to the following exclusivity provisions in the Scheme Implementation Agreement:

• No-shop: Mantra Group must not solicit, invite, encourage or initiate any inquiry, expression of interest, offer, proposal or discussion by any person in relation to, or which would reasonably be expected to encourage or lead to the making of, an actual, proposed or potential Competing Proposal or communicate to any person an intention to do any of these things;

• No-talk: Mantra Group must not:

– participate in or continue any negotiations or discussions with any third party in relation to, or which would reasonably be expected to lead to the making of, an actual, proposed or potential Competing Proposal;

– negotiate, accept or enter into, or offer or agree to negotiate, accept or enter into, any agreement, arrangement or understanding regarding an actual, proposed or potential Competing Proposal;

– disclose or otherwise provide any material non-public information about the business or affairs of Mantra Group to a third party with a view to obtaining, or which would reasonably be expected to encourage or lead to receipt of, an actual, proposed or potential Competing Proposal (including, without limitation, providing such information for the purposes of the conduct of due diligence investigations in respect of Mantra Group); or

– communicate to any person an intention to do anything referred to above.

However, this no-talk restriction does not prohibit or require any action or inaction by Mantra Group or any of its Representatives in relation to an actual, proposed or potential Competing Proposal to the extent that compliance with the no-talk restriction would, in the opinion of the Mantra Board, formed in good faith after receiving written advice from its external legal advisers, constitute, or would be likely to constitute, a breach of any of the fiduciary or statutory duties of the Mantra Directors, provided that the actual, proposed or potential Competing Proposal was not directly or indirectly brought about by, or facilitated by, a breach of the no-talk restriction (Fiduciary Exception).