scan inter public company limited - dcs-digital.com · system installation of ngv ... pipeline...

TRANSCRIPT

Scan Inter Public Company Limited

opportunity day

16 March 2015

1

2

Contents

I

II

Business Overview

Financial

I. Business Overview

3

4

Major Developments

Strong relationship with Thailand’s

major gas supplier and distributor

and global partners 2003-2009

Expansion into fully integrated of

gas-related business

2010-2014

Early establishment in Thailand

energy market

1988-2002

Introductory to the Market

Being Recognized in Thailand as Gas-Related

Industry with Global Partners

Become One of the Leaders in the Country

Gas-Related Business

“One of the leaders in Thai energy business with over 27 years of experience in gas-related business"our vision is to become the leader in energy technology in Asia Pacific

Initiate iCNG into Thai market

2015-PresentBecome the first trader & leader in iCNG

business

5

Natural Gas Pipeline

6

Natural Gas-Related Business Overview

Distribution Pipeline

Private Mother Station (PMS) Daughter Stations

Conventional Station

Car, Bus and Truck

Design, Construction,

Installation and Maintenance

NGV Station and Related Gas

System

Installation of NGV

and LPG Conversion

System in Vehicles

Other NGV Stations

NGV Station

Natural Gas

Transportation (TPL)

3

2

4

1

5

7

Design, Construction, Installation and Maintenance

NGV Station and Related Gas System

8

Natural Gas-Related Business Overview

Distribution Pipeline

Private Mother Station (PMS) Daughter Stations

Conventional Station

Car, Bus and Truck

Design, Construction,

Installation and Maintenance

NGV Station and Related Gas

System

Installation of NGV

and LPG Conversion

System in Vehicles

Other NGV Stations

NGV Station

Natural Gas

Transportation (TPL)

3

2

4

1

5

9

Private Mother Station (PMS)

10

Natural Gas-Related Business Overview

Distribution Pipeline

Private Mother Station (PMS) Daughter Stations

Conventional Station

Car, Bus and Truck

Design, Construction,

Installation and Maintenance

NGV Station and Related Gas

System

Installation of NGV

and LPG Conversion

System in Vehicles

Other NGV Stations

NGV Station

Natural Gas

Transportation (TPL)

3

2

4

1

5

11

Natural Gas Transportation (TPL)

12

Natural Gas-Related Business Overview

Distribution Pipeline

Private Mother Station (PMS) Daughter Stations

Conventional Station

Car, Bus and Truck

Design, Construction,

Installation and Maintenance

NGV Station and Related Gas

System

Installation of NGV

and LPG Conversion

System in Vehicles

Other NGV Stations

NGV Station

Natural Gas

Transportation (TPL)

3

2

4

1

5

13

Private Brand Station (PBS)

14

Natural Gas-Related Business Overview

Distribution Pipeline

Private Mother Station (PMS) Daughter Stations

Conventional Station

Car, Bus and Truck

Design, Construction,

Installation and Maintenance

NGV Station and Related Gas

System

Installation of NGV

and LPG Conversion

System in Vehicles

Other NGV Stations

NGV Station

Natural Gas

Transportation (TPL)

3

2

4

1

5

15

Installation of NGV and LPG Conversion

System in Vehicles

16

Future Growth NGV

Current NGV price is 13.00 Baht

PRICE

TON/DAY

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2546 2547 2548 2549 2550 2551 2552 2553 2554 2555 2556 2557

7 7.5 8.5 8.5 8.5 8.5 8.5 8.5 8.5 10.5 10.5 12

16 28 43 102 166 303 391 428 469 483 490 49738 85 153 260

652

2057

3740

5055

6415

77338542 8809

NGV Growth

PRICE STATION TON/DAY

17

Natural Gas-Related Business Overview

Distribution Pipeline

Private Mother Station (PMS) Daughter Stations

Conventional Station

Car, Bus and Truck

Design, Construction,

Installation and Maintenance

NGV Station and Related Gas

System

Installation of NGV

and LPG Conversion

System in Vehicles

Other NGV Stations

NGV Station

Natural Gas

Transportation (TPL)

Compressor Station for Project CNG for Industry

Factory

Natural gas

transportation

Future Project

3

2

4

1

5

6

18

Pressure Reducing System (PRS)

5

19

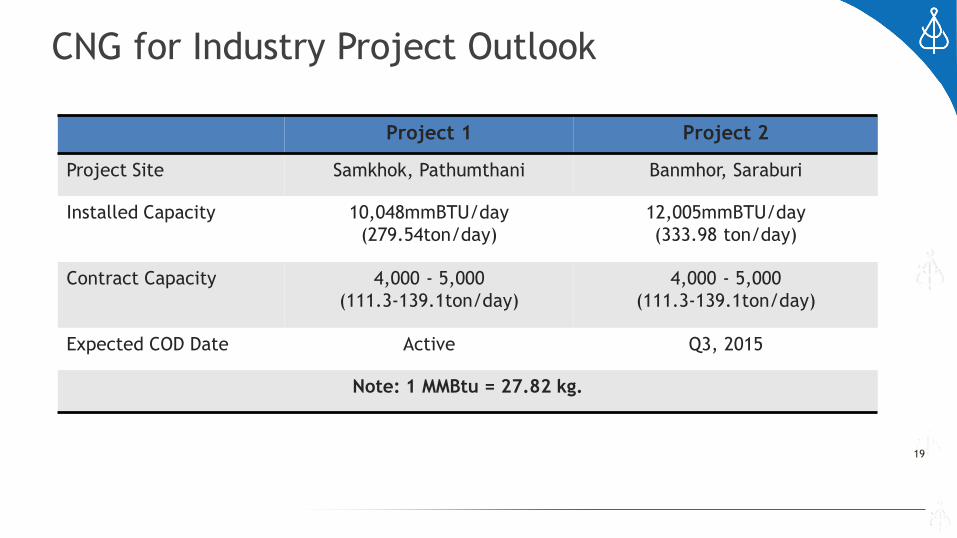

CNG for Industry Project Outlook

5

Project 1 Project 2

Project Site Samkhok, Pathumthani Banmhor, Saraburi

Installed Capacity 10,048mmBTU/day

(279.54ton/day)

12,005mmBTU/day

(333.98 ton/day)

Contract Capacity 4,000 - 5,000

(111.3-139.1ton/day)

4,000 - 5,000

(111.3-139.1ton/day)

Expected COD Date Active Q3, 2015

Note: 1 MMBtu = 27.82 kg.

20

iCNG VS Fuel Oil Price VS LPG Price

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

2012 2013 2014

iCNG Factor

FO

LPG

• iCNG is the price formula which is directly

related to Singapore Fuel Oil price and

exchange rate of US/THB and inversely

related to the consumption of each customer

• FO is the average fuel oil price in Thailand

SCN has researched

• LPG is the average LPG for industry price in

Thailand SCN has researched

• The graph shows that iCNG is the lowest cost of all three fuels

21

iCNG Entry Barrier

5

Pipeline Compressor Logistic PRS Factory

iCNG Mother Station

Need to be familiar with CNG equipment CNG compressor & high pressure equipment.

SCN strength • Low capacity investment

due to in house production of CNG Compressor and all relate equipment

• 27 years experiences with petro station

• The first company to be involve with NGV (CNG) since it’s first introductory in Thailand

Logistic

Need to be experience with hazardous product & petroleum fuel transportation.

SCN strength • Low capital investment due

to in house production of CNG trailer

• Highly experience by being one of the first company providing CNG logistic for PTT

Decompress

Need to find a method to reduce the pressure of CNG from 3600psi to the pipeline pressure(200psi) at a continuous rate.

SCN strength • The only patent holder for

the pressure reducing system(PRS), the essential component of the iCNGproject

Catalyze

Need to understand the construction and gas utilization rules and regulation.

SCN strength • Well experienced in NGV

and petro station construction(27 years experience )

II Financial

22

23

Strong Financial Performance with Distinguished Character

Continuous Revenue Growth with Sound Profitability

Revenue Growth Gross Profit Margin & Net Profit Margin

SCN’s revenue has increased continuously from THB1,542.5M in 2011 to THB2,112M or 17.01% of CAGR

It has been driven by growth in revenue of PMS, TPL, PBS, and newly established auto dealer business in the end of 2012

The Company’s 2014 profit margin shows impressively improvement:

– Gross profit margin increases from 15.9% in 2013 to 21.9% in 2014

– Net profit margin increases from 5.0% in 2013 to 10.8% in 2014

Improvement in 2014 gross profits are due to (1) Higher utilization rate from 73.5% into 87.8% of PMS (2) High margin on a high value project under construction & MA project

Profit margin has been adversely

effect by accountingreclassification and provision on

slow moving items in 2012 - 2013

1,542.5 1,592.3

2,119.7 2,112.0

-

500.0

1,000.0

1,500.0

2,000.0

2,500.0

Mil

lion T

HB

2011 2012 2013 2014 2011 2012 2013 2014

32.5%

21.9%

15.9%

21.9%

9.7%

5.9% 5.0%

10.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Gross Profit Margin Net Profit Margin

24

Strong Financial Performance with Distinguished Character

Continuing Revenue Growth with Sound Profitability (Cont’)

Note (1) The figure in 2014 excludes profit from disposing solar power plant(2) On September 26, 2015, SCN signed share purchase agreement to sell99.9% of SFEE’s shares to a listed company. Consequently, SCN will no longer receive revenue and profit from solar power plant

EBITDA Growth Net Profit Growth

Since 2012 EBITDA and net profit have risen substantially

SCN’s EBITDA has risen from THB303.7M to THB464.9M in 2013 or

23.7% of CAGR

Since 2012 SCN’s net profit, excluding profit from disposing solar power plant, has substantially increased from THB94.1mm to THB241.2mm in 2014 or 60.1% of CAGR

It has been driven by revenue growth from PMS and TPL in 2013 – 2014 and by revenue growth & higher margin in construction & MA business in 2014

410.5

303.7

351.5

464.9

0

50

100

150

200

250

300

350

400

450

500

2011 2012 2013 2014

TH

B M

M

149.0

94.1 104.9

241.2

0.0

50.0

100.0

150.0

200.0

250.0

300.0

2011 2012 2013 2014

TH

B M

25

Strong Financial Performance with Distinguished Character

Sizable Recurring Revenue with Potential Upside on Revenue from Construction & MA Projects

Recurring Revenue Recurring Revenue vs Construction & Maintenance Revenue

Stream of recurring revenue, which is generated from PMS, TPL, NGV Retail and R&M Contracts (Repair & Maintenance),

has strongly grown from 2011 – 2014

– Recurring revenue has risen from THB383.6M in 2011 to THB837.5M in 2014 or 30% of CAGR

– Compared 2013 to 2014, recurring revenue has also increased from THB637.6M to THB837.5M, or 31.36% of growth

The healthy growth results from significantly increase demand in PMS , TPL, R&M Contracts

Recurring revenue in a range of 24.9% - 39.7% of total revenue in 2011 – 2014

Beyond the recurring revenue, SCN’s performance is considerably enhanced by performance of construction & MA business

24.9% 33.5% 30.1% 39.7%

124.7 194.1 203.3 204.9 123.3

184.0 209.5 226.1 135.6

154.8 204.5 237.7

-

-

20.3

168.8

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

2011 2012 2013 2014

NGV Retail TPL PMS R&M Contract

383.6

532.9

637.6

837.5

567.3

464.3 388.01

641.79

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

2011 2012 2013 2014

Recurring R. Construction

26

Healthy Revenue Growth

Sizable Recurring Revenue with Potential Upside on Revenue from Construction & MA Projects

Between 2011 and 2014, SCN experienced healthy revenue growth with CAGR of 17.01% driven by an increase in revenue of PMS, TPL, PBS as well as auto

dealer business which commenced its operation in December 2012

Revenue from gas related business remained the biggest source of income contributing 56.4% and 71.5% of 2013 and 2014 total revenue respectively

Total Revenue Total Revenue Structure

1,542.5 1,592.3

2,119.7 2,112.0

-

500.0

1,000.0

1,500.0

2,000.0

2,500.0

Mil

lion T

HB

2011 2012 2013 2014

89.80% 87.10%

56.40%71.50%

6.10%

32.70%

22.70%

0.20% 2.70%1.60%9.30% 5.20% 7.10% 4.20%

0.90% 1.40% 1.10% 1.60%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014

Gas Related Business Auto Dealer Business Solar Power Plant

Other Business Other Revenue

27

Recovering of Gross Profit in Gas Related Business

A decline in GPM of gas related business between 2011 and 2013 resulted from

I. Accounting reclassification of depreciation expenses from administration expenses to COGS

II. Provision for slow moving inventory of THB33.13 mm in 2012 and THB24.26 mm in 2013

III. Provision for warranty of THB9.10 mm and THB2.13 mm in 2012 and 2013 respectively

IV. Rising of wage & salary according to government policy to promote minimum wage to be THB300/day

For 2014, SCN witnessed a significant improvement of GPM as the Company realized revenue from NGV cylinders installation work; a project with high

margin

Sale & Service Revenue – Gas-Related Business Gross Profit vs. GPM – Gas-Related Business

Profit margin has been adversely

effect by accounting

reclassification and provision on

slow moving items in 2012 - 2013

135.6 154.8 204.5 237.7123.3

184209.5 226.1124.7

194.1203.3 198.3

567.3464.3

408.3

810.6434.3 389.2

169.8

63.8

0

200

400

600

800

1000

1200

1400

1600

1800

2011 2012 2013 2014

TH

B M

PMS TPL

PBS Construction and Maintenanceof NGV Instruments

Installation of NGV and LPG Conversion System

1,386.4

1,195.4

1,536.51,385.2

471

311.4

216.3

377.5

34%

22.5%

18.10%

24.60%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

50

100

150

200

250

300

350

400

450

500

2011 2012 2013 2014

TH

B M

Gross Profit (LHS) GPM (RHS)

28

Most of Investment Already Incurred

The assets mainly consists of PPE, inventory and trade and other receivables

Since 2012, total assets continuously decreased. This was due mainly to a

decrease in inventory as the Company introduced Enterprise Resource

Planning (ERP) system for more efficient inventory management

On the other hand, PPE increased during 2011 to 2014 as a result of

business expansion. Particularly for 2014, SCN made an investment in

land, machinery and building for its CNG for Industry projects at Samkhok

and Banmhor

Asset Composition

CAPEX

1.0x

Liabilities Composition

2.4x 2.0x(IBD/E)

(THB M)1.4x

82.1 63.3 139.6 98.5

1215 1195.3 995.8672.2

1,093.70 1,036.90 1,148.40 1,489.70

247.1 368.7 368.7 419.10 197.5 190.8 194.5185.6

209.3 223.5 143.6

0

500

1000

1500

2000

2500

3000

3500

2011 2012 2013 2014

TH

B M

Cash InventoryPPE Trade and other receivablesFinance lease receivable Others

3,071 3,067 3,017.

62,823

332.3

206.2 231.8

434

0

50

100

150

200

250

300

350

400

450

500

2011 2012 2013 2014

TH

B M

756.71,215 958.9

538.2

528.7

478.5

483.2

326.5

506.6

341.1627.9

522.4

59.8 105.5

292.4

57.9

246.729.1

84.9

0

500

1000

1500

2000

2500

2011 2012 2013 2014

OD&ST Loan AP&Payable LT Loan Fin. Lease Others

29

Surging of Return & Sound Capital Structure

For 2014, the Company’s ROE&ROA increase to 21.6% and 7.5% respectively

D/E ratio and IBD/E ratio increased between 2011 and 2012 from an increase of long-term loan from financial institutions to support auto dealer business

and solar power plant

During 2011 to 2014, D/E ratio and IBD/E ratio continued to decrease due to repayment of overdraft, short-term loan and long-term loan from financial

institutions

D/E Ratio vs. IBD/E RatioROE & ROA

Note: (1) annualized figure, excluding profit from disposing solar power plant

17.7

11.213.1

21.6

6.1

3.2 3.4

7.5

0

5

10

15

20

25

2011 2012 2013 2014

%

ROE ROA

2.0

3.2

2.6

1.41.4

2.4

2.0

1.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2011 2012 2013 2014

Tim

es

D/E Ratio IBD/E