savoir être pour agir avec sens - 1 - presentation international commodities conference 2014...

TRANSCRIPT

Savoir être pour agir avec Sens - 1 -

Presentation International Commodities Conference 2014

Measuring the Effect of Oil Prices on Wheat Futures Prices*

Phillip A. Cartwright [1] Natalija Riabko Professor of Economics Market Analyst

ESG Management School Market Studies Department

25, rue Saint Ambroise FranceAgriMer 75011 Paris 12 rue Henri Roi-Tanguy

FRANCE 93555 Montreuil-sous-Bois cedex FRANCE

[1] Corresponding author: Professor Phillip A. Cartwright, ESG Management School, 25 rue Saint Ambroise, 75011, Paris, France.

Email: [email protected]. Natalija Riabko, DBA, is Market Analyst, France AgriMer.

* The authors wish to thank C.F Lee, Rutgers University; Octavio. Escobar, ESG Management School; Ted Bos, University of Alabama-Birmingham; and J. Roussel, Université Paris Dauphine for helpful comments and criticisms.

Savoir être pour agir avec Sens - 2 -

• Purpose – Research Questions• Background [Economic – Political]• Literature• Data and Modelling

– Regression– Random Coefficient– Time Series (GARCH)

• Empirical Results• Conclusions and Directions of Research

Savoir être pour agir avec Sens - 3 -

• Research Questions

– What is the empirical relationship between wheat futures prices and spot oil prices?

– What is the relevance of temporal and spatial aggregation for estimation and testing of the empirical relationship between wheat futures prices and spot oil prices?

Savoir être pour agir avec Sens - 4 -

• Background [Economic – Political]– Global importance of food and energy security for economic and political stability– Relative importance of the oil for food exchange– Developed countries – Developing countries

Savoir être pour agir avec Sens - 5 -

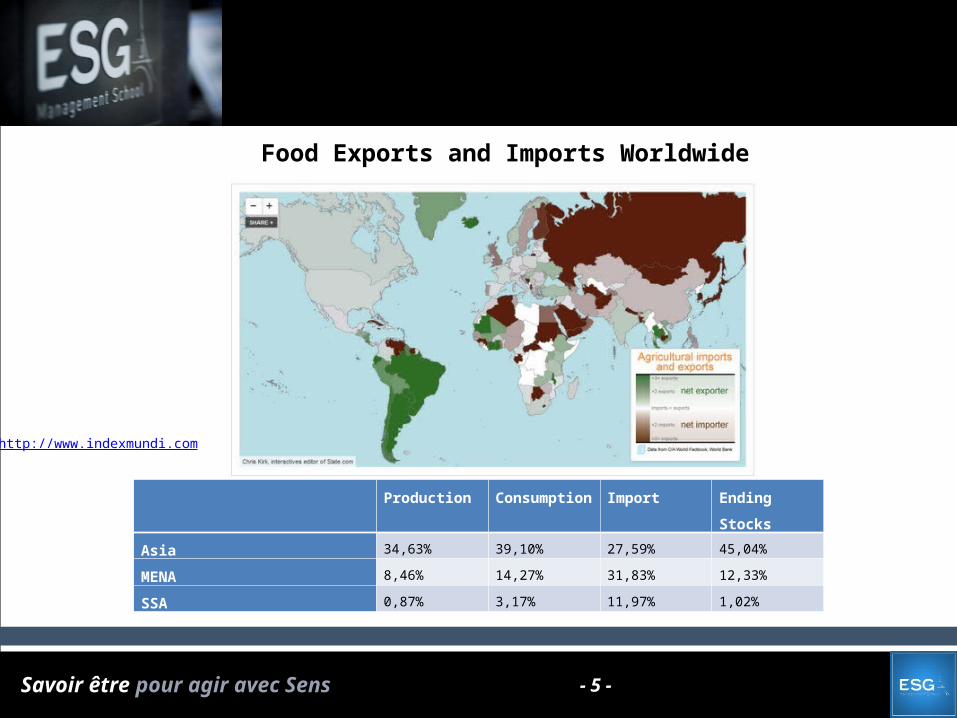

Food Exports and Imports Worldwide

http://www.indexmundi.com

Production Consumption Import Ending

Stocks

Asia 34,63% 39,10% 27,59% 45,04%

MENA 8,46% 14,27% 31,83% 12,33%

SSA 0,87% 3,17% 11,97% 1,02%

Savoir être pour agir avec Sens - 6 -

Crude Oil Exports and Imports Worldwide

http://www.indexmundi.com

• It is well known that the Middle East is pivotal for global oil production;

that it also imports a third of globally traded cereals, less so.

• Middle Eastern states consider food imports a strategic liability, similar to the West’s perception of its dependence on oil imports.

The World Financial Review, 2013 http://www.worldfinancialreview.com/?p=2773

Savoir être pour agir avec Sens - 7 -

• Literature– Relationship between energy and food commodity

prices• Baffles (2007), Muhammad and Kebede (2009) and Saghaian (2010, Roberts and

Schlenker (2013)

– Econometrics• Time Aggregation

– Zellner and Montmarquette, 1971; Engle, R.F. and Liu, T.C., 1972; Rowe, 1976; Cartwright and Lee, 1987; Marcellino, 1999; Silvestrini and Veredas, 2005

• Dynamics (Intertemporal Effects)– Merton (1976) and Black (1976) – Shiller (1987), Engel and West (2005), and Chen, Rogoff and Rossi (2008)

• Model Specification– Drost, F.C. and Nijman, T.E. (1993

Savoir être pour agir avec Sens - 8 -

• Data and Modelling– Data

• Data are collected on futures wheat contract price and spot prices for the United States and France. Data are collected on a daily basis beginning on 1 January 2006 through 31 December 2011.

• The empirical analysis is based on the daily, weekly and monthly FOB prices for U.S. Soft Red Winter (Gulf ports), and French Soft Wheat (Rouen) as well as on the corresponding products futures prices. All the rates series are quoted in nominal USD per ton.

• The US daily spot rates and U.S. daily futures rates were taken from the International Grain Council (IGC) data base which corresponds to Eurostat data. The French daily spot rates and French daily futures rates were taken from the International Grain Council (IGC) data base which also corresponds to Eurostat data.

• The ICE Brent Crude daily spot rates and daily futures rates were taken from the International Grain Council (IGC) data base which corresponds to International Exchange (ICE) data. The ICE Brent Crude Futures contract is a deliverable contract based on EFP delivery with an option to cash settle.

Savoir être pour agir avec Sens - 9 -

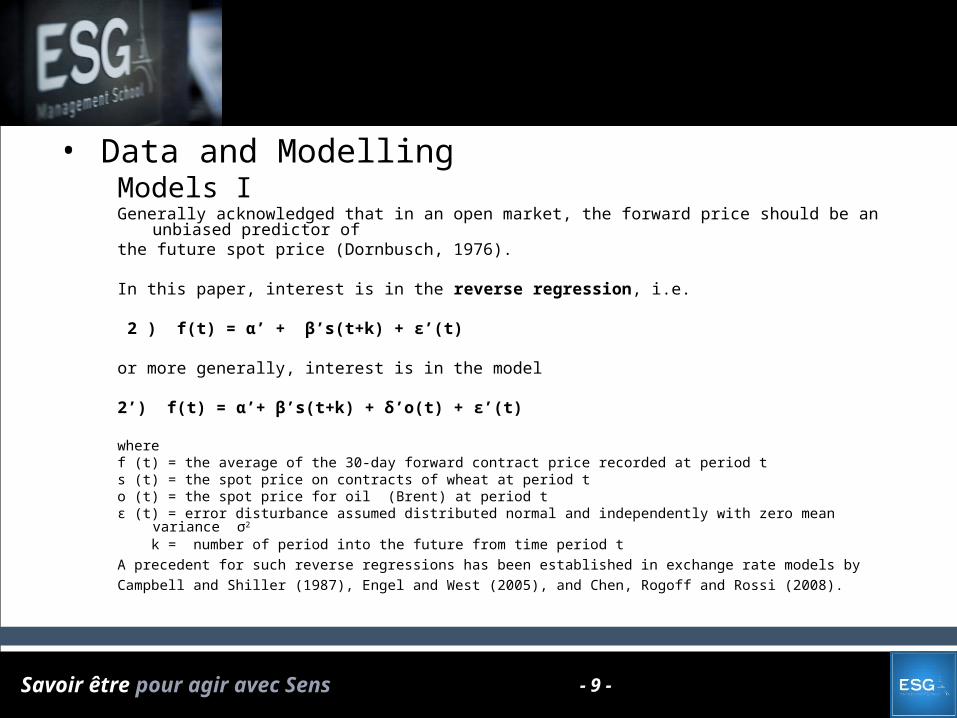

• Data and ModellingModels IGenerally acknowledged that in an open market, the forward price should be an unbiased predictor of the future spot price (Dornbusch, 1976).

In this paper, interest is in the reverse regression, i.e.

2 ) f(t) = α’ + β’s(t+k) + ε’(t) or more generally, interest is in the model

2’) f(t) = α’+ β’s(t+k) + δ’o(t) + ε’(t)

where f (t) = the average of the 30-day forward contract price recorded at period ts (t) = the spot price on contracts of wheat at period to (t) = the spot price for oil (Brent) at period tε (t) = error disturbance assumed distributed normal and independently with zero mean variance σ2

k = number of period into the future from time period tA precedent for such reverse regressions has been established in exchange rate models by Campbell and Shiller (1987), Engel and West (2005), and Chen, Rogoff and Rossi (2008).

Savoir être pour agir avec Sens - 10 -

Data and ModellingModels I

Savoir être pour agir avec Sens - 11 -

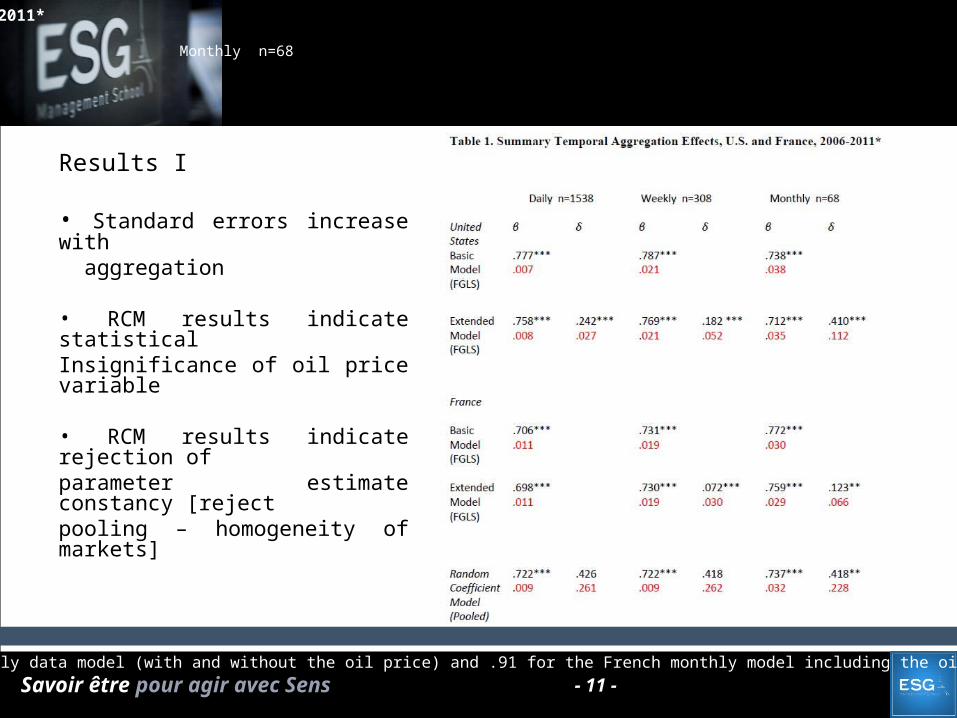

Results I

• Standard errors increase with aggregation

• RCM results indicate statistical Insignificance of oil price variable

• RCM results indicate rejection ofparameter estimate constancy [rejectpooling – homogeneity of markets]

Table 1. Summary Temporal Aggregation Effects, U.S. and France, 2006-2011*

Daily n=1538 Weekly n=308 Monthly n=68

*Standard errors are shown below the regression coefficient estimates in red. Adjusted R2 values range between .73 for the French daily data model (with and without the oil price) and .91 for the French monthly model including the oil price. The goodness-of-fit measure does not systematically increase or decrease with respect to model or unit of time aggregation.***Indicates significance at the 5 percent level or better. **Indicates significance at the 10 percent level or better.

Savoir être pour agir avec Sens - 12 -

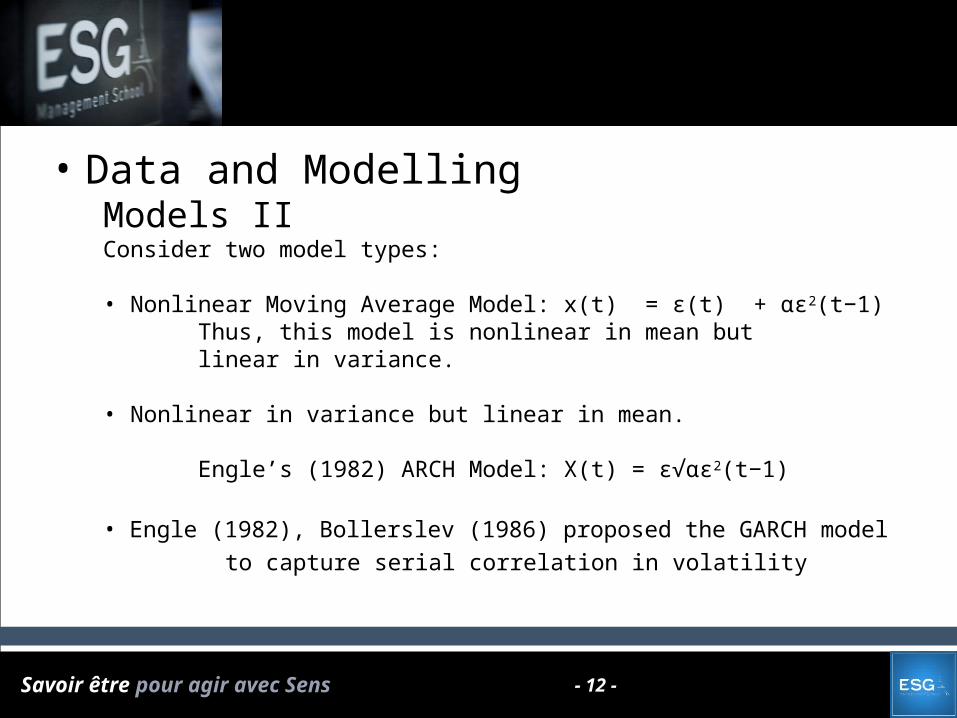

• Data and ModellingModels IIConsider two model types:

• Nonlinear Moving Average Model: x(t) = ε(t) + αε2(t−1) Thus, this model is nonlinear in mean but linear in variance.

• Nonlinear in variance but linear in mean.

Engle’s (1982) ARCH Model: X(t) = ε√αε2(t−1)

• Engle (1982), Bollerslev (1986) proposed the GARCH model to capture serial correlation in volatility

Savoir être pour agir avec Sens - 13 -

Data and ModellingModels II

Savoir être pour agir avec Sens - 14 -

Results II

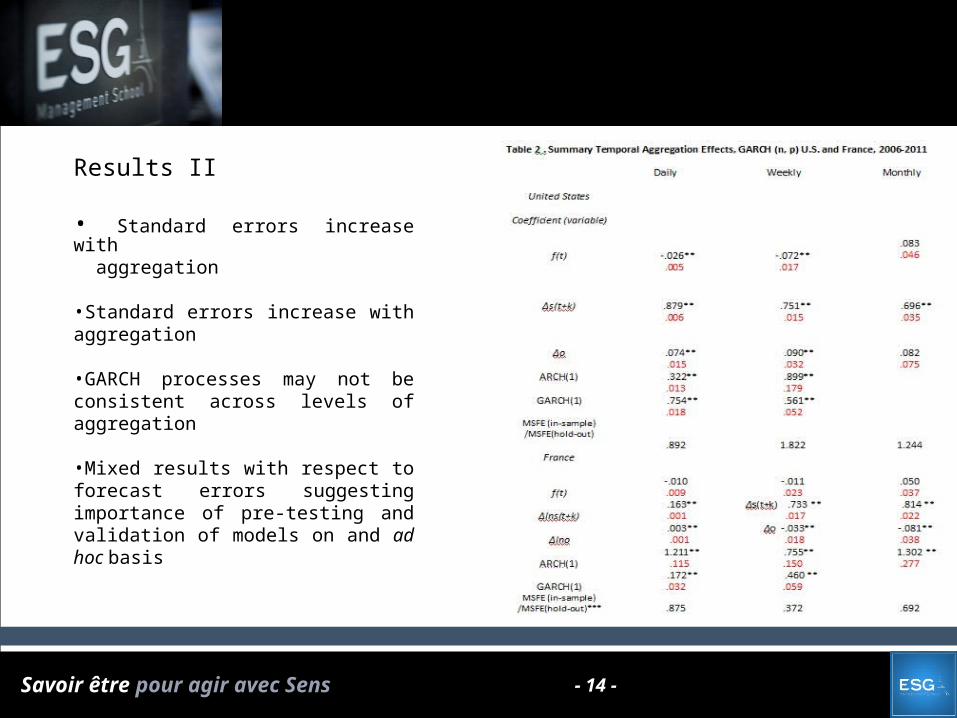

• Standard errors increase with aggregation

•Standard errors increase with aggregation

•GARCH processes may not be consistent across levels of aggregation

•Mixed results with respect to forecast errors suggesting importance of pre-testing and validation of models on and ad hoc basis

Savoir être pour agir avec Sens - 15 -

• Analyzed empirically the possible relationship between wheat futures prices and the relationship between wheat futures prices and spot oil prices

• Studied the effects model specification and of temporal aggregation on estimating the empirical relationship between prices in the two markets

• Wheat futures price and the spot oil prices are correlated as pointed out by Saghaian (2010).

• As to strict causality, the results are mixed, but it seems clear that model specification and temporal aggregation does impact evidence of the relationships between the variables indicated by model coefficient estimates, standard errors and forecasting accuracy.

• With respect to forecasting, this research points clearly toward the importance of using historical data to test forecast accuracy for specific series at alternative aggregation levels before generating out-of-sample predictions.