saturday, 7 th july, 2012 - wirc-icai.org · bhaumik colour, 120 ttj 865 (mum.) (sb) universal...

TRANSCRIPT

1

Saturday, 7th July, 2012Saturday, 7th July, 2012Direct Tax Refresher Course WIRC of ICAIBirla Matushri SabagrahaNew Marine Lines Mumbai

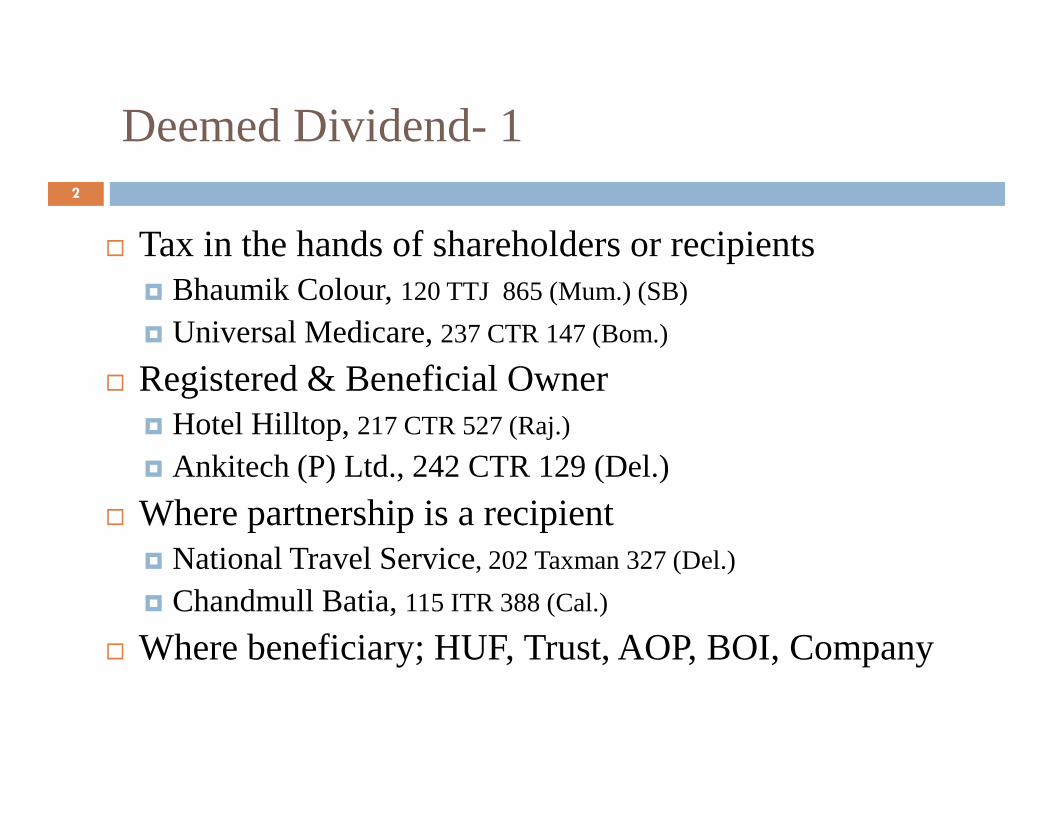

Deemed Dividend- 12

� Tax in the hands of shareholders or recipients� Bhaumik Colour, 120 TTJ 865 (Mum.) (SB)

� Universal Medicare, 237 CTR 147 (Bom.)

� Registered & Beneficial OwnerHotel Hilltop, � Hotel Hilltop, 217 CTR 527 (Raj.)

� Ankitech (P) Ltd., 242 CTR 129 (Del.)

� Where partnership is a recipient� National Travel Service, 202 Taxman 327 (Del.)

� Chandmull Batia, 115 ITR 388 (Cal.)

� Where beneficiary; HUF, Trust, AOP, BOI, Company

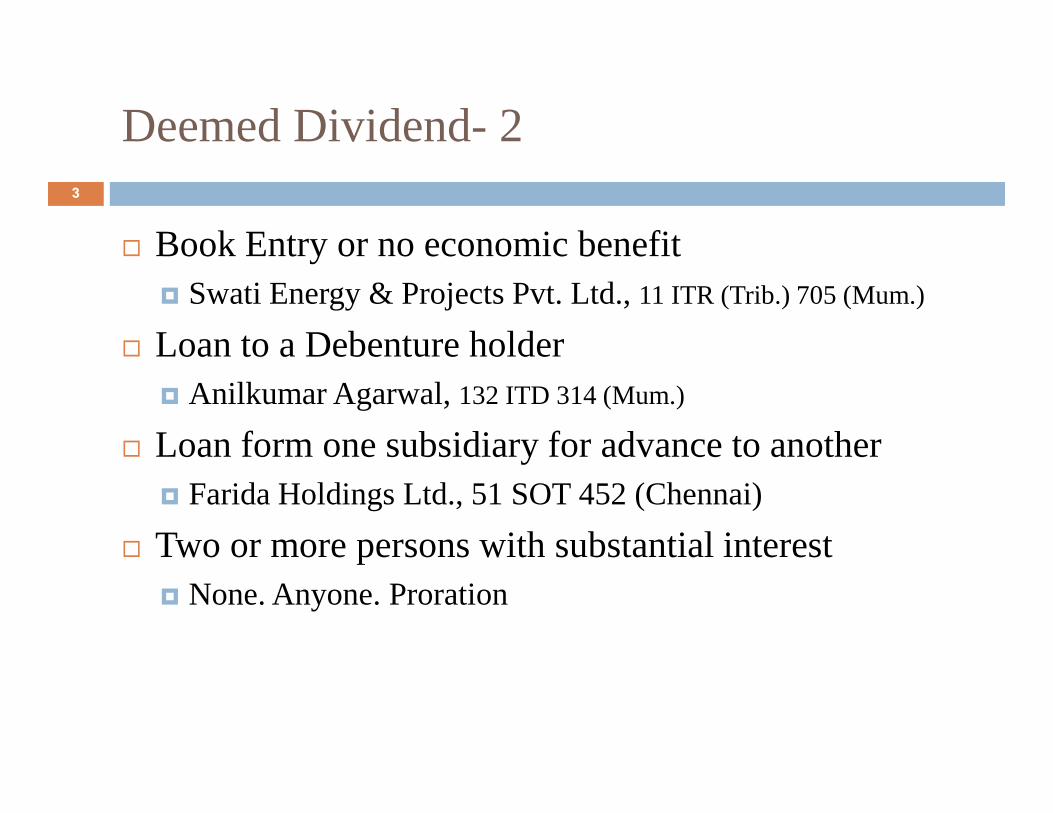

Deemed Dividend- 23

� Book Entry or no economic benefit� Swati Energy & Projects Pvt. Ltd., 11 ITR (Trib.) 705 (Mum.)

� Loan to a Debenture holder � AnilkumarAgarwal, 132 ITD 314 (Mum.)� AnilkumarAgarwal, 132 ITD 314 (Mum.)

� Loan form one subsidiary for advance to another � Farida Holdings Ltd., 51 SOT 452 (Chennai)

� Two or more persons with substantial interest� None. Anyone. Proration

Minimum Alternative Tax- 14

� Priority of credit u/s 115JAA over SC & EC� Classic Shares & Securities (Mum.), ITA No. 5869/Mum/2007

� Withdrawal from reserves � Indo Rama Synthetics Ltd. 2011-TIOL-01-SC

� Capital Gains credited to Reserves� Capital Gains credited to Reserves� Akshay Textile Trading, 304 ITR 401 (Bom.)

� Kopran Pharmaceuticals, 309 ITR 146 (AT) (Mum.)

� Deduction u/s 80HHC� Al Kabeer Exports Ltd. 32274 of 2010 (SC)

� Bhari Infotech Systems 328 ITR 380 (Mad.)

� FA 2011 Amendment and Deduction u/s 80HHC

Minimum Alternative Tax- 25

� Depreciation at different rates � Malayala Manorama Ltd, 300 ITR 251 (SC)

� Dynamic Orthopedics, 321 ITR 300 (SC)

� Loss on reduction in share capital� Sumi Motherson, 2010-TIOL-756-Delhi

� Finance Act, 2012 Amendments.� Compulsory credit( addition) to Book Profit� Revaluation reserve on retirement or disposal of asset� Year of debit

� ‘S.211(2) Proviso company’ – special P&L Account � Banking, Insurance, Electricity companies

Public Offer & Exemption u/s 10(38)6

� Amendment of Finance Act, 2012 for STT� Offer for sale of unlisted equity shares to public in an IPO� STT @ 0.2% by lead Merchant Banker form Seller � Subsequent Listing on recognized Stock Exchange

� Difficulty for s. 10(38) exemption up to A.Y. 2012-13� Difficulty for s. 10(38) exemption up to A.Y. 2012-13

� Bulk window & Block deal mechanism� SEBI circular, MRD/SE-7 dt. 14.01.2004� Guidelines� Private deal – SPA� Price Difference� Possible tax implications� Cost of controlling interest

Receipt of shares by CHC- s.56(2)(viia) - 1

7

� Receipt of shares of a non s. 2(18) company � By ‘firm’ and ‘company’ recipients

� s. 2(18) company excluded � LLP included

� With/out consideration > Rs. 50,000, whole� With/out consideration > Rs. 50,000, whole� FMV as per Rules 11U & 11UA� By or From –Resident or not � Substantive not clarificatory� Shares

� Preference shares included – CD not included � Rights not included - Shares of subsidiaries

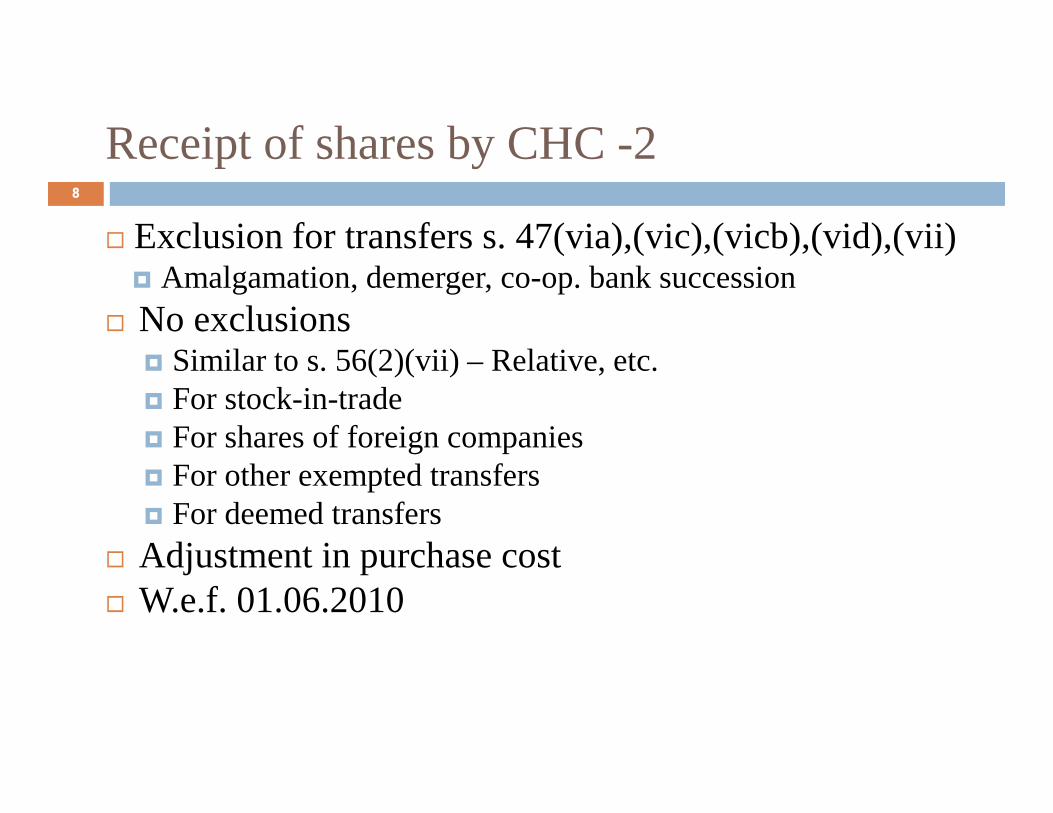

Receipt of shares by CHC -2 8

� Exclusion for transfers s. 47(via),(vic),(vicb),(vid),(vii)� Amalgamation, demerger, co-op. bank succession

� No exclusions � Similar to s. 56(2)(vii) – Relative, etc.� For stock-in-trade� For stock-in-trade� For shares of foreign companies � For other exempted transfers� For deemed transfers

� Adjustment in purchase cost� W.e.f. 01.06.2010

Receipt of shares by CHC - 39

� COA in hands of recipient – s.49(4)o ‘Subjected to tax’ u/s 56(2)(vii) & (viia)o Value that is ‘taken into account’o COA in cases where FMV < Rs. 50,000

S. 49(4) and s. 49(1)o S. 49(4) and s. 49(1)o Period of holding and s. 2(42A)

� Business receipts� Receipts on distribution� On credit by payer� Deductions admissible

Receipt of ‘premium’ by CHC - s.56(2)(viib)- 110

� Issue of shares by closely held company, A.Y. 2013-14

� Receipt’ by a ‘CHC’ from a ‘resident’

� Consideration for ‘issue’ of ‘shares’� Where exceeds face value

� Tax on excess over FMV of shares -Rs.50,000Tax on excess over FMV of shares -Rs.50,000� Exemption for issue by VCC, VCF and VCU

� FMV as per prescribed method or satisfaction of A.O.

� Non resident, R&NOR

� Preference shares

� Income of the company

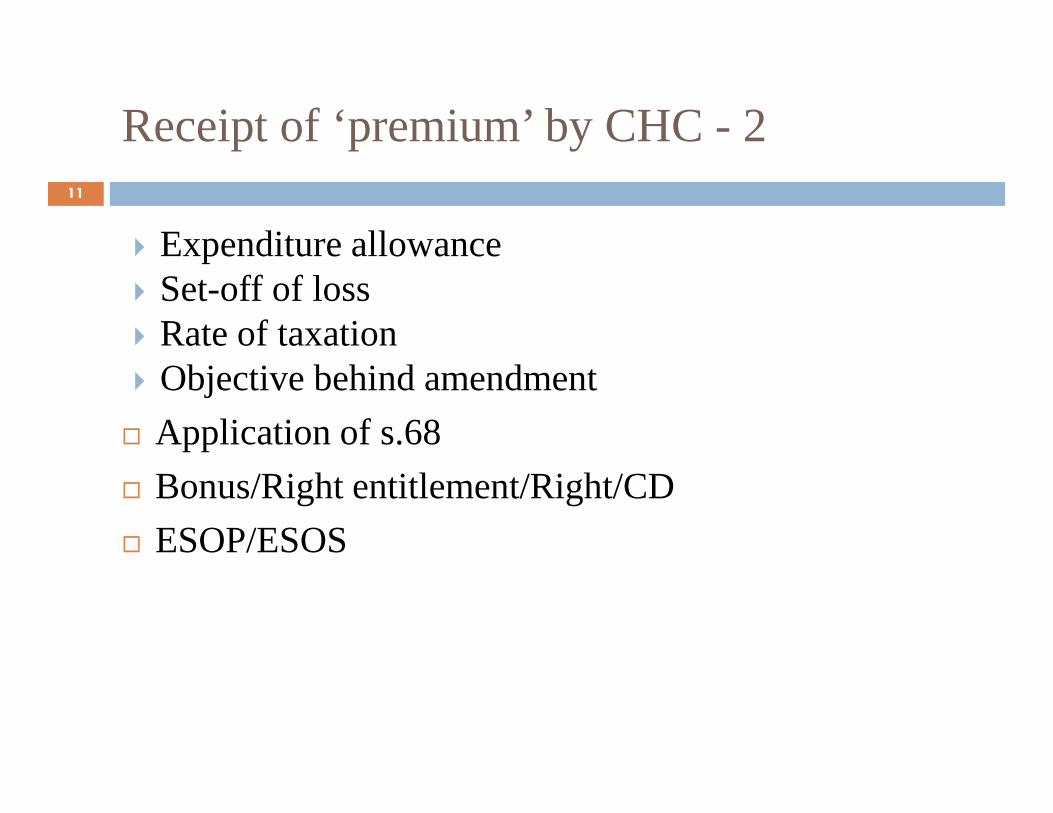

Receipt of ‘premium’ by CHC - 211

� Expenditure allowance� Set-off of loss� Rate of taxation� Objective behind amendment

� Application of s.68

� Bonus/Right entitlement/Right/CD

� ESOP/ESOS

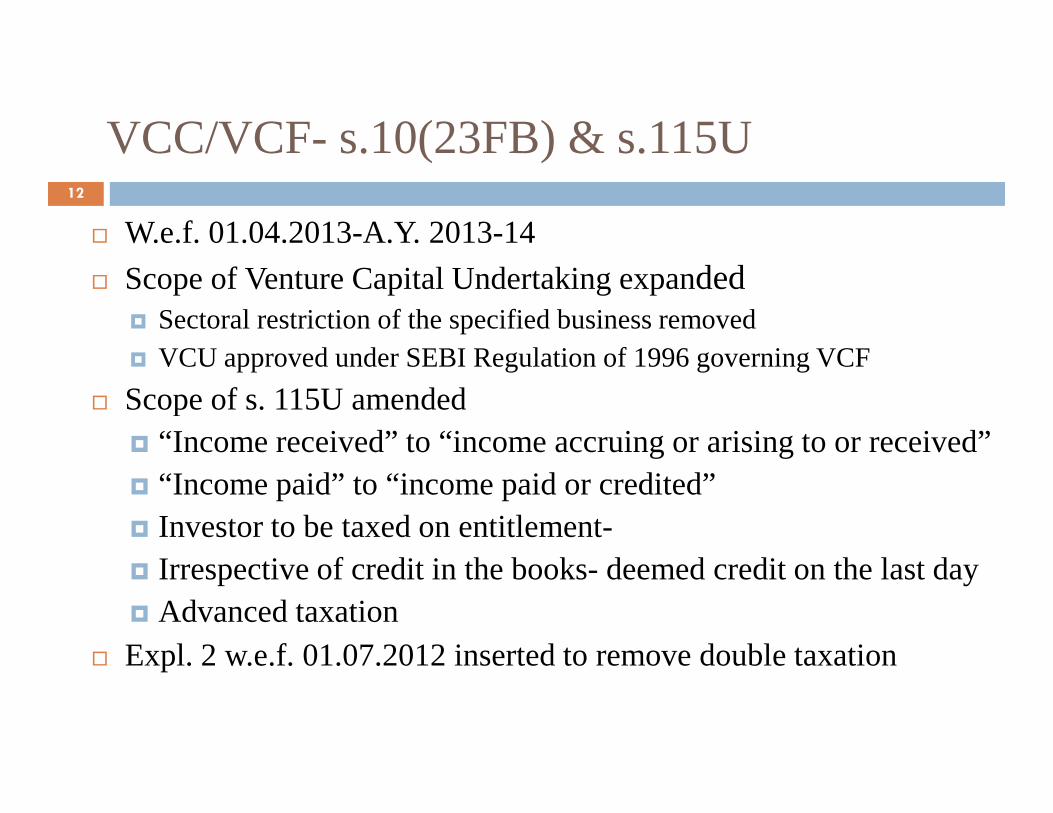

VCC/VCF- s.10(23FB) & s.115U12

� W.e.f. 01.04.2013-A.Y. 2013-14

� Scope of Venture Capital Undertaking expanded� Sectoral restriction of the specified business removed� VCU approved under SEBI Regulation of 1996 governing VCF

� Scope of s. 115U amended� Scope of s. 115U amended� “Income received” to “income accruing or arising to or received”� “Income paid” to “income paid or credited”� Investor to be taxed on entitlement-� Irrespective of credit in the books- deemed credit on the last day� Advanced taxation

� Expl. 2 w.e.f. 01.07.2012 inserted to remove double taxation

DDT- s.115-O (IA)

13

� W.e.f. 01.07.2012

� One cascading effect of DDT on Dividend relaxed

� Distribution by recipient domestic company eligible for reliefrelief� Need not be an ultimate holding company

� May be subsidiary of another upstream company

� Concession only for group companies

Share Capital and s.68- Amendments14

� Three Amendments of FA, 2012- w.e.f. A.Y. 2013-14

� Law of cash creditors upto A.Y. 2012-13� Provisions. Essentials. Case Laws. Rate

� Expanding and extending onus for certain receipts� Expanding and extending onus for certain receipts� Share capital. Share premium. Like receipts

� From resident- VCC & VCF excluded

� Closely held company

Share Capital and s.6815

� Onus to explain sources of source of receipt� Payer to offer explanation- nature & source

� Satisfaction of AO

� On notice by AO to Payer

� Relevance of satisfaction of Payer’s AO

� Consequence� Income of CHC

� Tax at 30% u/s 115BBE

� Absence of discretion

Case Law on Share Capital16

� Lovely Exports (P) Ltd., 216 CTR 195 (SC)

� Shareholders name & address

� Steller Investment Ltd., 115 Taxman 99 (SC)

� Non- genuine (Owners of Funds)� Non- genuine (Owners of Funds)

� Divine Leasing, 158 Taxman 440 (Del.)

� Non- genuine (Owners of Funds)

� Onus shifts to AO to examine capacity

Case Law on Source of Source of Capital17

� S. Hastimal, 49 ITR 273 (Mad.)

� TolaramDaga, 59 ITR 632 (Assam)

� Sarogi Credit Corpn., 103 ITR 344 (Pat.)

Share Capital and s.68 - Issues 18

� Receipt of such amount by whatever name called� Preference Shares. CD. Mergers. � Para IX. Rights. Sweat-Equity

� R& NOR, change of status� Conversion of loan into equityConversion of loan into equity� Expenditure for issue of capital� Set-off of losses� Motivation of payer� Dual taxation� Year of taxation� Credit in share capital account

Deemed Speculation 19

� Loss & Profit� Samba Trading& Investment, 58 TTJ 360(Mum)

� Application to a Broker� Priyasha Mever Finance P.Ltd., 5 ITR 441 (Mum)(Trib.)

� Relevance of legislative intent� Relevance of legislative intent� AMP Spg. & Wvg. Mills (P) Ltd., 101 TTJ 1113 (Ahd.)(SB)

� Excl. of speculation loss for deciding applicability� Paramount Info. Systems P.Ltd., 42-A BCAJ 169(Mum),

� Set-off of Explanation loss and amendment of 2006� Virendrakumar Jain, 42-A BCAJ 169(Mum.)

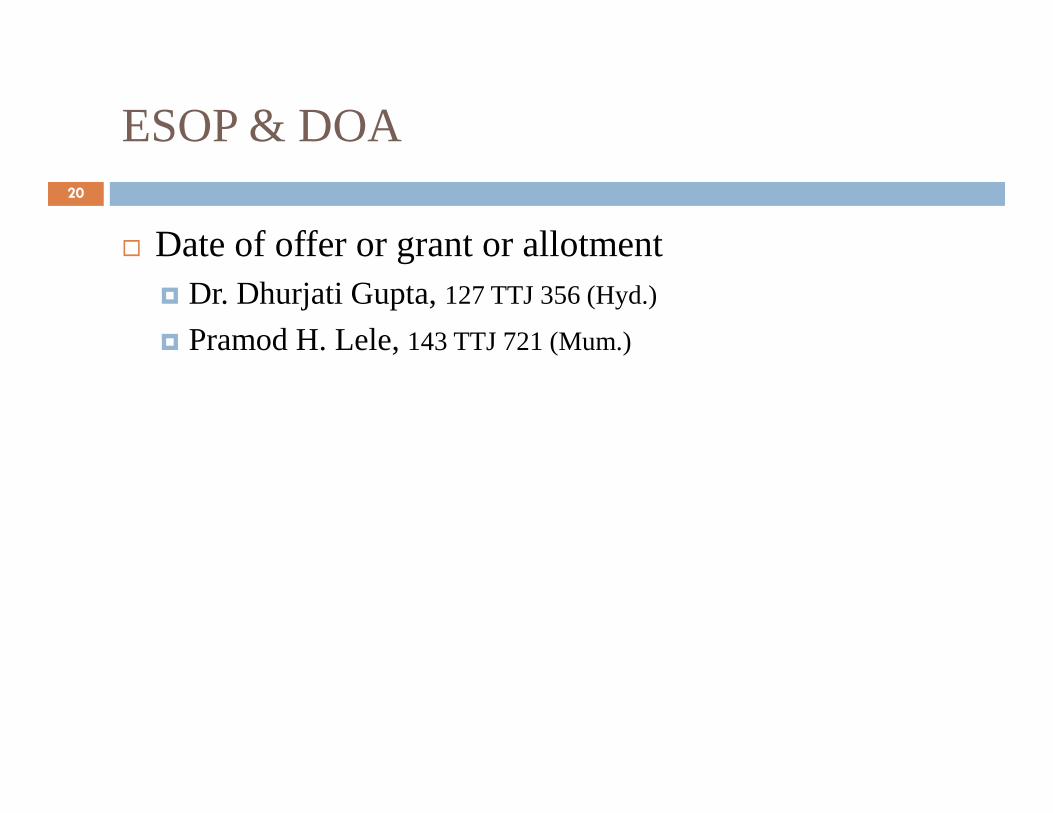

ESOP & DOA20

� Date of offer or grant or allotment� Dr. Dhurjati Gupta, 127 TTJ 356 (Hyd.)

� Pramod H. Lele, 143 TTJ 721 (Mum.)

Liquidation s. 46 -121

� COA of asset in the hands of shareholder� FMV on the date of distribution� Not to be reduced by Deemed dividend� S. 49 (1)(iii)(c) and s. 55(2)(b)(iii) - applicability� T.R.Srinivasan, 133 TTJ 49(Chennai)

� Piecemeal taxation and deduction of COA� Piecemeal taxation and deduction of COA� Cable and Wireless Ltd., 90 ITR 84 (Bom)� Inland Agencies (P) Ltd., 143 ITR 186 (Mad)

� Benefit of reinvestment� Ruby Trading Co. P. Ltd., 259 ITR 54 (Raj)� Brahmi Investment P. Ltd., 48 TTJ 326(Ahd.)

� Exemption – distribution of qualifying asset� ‘Purchase’ or not for s. 54F

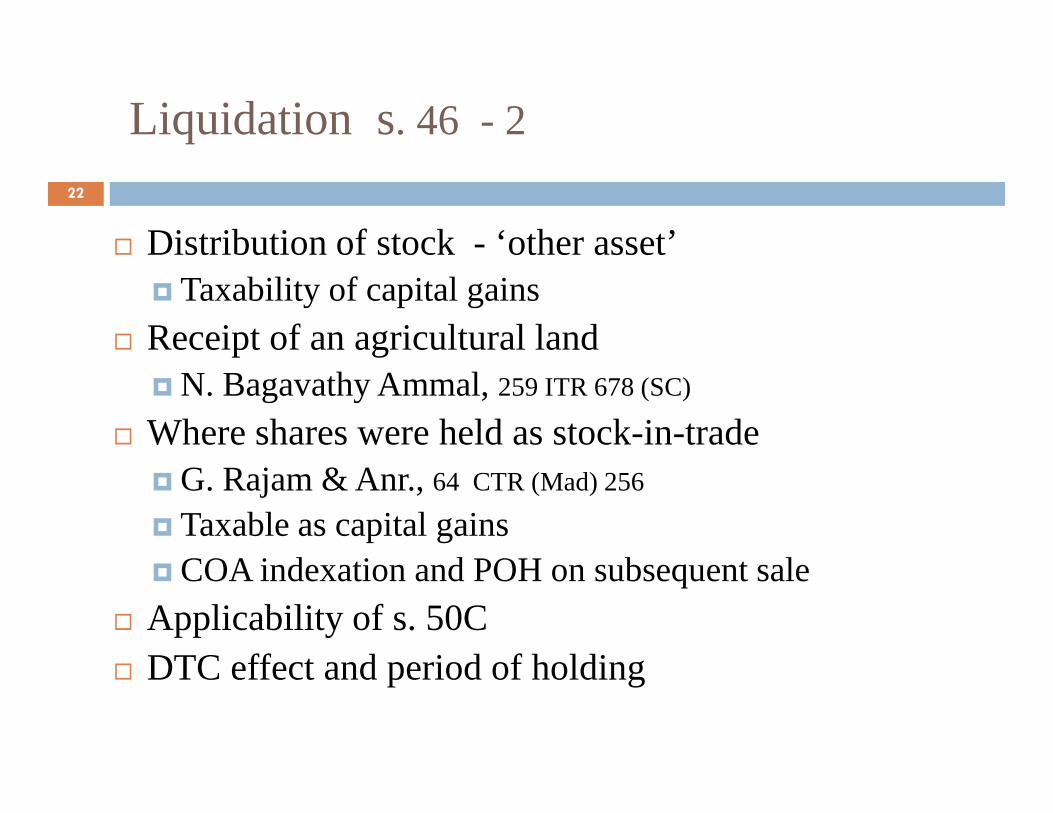

Liquidation s. 46 - 2

22

� Distribution of stock - ‘other asset’� Taxability of capital gains

� Receipt of an agricultural land� N. Bagavathy Ammal, 259 ITR 678 (SC)

� Where shares were held as stock-in-trade� G. Rajam& Anr., 64 CTR (Mad) 256

� Taxable as capital gains� COA indexation and POH on subsequent sale

� Applicability of s. 50C� DTC effect and period of holding

Amalgamation & Demerger –s.47(vii)(a), s.2(19AA) & s. 72A

23

� S.47(vii) and s.2(19AA)� W.e.f. 01.04.2013, A.Y. 2013-14

� Saving from allotment of shares in consideration

� Where concerned company a shareholder� Where concerned company a shareholder

� Prospective application, only

� Set-off of losses of amalgamated company- Reverse merger� Wrigley India (P) Ltd., 142 TTJ 23 (Del.)

Corporatization & s.47(xiii)24

� Time for issue of shares� Prakash Electric Co., 118 TTJ 539 (Bang.)

� Sanjay Singh., (2012) 19 taxmann.com 88 (Del.)

Method of Accounting, AS & Company25

� S.209 of Companies Act

� Cash system of accounting� Stup Consultants Pvt. Ltd., 13 ITR (Trib) 468 (Mum.)

Income during Construction Period26

� Tuticorin Alkali, 227 ITR 172 (SC)-Interest

� Bokaro Steel, 236 ITR 315 (SC)-Rent

� Neha Proteins Ltd, 306 ITR 102 (Raj.)- Set-off

� Winsome Dyeing, 10 DTR 207 (HP) -Taxable

� L.G. Electronics, 309 ITR 265 (Del.)-Set-off

VRS & s.35DDA27

� Scheme to be in accordance with Rule 2BA

� Implication of non-compliance� Warner Lambert, 143 TTJ 571 (Mum.)

� Sony India Ltd., 141 TTJ 432 (Del.)� Sony India Ltd., 141 TTJ 432 (Del.)

Loan to Subsidiary- s.36(1)(iii)28

� Interest free and investment in shares commercial expediency� S.A. Builders, 288 ITR 1 (SC)

� Tulip star Hotels Ltd. (SC)

� Effect of s.14A on investment in shares

Disallowance u/s 14A - 129

� Adequacy of owned funds � Reliance Utilities Ltd., 313 ITR 340 (Bom.)

� Position u/s 14A for owned funds� Bunge Agribusiness Ltd., 142 TTJ 817 (Mum.)

� Applicability to MAT� Applicability to MAT� Goetze (India) Ltd., 32 SOT 101 (Del.)

� Rule 8D and Stock-in-trade� CCI Ltd., ITA no. 359 of 2011 (Karnataka)

� Catholic Syrian Bank, 237 CTR 164 (Ker.)

� Maxopp Investment, 203 Taxman 364 (Del.)

� Leena Ramachandran, 235 CTR 512 (Ker.)

Disallowance u/s 14A - 230

� Interest (net or gross)� Morgan Stanley P. Ltd., 3077/M/2005

� Higher interest income� Trade Apartment Ltd., 1277/Kol/2011� Trade Apartment Ltd., 1277/Kol/2011

� Gillette Group, 267/Del/2012

� Lakshmi Ring Travellers, 2083/Chen/2011

� Administration Expenses @ 0.5%� Philips Carbon Black, 566/Kol/2009

Intangibles for s.3231

� Membership of stock exchanges� Techno Shares & Stocks, 327 ITR 323 (SC)

� Business & Commercial rights� Osram India (P) Ltd., 51 DTR 297 (Del.)� Areva T&D, 315 of 2010 (Del.) - Customers

ONGC Videsh, Prospection� ONGC Videsh, 37 SOT 97 (Del.) -Prospection� Ashoka Info, 123 TTJ 77 (Pune) -Toll collection

� License� Piem Hotels, 135 TTJ 228 (Mum.)

� Brand on amalgamation� KEC International Ltd., 41 SOT 43 (Mum.)

� Goodwill

Fluctuation in Rate of Exchange 32

� Currency translations – year end � Maruti Udyog Ltd., 320 ITR 729 (SC)� Woodward Governor , 312 ITR 254 (SC)

� Loss on refund of advance received � Loksons Pvt. Ltd., 11 DTR 206 (Bom)

Rollover premium and S. 36(1)(iii), 43A� Rollover premium and S. 36(1)(iii), 43A� Elecon Eng. Ltd., 322 ITR 20 (SC)

� Loss on advance against sales� Taiko CNCPL, 311 ITR 475(Delhi)

� Forex forward contracts� Open ended � Nature of loss� Accounting� Taxation

Non- Compete Fees 33

� Payer’s perspective� Revenue or capital� Depreciation- tangible or intangible

� Payee’s perspective� Capital receipts- capital gains, s. 55(2)� Business income s.28(va) � Business income s.28(va)

� Case Law � Guffic Chem Ltd., 332 ITR 602 (SC)

� Late Dr. B.V. Raju, 14 ITR (Trib.) 387 (Hyd.)

� Tecumseh Ltd., 127 ITD 1 (Del.) (SB)

� Ramesh D. Tainwala, 48 SOT 324 (Mum.)

� Savita N. Mandhana, 3900/M/2010

� Homi Aspi Balsara, 30 DTR 576 (Mum.)

� Pitney Bowes (P) Ltd., 204 Taxman 333 (Del.)

Disallowance u/s 40(a)(ia) & TDS34

� ‘Paid’ and ‘Payment’� Merilyn Shipping,146 TTJ 1 (Vizag) (SB)

� Short withholding, rate or section� Bunge Agribusiness Ltd., 142 TTJ 817 (Mum.)

� Chandabhoy & Jassobhoy, 49 SOT 448 (Mum.)

� Beekaylon Synthetics, 6506/M/2008 (Mum.)

S.K. Tekriwal, � S.K. Tekriwal, 1135/Kol/2010 (Kol.)

� Second proviso and retrospectivity� Bharati Shipyard, 132 ITD 53 (Mum.) (SB)

� Virgin Creations, ITA No. 302 of 2011 (Cal.)

� Rajamahendi Shipping, 51 SOT 242 (Vizag)

� Kotak Securities Ltd., 340 ITR333 (Bom.)

� DICGC Ltd., 14 ITR (Trib) 194 (Mum.)

� Dynamic Vertical Software, 332 ITR 222 (Del.)

� FA, 2012 Amendment� Relief

THANK YOU

35

THANK YOU