sahaviriya steel industries public company...

TRANSCRIPT

February 2005February 2005

Sahaviriya Steel Industries Public Company LimitedSahaviriya Steel Industries Public Company Limited

HK000IYENOT AN OFFER OF SECURITIES

DisclaimerThe information contained in this presentation is intended solely for your personal reference only. If

you are not an intended recipient, you must not read, disclose, copy, circulate , retain, distribute or take any action in reliance upon this material. This presentation is not intended to substitute your own

analysis and investigation, and should not be considered a recommendation to any recipient of this presentation. Some statements contained herein are forward-looking statements identified by the use of forward- looking terminology such as “may” , “will” , “expect” , “anticipate”, “intend” , “estimate” , “continue”, “plan” or other similar words, which are subject to various risks and uncertainties. These statements include statements with respect to the Company’s corporate plans, strategies and beliefs

and other statements that are not historical facts. . This presentation is prepared based on the assumptions and beliefs of Sahaviriya Steel Industries Public Company Limited (the “Company” or

“SSI”)’s management in light of the information currently available to the Company involving risks and uncertainties which may cause the actual results, performance or achievements to be materially

different from any future results, performance or achievements expressed or implied by such forward-looking statements. Nothing in this presentation is, or shall be relied on as promise or representation of

the Company as to the future.

DisclaimerThe information contained in this presentation is intended solelThe information contained in this presentation is intended solely for your personal reference only. If y for your personal reference only. If

you are not an intended recipient, you must not read, disclose, you are not an intended recipient, you must not read, disclose, copy, circulate , retain, distribute or take copy, circulate , retain, distribute or take any action in reliance upon this material. This presentation isany action in reliance upon this material. This presentation is not intended to substitute your own not intended to substitute your own

analysis and investigation, and should not be considered a recomanalysis and investigation, and should not be considered a recommendation to any recipient of this mendation to any recipient of this presentation. Some statements contained herein are forwardpresentation. Some statements contained herein are forward--looking statements identified by the use looking statements identified by the use of forwardof forward-- looking terminology such as looking terminology such as ““maymay”” , , ““willwill”” , , ““expectexpect”” , , ““anticipateanticipate””, , ““intendintend”” , , ““estimateestimate”” , , ““continuecontinue””, , ““planplan”” or other similar words, which are subject to various risks and or other similar words, which are subject to various risks and uncertainties. These uncertainties. These statements include statements with respect to the Companystatements include statements with respect to the Company’’s corporate plans, strategies and beliefs s corporate plans, strategies and beliefs

and other statements that are not historical facts. . This preseand other statements that are not historical facts. . This presentation is prepared based on the ntation is prepared based on the assumptions and beliefs of Sahaviriya Steel Industries Public Coassumptions and beliefs of Sahaviriya Steel Industries Public Company Limited (the mpany Limited (the ““CompanyCompany”” or or

““SSISSI””))’’s management in light of the information currently available to s management in light of the information currently available to the Company involving risks and the Company involving risks and uncertainties which may cause the actual results, performance oruncertainties which may cause the actual results, performance or achievements to be materially achievements to be materially

different from any future results, performance or achievements edifferent from any future results, performance or achievements expressed or implied by such forwardxpressed or implied by such forward--looking statements. Nothing in this presentation is, or shall belooking statements. Nothing in this presentation is, or shall be relied on as promise or representation of relied on as promise or representation of

the Company as to the future.the Company as to the future.

HK000IYENOT AN OFFER OF SECURITIES

Introduction to SSIIntroduction to SSI

4HK000IYE

NOT AN OFFER OF SECURITIES

The SSI TeamThe SSI Team

Dr. Maruey PhadoongsidhiDr. Maruey PhadoongsidhiChairman of Board of Directors Chairman of Board of Directors

11 years of industry experience11 years of industry experience5 years with SSI as Chairman 5 years with SSI as Chairman President, The Stock Exchange of President, The Stock Exchange of Thailand (1985Thailand (1985--1992) 1992) Ph.D. (Business) from University of Ph.D. (Business) from University of WisconsinWisconsin

Mr. Win ViriyaprapaikitMr. Win ViriyaprapaikitPresident and Executive Director President and Executive Director

>11 years of industry experience with >11 years of industry experience with the Sahaviriya Groupthe Sahaviriya Group6 years with SSI6 years with SSIDirector of Sahaviriya Group since 1999Director of Sahaviriya Group since 1999MBA from Chulalongkorn UniversityMBA from Chulalongkorn University

Mr. Wit Mr. Wit ViriyaprapaikitViriyaprapaikitChairman of Board of Executive DirectorsChairman of Board of Executive Directors

>50 years of industry experience >50 years of industry experience 15 years with SSI15 years with SSIChief Executive Officer of Sahaviriya Chief Executive Officer of Sahaviriya GroupGroupHonorary B.A. from Rajamungala Honorary B.A. from Rajamungala Institute of TechnologyInstitute of Technology

Ms. Vilai ChattanrassameeMs. Vilai ChattanrassameeVice President, Finance & AccountingVice President, Finance & Accounting

8 years of industry experience8 years of industry experience6 years with SSI6 years with SSIExecutive Vice President of Siam Executive Vice President of Siam Integrated Cold Rolled Sheet in 1996Integrated Cold Rolled Sheet in 1996--19981998M.S. Accounting from Thammasat M.S. Accounting from Thammasat UniversityUniversity

5HK000IYE

NOT AN OFFER OF SECURITIES

Asia1%

Indonesia1%

China3%

Canada2%

USA75%

Philippines18%

Export8%

Domestic92%

Company SnapshotCompany Snapshot

StreamlinedStreamlined2004 Volume2004 VolumeBreakdownBreakdown

By ProductBy Product By MarketBy Market

EstablishedEstablishedCoreCore

BusinessBusiness

# 1 steel company in Thailand, with sales of THB 37,093 mm and net profit of THB 5,333 mm in 2004Established in 1990 as the first and only conventional standalone hot strip mill in Thailand Largest hot strip mill in Thailand and in Southeast Asia

4.0 mm tpa(1) of Hot-rolled coil (HRC) capacityUp to 1.0 mm tpa of HRC Pickled and Oiled (HRC P/O) capacity

Dominant market position with 33% domestic market share of HRC

# 1 steel company in Thailand, with sales of THB 37,093 mm and net profit of THB 5,333 mm in 2004Established in 1990 as the first and only conventional standalone hot strip mill in Thailand Largest hot strip mill in Thailand and in Southeast Asia

4.0 mm tpa(1) of Hot-rolled coil (HRC) capacityUp to 1.0 mm tpa of HRC Pickled and Oiled (HRC P/O) capacity

Dominant market position with 33% domestic market share of HRC

Advantageous Advantageous LocationLocation

Bang Saphan, Prachuap Khirikhan Province, 400 km south of Bangkok“Coastal Mill” – in the same vicinity of Prachuap Port deep seaportPerfect strategic location for steel making business

Bang Saphan, Prachuap Khirikhan Province, 400 km south of Bangkok“Coastal Mill” – in the same vicinity of Prachuap Port deep seaportPerfect strategic location for steel making business

Commitment fromCommitment fromSahaviriya GroupSahaviriya Group

47.6% held by Sahaviriya Group (“SVG”) – leading Thailand steel conglomerate Provides negotiating power with suppliers/customers47.6% held by Sahaviriya Group (“SVG”) – leading Thailand steel conglomerate Provides negotiating power with suppliers/customers

Export By CountryExport By Country

________________________________________________________(1)(1) tpa = ton(s) per annumtpa = ton(s) per annum(2)(2) DWT= Deadweight Ton(s)DWT= Deadweight Ton(s)

Commercial Grade49%

Premium Grade51%

6HK000IYE

NOT AN OFFER OF SECURITIES

Overview of SSI’s Investment and Associated CompaniesOverview of SSI’s Investment and Associated Companies

SSISSI’’s Investments s Investments Selected SVG SubsidiariesSelected SVG Subsidiaries

Sahaviriya Plate Mill Co.,Ltd.Hot-rolled plateCapacity of 1 mm tpa

Sahaviriya Plate Mill Co.,Ltd.Hot-rolled plateCapacity of 1 mm tpa

Bangsaphan Bar Mill Public Company LimitedRound bar, deformed bar, hexagonal barCapacity of 1.0 mm tpaJV with Taiwanese partnerListed on SET(4) (1 Feb 2005)

Bangsaphan Bar Mill Public Company LimitedRound bar, deformed bar, hexagonal barCapacity of 1.0 mm tpaJV with Taiwanese partnerListed on SET(4) (1 Feb 2005)

Prapadaeng Shape Steel Co., Ltd.Equal angles, channels, flat bars, i-beamCapacity of 1.0 mm tpa

Prapadaeng Shape Steel Co., Ltd.Equal angles, channels, flat bars, i-beamCapacity of 1.0 mm tpa

B.P. Wire Rod Co., Ltd.Wire rods, capacity of 0.3 mm tpaSpecial bars, capacity of 0.3 mm tpa

B.P. Wire Rod Co., Ltd.Wire rods, capacity of 0.3 mm tpaSpecial bars, capacity of 0.3 mm tpa

Deep seaportDeep seaport

TCR(2) TCS(3)PPC(1)

1st established Cold-rolled steel sheet in ThailandCapacity of 1.2 mm tpaRaw material: HRCPurchase 35% of HRC supplies from SSIJV with Japanese partner

1st established Cold-rolled steel sheet in ThailandCapacity of 1.2 mm tpaRaw material: HRCPurchase 35% of HRC supplies from SSIJV with Japanese partner

Coated steel sheetCapacity of 180,000 tpaRaw material: CRC

Coated steel sheetCapacity of 180,000 tpaRaw material: CRC

51.0% 8.8% 3.7%

______________________________________________________________________________________(1)(1) PPC = Prachuap Port Co., Ltd.PPC = Prachuap Port Co., Ltd.(2)(2) TCR = Thai Cold Rolled Steel Sheet Pcl.TCR = Thai Cold Rolled Steel Sheet Pcl.(3)(3) TCS = Thai Coated Steel Sheet Co., Ltd.TCS = Thai Coated Steel Sheet Co., Ltd.(4)(4) SET = Stock Exchange of ThailandSET = Stock Exchange of Thailand* Listed company* Listed company

SVG

SPM

BSBM*

PSS

BPW

87.0%

47.8%

100.0%

47.6%

100.0%

7HK000IYE

NOT AN OFFER OF SECURITIES

SSISSI’’s 2004 Product s 2004 Product ApplicationsApplications

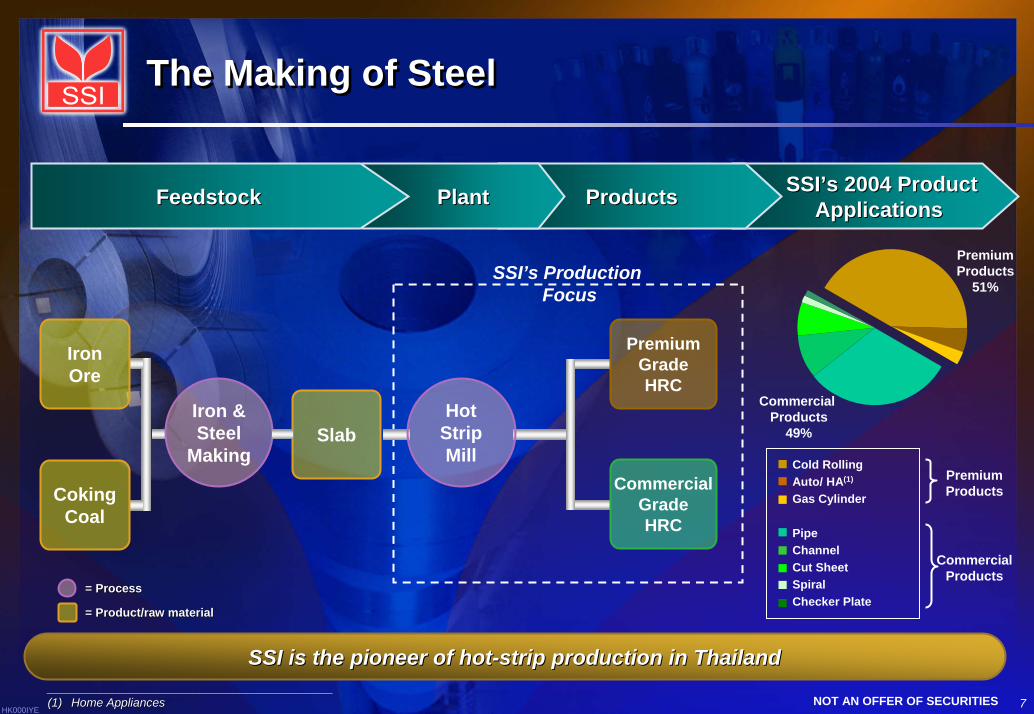

The Making of SteelThe Making of Steel

ProductsProductsPlantPlantFeedstockFeedstock

SSI is the pioneer of hotSSI is the pioneer of hot--strip production in Thailandstrip production in Thailand

Iron Ore

Coking Coal

Slab

Premium Grade HRC

Commercial GradeHRC

Hot Strip Mill

Iron & Steel

Making

= Process= Process

= Product/raw material= Product/raw material

Cold RollingAuto/ HA(1)

Gas Cylinder

PipeChannelCut SheetSpiralChecker Plate

PremiumProducts

51%

Commercial Products

49%

SSI’s Production Focus

______________________________________________________________________________________(1)(1) Home Appliances Home Appliances

PremiumProducts

CommercialProducts

HK000IYENOT AN OFFER OF SECURITIES

Company HighlightsCompany Highlights

9HK000IYE

NOT AN OFFER OF SECURITIES

Company HighlightsCompany Highlights

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable and Stable and Attractive MarginsAttractive Margins

Strong Financial Strong Financial PositionPosition

LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential

10HK000IYE

NOT AN OFFER OF SECURITIES

Favorable Industry EnvironmentFavorable Industry EnvironmentFavorable Industry Environment

Global Crude Steel ProductionGlobal Crude Steel Production Domestic Automobile ProductionDomestic Automobile Production

Domestic Finished Product DemandDomestic Finished Product Demand

Continued demand growth supported by robust expansion in downstrContinued demand growth supported by robust expansion in downstream steeleam steel--user industriesuser industries

(mm tons)

Electrical Appliances SupplyElectrical Appliances Supply

Thailand Construction ExpenditureThailand Construction Expenditure

11 12 14

2002 2003 2004E

450500

560

2002 2003 2004

(THB bn)

850904

9681,035

2001 2002 2003 2004

8.010.0 11.0

13.0

2001 2002 2003 2004

(mm tons)

Source: Thailand Automotive Institute, The Federation of Thai ISource: Thailand Automotive Institute, The Federation of Thai Industriesndustries

Source: The Federation of Thai Industries, Bank of Thailand, Source: The Federation of Thai Industries, Bank of Thailand, SSG research and SSISSG research and SSI’’s estimatess estimates

Source: National Economic and Social Development BoardSource: National Economic and Social Development Board

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable & Attractive Stable & Attractive MarginsMargins

Strong Financial PositionStrong Financial Position LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential

585751

2002 2003 2004

(‘000 units)

HRCHRCPrice/tonPrice/ton $241$241 $286 $286 $344$344 $561$561

928

(mm units)

Source: International Iron and Steel Institute, Iron and Steel Source: International Iron and Steel Institute, Iron and Steel Institute of Thailand,Institute of Thailand,and Organization for Economic Coand Organization for Economic Co--operation and Development operation and Development

11HK000IYE

NOT AN OFFER OF SECURITIES

SSI30%

Importers70%

Favorable Industry Environment (Cont’d)Favorable Industry Environment (ContFavorable Industry Environment (Cont’’d)d)

Largest HotLargest Hot--Rolled Strip Mill in Southeast AsiaRolled Strip Mill in Southeast Asia

0.5

1.51.51.52.0

4.0

PT KrakatauSteel

(Indonesia)

NSM(Thailand)

G Steel(Thailand)

Megasteel(Malaysia)

NationalSteel

(Philippines)

Competition: G-Steel and Nakornthai Strip Mill (NSM)

Target different market segments – various product gradesSSI produces higher-grade HRC

SSISSI’’s Dominant Domestic Market Positions Dominant Domestic Market Position(1)(1)

(mm tons)

Source: Newsrun and street dataSource: Newsrun and street data

Importers17%

NSM14%

SSI36%

G-Steel33%

Premium GradePremium GradeProductsProducts

Commercial Grade Commercial Grade ProductsProducts

Enjoy anti-dumping tariff advantageSSI not subject to U.S. AD tariffsIn 2004, Thailand was relieved of Countervailing Duties (CVD)

Competition: Japan & KoreaSSI’s edge

High quality and competitive pricingSupply shortage from importersThai anti-dumping tariffs until 2007

Export Export MarketMarket

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable & Attractive Stable & Attractive MarginsMargins

Strong Financial PositionStrong Financial Position LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential

______________________________________________________________________________________(1)(1) Calculation method based on data from Customs Department, and Calculation method based on data from Customs Department, and

Iron and Steel Institute of ThailandIron and Steel Institute of Thailand

12HK000IYE

NOT AN OFFER OF SECURITIES

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable & Attractive Stable & Attractive MarginsMargins

Strong Financial PositionStrong Financial Position LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential

Stable and Attractive MarginsStable and Attractive Margins

HRC HRC Spread Spread

AnalysisAnalysis

100

200

300

400

500

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

HRC Selling Price Slab Cost

(US$ per Ton)

Metal Spread (US$ per Ton)High $132Low $51Average $87Current $132

Resilience to economic and steel downturn

Sustainable metal spread even in economic/steel cycle downturn

Resilience to economic and steel downturn

Sustainable metal spread even in economic/steel cycle downturn

Shifting towards premium products

Stable quantity purchased by customers

Premium product is “non-commodity” – prices are less volatile

Ability to secure margin

Shifting towards premium products

Stable quantity purchased by customers

Premium product is “non-commodity” – prices are less volatile

Ability to secure margin

31% 39% 50%

2002 2003 2004

(mm tons)Premium Product as Premium Product as

% of Total Production% of Total Production

Shifting Shifting Towards Towards Premium Premium ProductsProducts

13HK000IYE

NOT AN OFFER OF SECURITIES

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable & Attractive Stable & Attractive MarginsMargins

Strong Financial PositionStrong Financial Position LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential

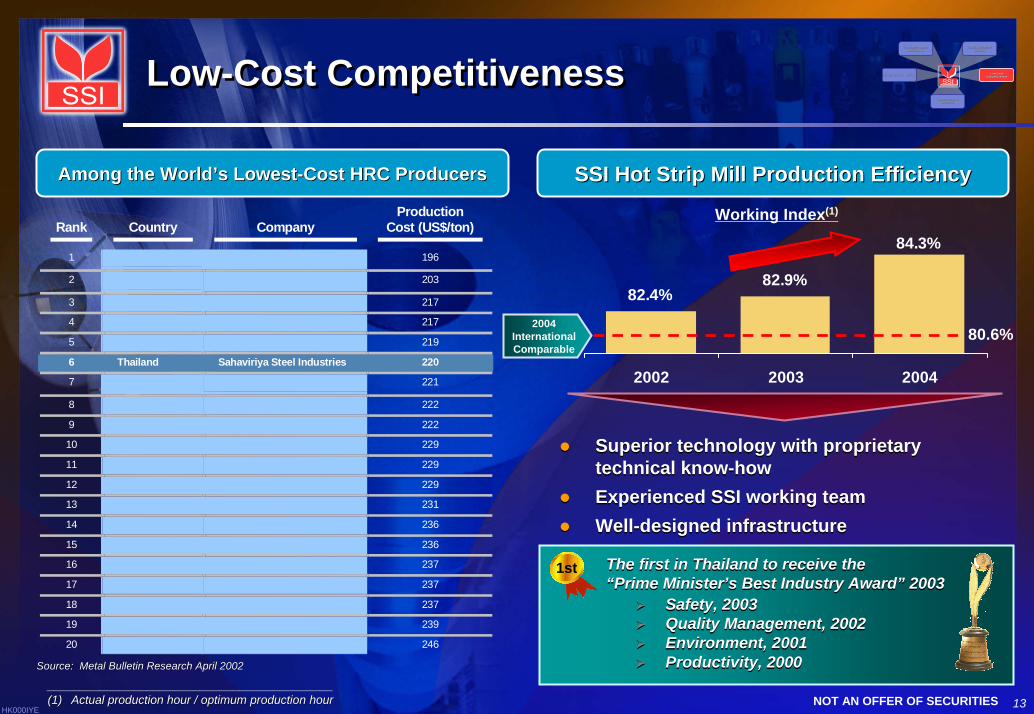

Low-Cost CompetitivenessLow-Cost Competitiveness

Rank Country Company Production

Cost (US$/ton)

1 196

2 203

3 217

4 217

5 219

6 Thailand Sahaviriya Steel Industries 220

7 221

8 222

9 222

10 229

11 229

12 229

13 231

14 236

15 236

16 237

17 237

18 237

19 239

20 246

82.4%82.9%

84.3%

2002 2003 2004

SSI Hot Strip Mill Production EfficiencySSI Hot Strip Mill Production EfficiencyAmong the WorldAmong the World’’s Lowests Lowest--Cost HRC ProducersCost HRC Producers

Superior technology with proprietary technical know-howExperienced SSI working teamWell-designed infrastructure

Superior technology with proprietary technical know-howExperienced SSI working teamWell-designed infrastructure

Working Index(1)

2004International Comparable

______________________________________________________________________________________(1)(1) Actual production hour / optimum production hour Actual production hour / optimum production hour

The first in Thailand to receive the “Prime Minister’s Best Industry Award” 2003

Safety, 2003Quality Management, 2002Environment, 2001Productivity, 2000

The first in Thailand to receive the “Prime Minister’s Best Industry Award” 2003

Safety, 2003Quality Management, 2002Environment, 2001Productivity, 2000

1st

Source: Metal Bulletin Research April 2002Source: Metal Bulletin Research April 2002

80.6%

14HK000IYE

NOT AN OFFER OF SECURITIES

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable & Attractive Stable & Attractive MarginsMargins

Strong Financial PositionStrong Financial Position LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential

Low-Cost Competitiveness (Cont’d)Low-Cost Competitiveness (Cont’d)

Diversified Source of SuppliersDiversified Source of Suppliers Logistical AdvantageLogistical Advantage

3-year average

Europe5%

Other16%

China7%

Brazil18%

Russia40%

Australia14%

BRAZIL

JAPAN

RUSSIA

UKRAINE

IRAN

SOUTH AFRICA

CHINA

GERMANY

ITALY

ALGERIA

AUSTRALIA

S. KOREA

MEXICO

NETHERLANDS

Securing slab suppliers at competitive price

World’s single largest slab buyer

Strong, long-standing relationships with global suppliers around the world

Securing slab suppliers at competitive price

World’s single largest slab buyer

Strong, long-standing relationships with global suppliers around the world

Close proximity between plant and deep-sea port

Ability to dock 2 x 100,000 DWT vessels – potential for expansion to 300,000 DWT

Close proximity between plant and deep-sea port

Ability to dock 2 x 100,000 DWT vessels – potential for expansion to 300,000 DWT

15HK000IYE

NOT AN OFFER OF SECURITIES

Total 56 daysof periodical

plant shutdowns to install new

capacity

Superior Growth PotentialSuperior Growth Potential

Capacity ExpansionCapacity Expansion

1.9 2.0 1.8

2.4 2.4 2.4

3.74.0

2002 2003 2004 2005 2006

Production Capacity

Margin EnhancementMargin Enhancement

0.620.77 0.83

0.07

2002 2003 2004

Premium HRC P/O

Growth in capacity will reach bottom line in 2005Growth in capacity will reach bottom line in 2005 Launched new high valueLaunched new high value--added products added products to command pricingto command pricing

Utilization Utilization RateRate 83% 83% 75%

(mm tons)(mm tons)

HRC P/OUS$657/ton(2)

HRC Premium Grade

US$603/ton(2)

____________________________________________________________________________(1) 11(1) 11--month operating capacity month operating capacity –– resumed production on 3 Feb 2005 after expansion resumed production on 3 Feb 2005 after expansion

shutdown starting 27 Dec 2004 shutdown starting 27 Dec 2004 (2) Average 4Q2004 selling price(2) Average 4Q2004 selling price

Commercial Grade HRC

US$558/ton(2)

1.0 mm tpa HRC P/O Capacity

(1)

2004 Utilization RateNSM: 29%

G Steel: 74%

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable & Attractive Stable & Attractive MarginsMargins

Strong Financial PositionStrong Financial Position LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential

16HK000IYE

NOT AN OFFER OF SECURITIES

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable & Attractive Stable & Attractive MarginsMargins

Strong Financial PositionStrong Financial Position LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential

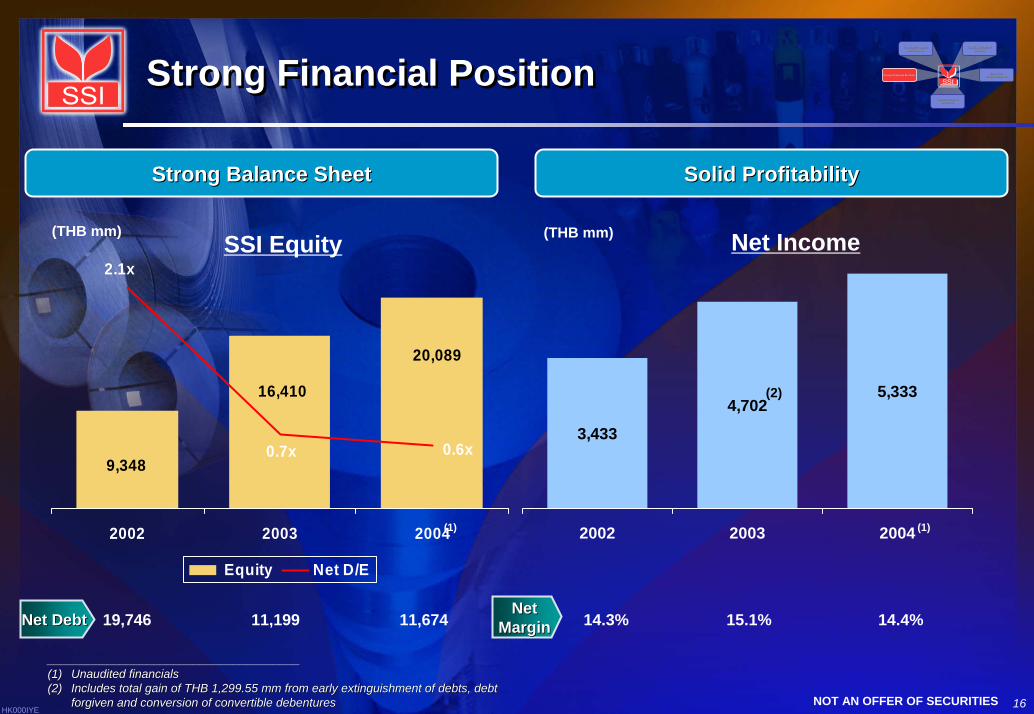

Strong Financial PositionStrong Financial Position

Strong Balance SheetStrong Balance Sheet Solid ProfitabilitySolid Profitability

3,433

4,7025,333

2002 2003 2004

(THB mm)(THB mm) Net IncomeSSI Equity

Net Net MarginMargin 14.3% 15.1% 14.4%

____________________________________________________________________________(1)(1) Unaudited financialsUnaudited financials(2) (2) Includes total gain of THB 1,299.55 mm from early extinguishmentIncludes total gain of THB 1,299.55 mm from early extinguishment of debts, debt of debts, debt

forgiven and conversion of convertible debentures forgiven and conversion of convertible debentures

(1) (1)

(2)

9,348

20,089

16,410

0.6x0.7x

2.1x

2002 2003 2004

Equity Net D/E

Net DebtNet Debt 19,746 11,199 11,674

HK000IYENOT AN OFFER OF SECURITIES

Financial HighlightsFinancial Highlights

18HK000IYE

NOT AN OFFER OF SECURITIES

Demonstrated Financial PerformanceDemonstrated Financial Performance

24,072

31,156

2002 2003 2004

RevenueRevenue EBITDAEBITDA

Operating ProfitOperating Profit Net IncomeNet Income

5,102 4,678

6,474

2002 2003 2004

3,433

4,702 5,333

2002 2003 2004

4,501.0 4,061.0

5,872.0

2002 2003 2004

CAGR: 24.1% CAGR: 12.6%

CAGR: 14.2%CAGR: 24.6%

(THB mm)

(THB mm)

(THB mm)

(THB mm)

Net Net MarginMargin 14.3% 15.1% 14.4%

EBITDA EBITDA MarginMargin 21.2% 15.0% 17.5%

EBIT EBIT MarginMargin 18.7% 13.0% 15.8%

(1) (1)

(1)(1)

____________________________________________________________________________(1)(1) Unaudited financialsUnaudited financials

37,093

19HK000IYE

NOT AN OFFER OF SECURITIES

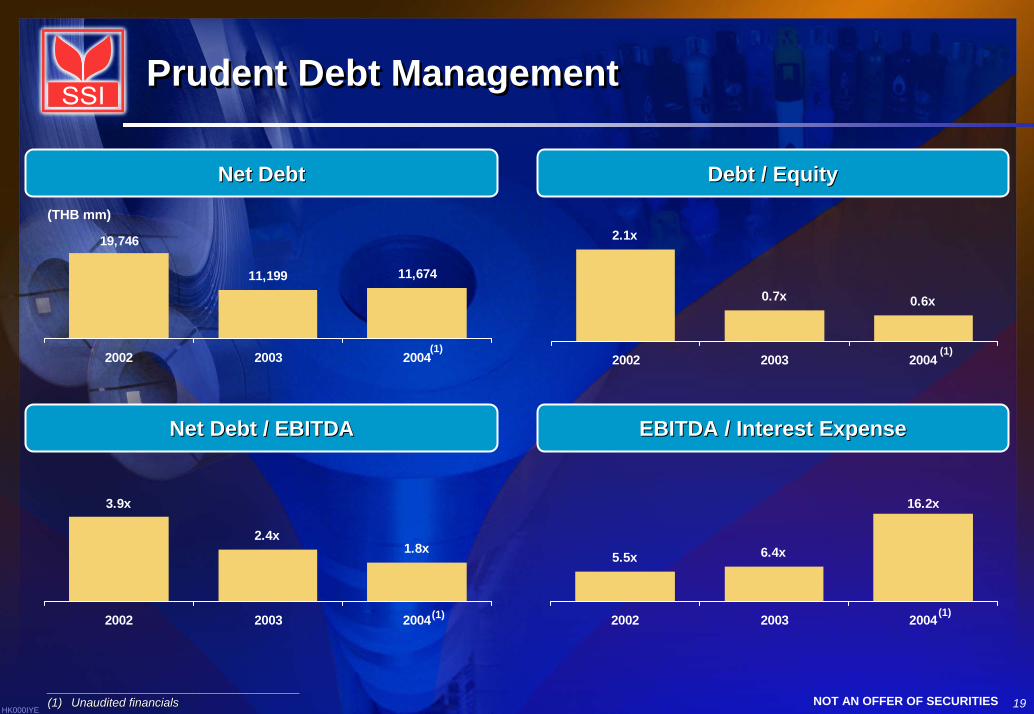

Prudent Debt ManagementPrudent Debt Management

Net DebtNet Debt Debt / EquityDebt / Equity

(THB mm)

0.7x 0.6x

2.1x

2002 2003 2004

19,746

11,199 11,674

2002 2003 2004(1) (1)

Net Debt / EBITDANet Debt / EBITDA EBITDA / Interest ExpenseEBITDA / Interest Expense

5.5x 6.4x

16.2x

2002 2003 2004

3.9x

2.4x1.8x

2002 2003 2004(1) (1)

____________________________________________________________________________(1)(1) Unaudited financialsUnaudited financials

20HK000IYE

NOT AN OFFER OF SECURITIES

590

1,147

4,312

2002 2003 2004

Sustaining Growth: Capacity ExpansionSustaining Growth: Capacity Expansion

HRC capacity increased from 2.4 mm tons to 4.0 mm tons through debottlenecking

Investment cost of ~THB 3,600 mm

Completed in February 2005

HRC capacity increased from 2.4 mm tons to 4.0 mm tons through debottlenecking

Investment cost of ~THB 3,600 mm

Completed in February 2005

Capture future demand growth in domestic market and exports

Lower investment cost per ton –improves ROIC

SSI: $208/tonG-Steel: $400/tonNSM: $260/ton

Capture future demand growth in domestic market and exports

Lower investment cost per ton –improves ROIC

SSI: $208/tonG-Steel: $400/tonNSM: $260/ton

Expansion ProjectExpansion Project CAPEXCAPEX

(THB mm)

(1)

____________________________________________________________________________(1)(1) Unaudited financialsUnaudited financials

Investment in HRC P/O line

Capacity Expansion

21HK000IYE

NOT AN OFFER OF SECURITIES

ConclusionConclusion

Favorable Industry Favorable Industry EnvironmentEnvironment

Stable and Stable and Attractive MarginsAttractive Margins

Strong Financial Strong Financial PositionPosition

LowLow--Cost Cost CompetitivenessCompetitiveness

Superior Growth Superior Growth PotentialPotential