s w wk s w wk - cashewinfo.com 18 issu 15.pdfin ˜ etnam, price of wet raw nuts has fallen from the...

TRANSCRIPT

A Product of

Cashew Market Commentaries from Experts

Indian Cashew Market Commentaries

International Cashew Market Commentaries

Almond Report

Prices of Nuts

Domestic Prices of Nuts

International Prices of Nuts

Currency Movement and Outlook

www.cashewinfo.com

CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK

A WEEKLY NEWSLETTER

In the Cashew Week... (An Exclusive Interview with Mr Jim

Fitzpatrick, Ingredient Sourcing Solutions, at

the World Cashew Convention, 09-11 Feb,

2017, Singapore)

USA Cashew kernel Import-Feb-2017

NewsHighlights

Upcoming Trade Events

|2|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|3|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|4|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|5|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|6|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|7|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Global Cashew Market at a Glance

India

RCN across major Indian markets traded in the region of INR 120 and INR 140 per kg, highest being

observed in Goa. In Maharashtra local industry is finding difficult to buy RCN, although it is available to

traders around INR 120 per kg. The price in Maharashtra is highly volatile. Today RCN quotes at INR

135 and INR 140 per kg.

Cashew kernel prices in the domestic markets ruled mixed during last week. In Mangalore, prices were

a tad higher for broken and split grades, while it was mostly unchanged for whole grades. The same is

the case in Kollam. Vetapalem markets were closed due to labour strike.

Vietnam

In Vietnam, price of wet raw nuts has fallen from the earlier peak of VND 45000 per kg to VND 35,000

per kg (USD1550 per tonne) during last week, as intermittent rains posed challenges to drying.

This year’s Vietnam cashew crop is likely to be short by at least 20-25 percent when compared with

last year’s estimated crop of 360,000 tonnes. Market participants forecast varies vastly. A clear picture

is likely to emerge by the end of this month or as early as first week of May.

Raw cashew nuts from West Africa will arrive in April/early May 2017 and are being quoted as follows:

Cote d’ivoire-48 lbs @$1,870/tonne, for Nigeria-47 lbs @$1,730/tonne, Benin-49 lbs @1900/tonne

and Ghana-49 lbs @2040/tonne ( CFR basis).

USA

The USA has imported 9193 tonnes of cashew kernel in the month of Feb-2017 as against 8278 tonnes

imported in Feb-2016.

In the first two months of 2017, the USA had imported 20,729 tonnes as against 18,421 tonnes

imported during the same period in 2016, reported an increase of 12.5 percent.

West Africa

Benin

After having fixed the raw nut price of 500 FCFA/kg during the 2017 cashew marketing campaign,

President Patrice Talon and his government has adopted new measures in the marketing of cashew

nuts. Last week, at its Council of Ministers meeting on April 6, the Benin government took new

measures in relation to the marketing of raw cashew nuts. First RCN export via land was banned.

Second, a levy of 50 FCFA (0.08 USD) per kg of raw cashew nuts exported was imposed. This is over

and above the existing tax of 10 FCFA / Kg provided by the Finance Law management act on each kg of

raw cashew nuts exported. These new measures could, in the coming weeks, affect prices of raw nuts,

which are already shown a relative decline in the various producing regions.

|8|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

The Minister of State and Secretary General of the Presidency of the Republic, Pascal Irénée Koupaki,

informed that this levy will be collected at the customs before any export is done.

ACA will hold talks with the Benin government, to review impact on its members, especially after Cote

d’Ivoire reforms its policy on RCN exports by road.

While harvesting is gradually being completed in the Zou and Collines areas and continues in the north

of the country, demand has remained stable. Supply has remained fairly high despite the retention of

stocks by some producers. In the Atacora and Donga departments, farm gate prices varied between

500 and 750 FCFA / kg (0.81-1.21 USD), while in the Borgou and Alibori, farm gate prices quoted

between 625 and 800 FCFA / kg (1.01-1.30 USD), a slight decrease of about 50 fcfa compared to

previous week. Warehouse prices, on the other hand, were in the range of 650 and 850 FCFA / kg

(1.05-1.38 USD). As far as the departments of the Zou and Collines, the prices offered by the farmers

were more or less stable with an average of 715 FCFA (1.16 USD) per kg in the various localities. In the

Ouémé and Plateau regions, producer prices showed a slight decrease and were quoted at 700 FCFA /

kg (1.14 USD) and 750 FCFA (1.21 USD) in the warehouses.

Burkina Faso

In Burkina Faso, RCN farm gate prices continued to remain higher. In Cascades and Hauts-Bassins, RCN

farm gate prices were seen stable in the region of 800 and 850 FCFA per kg. In South-West and other

regions, RCN farm gate prices were seen in the region of 750 and 850 FCFA per kg.

Cote d’Ivoire: The cashew arrivals in Abidjan have calmed down in the recent week. Some rumours

are circulating that there is no more stock in the bush. These rumours are just that: rumours. Reports

from major zones have not reported any major shortage. A better explanation is that the crop is not

making its way down to Abidjan as normal. There is more export activity taking place in Bouake than in

the past and the cargo seems to be moving across the borders more easily than the past. Recent rains

in the producing regions have led to slightly lower outturns in Abidjan. As these rains were

intermittent, farmers are expecting a heavy second crop. Arrivals in Abidjan are still hovering around

800-850 FCFA per kg depending on the quality and humidity. It does not seem like the price will drop

anytime soon as many had expected. At this point it is too early to determine anything definitive

about the crop and the bulk of the Ivorian crop should be delivered in this month of April.

RCN farm gate price varies in the region of 600 and 750 FCFA per kg depending on the place and the

quality of the crop.

Ghana

In Ghana, RCN prices continued to remain higher well above GHS 7 per kg, which is equivalent to 1.61

USD per kg. In some places the farm gate prices were close to 8 GHS/kg, which is very risky and may

not sustain at that level. Considering fluctuations in the local currency, central bank intervention in the

forex markets, buyers are unwilling to commit sales at elevated prices.

|9|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Nigeria

In Nigeria, Naira’s continued strength against the dollar has resulted in RCN prices scaling down

considerably. Last week RCN farm gate prices even breached N400 per kg in some places. Port delivery

prices of RCN were seen in the region of N520 and N550 per kg. Cashew marketing season is not so

fruitful for Nigeria due to sharp appreciation in Naira in recent months, especially since February.

Guinea: The Cashew market is mostly active in both Kankan and Boke regions of the country. The RCN

farm gate price continued to remain higher and traded in the region of USD 1.00 and 1.20 per kg

depending on the area and quality. As demand is high, expect RCN price to remain firm.

Currency

Indian rupee overall appreciating tone is set to continue for the time being. The RBI had kept its key

rate unchanged citing inflationary pressures going forward due to uncertainty over monsoon and on

impact on GST implementation.

Brazil real may weaken further towards 3.25 in the near term. Due to softening of inflation, which is at

its lowest since 2010, Brazilian central bank is expected to cut down the interest rates aggressively

going forward.

Source: Cashewinfo.com

The new season is on. As I had mentioned earlier, there has been no good rain in the entire rainy

season. Trees are dry. Therefore local cashew crop can’t be more than 25% in Tamil Nadu. But the

local cashew factory owners were expecting some sort of miracle and almost all of them were waiting

till 1st April to plan imports from African countries. Now the orders have been placed and we expect

raw nuts to arrive by May 2nd week.

CNSL is available at the rate of INR 23 per kg and cashew shells are quoted at around INR 7.90 per kg.

Cake is fetching INR 5.20 per kg. The oil is bought either by furnace oil people or by some distillation

industries. Unless shelling improves, the rates of CNSL and shells won’t decrease.

Source: Om Prakash Phadnis, Panruti

Cashew Market Commentaries from Experts-International

The cashew market over the past week has continued to look softer and there seems to be a change in

sentiment for now.

In West Africa, the only things in short supply in the sector are buyers and money. Small traders and

farmers who held out for higher prices may now find buyers harder to find. If they start to chase the

market as the second crops come in and with rumour of an early harvest in some of the countries

further west buyers may stay away until prices moderate. Processors who now have plenty of stock on

the way have largely resisted the temptation to drop offered kernels prices, but one gets the

impression that any buyer who ventures to put his head over the parapet will be picked off. In this

context the news of some difficulty with the Vietnamese crop has not had much attention. In terms of

fundamentals a short crop in Vietnam does not dramatically change the numbers as Vietnam is far

behind Cote D’Ivoire and India in production terms these days. On the other hand it may have an

|10|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

impact on Vietnamese processors, who will buy in excess of 1 million tonnes imported RCN this year,

sentiment which as we know can be powerful in cashews whatever the fundamentals suggest.

Kernels buyers, many of whom argue that the current prices are unworkable anyway, meantime will

be encouraged by these developments to wait and perhaps continue their hand to mouth approach in

as far as possible.

This season still has much information to give up. It is not yet justified to talk about the crop outcome

anywhere as “fact” but it does seem that misinformation and rumour is on the retreat for now.

Source: Jim Fitzpatrick

The cashew market remains a bit of a roller coaster. The one day sellers are discounting their kernel

prices as they have no demand and buyers are gone, while the next day some demand shows up for

limited quantities and prices immediately increase a couple of cents again.

Raw Cashew Nut (RCN) demand is almost as volatile, whereas there are a lot of rumours that impact

the sentiment in the market.

The facts (and rumours) at the moment are as follows:

1)The crops in West Africa are reported be good with the biggest producer Cote d ‘ivoire likely to

report a crop of over 800.000 tonnes of RCN – rumour.

Fact may be the crop comes in somewhat lower on volume and quality due to rain damage.

2) The crop in Guinea Bissau is 3-4 weeks earlier, so shipments from this producing origin are expected

to start during April/May – fact.

Demand is high and price may hit all-time highs.

3) Prices of raw seeds have eased a bit in various origins in Africa and are now stable – fact.

4) The Vietnamese and Cambodian crops are questionable both in terms of volume and quality. They

are definitely less in volume compared to last year and quality is a reason for concern in some areas –

fact.

This is having a negative impact on the supply for very short term and supply of RCN to the processors

will only reach some sort of saturation point till the shipments from West Africa will come in

significant quantities - fact.

5) The prices of kernels are moving on demand at the moment as written above - fact.

6) Most buyers are covered until May and will be in the market with new inquiries for June 2017

onwards – fact or rumour?

7) Most buyers are expecting prices to ease from June/July onwards – fact….but will this happen?

|11|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Keeping all the facts in mind, our expectation is that prices will remain firm probably slightly longer

than earlier anticipated because of the crop issues in Vietnam/Cambodia, but that generally prices will

come down during the 2nd half of 2017 when enough raw seeds from West Africa will arrive in India

and Vietnam. We do not expect prices to fall below Usd 4 per lbs (for WW320) again, but it will be

between Usd 4.15 and 4.50 per lbs (for WW320).

Our recommendation is therefore to be covered until July/August and be patient a bit for later

shipment positions.

Source: Kees, Global Trading Agency, The Netherlands

Vietnam

Constantly negative news of the poor crop has been told in the market and in fact this year’s Vietnam

crop would be down by about 30-35% in comparison with last year crop, due to abnormal whether

condition. Earlier expectation was that of a good crop, which was observed by experts here, but things

turned out to be otherwise. Based on the above mentioned circumstances the raw seed market

continued to be firm during the week. A lot of imported cargoes have reached to HCM city and afloat

cargoes are on the way to Vietnam ports, which means from end of April onwards processors could

have enough RCN to process.

Weak demands from kernels market as most buyers had covered for April shipment. From May – Aug

offers, buyers could only consider to pick up the offers if the prices are workable to them. W320 is

traded at Usd 4.55/4.65 per lb Fob for April shipments, sold by medium reliable packers. Demand for

W240 is weak and no buying interests shown for this grade for the time being, the gap between the

W240 and W320 should be established soon. W240 is being offered at Usd 5.30/5.35, W320 at Usd

4.65/4.75, W450 at Usd 4.50, Ws at Usd 3.65/3.75 and Lp at Usd 3.20/3.25 per lb fob for May – Aug

shipments.

Source: Mr. Kim, Khiem Nguyen Co., Ltd, Vietnam

Gambia

Stocks from North bank in The Gambia have started coming and the local prices in Banjul are anything

ranging between 77 ando 80 GMD per kg; in Sokone about CFA950 per kg. The cost of a Shipper at

C&F position will be about $2,000 per tonne. A few Shippers have signed contracts between $1950

and $2,100 depending on payment terms. Shipments will begin from The Gambia next week onwards.

It is just the onset of the the season - We will have more clarity from the 15th of April. Gambia and

Senegal have a good Relationship, so border issues are things of the past. Bumper crop is anticipated

and more over crop was early by two weeks.

Ziguinchor - The Cargo is yet to come but will begin by the 25th of April. Imports of Jute bags and

setting up of Stores are happening right now.

Bissau - Farm Gate prices have been fixed at CFA 500 per kg. Taxes and freight are supposed to be

higher than last year.

A lot of changes and restrictions to protect Local Guineas are being implicitly introduced.

|12|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

As usual everyone is kept guessing on the tax structure and export Licenses. Export licenses will be

given to people only to those who have Investments in the country. They should have a 12 month

operation in Guinea and have been operating for at least 5 years and being in order all other Rules of

the land.

Sales have happened on advance basis between $1700 ando $1900 per tonne on C&F Basis.

Source: Amrith Kurien, Comafrique

It has been nearly three weeks since the Vietnam new crop starts. Many factories have already

purchased some new crop for processing. Supplements from Vietnam are stronger than last month,

while kernel prices become stable. WW240 at 11.30-11.50 usd/kg,WW320 at 10.60-

10.80usd/kg,WW450 at 10.30-10.50usd/kg. Due to the high price of RCN, we think the price will

remain stable for a while, although the demand is weak in Chinese markets.

Source: Will Lee, China

Please visit www.cashewinfo.com for weather report

Fig 1: Cashew Kernel- W320- Average FOB prices at Tuticorin port, India (USD/lb)

|13|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

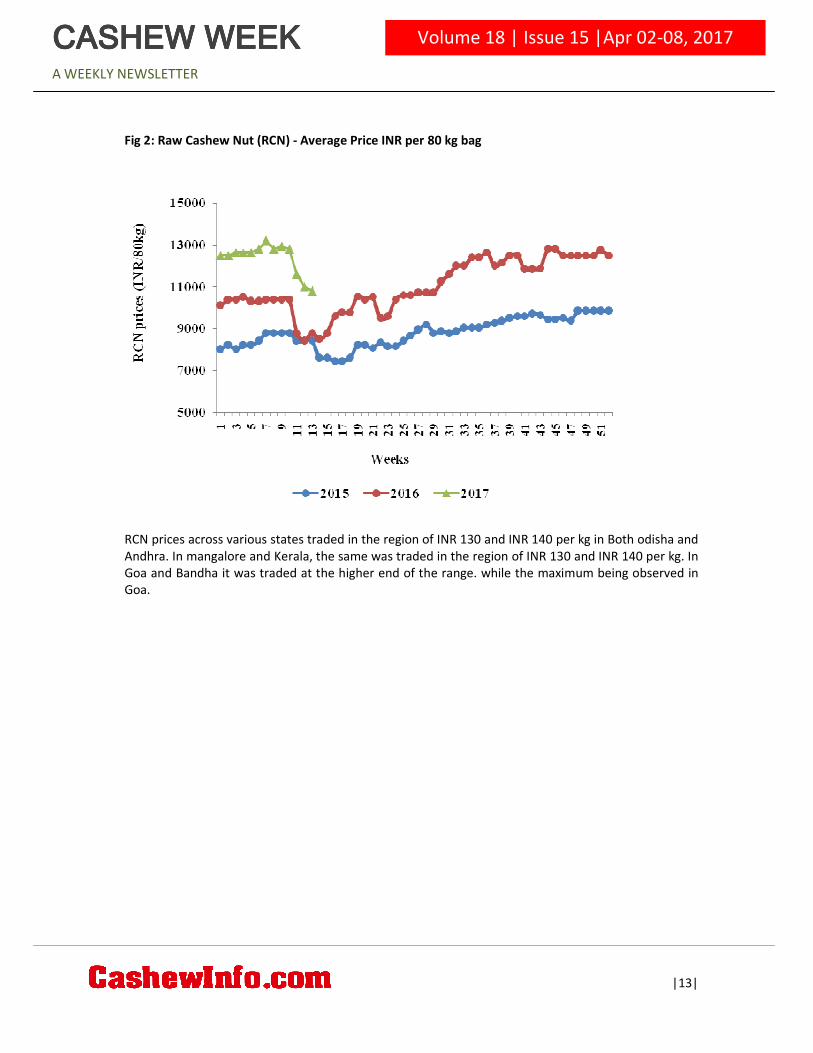

Fig 2: Raw Cashew Nut (RCN) - Average Price INR per 80 kg bag

RCN prices across various states traded in the region of INR 130 and INR 140 per kg in Both odisha and

Andhra. In mangalore and Kerala, the same was traded in the region of INR 130 and INR 140 per kg. In

Goa and Bandha it was traded at the higher end of the range. while the maximum being observed in

Goa.

|14|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|15|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Almond and other tree nuts report

The market in Delhi (India's) Khari Baoli Market for Dry Fruits and Nuts during last week closed (April

08-2017)for trading of Almonds at INR 16800-17000/40 Kg for 70% Sliding Scale Basis ( private

Packers, equivalent to $2.40-42/lb of Origin's CIF prices). BD is still commanding a premium and closed

last week at INR 17200-300/40 kg, While FAQ kernels were traded at INR 595-600/kg and Hand

Picked/Fancy at INR 605-610/kg.

USDINR closed last week at INR 64.28. Indian Currency has been volatile and strong with signs of

further appreciation in the coming days, though at the moment exporters were suffering due to strong

appreciation of rupee in the last two months.

Demand for Kernels and In Shell's has also been very low during the first week of FY 2017 as against

the last week. Traders were desperately waiting for some good news from California through the

TNT's (Terra Nova Trading) first estimate report, but the report came very positive on the crop

estimate for 2017 with an estimate of 2270 Million Lbs. This figure is largely due to excellent weather

and on increased and corrected acreage. Further it is estimated by TNT that the Non Pareil crop would

be around 850 Million (37.5%), Independence variety will also make a decent impression in the overall

mix of acceptance due to its high availability.

Post the TNT's estimate markets in California have shown signs of weakness and prices have slides

down by over 10 cents for NP In shell. The prices being offered from California are in the range of 2.43

and 2.46$/lbs for Current shipments, it was down from 2.56 to 2.60$/lbs on CIF basis, with new crop

offers in the range of $ 2.30 and 2.32/lbs on FAS Basis. This has also taken the HK/Dubai markets by

surprise and they will now have to liquidate their inventories very fast at prices better than USA.

Source: Ravinder Mehta, IFNO, New Delhi - India

|16|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Almond Price Chart

Almond kernel Californai prices had traded at Delhi settled last week unchanged at INR 603 per kg as

California market report surprised the markets with good crop prospects as well as the first week of

new fiancial year 2017-18. Similarly cashew W320 traded at Delhi, settled unchanged at INR 795 per

kg.

|17|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|18|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|19|

Volume 18 | Issue 15 |Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

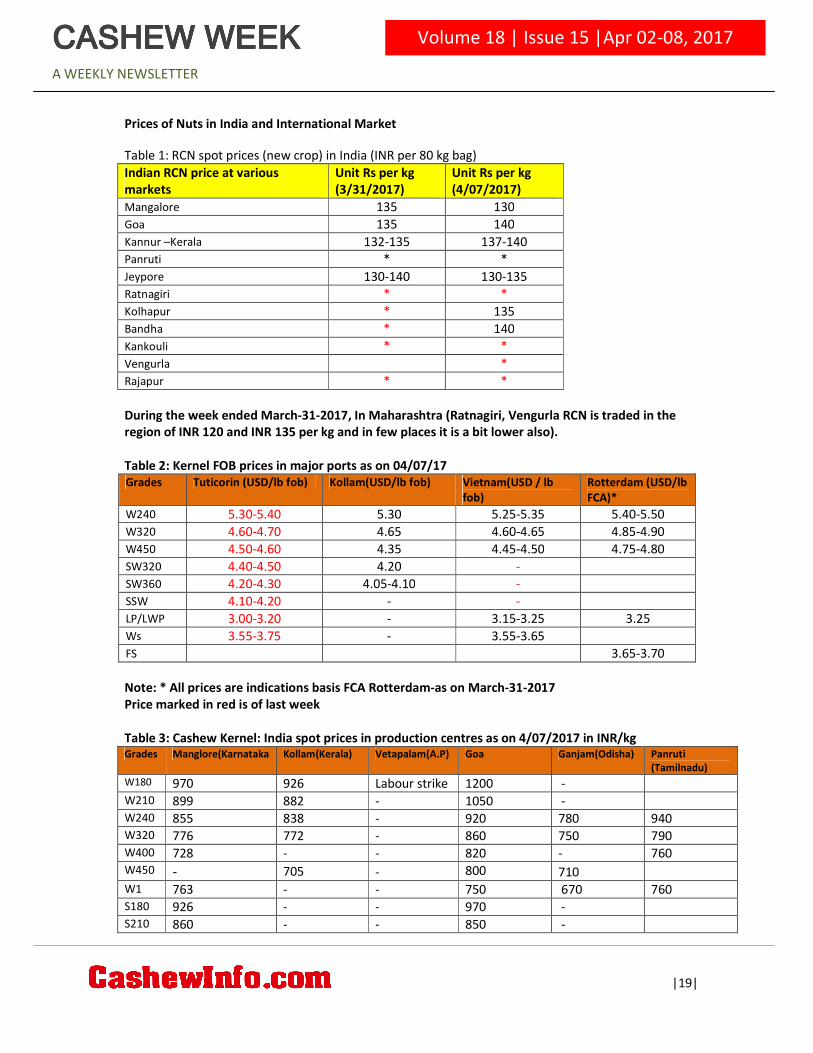

Prices of Nuts in India and International Market

Table 1: RCN spot prices (new crop) in India (INR per 80 kg bag)

Indian RCN price at various

markets

Unit Rs per kg

(3/31/2017)

Unit Rs per kg

(4/07/2017)

Mangalore 135 130

Goa 135 140

Kannur –Kerala 132-135 137-140

Panruti * *

Jeypore 130-140 130-135

Ratnagiri * *

Kolhapur * 135

Bandha * 140

Kankouli * *

Vengurla *

Rajapur * *

During the week ended March-31-2017, In Maharashtra (Ratnagiri, Vengurla RCN is traded in the

region of INR 120 and INR 135 per kg and in few places it is a bit lower also).

Table 2: Kernel FOB prices in major ports as on 04/07/17

Grades Tuticorin (USD/lb fob) Kollam(USD/lb fob) Vietnam(USD / lb

fob)

Rotterdam (USD/lb

FCA)*

W240 5.30-5.40 5.30 5.25-5.35 5.40-5.50

W320 4.60-4.70 4.65 4.60-4.65 4.85-4.90

W450 4.50-4.60 4.35 4.45-4.50 4.75-4.80

SW320 4.40-4.50 4.20 -

SW360 4.20-4.30 4.05-4.10 -

SSW 4.10-4.20 - -

LP/LWP 3.00-3.20 - 3.15-3.25 3.25

Ws 3.55-3.75 - 3.55-3.65

FS 3.65-3.70

Note: * All prices are indications basis FCA Rotterdam-as on March-31-2017

Price marked in red is of last week

Table 3: Cashew Kernel: India spot prices in production centres as on 4/07/2017 in INR/kg Grades Manglore(Karnataka Kollam(Kerala) Vetapalam(A.P) Goa Ganjam(Odisha) Panruti

(Tamilnadu)

W180 970 926 Labour strike 1200 -

W210 899 882 - 1050 -

W240 855 838 - 920 780 940

W320 776 772 - 860 750 790

W400 728 - - 820 - 760

W450 - 705 - 800 710

W1 763 - - 750 670 760

S180 926 - - 970 -

S210 860 - - 850 -

|20|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

S240 820 750 - 800 -

S 745 728 - 780 -

LWP 661 683 - 720 650 710

SWP 635 573 - 640 630 610

K 688 692 - 740 - 670

JH 758 728 - 800 690 710

SSW 732 617 - 730 -

BB 529 683 - 520 520

JK/JB 723 - - 760 -

SW 714 - 780 -

Prices of Nuts in Other Indian Markets

TABLE 4: Cashew kernel: India spot prices at terminal markets as on 4/07/2017 in INR/kg

Grades Delhi Sangrur(Punjab) Jalandhar(Punjab) Kolaphur(Maharastra) Mumbai

W180 1075 1015 890 1060 1050

W210 945 955 865 960 940-950

W240 895 915 790 900 875-880

W320 795 885 825 800 810-820

W400 - - - - 760

S 730 775 - 730 780

LWP 725 705 - 750 720

SWP 630 627.5 - 650 650

Currency Movement Forex rates in USD

Currency 3/31/2017 4/07/2017

Indian Rupee (INR)RBI ref rate 64.84 64.39

Euro (EUR) 1.07 1.06

Japanese Yen (JPY) 111.40 111.10

Brazilian Real (BRL) 3.12 3.15

Chinese Yuan (CNY) 6.89 6.90

Singapore Dollar (SGD) 1.40 1.40

Tanzanian Shilling (TZS) 2234.90 2233.75

Thai Baht (THB) 34.38 34.61

Mozambique New Metical (MZN) 67.90 66.67

Vietnam Dong (VND) 22755.00 22660.00

Indonesian Rupiah (IDR) 13328.00 13342.00

Benin CFA Franc BCEAO (XOF) 613.50 619.00

Ghanaian New Cedi (GHS) 4.30 4.21

|21|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

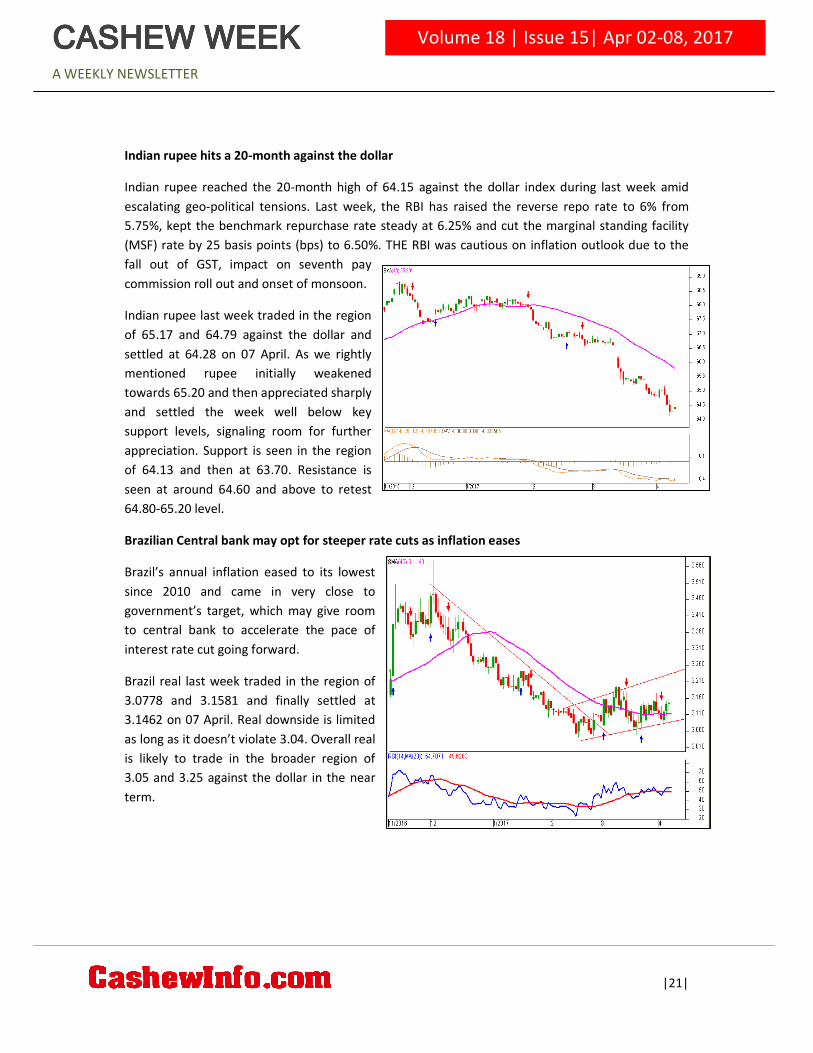

Indian rupee hits a 20-month against the dollar

Indian rupee reached the 20-month high of 64.15 against the dollar index during last week amid

escalating geo-political tensions. Last week, the RBI has raised the reverse repo rate to 6% from

5.75%, kept the benchmark repurchase rate steady at 6.25% and cut the marginal standing facility

(MSF) rate by 25 basis points (bps) to 6.50%. THE RBI was cautious on inflation outlook due to the

fall out of GST, impact on seventh pay

commission roll out and onset of monsoon.

Indian rupee last week traded in the region

of 65.17 and 64.79 against the dollar and

settled at 64.28 on 07 April. As we rightly

mentioned rupee initially weakened

towards 65.20 and then appreciated sharply

and settled the week well below key

support levels, signaling room for further

appreciation. Support is seen in the region

of 64.13 and then at 63.70. Resistance is

seen at around 64.60 and above to retest

64.80-65.20 level.

Brazilian Central bank may opt for steeper rate cuts as inflation eases

Brazil’s annual inflation eased to its lowest

since 2010 and came in very close to

government’s target, which may give room

to central bank to accelerate the pace of

interest rate cut going forward.

Brazil real last week traded in the region of

3.0778 and 3.1581 and finally settled at

3.1462 on 07 April. Real downside is limited

as long as it doesn’t violate 3.04. Overall real

is likely to trade in the broader region of

3.05 and 3.25 against the dollar in the near

term.

|22|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

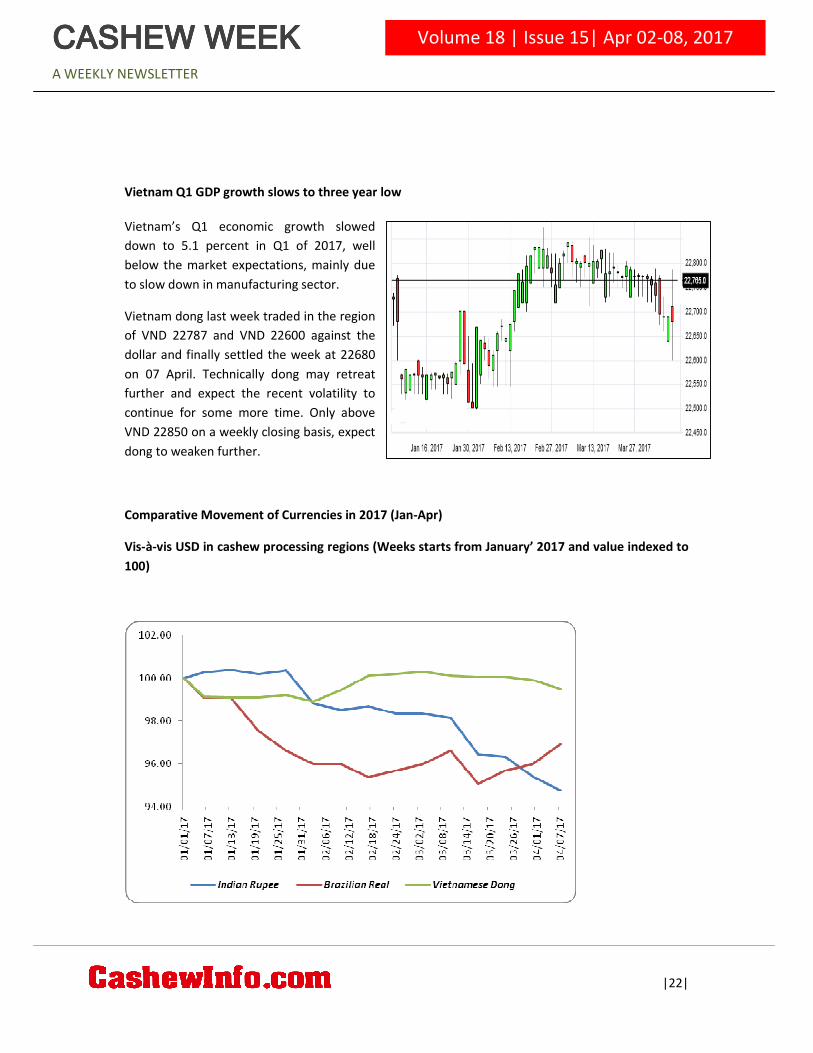

Vietnam Q1 GDP growth slows to three year low

Vietnam’s Q1 economic growth slowed

down to 5.1 percent in Q1 of 2017, well

below the market expectations, mainly due

to slow down in manufacturing sector.

Vietnam dong last week traded in the region

of VND 22787 and VND 22600 against the

dollar and finally settled the week at 22680

on 07 April. Technically dong may retreat

further and expect the recent volatility to

continue for some more time. Only above

VND 22850 on a weekly closing basis, expect

dong to weaken further.

Comparative Movement of Currencies in 2017 (Jan-Apr)

Vis-à-vis USD in cashew processing regions (Weeks starts from January’ 2017 and value indexed to

100)

|23|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

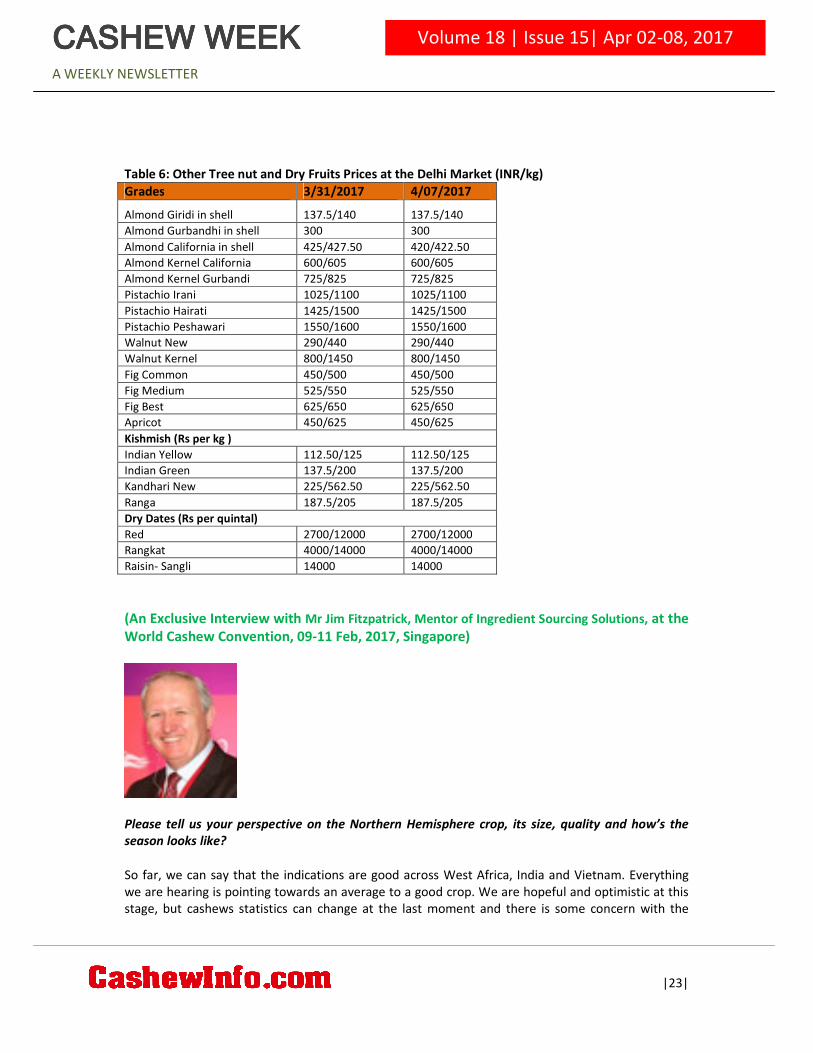

Table 6: Other Tree nut and Dry Fruits Prices at the Delhi Market (INR/kg)

Grades 3/31/2017 4/07/2017

Almond Giridi in shell 137.5/140 137.5/140

Almond Gurbandhi in shell 300 300

Almond California in shell 425/427.50 420/422.50

Almond Kernel California 600/605 600/605

Almond Kernel Gurbandi 725/825 725/825

Pistachio Irani 1025/1100 1025/1100

Pistachio Hairati 1425/1500 1425/1500

Pistachio Peshawari 1550/1600 1550/1600

Walnut New 290/440 290/440

Walnut Kernel 800/1450 800/1450

Fig Common 450/500 450/500

Fig Medium 525/550 525/550

Fig Best 625/650 625/650

Apricot 450/625 450/625

Kishmish (Rs per kg )

Indian Yellow 112.50/125 112.50/125

Indian Green 137.5/200 137.5/200

Kandhari New 225/562.50 225/562.50

Ranga 187.5/205 187.5/205

Dry Dates (Rs per quintal)

Red 2700/12000 2700/12000

Rangkat 4000/14000 4000/14000

Raisin- Sangli 14000 14000

(An Exclusive Interview with Mr Jim Fitzpatrick, Mentor of Ingredient Sourcing Solutions, at the

World Cashew Convention, 09-11 Feb, 2017, Singapore)

Please tell us your perspective on the Northern Hemisphere crop, its size, quality and how’s the

season looks like?

So far, we can say that the indications are good across West Africa, India and Vietnam. Everything

we are hearing is pointing towards an average to a good crop. We are hopeful and optimistic at this

stage, but cashews statistics can change at the last moment and there is some concern with the

|24|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

timing of the crop in Vietnam. I feel that we will have better crop than last year that will be a little

above than that of 2016. Again, it’s very early to make predictions.

The prices of RCN are continuously increasing. Do you foresee the same trend to continue even in

the new season? How is it going to impact the global cashew consumption?

I think the high prices of RCN had a shocker effect on the global processors and buyers of the kernel

throughout the sector. We saw prices rising sharply towards the end of the year that has been

sustained so far surprisingly. I feel there are some stocks unsold at this point of time. RCN market is

very constrained. Prices need to ease some more. We are looking for better crop from the Northern

Hemisphere. Hence it must impact on the price.

At the same time last year in Dubai, we were seeing things in a very similar manner. Tanzanian RCN

were at 2200 USD. I don’t think it’s sustainable as there are unsold stocks at the destination in the

East African countries and we have West African crop coming up. Hence, I feel, prices are going to

ease up a bit but am not expecting a collapse in price. Markets will ease down due to harvest

pressure. The prices might improve later in the month of June and going forward.

Coming to kernels, we have seen prices rising sharply throughout last year. In the last quarter, it was

dynamic explosive price which on the basis of supply and demand at the moment was unwarranted.

This has pressurized processors which is not good for the market. Volatility generally is not good for

business.

Consumption needs a little bit longer for higher prices to impact globally. If super markets, roasters

and processors are going to plan forward they are going to take a conservative approach. They

aren’t going to promote the product at this point of time. We are seeing kernel prices at the top end

range. In 2016, we saw all time high prices in RCN, cashew kernels and this don’t build confidence on

buyers. So here we are at a time where the consumers are very well disposed to order the product

and we are offering him high prices, volatility, uncertainty of supply and that is going to have an

effect on consumption if it continues for a longer time. 2017 might be a year, where we can witness

some impact in Europe. We have a lot of uncertainties throughout the world. Added to that these

high prices and the possibility of variability no one wants to commit to buying kernels at 5 pounds, in

market which could easily go back to 4 and thus it has an impact.

Now that the cashews aren’t the cheapest of all nuts, what’s its impact on the consumption of

other nuts? Do you see a shift in demand from cashews to other nuts?

First according to me there is no better nut for snacking, for sweets, for food usage than cashews. I

don’t believe almonds in terms of overall usage of these segments will ever come closer to cashews.

In the longer run, there is an upward pressure on the pricing for almonds as well that these prices

can come closer together. Now, it’s very easy for a consumer to reduce his cashew usage and

increase his almonds as almonds have a lot of scientifically proven health characteristics. Even

cashews have the characteristic, but we don’t have the proof. Almonds are much better marketed.

80% of almonds comes from California and brilliantly marketed. Within the cashew sector, to avoid

this insignificant threat, we do have to improve our game in terms of marketing, research and

promotion of our product.

What has been the consumption pattern of cashews in US and Europe?

|25|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Well, in recent years it’s been all good news. European consumption has started rising quickly and

US started showing dramatic growth in 2015 and a little bit of a correction in 2016, as a combination

of uncertainty, higher prices, high imports in 2015. Overall in those three major consuming areas-

North America, Europe and India - demand remains positive. Greater consumption in India is

because of wider spread, more affluence, more people interested in buying the products. In Europe,

it’s about health, as an alternative to add-in proteins instead of red meat. In US, it’s more on

snacking, health benefits. I believe the conditions are good for further growth. What can disrupt it,

its volatility and price? We should also consider risks are involved in the sector in terms of how the

consumer sees us. We need to look at working conditions in factories and food safety. These are

areas where at any moment if something goes wrong, we can have a devastating impact. According

to me, for the cashew sector the only way is UP! But it’s up to us as how to manage the sector’s

growth and sustain it over a long term.

Could you please elaborate on the FSMA act?

All of us need to be more serious on quality, quality management and systematized quality

management. Food Safety Modernization Act (FSMA) comes at a time, when the United States is

looking more and more like a country that’s very careful about the products it imports and this is

likely to be very seriously implemented. To some extent, in the domestic market cashews are going

to compete with the domestically produced almonds. In terms of FSMA, processors now need to

build relationship with their buyers, they need to work together to improve quality, start food safety

programmes concepts like ISO certification and other quarantine measures in serious real way.

There has been a number of certifications which is a photocopy of certificates and nothing more.

That’s not food safety that’s just playing games with the system. That will not work under this kind

of legislation. It’s been shown; companies providing better quality under the norms of food safety

with certifications are achieving better prices. At the moment, it will cost you more money on the

product, but in the future it’s a requirement. If you don’t have those certifications, you cannot

export.

Message for the delegates of WCC 2017

Great venue, great time, I see double the participants than the last time around in Dubai. Though we

talk together, we don’t work together as we couldn’t say we have an integrated sector. I think, your

idea at Cashewinfo is a forum for Vision 2025 and we can see a group of people from around the

world coming together to work on it. Though it might have conflicting views, opinions, different

ways of looking at things, the idea coming out for betterment is itself a major success. At the same

time, it is so nice to see so many people from different countries coming together having only one

thing in common- “cashews”. This is the most difficult product that somehow so many people make

a living out of, at least, millions of those farmers around the world who grow it.

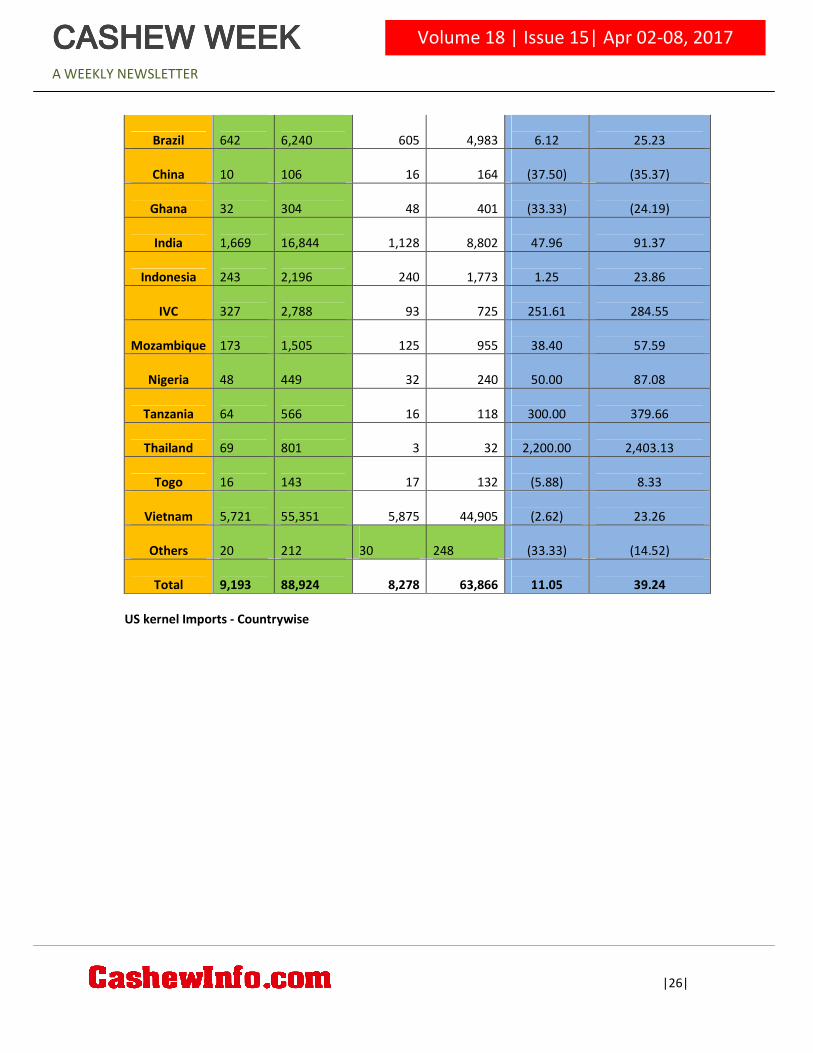

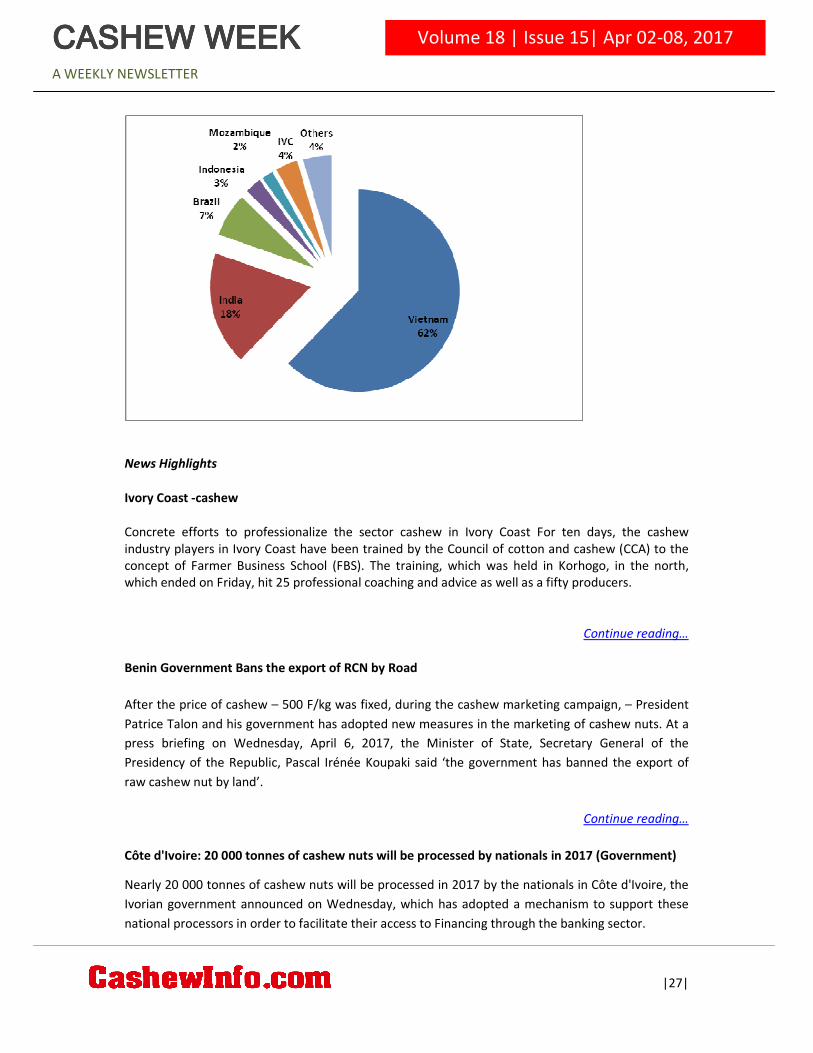

US Cashew Kernel Import Data – Feb-2017

Source wise import of Cashew Kernels into US -Feb-2017 vs Feb-2016

Country Of

Origin

Feb-17 Feb-16 Change in % (Feb-17 vs Feb-16)

Qty

(tons)

Value(1000

USD) Qty (tons)

Value(1000

USD) Qty (tons) Value(1000 USD)

Benin

159

1,419 50 388

218.00

265.72

|26|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Brazil

642

6,240 605 4,983

6.12

25.23

China

10

106 16 164

(37.50)

(35.37)

Ghana

32

304 48 401

(33.33)

(24.19)

India

1,669

16,844 1,128 8,802

47.96

91.37

Indonesia

243

2,196 240 1,773

1.25

23.86

IVC

327

2,788 93 725

251.61

284.55

Mozambique

173

1,505 125 955

38.40

57.59

Nigeria

48

449 32 240

50.00

87.08

Tanzania

64

566 16 118

300.00

379.66

Thailand

69

801 3 32

2,200.00

2,403.13

Togo

16

143 17 132

(5.88)

8.33

Vietnam

5,721

55,351 5,875 44,905

(2.62)

23.26

Others

20

212

30

248

(33.33)

(14.52)

Total

9,193

88,924 8,278 63,866

11.05

39.24

US kernel Imports - Countrywise

|27|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

News Highlights

Ivory Coast -cashew

Concrete efforts to professionalize the sector cashew in Ivory Coast For ten days, the cashew

industry players in Ivory Coast have been trained by the Council of cotton and cashew (CCA) to the

concept of Farmer Business School (FBS). The training, which was held in Korhogo, in the north,

which ended on Friday, hit 25 professional coaching and advice as well as a fifty producers.

Continue reading…

Benin Government Bans the export of RCN by Road

After the price of cashew – 500 F/kg was fixed, during the cashew marketing campaign, – President

Patrice Talon and his government has adopted new measures in the marketing of cashew nuts. At a

press briefing on Wednesday, April 6, 2017, the Minister of State, Secretary General of the

Presidency of the Republic, Pascal Irénée Koupaki said ‘the government has banned the export of

raw cashew nut by land’.

Continue reading…

Côte d'Ivoire: 20 000 tonnes of cashew nuts will be processed by nationals in 2017 (Government)

Nearly 20 000 tonnes of cashew nuts will be processed in 2017 by the nationals in Côte d'Ivoire, the

Ivorian government announced on Wednesday, which has adopted a mechanism to support these

national processors in order to facilitate their access to Financing through the banking sector.

|28|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Continue reading…

Benin: Tolaro Global: A loan of $50,000 helps to add value and jobs to the local economy by

starting a new factory to roast and pack cashew nuts.

Tolaro Global is a cashew nut processing business based in the outskirts of Parakou, a small town in

Northern Benin. Founded in 2010 by Jace (from the US) and Serge (from Benin), Tolaro sources raw

cashew nuts directly from local farmers and transforms them into processed cashew kernels for

export.

Continue reading…

Almond board to spend $4.7 million for grower efficiency

The Almond Board of California is continuing an effort to show that growers are good environmental

stewards by setting aside $4.7 million for research into irrigation efficiency, dust reduction and other

innovations.

Continue reading…

American pistachio industry on record-setting pace

The last two years was a tale of extremes for the American pistachio industry. What was by most

accounts a “crop failure” in 2015 was followed in 2016 by production more than three times the

amount and nearly twice the previous all-time record. Perhaps such a record – over 903 million

pounds of pistachios were harvested in California, Arizona and New Mexico in late 2016 – is fitting

for an industry organization celebrating its 10th anniversary, though it wasn’t just total production

the American Pistachio Growers (APG) had cause to celebrate at its annual conference held in

February in Palm Desert, Calif.

Continue reading…

|29|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|30|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|31|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|32|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

Are you planning to invest in new processing factory or modernize existing cashew processing

factory in India?

Cashew cultivation is expanding into new areas in India. Cashew processing too is being taken up in

non-traditional areas. Entrepreneurs face several questions when starting a new project, such as,

which technology to choose, what should be the scale, should we choose manual vs. semi-automatic

vs. fully automatic processing lines and where to set up the plant, what is the demand in my region

and what is the forecast and what are the risks in investing and so on.

The consulting arm of Cashewinfo.com would be happy to assist businesses in conducting Techno-

Economic Feasibility studies for either establishing a new factory or modernizing an existing factory.

Let us know your requirements, we would provide you with best advice. It is wise to talk to us before

investing your money.

Please write to [email protected] or talk to Swapna at +91 93428 40609

Event Name Date of Event City / Country

INC World Congress on

Nuts and Dried Fruits

19th - 21st May 2017

Chennai,

India

WAPA-Western Agricultural

Processors Association

2017-Annual Meeting 14th -16th June-2017 California

11th

ACA Conference 18th

- 21st

September-2017

Cotonou,

Benin

|34|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

|35|

Volume 18 | Issue 15| Apr 02-08, 2017 CASHEW WEEK CASHEW WEEK CASHEW WEEK CASHEW WEEK A WEEKLY NEWSLETTER

"Do you have an interesting story to share with us on cashew value chain (in your region/country),

innovation, processing, technology, financing or any topic related to cashew industry? If yes, write

REACH OUT

TO

GLOBAL CASHEW INDUSTRY

ADVERTISE IN

CASHEW WEEK & WWW.CASHEWINFO.COM

For Advertisement in Cashew Week

&

Banner Space on www.cashewinfo.com

CONTACT: [email protected]

Disclaimer: The data and information presented in this report are based on efforts of analysts at Foretell Business Solutions Private

Limited, Bangalore and opinions and data obtained from experts and various industry sources. While sufficient care has been taken to

check data and information prior to publishing, Foretell or its employees or external contributors will not be responsible for any kind of

errors or omissions or misrepresentation of data or for losses incurred by any party either directly or indirectly based on the information

published herein.

Caution to Readers

Although paid advertisements appear in this publication (in print, online, or in other electronic formats), Foretell Business

Solutions Private Limited (the owner of cashewinfo.com) does not endorse the advertised product, service, or company, or

any of the claims made by the advertisement. Readers are encouraged to do the necessary due diligence. However, in the

interest of the industry, please share your concerns, if any, by writing to us at [email protected]