russia, the persian gulf, and world oil...

TRANSCRIPT

Russia, the Persian Gulf, Russia, the Persian Gulf, and World Oil Supplyand World Oil Supply

Mikhail KhodorkovskyWashington, 7 February 2003

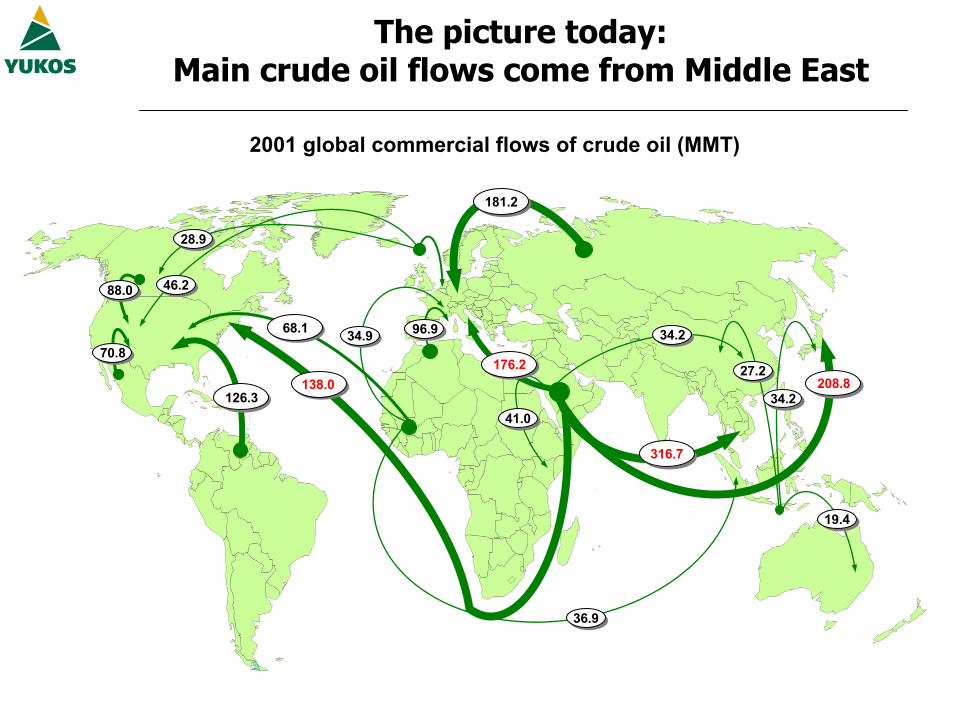

138.0

181.2

126.3208.8

176.2

36.9

68.1

88.0

70.827.2

316.7

46.2

28.9

34.9 34.296.9

19.4

34.241.0

2001 global commercial flows of crude oil (MMT)

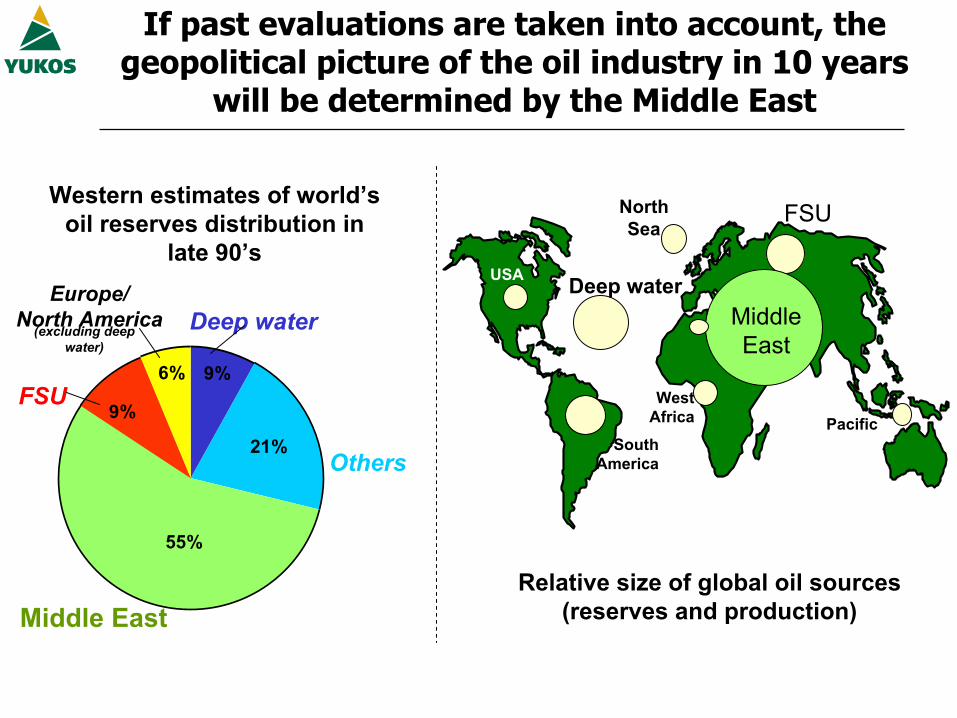

The picture today:Main crude oil flows come from Middle East

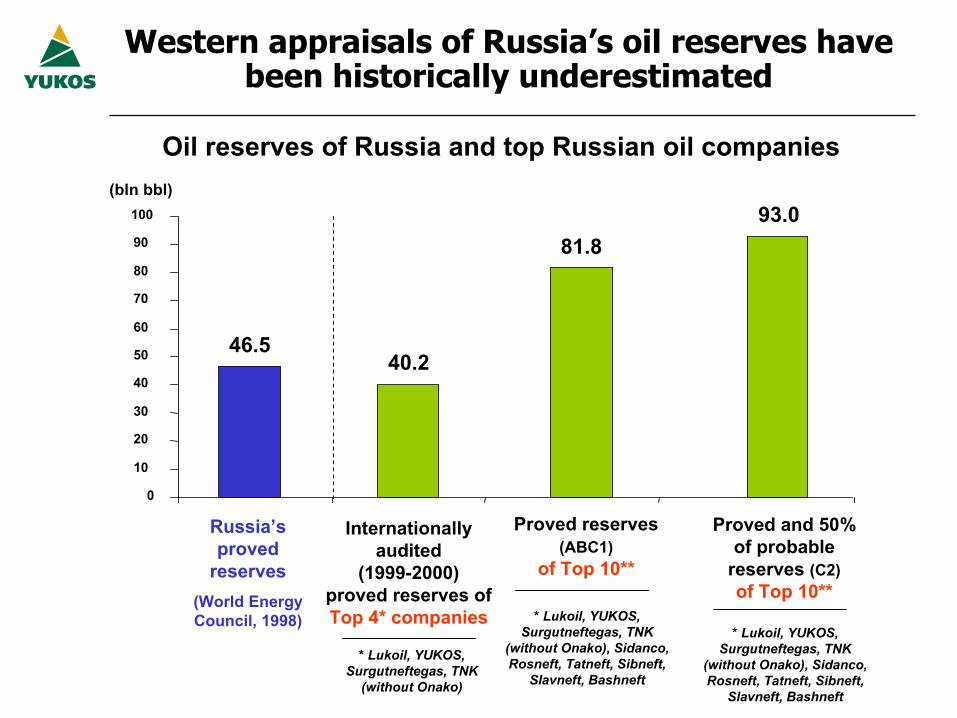

The West has begun to recognize that Russia’s oil reserves are much greater than previously thought

46.5 40.2

Internationally audited reserves of just a few top companies have demonstrated that Western appraisals of Russia’s oil reserves have

been historically underestimated

bln bblbln bbl

* Lukoil, YUKOS, Surgutneftegas,TNK (without Onako)

Internationally audited (1999-2000) proved reserves of Top 4*

companies

Russia’s proved

reserves(World Energy Council, 1998)

Russian oil industry has internal resources to finance production growth at lower than expected cost

Oil industry production increase

Oil industryCAPEX increase

+ 0.5 + $4.4 bln

8,800

CAPEX necessary to increase production

($ per bpd)

20,000

ActualWesternExperts’

Estimates**

mbpd

2001 200120012001 ** Richard Matzke, former VP Chevron/Texaco, 2002* RF Minenergo

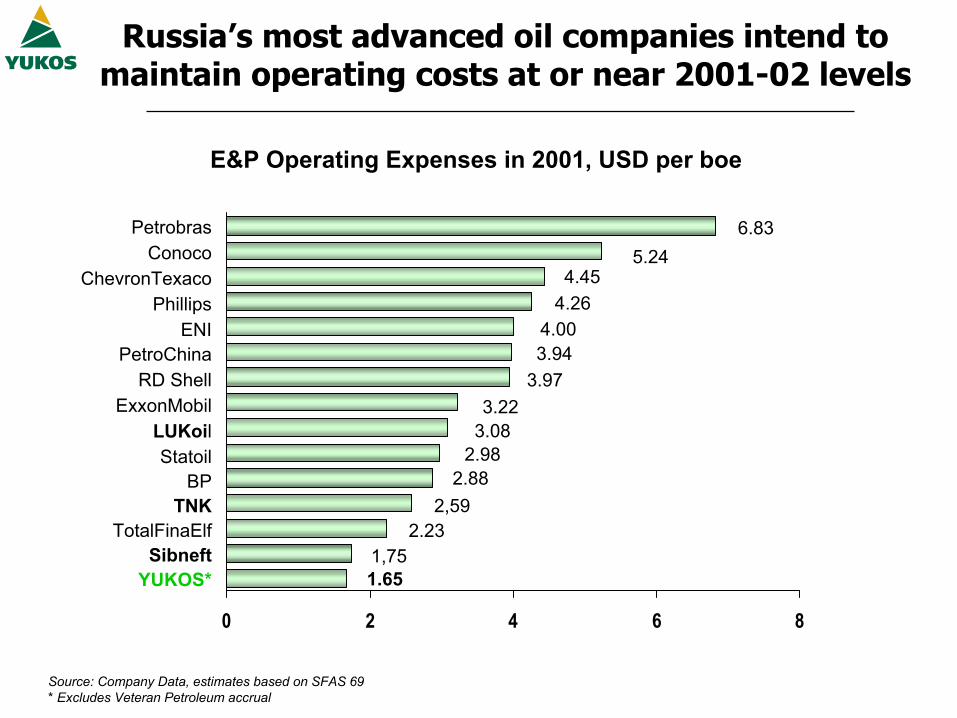

Source: Company Data, estimates based on SFAS 69* Excludes Veteran Petroleum accrual

E&P Operating Expenses in 2001, USD per boe

PetrobrasConoco

ChevronTexacoPhillips

ENIPetroChina

RD ShellExxonMobil

LUKoilStatoil

BPTNK

TotalFinaElfSibneft

YUKOS*

0 2 4 6 8

6.835.24

4.454.26

4.003.94

3.973.22

3.082.98

2.88

2.23

1.65

2,59

1,75

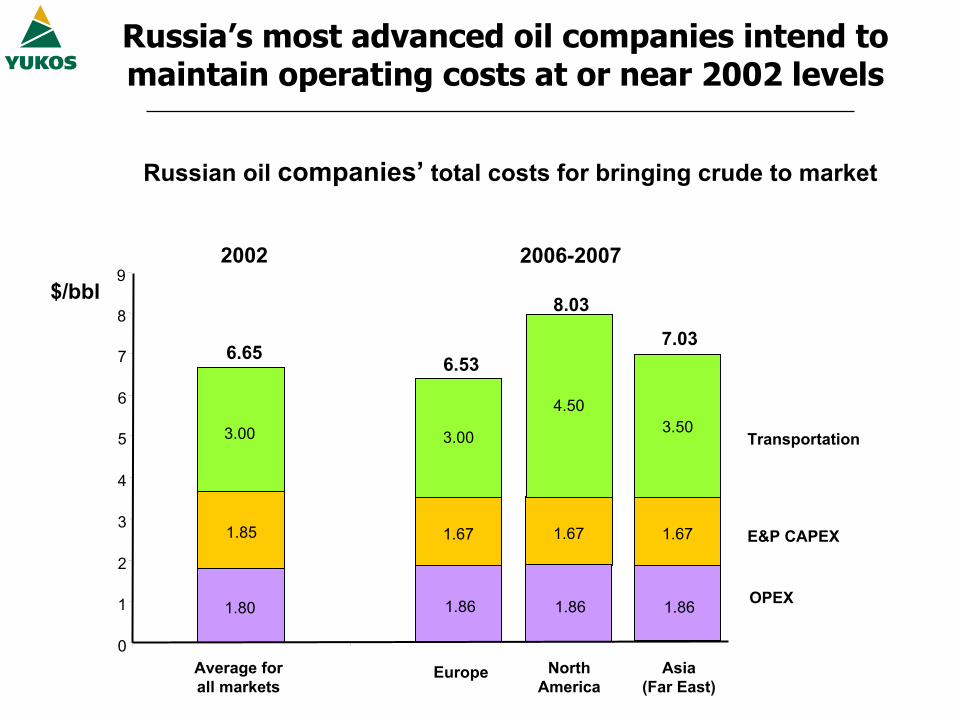

Russia’s most advanced oil companies intend to maintain operating costs at or near 2001-02 levels

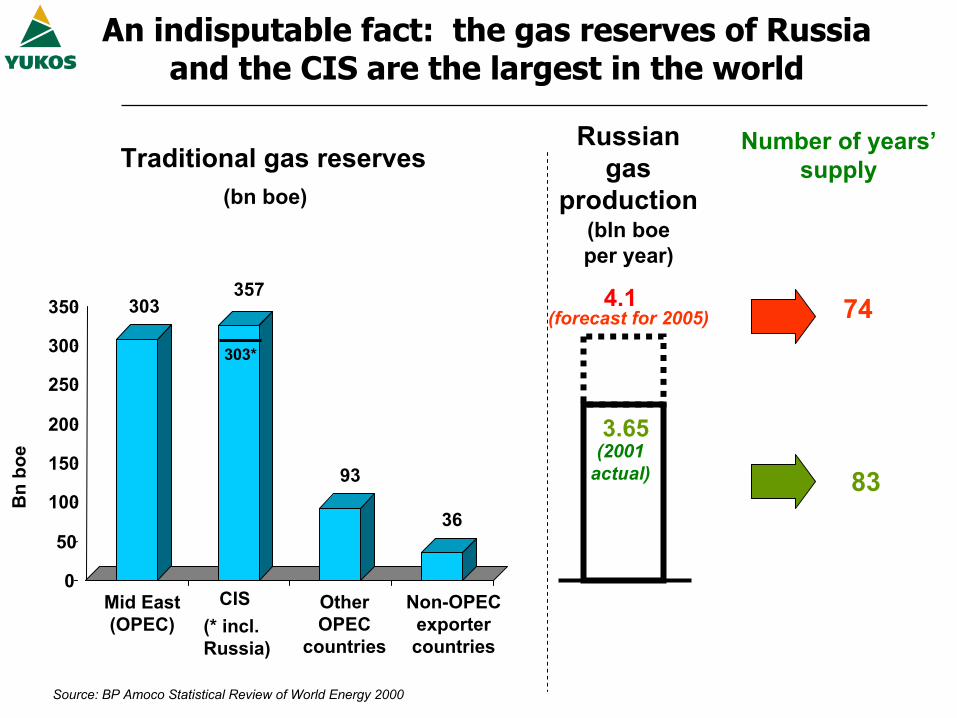

An indisputable fact: the gas reserves of Russia and the CIS are the largest in the world

303357

93

36

0

50

100

150

200

250

300

350

Mid East(OPEC) (* incl.

Russia)

CIS OtherOPEC

countries

Non-OPECexportercountries

Bn

boe

Traditional gas reserves

Source: BP Amoco Statistical Review of World Energy 2000

3.65

Russian gas

production(bln boe per year)

4.1(forecast for 2005)

(2001actual)

Number of years’supply

74

83

303*

(bn boe)

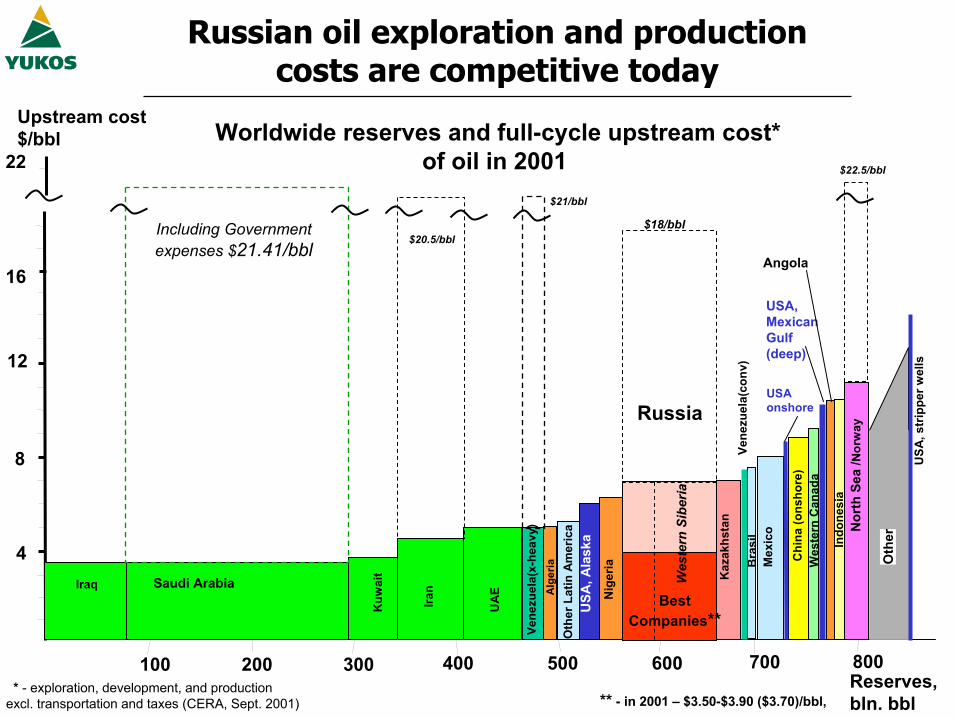

Upstream cost$/bbl

** - in 2001 – $3.50-$3.90 ($3.70)/bbl,

22 $22.5/bbl

* - exploration, development, and production excl. transportation and taxes (CERA, Sept. 2001)

Worldwide reserves and full-cycle upstream cost* of oil in 2001

Reserves,bln. bbl

100

16

12

8

4

200 300 400 500 600 700

Iraq

Kuw

ait

IranSaudi Arabia

UA

E

USA

, str

ippe

rwel

ls

Wes

tern

Sib

eria

Vene

zuel

a(x-

heav

y)

Oth

erLa

tinA

mer

ica

Nig

eria

Alg

eria B

rasi

l Nor

th S

ea/N

orw

ay

Wes

tern

Can

ada

Mex

ico

Chi

na(o

nsho

re)

Indo

nesi

a

USA, MexicanGulf(deep)

USA

, Ala

ska

USA onshore

Angola

Kaz

akhs

tan

Russia

Oth

er

800

BestCompanies**

Vene

zuel

a(co

nv)

$21/bbl

$20.5/bbl$18/bblIncluding Government

expenses $21.41/bbl

Russian oil exploration and production costs are competitive today

Russia’s most advanced oil companies intend to maintain operating costs at or near 2002 levels

1.80

1.85 1.67

0

1

2

3

4

5

6

7

2002 2006-2007

E&P CAPEX

3.00

8

9

3.00

6.65

Transportation

$/bbl

6.53

1.67

4.50

8.03

1.67

3.50

7.03

Average for all markets

Europe North America

Russian oil companies’ total costs for bringing crude to market

Asia(Far East)

1.86 1.86 1.86 OPEX

0

2

4

6

1995

1996

1997

1998

1999

2000

2001

2005

(forec

ast)

2010

(forec

ast)

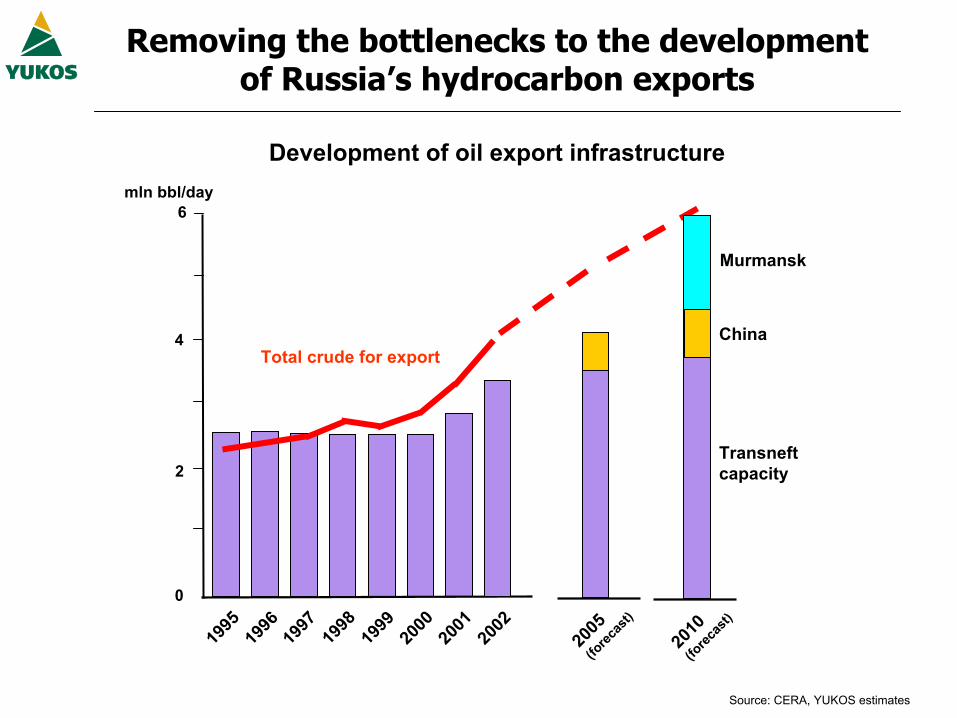

Total crude for export

Transneft capacity

Murmansk

China

Removing the bottlenecks to the development of Russia’s hydrocarbon exports

Development of oil export infrastructure

Source: CERA, YUKOS estimates

2002

mln bbl/day

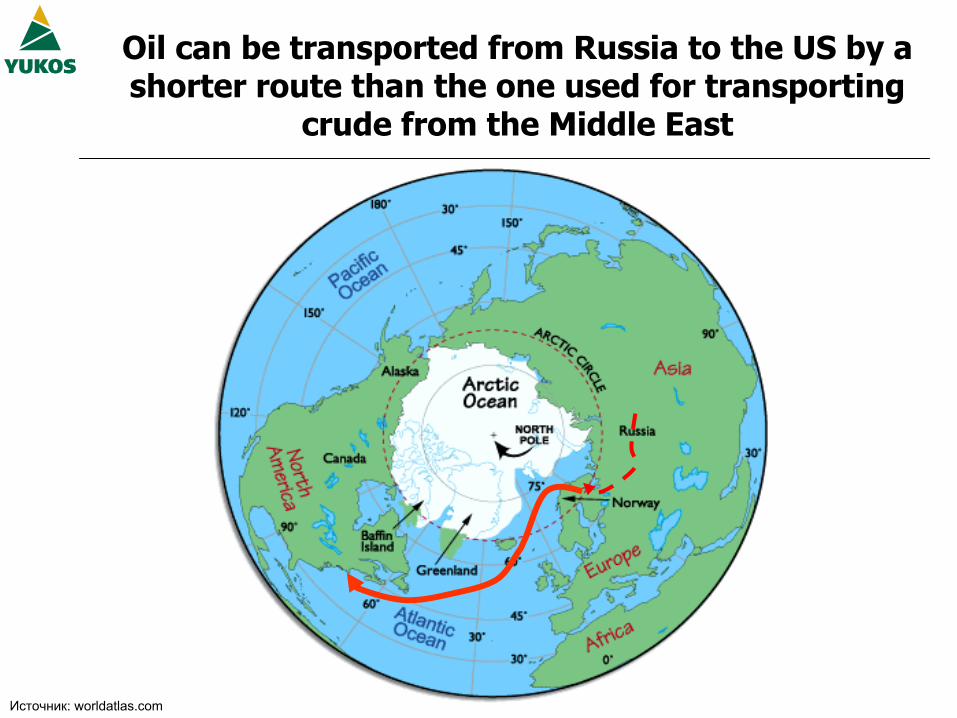

Источник: worldatlas.com

Oil can be transported from Russia to the US by a shorter route than the one used for transporting

crude from the Middle East

The Murmansk Pipeline Project

Nefteyugansk

UsaUkhtaVologda

Region

Murmansk

Moscow

Khanty-MansiyskAutonomous Area

KomiRepublic

Arkhangel’skRegion

Republic

of Karelia

Usa route

Length: 2500 kmCAPEX: $3.4 billion

(preliminary estimate)

Ukhta route

Length: 3600 kmCAPEX: $4.5 billion

(preliminary estimate)

Project milestones

27 Nov 2002: YUKOS signs Memorandum of Understanding with Lukoil, Sibneft, and TNK

April 2003: Declaration of Intent

2003-2004: Investment Case,Feasibility Study,Design Drawings

2004-2007: Construction

2007- : Operation

Mongolia

Russia

China

AngarskChita

Daqing

800 kbopd

~1600 km

~ 800 km

Lake

Baik

al

Facts and figures

• Length ~ 2400 km (1500 miles)

• Initial capacity 400 k bopd

• Estimated cost ~ 1.7 bln USD

• Agreed: pricing formula, volumes, delivery guarantees

• Operator - Transneft

Facts and figures

• Length ~ 2400 km (1500 miles)

• Initial capacity 400 k bopd

• Estimated cost ~ 1.7 bln USD

• Agreed: pricing formula, volumes, delivery guarantees

• Operator - Transneft

Timetable

• July 2002 - Feasibility study

• 2003 - Detailed project

• 2003-2005 - Construction

• 2005-2009 - 400 kbopd shipments

• 2010-2030 - 600 kbopd shipments

Timetable

• July 2002 - Feasibility study

• 2003 - Detailed project

• 2003-2005 - Construction

• 2005-2009 - 400 kbopd shipments

• 2010-2030 - 600 kbopd shipments

capacity

The most promising projects to the Far East:a pipeline to China

Source: CERA research, Yukos estimates

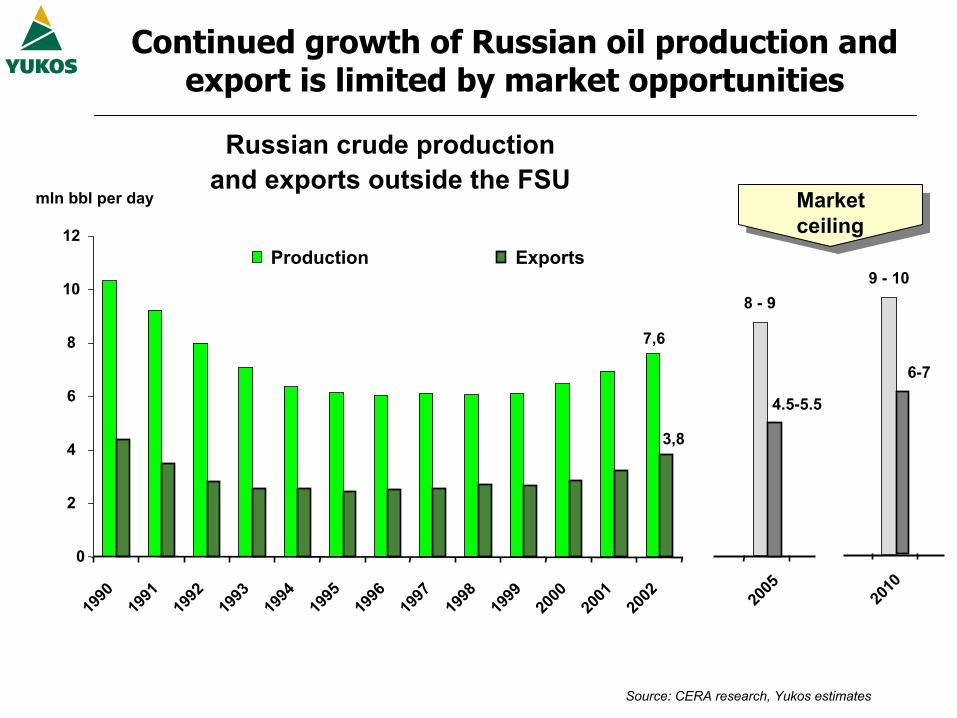

Continued growth of Russian oil production and export is limited by market opportunities

mln bbl per day

Russian crude productionand exports outside the FSU

Marketceiling

0

2

4

6

8

10

12

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Production Exports

2005

2010

7,6

3,8

8 - 99 - 10

4.5-5.5

6-7

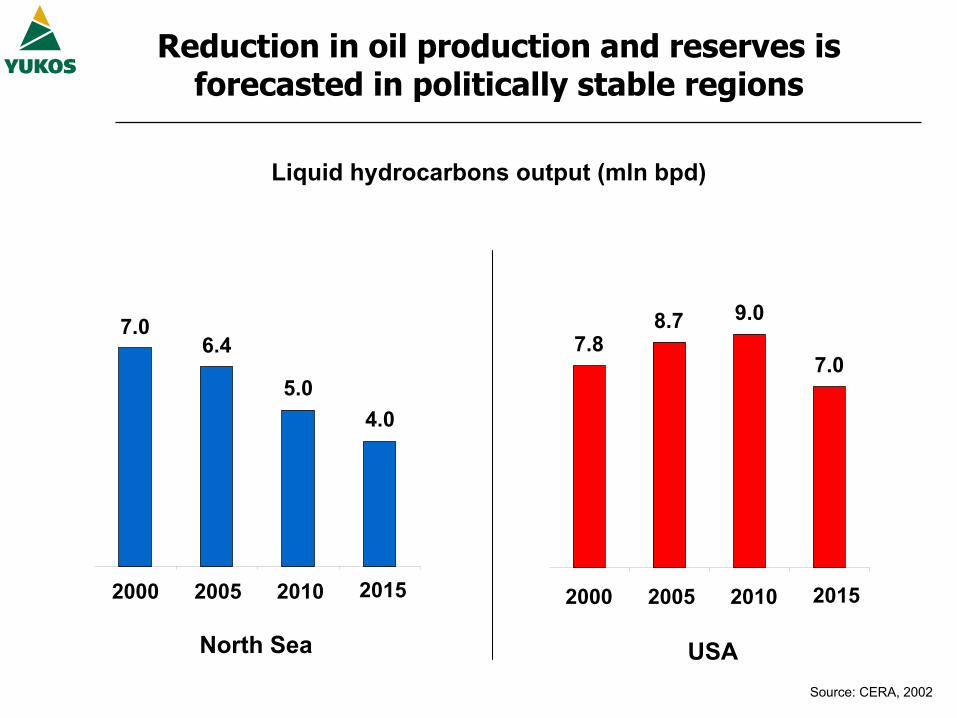

7.06.4

5.04.0

2000

7.88.7 9.0

7.0

2005 2010 2015

Reduction in oil production and reserves is forecasted in politically stable regions

2000 2005 2010 2015

Liquid hydrocarbons output (mln bpd)

North Sea USASource: СERA, 2002

If past evaluations are taken into account, the geopolitical picture of the oil industry in 10 years

will be determined by the Middle East

Relative size of global oil sources(reserves and production)

9%

21%

55%

9%

6%

Europe/North America

(excluding deep water)

Deep water

FSU

Middle East

Others

Western estimates of world’s oil reserves distribution in

late 90’sUSA Deep water

NorthSea

SouthAmerica

MiddleEast

FSU

WestAfrica Pacific

Western appraisals of Russia’s oil reserves have been historically underestimated

Oil reserves of Russia and top Russian oil companies

46.540.2

81.893.0

0

10

20

30

40

50

60

70

80

90

100

(bln bbl)

Internationally audited

(1999-2000) proved reserves of Top 4* companies

Russia’s proved

reserves(World Energy Council, 1998)

* Lukoil, YUKOS, Surgutneftegas, TNK

(without Onako)

Proved reserves (ABC1)

of Top 10**

* Lukoil, YUKOS, Surgutneftegas, TNK

(without Onako), Sidanco, Rosneft, Tatneft, Sibneft,

Slavneft, Bashneft

Proved and 50% of probable

reserves (C2)of Top 10**

* Lukoil, YUKOS, Surgutneftegas, TNK

(without Onako), Sidanco, Rosneft, Tatneft, Sibneft,

Slavneft, Bashneft

80 81 82 92 9383 84 85 86 87 88 89 90 91 94 95 96 97 98 99

World Oil Annual Reports 1980-1999. Petroconsultants

Sudden statistical leaps in combined oil reserve figures forAbu Dhabi, Dubai, Iran, Iraq, Kuwait, and Saudi Arabia

100

200

300

400

500

600

There are grounds to believe that Middle Eastern reserves may be overstated

+ 193increase in one year

Petroconsultantsestimate

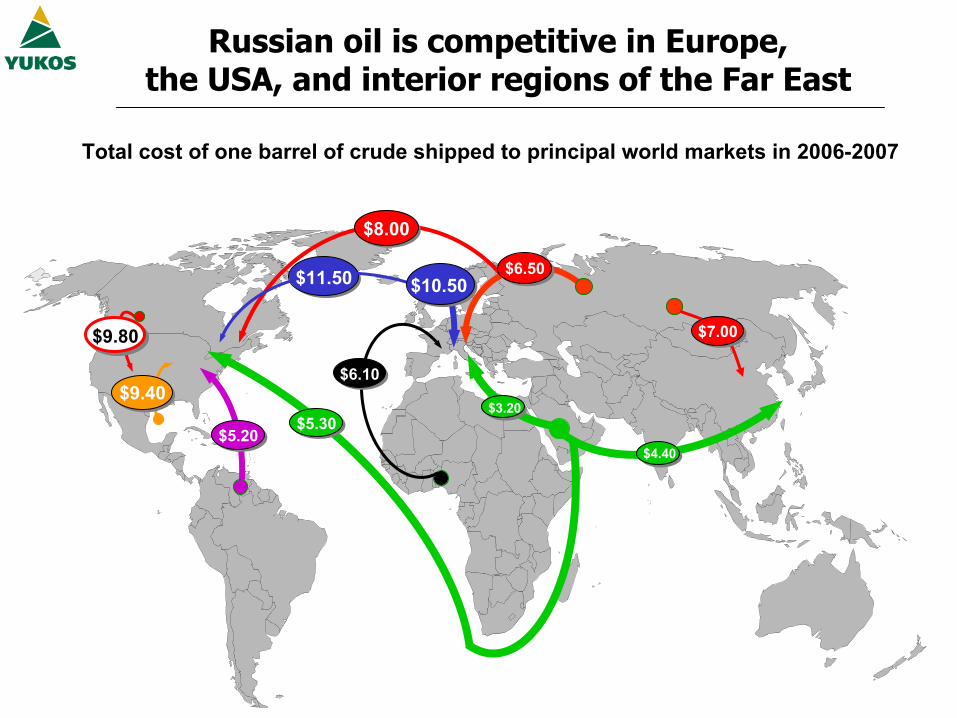

$5.30$5.20

$9.80

$9.40$6.10

Total cost of one barrel of crude shipped to principal world markets in 2006-2007

Russian oil is competitive in Europe,the USA, and interior regions of the Far East

$8.00

$11.50

$3.20

$6.50$10.50

$4.40

$7.00

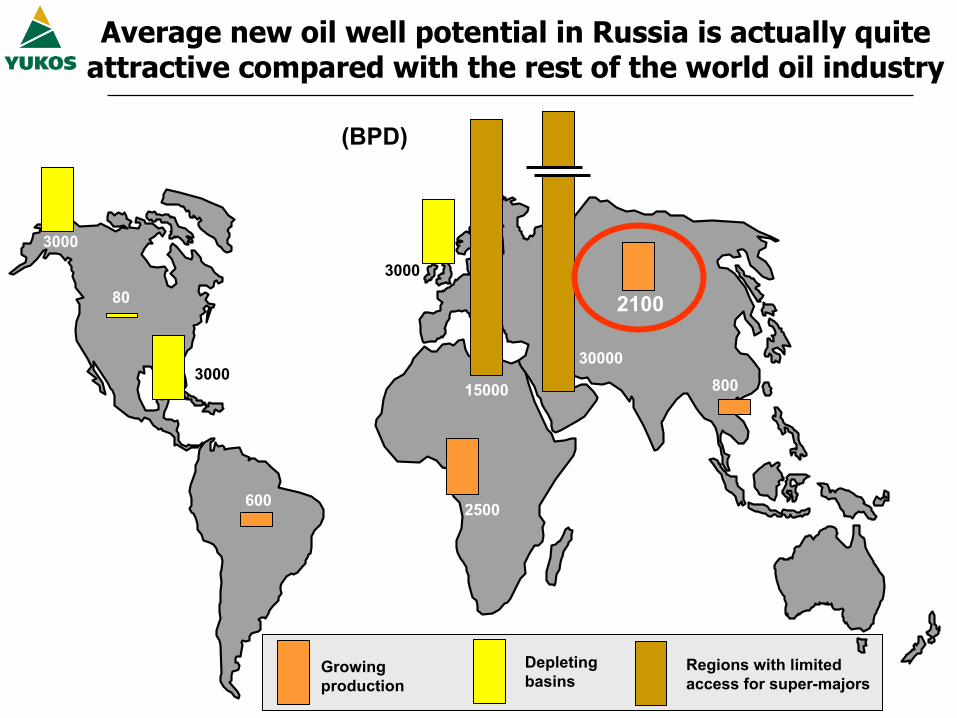

Average new oil well potential in Russia is actually quite attractive compared with the rest of the world oil industry

30000

15000

2500

800

3000

3000

2100

3000

600

80

Depletingbasins

(BPD)

Regions with limitedaccess for super-majors

Growingproduction

Source: Company data

-2%-1%

1%1%1%

2%4%

5%5%

6%6%

11%13%

17%

20%18%

SibneftConoco

YUKOSPhillips

RosneftTNK

BP Petrobras

SurgutneftegasChevronTexaco

Royal Dutch/ShellLUKoil

TotalFinaElfPetroChinaExxonMobil

ENI*

* - excl. Lasmo

Several Russian companies are among the world leaders in oil industry production growth

Relative Production change for selected companies, 2001/2000, %

2000 2005 2010

14.1 14.2 14.4

Source: CERA, 2002

7.06.4

5.0

18% 25%

Western European oil consumption will be more and more dependent on imports in the future

MMBPD

Russia can become a reliable source of crude for Europe for many years to come

North Sea production

ImportsRussia’s

share in 2000Possible Russian

share in 2010

Russia can meet 10% or more of China’s oil import requirements

0

50

100

150

200

250

300

350

1995 2000 2005 2010

170

Chinese domestic production

Imports

Imports from Russia

170 160

320

30

20

260

220

China’s crude requirements (MMT)

The geopolitical imperative for today is to diversify energy sources and concentrate

on the most reliable ones

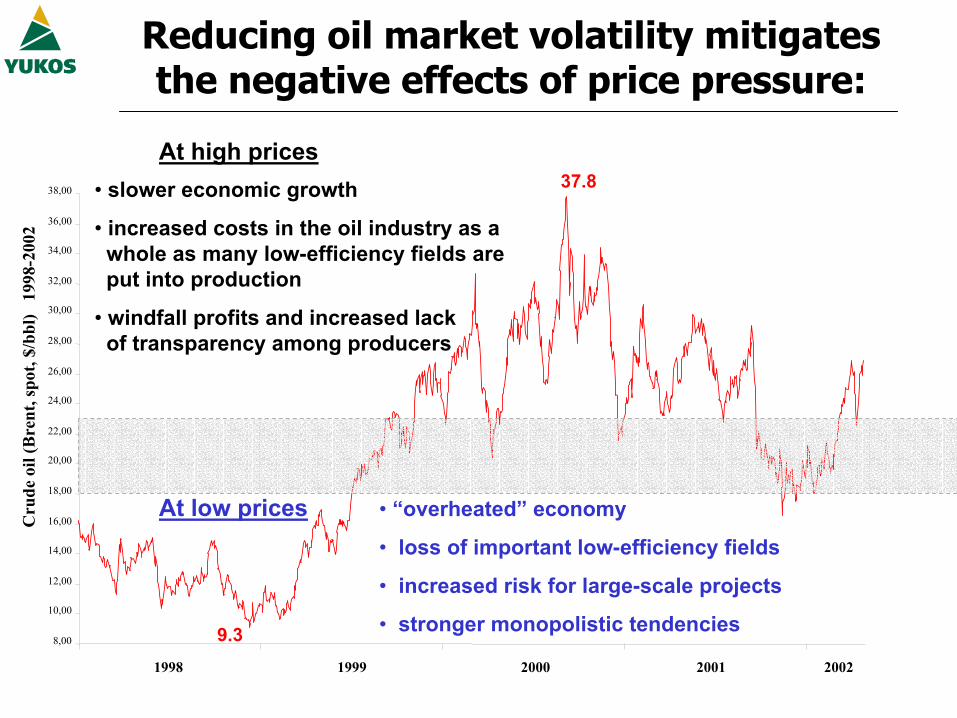

Reducing oil market volatility mitigates the negative effects of price pressure:

Cru

de o

il(B

rent

, spo

t, $/

bbl)

199

8-20

02

1998

8,00

10,00

12,00

14,00

16,00

18,00

20,00

22,00

24,00

26,00

28,00

30,00

32,00

34,00

36,00

38,00

1999 2000 2001 2002

• slower economic growth

• increased costs in the oil industry as awhole as many low-efficiency fields areput into production

• windfall profits and increased lackof transparency among producers

• “overheated” economy

• loss of important low-efficiency fields

• increased risk for large-scale projects

• stronger monopolistic tendencies

37.8

9.3

At high prices

At low prices

A multi-polar geopolitical picture is optimal

• a price range of $18-23 per barrel• a mix of long-term and spot contracts• a rational tax policy in producer and consumer countries

Conditions:

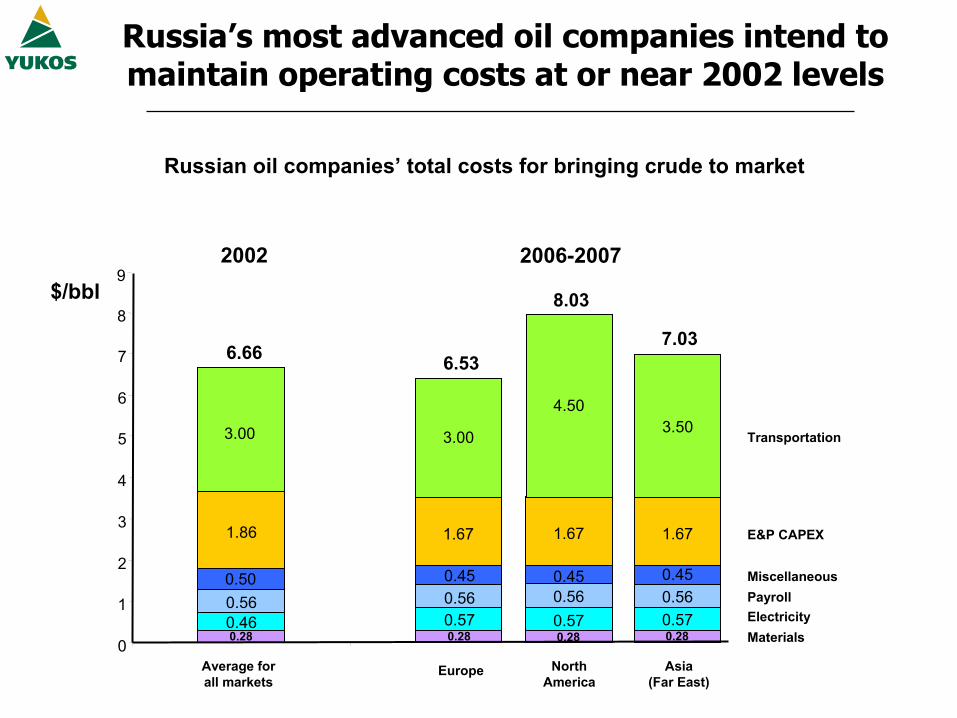

Russia’s most advanced oil companies intend to maintain operating costs at or near 2002 levels

0.28 0.280.46 0.570.56 0.560.50 0.45

1.86 1.67

0

1

2

3

4

5

6

7

2002 2006-2007

MaterialsElectricityPayrollMiscellaneous

E&P CAPEX

3.00

8

9

3.00

6.66

Transportation

$/bbl

6.53

0.280.570.560.45

1.67

4.50

8.03

0.280.570.560.45

1.67

3.50

7.03

Average for all markets

Europe North America

Russian oil companies’ total costs for bringing crude to market

Asia(Far East)