russia economic outlook 2014 | aranca articles and publications

DESCRIPTION

Russia’s economic growth declined from 2% in 4Q 2013 to 0.7% in 3Q 2014. Russia’s poor run began with the imposition of sanctions by western countries in 2014. Learn more about inflation, imports & exports, GDP growth of Russian economy.TRANSCRIPT

Russia’s faltering economy January 2015

© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company.

P a g e | 1

Oil price decline and western sanctions push Russia's economy into free fall

The year 2014 was a forgettable one for Russia. The country was engulfed by serious geopolitical and financial problems that started

with the rising political tensions in Ukraine, leading to the imposition of trade sanctions by western countries on Russia. The country

reacted by imposing counter-sanctions, resulting in its isolation and grave financial troubles. Although Russia tried to fight the problems

related to sanctions, inflation, and currency depreciation, the sudden fall in oil prices has dealt a severe blow to its economy. Russia’s

economy depends heavily on the production and export of hydrocarbons; and, the recent decline in oil prices has made it inevitable for

the USD2tn economy to slip into recession. Although the central bank and the government have intervened to revive the economy, any

favorable impact of the measures taken remains to be seen.

Russia had a gloomy 2014. The country is staring at a GDP growth rate of less than 1.0% for 2014 for the first time since 2010. Anton

Siluanov, Russia’s Finance Minister, has already warned against a GDP contraction of 4% in 2015 and a budget deficit of over 3% if oil

prices stay at USD60 per barrel. In view of the weak outlook for oil prices and unabated tensions in Ukraine, even the IMF downgraded

Russia’s growth projection for 2014 and 2015 to 0.2% and 0.5%, respectively.

Russia’s economic growth declined from 2% in 4Q 2013 to 0.7% in 3Q 2014. The sanctions imposed by western countries, following

the geopolitical tensions in Ukraine, and the declining oil prices have wrecked the country’s economy. Investor confidence in the

country has been eroded by the recent turn of events, which is evident from the data released by Russia’s central bank, showing net

capital outflows in excess of USD85bn in the first three quarters of 2014 as against total outflows of USD61bn in 2013. Russia’s

problems have been further compounded by a plunging currency; the value of Russian ruble has declined over 60% against the US

dollar since the beginning of 2014.

Russia’s GDP growth and net capital flows

Source: Bloomberg, IMF, World Bank, Central Bank of Russia, Government estimates

Western sanctions derail Russia’s growth engine

Russia’s poor run began with the imposition of sanctions by western countries in 2014, following the country’s military intervention to

support the separatists in Ukraine. Condemning this invasion on Ukraine’s sovereignty and independence, western nations imposed

stiff economic sanctions on major Russian state banks and corporations. Consequently, Russia’s status as a super power came under

threat and trade in key sectors including energy and defense, and state finances was affected. The financial sector was deprived of the

much needed funds to support critical growth and development projects. Many large state-owned banks, accounting for more than half

(60)

(40)

(20)

-

20

40

60

-6%

-4%

-2%

0%

2%

4%

6%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

GDP (LHS) Net capital flows (RHS)

(y –o–y change) (USD bn)

2010 2011 2012 2013 2014

Russia’s faltering economy January 2015

© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company.

P a g e | 2

of Russia’s banking assets, were severed from the US and European Union’s financing systems, resulting in a credit crunch. Presently,

Russian companies are finding it difficult to borrow money to even finance their own operations. In fact, the Finance Minister expects

that if the sanctions are extended and continue throughout the next year, Russia could stand to lose about USD40bn (about 1.9% of its

GDP) in economic activity.

Counter-sanctions drive up inflation, especially for food commodities

Russia’s act of imposing counter-sanctions by banning the import of essential food products such as fruits, vegetables, meat, and

various dairy products, including milk, from the US, the EU, Norway, Canada and Australia, has worsened the situation. Every year,

Russia imports about 25% of its meat requirements and about 70% of the fruits consumed in the country. The ban has pushed up the

prices of key food products that constitute nearly two-thirds of the food inflation index, which has caused the food inflation to rise from

8.6% in March to 11.5% in October 2014.

Oil price plunge not only eats into reserves but also brings economy to a standstill

The sharp fall in the oil prices over the past few months has dealt a severe blow to the Russian economy, already reeling under the

effect of sanctions. In September 2014, the Finance Minister stated that in addition to losing USD40bn a year due to the economic

sanctions, the country would lose another USD90–100bn due to the ~30% drop in the oil prices since the beginning of the year. With oil

prices having witnessed a decline of ~48% in 2014, we expect the impact on the economy to be even greater.

The Finance Minister has already issued a warning about GDP contraction in 2015 and a swelling budget deficit if oil prices remain at

around USD60 per barrel. Plummeting oil prices have sharply dragged down Russia’s energy exports, which form nearly 67% of the

total exports and around 15% of the GDP. The current commodity scenario is likely to propel Russian policymakers to seriously rethink

budget strategies as the current budget had reckoned the price of oil to remain around USD100 per barrel of oil, with taxes on oil

contributing nearly 50% to the total fiscal receipts. According to Tatyana Nesterenko, Russia’s first Deputy Finance Minister, the

continued decline in oil prices is likely to considerably eat into the USD74bn reserve fund created by the government to sustain energy

price fluctuations.

Composition of exports (2013) Composition of imports (2013)

Source: Bloomberg

The turn of events has unearthed a structural weakness in Russia’s economy, stemming from the over-dependence on hydrocarbons.

The debt crisis of 1998, when oil prices plunged to USD10 per barrel, seems to have returned to haunt them. Back then, large fiscal

Crude oil 33%

Oil Products 21%

Gas 13%

Metals 6%

Machinery 5%

Fertilizers & chemicals

2%

Others 20%

Machinery 49%

Automobiles 6%

Food 5%

Medicines 4%

Clothing 3%

Energy 1%

Others 32%

USD 314.9bn USD 527.3bn

Russia’s faltering economy January 2015

© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company.

P a g e | 3

deficits and low foreign reserves had forced Russia to default on the dollar-denominated public and private debt. Further, the country

suffered from hyper-inflation, which led to a lot of wealth being wiped out.

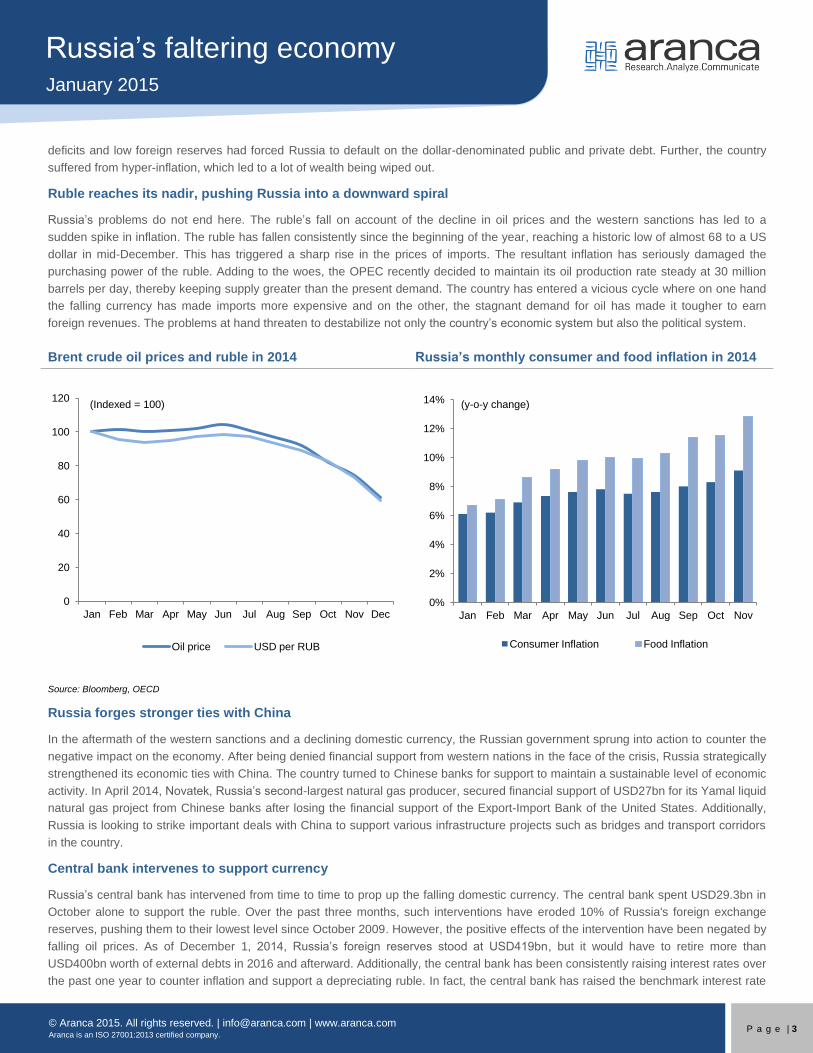

Ruble reaches its nadir, pushing Russia into a downward spiral

Russia’s problems do not end here. The ruble’s fall on account of the decline in oil prices and the western sanctions has led to a

sudden spike in inflation. The ruble has fallen consistently since the beginning of the year, reaching a historic low of almost 68 to a US

dollar in mid-December. This has triggered a sharp rise in the prices of imports. The resultant inflation has seriously damaged the

purchasing power of the ruble. Adding to the woes, the OPEC recently decided to maintain its oil production rate steady at 30 million

barrels per day, thereby keeping supply greater than the present demand. The country has entered a vicious cycle where on one hand

the falling currency has made imports more expensive and on the other, the stagnant demand for oil has made it tougher to earn

foreign revenues. The problems at hand threaten to destabilize not only the country’s economic system but also the political system.

Brent crude oil prices and ruble in 2014 Russia’s monthly consumer and food inflation in 2014

Source: Bloomberg, OECD

Russia forges stronger ties with China

In the aftermath of the western sanctions and a declining domestic currency, the Russian government sprung into action to counter the

negative impact on the economy. After being denied financial support from western nations in the face of the crisis, Russia strategically

strengthened its economic ties with China. The country turned to Chinese banks for support to maintain a sustainable level of economic

activity. In April 2014, Novatek, Russia’s second-largest natural gas producer, secured financial support of USD27bn for its Yamal liquid

natural gas project from Chinese banks after losing the financial support of the Export-Import Bank of the United States. Additionally,

Russia is looking to strike important deals with China to support various infrastructure projects such as bridges and transport corridors

in the country.

Central bank intervenes to support currency

Russia’s central bank has intervened from time to time to prop up the falling domestic currency. The central bank spent USD29.3bn in

October alone to support the ruble. Over the past three months, such interventions have eroded 10% of Russia's foreign exchange

reserves, pushing them to their lowest level since October 2009. However, the positive effects of the intervention have been negated by

falling oil prices. As of December 1, 2014, Russia’s foreign reserves stood at USD419bn, but it would have to retire more than

USD400bn worth of external debts in 2016 and afterward. Additionally, the central bank has been consistently raising interest rates over

the past one year to counter inflation and support a depreciating ruble. In fact, the central bank has raised the benchmark interest rate

0

20

40

60

80

100

120

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Oil price USD per RUB

0%

2%

4%

6%

8%

10%

12%

14%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Consumer Inflation Food Inflation

(Indexed = 100) (y-o-y change)

Russia’s faltering economy January 2015

© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company.

P a g e | 4

from 7% in March 2014 to 10.5% in December 2014. Also, on December 15, the central bank hiked the interest rate to 17% from

10.5%, which is the largest increase since the economic crisis of 1998. However, these interventions are yet to show any substantial

results. On a separate note, President Vladimir Putin has passed a new law to double the deposit guarantee for deposits in bank

accounts to USD25,370 in order to protect the interests of common citizens. Steps are also being taken to recapitalize local banks if

they face any financial crisis.

Russia’s foreign exchange reserves Russia central bank interest rates in 2014

Source: Bloomberg

Uncertainly looms large

The slump in oil prices has pushed the world’s largest energy exporter to the verge of recession. Even a positive contribution from the

exports cannot offset the effect of contraction in domestic demand and the damage to the banking system and consumer sentiment. It

is felt that the fall in oil prices and the economic sanctions would weigh heavily on Russia’s prospects, going forward. Due to its heavy

dependence on food imports, the country’s ability to curb inflation through a tight monetary policy is limited. The country faces political

isolation from its western counterparts, which makes Russia’s dependence on China for its recovery all the more important.

Research Note by: Rahul Kumar and Akanksha Kumar

419

300

350

400

450

500

550

600

2010 2011 2012 2013 1Q 2Q 3Q 4Q*

17%

0%

4%

8%

12%

16%

20%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(USD bn)

2014

Russia’s faltering economy January 2015

© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company.

P a g e | 5

ARANCA DISCLAIMER

This report is published by Aranca, Inc. Aranca is a customized research and analytics services provider to global clients.

The information contained in this document is confidential and is solely for use of those persons to whom it is addressed and may not

be reproduced, further distributed to any other person or published, in whole or in part, for any purpose.

This document is based on data sources that are publicly available and are thought to be reliable. Aranca may not have verified all of

this information with third parties. Neither Aranca nor its advisors, directors or employees can guarantee the accuracy, reasonableness

or completeness of the information received from any sources consulted for this publication, and neither Aranca nor its advisors,

directors or employees accepts any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this

document or its contents or otherwise arising in connection with this document.

Further, this document is not an offer to buy or sell any security, commodity or currency. This document does not provide individually

tailored investment advice. It has been prepared without regard to the individual financial circumstances and objectives of persons who

receive it. The appropriateness of a particular investment or currency will depend on an investor’s individual circumstances and

objectives. The investments referred to in this document may not be suitable for all investors. This document is not to be relied upon

and should not be used in substitution for the exercise of independent judgment.

This document may contain certain statements, estimates, and projections with respect to the anticipated future performance of

securities, commodities or currencies suggested. Such statements, estimates, and projections are based on information that we

consider reliable and may reflect various assumptions made concerning anticipated economic developments, which have not been

independently verified and may or may not prove correct. No representation or warranty is made as to the accuracy of such statements,

estimates, and projections or as to its fitness for the purpose intended and it should not be relied upon as such. Opinions expressed are

our current opinions as of the date appearing on this material only and may change without notice.

© 2015, Aranca. All rights reserved.