rural livelihood development company - tzdpg.or.tz · pdf fileniras would like to thank the...

TRANSCRIPT

Rural Livelihood Development Company

Survey on Dairy Products Market in Tanzania

Final Report

12 May 2010

Survey on Dairy Products Market in Tanzania

i

ACKNOWLEDGEMENT NIRAS would like to thank the Rural Livelihood Development Company (RLDC) for hiring NIRAS to carry out this interesting and strategically important study. First and foremost we appreciated the technical, logistical and administrative input provided by RLDC team led by Mr. Charles Ogutu, CEO, Mr. Heini Conrad, Advisor and Dairy Sector Team Leader, and Ms Ajuaye Sigalla, Dairy Sector Team Leader. Members of Tanzania Milk Processors Association (TAMPA) who actually are the primary users of the study outputs worked very closely with the team, they provided more information on the scope and objectives of the study and also facilitated communication between the Consultant and processors as well as availing some reference materials. The valuable support from TAMPA involved interactions with Dr. D. Mmari, the Chairman of TAMPA and CEO of Tandairies, Mrs. Mboka M. Massawe, Executive Secretary and Mr. Edmund Mariki – Business Manager. NIRAS thanks Tanzania Dairy Board through its Executive Director Mr. Charles Mutagwaba who further clarified on the research questions and provided important information including some background materials. Still at TDB, Prof. Lusato Kurwijilla spared his weekend time to meet with the consultants and shared his wealth of knowledge in the industry. Equally key to this work had been the processors namely Mr. James Matayo – Managing Director of Mara Milk Limited, Dr. E. Mazara – Interim Managing Director, Mr. Samwel Simiyu – Finance Manager, Ms Rebecca Sangura – Milk Collection Centers Coordinator all of New Musoma Dairy Limited. In Arusha the team had the privilege to discuss with Mr. Peter Ngasa – Managing Director of Arusha Dairies Limited, Mrs. Matilda Bella, Acting Head of Economic Development Cluster in Arusha Region and Mr. Yusuph M. Alladin of International Diaries Company Limited. In Arusha the Consultant also met with Mr. Carilus Alando – Zonal Sales and Marketing Manager for Brookside. The work in Tanga involved consultations with to Mr. Alnoor Hussein. – CEO of Tanga Fresh Limited and Mr. Lut Zylstra of Mifugo Bora Company Ltd. The team consisted of two consultants namely Mr. Leif Enemark and Mr. Hebron Mwakalinga, and was supported by the Niras Tanzania office in logistics and quality assurance as well as in project management. Due to the limited time allocated for the work on one side and the relatively demanding scope of output, the team solicited and received support from Mr. Zephania Mposo (MBA Marketing) who followed up data from TRA and assisted coordination of retailer interviews in Arusha, Mr. Ikunda Terry (MBA Student) who worked with the team throughout conducting a survey with retailers and Mr. Charles (BA) who carried out the interview of retailers in Arusha. NIRAS shares any credit for this work with all those mentioned above. However, the liability of any shortcoming shall remain the sole responsibility of Niras. Niras Finland Oy P.O.Box 23070 Dar es Salaam Tanzania Tel. 022 260 2360 Mob.0753 102 006 Email. [email protected] / [email protected]

Survey on Dairy Products Market in Tanzania

ii

TANZANIA COUNTRY PROFILE 2004 2005 2006 2007 2008 Population in millionsi 36.31 37.27 38.67 39.45 40.67 Annual growth of GDP in percent - at 2001 pricesi 7.80 7.40 6.70 7.10 7.40 Growth of livestock sector at 2001 pricesi 6.60 4.40 4.00

4.50

5.10

Percentage contribution–of livestock sector to GDP at 2001 pricesi

4.50

4.40

4.20

4.00

3.80

Domestic milk production in million litres 1,386ii 1,410ii 1,420ii 1,664iii

Exchange rate (in Tshs/USD) iv 1,089 1,123 1,252 1,132 1,280 NOTES i Economic Survey, 2008 ii Match Maker Associates, 2008 iii Ministry of Finance and Economic Affairs, 2009 iv Bank of Tanzania (BOT)

Survey on Dairy Products Market in Tanzania

iii

Contents 1.0 Introduction.....................................................................................................................1

1.1 Background .................................................................................................................1

1.2 Study Objectives, Outputs and Deliverables...............................................................3

1.3 Scope and Methodology of the Study .........................................................................5

1.4 Study Limitations ........................................................................................................5

1.5 Organization of the Report ..........................................................................................6

2.0 Findings ...........................................................................................................................7

2.1 Dairy Market Structure................................................................................................7

2.2 Distribution of Dairy Products ..................................................................................20

2.3 Milk Processing.........................................................................................................32

3.0 Conclusions and recommendations ...............................................................................36

3.1 Conclusions ...............................................................................................................36

3.2 Recommendations .....................................................................................................38

References................................................................................................................................43

Annex I: List of Dairy Processing Plants.................................................................................44

Annex II: Relation Between Population and Installed Dairy Processing Capacity .................45

Annex III (A): Dairy Product Imports by Country of Origin, Value and Quantity (2009) .....46

Annex IV (B): Imports of Dairy Products, by Value and Quantity; 2004 - 2009....................50

Annex IV: Types of Dairy Products Consumed .....................................................................51

Annex V: Abridged Terms of Reference .................................................................................52

Annex VI: Tool Used to Collect Information from Retailers ..................................................54

Annex VII: Comments Made by Participants on the Report ..................................................59

General Comments...............................................................................................................59

Group No. One: How Can We Engage The Government Effectively In The Development Of The Dairy Sector? ................................................................................................................61

Group No. Two: How Can We Improve Cost Competitiveness In Dairy Value Chains? ...63

Survey on Dairy Products Market in Tanzania

iv

LIST OF FIGURES Figure 1.1.1 An Overview Map of the Dairy Sector

Figure 2.1.1 Main Dairy Industry Products in Tanzania based on Installed Capacity

Figure 2.1.2 The Average Composition of Dairy Products Imported in Tanzania by Volume (2004 – 2009)

Figure 2.1.3. Pattern of dairy product consumption over the year

Figure 2.2.1. Relative Position of Dairy Processing Installed Capacity in Tanzania

Figure 2.2.2 Trend of Dairy Products Imports in USD

Figure 2.1.3. Pattern of dairy product consumption over the year

Figure 2.2.1 Product Visibility at Retail Point

LIST OF TABLES

Table 1.1.1 An Overview of the Structure of the Milk Sector

Table 2.1.1 Percentage of Households Consuming Packed Milk (2007)

Table 2.1.2. Locations at Which Consumer Bought Dairy Products (2007).

Table 2.1.3 Estimation of Market Size for Processed Dairy Products in Dar es Salaam in 2007

Table 2.1.4 Relative Price of Pasteurized Milk per Litre (1991, 1998 and 2010)

Table 2.1.5 Cost Structure of Processing One litre into Pasteurised Milk packed in Poly Pouch

Table 2.2.1 Population (Market Potential) Relative to Processing Capacity

Table 2.2.2 Return on Investment on Operating a Refrigerated Truck Between Musoma and Dar es Salaam.

Table 2.2.3 Estimated Capacity to Service a Refrigerator Loan

Table 2.2.4 General Comments by Retailers on How to Improve Distribution

Table 2.2.5 Utilisation of Dairy Processing Capacity in EA (2006)

Survey on Dairy Products Market in Tanzania

v

LIST OF ABBREVIATIONS

BOT Bank of Tanzania

FMCGs Fast moving consumer goods

GDP Gross Domestic Product

HBS Household Budget Survey

kW(H) Kilowatt (Hour)

lme Liquid milk equivalent

lpa Litres per annum

lpd Litres per day

MFEA Ministry of Finance and Economic Affairs

ML&FD Ministry of Livestock and Fisheries Development

MMA Match Maker Associates Limited

Mt. Metric tone

NBS National Bureau of Statistics

NMDL New Musoma Dairy Ltd.

RLDC Rural Livelihood Development Company

TAHA Tanzania Horticulture Association

TAMPA Tanzania Milk Processors Association

TDB Tanzania Dairy Board

TFL Tanga Fresh Limited

UHT Ultra high temperature

USD United States Dollar

Survey on Dairy Products Market in Tanzania

vi

EXECUTIVE SUMMARY Introduction Tanzania has a big potential to develop its dairy industry, in 2008 it was estimated to have 18.8 million heads of cattle, the third in Africa after Ethiopia and Sudan. However the performance of the sector has been dismal in absolute context, the output of milk per cow is such low that in 2008 Tanzania produced 1,664 million litres of milk. A study in 2009 that covered Dodoma, Manyara, Morogoro, Shinyanga, Singida and Tabora indicated that output per traditional cattle is as low as 0.5 litres per lactating day/cow. It is estimated that the dairy sector accounts for 30% of livestock GDP valued at USD 262 million equivalent to Tshs 300 billion. Tanzania has an annual installed milk processing capacity of 353,100 litres per day, in 2009 the milk processed was 88,440 lpd or 32.28 million litres per annum. Thus the installed capacity can absorb 7.75% of domestically produced milk. In 2008 dairy plants operated at about 25% of their capacity, this is 1.94% of the total milk produced in Tanzania. The current situation contrasts sharply with the situation in the 1980s and early 1990s when processing plants were able to process and dispose about 400,000 lpd. The objective of the study is to look into products produced, the market structure relating consumers buying pattern and ability, prices, competition from domestically produced and imported goods. It also looks how distribution is organised and carried out. The findings that culminated into recommendations are expected to help processors develop appropriate strategies in increasing sales for their products. The study used a combination of approaches; an extensive review of literature from both within Tanzania and outside with special interest on neighbouring countries. Preliminary consultations were done with RLDC, TDB and TAMPA representatives. This was followed by data collection from processors and retailers. A limited number of consumers were interviewed. The processors covered chronologically are those in Mara, Arusha, Tanga and Dar es Salaam. Interviews with retailers took place in Musoma, Mwanza, Shinyanga, Singida, Dodoma and Dar es Salaam. Mining of HBS data was done to supplement data collected in the field. Also this report benefited from inputs availed by a team from RLDC and TAMPA on February 17th, 2010. Dairy Market Structure Product Range in the Market: In the market there are a variety of products comprising of domestic and international brands, Tanzania processors however produce fewer products. About 54% of the capacity of processors is used to produce cultured milk, UHT takes 23% followed by yoghurt at 12% and cheese at 11%. Other products produced locally include ghee and cream. Imports of dairy products in liquid milk equivalent between 2004 and 2009 have averaged at 25.925 million litres per annum, growing 9.41% p.a. In 2009 dairy products under milk and cream, concentrated or sweetened account for 68% of the volume of imports, non concentrated or sweetened milk and cream made 16% and cheese and curd at 6%. Butter and other fats and oils accounted for 5%, buttermilk, curdled milk and cream, yoghurt, etc. were at 3%. Whey and other natural milk constituents made 2%. Major sources of imported dairy products are Kenya, South Africa and United Arab Emirates.

Survey on Dairy Products Market in Tanzania

vii

Household Market Segment: Consumption of packed milk is very low even in urban areas, the 2007 HBS estimates that only 0.078% of the households consume processed milk, Dar es Salaam Urban has the highest rate at 1.148% followed by Mara Urban by 0.78%. The low uptake of packed milk could be attributed to relative higher prices, negative consumer perception that processed milk has most of its nutrients taken out, limited distribution capacity of processors and most importantly readily availability of raw milk. Among the surveyed towns, kiosks/small shops are the most important point of sale for processed milk in Arusha and Dar es Salaam, in Dodoma it is the gulio while in Mwanza it they prefer large shops.

Dar es Salaam dairy product market is estimated to be worth Tshs 2.68 billion per month or Tshs 32.12 billion per annum. The total demand of milk in Tanzania then could be around Tshs 96.36 billion or USD 74 million. Imports that occupy 48% at present market for processed dairy products do therefore represent about 11% of the potential market. The current domestic production has a base value of USD 27.41 million leaving a gap of more than USD 40 million. It should be remembered however that milk is sensitive to price. If we look at price trend for processed milk in Tanzania in dollar terms, a litre of processed milk has increased 2.7 times suppressing consumption.

Other Segments: Institutional clientele shows a mixed picture, few organizations provide milk to workers, most don’t. There is no single policy even in the Government setup. It is a market segment that needs different strategies depending on the circumstances. Some processors indicated to sell loose (bulk) milk to offices. The market entry strategy to this segment is to educate workers on the advantages of consuming products that are local, tested and approved instead of imported or raw (non-certified) milk. Restaurants and hotels are quite potential market segment for bulk milk deliveries, like offices most of them buy raw milk under contract supply from cattle keepers or distributors. Processors will have an edge if regulations to require hawkers have their products certified comes into force. Competition among domestic producers in the dairy industry is not very strong, the most serious competition is from hawkers and imports to some extent. Competition with imports is growing in UHT and some cold range products in Arusha. Hawkers (of raw milk) however have a number of advantages over processors including price, efficiency and cost-effectiveness. Major competing countries are Kenya, South African and United Arab Emirates. Weaknesses in enforcing common EAC external tariffs have seen imports compete with domestic products pricewise. Distribution of Dairy Products Mara accounts for 39.5% of the national milk processing capacity, in 2008 they operated at 20.9% contributing 32.9% of the processed milk. Tanga has 14.73% of the total installed capacity, it operated at 49% accounting for 28.8% of the national output. Arusha processors with 17.98% of the national capacity contributed 7.5% of the volume of processed dairy products. Iringa contributed 9.0% from its installed capacity that makes 6.23% of the national capacity operating at 36.4% capacity utilisation. Dar es Salaam accounted for 9% of the total processed output, it had 9.3% of the national installed capacity operating at 24.2%. The major markets are Dar es Salaam, Arusha, Moshi and Mwanza, if operating capacity of the plants is increased the transport cost to the markets becomes less significant. The challenge at present is low volumes, to improve the transport services some companies have hived off the management or ownership of transport services.

Survey on Dairy Products Market in Tanzania

viii

Lack of cooling facilities at retail point is another major constraints facing distribution of milk, most retail shops use refrigerators meant for households, they are not transparent and are mixed with many other products. Some processors are planning to invest in refrigerators it is an important strategy in projecting their brands in the market. Many shop keepers feel cold range dairy products are very risky and are not willing/ready to stock them, education and efficient supply system can help alley this fear. The issue of quality deterioration has been identified to be less significant, very few complaints were reported by retailers, of the very few complaints, quality deterioration before expiry date was the most referred to. Information message to the consumers about the products is very limited as none of the companies do serious promotion, TFL has the highest number of posters in Dar es Salaam and Dodoma. Brookside UHT milk is the most conspicuous dairy product. The processors employ multiple channels but the dominant is the processor-agent-retailer-consumer setup that gives the processors a good balance between control over supply chain and outreach. Many processors however complain of agents being not consistent in delivery and or pricing undermining retailer royalty. To overcome this, some processors have their own depots as agents to moderate the supply behavior while others are contemplating to enhance the monitoring of agents. Among the challenges facing channel management include shortage of transport equipment adapted to various channel and market segment. The optimum truck size for distribution of goods within the urban areas is about 500 – 2,000kgs, bicycles are being used though the narrow margins has rendered this option not very attractive. Milk Processing On the overall milk processing activities in Tanzania are not well developed, the total operable1 installed capacity attends to hardly 7.1% against about 25% in Kenya. International Dairy has a capacity of 10.000 l/day and is at present processing 3.000 l/day. Major products processed are Mtindi in 500 ml sachets, Yoghurt in cups of 250 ml and 500 ml and Cheese (cheddar, mozzarella and feta). Arusha Dairy processes 2.000 l/day, the equipment have a 500 l/hour capacity installed. The major products are full cream pasteurized milk in 500 ml sachets, low fat pasteurized milk in 500 ml sachets, Mala in 500 ml bottles or 500 ml sachets, Flavoured and plain yoghurt in 500 ml sachets, Gouda cheese in 500g blocks, Butter/cream and loose (unpasteurized) bulk milk. Brookside has closed down for lack of raw milk, the installed capacity is 45.000lpd. The facilities are used to store imported dairy products from Brookside Kenya like UHT, mala, cheese and butter. Musoma Dairy overall capacity is approximately 40,000lpd, used for UHT, Yoghurt, Mtindi, Butter and Ghee production. Its major output shall be UHT (70% of the capacity). Mara Milk has a capacity of 16,000lpd, besides the UHT, it produces pasteurised milk, Mtindi and Ghee. The plant UHT unit had stopped working waiting for experts from China. Presently TFL processes about 30.000 l/day, the product mix is pasteurised milk in plastic sachets (500 ml and 250 ml), Mtindi in plastic sachets (500 ml and 250 ml), Yoghurt in cups (250 ml and in bulk), Fresh cream in cups (250 ml and in bulk), Mozzarella cheese in

Survey on Dairy Products Market in Tanzania

ix

packages of 2 kg and 500g and Butter and ghee both in bulk primarily for bakeries. It is currently opening up markets in other parts of the country including Dodoma, Arusha, Kilimanjaro, etc. Tan Dairies has a 10,000 lpd plant, it produces pasteurised milk (250 ml and 500 ml), Mtindi (250 ml and 500 ml) and yoghurt (250 ml) and Mozzarella cheese. The plant faces severe milk supply shortages during the dry season because it relies in a drier milk supply belt. The biggest challenge facing processing plants are frequent power cuts, limited number of dairy specialists in the labour market as many have been forced to hire from Kenya and abroad, very diverse technology even within one production line and taxation that penalise Tanzanian producers. Conclusions Seasonality of milk supply in the market has a high impact on processors cash flows, milk supply can drop to as low as 30% of the volume during flush period pushing prices to the extent that it does not make sense for processors. Hawkers are and will continue to play a dominant role in milk marketing and distribution and giving the formal milk marketing stiff but unfair competition. They however are a blessing to the farmers as they are quite close to them. It is not very evident from organizational setups of many processors whether it is the market that is driving the business or it is the production that drives the business. There are little initiatives to learn from consumers and retailers as good marketing practices recommend. None of the processors has been promoting the products at present because of first lack of production capacity, Tommy Dairy and Cowbell had in the past used media campaign to improve the market position of their products. Cases of products with poor quality might seem to be low as indicated by retailers, however many consumers may not provide the feedback under the knowledge that the feedback won’t change the status quo. Dairy products have unitary own-price elasticity, on the overall prices for dairy products are high that might be related to low consumption of processed dairy products, Production cost structure and consumer-unfriendly margins are some of the major reasons for relatively higher prices of products. Retailers wield more power in setting consumer price and have been found to penalise local UHT by selling at the same price as imported ones.

Dairy products excluding those “Specially prepared for infants” enjoy a protection from a 60% duty and a VAT of 18% making a protection rate of 78% of CIF value. The analysis for UHT however shows that under the cost structure in Tanzania CIF prices will have to be abnormally low to arrive at a retail of Tshs 2,500 per litre at a supermarket. This suggests weaknesses in enforcing duties at our border/entry points.

Recommendations Stabilizing milk supply in the market: In the short run, is proposed that TAMPA work with TDB to seek a stop-gap concession to import powder milk for reconstitution during the dry period to improve the opera. Processors should request for a 78% tax waiver for the quantities needed by each processor per annum, the proposal should certainly indicate how to protect the arrangement against abuse. In the medium term, processors should assess the viability of cheaper, easy to operate and scalable autoclave technology for production of sterilized (long-shelf life) milk products. In the long-run, the Government in collaboration with producers and

Survey on Dairy Products Market in Tanzania

x

processors should work out a programme to improve farmers’ capacity to produce milk during dry season. Improving the Product Mix through Linkage with Smallholder Farmers: Ways to give value to the milk that does not reach the market should be looked into, a good case will be cheese that could be extracted by farmers, improved, branded and marketed by processors. To improve quality the project could be linked with institutions like Sokoine University. Improving Capacity of firms to Undertake Marketing: Any support to train and re-train managers on marketing strategies in a competitive environment will be quite useful as the tendency now with many is more about selling than marketing. Other topics could include organizing, monitoring, supporting agents and retailers and market information. For retailers the education could focus on display, storage, hygiene, customer care and information management. Market Promotion; There is a need to seek support for promoting milk consumption through messages based on medical facts, the funding of generic messages to promote consumption should be funded by the Government as it will benefit every stakeholder. Some companies are looking for funds to put their brands in the market. Support in terms of resources to launch such campaigns using TV, radio and other media will be plausible and effective. Stimulating Demand through Appropriate Pricing Processors need to keep a close eye on prices as they stifle demand, affect sales, it is possible to promote flavoured milk and can promote yoghurt as a market entry product instead of the current context that it is a high income consumer product. Yoghurt can work as brand-flag-carrier for long term recognition as the main consumers are the children. Successful promotion that targets children is more effective as they wield power in decision making for most urban families. Improving Distribution: A number of issues are recommended: -

To achieve cost effectiveness in transporting dairy products processors especially in the Lake Zone could collaborate to make joint shipments

The initiative by the actors to have a dedicated location is a novel one, to minimize investment costs, it should be designed to park reefer containers. The arrangement can learn from common storage and logistic facility owned by Tanzania Horticulture Association (TAHA) members.

Education on channel management among agents will be useful as agents have cited as the cause of irregular deliveries hence eroding the supply chain trust and brand loyalty.

A sector development fund would have been ideal to enable actors (not necessarily processors) access technologies and facilities such as milk collection centres, trucks, refrigerators, etc. in the context of poverty reduction.

Seek for Tax Exemption. Tanzania firms are less competitive because of inherent cost structure of the industry and unfavourable tax regime, efforts by TAMPA and TDB to seek for zero rating all inputs into dairy business should be stepped up. Further, given the nascent nature of the sector it is recommended that actors seek VAT exemption in dairy products that are “wrongly perceived as non basic dairy products like yoghurt.

Survey on Dairy Products Market in Tanzania

1 Niras Finland Oy

1.0 INTRODUCTION

1.1 Background

Tanzania has the third largest herd of cattle in Africa after Sudan and Ethiopia, it is estimated in 2008 to have 18.8 million heads of cattle. The traditional Zebu makes 96.24% while the remaining 3.76% is of improved breeds (MMA, 2007). Between 2001 and 2005 the livestock population grew at an annual rate of 2.2% [MMA, 2007], RLDC reported in 2009 that the sector is growing at a rate 2.1% percent per annum [RLDC, 2009]. In 2008 the livestock sector contributed 3.8%2 to the total gross domestic product (GDP). According to the Ministry of Finance and Economic Affairs (MFEA), in 2008 Tanzania produced 1,664 million litres of milk. It is reported that 90% of the raw milk is consumed at the point of production, hence 10% i.e. 166.4 million litres is marketed. Of the marketed quantity from local production, the Ministry indicates that 90% (that is 149.76 million litres) is distributed through informal marketing channels and the remaining 10% of the marketed milk or 16.64 million litres is marketed through formal channels (Guardian, November 23rd, 2009). Assuming the population of Tanzania in 2008 was 40.67 million [MFEA] the implied annual consumption per capita is therefore 40.6 litres. This compares favourably with 31 litres reported by Scanagri/Business Care Services in 2005.Citing the Agriculture Sector Review MMA [2007] notes however that milk consumption curve over time is not a smooth one, in fact it fell between 2005 and 2007 from 40 litres to 39 litres respectively. A study by Astroproject Association in 2009 that covered Dodoma, Manyara, Morogoro, Shinyanga, Singida and Tabora indicated that output per traditional cattle is as low as 0.5 litres per lactating day/cow, Business Care Services Limited (2008) reported 2.7 litres from a baseline survey for 13 districts3. Despite all the odds facing the dairy sector, a consensus that should be the major driver in the development of the sector is stated in RLDC Strategy which states that:-

If adequately linked to the markets, the dairy sector can make a considerable contribution to poverty alleviation for the cattle keeping rural households in the country.

[Dairy sub-sector Development Strategy, 2009]. The dairy sector accounts for 30% of livestock GDP valued at USD 262 million equivalent to Tshs 300 billion (RLDC, 2009). The other way to look at the value of the dairy industry at farm gate is to extrapolate the data from the Ministry of Finance and Economic Affairs [MFEA], with a farm gate price of Tshs 300/per litre, the value of milk can then be estimated to be worth Tshs 499.2 billion or USD 372.54 million. The value should increase with value addition upstream.

2 At 2001 constant prices. By Ministry of Finance and Economic Affairs, June 2009. 3 Districts of Meru, Monduli, Iringa Rural, Mbarali, Mbozi, Mbeya Rural, Mufindi, Njombe, Kyela, Morogoro Rural, Kilombero, Namtumbo and Songea Rural.

Survey on Dairy Products Market in Tanzania

2 Niras Finland Oy

When explaining the industry structure, there is an adjustment to the volume of milk marketed through formal and informal channel. According to the Ministry of Livestock and Fisheries Development’s 2009 Budget Statement, Tanzania had an annual installed milk processing capacity of 353,100 litres per day (lpd) if Brookside Tanzania Limited (with a 45,000lpd) capacity is included. The milk processed was 88,440 lpd or 32.28 million litres. Brookside was reported to have worked at 2,000 lpd. If we include Brookside the installed capacity can absorb 7.75% of domestically produced milk. On the overall, in 2008 processing plants operated at about 25% of their capacity producing 88,440lpd or 32.28 million litres per annum, this is 1.94% of the total milk produced in Tanzania. Relaxing the definition of formal marketing to include non-processed but tested and sold in hygienically approved and organized environment4, the formal channel may be accounting for more than 2%. In summary the computation is as follows:- Table 1.1.1 An Overview of the Structure of the Milk Sector In million

Litres Percent

Total milk available 1,690.14 100.0%

From imports 26.14 1.5%

Total domestic production 1,664.00 98.5%

From traditional cattle 1,164.80 68.9%

From improved breeds 349.44 20.7%

On the farm consumption1 490.88 29.0%

Available raw milk for marketing 1,173.12 69.4%

Formally marketed raw milk2 32.28 1.9%

Informally marketed from domestic production 1,140.84 67.5%

Installed capacity for processing 128.88 7.6%

Milk processed domestically 32.28 1.9%

By large processors 27.27 1.6%

By small processors 5.02 0.3% Main Source: MF&EA, ML&FD 1 From RLDC comment on feedback, the Consultant is also of strong opinion that around 30% may be consumed by livestock keepers in form of raw, sour or ghee. 2 Note that the MF&EA reported that formal market makes 1% of milk produced in Tanzania, however the operating capacity in 2008 suggests a higher percent of more than 19.4%. 4 A good example is in Mbeya where dairy farmers in Rungwe have organised distribution networks for bulk milk in Mbeya City following to good milk handling regulations but may not be appearing under formal marketing channel..

Survey on Dairy Products Market in Tanzania

3 Niras Finland Oy

1.2 Study Objectives, Outputs and Deliverables

This Milk Market Study builds upon past works that have largely addressed challenges facing the dairy sector in production and marketing areas, many organizations have studied production and marketing (in broad context) to mention but a few, they include the Ministry of Livestock and Fisheries Development, the Ministry of Industry, Trade and Marketing, TAMPA,

Figure. 1.1.1 An Overview Map of the Dairy Sector

Survey on Dairy Products Market in Tanzania

4 Niras Finland Oy

UNDP/TetraPak, SNV, Rural Livelihood Development Company/Astroproject, Land O Lakes, etc. The key research questions in this study have been; Firstly, if Tanzanians in 1980s and early 1990s then with a population of about 26 million people (Population Census, 1988) were able to absorb about 400,000lpd of processed milk from Tanzania Dairy Limited plants (then located in Arusha, Tanga, Musoma, Tabora, Dar es Salaam and Mbeya), why is that at present milk processing plants with about 15% to 20% of the early 1990s capacity are finding it difficult to profitably sell their products? Consumption of processed milk was expected to grow as a result of urbanization rate, population growth, economic growth and increase in educated population. Secondly, in another dimension of the paradox, why there is an increase in imports both in volume and value while local processing capacity had been shrinking? Between 2004 and 2009 imports year-on-year growth has averaged at 9.41% in volume, this is higher than the economic growth that over the period has averaged at 7.28%. Kurwijila (FAO, Undated) estimated that in 1990s there was a supply gap of about 12.5 million litres of milk per annum in Dar es Salaam alone. The local capacity was able to meet about 33% of the demand (TDL/AGRIS, 1994). In sum, the local dairy firms’ market share has been rather staggering while imported products have experienced significant growth. The question then is; how are processors connected to the end markets because principles of competitive value chain development states that

“End markets are a key driver of value chain growth and development. End-market demand informs supply chain actors who in turn build capacity to meet demand and compete in the marketplace. ….. In general, however, successful value chain development relies on a flow of information, requests and purchase orders from end markets. Thus market-led (or market-driven) development should start with end markets, whether they are local, national, regional or global.” and that, “It is one thing to argue for connections with markets; it is another to look to – and accept – demand as the engine of the process. Understanding demand and recognizing that demand pulls supply is a central operating principle. … Production is focused on what can be sold, not on selling what can be produced” [http://www.apps.develebridge.net/amap/index.php/End_market, October 15th, 2009 at 14:00hrs]

In view of the above, RLDC and TAMPA are of the view that there might be some strong reasons/factors that hinder local processors from tapping into the market estimated to be worth of tens of millions of USD per annum. While addressing the situation above, a number of factors needed to be looked into, they included the market structure particularly demand and supply. With the market analysis attempt has been made to relate consumers buying pattern and ability, prices, competition from domestically produced and imported goods. On the supply side, the analysis has looked at competitive elements that include product mix and technology and how they relate to demand. It is pertinent that competitiveness of local products is benchmarked against other successful countries and to draw lessons there from. A firm can gain sustainable competitiveness either by being cost effective in the industry or and differentiating its products

Survey on Dairy Products Market in Tanzania

5 Niras Finland Oy

by targeting certain market segment. Also critical in today’s market is efficiency in distribution systems as well as branding efforts for sustaining and growing market share. RLDC initiated this market study to zoom into distribution aspects of the dairy products value chains in Tanzania. The objective of the study had been to find out the constraints that face the dairy market particularly in the distribution and make practical recommendations to processors so that they can generate strategies to become competitive in the market. Increased marketed volumes are expected to pull milk from farmers who in turn will improve their incomes from reliable market of milk. However in order to have a complete picture the study had to cover other facets of the market including its structure, imports and export, estimation of demand for milk and processing capacity. More information on the study objective can be found in the TORs attached as Annex IV.

1.3 Scope and Methodology of the Study

The major focus of the study is to help medium and large dairy processing plants to understand and use the findings in improving access to markets for their products. The initial phase of the survey involved consultations with RLDC in Dar es Salaam and Dodoma and later with TAMPA and Tanzania Dairy Board. A review of various reports was done before going into the field. Discussions with processors took place between February 8th and 16th , 2010 in Musoma with Mara Milk Limited and Musoma Dairy Limited, in Arusha with Arusha Dairies Limited, International Dairies and Brookside Tanzania Limited, in Tanga with Tanga Fresh Limited) and in Dar es Salaam with Tan Dairies Limited. Apart from consulting the processors, a parallel exercise took place with milk retailers to learn on the distribution and consumer behaviour. Two research assistants were engaged, one who worked closer to the team collected information in Musoma, Mwanza, Shinyanga, Singida and Dodoma. In Arusha the coverage of traders was done by a local research assistant after being trained by the Consultant. A total of 25 outlets stocking milk were consulted during the study, to get a fairer opinion outlets covered outlets in areas designated as low income, middle income and city/municipal centres. A questionnaire was used to collect information from traders and a checklist was used for processors (See Annex V a. and b.). The estimation for demand of milk in Tanzania relied on the review of past studies and data particularly those from 2007 Household Budget Survey. As for lessons from other countries, the study drew significantly from Kenya partly because it has a well developed dairy industry but also because of the EAC Common Market subjects Tanzania to an emerging single market.

1.4 Study Limitations

There were few issues that limited the study comprehensiveness particularly in terms of geographical coverage and depth as highlighted below. Timing of the assignment: The Team worked was in the field between February 7th and 15th, this is the flush period thus it was expected that processors will operating at a relatively higher capacity. Unfortunately, New Musoma Dairy Ltd had stopped production pending the injection of working capital from shareholders and installation of the new Board and Management. Data availed shows that production had stopped from December 2009. At Mara Milk Limited

Survey on Dairy Products Market in Tanzania

6 Niras Finland Oy

production of UHT had been stalled due to technical a problem in the aseptic packaging unit. In Arusha Brookside had stopped production since 2009. International Dairy Limited and Arusha Dairy Limited are operating though at a lower capacity (at 30% and 40% of the optimum capacity5 respectively). At Tanga Fresh Limited operations were on going at a normal level. The challenge had therefore been how to attribute the obtaining performance level to either market-related (exogenous) constraints or firm level (endogenous) technical and managerial constraints. The Client had directed the Consultants to focus on distribution. Area covered vs national picture: The TOR had wanted to obtain a national picture of the constraints facing the distribution of dairy products. Given the limited time, the Consultant visited and obtained in depth inputs from New Musoma Dairy Limited (NMDL), Mara Milk Limited (MML), Brookside Tanzania Limited (BTL), Arusha Dairy Limited (ADL), International Dairies Limited (IDL), Tanga Fresh Limited (TFL) Tan Dairies Limited (TDL). A limited sample of retailers in Musoma, Mwanza, Arusha, Shinyanga, Singida, Dodoma and Dar es Salaam was used. ASAS and CEFA were interviewed by phone which limited information gathered. Import Data: While it is important to recognize the efforts done by Tanzania Revenue Authority to disaggregate dairy products for recording imports, there is high prevalence of products that were not properly classifiable, e.g. the dairy products classified as “Specially prepared for infants” (code number 04022110), goods worth 61.9 million were able to be placed under this code while goods worth Tshs 394.3 million were classified as “other” (code number 04022190) below the category. Inability to classify properly reduces the accuracy of rationalized volume of imports in milk equivalent that is used as a common denominator.

1.5 Organization of the Report

This report has four main chapters. As noted hereto, the first chapter is the introduction that explained the background of the sector and the study. It also contains the scope and methodology. The findings are placed in Chapter Two where there are three sections, section one looks at the market structure that includes demand and consumer behavior, section two addresses distribution that is the core subject of the study while section three looks at processing of dairy products. Chapter three conclusions and recommendations. Note that tables, figures and other exhibits have been numbered according the sections they belong to.

5 Optimum capacity is what the processor can or had achieved when the conditions were favourable, it is normally lower than the installed or rated capacity.

Survey on Dairy Products Market in Tanzania

7 Niras Finland Oy

2.0 FINDINGS

2.1 Dairy Market Structure

The dairy market structure start by looking at products available in the market then gets back to learn how the market needs are being addressed by processors in terms of product mix and volume demanded. Thereafter the section looks at consumer pattern and demand in order to establish quantity demand demanded. Issues to do with prices are discussed under this section.

2.1.1 Product Range in the Market In the market there is a wide array of dairy products, however from domestic production point of view the product range is relatively narrow, there are fermented milk, (mtindi/mala), pasteurized fresh milk, UHT milk and to a small extent, yoghurt, cheese, butter and ghee. Mtindi, cultured milk or mala: The different names are used at different regions but basically the process is the same. To the pasteurised milk a bacteria culture is added. When the acidity in the milk has reached the required level the mtindi is cooled and ready for sale. The shelf life under refrigeration is normally 18-20 days. The texture of the product can vary considerably from smooth uniform to the type with distinct lumps in it. The difference is due to the physical handling of the product. Mtindi is often packed in sachets. But also gable top cartons and bottles are used. UHT (ultra high temperature) milk: The milk is treated at 140 degree Celsius for 3-4 seconds. After this process the commercial sterile milk is aseptic packet. The packing is normally packet in special cartons (blocks), with a shelf life of 6 -12 months without refrigeration. The UHT milk can also be packet in plastic sachets or bottles. Because of the high temperatures used in processing there is a slight difference in taste compared to pasteurised milk. But as most milk irrespective of treatment is being boiled before use the change in taste is probably not being important in marketing. Pasteurised milk: The milk is only treated at 72 degree Celsius in 15 seconds before being packet in gable top cartons or in plastic sachets. Because of the lower temperatures the milk is not sterile and the shelf life is reduced to 5-7 days under refrigeration. Yoghurt: Yoghurt is, like mtindi fermented milk. The cultures used require a constant incubation temperature and in order to get a more thick and creamy texture about 5 % milk powder is added. Yoghurt is often sold in cups of various sizes with addition of flavours or processed fruits. Cheese: There is a large number of cheese types around the world. The most common types produced in Tanzania are Cheddar and Mozzarella. To process cheese you require about 10 l of milk to make one kg of cheese, for Cheddar a little more and for mozzarella a little less. Cheddar cheese requires a ripening period of several months, while mozzarella cheese can be marketed right after processing.

Survey on Dairy Products Market in Tanzania

8 Niras Finland Oy

Cream: Both full cream milk, mtindi and yoghurt require standardisation of the milk. Normally the standard milk will contain 3.2 % fat. As most milk contains more fat, the surplus will be separated as cream. The cream can after pasteurisation be sold as fresh cream or it can be fermented to sour cream. Normally there is either 36 % or 17 % fat in the cream. Butter: The cream containing 36 % fat can be processed into butter. The cream is sometimes fermented with bacteria cultures or used as it is (sweet butter). Depending on customers preference salt can be added. After being processed in the butter churn it is ready for packing. The liquids remaining (butter milk) can be used as refreshing drink. In the butter there will be approximately 86 % fat, the rest being water. Ghee (butter oil): The butter can be turned into ghee simply by evaporating the remaining water in the butter (about 16 %). Heating the butter needs to be done in gentle way otherwise the butter oil will be dark and have a burnt smell. Other dairy products: There are numerous other imported dairy products on the shelves of the supermarkets. Some of them could be fairly easily to be processed locally like sour cream and cottage cheese. The products can be made without sophisticated and expensive equipment and if a market is emerging the opportunity should by all means be utilised. Very special cheese types requiring experienced staff to process may appear attractive when looking at the prices to be obtained, but the potential market will be limited and economies of scale are not likely to be reached. But development of dairy products specifically appealing to the Tanzanian consumers should be encouraged. About 54% of the capacity of processors is used to produce cultured milk, the percentage is even higher when NMDL is taken out because more than 70% of its capacity will be for UHT. In a bid to add value many processors have increased the volume of yoghurt, it accounts for more than 12% of the capacity6. In international trade, dairy products are generically categorized and coded to facilitate information aggregation. 6 Excluding figures from ASAS and CEFA who were not covered

Figure 2.1.1 Main Dairy Industry Products in Tanzania based on Installed Capacity

Survey on Dairy Products Market in Tanzania

9 Niras Finland Oy

In rationalising imports of dairy products into liquid milk equivalent (lme) for the purpose of having a common denominator, conversion ratios were applied at the four digit code level. In 2009 dairy products under milk and cream, concentrated or sweetened account for 68% of the volume of imports, non concentrated or sweetened milk and cream made 16% and cheese and curd at 6%. Butter and other fats and oils derived from milk accounted for 5%, buttermilk, curdled milk and cream, yogurt, etc were at 3% and whey and other natural milk constituents making 2%7.

2.1.2 Consumption Pattern The analysis of consumer pattern relied heavily on data mining from 2007 HBS that surveyed 10,460 households of which 4,935 consumed dairy products during the year. Hence, about 49% of the Tanzanians consume milk8. NOTE that the HBS data recorded expenditure for one year in selected households in the national master sample. The households were classified based on assets in quintiles. The foregoing analysis indicates expenditure by quintiles.

2.1.2.1 Products Consumed Based on HBS, the widely consumed dairy product is fresh milk where households covered show that Mtwara Rural, Ruvuma Rural, Dar es Salaam (Rural) and Lindi had the highest, above 98% of the households who reported to consume dairy products use fresh milk. In the second tier of between 90% and 98% are Pwani Mixed, Arusha Rural, Manyara Rural, Dodoma Urban, Ruvuma Mixed, Mara Rural and Mixed, Dar es Salaam Mixed, Arusha Mixed, Dodoma Mixed, Morogoro Mixed, Mara Urban, Iringa Mixed and Tabora Urban. It can be seen that consumption of fresh milk intensity along the rural, mixed, urban spatial view forms a concentric circle with an exception of Tabora and Dodoma, in most regions areas in the rural and peri-urban (mixed) have a higher percentage of people consuming fresh milk.

7 In order to understand the aggregate supply of processed dairy products in the market one has to add imports with domestic production, this is however difficult because the classification of products by TRA differs with the categories in market. 8 The figure needs reconfirmation from NBS

Figure 2.1.2 The Average Composition of Dairy Products Imported in Tanzania by Volume (2004 – 2009)

Survey on Dairy Products Market in Tanzania

10 Niras Finland Oy

One important conclusion from this scenario is that households in rural, peri-urban and urban are aware of and use fresh milk because of the availability and efficient hawkers-based distribution system.

2.1.2.2 Fermented milk Fermented milk is the second most important form of dairy products, it ranks high in Rukwa, Mbeya, Kigoma, Tabora, Singida, Dodoma, Manyara and Morogoro. Part of the reasons for this pattern could be low capacity to move the milk to the market letting a higher percentage to ferment. Regions with higher processing capacity of Arusha, Tanga and Mara are low in the list of main consumers of fermented milk most likely because some considerable amount is hauled for processing.

2.1.2.3 Packed Milk Perhaps of key interest with the HBS is the situation with packed milk, this category is that of processed and packed milk. Data show that consumption of packed milk is very low albeit in urban areas, the national average is 0.078% of those who reported to consume milk. The highest slot is held by Dar es Salaam Urban where 1.148% reported to consume packed milk. It is followed by Mara Urban by 0.78%. Unexpectedly Ruvuma Mixed had a third position, Mwanza Urban at a fourth place with 0.709%. Others areas were Tabora Mixed, Tanga Urban, Mwanza Mixed, Morogoro Mixed and Arusha Mixed. The figures above have significant implication on market targeting for major urban areas. The low uptake of packed milk as compared to fresh milk is expected because: -

i. Milk has unitary own price elasticity hence a premium of more than 100% for processed milk over unprocessed should certainly curtail consumption of packed products.

ii. Consumer perception that fresh milk is “not baptized” – is sold in its natural form i.e. has a higher fat and more rich in flavour. Also that it is not homogenized which both changes the taste but also make the fat invisible.

iii. Competition with hawkers that have relatively more efficient distribution network compared to processors and their agents in terms of outreach makes fresh milk more accessible.

2.1.2.4 Locations where households buy milk products in Dar es Salaam, Mwanza, Arusha and Dodoma Urban.

Kiosks are the most important point of sale for processed milk in Arusha and Dar es Salaam. In Dodoma due to limited presence of specialised outlets consumers depend on gulio. In Mwanza

Table 2.1.1 Percentage of Households Consuming Packed Milk (2007) Region Urban

/Rural Percent

D'Salaam Urban 1.148%Mara Urban 0.787%Ruvuma Mixed 0.769%Mwanza Urban 0.709%Tabora Mixed 0.355%Tanga Urban 0.236%Mwanza Mixed 0.189%Morogoro Mixed 0.114%Arusha Mixed 0.055%National Average 0.078%

Source: HBS 2007: NBS

Survey on Dairy Products Market in Tanzania

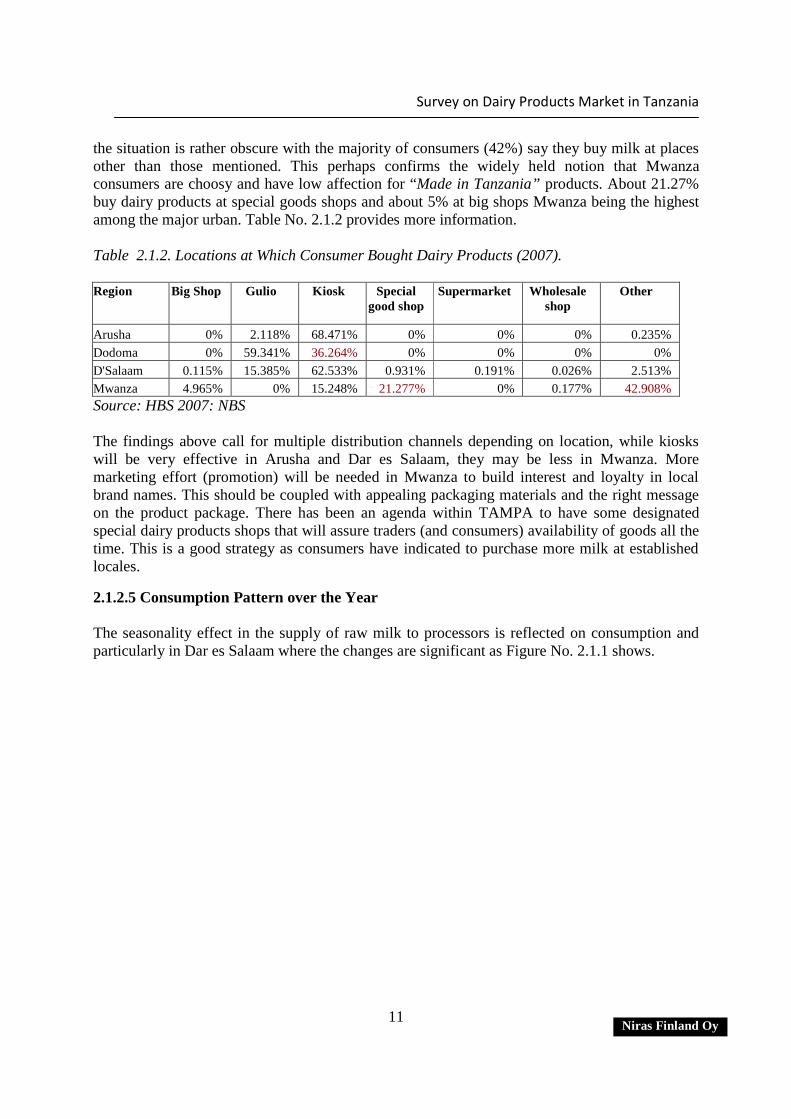

11 Niras Finland Oy

the situation is rather obscure with the majority of consumers (42%) say they buy milk at places other than those mentioned. This perhaps confirms the widely held notion that Mwanza consumers are choosy and have low affection for “Made in Tanzania” products. About 21.27% buy dairy products at special goods shops and about 5% at big shops Mwanza being the highest among the major urban. Table No. 2.1.2 provides more information. Table 2.1.2. Locations at Which Consumer Bought Dairy Products (2007). Region Big Shop Gulio Kiosk Special

good shop Supermarket Wholesale

shop Other

Arusha 0% 2.118% 68.471% 0% 0% 0% 0.235% Dodoma 0% 59.341% 36.264% 0% 0% 0% 0% D'Salaam 0.115% 15.385% 62.533% 0.931% 0.191% 0.026% 2.513% Mwanza 4.965% 0% 15.248% 21.277% 0% 0.177% 42.908% Source: HBS 2007: NBS The findings above call for multiple distribution channels depending on location, while kiosks will be very effective in Arusha and Dar es Salaam, they may be less in Mwanza. More marketing effort (promotion) will be needed in Mwanza to build interest and loyalty in local brand names. This should be coupled with appealing packaging materials and the right message on the product package. There has been an agenda within TAMPA to have some designated special dairy products shops that will assure traders (and consumers) availability of goods all the time. This is a good strategy as consumers have indicated to purchase more milk at established locales.

2.1.2.5 Consumption Pattern over the Year The seasonality effect in the supply of raw milk to processors is reflected on consumption and particularly in Dar es Salaam where the changes are significant as Figure No. 2.1.1 shows.

Survey on Dairy Products Market in Tanzania

12 Niras Finland Oy

Figure 2.1.3. Pattern of dairy product consumption over the year

The higher variation in Dar es Salaam may be attributed by its dependence on processed milk and as processors scale down production in August through November Dar es Salaam is hard hit. It is important therefore that processors continue to work hard to minimise the seasonality effect on the end market. The shortage is a lost market.

2.1.3 Other market segments

2.1.3.1 Offices The habit of using milk at work place dates back during the dominance of parastatal companies in the 1970s and 80s, it was a policy of almost all organizations that they should provide milk or and white tea to workers. The culture has however waned with the demise of parastatal organizations, even within Government offices there is no policy for such a service. For example at Arusha Regional office workers take about 300mls of milk. At Musoma Hospital milk supply to staff has been scaled down, only the theatre section is provided with milk, maternity and child sections used to get milk until 2007. There is a mixed feeling about Government office because they buy on credit and payments are not certain. One processor has had a significant outstanding bill with the army. Competition with milk powder at workplace is common, even at Arusha Regional Office about 30% of the personnel take NIDO instead of fresh milk. It will be difficult to estimate the market value of this segment but it could be significant for example one processor has managed to secure a market for bulk fresh milk at workplace that account for about 10% of the daily processing capacity. Processors need to make more effort to approach, raise awareness and market their fresh milk to potential volume of this segment.

Survey on Dairy Products Market in Tanzania

13 Niras Finland Oy

2.1.3.2 School Feeding Programme Among the strategies that was used to develop the sector in Kenya was to create a generation of people who value and consume milk, school feeding programmes were instituted. There have been efforts in Tanzania to replicate the strategy by stakeholders. The basic constraint to such programme at present will be the capacity to produce, haul milk from farmers to processors, process and distribute it equitably throughout the country.

2.1.3.3 Restaurants and Hotels This is a potential market segment for bulk milk deliveries, at Musoma some hotels are supplied with milk from processors (at least Afrilux Hotel). There are 11 large hotels that could order not less than 20 lpd, 7 middle level hotels that can consume around 10 lpd and 49 restaurants with a potential for at least 10lpd. The combined demand for this segment in Musoma alone could be more than 800 lpd. The quantity is significant if one takes into account district centres and adjoining cities/towns (e.g. Mwanza for Mara based processors). However some hotels e.g. New Mwanza Hotel procures milk from farmers or traders and process (skim) the milk in house. To a large extent processors will have an edge if regulations to require hawkers have their products certified comes into force.

2.1.4 Demand Estimates for Household Segment

Estimating demand for dairy products in Tanzania has been a big challenge, even when one would like to assume that all the off take milk is consumed it is still not enough to ascertain the amount consumed because of non-reliability of production data (as indicated in Scanagri/BCS [2005]. As noted in Section 1.1 above the country processes 32.28 million litres per annum, imports add into the market an equivalent of 29.793 million litres, if the two sources are added imports account for 48% of the market for processed dairy products in Tanzania. An increasing trend on imports show existence of unfulfilled demand. Citing the EAC/COMESA, DA&PPDC (2006) reported that in 2003 Tanzania had a deficit of 386,040 mt of dairy products then. Assuming that the demand grows at a natural rate of the GDP growth, such a deficit, in 2009 the deficit would be around 581,000mt indicating a huge opportunity in the dairy industry.

Since most processors are targeting Dar es Salaam, an attempt to compute the market size has been done based on 2007 Household Budget Survey data. It is estimated that the city with an estimated population of 3.2 million present a market worth Tshs 2.68 billion per month or Tshs 32.12 billion per annum as indicated in Table No. 2.1.3.

Survey on Dairy Products Market in Tanzania

14 Niras Finland Oy

Table 2.1.3 Estimation of Market Size for Processed Dairy Products in Dar es Salaam in 2007

Mean expenditure per household per month in Tshs 154,904

Percent of household income spent on dairy products*

Fresh milk 1.24

Cultured/fermented milk 0.7

Cheese 0.45

Powder milk 0.03

Packed milk 0.01

Total percentage 2.43

Expenditure on Dairy Products in Tshs/month 3,764.17

Estimated number of households in Dar es Salaam 720,000

Total market value per month in Tshs million 2,677

Total dairy product market per annum in Dar es Salaam in million Tshs 32,121

Total dairy product market per annum in million USD 24.84 Some informed opinion has generated a rule of thumb that the combined demand for other urban areas in Tanzania will be twice that of Dar es Salaam, it follows therefore that demand for other urban areas will be Tshs 5.353 billion per month or Tshs 64.241 billion per annum. The total demand of milk in Tanzania then could be around Tshs 96.36 billion or USD 74 million. Imports in this regard take just about 11% of the potential market, domestic production is at a base value of USD 27.41 million, the market (unmet) demand for processed milk is thus around USD 40 million per annum.

2.1.5 Demand Behaviour for Processed Milk In their analysis, Weliwita, Nyange and Tsuji [2003]9 they established that foodstuffs like maize, rice, other cereals, pulses, sugar, edible oils, fish, starch, fruits and vegetables, meat, and others are price inelastic while milk and dairy products have unitary elasticity of demand. This finding had been the basis of extending the analysis further to look into the relationship between household income and consumption of dairy products as well as issues around pricing strategies among value chain actors particularly with respect to UHT milk

9 Food Demand Patterns in Tanzania: A Censored Regression Analysis of Microdata in Sri Lankan Journal of Agricultural Economics. Volume 5. No. 1, 2003

Survey on Dairy Products Market in Tanzania

15 Niras Finland Oy

Confirming what has been widely stated as lack of milk consumption culture in Tanzania, Weliwita, et al noted then that milk and dairy products group had the smallest budget share among all food groups. The report further notes that since dairy products have unitary elasticity of own price it imply that people are likely to consume more products when prices drop. The situation seem to have not changed significantly as data for 2007 indicate that the percentage of household expenditure going to dairy products is still small, it was 3.55% in 2001 and was 2.43% in 2007. In order to understand the impact of decreased percentage of household expenditure going dairy products, it is important to measure the aggregate household income between 2001 and 200710.

2.1.6 Price Level and its Impact on Demand Pricing is a decisive factor for business survival or growth, a number of factors need to be looked at before setting prices. The factors include; most important price elasticity of demand, long term vision of the firm, cost structure, degree of competition from both domestic and foreign, price level of similar or close substitutes, legal and policy framework, degree of diversification and integration, etc. Price elasticity of demand. Studies have shown that in Tanzania price elasticity of demand for dairy products is unitary (Weliwite,at. al.) implying decline in price leads to proportionate increase in consumption, so is the converse. Writing about elasticity for consumers in Kenya, Development Associates a/s and PPD Consultants (DA&PPDC) [2006] notes that…

….price elasticity of demand for raw milk was low with respect to low income groups and high with respect to high income groups. This would indicate that increased price of raw milk will not affect the demand for the product by low income groups, but could reduce demand by high income groups. Similarly, price elasticity of demand for processed milk is high for low income groups and low for high income groups. This means that while the price increase in processed milk will lead to reduced demand by low income groups, it will not affect the demand for the product by the high income groups.

The same reports attributes the success in the market of dairy products to decrease in consumer price that resulted from reduction in the cost of packing materials from as the industry shifted from tetra pack to poly pouches where they state that…

It should be emphasized that the processed milk segment is sensitive to price. This explains why the recent reduction on consumer price through the entry of the “pouch” processed milk has led to the dramatic increase in consumption of the relevant brands.

[DA & PPDC, 2006] If we look at price trend for processed milk in Tanzania in dollar terms a litre of processed milk has increased 2.7 times.

10 Data for absolute income in 2007 is available, the 2001 is missing.

Survey on Dairy Products Market in Tanzania

16 Niras Finland Oy

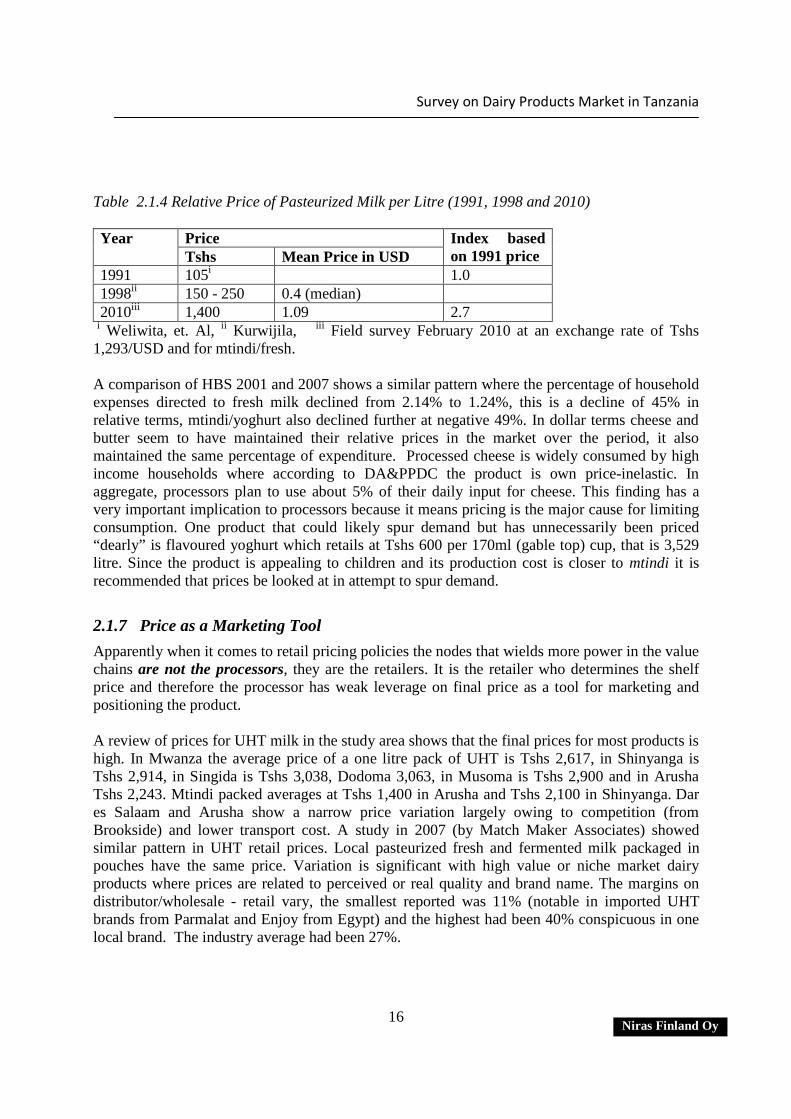

Table 2.1.4 Relative Price of Pasteurized Milk per Litre (1991, 1998 and 2010)

Price Year Tshs Mean Price in USD

Index based on 1991 price

1991 105i 1.0 1998ii 150 - 250 0.4 (median) 2010iii 1,400 1.09 2.7

i Weliwita, et. Al, ii Kurwijila, iii Field survey February 2010 at an exchange rate of Tshs 1,293/USD and for mtindi/fresh. A comparison of HBS 2001 and 2007 shows a similar pattern where the percentage of household expenses directed to fresh milk declined from 2.14% to 1.24%, this is a decline of 45% in relative terms, mtindi/yoghurt also declined further at negative 49%. In dollar terms cheese and butter seem to have maintained their relative prices in the market over the period, it also maintained the same percentage of expenditure. Processed cheese is widely consumed by high income households where according to DA&PPDC the product is own price-inelastic. In aggregate, processors plan to use about 5% of their daily input for cheese. This finding has a very important implication to processors because it means pricing is the major cause for limiting consumption. One product that could likely spur demand but has unnecessarily been priced “dearly” is flavoured yoghurt which retails at Tshs 600 per 170ml (gable top) cup, that is 3,529 litre. Since the product is appealing to children and its production cost is closer to mtindi it is recommended that prices be looked at in attempt to spur demand.

2.1.7 Price as a Marketing Tool Apparently when it comes to retail pricing policies the nodes that wields more power in the value chains are not the processors, they are the retailers. It is the retailer who determines the shelf price and therefore the processor has weak leverage on final price as a tool for marketing and positioning the product. A review of prices for UHT milk in the study area shows that the final prices for most products is high. In Mwanza the average price of a one litre pack of UHT is Tshs 2,617, in Shinyanga is Tshs 2,914, in Singida is Tshs 3,038, Dodoma 3,063, in Musoma is Tshs 2,900 and in Arusha Tshs 2,243. Mtindi packed averages at Tshs 1,400 in Arusha and Tshs 2,100 in Shinyanga. Dar es Salaam and Arusha show a narrow price variation largely owing to competition (from Brookside) and lower transport cost. A study in 2007 (by Match Maker Associates) showed similar pattern in UHT retail prices. Local pasteurized fresh and fermented milk packaged in pouches have the same price. Variation is significant with high value or niche market dairy products where prices are related to perceived or real quality and brand name. The margins on distributor/wholesale - retail vary, the smallest reported was 11% (notable in imported UHT brands from Parmalat and Enjoy from Egypt) and the highest had been 40% conspicuous in one local brand. The industry average had been 27%.

Survey on Dairy Products Market in Tanzania

17 Niras Finland Oy

Consultation with some processors suggested that efforts is needed to empower consumers by indicating recommended prices on packets, this had a mixed feeling because while Unilever has succeeded managed to successfully inform consumers and major outlets are following, Coca Cola, Pepsi Cola and beer manufacturers are finding it difficult to ensure retailers comply to recommended prices. In the case of Coca Cola for example, a distributor has been earmarked a margin of 5.8% and a retailer a margin of 17.8%, the common practice has been to hike the price of from the recommended Tshs 400 to 500 hence elevating their margins to a whopping 32%. Note that these companies wield some power because they even supply refrigerators. To address these challenges the companies have produced smaller 200ml bottles to keep low income consumers. The Cola industry in Tanzania like other major commodities (beer, cement, etc.) is oligopolistic it can survive with the obtaining market dynamics. If local processors can not have a clear competitive edge in the market they may not realize the desired growth path. Considering how important the price is in stimulating demand TAMPA ought to facilitate an industry wide strategy debate to see if there is common interest amongst processors to make a uniform strategy with regard to pricing as a strategy for improving demand as well as countering imports. Care has to be exercised lest people’s opinion is swayed to think cheaper is poor quality. A campaign to instill consumer confidence coupled with rigorous quality assurance mechanism should be agreed and implemented.

2.1.8 Competition

2.1.8.1 Competition among Domestically Produced Products A rapid assessment of retailers in Musoma, Mwanza, Shinyanga, Singida, Dodoma and Dar es Salaam showed that there are no activities by processors geared to edge out one another in the market. All processors acknowledge the existence of low capacity relative to the potential market demand as signified by ever growing imports. Of the eight processors, two have diversified into UHT otherwise for the rest there is a product mix overlap with more than 50% of the capacity dedicated to mtindi/mala. None of the processors is working hard to project its brand name at the expense of others. An observation at Shoprite and BP Petrol Station convenience groceries found out mtindi from Tanga Fresh and ASAS get equal space in the cooler, what exists is more of a consumers’ choice since even small processors (less than 3,000lpd) find market for their products. In some cases larger processors have conceded being outcompeted by small processors because they have managed to adapt their products to consumer preference of full fat milk while larger ones take out a significant amount of fat.

A Hawker in Mwanza Sells up to 40Lts per day at Tshs 600 per litre, purchases the milk at Tshs 300 per litre through a month credit from suppliers month at 300/= per Ltr In order to minimize losses the hawker boils part of the milk that is sold later over the day. Some own lactometers to check density before accepting the milk from suppliers. Hawking is done using aluminium containers on a bicycle.

Survey on Dairy Products Market in Tanzania

18 Niras Finland Oy

The competition that impacts the industry comes from hawkers, they have been mentioned in many reports to be the major impediments to sector growth as it accounts for a considerable volume of milk marketed (90%). Their competitive edge include: - Undercutting processors in consumer price by a wide margin, in Mwanza for example a litre

sells at Tshs 600 as against about Tshs 1,400 i.e. 2.3 times. Flexibility in terms of trade, many hawkers trades on credit on both the supplier and buyer

sides, It has been mentioned also that some hawkers adulterate the milk with water or other

materials (cassava juice was mentioned in Musoma) to increase the volume. They have higher level of versatility in terms of timing consumers preferred time and making

door to door delivery. The margins are hefty hence more rewarding and motivating than those earned by vendors selling processed products. Industry players in Dar es Salaam contend that informal milk channels have an upper hand in delivering milk to all segments i.e. households, restaurants/hotels and institutions. Raw milk sold in Dar es Salaam comes from Kibaha, Chalinze, Bagamoyo, Kigamboni, etc. Wholesale price ranges from Tshs 500 to 600 while retails at Tshs 700 – 800 while pasteurised fresh milk retails at Tshs 1,400. Interviews done in Temeke with restaurants/food vendors confirm that they use raw milk from informal channels.

2.1.8.2 Competition between Domestic and Imported Products Between 2004 and 2009, Tanzania annual import bill for dairy products stood at 25.92 million lme worth USD 4.22 million. In 2009 imports accounted for 1.79% of the national supply, but up the value chain it account for 48% of the processed dairy products end market. The trend shows that imports have been growing at an annual rate of 9.41% per annum, far ahead of the local production (estimated at 6.7% between 2007 and 2008). In 2009 Tanzania imported milk from 37 countries, major ones are South Africa, Kenya, United Arab Emirate, The Netherland, Denmark and Ireland. Others are Australia, China, Cyprus, Egypt, France, Germany, India, Indonesia, Italy, Lebanon, Malaysia, Mauritius, Mauritania, New Zealand, Oman, Pakistan, Poland, Portugal, Saudi Arab, Singapore, Swaziland, Switzerland, Syria, Thailand, Uganda, Ukraine, United Kingdom, United States and Yemen. Annex III provides the list with values.

Figure 2.1.3 Trend of Dairy Products Imports in USD

Source: TRA

Survey on Dairy Products Market in Tanzania

19 Niras Finland Oy

The competition with imported dairy products from EAC countries is expected to grow particularly from Kenya where the sector is bigger, stronger and it seems there is a unified strategy to promote exports particularly to Tanzania and Uganda. Further, Kenya’s vicinity to Tanzania implies they can at short notice enter into cold range products expanding the scope of competition at product level. Already products from Brookside have higher frequency of citation in retail shop in Musoma, Mwanza and Arusha. While the through common external tariff (CET) the EAC market enjoys some through a 60% (80%?) duty there is a strong feeling that some structural constraints to the sector makes it less competitive even with the level of protection. One hypothesis would be that the cost structure in Tanzania is such ineffective that even tariffs of that magnitude can mot work. The second builds on the assumption that the industry is competitive in terms of cost structure, thus, there is weakness in enforcing the well intentioned protection system. The analysis indicate that it is not either or, it could be that the two forces interplay to undercut domestic processors to the extent that even a 60% protection is ineffective. Table 2.1.5 Cost Structure of Processing One litre into Pasteurised Milk packed in Poly Pouch

Tanzanian Firm Kenyan Firm* Variation

(Ke - Tz)

Tshs % Kshs Tshs

Equivalent % Cost of raw milk at factory gate 470 41.59% 20.00 340 52.63% - 130.00 Variable cost 88 7.79% 3.66 62 9.63% - 25.78 Packaging material 50 4.42% 2.30 39 6.05% - 10.90 Total cost at factory gate 608 53.81% 25.96 441 68.32% - 166.68 Transport outward 28 2.48% 1.00 17 3.00% - 11.00 Distribution/retailing cost 145 12.83% 4.00 68 11.00% - 77.00 Total cost 778 68.85% 56.92 526 149.79% - 251.68 Selling price 1,130 100.00% 38 646 100.00%

Source*: DA&PPDC (2006) The table above shows that the cost of processing a litre milk in Tanzania is higher than in Kenya by a significant margin of 48% with the price of raw milk accounting for 51% of the difference. Distribution cost attributes 31% of the difference and processing costs makes 10%. According to actors, the cost of raw materials is high in Tanzania because of dominance of informal marketing activities, less organized milk producers, higher cost of transport due to poor infrastructure and limited access for electricity to power cooling centres. One processor called for industry wide effort to ensure that in the long run producer price stay closer to other countries in the EAC, but indicated that this will require support to farmers from a third party to increase output per cow in order to compensate for loss on price. This strategy could be acceptable if it guarantees a farmer more income through increased productivity of his cow coupled with stable/reliable market. Note that a smallholder farmer in Kenya produces 2.9 ltr/day, Mchau, et. Al (2009) says the average output per cow per lactating day in Tanzania Central Corridor is 0.5litres! Hence, working to improve output is a long-term strategy. Quite

Survey on Dairy Products Market in Tanzania

20 Niras Finland Oy

encouraging, in its strategy, RLDC is going to support actors in the dairy chain in the central corridor to increase output of milk by 4 million litres through facilitating establishment of milk collection centers (MCC), organization and training of producers and supporting producer associations [RLDC Strategy]. Other areas of inefficiency are; transport due to poor infrastructure making per unit cost higher; electricity/power due to higher tariffs and frequent outages; cost of skilled manpower is higher because in Tanzania there are few dairy industry specialists11 caused by shortage of requisite skills has added to the overheads.

2.2 Distribution of Dairy Products

Distribution involves moving dairy products (or stocks or flows) from one market node to another (transportation), warehousing i.e. keeping products in the required conditions with manageable losses in quantity or quality and inventory management particularly receiving and supplying goods based on optimization principles. Effective and efficient distribution is critical because of competition and sophistication of consumers, some companies have emerged successful in the market because they have robust distribution system. In this section we look at how distribution of processed dairy products is organized and its effectiveness. The section looks at the spatial aspects between production and market nodes, then the organization and management of distribution.

2.2.1 Spatial Spread of Production Capacity and Market In its effort to industrialize, the country in the 1970 identified and earmarked locations with comparative advantage either in resource or market for establishment of industries. As for dairy firms the TDL plants were located in Dar es Salaam (market), Tanga (resources), Mara (resources), Tabora (resources and market) and Mbeya (resources and market). Table No 2.2.1 provides more information while figure 2.2.1 gives a visual presentation.

11 Dr. D. Mmary attributes the skilled labour challenge to lack of polytechnic education in Tanzania and neglect of the sector by the Government. Many processors outsource experts from Kenya. One processors in the past used to pay more than USD 10,000 to have a specialist supervise a batch of production because of lack local experts, another processor has one production unit stalling the production flow because there is no person to repair the machine.

Survey on Dairy Products Market in Tanzania

21 Niras Finland Oy

Table 2.2.1 Population (Market Potential) Relative to Processing Capacity Zone Population

(Market) Installed capacity

(Production) Lake (Mara, Mwanza, Kagera, Shinyanga) 10,985,806 (28%) 150,400* (46.2% Coast (Dar es Salaam, Coast, Morogoro) 5,997,851 (15%) 22,500 (7.0%) North Eastern (Arusha, Manyara, Tanga, Kilimanjaro) 6,328,275 (16%) 118,200 (36.3%) Southern Highlands (Mbeya, Iringa, Rukwa, Ruvuma) 6,884,282 23,900 (7.3%) Central (Singida, Dodoma) 3,299,128 (8%) 600 (0.2%) Kigoma 1,692,078 (4% ) (0%)

Tabora 1,692,078 (5%) 10,000 (3.1%) South (Lindi and Mtwara) 2,159,346 (5%) (0%)