rural finance sector restructuring and development - vol 2

TRANSCRIPT

Technical Assistance Consultant’s Report

This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. All the views expressed herein may not be incorporated into the proposed project’s design.

Volume 2: Regional Rural Banks Project Number: 36343 December 2003

INDIA: Rural Finance Sector Restructuring and Development (Financed by the Government of the United Kingdom)

FINAL REPORT

Prepared by

PriceWaterHouse Coopers PVT. Limited (Finance & Governance), India in association with Bhartiya Samurdhi Investment and Consulting Services Limited (BASIX), India

For Ministry of Finance, Department of Economic Affairs (Banking Division) TA Management Committee formed by the Ministry of Finance, Department of Economic Affairs (Banking Division)

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 1

TABLE OF CONTENTS

1 INTRODUCTION 3

1.1 COUNTRY CONTEXT 3 1.2 REGIONAL RURAL BANKS 3 1.3 PAST EFFORTS TO IMPROVE VIABILITY OF RRBS 5 1.4 THIS PROJECT 7

2 RRBS: OVERVIEW OF PERFORMANCE AND KEY ISSUES 8 2.1 OVERVIEW OF PERFORMANCE 8 2.2 KEY ISSUES 8

3 ANDHRA PRADESH 11 3.1 THE STATE 11 3.2 THE ANDHRA PRADESH RRBS 12

4 POVERTY, SOCIAL, AND GENDER ANALYSIS 15 4.1 INDIA 15 4.2 ANDHRA PRADESH 15

5 ENVIRONMENTAL ANALYSIS 17 5.1 OVERVIEW 17 5.2 ENVIRONMENTAL IMPACT OF PROSPECTIVE SUBPROJECTS 17

6 THE PROJECT 19 6.1 STRATEGY 19 6.2 STRUCTURE 19 6.3 LAWS AND REGULATIONS 22 6.4 GOVERNANCE 23 6.5 OPERATIONS 23 6.6 HUMAN RESOURCES 24 6.7 MANAGEMENT INFORMATION SYSTEM AND TECHNOLOGY 27 6.8 CONTROL AND SUPERVISION 28 6.9 FINANCIAL RESTRUCTURING 29 6.10 MANAGING RISKS 30

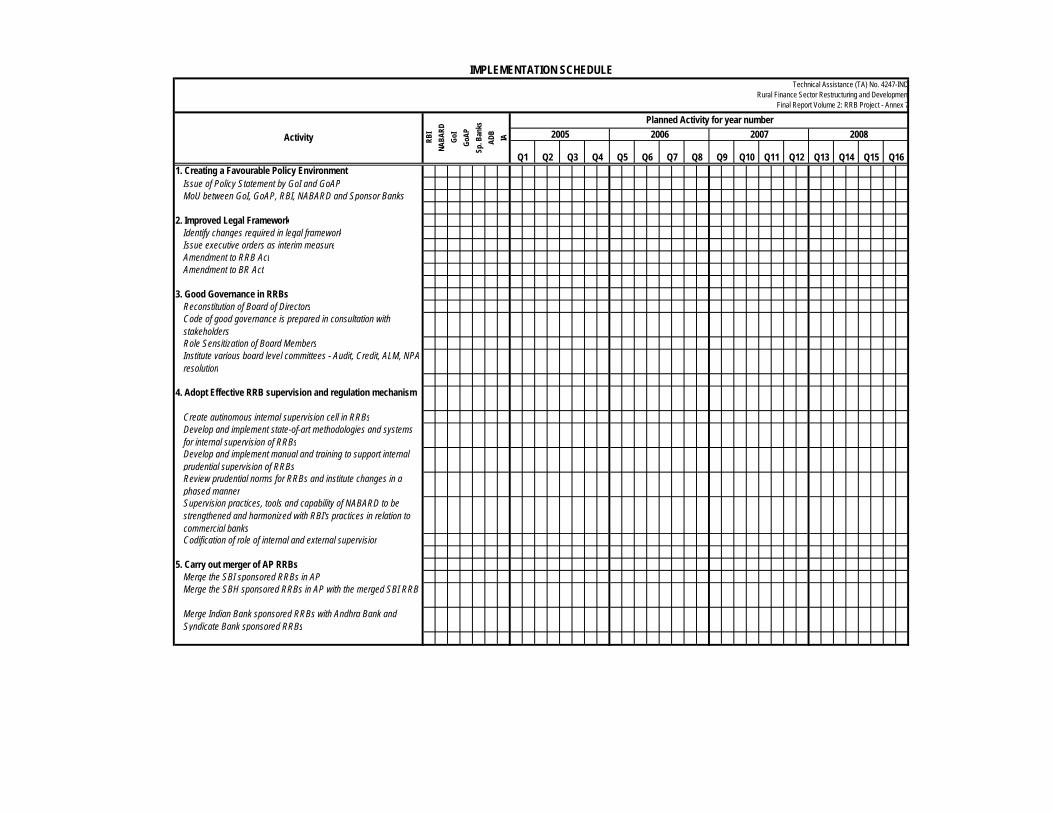

7 PROGRAMME FRAMEWORK 31 7.1 BUDGET OVERVIEW 33 7.2 IMPLEMENTATION SCHEDULE 33

8 IMPLEMENTATION ARRANGEMENTS 34 9 ROLES AND RESPONSIBILITIES 35 10 POLICY MATRIX 38 11 RISK ANALYSIS AND MITIGATION 41 ANNEXES: 1. SOCIAL, POVERTY AND GENDER ANALYSIS 2. INITIAL ENVIRONMENTAL ANALYSIS 3. INDICATIVE HARDWARE AND SOFTWARE CONFIGURATION 4. FINANCIAL RESTRUCTURING AND MODEL RESTRUCTURING PLAN 5. PROGRAMME FRAMEWORK 6. DETAILED BUDGET 7. IMPLEMENTATION PLAN

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 2

Glossary AP Andhra Pradesh BPL Below Poverty Line BRA Banking Regulation Act CCS Credit Cooperative Structure CD Credit Deposit CRM Customer Relationship Management Crore Ten million DAP Development Action Plan DCCB District Central Cooperative Bank FY Financial Year GDP Gross Domestic Product GoAP Government of Andhra Pradesh GoI Government of India HDI Human Development Index HO Head Office HR Human Resources ID Investment Deposit IDBI Industrial Development Bank of India IFCI IFCI Ltd., formerly Industrial Finance Corporation of India INR Indian Rupees IT Information Technology JLG Joint Liability Group LAB Local Area Bank Lac/ Lakh Hundred Thousand MFI Microfinance Institution MoU Memorandum of Understanding NABARD National Bank for Agriculture and Rural Development NAIS National Agriculture Insurance Scheme NPA Non Performing Asset PIU Programme Implementation Unit RBI Reserve Bank of India RFI Rural Finance Institution RO Regional Office RRB Regional Rural Bank SBH State Bank of Hyderabad SBI State Bank of India SC Scheduled Caste SHG Self Help Group ST Scheduled Tribe TA Technical Assistance TOR Terms of Reference UTI Unit Trust of India

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 3

1 INTRODUCTION

1.1 Country Context 1-1 Rural India contributes approximately 40% of India’s GDP and has a population of nearly 700 million. Three quarters of this population is dependent on agriculture for its livelihood. India has one of the world’s most extensive formal rural credit systems, with nearly 46,000 bank branches and more than twice as many cooperative credit outlets in rural areas. Physical outreach is not an issue, except in some remote areas, however access to rural financial services is. 1-2 Commercial Bank credit to rural areas is 10% of total bank credit as against rural contribution to GDP of 40%. The Regional Rural Banks (RRBs) account for just 8% of the total formal sector credit, with nearly 60% thereof being lent to the “non-target group”. Similarly, the Cooperative Credit Structure (CCS) is known to serve the interests of middle and larger farmers. Studies indicate that less than half of the credit usage by rural households comes from formal sources. Rural financial institutions (RFIs) typically function in a backdrop of poor credit discipline in rural areas and frequent extensions of populist measures such as interest and loan waivers, which have led to their being unprofitable and a substantially eroded capital base for these RFIs. RRBs were recapitalised with an infusion of over Rs. 21 billion, while the Government of India (GoI) has recently announced its intention to recapitalise the CCS also. 1-3 The landless, who constitute the bulk of the rural poor, do not get much credit from any formal financial institution. The recent bank loans through self-help groups (SHGs) are the sole exception, where the landless and other poor are being reached significantly. A variety of microfinance institutions (MFIs) working with the poor, while being effective, lack scale due to their limited ability to raise resources and function without facilitative regulations. None of the existing institutions, however, have been able to provide savings services to the poor. The near absence of risk mitigation instruments and mechanisms such as insurance for life, health, crops and assets and commodity derivative contracts to deal with price risks, only exacerbates the vulnerability of the poor. 1-4 The RFIs and apex institutions were conceived in an era when the challenges were quite different – the predominant one being to ensure food self-sufficiency in India. Thus, these institutions, need to revisit their raison d’etre, and devise a strategy, which would make them dynamic and responsive players to the emerging challenges and opportunities of rural financing in India in the post-reform era.

1.2 Regional Rural Banks 1-5 Regional Rural Banks were set up consequent to the Banking Commission observation in 1972 that despite massive expansion of network of commercial banks (consequent to nationalisation of commercial banks), there was still a need for having specialised network of bank branches to cater to the needs of the rural poor. The RRB Act was passed in 1976 and RRBs were set up so as to hybridise

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 4

commercial banking culture with rural ethos. The thinking was to set up RRBs as state-sponsored, region-based, rural-oriented commercial banks having the low cost profile of cooperatives with professional discipline and modern outlook of commercial banks. Between 1975 and 1987, 196 RRBs were established. A large number of branches of RRBs were opened in the hitherto unbanked or underbanked areas providing services to the interior and far- flung areas of the country. RRBs were expected to cover primarily the small and marginal farmers, landless labourers, rural artisans, small traders and other weaker sections of the rural community. 1-6 RRBs have played a significant role in providing banking services in remote rural areas. At the same time, during the very first 10 years of the setting up of RRBs, 152 out of 188 RRBs had accumulated losses of Rs 3.4 billion. The losses went up sharply in 1992 on account of implementation of the National Industrial Tribunal award bringing parity in wage structure of RRBs with that of commercial banks. 1-7 Since then several committees were set up to look into the problems and issues faced by RRBs and suggest ways and means to address the same. Over the period during 1994-2000, 187 RRBs were provided with a total of Rs 22 billion for recapitalisation. However, their financial viability continues to be shaky by policy rigidities coupled with a low capital base in an environmental of inadequate infrastructure and deep social and economic disparities. 1-8 The 196 RRBs, with 14,433 branches spread over 516 districts, vary widely in coverage and size:

• 45 RRBs cover just one district each while another 109 cover 2-3 districts each; 29 RRBs service 4-5 districts while 13 RRBs have a service range of 6-9 districts each;

• 70 RRBs have upto 50 branches each; 109 RRBs have between 51 – 150 branches each while 17 RRBs have over 150 branches each;

• 82 RRBs have assets upto Rs. 2 billion, another 82 RRBs have assets between Rs. 2 billion – Rs. 5 billion while 32 RRBs have assets over Rs. 5 billion.

1-9 Further, although RRBs branch presence is remarkable in the rural areas, in terms of providing services in very remote and inaccessible locations, their performance in the provision of financial services is not commensurate. At present, RRBs’ share in agriculture credit is 8% while that of commercial banks is about 50% and that of CCS is 42%. Such low market share coupled with poor financial performance raises serious issues about the RRB model. Studies have also pointed out that in an effort to meet financial performance expectations of shareholders, RRBs appear to be drifting from their mission to serve the underserved and unreached in a cost effective way.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 5

1.3 Past Efforts to improve viability of RRBs 1-10 Past efforts to improve financial viability of RRBs have ranged from recapitalization (as discussed earlier), to a series of initiatives1 including, among others:

• Deregulation of interest rates • Permission to lend outside target groups • Introduction of prudential norms for income recognition and asset

classification • Provision for rationalization of branches • Preparation of development action plan (DAP) and signing of MoU with

sponsor banks for sustained viability in a planned manner • Provision for greater role and larger operational responsibilities to Sponsor

Banks in the management of RRBs 1-11 The various committees set up to review the working of RRBs and their key recommendations include:

• Dantwala committee (1977): Recommended increasing number of RRBs and control to be vested with NABARD;

• Agricultural Credit Review Committee (1989): Observed that RRBs no longer enjoyed a low-cost advantage since their pay scales were at par with commercial banks and recommended merger with concerned Sponsor Banks by making necessary regulatory amendments;

• Narsasimham Committee on Financial System (1991): Recommended setting up of rural banking subsidiaries by public sector banks and transfer of respective rural branches to these subsidiaries. RRBs and their Sponsor Banks to decide on RRBs retaining their separate identity or merger of RRBs with rural subsidiaries.

• Bhandari Committee on Restructuring of RRBs (1994): Identified 49 RRBs for comprehensive restructuring (including preparation of DAP) and made recommendations regarding delineation of roles and responsibilities of supervising agencies, HR issues, augmentation of share capital, States’ role in recovery of dues, deregulation of interest rates and rationalization of branch licensing policy.

• Basu Committee on Revamping of RRBs (1996): Identified 68 RRBs for restructuring and recommended introduction of prudential norms for RRBs and liquidation of RRBs, which might not be able to respond positively to revamping strategy.

• Thingalaya Committee (1997): Recommended categorisation of RRBs based upon their viability status and size, special package for RRBs in North-Eastern sector and delineation of roles of RBI, NABARD and Sponsor Banks.

• Agrawal Committee on Manpower Norms (2000): Recommended that norms for staffing in RRBs be pegged at 4.20 per unit with relaxation for RRBs in North-Eastern Region and hilly/desert areas.

1 Based on select recommendations of various committees

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 6

• Expert Committee on Rural Credit (2001): Recommended recognition of RRBs which do not carry forward any accumulated losses as Local Area Banks (LABs) and conversion into banking companies to facilitate larger capital flow from new investors.

1-12 It would be pertinent to mention that while financial support extended by the Central Government to UTI, IDBI, IFCI and few nationalized banks exceeded Rs. 250 billion2 since 1991, fresh capital infusion in rural financial institutions has not exceeded Rs. 30 billion since 1991. 1-13 Two recent reviews with rather different structural recommendations, the Chalapathy Rao Committee (2002) and the Sponsor Banks’ report to Government of India (2004) are summarized below in a little more detail. 1-14 Key recommendations of the Chalapathy Rao Committee include: • Differentiated ownership structure based on the specified financial health

categories • Structural consolidation of RRBs: Amalgamation of RRBs falling within the same

socio-economic zone to create one or few RRBs in each state. • Business Development and Management Issues in RRBs to be addressed • Governance Structure of RRBs

o Number of Board members not to be fixed uniformly for all RRBs and to range from 5-11;

o Board representation to be in proportion to the shareholding; o As part of the consolidation process some Sponsor Banks may be eased

out and other financial institutions or other strategic partners may take over as Sponsor Institution.

• Regulatory and Supervision issues o RRBs to obtain license from RBI on the lines of similar provisions of

Banking Regulation Act (BRA), 1949 within a specified timeframe; o Phased introduction of capital adequacy norms; o Recapitalization amount outstanding under “Share Capital Deposit

Account” may be utilized to wipe out accumulated losses. • Operating Structure and Human Resource Development

o While organization structure may be decided by the Board, a proposed structure may include

Head Office focusing on corporate policy issues District Offices/Branches and rural branches managing and

developing field work. o Flexibility to open and close branches; o Respective RRB boards to decide on operational, remuneration and

promotion policies and training strategy in consultation with Sponsor Institution.

• Proposed amendments in the Regional Rural Banks Act, 1976 include those relating to licensing of RRBs, change in capital structure and shareholding

2 Source: SBI monthly review October 2004

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 7

pattern, devolution of select powers of the Central Government to the RBI and RRB boards, and setting up of a Supervisory Authority, among others.

• Technology Induction plan to be drawn up by RRBs considering their financial resources, constraints/requirements of rural areas and compatibility with systems of Sponsor Banks.

1-15 Key recommendations of Sponsor Banks Report to Government of India (“Sponsor Banks Report”): • Amalgamation of 196 RRBs to create 6 Zonal Banks; • Regional Bank to function as Commercial Banks/Local Area Banks providing all

banking facilities; • Share capital participation of Sponsor Banks to continue but one major bank to

take over management role; • Share capital contribution of State Governments and Central Government to

continue as is; • NABARD to continue as Supervisory and Regulatory Authority. 1-16 Since then, the Finance Minister and his ministry have said that sponsor banks must take responsibility for RRBs but no definite scheme has been proposed.

1.4 This Project 1-17 As may be seen from the above there has been no dearth of good ideas to improve the working of RRBs. This project focuses on details of implementation for realigning RRBs in the state of Andhra Pradesh to their mission in a sustainable way and draws substantially from the various studies , task forces and reports commissioned by GOI to revitalize, reform and restructure RRBs.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 8

2 RRBS: OVERVIEW OF PERFORMANCE AND KEY ISSUES

2.1 Overview of Performance The table below presents key performance parameters for RRBs (196 in numbers)

Rs. Billion Year Ended March 31 1999 2000 2001 2002 2003No. of Branches 14,499 14,301 14,313 14,390 14,433 Staff 71,095 70,294 70,141 69,876 69,547 Deposits 271 322 383 445 501Annual Growth in Deposits 19% 19% 16% 12%Borrowings 36 38 41 45 48Owned Funds 22 30 35 41 47Outstanding Advances 114 132 158 186 222Annual Growth in Advances 16% 20% 18% 19%Investments 189 229 276 305 331Annual Growth in Investments 21% 20% 10% 8%Credit Deposit (CD) Ratio 42% 41% 41% 42% 44%Investments Deposit (ID) Ratio 70% 71% 72% 69% 66%Net Profit/ Loss 2 4 6 6 5Accumulated Loss 31 30 28 27 28No. of RRBs having Accumulated Losses 153 141 116 110 97No. of RRBs in Profit 147 162 170 167 156No. of RRBs in Loss 49 34 26 29 40NPA % 28% 23% 19% 16% 14%Recovery % ( as on 30 June of previous year) 60% 64% 68% 71% 72% Source : NABARD

2.2 Key Issues 2-1 Key issues are discussed below: Misalignment of Ownership and Management 2-2 The most pressing issue for RRBs is the misalignment of management of ownership and management. While the largest owner, the Central Government (50%) is too distant to manage, the nearest, the State Government (15%), has too little a shareholding. The Sponsor Bank with 35% shareholding plays the key management role but does not own a majority of the shares. Though shareholding by the governments (central and state) to the extent of 65% has added to the confidence of the depositors, it is proving to be difficult in the restructuring exercise in terms of stakeholders agreement to an effective restructuring. Risk Aversion and Mission Drift 2-3 In the decade and a half since banking sector liberalization and ensuing focus on financial performance, RRBs have drifted away from their mission. During the last 5 years gross loans and advances grew at an average growth rate of 19% with the CD ratio stagnant at around 41%-44% during this period. The CD ratio during

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 9

FY2003 stood at 44% as against the RBI stipulation of 60%. This has serious implications for provision of credit to meet the needs of the rural borrowers. The ID ratio has been at around 66%-72% during these years indicating the relative preference of RRBs towards investment rather than the main business of lending. High Cost Operations 2-4 As on 31 March 2003, the liabilities of RRBs on a consolidated basis comprised owned funds3 (Rs 47 billion), deposits (Rs 501 billion) and borrowings (Rs 48 billion). Deposits grew at an average growth rate of 17% during the last 5 years. Though the RRBs are helping in mobilisation of savings in the rural areas, it is at a higher cost as a large proportion of deposits are term rather than demand deposits. Commercial bank branches in the rural areas offer competition for lower cost current accounts from traders etc., and government funds, as they can service such customers better. Inadequate Loan Loss Provisioning 2-5 RRBs have shown improvements in loan management over the last five years and NPAs have come down from a high of 27.8% during 1999 to 14.4% as on March 31, 2003. This has also been coupled with an increase in recovery rates to around 72% in FY2003. While standard assets have increased from 56% to 72%, substandard and doubtful assets have declined from 9% and 28% to 8% and 17% respectively. Loss assets came down to 3% from 6% from 1995 to 1999. Even though asset quality appears to be improving with a decline in NPA levels and increase in recovery, RRBs have relatively low provisioning levels (as compared to commercial banks4) with 162 RRBs having provisioning at less than 50% of Gross NPAs. Low Capital Adequacy 2-6 Despite recapitalisation, the Net Capital to Assets ratio (proxy for capital adequacy ratio) of RRBs is low with 98 RRBs at less than 4%. Thus, significant proportion of the deposit base can be considered at risk. Though risk is mitigated to some extent on account of the ownership structure (Government of India 50%, Sponsor Bank 35% and respective State government 15%) of RRBs, the low capital base of RRBs has also led to low performance across different financial indicators. Capital infusion required to achieve a minimum 12% net capital to asset ratio works out to over Rs. 55 billion based on the consolidated picture as on 31st March, 2003. If this level of capital adequacy were to be achieved for individual RRBs, the amount required would be larger. Inspite of the growth witnessed by RRBs, the share capital is pegged at Rs 10 million and additional capital infused has been kept as ‘share capital deposit’ pending amendment in the RRB Act 1976.

3 Share capital + share capital deposit + reserves 4 Provisioning levels are over 50% of NPA for most commercial banks

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 10

Low Profitability, High Accumulated Losses 2-7 Inadequate capitalization of RRBs is further compounded by continuing losses. RRBs experience intense pressure on margins due to high costs and setting of lending rates without taking full costs into account. The number of RRBs in profit had gone up to 170 in FY2001 but declined again to 156 by FY2003. Of the 196 RRBs, 40 (increased from 29 in FY2002) recorded losses in FY2003 and 97 (decreased from a high of 153 in FY1999) had accumulated losses, aggregating Rs. 27.5 billion. Accumulated losses have resulted in 55 RRBs having negative networth and deposit erosion of greater than 10% in 52 RRBs. Overall profitability was adversely affected in FY2003 with net margins declining from 1.24% in FY2002 to 0.92% in FY2003. Net margins are likely to be under pressure with interest rates easing out and yield on investments declining. Completion with Sponsor Banks The RRBs do not have adequate integration with the financial markets of the country and for every financial/business initiative they are heavily dependent on Sponsor Banks which themselves have got a presence in the same rural areas and as such at the field level the RRBs are perceived as potential competitors. Need for Capacity Building RRBs have high cost resources with inadequate training, low productivity and insufficient systems and technology support. These issues will need to be addressed on priority if RRBs are to be revitalized.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 11

3 ANDHRA PRADESH

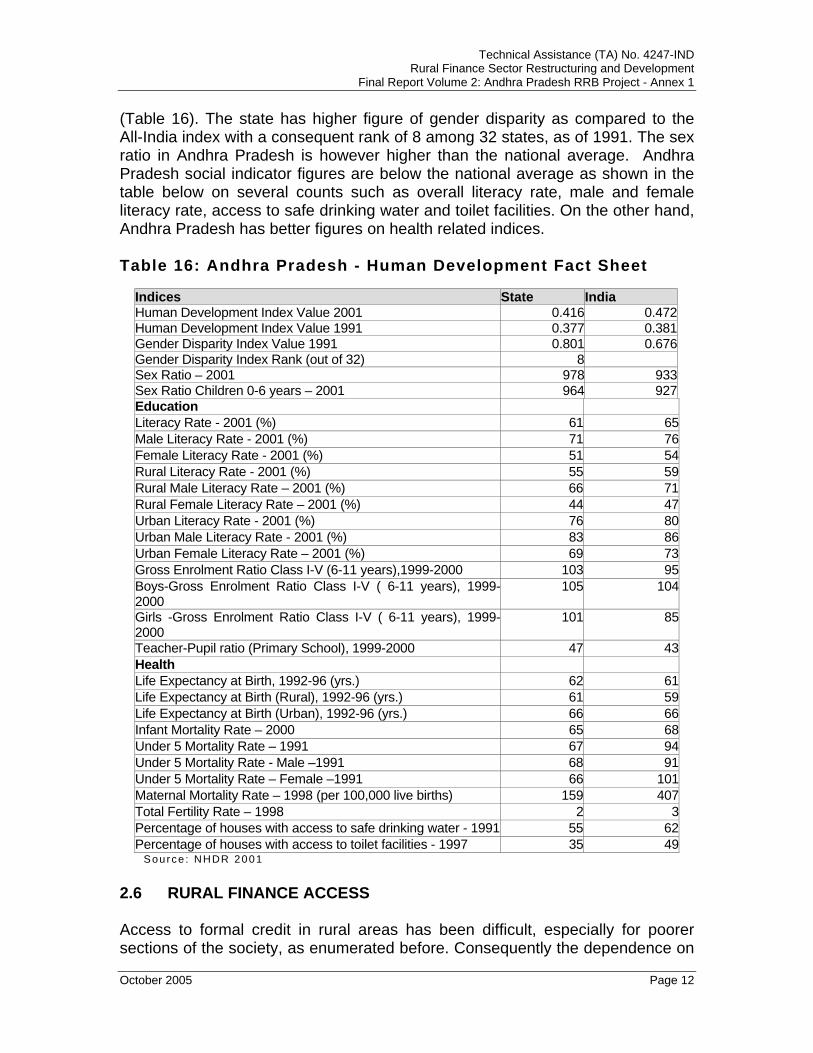

3.1 The State 3-1 Andhra Pradesh (AP) state in India is situated in the southern peninsula. The state is organized into 1110 mandals (administrative divisions) in 23 districts. The total population is 75.7 million, of whom 55.2 million (73 %) live in 26,586 villages and the rest in cities/ towns.

Andhra Pradesh: A Snapshot5

Geographic Details Number of Districts 23 Number of Blocks 1110 Number of Villages 26,586 Total Land Area (million hectares) 27.44 Total Forest Area (% of Total Land Area)

22.59

Total Sown Area (million hectares) 9.73 (35.5% of Total Land Area) Total Irrigated Area (million hectares) 3.61 (13.2% of Total Land Area)

Demographic Details Population 75.7 million Rural Population 73% Population Density 275 persons per sq. km Literacy Percentage 61% Male literacy 76% Female literacy 51% Below Poverty Line (BPL) population6 16% (11.9 million) Rural population Below the Poverty Line

11%

Urban population Below the Poverty Line

26%

Trend of contribution of various sectors to State Income at Current Prices

(INR Billion) Item 1960-61 1970-71 1980-81 1990-91 1997-98State Income

9.83 25.23 73.24 298.67 787.05

Primary Sector

5.78 (58.7%)

14.42(57.14%)

34.14(46.61%)

108.77 (36.41%)

255.56(32.47%)

Secondary Sector

1.26 (12.81%)

3.39(13.43%)

12.17(16.61%)

65.70 (21.99%)

175.15(22.25%)

5 Source: Census 2001 6 The planning commission defines the poverty line as a per capita monthly expenditure of Rs. 49 for rural areas, and Rs. 57

in urban areas, at 1973-74 all India prices. These poverty lines correspond to a total household per capita expenditure sufficient to provide, in addition to basic non food items that is clothing and transport, a daily intake of 2400 calories per person for rural areas, and 2100 in urban areas. Individuals who do not meet these calorie norms fall below the poverty line.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 12

Tertiary Sector

2.79 (28.38%)

7.42(29.41%)

26.93(36.76%)

124.10 (41.55%)

356.35(45.27%)

Source: Vision 2020 document 3-2 There has been a persistent decline of the contribution of the primary sector to the state economy with a concomitant increase from the tertiary sector. According to the Vision 2020 document, the state is planning a growth of 6 percent per annum in agriculture but at same time reduction in share of employment to 45 percent in the year 2020. This would be through absorption of the labour force in the other sectors of the economy. 3-3 The following tables provide a profile of banking in Andhra Pradesh and of sector wise credit flow during 2003-04. Financial sector:

Banking Profile as on 31.3.2003

Particulars Commercial

banks RRBs

State Cooperative

Bank DCCBs

Local Area Bank Total

No.of banks 48 16 1 22 2 89 No.of branches 4041 1168 24 575 11 5819 69.4% 20.1% 0.4% 9.9% 0.2% 100.0% Of which rural 1531 915 0 374 9 2829 54.1% 32.3% 0.0% 13.2% 0.3% 100.0% Source: Andhra Pradesh State Credit Plan 2004-2005-State Level Bankers' Committee,Andhra Bank

ANNUAL CREDT PLAN -SECTOR WISE FLOW DURING 2003-04 Sector

Agriculture Agri Allied Non-Farm SectorOther Priority

Sector Total % Sl.No.

Category of the Banks

1 Commercial

Banks 457048 52.9% 24578 64.2% 262171 77.5% 422026 76.3% 743797 60.0%

61.4% 3.3% 35.2% 56.7% 100.0%

2 Regional

Rural Banks 133147 15.4% 3737 9.8% 9819 2.9% 74897 13.5% 146703 11.8%

90.8% 2.5% 6.7% 51.1% 100.0%

3 Cooperative

Banks 271186 31.4% 9856 25.8% 4492 1.3% 43247 7.8% 285534 23.0%

95.0% 3.5% 1.6% 15.1% 100.0%

4 Others 2270 0.3% 102 0.3% 61998 18.3% 13167 2.4% 64370 5.2%

3.5% 0.2% 96.3% 20.5% 100.0%

Total 863651 100.0

% 38273 100.0

% 338480100.0

% 553337 100.0

% 1240404 100.0%

69.6% 3.1% 27.3% 44.6% 100.0%

Source: Andhra pradesh State Credit Plan 2004-2005-State Level Bankers' Committee,Andhra Bank

3.2 The Andhra Pradesh RRBs 3-4 There are 16 RRBs spread across 23 districts of AP, sponsored by 5 Commercial Banks namely SBI (5), SBH (4), Syndicate Bank (3), Indian Bank (2)and

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 13

Andhra Bank (2). Of the 1168 RRB Branches in AP, SBI has the highest number at 487 followed by Syndicate Bank with 330. The staff strength at state level is 5724. RRBs account for 32% of bank branches in rural AP as compared with commercial bank branches (54% of total) and DCCBs (13% of total). However, these branches account for only 15.4% of agricultural credit flow in the state (11.8% total credit). 3-5 In FY2004, Net Profits recorded by RRBs in AP aggregated Rs. 1149 million. Syndicate Bank sponsored RRBs recorded the highest profits at Rs.611 Million. SBI sponsored Kakatiya RRB is the only RRB with current losses and three RRBs namely, Kakatiya, Nagarjuna and Sri Visakha, all SBI sponsored have accumulated losses (Rs. 292 Million). 3-6 The total networth of all RRBs in AP was Rs. 5,138 million as on March 31, 2004 with Syndicate Bank sponsored RRBs (networth Rs. 2,367 million) accounting for around 46%. 3-7 The total deposits of RRBs in the state were Rs. 47,834 million as on March 31, 2004. SBI sponsored RRBs had a total deposit base of Rs. 16,805 million while Indian Bank sponsored RRBs had the lowest deposit base (Rs. 4400 million) as on March 31, 2004. 3-8 CD ratio at the state level stood at 71% as on March 31, 2004. Andhra Bank sponsored RRBs recorded a CD ratio of 82% while SBH sponsored RRBs recorded a CD ratio of 54%. 3-9 Total net Loans and Advances were Rs. 33,011 Million as on March 31, 2004 with SBI sponsored RRBs (Rs. 11,903) accounting for 36%.

3-10 NPAs at state level stood at Rs.2752 Million (9% of loans outstanding) as on March 31, 2004 with SBI sponsored RRBs accounting for 52% of total NPAs. 3-11 The exhibit below provides key performance parameters of RRBs state-wise for year ended March 31, 2003.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 14

Year Ended March 31, 2003 Rs. Million Name of the RRB Districts Branches Owned Deposits Gross Acc. NPAs NPA Net

Funds Loans Losses Profit Loss % Margin%

HARYANA 18 293 1,801 12,832 6,762 171 469 - 490 7.2 3.1HIMACHAL PRADESH 7 133 350 6,495 1,963 - 41 - 128 6.5 0.6JAMMU & KASHMIR 13 268 744 8,623 1,611 997 99 (158) 208 12.9 -0.6PUNJAB 16 204 1,400 8,374 3,507 - 354 - 184 5.2 3.8RAJASTHAN 34 1,014 2,093 30,894 13,770 1,967 390 (73) 1,159 8.4 1.0ARUNACHAL PRADESH 6 19 31 414 327 223 - (112) 258 79.0 -20.7ASSAM 23 398 896 13,739 4,682 1,038 47 (33) 839 17.9 0.1MANIPUR 9 29 100 254 139 142 - (21) 49 35.0 -5.5MEGHALAYA 4 51 234 1,554 406 - 31 - 136 33.6 1.6MIZORAM 8 54 90 1,007 337 56 3 - 103 30.6 0.3NAGALAND 5 8 31 91 43 16 - (2) 6 14.4 -1.2TRIPURA 4 86 424 6,467 1,781 1,390 21 - 653 36.7 0.3BIHAR 38 1,486 3,014 45,844 11,439 5,264 480 (607) 2,321 20.3 -0.3JHARKHAND 21 391 822 12,877 3,371 1,217 39 (236) 972 28.8 -1.4ORISSA Total 30 835 1,840 24,999 14,080 4,598 131 (440) 2,231 15.8 -1.0WEST BENGAL 20 873 1,603 36,211 13,640 2,820 86 (85) 2,274 16.7 0.0CHHATTISGARH 17 438 930 12,376 3,313 1,501 55 (56) 577 17.4 0.0MADHYA PRADESH 44 1,056 2,428 33,461 13,234 2,566 170 (55) 1,877 14.2 0.3UTTARANCHAL 13 171 458 5,106 1,796 20 76 - 158 8.8 1.3UTTAR PRADESH 72 2,845 13,610 119,502 39,859 1,574 2,407 (52) 8,140 20.4 1.8GUJARAT 23 368 1,397 13,023 6,312 258 240 - 869 13.8 1.5MAHARASHTRA 20 588 1,163 14,440 6,852 1,303 42 (185) 1,540 22.5 -0.9ANDHRA PRADESH 23 1,158 4,563 41,927 29,535 402 906 (23) 2,725 9.2 1.7KARNATAKA 29 1,103 4,227 30,793 25,484 - 770 (10) 2,700 10.6 1.9KERALA 10 354 1,763 12,722 12,043 - 298 - 1,169 9.7 1.8TAMILNADU 9 210 649 6,958 5,292 - 183 - 231 4.4 2.1

ALL INDIA 516 14,433 46,660 500,983 221,578 27,522 7,340 (2,147) 31,997 14.4 0.9

Current

Source: NABARD 3-12 As seen from the above exhibit, RRBs in the Southern States performed relatively better than RRBs in other regions7 in terms of net profits and NPA levels in FY2003. In terms of owned funds, loans and deposit size, AP RRBs are the largest among southern states and the top three on an all-India basis. AP is the only southern state to have accumulated losses and achieved net margins of 1.7% in FY2003, lowest among southern states but higher than the all-India level. RRBs in AP have improved their performance (particularly, considering FY2004 indicators) post capitalization but have potential for further improvement in profitability and asset quality as achieved by RRBs in states including Tamil Nadu, Kerala, Haryana and Punjab. Further, it is critical that RRBs are reoriented to their mission of outreach while focusing on sustainable operations.

7 Besides Haryana and Punjab

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 15

4 POVERTY, SOCIAL, AND GENDER ANALYSIS

4.1 India 4-1 India is the second most populous country in the world with a population of over one billion. As of 2001, over 30% of its population was under 15 years of age. India’s HDI ranking in 2003 was at 127 in a list of 175 countries. Compared with an annual population growth rate of 2% in 1975-2001, the projected rate for the next fifteen years is 1.3%8. 4-2 Poverty levels in independent India increased from around 45% to 57% in the first three decades. The decline in poverty began from the early 1980s, largely as a result of a sharp decline (20%) in incidence of poverty in the rural areas as compared to urban areas. As of the NSS 55th round (1999-2000), the poverty levels (measured by the head count ratio) are at around 26% for all India, broken down into 27% percent for rural areas and 23.6% for urban areas. The gini index of income and consumption inequality was 37.8% for 1997. The quantum and incidence of poverty in rural areas have a far greater influence on the national average than that of urban areas as 70 percent of the total population lives in the rural areas. 4-3 There are wide regional disparities with regard to poverty levels within India. Eastern and North Eastern states still have poverty levels above 40%, and states like Haryana, Punjab, Kerala have poverty levels less than 10%. The head count ratio among the SC and ST population is very high at over 50%. The growth rate of employment has gone down between 1993 and 2000, and the decline is more marked in rural areas. The All India unemployment rate was at 7.32% in 1999-2000, with 26.6 million unemployed persons. The overall literacy levels are at around 65% (as of 2001), but female literacy is 20% lower than male literacy. The life expectancy at birth (2001) was 63.3 years.

4.2 Andhra Pradesh 4-4 Andhra Pradesh is one of the larger states in India, located in the South of the country. Around 73% of its population of 75 million lives in rural areas. The decadal population growth rate at 13.5% is much lower than the national average of 21%. The Net State Domestic Product at current prices was INR 1289 billion in 2000-01, and it went up to INR 1365 billion in 2001-02. The per capita income in the state was INR 14705 in 1999-2000 compared to INR 16047 for India. 4-5 Unlike in most states, urban poverty in Andhra Pradesh (26.63%) is much higher than rural poverty (11.05%). Moreover around 40% of the poor belong to the 20-35 age group indicating low employment for this category. Also around 10% of the poor belong in the old age group making them vulnerable.

8 UNDP HDR 2003

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 16

4-6 The growth rate for employment in both rural (0.29%) and urban (0.01%) Andhra Pradesh has not only declined but is lower than the all India figures (rural 0.67%; urban 1.34%) for the period 1993-94 to 1999-2000. Over 90% of the employment in Andhra Pradesh is in the unorganised sector and the incidence of child labour is very high. The sectoral distribution of workers in rural Andhra has remained more or less constant between 1983 and 2000, with around 79% of the population engaged in the primary sectors. 4-7 As per the Human Development Index of 1991, Andhra Pradesh ranks 23rd out of 32 states, and as per the HDI 2001 it ranked 10th out of 15 states. While the relative position has not changed much, the value of the HDI has moved up from 0.377 in 1991 to 0.416 in 2001. The overall literacy rate (61%) is lower than the national average (65%). 4-8 In terms of health indicators, life expectancy is more or less at par with national figures. The infant mortality ratio was slightly lower than the national average, but the maternal mortality ratio (159) was much lower than the all India figure (407). Andhra fares better than all India figures on access to safe drinking water and toilet facilities. 4-9 The gender related indicators convey a mixed picture. The enrolment ratio for girls in the six to eleven years age group (101) was lower than those for boys (104) in the state, but much higher than the corresponding all India figures (85). Literacy rates for women in Andhra are lower than national averages. Andhra Pradesh has a very high incidence of child labour, which is around twice the national average. Rural Andhra has 13.6% of girls in the age group 5-14 working compared to 11.4% of the boys working, the national rural averages being much lower at 6.3% and 6.6% respectively. 4-10 Andhra Pradesh has been the forerunner in the Self Help Group (SHG) movement in the country, however access to formal credit in rural areas is still wanting. The amount of bank finance extended through SHGs has gone up from INR 20 million in 1995-96 to INR 3,396 million in 2002-03. 4-11 While there are disparate claims regarding the extent of poverty reduction in Andhra Pradesh, a declining poverty level is a heartening phenomenon. The improved health indicators considered with mixed gender indicators indicates the need for further efforts in these areas. The SHG movement has not only helped improve access to finance but also improved status of women as the movement has been directed primarily at women. There is however much to be desired in terms of access to finance as the overall outreach of the movement has been limited despite the fact that Andhra Pradesh has attracted the maximum amount of government attention and funds for the SHG movement. 4-12 A comprehensive analysis is provided in Annex 1.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 17

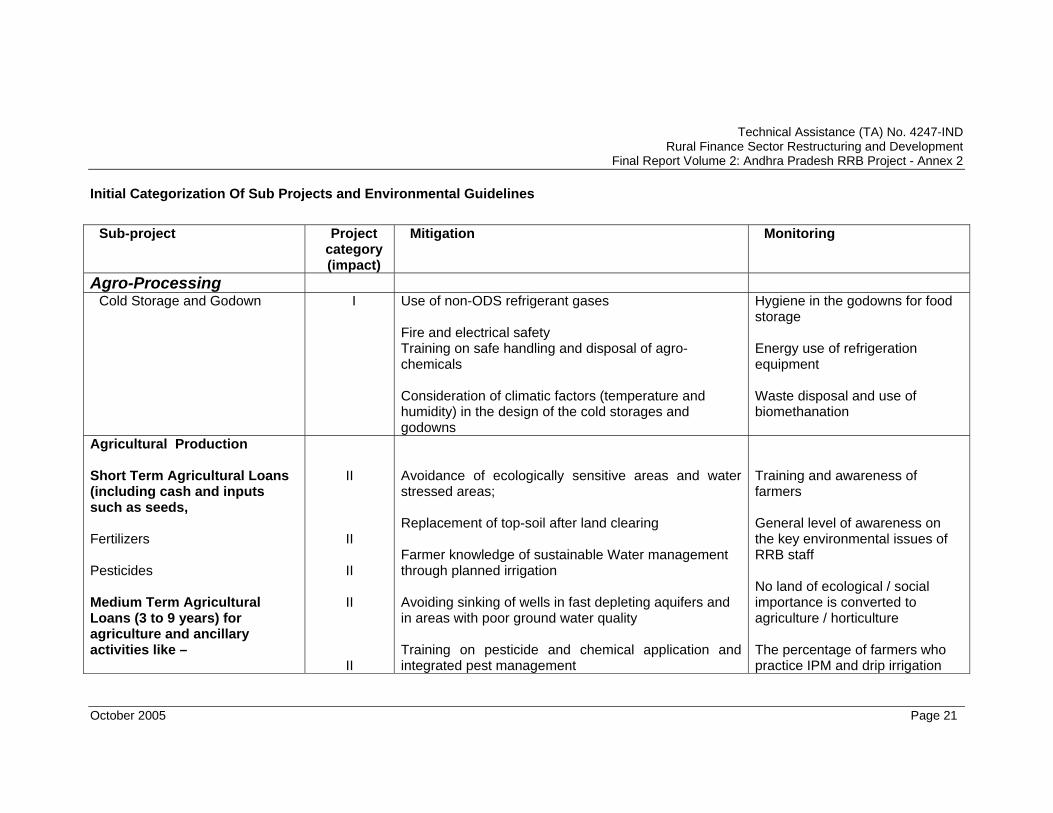

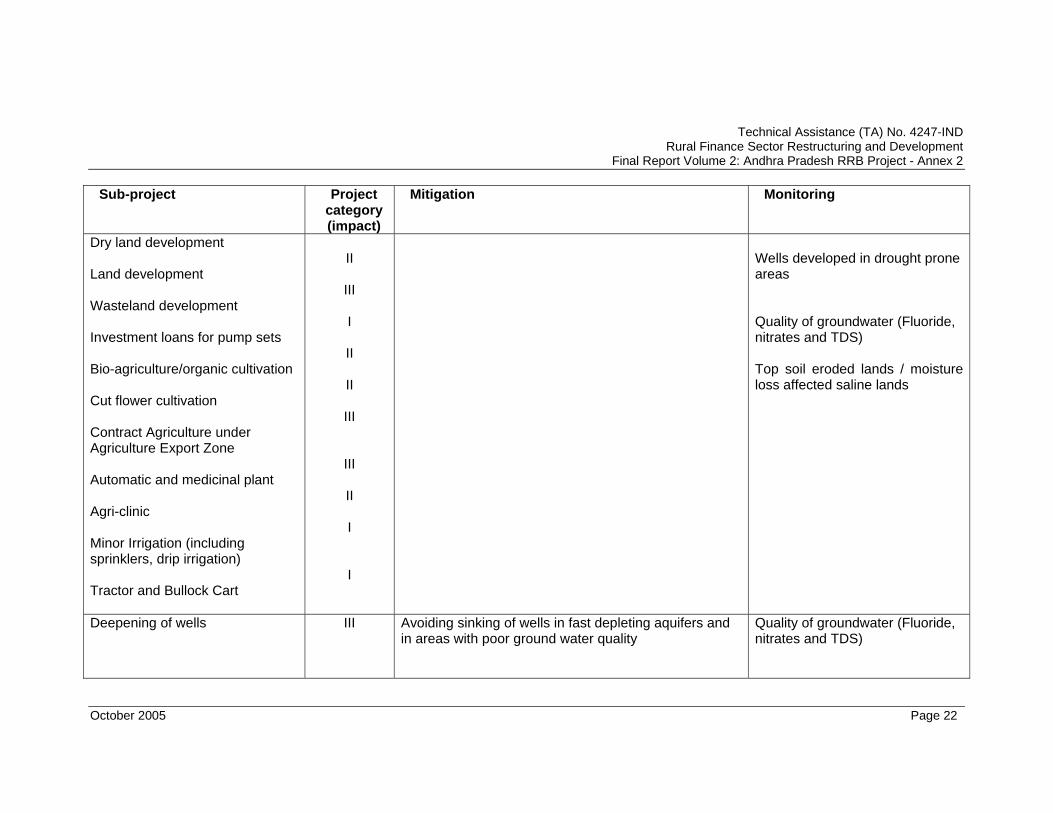

5 ENVIRONMENTAL ANALYSIS

5.1 Overview 5-1 Andhra Pradesh is the fifth largest state in India. The state is divided into three agro climatic zones, Coastal Andhra, Telangana and Rayalseema. Coastal Andhra is the richest agriculturally. There are hill ranges from the North to the South dividing the state into Western and Eastern or Coastal Andhra. 5-2 The temperature tends to be very high in summers, leading to frequent heat waves. Humidity is low, rainfall varies in different parts. Cosatal Andhra experiences very high rainfall and cyclonic conditions, which often lead to destruction of crops and disruption and damage to human life. Rainfall decreases from North to South in the state. 5-3 Of the total land area of 14.58 million hectares of arable land, around 72% is under dryland agriculture and only around 28% has irrigation facilities. Around 65% of the land area is covered under red soil. In Andhra Pradesh 23% of the total land area is covered under forest area, and a large part of this is dense forest cover. Forest cover in Andhra is dwindling because of smuggling of timber, illegal felling of trees due to lack of alternate livelihood options, and mining and sand and stone quarrying. 5-4 Andhra Pradesh has water from two major rivers – Godavari and Krishna. Besides these there are 37 small rivers. The Godavari basin has surplus water whereas the Krishna’s water is completely utilized. The ground water situation has been worsening and there is fluorosis in many areas.

5.2 Environmental Impact of Prospective Subprojects 5-5 The activities under the project are directed at enhancing incomes and income generation opportunities primarily in agriculture and allied activities, agro processing, cottage industries, small scale trading and small commercial activities. As the project activities will contribute to an enhancement in household incomes of rural families, it is likely to have an overall beneficial impact on the environment. Intensification of crop and livestock production will lessen marginal land degradation, livestock grazing on fragile lands (due to stall feeding) and cropping of the most infertile and erosion prone soils. 5-6 Notwithstanding the general positive environmental prognosis, individual sub project loans provided for certain micro-enterprises may occasion deleterious environment impacts. There is therefore a need to regularly monitor and mitigate these risks as much as possible. 5-7 Some illustrative examples of the possible harmful environment impacts from activities to be financed under the project are:

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 18

Agricultural production: To the extent that more and more land area is brought under cultivation, unplanned settlements and roads leading to that area are likely to lead to the irreversible loss of habitat. Increased agricultural production will also impinge on the sustainable use of water and land resources. Inappropriate use of pesticides may lead to impairment of surface and groundwater and soil quality. Agro processing industries: Ozone depleting substances could be in use in the refrigeration equipment. Also if chemicals are stored in godowns, handling and disposal of chemical waste becomes an issue. Livestock loans: Pathogens in manure from animal waste can cause diseases in humans if people come in contact with them. Food safety becomes a concern if manure application is inappropriate. Additional pressure on forests and land resources could result from incremental fodder needs. Non farm sector loans: Loans to cottage industry, artisans for handicrafts are not expected to have large impacts. There could be localized impacts due to the use of hazardous chemicals, emissions from fuel use and wastewater from washing and cleaning. Some cottage industries could use high value forest products such as timber, bamboo and fuelwood causing depletion of a resource faster than the natural rate at which the resource is replenished. Retail trade and business enterprise loans: Loans to retail trade are not expected to have any impact. There could be localized impact due to use of hazardous chemicals, emissions and waste generation for some business enterprise loans. 5-8 While some sub project loans could lead to some environmentally undesirable consequences, the micro/small scale of these sub project activities and the likely low intensity of lending in a given location/ area, should ensure that the environmental effects of the project as a whole should not be of significant concern. Nevertheless, in order to ensure maximum productivity of the loans and at the same time minimum adverse impact on the environment, desirable interventions to mitigate the possible harmful effects of these sub project loans as well as regular monitoring requirements have been specified. 5-9 A complete environmental analysis can be found in Annex 2.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 19

6 THE PROJECT

6.1 Strategy 6-1 The considered opinion of most committees, as well as our assessment of the performance of RRBs converges on and underlines the need for unity of ownership and accountability i.e. for majority ownership and management control by a single stakeholder for effective functioning and viability of RRBs. Of the four stakeholders (Central Government, State Government, Sponsor Banks and NABARD), complete ownership and accountability with either the Central Government or State Government is unlikely to lend the required business focus while NABARD is well entrenched in its refinance and supervisory role and a triple role may not be prudent. Sponsor Banks, being engaged in similar business activity, are synergistically well positioned to take a lead role in ownership and management of RRBs, an opinion also voiced by the Finance Minister in his budget speech in June, 2004. This was also reiterated by the Ministry of Finance in a press statement on 30 November, 2004.9 We would go a step further and suggest that substantial synergies will be realised when the sponsor banks manage their entire rural portfolio including their own branches as single a strategic business unit. This project focuses on consolidation within a state and institutional revitalization of the consolidated entities to realign these entities to the mission in a sustainable way as a first step towards that goal. 6-2 The project proposes that RRBs in the state of Andhra Pradesh be consolidated under three banks which have significant operations in the state. The project will assist in this consolidation through TA support for change management encompassing structural, governance, human resources, policies, systems and products initiatives as also soft loan support for reaching a specified capital adequacy level at each consolidated entity level within 5 years. Changes are required in the legal framework, in particular in relation to the RRB Act. However, recognizing that legislative changes will take time, the project proposes to work through agreement among the stakeholders on key issues. The Components of the strategy are outlined below:

6.2 Structure 6-3 In Andhra Pradesh, State Bank of India (SBI) has sponsored five RRBs operating in eight districts and State Bank of Hyderabad (SBH) has sponsored four RRBs operating in four districts. Syndicate Bank has sponsored three RRBs operating in five districts. Andhra Bank and Indian Bank have sponsored two RRBs each, and each RRB operates in one district. 6-4 It is proposed to carry out the consolidation in two steps in restructuring RRBs in AP: 9 The public sector banks have been asked to merge RRBs with themselves keeping in mind the specific region of their operations. The urge to merge RRBs with the sponsor bank comes from two drivers. The MoF feels that with the merger the public sector banks would reach out to the rural areas and help in pushing up the rural credit take off…. The second reason is the sacricity of fresh capital..” Times of India, 1 December, 2004.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 20

Step 1: Merging all RRBs sponsored by SBI 6-5 There are five SBI sponsored RRBs in AP. They are: Nagarjuna Grameen Bank covering the Nalgonda and Khammam districts. Sri Visakha Grameen Bank covering the Vishakhapatnam, Srikakulam and Vizianagaram districts, Sangameshwara Grameen Bank covering Mahaboobnagar district, Majeera Grameen Bank covering Medak district and Kakatiya Grameen Bank covering Warangal district, respectively. No legal changes are required for this amalgamation (as the RRB Act permits Amalgamation) and the stakeholders are the same across the RRBs (so there will be lower legal and institutional complexity). This initial exercise will enable the Project Implementation Team to get to grips with basic issues in such consolidation without too much complexity. 6-6 The proposed merger will also address the immediate requirement of fresh Tier 1 capital infusion with three SBI owned RRBs which have accumulated losses, by creating a single entity with a positive net worth. The project will provide Tier 2 capital and TA support as described below. 6-7 The table below presents a picture of what key parameters would have been had these banks been merged as of 31st March 2004.

Parameter Value Total Net Worth Rs. Million 1,202 Total Deposits Rs. Million 16,805 Total Net Advance Rs. Million 11,903 Total Branches 487

Total Staff 2315 Gross NPAs as % of gross outstandings 12% Total Profits Rs. Million 296 Profits/Avg. Assets % 1.3% No. of States involved 1 No. of Sponsor Banks involved 1 No. of RRBs involved 5

Step 2A: Merging all RRBs sponsored by State Bank group (SBI, SBH) Step 2 B: Merging RRBs sponsored by Indian Bank with Andhra Bank and Syndicate Bank 6-8 There are four RRBs in AP sponsored by SBH. They are: Golconda Grameen bank covering Ranga Reddy district (Hyderabad Rural), Sri Rama Grameen bank covering Nizamabad, Sri Shatavahana Grameen Bank covering Karimnagar and Saraswathi Grameen Bank covering Adilabad districts. All these four districts fall in Telengana region and are contiguous with each other as well as with geographical area covered by RRBs of SBI. Thus, it would make strategic sense for SBI to merge these RRBs, with the SBI RRBs, so that the entire RRB operational area of Telengana region would be covered by SBI.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 21

6-9 Andhra Bank has sponsored two RRBs: Chaitanya Grameen Bank covering Guntur district and Godavary Grameen Bank covering East and West Godavari districts. 6-10 Syndicate Bank has three RRBs: Anantha Grameen Bank operating in Anantpur district, Pinakini Grameen Bank operating in Nellore and Prakasam districts, Rayalaseema Grameen Bank covering Kurnool and Kadapa districts. 6-11 Indian Bank has sponsored two RRBs: Kanakadurga Grameen Bank operating in Krishna district and Sri Venkateswara Grameen Bank covering Chittoor district. Indian Bank has a minor presence in AP and the two RRBs are located in two different regions (Rayalaseema and Coastal). Indian Bank may accordingly divest the two RRBs that it has sponsored in AP. In such a case, Andhra Bank could take over Kanakadurga Grameen Bank operating in Krishna district and Syndicate Bank could take over Sri Venkateswara Grameen Bank operating in Chittoor district.10 6-12 With the above restructuring, the RRBs in AP would be under three groups: State Bank group, Andhra Bank group and Syndicate Bank group. The merged entities would have the following parameters as of March 31, 2004: Parameter State Bank RRB

Holding Co. (9 RRBs of

State Bank group)

Andhra Bank RRB Holding Co. (3

RRBs under Andhra Bank)

Syndicate Bank RRB Holding Co.

(4 RRBs under Syndicate Bank)

Total Net Worth Rs. Million

1,961 549 2,628

Total Assets Rs Million 35,735 5,211 25,825Total Deposits Rs Million

24,800 3,832 19,203

Total Net Advances Rs Million

16,120 2,962 1,392

Total Branches 652 113 405Total Staff 3,011 474 2,239Gross NPAs as % of total o/s

11% 9% 5%

Total Profits Rs. Million 428 69 652Profits / Avg Assets % 1.3% 1.3% 2.7%No of States involved 1 1 1No of Sponsor Banks involved

2 2 2

No of RRBs involved 9 3 4 6-13 It is proposed that the three Sponsor Banks (SBI, Syndicate and Andhra Bank) be given operational control of the respective consolidated RRBs through a Memorandum of Understanding between GoI, GoAP and respective Sponsor Banks.

10 While a further consolidation of Andhra Bank RRBs with either State Bank or Syndicate Bank could have been considered, it is likely that Andhra Bank would wish to consolidate its rural presence in Andhra Pradesh. Syndicate Bank RRBs are among the best performing and it is expected that it will wish to retain these.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 22

Eventually, the RRB Act would be suitably amended or repealed( to facilitate divestment by GoI and GoAP in favour of the respective Sponsor Banks). Sponsor Banks may then choose to merge RRB holding companies with themselves or retain them as 100% Subsidiaries and/or transfer Sponsor Bank rural commercial branches to the subsidiary. 6-14 The merging of RRBs, is proposed not just to enhance their financial size and derive scale economies but also restructure the institutions in terms of systems and operations. This is in order to make rural operations not just viable but a strategic business for the sponsor banks. The restructuring should address the issues of expanding outreach, Customer Relationship Management (CRM), Treasury Management, Information Technology (IT), Internal Control and Supervision as well as issues related to human resources include fresh recruitment, training, capacity building, performance management, staff redeployment etc. The project will support these initiatives as described below.

6.3 Laws and Regulations 6-15 The ideal solution will be for the RRB Act to be repealed and if the sponsor banks wish to retain their rural operations or the consolidated RRBs as separate legal entities, for such entities to receive licences from the RBI as scheduled commercial banks. The RBI could and perhaps should have a differentiated policy for regional banks (as different from national banks) in matters relating to expansion, risk management and other critical areas. However, at the minimum, for this project, certain key constraints imposed by provisions of the RRB Act have to be addressed, initially through MOUs/agreements among parties and eventually through amendments in the Act. The constraints are primarily of two types: A: Where the Act specifies what can be done e.g. proportion of shareholding

among the three shareholders, size of authorized capital etc. B: Where powers under the Act are given to the Central Government Clearly, any change in ownership structure of RRBs can only be done through legislative action. However, it should be possible for the Central Government, to rely on the sponsor banks’ actions in order to discharge its statutory obligations and to codify expectations and agreements appropriately. The list of such actions includes the following: Issue Current Situation Proposed Action Composition of Board of Directors

2 (GOI) + 1 (NABARD) + 1 (RBI) + 2 (Sponsor Bank) + 2 (State Government)

Majority to be nominated by Sponsor Bank, none by RBI/NABARD

Appointment of Chair & Salary of Chair

Approval required of GOI and NABARD

Deemed approval for Sponsor bank nominee within norms

Salary Structure To be determined by GOI Deemed approval for Sponsor bank action within certain norms

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 23

Issue Current Situation Proposed Action Board Committees and Remuneration of Directors

Approval required by GOI Deemed approval for Sponsor bank action within certain norms

Rules GOI can make rules on Board, Staff matters

GOI to desist other than rules to permit sponsor banks/ RRBs to make rules.

6.4 Governance 6-16 Governance in any institution is provided by the shareholders, the Board of Directors and Board Committees as also by senior management and regulatory authorities. However, the pivotal point through which all these players connect to governance is through the Board of Directors. At present RRB Board members function as interest groups representing the particular shareholder they represent. The central government nominees are generally concerned with lowering of interest rates and increased lending in specific areas/ villages rather than the smooth operation of the bank. The state government nominees keep changing often, as they are ex-officio, and their main concern is to get the RRB to cooperate with government programs in which loans are involved so that targets can be met. The sponsor bank nominee director sees the RRB as a poor cousin and a competitor at the same time. The NABARD and RBI nominee directors have conflicting roles as re-financiers, supervision agencies and regulators. The Boards need to be reconstituted to give sponsor bank a majority and to bring in required expertise through induction of independents. Pending legislative changes, this will need to done through agreement among the shareholders. The Boards have to be provided with adequate autonomy in decision-making and be held accountable for the overall performance of the RRB. 6-17 The project will work to improve the role perceptions amongst the reconstituted Board of Directors. The project will also provide intensive inputs to Board Committees in relation to their governance responsibilities in general and technical issues of current relevance in particular.

6.5 Operations 6-18 In order to strengthen the consolidated RRBs to cater to the needs of the rural economy for all kinds of financial services, diversification of their business has to be encouraged without losing focus on fulfilling the financial needs of the rural poor. RRBs will be encouraged to develop their own customer-segment specific products for deposits, term-investments, loans & advances etc. depending upon the needs of the local rural economy as also to enter into agency arrangements with the Sponsor banks or other financial institutions for extending various financial services including those for remittances and collections, cash management, engaging in foreign exchange business on a bank/ branch specific basis, crop and general insurance, trading in Government securities and other securities, pension of government employees in rural areas etc.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 24

6-19 Several of the RRBs in AP are already doing this. For example Sangameshwara Grameen Bank, a SBI RRB has entered into cash management agreement with SBI and is also retailing life insurance policies for SBI Life Insurance Co. Crop insurance is being offered as part of the National Agricultural Insurance Scheme (NAIS). The project will leverage the internal experience of the RRBs to provide inputs to the others. This will be supplemented by TA support for capacity building for sourcing and developing new opportunities including negotiations with the State Government in respect of certain services such as payment of pensions for government servants, acceptance of guarantees and temporary deposits of government departments/undertakings operating in rural areas etc. Offering a complete array of services will improve the image of the RRBs as a professional organisation, thus attracting more customers. 6-20 RRBs should maximize their outreach. RRBs are currently providing around 11.8% of priority sector loans and around 15.4% of agricultural loans in AP in spite of having 32% of bank branches in AP. The outreach of the RRBs as well as their share in rural lending needs to be improved. Moreover, we must remember that the formal financial system addresses only a small portion of the total demand for these services. The project has built in specific support to each Consolidated RRB in sensitising and training its Board Members and officers in developing products and schemes, building linkages and undertaking a range of initiatives to extend the reach of the RRBs to women and the unreached and underserved. 6-21 Another important problem plaguing the system is recovery of loans. The project will aim to provide training and inputs to consolidated RRBs so that these organizations intensively use micro-finance best practices in their lending methodology. These include the group model, because this model has proven to be creditworthy. It could be through the SHG concept (recovery rate throughout the country is over 96%) but also, primarily for crop loans, through the JLG (joint liability group) model where the loans are individual loans but the whole group is liable for repayment. This will also improve social and poverty outreach as loans can be extended without collateral. Other micro-finance best practices that need to be mainstreamed are credit appraisal based on appraisal of income of the family from all sources, regular monitoring and recovery of loans at regular intervals (e.g. at the end of a crop season rather than the end of a year) and intensive use of technology so that staff can concentrate on human contact related tasks rather than book keeping and reporting. 6-22 In tune with the changing environment and rising customer preference for technology driven services in banks even in rural areas, consolidated RRBs will also be supported to introduce automated services like multi-service credit/debit cards, smart cards, automated teller machines, touch-screen services etc. at least on selective basis in select major branches.

6.6 Human resources 6-23 The RRBs have in general good human resources. To revitalize and reorient these institutions back to their Mission, a well thought out and coordinated strategy

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 25

for rationalizing and energizing human resources and strengthening the institutional frameworks at all levels will be required. 6-24 A particular issue to handle carefully and with sensitivity will be disbanding of multiple HOs. In Andhra Pradesh, upon full consolidation, we envisage 3 HOs (one for each consolidated RRB) with perhaps one or two area offices in the case of State Bank of India instead of the 16 HOs that are currently there. This will call for rationalization of staff positions to move a large proportion of HO staff back to field positions (and some to move up in the commercial bank business). As the banking sector in India has developed a lot of rigidities in terms of staff grade levels expected to be deployed in particular ways, this exercise will call for a lot of thoughtful planning and taking into confidence of affected staff members as well as staff and officer unions. 6-25 The RRB Act has a lot of rigidies in relation to staff matters with powers resting with the Central Government in relation to Wage structure etc. These will need to be alienated, initially through agreements and subsequently through legislative changes. 6-26 There are at least four distinct layers within each organization, which will need to be addressed for realignment, redeployment and revitalization of human resources.

The board The executive/senior management layer The supervisory layer Front line staff

Adaptive Challenges 6-27 Institutional Capacity

Governance issues have to be addressed – by a functioning ‘intelligent’ board

Banks have to take risk and lend sustainably Business development for the target clients should become the focus Managerial or operational efficiency should be ensured by proper

planning, executive initiative and monitoring /inspections/audit etc. from within as well as by stakeholder accountability.

6-28 Individual Capacity

At present the executive layer of these institutions are usually drawn from the sponsor banks. While this in itself is not an issue, focus on the Mission and accountability to the RRBs can be at least in some cases. This will need to be addressed. Staff may also require reskilling, specially in context of redeployment as well in context of introduction of new products, systems, technologies and approaches.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 26

Steps in HR Strategy 6-29 The strategy should be built on developing the capacities of the four layers. 6-30 Individual’s Capacity

Building an alignment Developing a clear focus for each level Communicating priorities and requirements Developing required skills

6-31 Institutional Resilience

Orientation to the rural markets and rural poor Technology solutions Re-skilling challenges and exit routes for staff Recruiting/induction/skill development/compensation benefits/career

development strategies Role definitions/delegation, control supervision and monitoring Team development

6-32 An illustrative list of institutional capacity building inputs required at the four layers is provided below. This will need to be detailed and elaborated during project implementation. Layer Key Issues Key Inputs Governance ( Board)

Role of board, the board members has more responsibilities than rights

Norms about requisites for board members. Orientation workshops for board members Training in meeting management, secretarial tasks, etc. TORs for Committees, training for committee members

Managerial and supervisory levels

Operational efficiency. Concern for customer Openness to IT Anxiety about reviving the system Mission orientation Risk Aversion

Performance monitoring system Strong measures to deal with corruption Emphasis on recoveries Customer orientation, service quality etc. Credit appraisal and loan processing skills Appropriate IT based solutions for loan processing, tracking and CRM Innovation in service delivery Profit planning systems in place Standard norms about compensation etc. performance linked pay Orientation to team Job descriptions, manuals on procedures and systems

New perspectives to be absorbed

Changes in various systems, viz: Recruitment/enrolment – induction –

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 27

compensation benefits Career development – punishment –

grievance redressal – exit route Frontline staff Owing responsibility for

business growth and performance on twin criteria – away from bureaucratised control systems

Training in business orientation Strengthening business planning processes Individual/unit level goals and objectives Performance based evaluation Financial + livelihood support services Sensitivity to social issues – gender caste etc. Better understanding of pricing policies Delegation system/control and monitoring systems. Skills required by the contemporary banker Training on new products, procedures, systems and technologies

6-33 The Indian banking system has training institutions in place, therefore participating commercial banks will be provided with Project inputs to review their training modules, effectiveness and suitably of training and remodel the same to meet the requirement. There may also a need to develop mobile training units to ensure on the job training where the number of officers does not easily allow for someone to leave his work place for an extended period. The restructuring plan should include training plans for each target groups. With the help of training facilities complemented by external resource persons and trainers, the participant banks will elaborate adapted curriculum, and training schedule to reach a maximum of trainees.

6.7 Management Information System and Technology 6-34 The RRBs have good accounting systems in place although there are inconsistencies in application. Similarly required MIS reports are specified and are fairly clear as to what is required. The key issue is that compilation of reports is generally manual and very labour intensive. This coupled with a substantial ad-hoc reporting requirement from the multiple stakeholders puts a large burden on the branches which are generally tightly staffed leading to inadvertent mistakes and sometimes ‘rule of thumb’ reporting. An even more important issues is lack of action on reported trends, reducing the reporting to a matter of record rather than a decision making tool. 6-35 The project will work with the consolidated RRBs to rationalize report generation and strengthen usage of reports for decision making and for informing operating policy. 6-36 The management information systems in RRBs in AP are computerized partially. The Regional Rural Banks are in the process of automating their banking activities. Where computerization effort is on, the staff at both the H.O. and Branches are fully involved in the process. There is a systematic approach to the computerization; the plan and IT policy are in place.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 28

6-37 The Computerization Plans of the Consolidated RRBs will need to build on these successes and take into account new products and procedures. 6-38 Communication is also nowadays an intrinsic feature of a modern organisation. To accelerate processing of information branches will be linked to HOs/Regional offices as required (based on business volume). 6-39 A study on technology application will be commissioned by the project to measure the opportunity to use new technology strategically. The main goal will be to increase efficiency in the system, and services to the members. Technologies initially identified for exploration include the usage of smart cards, low cost ATMs, and mobile computing. Use of handheld devices may be explored to capture transactions at the field level to improve customer service and to avoid duplication of data entry. This can permit the already scarce staff at the RRB branches to focus more on verification of data entered as also other developmental activities like fresh disbursement and intensified recovery. 6-40 Just getting the technology right is not enough, a plan to address motivation, training and resistance issues must be developed and the implementation be driven from the top. 6-41 The Project will support development of a Computerization Plan detailing the systems and procedures required to be followed for successful computerization. Staff will be identified, trained and motivated for faster and effective implementation of Information Technology to streamline MIS compilation and reporting to the appropriate authorities. The investments made for IT (hardware and software) would be monitored closely and remedial action taken in case of delays or improper/ inadequate utilization of hardware and software resources. 6-42 RFIs found to be separately taking up the exercise of software development with various unknown or local software development agencies having inadequate knowledge and experience about Banking Laws and Practice as also the MIS needs of the RRBs units. The project will support short-listing of reputed software agencies as also their Banking Software Applications after a thorough review and audit of the software applications available in the market. The project will also support Open Platforms as far as the Operating System, Databases and other telecommunication and utility programs are concerned. This would help RRBs units in substantially bringing down the cost of ownership as there would be significant savings on License Fees. Please see Annex 3 for recommended hardware and software configuration and indicative costing.

6.8 Control and Supervision 6-43 The need for a strong internal control system has to be recognized so as to improve monitoring of adherence to the statutory and the regulatory requirements as also to internal policy guidelines, operation of Risk Management and Assets-Liability Management Systems, Transparency and Disclosures and various Internal Control Measures. With the strengthening of the computer-based data management system and likely increase in number of branches as also their geographical span in view of

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 29

proposed consolidation, the emphasis should be more on off-branch surveillance of the branches to be integrated with the regular branch inspection process. The internal control system must be placed for overall guidance under an Audit Committee of the Board. The Audit Committee should be empowered for taking decisions on various aspects of an efficient internal control mechanism, review of the policies framed by the Board and its implementation, compliance to the regulatory obligations of the bank and ensuring integrity of information supplied to various regulatory or supervisory authorities, decisions relating to finalisation of annual balance sheets and profit and loss accounts as also accounting policies related thereto, review of audit of annual accounts and its compliance as also compliance of various inspections undertaken by the supervisory authorities. 6-44 The Sponsor Banks should streamline their supervision process of the RRBs in line with that being followed for rural commercial branches. 6-45 So long as RRBs remain independent legal entities, they will also need to be regulated and supervised as such. RBI needs to regulate these on the lines of commercial banks, albeit with a modified approach in line the regional (rather than national) operations. Supervision needs to be consolidated in a single supervisory authority, which at present would appear to be NABARD. However, it is critical that NABARD’s supervisory role vis-à-vis RRBs is clarified in relation to RBI’s regulatory role and that of sponsor banks exercising internal control. The project will provide support in this exercise of role clarification and norm setting.

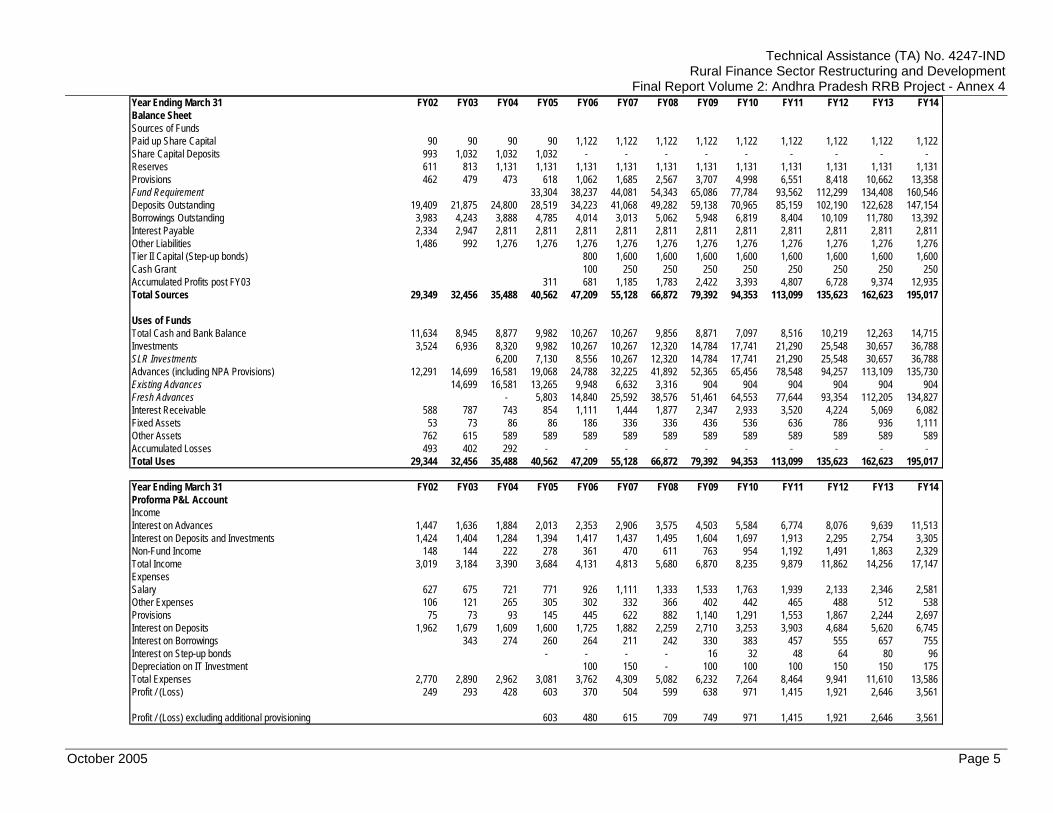

6.9 Financial Restructuring 6-46 The three consolidated RRBs would have a positive net worth as on 31.3.2004 if the consolidation were carried as of that date. Two of these (Andhra Bank RRB and Syndicate Bank RRB) would also meet the extant capital adequacy requirements of 9%. If provisioning is increased to 50% of NPA and the target capital adequacy is 12%, the SBI Group RRBs require around Rs 1,600 million, as on March 31, 2004. The project will support the restructuring effort by providing step up coupon bonds on soft terms to enable the consolidated RRBs to absorb the additional provisioning requirements and to build up adequate capital to weather risks inherent in the business. Annex 4 provides a forecast of the SBI group RRBs under the following conditions.

Business growth in line with expectation of renewed focus on Mission Fresh NPA occurrence at 4%-5% of fresh loans Provisioning at 50% of NPA Less than proportionate increase in salary and establishment costs on

account of reduced HO requirements Step up coupon bonds of Rs. 1,600 Million for the SBI-SBH RRB Grant support for institutional revitalization including training, MIS and

technology support for all the three consolidated entities. 6-47 Sensitivity analysis to key assumptions has been carried out and shows the forecasts to be sensitive to business growth, provisioning assumptions.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 30

6.10 Managing Risks 6-48 The rural/ poor households are vulnerable to a number of risks. Some of these are frequent, such as minor illnesses but have relatively little impact, while others can be infrequent, such as a cyclone, with great impact. While the former are best handled by dipping into one’s savings, or occasional borrowing, the latter require outside support, either in the form of insurance payouts or disaster relief. One can also distinguish between idiosyncratic and covariant shocks. Covariant shocks, such as drought, can affect all households in a locality while an idiosyncratic shock, such a theft, may be restricted to only a given household. 6-49 The poor adopt a mix of strategies depending on the severity and co-variability of the shocks. Self-insurance strategies include a) reduced consumption of food grains b) taking children out of school c) temporary migration d) diversification of income sources. It may be noted that some of the above strategies reduce the ability to withstand future shocks and thus if there are successive droughts or bouts of illness, then the family becomes more and more prone to risk. 6-50 Therefore, it is critical that the RRBs build inherent capacity to address the risk of its clientele as well as risk to its own sustainability in context of the risk proneness of its clientele by: • Expanding outreach of savings and insurance services to its members. The

project will focus on development of suitable products and linkages between insurance product providers and the RRBs.

• Mainstreaming micro finance best practices in the RRBs: best practices are being incorporated in each of the section of this strategy. A full review of products, procedures and processes will be carried out to introduce MFI best practices to the RRBs.

• Hedging the portfolio risk through weather derivatives: hedging agricultural risk is very difficult, but there are derivative products available (such as rain fall insurance) which could serve to mitigate risk. The project will provide support for pilot activities in this area.

• Disseminating commodity pricing and knowledge will enable the farmer to mitigate price risk. The project will implement pilots.

• Creating Risk Fund: If the agricultural lending is to be sustainable, without resorting to changes in prudential norms, it will be necessary to make adequate provision for normal risk and to include this risk cost in pricing. The project will facilitate product costing and sensitisation of top management to pricing based on costing taking into account normal risk. Further, financial restructuring support is being provided to take capital adequacy to 12% of risk weighted assets (as against the current regulatory requirement of 9%). Over time RRBs and other commercial banks need to be encouraged to build a risk fund from out of profits to cope with abnormal risk.

Technical Assistance (TA) No. 4247-IND Rural Finance Sector Restructuring and Development

Final Report Volume 2: Andhra Pradesh RRB Project

October 2005 Page 31

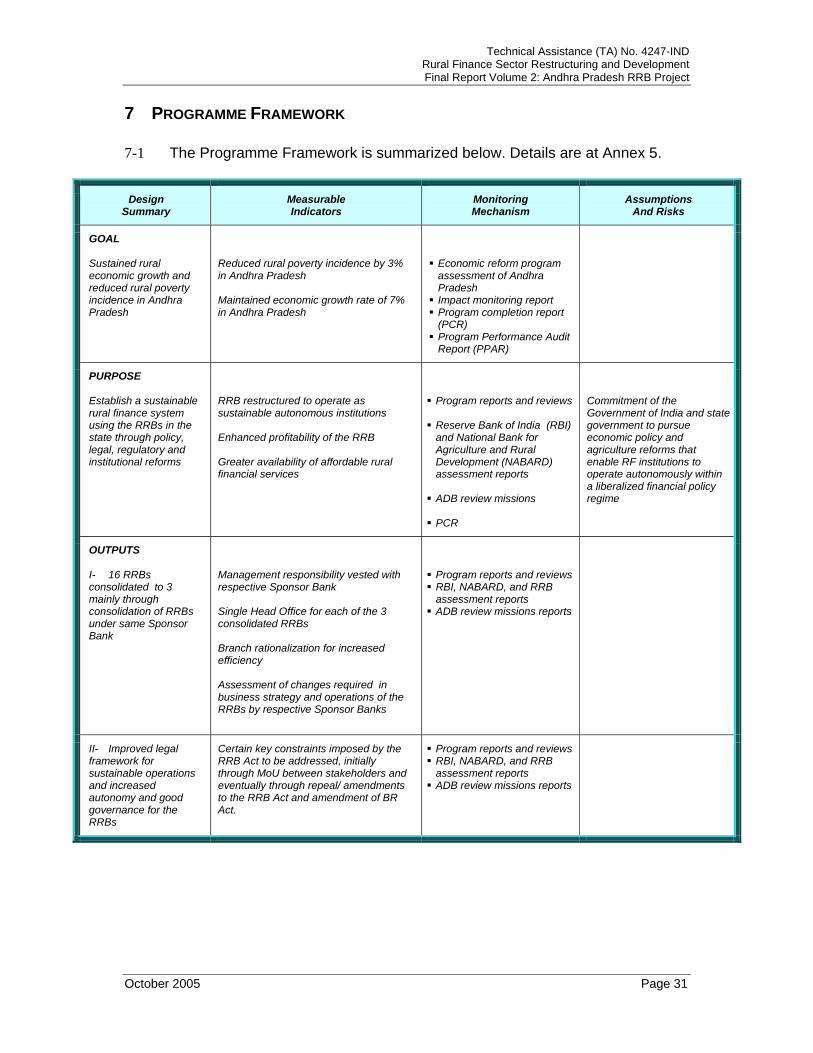

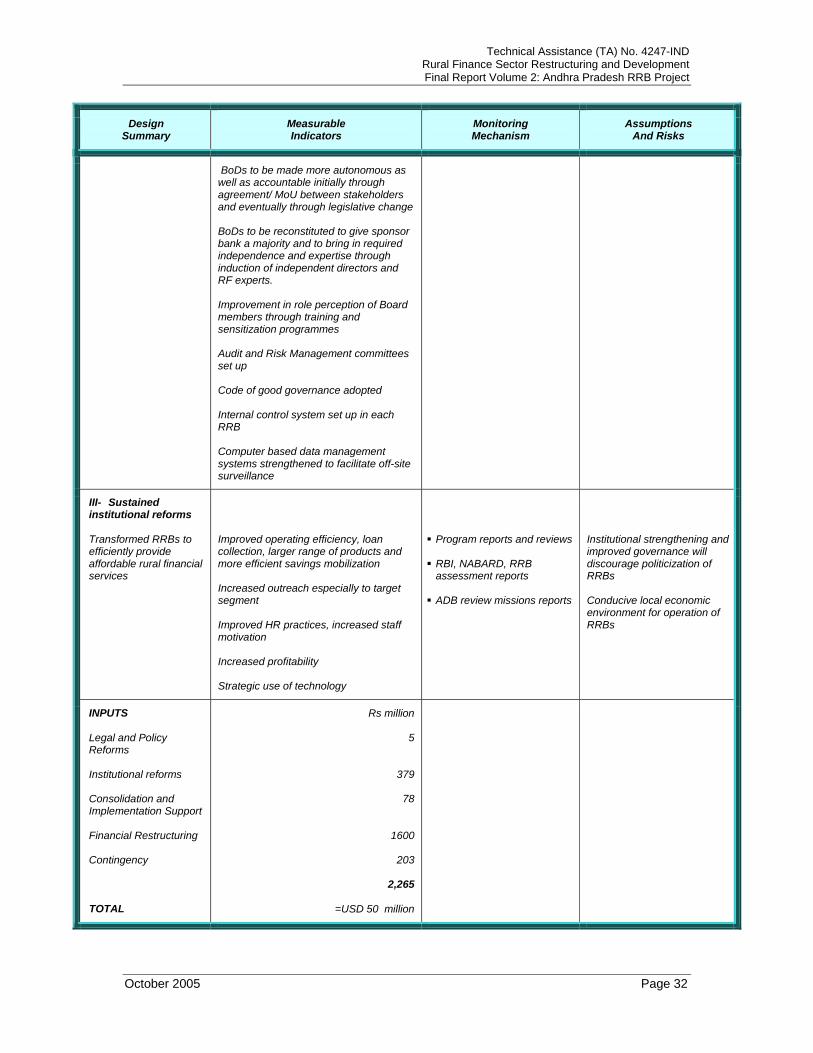

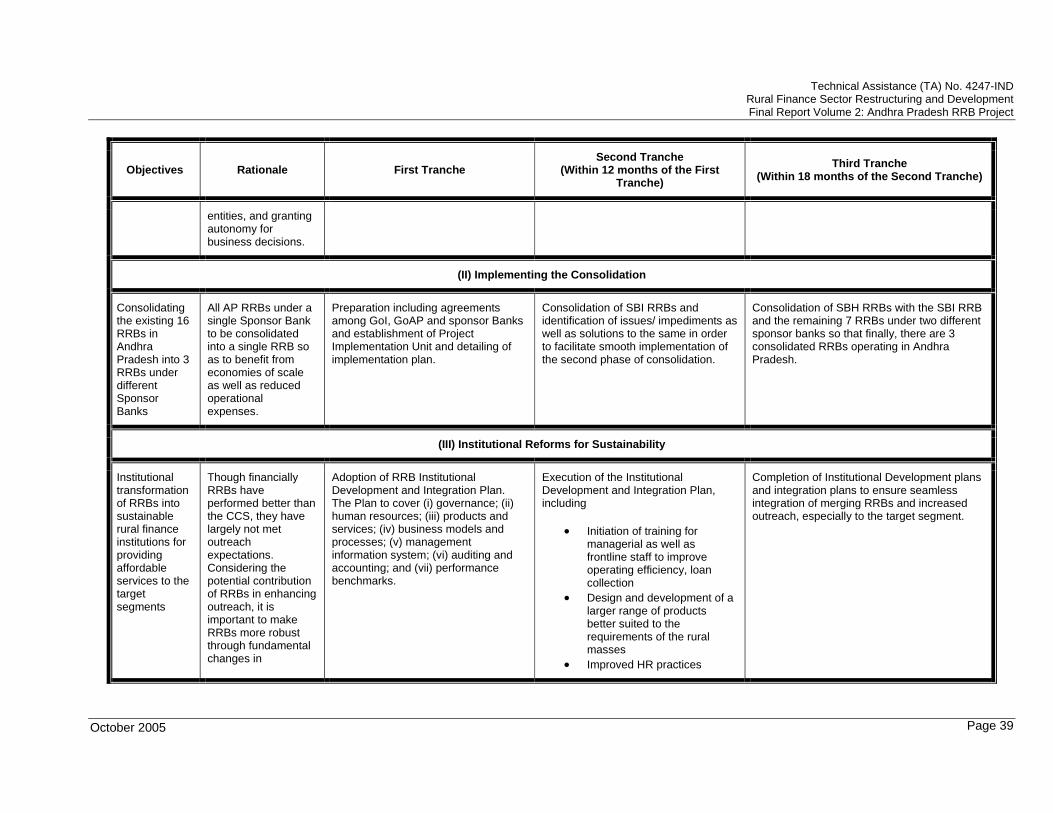

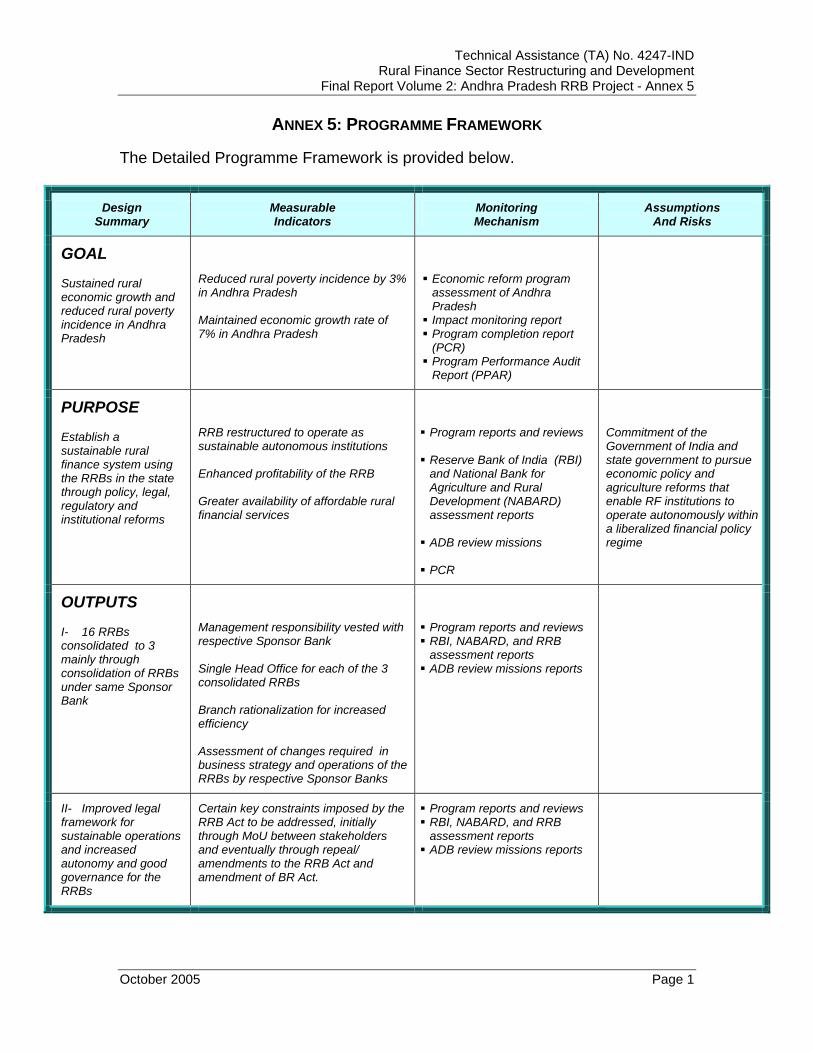

7 PROGRAMME FRAMEWORK 7-1 The Programme Framework is summarized below. Details are at Annex 5.

Design Summary

Measurable Indicators

Monitoring Mechanism

Assumptions And Risks

GOAL Sustained rural economic growth and reduced rural poverty incidence in Andhra Pradesh

Reduced rural poverty incidence by 3% in Andhra Pradesh Maintained economic growth rate of 7% in Andhra Pradesh

Economic reform program assessment of Andhra Pradesh