royal philips electronicsimages.philips.com/is/content/philipsconsumer/campaigns... · 2015. 10....

TRANSCRIPT

Royal Philips ElectronicsThird Quarter 2008Information booklet

October 13th, 2008

3

Important informationForward-looking statementsThis document and the related oral presentation, including responses to questions following the presentation may contain certain forward-looking statements with respect to the financial condition, results of operations and business of Philips and certain of the plans and objectives of Philips with respect to these items. We caution readers that no forward-looking statement is a guarantee of future performance and that actual results could differ materially from those contained in the forward-looking statements. Examples of forward-looking statements include statements made about our strategy, estimates of sales growth, future EBITA and cost savings and future developments in our organic business as well as the benefit of future acquisitions, and our capital position. By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances and there are many factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements. These factors include but are not limited to domestic and global economic and business conditions, the successful implementation of our strategy and our ability to realize the benefits of this strategy, our ability to develop and market new products, changes in legislation, legal claims, changes in exchange and interest rates, changes in tax rates, pension costs, raw materials and employee costs, our ability to identify and complete successful acquisitions and to integrate those acquisitionsinto our business, our ability to successfully exit certain businesses or restructure our operations, the rate of technological changes, political, economic and other developments in countries where Philips operates, industry consolidation and competition. As a result, Philips’ actual future results may differ materially from the plans, goals, and expectations set forth in such forward-looking statements.Additional risks and factors are identified in our Annual Report for the fiscal year ended December 31, 2007 and our Annual Report on Form 20-F filed with the U.S. Securities and Exchange Commission (the “SEC”), which is available on the SEC’s website at www.sec.gov. Readers should consider the disclosures in that Report and any additional disclosures that we have made or may make in documents that we have filed or furnished to the SEC or may file with or furnish to the SEC or other regulatory authorities. Any forward-looking statements made by or on our behalf speak only as of the date they are made. We do not undertake to update forward-looking statements to reflect any changes in expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is based. Statements regarding market share, including as to Philips’ competitive position, contained in this document are based on outside sources such as specialized research institutes, industry and dealer panels in combination with management estimates. Where information is not yet available to Philips, those statements may also be based on estimates and projections prepared by outside sources or management. Rankings are based on sales unless otherwise stated.

US GAAP basis of presentationThe financial information included in this document is based on US GAAP, unless otherwise indicated. As used in this document, the term EBIT has the same meaning as Income from operations (IFO).

Use of non-GAAP InformationIn presenting and discussing the Philips Group’s financial position, operating results and cash flows, management uses certain non-US GAAP financial measures, like: comparable growth; EBITA; NOC; net debt (cash); and cash flow before financing activities. These non-US GAAP financial measures should not be viewed in isolation as alternatives to the equivalent US GAAP measures. In our Quarterly report, Annual report or form 20-F we’ve included a reconciliation of such non-US GAAP financial measures to the most directly related US GAAP measures.

Use of fair value measurementsIn presenting the Philips Group’s financial position, fair values are used for the measurement of various items in accordance with the applicable accounting standards. These fair values are based on market prices, where available, and are obtained from sources that are deemed to be reliable. Readers are cautioned that these values are subject to changes over time and are only valid at the balance sheet date. When a readily determinable market value does not exist, fair values are estimated using valuation models, which we believe are appropriate for their purpose. They require management to make significant assumptions with respect to future developments which are inherently uncertain and may therefore deviate from actual developments. Critical assumptions used are disclosed in the financial statements. In certain cases, independent valuations are obtained to support management’s determination of fair values. 3

4

Agenda

Philips – who we are

• Results Q3 2008

• Moving to Philips ‘Vision 2010’

• Sector insights – Healthcare, Consumer Lifestyle & Lighting

• Management agenda 2008

4

5

• Founded in 1891; headquarters in Amsterdam, The Netherlands

• One of the largest global diversified industrial companies with sales in 2007of almost € 27 billion

• Multinational workforce of over 128,000employees*

• R&D expenditures € 1.6 billion; owner of 60,000 patents

• Strong position in emerging markets

• Number 43 of the world’s most valuable brands

* As per September 2008 5

6

We are everywhere you go on the planet

• 70% of the top-50 US hospitals have chosen Philips solutions for cardiology

• We light 65% of world’s top airports, 30% of offices and hospitals, and landmarks such as the Eiffel Tower, the Sydney Opera House, the Great Pyramids

• One-in-three cars worldwide uses Philips automotive lighting

• Each day more than a million of our consumer lifestyle products are purchased

6

7

Agenda

• Philips – who we are

Results Q3 2008

• Moving to Philips ‘Vision 2010’

• Sector insights – Healthcare, Consumer Lifestyle & Lighting

• Management agenda 2008

7

8

Highlights

Healthcare and Lighting maintained solid growth in much tougher markets, with sales up 5% and 6% respectively on a comparable basis.

Sales at Consumer Lifestyle declined by € 600 million, of which more than half was attributable to the implementation of the new TV strategy.

Net income amounted to € 357 million, including a € 302 million gain on the sale of the remaining stake in TSMC.

EBITA of € 128 million was negatively impacted by net incidental charges totaling € 285 million, notably a charge for the final settlement of an asbestos liability.

Repurchases under the current share buy-back program reached almost € 3 billion by the end of Q3.

8

9

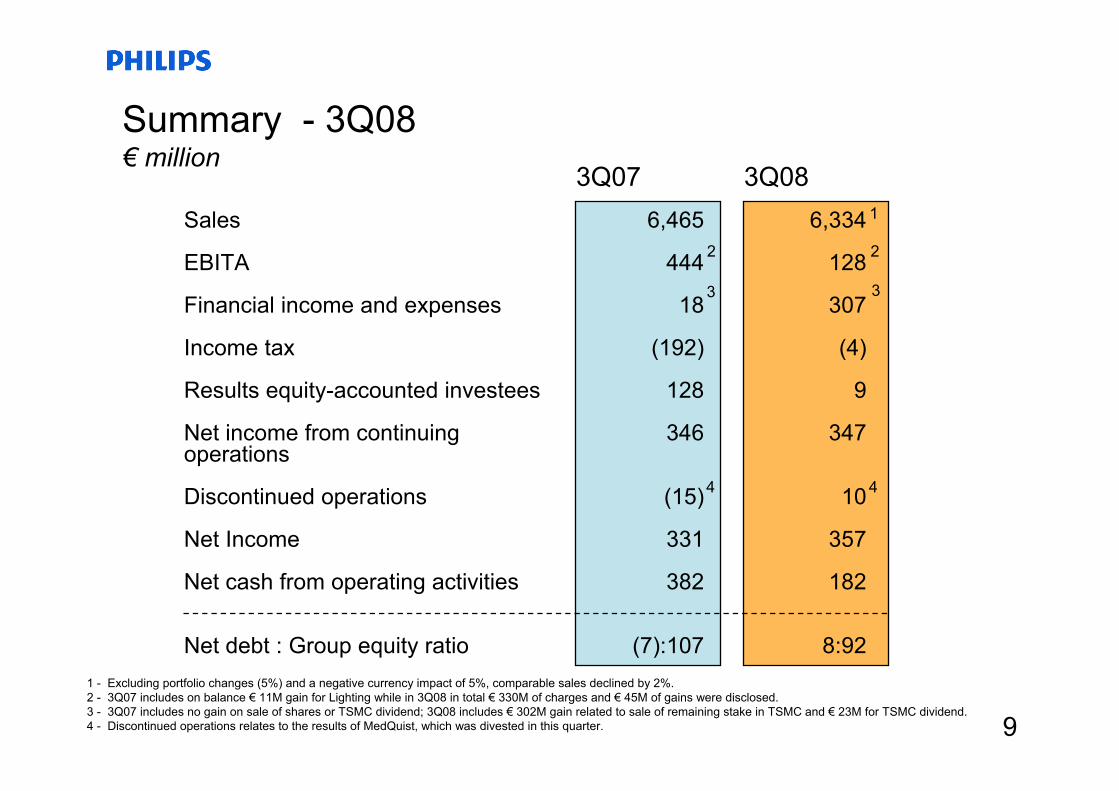

Summary - 3Q08 € million

3Q083Q076,465

444

18

(192)

128

346

(15)

331

382

(7):107

6,334

128

307

(4)

9

347

10

357

182

8:92

Sales

EBITA

Financial income and expenses

Income tax

Results equity-accounted investees

Net income from continuing operations

Discontinued operations

Net Income

Net cash from operating activities

Net debt : Group equity ratio

4

2

1

3 3

9

1 - Excluding portfolio changes (5%) and a negative currency impact of 5%, comparable sales declined by 2%.2 - 3Q07 includes on balance € 11M gain for Lighting while in 3Q08 in total € 330M of charges and € 45M of gains were disclosed.3 - 3Q07 includes no gain on sale of shares or TSMC dividend; 3Q08 includes € 302M gain related to sale of remaining stake in TSMC and € 23M for TSMC dividend.4 - Discontinued operations relates to the results of MedQuist, which was divested in this quarter.

2

4

10

Sales to thirds by sector – 3Q08€ million

Healthcare

Consumer Lifestyle

Lighting

I&EB

Group sales

19

(18)

14

3Q07 3Q08

(2)

6

(8)

5

(2)

% nom

6,465

(31) (27)

% comp

6,334

1,585

3,238

1,496

102

1,806

2,639

1,785

70

GMS (23) (19)44 34

10

11

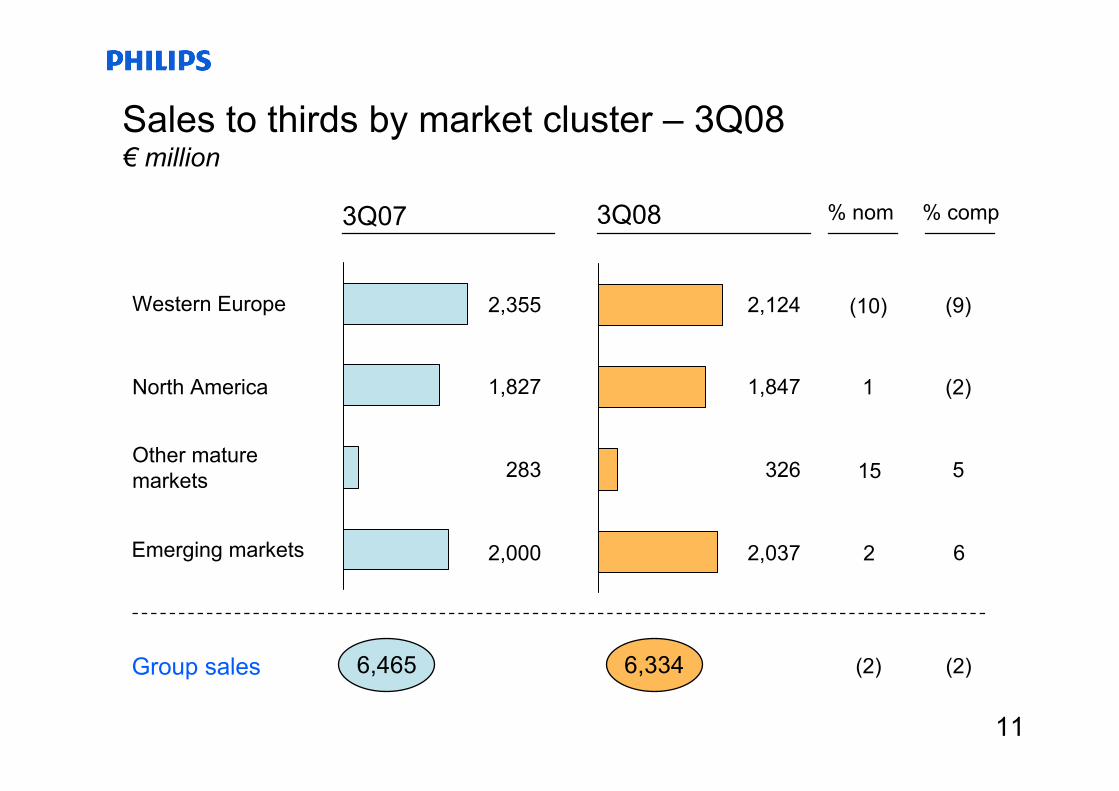

Sales to thirds by market cluster – 3Q08€ million

Western Europe

North America

Other mature markets

Emerging markets

Group sales

15

1

(10)

3Q07 3Q08

(2)

5

(2)

(9)

(2)

% nom

6,465

2 6

% comp

6,334

2,355

1,827

283

2,000

2,124

1,847

326

2,037

11

1212

EBITA by sector – 3Q08 € million

Healthcare

Consumer Lifestyleof which Television

Lighting

Innovation & Emerging Bus.

Group Mgt & Services

Philips Group

as % of sales

3Q083Q07

188

171 (43)

190

(35)

(70)

444

6.9

197

95(73)

196

(46)

(314)

128

2.01 - includes € 17M of acquisition and integration-related charges and € 45M gain related to sale of Philips Speech Recognition Systems2 - includes € 61M of restructuring charges , of which € 40M related to Television and € 21M mostly to the other former CE businesses3 - includes € 11M of restructuring and acquisition-related charges in 3Q08; 3Q07 includes on balance € 11M gain4 - includes € 241M for the final settlement of asbestos-related claims and associated legal fees as announced on September 26, 2008

2

1

3 3

4

13

Cash Flow from continuing operations – 3Q08€ million

3Q07

331

15

209

(59)

(128)

(10)

24

382

(147)

(363)

(128)

Net income

Income/loss discontinued operations

Depreciation / amortization / impairments

Net gain on sale of assets

Income from equity accounted investees

Decrease in WC/other current assets

Other

CF from operations

Gross capital investments

Acquisitions/divestments/other

CF before financing activities

3Q08

357

(10)

267

(403)

(5)

(36)

12

182

(188)

852

846

13

14

Fixed assets expenditures & Depreciation by sector *€ million

3Q083Q07

38

38

56

13

2

147

64

35

87

2

0

188

Healthcare

Consumer Lifestyle

Lighting

I&EB

GMS

Group

Gross CapEx

3Q083Q07

22

39

57

10

14

142

36

41

60

7

13

157

Depreciation

* Excluding software related capital expenditures and depreciation 14

15

• The Philips brand is a long-established household name in key emerging markets

• Driven by enhanced consumer insight, we create products specifically tailored to emerging markets needs/tastes

• We continue to enhance our position through smaller but targeted JV or acquisitions of leading companies in emerging markets, particularly in Healthcare

– Philips-Neusoft JV in China (X-Ray) – VMI in Brazil (X-Ray)– Goldway in China (Patient Monitoring)– Dixtal in Brazil (Patient Monitoring)– Alpha X-Ray in India (X-Ray)

Emerging Markets: reached 30% of sales in 2007 and continue to show strong growth

Emerging

Mature

30%

Growth in emerging markets

0%2%4%6%8%

10%12%14%16%18%

2005 2006 2007 1Q08 2Q08 3Q08 15

16

Emerging MarketsSales in emerging markets Q3 2008

Philips Group

16

Healthcare 15%

ConsumerLifestyle 42%

Lighting 35%

15%

42%

35%

Mature 68%

Emerging 32%

17

Emerging marketsSales growth in emerging markets

Healthcare

Consumer Lifestyle

Lighting

Philips Group

FY 2007Q3 2007

8 %

15 %

14 %

15 %

8 %

7 %

16 %

10 %

Q3 2008

5 %

2 %

17 %

6 %

17

18

-

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2025 2026 2038

Other debt LT debt Undrawn committed facilities

Philips proactively refinanced maturing debt earlier in the year and first maturity is now in 2011€ millions

Note: Other debt consists mainly of local credit facilities that are being rolled forward on a continuing basis

Long Term funding has been restructured: • Maturities up to 2038• Average tenor of outstanding debt is at 9.4 years• No financial covenants

18

19

2,400Total 565Several countries with best rated banks

57AA- bank178AAA bank600Dutch state AAA

1,000Dutch state owned banks AAA1,835Cash in KPENV

Q3 2008in millions of eurosCash position per Q3 2008

AAA bank

AA- bank

Dutch state owned banks

AAA

DutchState AAA

Several countries with best

rated banks

€ 2.4 billion cash with at least 74% of the cash deposited with AAA banks and government

19

20

Acceleration of plans to improve margins

20

• Healthcare will accelerate a number of initiatives to improve margins and to further optimize its operations structure, particularly in Imaging Systems. This is expected to lead to charges of approximately € 50 million in Q4.

• Consumer Lifestyle expects to incur further restructuring charges of around € 60 million in Q4, largely in the Television business. This will bring the total amount to approximately € 190 million for the full year, of which € 130 million relates to Television.

• Lighting expects to take a charge of up to € 100 Million in the fourth quarter to further increase organizational effectiveness and strengthen its position as the industry leader.

In view of macro-economic developments, Philips will accelerate their planned initiatives to further increase organizational effectiveness by streamlining operations and simplifying the structure.

21

Share repurchase program

21

Philips has a strong balance sheet. To date, we have completed € 3.1 billion of our current € 5 billion share repurchase program which we announced in December 2007.

Going forward, in light of both the risks and opportunities presented by the deterioration of the economy and the financial market turbulence, we will slow down the completion of the program.

* To date € 3.1 billion is bought back compared to € 2.9 billion end of Q3 2008.

Status Share Buy Back Actual Actual Actual Actual ActualEnd 2007 Q1 '08 Q2 '08 Q3 '08 Q3 YTD

Shares repurchased (in € M) (975) (1,139) (811) (2,925) Numbers of shares (in M) 37 47 38 123 Average share price 26.10 24.12 21.25 23.83

Shares outstanding 1,065 1,028 984 946

2222

• Equipment order intake grew 4% on a currency-comparable basis, supported largely by growth at Patient Monitoring and Clinical Care Systems. Year-to-date equipment order intake growth now stands at 5%.

• Sales grew 5% comparably year-on-year, with higher sales visible in all businesses, and particularly strong growth at Customer Services and Patient Monitoring. Respironics grew in line with expectation at 14% compared to 3Q07.

• EBITA included a € 45M gain on the sale of Speech Recognition Systems. Adjusted for this gain and € 17M of acquisition and integration-related charges, EBITA was below 3Q07 at € 169M or 9.4% of sales. Higher earnings at Clinical Care Systems and Home Healthcare Solutions were offset by lower earnings at Imaging Systems, which was impacted by lower volume and margin pressures.

• Net operating capital and the number of employees increased, mainly due to acquisitions.

Sales % sales growth comp.EBITAEBITA as % of salesEBITEBIT as % of salesNOCEmployees (FTEs)

Healthcare€ million unless otherwise stated

Emerging

Looking ahead

3Q07

1,5854

18811.91549.7

4,75128,473

2Q08

1,8065

19710.91387.6

8,76935,841

3Q08

• For 2008, acquisition and integration charges are estimated at approximately € 95M, of which around € 25M is expected to impact EBITA in Q4.

• Healthcare will accelerate a number of initiatives to improve margins and to further optimize its operations structure, particularly in Imaging Systems. This is expected to lead to charges of approximately € 50M in Q4.

• Philips will become the first-ever MR equipment maker in Latin America when it commences production at its factory in Brazil in late October ‘08, further strengthening Philips’ industrial footprint in emerging markets

Financial performanceKey figures

Sales per region 3Q08 Emerging markets

1,8003

19510.81387.7

8,38235,087

North America

50%

Latin America

5%

Asia Pacific17%

Europe/ Africa28% 15%

2323

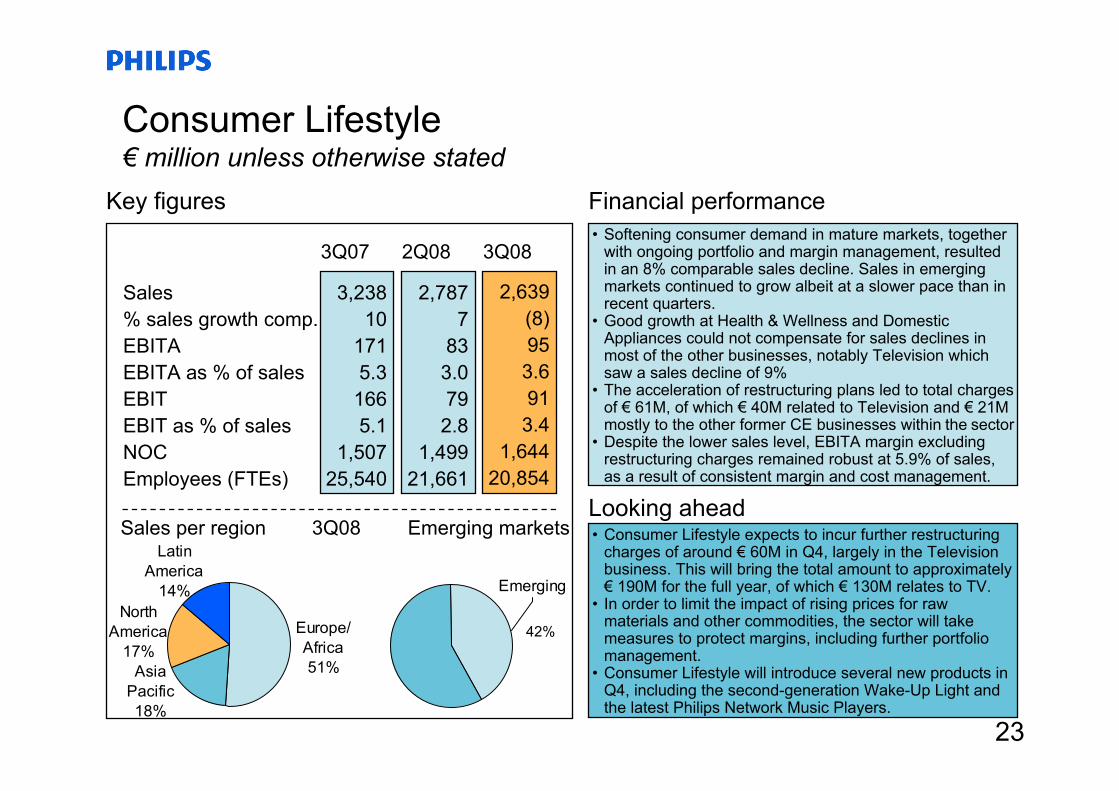

Sales% sales growth comp.EBITAEBITA as % of salesEBITEBIT as % of salesNOCEmployees (FTEs)

Consumer Lifestyle € million unless otherwise stated

Emerging

3,23810

1715.3

1665.1

1,50725,540

2,639(8)953.6913.4

1,64420,854

Key figures Financial performance

3Q07 2Q08 3Q08

2,7877

833.0792.8

1,49921,661

• Softening consumer demand in mature markets, together with ongoing portfolio and margin management, resulted in an 8% comparable sales decline. Sales in emerging markets continued to grow albeit at a slower pace than in recent quarters.

• Good growth at Health & Wellness and Domestic Appliances could not compensate for sales declines in most of the other businesses, notably Television which saw a sales decline of 9%

• The acceleration of restructuring plans led to total charges of € 61M, of which € 40M related to Television and € 21M mostly to the other former CE businesses within the sector

• Despite the lower sales level, EBITA margin excluding restructuring charges remained robust at 5.9% of sales, as a result of consistent margin and cost management.

Looking ahead• Consumer Lifestyle expects to incur further restructuring

charges of around € 60M in Q4, largely in the Television business. This will bring the total amount to approximately € 190M for the full year, of which € 130M relates to TV.

• In order to limit the impact of rising prices for raw materials and other commodities, the sector will take measures to protect margins, including further portfolio management.

• Consumer Lifestyle will introduce several new products in Q4, including the second-generation Wake-Up Light and the latest Philips Network Music Players.

Sales per region 3Q08 Emerging markets

North America

17%

Latin America

14%

Asia Pacific18%

Europe/ Africa51%

42%

2424

Sales% sales growth comp.EBITAEBITA as % of salesEBITEBIT as % of salesNOCEmployees (FTEs)

Lighting € million unless otherwise stated

Emerging

Looking ahead

• Comparable sales grew 6% compared to Q3 2007, driven by continued strong growth in emerging markets (17%) and energy-efficient lighting applications (18%), including very strong growth in LED solutions. This growth was tempered by a continued market slowdown in Western Europe and North America.

• Despite the visible market slowdown, both the European Professional Luminaires business and Genlyte in North America delivered comparable sales growth year-over-year

• Earnings of € 196M, including € 11M of restructuring and acquisition-related charges, were € 6M above the level of Q3 2007, which included net incidental gains of € 11M. The positive impact of the addition of the Genlyte EBITA was offset by margin compression in mature markets as a result of slowing demand, particularly in the construction and automotive segments.

• The increase in net operating capital and employees was primarily a result of the Genlyte acquisition in Q1 2008.

1,4962

19012.717811.9

4,11654,951

1,7856

19611.01689.4

6,34959,875

Financial performanceKey figures

3Q07 2Q08 3Q08

1,7396

20211.617510.1

6,12059,788

• Lighting expects to take a charge of up to € 100M in Q4 to further increase organizational effectiveness and strengthen its position as the industry leader.

• Lighting will also continue to focus on working capital and selectively increase prices further to protect margins.

• In the coming months, Lighting will expand its LED offerings for the professional and consumer segments, launching a range of innovative LED products.

Sales per region 3Q08 Emerging markets

North America

27%

Latin America

6%

Asia Pacific22%

Europe/ Africa45%

35%

2525

Sales% sales growth comp.

EBITA Technologies / Incubators

EBITA Others

EBITA

EBIT

NOCEmployees (FTEs)

Innovation & Emerging Businesses€ million unless otherwise stated

Looking ahead

• EBITA of Innovation & Emerging Businesses was in line with expectation. The earnings decline compared to Q3 2007 was attributable to higher investment in the Incubators and emerging markets, as well as lower IP license income.

1038

(35)

(6)

(41)

(41)

1895,534

10238

(33)

(2)

(35)

(35)

2176,057

70(27)

(40)

(6)

(46)

(46)

1525,509

Financial performanceKey figures

3Q07 2Q08 3Q08

• Investment in Innovation & Emerging Businesses is expected to be lower than the run rate of € 40 million per quarter, consistent with previous guidance.

• Triggered by the ongoing weakness in the semiconductor market, Assembléon expects restructuring activities in Q4, leading to charges estimated at € 18 million

2626

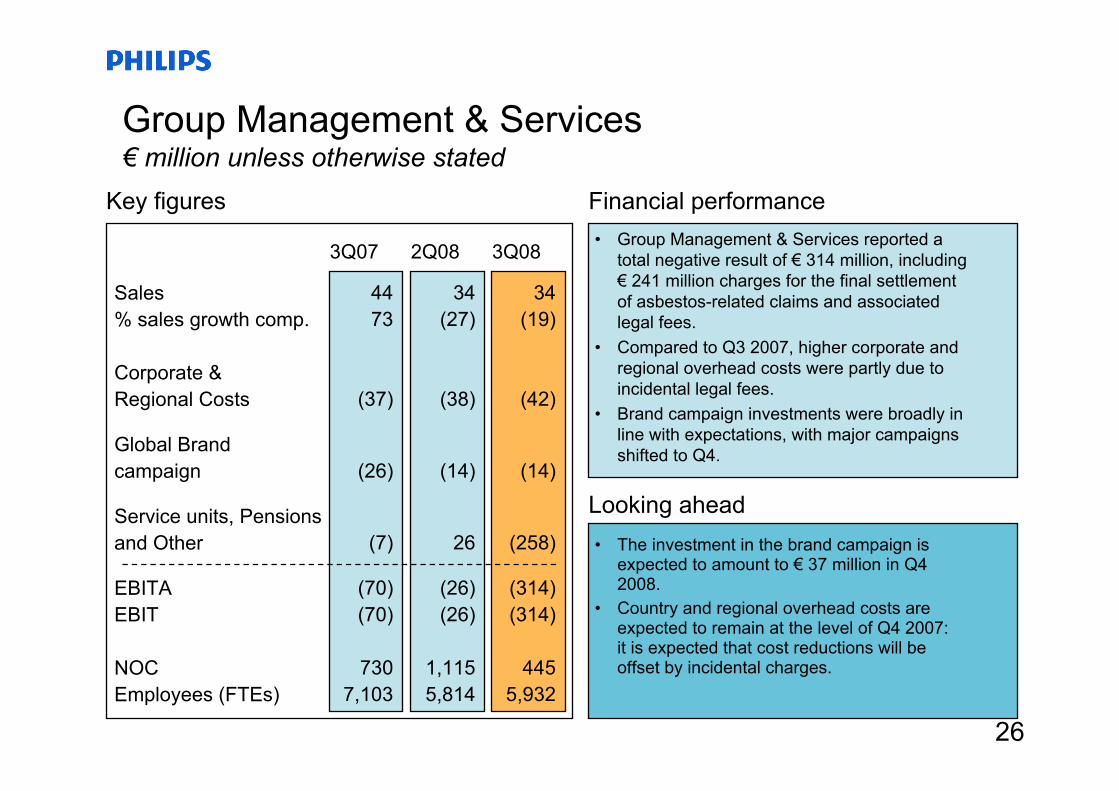

Sales% sales growth comp.

Corporate & Regional Costs

Global Brandcampaign

Service units, Pensionsand Other

EBITAEBIT

NOCEmployees (FTEs)

Group Management & Services€ million unless otherwise stated

Looking ahead

• Group Management & Services reported a total negative result of € 314 million, including € 241 million charges for the final settlement of asbestos-related claims and associated legal fees.

• Compared to Q3 2007, higher corporate and regional overhead costs were partly due to incidental legal fees.

• Brand campaign investments were broadly in line with expectations, with major campaigns shifted to Q4.

4473

(37)

(26)

(7)

(70)(70)

7307,103

34(19)

(42)

(14)

(258)

(314)(314)

4455,932

• The investment in the brand campaign is expected to amount to € 37 million in Q4 2008.

• Country and regional overhead costs are expected to remain at the level of Q4 2007: it is expected that cost reductions will be offset by incidental charges.

Financial performanceKey figures

3Q07 2Q08 3Q08

34(27)

(38)

(14)

26

(26)(26)

1,1155,814

27

Agenda

• Philips – who we are

• Results Q3 2008

Sector insights – Healthcare, Consumer Lifestyle & Lighting

• Moving to Philips ‘Vision 2010’

• Management agenda 2008

27

28

Simplified business structure in 3 core sectors: Healthcare, Lighting and LifestyleLTM September 2008

Net Operating CapitalSales100% = € 27.3B * 100% = € 16.8B *100% = € 2.4B *

EBITA

HealthcareConsumerLifestyle

Lighting

HealthcareConsumerLifestyle

Lighting

28%

34%

38%27%

27%

46%53%

9%

38%

ConsumerLifestyle

LightingHealthcare

* Excluding Central sectors (I&EB; GM&S), including pro forma numbers for Respironics and GenlyteSales of € 0.7B is included for 4Q07 and 1Q08 for Respironics and Genlyte EBITA of € 0.1B is included for 4Q07 and 1Q08 for Respironics and Genlyte 28

29

Recent acquisitions & divestments, coupled with further organic growth, leads to an increasingly well-balanced portfolioSales split

* Excluding Central sectors (I&EB; GM&S)

Healthcare

ConsumerLifestyle

Lighting

ConsumerLifestyle

Lighting

Healthcare

2007 > 2008

29

30

We simplify healthcare by focusing on the people in the care cycle – patients and care providers. Through combining human insights and clinical expertise, we aim to improve patient outcomes while lowering the burden on the healthcare system.

Healthcare

30

31

13%

15%

13%

25%

34%

Healthcare: Sales growth* 6 – 8%; 2010 margin 15 – 17%

15%

4%

53%

28%

Europe

North America

LatinAmerica

AsiaPacific

Imagingsystems

Customer services

HealthcareInformatics

Sales LTM September 2008

4% HomeHealthcare

• Strong market position and market share. • Focused approach to care cycles: Oncology, Cardiology, Women's Health• Ongoing growth, particularly in Monitoring/HI, Service and Clinical Care • Leader in new, growing Home Healthcare: Respironics, Lifeline, Raytel • Strong growth in emerging markets driven by brand and acquisitions• Margin improvement through increased low-cost sourcing, improved

supply chain & industrial footprint and lower IT costs

Including pro forma LTM Sep-2008 sales of € 0.4B for Respironics * Annual average comparable sales growth 31

Clinical care

3232

Key products and services of Philips HealthcareProviding comprehensive support

33

… we apply our technology to improve healthcare quality and reduce cost

The Philips healthcare difference

because meaningful innovations create valuefor patients and care providers.

33

34

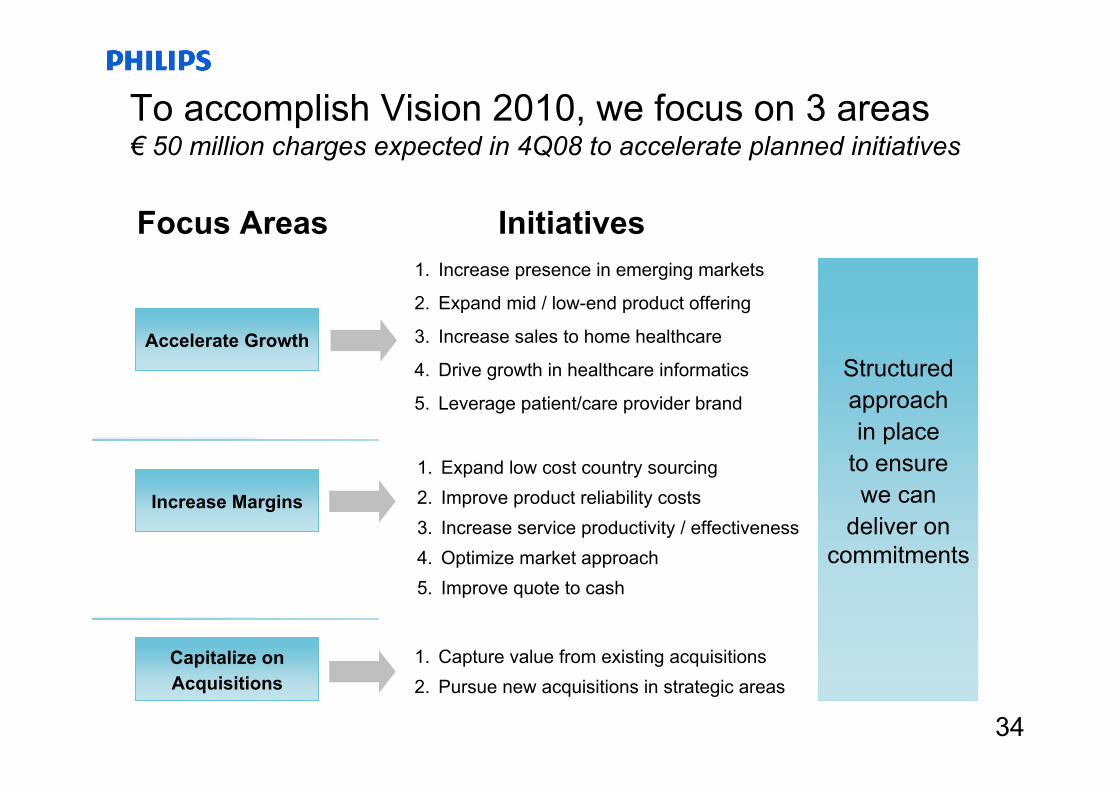

1. Increase presence in emerging markets

2. Expand mid / low-end product offering

3. Increase sales to home healthcare

4. Drive growth in healthcare informatics

5. Leverage patient/care provider brand

To accomplish Vision 2010, we focus on 3 areas€ 50 million charges expected in 4Q08 to accelerate planned initiatives

1. Expand low cost country sourcing2. Improve product reliability costs3. Increase service productivity / effectiveness4. Optimize market approach5. Improve quote to cash

1. Capture value from existing acquisitions2. Pursue new acquisitions in strategic areas

Focus Areas Initiatives

Accelerate Growth

Increase Margins

Capitalize on Acquisitions

34

Structuredapproachin place

to ensurewe can

deliver on commitments

35

• Announced on December 21, 2007; Closing March 10, 2008.• Respironics, with calendar ‘07 revenues of US$ 1.3B, EBITA of US$ 200M and a

CAGR in previous 5-years of 19%, strengthens Philips’ leadership position in Home Healthcare as well as “hospital based” healthcare given Respironics’ strong non-invasive ventilation and respiratory products for hospitals and clinics.

• Acquisition presents Philips with a leading position in the high growth respiratory devices and sleep apnea market and top 5 positions in oxygen therapy and ventilation

• The transaction further strengthens Philips’ strategy of developing solutions across the patient care cycle and expands its presence in home healthcare

• Respironics is an acquisition that positively differentiates us from our key competitorsby market segment, device segment, care cycle focus and disease focus

• Based on Respironics' management plan and our synergies, value would be created after the third year and with a more conservative view that we have used in our decision-making, we will be creating value within year five. The transaction will add to revenue growth and EBITA margin. Expected cost synergies approximately US$ 50M by 2010 run rate, and revenue synergies of approx US$ 180M by 2012 with an EBITA contribution of US$ 50M

• Q3 sales and EBITA in line with plan

Respironics: Leading player in respiratory marketEnterprise value € 3.2 billion

35

36

Guided by our brand promise of “sense and simplicity” and starting from our consumer insights, Philips offers rich, new consumer experiences that meet consumers’ desire for health and wellbeing.

Consumer Lifestyle

36

37

Consumer Lifestyle: Sales growth* around 6%; 2010 margin 8–10%

15%

11%

18%

56%

EuropeNorth

America

LatinAmerica

AsiaPacific

5%9%

14%

48%

10%

4%10%

Shaving &Beauty Health &

WellnessDomestic

Appliances

Television

Peripherals & Accessories

Other

AVM

• Strong marketing & sales capabilities; leveraging Philips brand• Focused on innovative lifestyle solutions for personal well-being• Consumer-driven insights and dedicated business models driving

innovation and differentiation• Expand category management to all businesses and regions • Deal with unsatisfactory EBITA margins in Television• Drive growth by strengthening presence in Emerging Markets

Excluding LTM Sep-2008 sales of € 0.3B for Home Network business that was divested in Q2 2008

* Annual average comparable sales growth

TVN-A

37

Sales LTM September 2008

Television Audio, Video &Multimedia

Shaving & Beauty

DomesticAppliances

Peripherals & Accessories

Health & Wellness

38

Process optimization

Realizing the cost synergies in Consumer lifestyleIn total € 190 million restructuring charges expected for the full year

38

Overall we are well on track to realize the upper end of the € 150 – 200 million savings as announced in September 2007

Organizational Structure

Geographical Footprint

• Functions focused on value delivery for increased efficiency• Rationalization of back office support• Greater relevance with 3rd party suppliers and partners• Improved supply chain effectiveness through shared platforms• Increased marketing effectiveness

• Elimination of duplication in functions at the executive level• Optimization of sales structure through clusters• Delayering our overall organization

• Footprint rationalization – Sales organization– Manufacturing & Supply– R&D

• Increased efficiency in locations and offices

39

As the world’s leader in Lighting, Philips is driving the switch to energy-efficient solutions, as well as shaping the future with exciting new lighting applications and technologies.

Lighting

39

40

Lighting: Sales growth* around 6%; 2010 margin 12 – 14%

21%

6%

28%

45% Europe

North America

LatinAmerica

AsiaPacific

• Global Leader in Lighting• Strong presence across the complete Solid State Lighting value chain• Readily available portfolio of innovative, energy efficient lighting solutions• Technology base and application IP will help to lead the changeover to new

lighting solutions• Profitable growth in fast-growing economies and innovative new market segments • End-user driven Innovation and Brand both drive our profitable growth

Including pro forma LTM Sep-2008 sales of € 0.3B for Genlyte* Annual average comparable sales growth 40

37%

11% 11% 4%

37%Lamps

LumiledsAutomotive & Spec.Light.Applic. Lighting Electronics

Luminaires

Sales LTM September 2008

41

Philips Lighting – balanced portfolio

Business structure * Geographic distribution *

37%

31%

11%

11%Lamps

ConsumerLuminaires

5%

ProfessionalLuminaires

Automotive &Spec. LightingApplications

LEDcomponents

4%

48% Applications 52% Components, Light sources

*) as if Genlyte would be consolidated, LTM Sept-2008**) as if Genlyte would be consolidated, 2007

33% of Philips Lighting sales from emerging markets

Market segmentation **

Homes

22%

19%

15%

13%

13%

8%4% 6%

Offices

OutdoorIndustry

Shops

TransportHospitality

Other

6%

5 key segments cover82% of our market

LightingElectronics

17%

4%

35%

WesternEurope

KeyEmerging

OtherMature 28%

OtherEmerging

NorthAmerica

16%

41

42

Lighting sales breakdown

Total WENA Other regions

Residential * 11% = 7% + 4%

Commercial * 30% = 20% + 10%

New build 41% = 27% + 14%

* Residential: Residential, Housing Commercial: Retail, Office, Industrial, Hospitals, Schools, Hotels, …Other: Road & Tunnel, City Beatification, Sport & Area, AutomotiveSource: Philips Lighting estimates

There is a significant correlation between the ‘Building & Construction industry dynamics’and ‘Residential & Commercial sales for Philips Lighting in Western-Europe & North-America (WENA)’ which accounts for around 27% of Lighting sales.

42

Lighting market - dynamic economic conditions

26%7%19%Other

100%39%61%Total

52%22%30%Commercial

22%11%11%Residential

TotalReplace-ment

NewBuild

43

Lighting market – full spectrum of measures€ 100 million charges expected in 4Q08 to further increase organizational effectiveness

State-of-the-art price management Focus on renovation & Total Cost of Ownership

Adequate strategies to deal with the Lighting industry dynamics

• Mix management• Cost productivity and efficiency• Purchasing effectiveness• Supply chain optimization• Channel diversification• Acquisition pipeline

Rundbau Gerling Konzern, Cologne, Germany• Renovation, 40 year old building.• TL-5 luminaires with omnisense;

– Presence detection– Daylight regulation

• Energy saving of up to 70%

Effective execution of Philips Lighting initiatives

e.g. Lumileds e.g. Lamps Prof Lum Cons Lum

ApplicationsLight SourcesComponents

Trade PricingTransaction Pricing Project Pricing

• Active price management in all parts of our business• Active focus on customer profitability

• Highly energy efficient solutions • New Solid State Lighting applications• Symbiosis between art and science,

function and fashion

Best practices and new ways of working Faster and better innovation

43

44

# 1

Philips Lighting – global leadership

Lamps

Professional Luminaires

Lighting Electronics

Solid State Lighting

AutomotiveLighting

Special Lighting

Western Europe

Eastern Europe

North America

Latin America

Japan Asia/ Pacific

Total# 2 or 3Philips position < # 3

ConsumerLuminaires

No data

44

45

Genlyte: Leading N-A Luminaires manufacturerEnterprise value € 1.8 billion

• Closed on January 22, 2008.

• Acquisition is consistent with Philips’ strategy to strengthen its leadership position in Lighting. Combination created the #1 Lighting company in North America and established Philips as the largest Luminaires company globally.

• Luminaires & Controls are a spearhead in developing “green” lighting markets, including Solid State Lighting (SSL). Genlyte will be a cornerstone of growth in SSL.

• Post merger integration is well on track to deliver the expected synergies.

• Sales growth in Q3 was 2%, despite softer market conditions.

45

46

Agenda

• Philips – who we are

• Results Q3 2008

• Sector insights – Healthcare, Consumer Lifestyle & Lighting

Moving to Philips ‘Vision 2010’

• Management agenda 2008

46

47

Having delivered on our 3 year target in 2007, we have announced a new ‘Vision 2010’ ambitionAnnounced April 2008

Doubling of 2010 EBITA per share compared to 2007 through:

• Improvement of Group EBITA from 7.7% in 2007 to 10-11% in 2010

• Driving comparable growth at a minimum of 6% average per year for the period 2008-2010

Achieve a return on invested capital for 2010 at the level of 12% - 13%

47

Healthcare

Lighting

Consumer Lifestyle

Reduce group overhead cost as % of sales

13.2%

11.9%

6.4%

15 – 17%

12 – 14%

8 – 10%

20102007EBITA margin

48

Vision 2010 scorecard

IMPROVEMENT OF EBITA % TO 10 – 11%

ANNUAL AVG. GROWTH OF 6% FOR '08-'10

SHARE BUY-BACK OF € 5B

M&A

ROIC of 12 – 13% by 2010

48

Doubling of EBITA per

share by 2010 compared to

2007

- Acceleration of plans to improve margins

- Impacted by macro economic developments

- € 3.1B* worth of shares bought back- Significantly slowdown of completion

- Post merger integration on track- Further acquisitions

* per October 10, 2008

49

Well-positioned to leverage a number of key global trends centered around health & well-being

Global trends

Climate Change

Aging population

Globalization, urbanization and rise of emerging markets

Consumer empowerment

Sustainable development

Better healthcare for all at lower cost

Home care, independent living

Personalized experiences and atmospheres

Personal well-being

Energy efficiency

Philips opportunities Philips focus

Brand“sense and simplicity”

InnovationOpen innovation

49

50

0

1000

2000

3000

4000

5000

6000

7000

1970 1980 1990 2000 2005

CanadaFranceItalyJapanUnited KingdomUnited StatesChina

Healthcare trends – aging population, cost pressures, health-at-home, emerging markets growth

Source: UN, 2006 Revision of World Population Prospects and World Health Organization website

• Global population is increasing and continues to age

• People are living longer with chronic diseases

• Healthcare costs – especially in mature economies – are becoming unsustainable

• Healthcare at home is an increasingly viable and cost effective complement to in-hospital care

• People are becoming increasingly aware of the impact of lifestyle on health

World population by age group, 1950-2050

Healthcare expenditure per capita, US $

People over 60

50

5151

ActiveCrystals

Arcitec

PortableMedia devices

Flexcare

Lifestyle trends – healthy living/healthy home, more personal care, technology-made-easy, design

• Core well-being consumer shows attractive demographics and is likely to be a highly profitable customer

• The Lifestyle targeted market is 3x the size of the CE market + DAP market

• Increased demand for personal care product categories and technology-advanced, easy-to-use customer solutions

• Design has become an important competitive differentiator

• Consumers are becoming increasingly ‘eco-aware’of issues facing the planet

52

0

20

40

60

80

100

120

1995 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 2008

Oil at a historical high, yearly average price (US dollar) *

Huge potential for energy saving

Area of lighting Energy saving

CO2 savings per lamp per year

Road lightingShop LightingOffice & Industrial LightingHome LightingLEDs

57%80%61%80%80%

132 kg CO2

140 kg CO2

93 kg CO2

41 kg CO2

41 kg CO2

• Energy costs are rising across the globe, driven by high oil prices

• Increased awareness/legislation around climate change is driving a reduction in CO2

• Atmosphere-creating and safety-enhancing lighting solutions increasingly become part of individual and community well-being

• Demand for (energy-efficient) lighting in emerging markets continues to grow

• Future LED solutions: application IP and luminaries will be key

Lighting trends – rising energy costs, increasing awareness of climate change, product innovation

* Source: OPEC Reference Basket (ORB), www.opec.org 52

US dollar

53

Sustainability is a strategic driver• Our superb heritage in innovation and

design helps us realize meaningful innovations in Healthcare, Lighting and Consumer lifestyle

• Our brand promise Sense and Simplicityand sustainability provide the framework for the way we do business.

• Our “Vision 2010” strategy fuels growth through sharpened, market-focused, people-centric strategies

• One of the strategic drivers behind Vision 2010 is a commitment to sustainability and making a difference in energy efficiency

Clear example of how we are driving business growth through Sustainability is the launch of our EcoVision4 program in 2007:• Generate 30% of revenues from Green Products over a period of 5 yrs (‘07-’12) – up from 15%• Double our investment in Green Innovations to € 1 billion by 2012; and• Further increase the energy efficiency of our operations by 25% by 2012. 53

54

Agenda

• Philips – who we are

• Results Q3 2008

• Sector insights – Healthcare, Consumer Lifestyle & Lighting

• Moving to Philips ‘Vision 2010’

Management agenda 2008

54

55

In 2008, our focus will be on executionThe Management Agenda for this year

• Integrate and leverage recent acquisitions, delivering anticipated return on investment

• Take decisive steps to structurally deal with unsatisfactory EBITA margins in Television business

• Improve productivity as a driver for margin expansion

• Step up resource investment in Developing Markets to accelerate growth in excess of 2x GDP

• Increase innovation focus in support of Philips growth ambition

• Continue to drive a culture of superior customer experience

• Bring employee engagement to high performance benchmark

55

56

Summary

CreatingShareholder

Value

• Simplified portfolio of world-class businesses built around a strong, global brand

• Well-positioned to leverage a number of important global trends to drive future growth and profitability

• Superior user-insight driving application of our technology in the simplest way possible resulting in smartly-designed, innovate, easy-to use products and applications

• Focus on integration and leverage of recent acquisitions

• Continued investment in growth in emerging markets

• Improved predictability of results

• Ambition to more than double EBITA per share by 2010

56

58

Appendix

58

59

SalesComparable sales growth %

EBITAEBITA as % of sales

Net income

Cash flow from operations

Dividend per share

Dividend yield

2006 2007

26,6826.4%

1,3865.2%

5,383

330

0.60

2.0%

26,7934.9%

2,0657.7%

4,168

1,519

0.70

2.3%

1 – MedQuist has been restated to Discontinued Operations in all years2 – Dividend per share based on its year’s profit; payout in next year; in €.3 – Dividend yield is calculated as dividend based on prior-year profit divided by average share price of prior year

3

Solid progress on key financials€ million

2005

25,4454.5%

1,6526.5%

2,868

1,147

0.44

1.9%

Includingproduct reliability charges of € 256 million

IncludingPension funding and TSMC tax payment totaling € 1 billion

1

2

59

60

–

–

–

1,831

670

–

–

2,501

Total

950

1,106

1,604

6,684

3,155

154

6,960

20,613

2007

–

–

–

4,083

1,547

–

(99)

5,531

2008

Cash generated from sale of major participations€ million

Sale securities

Atos Origin

NAVTEQ

TSMC

LG Displays

FEI

Semiconductors (NXP)

Total

20052004

883

552

672

–

–

–

–

2,107

67

554

932

770

938

–

–

3,261

2006

–

–

–

–

–

154

7,059

7,213

60

61

Cash utilization€ million

Acquisition StentorAcquisition Witt BiomedicalAcquisition LifelineAcquisition Intermagnetics Acquisition VISICUAcquisition RespironicsAcquisition LumiledsAcquisition PLIAcquisition Color KineticsAcquisition GenlyteAcquisition Avent

Extra funding pensions (UK&US)Share repurchase programDividend

€ 5.0 billion buy-back program

Total

2005/2007194110583993

––

788561515

–689683

5,1871,686

–

11,989

Announced /being implemented

––––

1983,196

–––

1,805–––

6985,000

10,897

Total

9,63242.1 %

6833.0 %

12,57154.9 %

22,886* Still to be completed** Excluding acquisitions of Bodine, Power Sentry, TIR, Health Watch, DLO, LTI, Ximis,

Raytel, Emergin, Tomcat, Goldway and Dixtal because of relative size.

*

**C

onsu

mer

Life

styl

e, L

ight

ing

&H

ealth

care

61

6262

1,2821,201

1,107 1,098 1,063 1,065 1,028984 946

848

1,087

4Q04 4Q05 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 **

Basic shares outstandingMillion

(34)%

* After finalizing the € 5B repurchase program; calculation includes avg. purchase price of € 21/share for remaining buy-back** Going forward, in light of both the risks and opportunities presented by the deterioration of the economy and the financial

market turbulence, we will slow down the completion of the program.

Estimate on completion of

€ 5B buy-back *

6363

Peer group adapted to Philips’ transformation

Previous peer group (until 2006)

ElectroluxEmerson ElectricGeneral ElectricHitachiPanasonicSiemens

EricssonGilletteIBMIntelLG ElectronicsLucentMarconiMotorolaNEC

Maintained membersElectroluxEmerson ElectricGeneral ElectricHitachiPanasonicSiemens

New membersHoneywellJohnson & JohnsonSchneider ElectricToshiba3M

Existing peer group (2007-)

NokiaSamsungSanyo ElectricSharpSonyTexas InstrumentsTyco InternationalWhirlpool

Maintained members

64

Major investments

Quoted

LG Displays

TPV

Non-quoted

NXP

Total

number shares rounded in millions

47

263

18

% ownership

13.2

13.4

19.9

Market value

644

48

Book value

555

1,247

1

October 9th, 2008in € million

1 Economic ownership 64

65

Major investmentsDevelopment of major investments

% Holding TSMC

0%2%4%6%8%

10%12%14%16%18%20%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2005 2006 2007 2008

% Holding LG Displays

0%5%

10%15%20%25%30%35%40%45%50%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2005 2006 2007 2008

65

66

Overview€ million

66

Sales and Comparable growth by sector 2006 2007 per quarter 2007 2008 per quarterJan.-Dec. 1st 2nd 3rd 4th Jan.-Dec. 1st 2nd 3rd

Healthcare 6,562 1,431 1,625 1,585 1,997 6,638 1,474 1,800 1,8064% 4% 4% 3% 4% 5% 3% 5%

Consumer Lifestyle * 13,108 2,816 2,786 3,238 4,490 13,330 2,662 2,787 2,639-2% -6% 10% 11% 4% 0% 7% -8%

Lighting 5,466 1,474 1,464 1,496 1,659 6,093 1,711 1,739 1,7858% 6% 2% 8% 6% 3% 6% 6%

I&EB 1,379 160 110 102 163 535 79 103 70

GMS 167 49 48 44 56 197 39 34 34

Philips Group 26,682 5,930 6,033 6,465 8,365 26,793 5,965 6,463 6,3343% 0% 7% 8% 5% 1% 6% -2%

* of which Television business 6,559 1,293 1,258 1,511 2,208 6,270 1,227 1,359 1,195

EBITA and EBITA% by sector 2006 2007 per quarter 2007 2008 per quarterJan.-Dec. 1st 2nd 3rd 4th Jan.-Dec. 1st 2nd 3rd

Healthcare 860 119 218 188 348 873 121 195 19713% 8% 13% 12% 17% 13% 8% 11% 11%

Consumer Lifestyle * 692 141 106 171 430 848 77 83 955% 5% 4% 5% 10% 6% 3% 3% 4%

Lighting 608 186 161 190 185 722 200 202 19611% 13% 11% 13% 11% 12% 12% 12% 11%

I&EB -75 (31) (36) (35) 21 (81) (68) (41) (46)

GMS -699 (45) (63) (70) (119) (297) (65) (26) (314)

Philips Group 1,386 370 386 444 865 2,065 265 413 1285% 6% 6% 7% 10% 8% 4% 6% 2%

* of which Television business 155 (51) (69) (43) 95 (68) (95) (112) (73)2% -4% -5% -3% 4% -1% -8% -8% -6%