royal frieslandcampina n.v. cooperative entrepreneurship! jan uijttewaal (frieslandcampina).pdf ·...

TRANSCRIPT

Royal FrieslandCampina N.V.Cooperative entrepreneurship!

Madrid, 13 May 2014

19,000 ambitiousmember farmers arethe owners ofFrieslandCampina

Introduction Mr Jan Uijttewaal

2

3

Six farmersfound the firstdairy cooperative

1886

Friesland Foodsreceives royaldesignationon its 152thanniversary

2004

Acquisitionof Nutricia

Dairy & Drinks Group

2001

Merger of Coberco,Friesland Dairy Foods,

De-Zuid-Oost-Hoekand De twee Provinciën

1997Founding of Cobercoin Zutphen

1965Founding of CCF

in Leeuwarden

1913

Nine farmerstake over a

cheese factoryin the Dutch

Wieringerwaard

1871

1880Founding of the

first dairycooperatives

1926Founding of the

De Meijerij Veghel/De Melkindustrie Veghel

1947Campina brand

introduced

1979DMV Campina andMelkunie Holland

introduced

1989Founded

Campina Melkunie

2001International launchof formation ofinternational Campinabrand and Cooperative

1993Acquisition ofSüdmilch(Heibronn)

2012Acquisition ofAlaska MilkCorporation,Philippines

Acquisition ofIDB Belgium N.V.

2012

2008

2013Acquisition ofZijerveld enVeldhuyzen B.V.and G. den HollanderHolding B.V.

Friese Flag, Dutch Babyand Bonnet Rougeare registered forinternational markets

1919

Cooperative tradition ofover 140 years

and a clear ambition:to create the mostsuccessful,professional andattractive dairy cooperative

5

Every day wenourish millionsof consumersaround the world

6

Milk is a natural source of

nutrients.

We process the milk,

supplied by our member

dairy farmers, into a wide

range of dairy products

Ambition

Foundation

Growthcategories

Respondto needs

Capabilities

To create the most successful, professional and attractive dairycompany for its member dairy farmers, employees, customersand consumers and for society by providing people around theworld with essential nutrients from dairy products during everyphase of their lives

route2020: sustainable growth andvalue creation

Dairy-basedbeverages

Infantnutrition(B2B, B2C)

Strongholds& geographicexpansion

Brandedcheese

Food-servicein Europe

Basicproducts

Growth &development

Dailynutrition

Health &wellness

Functionality

Talentmanagement

Milkvalorisation

Innovation Business model& cost focus

Chainadvantages

Sustainable dairyfarming &business operations

The way weWork & safety

Goodnessof dairy

8

Our farmers

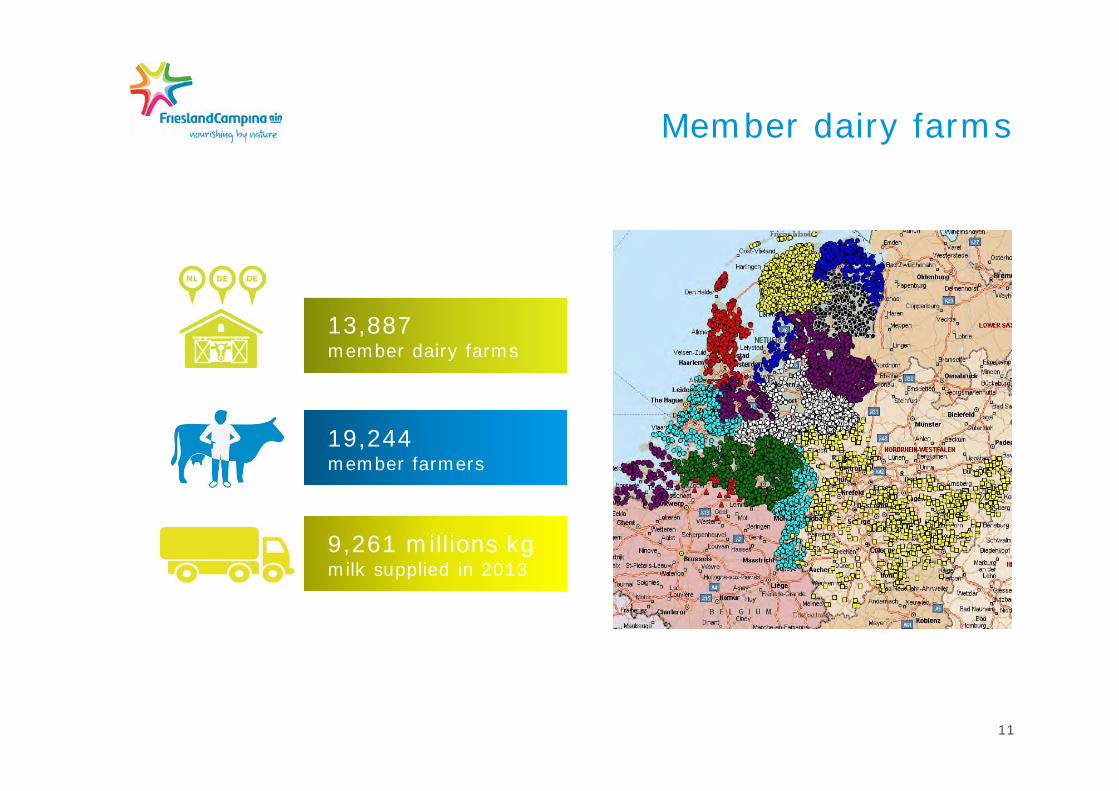

We are 100 percent owned by ZuivelcoöperatieFrieslandCampina, which has more than 14,000 memberdairy farms in the Netherlands, Germany and Belgium

Cornerstones of the co-operative

Members have the right to● Deliver all the milk to FrieslandCampina● Take part in decision-making process/voting● Pass on membership to successor

Members are obliged to● Deliver all produced farm milk to FrieslandCampina● Take part in the members’ financing of the company● Comply with the regulations

19,000 ambitiousmember farmers arethe owners ofFrieslandCampina

11

Member dairy farms

13,887member dairy farms

19,244member farmers

9,261 millions kgmilk supplied in 2013

12

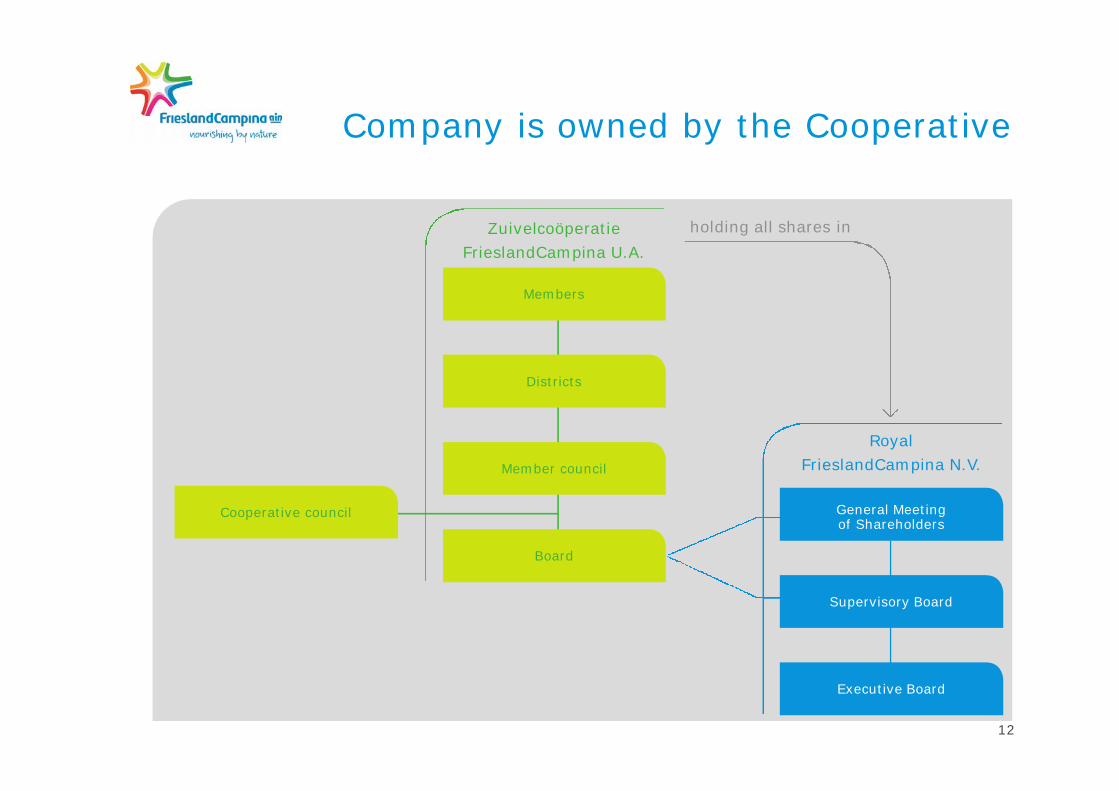

Company is owned by the Cooperative

Cooperative council

Members

Member council

Supervisory Board

Districts

Board

Executive Board

Zuivelcoöperatie

FrieslandCampina U.A.

Royal

FrieslandCampina N.V.

General Meetingof Shareholders

holding all shares in

13

Four business groups

Executive Board

Corporate Centre

Consumer ProductsEurope, Middle East

& Africa

Consumer ProductsAsia

Cheese, Butter& Milkpowder Ingredients

FrieslandCampina BrandedNetherlands / Belgium

FrieslandCampina Retail Brands Europe

FrieslandCampina Germany

FrieslandCampina Hellas

FrieslandCampina Hungary

FrieslandCampina Romania

FrieslandCampina Russia

FrieslandCampina Professional

FrieslandCampina UK

FrieslandCampina Middle East

FrieslandCampina WAMCO Nigeria

FrieslandCampina West Africa

FrieslandCampina Indonesia

FrieslandCampina Malaysia / Singapore

FrieslandCampina Thailand

FrieslandCampina Vietnam

Alaska Milk Corporation, Philippines

FrieslandCampina China

FrieslandCampina Hong Kong

FrieslandCampina Cheese

FrieslandCampina Cheese Specialties

FrieslandCampina Butter

FrieslandCampina Milkpowder

FrieslandCampina Cheese Germany

FrieslandCampina Cheese France

FrieslandCampina Cheese Spain

FrieslandCampina Export

Yoko Cheese, Belgium

Zijerveld, the Netherlands

Den Hollander Food, the Netherlands

FrieslandCampina Domo

FrieslandCampina DMV

FrieslandCampina Kievit

FrieslandCampina Creamy Creation

FrieslandCampina Nutrifeed

Satro

DFE Pharma

14

In order to valorise the milk supplied

The objectiveof a business withno member milk isto generate profitabove our EBIT

hurdle

Profitability

The objective ofour member milk

intense businessesis to valorise

milk at positiveEBIT margins

Member milk usage

151 before goodwill impairment

With good results

Figures 2013

10.8% up

Revenue

313 million euro

Operating profit

513 million euro

before goodwill impairment

2.7%Operating profit as a % of net revenue

4.5%before goodwill impairment

Revenuein millions of euros

11,41810,309

9,626

8,972

2013

2012

2011

2010

Operating profitin millions of euros

513487

403

434

20131

2012

2011

2010

2013 313

Operating profit as a % of net revenuein percentages

4.54.7

4.2

4.8

20131

2012

2011

2010

2013 2.7

CooperativeCouncil (21)

Clear roles and responsibilitiesin the cooperative

Members(14.132)

District Council(21 x 10)

Members’Council (210)

Board of theCooperative(9)

• Each Member has voting rights based on supplied milk• Right of initiative: 100+ members

• Authorised and responsible for number of activities asmember-involvement nd in the region

• Contact point for Members, knows what moves them

• General Assembly of the cooperative• Approval of specified important decisions taken by the

Board in its role as General Assembly of Shareholders ofthe company

• Sounding Board for Board and Members• Advises Board for larger in-/divestments, acquisitions &

mergers

• Manages the coop., responsible for decisions and process• Form (with 4 externals) Supervisory Board of the company• Voting right for the shares in the company held by the coop.

Milk price

Guaranteed price

● Equal to the average milk prices in Germany,The Netherlands, Denmark and Belgium(46 bn kgs of milk)(reflects the market value for raw milk)

● Independent from the results of FrieslandCampina

● Monthly estimated payment during the year

● Starting point to calculatethe profit of the companyFrieslandCampina

● Performance Premium

● Addition member bonds

Profit appropriation 2014-15-16

Companyprofit

35%

20%

45%

Performancepayment

Fixed memberbonds

General reserve

Evaluation every three years

How members finance their company

General reserve● addition every year● depends on profit of the company

Fixed member bonds● addition every year● depends on profit of the company

● transformed in free member bonds after farmer ends farming

Member certificates● generated once, in Dec 2008, with the merger● transformed in free member bonds after farmer ends farming

Free member bonds● Members can buy and sell free member bonds at an internal market

Companyprofit

35%

20%

45%

Performancepayment

Fixed memberbonds

General reserve

20

2009 2010 2011 2012 2013 2009 2010 2011 2012 2013

Revenuein millions of euros

8,160

8,9729,626

10,309

11,418

Performance premium +member bondsin euros per 100 kilos milk

0.94

1.96 1.83

2.37

3.04

Five years of FrieslandCampina

Our position in the dairy sector

21Figures 2012in billion of euros

Company Dairy Revenue

3.3

3.5

4.1

4.4

4.4

4.5

4.5

4.5

5.1

5.8

6.0

6.5

6.9

8.4

9.4

10.5

12.5

14.0

15.1

23.4

20. Müller - Germany

19. Schreiber Foods - USA

18. Bongrain - France

17. DMK - Germany

16. Kraft Foods - USA

15. Mengniu - China

14. Sodiaal - France

13. Morinaga - Japan

12. Yili - China

11. Unilever - Netherlands/UK

10. Meiji - Japan

9. Saputo - Canada

8. Dean Foods - USA

7. Arla Foods - Denmark/Sweden

6. Dairy Farmers of America - USA

5. FrieslandCampina - Netherlands

4. Fonterra - New Zealand

3. Lactalis - France

2. Danone - France

1. Nestlé - Switzerland

5. FrieslandCampina - Netherlands

Source: Rabobank, August 2013

North andSouthAmerica

UnitedStatesaten

Africa and theMiddle East

NigeriaGhanaUnited Arab EmiratesSaudi Arabia

Asia andOceania

IndonesiaMalaysiaSingaporeThailandVietnamPhilippinesChinaHong KongIndiaJapanNew Zealand

Figures 2013* in millions of euro’s

Europe

NetherlandsGermanyBelgiumGreeceHungaryRomaniaRussiaFranceSpainItalyAustriaUnitedKingdom

19locations

30locations

68locations

6locations

69 production locations worldwide

2,5 billion euros of investments

236

261

376

423

559

652

2009

2010

2011

2012

2013

2014

>70%

€ 1,8 billion

€ 2,5 billion

in million euros

Thisim

FrieslandCampina Innovation Centre

400 specialists are working in new R&D Center in Q2 - 2013

Thisim

25

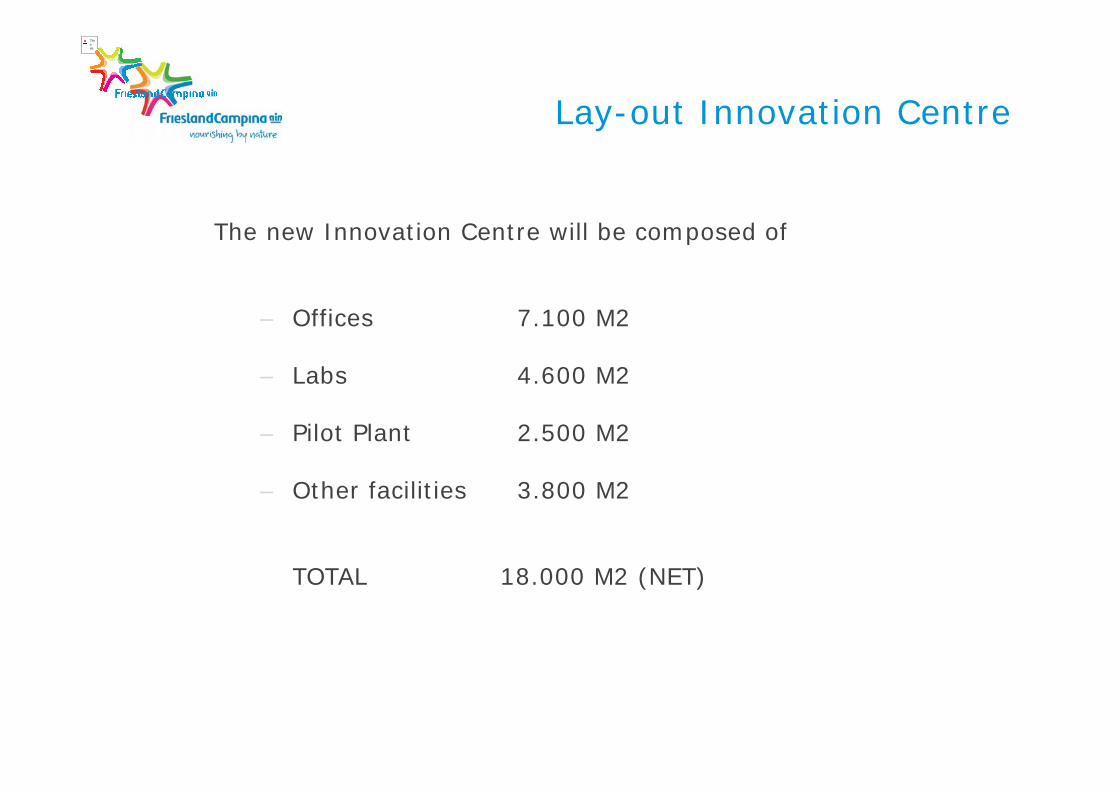

Lay-out Innovation Centre

The new Innovation Centre will be composed of

– Offices 7.100 M2

– Labs 4.600 M2

– Pilot Plant 2.500 M2

– Other facilities 3.800 M2

TOTAL 18.000 M2 (NET)

Strategy route2020

Sustainable growth and value creation

Ambition

Foundation

Growthcategories

Respondto needs

Capabilities

To create the most successful, professional and attractive dairycompany for its member dairy farmers, employees, customersand consumers and for society by providing people around theworld with essential nutrients from dairy products during everyphase of their lives

route2020: sustainable growth andvalue creation

Dairy-basedbeverages

Infantnutrition(B2B, B2C)

Strongholds& geographicexpansion

Brandedcheese

Food-servicein Europe

Basicproducts

Growth &development

Dailynutrition

Health &wellness

Functionality

Talentmanagement

Milkvalorisation

Innovation Business model& cost focus

Chainadvantages

Sustainable dairyfarming &business operations

The way weWork & safety

Goodnessof dairy

28

Consumer Products Europe,Middle East & Africa

Consumer Products Asia

Cheese, Butter & Milkpowder Ingredients

29

Our customers and consumers

● Consumers around the world

● Retail chains, wholesalers, local shops

● Professionals in the hotel, restaurant, café and bakery

● Food producers and pharmaceutical companies

30

FrieslandCampina brands

Consumer products Professionalmarket

Ingredients

Wheels(10%)

Pre-packs (20%)

Fresh-packs (70%)Eroski & Carrefour

FrieslandCampina brands in Spain

FrieslandCampina brands in Spain

33

●10,8%

volume growthin infant nutrition

●10,8%volume growthin dairy-basedbeverages inAsia and Africa

●9,5%volume growth inbranded cheese byincreasing exports

● Investments:559 miljoen euro:

Mainly in expansionof productioncapacity for infantnutrition

●Safety and safetyawarenesssubstantially improved

Acceleration ofour strategy route2020

●Ongoingimplementation ofsustainabilityprogrammes

34

Sustainability

● Safety and safetyawarenessimproved

● Progress inprogrammes saltand sugar reduction

● Sino-Dutch DairyDevelopmentCentre in China

● Support of 130.000small farmers inIndonesia, Vietnam,Thailand andMalaysia

● Partnerships RedCross and Agriterra

● Action planfor manureminerals engreenhouse gases

● Sustainable energyprojects memberfarmers and plants

● 80% memberfarmers applyoutdoor grazing

● Vision onsustainabledevelopment ofdairy sector

35

Responsible dairy farming: Actual levelat farm and processing level since 1990

At farm level: At processing level:

Improved animal health, food safety andlandscape quality

Reduction of minerals (N and P to water)

Cross compliance EU: Meadow birds,biodiversity improvements etc

Reduction of GHG 1990 – 2009 -> 20%

Energy agreements -> reduction ofenergy use of >20% since 1995

Reduced: water use, -waterpollution

re-use of waste,

acidified emissions (NOx, SO2)

36

4 pillars of the sustainabilityapproach and objectives

4. Outdoor grazing: at actual level

Reduction of GHGwith 30% between

1990 and 2020

2% energyreduction per year

Visible care for nature

Reductionantibiotics

Mastitis/clawproblems: atnatural level

1. Energy andclimate

2. Animalhealth and -

wellness3. Biodiversity

Responsible soy from2015

Improved mineralbalance

37

2008: MergerFriesland Foods and Campina

Why merge?

allowing for more power, appeal,stability and continuitySize

Synergy

Strategy

resulting in lower costs, higher revenuesand accelerated knowledge development

converting members’ milk intomore value for consumers, customers,employees, and thus for members

FrieslandCampina will benefit best from the increasingglobal milk product demand and from the liberalisation of theEuropean dairy sector, through:

1

2

3

39

Strategic assessment and target selection

Merger between Friesland Foods and Campina best option

24

26

28

30

32

34

36

2007 2008 2009 2010 2011 2012 2013 2014 2015

EU and WW milk price will convergeThe world is changing

EU price forecast

World price forecast

Consumerdemand

Competitivepressure

Tradeglobalisation

Industrialinnovation

Arranged before the merger

• Chairman of the cooperative board

• Chairman executive board

• Name of the new company and cooperative

• Location headquarters

• Financing structure

• Milk payment system for the members

• Storyline: why merge

Overview merger phases

• Convenant Nov. 2007

• Letter of Intent Dec. 2007

• Merger agreement May 2008

• Pre merger integration planning Dec. 2008

• Merger Dec. 2008

• Post merger implementation Jan 2009onwards

42

Specific topics in cooperatives merger

• Performance price reflectspast

• Milk price future should beequal

• Equity value should beequal per KG milk

• Difficult to obtain additionalpayments from the farmers

Valuation

• Milk price structure

• Financing structure

• Governance structureCooperative

• Relation betweenCooperative (UA) andCompany (NV)

Governance

43

SepJul2008

OctAugApr May Jun Nov Dec

First phase

Activity

Second phase

Pre-notification

EC clearance before year end

Pre-notification phase

• Focal issues:– laborious process with

20 affected markets– very significant

information requestsby EC (just describingBasic Dairy has takenfull month)

• Focal issues:– Filing on June 12 so as to

have a full Phase I and IIbefore year-end

– Goal is to reduce thenumber of critical markets

First phase Second phase

• Focal issues:– Full use of Phase II

results in a decision endDecember

– Early agreement onremedies could advancethis timing

1

44

Transition plan focus on Day 1 and Day 100

Pre – Day 1 First 100 Days

Dec, 2008 Mar 30, 2009

Day 1

Dec 2011

First 1,000 Days

Focustransitionplans

‘Integrate thecompany’• Stabilize

organization• Communicate• Share information

and clarify

‘Capture iniatives’

‘Strengthenperformance’Stabilize organization• Finalize transition• Organize for growth

Integration plan

‘Close deal’• Approval regulator,

unions, members

‘Prepare for post-close’• Prepare for

organization, locationchanges

• Prepare for quick-wins

24

DecNovOctSep

44

AugJul

474645

Jun

434241 484039383736 525150493534333231302928272625

Finalize locationsand prepare impl.

Develop org. transition plan

Develop applications

Prepare impl.

Prepare imp.

EC reaction period

Development Corporate ID

Translate initiativesinto transition plan

Fine tune processes and create process transition plan

B-2 org. andprepare locations

Prepare for Day 1communication

Fill in Form Ro

Prepare impl.

Prepare closure

Pitch

Create change plan

Develop other “deeladviesaanvragen”

Prepare for Form Ro anddecide on all open issues

Design to-be pro-cesses (blueprint)

Review strategy

Develop First 100 Days communication plan

Prepare appointments B-2

Develop “deelaanvraag” and get approval from unions/COR

Brand Key

Define direc-tion (OBT)

B-1 org.

Identify and compare key as-is processes

Confirm old and identify new initiatives, synergies andprocess improvements

Develop com. planQ3/Q4

Prepare appointments B-1

Prepare legal documents and prepare closure

Phase 1

Harmonize cooperation: procedures and processes

Themes / teams

• Way we work(OBT, HR, Com, Corp ID)

• Appointments/talentretention (HR + OBT)

• Cooperationharmonization

• Corporate ID

• Strategy, organization& location(BGs & CC & SS)

• Communication

Exp. ap.ECend Nov

• Medezeggenschap/HR

• Initiatives(BGs & CC & SS +Procurement)

• Mededinging

• Legal

Day 1Dec 20

LegalclosureDec 15

Teams impl.readymid Nov

Form Roto EC

CORC AVCSep 16

Internaldeadlinefor FORMRO Sep 16

Today

• Processes(Functional teams)

Phase 1 - Finalize initiatives and organizationPhase 2 - Develop transition plan and prepare forimplementation

Key interdependencies*Time passed Completed

Behind schedule

Critical

Close Deal

EnableTransition

Createvalue

On schedule

DA

Y1

–D

ecem

ber

20

Pre-merger integration planning