roscas and credit cooperatives -...

TRANSCRIPT

ROSCAs and Credit Cooperatives

September 2007

() ROSCAs September 2007 1 / 24

There is a wide spectrum of indigenous �nancial institutions

,! family and friends

,! ROSCAs

,! credit cooperatives

,! moneylenders

Understanding ROSCAs and credit cooperatives helps to undertandcosts and bene�ts of group lending

,! also emphasizes link to savings constraints (not just credit problems)

() ROSCAs September 2007 2 / 24

Rotating Savings and Credit Associations (ROSCAs)

Also known as tontines (Africa), hui (Taipei), tanda (Mexico)

Very common throughout the world and very important

,! 40% of micro�nance borrowers in Indonesia

,! funds involved equal 10% of GDP in Ethiopia (1977)

,! 1/2 of rural residents in Cameroon, Cote d�Ivoire, Congo, Liberia,Togo and Nigeria

,! 1/5 of Taiwanese population (1977-95)

Several alternative structures:

,! pre-determined order ROSCA

,! random ROSCA

,! bidding ROSCA

() ROSCAs September 2007 3 / 24

Characteristics

"Local" institution (neighboourhood, workplace)

Varying membership: e.g. 5 to 100 in Bangladesh (Rutherford 1997)

Varying pot size (e.g. $25 to $400 in Rutherford�s survey)

Indivisible goods (e.g. school fees, rent, medical costs, equipment)

() ROSCAs September 2007 4 / 24

A Simple Model of a Random ROSCA

Number of individuals = n

Preferences at each date

U =�v(c) without indivisible goodv(c) + θ with indivisible good

where

v(c) =�

c if c � c�∞ if c < c

y = monthly income

B = cost of indivisible good

T = planning horizon

t = acquisition date (endogenous)

() ROSCAs September 2007 5 / 24

Problem faced by individual outside ROSCAConstrained maximization problem:

maxc ,t

tc + (T � t) (y + θ)

subject to

c � c

t(y � c) � B

Constrained maximum is where c = c and

t� =B

y � cUtility of agent is

UA =�

By � c

�c + (T � B

y � c ) (y + θ)

() ROSCAs September 2007 6 / 24

c

t

c

SavingsConstraint

() ROSCAs September 2007 7 / 24

c

t

c

SavingsConstraint

IncreasingUtility

() ROSCAs September 2007 8 / 24

c

t

c

SavingsConstraint

t*

ConstrainedMaximum

() ROSCAs September 2007 9 / 24

Problem faced by ROSCA participant

Let n = number of periods that cycle lasts

If agent ends up being the ith receiver of the pot, her utility is

ui = ic + (n� i)(c + θ) + (T � n)(y + θ)

= nc + θ(n� i) + (T � n)(y + θ)

Her (ex ante) expected utility of joining the ROSCA is then

UR =1n

n

∑i=1ui

= nc + θ

�n� n+ 1

2

�+ (T � n)(y + θ)

() ROSCAs September 2007 10 / 24

Optimal design of ROSCA so that

c = c

and

n� =B

y � cand so

UR =

�B

y � c

�c + (T � B

y � c ) (y + θ) + θ

�n� � n

� + 12

�= UA + θ

�n� � n

� + 12

�Example illustrates the "early pot motive":

,! even though saving pattern is unchanged, ROSCA participation giveseach member the chance of receiving pot early

() ROSCAs September 2007 11 / 24

Enforcement

What stops a member who has received the pot early from reneging?

,! Kenya: place "least trustworthy" at end of cycle ) requires ex antescreening

,! ban past absconders

,! social sanctions

Lack of alternative ways of saving keeps ROSCAs intact

,! most common response when asked why join

,! key feature of ROSCAs: do not require a place to store money

e.g. Anderson and Baland (2003)

() ROSCAs September 2007 12 / 24

Limits of ROSCAs

In�exible pot size

,! adding members ) hard to manage

Do not introduce new funds into system from outside

,! "bidding ROSCAs": pot goes to member that bids the most

,! but problematic "bidding wars" during downturns

() ROSCAs September 2007 13 / 24

Credit Cooperatives

Modi�cation of ROSCA that allows some participants to mainly saveand others to mainly borrow

Old idea going back to 1850s rural Germany (Friedrich Rai¤eissen)

,! by 1910, there were 15,000 institution serving 2.5 million people (9%of German banking market)

Spread to Madras and Bengal (India) in the 1890s. By 1946membership exceeded 9 million

() ROSCAs September 2007 14 / 24

Key features

Credit cooperatives di¤er from ROSCAs in several ways:

,! members do not have to wait their turn to borrow

,! participants (savers and borrowers) are all shareholders

,! key decisions (interest rates, loan size) determined democratically

In the Rai¤eisen model (Prinz, 2000):

,! members were from same local parish

,! unlimited liability: defaulters lose all current assets

,! low income borrowers could not be discriminated against

,! cooperative performed other functions (e.g. purchasing of inputs)

,! extended short and long term loans

() ROSCAs September 2007 15 / 24

Credit Cooperatives as a Vehicle for Saving

Saver-borrowers each with initial wealth w

Two ways of saving:(1) inside the cooperative yields gross interest θ(2) another commercial bank in the city yields θ � δ

Each member has access to a project with unit cost and

output =�y with probability e0 with probability 1� e

where ε < e < 1 and cost of e¤ort = Ce

,! assume that θε < θ � δ

In case of failure borrowers loses wealth invested in cooperative, plusa non-monetary sanction

Gross interest rate on loans = r

Timing: (1) borrowers decide how much to invest, and (2) giveninvestment, how much e¤ort to provide

() ROSCAs September 2007 16 / 24

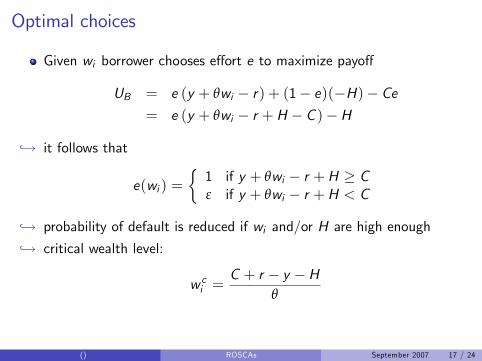

Optimal choices

Given wi borrower chooses e¤ort e to maximize payo¤

UB = e (y + θwi � r) + (1� e)(�H)� Ce= e (y + θwi � r +H � C )�H

,! it follows that

e(wi ) =�1 if y + θwi � r +H � Cε if y + θwi � r +H < C

,! probability of default is reduced if wi and/or H are high enough

,! critical wealth level:

w ci =C + r � y �H

θ

() ROSCAs September 2007 17 / 24

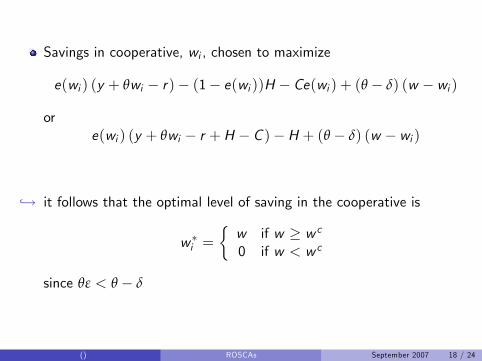

Savings in cooperative, wi , chosen to maximize

e(wi ) (y + θwi � r)� (1� e(wi ))H � Ce(wi ) + (θ � δ) (w � wi )

ore(wi ) (y + θwi � r +H � C )�H + (θ � δ) (w � wi )

,! it follows that the optimal level of saving in the cooperative is

w �i =�w if w � w c0 if w < w c

since θε < θ � δ

() ROSCAs September 2007 18 / 24

Implications

Investing in the cooperative acts as a "commitment device" for theborrower

,! induces the borrower to minimize default probability and takeadvantage of higher (risk-adjusted) return on savings

high social sanctions,H, and su¢ ciently high relative return δ allowcooperative to mobilize savings

higher return may also increase overall savings, w

() ROSCAs September 2007 19 / 24

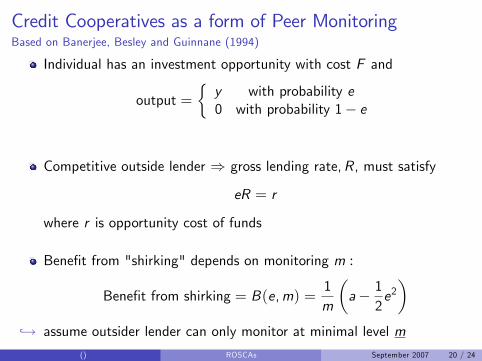

Credit Cooperatives as a form of Peer MonitoringBased on Banerjee, Besley and Guinnane (1994)

Individual has an investment opportunity with cost F and

output =�y with probability e0 with probability 1� e

Competitive outside lender ) gross lending rate,R, must satisfy

eR = r

where r is opportunity cost of funds

Bene�t from "shirking" depends on monitoring m :

Bene�t from shirking = B(e,m) =1m

�a� 1

2e2�

,! assume outsider lender can only monitor at minimal level m

() ROSCAs September 2007 20 / 24

Borrower chooses e to maximize

UB = e(y � RF ) +1m

�a� 1

2e2�

,! yields (constrained) optimal e¤ort

e = m(y � RF )

() ROSCAs September 2007 21 / 24

Simple (2 member) Credit Cooperative

Now suppose borrower forms a cooperative with another individual

This "insider" plays three roles:

,! partial lender, provides F � b,! guarantor: promises w � rb to outside lender in case of default

) lender faces no risk and can o¤er rate r

,! monitor: can optimally adjust monitoring, m, subject to cost C (m)

Why would the insider do this?

,! must receive a big enough share of pro�ts, α

() ROSCAs September 2007 22 / 24

Optimal choice of e¤ort by borrower is now

e�(m) = m(1� α)(y � rb) (IC)

If cost of monitoring isC (m) =

c2m2

,! insiders payo¤ is

UI = e�(m)α(y � rb)� (1� e�(m))w � C (m)� r(F � b)= m(1� α)(y � rb) [α(y � rb) + w ]� c

2m2 � w � r(F � b)

) optimal monitoring level

m�(α,w) =1c(1� α)(y � rb) [α(y � rb) + w ]

() ROSCAs September 2007 23 / 24

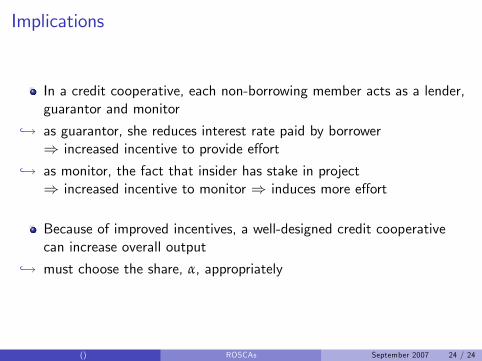

Implications

In a credit cooperative, each non-borrowing member acts as a lender,guarantor and monitor

,! as guarantor, she reduces interest rate paid by borrower) increased incentive to provide e¤ort

,! as monitor, the fact that insider has stake in project) increased incentive to monitor ) induces more e¤ort

Because of improved incentives, a well-designed credit cooperativecan increase overall output

,! must choose the share, α, appropriately

() ROSCAs September 2007 24 / 24