romanian statistical review … · 6 romanian statistical review nr. 2 / 2017 some authors argue...

TRANSCRIPT

PANEL DATA ANALYSIS APPLIED IN FINANCIAL PERFORMANCE ASSESSMENT 3Elisabeta JABA, Professor Emeritus, PhD, Alexandru Ioan Cuza University of Iasi, RomaniaIoan-Bogdan ROBU, Lecturer, PhD, Alexandru Ioan Cuza University of Iasi, RomaniaChristiana Brigitte BALAN, Associate Professor, PhD, Alexandru Ioan Cuza University of Iasi, Romania

THE LINK BETWEEN SOCIAL INEQUALITIES, HEALTH’ SYSTEM CHARACTERISTICS AND R&D EXPENDITURE- WORLDWIDE EVIDENCE 21Celia Dana BESCIU PhD. Candidate, Bucharest University of Economic StudiesArmenia ANDRONICEANU PhD. Bucharest University of Economic Studies

RE-TESTING FOR FINANCIAL INTEGRATION OF THE TURKISH STOCK MARKET AND THE US STOCK MARKET: AN EVIDENCE FROM CO-INTEGRATION AND ERROR CORRECTION MODELS 43Turgut TURSOYNear East University, Department of Banking and Finance, Nicosia, North CyprusFaisal FAISALNear East University, Department of Banking and Finance, Nicosia, North Cyprus

MAIN DEVELOPMENTS AND PERSPECTIVES OF THE EUROPEAN UNION 57Prof. Constantin ANGHELACHE PhD Bucharest University of Economic Studies / „Artifex” University of BucharestAssoc. prof. Mădălina-Gabriela ANGHEL PhD „Artifex” University of Bucharest Assoc. prof. Mirela PANAIT PhD Petroleum-Gas University of Ploiesti

BANDWIDTH SELECTION PROBLEM FOR NONPARAMETRIC REGRESSION MODEL WITH RIGHT-CENSORED DATA 81Dursun AYDINErsin YILMAZMugla Sitki Kocman University, Turkey

Romanian Statistical Review nr. 2 / 2017

CONTENTS 2/2017

ROMANIAN STATISTICAL REVIEW www.revistadestatistica.ro

Romanian Statistical Review nr. 2 / 20172

Romanian Statistical Review nr. 2 / 2017 3

Panel data analysis applied in fi nancial performance assessmentElisabeta JABA, Professor Emeritus, PhD, [email protected] Ioan Cuza University of Iasi, Romania

Ioan-Bogdan ROBU, Lecturer, PhD, [email protected] Ioan Cuza University of Iasi, Romania

Christiana Brigitte BALAN, Associate Professor, PhD, [email protected] Ioan Cuza University of Iasi, Romania

ABSTRACT This paper aims to present the use of panel data analysis in order to assess the state and dynamics of fi nancial performance of the companies listed on the Bucha-rest Stock Exchange under the infl uence of determinant factors. Financial performance may be assessed by means of return on equity – ROE. Its main determinant factors suggested by literature are return on assets - ROA and own or fi nancial leverage (FL). This paper provides a theoretical background and applied panel data analysis of two case studies that use fi xed and random-effects models (investigating the infl uence of ROE of previous period on ROE for the current period). The selection of one of the two types of models is based on the results obtained by applying the Hausman test. The study includes Romanian companies listed on Bucharest Stock Exchange (BSE) during 2006-2015 and uses balanced samples. The authors used SAS 9.2 for data processing. Keywords: panel data analysis, fi nancial performance, return on equity, re-turn on assets, fi nancial leverage JEL Classifi cation: C23, C58, G31, M41

INTRODUCTION

Repeated recording of the same population requires a cross-sectional analysis of the infl uence of factor variables on resultative variables. The development of econometric modeling techniques, advanced statistical methods and computer applications of data processing contributed to the appearance of panel data analysis.

Romanian Statistical Review nr. 2 / 20174

First applications of this type of data are mainly found in longitudinal studies of sociological problems (Lazarsfeld, 1948). The increase of interest for studying events at the macroeconomic level and high availability of data for specifi c samples have signifi cantly contributed to further use of panel data analysis in the research of macroeconomic indicators dynamics (Gujarati, 2004). In microeconomics, main lines of research investigated features and behavior of companies, labor force and consumers (Sevestre, 2002). The use of this type of data has been recently noted in accounting (Jager, 2008; Jaba et al., 2013; Jaba et al., 2016a). Seen as a business project that occurs over time and is subject to multiple risks (de La Bruslerie, 2006), the company and the analysis of its performance are extremely important to its shareholders. Shareholders ground their decisions to put the available funds into company’s assets on performance criteria (Penman, 2007). Assessment of company performance based on the degree of shareholders’ equity refl ects the return on equity (Fabozzi and Peterson, 2003). The return on shareholders’ equity, namely, the total own equity may be assesed using a performance indicator known in literature under the name of return on equity (ROE) (Bragg, 2002). Return on equity may vary from one company to another (during the same period) depending on a set of features specifi c to fi nancial leverage or effi ciency of capital goods (de La Bruslerie, 2006). Additionally, return on equity may vary from one period to another (for the same company) depending on the economic context in which the company operates (Jaba et al., 2016a). The occurrence of such differences between companies or fi nancial periods requires the use of panel data analysis to assess over time the effects of determinant factors on return on equity. In this chapter, we aim to provide a theoretical presentation of panel data analysis in the fi eld of fi nance and accounting and its practical use in the assessment of the infl uence of determinant factors on return on equity. The applicative part includes two case studies of Romanian companies listed on Bucharest Stock Exchange during 2006-2015. In the analysis of panel data, the selection the two types of models is based on the results obtained after applying the Hausman test. Data were processes using SAS 9.2. In the case studies, main results obtained by applying panel data analysis measuring the infl uence of determinant factors on return on equity aim to produce the descriptive statistics of the analyzed variables, values of the Hausman test and choose one of the two suggested models (fi xed effects or random effects, estimate parameters of regression models (in case of fi xed- effects models, the estimation of fi xed effects of time and between companies). The results suggest that economic performance of companies listed on Bucharest Stock Exchange expressed as return on equity varies both between

Romanian Statistical Review nr. 2 / 2017 5

companies and from one fi nancial period to another depending on return on assets and on own and fi nancial leverage.(FL).

1. THE PRINCIPLES OF PANEL DATA ANALYSIS

In specialized literature, panel data also appear under the name of pooled data or longitudinal data (Gujarati, 2004). A panel dataset is a set of cross-section data Ynt (n = 1,...,N and t = 1,...,T) obtained by means of statistical observation performed periodically in a defi ned time interval T of variables characteristic for a group of N individuals (Baltagi, 2005). Panel dataset involves a variability of observations for the same individuals over time leading to recording of N·T observations (Guiso et al., 2002). From the perspective of this representation, statistical observation shows a variation of individual features contributing to the increase of variability of observations and accuracy of estimation (Sevestre, 2002).

1.1. Features of panel data analysis Panel data is the outcome of a successive recording of the same individuals in a selected sample for a specifi c period of time. Even if in the observed sample the criterion for random selection may be very restrictive, eventual correlations may be made among indicators describing individuals over time. By the size of the sample, panel data may be: balanced (individuals are observed over equal periods of time) or unbalanced (individuals are observed over different periods of time). By the selection method of individuals, panel data set may be classifi ed into: continuous (individuals selected in the sample remain unchanged during recording observations) or rotative (a series of individuals are observed during a number of specifi ed periods, then these may be eliminated from the sample being replaced by other individuals for whom new observations will be recorded) In what regards the structure of analyzed data, panel data analysis will consider for N indiiduals, K variables for T different moments. For statistical observation, we may identify three perspectives for panel data analysis: individual n, time t and variable Y. Based on these notations, Ynt is the observed variable Y for individual n at moment t (Sevestre, 2002). If individuals remain constant, chronological series are obtained and if the period is constant, there will be a sequential series of individuals included in the sample. Depending on the purpose of analysis, panel data set may have more than two dimensions (temporal and individual) by including other factors that will be used to structure the analyzed sample (N individuals over T period for C groups).

Romanian Statistical Review nr. 2 / 20176

Some authors argue that in order to make recordings of the panel type, the time variation is not a key criterion if the variation of recorded observations may be explained by at least one dimension (N individuals observed by C criteria) (Guiso et al., 2002). As shown above, panel data set is characterized by double dimensional representation, temporal and transverse, conferring them a signifi cant advantage compared to other types of data (Sevestre, 2002). Temporal dimension enables us to observe individual’s evolution over time depending on studied variables. This dimension determines statistical recording of data of each observed statistical unit as time series. For this dimension, the breakdown of total variability in each recorded observation should mainly consider the number periods used in the study. For this case, total variance may be broken down as follows (Sevestre, 2002): Total variance = Intertemporal variance + Intratemporal variance, or

(1)

Transversal dimension (individual) allows to observe the variance of features from one individual to another irrespective of period of time t for which observations have been recorded and total variance may be decomposed, as follows (Sevestre, 2002): Total variance = Inter-individual variance + Intra-individual variance, or

(2)

By active combining of the two dimensions, total variance of recorded observations may be decomposed, as follows (Sevestre, 2002): Total variance = Inter-individual variance + Inter-temporal variance + Intra-individual-temporal variance, or

(3)

Main difference between the last breakdown and the fi rst two lies in simultaneous consideration of intra-temporal and intra-individual differences. The breakdown method of total variance as in the last model is the main advantage of studying individuals’ behavior from the perspective of the individual and the temporal dimensions (Jaba et al., 2013).

Romanian Statistical Review nr. 2 / 2017 7

1.2. Models of panel data analysis To analyze panel data, we start from a series of data recorded for N individuals observed for a T period of time. For these data, the following general model may be written used for the analysis of a resultative variable (Y) by determinant factors (Xk):

(4)

n = 1,...,N and t = 1,...,T, where ynt represents values of dependent variable, xknt, values K for dependant variable, b0nt, a constant and wnt, the error component (Sevestre, 2005). Coeffi cients b0nt and bknt, k = 1,...,K varies in time and between individuals. As the behavior of individuals may change in time that regards dependent variables of the studied sample, we may observe in the studied sample the absence of recorded data homogeneity. As the number of coeffi cients (NT(K + 1)) is higher to the total number of observations (NT), it is diffi cult to estimate the model using traditional methods. In this case, contrasts between coeffi cients should be used by defi ning two canonic models: fi xed effects models (individual or temporal) and composed error models (random effects)

Fixed effects models In case of fi xed effects models, it is assumed that the infl uence of considered factor variables (xknt) on the dependent variable (ynt) is identical for all individuals during the entire analyzed period (bknt = bk). In this case, the constant b0nt may be broken down as follows:

(5)

where, b0nt is the constant of the regression model, b0, a constant an indicates unobservable differences between individuals and dt temporal differences that may appear in individuals. Based on this breakdown, the regression model may be written as follows (Sevestre, 2002):

(6)

To estimate parameters of the fi xed effects model we may consider the individual and temporal specifi city by introducing specifi c effects also called fi xed effects in individuals and periods that represent coeffi cients to be

Romanian Statistical Review nr. 2 / 20178

estimated. In case of a model for a specifi c period, two companies that have the same observable features should have the same values for the resultative variables:

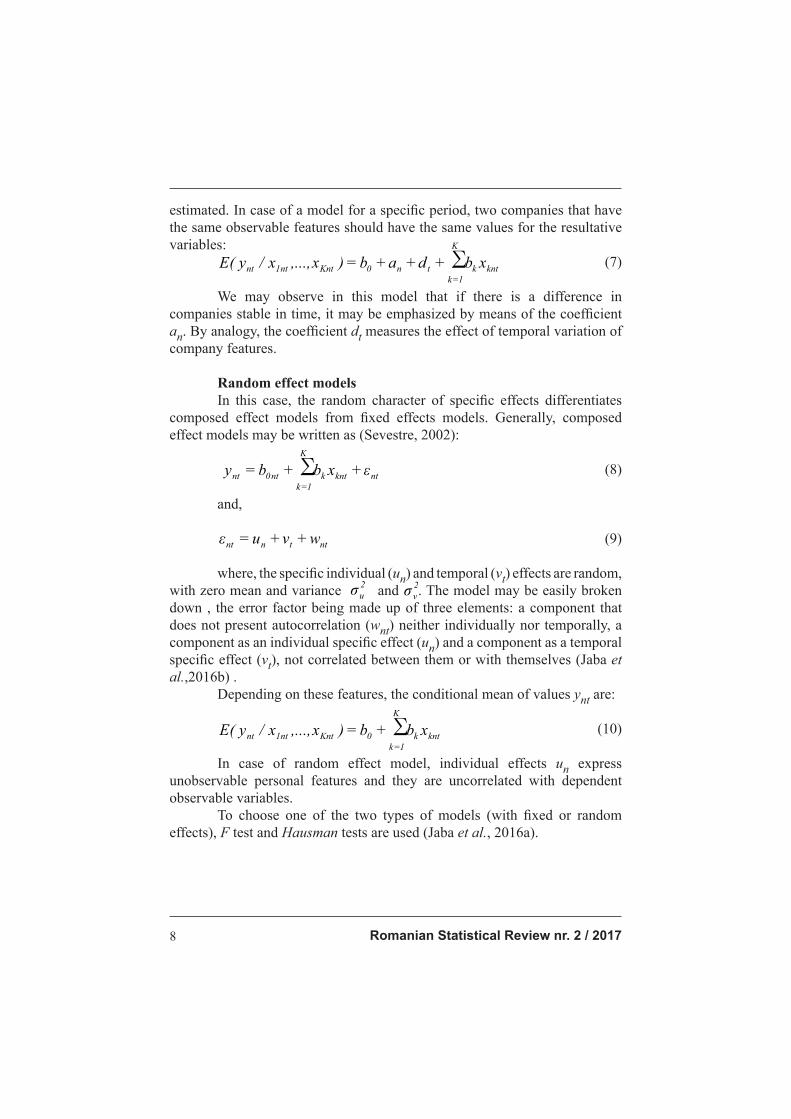

(7)

We may observe in this model that if there is a difference in companies stable in time, it may be emphasized by means of the coeffi cient an. By analogy, the coeffi cient dt measures the effect of temporal variation of company features.

Random effect models In this case, the random character of specifi c effects differentiates composed effect models from fi xed effects models. Generally, composed effect models may be written as (Sevestre, 2002):

(8) and,

(9)

where, the specifi c individual (un) and temporal (vt) effects are random, with zero mean and variance and . The model may be easily broken down , the error factor being made up of three elements: a component that does not present autocorrelation (wnt) neither individually nor temporally, a component as an individual specifi c effect (un) and a component as a temporal specifi c effect (vt), not correlated between them or with themselves (Jaba et al.,2016b) . Depending on these features, the conditional mean of values ynt are:

(10)

In case of random effect model, individual effects un express unobservable personal features and they are uncorrelated with dependent observable variables. To choose one of the two types of models (with fi xed or random effects), F test and Hausman tests are used (Jaba et al., 2016a).

Romanian Statistical Review nr. 2 / 2017 9

1.3. Advantages and limitations of panel data analysis use The use of panel data brings some advantages (Baltagi, 2005): control over individual heterogeneity as panel data are mainly oriented towards individuals observed over time; combining time series with cross-section observations enables panel data to provide additional information about them, limit collinearity of selected variables, to provide more degrees of freedom by independent values that may vary even more the effi ciency in analysis; panel data are more indicated in the study of adjustment and variation dynamics; panel data enable to identify and measure the effects that cannot be identifi ed by simple use of cross-section analysis or time series; using panel data complex models associated to reality may be built and tested more easily, unlike the use of cross-section data or time series, panel data enable the reduction or elimination of diffi culties related to data aggregation (biais). Also, using panel data analysis contributes to improved accuracy in estimating regression models parameters, better analysis of an event by including individual and time dimensions into the model, simplifi ed statistical inference process (compliance with classical hypotheses of regression analysis not being needed) (Hsiao, 2003). In case of panel data, their analysis may be limited by a series of factors related to data selection and collection, distortion measurement errors, sample selection, time series for short periods, cross-sectional dependence of factors (Baltagi, 2005). Building and collecting panel-type data attracts with it a set of problems typical for sampling: representativeness, non-responses, inexact responses or outliers, frequency of data collection, set reference period (Baltagi, 2005). Distortion measurement errors are another limitation of panel data use. It appears if there are erroneous recordings of responses needed to build a data base (Sevestre, 2002). In terms of problems generated by the selection of individuals included in the sample, there are some limitations caused by the censorship of some individuals leading to related data, appearance of non-responses, the omission of individuals associated data, decrease of the ability to record data for consecutive periods (Baltagi, 2005). In most cases, panel data regarding macroeconomics cover short periods of time recorded for each individual and do not allow to make long-term forecasts (Baltagi, 2005). Another problem occurs when panel data are used for long time series to analyze macroeconomic events. In this case, the use of panel data does not consider eventual cross-sectional dependencies that may appear among factors (Baltagi, 2005).

Romanian Statistical Review nr. 2 / 201710

2. ANALYSIS OF THE COMPANY PERFORMANCE BASED ON RETURN ON EQUITY (ROE)

Understanding the economic performance of a company and assessment of its ability to continue its operation are important for its main suppliers of capital, namely, for its current shareholders, potential investors and creditors (Robu et al., 2012). For this purpose, the fi rst and second categories of stakeholders are interested in obtaining benefi ts as dividends in exchange for equity made available to the company (Penman, 2007). Measurement of equity provided by the shareholders and their analysis of company performance is made by means of return on equity (ROE). ROE is calculated as a ratio between net income (after paying fees and taxes to the state) and own equity (EQ; and EQ = TA – L ; where TA = Total assets, and L = Total debt). The use of net income in the calculation of return on equity is justifi ed as it is used as a basis for paying dividends to shareholders proportional to the amount of equity made available to the company (Bragg, 2002). For the company, net income is obtained by adding the operating income and fi nancial income. The operational or main activity is used to obtain operating income as a difference between operating revenue and expenses. Operating income is based on company’s assets used to obtain future economic benefi ts. Therefore, the effi ciency of using company’s assets may be assessed by means of return on assets (ROA) calculated as a ratio between operating income and operating assets (Fabozzi and Peterson, 2003). Financial income is a difference between revenue and fi nancial expenses (not related to operational activity). Financial revenue is usually the interest receivable or favorable foreign exchange differences related to assets or debts of the company (de La Bruslerie, 2006). Financial expenses are usually interest payable for borrowed equity from creditors to fi nance operations and favorable foreign exchange differences related to monetary and non-monetary assets of the company (de La Bruslerie, 2006). The calculation of net income if the company uses external funding (for example, medium and long term bank loans for which annually an interest D will be paid, calculated as a percentage d% of the amount of loans) and the tax rate is p% (from gross income), may be made as follows (Penman, 2007): NI = IBT – Tx (11)where: IBT = OI + NOI (12) Tx = p% · IBT (13) OI = OR – OE (14)

Romanian Statistical Review nr. 2 / 2017 11

NOI = NOR – NOE (15)where, NI = Net income; IBT = Income before taxes; Tx = Taxes; OI = Operating income; OR = Operating revenues; OE = operating expenses; NOI = Non-operating income; NOR = Non-operating revenues; NOE = Non-operating expenses. Starting from the equation (11) and considering hypothetically that the company records in its fi nancial operation only expenses and no revenue (NOR = 0) and the tax rate is p is 0%, Net income is calculated as follows (Penman, 2007): NI = OI – NOE (16) where, NOE = Interest expenses = D = d% · Debts (17) Calculated this way, NI is used to calculate the return on equity: ROE = (NI / EQ) · 100 (18) i.e. ROE = (NI / EQ) · 100 = [(OI – D)/EQ] · 100 (19) By breaking down the equation (3.9), we get: ROE = (OI/EQ – D/EQ) · 100 (20) The (20) equation is multiplied by (TA/TA) and is written as: ROE = [(OI/EQ) · (TA/TA) – (D/EQ) · (TA/TA)] · 100 (21)or ROE = [(OI/TA) · (TA/EQ) – (D/EQ) · (TA/TA)] · 100 (22) Also, the (22) equation is multiplied by (L/L), and written as: ROE = [(OI/TA) · (TA/EQ) · (L/L) – (D/EQ) · (TA/TA) · (L/L)] · 100 (23)or: ROE = [(OI/TA) · (EQ + L)/EQ) – (D/L) · (L/EQ)] · 100 (24)but ROA = OI/TA (25)and, FL = L/EQ (26) Where, FL is an indicator of fi nancial structure and indicates company’s degree of external fi nancing (FL > 1) or own funds (FL < 1). Starting from the equations (25) and (26), the equation (24) may be rewritten as follows: ROE = [ROA · (1 + FL) – d · FL] · 100 (27)i.e. ROE = (ROA + ROA · FL – d · FL) · 100 (28)or ROE = [ROA + (ROA – d) · FL] · 100 (29)

Romanian Statistical Review nr. 2 / 201712

If p > 0%, ROE = [ROA + (ROA– d) · FL · (1-p)] · 100 (30) Based on equations (29) and (30), if d and p are not known, ROE is a function of ROA and FL, thus: ROE = f (ROA; FL), the return on equity depends both on operational return and the fi nancial leverage (FL) having a direct impact on the cost of borrowed equity (d).

3. CASE STUDIES ON THE USE OF PANEL DATA ANALYSIS

Financial performance of a company may be assessed using ROE. This indicator is used to assess the degree to which the equity made available by shareholders (total own equity) may be remunerated based on net income of the company as the main source for dividend payment (Penman, 2007). Return on equity may vary in time (depending on the business context in which the company operates) and also from one company to another (depending on operational and fi nancial policies used by the management) (Jaba et al., 2016a). For simultaneous analysis of ROE variations between companies and over time under the infl uence of determinant factors (ROA and FL), panel data analysis should be used. Using this type of analysis, we may assess the variation of return on equity (ROE) over time and the signifi cant differences that may exist among companies.

3.1. Results and discussions about the use of fi xed effects models In case of panel analysis of ROE variation under the infl uence of determinant factors, the study suggests the following fi xed effects model: ROE = β0 + αn + δt + β1ROA + β2FL + εnt (31) where, β0 is a constant, β1 and β2 are regression model parameters, αn are cross-sectional fi xed effects (inter-individual), δt are temporal fi xed effects and εnt is the error random variable. The target population aimed by the study includes all companies listed on BSE on the regulated market between 2006 and 2015, where 85 companies had been listed on BSE under the regulated market section by the end of 2015. A balanced sample of 58 companies was extracted from this population. Data were collected from Thomson Financial database by means of Datastream Advanced 4.0 using the source code assigned to each variable included in the model: [WC08301] for ROE; [WC01250]/ [WC02999] for ROA and [WC08231] for FL. Descriptive statistics for each analyzed variable of the selected sample are shown in Table 1.

Romanian Statistical Review nr. 2 / 2017 13

Descriptive statisticsTable 1

Variable Mean Median Std DeviationROE 0.032 0.040 0.099ROA 0.036 0.033 0.057FL 0.787 0.471 0.795

The results from Table 1 show in the means of companies listed on BSE we may see reduces values of ROE, 3.2% that indicates a low return on equity (for 100 units invested by shareholders, they will receive 3.2 units as dividends) Even though ROA is positive (3.6%), low value of ROE may be explained by the fact that the obtained operating income does not cover the cost of indebtedness. High degree of indebtedness of companies listed on BSE, (FL = 0.787) also brings a high cost of borrowed equity expressed by interest payable that have a direct impact on net income in the sense of its diminishing. For the analyzed sample, the source code in SAS 9.2 used to perform the panel data analysis in case of fi xed effects models is as follows:

PROC TSCSREG DATA = WORK.DATABASE; MODEL ROE= ROA FL /

FIXTWO ; ID Firm Year ;

RUN; QUIT;

Main results obtained in SAS 9.2 refer to a set of statistics related to the estimated model (Table 2), test the fi xed effects model using F test (Table 3), test the model using the Hausman test (Table 4.4) and estimate fi xed effects model (Table A.1 from Appendix).

Fit statistics for the model with fi xed effects (cross and time fi xed effects)Table 2

Fit StatisticsSSE 1.4560 DFE 510MSE 0.0029 Root MSE 0.0534

R-Square 0.7416 (SSE = Sum of squares due to errors; DFE = degrees of freedom for the

error: the numbers of the observations in the data set minus the numbers of the parameters; MSE = Mean sum of squares due to errors).

Romanian Statistical Review nr. 2 / 201714

Based on the value of R2, it may be noted that 74.16% of ROE variation is explained by the infl uence of ROA and FL in case of cross and time fi xed effects model.

Testing fi xed effects model using F testTable 3

F Test for No Fixed EffectsNum DF Den DF F Value Pr > F

66 510 3.78 <.0001

The value of F test calculated as a ratio between mean of squares due to the model (MST) and mean of squares due to the error is of 3.78. This model indicates that fi xed effects model explains in a signifi cant proportion the variation of ROE under the infl uence of factors.

Testing the fi xed effects model using the Hausman testTable 4

Hausman Test for Random EffectsDF m Value Pr > m2 7.06 0.0294

Table 4 completes Table 3 that shows the result after applying the Hausman test (H0: the model shows the random effects; H1: the model does not show the random effects). Hausman specifi cation test (H) is used for testing the consistency of the estimated parameters; in the case of fi xed effects, on the null hypothesis (H0), the parameters of the model are consistent but ineffi cient, and on the alternative hypothesis (H1) the parameters of the model are consistent and possibly effi cient (Jaba et al., 2016b) . Based on the obtained results, we may state that the estimated model does not show random but only cross and time fi xed effects. For the fi xed effects model, the estimations of the regression model are presented in Table A.1 in the appendix. The table shows that ROA and FL have a signifi cant infl uence on ROE: an increase of 100% of ROA (operational effi ciency) duet o an increase of ROE by 128.13% and an increase of degree of indebtedness by one unit (its doubling) causes a reduction of ROE by 3.64% due to interest payable for borrowed equity and that contribute to the reduction of net income. Also, Table A.1 shows a set of signifi cant cross-sectional and time differences. We may underline that in the analysis, the last company in the sample is set as a reference unit for the estimation of individual differences. Table A.1 shows that there is a set of signifi cant differences related to the level of ROE, between the companies number 58 (reference) and companies

Romanian Statistical Review nr. 2 / 2017 15

under the following numbers: 22, 24, 27, 32 and 41. These companies have higher values of ROE than the value estimated for company 58 (reference) with estimated values of cross differences. In what regards time fi xed effects, we may observe that for a company from the sample, the value of ROE estimated for the third year (2008) of the studied period is lower (by 2,131%) than the ROE estimated for the last year (2015), for which ROE is 1.90% (Intercept). Except year 2008, there are no signifi cant differences of ROE of the calculated value in the studied sample during 2006-2015. 3.2. Results and discussions on the use of random effects models. In case of panel analysis of ROE variation under the determinant factors, the study suggests the following random effects model:

ROE = β0 +β1ROA + β2FL + un + νt + wnt (32) where, β0 is a constant, β1 and β2 are regression models parameters, un, individual random effects (zero mean and variance ), vt, temporal random effects (zero mean and variance ), wnt is the error component without autocorrelation neither in the individual, nor in the temporal dimensions. The same target population is included in this case study. It contains all Romanian companies listed on BSE, on the regulated market, 85 companies during 2006-2015. In case of random effects model, randomly a reduced number of companies is chosen, the sample includes only 3 companies observed over a period of 10 years. It is important that the 3 companies are representative as they are included in the BET index of BSE. In this case, the source of data is Thomson Financial database, using Datastream Advanced 4.0, using the source code assigned to each variable included in the model: [WC08301] for ROE; [WC01250]/ [WC02999] for ROA and [WC08231] for FL. Descriptive statistics for the analyzed variables of the selected sample are shown in Table 5.

Descriptive statisticsTable 5

Variable Mean Median Std DeviationROE 0.119 0.120 0.044ROA 0.098 0.103 0.035FL 0.332 0.339 0.217

The results of Table 5 show that in the means of companies listed on BSE and that are included in the calculation of the BET index we may note positive ROE, of 11.9% indicating a high degree of return on equity (for

Romanian Statistical Review nr. 2 / 201716

100 units invested by shareholders, they will get 11.9 units as dividends). Compared to ROE, ROA is positive (9.8%) but lower: for 100 units of assets used in operation, the resulting benefi ts are of 9.8 units. The degree of indebtedness is reduced (FL = 0,332) for companies listed on BSE included in the calculation of ET causing a low cost of borrowed equity. For the studied sample, the source code in SAS 9.2 used in the panel data analysis, in case of random effects models, is as follows:

PROC TSCSREG DATA = WORK.DATABASE; MODEL ROE= ROA FL /

PARKS RHO RANTWO ; ID Firm Year ;

RUN; QUIT;

Main results obtained in SAS 9.2 include a set of statistics related to the estimated model (Table 6), a breakdown of the total variance (Table 7), model testing using the Hausman test (Table 8), estimation of the random effects model (Table 9) and the estimation of parameters related to individual random effects (Table 10).

Fit statistics for the model with random effectsTable 6

Fit StatisticsSSE 20.4569 DFE 27MSE 0.7577 Root MSE 0.8704

R-Square 0.8648 (SSE = Sum of squares due to errors; DFE = degrees of freedom for the

error: the numbers of the observations in the data set minus the numbers of the parameters; MSE = Mean sum of squares due to errors).

Based on the value of R2, we may note that 86.48% of ROE variance is explained by the infl uence of ROA and FL in case of random effects models.

Romanian Statistical Review nr. 2 / 2017 17

Table 7. Total variance breakdownVariance Component Estimates

Variance Component for Cross Sections 0.000106Variance Component for Time Series 0

Variance Component for Error 0.00029

Results shown in Table 7 indicates the presence of individual random effects (associated variance > 0), as well as the absence of temporal random effects (associated variance = 0).

Testing random effects model using the Hausman testTable 8

Hausman Test for Random EffectsDF m Value Pr > m2 2.27 0.3213

The results obtained by applying the Hausman test (H0: the model shows random effects; H1: the model does not show random effects) indicates that the estimated model shows random effects

Parameter estimates for the random effects modelTable 9

Parameter EstimatesVariable DF Estimate Standard Error t Value Pr > |t|

Intercept 1 -0.01914 0.0138 -1.38 0.1776ROA 1 1.118663 0.1136 9.84 <.0001FL 1 0.095449 0.0165 5.78 <.0001

Based on the results shown in Table 9, we may observe that ROA and FL have a signifi cant infl uence on ROE: an increase by 100% of ROA (operational effi ciency) produces an increase of ROE by 111.86% and an increase of the degree of indebtedness by one unit (it doubling) causes an increase of ROE by 9.54%. This may be mainly explained in case of high-performance companies that generate profi t from operations that may be used to cover the cost of borrowed equity, enough profi t remaining to be distributed to shareholders. Also, a high degree of indebtedness refl ecting borrowed funds that are invested to obtain future business benefi ts (profi table investments) signifi cantly contribute to the increase of return on equity.

Romanian Statistical Review nr. 2 / 201718

Table 10. Estimations of parameters related to individual random effectsFirst Order Autoregressive Parameter Estimates

Firm RhoFirm 1 (OMV PETROM S.A.) 0.285824

Firm 2 (S.N.G.N. ROMGAZ S.A.) 0.506226Firm 3 (SNTGN TRANSGAZ SA MEDIAS) 0.051735

Table 10 s shows the parameters of individual random effects for the 3 companies included in the sample. Based on this, we may state that for each company, ROE increases from one period to another with an estimated value Rho (ex: on the average, fi rst company ROE increases year by year by 28.58%, second company ROE by 50.62% and third company ROE by 5.17%).

CONCLUSIONS

Economic performance of a company assessed by means of return on equity may vary from one company to another (over the same fi scal year) depending on a set of features specifi c to the use of capital goods and fi nancial leverage and from one period to another (for the same company) based on the context in which the company operates. The analysis and estimation of such differences among companies and fi scal years may be made using panel data analysis to assess over time the effects of the determinant factors on return on equity. This chapter presented main theoretical and methodological aspects related to the panel data analysis and fi xed and random effects models, main concepts of economic performance, methods of their assessment using ROE and the infl uence of main determinant factors and the fi nal part included two case studies in SAS 9.2 of panel analysis of ROE under the infl uence of ROA and FL by applying the two types of suggested models. Main results obtained by applying the panel data analysis investigating the infl uence of determinant factors on return on equity include: descriptive statistics of studied variables, values of the Hausman test and choosing one of the models (fi xed or random effects), estimating the parameters of regression models ( and in case of fi xed and random effects models, their estimation). Based on the obtained results, we may note that fi nancial performance of listed companies varies among companies and in dynamics from one fi scal year to another depending on the return on assets (ROA) and own or foreign fi nancial leverage (FL). Methodologically, panel analysis of return on equity may be used to assess company performance both in terms of structure and in dynamics.

Romanian Statistical Review nr. 2 / 2017 19

REFERENCES 1. Baltagi, B., 2005, Econometric Analysis of Panel Data, 3rd ed., John Wiley & Sons,

West Sussex 2. Bragg, S.M., (2002), Business ratios and formulas: a comprehensive guide, John Wiley

& Sons, New Jersey 3. de Jager, P., (2008), ”Panel data techniques and accounting research”, Meditari

Accountancy Research, 16(2), pp. 53 – 68 4. de La Bruslerie, H., (2010), Analyse fi nancière, diagnostic et évaluation, Dunod, Paris 5. Fabozzi, F., Peterson, P., (2003), Financial management and analysis, 2nd ed., John

Wiley & Sons, New Jersey 6. Gujarati, D., (2004), Basic Econometrics, 4th ed., McGraw-Hill, New York 7. Hsiao, C., (2003), Analysis of panel data, 2nd ed., Cambridge University Press,

Cambridge 8. Jaba, E., Mironiuc, M., Roman, M., Robu, I.B., Robu, M.A., 2013, “The Statistical

Assessment of an Emerging Capital Market Using the Panel Data Analysis of the Financial Information”, Economic Computation and Economic Cybernetics Studies and Research, 47(2), pp. 21-36

9. Jaba, E., Robu, I.B., Istrate, C., Balan, C.B., Roman, M., 2016a, “Statistical Assessment of the Value Relevance of Financial Information Reported by Romanian Listed Companies”, Romanian Journal of Economic Forecasting, 19(2), pp. 27-42

10. Jaba, E., Chirianu, I.A., Balan, C.B., Robu, I.B., Roman, M., 2016b, “The analysis of the effect of women’s participation in the labor market on fertility in european union countries using welfare state models”, Economic Computation and Economic Cybernetics Studies and Research, 50(1), pp. 69-84

11. Lazarsfeld, H.B., 1948, ”The use of panels in social research”, Proceedings of the American Philisophical Society, 92, pp. 405-410

12. Penman, S.H., 2007, Financial Statement Analysis and Security Valuation, 3rd edition, McGraw Hill

13. Robu, I.B., Balan, C.B., Jaba, E., 2012, “The Estimation of the Going Concern Ability of Quoted Companies, Using Duration Models”, Procedia - Social and Behavioral Sciences, 62, pp. 876-880

14. Sevestre, P., 2002, Économetrie des données de panel, Dunod, Paris

AppendixParameters estimates for the fi xed effects model

Tabel A.1 Parameter Estimates

Variable DF Estimate Standard Error t Value Pr > |t| LabelCS1 1 0.037537 0.0239 1.57 0.1176 Cross Sectional Effect 1CS2 1 -0.008 0.0241 -0.33 0.7400 Cross Sectional Effect 2CS3 1 0.014383 0.0244 0.59 0.5560 Cross Sectional Effect 3CS4 1 0.027985 0.0241 1.16 0.2452 Cross Sectional Effect 4CS5 1 0.011817 0.0245 0.48 0.6302 Cross Sectional Effect 5CS6 1 0.001743 0.0239 0.07 0.9419 Cross Sectional Effect 6CS7 1 -0.00909 0.0260 -0.35 0.7265 Cross Sectional Effect 7CS8 1 0.019953 0.0240 0.83 0.4070 Cross Sectional Effect 8CS9 1 -0.0066 0.0239 -0.28 0.7825 Cross Sectional Effect 9CS10 1 -0.03287 0.0239 -1.37 0.1700 Cross Sectional Effect 10CS11 1 0.015327 0.0243 0.63 0.5283 Cross Sectional Effect 11CS12 1 -0.00789 0.0242 -0.33 0.7445 Cross Sectional Effect 12CS13 1 0.008234 0.0244 0.34 0.7356 Cross Sectional Effect 13CS14 1 0.025827 0.0255 1.01 0.3124 Cross Sectional Effect 14CS15 1 0.012734 0.0244 0.52 0.6021 Cross Sectional Effect 15

Romanian Statistical Review nr. 2 / 201720

Parameter EstimatesVariable DF Estimate Standard Error t Value Pr > |t| LabelCS16 1 0.027802 0.0244 1.14 0.2559 Cross Sectional Effect 16CS17 1 0.013646 0.0241 0.57 0.5712 Cross Sectional Effect 17CS18 1 -0.01355 0.0255 -0.53 0.5954 Cross Sectional Effect 18CS19 1 0.003471 0.0247 0.14 0.8884 Cross Sectional Effect 19CS20 1 0.005969 0.0240 0.25 0.8036 Cross Sectional Effect 20CS21 1 -0.00674 0.0247 -0.27 0.7847 Cross Sectional Effect 21CS22 1 0.053597 0.0252 2.12 0.0341 Cross Sectional Effect 22CS23 1 0.0089 0.0248 0.36 0.7200 Cross Sectional Effect 23CS24 1 0.049292 0.0245 2.01 0.0449 Cross Sectional Effect 24CS25 1 0.022734 0.0241 0.94 0.3453 Cross Sectional Effect 25CS26 1 -0.00396 0.0262 -0.15 0.8802 Cross Sectional Effect 26CS27 1 0.121601 0.0261 4.65 <.0001 Cross Sectional Effect 27CS28 1 -0.01162 0.0248 -0.47 0.6402 Cross Sectional Effect 28CS29 1 -0.01032 0.0245 -0.42 0.6742 Cross Sectional Effect 29CS30 1 -0.02769 0.0240 -1.15 0.2487 Cross Sectional Effect 30CS31 1 -0.00109 0.0243 -0.04 0.9642 Cross Sectional Effect 31CS32 1 0.154169 0.0250 6.17 <.0001 Cross Sectional Effect 32CS33 1 0.024016 0.0239 1.00 0.3158 Cross Sectional Effect 33CS34 1 0.049645 0.0260 1.91 0.0571 Cross Sectional Effect 34CS35 1 0.008588 0.0242 0.36 0.7223 Cross Sectional Effect 35CS36 1 0.032076 0.0242 1.32 0.1858 Cross Sectional Effect 36CS37 1 0.02045 0.0246 0.83 0.4059 Cross Sectional Effect 37CS38 1 0.017362 0.0242 0.72 0.4737 Cross Sectional Effect 38CS39 1 -0.0118 0.0258 -0.46 0.6474 Cross Sectional Effect 39CS40 1 -0.01746 0.0239 -0.73 0.4655 Cross Sectional Effect 40CS41 1 0.15365 0.0259 5.92 <.0001 Cross Sectional Effect 41CS42 1 -0.03606 0.0239 -1.51 0.1325 Cross Sectional Effect 42CS43 1 0.004022 0.0241 0.17 0.8677 Cross Sectional Effect 43CS44 1 0.020563 0.0241 0.85 0.3948 Cross Sectional Effect 44CS45 1 0.005232 0.0243 0.22 0.8298 Cross Sectional Effect 45CS46 1 0.01494 0.0239 0.62 0.5325 Cross Sectional Effect 46CS47 1 -0.00942 0.0240 -0.39 0.6951 Cross Sectional Effect 47CS48 1 0.012479 0.0241 0.52 0.6053 Cross Sectional Effect 48CS49 1 0.018871 0.0241 0.78 0.4340 Cross Sectional Effect 49CS50 1 0.009932 0.0247 0.40 0.6882 Cross Sectional Effect 50CS51 1 -0.02127 0.0250 -0.85 0.3956 Cross Sectional Effect 51CS52 1 -0.00861 0.0241 -0.36 0.7216 Cross Sectional Effect 52CS53 1 -0.00363 0.0243 -0.15 0.8811 Cross Sectional Effect 53CS54 1 0.006331 0.0242 0.26 0.7939 Cross Sectional Effect 54CS55 1 0.003847 0.0243 0.16 0.8744 Cross Sectional Effect 55CS56 1 -0.00714 0.0246 -0.29 0.7713 Cross Sectional Effect 56CS57 1 0.027594 0.0241 1.14 0.2532 Cross Sectional Effect 57TS1 1 0.016132 0.0100 1.61 0.1080 Time Series Effect 1TS2 1 -0.00658 0.00997 -0.66 0.5098 Time Series Effect 2TS3 1 -0.02131 0.00995 -2.14 0.0326 Time Series Effect 3TS4 1 -0.01521 0.00993 -1.53 0.1262 Time Series Effect 4TS5 1 -0.01592 0.00998 -1.60 0.1113 Time Series Effect 5TS6 1 -0.00835 0.00993 -0.84 0.4011 Time Series Effect 6TS7 1 0.002133 0.0101 0.21 0.8321 Time Series Effect 7TS8 1 0.001671 0.0101 0.17 0.8681 Time Series Effect 8TS9 1 -0.00017 0.0100 -0.02 0.9862 Time Series Effect 9Intercept 1 0.005223 0.0190 0.27 0.7836 InterceptROA 1 1.281315 0.0587 21.84 <.0001 FL 1 -0.03638 0.00494 -7.36 <.0001

(Signifi cant values for a level of 0.05)

Romanian Statistical Review nr. 2 / 2017 21

The link between social inequalities, health’ system characteristics and R&D expenditure- worldwide evidence Celia Dana BESCIU ([email protected])PhD. Candidate, Bucharest University of Economic Studies

Armenia ANDRONICEANU ([email protected])PhD. Bucharest University of Economic Studies

ABSTRACT: The aim of this paper is to analyze the link between social inequality, mea-sured by GINI index, health systems characteristics and R&D expenditure and to pro-vide worldwide evidence. An undeveloped health system can have a negative impact on health status, can determine both the decrease of work capacity and earnings and can generate the increase of social inequality level measured by GINI index. This paper analyses and measures the correlation between GINI Index and the number of infant deaths, health work force density, health infrastructure and re-search and development expenditures from GDP The analysis was conducted using data and information from World Bank and World Health Organization. The used sam-ple included all the observations that had available data. Depending on the number of observations that we have, we used panel data model or linear regression models. The results confi rms our assumptions that high levels of GINI Index can be reduced through the increase of health work force density and through a high level of allocation from GDP for research and development expenditure Moreover, GINI index is posi-tively related with the need of health infrastructure and the number of infants deaths. For future research, higher attention should be paid for the causality relations between immigration control, health resources and social inequalities, aspects that could deter-mine macroeconomic imbalances at the world level. Key-words: social equity, health system, GINI Index, infant deaths, health work force density, R&D expenditure JEL Classifi cation:A13, I14, I15, I18, D60

Romanian Statistical Review nr. 2 / 201722

1. INTRODUCTION

The global fi nances crisis impacted the economy at all levels, including the education and health sector. An important role in launching the economy was attributed to IMF (IMF, 2016) as it increased its fi nancial power and agreed with large borrowing agreements. Moreover, the IMF undertook reform policies towards low income countries and increased the resources for concessional lending up to four times. The International Monetary Fund provided policy advices and risk analysis in order to help member countries to deal with the economic crisis. After the crisis, the IMF implemented major initiatives that deal with strengthening and surveillance requirements adapted to a more interlinked world. For emerging countries, the IMF agreed with several government reforms that help them launching the economy, while the underdeveloped countries remained under its infl uence. This behavior is in accordance with IMF’s old policy (starting from 1999) that states that its aimed is to reduce the poverty level and to ensure growing facilities for underdeveloped and developing states (Androniceanu, Ohanyan, 2016). Several studies such as the ones conducted by Bruno, Ravallion and Squire (1998), or Adams (2002) found both that there is a negative relationship between poverty growth and the mean income growth and that there is no statistically signifi cant relationship between economic growth and income inequality. Moreover, Dagdeviren,Van der Hoeven and Weeks (2002) considers that economic growth is not the best way to reduce poverty and that it should be mixed with income redistribution in order to decrease the level of poverty. In the same time, redistribution policy effects depend on the characteristics of the developing country. From a multidimensional approach, the income is a measure though which human capabilities can be achieved, including things like probability of living a healthy and a long life (Sen, 1999). As a consequence, the most important commitments that states have to achieve are the increase of human capital (Jakubowska, 2016) and the release of long term economic growth though the development of both national healthcare system and the educational one (Androniceanu, Ohanyan, 2016). At global level, healthcare poverty and social inequality are one of the biggest concerns that people have. On one hand, the competitiveness between countries is based on improving the quality of human capital (Balcerzak, 2016) by increasing the accessibility to higher education and healthcare systems for all social categories (Androniceanu, 2015b). Thus,the competitiveness between countries looks at ensuring proper living conditions like lower unemployment, higher productivity, real knowledge of income indicators

Romanian Statistical Review nr. 2 / 2017 23

(Bayar, 2016). According to Hayes et. all (1994), there is a bi-directional relationship between labor productivity and poverty, as poverty reduces the ability of people to become more productive, while rising productivity growth is associated with decreasing poverty growth. At European level, the 2020 Strategy is based on fi ghting with poverty and social exclusion. At the end of 2020, the goal is to have with at least 20 million fewer people that are supposed to risk of poverty and social exclusion. According to Androniceanu (2015a), the goals are related with reducing extreme poverty and reducing child mortality. Moreover, at EU-28 level, the risk of poverty increases by 4% for people who have health problems compared with persons that do not have such problems (Jakubowska, 2016). As a consequence, eHealth Action Plan 2012-2020 was implemented and aims to prevent multi-morbidity and to ensure the sustainability of health systems in Europe (Kautsch, 2016). C o n s i d e r i n g these, the aim of this paper is to reveal the link between several factors such as infant deaths, health infrastructure, health work force density and research and development expenditure as a percentage of GDP with GINI index, the measure for social inequality. The research is based on four hypotheses of research H1. Higher value of GINI index is, higher the value of infant deaths is. H2 Higher the value GINI index is, higher the need for health

infrastructure is H3 Higher the health work force density is, lower the value of GINI

Index is H4. Higher the expenditures for R&D are, lower the value of GINI

Index is. The structure of the paper is divided in several sections: the fi rst one looks at the literature review, the second one deals with data collection and the used methodology, the third one presents the results and the discussion of them, while the last one presents the conclusions, reveals the problem of research and provides future research ideas.

2. LITERATURE REVIEW

One of the major problems that the global economy has is dealing with income inequality. The literature in the fi eld reveals that an important factor of income inequality comes with the increase of mortality at all levels, without depending on the level of income per capita (Lynch et al., 1998). According to Kennedy at al (1996), there is a positive relationship between the level of total

Romanian Statistical Review nr. 2 / 201724

mortality and the value of Robin Hood index or the value of GINI index (as a measure of poverty or income inequality). That means that when the index increases, the level of total mortality also increases. Similar conclusions were found by Leiyu Shi et al. (2003). Using a weighted multivariate regression, they reveal that income inequalities, measured by the GINI index and by Robin Hood index, are signifi cantly associated with all-causes of mortality. Moreover, Kawachi et al. (1997) provided evidence that income inequality is correlated with social trust and with group membership that were affected by total mortality rate, including infant mortality. A negative correlation between GINI index and infant mortality only exists in the case children are early registered to certain forms of education (Deaton, 2003) New evidence emphasizes that there is a link between income inequalities, life expectancy and specifi c causes of high mortality. According to Yannan, Frank, Mackenbach, 2015), higher the mortality is, higher the inequality in terms of income is. It can be emphasized that inequality appears especially in areas with high concentration of poverty, in specifi c environments where the quality of living is low and where the level of infant mortality is high (Szwarcwald et al 2002). Consequently, by improving the aspects of the health care system, the negative effects of social inequities on the health of the population can be offset (Macinko, et al., 2004). One feature of the healthcare system is related with health infrastructure. The development of public networks that provide health facilities is not enough to sustain and to ensure equity regarding the access of individuals to healthcare services (Valdivia, 2002). Hospital’s infrastructure can be strengthened by equitable distribution of resources and healthcare services (Starfi eld, Leiyu Shi, 2002). On the other hand, unequal expenditures for healthcare, including infrastructure and health work force, can generate gaps between rural and urban areas and can affect vulnerable groups (Zare et al., 2013). This is why rethinking the ways of fi nancing health systems can restore the social equity. As a fact, the costs involved for isolated areas that do not provide medical care should be reconsidered (Botman, Porter, 2008) together with the increase the population’s access to health insurance scheme (Acosta, 2014). Moreover, the inequality regarding the access to health care services, with or without income inequalities, negatively affects individual health and weakens the economic growth (Grimm, 2011, Kondo, 2012) as macroeconomic differences have impact on living standards (Rodriguez-Pose, Maslauskaite, 2011).

Romanian Statistical Review nr. 2 / 2017 25

On the other hand, the increase of national wealth is linked with high or improved health status. According to Suhrcke et al. (2005), Grossman made the fi rst distinction between health as a commodity that has utility for individuals and health as a capital good which contribute to the development of activities on the economic market. As a fact, the existence of good health status increases the work productivity, and thus, human capital performance (Muhamamad, 2010). Opposite to this, the deterioration of health because of the reduction of income leads to an increase in the rate of illnesses and to an increase in the rate of mortality that society has (Peykarjou et al., 2011).Considering the fact that healthcare system is a major sector that has long-term effects on personnel and on local economies (Kabajulizi, 2016), it is important to establish the relationship between health system and economy, at macroeconomic level. According to Bloom, Canning (2008), although not a direct effect on the economy was detected, the values associated with health refl ect economic stability. Moreover, poor health affects the dynamics of savings, while the increase of saving levels allows their use for the purpose of medical care when retirement comes (Chovancova et al., 2015) and for the purpose to reduce the risk of aging early (Popescu, Dumitrescu, 2016).The investment in health is an instrument of macroeconomic policy that reduces economic disparities and social inequalities (Aguayo Rico, et al, 2005).The reanalysis of research and development systems (Paunica et al, 2009) and the investments in research provide not only economic and social benefi ts but also determine the increases of quality of life and reduce the mortality. (MRC, 2011). For example, in countries where certain facilities exists for the investors, there is a high level of quality of life. (Belas et al., 2015)

3. DATA AND METHODOLOGY OF THE RESEARCH

The variables used in this analysis, were selected both from the online database of the World Bank and World Health Organization. They were included into regression models (linear or panel ones) and are presented in brief in Table 1.

Romanian Statistical Review nr. 2 / 201726

The Variables Used in the Conducted AnalysisTable 1

Variable Meaning Data source

1.Gini index (poverty and equity

Measures the extent to which income distribution (or in some cases, consumption expenditure) among individuals or households within an economy deviates from a perfectly equal distribution. It looks at poverty and income distribution

World Bank

2.Infant deaths Measures the magnitude of child mortality.

World Health Organization- Global Health Observatory

3.Health infrastructure Measures the number of medical units per 100.000 inhabitants; World Bank

4. Health work force density Measures Health workforce density per 1000 inhabitants.

World Health Organization

5. Research and development expediture (% of GDP) - R&D

Represents current capital expenditures (both public and private sources) for research and development used for increasing the level of new knowledge and the usage of new applications.

World Bank – UNESCO

We used the fi ve indicators in order to reveal the link between poverty, measured by GINI index and health characteristics like the number of infants deaths, the value of health infrastructure and the value of health work force. Moreover, we looked at the relationship between GINI index and the research and development expenditure as a percentage from GDP. The data was collected from 2010 and 2013 for all countries that have available information. The selection was made from more than 100 countries that reported data on World Health Organization and on World Bank, by applying VLOOKUP function on data contained in Excel. The variables included into the analysis are presented in Table 2.

Romanian Statistical Review nr. 2 / 2017 27

The Variables’ Defi nitionTable 2

Variable Explanation

GINI Index

The value of GINI Index is between 0- that means perfect equality and 100 that implies perfect inequality. It measures relative and not absolute welfare, worldwide. There are particular cases when GINI index of a developed country increases, while the number of population that lives in absolute poverty decreases. Even though World Bank have information regarding the income distribution for all the states that provided the data, it displays poverty level only for low and middle income countries that are eligible to receive loans from the World Bank. In general, income distribution is more unequal than the distribution of consumption. GINI Index provides a summary regarding acceptable degree of inequality worldwide

Total number of infant deaths

The number of infant deaths (expressed in thousands) before reaching the age of fi ve and the number of infant deaths (expressed in thousands) before reaching the age of one

Number infant deaths under-fi ve

The number of infant deaths (expressed in thousands) before reaching the age of fi ve

Number infant deaths under-one

The number of infant deaths (expressed in thousands) before reaching the age of one

Total Health infrastructure

The value of care units per 100000 inhabitants worldwide composed of: the number of hospitals per 100000 inhabitants, the number of health centers per 100000 inhabitants, the number of health posts per 100000 inhabitants, the number of rural hospitals 100000 inhabitants, the number of provincial hospitals per 100000 inhabitants, the number of specialized hospitals that provide care to 100000 inhabitants;

Total health work force density

The value of health work force density per 1000 people composed of: physicians density per 1000 population, nursing and midwifery personnel density per 1000 population, dentistry personnel density per 1000 population, pharmaceutical personnel density per 1000 population, laboratory health workers density per 1000 population, Laboratory health workers density per 1000 population, environmental and public health workers density per 1000 population, community and traditional health workers density per 1000 population, Other health workers density per 1000 population, Health management and support workers density per 1000 population

Total R&D Expenditures (% of GDP)

The research and development expenditure that a country has as a percentage from GDP

Romanian Statistical Review nr. 2 / 201728

In order to conduct the analysis and to reveal the impact of healthcare system characteristics on social inequality and the infl uence of R&D expenditure on social inequality, we provided descriptive statistics of the variables included into the analysis, revealing their maximum and their minimum level. We conducted Granger test in order to provide evidence on the direction of correlation, if inequality infl uences healthcare system characteristics and R&D expenditure or if healthcare system characteristics and R&D expenditure impacts the social inequality. The method of estimation was both panel data models and linear regression, depending on the available information. As a fact, if the data was found for more than one year (without gaps between the beginning period and the ending one), the panel model was used. The model was tested for fi xed effects and random effects. The selection between them was based on Hausman Test, while the selection between random and pooled model was realized considering the statistically signifi cance of the coeffi cients of variables included into the analysis. Otherwise, if gaps between the beginning period and the ending one were detected, the simple linear regression model was used. This is the main reason why the dimension of the samples varies from one analysis to another and why the panel model analysis is conducted on 2010-2013 and the regression model analysis is conducted on 2010 or 2013. The independent variable was chosen based on the Granger test. The analysis was conducted using Eviews 7.0. The aim of the paper was to reveal what the relationship between social inequality and healthcare system characteristics is and if R&D expenditures can affect the value of Social inequality. In order to conduct this analysis, we restate the hypothesis of research.

H1. Higher the value of GINI index is, higher the value of infant deaths is.

H2. Higher the value GINI index is, higher the need for health infrastructure is

H3. Higher the health work force density is, lower the value of GINI Index is

H4. Higher the expenditures for R&D are lower the value of GINI Index is.

Romanian Statistical Review nr. 2 / 2017 29

4. ANALYSIS OF THE RESULTS

The purpose of this research was to provide evidence on the correlation of social inequality with health system characteristics and with research and development expenditure. In order to conduct this analysis, we reveal the highest values and the lowest values of the variables included. It has to be mentioned that for each variable the highest or the lowest values were presented according the worst situation. For example, for infant deaths is worst to have a highest number, while for health work force density is worst to have lowest values. As the dataset is different base on the available information, we decided to present two summaries, the fi rst one being related with 2010 and the second one revealing with 2013. The sample included consists of all countries that reported data on the analyzed period of time. In Table 3 it can be seen the top ten states with the highest values for GINI Index, the values being reported at the end of 2010. Therefore, for Zambia the GINI index has the highest value (55.62), followed by Colombia (55.5) and Lesotho (54.18).It should be noted that the values for the GINI Index should be as small as possible to refl ect an acceptable level of social justice among individuals. If the GINI Index has a high value and close to 100, this means the wealth is low and the incomes are unequal distributed. Regarding the number of Infants Deaths, at the end of 2010, Nigeria has the highest value (513), followed by Pakistan (383) and Democratic Republic of the Congo (238). In terms of economic signifi cance, it can be said that higher the number of infant deaths is, lower is the equality between individuals and higher is the discrepancy considering their living conditions. The third variable: health infrastructure has alarming values when they are really small. The lowest values were detected for Democratic Republic of the Congo (0.46), Malaysia (0.48) and Haiti (0.55). We consider that lower health infrastructure could be correlated with higher values for infants deaths lower values of health work force density that leads to poverty and social inequalities between individuals. When we look at Health work force density we concluded that there are still countries where the density of medical force is less than 1 per 1000 inhabitants. The smallest values at the end of 2010 were recorded in Saint Lucia (0.167), Sierra Leone (0.398) and Afghanistan (0,561)

Romanian Statistical Review nr. 2 / 201730

Worst Values for the Analyzed Variables at the End of 2010Tabel 3

Top 10 highest values at the end of 2010 Top lowest values at the end of 2010

GINI index Infants deaths Health infrastructure Health work force density

Zambia (55.62) Nigeria (513) Democratic Republic of the Congo (0.46) Saint Lucia (0.167)

Colombia (55.5) Pakistan (383) Malaysia (0.48) Sierra Leone (0.398)

Lesotho (54.18) Democratic Republic of the Congo (238) Haiti (0.55) Afghanistan (0,561)

Honduras (53.39) India (235) Israel (0.59) Mozambique (0.575)

Panama (51.91) China (216) Jamaica (0.76) Nauru (0.714)

Paraguay (51.83) Ethiopia (150) Netherlands (0.77) Cape Verde (0.919)

Rwanda (51.34) Indonesia (127) Poland (0.94) Iraq (0.929)

Guinea-Bissau (50.66) Bangladesh (123) Saudi Arabia (1.09) Burkina Faso (0.974)

Ecuador (49.25) Angola (108) Luxembourg (1.19) Ghana (1.022)

Mexico (48.13) Afghanistan (82) Sierra Leone (1.26) Kenya (1.047) Source: authors ‘computation on available data

In order to conduct a comparison between the values registered in 2010 and the values registered in 2013, we decided to present the highest values, respectively the lowest values also for 2013, based on their worst values. The data is presented in Table 4. The idea is to detect if countries with worst conditions have improved their situation or not.

Romanian Statistical Review nr. 2 / 2017 31

Worst Values for the Analyzed Variables at the End of 2013Table 4

Top 10 highest values at the end of 2010 Top lowest values at the end of 2010GINI index Infants deaths Health infrastructure Health work force

densityHonduras (53.67) Pakistan (369) Haiti (0.77) Portugal (0.76)

Colombia (53.49) Democratic Republic of the Congo (234)

Democratic Republic of the Congo (0.9) Afghanistan (0.792)

Brazil (52.87) Ethiopia (136) Malaysia (0.94) Kenya (1.135)Panama (51.67) Indonesia (129) Israel (1.13) Vietnam (2.426)Chile (50.45) Bangladesh (106) Sierra Leone (1.21) Costa Rica (2.498)

Costa Rica (49.18) Afghanistan (72) Jamaica (1.51) Ireland (2.67)Paraguay (48.3) Uganda (63) Netherlands (1.52) Oman (3.334)Bolivia (48.06) Sudan (62) Egypt (1.87) Argentina (3.859)

Ecuador (47.29) Kenya, Cote d’IvoireEgypt (56) Poland (1.88) Georgia (4.411)

Dominican Republic (47.07) Mali (55) Saudi Arabia (2.08) Nicaragua (5.152)

Source: authors ‘computation on available data

From Table 4, we can observe that in 2010 the values of the indicators are worst then the values found in 2013. This could reveal that states are trying to improve the living conditions of their citizen, are trying to improve the level of health that the country has and moreover, are promoting fi scal and budgetary policies in order to re-launch the health sector. According to the data presented, it can be seen that we have in both statistics countries that have high value of GINI index (high level of inequality between individuals) like Ecuador, Colombia or Honduras. Similar results are found when the number of infant deaths exists. For example, Democratic Republic of the Congo, Pakistan, Ethiopia, Bangladesh have a high number of infant deaths both in 2010 and 2013. When the lowest values are analyzed, we observed that for the health infrastructure among the top ten there is Democratic Republic of the Congo, Haiti, Israel, Jamaica. Important discrepancies could be found when the information about health work force is disseminated as there seems to be other countries that registered lowest values in health work force density. One explanation is based on the fact that there are only 33 world countries that reported data on the value of health work force The statistics presented in Table 4 are related with all the available information that we had. However, the number of countries included into the

Romanian Statistical Review nr. 2 / 201732

analysis could be different as information for all the variables included was necessary. In order to see if the reveal what the relationship between social inequality and healthcare system characteristics is, we conducted several analyzed considering both the regression model and the panel data model (when available information exists). The idea was to conduct additional analysis with the purpose of making the results trustworthy.

Descriptive Statistics, Correlation Between GINI Index & Infant Deaths, 2010-2013

Table 5Common sample

GINI Index Infant deaths Mean 39.184 5.6667

Median 39.4 3 Maximum 57.4 42 Minimum 24.55 1 Std. Dev. 9.2782 6.8747 Skewness 0.1329 3.0850 Kurtosis 1.7792 15.2582

Jarque-Bera 6.8294 823.9677 Probability 0.03288 0

Observations 105 105Data source: authors ‘computation on available data

As we observe in Table 5, the minimum value for GINI index at world level for the years 2010-2013 it was 24.55 (in Ukraine, in 2011) and the maximum value is 57.4 (in Honduras, both in 2011 and 2012). In terms of standard deviation, if its value is lower than the analyzed values are grouped around the mean. In our case, we consider that the dataset values are more clustered around the mean value, respectively 39.184. As regarding Skewness and Kurtosis, indicators that concern normal distribution, we can conclude that the distribution is not normal as the difference between them is not 3. The relationship between GINI index and the number of infant deaths is presented in Table 6. Based on the Granger test, the GINI index does Granger Cause Infant Deaths.

Romanian Statistical Review nr. 2 / 2017 33

Model of Relationship Between GINI Index & Infant Deaths 2010-2013Table 6

Dependent variable log(infant_deaths)Variables Coeffi cientConstant 0.3676 (p=0.3799)GINI INDEX 0.0219 **

Quality of the model indicatorsR squared 4.21%F statistic and probability 4.5380**DW 0.0008Fixed effect cross sectional 525.16**Fixed effect period 0.6416 (p=0.59)Random effect cross sectional 1.4575 (0.2273)Random efect period 1.2718 (0.2594)Number of obs 105Cross sectional included 33Data source: authors ‘computation,Where ** shows the signifi cance threshold at 5%

The results from Table 6 reveal that there is a positive correlation between the value of GINI index and the number of infant deaths. The higher the value of GINI Index is, the higher the value of infant deaths is. This aspect is economically relevant, taking into account that higher the GINI Index is, higher the inequity between individuals is. Thus, the discrepancy between the rich people and the poor people increases having a negatively impact on the number of infant deaths (the living condition are harder for poor people). For example, if we consider the median of infants deaths 3 than an increase in GINI generates an increase in the number of infant deaths with 0.0219%. In this case, the null hypothesis is rejected because the probability of rejecting the null hypothesis (That the value of the coeffi cient is not statistically different from zero) is under 5%. Regarding the constant term, it is not statistically signifi cant as its coeffi cient probability is higher than 10% (0.3799). R-squared illustrates the fraction of the variation of dependent variable that is explained by the independent variable. Regarding F statistic, this is 4.5380 and its probability is below the tested signifi cance threshold (the model is valid) D.W shows that there are evidences of positive serial correlation of the residuals, but they cannot be corrected due to the lower number of years on which the analysis was conducted The results provide evidence that H1 is confi rmed. As the data that we have were different for each indicator and as the panel analysis was not possible for testing the hypotheses H2-H4, we tried

Romanian Statistical Review nr. 2 / 201734

to demonstrate their relevance by conducting linear regression on 2010 or 2013 based on where we have larger observations. In Table 7 the descriptive statistics of the variables that are in relationship with GINI are presented for year 2010.

Descriptive Statistics for 2010Table 7

Common sample

Correlation between GINI index and health

infrastructure

Correlation between GINI index and

health work force density

Correlation between GINI index and R&D

expenditure

Element GINIIndex

HeathInfrastructure

GINIIndex

Health work force

density

GINIIndex

R&D Expenditures

Mean 36.3542 26.395 36.1937 8.3348 34.667 1.1827

Median 33.55 12.94 33.76 7.382 33.21 0.7640

Maximum 55.62 230.81 55.62 27.58 55.5 3.9299

Minimum 24.94 0.59 26.43 1.094 24.82 0.0672

Std. Dev. 8.1564 41.2413 7.9281 6.2318 7.1574 0.9849

Skewness 0.7890 3.0220 1.1621 1.2349 1.0416 1.0423

Kurtosis 2.4221 13.2838 3.4943 4.3389 3.4976 3.2806

Jarque-Bera 6.5908 332.0079 8.2351 11.5117 10.3229 9.9547

Probability 0.0370 0 0.0162 0.0031 0.0057 0.0068

Observations 56 56 35 35 54 54Data Source: authors ‘computation

From Table 7 we can observe that the number of observation differs from one situation to another. For example, when the GINI index is considered, we can see that its minimum and maximum values differ from one scenario to another. For example, in the fi rst case, the maximum level is 55.62 and is associated to Zambia, while for the third scenario the maximum value is 55.5 and is associated for Colombia. Regarding the minimum values, less inequality, we have Slovenia with 24.94, Iceland with 26.43 and Ukraine with 24.82. When health infrastructure is analysed, we observed that the minimum and maximum values are found in Israel with 0.59 units per 100000 inhabitants and in Czech Republic. In terms of minimum and maximum values for health work force density, the maximum is 27 doctors per 1,000 inhabitants for Iceland and 1 doctor per 1,000 inhabitants is for Cambodia

Romanian Statistical Review nr. 2 / 2017 35

Regarding the minimum and maximum values for expenditures for research and development (% of GDP) at the world level, the maximum is 3.92% and the minimum is 0.06%. For all the scenarios, the distribution is not normal. Based on the data presented in Table 7, we conducted regression analysis using Eviews 7.0. The dependent and independent variables were established considering the Granger cause test. The results are presented in Table 8

MODEL OF THE RELATIONSHIP FOR 2010Table 8

Common sampleBetween GINI

index and health infrastructure

Between GINI index and health work

force density

Between GINI index and R&D expenditure

Dependent variable Health infrastructure GINI index GINI index

Coeffi cient Coeffi cient Coeffi cient

Constant -26.7284 (p=0.2808) 41.7520*** 37.3330***

Independent variable GINI index 1.4612**Health work force

density -0.6668***

R& D expenditure-2.2534**

Quality of the model indicators

R squared 8.35% 27.47% 9.61%F statistic and probability 4.9211** 12.5034*** 5.5324**

DW 1.83 2.001 1.66

Heteroscedasticity Noyes, corrected with covariance White

matrix

yes, corrected with covariance matrix White

Normality No Almost AlmostData Source: authors ‘computationWhere ***, ** shows the signifi cance threshold at 1% and 5%

The results presented in Table 8 reveal a positive correlation between GINI Index and Health infrastructure. Higher the GINI index is, higher the need for health infrastructure is. We interpret the results in the sense that the level of poverty at the world level it is infl uenced by the limited access of the population to the health care services because of underdeveloped infrastructure. Considering that, an increase of 1 for GINI Index determines an increase with 1.4612 of the need of total health infrastructure at world level. The coeffi cient is statistically signifi cant at a threshold of 5%. The model is statistically signifi cant and about 8.35% of health infrastructure is due to

Romanian Statistical Review nr. 2 / 201736

the value of GINI index and there is almost no correlation between residuals (the value of DW is 1.83) Based on these, a relationship between GINI index and health infrastructure exists. As the model is statistically signifi cant, we consider that the results confi rm the H3. Regarding the relationship between GINI index and health work force density, we identify a negative correlation between Health work force density and GINI index. Higher the density of health work force is, lower the GINI index is. Thus, when health work force density increases with 1 doctor per 1.000 inhabitants then the GINI index decreases with 0.66 units. The value of DW threshold shows us that between the residues of the regression there is no autocorrelation. Regarding heteroscedascky (the volatility of the residuals-their variance is not constant) it was corrected with covariance White matrix. The results confi rm the H4 that higher the health work force density is, lower the value of GINI Index is. The last relationship that was tested was based on the link between R& D expenditure and GINI index. The results reveal that there is a negative correlation between the expenditures for R&D ( as a % from GDP) and the GINI Index. When the expenditures for R&D increases with 1% from GDP, the GINI index decreases with 2.25 (the coeffi cient is statistically signifi cant at 5% - its value is not zero). The results present the fact that the higher the expenditures for R&D are the lower GINI Index is. More than 9% of the variation of the GINI index is explained by the R&D expenditure as a %from GDP. The probability associated to F statistic shows that the model is valid (at least one coeffi cient differs signifi cantly from zero). The errors of the model could be positively correlated, , while heteroscedasticity was corrected with covariance White matrix. The results confi rm H4 that higher the expenditures for R&D are, lower the value of GINI Index is. Subsequently we tried to link these indicators also for 2013, in order to see to what extent the values have changed, but the small number of observations generated irrelevant statistical models. Only the relationship between GINI index and health work force density was validated for 2013. The data – the descriptive statistics and the model of the relationship between the two variables are presented in Table 9.

Romanian Statistical Review nr. 2 / 2017 37

Descriptive Statistics and Model of the Relationship Between GINI Index & Health Work Force Density, 2013

Table 9

Common sample

Correlation between GINI index and health work force- descriptive

statistics

Model of the relationship between GINI index and health

work force

Element GINIIndex

Health work force

density

Dependent variableGINI index

Mean 37.1 9.2868

Median 34.4 8.408 Constant 40.9947***

Maximum 63.1 33.653 Health work force density -0.4193**

Minimum 25.6 0.792 Quality of the model indicators Std. Dev. 9.4532 6.8616 R squared 9.26%

Skewness 1.1964 1.6538 F Statistic and probability 2.45*

Kurtosis 3.6637 7.1074 DW 1.35 Jarque-Bera 6.6801 30.129 Heteroscedasticity No Probability 0.0354 0 Normality No

Observations 26 26

Data Source: authors ‘computationWhere ***, **, * shows the signifi cance threshold at 1% 5% and 10%