role of national development banks in sme financing 5_farhad... · · 2017-10-23role of national...

TRANSCRIPT

Role of National Development

Banks in SME Financing

Naoyuki YOSHINO, Ph.D.Dean, Asian Development Bank Institute (ADBI)

Professor Emeritus, Keio University, Japan

Farhad TAGHIZADEH-HESARY, Ph.D.Faculty member, Keio University, Tokyo, Japan

Sep 28, 2017

Bangkok

UN-ESCAP

1. IntroductionNational Development Banks (NDBs) can contribute to

solving a number of market failures.

NDBs can promote financial sector development by offering

long-term loans with lower interest rate to SMEs and helping to

create inclusive financial sectors. SMEs have information

asymmetry and many private FIs are not interested to lend

them.

NDBs also enhance the climate for business and attract private

sources of capital in the domestic economy.

NDBs can act as a catalyst and promoting and supporting

SMEs how ever there are some considerations with this regard

that will be highlighted in this presentation.

Copyright: Yoshino & Taghizadeh-Hesary (2017)

2

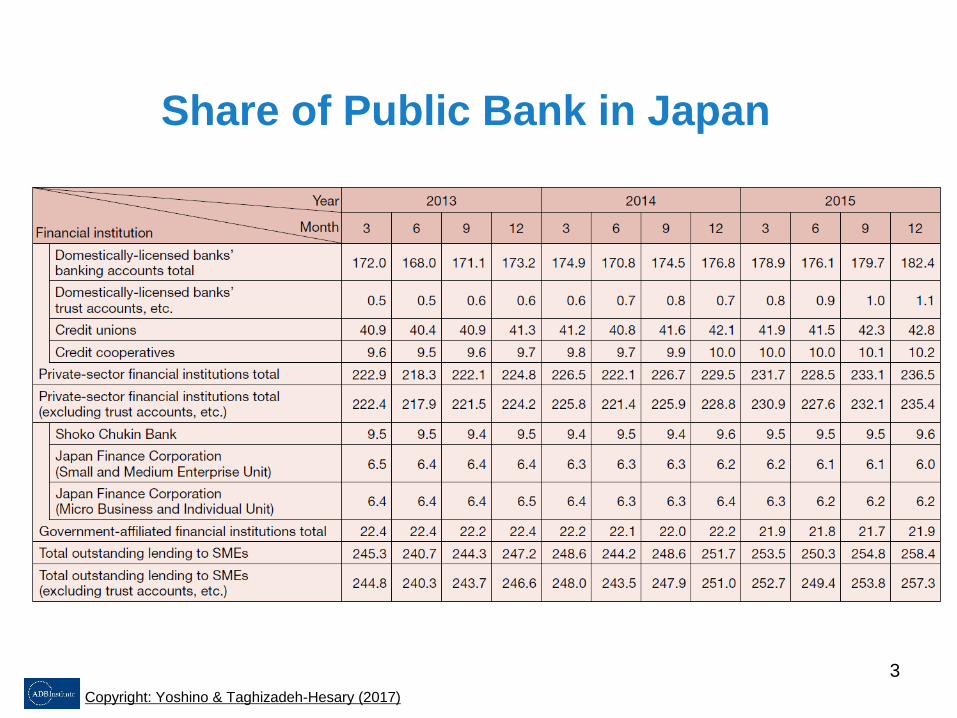

Share of Public Bank in Japan

Copyright: Yoshino & Taghizadeh-Hesary (2017)

3

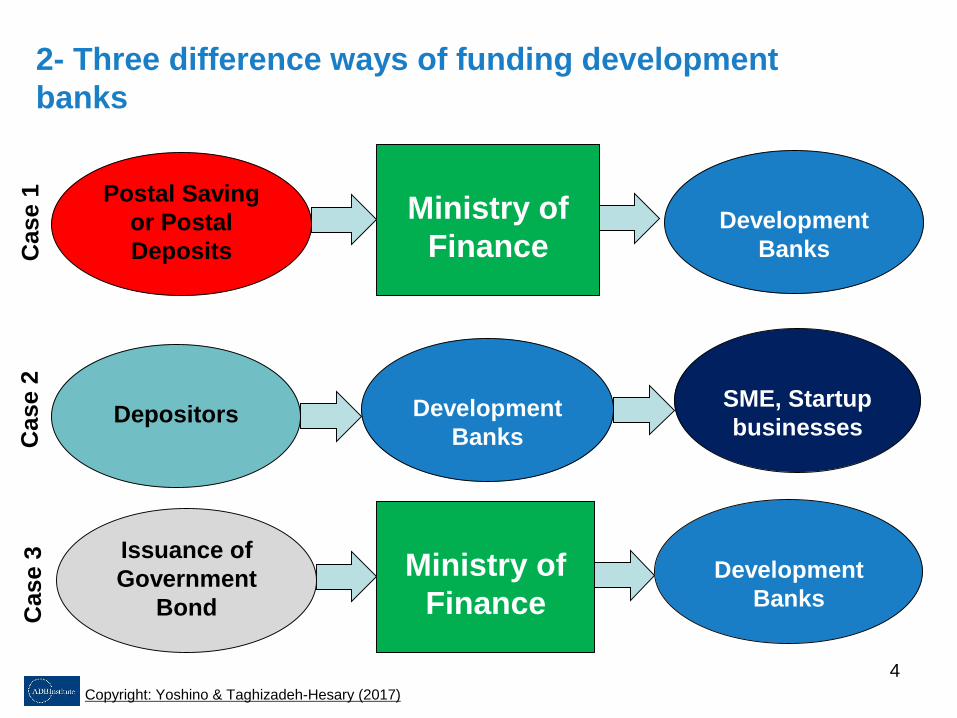

2- Three difference ways of funding development

banks

Postal Saving

or Postal

Deposits

Ministry of

Finance Development

BanksCase 1

Development

Banks

Development

Banks

Ministry of

Finance

DepositorsSME, Startup

businesses

Issuance of

Government

Bond

Case 2

Case 3

Copyright: Yoshino & Taghizadeh-Hesary (2017)

4

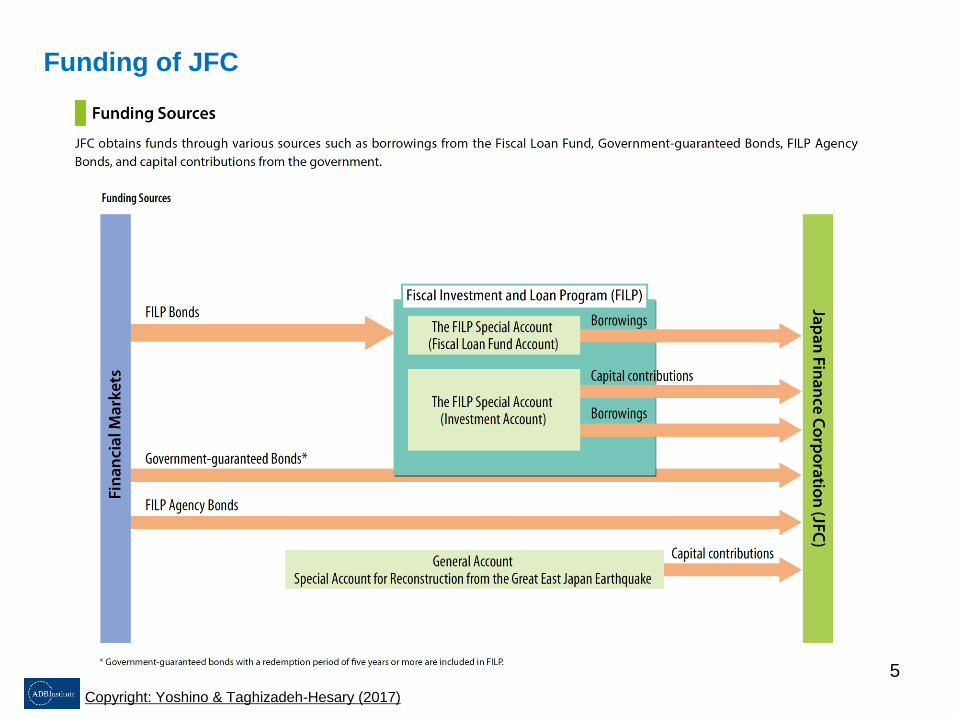

Funding of JFC

Copyright: Yoshino & Taghizadeh-Hesary (2017)

5

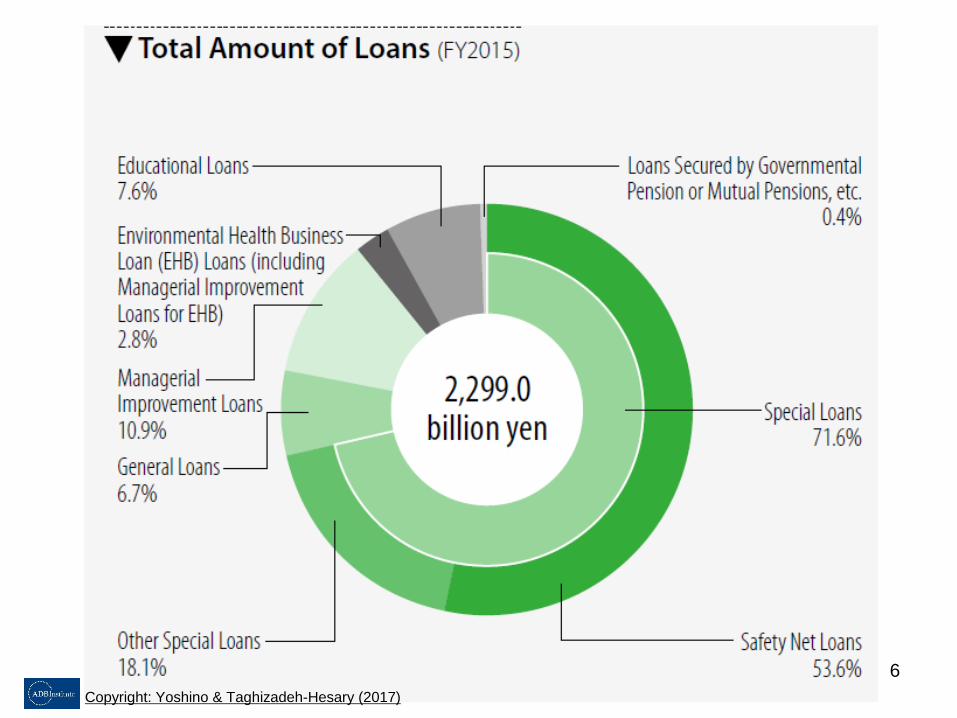

6

Copyright: Yoshino & Taghizadeh-Hesary (2017)

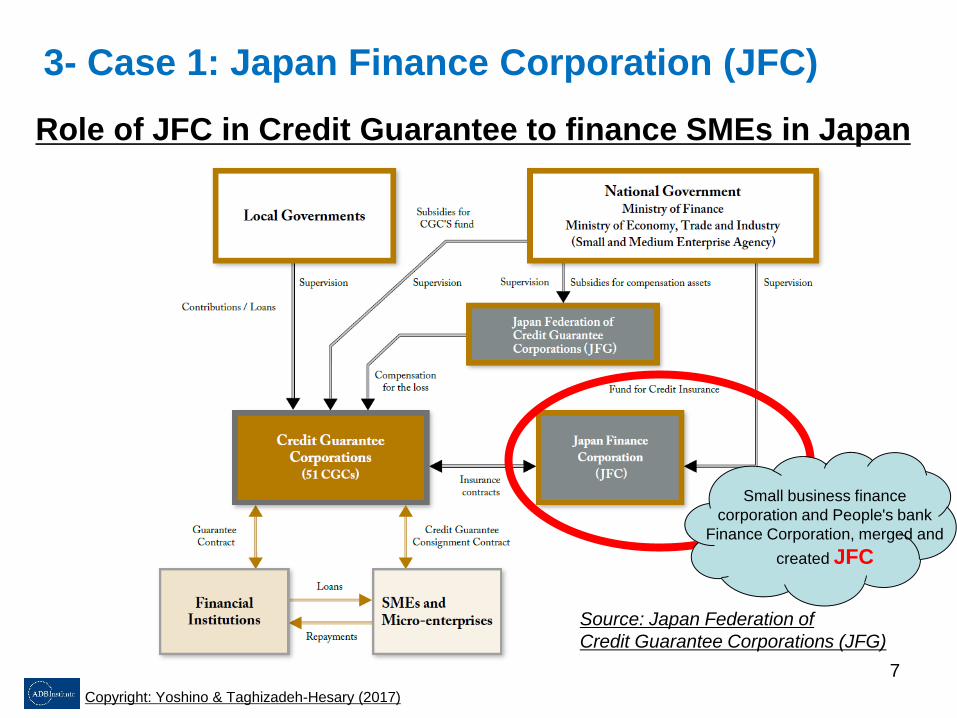

Role of JFC in Credit Guarantee to finance SMEs in Japan

Source: Japan Federation of

Credit Guarantee Corporations (JFG)

3- Case 1: Japan Finance Corporation (JFC)

Small business finance

corporation and People's bank

Finance Corporation, merged and

created JFC

Copyright: Yoshino & Taghizadeh-Hesary (2017)

7

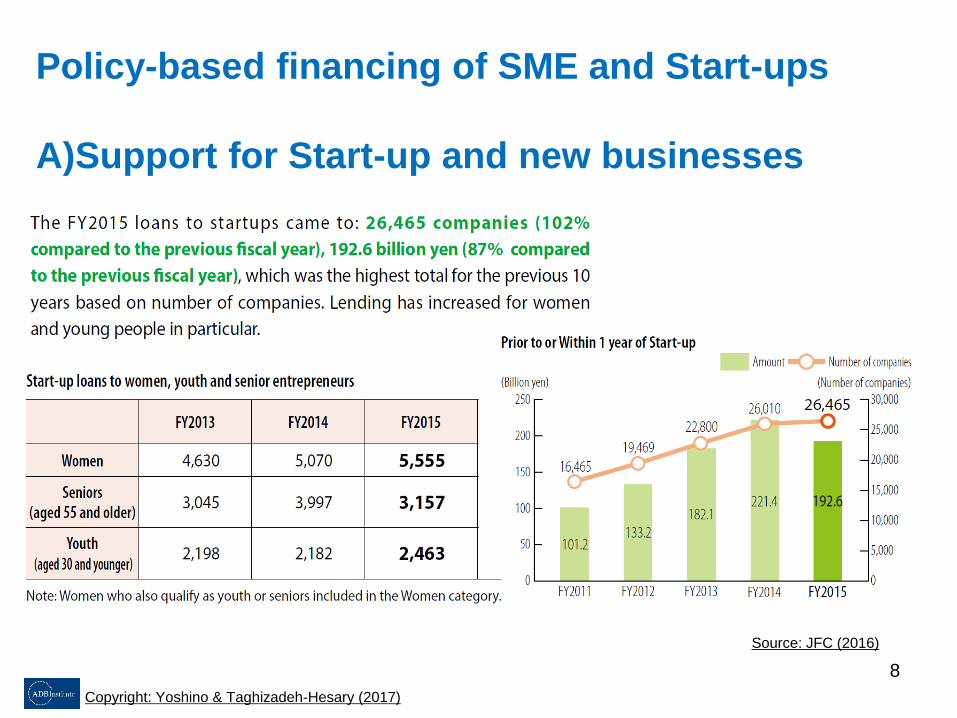

Policy-based financing of SME and Start-ups

A)Support for Start-up and new businesses

Source: JFC (2016)

Copyright: Yoshino & Taghizadeh-Hesary (2017)

8

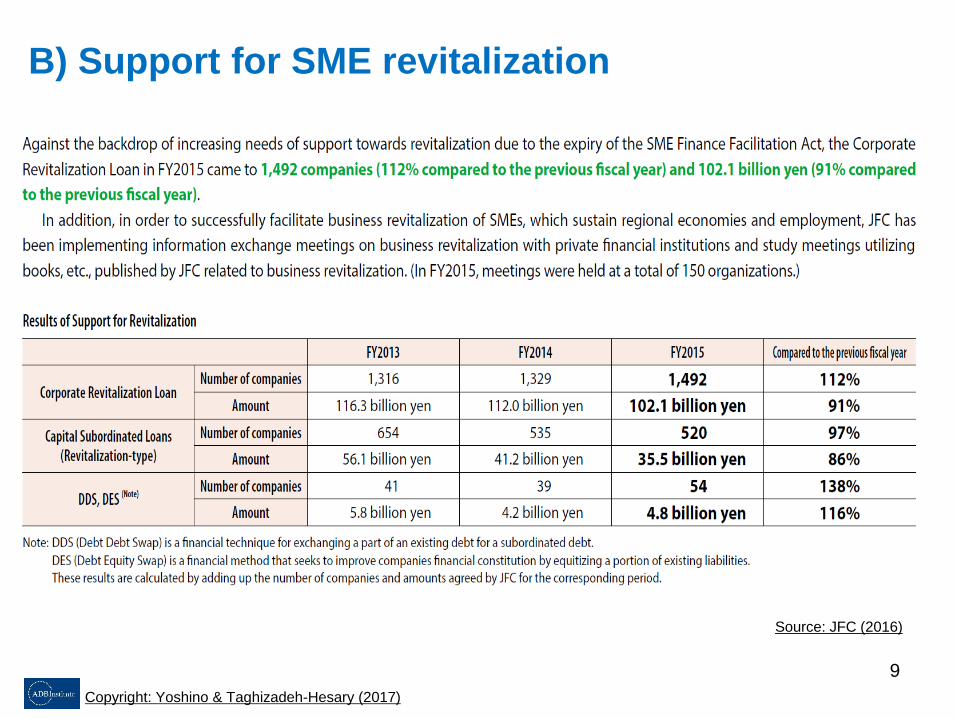

B) Support for SME revitalization

Source: JFC (2016)

Copyright: Yoshino & Taghizadeh-Hesary (2017)

9

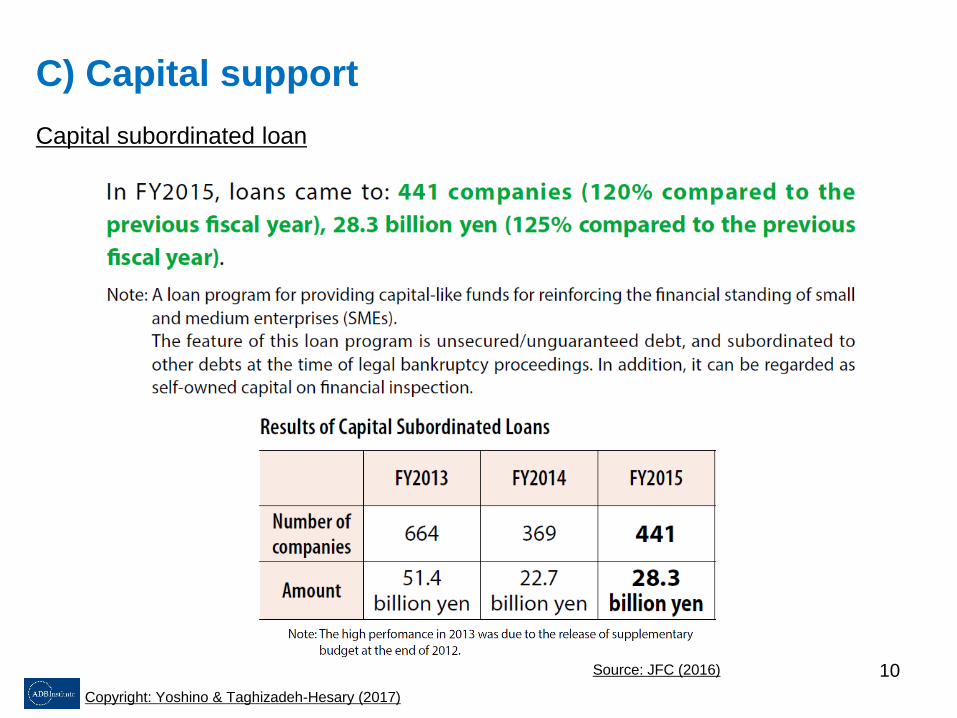

C) Capital support

Source: JFC (2016)

Capital subordinated loan

Copyright: Yoshino & Taghizadeh-Hesary (2017)

10

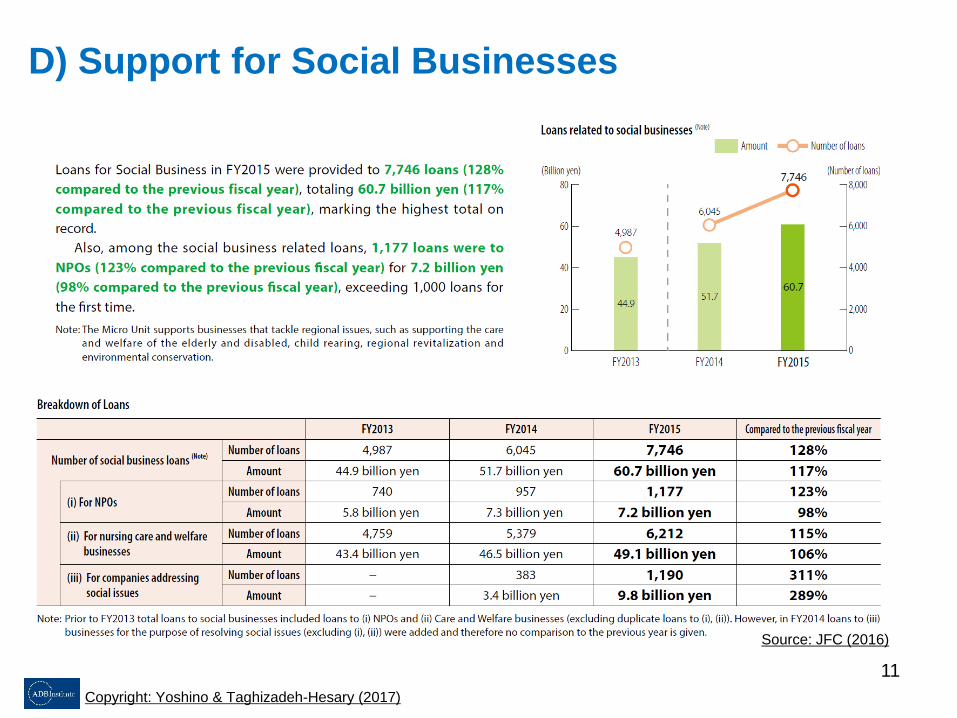

D) Support for Social Businesses

Source: JFC (2016)

effete

Copyright: Yoshino & Taghizadeh-Hesary (2017)

11

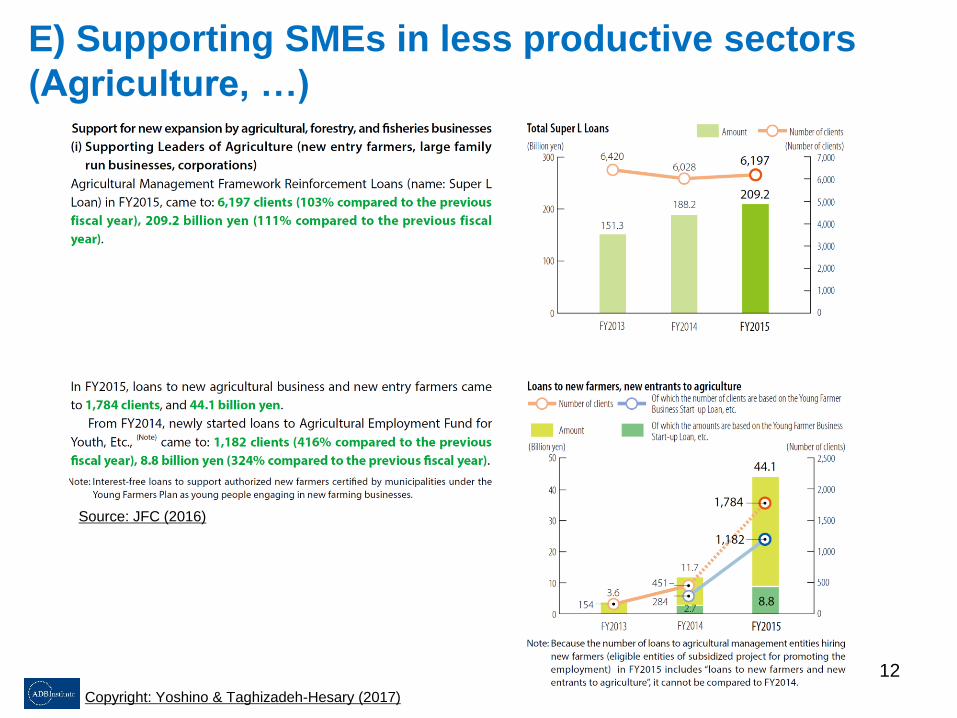

E) Supporting SMEs in less productive sectors

(Agriculture, …)

Source: JFC (2016)

Copyright: Yoshino & Taghizadeh-Hesary (2017)

12

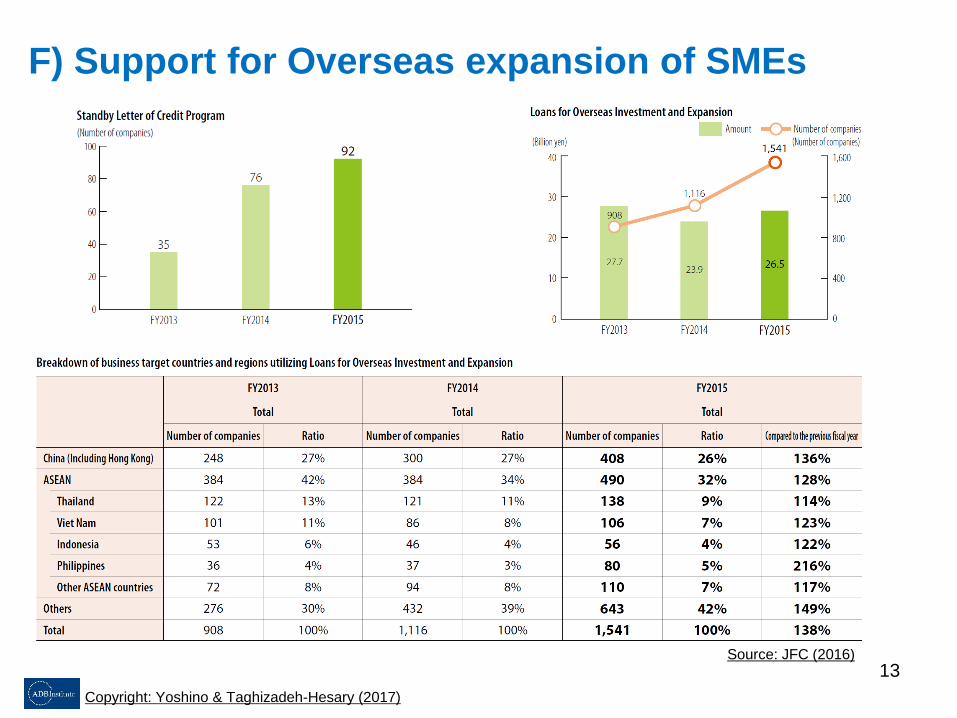

F) Support for Overseas expansion of SMEs

Source: JFC (2016)

kejdklejfekl

Copyright: Yoshino & Taghizadeh-Hesary (2017)

13

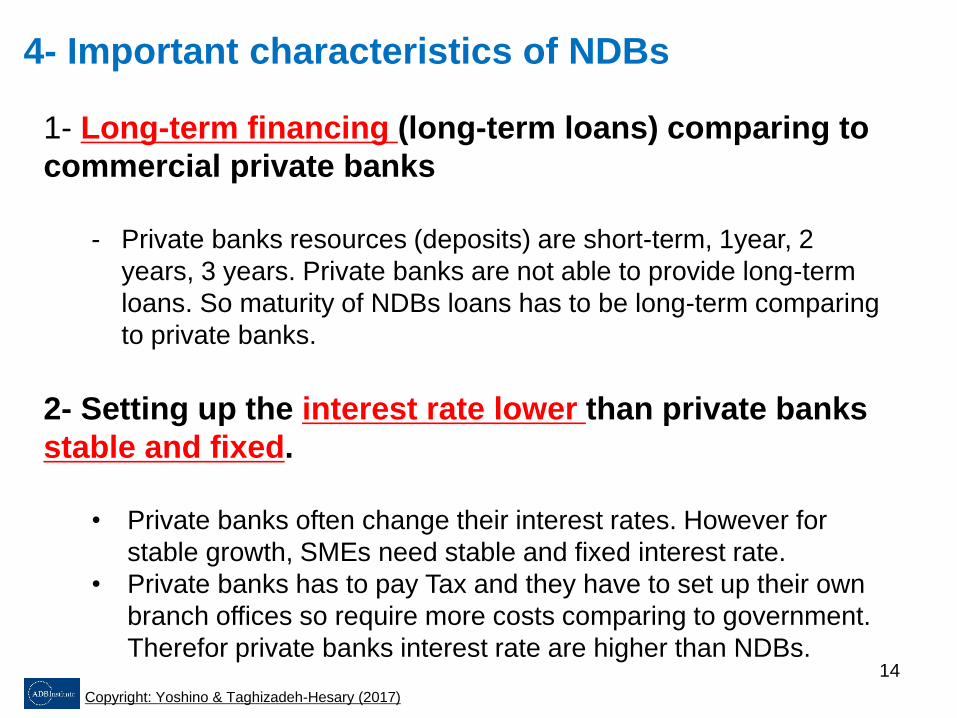

4- Important characteristics of NDBs

1- Long-term financing (long-term loans) comparing to

commercial private banks

- Private banks resources (deposits) are short-term, 1year, 2

years, 3 years. Private banks are not able to provide long-term

loans. So maturity of NDBs loans has to be long-term comparing

to private banks.

2- Setting up the interest rate lower than private banks

stable and fixed.

• Private banks often change their interest rates. However for

stable growth, SMEs need stable and fixed interest rate.

• Private banks has to pay Tax and they have to set up their own

branch offices so require more costs comparing to government.

Therefor private banks interest rate are higher than NDBs.

Copyright: Yoshino & Taghizadeh-Hesary (2017)

14

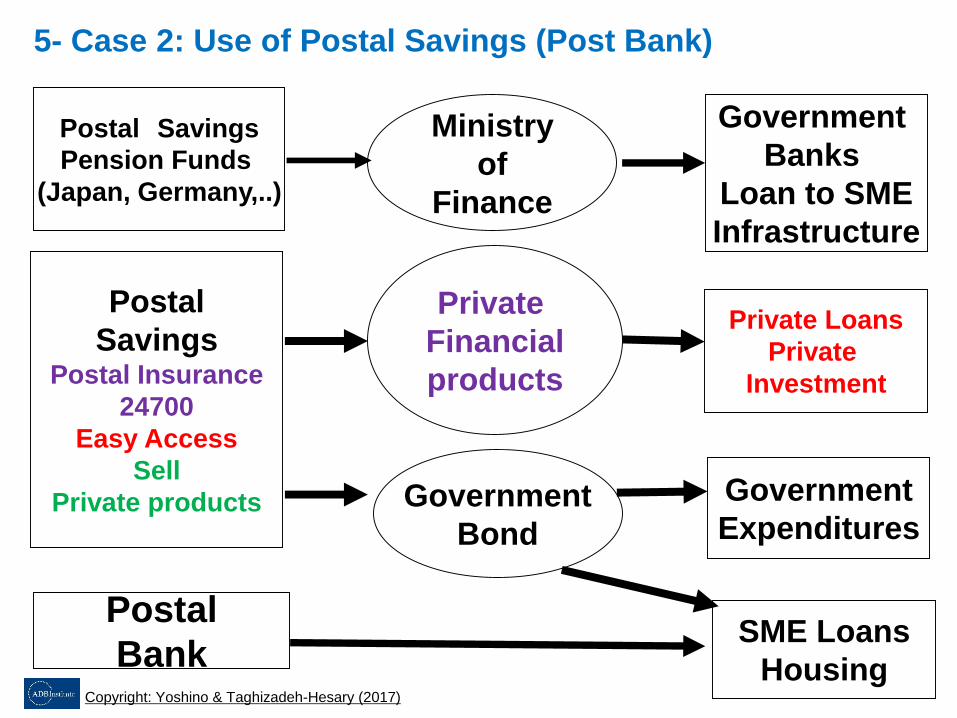

5- Case 2: Use of Postal Savings (Post Bank)

Postal Savings

Pension Funds

(Japan, Germany,..)

Ministry

of

Finance

Postal

SavingsPostal Insurance

24700

Easy Access

Sell

Private products

Government

Banks

Loan to SME

Infrastructure

Government

Bond

Government

Expenditures

Postal

BankSME Loans

Housing

Private

Financial

products

Private Loans

Private

Investment

Copyright: Yoshino & Taghizadeh-Hesary (2017)

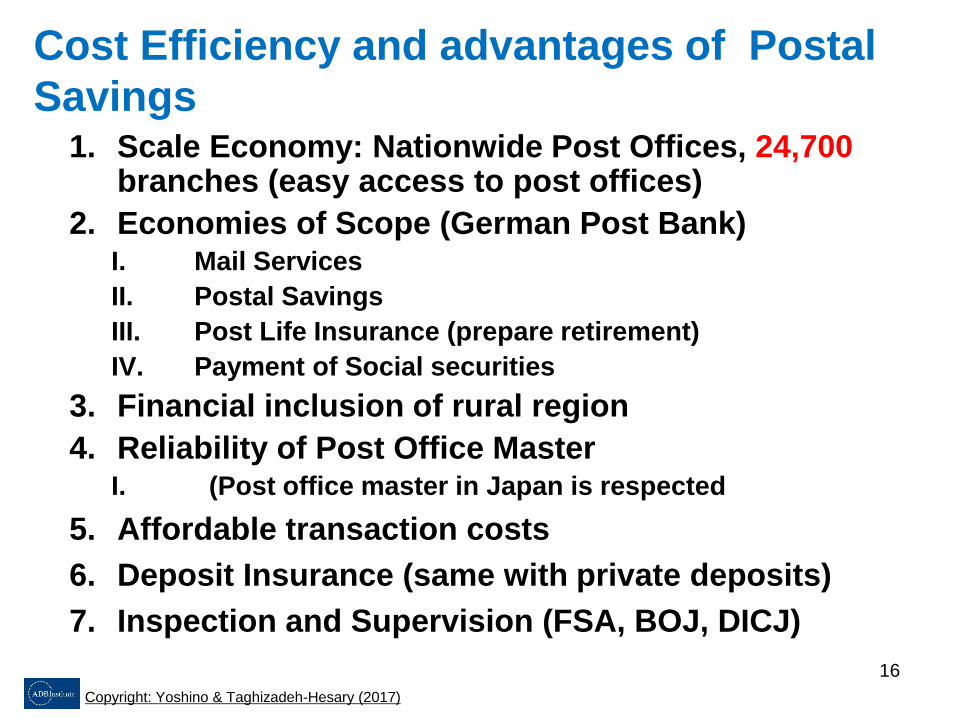

Cost Efficiency and advantages of Postal

Savings1. Scale Economy: Nationwide Post Offices, 24,700

branches (easy access to post offices)

2. Economies of Scope (German Post Bank)I. Mail Services

II. Postal Savings

III. Post Life Insurance (prepare retirement)

IV. Payment of Social securities

3. Financial inclusion of rural region

4. Reliability of Post Office MasterI. (Post office master in Japan is respected

5. Affordable transaction costs

6. Deposit Insurance (same with private deposits)

7. Inspection and Supervision (FSA, BOJ, DICJ)

Copyright: Yoshino & Taghizadeh-Hesary (2017)

16

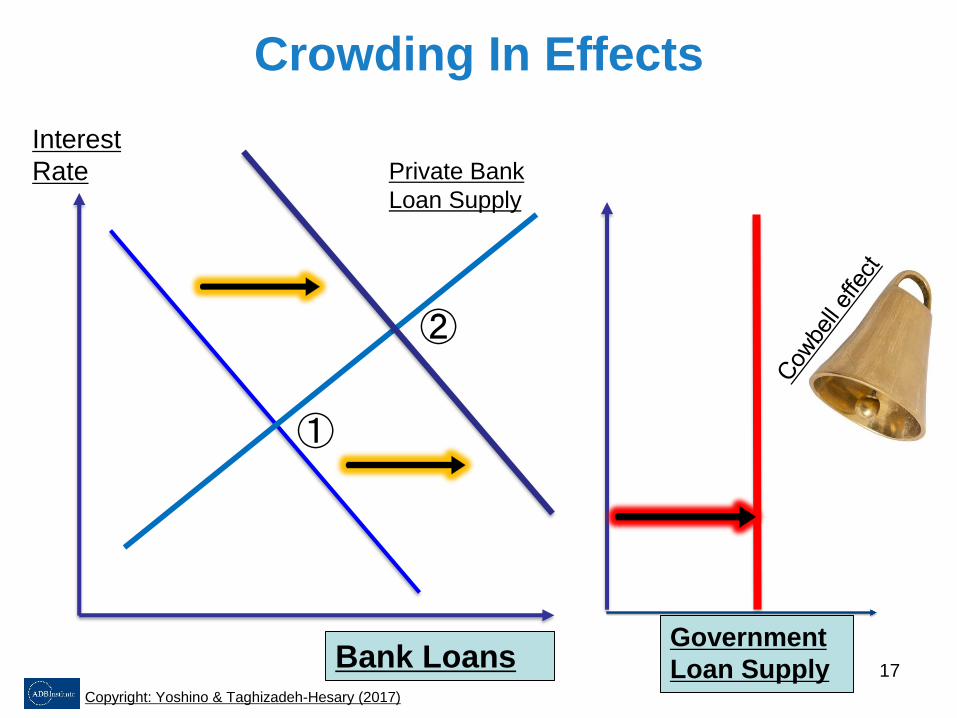

Crowding In Effects

Interest

Rate

Government

Loan Supply

Private Bank

Loan Supply

Bank LoansCopyright: Yoshino & Taghizadeh-Hesary (2017)

①

②

17

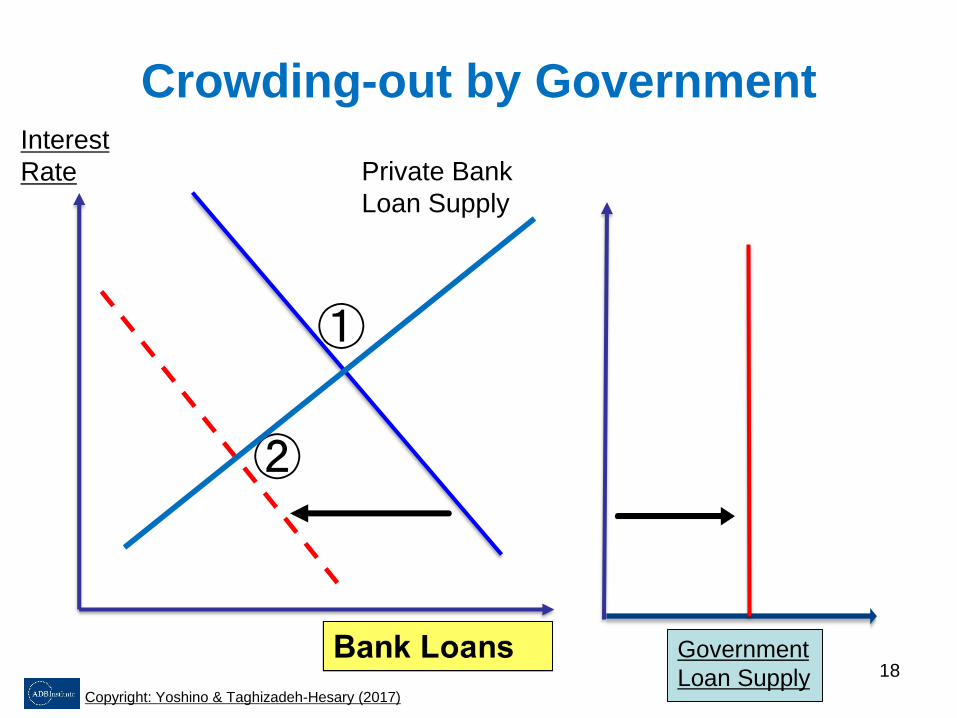

①

②

Crowding-out by GovernmentInterest

Rate

Government

Loan Supply

Private Bank

Loan Supply

Copyright: Yoshino & Taghizadeh-Hesary (2017)

18

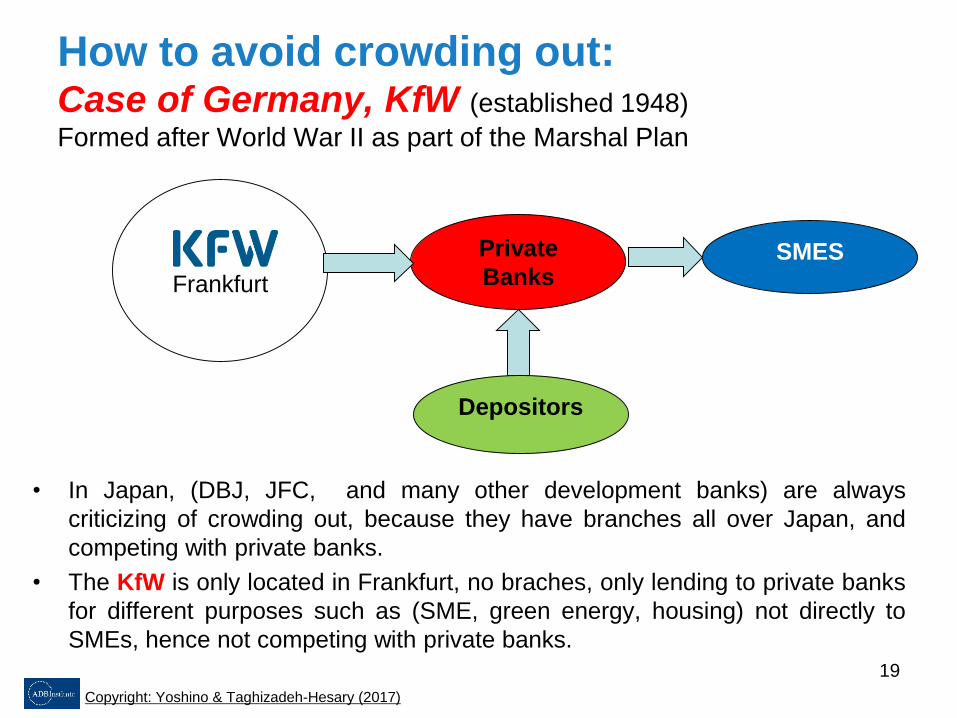

How to avoid crowding out: Case of Germany, KfW (established 1948)

Formed after World War II as part of the Marshal Plan

• In Japan, (DBJ, JFC, and many other development banks) are always

criticizing of crowding out, because they have branches all over Japan, and

competing with private banks.

• The KfW is only located in Frankfurt, no braches, only lending to private banks

for different purposes such as (SME, green energy, housing) not directly to

SMEs, hence not competing with private banks.

Frankfurt

Private

Banks

Depositors

SMES

Copyright: Yoshino & Taghizadeh-Hesary (2017)

19

6. Conclusion

1. Lower interest rate, stable, and long-term loans

by NDBs

2. Avoid Bad Effects of government lending

through NDBs:

– Increase of government role

– Crowd out private deposits and loans

3. German KfW: successful case– Government money goes through private banks to SMEs,

housing, green energy and etc.

4. Make loans by NDBs where:

– private banks cannot make loans

Copyright: Yoshino & Taghizadeh-Hesary (2017)

20

Reference:1. UN (2006). Rethinking the Role of National Development Bank. United Nations Department of

Economic and Social Affairs.

2. Yoshino, N. (2012). Global Imbalances and the Development of Capital Flows among Asian

Countries. OECD Journal: Financial Market Trends. Vol. 2012/1.

3. Yoshino, N. (2013). The Background of Hometown Investment Trust Funds. In N. Yoshino and S.

Kaji, eds. Hometown Investment Trust Funds: A Stable Way to Supply Risk Capital. Tokyo:

Springer.

4. Yoshino, N. and F. Taghizadeh-Hesary (2014). An Analysis of Challenges Faced by Japan’s

Economy and Abenomics. The Japanese Political Economy 40: 1–26. DOI:

10.1080/2329194X.2014.998591

5. Yoshino, N. and F. Taghizadeh-Hesary (2014). Analytical Framework on Credit Risks for

Financing SMEs in Asia. Asia-Pacific Development Journal. United Nations Economic and Social

Commission for Asia and the Pacific (UN-ESCAP). 21(2): 1-21.

6. Yoshino, N., Taghizadeh-Hesary, F., Nili, F. (2015), ‘Estimating Dual Deposit Insurance Premium

Rates and Forecasting Non-performing Loans: Two New Models’. ADBI Working Paper 510.

Asian Development Bank Institute: Tokyo

7. Kuwahara, S., N. Yoshino, M. Sagara, and F. Taghizadeh-Hesary. (2015). Role of the Credit Risk

Database in Developing SMEs in Japan: Lessons for the Rest of Asia. ADBI Working Paper 547.

Tokyo: Asian Development Bank Institute.

8. Yoshino, N. and F. Taghizadeh-Hesary. (2015). Analysis of Credit Risk for Small and Medium-

Sized Enterprises: Evidence from Asia. Asian Development Review (ADR). Vol. 32 No. 2.: 18-37,

MIT Press.

Copyright: Yoshino & Taghizadeh-Hesary (2017)

21