risk & return analysis - bonds market in pakistan

TRANSCRIPT

RISK & RETURN ANALYSIS OF BOND MARKET IN PAKISTAN

Faculty Advisor:Ms. Tazeen Arsalan

Researchers:Abdul Hadi Khanani

Armoghan MoinQandeel Fatima Memon

Samra JavedSyed Jahanzeb Haider

Yamna ShumasZoya Talat

SPECIAL THANKS TO CDC

OBJECTIVES OF THE STUDY

To Analyze The Risk And Return Of Bond Market

in Pakistan

To Analyze The Factors

affecting Return on Bond

Market in Pakistan

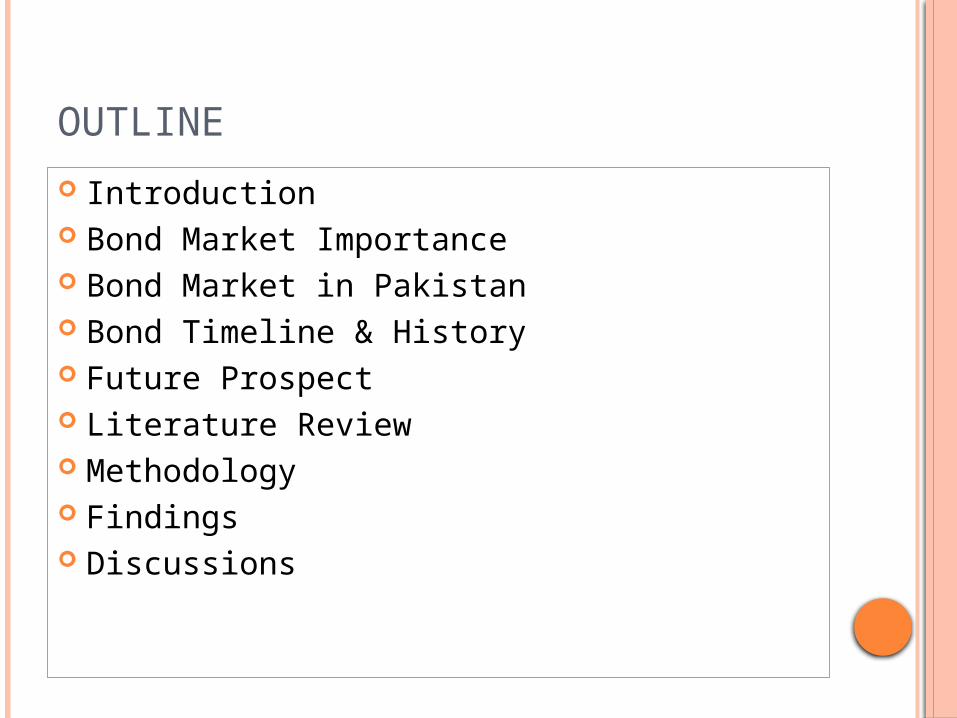

OUTLINE Introduction Bond Market Importance Bond Market in Pakistan Bond Timeline & History Future Prospect Literature Review Methodology Findings Discussions

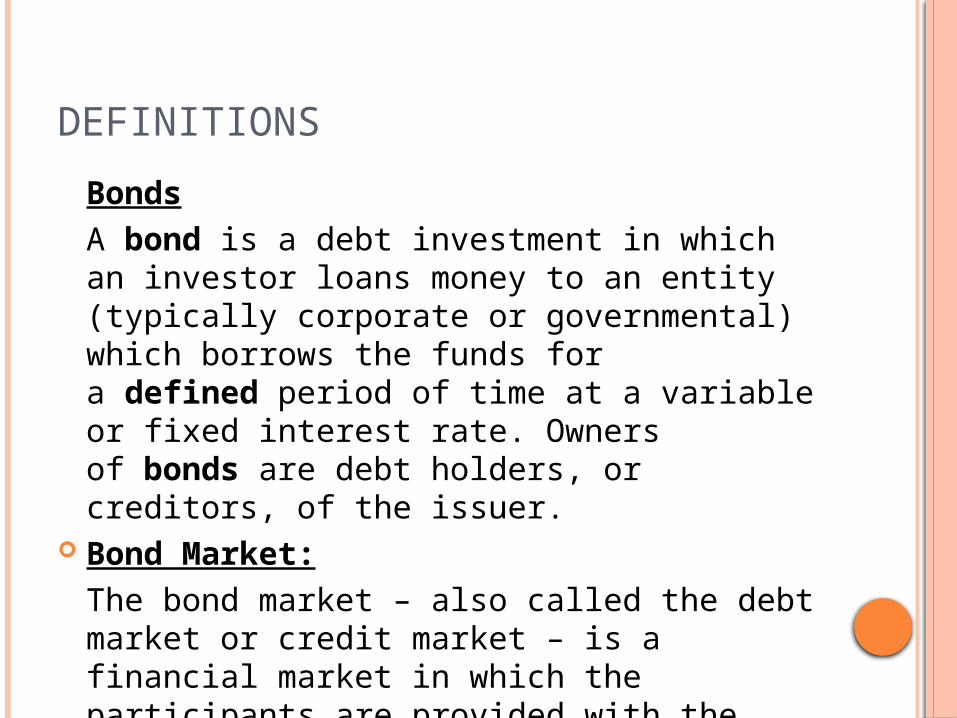

DEFINITIONSBondsA bond is a debt investment in which an investor loans money to an entity (typically corporate or governmental) which borrows the funds for a defined period of time at a variable or fixed interest rate. Owners of bonds are debt holders, or creditors, of the issuer.

Bond Market:The bond market – also called the debt market or credit market – is a financial market in which the participants are provided with the issuance and trading of debt securities.

DIMENSIONS OF BOND MARKETS

BUYERS-Companies-Government- Individuals

ISSUERS-Companies-Government

IMPORTANCE OF BOND MARKETSBUYERS ISSUERSSteady income Cost EffectiveSmall investors Competition to banksDiversification Alternative means of raising debt

capital

Central Banks issue bonds to:• develop infrastructure of the country

• Invest to earn return

• To monitor currency value

• to control money supply, and subsequently

• To control inflation

BENEFITS OF BOND MARKET ON ECONOMY

Avenue to investDirect competition to banksGood indicator of wider macro-

level signalsMoney supply is absorbedInflation is controlledImprovement in currencyForeign portfolio investment

NEED FOR DEBT MARKET Microeconomic Role

• Local Borrowing – Elimination of maturity mismatch

• Foreign Borrowing – Twin Mismatch (Maturity, FOREX Risk)• Facilitates Development of Risk

Management Instruments Macroeconomic Role

• Alternative Source of Borrowing• Credit Risk Dispersion• Risk – Possible Contagion Effect

TYPES OF BONDS2)Government bonds

• Pakistan Investment Bonds

• US Special Dollar Bonds

• WAPDA Bonds

• National Saving Bonds

• Sukuk

1)Corporate Bonds

Engro Bonds

HISTORY OF BOND MARKET IN PAKISTAN

1960 To cover non-banking segment, Prize Bonds were introduced followed by various NSS Schemes.

1990s Market based Government Securities came into existence.

1992 Introduction of long term paper (FIB).Long term yield curve emerged giving opportunity to the corporate to come up with instruments.

1995 Foundation of the corporate bond market was laid with the first issue of Term Final Certificates (TFC).

2000 Introduction of Pakistan Investment Bonds. (PIBs).

Long term instruments gained momentum.

SBP introduced selective Primary Dealer System (PD).

2001 KIBOR/KIBID rates were introduced to provide inter-bank call money curve.

2001-05 Corporate Bond market was vibrant, adding approximately PKR 65 Billion issuance or 98% of total issuance to date.

2005 SBP issued guidelines on Forward Rate Agreement (FRA), Interest Rate Swaps (IRS) and Currency Options.

2007 Introduction of Engro bonds of Rs 4 billion.

2008 Introduction of GoP Ijara Sukuk.

2009-10 The Government raised Rs. 64.31 billion, as against the target of Rs. 60 billion, through the auctions of Pakistan Investment Bonds (PIBs).

A total of four tranches of GoP Ijara Sukuk had been issued.

Bond Automated Trading System (BATS), a new debt market platform was introduced. It allows electronic order entry and matching facility, which will provide a more efficient and transparent way to trade debt market securities.

April 12, 2009 KSE and MUFAP joined hands for the development corporate debt marketTrading – KSE, Settlement – NCC, Custodian – CDCTFCs to be traded through BATS in the first phaseGovernment securities to be traded in the 2nd phase

2010-11 Development of an electronic fixed income trading platform provided by Bloomberg called E-BOND : Electronic Bond Trading Platform.

2012 According to SBP and SECP, the domestic bonds outstanding were 30 percent of the GDP, which mostly consisted of government bonds, as the corporate bonds market was less developed.

2014 Pakistani bonds revived investor interest Corporate market came under investors focus.

Pakistan rose $2 billion through Euro Bonds.

2015 Pakistan issued $500 million Euro Bonds.

October 2016 Pakistan rose $1 billion through Sukuk bonds.

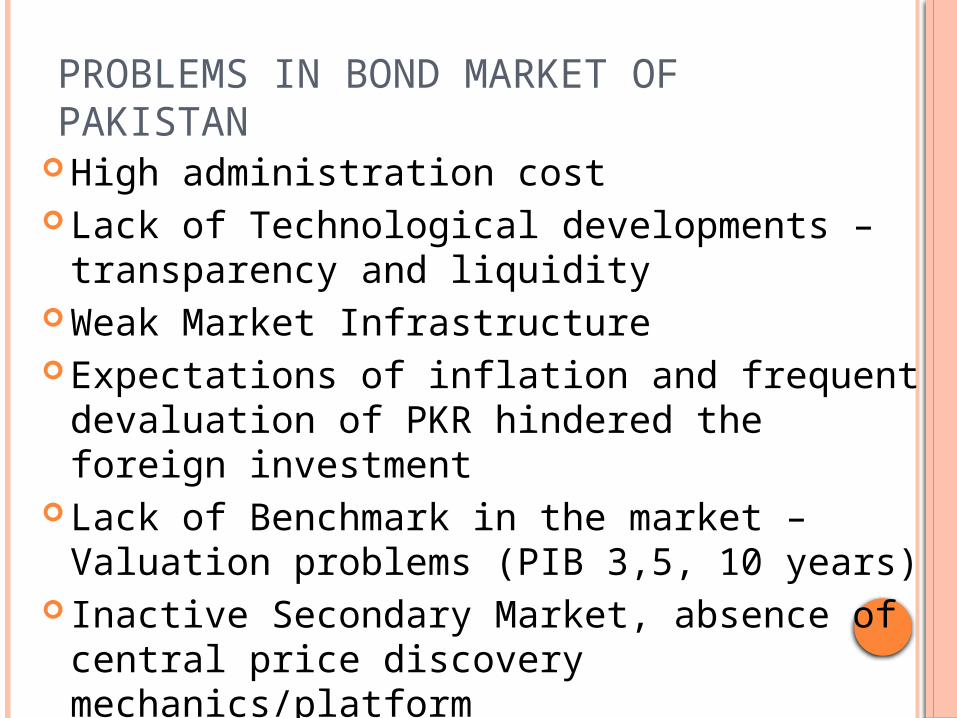

PROBLEMS IN BOND MARKET OF PAKISTAN

High administration cost Lack of Technological developments –

transparency and liquidity Weak Market Infrastructure Expectations of inflation and frequent

devaluation of PKR hindered the foreign investment

Lack of Benchmark in the market – Valuation problems (PIB 3,5, 10 years)

Inactive Secondary Market, absence of central price discovery mechanics/platform

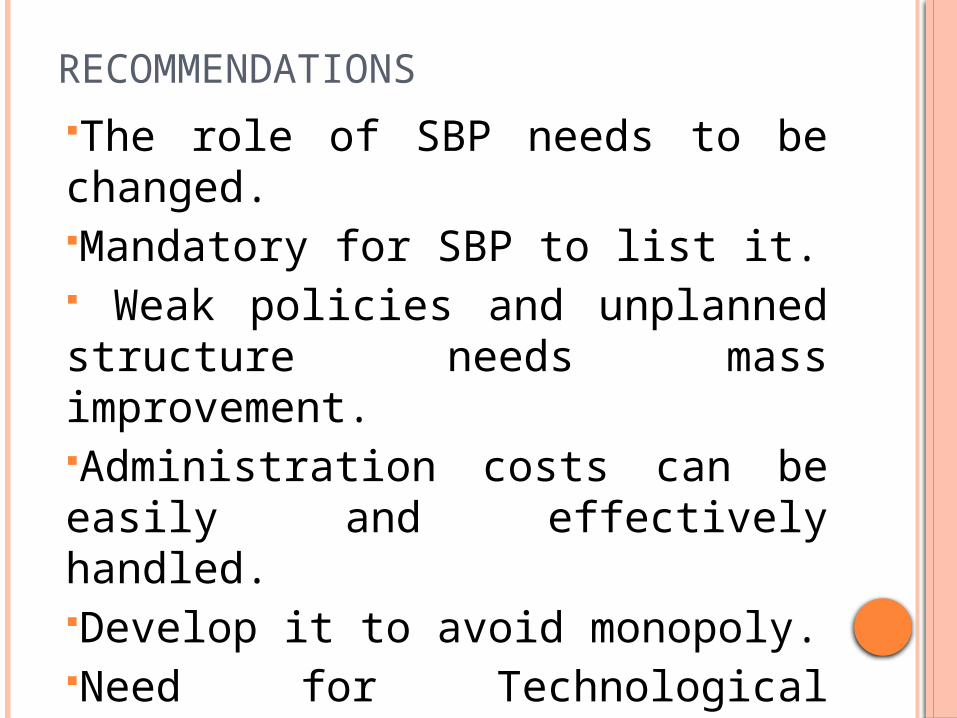

RECOMMENDATIONSThe role of SBP needs to be changed.Mandatory for SBP to list it. Weak policies and unplanned structure needs mass improvement.Administration costs can be easily and effectively handled.Develop it to avoid monopoly.Need for Technological developments – transparency and liquidity

LITERATURE REVIEW

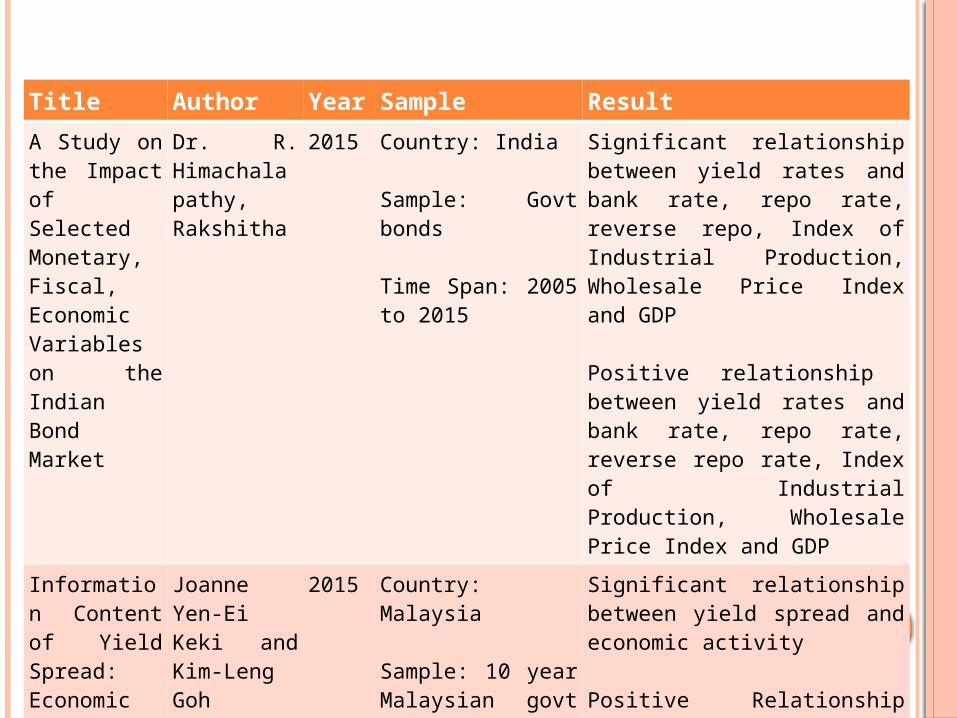

Title Author Year Sample ResultA Study on the Impact of Selected Monetary, Fiscal, Economic Variables on the Indian Bond Market

Dr. R. Himachalapathy, Rakshitha

2015 Country: India

Sample: Govt bonds

Time Span: 2005 to 2015

Significant relationship between yield rates and bank rate, repo rate, reverse repo, Index of Industrial Production, Wholesale Price Index and GDP

Positive relationship between yield rates and bank rate, repo rate, reverse repo rate, Index of Industrial Production, Wholesale Price Index and GDP

Information Content of Yield Spread: Economic Growth of Malaysia

Joanne Yen-Ei Keki and Kim-Leng Goh

2015 Country: Malaysia

Sample: 10 year Malaysian govt security and 3 month T-Bills

Time Span:1997 to 2012

Significant relationship between yield spread and economic activity

Positive Relationship between yield and economic factors

Title Author Year Sample ResultA Comparative Analysis of Returns of Various Financial Asset Classes in South Africa, A Triumph of Bonds

C. Auret and R. Vivian

2014 Country: South Africa

Sample: Equities, bonds and cash in South Africa

Time Span: 1986 to 2013

No significant relationship between the returns of equities over long bonds even before adjusting for risk

Exchange Rate Risk and Local Currency Sovereign Bond Yields in Emerging Markets

Blaise Gadanecz, Ken Miyajima, Chang Shu

2014 Country: 20 economies

Sample: 5 year local currency sovereign bonds of 20 economies

Time Span: 2005 to 2013

Significant relationship between exchange rate risk of emerging market economies and local currency sovereign bond yields

Positive relationship

Title Author Year Sample ResultThe Interest rate Effects on Government Debt Maturity

Jagjit S Chadha, Philip Turner and Zampolli

2013 Country: US

Sample: 5 & 10 year T-Bills

Time Span: 1976 to 2006

Significant relationship between dividend yield, CPI and GDP

Positive relationship

An Empirical Analysis of the Performance of the Ghana Stock Exchange and Treasury Bills

Samuel Antwi

2012 Country: Ghana

Sample: Annual returns of the Ghana Stock Exchange all-share index and Treasury bill

Time Span: 1990 to 2010

Significant relationship between risk and return of equity market and significant relationship between risk and return of debt market.

Positive relationship

Title Author Year Sample ResultThe Impact of Changes in Financial and Macroeconomics Variable on Term Structure of Interest Rates in Malaysia

Ong Tze San, Lai Yoke and Heng

2012 Country: Malaysia

Sample: One and 10 year Malaysian govt securities

Time Span:1997 to 2009

Money supply and current account have significant relationship on bond yield

Money supply has a positive relationship with bond yield, whereas current account has a negative relationship with bond yield

Fiscal Deficits, Public Debt, and Sovereign Bond Yields

Baldacci and Kumar

2010 Country: 31 advanced and emerging market economies

Sample: Fiscal deficit and government debt in 31 countries

Time Span: 1980 to 2008

Higher deficits and public debt lead to a significant increase in long-term interest rates

Positive relationship between large fiscal deficits and public debts and sovereign bond yields

Factors Influencing Yield Spreads of the Malaysian Bonds

Norliza Ahmad and Joriah Muhammad

2009 Country: Malaysia

Sample: Govt securities and corporate bonds

Time Span: 2001 to 2008

CPI and interest rates have a significant relationship with the yield spread of Malaysian Government Securities

Positive relationships

FACTORS IDENTIFIED THROUGH LITERATURE REVIEW

Risk

Interest Rate

Fiscal Deficit

Exchange Rate

GDP

METHODOLOGY

Interviews Literature Review

RESEARCH TECHNIQUE

QUALITATIVE

QUANTITATIVE

Regression of Bonds’ Data & External Factors’ data run on Stata

VARIABLES

PIB 3, 5 & 10 YEAR BONDSDEPENDENT VARIABLE

INDEPENDENT VARIABLES

Standard Deviation Interest Rate Fiscal Deficit Gross Domestic Product Exchange Rate

Reuters, World Bank & Pakistan Economic Survey

TIME PERIOD

2005 to 2015 (11 years)

DATA COLLECTION

REGRESSION MODELThe following regressions are performed in our

study-

Pooled Fixed Random

Four models are developed to check the relationship.

EQUATION Model (1 – All Bonds,

2 – Three Year PIBs 3 – Five Year PIBs 4 – Ten Year PIBs)

Bond Yields = f (Risk, fiscal deficit, interest rate, exchange rate, GDP)

OR

Y = βo + β1X1(Risk) + β2X2(Fiscal Deficit) + β3X3(GDP) +β4X4(Interest Rate) + β5X5(Exchange Rate)

There exists a Positive relationship between Risk and bond yield.

There exists a positive relationship between interest rate and bond yield.

There exists a negative relationship between exchange rate and bond yield.

There exists a negative relationship between GDP and bond yield.

There exists a positive relationship between fiscal deficit and bond yield.

Hypothesis

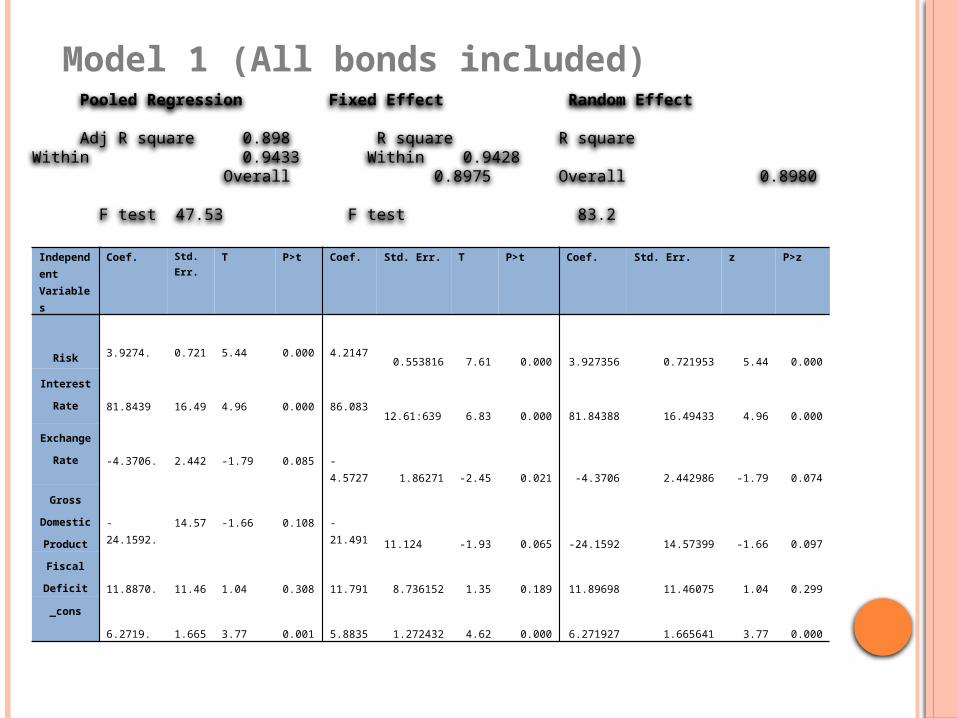

RESULTS

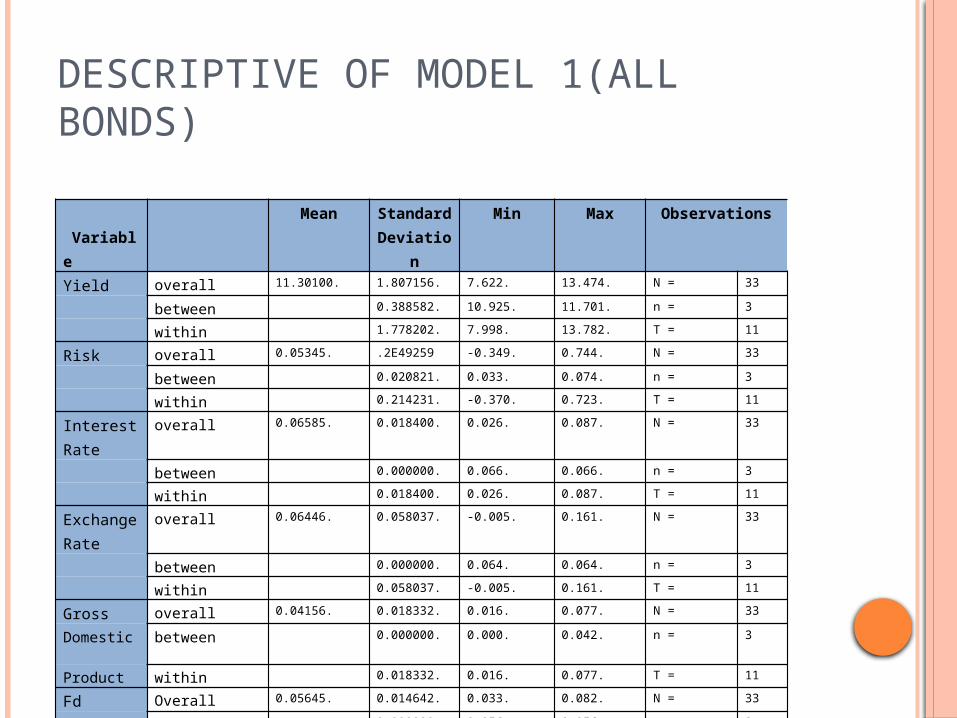

DESCRIPTIVE OF MODEL 1(ALL BONDS)

VariableMean Standard

DeviationMin Max Observations

Yield overall 11.30100. 1.807156. 7.622. 13.474. N = 33

between 0.388582. 10.925. 11.701. n = 3

within 1.778202. 7.998. 13.782. T = 11

Risk overall 0.05345. .2E49259 -0.349. 0.744. N = 33

between 0.020821. 0.033. 0.074. n = 3

within 0.214231. -0.370. 0.723. T = 11

Interest Rate

overall 0.06585. 0.018400. 0.026. 0.087. N = 33

between 0.000000. 0.066. 0.066. n = 3

within 0.018400. 0.026. 0.087. T = 11

Exchange Rate

overall 0.06446. 0.058037. -0.005. 0.161. N = 33

between 0.000000. 0.064. 0.064. n = 3

within 0.058037. -0.005. 0.161. T = 11

Gross overall 0.04156. 0.018332. 0.016. 0.077. N = 33

Domestic between 0.000000. 0.000. 0.042. n = 3

Product within 0.018332. 0.016. 0.077. T = 11

Fd Overall 0.05645. 0.014642. 0.033. 0.082. N = 33

between 0.000000. 0.056. 0.056. n = 3

within 0.014642. 0.033. 0.082. T = 11

Independent Variables

Coef. Std. Err.

T P>t Coef. Std. Err. T P>t Coef. Std. Err. z P>z

Risk 3.9274. 0.721 5.44 0.000 4.21470.553816 7.61 0.000 3.927356 0.721953 5.44 0.000

Interest

Rate 81.8439 16.49 4.96 0.000 86.08312.61:639 6.83 0.000 81.84388 16.49433 4.96 0.000

Exchange

Rate -4.3706. 2.442 -1.79 0.085 -4.57271.86271 -2.45 0.021 -4.3706 2.442986 -1.79 0.074

Gross

Domestic

Product-24.1592. 14.57 -1.66 0.108 -21.491

11.124 -1.93 0.065 -24.1592 14.57399 -1.66 0.097

Fiscal

Deficit 11.8870. 11.46 1.04 0.308 11.791 8.736152 1.35 0.189 11.89698 11.46075 1.04 0.299

_cons

6.2719. 1.665 3.77 0.001 5.8835 1.272432 4.62 0.000 6.271927 1.665641 3.77 0.000

Pooled Regression Fixed Effect Random Effect

Adj R square 0.898 R square R squareWithin 0.9433 Within 0.9428Overall 0.8975 Overall 0.8980

F test 47.53 F test 83.2

Model 1 (All bonds included)

MODEL 2 ( 3 YEAR PIB BOND)

Independent Variables

Coef. Std. Err. T P>t

Risk 4.1242. 1.015386 4.06 0.010

Gross Domestic Product

-32.7755. 24.33905 -1.35 0.236

Interest Rate 96.6465. 28.1523 3.43 0.019

Exchange Rate -6.3025. 4.282961 -1.47 0.201

Fiscal Deficit 7.7628. 19.86533 0.39 0.712

_cons 5.5210. 2.8443616 1.94 0.110

Pooled Regression

Adj R square 0.9502

F test 19.08

MODEL 3 ( 5 YEAR PIB BOND)

Independent Variables

Coef. Std. Err. T P>t

Risk 5.058. 0.8662832 5.84 0.002

Interest Rate 99.17184 - 18.60818 5.33 0.003

Exchange Rate-5.195. 2.655264

1.96 0.108

GDP-13.354. 16.17758

0.83 0.447

Fiscal Deficit 12.648. 12.40545 1.02 0.355

_cons 4.601.202 1.87641 2.45 0.058

Pooled Regression

Adj R square 0.9502

F test 19.08

MODEL 4 ( 10 YEAR PIB BOND)

Pooled Regression

Adj R square 0.9937

F test 316.78

Independent Variables

Coef. Std. Err. T P>t

Risk 6.327. 0.4194798 15.08 0.000

Gross Domestic Product

8.071. 6.068317 1.33 0.241

Interest Rate 98.758. 6.831279 14.46 0.000

Exchange Rate -3.417. 0.8774736 -3.89 0.011

Fiscal Deficit 11.578. 4.201141 2.76 0.040

_cons 4.187. 0.6747056 6.21 0.002

DISCUSSION

HYPOTHESIS: YIELD HAS A POSITIVE RELATIONSHIP WITH STANDARD DEVIATION (RISK)

Results shows that as risk increase return increase

Risk is a measure of volatility

Bonds with high volatility risk have higher yield Bonds with low volatility have lower yield

PIBS are sovereign bonds, it doesn’t have liquidity, default risk.

HYPOTHESIS: YIELD HAS A POSITIVE RELATIONSHIP WITH STANDARD DEVIATION (RISK)

PIBs have inflation risk and interest rate risk

Coupon payments are fixed it doesn’t increase with inflation

YIELD HAS A POSITIVE RELATIONSHIP WITH INTEREST RATE

Interest rate is an important factor and affects returns of all investments

Increase in interest rate increase a return on bonds

Bond yield is directly correlated with interest rate as interest rate increases bond yield increase and coupon payment on bonds increase.

As interest rate increases the prices of previously issued bond decrease as new bonds would offer higher yield.

HYPOTHESIS: YIELD HAS A NEGATIVE RELATIONSHIP WITH GDP

According to academic theories increase in GDP is due to increase total investment

It increases demand pull inflation

To overcome demand pull inflation government increases interest rate which increase bond yield.

In Pakistan bond yield and GDP have negative relationship

HYPOTHESIS: YIELD HAS A NEGATIVE RELATIONSHIP WITH GDP

Pakistan has done huge borrowings from IMF and is moving towards new era of growth due to CPEC.

Foreigners and locals are investing huge amount of money in mega projects

Government is decreasing interest rate to encourage investment and discourage fixed deposits

It gives incentive to companies to invest in business leading to increase in investment component leading in increase in GDP.

HYPOTHESIS: YIELD HAS A NEGATIVE RELATIONSHIP WITH EXCHANGE RATE

Pakistan has done huge borrowing from IMF and World

Bank to overcome its fiscal deficit

Under current IMF program Pakistan is forced to devalue its local currency and decrease its interest rate

It would increase money supply in an economy and discourage deposits in saving account to encourage investment in an economy

The purpose is to increase growth through investment

HYPOTHESIS: YIELD HAS A POSITIVE RELATIONSHIP WITH FISCAL DEFICIT

Bond Yield and fiscal deficit has positive relationship

Fiscal deficit increases ,yield increase.

In Pakistan government tries to fill a gap of fiscal deficit by issuing debts

Fiscal deficit increase government increase an interest rate

It attracts investors to buy the extra debt and limit the money supply in economy

HYPOTHESIS: YIELD HAS A POSITIVE RELATIONSHIP WITH FISCAL DEFICIT

Banks heavily invest in T-Bills and PIBS. Same was happening in 2008.

Creates “Crowding Out” effect by borrowing more money and leaves less money for private sector

Higher interest rates also can reduce the private sector's demand for capital

It reduce the demand for commercial and retail borrowing

SUMMARY OF RESULTS

Variables RelationshipRisk +Exchange Rate -Interest Rate +Fiscal Deficit +GDP -

LIMITATIONS OF THE STUDY Only 3, 5 and 10 year PIB Bonds are included

in the study

The Research is done only on Pakistani Bonds.

Only 11 years of data is has been included i.e. 2005 to 2015.

SUMMARY OF STOCK & BOND RESULTS

Variables Stocks Bonds

Risk + +

Exchange Rate - -

Inflation - Not Applicable

Foreign Direct Investment + Not Applicable

Interest Rate + +

Money Supple + Not Applicable

GDP + -

Fiscal Deficit +

INVESTOR’S MANUAL

KNOW WHAT INVESTMENT PRODUCTS ARE AVAILABLE:

Ordinary shares of listed companies Unit trust schemes Mutual funds certificates Corporate bonds i.e., Term Finance

Certificates (TFCs) Government securities i.e., Federal

Investment Bonds(FIBs), Pakistan Investment Bond (PIBs) Special US Dollar Bonds

STRATEGIES FOR INVESTMENT.

Top down Bottom up Value or growth Large or small cap Ethical investment and technical analysis

TIPS FOR INVESTING WISELY

When trading in the Stock Market, one should avoid: Greed Making the same mistake twice Following the crowd Putting all your ‘eggs in one basket’ Using rumors as tips Emotions; being emotional can effect

reasoning Traders should use research backed by

fundamental reasoning. Impatience Over borrowing

IMPORTANT CONSIDERATIONS FOR INVESTORS

How Much Money Can You Afford to Invest?

How Do You Want to Invest?

Questionnaire Analysis

RELIGION

59; 98%

1; 2%

Muslim Non Muslim

AGE

30%

22%13%

35%

Chart Title

<30 years 30-39 years 40-49 years 50 and above

QUALIFICATIONS

38%

23%

38%

Chart Title

University/College ProfessionalBoth University/Professional

YEARS WITH THE PRESENT ORGANIZATION

28%

25%15%

32%

Chart Title

0-1 years 1-5 year6-10 years more than 10 years

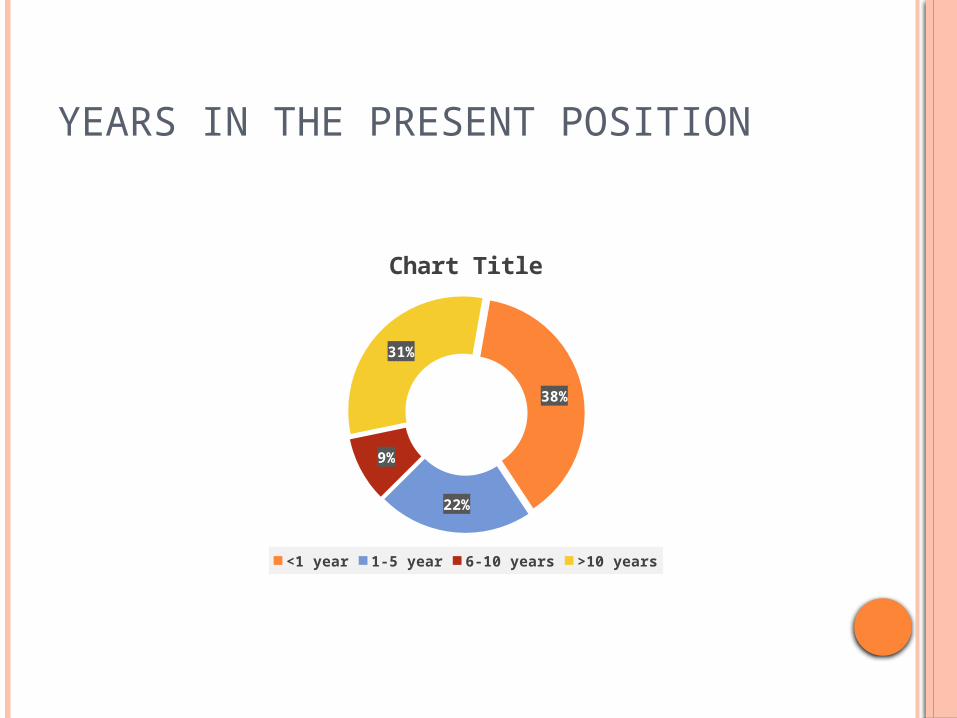

YEARS IN THE PRESENT POSITION

38%

22%

9%

31%

Chart Title

<1 year 1-5 year 6-10 years >10 years

INCOME

20%

37%

15%

28%

Chart Title

Less than 25K Between 25K and 100KBetween 100K and 200K More than 200K

PROFESSION

17%

17%

17%17%

17%

17%

Chart Title

Student Doctor BrokerTeacher Investor Other (Please Specify)

DO YOU KNOW ABOUT BOND MARKET?

78%

22%

Chart Title

Yes No

WHICH OF THE FOLLOWING TERMINOLOGIES DO YOU KNOW OF

44

20 2315

3929 32 29

3522

7 5

Chart Title

WHY DO YOU THINK PEOPLE INVEST IN BOND MARKET?

Low risk High returns For diversification Other (Please Specify)

44

7

31

5

Chart Title

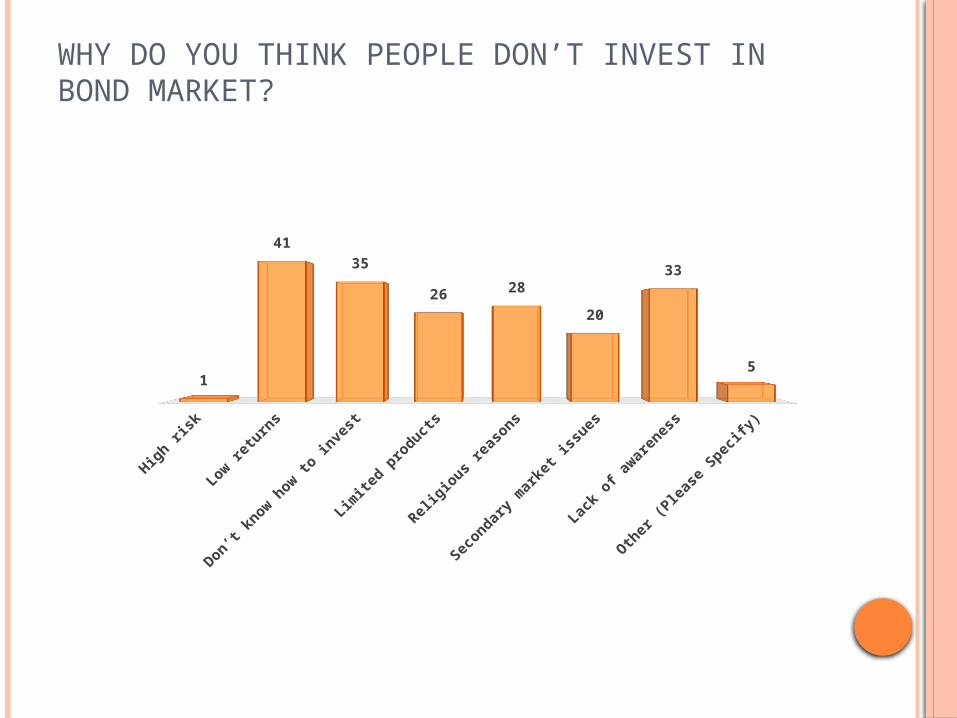

WHY DO YOU THINK PEOPLE DON’T INVEST IN BOND MARKET?

1

4135

26 2820

33

5

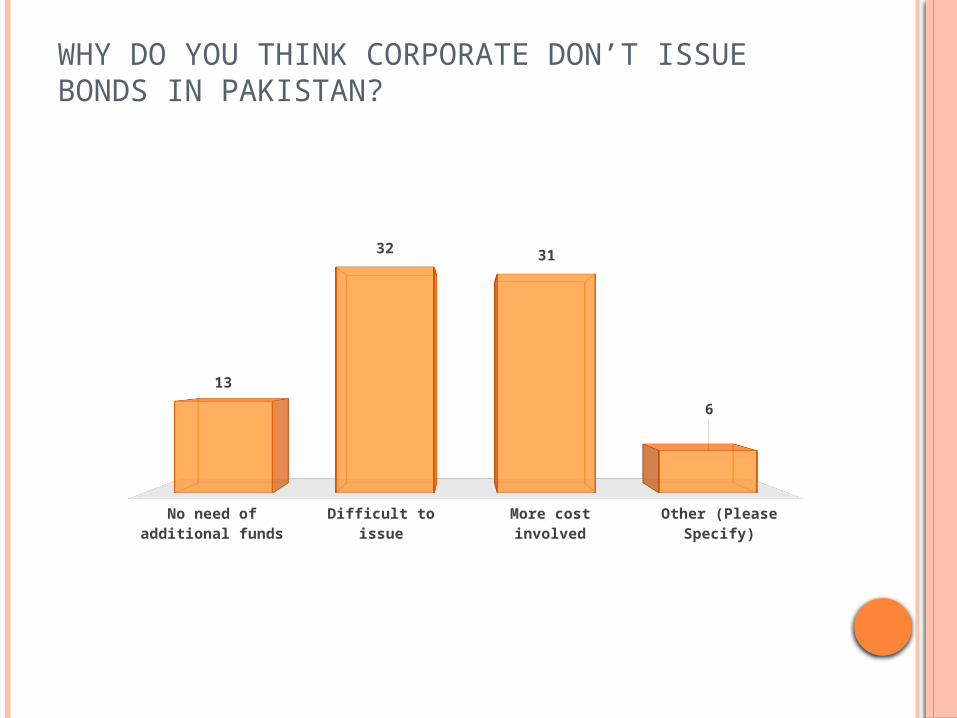

WHY DO YOU THINK CORPORATE DON’T ISSUE BONDS IN PAKISTAN?

No need of ad-ditional funds

Difficult to issue More cost involved Other (Please Specify)

13

32 31

6

DO YOU INVEST IN CAPITAL MARKETS?

40%60%

Chart Title

Yes No

HOW MANY TIMES DO YOU INVEST?

17%

67%

13% 4%

Chart Title

Daily Monthly Yearly Once in five years

IN WHICH SEGMENTS OF CAPITAL MARKET DO YOU INVEST?

Property Bond Market

Stock Market

Mutual Funds

Currency Other (Please Specify)

18

3

23

7

20

WHAT IS YOUR PORTFOLIO SIZE?

8%

17%

4%71%

Chart Title

Less than 100K Between 100K and 300KBetween 300K and 500K More than 500K

WHICH TYPE OF BONDS ARE YOU FAMILIAR WITH?

Government securities Corporate bonds

16

21

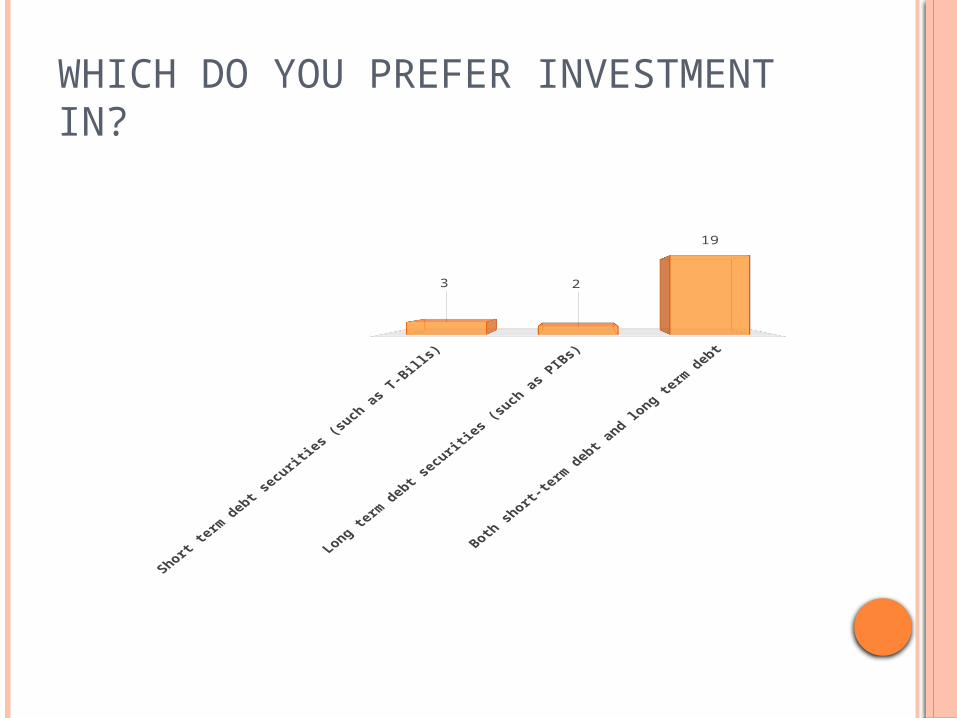

WHICH DO YOU PREFER INVESTMENT IN?

3 2

19

WHAT ARE BONDS MOST SUITABLE FOR?

13

68

0

ARE YOU AWARE OF THE PROCEDURE TO PURCHASE BONDS IN THE PAKISTAN MARKET?

33%

67%

Yes No

AMONG THE RISK-LESS FORMS OF INVESTMENTS (BANK DEPOSITS, NATIONAL SAVINGS CERTIFICATES), WHY DO YOU THINK THAT THE BOND MARKET IS THE LEAST DEVELOPED?

2217 19 18

0

IN YOUR OPINION, DOES BOND MARKET NEED FURTHER DEVELOPMENT BEFORE IT CAN START TO ATTRACT HIGH NET WORTH INVESTORS?

96%

4%

Chart Title

Yes No

WHAT MEASURES CAN BE TAKEN TO IMPROVE THE BOND MARKET IN PAKISTAN?

Majority said that the awareness is the key for improving the bond market

Another key factor would be proper regulatory body for maintaining transparency

WHY DO YOU THINK THERE IS A NEED FOR STRONG BOND MARKET?

Excess to extra funds for the issuer

Another investing option would be created for the investors

Bond markets are a source of funding

IF YOU CHOSE ‘BOND MARKET’, SPECIFY WHICH TYPE

Majority invested in government bonds as they are risk free in nature

Corporate bonds do not have much awareness

WHY DO YOU INVEST IN THE SEGMENTS WHICH YOU MARKED?

Majority responded higher returns being the most important reason for investing in any capital market

More then 80% of the respondents went with higher return being an important reason for the selection of their market

Other respondents also selected diversification as another reason for the selection of their capital market

WOULD YOU PREFER ALTERNATIVE FORMS OF INVESTMENTS OVER BONDS? SPECIFY THE REASON?

Majority of the respondents said they would prefer alternative forms of investments, specifically; mutual funds

Others preferred equity as it is more liquid

Lack of information about bonds was the reason of this preference

IN YOUR OPINION, SHOULD STEPS BE TAKEN TO INCREASE AWARENESS AMONG POTENTIAL BOND MARKET INVESTORS? IF YES, PLEASE SPECIFY THE STEPS

Majority said proper marketing campaigns should be introduced

Proper workshops should be held at institutes

Some suggested allocation of budget to regulatory bodies

THANK YOU!