risk based supervision under basel ii jeffrey carmichael cartagena february 16-18, 2004

TRANSCRIPT

Risk Based Supervision under Risk Based Supervision under Basel IIBasel II

Jeffrey CarmichaelJeffrey Carmichael

Cartagena

February 16-18, 2004

Presentation: Jeff CarmichaelColombia February 2004 Page 2

OutlineOutline

What is the risk based approach?How does it apply to banks?How does it apply to regulation?How does it apply to supervision?Challenges arising from Basel II

Presentation: Jeff CarmichaelColombia February 2004 Page 3

What is the Risk-Based Approach?What is the Risk-Based Approach?

• No universally-accepted definition• Meaning depends on the situation• Most widely accepted proposition would

be that a risk-based approach requires that you:

Identify risks and apply resources where the risks are greatest

Presentation: Jeff CarmichaelColombia February 2004 Page 4

1. How Does this Apply to Banking?1. How Does this Apply to Banking?

Major sources of banking risk:• Credit Risk• Market Risk• Liquidity Risk• Operational Risk

Question: Which is the greatest risk?

Presentation: Jeff CarmichaelColombia February 2004 Page 5

Experience Late 80s & Early 90sExperience Late 80s & Early 90s

• Widely agreed that credit risk is dominant - experience in the 80s/90s was good reminder

• Developed markets - worst loan losses for 50 years

• Common characteristics:

o excessive exposures to individual borrowerso excessive exposures to sectorso excessive reliance on collateralo poor credit evaluation

All arose primarily from credit risk

Presentation: Jeff CarmichaelColombia February 2004 Page 6

RMA & FMCG SurveyRMA & FMCG Survey

Better Credit Mgt. = Higher & More Stable Returns

Presentation: Jeff CarmichaelColombia February 2004 Page 7

Also Found ...Also Found ...

Payback to better risk management goes beyond protecting share price

Returns to investing in risk management are very high

• compared losses under best practice with cost of improvements - suggested return of 1,000% over 10 years

• helped better serve customer needs• enabled better business decisions

Presentation: Jeff CarmichaelColombia February 2004 Page 8

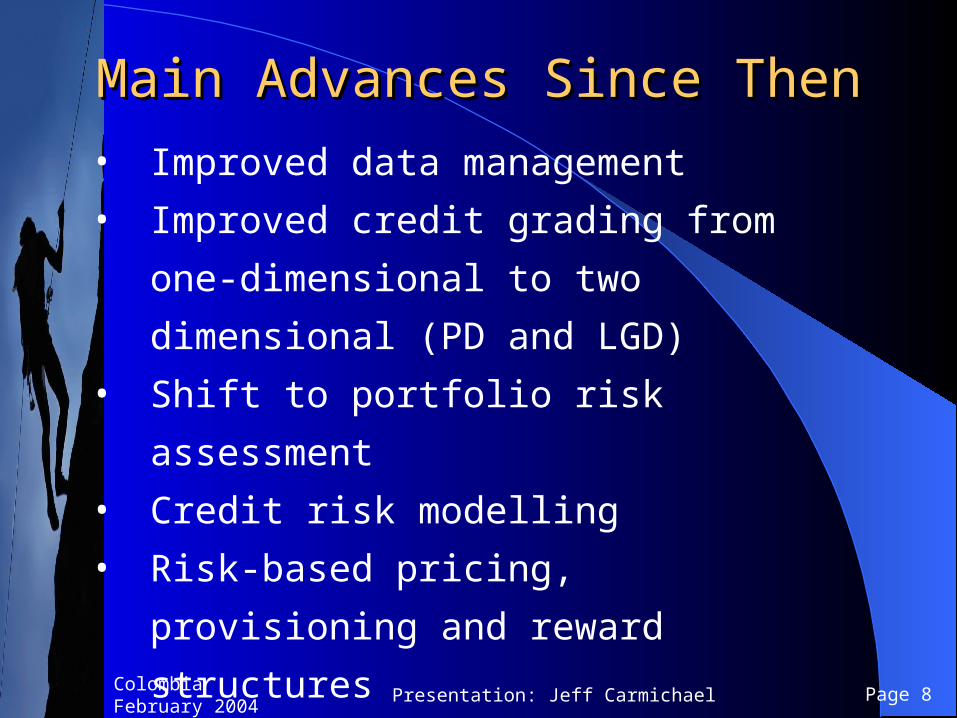

Main Advances Since ThenMain Advances Since Then

• Improved data management

• Improved credit grading from one-dimensional

to two dimensional (PD and LGD)

• Shift to portfolio risk assessment

• Credit risk modelling

• Risk-based pricing, provisioning and reward

structures

• Integrated risk management

• Risk-based capital allocation

Presentation: Jeff CarmichaelColombia February 2004 Page 9

Motivation for AdvancesMotivation for Advances

• Bankers remember the pain

• Shareholders react to differential losses

• Competition is increasing

• The tools are available

• There is more to lose (rewards are tied to performance)

Presentation: Jeff CarmichaelColombia February 2004 Page 10

2. “Risk-Based” Regulation2. “Risk-Based” Regulation

• The central Pillar of banking regulation is capital adequacy

• Starting with the first Capital Accord in 1988 banking regulators began imposing risk-weighted capital adequacy requirement

• The philosophy is straightforward - greater risk requires greater capital

Presentation: Jeff CarmichaelColombia February 2004 Page 11

Interaction Between Regulation Interaction Between Regulation and Banking Practiceand Banking Practice

• As noted - banks now allocate capital internally to activities and areas according to the risks taken

• Not widespread before the first Basel Accord in 1988• Accord encouraged banks to think in terms of risk-based

capital allocation• Since then, banks have generally gone well beyond the

1988 Accord - hence one of the primary motivations for Basel II …

• Case for change is in the divergence between regulatory capital and banks’ assessments of economic capital required for risk - illustration ….

Presentation: Jeff CarmichaelColombia February 2004 Page 12

Economic Vs Regulatory CapitalEconomic Vs Regulatory Capital

Basel I 8%

Economic

Presentation: Jeff CarmichaelColombia February 2004 Page 13

The Challenge for Basel IIThe Challenge for Basel II

Need for greater risk sensitivity than Basel 1 and its “one size fits all” Approach Need for a framework that is credible, sound and reflective of industry practices Need to be more incentive compatible with desire of regulators to promote and

enhance good credit risk management Problem - there is no standardized approach agreed by industry for the

measurement and management of credit risk (unlike market risk)

Presentation: Jeff CarmichaelColombia February 2004 Page 14

The OutcomeThe Outcome A “menu” approach:

– Standardized (modified from Basel I);– IRB Foundation– IRB Advanced

Standardized is still “blunt” like Basel I IRB approaches are an attempt to “approximate” what the industry is doing It stops short of allowing banks to use their own models entirely for assessing capital adequacy It allows banks to use some of the critical inputs to their models (PD, LGD, EAD) but constrains the way they are

combined to assess capital adequacy

Presentation: Jeff CarmichaelColombia February 2004 Page 15

3. “Risk-Based” Supervision3. “Risk-Based” Supervision

• Again the idea of a risk-based approach = apply resources where the risks are greatest

• Thus a supervisor following a risk-based approach will attempt to:

• Identify those banks in which risks are greatest

• Identify within each bank those areas in which risks are greatest

• Apply scarce supervisory resources so as to minimizing the overall “regulatory” risk

Presentation: Jeff CarmichaelColombia February 2004 Page 16

Risk Rating BanksRisk Rating Banks

• Most regulators use some form of rating system (e.g. CAMELS) for banks

• Following the experience of banks many have moved to a two-dimensional grading scale; e.g.

• PF - probability of failure

• CGF - (systemic) consequences given failure

Presentation: Jeff CarmichaelColombia February 2004 Page 17

Example - PAIRSExample - PAIRS

• APRA Reviewed developments in US, UK and Canada

• Developed PAIRS system (Probability and Impact Rating System)

• As in banking - risk grading system should not eliminate subjectivity but the discipline imposed by a structured approach should increase objectivity

• Back up with peer review and quality control

Presentation: Jeff CarmichaelColombia February 2004 Page 18

Conceptual Framework for PFConceptual Framework for PF

Inherent Risk

Management & Control

Capital Support

Risk of Failure PF__

Presentation: Jeff CarmichaelColombia February 2004 Page 19

The Structured ApproachThe Structured Approach• The Impact rating is based largely on size - with

some management over-ride if needed

• PF x Impact (CGF) = index of supervisory attention

• The Index of Supervisory Attention is exponential from 1 to 56,000

• The Index is grouped into:• Normal

• Oversight

• Mandated Improvement

• Restructure

Presentation: Jeff CarmichaelColombia February 2004 Page 20

Supervisory Attention GridSupervisory Attention Grid

'PAIRS' PROBABILITY RATING

LOW MEDIUM HIGH EXTREMEI low highM MANDATED

P EXTREME NORMAL OVERSIGHT IMPROVEMENT RESTRUCTURE RESTRUCTURE

AP C MANDATED

A T HIGH NORMAL OVERSIGHT IMPROVEMENT RESTRUCTURE

IR R MANDATED

S A MEDIUM NORMAL NORMAL OVERSIGHT IMPROVEMENT RESTRUCTURE

T

I MANDATED

N LOW NORMAL NORMAL IMPROVEMENT RESTRUCTURE

G

Presentation: Jeff CarmichaelColombia February 2004 Page 21

Beyond Risk GradingBeyond Risk Grading

• Risk-based supervision requires better risk grading to identify the institutions posing the greatest risks

• It also requires targeted inspections and investigations

• It requires judgement and graduated supervisory responses

• This is where Basel II has focused its attention through Pillar 2

Presentation: Jeff CarmichaelColombia February 2004 Page 22

Pillar 2 - Supervisory ReviewPillar 2 - Supervisory Review

Philosophy:

1. Pillar 1 Capital Framework is only an approximation - it is not entirely comprehensive

2. Capital is critical in mitigating risk but it is not the only relevant factor - a bank should have sound processes and procedures for measuring, monitoring and managing risk

Presentation: Jeff CarmichaelColombia February 2004 Page 23

Supervisory Review ProcessSupervisory Review Process

• Use tools available to assess how accurately Pillar 1 matches minimum capital with risks taken by the bank

• Use tools available to understand how strong a bank’s processes & procedures are and how well they are implemented

• Use supervisory judgement to impose additional supervisory requirements (including capital) where residual risk is excessive

Presentation: Jeff CarmichaelColombia February 2004 Page 24

Assessing the Adequacy of a Bank’s Assessing the Adequacy of a Bank’s CapitalCapital

• Principle 1: Banks should have a process for assessing capital relative to risks and a strategy for maintaining it

• Supervisors:

• Review the risk assessment processes for relevance and comprehensiveness - does the bank recognise other risks such as interest rate risk?

• Identify inconsistencies• Check that management is engaged• Assess application and controls - are processes

followed?• Require stress tests

Presentation: Jeff CarmichaelColombia February 2004 Page 25

Specific Guidance Specific Guidance

• Interest Rate Risk in the banking book

• Operational Risk

• Definition of default

• Risk mitigation

• Concentration Risk

• Securitization

Presentation: Jeff CarmichaelColombia February 2004 Page 26

Demands Related to IRBDemands Related to IRB

• Banks that choose IRB need to meet a series of demanding qualifying and validation criteria

• These have been set out in detail by the Basel Committee - along with guidance about what and how to check

• The on-going monitoring of the appropriateness and application of these model-based risk management processes is a fundamental part of Pillar 2 supervisory review - especially stress testing

Presentation: Jeff CarmichaelColombia February 2004 Page 27

Responding to Assessed RisksResponding to Assessed Risks

• Principle 2: Supervisors should take enforcement action if not satisfied with a bank’s approach to risk management

• Principle 3: Supervisors should expect banks to hold above the minimum and should be able to require them to do so

• Principle 4: Supervisors should intervene early to prevent capital falling through the minimum

Presentation: Jeff CarmichaelColombia February 2004 Page 28

Is Pillar 2 Really Anything New?Is Pillar 2 Really Anything New?• To the extent that Pillar 2 emphasises:

• Assessment of risks

• Supervisory judgement & discretion

• Active enforcement

• It is just an extension of the already growing risk-based approach to supervision

• It does provide detailed guidance - but many countries already exercised this type of approach

• Problem was - not all countries could!

• Pillar 2 formalises the central role of flexibility

• Without that flexibility Basel II is a waste of time

Presentation: Jeff CarmichaelColombia February 2004 Page 29

SummarySummary• The “risk-based” approach is about identifying risks and

devoting resources to where they will be most effective in reducing risks

• This approach is as critical in banking as it is in regulation and supervision

• In regulation it requires that capital requirements are greater where risks are greater

• In supervision it requires supervisors to:

• Assess where the risks are greatest

• Intervene and enforce standards flexibly where the risks are greatest

• Pillar 2 of Basel II provides a framework for the assessment and intervention process

• Pillar 2 is a fundamental component of Basel II

Presentation: Jeff CarmichaelColombia February 2004 Page 30

Thank YouThank You

Risk-Based Supervision: Risk-Based Supervision: Challenges under Basel IIChallenges under Basel II

ARMICHAEL ONSULTING Pty Ltd