review of shareholder activism - q1 2020 - lazard...companies have taken in response to the...

TRANSCRIPT

Review of Shareholder Activism - Q1 2020

L A Z A R D ' S S H A R E H O L D E R A D V I S O R Y G R O U P

A P R I L 2 0 2 0

Lazard has prepared the information herein based upon publicly available

information and for general informational purposes only. The information is not

intended to be, and should not be construed as, financial, legal or other advice,

and Lazard shall have no duties or obligations to you in respect of the information.

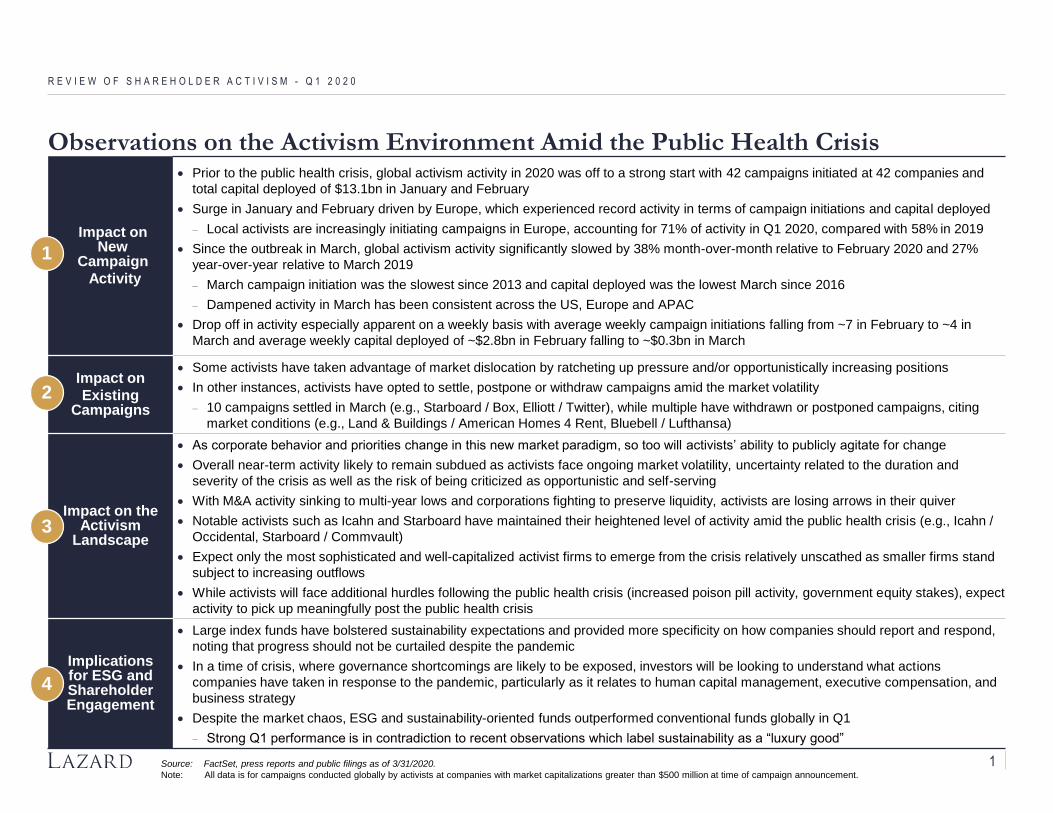

Observations on the Activism Environment Amid the Public Health Crisis

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Source: FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement.

Impact on New

Campaign

Activity

• Prior to the public health crisis, global activism activity in 2020 was off to a strong start with 42 campaigns initiated at 42 companies and

total capital deployed of $13.1bn in January and February

• Surge in January and February driven by Europe, which experienced record activity in terms of campaign initiations and capital deployed

− Local activists are increasingly initiating campaigns in Europe, accounting for 71% of activity in Q1 2020, compared with 58% in 2019

• Since the outbreak in March, global activism activity significantly slowed by 38% month-over-month relative to February 2020 and 27%

year-over-year relative to March 2019

− March campaign initiation was the slowest since 2013 and capital deployed was the lowest March since 2016

− Dampened activity in March has been consistent across the US, Europe and APAC

• Drop off in activity especially apparent on a weekly basis with average weekly campaign initiations falling from ~7 in February to ~4 in

March and average weekly capital deployed of ~$2.8bn in February falling to ~$0.3bn in March

Impact on

Existing Campaigns

• Some activists have taken advantage of market dislocation by ratcheting up pressure and/or opportunistically increasing positions

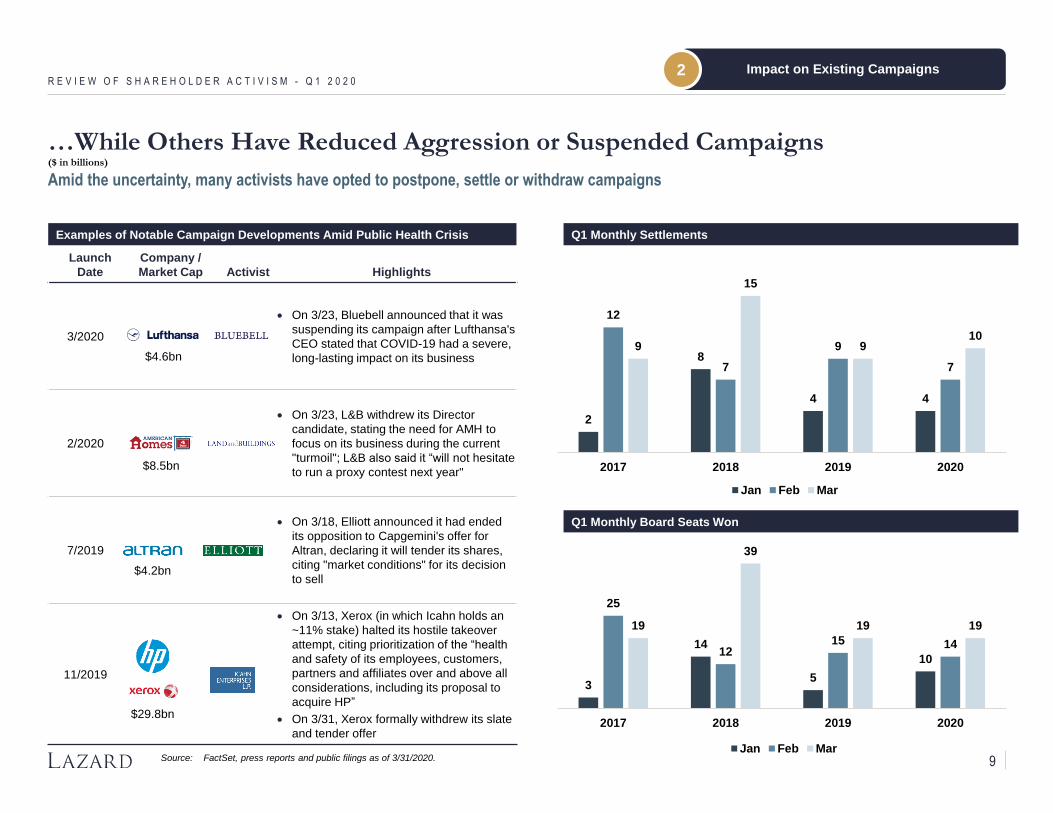

• In other instances, activists have opted to settle, postpone or withdraw campaigns amid the market volatility

− 10 campaigns settled in March (e.g., Starboard / Box, Elliott / Twitter), while multiple have withdrawn or postponed campaigns, citing

market conditions (e.g., Land & Buildings / American Homes 4 Rent, Bluebell / Lufthansa)

Impact on the Activism

Landscape

• As corporate behavior and priorities change in this new market paradigm, so too will activists’ ability to publicly agitate for change

• Overall near-term activity likely to remain subdued as activists face ongoing market volatility, uncertainty related to the duration and

severity of the crisis as well as the risk of being criticized as opportunistic and self-serving

• With M&A activity sinking to multi-year lows and corporations fighting to preserve liquidity, activists are losing arrows in their quiver

• Notable activists such as Icahn and Starboard have maintained their heightened level of activity amid the public health crisis (e.g., Icahn /

Occidental, Starboard / Commvault)

• Expect only the most sophisticated and well-capitalized activist firms to emerge from the crisis relatively unscathed as smaller firms stand

subject to increasing outflows

• While activists will face additional hurdles following the public health crisis (increased poison pill activity, government equity stakes), expect

activity to pick up meaningfully post the public health crisis

Implications for ESG and Shareholder Engagement

• Large index funds have bolstered sustainability expectations and provided more specificity on how companies should report and respond,

noting that progress should not be curtailed despite the pandemic

• In a time of crisis, where governance shortcomings are likely to be exposed, investors will be looking to understand what actions

companies have taken in response to the pandemic, particularly as it relates to human capital management, executive compensation, and

business strategy

• Despite the market chaos, ESG and sustainability-oriented funds outperformed conventional funds globally in Q1

− Strong Q1 performance is in contradiction to recent observations which label sustainability as a “luxury good”

1

2

3

4

1

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Source: FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement.

1 Companies spun off as part of campaign process counted separately.

2 Calculated as of campaign announcement date. Does not include derivative positions.

3 4-year average based on aggregate value of activist positions.

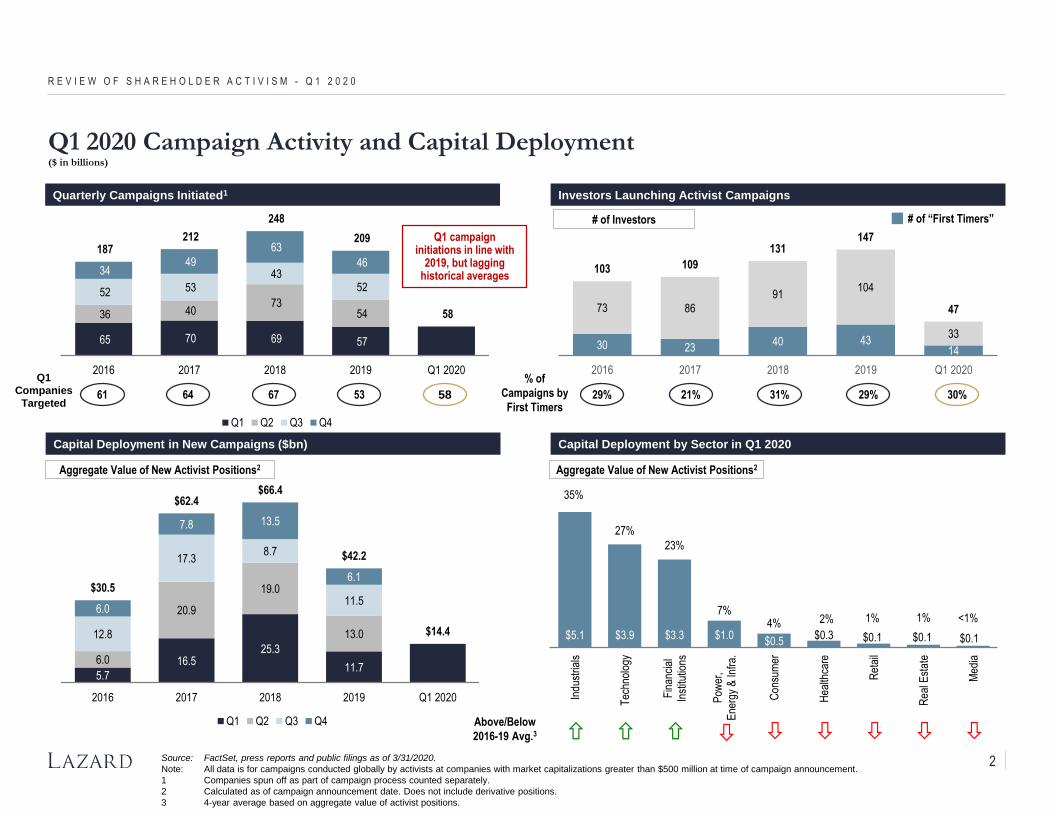

Quarterly Campaigns Initiated1

Aggregate Value of New Activist Positions2

Capital Deployment by Sector in Q1 2020

Aggregate Value of New Activist Positions2

65 70 69 57

36 40 73

54

52 53 43

52

34 49

63

46 187

212

248

209

58

2016 2017 2018 2019 Q1 2020

Q1 Q2 Q3 Q4

5.7

16.525.3

11.76.0

20.9

19.0

13.012.8

17.38.7

11.56.0

7.8 13.5

6.1$30.5

$62.4 $66.4

$42.2

$14.4

2016 2017 2018 2019 Q1 2020

Q1 Q2 Q3 Q4

$5.1 $3.9 $3.3 $1.0$0.5

$0.3 $0.1 $0.1 $0.1

35%

27%

23%

7% 4% 2% 1% 1% <1%

Indu

stria

ls

Tec

hnol

ogy

Fin

anci

alIn

stitu

tions

Pow

er,

Ene

rgy

& In

fra.

Con

sum

er

Hea

lthca

re

Ret

ail

Rea

l Est

ate

Med

ia

Q1 2020 Campaign Activity and Capital Deployment($ in billions)

Above/Below

2016-19 Avg.3

Capital Deployment in New Campaigns ($bn)

64

Q1

Companies

Targeted6761 5853

Investors Launching Activist Campaigns

30 2340 43

14

73 86

91104

33

103 109

131147

47

2016 2017 2018 2019 Q1 2020% of

Campaigns by

First Timers

# of “First Timers”# of Investors

29% 21% 31% 30%29%

Q1 campaign initiations in line with

2019, but lagging historical averages

2

39 28 36 28 14

106

75

125

94

29

145

103

161

122

43

27% 27% 22% 23% 33%

2016 2017 2018 2019 Q1 2020

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

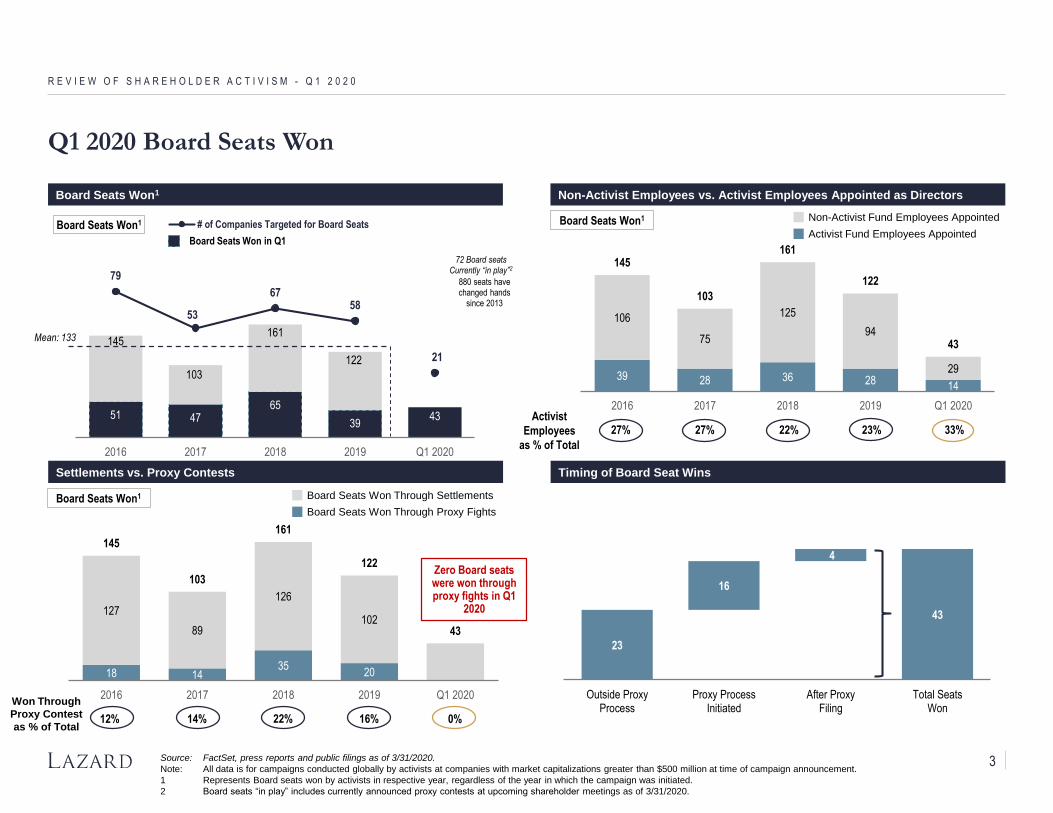

Board Seats Won1 Non-Activist Employees vs. Activist Employees Appointed as Directors

Settlements vs. Proxy Contests Timing of Board Seat Wins

Source: FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement.

1 Represents Board seats won by activists in respective year, regardless of the year in which the campaign was initiated.

2 Board seats “in play” includes currently announced proxy contests at upcoming shareholder meetings as of 3/31/2020.

Activist

Employees

as % of Total

Board Seats Won1 Non-Activist Fund Employees Appointed

Activist Fund Employees Appointed

Board Seats Won1 Board Seats Won Through Settlements

Board Seats Won Through Proxy Fights

51 4765

39

145

103

161

122

43

79

53

6758

21

72 Board seatsCurrently “in play”2

880 seats have changed hands

since 2013

2016 2017 2018 2019 Q1 2020

# of Companies Targeted for Board SeatsBoard Seats Won1

Mean: 133

Board Seats Won in Q1

18 1435

20

0

127

89

126

102

145

103

161

122

43

12% 14% 22% 16% 0%

2016 2017 2018 2019 Q1 2020Won Through

Proxy Contest

as % of Total

Q1 2020 Board Seats Won

43

23

16

4

Outside ProxyProcess

Proxy ProcessInitiated

After ProxyFiling

Total SeatsWon

Zero Board seats were won through proxy fights in Q1

2020

3

18

25

30

17 16

28

2113

18

26

46 46

43

35

42

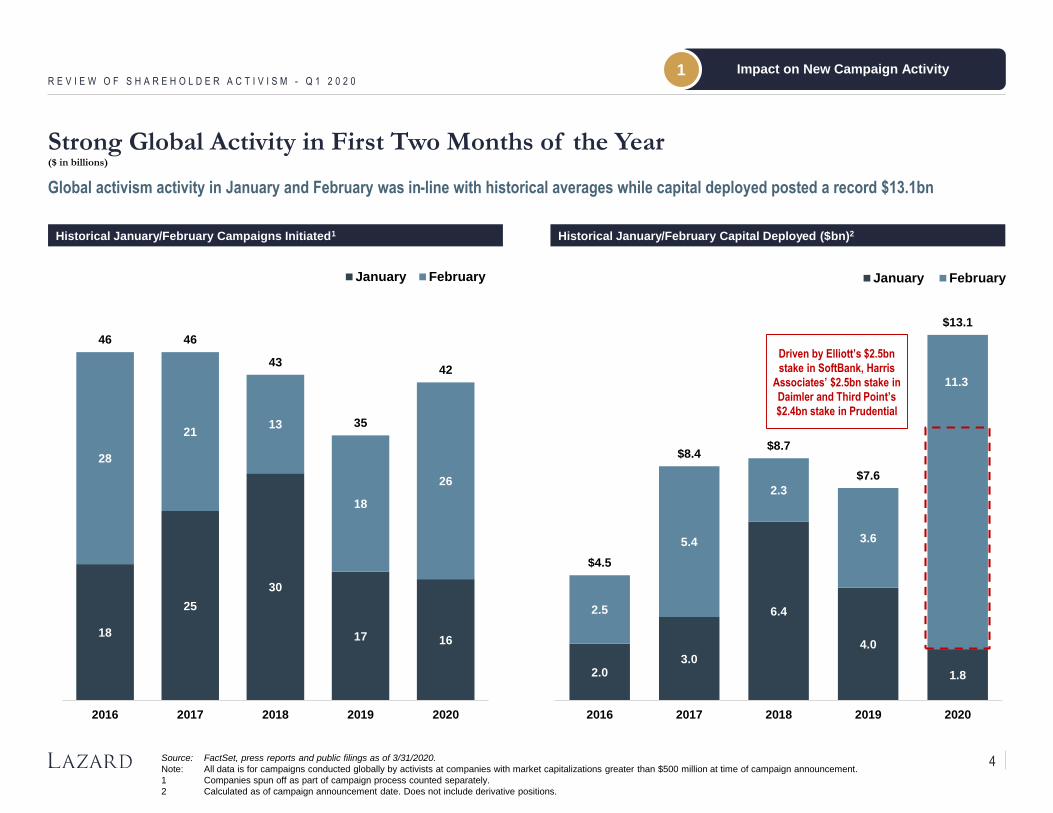

2016 2017 2018 2019 2020

January February

2.03.0

6.4

4.0

1.8

2.5

5.4

2.3

3.6

11.3

$4.5

$8.4$8.7

$7.6

$13.1

2016 2017 2018 2019 2020

January February

Strong Global Activity in First Two Months of the Year($ in billions)

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Global activism activity in January and February was in-line with historical averages while capital deployed posted a record $13.1bn

Historical January/February Capital Deployed ($bn)2Historical January/February Campaigns Initiated1

Source: FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement.

1 Companies spun off as part of campaign process counted separately.

2 Calculated as of campaign announcement date. Does not include derivative positions.

Driven by Elliott’s $2.5bn

stake in SoftBank, Harris

Associates’ $2.5bn stake in

Daimler and Third Point’s

$2.4bn stake in Prudential

Impact on New Campaign Activity1

4

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Strong January and February Activity in Europe($ in billions)

Source: FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted at companies with market capitalizations greater than $500 million at time of campaign announcement.

1.3

3.1

4.9

3.9

0.9

$9.2

$6.5

2019 Q1 2020

Q1

Rest of the Year 14

16 16

9

21

8

11

15

10

14

15

9

21

4

10

17

8

14

2016 2017 2018 2019 2020

Average Q1 initiations

16 out of 21 campaigns took place before COVID-

19 market downturn

Impact on New Campaign Activity1

Europe witnessed a historic number of campaigns in the beginning of 2020

During Q1, activists deployed ~70% of the amount of capital deployed in all of 2019

2020 Q1 saw an acceleration of campaigns leveling up to historic highs, with the UK and Germany representing

more than 57% of campaigns

Capital Deployment in New Campaigns in Europe ($bn) Quarterly Campaigns Initiated in Europe

Harris Associates’ $2.5bn

stake in Daimler and Third

Point’s $2.4bn stake in

Prudential accounts for

$4.9bn out of $6.5bn

Q4

Q3

Q2

Q1

5

Q4

Q3

Q2

Q1

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

In Europe, U.S. Agitators Remain the Main Players but are Joined by Local Players

Source: FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted at companies with market capitalizations greater than $500 million at time of campaign announcement.

Activists # Campaigns

2

2

• Despite the success of many U.S. activists, Europe has continued to attract

new European players

• Several players became more vocal and visible in the European landscape,

competing with global players

Q1 2020

U.S Agitators are Outnumbered by Local Players…

Most Prolific European Activists

Activists # Campaigns

6

2

2

2

20192018

Activists # Campaigns

3

3

2

2

47%27

58%28

71%15

2%1

51%29

42%20

29%6

57

48

21

2018

2019

Q1 2020

Campaigns launched by European activists Campaigns launched by others

Campaigns launched by U.S. activists

• During the first quarter, U.S. agitators deployed ~$5.5bn in new campaigns

• Elliott remains “the most active activist” in Europe. The fund has launched

the most new campaigns in Europe so far this year, even if those

investments are generally smaller compared to other Elliott holdings

… but Continue to Lead the Effort

U.S. Agitators’ 2020 European campaigns

$0.2bn

$0.4bn

Rumored

$ Investment size

$2.4bn

$2.5bn

<$0.1bn

Impact on New Campaign Activity1

6

7 810

610

8

2

6

5

11

52

6

34

3

12

1

2

213

20

13

16

26

16

October November December January February March

Activism Campaigns Slowed Substanially in March($ in billions)

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Campaign Initiations in Last Six Months1

Source: FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement.

1 Companies spun off as part of campaign process counted separately.

2 Calculated as of campaign announcement date. Does not include derivative positions. Excludes positions not publicly disclosed.

Impact on New Campaign Activity1

0.71.7

0.5 1.12.7

0.70.2

0.7

0.3

5.9

0.4

1.5

0.30.4

2.5

0.20.30.1

0.2

$1.3

$3.9

$0.9

$1.8

$11.3

$1.3

October November December January February March

Capital Deployed in Last Six Months ($bn)2

Q1 Campaign Initiations by Week1 Q1 Capital Deployed by Week ($bn)2

United States Europe APAC Rest of World United States Europe APAC Rest of World

Week

Ended:Week

Ended:

2

45 5

7

5 5

9

23

5

2

4

1/10 1/17 1/24 1/31 2/7 2/14 2/21 2/28 3/6 3/13 3/20 3/27 4/3

Campaigns Initiated 4 Week Rolling Average

$0.0$0.4

$1.1

$0.4

$3.1

$0.3

$3.1

$4.8

$0.1 $0.1$0.3

$0.1

$0.7

1/10 1/17 1/24 1/31 2/7 2/14 2/21 2/28 3/6 3/13 3/20 3/27 4/3

Capital Deployed 4 Week Rolling Average

2

7

In March, campaign initiations dropped by 38% and weekly capital deployed decreased from ~$2.8bn to ~$0.3bn, compared with February

Launch

Date

Company /

Market Cap Activist Highlights

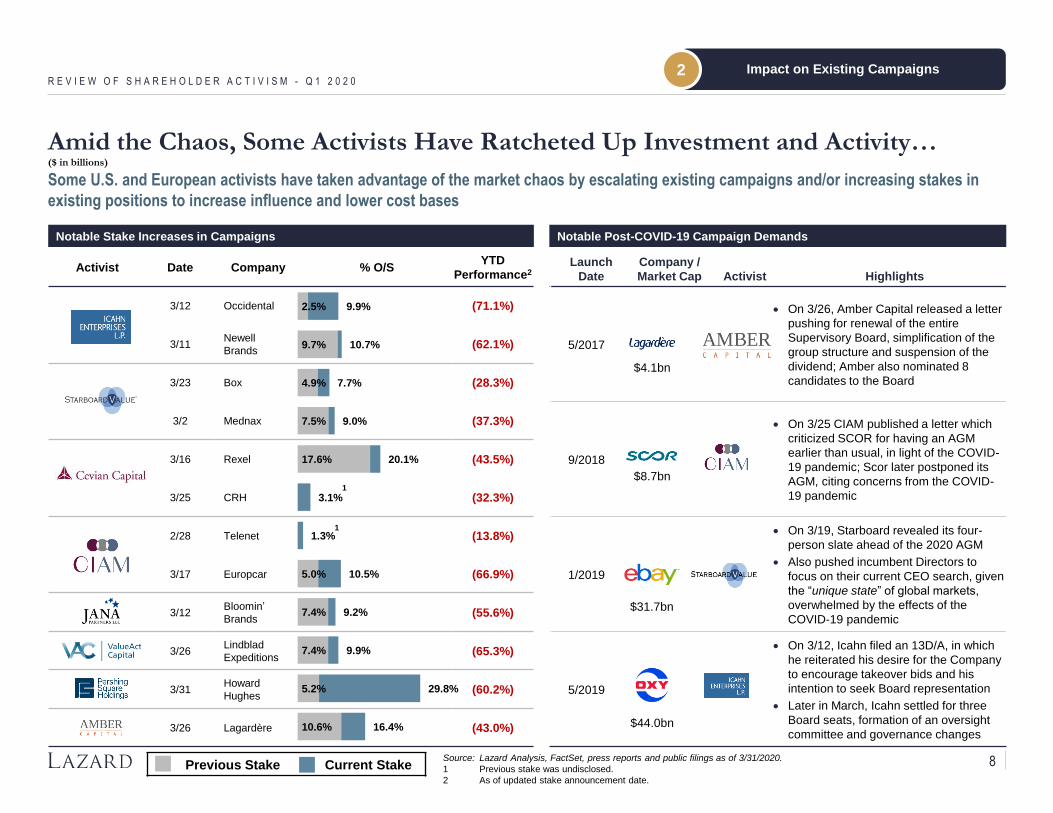

5/2017

• On 3/26, Amber Capital released a letter

pushing for renewal of the entire

Supervisory Board, simplification of the

group structure and suspension of the

dividend; Amber also nominated 8

candidates to the Board

9/2018

• On 3/25 CIAM published a letter which

criticized SCOR for having an AGM

earlier than usual, in light of the COVID-

19 pandemic; Scor later postponed its

AGM, citing concerns from the COVID-

19 pandemic

1/2019

• On 3/19, Starboard revealed its four-

person slate ahead of the 2020 AGM

• Also pushed incumbent Directors to

focus on their current CEO search, given

the “unique state” of global markets,

overwhelmed by the effects of the

COVID-19 pandemic

5/2019

• On 3/12, Icahn filed an 13D/A, in which

he reiterated his desire for the Company

to encourage takeover bids and his

intention to seek Board representation

• Later in March, Icahn settled for three

Board seats, formation of an oversight

committee and governance changes

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Source: Lazard Analysis, FactSet, press reports and public filings as of 3/31/2020.

1 Previous stake was undisclosed.

2 As of updated stake announcement date.

Amid the Chaos, Some Activists Have Ratcheted Up Investment and Activity…($ in billions)

Notable Stake Increases in Campaigns

Previous Stake Current Stake

Some U.S. and European activists have taken advantage of the market chaos by escalating existing campaigns and/or increasing stakes in

existing positions to increase influence and lower cost bases

$44.0bn

$8.7bn

$31.7bn

Notable Post-COVID-19 Campaign Demands

Impact on Existing Campaigns2

$4.1bn

1

1

Activist Date Company % O/SYTD

Performance2

3/12 Occidental (71.1%)

3/11Newell

Brands(62.1%)

3/23 Box (28.3%)

3/2 Mednax (37.3%)

3/16 Rexel (43.5%)

3/25 CRH (32.3%)

2/28 Telenet (13.8%)

3/17 Europcar (66.9%)

3/12Bloomin’

Brands(55.6%)

3/26Lindblad

Expeditions(65.3%)

3/31Howard

Hughes (60.2%)

3/26 Lagardère (43.0%)10.6%

5.2%

7.4%

7.4%

5.0%

17.6%

7.5%

4.9%

9.7%

2.5%

16.4%

29.8%

9.9%

9.2%

10.5%

1.3%

3.1%

20.1%

9.0%

7.7%

10.7%

9.9%

8

…While Others Have Reduced Aggression or Suspended Campaigns($ in billions)

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Launch

Date

Company /

Market Cap Activist Highlights

3/2020

• On 3/23, Bluebell announced that it was

suspending its campaign after Lufthansa's

CEO stated that COVID-19 had a severe,

long-lasting impact on its business

2/2020

• On 3/23, L&B withdrew its Director

candidate, stating the need for AMH to

focus on its business during the current

"turmoil"; L&B also said it “will not hesitate

to run a proxy contest next year"

7/2019

• On 3/18, Elliott announced it had ended

its opposition to Capgemini's offer for

Altran, declaring it will tender its shares,

citing "market conditions" for its decision

to sell

11/2019

• On 3/13, Xerox (in which Icahn holds an

~11% stake) halted its hostile takeover

attempt, citing prioritization of the “health

and safety of its employees, customers,

partners and affiliates over and above all

considerations, including its proposal to

acquire HP”

• On 3/31, Xerox formally withdrew its slate

and tender offer

$8.5bn

$4.6bn

$29.8bn

$4.2bn

Source: FactSet, press reports and public filings as of 3/31/2020.

Amid the uncertainty, many activists have opted to postpone, settle or withdraw campaigns

Q1 Monthly Settlements

2

8

4 4

12

7

9

7

9

15

910

2017 2018 2019 2020

Jan Feb Mar

3

14

5

10

25

1215 14

19

39

19 19

2017 2018 2019 2020

Jan Feb Mar

Q1 Monthly Board Seats Won

Impact on Existing Campaigns2

Examples of Notable Campaign Developments Amid Public Health Crisis

9

The Diminishing Activist Toolkit: M&A

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Source: Lazard analysis, FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement

1 Includes all completed or pending transactions >$500mm. Sorted by date announced.

21 1923

2720

59

76

84

99

2016 2017 2018 2019 2020

Campaigns with M&A Thesis

Only 5 of 16 campaigns

initiated in March had an

M&A thesis

With M&A activity sinking to multi-year lows, activists will face near-term challenges in urging for consolidation or divestitures

32% 36% 34% 34%% of Total

Campaigns47%

Impact on the Activism Landscape3

March

marked the

2nd slowest

month in

seven years 5

Median: 64 Deals

March

37

2016 2017 2018 2019 2020

Historical M&A Activity by Month (Number of Announced Deals)1

Q2 – Q4

Q1

10

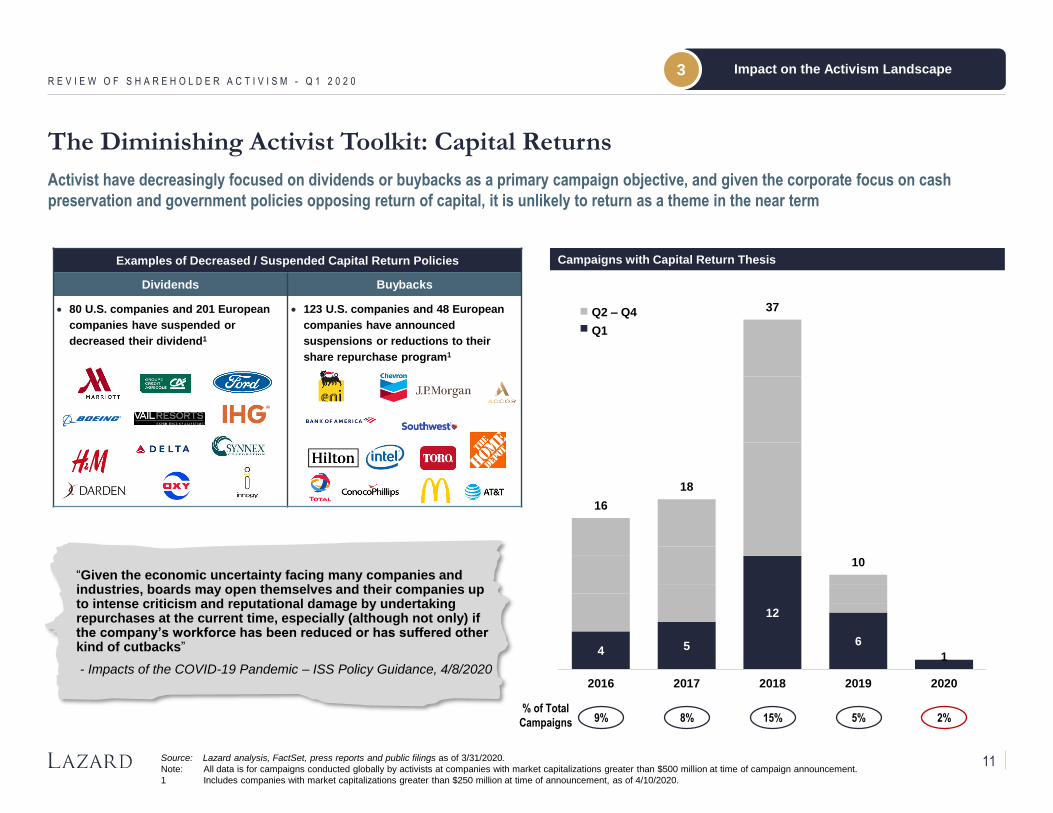

The Diminishing Activist Toolkit: Capital Returns

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Source: Lazard analysis, FactSet, press reports and public filings as of 3/31/2020.

Note: All data is for campaigns conducted globally by activists at companies with market capitalizations greater than $500 million at time of campaign announcement.

1 Includes companies with market capitalizations greater than $250 million at time of announcement, as of 4/10/2020.

Activist have decreasingly focused on dividends or buybacks as a primary campaign objective, and given the corporate focus on cash

preservation and government policies opposing return of capital, it is unlikely to return as a theme in the near term

Impact on the Activism Landscape3

4 5

12

6

1

16

18

37

10

2016 2017 2018 2019 2020

9% 8% 15% 2%5%

Campaigns with Capital Return ThesisExamples of Decreased / Suspended Capital Return Policies

Dividends Buybacks

• 80 U.S. companies and 201 European

companies have suspended or

decreased their dividend1

• 123 U.S. companies and 48 European

companies have announced

suspensions or reductions to their

share repurchase program1

“Given the economic uncertainty facing many companies and industries, boards may open themselves and their companies up to intense criticism and reputational damage by undertaking repurchases at the current time, especially (although not only) if the company’s workforce has been reduced or has suffered other kind of cutbacks”

- Impacts of the COVID-19 Pandemic – ISS Policy Guidance, 4/8/2020

% of Total

Campaigns

Q2 – Q4

Q1

11

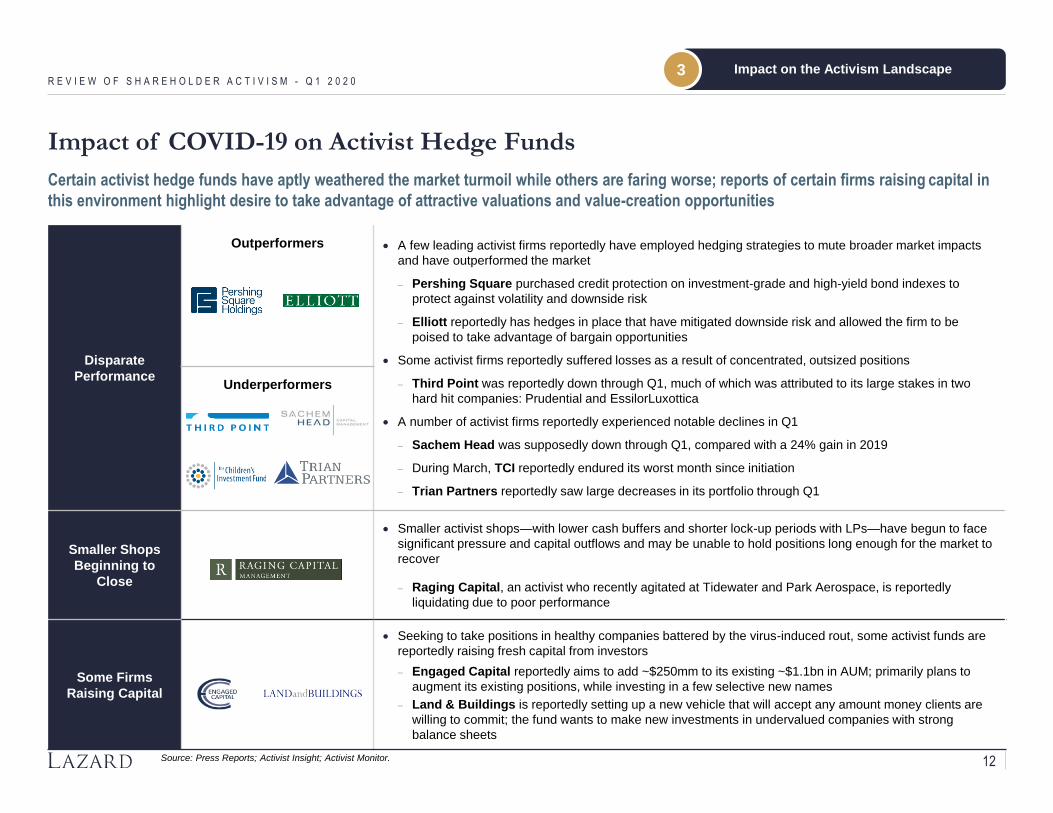

Impact of COVID-19 on Activist Hedge Funds

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Disparate

Performance

Outperformers • A few leading activist firms reportedly have employed hedging strategies to mute broader market impacts

and have outperformed the market

− Pershing Square purchased credit protection on investment-grade and high-yield bond indexes to

protect against volatility and downside risk

− Elliott reportedly has hedges in place that have mitigated downside risk and allowed the firm to be

poised to take advantage of bargain opportunities

• Some activist firms reportedly suffered losses as a result of concentrated, outsized positions

− Third Point was reportedly down through Q1, much of which was attributed to its large stakes in two

hard hit companies: Prudential and EssilorLuxottica

• A number of activist firms reportedly experienced notable declines in Q1

− Sachem Head was supposedly down through Q1, compared with a 24% gain in 2019

− During March, TCI reportedly endured its worst month since initiation

− Trian Partners reportedly saw large decreases in its portfolio through Q1

Underperformers

Smaller Shops

Beginning to

Close

• Smaller activist shops—with lower cash buffers and shorter lock-up periods with LPs—have begun to face

significant pressure and capital outflows and may be unable to hold positions long enough for the market to

recover

− Raging Capital, an activist who recently agitated at Tidewater and Park Aerospace, is reportedly

liquidating due to poor performance

Some Firms

Raising Capital

• Seeking to take positions in healthy companies battered by the virus-induced rout, some activist funds are

reportedly raising fresh capital from investors

− Engaged Capital reportedly aims to add ~$250mm to its existing ~$1.1bn in AUM; primarily plans to

augment its existing positions, while investing in a few selective new names

− Land & Buildings is reportedly setting up a new vehicle that will accept any amount money clients are

willing to commit; the fund wants to make new investments in undervalued companies with strong

balance sheets

Source: Press Reports; Activist Insight; Activist Monitor.

Certain activist hedge funds have aptly weathered the market turmoil while others are faring worse; reports of certain firms raising capital in

this environment highlight desire to take advantage of attractive valuations and value-creation opportunities

Impact on the Activism Landscape3

12

63%23%

14%

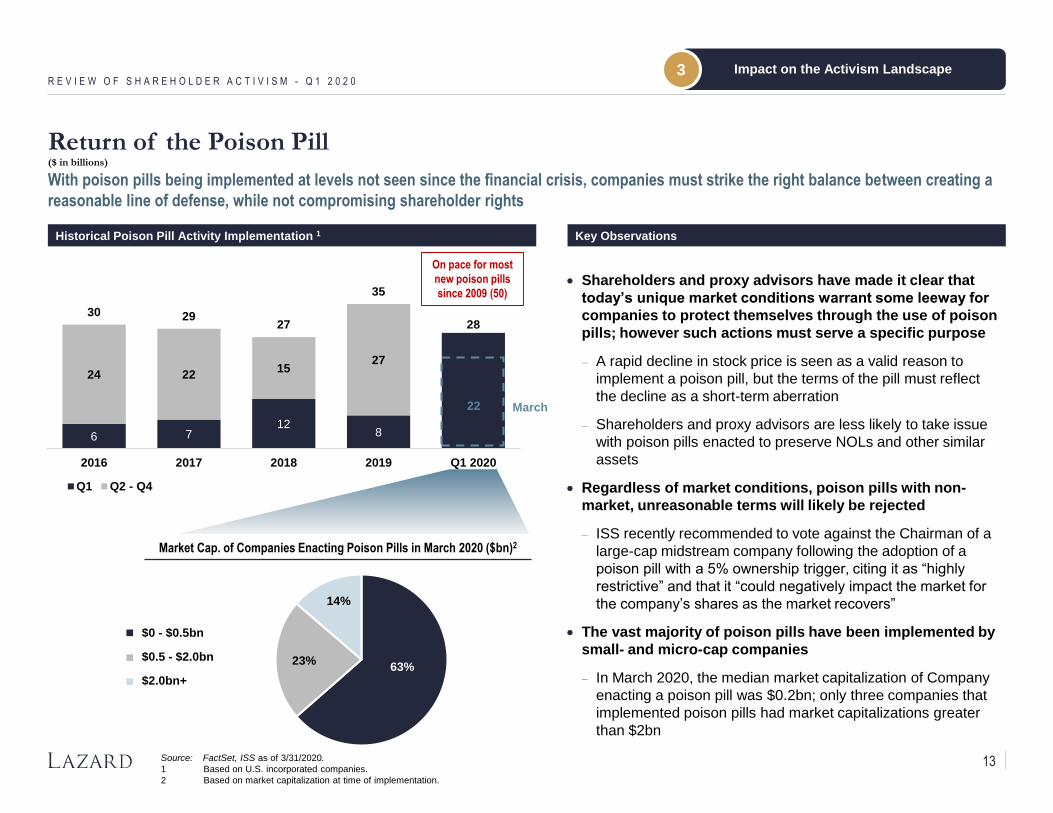

Return of the Poison Pill($ in billions)

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Source: FactSet, ISS as of 3/31/2020.

1 Based on U.S. incorporated companies.

2 Based on market capitalization at time of implementation.

With poison pills being implemented at levels not seen since the financial crisis, companies must strike the right balance between creating a

reasonable line of defense, while not compromising shareholder rights

Impact on the Activism Landscape3

Historical Poison Pill Activity Implementation 1

• Shareholders and proxy advisors have made it clear that

today’s unique market conditions warrant some leeway for

companies to protect themselves through the use of poison

pills; however such actions must serve a specific purpose

− A rapid decline in stock price is seen as a valid reason to

implement a poison pill, but the terms of the pill must reflect

the decline as a short-term aberration

− Shareholders and proxy advisors are less likely to take issue

with poison pills enacted to preserve NOLs and other similar

assets

• Regardless of market conditions, poison pills with non-

market, unreasonable terms will likely be rejected

− ISS recently recommended to vote against the Chairman of a

large-cap midstream company following the adoption of a

poison pill with a 5% ownership trigger, citing it as “highly

restrictive” and that it “could negatively impact the market for

the company’s shares as the market recovers”

• The vast majority of poison pills have been implemented by

small- and micro-cap companies

− In March 2020, the median market capitalization of Company

enacting a poison pill was $0.2bn; only three companies that

implemented poison pills had market capitalizations greater

than $2bn

6 712

8

28

24 2215

27

30 2927

35

2016 2017 2018 2019 Q1 2020

Q1 Q2 - Q4

Market Cap. of Companies Enacting Poison Pills in March 2020 ($bn)2

On pace for most

new poison pills

since 2009 (50)

Key Observations

$0 - $0.5bn

$0.5 - $2.0bn

$2.0bn+

March22

13

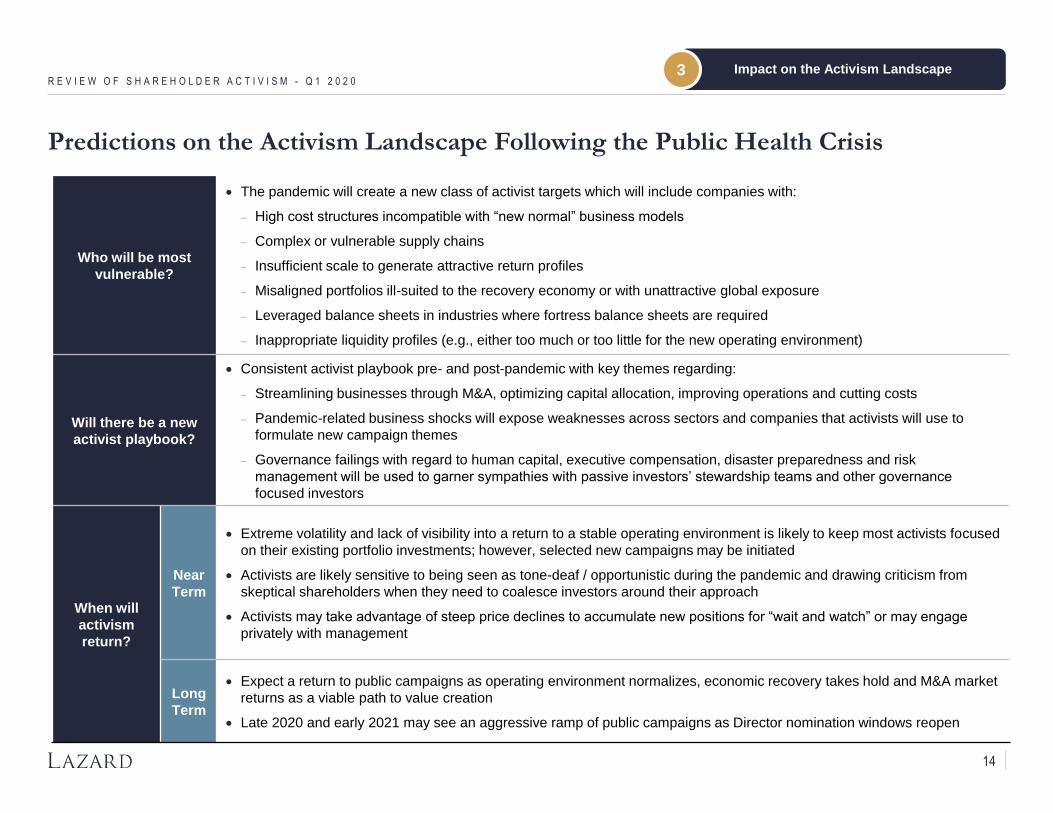

Predictions on the Activism Landscape Following the Public Health Crisis

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Who will be most

vulnerable?

• The pandemic will create a new class of activist targets which will include companies with:

− High cost structures incompatible with “new normal” business models

− Complex or vulnerable supply chains

− Insufficient scale to generate attractive return profiles

− Misaligned portfolios ill-suited to the recovery economy or with unattractive global exposure

− Leveraged balance sheets in industries where fortress balance sheets are required

− Inappropriate liquidity profiles (e.g., either too much or too little for the new operating environment)

Will there be a new

activist playbook?

• Consistent activist playbook pre- and post-pandemic with key themes regarding:

− Streamlining businesses through M&A, optimizing capital allocation, improving operations and cutting costs

− Pandemic-related business shocks will expose weaknesses across sectors and companies that activists will use to

formulate new campaign themes

− Governance failings with regard to human capital, executive compensation, disaster preparedness and risk

management will be used to garner sympathies with passive investors’ stewardship teams and other governance

focused investors

When will

activism

return?

Near

Term

• Extreme volatility and lack of visibility into a return to a stable operating environment is likely to keep most activists focused

on their existing portfolio investments; however, selected new campaigns may be initiated

• Activists are likely sensitive to being seen as tone-deaf / opportunistic during the pandemic and drawing criticism from

skeptical shareholders when they need to coalesce investors around their approach

• Activists may take advantage of steep price declines to accumulate new positions for “wait and watch” or may engage

privately with management

Long

Term

• Expect a return to public campaigns as operating environment normalizes, economic recovery takes hold and M&A market

returns as a viable path to value creation

• Late 2020 and early 2021 may see an aggressive ramp of public campaigns as Director nomination windows reopen

Impact on the Activism Landscape3

14

“A Fundamental Reshaping of Finance”

• BlackRock believes that climate change is leading

to a “fundamental reshaping of finance” and

therefore expects portfolio companies to:

− Publish in line with Sustainability Accounting

Standards Board (SASB) industry guidelines

− Disclose climate risks according to Task Force on

Climate-related Disclosure (TCFD) recommendations

− Be prepared to discuss the UN Sustainable

Development Goals in stewardship engagements

• BlackRock plans on enforcing this belief by voting

against Directors at companies that have not

implemented SASB and TCFD climate reporting by

the end of 2020

• Additional actions BlackRock is undertaking to

address climate change:

− Defaulting to sustainable investment strategies

across its main offerings

− Incorporating ESG as a core risk area in all active

portfolio strategies

− Exiting high-risk sectors across its active portfolio and

doubling offering of ESG ETFs

− Improving transparency around its sustainable

product offerings and voting practices

The Four Principles of Good Governance

• Board Composition

− Boards should be comprised of independent Directors

with adequate time and experience

− Companies should disclose Board diversity on

expertise, tenure and personal characteristics

− Boards should evolve with long-term strategy

• Oversight of Strategy and Risk

− Oversight of long-term strategy and relevant risks is

the Board’s responsibility

− Boards should understand and be involved in

executing the long-term strategy

− Long-term, material risks should be comprehensively

disclosed

• Executive Compensation

− Compensation should be performance linked and

should incentivize outperformance in the long term

− If a company underperforms, executive compensation

should reflect that

• Governance Structures

− Governance structure must protect shareholder rights

− Boards need to hold themselves accountable to

shareholders

The “Responsibility” Factor

• State Street has indicated that it views ESG issues,

such as climate change, labor practices and

consumer product safety, as intrinsically tied to

shareholder value

• State Street will increasingly use its “R-Factor” –

the “R” stands for “Responsibility” – tool in its

evaluation of whether companies are incorporating

ESG into their long-term strategies

− “R-Factor” is a proprietary ESG scoring system that

uses SASB’s materiality framework and four ESG-

related data sources to assign companies a score

measuring “the performance of a company’s

business operations and governance as it relates to

financially material ESG challenges facing the

company’s industry”

• Beginning in 2020, State Street will take

“appropriate voting action” against companies

with a poor R-Factor score who cannot explain

how they will improve their score

• Starting in 2022, State Street will begin voting

against Directors at companies where their “R-

Factor” score lags peers

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Updates From the “Big 3” Index Funds Views on ESG

Source: Company websites, press reports and public filings as of 3/31/2020.

BlackRock, Vanguard and State Street have made clear the thematic priorities they believe influence long-term corporate performance and the

ways they will evaluate them

Implications for ESG and Shareholder Engagement4

15

Key Considerations for Navigating Shareholder Engagement in 2020

Despite COVID-19, expectations for shareholder engagement remain high, with investor focus areas expanding to include company directives

regarding the pandemic and their impact on human capital, executive compensation and business strategy and operations

Source: Investor Websites, ISS.

“Boards contemplating defensive maneuvers may want to consider that an effectiveresponse to the pandemic could be more advantageous than any pill. Althoughthe outbreak of COVID-19 may not have been…predictable…the risk oversightfunction of many boards will…be under a microscope once the market begins toemerge from this downturn and activists sift through the wreckage for newtargets…Companies that fail to safeguard the health of their employees, orwhose business continuity plans prove to be inadequate, could eventuallyface…opposition.“

ISS SPECIAL SITUATIONS RESEARCH, 20 MARCH 2020

Selected Stakeholder Perspectives

“How are we engaging with companies? Virtually. On March 11 and 12, for example,we hosted the very first Buy-side Global Consumer CEO Conference. It was plannedmonths ago as an in-person event, but in less than a week, we pivoted to makeit 100% virtual. We still had 23 consumer company CEOs participate. We continueto have a steady flow of virtual meetings with companies to ensure we stayclose to the changing business dynamics they are experiencing”

BRENDAN SWORDS, WELLINGTON MANAGEMENT, 11 MARCH 2020

“The sell side is doing its best to convert planned corporate access meetings to eitherconference calls or videoconference calls whenever possible…The best thingissuers can do for the investment community is keep the lines ofcommunication open and try to provide as much transparency as possible.”

LISA RUBINGER, ASHLER CAPITAL (CITADEL), 18 MARCH 2020

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Range of Discussion Topics Pertaining to the Public Health Crisis

“We recognize that our engagement conversations will shift to more immediate ESGissues such as employee health, serving and protecting customers andensuring the overall safety of supply chains in the context of the current crisis—the scope and duration of which none of us can predict…we encourage you tocommunicate to investors COVID-19’s short- and medium-term potential impact toyour business, overall operations and supply chains, including managementpreparedness and scenario-planning analysis”

CYRUS TARAPOREVALA, 6 APRIL 2020

Financial Impact / LiquidityImpact of Government

Stimulus Package

Operational

and Business Continuity

Short- and Long-Term

Changes to Capital Allocation

Employee-Related MattersCustomer / Supply Chain

Maintenance

Board Oversight of

Response Plan and

Broader Risk Management

Changes to CEO /

Director Compensation

Implications for ESG and Shareholder Engagement4

16

What Now For

Sustainability?

• Certain investors and market observers view sustainability as a “luxury

good” viable only in bull markets

− In the near-term, the steep drop in the prices of public equities may

invite these market participants to focus on low valuations while

placing less emphasis on the ESG practices of a company

• However, over the long term, the COVID-19 pandemic could cause

increased focus on sustainability initiatives as investors will desire

stable businesses that can withstand sudden macroeconomic shocks

− In particular, the sustainable investment community may heighten its

attention on areas such as the health and safety of employees,

customers, suppliers and other stakeholders, as well as crisis

management planning

Sustainable

Fund Inflows

Continue

• Total inflows to sustainable equity ETFs since the start of market

turbulence in late February remain positive year-to-date, whereas the

top non-ESG focused U.S. equity ETFs have seen substantial outflows

Sustainable

Funds

Outperformance

• While still suffering losses due to the rapid market sell-off, ESG-

oriented funds outperformed conventional funds globally

− According to Morningstar, during Q1, 70% of ESG-focused funds had

returns in the top half of peer groups, while only 11% finished in the

bottom quartile1

− In the U.S., 24 out of 26 sustainable index funds had returns superior

to those of their closest conventional index fund1

Sustainable Investing in the Current Market Environment

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

While it is unclear whether COVID-19 and the steep decline in oil prices will have a longer term effect on the growth of sustainable investing,

common themes of sustainable investing—including managing tail-end risks and employee wellbeing—have arguably become more

prominent as the pandemic evolves

Source: Equity research, Morningstar, press reports

1 Based on Morningstar categorizations.

“The concept of long-term sustainability would suggest thatcompanies that come through [COVID-19 pandemic] and dowell would be exactly the kinds of companies you wouldlook to as role models…Companies can still demonstratethat they have effective leadership. In times of crisis thatbecomes more apparent, not less apparent.”

MICHELLE EDKINS, BLACKROCK, 18 MARCH 2020

“There is obviously a lot of volatility and a lot of big openquestions just in the very near term that need to getanswered…Over the long term, I think if anything [theCOVID-19 pandemic] would likely accelerate the focus onESG from an investor standpoint”

JEFF MELI, BARCLAYS, 24 MARCH 2020

“We have long argued that companies don’t operate in avacuum. Their success reflects their ability to adapt tochallenges and trends in the societies to which they belong.That is more true now than ever; social and environmentalchallenges, and investment drivers, are increasinglyoverlapping.”

ANDREW HOWARD, SCHRODERS, 24 MARCH 2020

Implications for ESG and Shareholder Engagement4

17

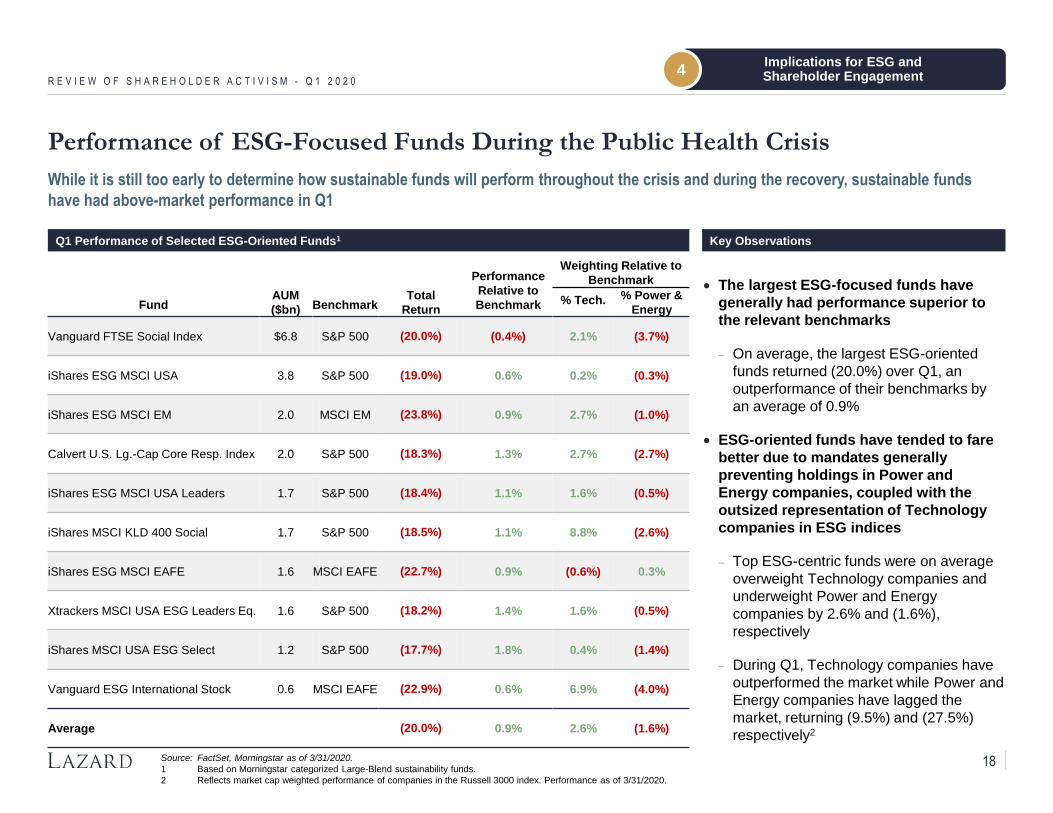

Performance of ESG-Focused Funds During the Public Health Crisis

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

While it is still too early to determine how sustainable funds will perform throughout the crisis and during the recovery, sustainable funds

have had above-market performance in Q1

Source: FactSet, Morningstar as of 3/31/2020.

1 Based on Morningstar categorized Large-Blend sustainability funds.

2 Reflects market cap weighted performance of companies in the Russell 3000 index. Performance as of 3/31/2020.

Implications for ESG and Shareholder Engagement4

FundAUM

($bn) BenchmarkTotal

Return

Performance

Relative to

Benchmark

Weighting Relative to

Benchmark

% Tech. % Power &

Energy

Vanguard FTSE Social Index $6.8 S&P 500 (20.0%) (0.4%) 2.1% (3.7%)

iShares ESG MSCI USA 3.8 S&P 500 (19.0%) 0.6% 0.2% (0.3%)

iShares ESG MSCI EM 2.0 MSCI EM (23.8%) 0.9% 2.7% (1.0%)

Calvert U.S. Lg.-Cap Core Resp. Index 2.0 S&P 500 (18.3%) 1.3% 2.7% (2.7%)

iShares ESG MSCI USA Leaders 1.7 S&P 500 (18.4%) 1.1% 1.6% (0.5%)

iShares MSCI KLD 400 Social 1.7 S&P 500 (18.5%) 1.1% 8.8% (2.6%)

iShares ESG MSCI EAFE 1.6 MSCI EAFE (22.7%) 0.9% (0.6%) 0.3%

Xtrackers MSCI USA ESG Leaders Eq. 1.6 S&P 500 (18.2%) 1.4% 1.6% (0.5%)

iShares MSCI USA ESG Select 1.2 S&P 500 (17.7%) 1.8% 0.4% (1.4%)

Vanguard ESG International Stock 0.6 MSCI EAFE (22.9%) 0.6% 6.9% (4.0%)

Average (20.0%) 0.9% 2.6% (1.6%)

• The largest ESG-focused funds have

generally had performance superior to

the relevant benchmarks

− On average, the largest ESG-oriented

funds returned (20.0%) over Q1, an

outperformance of their benchmarks by

an average of 0.9%

• ESG-oriented funds have tended to fare

better due to mandates generally

preventing holdings in Power and

Energy companies, coupled with the

outsized representation of Technology

companies in ESG indices

− Top ESG-centric funds were on average

overweight Technology companies and

underweight Power and Energy

companies by 2.6% and (1.6%),

respectively

− During Q1, Technology companies have

outperformed the market while Power and

Energy companies have lagged the

market, returning (9.5%) and (27.5%)

respectively2

Key ObservationsQ1 Performance of Selected ESG-Oriented Funds1

18

C O N F I D E N T I A L

Appendix

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

C O N F I D E N T I A L

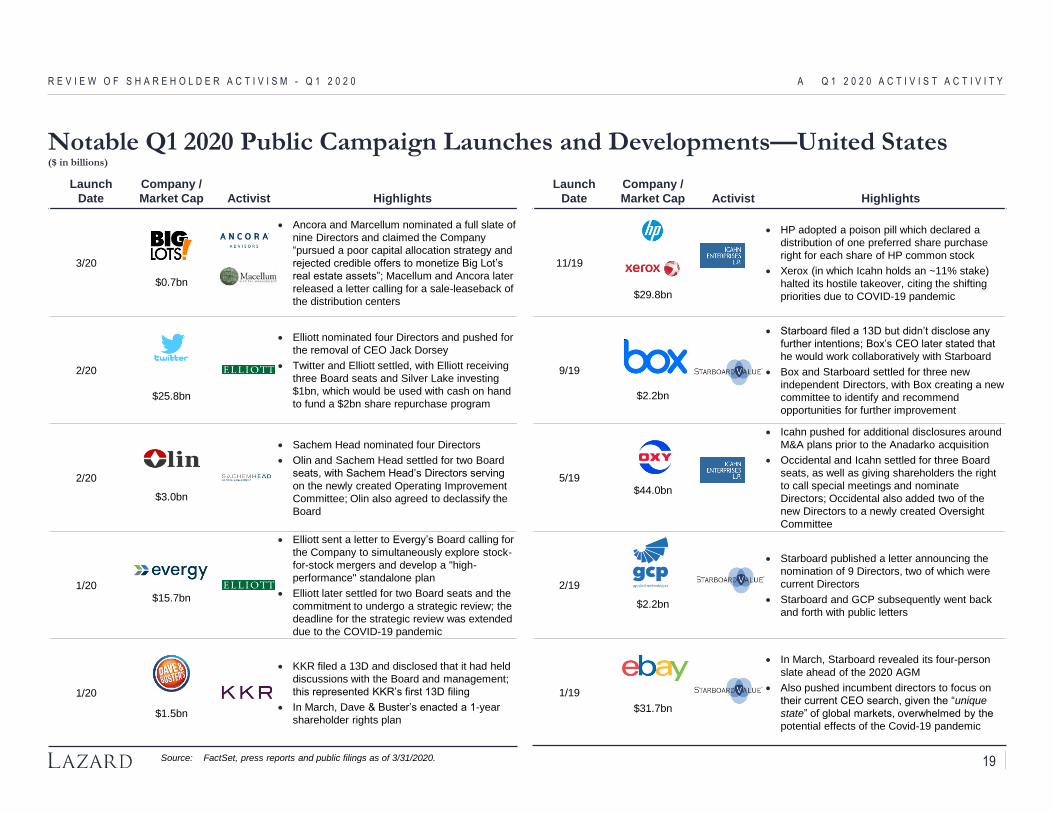

A Q1 2020 Activist Activity

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Launch

Date

Company /

Market Cap Activist Highlights

11/19

$29.8bn

• HP adopted a poison pill which declared a

distribution of one preferred share purchase

right for each share of HP common stock

• Xerox (in which Icahn holds an ~11% stake)

halted its hostile takeover, citing the shifting

priorities due to COVID-19 pandemic

9/19

$2.2bn

• Starboard filed a 13D but didn’t disclose any

further intentions; Box’s CEO later stated that

he would work collaboratively with Starboard

• Box and Starboard settled for three new

independent Directors, with Box creating a new

committee to identify and recommend

opportunities for further improvement

5/19$44.0bn

• Icahn pushed for additional disclosures around

M&A plans prior to the Anadarko acquisition

• Occidental and Icahn settled for three Board

seats, as well as giving shareholders the right

to call special meetings and nominate

Directors; Occidental also added two of the

new Directors to a newly created Oversight

Committee

2/19

$2.2bn

• Starboard published a letter announcing the

nomination of 9 Directors, two of which were

current Directors

• Starboard and GCP subsequently went back

and forth with public letters

1/19

$31.7bn

• In March, Starboard revealed its four-person

slate ahead of the 2020 AGM

• Also pushed incumbent directors to focus on

their current CEO search, given the “unique

state” of global markets, overwhelmed by the

potential effects of the Covid-19 pandemic

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0 A Q 1 2 0 2 0 A C T I V I S T A C T I V I T Y

Launch

Date

Company /

Market Cap Activist Highlights

3/20

$0.7bn

• Ancora and Marcellum nominated a full slate of

nine Directors and claimed the Company

“pursued a poor capital allocation strategy and

rejected credible offers to monetize Big Lot’s

real estate assets”; Macellum and Ancora later

released a letter calling for a sale-leaseback of

the distribution centers

2/20

$25.8bn

• Elliott nominated four Directors and pushed for

the removal of CEO Jack Dorsey

• Twitter and Elliott settled, with Elliott receiving

three Board seats and Silver Lake investing

$1bn, which would be used with cash on hand

to fund a $2bn share repurchase program

2/20

$3.0bn

• Sachem Head nominated four Directors

• Olin and Sachem Head settled for two Board

seats, with Sachem Head’s Directors serving

on the newly created Operating Improvement

Committee; Olin also agreed to declassify the

Board

1/20$15.7bn

• Elliott sent a letter to Evergy’s Board calling for

the Company to simultaneously explore stock-

for-stock mergers and develop a "high-

performance" standalone plan

• Elliott later settled for two Board seats and the

commitment to undergo a strategic review; the

deadline for the strategic review was extended

due to the COVID-19 pandemic

1/20

$1.5bn

• KKR filed a 13D and disclosed that it had held

discussions with the Board and management;

this represented KKR’s first 13D filing

• In March, Dave & Buster’s enacted a 1-year

shareholder rights plan

Source: FactSet, press reports and public filings as of 3/31/2020.

Notable Q1 2020 Public Campaign Launches and Developments—United States($ in billions)

19

Launch

Date

Company /

Market Cap Activist Highlights

11/19 $5.5bn

• CIAM stated it had met with Management

several times to discuss strategy, governance

and financials; CIAM also called for an

additional EUR 970mm extraordinary dividend

payment ahead of the AGM

11/19$19.2bn

• IFP urged Kirin to reverse its diversification

strategy, to dispose of certain non-core stakes

and questioned its Board overhaul; IFP also

pushed for two Board seats

• Kirin announced that shareholders rejected the

proposals from IFP to divest and launch a

share repurchase program, as well as rejected

the two dissident Director candidates

7/19$4.2bn

• In January, Capgemini’s tender offer for Altran

was successful

• In March, Elliott announced it had ended its

opposition to Capgemini's offer for Altran, citing

"market conditions"

2/19 $2.3bn

• Argo and Voce settled for three Board seats,

with Voce being reimbursed up to $1.8mm,

ending Voce’s push for five Board seats

5/17 $4.1bn

• Amber called for a renewal of the entire

Supervisory Board, simplification of group

structure and suspension of the dividend;

Amber also stated the Company should

develop certain business segments and later

nominated eight Directors to the Board

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0 A Q 1 2 0 2 0 A C T I V I S T A C T I V I T Y

Launch

Date

Company /

Market Cap Activist Highlights

2/20 $47.8bn

• Third Point called for Prudential to separate its

U.S. and Asian operations, initiate cost-cutting

procedures and improve its capital allocation

strategy

• Prudential later announced that it would IPO

part of its U.S. insurance business

2/20 $3.4bn

• Bluebelll pushed for management change and

stated that it may have people to suggest for

the Supervisory Board (however, none of its

partners were interested in Board seats)

• Hugo Boss announced that its CEO would step

down

2/20 $89.8bn

• Elliott announced a $2.5bn position and

pushed for governance improvements and

substantial share repurchases

• SoftBank announced a $4.8bn share

repurchase program; SoftBank later approved

a $41bn asset sale to fund $18bn in additional

share repurchases

1/20 $0.9bn

• Oasis pushed to improve operations corporate

governance and to dispose of non-core assets

through an investor presentation and campaign

website

12/19 $0.7bn Murakami

• Murakami’s Reno withdrew its proposal to

remove 10 Directors after failing to secure

support from Ardisia Investment (a ~16%

shareholder)

• Shareholders rejected the Reno nominee, but

approved the independent Directors that

management recommended

Source: FactSet, press reports and public filings as of 3/31/2020.

Notable Q1 2020 Public Campaign Launches and Developments—Rest of World($ in billions)

20

C O N F I D E N T I A L

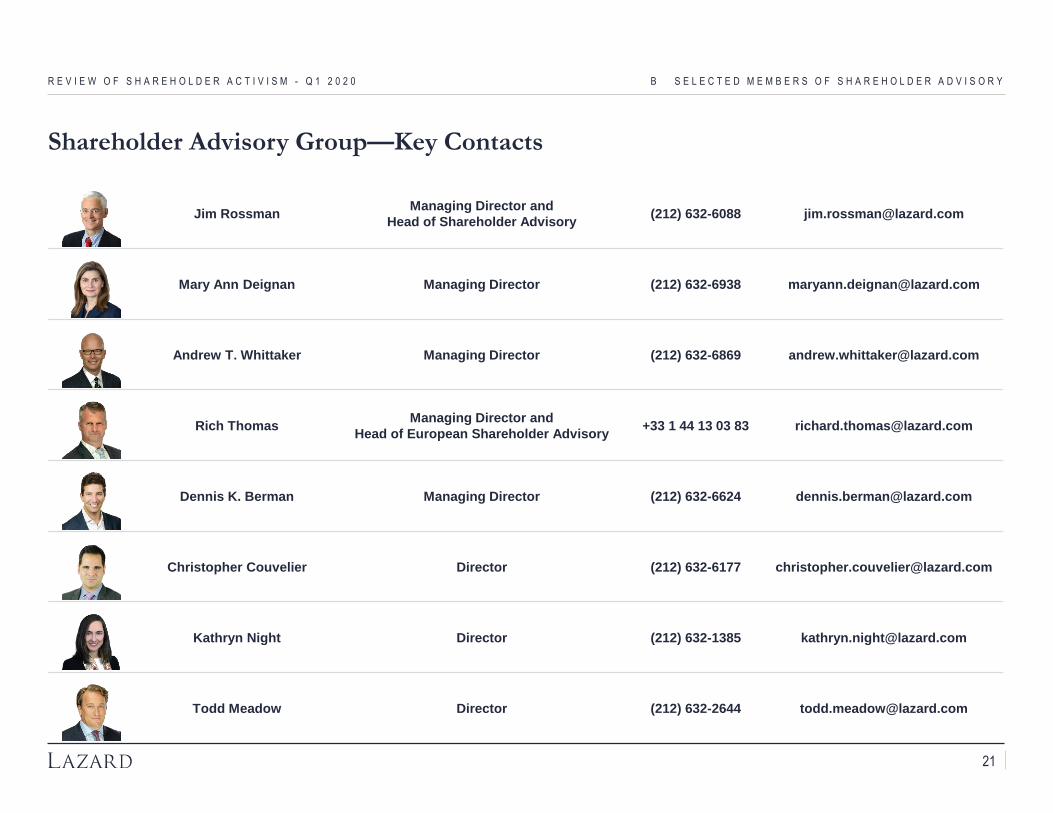

B Selected Members of Shareholder Advisory

R E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Shareholder Advisory Group—Key Contacts

B S E L E C T E D M E M B E R S O F S H A R E H O L D E R A D V I S O R YR E V I E W O F S H A R E H O L D E R A C T I V I S M - Q 1 2 0 2 0

Jim RossmanManaging Director and

Head of Shareholder Advisory(212) 632-6088 [email protected]

Mary Ann Deignan Managing Director (212) 632-6938 [email protected]

Andrew T. Whittaker Managing Director (212) 632-6869 [email protected]

Rich ThomasManaging Director and

Head of European Shareholder Advisory+33 1 44 13 03 83 [email protected]

Dennis K. Berman Managing Director (212) 632-6624 [email protected]

Christopher Couvelier Director (212) 632-6177 [email protected]

Kathryn Night Director (212) 632-1385 [email protected]

Todd Meadow Director (212) 632-2644 [email protected]

21