retail property in belgium - jll · 2016-06-22 · quarterly market update - pulse june 2016 retail...

TRANSCRIPT

Quarterly Market Update - Pulse June 2016

Retail Property in BelgiumLarge project pipeline for 2016

146,000 sq.m. taken up as at mid-May 2016, of which 105,300 sq.m. in the first quarter alone.

115,200 sq.m. delivered in Q1 2016, the highest quarterly volume of the past five years.

€ 168 million invested as at mid-May 2016, of which € 113 million in the first quarter.

€ 2,000/sq.m./year prime rent for high streets. Prime rents forecast to remain stable for prime locations.

€

2 | pulse | BELGIAN RETAIL MARKET | JUNE 2016 www.jll.be

*DEFLATED AND DESEASONALISED - 2010 = 100**LTM : LAST 12 MONTHS

Sources : Eurostat, NBB, JLL Research

Market conditions Q4 2015 Q1 2016 Change Outlook

Consumer Confidence (NBB/BNB) -3 -7 -4

Retail Sales Vol. Index* (Eurostat) 101.26 100.08 -118bps

Occupier market Q4 2015 Q1 2016 Change Outlook

Take-up - current quarter (sqm) 135,200 105,300 -22%

Take-up - LTM** cumulative (sqm) 384,800 417,000 8%

Completions - LTM** cumul. (sqm) 159,000 247,500 56%

Prime Rent (€/sq.m./year) 2,000 2,000 0%

Investment market > 2.5 MEUR Q4 2015 Q1 2016 Change Outlook

Investment volume LTM** cumulative (MEUR) 2,086 2,016 -3%

Prime Yield % - high street 3.75 3.75 0%

Prime Yield % - shopping centres 4.25 4.25 0%

Prime Yield % - retail warehousing 5.75 5.75 0%

Key Market Indicators• Total take-up in Q1 2016 was 105,300 sq.m., the highest level recorded in a first quarter in the

past three years, but 20% below the volume registered the previous quarter. As at mid-May the take-up volume had risen to 146,000 sq.m., mainly retail warehousing.

• Large transactions in 2016 so far include 4,000 sq.m. let by Decathlon in Hasselt, 1,800 sq.m. let by JD Sports in Brussels (Rue Neuve) and 1,650 sq.m. let by H&M in Geraardsbergen.

• Over 115,200 sq.m. were delivered in Q1 2016, the highest quarterly volume of the past five years.

• Prime rents in high streets amount to €2,000/sq.m. p.a. and apply to the prime high streets in Brussels (Rue Neuve, Avenue Louise) and to Antwerp (Meir, Schuttershofstraat).

• € 168 mln were invested in retail so far this year, €113 mln of which in the first quarter, 16% below the volume recorded in the same quarter last year. The pipeline, however, is worth close to €1.3 billion.

• Prime yields for high streets amount to 3.75%, 4.25% for shopping centres and 5.75% for retail warehousing. The downward trend persists.

• Market conditions are difficult due to the lockdown after the terrorist attacks in Paris and Brussels. As a consequence online sales grew 34% in 2015, to €8.2 bn, but overall retail sales still declined q-o-q. Consumer confidence stabilised at -8 in May after declining in the first four months of the year, mainly due to deteriorating prospects for the general economy and for employment.

3 | pulse | BELGIAN RETAIL MARKET | JUNE 2016 www.jll.be

Take-up

Shopping Centres

71,600 sq.m. were taken up in retail warehousing in Q1 2016, rising to 99,000 sq.m. as at mid-May. The volume at mid-May equals 48% of the total volume of the market segment last year, which was the highest volume of the last four years. The major part representing 76% of the take-up volume so far this year was recorded in Flanders, 14% in Wallonia and 4% in Brussels. Large transactions were recorded in Hasselt, where Decathlon took 4,000 sq.m., in Mechelen where Intercarro let 2,785 sq.m. and in Knokke-Heist, where Albert Heijn let 2,365 sq.m. in the Duinenwater project.

Retail Warehousing

“Despite difficult market conditions, take-up is expected to repeat the solid performance recorded in 2015, thanks to large transaction volumes in retail

warehousing parks.”WALTER GOOSSENS, HEAD OF RETAIL AGENCY

TAKE-UP PER MARKET SEGMENT

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

2011 2012 2013 2014 2015

sq.m.

Shopping Centres High Street Retail Warehousing 5-yr Ave

Just under 25,000 sq.m. were taken up in the Belgian high streets in the first quarter of 2016, up 11% on the first quarter last year, and 26% above the average volume recorded in a first quarter in the past five years. As at May 2016 the total volume registered in high streets had risen to 35,600 sq.m. The Big Six cities (Brussels, Antwerp, Ghent, Liège, Brugge and Hasselt) attracted two thirds of the volume taken up in high streets so far this year, in line with previous years. This year so far the volume represents over 23,000 sq.m.. The highest volume was recorded in Brussels (10,430 sq.m.), followed by Antwerp (6,000 sq.m.) and Ghent (2,650 sq.m.). 1,750 sq.m. were taken up in Brugge, 831 sq.m. in Liège and 670 sq.m. in Hasselt.

With regard to number of transactions, 191 transactions were recorded as at mid-May 2016, representing already 47% of the average number of transactions for a whole year, 405. The largest transactions in high streets were the letting by JD Sports of 1,800 sq.m. in Brussels Downtown, Rue Neuve 48, formerly occupied by Bershka, 1,650 sq.m. let by H&M in Geraardsbergen and 850 sq.m. let by Fish & Chips in Antwerp (Kammenstraat).

High Streets

Approx. 8,800 sq.m. were taken up in shopping centres in Q1 2016, nearly triple the volume registered in the same quarter last year and the highest volume for a first quarter of the past four years. It remains nevertheless 30% below the average quarterly volume of the past five year, 12,500 sq.m., which confirms that a first quarter is usually the weakest quarter of the year. As at mid-May, the take-up volume had risen to 11,500 sq.m. As at mid-May, 7 transactions were recorded in Waasland Shopping Center, some 10 pre-lettings were signed in Docks Bruxsel and 6 transactions in Les Grands Prés in Mons. The largest transactions so far this year were signed by Rekhet (1,060 sq.m., Den Tir Antwerp), by JBC (825 sq.m. in K in Kortrijk), and by Bel & Bo (710 sq.m. in Ring Shopping Kortrijk). 47 % of the take-up was recorded in shopping centres in Flanders, 27% in the Walloon Region and 24% in Brussels.

4 | pulse | BELGIAN RETAIL MARKET | JUNE 2016 www.jll.be

PROJECTS DELIVERED

SOLID PROJECT PIPELINE IN 2016-2017

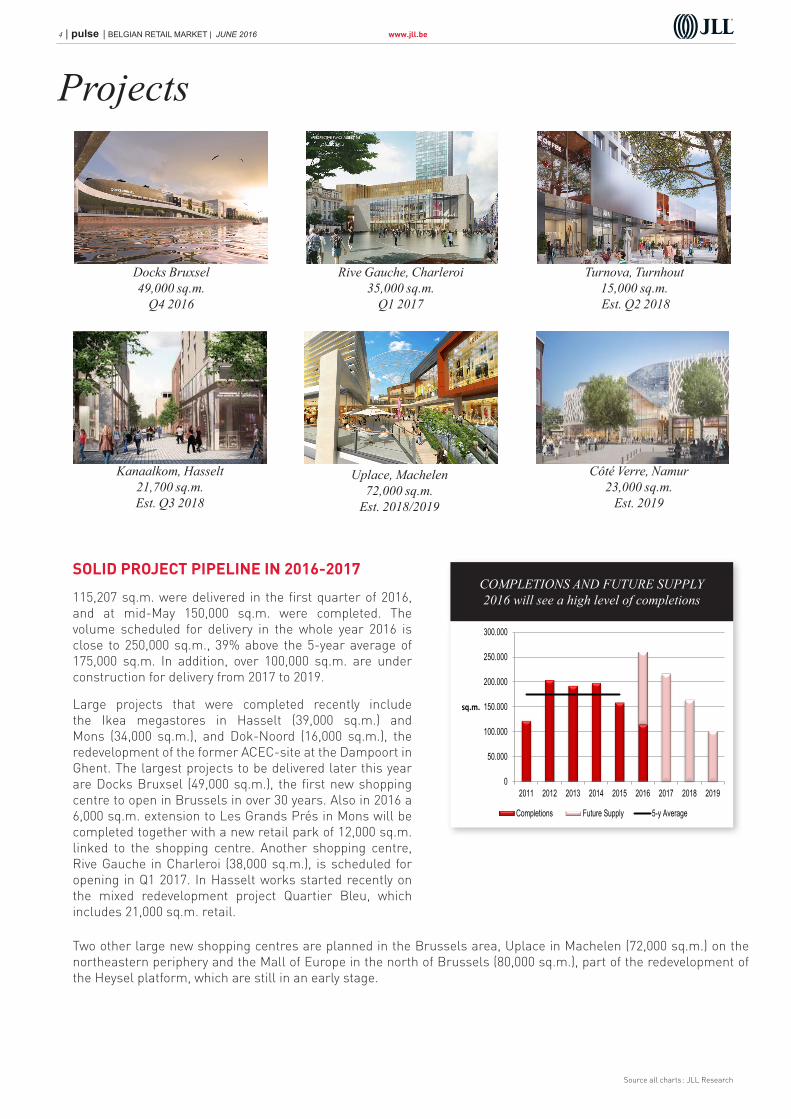

115,207 sq.m. were delivered in the first quarter of 2016, and at mid-May 150,000 sq.m. were completed. The volume scheduled for delivery in the whole year 2016 is close to 250,000 sq.m., 39% above the 5-year average of 175,000 sq.m. In addition, over 100,000 sq.m. are under construction for delivery from 2017 to 2019.

Large projects that were completed recently include the Ikea megastores in Hasselt (39,000 sq.m.) and Mons (34,000 sq.m.), and Dok-Noord (16,000 sq.m.), the redevelopment of the former ACEC-site at the Dampoort in Ghent. The largest projects to be delivered later this year are Docks Bruxsel (49,000 sq.m.), the first new shopping centre to open in Brussels in over 30 years. Also in 2016 a 6,000 sq.m. extension to Les Grands Prés in Mons will be completed together with a new retail park of 12,000 sq.m. linked to the shopping centre. Another shopping centre, Rive Gauche in Charleroi (38,000 sq.m.), is scheduled for opening in Q1 2017. In Hasselt works started recently on the mixed redevelopment project Quartier Bleu, which includes 21,000 sq.m. retail.

Projects

COMPLETIONS AND FUTURE SUPPLY2016 will see a high level of completions

Source all charts : JLL Research

Two other large new shopping centres are planned in the Brussels area, Uplace in Machelen (72,000 sq.m.) on the northeastern periphery and the Mall of Europe in the north of Brussels (80,000 sq.m.), part of the redevelopment of the Heysel platform, which are still in an early stage.

Docks Bruxsel49,000 sq.m.

Q4 2016

Rive Gauche, Charleroi35,000 sq.m.

Q1 2017

Turnova, Turnhout15,000 sq.m. Est. Q2 2018

Kanaalkom, Hasselt21,700 sq.m.Est. Q3 2018

Côté Verre, Namur23,000 sq.m.

Est. 2019

Uplace, Machelen 72,000 sq.m.

Est. 2018/2019

0

50.000

100.000

150.000

200.000

250.000

300.000

2011 2012 2013 2014 2015 2016 2017 2018 2019

sq.m.

Completions Future Supply 5-y Average

5 | pulse | BELGIAN RETAIL MARKET | JUNE 2016 www.jll.be

Prime Rents & InvestmentPRIME RENTS

PRIME YIELDSDownward trend persists

“2015 was exceptional both in terms of volume invested and yields, and 2016 looks

promising.ˮ

JEAN-PHILIP VRONINKS, HEAD OF CAPITAL MARKETS

Source all charts : JLL Research

STRONG INVESTMENT PIPELINE

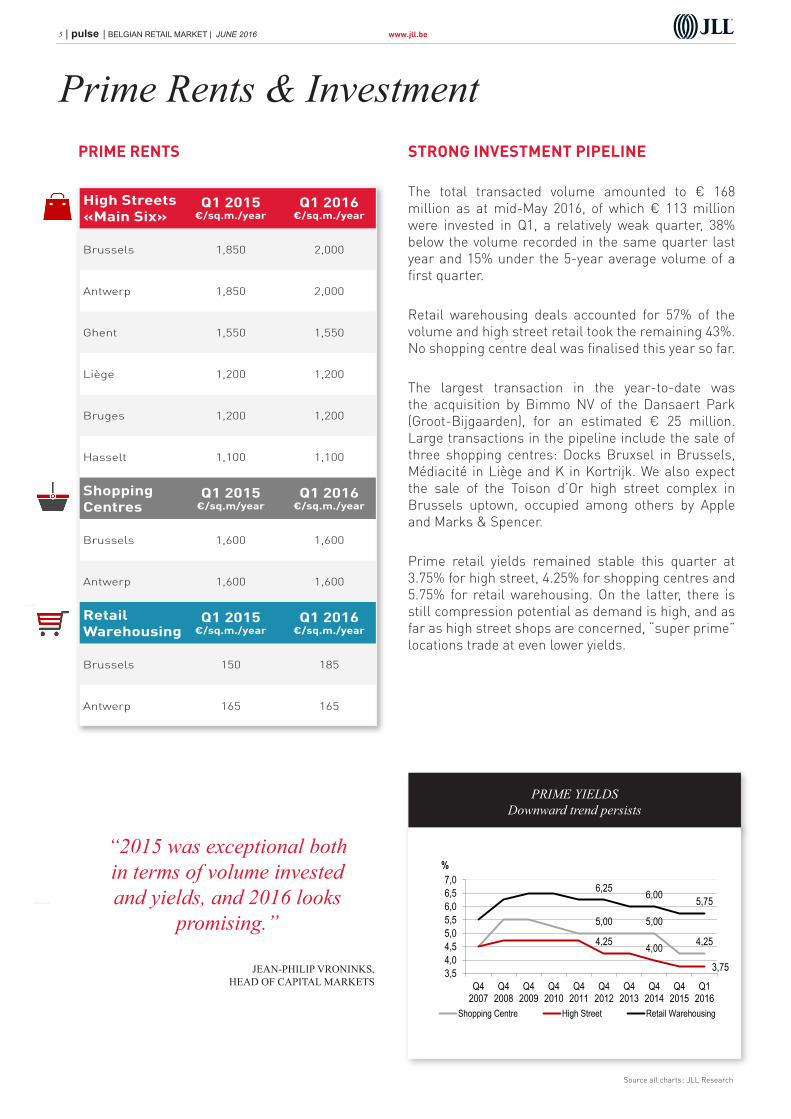

The total transacted volume amounted to € 168 million as at mid-May 2016, of which € 113 million were invested in Q1, a relatively weak quarter, 38% below the volume recorded in the same quarter last year and 15% under the 5-year average volume of a first quarter.

Retail warehousing deals accounted for 57% of the volume and high street retail took the remaining 43%. No shopping centre deal was finalised this year so far.

The largest transaction in the year-to-date was the acquisition by Bimmo NV of the Dansaert Park (Groot-Bijgaarden), for an estimated € 25 million. Large transactions in the pipeline include the sale of three shopping centres: Docks Bruxsel in Brussels, Médiacité in Liège and K in Kortrijk. We also expect the sale of the Toison d’Or high street complex in Brussels uptown, occupied among others by Apple and Marks & Spencer.

Prime retail yields remained stable this quarter at 3.75% for high street, 4.25% for shopping centres and 5.75% for retail warehousing. On the latter, there is still compression potential as demand is high, and as far as high street shops are concerned, “super prime” locations trade at even lower yields.

High Streets«Main Six»

Q1 2015€/sq.m./year

Q1 2016€/sq.m./year

Brussels 1,850 2,000

Antwerp 1,850 2,000

Ghent 1,550 1,550

Liège 1,200 1,200

Bruges 1,200 1,200

Hasselt 1,100 1,100

Shopping Centres

Q1 2015€/sq.m/year

Q1 2016€/sq.m./year

Brussels 1,600 1,600

Antwerp 1,600 1,600

Retail Warehousing

Q1 2015€/sq.m./year

Q1 2016€/sq.m./year

Brussels 150 185

Antwerp 165 165

5,00 5,00

4,254,25 4,00

3,75

6,25 6,00 5,75

3,54,04,55,05,56,06,57,0

Q42007

Q42008

Q42009

Q42010

Q42011

Q42012

Q42013

Q42014

Q42015

Q12016

Shopping Centre High Street Retail Warehousing

%

6 | pulse | BELGIAN RETAIL MARKET | JUNE 2016 www.jll.be

Year Qtr City Address Type Sq.m. Retailer

2016 1 Hasselt Kuringensteenweg 491 Letting 4,000 Decathlon

2016 1 Mechelen Jubellaan 78 Letting 2,800 Intercarro

2016 1 Knokke-Heist Project Duinenwater Letting 2,400 Albert Heijn

Top transactions

Year Qtr City Address Type Sq.m. Retailer

2016 1 Brussels Rue Neuve 48-50 Letting 1,800 JD Sports

2016 1 Geraardsbergen Oudenaardsestraat 35 Letting 1,650 H&M

2016 1 Antwerpen Kammenstraat Letting 850 Fish & Chips

High Streets

Year Qtr City Shopping Centre Type Sq.m. Retailer

2016 2 Brussels Docks Bruxsel Pre-letting 3,108 Zara*

2016 1 Wijnegem Wijnegem Shopping Letting 2,700 C&A

2016 2 Brussels Docks Bruxsel Pre-letting 2,000 Kiabi*

Shopping Centres

Retail Warehousing

Transactions in bold were advised by JLL - *:JLL co-agent

OCCUPIER MARKET 2016

INVESTMENT MARKET 2016 (as at mid-May)

Year Qtr Type** City Building Price MEUR

Yield % Seller Buyer

2016 1 RW Groot-Bijgaarden Dansaert Park 25 + 5 FRI Bimmo NV

2016 2 HS Brussels Toison d’Or 14-15 (&Other Stories) 22 - JV Besix RED &

D. Janne Group Hayen

2016 1 RW Deinze D-Shopping 18 5 NV B.Kernretail Bimmo NV

2016 1 HS Brussels Bd de Waterloo 57 14 3.5 Family Hocedez Ramy Baron

2016 2 RW Sint-Genesius-Rode Retail & kmo-park 13.02 - Private Warehouses

Estates Belgium

**RW : retail warehousing HS : high street SC : shopping centre

JLL Research Advisory Services

JLL timeseries for quarterly and submarket data are available on request, as well as tailormade consulting. This is a fee-based service.

JLL Research produces on a quarterly basis detailed submarket reports about Brussels office districts and the Belgian industrial and logistics property market. These are available on request against paying subscription.

Our Research & Advisory service also propares micro-location studies for landlords with a focus on rental analysis, existing and future competition analysis with GIS mapping, transaction analysis and SWOT.

Avenue Marnixlaan, 23 b1B – 1000 Bruxelles BrusselT 32 (0) 2 550 25 25F 32 (0) 2 550 26 26

Jan Van Gentstraat 1 bus 402B – 2000 AntwerpenT 32 (0) 3 232 39 30F 32 (0) 3 233 76 85

www.jll.be

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. It is based on material that we believe to be re-liable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such errors in order to correct them.

JLL OFFICES - BELGIUM

CONTACTS

VINCENT H. QUERTONCEO Benelux+32 (0) 2 550 25 25Vincent [email protected] l l .com

JEAN-PHILIP VRONINKS *

Head of Capital Markets Belux+32 (0) 2 550 26 64Jean-Phi l ip [email protected] l l .com*Revron GCV

PIERRE-PAUL VERELSTHead of Research Belux+32 (0) 2 550 25 04Pierre-Paul .Verels t@eu. j l l .com

ANN VANDERWEGENSenior Research Analyst+32 (0) 2 550 26 [email protected] l l .com

WALTER GOOSSENSHead of Retail Leasing Belgium+32 (0)2 550 25 [email protected] l l .com

THIERRY DEBOURSE *

Head of Retail Benelux+32 (0) 2 550 25 [email protected] l l .com*SPRL ECML Consulting