rest pension · rest pension customer service personnel are not representatives of the trustee. any...

TRANSCRIPT

REST PensionProduct Disclosure Statement and forms

Effective 1 October 2015

Issued by Retail Employees Superannuation Pty Limited (Trustee) ABN 39 001 987 739 AFSL 240003 Retail Employees Superannuation Trust ABN 62 653 671 394 Unique Superannuation Identifier RES0102AU

rest.com.au 1300 305 778

1. Why join REST Pension? 3

2. How REST Pension works? 5

Are you eligible? 5

Current REST members 5

Members new to REST 5

Investment choice overview 5

Payment options 6

Estate planning decisions 7

3. Fees and other costs 9

Investment fees 9

Administration fee 9

Other costs 9

4. Investment options and risk 14

5. Tax implications 20

6. Centrelink implications 22

7. Other important information 23

8. Forms 28

Checklist for REST Pension application 29

Application form

Rollover initiation request form

Transfer part of your superannuation form

TFN declaration form

Contents

Who is REST’s Trustee?This Product Disclosure Statement (PDS) has been issued by the Trustee company, Retail Employees Superannuation Pty Limited, Australian Business Number (ABN) 39 001 987 739, Australian Financial Services Licence (AFSL) 240003, referred to in this PDS as ‘the Trustee’, ‘we’, ‘our’, ‘us’ or ‘REST’. REST Pension is a product of the Retail Employes Superannuation Trust ABN 62 653 671 394 (The Fund).

The Trustee’s registered address is Level 7, 50 Carrington Street, Sydney NSW 2000, postal address: Locked Bag 5042, Parramatta NSW 2124. The Trustee maintains professional indemnity insurance. REST is administered by Australian Administration Services Pty Ltd (AAS), ABN 62 003 429 114, referred to in the PDS as REST Pension Customer Service. REST Pension Customer Service personnel are not representatives of the Trustee. Any general financial product advice given by REST Pension Customer Service personnel is provided by AAS.

Important noticeThis PDS should not be used as a substitute for personal financial advice. The PDS intends to provide information, not advice. This PDS was prepared without taking into account your individual objectives, financial situation or needs. Accordingly, before acting on the contents of this PDS, you should consider whether it is appropriate to you, having regard to your objectives, financial situation and needs.

You should read the PDS in its entirety before making any decision in connection with this product.

REST is governed by a trust deed. As a member you will be bound by the terms of the trust deed and its rules, which may be amended, subject to superannuation law. The trust deed and rules provide for many of the rights, duties and responsibilities of the Trustee, members, other beneficiaries and employers.

There is currently some uncertainty about the terms of the trust deed for the Fund. The Trustee is seeking to confirm the terms of the trust deed in the Supreme Court of South Australia. This might mean that the terms of the trust deed will change. The Trustee does not think that any changes or the court proceedings will have any practical effect on members or on our administration of the Fund.

If you are printing an electronic copy of this PDS, you must print all pages, including the application forms. An electronic copy of the PDS can be downloaded at rest.com.au/pensionpds A paper copy of the PDS, the trust deed, and any supplementary documents can be obtained free of charge on request by contacting REST Pension Customer Service on 1300 305 778.

Up to date informationThe information contained in this PDS is up to date at the time of preparation. Some of the information may also be subject to change without notice, such as information about other management costs, other fees or the investment strategy or asset allocation of a particular investment option. The Trustee will issue a supplementary or replacement PDS if there is a materially adverse omission or change to information in the PDS. From time to time there may be changes to non-materially adverse information which may be updated through member communications or on our website at rest.com.au/governance, other than the PDS. Non-materially adverse updated information, including a paper copy, can be obtained free of charge from REST Pension Customer Service on 1300 305 778 (between 8am and 6pm, weekdays) or the REST website, rest.com.au

Who can invest?The invitation to invest in this product is only available to persons receiving the PDS in Australia. It is not made, directly or indirectly, to persons in any other country. The issuer is not bound to accept an application for this product.

2

What is a pension?The type of pension explained in this Product Disclosure Statement (PDS) is an account-based pension or income stream offered by a super fund.

An account-based pension works like this:

• you put superannuation money into it• your money is invested in your choice of investment

option(s), which generates a tax-free return• you receive a regular income based on the level you

choose (within limits set by the government).

Great benefits, whether you’re retired or still workingIf you’re retired, REST Pension could help you:

• invest in a tax-effective way• manage your income and spending• seek to maximise the length of time your super lasts. If you’re still working, REST Pension could help you:• boost your super in the lead-up to retirement, or • scale back your work hours without reducing

your income.

REST is an award-winning fundREST is proud to have been recognised by the industry for the value and service we offer to members. For further information about the awards won by REST, please go to rest.com.au/ourawards

Advice when you need itObtaining personal financial advice about your retirement plans when you need it is important. REST can put you in touch with Money Solutions2. Once you are a REST member, and subject to superannuation law we will pay for your first, single superannuation or pension related question over the phone with a Money Solutions Coach.

You can contact REST Pension Customer Service on 1300 305 778 to be put through to a Money Solutions Coach.

Communicating with RESTYou can keep track of your REST Pension 24/7 via the secure website, MemberAccess at rest.com.au

When you join REST Pension, we will send you a unique REST Pension member number. Use this number to register online for a password that allows you to login to MemberAccess.

You can receive most of your member communications electronically by setting up your communication preferences via the ‘Personal details’ tab under the ‘Member’ tab.

Selecting eStatements means you will receive your annual member statement earlier than the paper copy, and you will also have instant online access to your statement history. Going paperless also keeps the clutter out of your letterbox, helps the environment, and also helps the Trustee to keep costs down.

Login to MemberAccess to:

• view your account balance• view and update your account details• update your personal details• check your nominated beneficiary details• change your non-binding beneficiary nomination• view your asset allocation• view transaction history• make an investment switch• change your pension payment amount or frequency• make a lump sum withdrawal3.

1. Why join REST Pension?

REST has been helping Australians build their retirement savings for more than 25 years. Today with around 2 million members and more than $37 billion in funds under management, REST is one of the largest super funds in Australia – around one in six Australian workers1 is a REST member.

1. Number of working Australians sourced from Australian Bureau of Statistics 2015, Labour force, Australia, ‘Summary - June 2015 Key Figures’, cat. no. 6202.0, viewed in July 2015.

2. Money Solutions Pty Limited ABN 36 105 811 836, AFSL No. 258145. Money Solutions personnel are not representatives of the REST Trustee. Any financial product advice given by Money Solutions is provided under the Money Solutions AFSL. The Trustee does not accept liability for any loss or damage incurred by any person as a result of using products or services provided by Money Solutions.

3. In MemberAccess, account-based pension members can make partial withdrawals of between $1,000 and $10,000 (excluding Transition to Retirement pensions).

REST Pension Product Disclosure Statement | 3

Tax and Centrelink implications

What tax will I pay? If you’re 60 and over, your pension income is completely tax free. If you’re under 60, your pension income may provide you with some tax advantages.

See page 20

Will I receive favourable Centrelink treatment?

Income and asset tests are used to determine any income support payment from the Government such as the Age Pension. Your REST Pension will be included in the income test.

See page 22

Investments

Investment fee (not directly deducted from your account)

Estimates of between 0.04% pa to 0.76% pa, including estimated performance fees of up to 0.13% pa.

See page 12

Establishment fee, Switching fee, Exit fee, Withdrawal fee

Nil See page 9

How can my money be invested?

You have the choice of 13 investment options in your REST Pension and you can nominate which options your transactions, including pension payment, will come from.

See page 16

Fees and costs

Administration fee $1.25 per week, plus a yearly asset based fee based on your account balance.

See page 9

Asset based feeAccount balance Yearly asset based fee

First $300,000 0.18%

Next $500,000 0.12%

Portion over $800,000 0.00%

Yearly asset based fee is capped at $1,140

See page 9

Estate planning decisions

What happens if I die? (Beneficiary nominations)

To help with estate planning, REST Pension offers three types of beneficiary nominations, so you can choose who benefits from your pension in the event of your death.

See page 7

Account and payments

How often can I receive payments?

You can choose to receive income payments: twice a month, monthly, quarterly, half yearly or yearly.

See page 6

How much are the payments?

You can choose how much you get paid, subject to minimums set by the government. There is also a maximum amount if you choose the ‘Transition to Retirement’ option.

See page 6

Can I put extra money in once it has started?

No, although you can start an additional REST Pension, provided you have at least $10,000 to invest.

See page 6

Are you eligible?

How much do I need? A minimum of $10,000 to invest. See page 5

Who can join? Find out if you meet the eligibility conditions. See page 5

Already a REST member? Find out how to move from your current REST account to REST Pension.

See page 5

Snapshot of REST Pension

4

Are you eligible? Answering these questions will help you determine if you’re eligible to start a REST Pension.In all cases, you need a minimum of $10,000 to commence a REST Pension.

Have you reached ‘preservation age’?

Your preservation age depends on when you were born

Date of birth Preservation age

Before 1 July 1960 55

1 July 1960 to 30 June 1961 56

1 July 1961 to 30 June 1962 57

1 July 1962 to 30 June 1963 58

1 July 1963 to 30 June 1964 59

1 July 1964 or after 60

The above table will help you determine your ‘preservation age’ – the age at which you may be able to access some of your super.

If you have not reached your preservation age, but have satisfied another condition of release, you may be eligible to transfer your super to REST Pension.

If you have not reached your preservation age, you are not eligible for a REST Pension unless you have a super benefit that can be cashed for other reasons. Please refer to ‘Other super benefits that could be used to start a REST Pension’ below.

What is your retirement status?I’ve permanently retired and reached my preservation age• You are eligible to start a REST Pension.I’m not yet retired.• If you are 65 years or over, you are eligible to start

a REST Pension.• If you are aged 60 to 64 and leave or change

employment, you are eligible to start a REST Pension.• If you have reached your preservation age and do not

intend to work 10 hours or more per week ever again, you are eligible to start a REST Pension.

• If you have reached preservation age but you’re not retired and don’t fall within one of the three bullet points immediately above, then you can start your REST Pension as a ‘Transition to Retirement pension*’.

* Please note if you are transferring your benefits from another REST or Acumen account to start a REST Pension account, you must keep at least $5,000 in your superannuation account.

Other super benefits that could be used to start a REST Pension

If you’ve got at least $10,000 of ‘unrestricted non-preserved’ super, you can start a REST Pension, regardless of your age and retirement status.

For example, a payment to the beneficiary of a Death or Total and Permanent Disablement (TPD) benefit.

If you’ve received a superannuation death or TPD benefit, this money becomes classified as ‘unrestricted non-preserved’ while remaining in the super fund.

There are also some other ways you may have acquired ‘unrestricted non-preserved’ super, and you can check if you do on your latest statement or by calling your super fund.

Are you over the preservation age?If you are aged over the preservation age, less than 65 but are not ready to retire, you may wish to talk to a financial adviser because a REST Transition to Retirement Pension could help you:• work less but maintain your current income• boost your super so you have more money when

you finally retire.

Are you currently a REST member?REST Pension will be created as a separate account to your existing REST super account. Therefore you will still be required to fill out the application form. If you do not change your investment option from your current super selection, then you will be invested in the same options and will not need to fill in the ‘Opening balance’ part in section 4 of the application form.

Members new to RESTPlease read this PDS carefully and ensure you understand all the facts before making any decision. The Snapshot of REST Pension on page 4 will help to provide an overview of the product and the Checklist for REST Pension Application on page 29 will help you with the application process.

Investment choice overview Which investment choice will best suit you? This will depend on your investment timeframe, financial goals and what level of risk you are comfortable with. REST offers 13 investment options for you to choose from, with different levels of risk and potential return.

Existing REST members will commence REST Pension with the current investments held in their existing account, rounded to the nearest whole percentage unless you advise otherwise.

What can I invest in?You may invest in a single option or in a mix of the Core Strategy, Structured and Member-tailored options.

If you have elected to build your own portfolio, you may need to regularly review and occasionally rebalance your investments to ensure they continue to reflect your preferred asset allocation. Refer to page 14 for a full explanation of the investment options.

Unsure about your investment choices?If you are new to REST and don’t want to make a choice or just need more time to think about your options, we will invest your savings in REST Pension’s default investment option – the Balanced option.

We recommend you obtain professional financial advice from a licensed financial adviser before making an investment decision. A licensed financial adviser can help you make investment decisions based on your individual circumstances.

REST can put you in touch with Money Solutions. Once you are a REST member, subject to superannuation law, we will pay for your first, single superannuation or pension related question over the phone with a Money Solutions Coach. See ‘Advice when you need it’ on page 3 for more information.

Can I change my investment choice?Yes, you have the option to change your investment choice at any time. Your switch will become effective in accordance with the terms on ‘How to switch an investment option’ on rest.com.au/investments

If you switch online you will receive a confirmation page that you can print. You will also receive confirmation in writing once your switch is processed.

2. How REST Pension works

REST Pension Product Disclosure Statement | 5

2. How REST Pension works (continued)

You can switch your investment options at rest.com.au by logging into your MemberAccess account using your password. Alternatively you can use the ‘Application to make an investment choice – REST Pension’ form, which you can download from our website or call REST Pension Customer Service on 1300 305 778.

How do I create my own portfolio?You can create your own portfolio by choosing the percentages of one or more investment options. Your selected percentages must total 100%. Your money will stay in your selected investment option(s) until you switch it to another option(s).

If you invest in more than one investment option, you can select which options and in what proportions your pension payments, fees and charges are deducted.

You can nominate your payment choice under ‘Future transaction’ in ‘Section 4: How would you like to invest the money?’ of the application form*.

For example, if you are invested 80% in the Balanced option and 20% in the Cash option, you may choose to have all your pension payments, fees and charges deducted from just one option like the Cash option. If the account balance in this option runs out, payments will be deducted proportionally from across your other investment options. You will need to monitor these deductions to ensure your payments continue to be made from the option you prefer. If you do not make a nomination, that’s OK too. Payments will be deducted proportionally from each investment option.

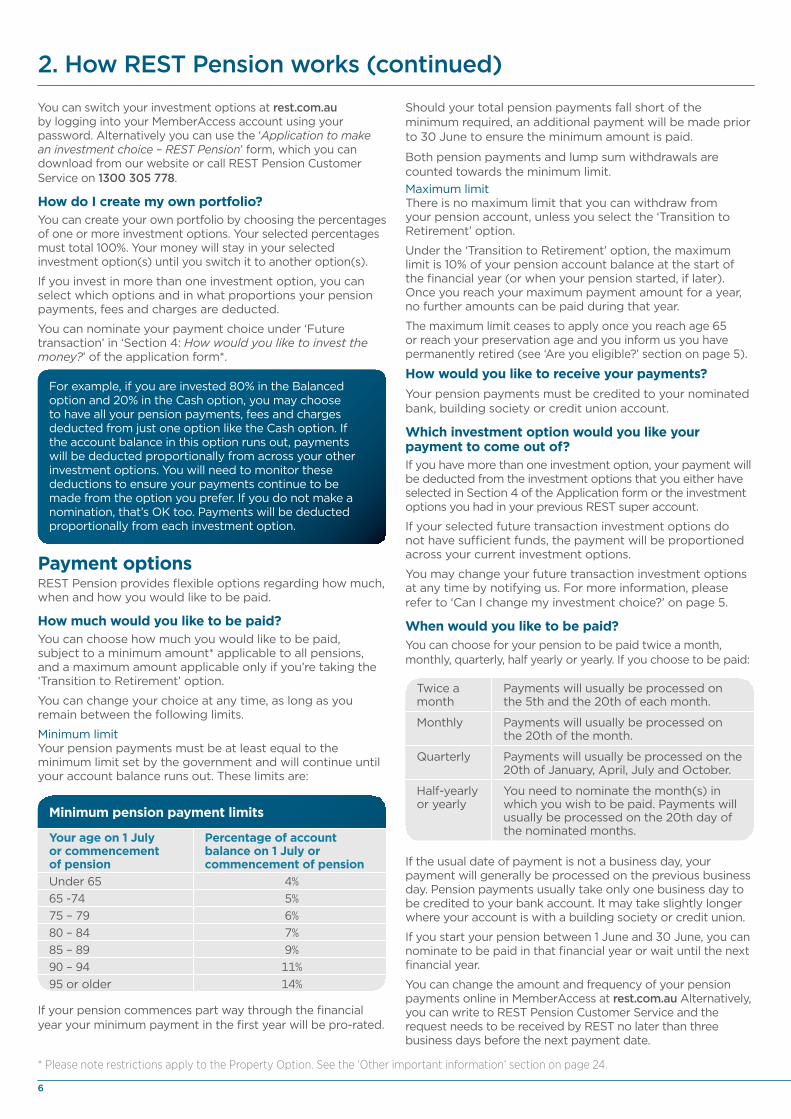

Payment optionsREST Pension provides flexible options regarding how much, when and how you would like to be paid.

How much would you like to be paid?You can choose how much you would like to be paid, subject to a minimum amount* applicable to all pensions, and a maximum amount applicable only if you’re taking the ‘Transition to Retirement’ option.

You can change your choice at any time, as long as you remain between the following limits.

Minimum limit Your pension payments must be at least equal to the minimum limit set by the government and will continue until your account balance runs out. These limits are:

Minimum pension payment limits

Your age on 1 July or commencement of pension

Percentage of account balance on 1 July or commencement of pension

Under 65 4%65 -74 5%75 – 79 6%80 – 84 7%85 – 89 9%90 – 94 11%95 or older 14%

If your pension commences part way through the financial year your minimum payment in the first year will be pro-rated.

Should your total pension payments fall short of the minimum required, an additional payment will be made prior to 30 June to ensure the minimum amount is paid.

Both pension payments and lump sum withdrawals are counted towards the minimum limit. Maximum limitThere is no maximum limit that you can withdraw from your pension account, unless you select the ‘Transition to Retirement’ option.

Under the ‘Transition to Retirement’ option, the maximum limit is 10% of your pension account balance at the start of the financial year (or when your pension started, if later). Once you reach your maximum payment amount for a year, no further amounts can be paid during that year.

The maximum limit ceases to apply once you reach age 65 or reach your preservation age and you inform us you have permanently retired (see ‘Are you eligible?’ section on page 5).

How would you like to receive your payments? Your pension payments must be credited to your nominated bank, building society or credit union account.

Which investment option would you like your payment to come out of?If you have more than one investment option, your payment will be deducted from the investment options that you either have selected in Section 4 of the Application form or the investment options you had in your previous REST super account.

If your selected future transaction investment options do not have sufficient funds, the payment will be proportioned across your current investment options.

You may change your future transaction investment options at any time by notifying us. For more information, please refer to ‘Can I change my investment choice?’ on page 5.

When would you like to be paid?You can choose for your pension to be paid twice a month, monthly, quarterly, half yearly or yearly. If you choose to be paid:

Twice a month

Payments will usually be processed on the 5th and the 20th of each month.

Monthly Payments will usually be processed on the 20th of the month.

Quarterly Payments will usually be processed on the 20th of January, April, July and October.

Half-yearly or yearly

You need to nominate the month(s) in which you wish to be paid. Payments will usually be processed on the 20th day of the nominated months.

If the usual date of payment is not a business day, your payment will generally be processed on the previous business day. Pension payments usually take only one business day to be credited to your bank account. It may take slightly longer where your account is with a building society or credit union.

If you start your pension between 1 June and 30 June, you can nominate to be paid in that financial year or wait until the next financial year.

You can change the amount and frequency of your pension payments online in MemberAccess at rest.com.au Alternatively, you can write to REST Pension Customer Service and the request needs to be received by REST no later than three business days before the next payment date.

* Please note restrictions apply to the Property Option. See the ‘Other important information’ section on page 24.

6

Making one-off withdrawalsIn addition to making your regular pension payments, you may be able to make a one-off withdrawal at any time^§. Under the ‘Transition to Retirement’ option, lump sum withdrawals are only permissible in very limited circumstances. However, you may be able to make a lump sum withdrawal from the unrestricted non-preserved benefit of your pension account. Importantly, this withdrawal will count towards your minimum annual pension payment amount but will not count towards the maximum annual pension payment limit under the Transition to Retirement option.

You can make partial withdrawals online in MemberAccess§#.

Once your account balance goes below $1,000 your account will be closed, we’ll notify you and pay the remainder of your account into your nominated bank account.^ If you want to withdraw an amount that would leave your account

with insufficient funds to pay the minimum payment (see previous page) for that year, then you first have to draw the minimum pension payment before making your one- off withdrawal

§ Excluding Transition to Retirement pensions# In MemberAccess, account-based pension members can make

withdrawals of between $1,000 and $10,000.

Switches and withdrawals may be delayedWe may delay or suspend switches or withdrawals from your account if:

• there are delays by third parties in processing our requests for example, if an underlying fund delays or suspends issuing unit prices,

• a switch or withdrawal would adversely affect the fund, or

• we cannot realise sufficient assets to satisfy your payment due to circumstances outside our control for example, markets have been restricted or suspended.

The delays or suspensions of payment could be significant. We are not responsible for any losses caused by these delays.

Estate Planning DecisionsWhen you apply for a REST Pension you are asked to indicate who will receive your pension if you die before your account balance runs out and how it should be paid to them.

As it’s a very important decision, you may want to get professional advice from a lawyer or a licensed financial planner.

Nominations do not carry over from other or previous super accounts (even if you have another REST or Acumen account) so you need to make a new nomination for your REST Pension account. With REST Pension, you have three options for making a nomination.

1. Reversionary beneficiary nominationYou can only nominate a dependant (please refer to definition in the next column) as your reversionary beneficiary. If you nominate a reversionary beneficiary, your dependant will receive ongoing pension payments after you die. If you nominate a reversionary beneficiary, following your death, your dependant will have authority to manage the account in the same way as you now do (except that they cannot lodge a reversionary beneficiary nomination). You can select only one reversionary beneficiary, and you can’t change or delete your nomination.

Legal personal representative refers to the person who is legally recognised to manage your affairs in the event of your death (ie the legal executor or administrator of your estate).

If you need to change or remove your reversionary beneficiary you must close the pension and commence a new pension. If your pension started prior to 1 January 2015 and you were exempt from the deeming rules, your new pension if commenced from 1 January 2015 or after will not be exempt from the deeming rules.

If you nominate a reversionary beneficiary, they must also be alive and be your dependant at time of your death, otherwise the nomination will be invalid and the Trustee will decide to pay your money to your dependant or to your legal personal representative (estate). Please refer to the definition above.

You can nominate your child to be your reversionary beneficiary in certain circumstances, although there are restrictions over how and when they can receive payments. Please refer to below for further information.

2. Non-lapsing binding beneficiary nomination These are nominations that REST, subject to REST consenting to the nomination, must follow, and that do not lapse after any period of time. Therefore, if you make one of these nominations, it is important to update it if your circumstances change, otherwise your money may not be paid as you would prefer.

REST will still have discretion over your death payment to pay your money to your dependant(s) or to your legal personal representative (estate) if your non-lapsing binding death nomination is invalid, or if the beneficiary you nominated was not a dependant at the time of your death.

REST will write to you if it does not accept your non-lapsing binding death nomination and give you the opportunity to make a new non-lapsing binding death nomination.

3. Non-binding beneficiary nomination A non-binding beneficiary nomination will indicate your beneficiary preference and is important in helping REST determine who should receive your money. However, the Trustee has absolute discretion to pay your money to your dependant(s) or to your legal personal representative (estate) but will take into account your nomination. Your beneficiary should be a dependant or your legal personal representative (estate). Please refer to the definition above.

Information about nominating a beneficiaryFollowing is some additional information for members who are considering nominating a child as a reversionary beneficiary, or require information about who can qualify as a ‘dependant’.

Definition of a dependant

A dependant can be:• your spouse (including de facto or same-sex spouse)• your children (including adopted, stepchild and

ex-nuptial child)• a person who is wholly or partially financially dependent

on you at the time of your death• a person with whom you have an interdependency

relationship when you die. Refer over the page for a definition of an ‘interdependency relationship’.

REST Pension Product Disclosure Statement | 7

For tax purposes, the definition of dependant is generally the same as this definition, although a child age 18 or more is only considered dependent if they are financially dependent on you or there is an interdependency relationship.Definition of an interdependency relationship

Generally, two people have an interdependency relationship if:

• they have a close personal relationship, and• they live together, and• one or each of them provides the other with financial

support, and• one or each of them provides the other with domestic

support and personal care, or care of a type and quality normally provided in a close personal relationship, rather than by a mere friend or flatmate.

If the two people have a close relationship but do not meet the other criteria listed because either or both of them suffer from a physical, intellectual or psychiatric disability or were temporarily living apart, they may still be regarded as having an interdependency relationship.

Pets and organisations are not accepted.

Nominating your child as a reversionary beneficiary

If you choose to nominate your child as a reversionary beneficiary, there are restrictions upon when and how they can receive payments.

To be eligible to receive your money as a pension, your child, at the date of your death, must be under age 18, or between 18 and 25 and financially dependent on you.

Pension payments can only continue until they are aged 25, at which point the balance will be paid as a lump sum.

If the child is disabled (as described in the Disability Services Act 1986), there are no age restrictions and your pension payments do not have to cease. There may be social security implications if you nominate your child as a reversionary beneficiary. You should always obtain independent, quality advice before making decisions.

If you don’t make a nominationIf you do not make a nomination, REST will consider information provided by your dependants, the legal personal representative* (estate) and other relevant parties to determine who will receive your money. That’s why it’s important for you to make a nomination and keep this information up to date, especially if your circumstances change. REST will only act on a valid nomination.

Paying money to your legal personal representative (estate)If REST decides to pay your money to your legal personal representative* (estate) it will be paid as a lump sum to your estate. It will then be distributed according to the terms of your Will or the relevant intestacy legislation that applies where you resided.

To change your nominationTo change a non-binding nomination please log on to MemberAccess. To change a non-lapsing binding beneficiary nomination, please download a ‘Nomination of beneficiary’ form on our website.

Anti-detriment paymentsAn anti-detriment payment is an additional lump sum amount a beneficiary receives in addition to the account balance of the deceased member. REST will pay anti-detriment payments to spouses, former spouses and children of the deceased.

It is only payable where the death benefit is being paid out as a lump sum, and represents a refund of the 15% contributions tax levied against the deceased member’s superannuation entitlements during their lifetime.

Super funds are not required to pay anti-detriment payments under superannuation law.

2. How REST Pension works (continued)

*As defined on page 7.

8

3. Fees and other costs

Consumer Advisory WarningDid you know?Small differences in both investment performance and fees and costs can have a substantial impact on your long-term returns.

For example, total annual fees and costs of 2% of your account balance, rather than 1%, could reduce your final return by up to 20% over a 30 year period (for example, reduce it from $100,000 to $80,000).

You should consider whether features such as superior investment performance or the provision of better member services justify higher fees and costs.

Your employer may be able to negotiate to pay lower administration fees where applicable. Ask the fund or your financial adviser.

To find out moreIf you would like to find out more, or see the impact of the fees based on your own circumstances, the Australian Securities and Investments Commission (ASIC) website (moneysmart.gov.au) has a superannuation fee calculator to help you check out different fee options.

Please note that the Consumer Advisory Warning is a government prescribed warning.

Lower administration fees cannot be negotiated with REST. The calculator on the ASIC website at moneysmart.gov.au can be used to calculate the effect of fees and costs on your superannuation account balance.

This document shows fees and other costs that you may be charged. These fees and other costs may be deducted from your money, from the returns on your investment or from the assets of the superannuation entity as a whole. Other fees, such as activity fees, advice fees for personal advice, and insurance fees, may also be charged, but these will depend on the nature of the activity, advice or insurance chosen by you. Taxes, insurance fees and other costs relating to insurance are set out in another part of this document. You should read all the information about fees and other costs because it is important to understand their impact on your investment.

The fees and costs for each investment option offered by the superannuation entity are set out on page 12.

REST Pension

Type of fee Amount How and when paid

Investment fee Estimates of between 0.04% to 0.76% pa, including estimated performance fees of up to 0.13% pa.

Accrued and reflected in an option’s unit price. It is not deducted directly from your account

Administration fee $1.25 per week, plus a yearly asset based fee based on your account balance.

Account balance Yearly asset based fee

First $300,000 0.18%

Next $500,000 0.12%

Portion over $800,000 0.00%

Yearly asset based fee is capped at $1,140

Administration fee including asset based fee is deducted from your account at the end of each month and is based on the value of your account on the day of deduction.

If you have more than one REST Pension, the asset based fee is calculated on the combined balance of your accounts.

Buy/sell spread Buy spread range 0.01 - 0.47%

Sell spread – 0.00%

Included in the relevant price and applied to your account or transaction as applicable at the time of the transaction.

Switching fee Nil Not applicable

Exit fee Nil Not applicable

Advice feesrelating to all members investing in a particular MySuper product or investment option

Nil Nil

Other fees and costs1

Family law split fee of $50 per split Split between your account and your spouse’s account when the split is made

Personal advice fees, if you agree a fee with Money Solutions

As agreed with Money Solutions2

Indirect cost ratio Nil Nil

1 For information regarding the definitions of the fees and costs incorporated in the table above, please refer to the ‘Additional explanation of fees and costs’ and ‘Defined fees’ section on page 10 of this document. These definitions can also be found at rest.com.au/definedfees

2 For information regarding this fee, please refer to the Additional explanation of fees and costs section on page 10 of this document.

REST Pension Product Disclosure Statement | 9

3. Fees and other costs (continued)

Additional explanation of fees and costsAdditional explanation of fees and costsDefined fees

Defined fees

Type of fee or cost Definition

Activity fees A fee is an activity fee if:(a) the fee relates to costs incurred by the Trustee of the superannuation entity that are directly

related to an activity of the Trustee:(i) that is engaged in at the request, or with the consent, of a member; or(ii) that relates to a member and is required by law; and

(b) those costs are not otherwise charged as an administration fee, an investment fee, a buy/sell spread, a switching fee, an exit fee, an advice fee or an insurance fee.

Administration fees

An administration fee is a fee that relates to the administration or operation of the superannuation entity and includes costs incurred by the Trustee of the entity that:(a) relate to the administration or operation of the entity; and(b) are not otherwise charged as an investment fee, a buy/sell spread, a switching fee, an exit fee,

an activity fee, an advice fee or an insurance fee.

Advice fees A fee is an advice fee if:(a) the fee relates directly to costs incurred by the Trustee of the superannuation entity because

of the provision of financial product advice to a member by:(i) a Trustee of the entity; or(ii) another person acting as an employee of, or under an arrangement with,

the Trustee of the entity; and(b) those costs are not otherwise charged as an administration fee, an investment fee, a switching

fee, an exit fee, an activity fee or an insurance fee.

Buy/sell spreads A buy/sell spread is a fee to recover transaction costs incurred by the Trustee of the superannuation entity in relation to the sale and purchase of assets of the entity.

Exit fees An exit fee is a fee to recover the costs of disposing of all or part of members’ interests in the superannuation entity.

Indirect cost ratio The indirect cost ratio (ICR) for a MySuper product or an investment option offered by a superannuation entity, is the ratio of the total of the indirect costs for the MySuper product or investment option, to the total average net assets of the superannuation entity attributed to the MySuper product or investment option.Note: A dollar-based fee deducted directly from a member’s account is not included in the indirect cost ratio.

Investment fees An investment fee is a fee that relates to the investment of the assets of a superannuation entity and includes:(a) fees in payment for the exercise of care and expertise in the investment of those assets

(including performance fees); and(b) costs incurred by the Trustee of the entity that:

(i) relate to the investment of assets of the entity; and(ii) are not otherwise charged as an administration fee, a buy/sell spread, a switching fee, an

exit fee, an activity fee, an advice fee or an insurance fee.

Switching fees A switching fee is a fee to recover the costs of switching all or part of a member’s interest in the superannuation entity from one class of beneficial interest in the entity to another.

Why comparing fees is importantEvery fee you pay reduces the length of time that your retirement funds will last, so finding a fund with low fees can make a big difference to your future.

What makes REST different?As one of Australia’s largest industry super funds, our fees are low and we pay no commissions to financial advisers, planners or accountants.

Activity fee REST charges members for the following activity fee as outlined in the ‘Fees and other costs’ on page 9 of this Product Disclosure Statement.

10

Type of fee or cost Definition

Family law split fee The fee charged if we receive an order or agreement to split your superannuation with your spouse

Administration fees Following are worked examples of how the asset based fee is calculated.

Example - Administration fees

Asset based fee for an account balance of $150,000 is $150,000 x 0.18% = $270 per year

Asset based fee for an account balance of $400,000

First $300,000: $300,000 x 0.18% = $540

Next $100,000: $100,000 x 0.12% = $120

Total asset based fee: $540 + $120 = $660 per year

This example is illustrative only.

Other fees and costs The following fees and costs are charged to members as outlined in the ‘Fees and other costs’ table on page 9 of this PDS.

Type of fee or cost Definition

Personal advice fee The fee agreed between you and Money Solutions Pty Ltd (AFSL 258145) for personal superannuation advice.

Buy/sell spreads Member’s transactions may result in underlying assets being purchased or sold. These underlying asset transactions generally incur a transaction cost. Buy/sell spreads represent the estimated transaction costs, including brokerage fees and stamp duty, incurred when buying or selling underlying assets in relation to each investment option.

There will be a separate buy and sell unit price for each investment option, the difference between the prices representing the total buy/sell spread. When money is invested in an option it will generally use the buy price. When money is withdrawn from an option it will generally use the sell price.

Buy/sell spreads are not a fee paid to REST or investment managers but are used to meet underlying transaction costs when incurred. The spread charged will be an additional cost to you when you contribute or withdraw from your account, if you switch between investment options or any other transaction is processed in your account balance (for example deduction of fees or insurance fees).

If you transfer your account balance from one REST product to another (for example REST Super to REST Pension), a buy/sell spread will only apply if you also change the underlying investment options. If this occurs, your existing investment options will be transferred to REST Pension and you will be switched to your new investment options effective two business days after the transfer is finalised.

The buy/sell spreads are set by the Trustee and may change without prior notice. The spreads will be reviewed on a regular basis and available online at rest.com.au You should consider these costs when making any investment decision. For further information regarding the buy/sell spread, please refer to the ‘Buy-sell spread explained’ fact sheet available for download on rest.com.au

REST Pension Product Disclosure Statement | 11

Example of buy/sell spreadIf you have 25,000 units invested 100% in Core Strategy and decide to switch to 100% Balanced option, the buy/sell spreads would be calculated as follows, assuming the unit prices were:

Sell price for Core Strategy $1.0500

Buy price for Balanced $2.6624

Sell price for Balanced $2.660.

Transaction type Calculation

Sell Core Strategy 25,000 units at sell price of $1.0500 25,000 x $1.0500 = $26,250.00

Buy $26,250 of Balanced units at buy price of $2.6624 per unit $26,250 / $2.6624 = 9,859.52 units

Account balance after switch: 9,859.52 units at Balanced sell price of $2.6600 per unit

9,859.52 x $2.6600 = $26,226.32

Buy/sell spread (transaction cost): initial account balance prior to switch less account balance after switch

$26,250 - $26,226.32 = $23.68

This example is illustrative only.

Investment fees Investment fees include expenses that have been paid and/or accrued such as investment management fees (including performance fees), custody fees, investment adviser fees and other investment related costs. These expenses are accrued and reflected in an option’s unit price. They are not deducted directly from your account. The investment fee is expressed as an annual percentage of each investment option.

For each investment option, the investment fees (including performance fees) listed below are estimates only, which are based on the financial year ended 30 June 2015. Actual fees applied in the future may differ (ie higher or lower) from the estimated fees and may change without prior notice. Your annual statement will disclose the actual investment fees (including performance fees) applied for the year. For the latest investment fees please refer to rest.com.au

Investment option

Estimated performance fee pa

Total estimated investment fee pa (including

performance fee)

Buy spread range Sell spread*

Core Strategy 0.10% 0.63% 0.02 - 0.18% 0%

Cash Plus 0.02% 0.14% 0.01 - 0.03% 0%

Capital Stable 0.07% 0.44% 0.03 - 0.10% 0%

Balanced 0.09% 0.56% 0.04 - 0.12% 0%

Diversified 0.12% 0.70% 0.06 - 0.13% 0%

High Growth 0.13% 0.76% 0.07 - 0.16% 0%

Basic Cash 0.00% 0.05% 0.01 - 0.03% 0%

Cash 0.00% 0.04% 0.01 - 0.03% 0%

Bond 0.00% 0.18% 0.02 - 0.05% 0%

Shares 0.08% 0.60% 0.05 - 0.10% 0%

Property 0.04% 0.58% 0.31 - 0.47% 0%

Australian Shares 0.13% 0.59% 0.04 - 0.10% 0%

Overseas Shares 0.05% 0.60% 0.05 - 0.10% 0%

* As the sell spread is 0% there is no sell spread range.

3. Fees and other costs (continued)

12

Performance feesPerformance fees are included in, and increase investment fees, but don’t affect administration fees. They are not an additional fee. Performance fees change each year and vary for each investment option. REST pays performance fees to investment managers that outperform a defined investment return objective. Performance fees can affect any REST investment option, except Basic Cash. The percentage fee investment managers receive and the investment return objectives vary.

Performance fees for each investment manager may be calculated differently. However, they all have the following common elements:

• A performance fee is only payable to a manager if they exceed a target level of return;• Performance fees are calculated and accrued regularly (generally monthly) and incorporated into the calculation

of unit prices; and• Performance fees are typically payable annually.

Fee changesAll fees and charges are current and may be revised or adjusted by REST from time to time without your consent. We may also introduce new fees. Where there is an increase in fees or charges, we will give you at least 30 days prior notice, as required by law. This excludes investment fees which the Trustee reviews regularly.

TaxTaxes are set out on page 20.

Example of annual fees and costs for the Core Strategy investment option

This table gives an example of how fees and costs for the Core Strategy investment option for this superannuation product can affect your superannuation investment over a 1 year period. You should use this table to compare this superannuation product with other superannuation products.

Example – the Core Strategy investment option Balance of $50,000

Investment fees 0.63% pa including performance fee of 0.10%

For every $50,000 you have in the Core Strategy investment option you will be charged $315 each year

PLUS Administration fees $65 pa ($1.25 per week) plus 0.18% pa of your account balance at the end of the month

And, you will be charged $65 in administration fees regardless of your balance, plus $90

PLUS Indirect costs for the Core Strategy investment option

0% And, indirect costs of $0 each year will be deducted from your investment

EQUALS Cost of product If your balance was $50,000 then for that year you will be charged fees of $470 for the Core Strategy investment option.

Note: Additional fees may apply.

REST Pension Product Disclosure Statement | 13

Risk and return‘Risk’ means that returns might be variable (or ‘volatile’). Regardless of the investment options chosen, the value of your investment can fall as well as rise. Even where your investment does not fall in value, it may not perform according to your expectations. Risk can be minimised but it cannot be completely eliminated. There is always the chance that you may lose money on your investment. Even the most conservative investments carry some risk, but some investments are riskier than others. Generally, the higher risk an investment has, the greater its potential return. Investments like shares and property are generally considered ‘high risk’ or ‘growth’ assets.

Investments like cash and bonds are generally considered ‘low risk’ or ‘defensive’ assets. The diagram on this page indicates roughly where each of REST Pension’s investment options fits on a scale of ‘defensive’ to ‘growth’.

Please see page 25 for further information on types of assets.

It is important to consider the risks of investing in superannuation, as the decisions you make will influence whether you have enough superannuation savings to adequately provide for your retirement.

All investments have some level of risk. Super funds invest in a range of asset classes – for example, cash, bonds, property and shares – that have different levels of risk. The likely investment return, and the risk of a negative return, is different for each investment option depending on the underlying mix of assets in the relevant investment option. Assets with the highest potential return over the longer term (such as shares), generally also have the highest risk of negative returns over the short-term.

When considering your investment in super, it is important to understand that:

• the value of investment options can go up and down• future returns may differ from past returns• returns are not guaranteed, will vary, and you may lose

some of your money• superannuation, social security and laws may change

in the future• the amount of your future superannuation savings

(including contributions and returns) may not be enough to adequately provide for your retirement.

The appropriate level of risk for you will vary depending on a range of factors including your age, investment time frame, where your other assets are invested and how comfortable you are with the possibility of a negative return in some years.

Other significant risks include:• market risk – investment returns may be affected by

economic conditions, government regulations, market sentiment, international events and other factors

• company specific risk – an investment in a specific company may be affected by changes to the company such as loss of a major customer, changes in management and other internal and external factors

• currency risk – investments in international assets may be negatively affected by currency fluctuations

• interest rate risk – changes in interest rates in Australia and overseas can have a direct or indirect impact upon the value and return of all types of assets

• liquidity risk – from time to time some investments may not be easily converted to cash due to abnormal or difficult market conditions

4. Investment options and risk

REST Pension offers 13 investment options. You can decide which investment option (or combination of options) is right for you.

Growth

Asset Type

Defensive

Cash Plus

Cash

Basic Cash

Capital Stable

Balanced

Diversified

Shares

Core Strategy

HighGrowth

OverseasShares

Australian Shares

Property

Bond

Your investment choices

1 2 3 4 5 6 7Lower risk Risk band and level Higher risk

14

• adequacy risk – the risk that your super savings may be insufficient to generate the retirement income that meets your retirement needs

• inflation risk – the risk that your super savings are unable to keep up with the rising cost of living over time (inflation)

• longevity risk – the risk that you will outlive your retirement savings.

What is the Standard Risk Measure telling us?The Standard Risk Measure calculates risk in terms of the likelihood of achieving a negative return in any one year ie it describes expected volatility in investment markets which is actually just one way that you could think about risk.

There’s no such thing as not taking any investment risk. The type and degree of risk will vary depending on the investments you choose. Every investment holds some level of risk. Only you know how much risk you’re comfortable with. What’s important is that you find the right balance of risk and reward to help you meet your long-term goals, regardless of what happens in the short term. Your risk tolerance depends on several factors, including your age, when you’ll need your money, your financial needs and your assets. The risk measure helps highlight the probability of the number of negative annual returns over a 20 year period. The expected chance of loss is on a before tax basis not taking into account imputation credits, and is before administration fees, but after taking account of investment management fees.

The Standard Risk Measure is not a complete assessment of all forms of investment risk. For example, it will not predict when market declines will happen, or, how long a decline will last. Importantly, it does not detail what the size of a negative return could be or take into account the potential for a positive return to be less than you may require to meet your investment objectives.

What are some different ways of thinking about risk?Many people define risk as the volatility of the markets, especially in the short run. That’s why, over the long run, your time frame is perhaps the most critical component in planning your investments.

A more complete measure of risk might be the risk that you do not save enough and invest appropriately during your working life to achieve the level of retirement income that you aspire to.

This may be due to the adequacy risk, longevity risk or inflation risk outlined above.

Adequacy and longevity risk A few factors are at play when considering the adequacy of your super savings, including your super balance, the regular income required (which might affect your withdrawal rate) and your retirement plans. A related risk is that you outlive your retirement savings required for you to live per your retirement plans.

Inflation riskOne big risk most investors face is that their purchasing power will be eroded by rising prices due to inflation. ‘Playing it safe’ and accepting lower market volatility also generally means accepting the potential for lower returns – a risky strategy if you are trying to keep up with or beat inflation. Some investment options have inflation or Consumer Price Index (CPI) included as part of their objectives, so this is worth considering when selecting the most appropriate options for your retirement needs.

Market risk If you’re close to retirement, you may not have the time to ride out a market downturn. Your tolerance for volatile returns may be lower and you may want to consider investments that historically produce smoother returns from year-to-year. However, even after you retire, you may still want to keep some of your assets in growth-oriented investments — after all, you may be retired for 10, 20 years or more.

The following pages outline REST Pension’s investment options in detail. This information will help you compare the different investment options so you can make an informed investment choice that’s right for you.

The investment return objectives quoted on pages 16 to 19 of this document are not guaranteed.

Your investment in REST is not guaranteed, and it can rise or fall in value. The returns indicated for each investment option reflect past performance of investment markets that may not be repeated in the future. Past performance is not an indication of future performance. You should consider obtaining financial advice before making a decision.

REST Pension Product Disclosure Statement | 15

Core Strategy Structured options

Cash Plus Capital Stable Balanced Diversified High Growth

Aim1 To achieve a balance of risk and return by investing in both growth assets and defensive assets

Maintain the purchasing power of the funds invested by earning a slightly higher return on cash while minimising the risk of any capital loss

A stable pattern of returns that at the same time maintains a low probability of a negative return in any 1 year

A good balance of risk and return by investing in approximately equal proportions of growth assets and defensive assets

Strong returns over the longer term by investing in a diversified mix of assets weighted towards shares and other growth assets

Maximise returns over the long-term by investing predominantly in growth assets

Investmentreturn objective2

CPI + 3% pa over the long-term (rolling 10 year period)

Outperform the Bloomberg AusBond Bank Bill Index over the short term (rolling 2 year period)

CPI + 1% pa over the medium-term (rolling 4 year period)

CPI + 2% pa over the medium-term (rolling 6 year period)

CPI + 3% pa over the long-term (rolling 10 year period)

CPI + 4% pa over the very long-term (rolling 12 year period)

Asset allocation3

22% defensive, 78% growthA mix of shares and bonds (both Australian and overseas), property, infrastructure, alternative assets and cash

6%11%

19%

29%

6%

10%

13%

6%

Cash securities 6% (0-25%) Bonds 6% (5-75%) Defensive alternatives 10% (0-25%) Growth alternatives 13% (0-25%) Infrastructure 6% (0-15%) Property 11% (0-25%) Australian shares 19% (15-45%) Overseas shares 29% (5-35%)

100% defensiveCash plus a small allocation to Defensive Alternatives. Cash consists of a portfolio of securities with a low level of interest rate risk (12 months or less), including bank deposits, bank bills, commercial paper and floating rate notes, for example, residential mortgage backed securities

10% 90%

Cash securities 90% Defensive alternatives 10%

62% defensive, 38% growthMainly bonds (both Australian and overseas) and cash, with smaller proportions of shares (both Australian and overseas), property, infrastructure and alternative assets

32%

16%14%

9%

4%

5%

8%

12%

Cash securities 32% Bonds 16% Defensive alternatives 14% Growth alternatives 9% Infrastructure 4% Property 5% Australian shares 8% Overseas shares 12%

43% defensive, 57% growthA mix of shares and bonds (both Australian and overseas), property, infrastructure, alternative assets and cash

20%

10%

13%

10%5%7%

14%

21%

Cash securities 20% Bonds 10% Defensive alternatives 13% Growth alternatives 10% Infrastructure 5% Property 7% Australian shares 14% Overseas shares 21%

22% defensive, 78% growthAustralian and overseas shares, property, infrastructure, alternative assets, plus lesser amounts of bonds (both Australian and overseas) and cash

6%7%

7%

9%

9%21%

30%

11%

Cash securities 6% Bonds 7% Defensive alternatives 9% Growth alternatives 11% Infrastructure 7% Property 9% Australian shares 21% Overseas shares 30%

7% defensive, 93% growthAustralian and overseas shares, property, infrastructure and alternative assets

7%

12%

7%

10%

26%

38%

Defensive alternatives 7% Growth alternatives 12% Infrastructure 7% Property 10% Australian shares 26% Overseas shares 38%

Minimum suggested timeframe

10+ years 2+ years 4+ years 6+ years 10+ years 12+ years

Standard risk measure4

Estimated number of negative annual returns over any 20 year period, 3 to less than 4

Estimated number of negative annual returns over any 20 year period, less than 0.5 of a year

Estimated number of negative annual returns over any 20 year period, 1 to less than 2

Estimated number of negative annual returns over any 20 year period, 2 to less than 3

Estimated number of negative annual returns over any 20 year period, 3 to less than 4

Estimated number of negative annual returns over any 20 year period, 4 to less than 6

Risk band and level5 Risk band 5, Medium to High Risk band 1, Very Low Risk band 3, Low to Medium Risk band 4, Medium Risk band 5, Medium to High Risk band 6, High

What this option has returned6

Past performance is not an indication of future performance

Yearly return2011 10.71%2012 1.18%2013 20.76%2014 14.41%2015 9.93%

Annualised returnFive year 11.21%Ten year n/a

Yearly return2011 5.49%2012 4.77%2013 4.34%2014 3.43%2015 3.16%

Annualised returnFive year 4.24%Ten year 4.67%

Yearly return2011 8.41%2012 5.25%2013 11.88%2014 8.40%2015 8.00%

Annualised returnFive year 8.37%Ten year 7.03%

Yearly return2011 9.49%2012 3.42%2013 15.92%2014 11.01%2015 9.93%

Annualised returnFive year 9.88%Ten year 7.66%

Yearly return2011 10.60%2012 1.20%2013 21.26%2014 14.35%2015 12.40%

Annualised returnFive year 11.77%Ten year 8.53%

Yearly return2011 11.19%2012 -0.46%2013 24.50%2014 16.30%2015 13.97%

Annualised returnFive year 12.80%Ten year 8.91%

Investment options with an exposure to the Australian shares asset class may include companies listed in Australia whose legal domicile is overseas. In addition, up to 10% of this asset class may be invested in stocks listed on the New Zealand Stock Exchange.† The Core Strategy’s returns are based on unit pricing from 1 January 2013 onwards. Prior to that a crediting rate was used.1. Aim - This is the goal or objective of the investment option. 2. Investment return objective - This is what the Trustee uses to determine asset allocation. It is also used to measure if the investment objective

is met. It is not a guaranteed rate of return. REST does not use the Return Target (shown in the Product Dashboard) to set the investment return objective.

3. Asset allocation - For the Core Strategy option, the asset allocation will vary year to year within the ranges shown in brackets. This also means the allocation to defensive assets and growth assets will vary from time to time. The Trustee reserves the right to vary the asset allocations, including the benchmarks and ranges, of all or any of the investment options, introduce new options or close or terminate existing options without prior notice (where permitted by law).

16

Core Strategy Structured options

Cash Plus Capital Stable Balanced Diversified High Growth

Aim1 To achieve a balance of risk and return by investing in both growth assets and defensive assets

Maintain the purchasing power of the funds invested by earning a slightly higher return on cash while minimising the risk of any capital loss

A stable pattern of returns that at the same time maintains a low probability of a negative return in any 1 year

A good balance of risk and return by investing in approximately equal proportions of growth assets and defensive assets

Strong returns over the longer term by investing in a diversified mix of assets weighted towards shares and other growth assets

Maximise returns over the long-term by investing predominantly in growth assets

Investmentreturn objective2

CPI + 3% pa over the long-term (rolling 10 year period)

Outperform the Bloomberg AusBond Bank Bill Index over the short term (rolling 2 year period)

CPI + 1% pa over the medium-term (rolling 4 year period)

CPI + 2% pa over the medium-term (rolling 6 year period)

CPI + 3% pa over the long-term (rolling 10 year period)

CPI + 4% pa over the very long-term (rolling 12 year period)

Asset allocation3

22% defensive, 78% growthA mix of shares and bonds (both Australian and overseas), property, infrastructure, alternative assets and cash

6%11%

19%

29%

6%

10%

13%

6%

Cash securities 6% (0-25%) Bonds 6% (5-75%) Defensive alternatives 10% (0-25%) Growth alternatives 13% (0-25%) Infrastructure 6% (0-15%) Property 11% (0-25%) Australian shares 19% (15-45%) Overseas shares 29% (5-35%)

100% defensiveCash plus a small allocation to Defensive Alternatives. Cash consists of a portfolio of securities with a low level of interest rate risk (12 months or less), including bank deposits, bank bills, commercial paper and floating rate notes, for example, residential mortgage backed securities

10% 90%

Cash securities 90% Defensive alternatives 10%

62% defensive, 38% growthMainly bonds (both Australian and overseas) and cash, with smaller proportions of shares (both Australian and overseas), property, infrastructure and alternative assets

32%

16%14%

9%

4%

5%

8%

12%

Cash securities 32% Bonds 16% Defensive alternatives 14% Growth alternatives 9% Infrastructure 4% Property 5% Australian shares 8% Overseas shares 12%

43% defensive, 57% growthA mix of shares and bonds (both Australian and overseas), property, infrastructure, alternative assets and cash

20%

10%

13%

10%5%7%

14%

21%

Cash securities 20% Bonds 10% Defensive alternatives 13% Growth alternatives 10% Infrastructure 5% Property 7% Australian shares 14% Overseas shares 21%

22% defensive, 78% growthAustralian and overseas shares, property, infrastructure, alternative assets, plus lesser amounts of bonds (both Australian and overseas) and cash

6%7%

7%

9%

9%21%

30%

11%

Cash securities 6% Bonds 7% Defensive alternatives 9% Growth alternatives 11% Infrastructure 7% Property 9% Australian shares 21% Overseas shares 30%

7% defensive, 93% growthAustralian and overseas shares, property, infrastructure and alternative assets

7%

12%

7%

10%

26%

38%

Defensive alternatives 7% Growth alternatives 12% Infrastructure 7% Property 10% Australian shares 26% Overseas shares 38%

Minimum suggested timeframe

10+ years 2+ years 4+ years 6+ years 10+ years 12+ years

Standard risk measure4

Estimated number of negative annual returns over any 20 year period, 3 to less than 4

Estimated number of negative annual returns over any 20 year period, less than 0.5 of a year

Estimated number of negative annual returns over any 20 year period, 1 to less than 2

Estimated number of negative annual returns over any 20 year period, 2 to less than 3

Estimated number of negative annual returns over any 20 year period, 3 to less than 4

Estimated number of negative annual returns over any 20 year period, 4 to less than 6

Risk band and level5 Risk band 5, Medium to High Risk band 1, Very Low Risk band 3, Low to Medium Risk band 4, Medium Risk band 5, Medium to High Risk band 6, High

What this option has returned6

Past performance is not an indication of future performance

Yearly return2011 10.71%2012 1.18%2013 20.76%2014 14.41%2015 9.93%

Annualised returnFive year 11.21%Ten year n/a

Yearly return2011 5.49%2012 4.77%2013 4.34%2014 3.43%2015 3.16%

Annualised returnFive year 4.24%Ten year 4.67%

Yearly return2011 8.41%2012 5.25%2013 11.88%2014 8.40%2015 8.00%

Annualised returnFive year 8.37%Ten year 7.03%

Yearly return2011 9.49%2012 3.42%2013 15.92%2014 11.01%2015 9.93%

Annualised returnFive year 9.88%Ten year 7.66%

Yearly return2011 10.60%2012 1.20%2013 21.26%2014 14.35%2015 12.40%

Annualised returnFive year 11.77%Ten year 8.53%

Yearly return2011 11.19%2012 -0.46%2013 24.50%2014 16.30%2015 13.97%

Annualised returnFive year 12.80%Ten year 8.91%

4. Standard risk measure - This is a guide as to the likely number of negative annual returns expected over any 20 year period. See ‘What is the Standard Risk Measure telling us?’ section on page 14.

5. Risk band and level - The risk band and risk level is based on the Standard Risk Measure. The Standard Risk Measure includes seven risk bands, from 1 (very low risk) to 7 (very high risk). Refer to page 14 for more information on Standard Risk Measure.

6. What this option has returned - Returns are net of investment fees and untaxed as at 30 June. The returns are based on the valuation of the underlying assets as at 30 June.

REST Pension Product Disclosure Statement | 17

Investment options with an exposure to the Australian shares asset class may include companies listed in Australia whose legal domicile is overseas. In addition, up to 10% of this asset class may be invested in stocks listed on the New Zealand Stock Exchange.1. Aim - This is the goal or objective of the investment option. 2. Investment return objective - This is what the Trustee uses to determine asset allocation. It is also used to measure if the investment objective

is met. It is not a guaranteed rate of return. REST does not use the Return Target (shown in the Product Dashboard) to set the investment return objective.

3. Asset allocation - For the Core Strategy option, the asset allocation will vary year to year within the ranges shown in brackets. This also means the allocation to defensive assets and growth assets will vary from time to time. The Trustee reserves the right to vary the asset allocations,

Member-tailored options

Basic Cash Cash Bond Property Shares Australian Shares Overseas Shares

Aim1 Provide members with the opportunity to construct portfolios that are appropriate to their own particular circumstances. A member’s portfolio may be constructed from 1 or more of the Basic Cash, Cash, Bond, Property, Shares, Australian Shares and Overseas Shares options, as well as from the Structured options and the Core Strategy. This permits the construction of members’ portfolios with an extremely wide range of risk/return objectives.

Provide you with the opportunity to construct a portfolio that is appropriate to your own particular circumstances. Your portfolio may be constructed from 1 or more of the Basic Cash, Cash, Bond, Property, Shares, Australian Shares and Overseas Shares options, as well as from the structured options and the Core Strategy. This permits the construction of members’ portfolios with an extremely wide range of risk/return objectives.

Investmentreturn objective2

Match the return of the Reserve Bank cash rate target before tax and before fees over rolling 1 year period.

Perform in line with the Bloomberg AusBond Bank Bill Index (before tax and after fees) over rolling 1 year period.

Outperform the benchmark return (before tax and after fees) over rolling 2 year period.

The benchmark is calculated using the Bloomberg AusBond Composite 0+ Yr Index, Bloomberg AusBond Inflation 0+ Yr Index, Citigroup World Government Bond Index (hedged), and Barclays Global Inflation linked Bond Index (hedged).

Outperform both the Mercer Unlisted Property Index (before tax and after fees) over rolling 3 year period and the 10 year bond rate plus 3% pa over rolling 5 year period.

Outperform the benchmark return (before tax and after fees) over rolling 3 year period. The benchmark is calculated using the S&P/ASX 300 Accumulation Index and the MSCI All Country World ex-Australia Index in AUD.

Outperform the S&P/ASX 300 Accumulation Index (after fees and including an estimation of imputation credits) over rolling 3 year period.

Outperform the MSCI All Country World ex-Australia Index in AUD (before tax and after fees) over rolling 3 year period.

Asset allocation3

100% defensive

The portfolio will invest in deposits with, or short-term discount securities (bank bills and negotiable certificates of deposit) issued by, banks rated at least AA- at the time of purchase. It may also invest in short-dated debt issued and guaranteed by the Australian Commonwealth or State Governments. All securities will have a maximum term to maturity of three months

100%

Cash securities 100%

100% defensive

A portfolio of securities with a low level of interest rate risk (12 months or less), including bank deposits, bank bills, commercial paper and floating rate notes, for example, residential mortgage backed securities

100%

Cash securities 100%

100% defensive

A mixture of Australian and overseas debt securities issued by Governments, semi-government authorities and companies

100%

Bonds 100%

100% growth (For further information, please see page 24)

100%

Property 100%

100% growth

A mixture of Australian and overseas shares

40%60%

Australian shares 40% Overseas shares 60%

100% growth

90-100% Australian shares. Limited exposure of up to 10% listed New Zealand shares

100%

Australian shares 100%

100% growth

100%

Overseas shares 100%

Minimum suggested timeframe

3 months or less 1 to 2 years 4+ years 10+ years 12+ years 12+ years 12+ years

Standard risk measure4

Estimated number of negative annual returns over any 20 year period, less than 0.5 of a year

Estimated number of negative annual returns over any 20 year period, less than 0.5 of a year

Estimated number of negative annual returns over any 20 year period, 3 to less than 4

Estimated number of negative annual returns over any 20 year period, 3 to less than 4

Estimated number of negative annual returns over any 20 year period, 4 to less than 6

Estimated number of negative annual returns over any 20 year period, 6 years or greater

Estimated number of negative annual returns over any 20 year period, 4 to less than 6

Risk band and level5 Risk band 1, Very low Risk band 1, Very low Risk band 5, Medium to High Risk band 5,

Medium to High Risk band 6, High Risk band 7, Very High Risk band 6, High

What this option has returned6

Past performance is not an indication of future performance

Yearly return2011 4.99%2012 4.45%2013 3.19%2014 2.61%2015 2.40%

Annualised return Five year 3.52%Ten year n/a

Yearly return2011 5.54%2012 4.71%2013 3.79%2014 3.09%2015 2.89%

Annualised returnFive year 4.00%Ten year 4.65%

Yearly return2011 7.52%2012 10.63%2013 8.43%2014 5.83%2015 6.72%

Annualised returnFive year 7.81%Ten year 7.26%

Yearly return2011 7.36%2012 6.15%2013 7.86%2014 8.80%2015 6.78%

Annualised returnFive year 7.39%Ten year 6.79%

Yearly return2011 9.46%2012 -4.17%2013 30.99%2014 20.89%2015 16.87%

Annualised returnFive year 14.19%Ten year 8.95%

Yearly return2011 14.47%2012 -4.88%2013 25.70%2014 20.30%2015 8.48%

Annualised returnFive year 12.30%Ten year 9.79%

Yearly return2011 4.78%2012 -3.55%2013 34.90%2014 21.97%2015 22.74%

Annualised returnFive year 15.34%Ten year 7.37%

18

including the benchmarks and ranges, of all or any of the investment options, introduce new options or close or terminate existing options without prior notice (where permitted by law).

4. Standard risk measure - This is a guide as to the likely number of negative annual returns expected over any 20 year period. See ‘What is the Standard Risk Measure telling us?’ section on page 14.

5. Risk band and level - The risk band and risk level is based on the Standard Risk Measure. The Standard Risk Measure includes seven risk bands, from 1 (very low risk) to 7 (very high risk). Refer to page 14 for more information on Standard Risk Measure.

6. What this option has returned - Returns are net of investment fees and untaxed as at 30 June. The returns are based on the valuation of the underlying assets as at 30 June.

Member-tailored options

Basic Cash Cash Bond Property Shares Australian Shares Overseas Shares

Aim1 Provide members with the opportunity to construct portfolios that are appropriate to their own particular circumstances. A member’s portfolio may be constructed from 1 or more of the Basic Cash, Cash, Bond, Property, Shares, Australian Shares and Overseas Shares options, as well as from the Structured options and the Core Strategy. This permits the construction of members’ portfolios with an extremely wide range of risk/return objectives.

Provide you with the opportunity to construct a portfolio that is appropriate to your own particular circumstances. Your portfolio may be constructed from 1 or more of the Basic Cash, Cash, Bond, Property, Shares, Australian Shares and Overseas Shares options, as well as from the structured options and the Core Strategy. This permits the construction of members’ portfolios with an extremely wide range of risk/return objectives.

Investmentreturn objective2

Match the return of the Reserve Bank cash rate target before tax and before fees over rolling 1 year period.

Perform in line with the Bloomberg AusBond Bank Bill Index (before tax and after fees) over rolling 1 year period.

Outperform the benchmark return (before tax and after fees) over rolling 2 year period.

The benchmark is calculated using the Bloomberg AusBond Composite 0+ Yr Index, Bloomberg AusBond Inflation 0+ Yr Index, Citigroup World Government Bond Index (hedged), and Barclays Global Inflation linked Bond Index (hedged).

Outperform both the Mercer Unlisted Property Index (before tax and after fees) over rolling 3 year period and the 10 year bond rate plus 3% pa over rolling 5 year period.

Outperform the benchmark return (before tax and after fees) over rolling 3 year period. The benchmark is calculated using the S&P/ASX 300 Accumulation Index and the MSCI All Country World ex-Australia Index in AUD.

Outperform the S&P/ASX 300 Accumulation Index (after fees and including an estimation of imputation credits) over rolling 3 year period.

Outperform the MSCI All Country World ex-Australia Index in AUD (before tax and after fees) over rolling 3 year period.

Asset allocation3

100% defensive

The portfolio will invest in deposits with, or short-term discount securities (bank bills and negotiable certificates of deposit) issued by, banks rated at least AA- at the time of purchase. It may also invest in short-dated debt issued and guaranteed by the Australian Commonwealth or State Governments. All securities will have a maximum term to maturity of three months

100%

Cash securities 100%

100% defensive

A portfolio of securities with a low level of interest rate risk (12 months or less), including bank deposits, bank bills, commercial paper and floating rate notes, for example, residential mortgage backed securities

100%

Cash securities 100%

100% defensive

A mixture of Australian and overseas debt securities issued by Governments, semi-government authorities and companies

100%

Bonds 100%

100% growth (For further information, please see page 24)

100%

Property 100%

100% growth

A mixture of Australian and overseas shares

40%60%

Australian shares 40% Overseas shares 60%

100% growth