residential markets

DESCRIPTION

Residential markets in France, Germany and the Netherlands and Researchwork in the real estate marketTRANSCRIPT

Residential markets in France,

Germany and the Netherlands

and Researchwork in the

real estate market

Bucarest 24th.october 2013

Han Joosten,

Director Market Research

A leading European area developer

Known fact:

• The requirements of living and area

development are changing constantly

Bouwfonds Property Development turns

these changes for the better

• Development of areas based on careful

consideration of use, space, community

need and sustainability

• Makes the everyday things affordable and

the special things achievable

That’s how we provide the best solution to

every need of:

• residents

• end-users

• governments

• market players

• the environment

How do we improve the quality of

entire areas? 1 2

3

Development of integrated residential

areas and small-scale mixed-use projects

Development in a wide range of locations:

• in suburban and rural areas

• in city centres

• in restructuring sites

• in changed-use areas

On all possible levels:

• from 6 to 6,000 houses

• from reasonably priced to the luxury

segment

Also development of public facilities:

• schools, shops, care centres

• parks, gardens and water

• public areas

Overall direction of risk-bearing

exploitations of the area

• acquisition

• head for the area exploitation process

• in cooperation with local governements

Cooperation: basis for success

• local governments

• housing corporation

• market players

• public organisations

• end-users

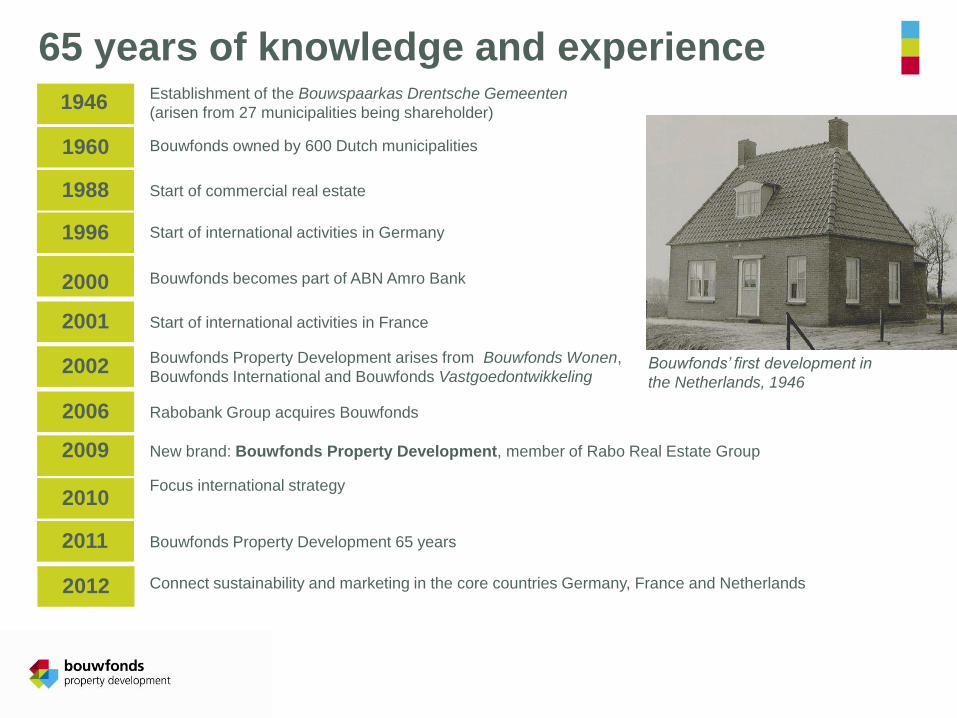

65 years of knowledge and experience Establishment of the Bouwspaarkas Drentsche Gemeenten

(arisen from 27 municipalities being shareholder) 1946

1960

1988

1996

2000

2001

2002

2006

2009

Bouwfonds owned by 600 Dutch municipalities

Start of commercial real estate

Start of international activities in Germany

Bouwfonds becomes part of ABN Amro Bank

Start of international activities in France

Bouwfonds Property Development arises from Bouwfonds Wonen,

Bouwfonds International and Bouwfonds Vastgoedontwikkeling

Rabobank Group acquires Bouwfonds

New brand: Bouwfonds Property Development, member of Rabo Real Estate Group

Bouwfonds’ first development in

the Netherlands, 1946

2010 Focus international strategy

2011 Bouwfonds Property Development 65 years

2012 Connect sustainability and marketing in the core countries Germany, France and Netherlands

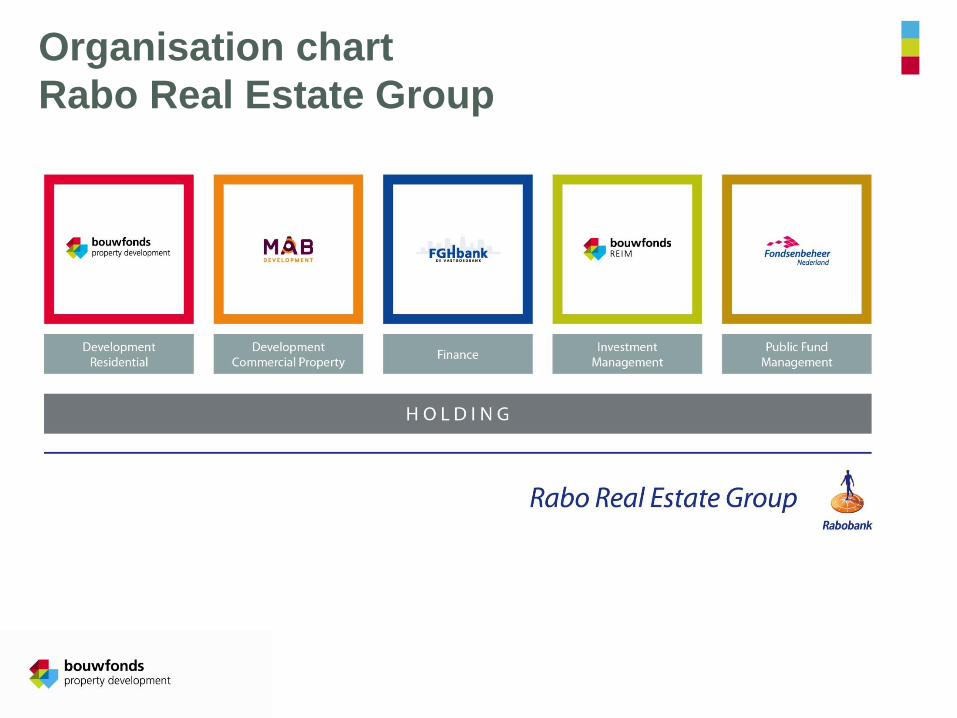

Organisation chart

Rabo Real Estate Group

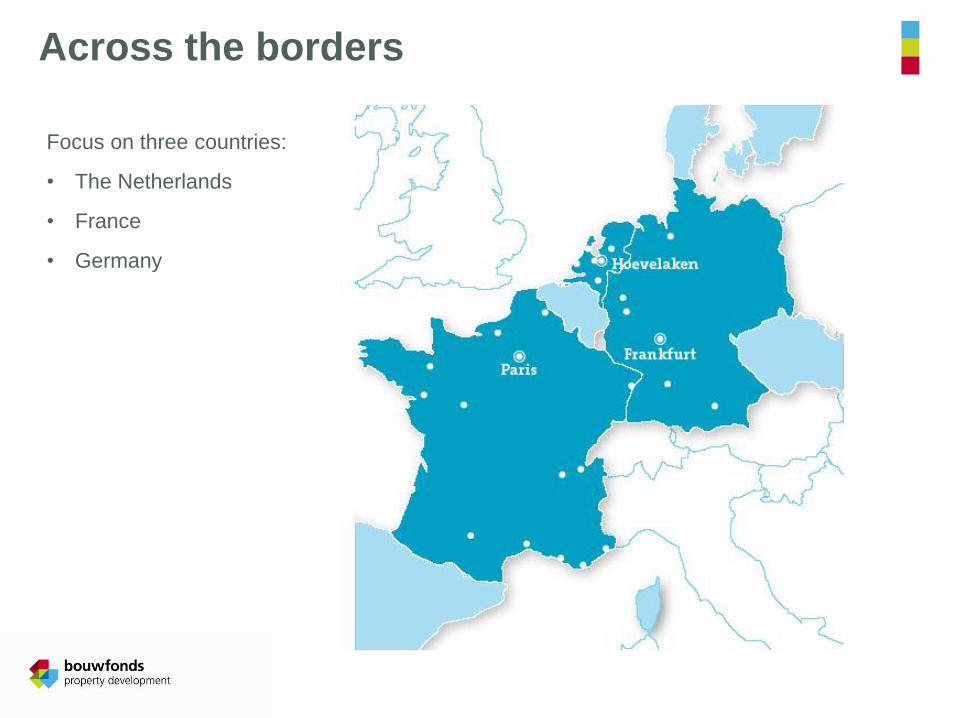

Across the borders

Focus on three countries:

• The Netherlands

• France

• Germany

A leading European area developer

From a typical Dutch organisation to a

successful international company

Exporting the ‘product’ area

development

A pan-European focus with a local

approach

• Continuous communication between

the various international offices

• International experience and knowledge

of European trends and best practices

are shared effectively and efficiently

Result: prominent residential area

developer in France and Germany

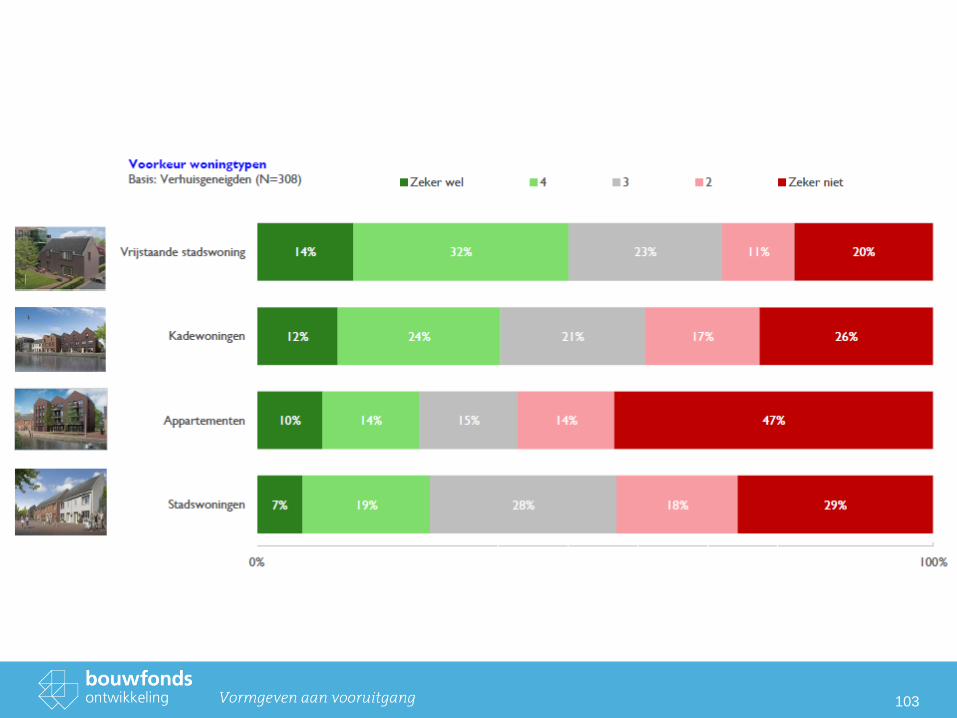

Above 65 years of in-depth expertise

Usage and expansion of real estate expertise

• International experience and knowledge are being

translated to local circumstances

• Knowledge of local markets by track record and by

continuous market research

Also a keen eye for developments in society

• Thanks to 55 years of ownership by 600 Dutch

municipalities

Development in a wide range of projects

• Partnerships with governments, market players and

end-users

• Small and large-scale projects

• Innovative, sustainable and realistic projects

• Projects that improve the quality of entire areas

Aiming at the highest level of quality

Solid and experienced in process management

• High quality of the development proces

• Cooperation: building partnerships

• Having an eye for return and risk

• In-depth knowledge of architecture and town

planning

Looking for winning ideas

• Development of prominent concepts, adjusted to

the needs of a specific target audience

High standards for customer satisfaction

• Client demand: the most important basis for area

development

Enterprising way of area development

Innovative

• On a small-scale development of excellent

concepts and invest in them

• Application of proven innovations

Visionary

• Having and communicating notions regarding

relevant issues

• Active participation in public discussions

• Inspiring the development of the specialism of

area development

Start early

Participate timely

• Perceiving opportunities

• Start the planning process at an early stage

Development of concepts

• Introduce a new concept of area development and apply it

to several locations

Location management

• Conditioning area development

• Shaping processes and procedures

• Assisting the public authorities

Cooperations

• Building partnerships with local governments, market

players, housing corporations, social organisations, end-

users, Rabobank and its local banks, our related

organisations at Rabo Real Estate Group

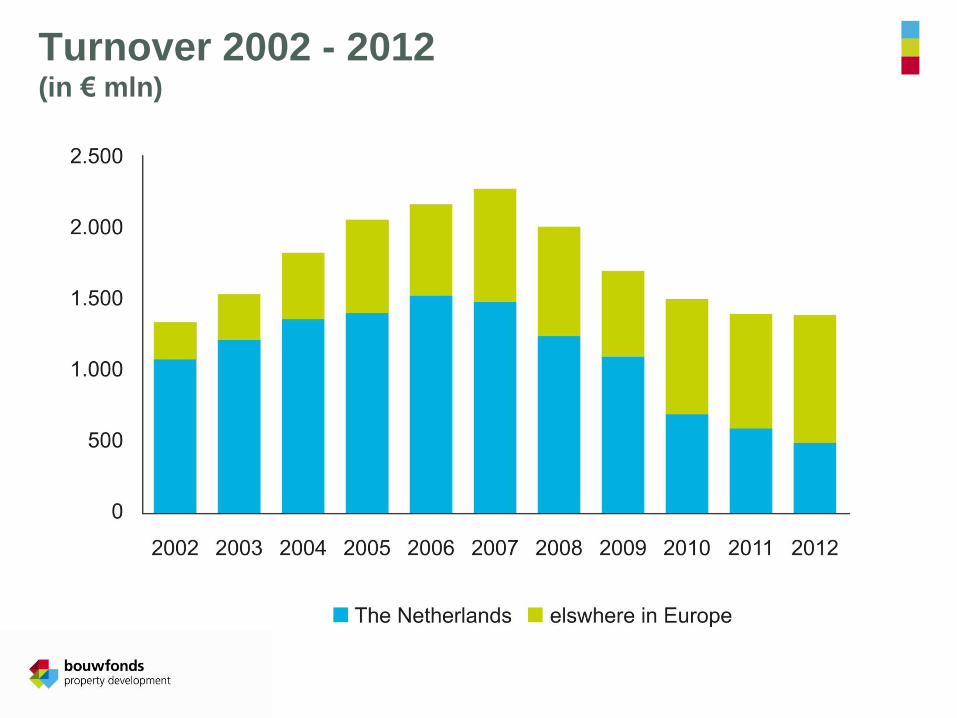

Facts & figures

Turnover 2002 - 2012 (in € mln)

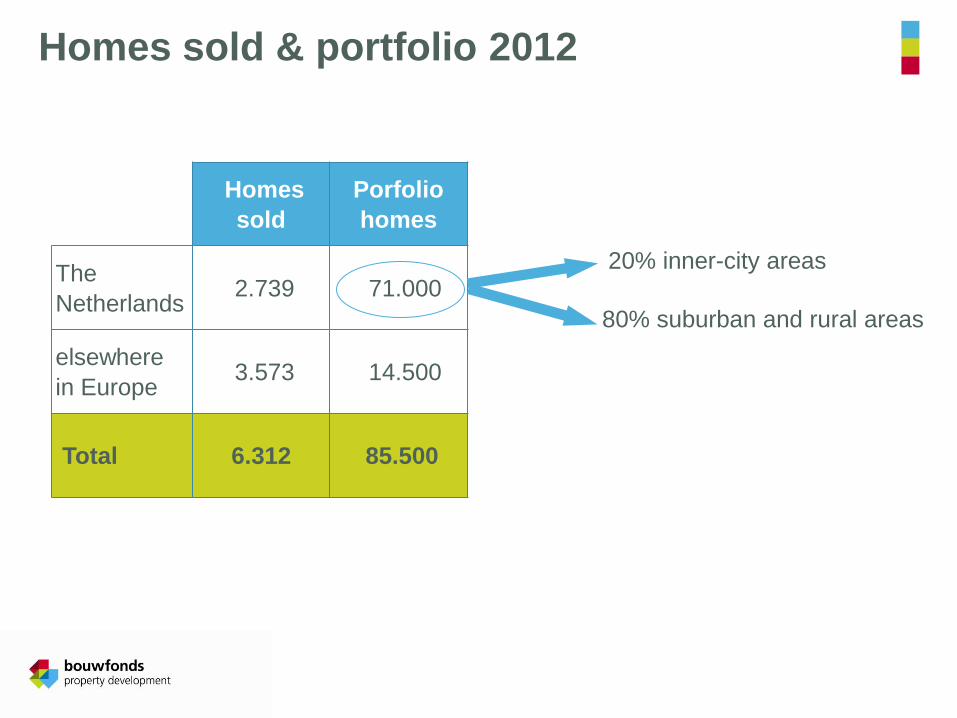

Homes sold & portfolio 2012

Homes

sold

Porfolio

homes

The

Netherlands 2.739 71.000

elsewhere

in Europe 3.573 14.500

Total 6.312 85.500

20% inner-city areas

80% suburban and rural areas

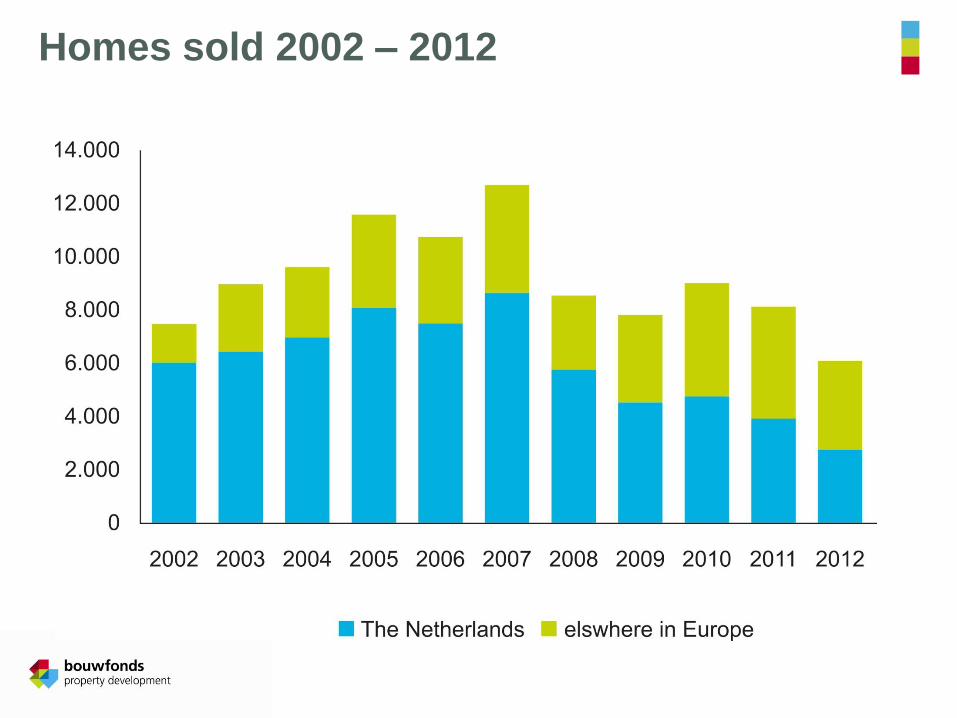

Homes sold 2002 – 2012

Show cases

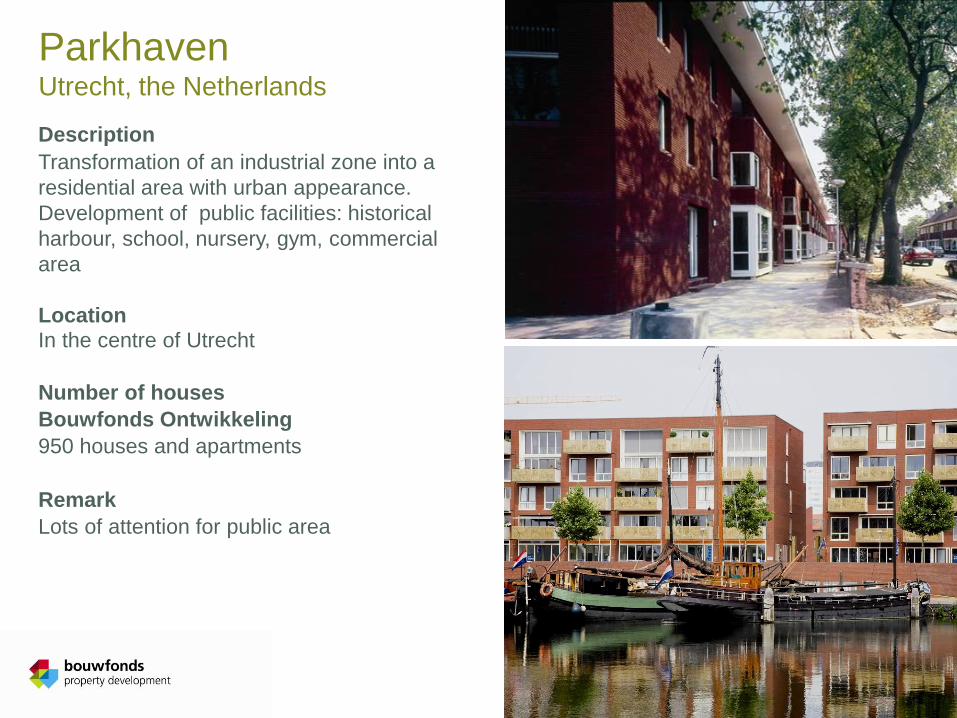

Parkhaven Utrecht, the Netherlands

Description

Transformation of an industrial zone into a

residential area with urban appearance.

Development of public facilities: historical

harbour, school, nursery, gym, commercial

area

Location In the centre of Utrecht

Number of houses

Bouwfonds Ontwikkeling

950 houses and apartments

Remark

Lots of attention for public area

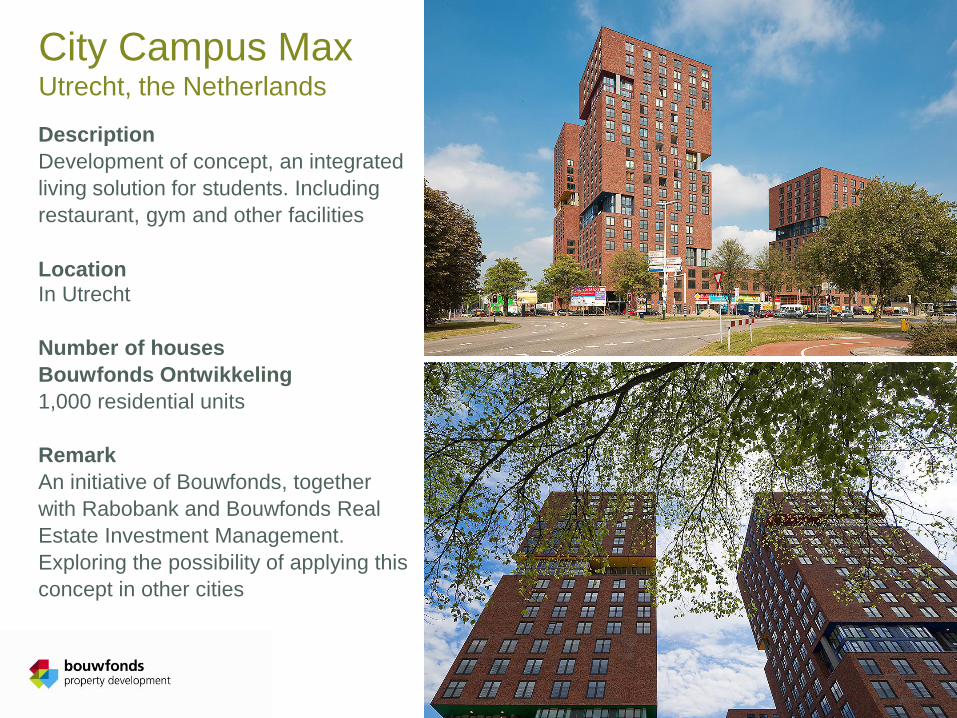

City Campus Max Utrecht, the Netherlands

Description

Development of concept, an integrated

living solution for students. Including

restaurant, gym and other facilities

Location

In Utrecht

Number of houses

Bouwfonds Ontwikkeling

1,000 residential units

Remark

An initiative of Bouwfonds, together

with Rabobank and Bouwfonds Real

Estate Investment Management.

Exploring the possibility of applying this

concept in other cities

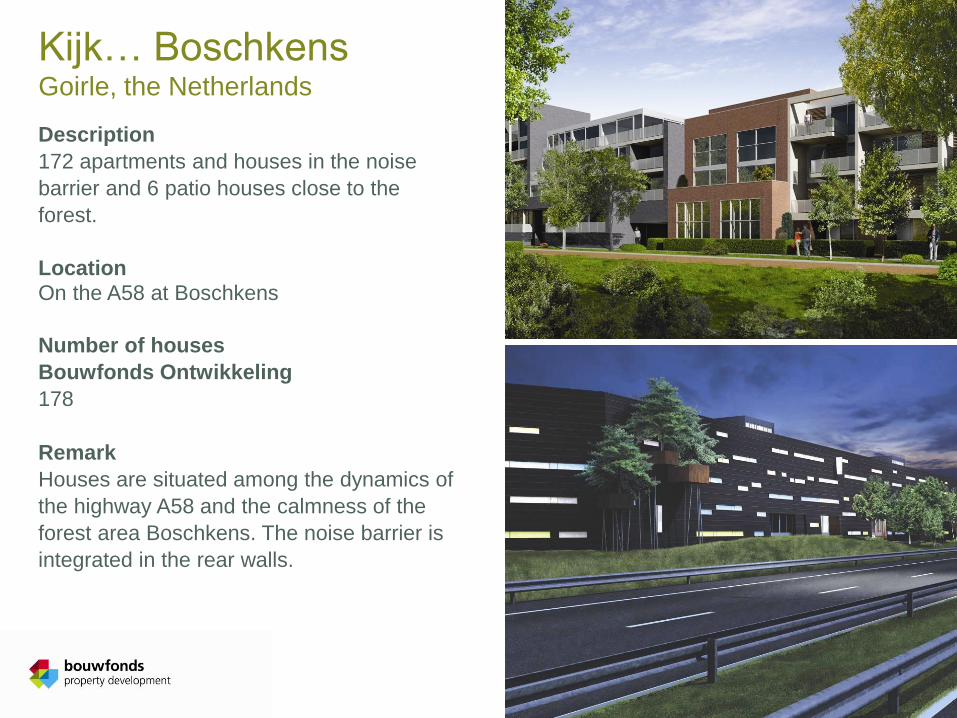

Kijk… Boschkens Goirle, the Netherlands

Description

172 apartments and houses in the noise

barrier and 6 patio houses close to the

forest.

Location

On the A58 at Boschkens

Number of houses

Bouwfonds Ontwikkeling

178

Remark

Houses are situated among the dynamics of

the highway A58 and the calmness of the

forest area Boschkens. The noise barrier is

integrated in the rear walls.

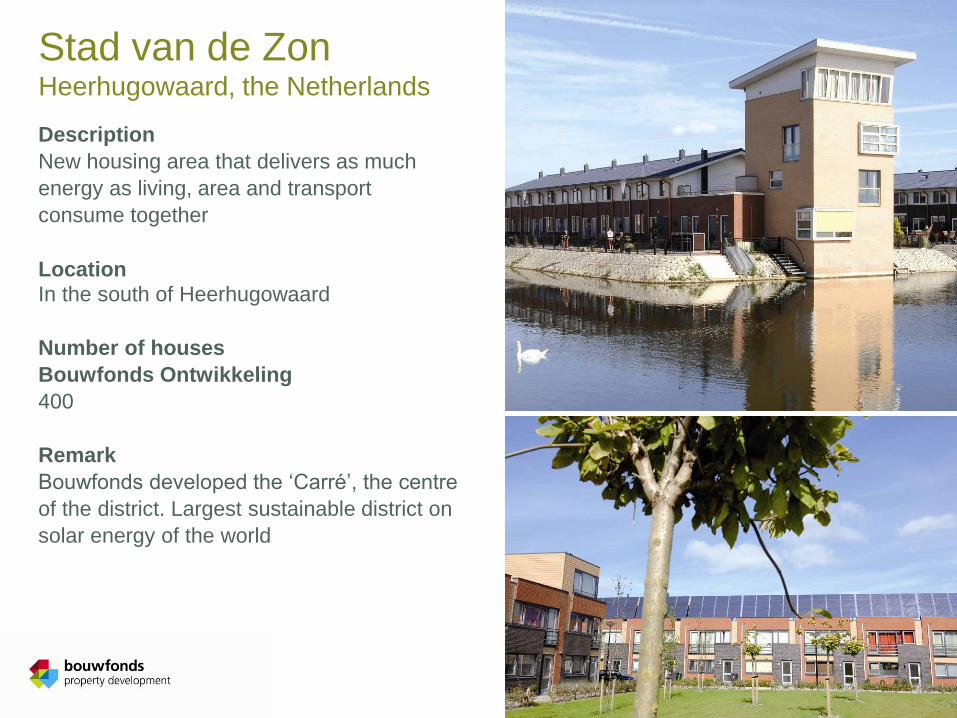

Stad van de Zon Heerhugowaard, the Netherlands

Description

New housing area that delivers as much

energy as living, area and transport

consume together

Location

In the south of Heerhugowaard

Number of houses

Bouwfonds Ontwikkeling

400

Remark

Bouwfonds developed the ‘Carré’, the centre

of the district. Largest sustainable district on

solar energy of the world

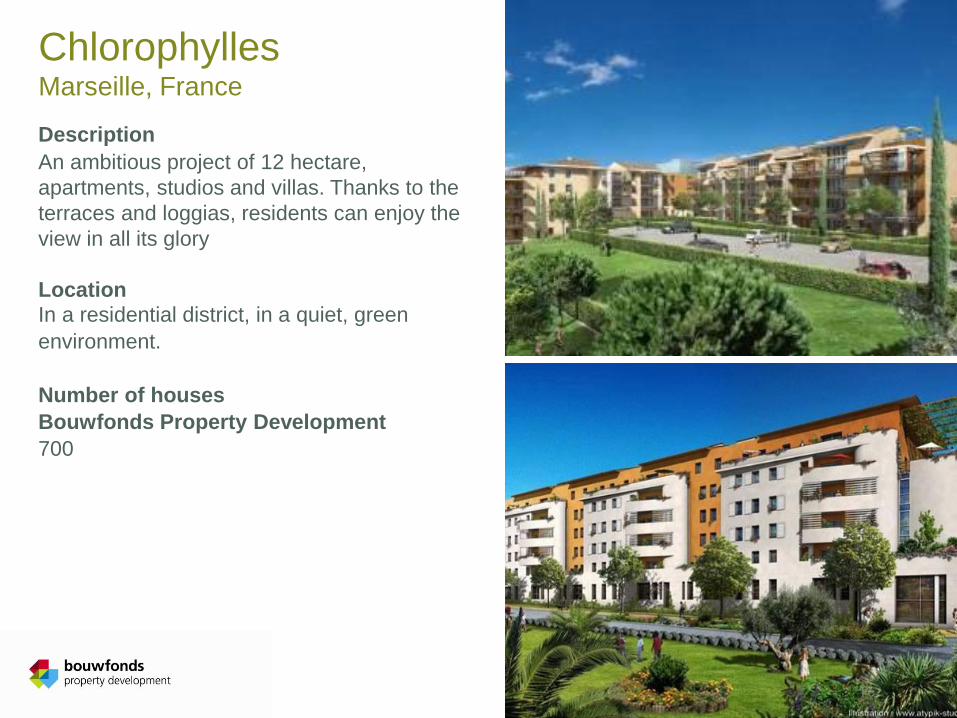

Chlorophylles Marseille, France

Description

An ambitious project of 12 hectare,

apartments, studios and villas. Thanks to the

terraces and loggias, residents can enjoy the

view in all its glory

Location

In a residential district, in a quiet, green

environment.

Number of houses

Bouwfonds Property Development

700

Lyon Islands Lyon, France

Description

Redevelopment of an old industrial district.

Development of houses, shops and

commercial areas.

Location

In the old industrial district ’La Confluence’

Number of houses

Bouwfonds Property Development

300 apartments and 1,800 m2 of retail

Remark

Lots of attention for sustainability, quality and

integration in existing environment

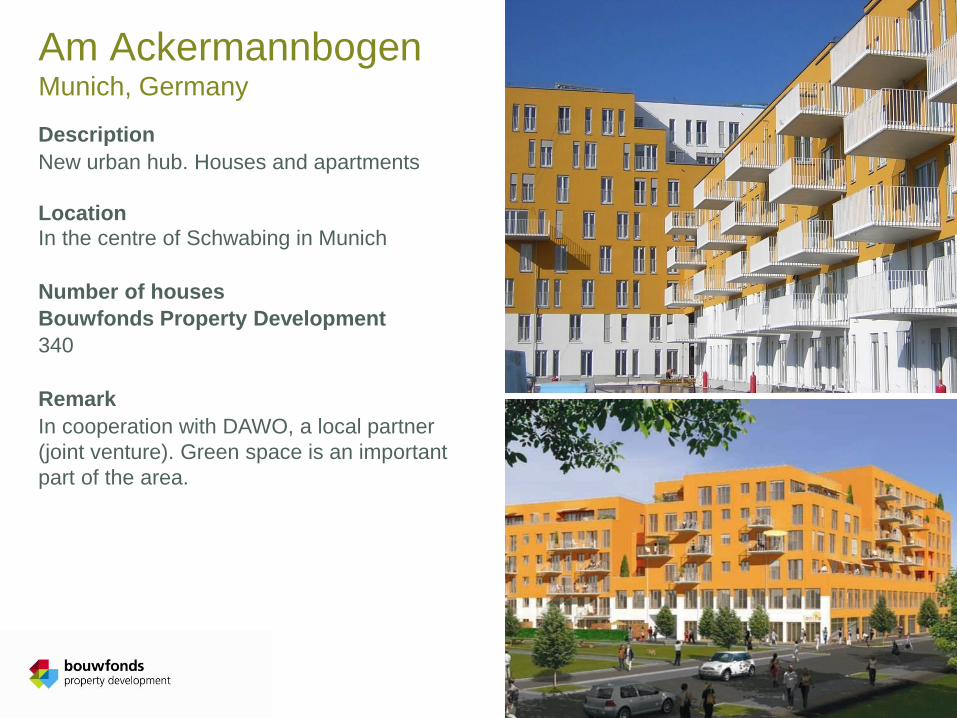

Am Ackermannbogen Munich, Germany

Description

New urban hub. Houses and apartments

Location

In the centre of Schwabing in Munich

Number of houses

Bouwfonds Property Development

340

Remark

In cooperation with DAWO, a local partner

(joint venture). Green space is an important

part of the area.

24

Crisis?

25

Or a booming market?

Dutch population and household figures

Naam presentatie, Datum 26

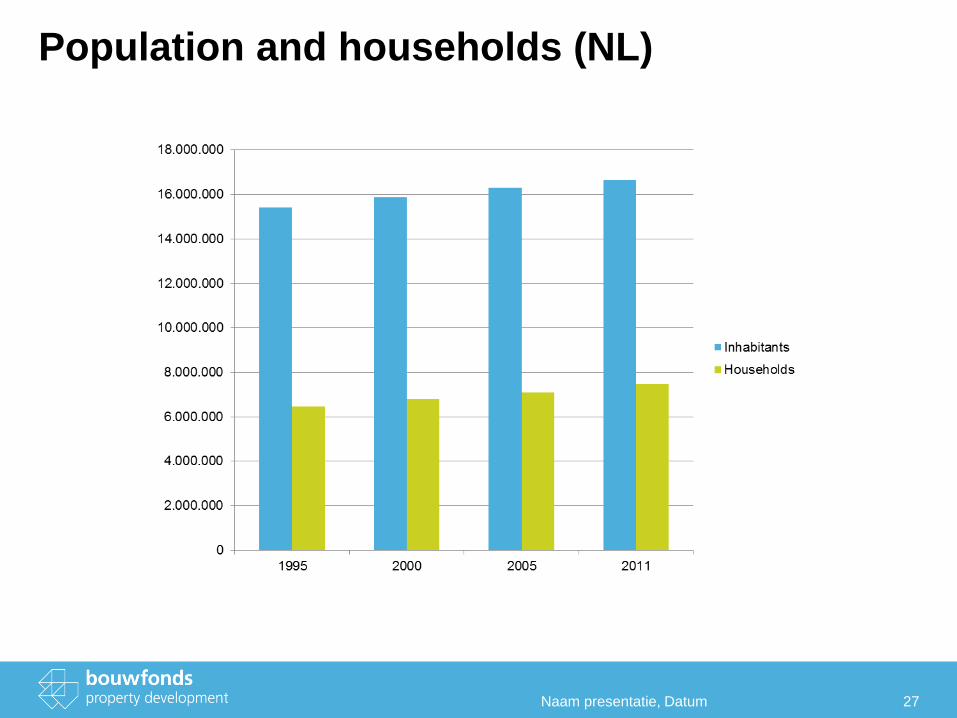

Population and households (NL)

Naam presentatie, Datum 27

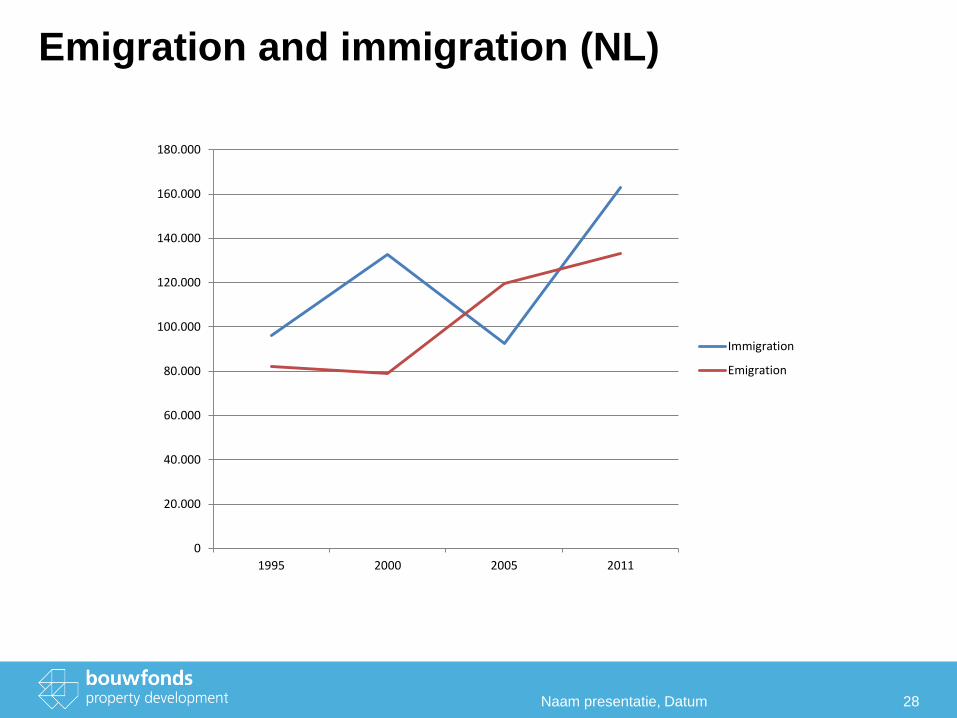

Emigration and immigration (NL)

Naam presentatie, Datum 28

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

160.000

180.000

1995 2000 2005 2011

Immigration

Emigration

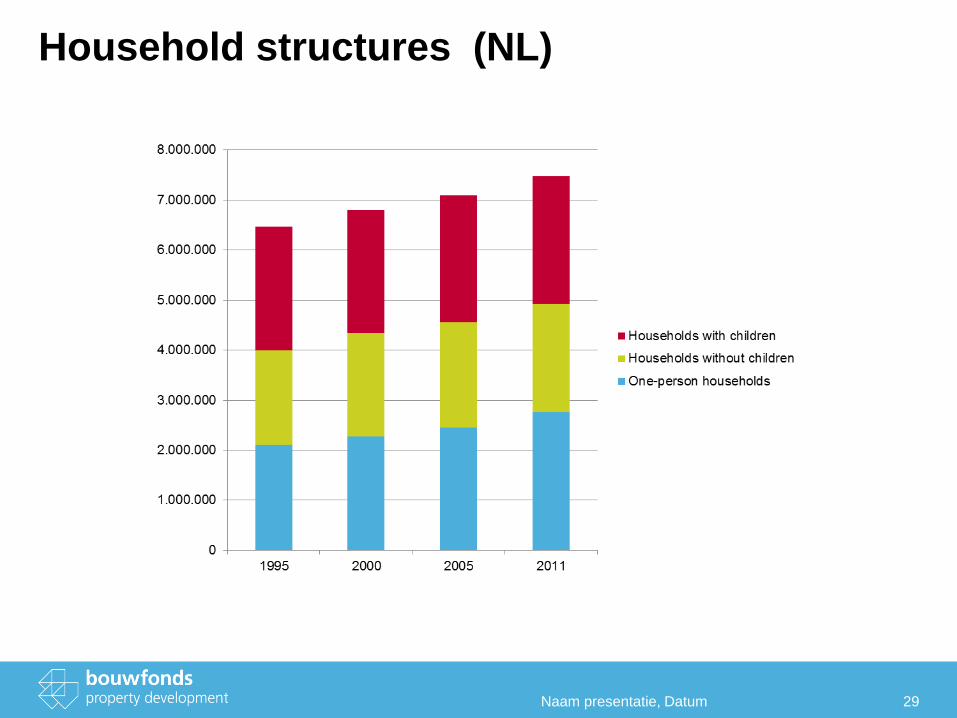

Household structures (NL)

Naam presentatie, Datum 29

30

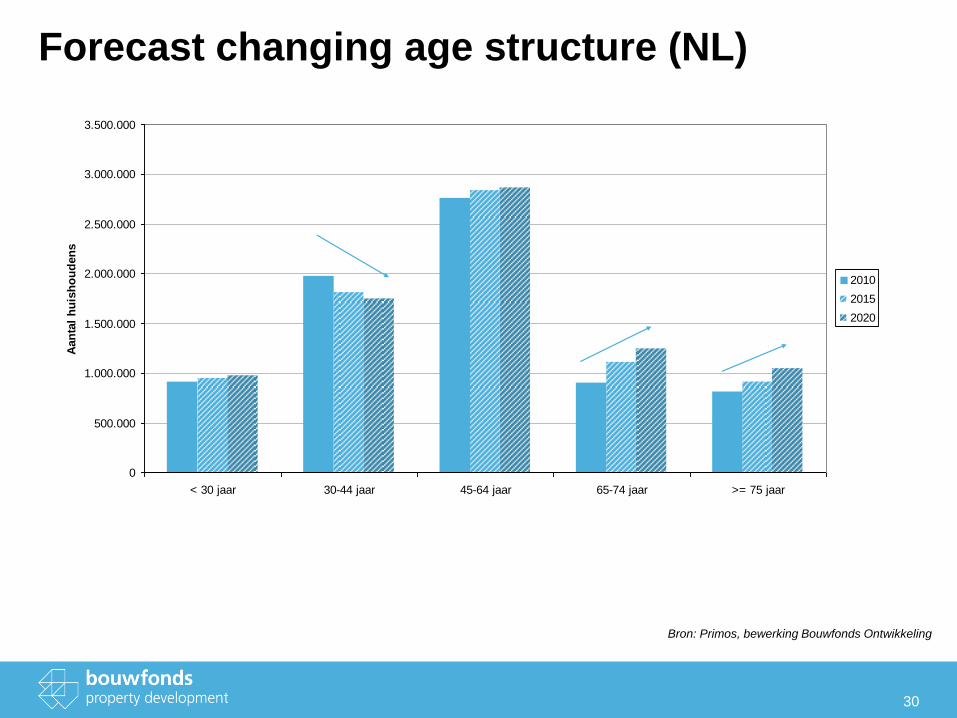

Forecast changing age structure (NL)

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

3.500.000

< 30 jaar 30-44 jaar 45-64 jaar 65-74 jaar >= 75 jaar

Aan

tal

hu

ish

ou

den

s

2010

2015

2020

Bron: Primos, bewerking Bouwfonds Ontwikkeling

31

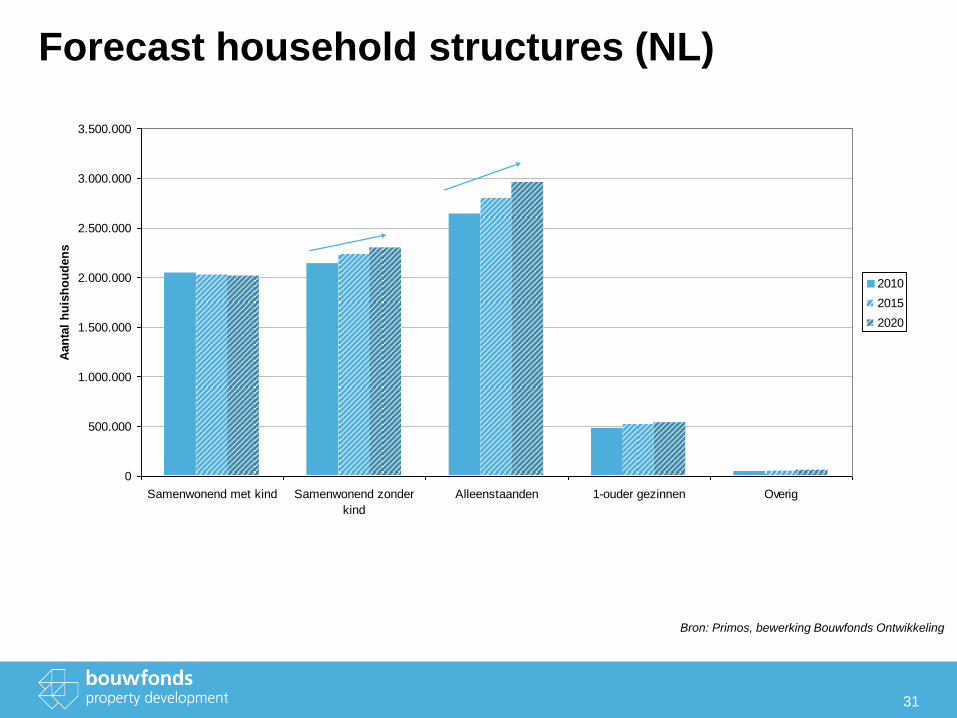

Forecast household structures (NL)

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

3.500.000

Samenwonend met kind Samenwonend zonder

kind

Alleenstaanden 1-ouder gezinnen Overig

Aan

tal

hu

ish

ou

den

s

2010

2015

2020

Bron: Primos, bewerking Bouwfonds Ontwikkeling

To sum up

• The Dutch population is still growing

• The immigration is still on a low level and almost completely compensated by

emigration

• The amount of households is still growing

• 35% are single households, going to 40% in the coming 10 years

• The aging of the society has just started

Naam presentatie, Datum 32

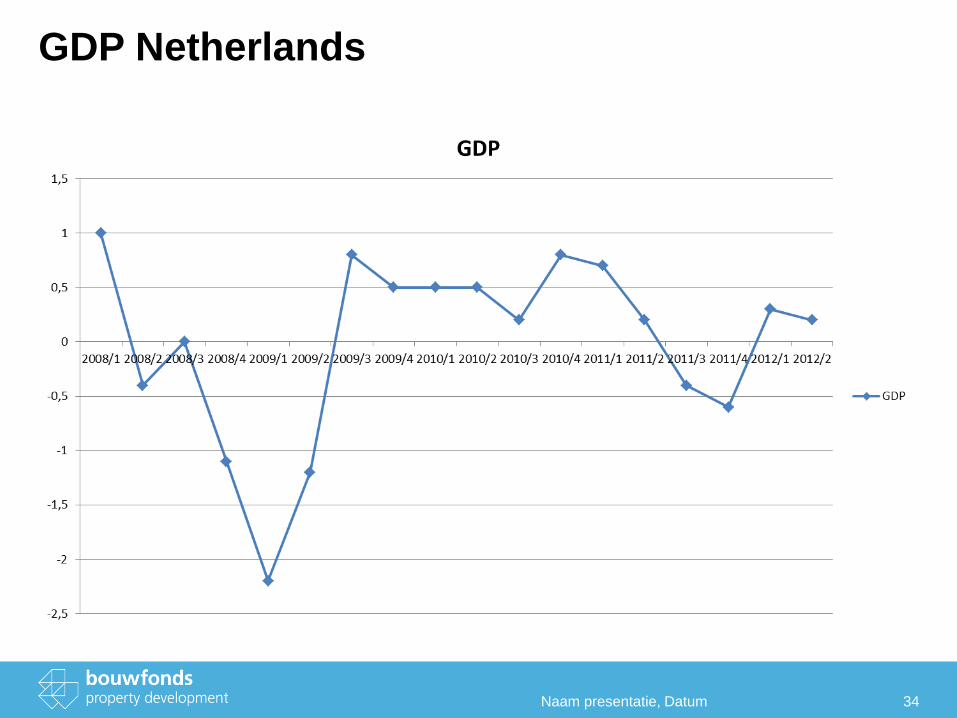

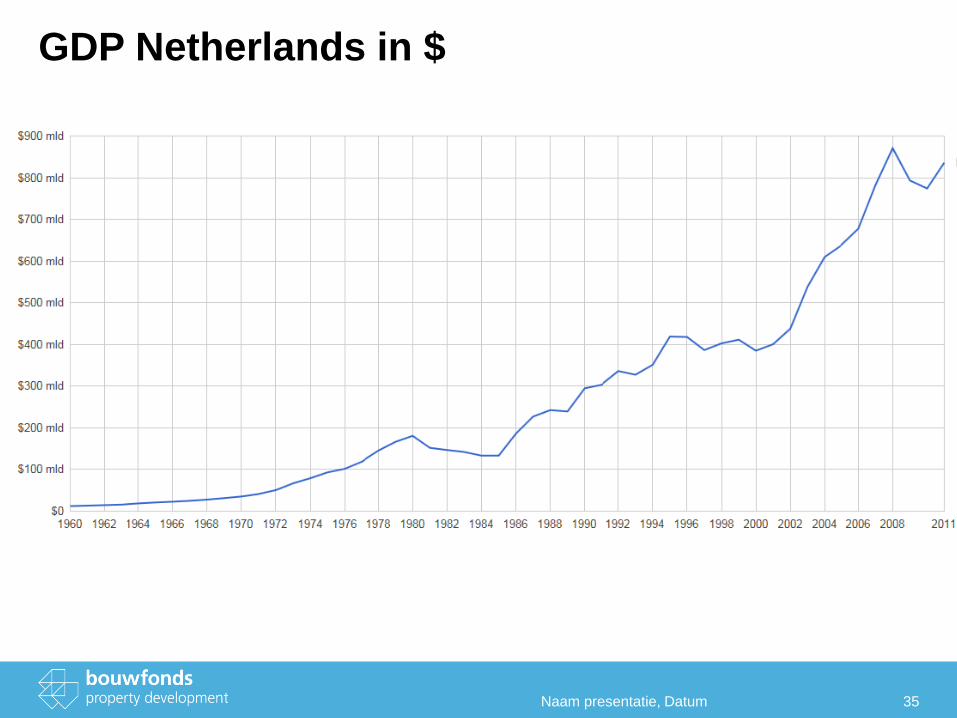

The Dutch economy

Naam presentatie, Datum 33

GDP Netherlands

Naam presentatie, Datum 34

GDP Netherlands in $

Naam presentatie, Datum 35

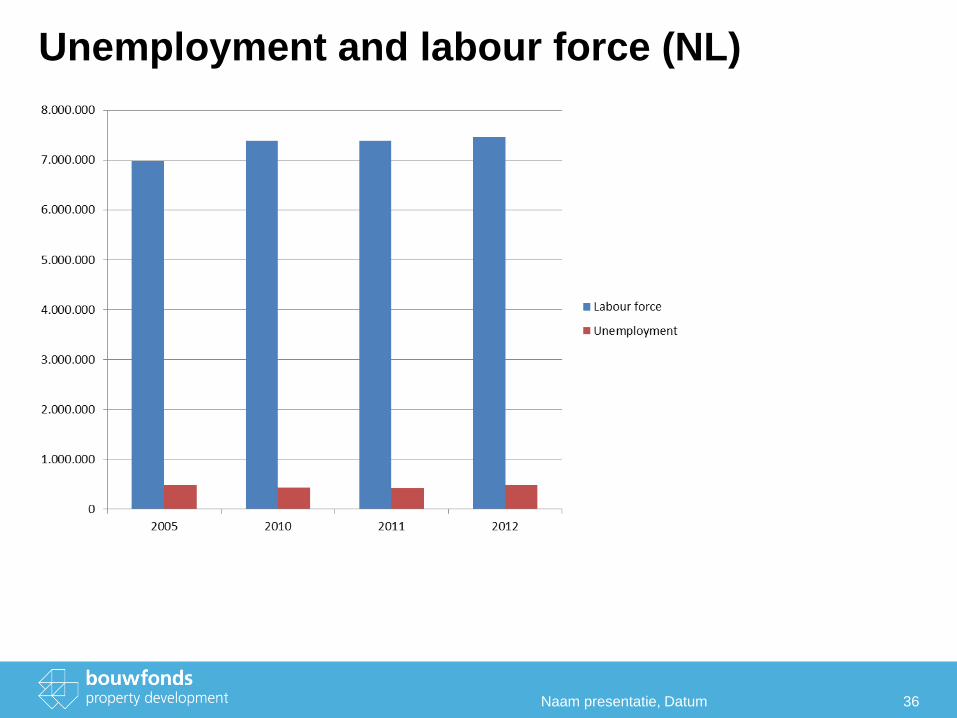

Unemployment and labour force (NL)

Naam presentatie, Datum 36

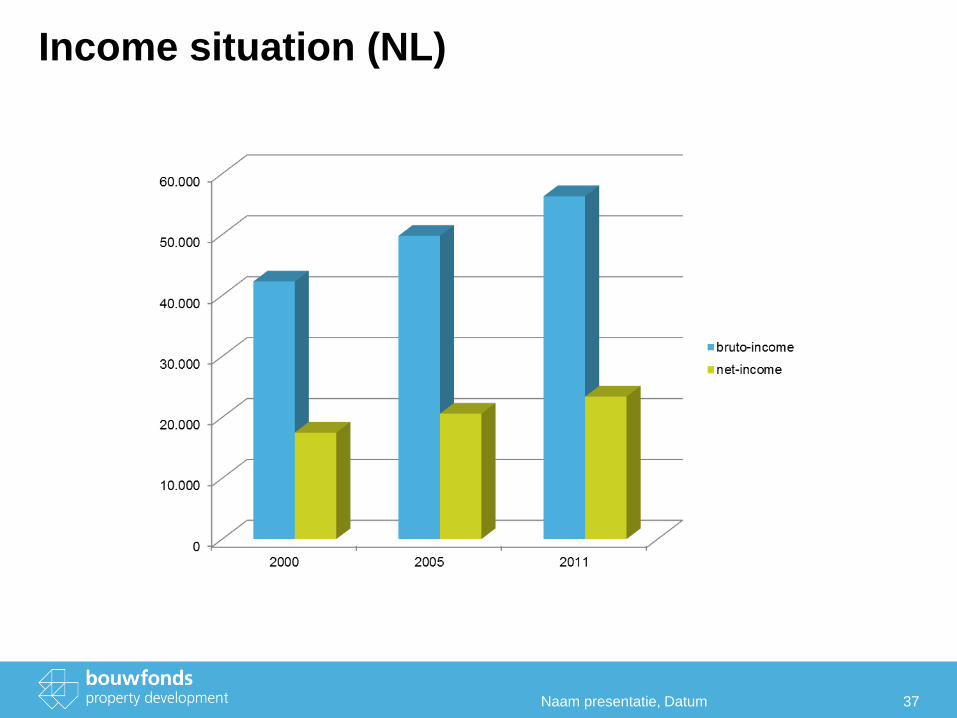

Income situation (NL)

Naam presentatie, Datum 37

To sum up

• The economic situation in the Netherlands is better than the general feeling of

the population

• The unemployment rates are still one of the lowest in Europe

• There is a growing gap between the earned incomes and the spendable

incomes.

Naam presentatie, Datum 38

The residential market in the Netherlands

Naam presentatie, Datum 39

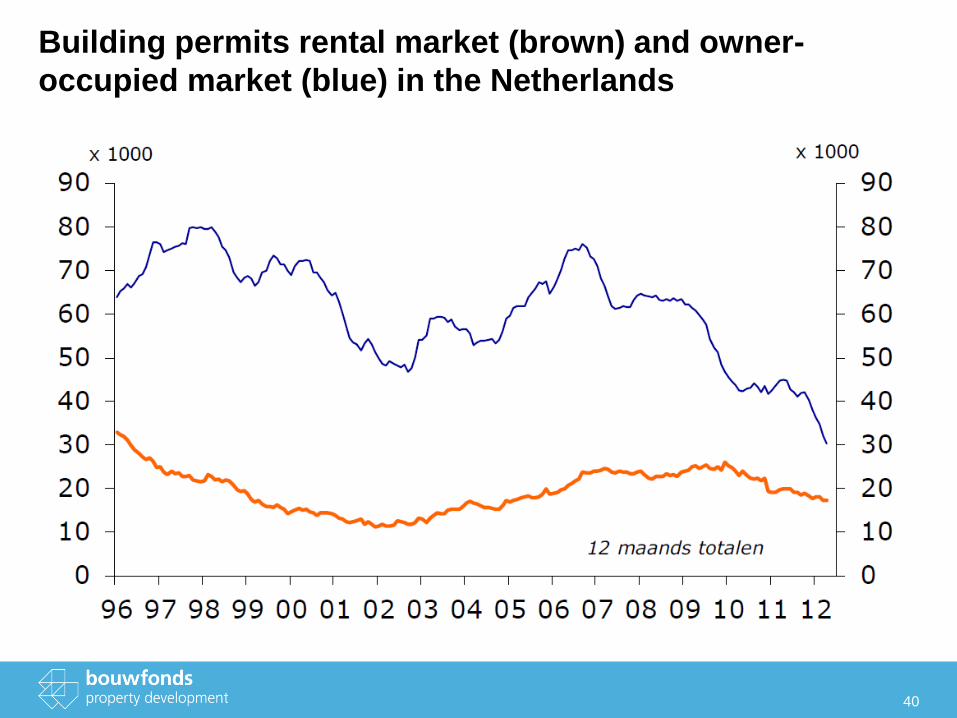

40

Building permits rental market (brown) and owner-

occupied market (blue) in the Netherlands

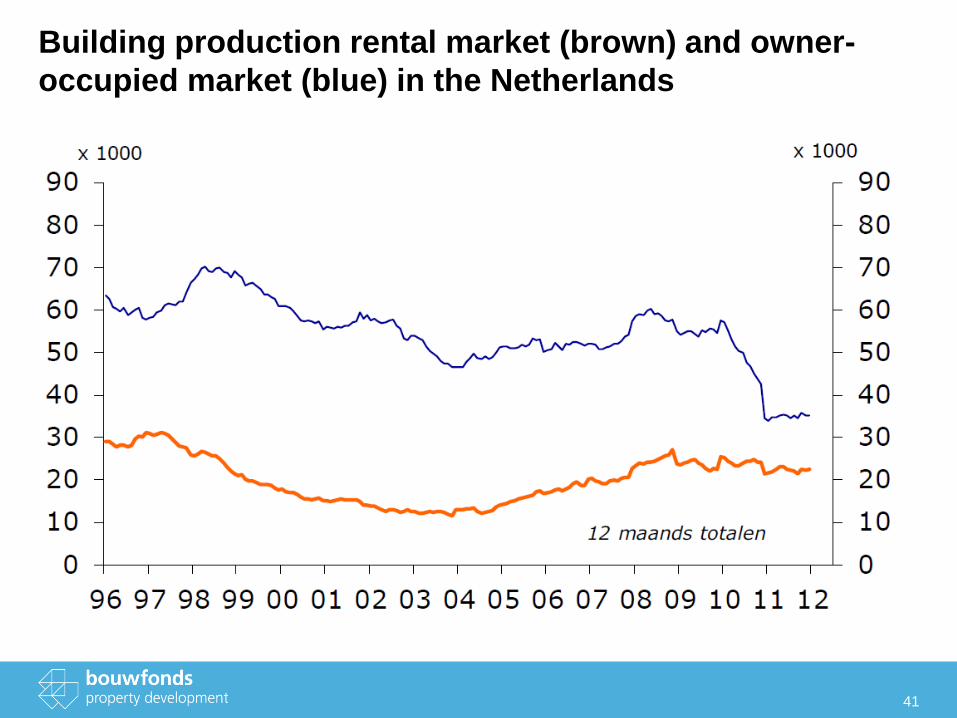

41

Building production rental market (brown) and owner-

occupied market (blue) in the Netherlands

42

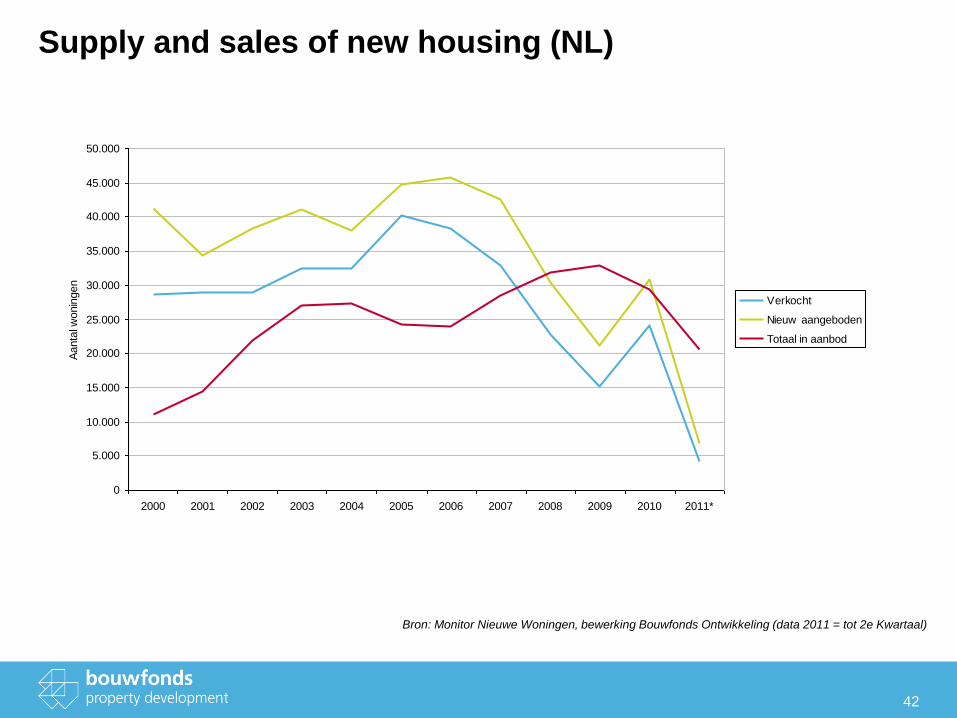

Supply and sales of new housing (NL)

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Aanta

l wonin

gen

Verkocht

Nieuw aangeboden

Totaal in aanbod

Bron: Monitor Nieuwe Woningen, bewerking Bouwfonds Ontwikkeling (data 2011 = tot 2e Kwartaal)

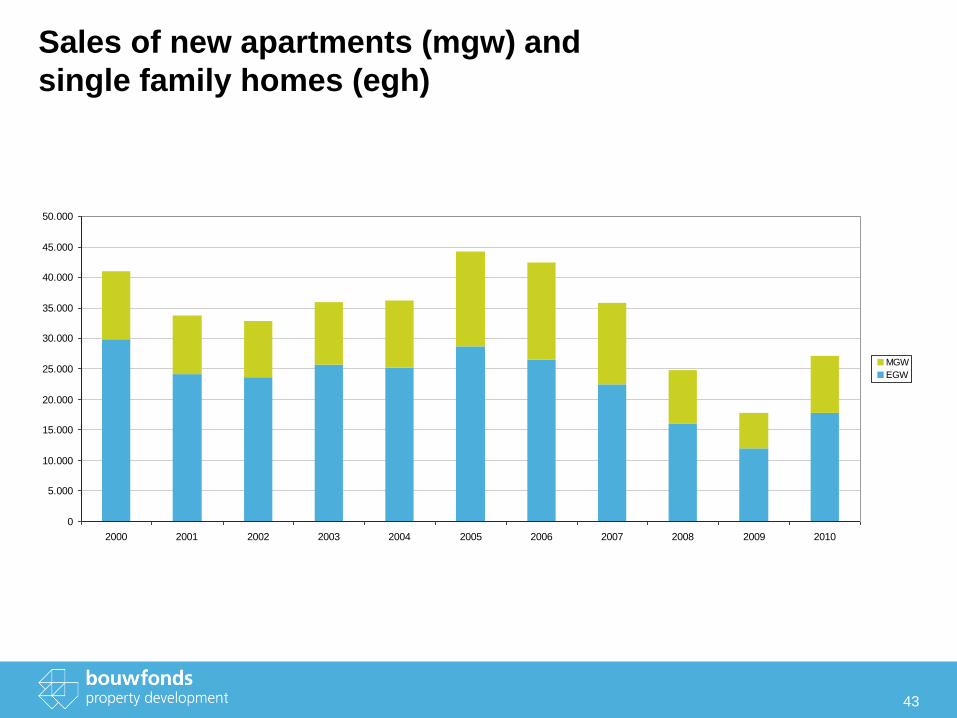

43

Sales of new apartments (mgw) and

single family homes (egh)

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

MGW

EGW

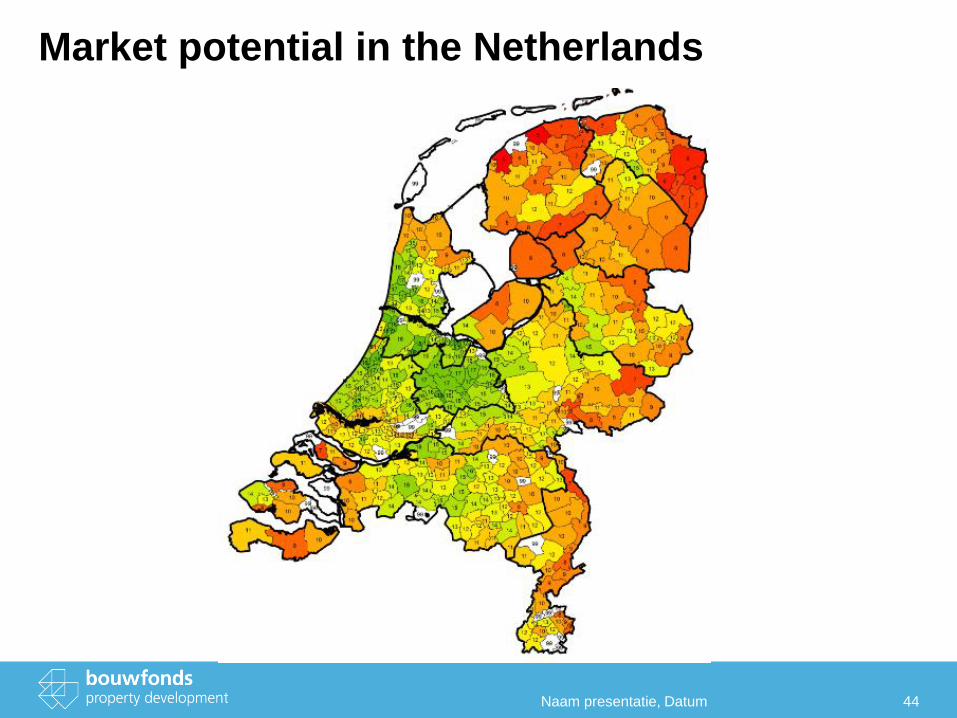

Market potential in the Netherlands

Naam presentatie, Datum 44

To sum up

• The Dutch housing market has come to an almost complete on-hold as far as it

concerns the housing sales

• The rental market is not really attacked

• The supply of new housing stock is reduced by more than 50%.

• The price gap between new and existing houses is growing

• The sales prices of new houses in attractive regions are relative stabile. But the

competition between regions will clearly bring winners and losers

• The people, who cannot afford to pay their monthly mortgage to the banks is still

very low (0, 06%)

Naam presentatie, Datum 45

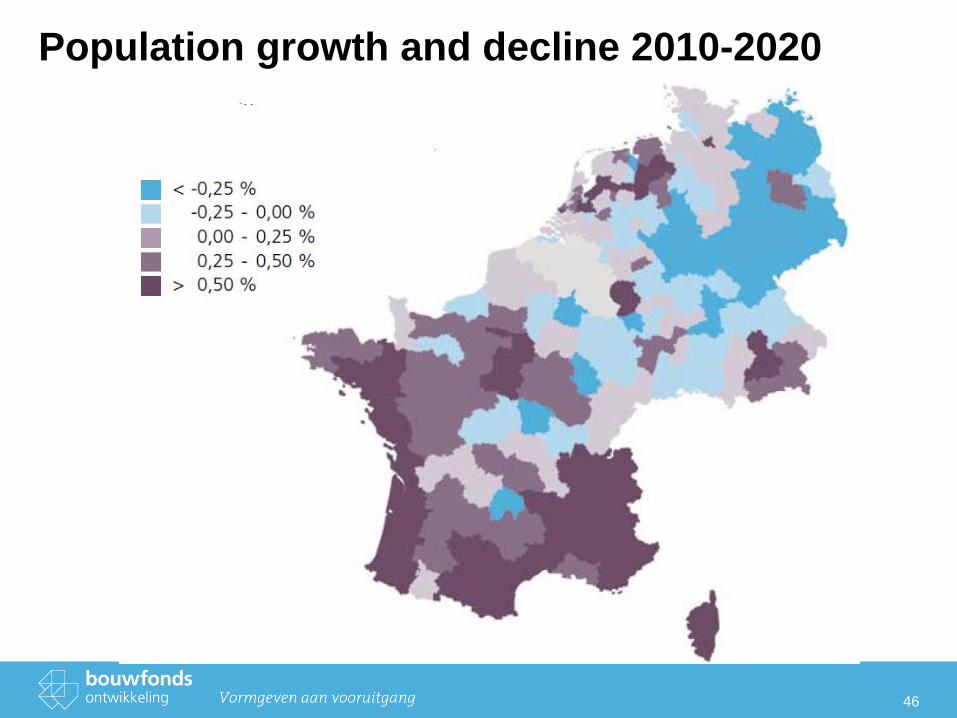

Population growth and decline 2010-2020

46

Employment growth and decline 2010-2020

47

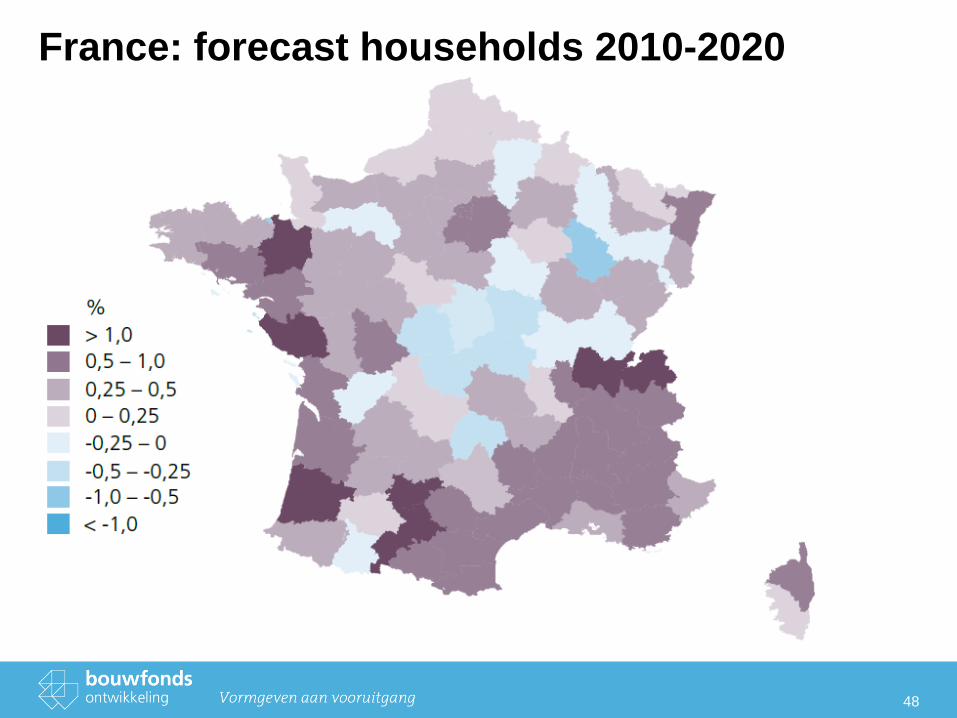

France: forecast households 2010-2020

48

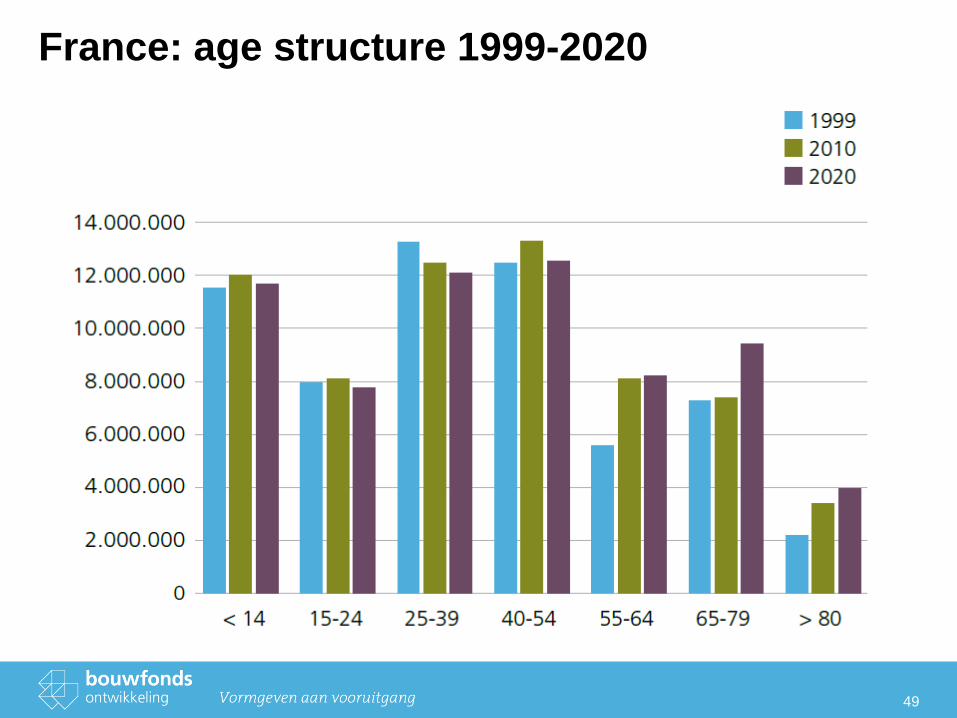

France: age structure 1999-2020

49

50

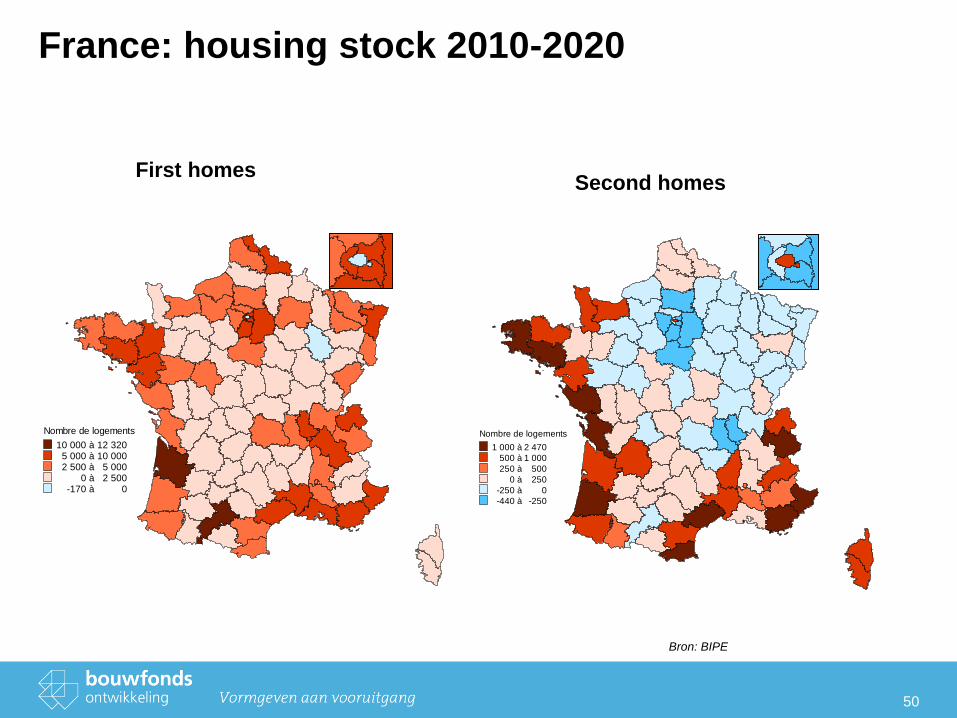

France: housing stock 2010-2020

Nombre de logements

10 000 à 12 3205 000 à 10 0002 500 à 5 000

0 à 2 500-170 à 0

Nombre de logements

1 000 à 2 470

500 à 1 000

250 à 500

0 à 250

-250 à 0

-440 à -250

First homes Second homes

Bron: BIPE

51

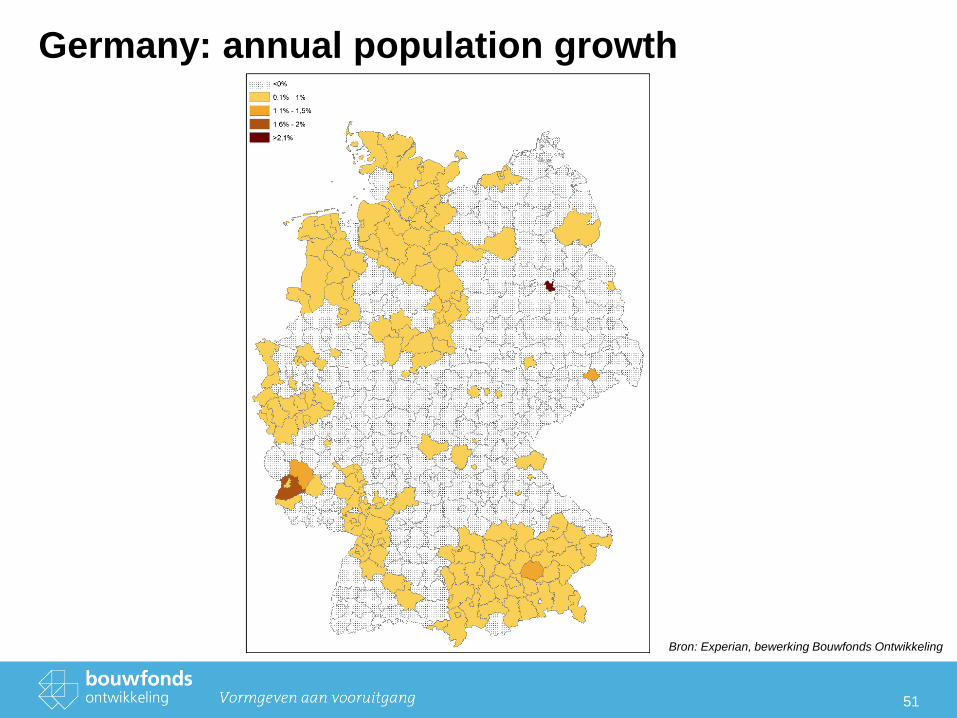

Germany: annual population growth

Bron: Experian, bewerking Bouwfonds Ontwikkeling

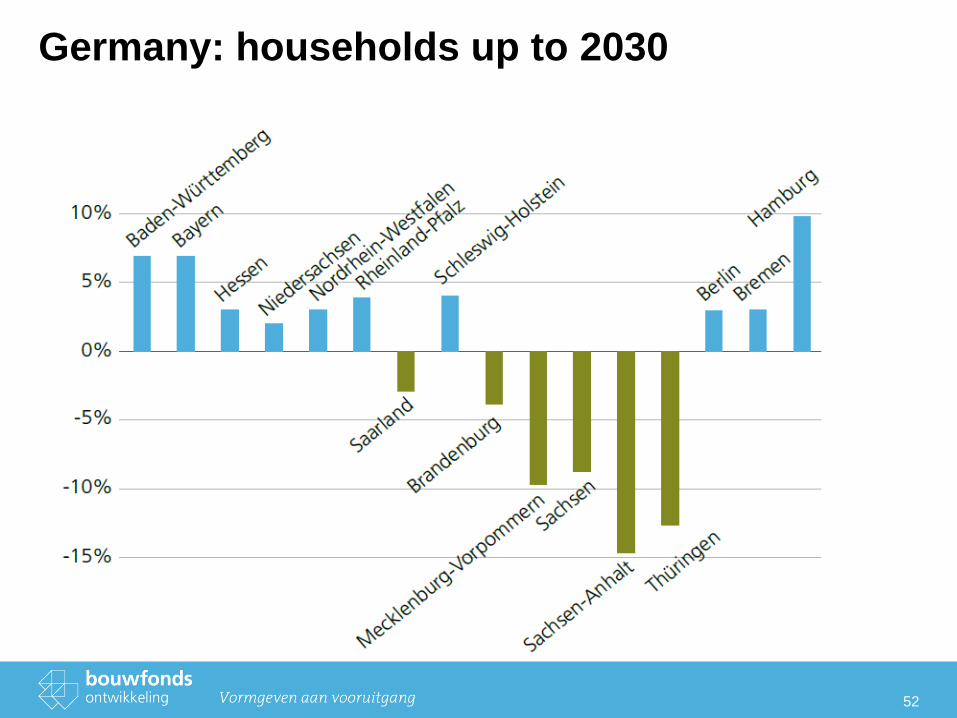

Germany: households up to 2030

52

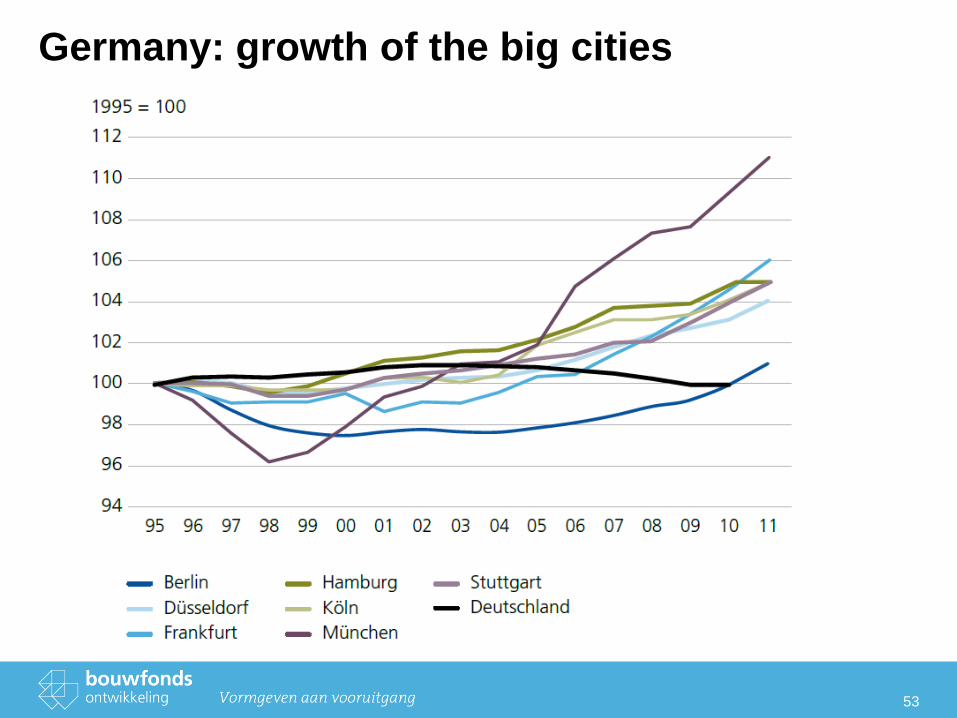

Germany: growth of the big cities

53

Germany: an ageing society

54

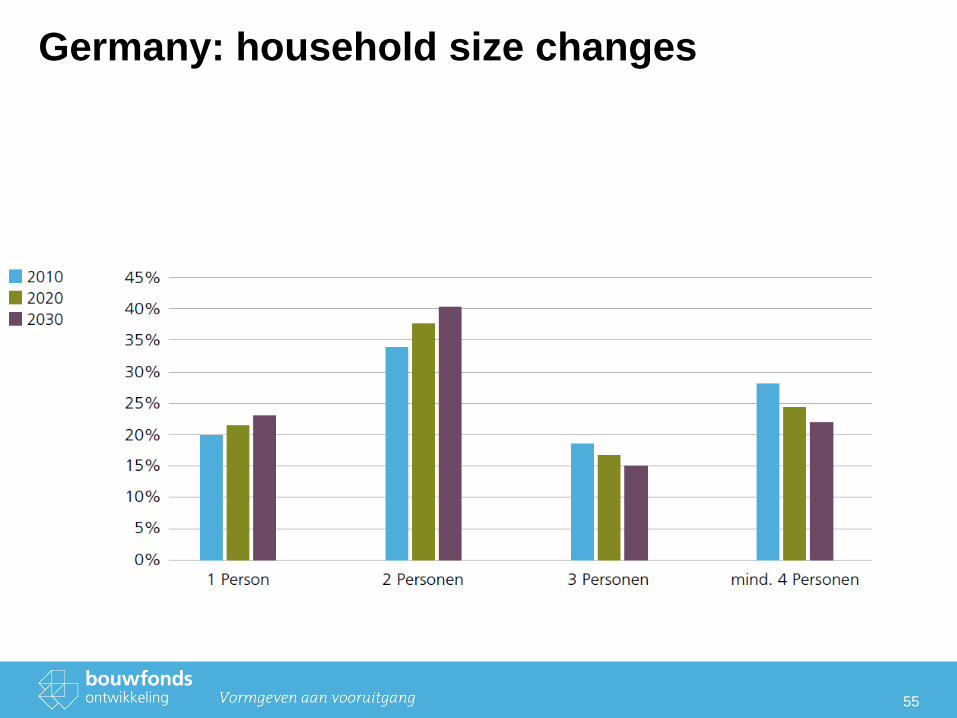

Germany: household size changes

55

56

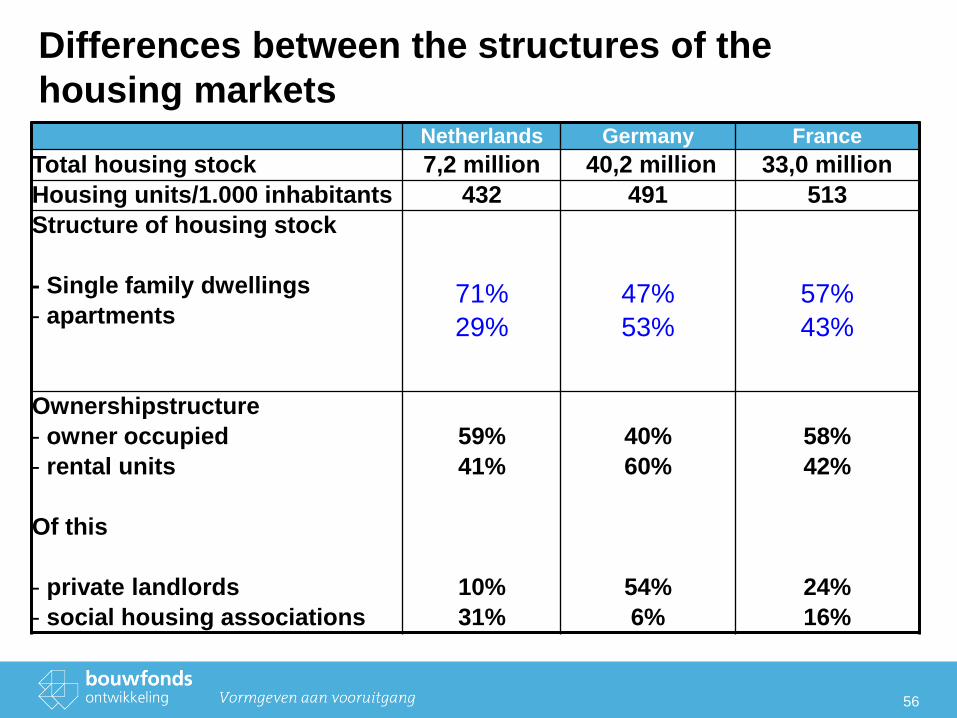

Differences between the structures of the

housing markets Netherlands Germany France

Total housing stock 7,2 million 40,2 million 33,0 million

Housing units/1.000 inhabitants 432 491 513

Structure of housing stock

- Single family dwellings

- apartments

71%

29%

47%

53%

57%

43%

Ownershipstructure

- owner occupied

- rental units

Of this

- private landlords

- social housing associations

59%

41%

10%

31%

40%

60%

54%

6%

58%

42%

24%

16%

57

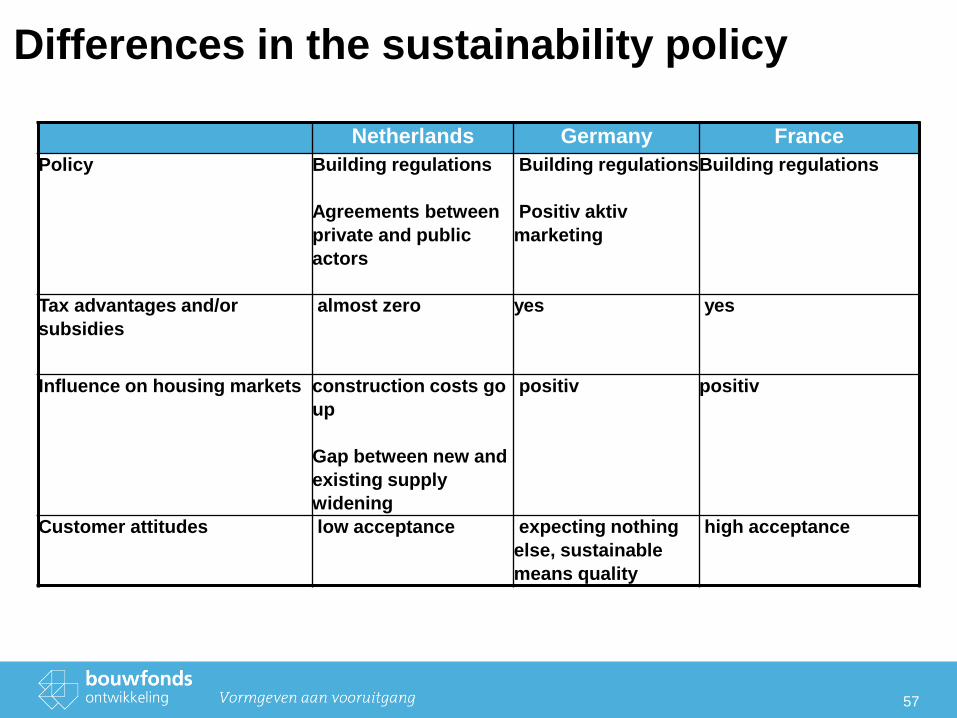

Differences in the sustainability policy

Netherlands Germany France

Policy Building regulations

Agreements between

private and public

actors

Building regulations

Positiv aktiv

marketing

Building regulations

Tax advantages and/or

subsidies

almost zero yes yes

Influence on housing markets construction costs go

up

Gap between new and

existing supply

widening

positiv positiv

Customer attitudes low acceptance expecting nothing

else, sustainable

means quality

high acceptance

58

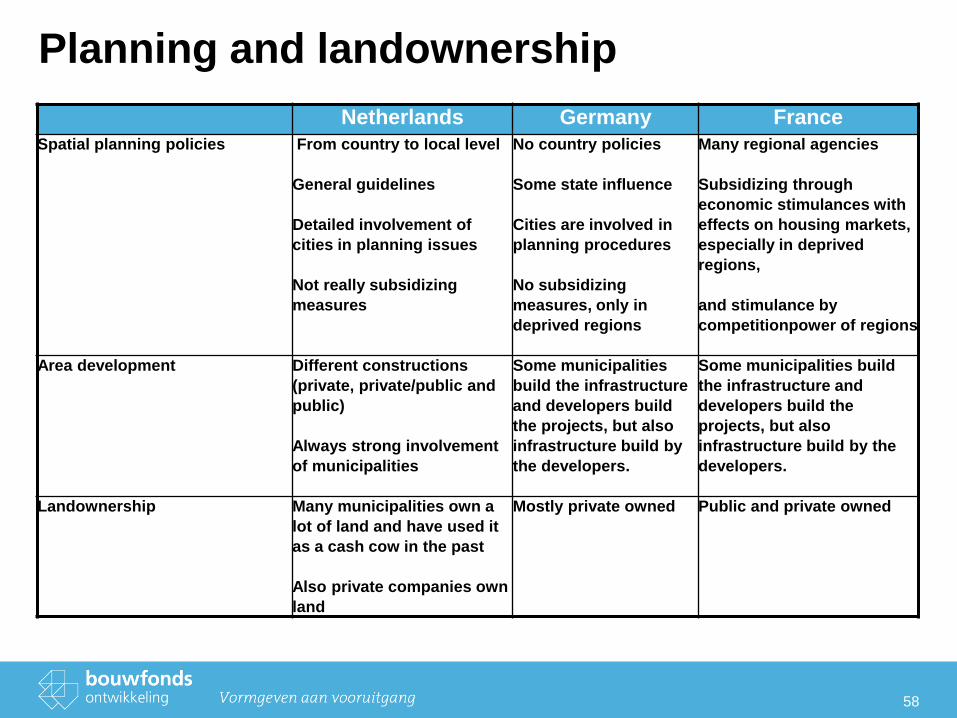

Planning and landownership

Netherlands Germany France

Spatial planning policies From country to local level

General guidelines

Detailed involvement of

cities in planning issues

Not really subsidizing

measures

No country policies

Some state influence

Cities are involved in

planning procedures

No subsidizing

measures, only in

deprived regions

Many regional agencies

Subsidizing through

economic stimulances with

effects on housing markets,

especially in deprived

regions,

and stimulance by

competitionpower of regions

Area development Different constructions

(private, private/public and

public)

Always strong involvement

of municipalities

Some municipalities

build the infrastructure

and developers build

the projects, but also

infrastructure build by

the developers.

Some municipalities build

the infrastructure and

developers build the

projects, but also

infrastructure build by the

developers.

Landownership Many municipalities own a

lot of land and have used it

as a cash cow in the past

Also private companies own

land

Mostly private owned Public and private owned

59

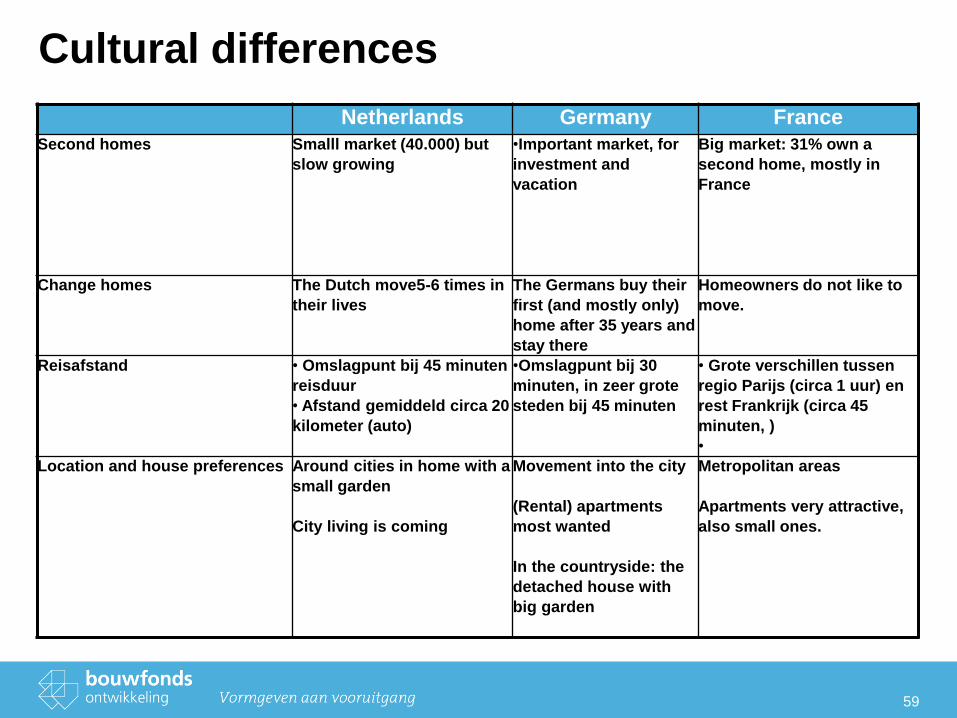

Cultural differences

Netherlands Germany France

Second homes Smalll market (40.000) but

slow growing

•Important market, for

investment and

vacation

Big market: 31% own a

second home, mostly in

France

Change homes The Dutch move5-6 times in

their lives

The Germans buy their

first (and mostly only)

home after 35 years and

stay there

Homeowners do not like to

move.

Reisafstand • Omslagpunt bij 45 minuten

reisduur

• Afstand gemiddeld circa 20

kilometer (auto)

•Omslagpunt bij 30

minuten, in zeer grote

steden bij 45 minuten

• Grote verschillen tussen

regio Parijs (circa 1 uur) en

rest Frankrijk (circa 45

minuten, )

•

Location and house preferences Around cities in home with a

small garden

City living is coming

Movement into the city

(Rental) apartments

most wanted

In the countryside: the

detached house with

big garden

Metropolitan areas

Apartments very attractive,

also small ones.

60

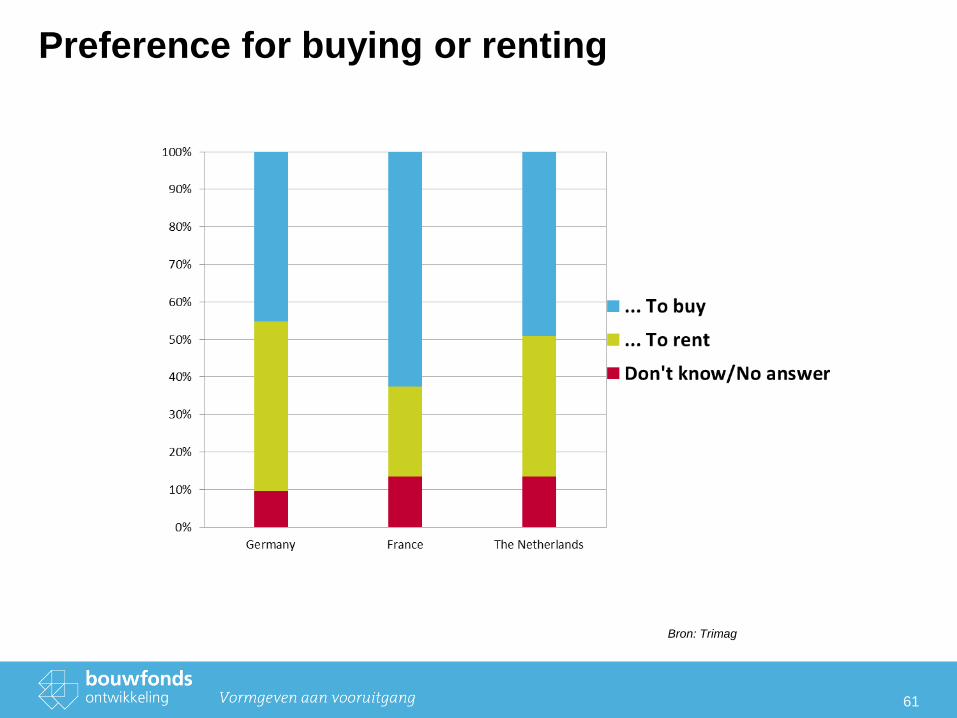

The big consumer survey

• Survey by phone in France and Germany, by phone+internet in the Netherlands

• 1.000 complete surveys for each country

• Representative on country level

• Feedback: France 48%, Germany 49%, Netherlands 20%

• Questionaire: 22 questions, average 11 minutes

61

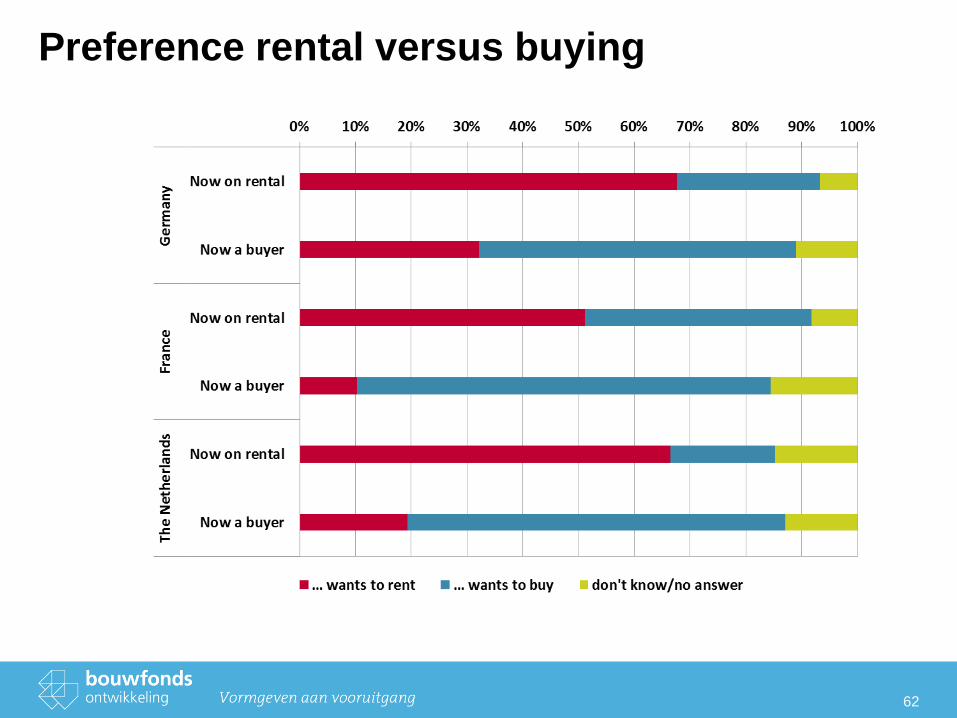

Preference for buying or renting

Bron: Trimag

Preference rental versus buying

62

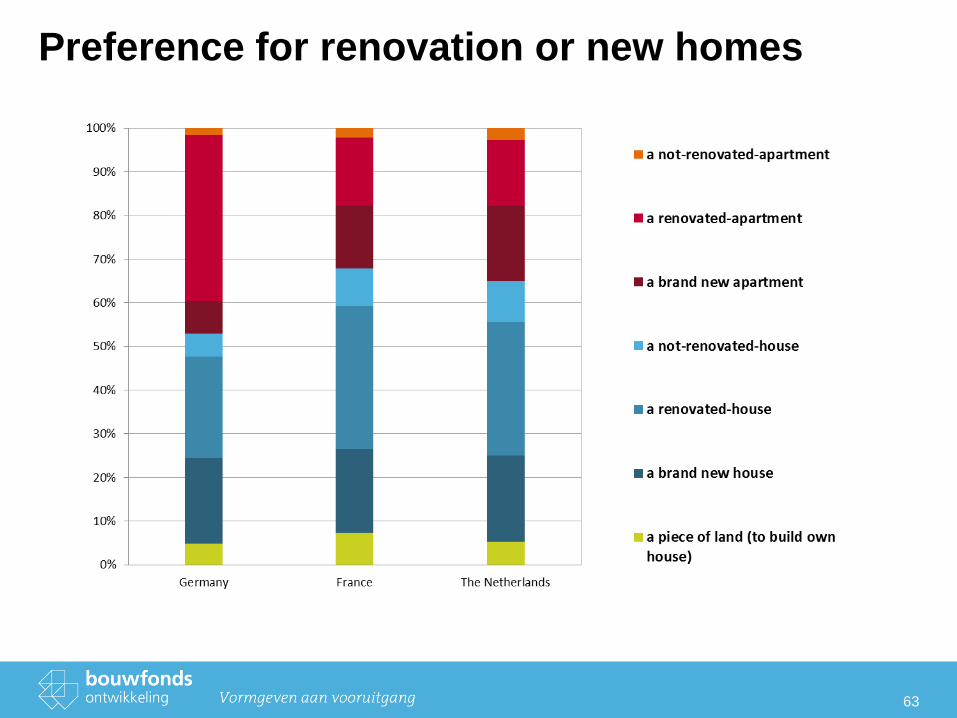

Preference for renovation or new homes

63

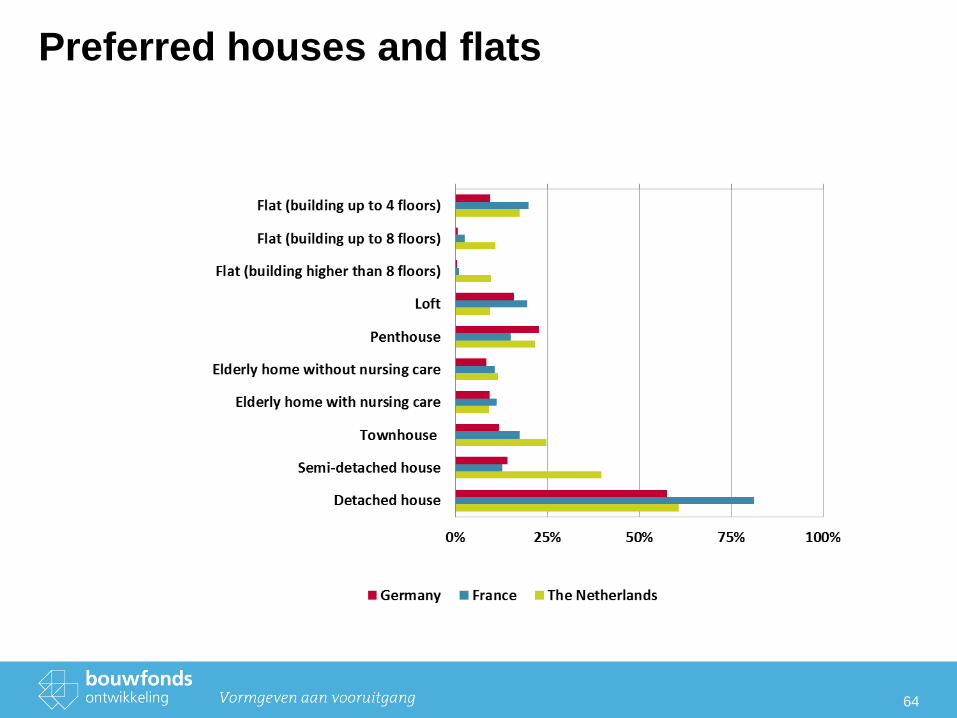

Preferred houses and flats

64

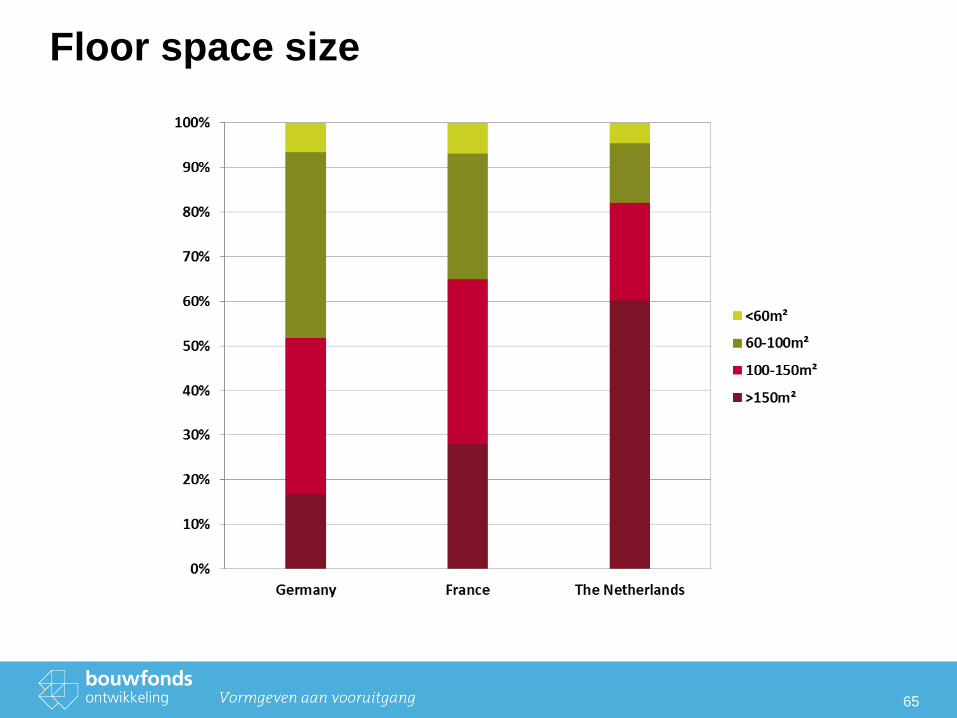

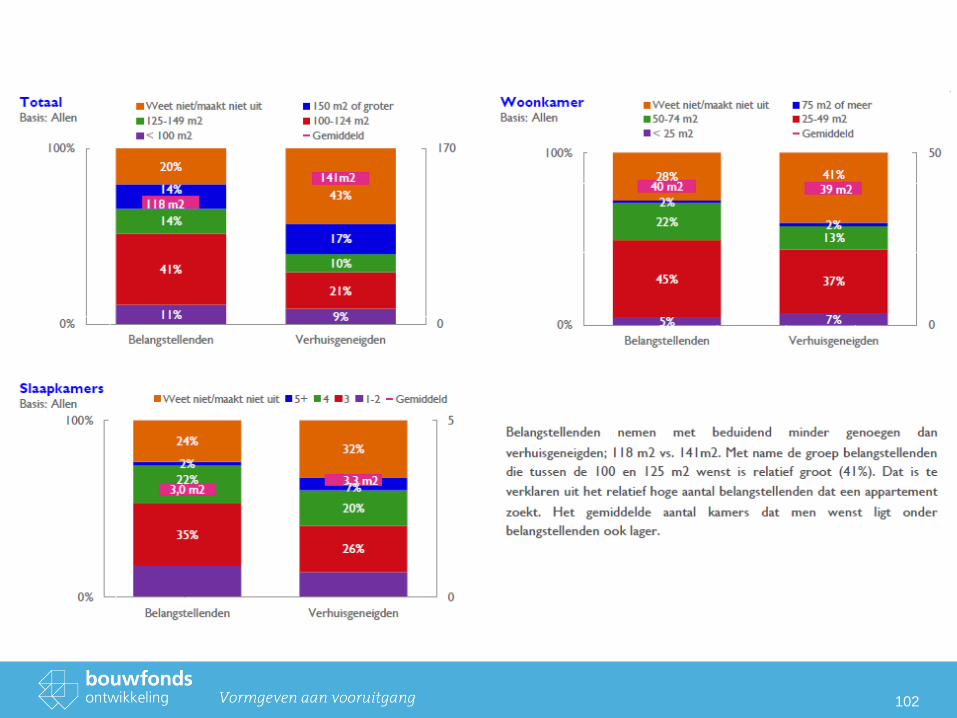

Floor space size

65

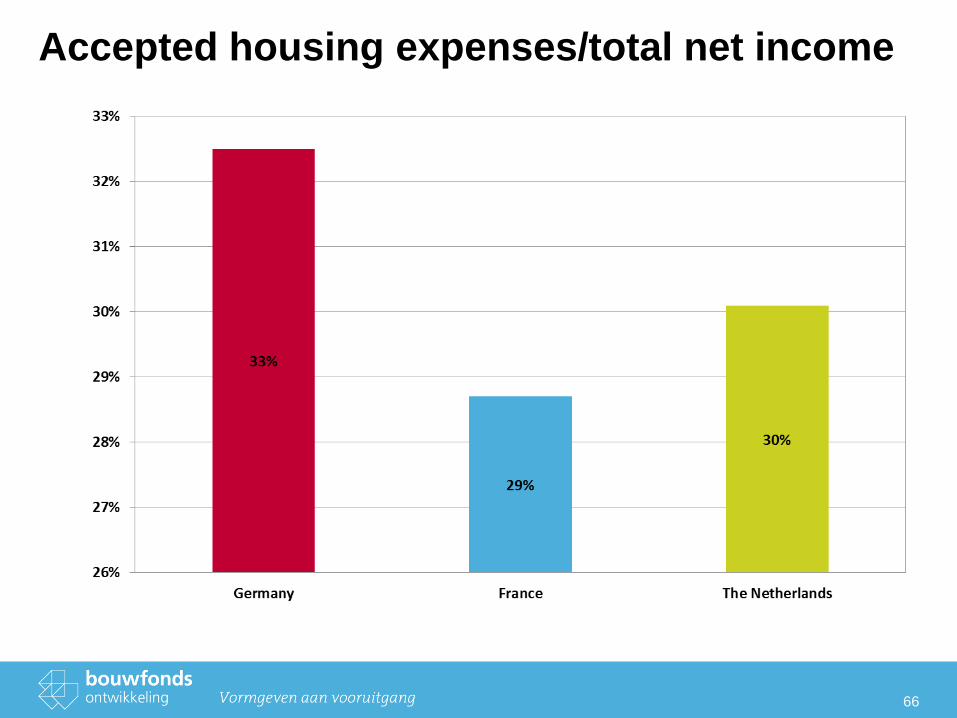

Accepted housing expenses/total net income

66

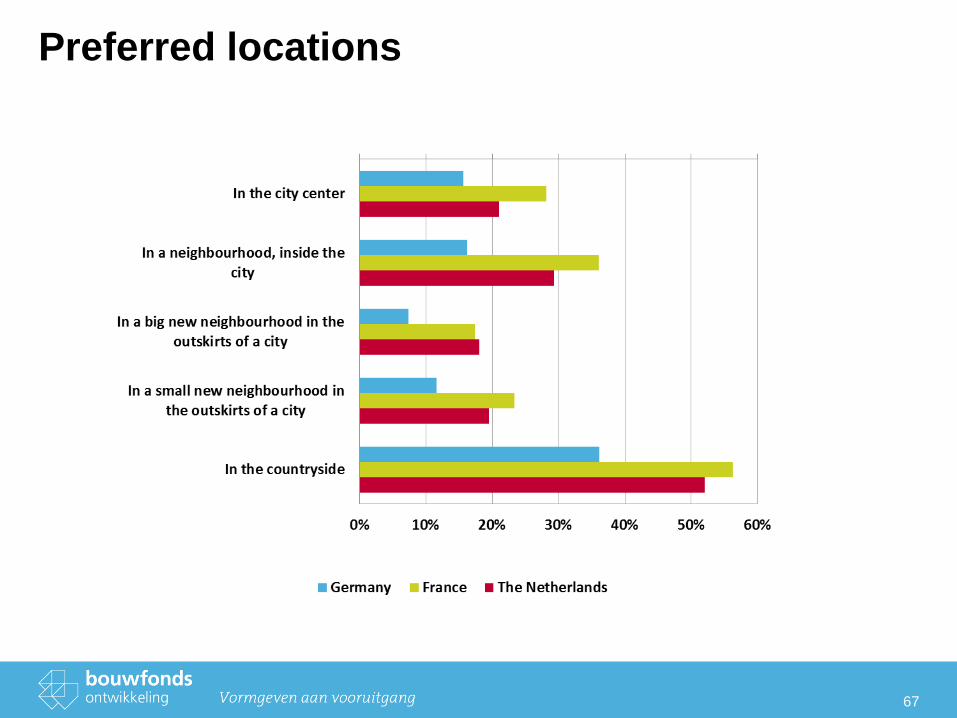

Preferred locations

67

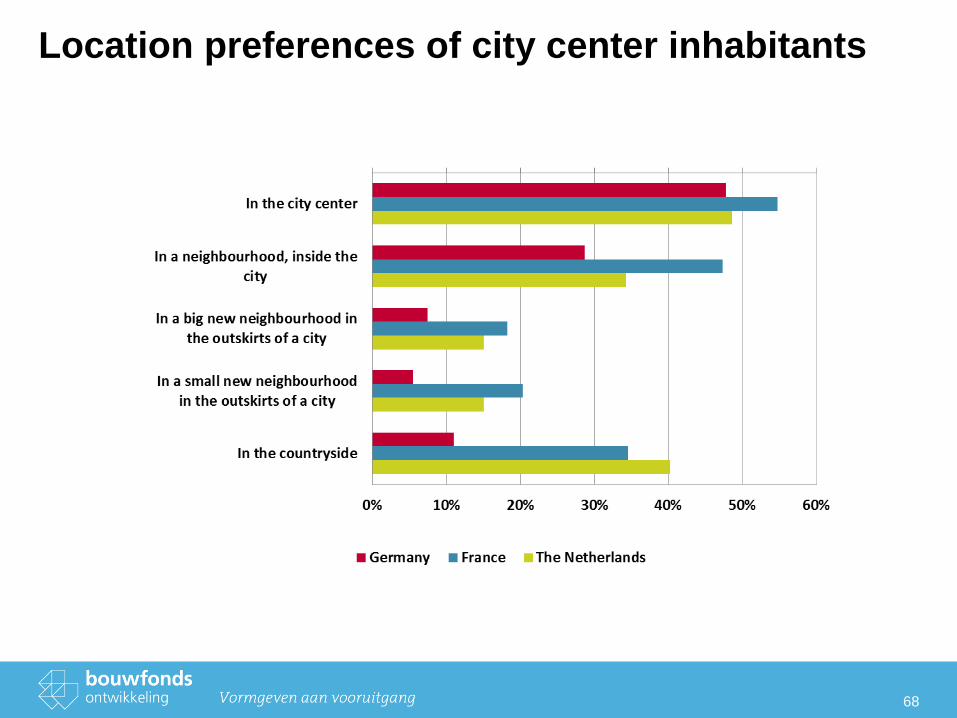

Location preferences of city center inhabitants

68

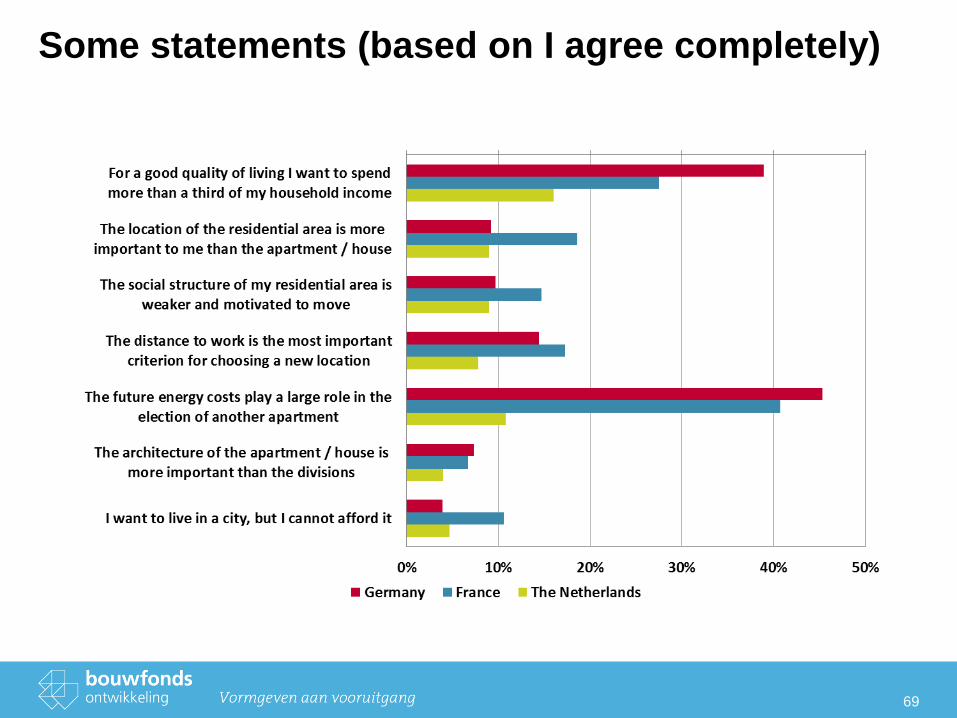

Some statements (based on I agree completely)

69

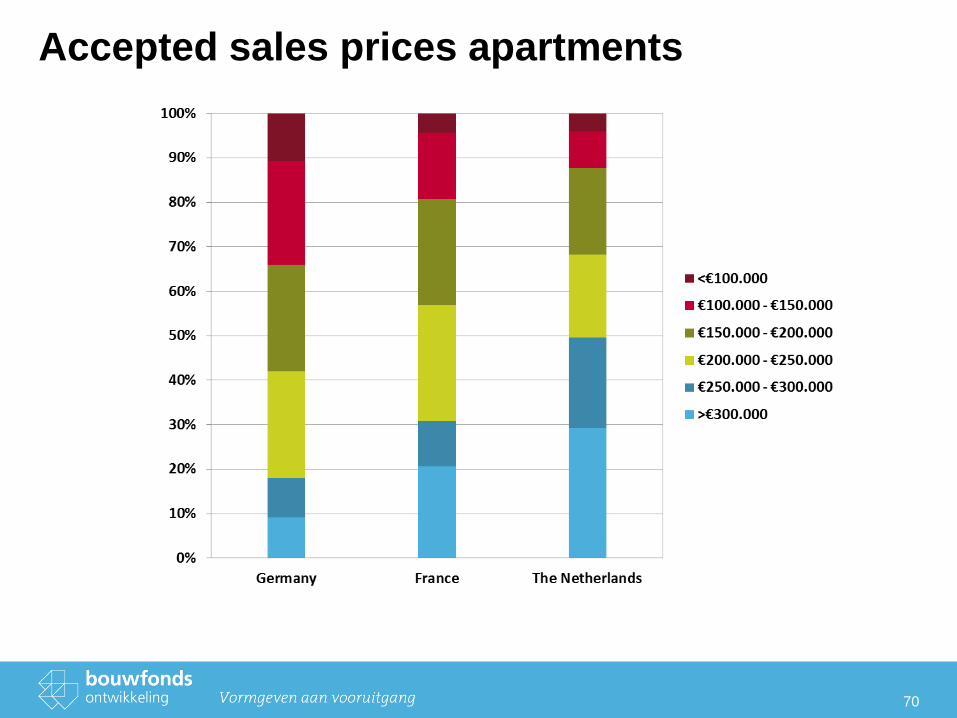

Accepted sales prices apartments

70

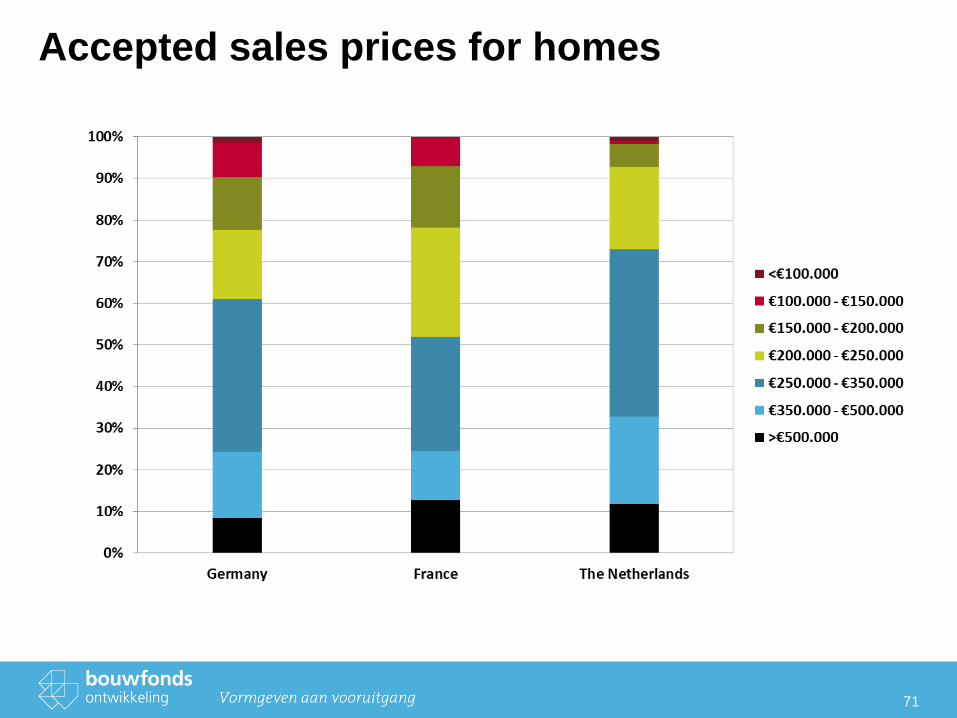

Accepted sales prices for homes

71

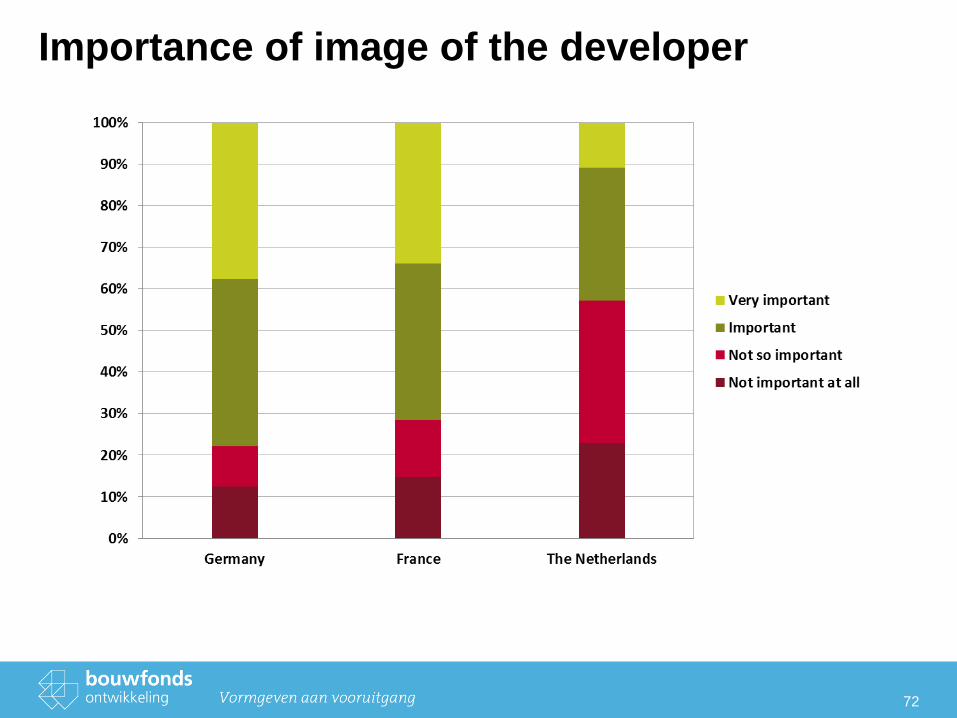

Importance of image of the developer

72

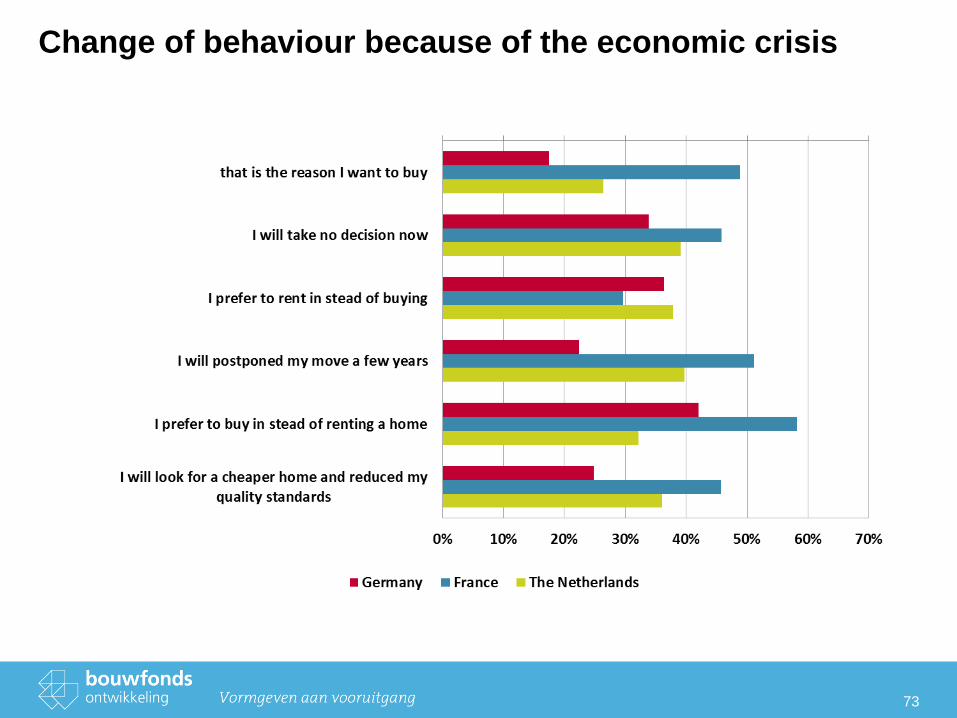

Change of behaviour because of the economic crisis

73

Researchtrends in the

residential market

75

Market research: knowledge is power

What kind of research can we do?

• Location-analysis and DNA-positioning

• Quantitative and qualitative demandanalysis

• Targetgroups

• Supply- and competitoranalysis

• Price-analysis

• Consumer satisfaction

76

Deskresearch and location analysis

Cottages

81

64

20

49

34

71

12

71

15

68

15

Jaren 30 originals

82

59

21

51

22

45

26

56

15

58

17

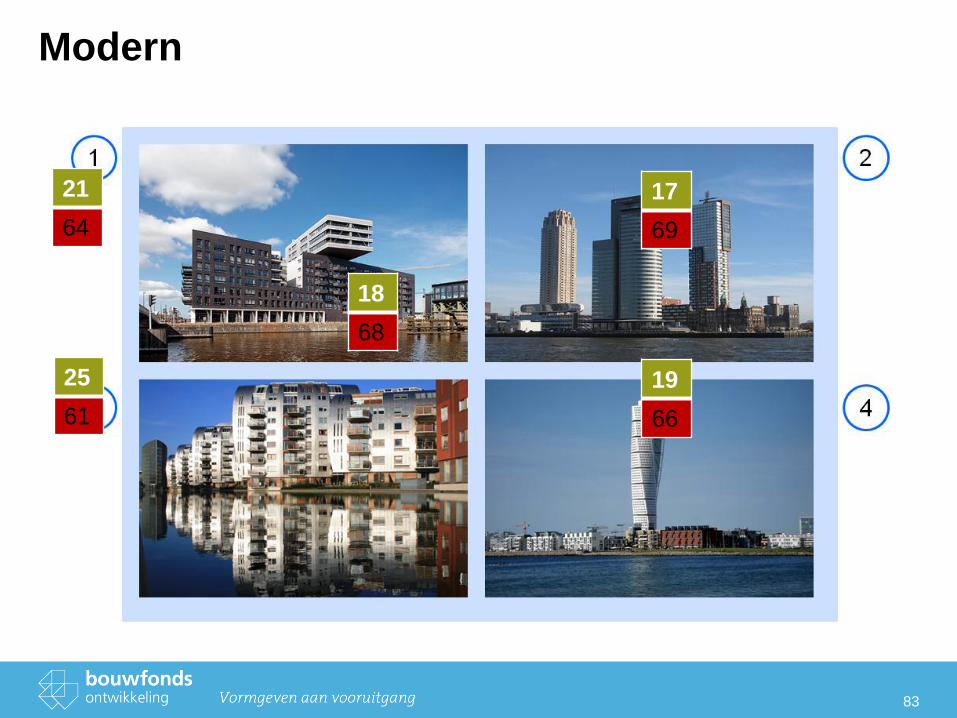

Modern

83

21

64

17

69

19

66

25

61

18

68

Focusgroupsessions

Name presentation, Date 85

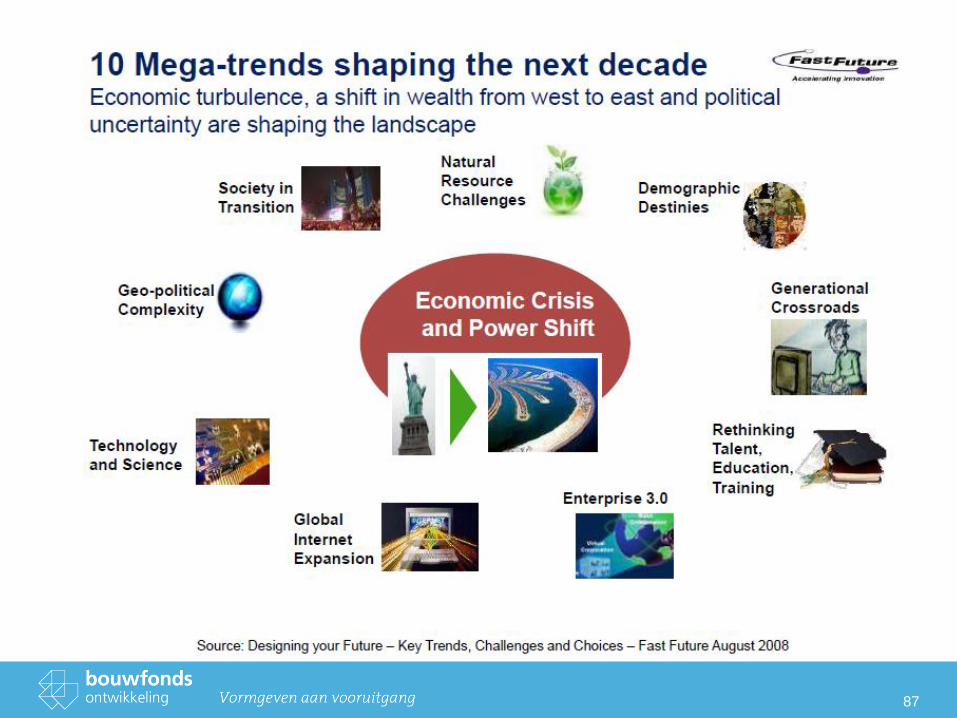

86

The 21e century:

big chances in

consumer behavior

87

88

89

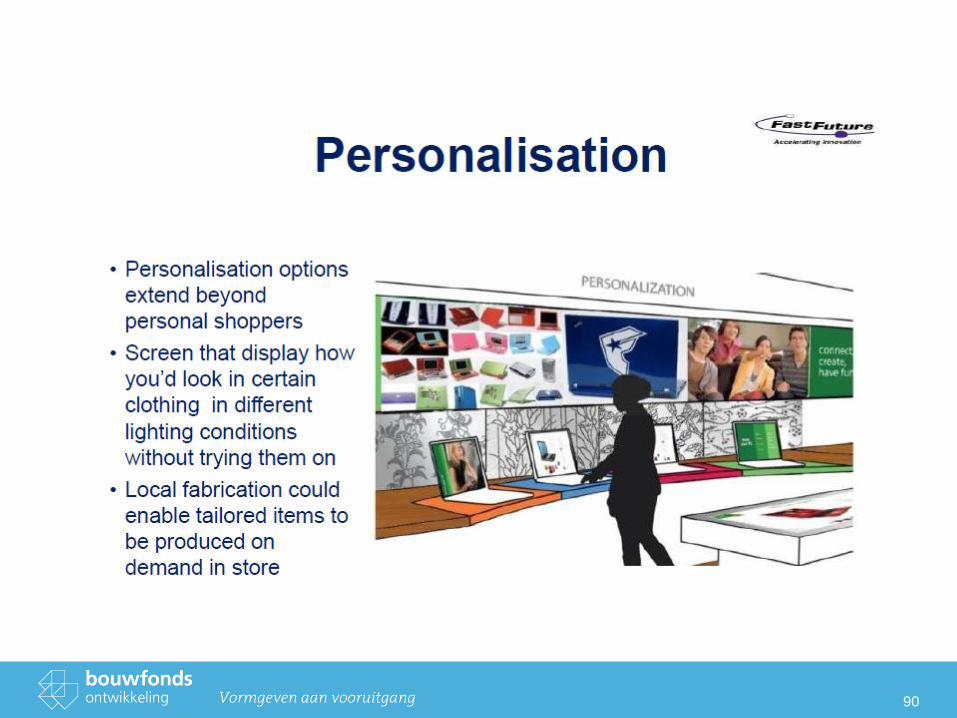

90

91

How do young people want to

live in 10 years?

92

93

94

95

96

97

98

99

100

Middel-hoogbouw: zonder

buitenruimtes een gevangenis-

gevoel (zelfs met zonnig weer)

Amsterdam-IJburg

Kopenhagen Stockholm

Consumersurveys

102

103

104

Mosaic Bouwfonds

1. Mosaic Experian – Introduction into a marketing database

2. Mosaic Bouwfonds - Our custom made segmentation

3. Data used building the segmentation

4. Usage as marketingresearch instrument

5. Five reasons to work with Mosaic Bouwfonds

6. Mosaic in France

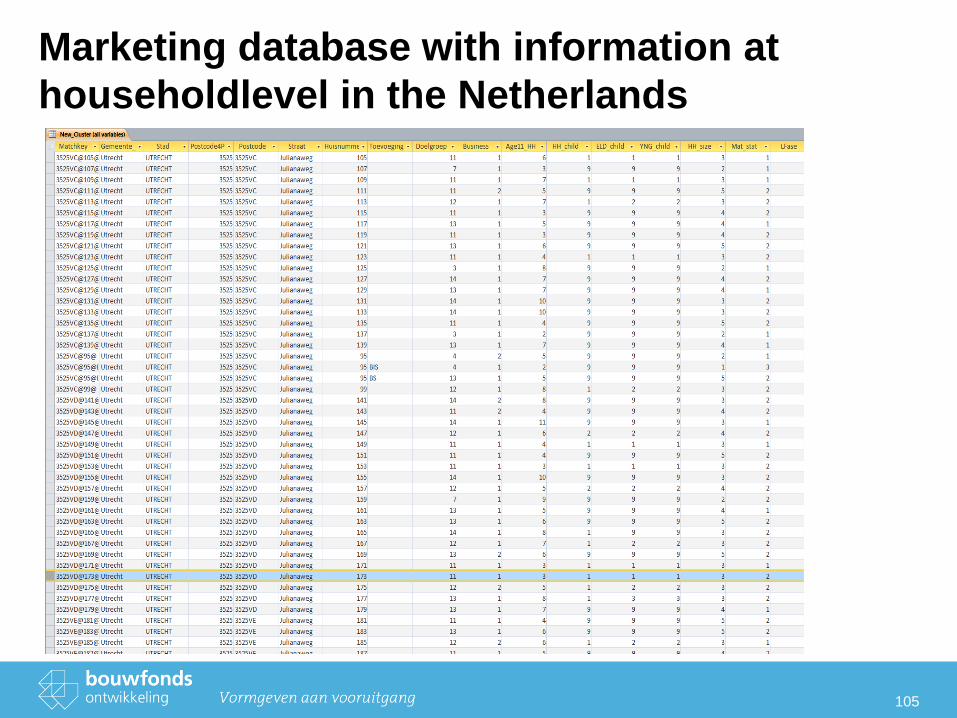

Marketing database with information at

householdlevel in the Netherlands

105

106

Mosaic Bouwfonds

1. Mosaic Experian – Introduction into a marketing database

2. Mosaic Bouwfonds Introduction into a custom made segmentation

3. Data used building the segmentation

4. Usage as marketingresearch instrument

5. Five reasons to work with Mosaic Bouwfonds

6. Mosaic in France

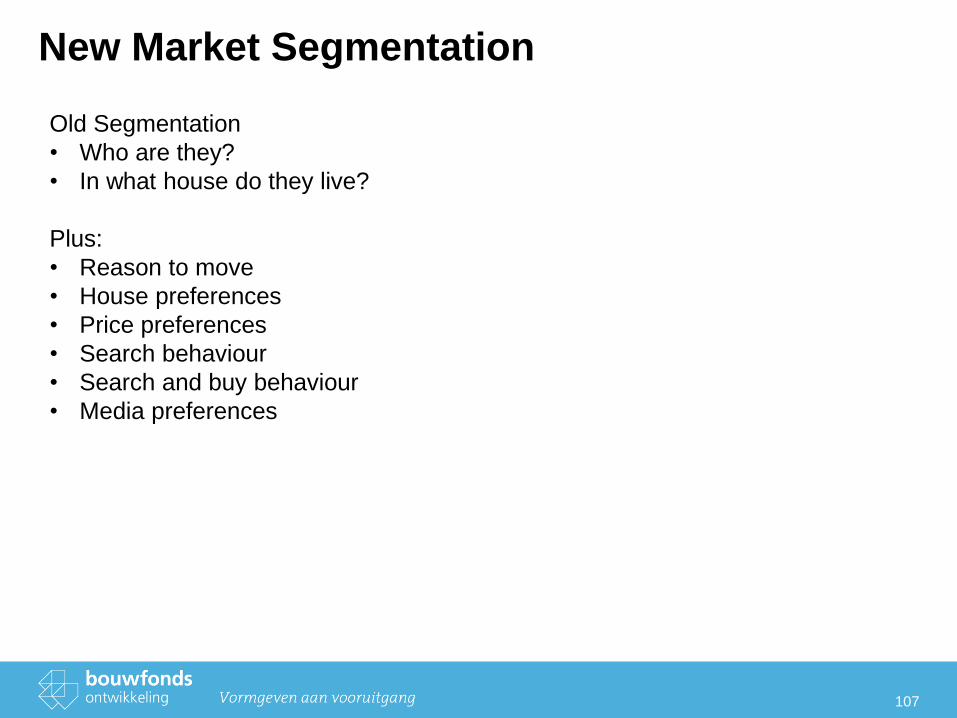

New Market Segmentation

107

Old Segmentation

• Who are they?

• In what house do they live?

Plus:

• Reason to move

• House preferences

• Price preferences

• Search behaviour

• Search and buy behaviour

• Media preferences

108

109

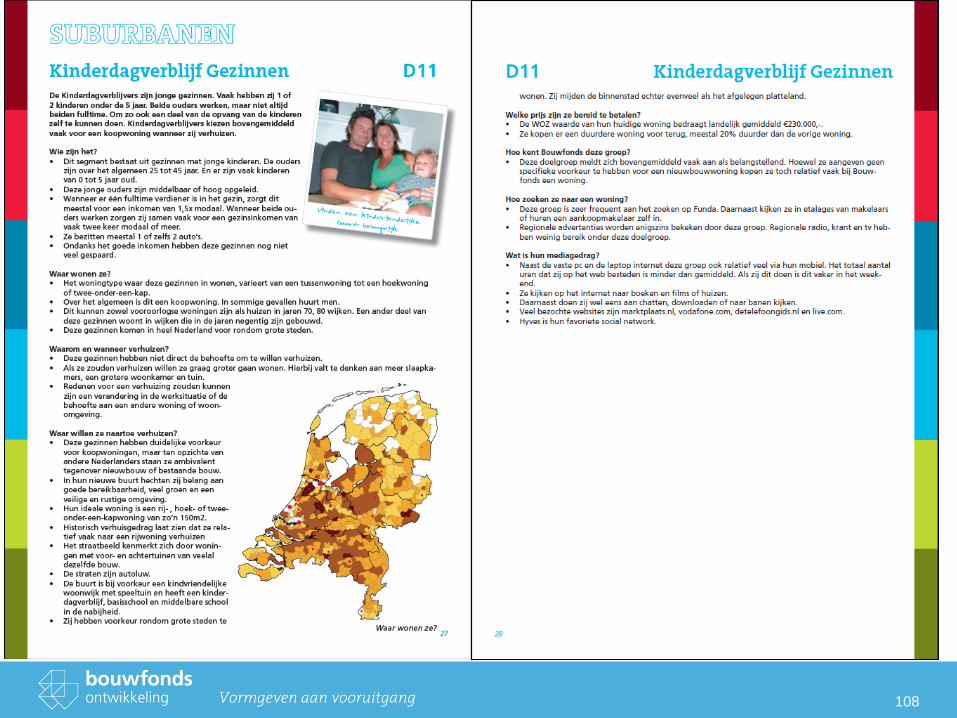

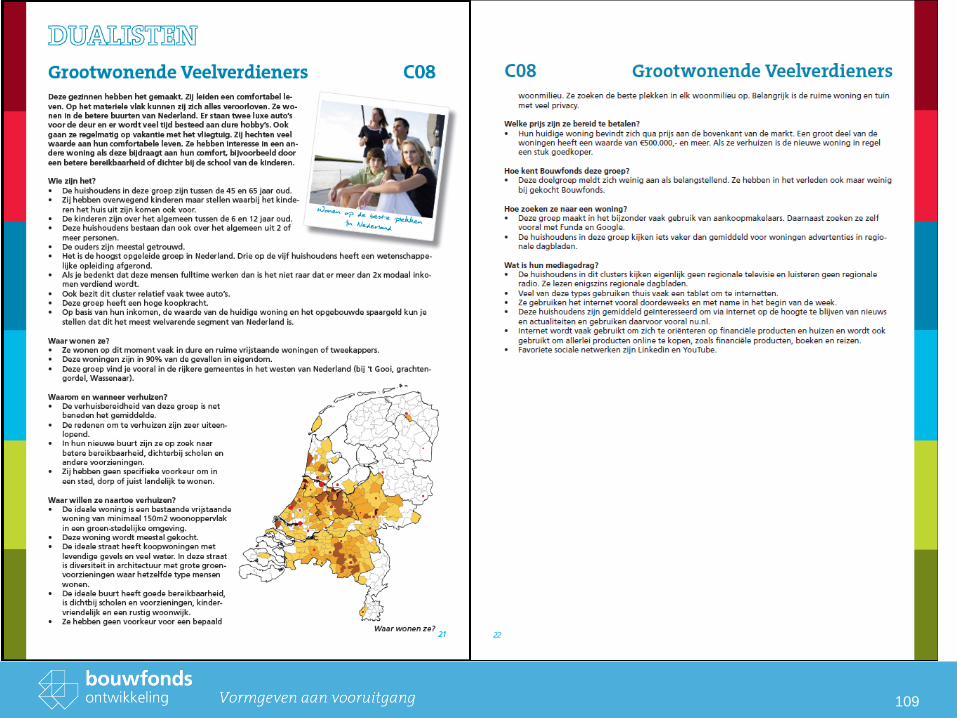

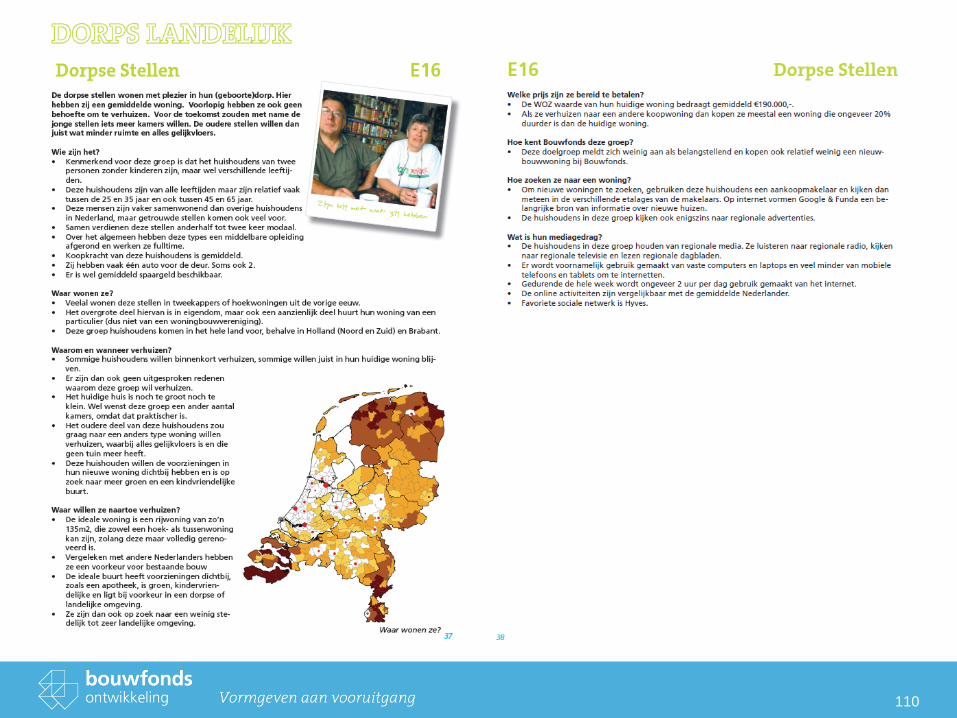

110

Doelgroepen

111

112

Mosaic Bouwfonds

1. Mosaic – Introduction into a marketing database

2. Mosaic Bouwfonds Segmentation

3. Data used building the segmentation

4. Usage as marketingresearch instrument

5. Five reasons to work with Mosaic Bouwfonds

6. Mosaic in France

113

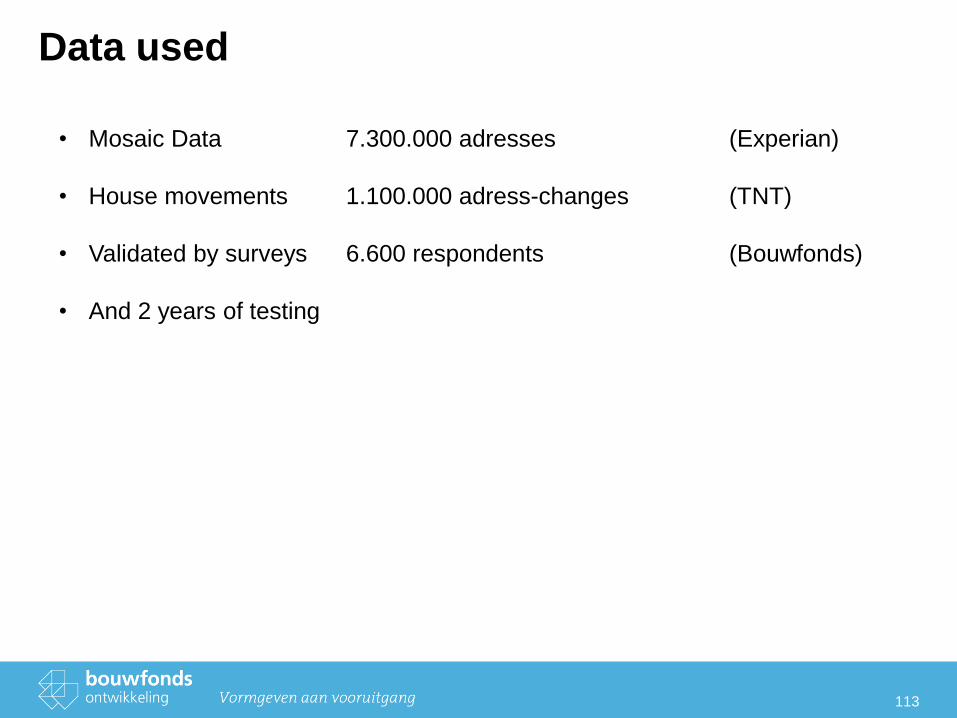

Data used

• Mosaic Data 7.300.000 adresses (Experian)

• House movements 1.100.000 adress-changes (TNT)

• Validated by surveys 6.600 respondents (Bouwfonds)

• And 2 years of testing

114

Mosaic Bouwfonds

1. Mosaic Experian – Introduction into a marketing database

2. Mosaic Bouwfonds Introduction into a custom made segmentation

3. Data used building the segmentation

4. Usage as marketingresearch instrument

5. Five reasons to work with Mosaic Bouwfonds

6. Mosaic in France

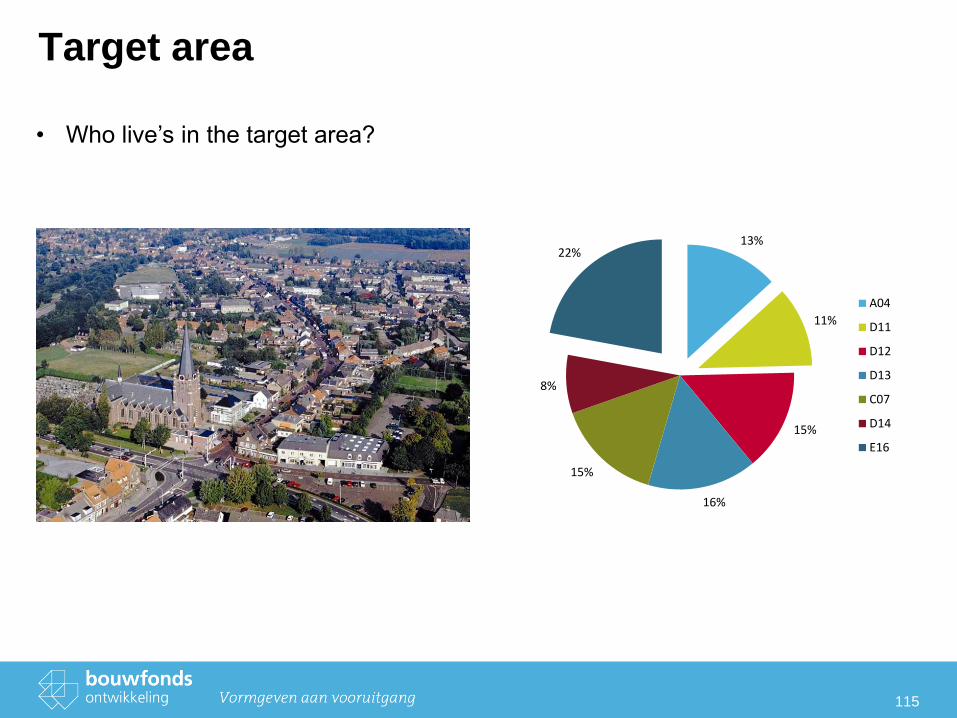

Target area

115

13%

11%

15%

16%

15%

8%

22%

A04

D11

D12

D13

C07

D14

E16

• Who live’s in the target area?

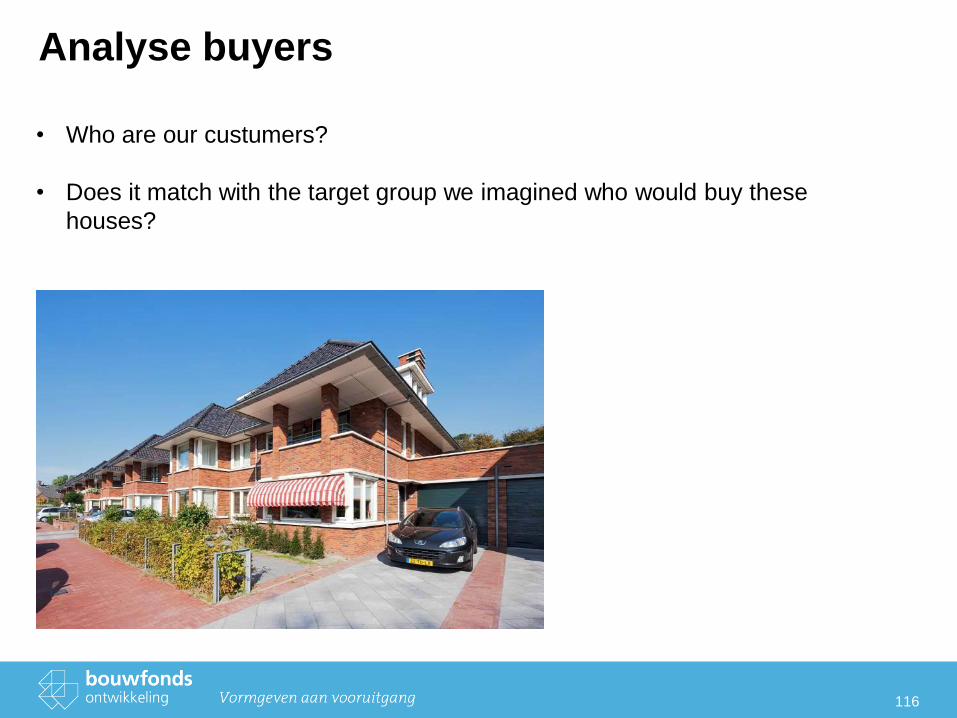

Analyse buyers

116

• Who are our custumers?

• Does it match with the target group we imagined who would buy these

houses?

Five reasons to work with Mosaic Bouwfonds

117

1. It’s a language, a better way to speak about target groups with

municipalities, advertisement agencies, business partners etc.

2. It’s a research instrument. It’s a way to analyse the market / target groups

in the target area.

3. It can be used during the whole proces of real estate development.

4. It’s a marketing instrument. It tells you how to adress target groups and

where to find them.

5. It’s a evaluation instrument. Marketing plans can be compared with the

(harsh) reality.

118

119