research article mean-variance-cvar model of...

TRANSCRIPT

Research ArticleMean-Variance-CvaR Model of Multiportfolio Optimization viaLinear Weighted Sum Method

Younes Elahi and Mohd Ismail Abd Aziz

Faculty of Science Department of Mathematics Universiti Teknologi Malaysia 81310 Johor Bahru Johor Malaysia

Correspondence should be addressed to Younes Elahi elahimathgmailcom

Received 16 July 2013 Accepted 22 January 2014 Published 30 March 2014

Academic Editor Hao Shen

Copyright copy 2014 Y Elahi and M I Abd Aziz This is an open access article distributed under the Creative Commons AttributionLicense which permits unrestricted use distribution and reproduction in any medium provided the original work is properlycited

We propose a new approach to optimizing portfolios to mean-variance-CVaR (MVC) model Although of several researches havestudied the optimal MVCmodel of portfolio the linear weighted summethod (LWSM) was not implemented in the area The aimof this paper is to investigate the optimal portfolio model based on MVC via LWSM With this method the solution of the MVCmodel of portfolio as the multiobjective problem is presented In data analysis section this approach in investing on two assets isinvestigated AnMVCmodel of the multiportfolio was implemented inMATLAB and tested on the presented problem It is shownthat by using three objective functions it helps the investors to manage their portfolio better and thereby minimize the risk andmaximize the return of the portfolio The main goal of this study is to modify the current models and simplify it by using LWSMto obtain better results

1 Introduction

In financial activity a portfolio is a set of assets that allowssomebody to choose from several choices in investing Themain problem in this area is to find out the optimal combi-nation to distribute a given fund on a set of existing assetsMaximization of expected return and minimization of riskare two main aims of this problem [1]

Our goal is to develop the MVCmodel for portfolio withthe weighted coefficients in which this approach is adaptiveof the weighted sum method (WSM) One of the aims is tooffer a practical method for the construction and optimizethe proposed model in order to produce the Pareto optimalsolutionThere are several researches that have been done onthe optimal mean-variance-CVaR (MVC) model of portfoliobut nomuch studies have been carried out in the area by usingthe linear weighted summethod (LWSM)This approach willgive better insight into the multiportfolio process and theposition of investing via finding the feasible solution set

The paper is organized into five sections In the nextsection this paper presents the properties of multiobjectiveportfolio optimization based on mathematical approach andMVC model of portfolio optimization Then MVC model

of portfolio based on LWSM will be presented After thatthe empirical example and some challenges will be shown toclarify the discussion For this aim an MVC model of themultiportfolio was implemented in MATLAB and tested onthe presented problem Finally results and some future worksare presented in the conclusion

2 MVC Model of Portfolio

We face making many decisions in the real world Thereare numerous methods to optimize them The aim of thispaper is to find the Pareto optimal solutions However in thetheoretical problem cases if Pareto set normally cannot besolved by an algorithm thenwe try to approximate the Paretosets [2]

For example the multiobjective model for five objectivefunctions 119891

1 119891

5and some constraints can be shown by

following model [3]

Max [1198911(119909) 119891

5(119909)]119879

Hindawi Publishing CorporationMathematical Problems in EngineeringVolume 2014 Article ID 104064 7 pageshttpdxdoiorg1011552014104064

2 Mathematical Problems in Engineering

st119872

sum119894=1

119909119894= 1 119909

119894ge 0

For 119894 = 1 119872(1)

MVC uses the three parameters (the expected value (119864)the variance (1205902) and the CVaR (conditional value at risk)at a specified confidence level 120572 isin (0 1)) for better modelingThe aim of the proposedmodel is to give a developedmethodfor the solution [4]

We can obtain a better model of portfolio by replacingthe three indexes instead of two parameters as usual so thatit increases the efficiency of the model [5] Several studieson portfolio optimizations viamathematical approaches havebeen investigated in the literature To start the construction ofthis model we consider some variables terms and objectivefunctions as the following nomenclature [6]

Let

119873 be the number of assets that are available119877119909= return (as a random variable) depending on a

decision vector 119909 that belongs to a feasible set 119860119909119894= amount of investing in ith asset

Ω = the feasible set of solutions or search space119904 = a solution of problem120583119894the expected mean of the 119894th asset

1205902(119877119909) = the variance belong to 119877

119909

119870 the number of assets to invest (119870 le 119873)

We define the variable

119911119894= 1 if the 119894th (119894 = 1 119873) asset is chosen0 otherwise

(2)

119909119894= money ratio (0 le 119909

119894le 1) invested in the 119894th (119894 =

1 119873) assetWe consider the MVC model based on Aboulaich et al

method with following formula [4]

(119875)

min CVaR minus119864 var

st 119909 isin

(1199091 119909

119899) |119899

sum119895=1

119909119895= 1

119909119895ge 0 forall119895 isin 1 119899

(3)

We note that for random variable the value of varianceis calculated by the following formula

1205902 (119877119909) = 119864 [(119877

119909minus 119864(119877

119909))2

] (4)

To calculate the variance let 119877119909= 11987711199091+ sdot sdot sdot + 119877

119899119909119899 so we

have

1205902 (119877119909) =119899

sum119894=1

119899

sum119895=1

119909119894119909119895120575119894119895 (5)

where 120575119894119895= cov(119877

119894 119877119895) In addition in the model above

preferring the random variable 119877119909than random variable

119877119910is as the following conditions

119864 (119877119909) ge 119864 (119877

119910) 1205902 (119877

119909) le 1205902 (119877

119910)

CVaR (119877119909) le CVaR (119877

119910)

(6)

in which CVaR is calculated according to following theorem

Proposition 1 (CVaR calculation and optimization) Let 119877119909

be a random variable depending on a decision vector 119909 thatbelongs to a feasible set119860 and 120572 isin (0 1) Consider the function

119865120572(119909 V) =

1

120572119864 [minus119877

119909 +V]+ minus V (7)

where [119906]+ = 119906 for 119906 ge 0 and [119906]+ = 0 for 119906 lt 0 Thenaccording to a function of V 119865

120572is finite and continuous (hence

convex) and

119862119881119886119877 (119865119909) = min

visinR119865120572(119909 V) (8)

In addition the set consisting of the values of V for which theminimum is attained denoted by119860

120572(119909) is a nonempty closed

and bounded interval Minimizing 119862119881119886119877120572with respect to 119909 isin

119860 is equivalent tominimizing119865120572with respect to (119909 V) isin 119860119909119877

min119909isin119860

119862119881119886119877120572(119877119909) = min(119909V)isin119860119909119877

119865120572(119909 V) (9)

In addition a pair (119909lowast Vlowast) minimizes the right-handside if and only if 119909lowast minimize the left-hand side and Vlowast isin119860120572(119909lowast) 119862119881119886119877

120572(119877119909) is convex with respect to 119909 and 119865

120572(119909 V)

is convex with respect to (119909 V)Thus if the set 119860 of feasible decision vectors is convex

(which is the case for the basic version of the portfolio selectionproblem) and even if we impose a further lower limit on theexpected return minimizing CVaR is a convex optimizationproblem [7]

On the other expression MVC model denotes as thefollowing

min1205902 (119909)

subject to 119865120572(119909 V) le 119911

119864 (119909) ge 119889

119909 isin 119860 V isin 119877

(10)

where variables = (1199091 119909

119899) isin 119860 sub 119877119899 V isin 119877 and

set of feasible decision vectors denotes via 119860 that is a convexset In the model above there is one multiobjective system forportfolio optimization that consists of three objective functionsThe first objective function is to minimize the conditionalvalue at risk for portfolio optimization The second objectivefunction denotes minimizing the expected value of return of theportfolio And the last objective function considers minimizingthe variance of returns This procedure shows that we canmanage our capital to invest in several assets [5]

Mathematical Problems in Engineering 3

Table 1 Situation of two assets

AltCriteria

1198621

0101198622

0051198623

030A1 15 10 25A2 30 20 10

3 MVC Model of Portfolio Based on LWSM

Thismethod was introduced by Zadeh in 1963 and it is one ofthe main ways of solving theMO (see [8])Three types of thismethod are used for multiobjective portfolio optimization(MPO) in previous researchThey are weighted summethodweight quadratic method and weight quadratic variation

One of the main ways of weighting methods is theweighted sum method The aim of weighting method is theoptimization of the objective functions that they arrangedby linear combination (weighted sum) Different efficientsolutions can be found by changing the weights of theobjective functions [9]

The weighted sum method changes the MO problemwith a single model of mathematical optimization problemIn the model of this method sum weighting coefficient 119908

119894

multiply each objective function 119891119894to make the structure of

the objective function as follows (note that normalization ofthose coefficients is not necessary)

min119896

sum119894=1

120596119894119891119894(119909)

st 119909 isin Ω

where 120596119894ge 0 forall119894 = 1 119896

119896

sum119894=1

120596119894= 1

(11)

With convexity supposition if 120596119894gt 0 forall119894 = 1 119896 then

the solution of the above system is Pareto optimalThismeansthat if that system is convex then any Pareto optimal solutioncan be found [10] There are three criteria to measure theweightThey are subjective preference of the decisionmakersthe variance measure and the independence of criteriaUsually two methods can be used to achieve this aim theequal weights and the rank-order weights [11 12]

Example 2 (see [13]) Consider that a multiobjective problemincludes three criteria which are denoted by the sameunit and two alternatives According to Table 1 let 119882

1=

010 1198822= 005 and 119882

3= 030 The values of 120572

119894119895are

assumed to be as follows

119860 = [15 10 2530 20 10

] (12)

Therefore the decision matrix for this MCDM problem is asfollows

Criteria 010 005 030Alternatives A1 A2

With (10) we obtain data as follows

A1 (WSM Score) = 15 times 010 + 10

times 005 + 25 times 030 = 275(13)

In the same ways

A2 (WSM Score) = 30 times 010 + 20

times 005 + 10 times 030 = 7(14)

So the optimal case in the minimization situation is alterna-tiveA1 because it has the lowestWSM scoreWe can write thealternative ranking as follows A1 lt A1 (where ldquoltrdquo denotesldquobetter thanrdquo)

Now we formulate the portfolio revision problem withtransaction costs as a standard mathematical optimizationproblem with the mean-risk framework We will employ thefollowing notation

119873 number of risky assets119890 vector with all entries equal to ones

Consider the optimization problem with the normalizedsingle objective as follows

Maximize 119891 (119909) =119897

sum119896=1

1205961198961198760119896(119909)

Subject to 119909 isin 119883 = 119909 | 119891119894(119909) ge 0 119892

119894(119909)= 0 1 119897

(15)

where the weights are denoted by 120596119894 and

120596119894ge 0

119897

sum119894=1

120596119894= 1 119894 = 1 119897 (16)

And the objective function of 119896th objective function119876119896(119909) after normalization is denoted by 1198760

119896(119909) 119896 = 1 119897

Also we call 119891119894(119909) 119892

119894(119909)inequality and equality constraints

respectively With LWSM approach we have

119876119896(119909) =

119897

sum119894=1

119886119896119894119909119894 119886119896119894isin 119877 (17)

Therefore normalized objective functions have the followingform

1198760119896(119909) =

119876119896(119909)

119878119896

=1198861198961

119878119896

1199091+ sdot sdot sdot +

119886119896119899

119878119896

119909119899 (18)

in which case the floating-point values 119878119896are evaluated in the

following way

119878119896=119899

sum119895=1

1003816100381610038161003816100381611988611989611989510038161003816100381610038161003816 = 0 (19)

Obviously in many practical problems the objectivefunctions are represented by various measure units (eg if

4 Mathematical Problems in Engineering

1198761is measured in kilos 119876

2in seconds etc) For this reason

the objective function normalization is required It is nowobvious that the coefficients have values of the segment [0 1]Denote that we now have the linear programming problem

Maximize 119891 (119909) =119897

sum119896=1

120596119896

119876119896(119909)

119878119896

= 1205961

1198861198961

119878119896

1199091

+ sdot sdot sdot + 120596119899

119886119896119899

119878119896

119909119899

Subject to 119909 isin 119883

(20)

The following theorem gives the practical criteria forthe detection of some Pareto optimal solutions of problem(24) Yu et al [14] presented mean-CVaR model of portfoliooptimization based on LWSM inwhich they assumed that thereturn of the portfolio is based on multi-t-distribution andthey obtained the model for

max (119906 (119908)) = max (1205721119864 (119877) minus 120572

2CVaR) (21)

as follows

max05 (119908119879120583) + 05(120572 + 1

119898 (1 minus 05)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(22)

There are some conditions for coefficients that are usedin WSM For example the sum of them equal 1 and theyare strictly positive In addition to LWSM they must benormalized With this idea the multiportfolio optimizationproblem is as follows

min (119906 (119908)) = min (12057211205902 (119877) minus 120572

2119864 (119877) + 120572

3CVaR)

Subject to 119909 isin 119860(23)

where 1205721 1205722 and 120572

3are strictly positive and 119860 is as the

above assumptions Since all objective functions on MVCmodel are convex we can define the model above to find thesolution as the Pareto optimal set [15] For instance if weconsider 120572

1= 1 120572

2= 0 and 120572

3= 0 the problem turns

to minimize the variance of the portfolio [5]Now according to (P2) as themultiobjective optimization

problem LWSM will be used to solve it as in the followingprocedure

Step 1 Construct the problem based on

min (119906 (119908)) = min (12057211205902 (119877) minus 120572

2119864 (119877) + 120572

3CVaR) (24)

There are several positions of investing for investorwho can manage hisher budget which is related to theamount of 120572

1 1205722 and 120572

3 This note creates several cases

for investors to increase the return or decrease the riskof a portfolio The risk (or return) has an inverse (direct)relation with those coefficientsThe LWSM leads to followingprocedure for MVC model of portfolio

Step 2 Consider

min1205721(119908119879120590119908) minus 120572

2(119908119879120583)

+ 1205723(120572 +

1

119898 (1 minus 120573)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(25)

where 120572 120573 are the belief degree and specific parameterrespectively In this paper it is considered that 120573 = 05 Inaddition according to sum119899

119894=1120572119894= 1 we have 1minus(120572

1+ 1205722) = 1205723

we rewrite problem of (18) as follows

min1205721(119908119879120590119908) minus 120572

2(119908119879120583) + (1 minus (120572

1+ 1205722))

times (120572 +1

119898 (1 minus 05)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894

0 le 119908119894le 1

(26)

where the belief degree of 120572 set is equal to 095 In additionin CVaR formula after linearization [16 17] we have

119865120573(119908 120572) = 120572 +

1

119898 (1 minus 120573)

119898

sum119896=1

[119891 (119908 119910119896) + 120572]

+

(27)

and 119891(119908 119910119896) is the loss function which can be defined [16]

by 119891(119908 119910119896) = minus119908119879119910

119896 We can rewrite (19) according to the

assumptions above as follows

min1205721(119908119879120590119908) minus 120572

2(119908119879120583) + (1 minus (120572

1+ 1205722))

times (095 +1

119898 (1 minus 05)

119898

sum119896=1

[minus119908119879119910119896+ 095]

+

)

st

[119906]+ = max 119906 0119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(28)

where 120583119896is return of 119896th asset In the model above we

consider119898 = 2 and we have

min1205721(119908119879120590119908) minus 120572

2(119908119879120583) + (1 minus (120572

1+ 1205722))

times (095 +1

2 (1 minus 05)2 ([minus119908119879119910

119896+ 095]

+

))

st

[119906]+ = max 119906 0119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(29)

Mathematical Problems in Engineering 5

4 Empirical Research and Challenges

In order to evaluate the model above to find the portfoliooptimization based on LWSM we consider two assets whosemean return 120583 and covariance matrix 120590 are as the followingdata (data from [14 16])

120583 = (0067609870034191

)

120590 = (0058884101 00004640430000464043 00003643663

)

(30)

According to the data above and the model of (29) we have

min119885 = min1205721(1199111) minus 1205722(1199112) + (1 minus (120572

1+ 1205722)) (1199113) (31)

where

1199111= 1205752119901= 119908119879120590119908 =

= (0058884101 lowast 1199081+ 0000464043 lowast 119908

2) lowast 1199081

+ (0000464043 lowast 1199081+ 00003643663 lowast 119908

2) lowast 1199082

1199112= 120583119901= 119908119879120583 = 006760987119908

1+ 0034191119908

2

1199113= (095 +

1

2 (1 minus 05)2 ([minus119908119879120583 minus 095]

+

))

= 095 +1

2 (05)

times 2 ([minus (0067609871199081+ 0034191119908

2) + 095]

+

)

[119906]+ = max 119906 0

119899

sum119894=1

119908119894

= 1 0 le 119908119894le 1

(32)

Now we consider this proposed model for 1205721= 025 120572

2=

025 Therefore we have

minZ = min (001472102525 lowast 11990821

+ 000058005375 lowast 1199081lowast 1199082

+00003643663 lowast 11990822)

minus (001690246751199081+ 000854775119908

2)

+ (0475 + ([minus (0067609871199081+ 0034191119908

2)

+095]+))

st

[119906]+ = max 119906 0119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(33)

01000

20003000

minus001

minus0005

0minus1

minus05

0

05

1

10

20

30

40

50

60

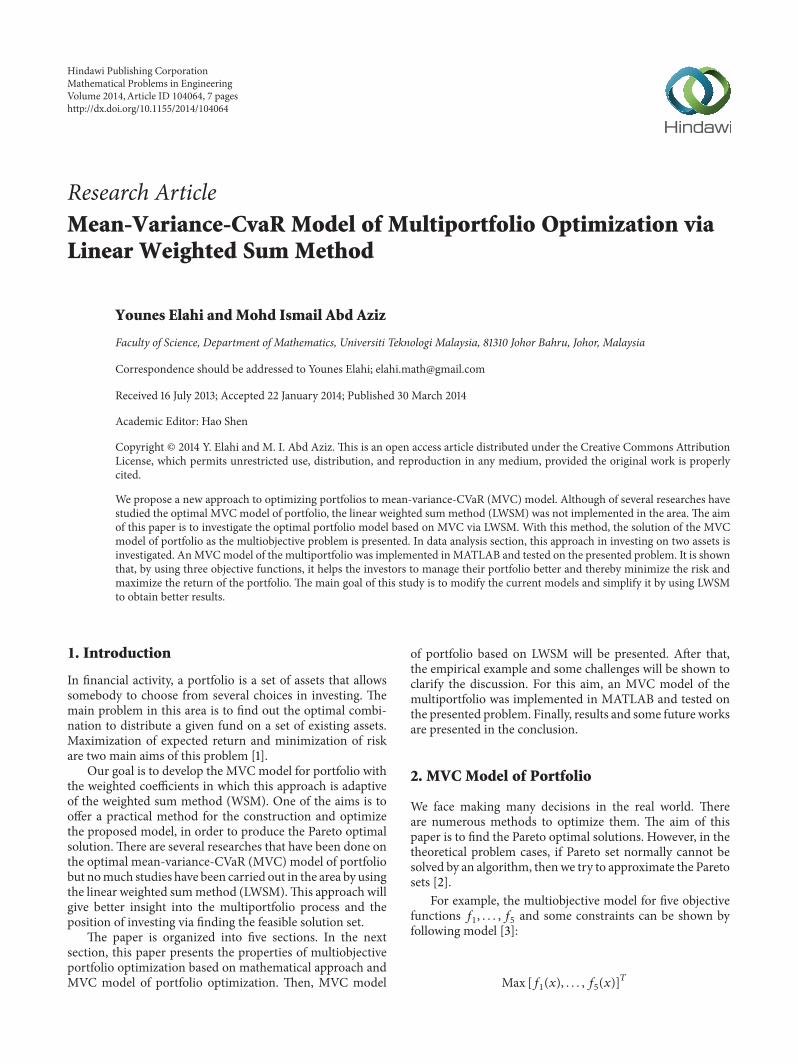

Figure 1 Mean-variance model of portfolio via LWSM

0

0

2000 4000 6000 8000 10000 120000

1

2

minus1

minus05

05

1

10

20

30

40

50

60

Data 1

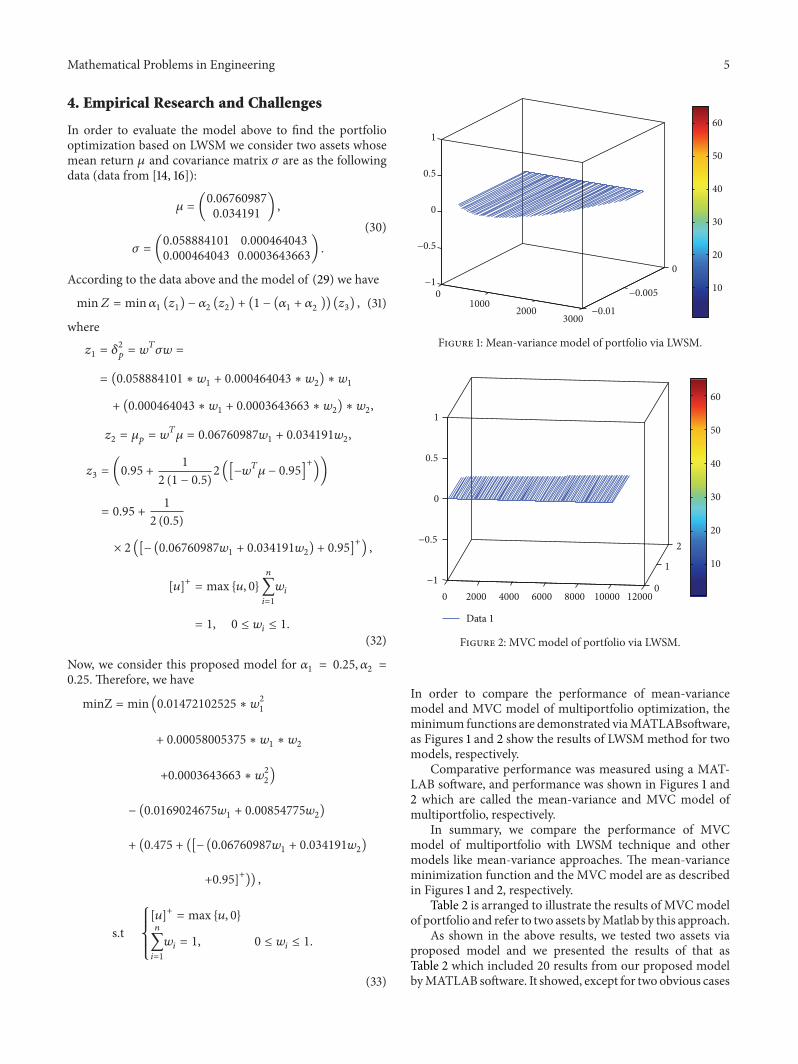

Figure 2 MVC model of portfolio via LWSM

In order to compare the performance of mean-variancemodel and MVC model of multiportfolio optimization theminimum functions are demonstrated viaMATLABsoftwareas Figures 1 and 2 show the results of LWSMmethod for twomodels respectively

Comparative performance was measured using a MAT-LAB software and performance was shown in Figures 1 and2 which are called the mean-variance and MVC model ofmultiportfolio respectively

In summary we compare the performance of MVCmodel of multiportfolio with LWSM technique and othermodels like mean-variance approaches The mean-varianceminimization function and the MVC model are as describedin Figures 1 and 2 respectively

Table 2 is arranged to illustrate the results of MVCmodelof portfolio and refer to two assets byMatlab by this approach

As shown in the above results we tested two assets viaproposed model and we presented the results of that asTable 2 which included 20 results from our proposed modelbyMATLAB software It showed except for two obvious cases

6 Mathematical Problems in Engineering

Table 2 Results of MVC model of portfolio refer to two assets (seeSection 4) by MATLAB

1199081= 0000000 119908

2= 1000000 119911 = 1083819

1199081= 0010000 119908

2= 0990000 119911 = 1086554

1199081= 0020000 119908

2= 0980000 119911 = 1089293

1199081= 0030000 119908

2= 0970000 119911 = 1092035

1199081= 0040000 119908

2= 0960000 119911 = 1094779

1199081= 0050000 119908

2= 0950000 119911 = 1097527

1199081= 0060000 119908

2= 0940000 119911 = 1100278

1199081= 0070000 119908

2= 0930000 119911 = 1103031

1199081= 0080000 119908

2= 0920000 119911 = 1105788

1199081= 0090000 119908

2= 0910000 119911 = 1108547

1199081= 0100000 119908

2= 0900000 119911 = 1111310

1199081= 0110000 119908

2= 0890000 119911 = 1114075

1199081= 0120000 119908

2= 0880000 119911 = 1116844

1199081= 0130000 119908

2= 0870000 119911 = 1119615

1199081= 0140000 119908

2= 0860000 119911 = 1122389

1199081= 0150000 119908

2= 0850000 119911 = 1125167

1199081= 0160000 119908

2= 0840000 119911 = 1127947

1199081= 0170000 119908

2= 0830000 119911 = 1130730

1199081= 0180000 119908

2= 0820000 119911 = 1133517

1199081= 0190000 119908

2= 0810000 119911 = 1136306

1199081= 0200000 119908

2= 0800000 119911 = 1139098

1199081= 0210000 119908

2= 0790000 119911 = 1141893

1199081= 0220000 119908

2= 0780000 119911 = 1144691

1199081= 0230000 119908

2= 0770000 119911 = 1147493

1199081= 0240000 119908

2= 0760000 119911 = 1150297

1199081= 0250000 119908

2= 0750000 119911 = 1153104

1199081= 0260000 119908

2= 0740000 119911 = 1155914

1199081= 0270000 119908

2= 0730000 119911 = 1158727

1199081= 0280000 119908

2= 0720000 119911 = 1161543

1199081= 0290000 119908

2= 0710000 119911 = 1164362

1199081= 0300000 119908

2= 0700000 119911 = 1167184

1199081= 0310000 119908

2= 0690000 119911 = 1170009

1199081= 0320000 119908

2= 0680000 119911 = 1172837

1199081= 0330000 119908

2= 0670000 119911 = 1175668

1199081= 0340000 119908

2= 0660000 119911 = 1178501

1199081= 0350000 119908

2= 0650000 119911 = 1181338

1199081= 0360000 119908

2= 0640000 119911 = 1184178

1199081= 0370000 119908

2= 0630000 119911 = 1187021

1199081= 0380000 119908

2= 0620000 119911 = 1189867

1199081= 0390000 119908

2= 0610000 119911 = 1192715

1199081= 0400000 119908

2= 0600000 119911 = 1195567

1199081= 0410000 119908

2= 0590000 119911 = 1198422

1199081= 0420000 119908

2= 0580000 119911 = 1201279

1199081= 0430000 119908

2= 0570000 119911 = 1204140

1199081= 0440000 119908

2= 0560000 119911 = 1207004

1199081= 0450000 119908

2= 0550000 119911 = 1209870

1199081= 0460000 119908

2= 0540000 119911 = 1212740

1199081= 0470000 119908

2= 0530000 119911 = 1215612

1199081= 0480000 119908

2= 0520000 119911 = 1218488

1199081= 0490000 119908

2= 0510000 119911 = 1221366

Table 2 Continued

1199081= 0500000 119908

2= 0500000 119911 = 1224248

1199081= 0510000 119908

2= 0490000 119911 = 1227132

1199081= 0520000 119908

2= 0480000 119911 = 1230019

1199081= 0530000 119908

2= 0470000 119911 = 1232910

1199081= 0540000 119908

2= 0460000 119911 = 1235803

1199081= 0550000 119908

2= 0450000 119911 = 1238699

1199081= 0560000 119908

2= 0440000 119911 = 1241599

1199081= 0570000 119908

2= 0430000 119911 = 1244501

1199081= 0580000 119908

2= 0420000 119911 = 1247406

1199081= 0590000 119908

2= 0410000 119911 = 1250314

1199081= 0600000 119908

2= 0400000 119911 = 1253225

1199081= 0610000 119908

2= 0390000 119911 = 1256140

1199081= 0620000 119908

2= 0380000 119911 = 1259057

1199081= 0630000 119908

2= 0370000 119911 = 1261977

1199081= 0640000 119908

2= 0360000 119911 = 1264900

1199081= 0650000 119908

2= 0350000 119911 = 1267826

1199081= 0660000 119908

2= 0340000 119911 = 1270755

1199081= 0670000 119908

2= 0330000 119911 = 1273687

1199081= 0680000 119908

2= 0320000 119911 = 1276622

1199081= 0690000 119908

2= 0310000 119911 = 1279560

1199081= 0700000 119908

2= 0300000 119911 = 1282501

1199081= 0710000 119908

2= 0290000 119911 = 1285445

1199081= 0720000 119908

2= 0280000 119911 = 1288392

1199081= 0730000 119908

2= 0270000 119911 = 1291341

1199081= 0740000 119908

2= 0260000 119911 = 1294294

1199081= 0750000 119908

2= 0250000 119911 = 1297250

1199081= 0760000 119908

2= 0240000 119911 = 1300209

1199081= 0770000 119908

2= 0230000 119911 = 1303170

1199081= 0780000 119908

2= 0220000 119911 = 1306135

1199081= 0790000 119908

2= 0210000 119911 = 1309103

1199081= 0800000 119908

2= 0200000 119911 = 1312074

1199081= 0810000 119908

2= 0190000 119911 = 1315047

1199081= 0820000 119908

2= 0180000 119911 = 1318024

1199081= 0830000 119908

2= 0170000 119911 = 1321003

1199081= 0840000 119908

2= 0160000 119911 = 1323986

1199081= 0850000 119908

2= 0150000 119911 = 1326971

1199081= 0860000 119908

2= 0140000 119911 = 1329960

1199081= 0870000 119908

2= 0130000 119911 = 1332951

1199081= 0880000 119908

2= 0120000 119911 = 1335946

1199081= 0890000 119908

2= 0110000 119911 = 1338943

1199081= 0900000 119908

2= 0100000 119911 = 1341944

1199081= 0910000 119908

2= 0090000 119911 = 1344947

1199081= 0920000 119908

2= 0080000 119911 = 1347953

1199081= 0930000 119908

2= 0070000 119911 = 1350963

1199081= 0940000 119908

2= 0060000 119911 = 1353975

1199081= 0950000 119908

2= 0050000 119911 = 1356990

1199081= 0960000 119908

2= 0040000 119911 = 1360008

1199081= 0970000 119908

2= 0030000 119911 = 1363030

1199081= 0980000 119908

2= 0020000 119911 = 1366054

1199081= 0990000 119908

2= 0010000 119911 = 1369081

1199081= 1000000 119908

2= 0000000 119911 = 1372111

Mathematical Problems in Engineering 7

(1199081= 0 and 119908

2= 1 119908

1= 1 and 119908

2= 0) that the minimum

situation ofMVCmodel ofmultiportfoliowill occurr on1199081=

001 and 1199082= 099 The results illustrate that the proposed

method is better for investing a small amount of assets suchas the above two assets

Despite of the several advantages this method has somedisadvantages which one of them is the weights 120572

1 1205722

and 1205723that are hard to understand [5] The other one is

how to use the Simplex method to solve the weightedsum problem The solution of this problem is using othertechniques (eg interior-point methods) [10]

5 Conclusion

In this investigation we consider three objective functions tomodel portfolio optimization with LWSM In addition wepropose a linear weighted sum method to solve the MCVmodel of portfolio optimization Also with empirical exam-ple and MATLAB software we evaluated proposed modelOur example includes two assets for investing However itis flexible to choose more assets and find the Pareto optimalaccording to procedures that are used in this paper

The contribution of this study is a presentation of MVCmodel of portfolio optimization based on LWSMThe empir-ical examples have shown that using the three objectivefunctions tomake a powerfulmulti-portfoliomodelWe havedescribed the MVC model of multiportfolio optimizationthat it is extended of the model presented by Yu et al [14]In addition we showed that theMVCmodel generally coversboth mean-variance and mean-CVaR models of portfoliooptimization (with changing the coefficients of 120572

119894 119894 = 1 3)

Furthermore this paper has given new insight into themultiobjective decision making process via WSM A hybridof this method and other techniques such as interior-pointmethods can be a good idea for future researchers

To sum up with using three objective functions it helpsthe investors to manage their portfolio better and therebyminimize the risk and maximize the return of the portfolioAlso using LWSM dues to modify the current models andsimplify it to obtain better results The same approach canalso be used for other multiobjective optimizationmodel andinvesting applications

Conflict of Interests

The authors declare that there is no conflict of interestsregarding the publication of this paper

Acknowledgment

Research reported in this publication was supported byUniversiti Teknologi Malaysia under grant number 4B112(Research Management Centre Universiti TeknologiMalaysia)

References

[1] Y Elahi and A A Mohd-Ismail ldquoMulti-objectives portfo-lio optimization challenges and opportunities for islamicapproachrdquoAustralian Journal of Basic and Applaied Sicence vol6 no 10 pp 297ndash302 2012

[2] I Radziukyniene and A Zilinskas ldquoEvolutionary methods formulti-objective portfolio optimizationrdquo in Proceedings of theWorld Congress on Engineering 2008

[3] C Chiranjeevi and V N Sastry ldquoMulti objective portfoliooptimization models and its solution using genetic algorithmsrdquoin Proceedings of the International Conference on ComputationalIntelligence andMultimediaApplications (ICCIMA rsquo07) Decem-ber 2007

[4] R Aboulaich R Ellaia and S El Moumen ldquoThe mean-variance-CVaR model for portfolio optimization modelingusing a multi-objective approach based on a hybrid methodrdquoMathematical Modelling of Natural Phenomena vol 5 no 7 pp103ndash108 2010

[5] D Roman K Darby-Dowman and G Mitra ldquoMean-riskmodels using two risk measures a multi-objective approachrdquoQuantitative Finance vol 7 no 4 pp 443ndash458 2007

[6] R Armananzas and J A Lozano ldquoAmultiobjective approach tothe portfolio optimization problemrdquo in Proceedings of the IEEECongress on Evolutionary Computation (CEC rsquo05) September2005

[7] D Roman K Darby-Dowman and G Mitra ldquoPortfolio con-struction based on stochastic dominance and target returndistributionsrdquo Mathematical Programming vol 108 no 2 pp541ndash569 2006

[8] L Zadeh ldquoOptimality and non-scalar-valued performancecriteriardquo IEEE Transactions on Automatic Control vol 8 no 1pp 59ndash60 1963

[9] K Kirytopoulos V Leopoulos G Mavrotas and D Voulgar-idou ldquoMultiple sourcing strategies and order allocation anANP-AUGMECON meta-modelrdquo Supply Chain Managementvol 15 no 4 pp 263ndash276 2010

[10] O Grodzevich and O Romanko ldquoNormalization and othertopics in multi-objective optimizationrdquo 2006

[11] J Jia GW Fischer and J S Dyer ldquoAttribute weightingmethodsand decision quality in the presence of response error asimulation studyrdquo Journal of Behavioral Decision Making vol11 no 2 pp 85ndash105 1998

[12] B Sawik ldquoA reference point approach to bi-objective dynamicportfolio optimizationrdquo Decision Making in Manufacturing andServices vol 3 no 1-2 pp 73ndash85 2009

[13] O Romanko A Ghaffari-Hadigheh and T Terlaky ldquoMulti-objective optimization via parametric optimization modelsalgorithms and applicationsrdquo Modeling and Optimization pp77ndash119 2012

[14] X Yu Y Tan L Liu and W Huang ldquoThe optimal portfoliomodel based onmean-CvaRwith linear weighted summethodrdquoin Fifth International Joint Conference on Computational Sci-ences and Optimization (CSO rsquo12) pp 82ndash84 June 2012

[15] J Jahn ldquoSome characterizations of the optimal solutions of avector optimization problemrdquo Operations-Research-Spektrumvol 7 pp 7ndash17 1985

[16] X YuH Sun andG Chen ldquoThe optimal portfoliomodel basedon mean-CVaRrdquo Journal of Mathematical Finance vol 1 no 3pp 132ndash134 2011

[17] S Uryasev ldquoConditional value-at-risk optimization algorithmsand applicationsrdquo in Proceedings of the IEEEIAFEINFORNS6th Conference on Computational Intelligence for FinancialEngineering (CIFEr rsquo00) pp 49ndash57 March 2000

Submit your manuscripts athttpwwwhindawicom

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Mathematical Problems in Engineering

Hindawi Publishing Corporationhttpwwwhindawicom

Differential EquationsInternational Journal of

Volume 2014

Applied MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Probability and StatisticsHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Mathematical PhysicsAdvances in

Complex AnalysisJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

OptimizationJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

CombinatoricsHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

International Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Operations ResearchAdvances in

Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Function Spaces

Abstract and Applied AnalysisHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

International Journal of Mathematics and Mathematical Sciences

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

The Scientific World JournalHindawi Publishing Corporation httpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Algebra

Discrete Dynamics in Nature and Society

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Decision SciencesAdvances in

Discrete MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom

Volume 2014 Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Stochastic AnalysisInternational Journal of

2 Mathematical Problems in Engineering

st119872

sum119894=1

119909119894= 1 119909

119894ge 0

For 119894 = 1 119872(1)

MVC uses the three parameters (the expected value (119864)the variance (1205902) and the CVaR (conditional value at risk)at a specified confidence level 120572 isin (0 1)) for better modelingThe aim of the proposedmodel is to give a developedmethodfor the solution [4]

We can obtain a better model of portfolio by replacingthe three indexes instead of two parameters as usual so thatit increases the efficiency of the model [5] Several studieson portfolio optimizations viamathematical approaches havebeen investigated in the literature To start the construction ofthis model we consider some variables terms and objectivefunctions as the following nomenclature [6]

Let

119873 be the number of assets that are available119877119909= return (as a random variable) depending on a

decision vector 119909 that belongs to a feasible set 119860119909119894= amount of investing in ith asset

Ω = the feasible set of solutions or search space119904 = a solution of problem120583119894the expected mean of the 119894th asset

1205902(119877119909) = the variance belong to 119877

119909

119870 the number of assets to invest (119870 le 119873)

We define the variable

119911119894= 1 if the 119894th (119894 = 1 119873) asset is chosen0 otherwise

(2)

119909119894= money ratio (0 le 119909

119894le 1) invested in the 119894th (119894 =

1 119873) assetWe consider the MVC model based on Aboulaich et al

method with following formula [4]

(119875)

min CVaR minus119864 var

st 119909 isin

(1199091 119909

119899) |119899

sum119895=1

119909119895= 1

119909119895ge 0 forall119895 isin 1 119899

(3)

We note that for random variable the value of varianceis calculated by the following formula

1205902 (119877119909) = 119864 [(119877

119909minus 119864(119877

119909))2

] (4)

To calculate the variance let 119877119909= 11987711199091+ sdot sdot sdot + 119877

119899119909119899 so we

have

1205902 (119877119909) =119899

sum119894=1

119899

sum119895=1

119909119894119909119895120575119894119895 (5)

where 120575119894119895= cov(119877

119894 119877119895) In addition in the model above

preferring the random variable 119877119909than random variable

119877119910is as the following conditions

119864 (119877119909) ge 119864 (119877

119910) 1205902 (119877

119909) le 1205902 (119877

119910)

CVaR (119877119909) le CVaR (119877

119910)

(6)

in which CVaR is calculated according to following theorem

Proposition 1 (CVaR calculation and optimization) Let 119877119909

be a random variable depending on a decision vector 119909 thatbelongs to a feasible set119860 and 120572 isin (0 1) Consider the function

119865120572(119909 V) =

1

120572119864 [minus119877

119909 +V]+ minus V (7)

where [119906]+ = 119906 for 119906 ge 0 and [119906]+ = 0 for 119906 lt 0 Thenaccording to a function of V 119865

120572is finite and continuous (hence

convex) and

119862119881119886119877 (119865119909) = min

visinR119865120572(119909 V) (8)

In addition the set consisting of the values of V for which theminimum is attained denoted by119860

120572(119909) is a nonempty closed

and bounded interval Minimizing 119862119881119886119877120572with respect to 119909 isin

119860 is equivalent tominimizing119865120572with respect to (119909 V) isin 119860119909119877

min119909isin119860

119862119881119886119877120572(119877119909) = min(119909V)isin119860119909119877

119865120572(119909 V) (9)

In addition a pair (119909lowast Vlowast) minimizes the right-handside if and only if 119909lowast minimize the left-hand side and Vlowast isin119860120572(119909lowast) 119862119881119886119877

120572(119877119909) is convex with respect to 119909 and 119865

120572(119909 V)

is convex with respect to (119909 V)Thus if the set 119860 of feasible decision vectors is convex

(which is the case for the basic version of the portfolio selectionproblem) and even if we impose a further lower limit on theexpected return minimizing CVaR is a convex optimizationproblem [7]

On the other expression MVC model denotes as thefollowing

min1205902 (119909)

subject to 119865120572(119909 V) le 119911

119864 (119909) ge 119889

119909 isin 119860 V isin 119877

(10)

where variables = (1199091 119909

119899) isin 119860 sub 119877119899 V isin 119877 and

set of feasible decision vectors denotes via 119860 that is a convexset In the model above there is one multiobjective system forportfolio optimization that consists of three objective functionsThe first objective function is to minimize the conditionalvalue at risk for portfolio optimization The second objectivefunction denotes minimizing the expected value of return of theportfolio And the last objective function considers minimizingthe variance of returns This procedure shows that we canmanage our capital to invest in several assets [5]

Mathematical Problems in Engineering 3

Table 1 Situation of two assets

AltCriteria

1198621

0101198622

0051198623

030A1 15 10 25A2 30 20 10

3 MVC Model of Portfolio Based on LWSM

Thismethod was introduced by Zadeh in 1963 and it is one ofthe main ways of solving theMO (see [8])Three types of thismethod are used for multiobjective portfolio optimization(MPO) in previous researchThey are weighted summethodweight quadratic method and weight quadratic variation

One of the main ways of weighting methods is theweighted sum method The aim of weighting method is theoptimization of the objective functions that they arrangedby linear combination (weighted sum) Different efficientsolutions can be found by changing the weights of theobjective functions [9]

The weighted sum method changes the MO problemwith a single model of mathematical optimization problemIn the model of this method sum weighting coefficient 119908

119894

multiply each objective function 119891119894to make the structure of

the objective function as follows (note that normalization ofthose coefficients is not necessary)

min119896

sum119894=1

120596119894119891119894(119909)

st 119909 isin Ω

where 120596119894ge 0 forall119894 = 1 119896

119896

sum119894=1

120596119894= 1

(11)

With convexity supposition if 120596119894gt 0 forall119894 = 1 119896 then

the solution of the above system is Pareto optimalThismeansthat if that system is convex then any Pareto optimal solutioncan be found [10] There are three criteria to measure theweightThey are subjective preference of the decisionmakersthe variance measure and the independence of criteriaUsually two methods can be used to achieve this aim theequal weights and the rank-order weights [11 12]

Example 2 (see [13]) Consider that a multiobjective problemincludes three criteria which are denoted by the sameunit and two alternatives According to Table 1 let 119882

1=

010 1198822= 005 and 119882

3= 030 The values of 120572

119894119895are

assumed to be as follows

119860 = [15 10 2530 20 10

] (12)

Therefore the decision matrix for this MCDM problem is asfollows

Criteria 010 005 030Alternatives A1 A2

With (10) we obtain data as follows

A1 (WSM Score) = 15 times 010 + 10

times 005 + 25 times 030 = 275(13)

In the same ways

A2 (WSM Score) = 30 times 010 + 20

times 005 + 10 times 030 = 7(14)

So the optimal case in the minimization situation is alterna-tiveA1 because it has the lowestWSM scoreWe can write thealternative ranking as follows A1 lt A1 (where ldquoltrdquo denotesldquobetter thanrdquo)

Now we formulate the portfolio revision problem withtransaction costs as a standard mathematical optimizationproblem with the mean-risk framework We will employ thefollowing notation

119873 number of risky assets119890 vector with all entries equal to ones

Consider the optimization problem with the normalizedsingle objective as follows

Maximize 119891 (119909) =119897

sum119896=1

1205961198961198760119896(119909)

Subject to 119909 isin 119883 = 119909 | 119891119894(119909) ge 0 119892

119894(119909)= 0 1 119897

(15)

where the weights are denoted by 120596119894 and

120596119894ge 0

119897

sum119894=1

120596119894= 1 119894 = 1 119897 (16)

And the objective function of 119896th objective function119876119896(119909) after normalization is denoted by 1198760

119896(119909) 119896 = 1 119897

Also we call 119891119894(119909) 119892

119894(119909)inequality and equality constraints

respectively With LWSM approach we have

119876119896(119909) =

119897

sum119894=1

119886119896119894119909119894 119886119896119894isin 119877 (17)

Therefore normalized objective functions have the followingform

1198760119896(119909) =

119876119896(119909)

119878119896

=1198861198961

119878119896

1199091+ sdot sdot sdot +

119886119896119899

119878119896

119909119899 (18)

in which case the floating-point values 119878119896are evaluated in the

following way

119878119896=119899

sum119895=1

1003816100381610038161003816100381611988611989611989510038161003816100381610038161003816 = 0 (19)

Obviously in many practical problems the objectivefunctions are represented by various measure units (eg if

4 Mathematical Problems in Engineering

1198761is measured in kilos 119876

2in seconds etc) For this reason

the objective function normalization is required It is nowobvious that the coefficients have values of the segment [0 1]Denote that we now have the linear programming problem

Maximize 119891 (119909) =119897

sum119896=1

120596119896

119876119896(119909)

119878119896

= 1205961

1198861198961

119878119896

1199091

+ sdot sdot sdot + 120596119899

119886119896119899

119878119896

119909119899

Subject to 119909 isin 119883

(20)

The following theorem gives the practical criteria forthe detection of some Pareto optimal solutions of problem(24) Yu et al [14] presented mean-CVaR model of portfoliooptimization based on LWSM inwhich they assumed that thereturn of the portfolio is based on multi-t-distribution andthey obtained the model for

max (119906 (119908)) = max (1205721119864 (119877) minus 120572

2CVaR) (21)

as follows

max05 (119908119879120583) + 05(120572 + 1

119898 (1 minus 05)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(22)

There are some conditions for coefficients that are usedin WSM For example the sum of them equal 1 and theyare strictly positive In addition to LWSM they must benormalized With this idea the multiportfolio optimizationproblem is as follows

min (119906 (119908)) = min (12057211205902 (119877) minus 120572

2119864 (119877) + 120572

3CVaR)

Subject to 119909 isin 119860(23)

where 1205721 1205722 and 120572

3are strictly positive and 119860 is as the

above assumptions Since all objective functions on MVCmodel are convex we can define the model above to find thesolution as the Pareto optimal set [15] For instance if weconsider 120572

1= 1 120572

2= 0 and 120572

3= 0 the problem turns

to minimize the variance of the portfolio [5]Now according to (P2) as themultiobjective optimization

problem LWSM will be used to solve it as in the followingprocedure

Step 1 Construct the problem based on

min (119906 (119908)) = min (12057211205902 (119877) minus 120572

2119864 (119877) + 120572

3CVaR) (24)

There are several positions of investing for investorwho can manage hisher budget which is related to theamount of 120572

1 1205722 and 120572

3 This note creates several cases

for investors to increase the return or decrease the riskof a portfolio The risk (or return) has an inverse (direct)relation with those coefficientsThe LWSM leads to followingprocedure for MVC model of portfolio

Step 2 Consider

min1205721(119908119879120590119908) minus 120572

2(119908119879120583)

+ 1205723(120572 +

1

119898 (1 minus 120573)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(25)

where 120572 120573 are the belief degree and specific parameterrespectively In this paper it is considered that 120573 = 05 Inaddition according to sum119899

119894=1120572119894= 1 we have 1minus(120572

1+ 1205722) = 1205723

we rewrite problem of (18) as follows

min1205721(119908119879120590119908) minus 120572

2(119908119879120583) + (1 minus (120572

1+ 1205722))

times (120572 +1

119898 (1 minus 05)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894

0 le 119908119894le 1

(26)

where the belief degree of 120572 set is equal to 095 In additionin CVaR formula after linearization [16 17] we have

119865120573(119908 120572) = 120572 +

1

119898 (1 minus 120573)

119898

sum119896=1

[119891 (119908 119910119896) + 120572]

+

(27)

and 119891(119908 119910119896) is the loss function which can be defined [16]

by 119891(119908 119910119896) = minus119908119879119910

119896 We can rewrite (19) according to the

assumptions above as follows

min1205721(119908119879120590119908) minus 120572

2(119908119879120583) + (1 minus (120572

1+ 1205722))

times (095 +1

119898 (1 minus 05)

119898

sum119896=1

[minus119908119879119910119896+ 095]

+

)

st

[119906]+ = max 119906 0119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(28)

where 120583119896is return of 119896th asset In the model above we

consider119898 = 2 and we have

min1205721(119908119879120590119908) minus 120572

2(119908119879120583) + (1 minus (120572

1+ 1205722))

times (095 +1

2 (1 minus 05)2 ([minus119908119879119910

119896+ 095]

+

))

st

[119906]+ = max 119906 0119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(29)

Mathematical Problems in Engineering 5

4 Empirical Research and Challenges

In order to evaluate the model above to find the portfoliooptimization based on LWSM we consider two assets whosemean return 120583 and covariance matrix 120590 are as the followingdata (data from [14 16])

120583 = (0067609870034191

)

120590 = (0058884101 00004640430000464043 00003643663

)

(30)

According to the data above and the model of (29) we have

min119885 = min1205721(1199111) minus 1205722(1199112) + (1 minus (120572

1+ 1205722)) (1199113) (31)

where

1199111= 1205752119901= 119908119879120590119908 =

= (0058884101 lowast 1199081+ 0000464043 lowast 119908

2) lowast 1199081

+ (0000464043 lowast 1199081+ 00003643663 lowast 119908

2) lowast 1199082

1199112= 120583119901= 119908119879120583 = 006760987119908

1+ 0034191119908

2

1199113= (095 +

1

2 (1 minus 05)2 ([minus119908119879120583 minus 095]

+

))

= 095 +1

2 (05)

times 2 ([minus (0067609871199081+ 0034191119908

2) + 095]

+

)

[119906]+ = max 119906 0

119899

sum119894=1

119908119894

= 1 0 le 119908119894le 1

(32)

Now we consider this proposed model for 1205721= 025 120572

2=

025 Therefore we have

minZ = min (001472102525 lowast 11990821

+ 000058005375 lowast 1199081lowast 1199082

+00003643663 lowast 11990822)

minus (001690246751199081+ 000854775119908

2)

+ (0475 + ([minus (0067609871199081+ 0034191119908

2)

+095]+))

st

[119906]+ = max 119906 0119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(33)

01000

20003000

minus001

minus0005

0minus1

minus05

0

05

1

10

20

30

40

50

60

Figure 1 Mean-variance model of portfolio via LWSM

0

0

2000 4000 6000 8000 10000 120000

1

2

minus1

minus05

05

1

10

20

30

40

50

60

Data 1

Figure 2 MVC model of portfolio via LWSM

In order to compare the performance of mean-variancemodel and MVC model of multiportfolio optimization theminimum functions are demonstrated viaMATLABsoftwareas Figures 1 and 2 show the results of LWSMmethod for twomodels respectively

Comparative performance was measured using a MAT-LAB software and performance was shown in Figures 1 and2 which are called the mean-variance and MVC model ofmultiportfolio respectively

In summary we compare the performance of MVCmodel of multiportfolio with LWSM technique and othermodels like mean-variance approaches The mean-varianceminimization function and the MVC model are as describedin Figures 1 and 2 respectively

Table 2 is arranged to illustrate the results of MVCmodelof portfolio and refer to two assets byMatlab by this approach

As shown in the above results we tested two assets viaproposed model and we presented the results of that asTable 2 which included 20 results from our proposed modelbyMATLAB software It showed except for two obvious cases

6 Mathematical Problems in Engineering

Table 2 Results of MVC model of portfolio refer to two assets (seeSection 4) by MATLAB

1199081= 0000000 119908

2= 1000000 119911 = 1083819

1199081= 0010000 119908

2= 0990000 119911 = 1086554

1199081= 0020000 119908

2= 0980000 119911 = 1089293

1199081= 0030000 119908

2= 0970000 119911 = 1092035

1199081= 0040000 119908

2= 0960000 119911 = 1094779

1199081= 0050000 119908

2= 0950000 119911 = 1097527

1199081= 0060000 119908

2= 0940000 119911 = 1100278

1199081= 0070000 119908

2= 0930000 119911 = 1103031

1199081= 0080000 119908

2= 0920000 119911 = 1105788

1199081= 0090000 119908

2= 0910000 119911 = 1108547

1199081= 0100000 119908

2= 0900000 119911 = 1111310

1199081= 0110000 119908

2= 0890000 119911 = 1114075

1199081= 0120000 119908

2= 0880000 119911 = 1116844

1199081= 0130000 119908

2= 0870000 119911 = 1119615

1199081= 0140000 119908

2= 0860000 119911 = 1122389

1199081= 0150000 119908

2= 0850000 119911 = 1125167

1199081= 0160000 119908

2= 0840000 119911 = 1127947

1199081= 0170000 119908

2= 0830000 119911 = 1130730

1199081= 0180000 119908

2= 0820000 119911 = 1133517

1199081= 0190000 119908

2= 0810000 119911 = 1136306

1199081= 0200000 119908

2= 0800000 119911 = 1139098

1199081= 0210000 119908

2= 0790000 119911 = 1141893

1199081= 0220000 119908

2= 0780000 119911 = 1144691

1199081= 0230000 119908

2= 0770000 119911 = 1147493

1199081= 0240000 119908

2= 0760000 119911 = 1150297

1199081= 0250000 119908

2= 0750000 119911 = 1153104

1199081= 0260000 119908

2= 0740000 119911 = 1155914

1199081= 0270000 119908

2= 0730000 119911 = 1158727

1199081= 0280000 119908

2= 0720000 119911 = 1161543

1199081= 0290000 119908

2= 0710000 119911 = 1164362

1199081= 0300000 119908

2= 0700000 119911 = 1167184

1199081= 0310000 119908

2= 0690000 119911 = 1170009

1199081= 0320000 119908

2= 0680000 119911 = 1172837

1199081= 0330000 119908

2= 0670000 119911 = 1175668

1199081= 0340000 119908

2= 0660000 119911 = 1178501

1199081= 0350000 119908

2= 0650000 119911 = 1181338

1199081= 0360000 119908

2= 0640000 119911 = 1184178

1199081= 0370000 119908

2= 0630000 119911 = 1187021

1199081= 0380000 119908

2= 0620000 119911 = 1189867

1199081= 0390000 119908

2= 0610000 119911 = 1192715

1199081= 0400000 119908

2= 0600000 119911 = 1195567

1199081= 0410000 119908

2= 0590000 119911 = 1198422

1199081= 0420000 119908

2= 0580000 119911 = 1201279

1199081= 0430000 119908

2= 0570000 119911 = 1204140

1199081= 0440000 119908

2= 0560000 119911 = 1207004

1199081= 0450000 119908

2= 0550000 119911 = 1209870

1199081= 0460000 119908

2= 0540000 119911 = 1212740

1199081= 0470000 119908

2= 0530000 119911 = 1215612

1199081= 0480000 119908

2= 0520000 119911 = 1218488

1199081= 0490000 119908

2= 0510000 119911 = 1221366

Table 2 Continued

1199081= 0500000 119908

2= 0500000 119911 = 1224248

1199081= 0510000 119908

2= 0490000 119911 = 1227132

1199081= 0520000 119908

2= 0480000 119911 = 1230019

1199081= 0530000 119908

2= 0470000 119911 = 1232910

1199081= 0540000 119908

2= 0460000 119911 = 1235803

1199081= 0550000 119908

2= 0450000 119911 = 1238699

1199081= 0560000 119908

2= 0440000 119911 = 1241599

1199081= 0570000 119908

2= 0430000 119911 = 1244501

1199081= 0580000 119908

2= 0420000 119911 = 1247406

1199081= 0590000 119908

2= 0410000 119911 = 1250314

1199081= 0600000 119908

2= 0400000 119911 = 1253225

1199081= 0610000 119908

2= 0390000 119911 = 1256140

1199081= 0620000 119908

2= 0380000 119911 = 1259057

1199081= 0630000 119908

2= 0370000 119911 = 1261977

1199081= 0640000 119908

2= 0360000 119911 = 1264900

1199081= 0650000 119908

2= 0350000 119911 = 1267826

1199081= 0660000 119908

2= 0340000 119911 = 1270755

1199081= 0670000 119908

2= 0330000 119911 = 1273687

1199081= 0680000 119908

2= 0320000 119911 = 1276622

1199081= 0690000 119908

2= 0310000 119911 = 1279560

1199081= 0700000 119908

2= 0300000 119911 = 1282501

1199081= 0710000 119908

2= 0290000 119911 = 1285445

1199081= 0720000 119908

2= 0280000 119911 = 1288392

1199081= 0730000 119908

2= 0270000 119911 = 1291341

1199081= 0740000 119908

2= 0260000 119911 = 1294294

1199081= 0750000 119908

2= 0250000 119911 = 1297250

1199081= 0760000 119908

2= 0240000 119911 = 1300209

1199081= 0770000 119908

2= 0230000 119911 = 1303170

1199081= 0780000 119908

2= 0220000 119911 = 1306135

1199081= 0790000 119908

2= 0210000 119911 = 1309103

1199081= 0800000 119908

2= 0200000 119911 = 1312074

1199081= 0810000 119908

2= 0190000 119911 = 1315047

1199081= 0820000 119908

2= 0180000 119911 = 1318024

1199081= 0830000 119908

2= 0170000 119911 = 1321003

1199081= 0840000 119908

2= 0160000 119911 = 1323986

1199081= 0850000 119908

2= 0150000 119911 = 1326971

1199081= 0860000 119908

2= 0140000 119911 = 1329960

1199081= 0870000 119908

2= 0130000 119911 = 1332951

1199081= 0880000 119908

2= 0120000 119911 = 1335946

1199081= 0890000 119908

2= 0110000 119911 = 1338943

1199081= 0900000 119908

2= 0100000 119911 = 1341944

1199081= 0910000 119908

2= 0090000 119911 = 1344947

1199081= 0920000 119908

2= 0080000 119911 = 1347953

1199081= 0930000 119908

2= 0070000 119911 = 1350963

1199081= 0940000 119908

2= 0060000 119911 = 1353975

1199081= 0950000 119908

2= 0050000 119911 = 1356990

1199081= 0960000 119908

2= 0040000 119911 = 1360008

1199081= 0970000 119908

2= 0030000 119911 = 1363030

1199081= 0980000 119908

2= 0020000 119911 = 1366054

1199081= 0990000 119908

2= 0010000 119911 = 1369081

1199081= 1000000 119908

2= 0000000 119911 = 1372111

Mathematical Problems in Engineering 7

(1199081= 0 and 119908

2= 1 119908

1= 1 and 119908

2= 0) that the minimum

situation ofMVCmodel ofmultiportfoliowill occurr on1199081=

001 and 1199082= 099 The results illustrate that the proposed

method is better for investing a small amount of assets suchas the above two assets

Despite of the several advantages this method has somedisadvantages which one of them is the weights 120572

1 1205722

and 1205723that are hard to understand [5] The other one is

how to use the Simplex method to solve the weightedsum problem The solution of this problem is using othertechniques (eg interior-point methods) [10]

5 Conclusion

In this investigation we consider three objective functions tomodel portfolio optimization with LWSM In addition wepropose a linear weighted sum method to solve the MCVmodel of portfolio optimization Also with empirical exam-ple and MATLAB software we evaluated proposed modelOur example includes two assets for investing However itis flexible to choose more assets and find the Pareto optimalaccording to procedures that are used in this paper

The contribution of this study is a presentation of MVCmodel of portfolio optimization based on LWSMThe empir-ical examples have shown that using the three objectivefunctions tomake a powerfulmulti-portfoliomodelWe havedescribed the MVC model of multiportfolio optimizationthat it is extended of the model presented by Yu et al [14]In addition we showed that theMVCmodel generally coversboth mean-variance and mean-CVaR models of portfoliooptimization (with changing the coefficients of 120572

119894 119894 = 1 3)

Furthermore this paper has given new insight into themultiobjective decision making process via WSM A hybridof this method and other techniques such as interior-pointmethods can be a good idea for future researchers

To sum up with using three objective functions it helpsthe investors to manage their portfolio better and therebyminimize the risk and maximize the return of the portfolioAlso using LWSM dues to modify the current models andsimplify it to obtain better results The same approach canalso be used for other multiobjective optimizationmodel andinvesting applications

Conflict of Interests

The authors declare that there is no conflict of interestsregarding the publication of this paper

Acknowledgment

Research reported in this publication was supported byUniversiti Teknologi Malaysia under grant number 4B112(Research Management Centre Universiti TeknologiMalaysia)

References

[1] Y Elahi and A A Mohd-Ismail ldquoMulti-objectives portfo-lio optimization challenges and opportunities for islamicapproachrdquoAustralian Journal of Basic and Applaied Sicence vol6 no 10 pp 297ndash302 2012

[2] I Radziukyniene and A Zilinskas ldquoEvolutionary methods formulti-objective portfolio optimizationrdquo in Proceedings of theWorld Congress on Engineering 2008

[3] C Chiranjeevi and V N Sastry ldquoMulti objective portfoliooptimization models and its solution using genetic algorithmsrdquoin Proceedings of the International Conference on ComputationalIntelligence andMultimediaApplications (ICCIMA rsquo07) Decem-ber 2007

[4] R Aboulaich R Ellaia and S El Moumen ldquoThe mean-variance-CVaR model for portfolio optimization modelingusing a multi-objective approach based on a hybrid methodrdquoMathematical Modelling of Natural Phenomena vol 5 no 7 pp103ndash108 2010

[5] D Roman K Darby-Dowman and G Mitra ldquoMean-riskmodels using two risk measures a multi-objective approachrdquoQuantitative Finance vol 7 no 4 pp 443ndash458 2007

[6] R Armananzas and J A Lozano ldquoAmultiobjective approach tothe portfolio optimization problemrdquo in Proceedings of the IEEECongress on Evolutionary Computation (CEC rsquo05) September2005

[7] D Roman K Darby-Dowman and G Mitra ldquoPortfolio con-struction based on stochastic dominance and target returndistributionsrdquo Mathematical Programming vol 108 no 2 pp541ndash569 2006

[8] L Zadeh ldquoOptimality and non-scalar-valued performancecriteriardquo IEEE Transactions on Automatic Control vol 8 no 1pp 59ndash60 1963

[9] K Kirytopoulos V Leopoulos G Mavrotas and D Voulgar-idou ldquoMultiple sourcing strategies and order allocation anANP-AUGMECON meta-modelrdquo Supply Chain Managementvol 15 no 4 pp 263ndash276 2010

[10] O Grodzevich and O Romanko ldquoNormalization and othertopics in multi-objective optimizationrdquo 2006

[11] J Jia GW Fischer and J S Dyer ldquoAttribute weightingmethodsand decision quality in the presence of response error asimulation studyrdquo Journal of Behavioral Decision Making vol11 no 2 pp 85ndash105 1998

[12] B Sawik ldquoA reference point approach to bi-objective dynamicportfolio optimizationrdquo Decision Making in Manufacturing andServices vol 3 no 1-2 pp 73ndash85 2009

[13] O Romanko A Ghaffari-Hadigheh and T Terlaky ldquoMulti-objective optimization via parametric optimization modelsalgorithms and applicationsrdquo Modeling and Optimization pp77ndash119 2012

[14] X Yu Y Tan L Liu and W Huang ldquoThe optimal portfoliomodel based onmean-CvaRwith linear weighted summethodrdquoin Fifth International Joint Conference on Computational Sci-ences and Optimization (CSO rsquo12) pp 82ndash84 June 2012

[15] J Jahn ldquoSome characterizations of the optimal solutions of avector optimization problemrdquo Operations-Research-Spektrumvol 7 pp 7ndash17 1985

[16] X YuH Sun andG Chen ldquoThe optimal portfoliomodel basedon mean-CVaRrdquo Journal of Mathematical Finance vol 1 no 3pp 132ndash134 2011

[17] S Uryasev ldquoConditional value-at-risk optimization algorithmsand applicationsrdquo in Proceedings of the IEEEIAFEINFORNS6th Conference on Computational Intelligence for FinancialEngineering (CIFEr rsquo00) pp 49ndash57 March 2000

Submit your manuscripts athttpwwwhindawicom

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Mathematical Problems in Engineering

Hindawi Publishing Corporationhttpwwwhindawicom

Differential EquationsInternational Journal of

Volume 2014

Applied MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Probability and StatisticsHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Mathematical PhysicsAdvances in

Complex AnalysisJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

OptimizationJournal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

CombinatoricsHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

International Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Operations ResearchAdvances in

Journal of

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Function Spaces

Abstract and Applied AnalysisHindawi Publishing Corporationhttpwwwhindawicom Volume 2014

International Journal of Mathematics and Mathematical Sciences

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

The Scientific World JournalHindawi Publishing Corporation httpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Algebra

Discrete Dynamics in Nature and Society

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Decision SciencesAdvances in

Discrete MathematicsJournal of

Hindawi Publishing Corporationhttpwwwhindawicom

Volume 2014 Hindawi Publishing Corporationhttpwwwhindawicom Volume 2014

Stochastic AnalysisInternational Journal of

Mathematical Problems in Engineering 3

Table 1 Situation of two assets

AltCriteria

1198621

0101198622

0051198623

030A1 15 10 25A2 30 20 10

3 MVC Model of Portfolio Based on LWSM

Thismethod was introduced by Zadeh in 1963 and it is one ofthe main ways of solving theMO (see [8])Three types of thismethod are used for multiobjective portfolio optimization(MPO) in previous researchThey are weighted summethodweight quadratic method and weight quadratic variation

One of the main ways of weighting methods is theweighted sum method The aim of weighting method is theoptimization of the objective functions that they arrangedby linear combination (weighted sum) Different efficientsolutions can be found by changing the weights of theobjective functions [9]

The weighted sum method changes the MO problemwith a single model of mathematical optimization problemIn the model of this method sum weighting coefficient 119908

119894

multiply each objective function 119891119894to make the structure of

the objective function as follows (note that normalization ofthose coefficients is not necessary)

min119896

sum119894=1

120596119894119891119894(119909)

st 119909 isin Ω

where 120596119894ge 0 forall119894 = 1 119896

119896

sum119894=1

120596119894= 1

(11)

With convexity supposition if 120596119894gt 0 forall119894 = 1 119896 then

the solution of the above system is Pareto optimalThismeansthat if that system is convex then any Pareto optimal solutioncan be found [10] There are three criteria to measure theweightThey are subjective preference of the decisionmakersthe variance measure and the independence of criteriaUsually two methods can be used to achieve this aim theequal weights and the rank-order weights [11 12]

Example 2 (see [13]) Consider that a multiobjective problemincludes three criteria which are denoted by the sameunit and two alternatives According to Table 1 let 119882

1=

010 1198822= 005 and 119882

3= 030 The values of 120572

119894119895are

assumed to be as follows

119860 = [15 10 2530 20 10

] (12)

Therefore the decision matrix for this MCDM problem is asfollows

Criteria 010 005 030Alternatives A1 A2

With (10) we obtain data as follows

A1 (WSM Score) = 15 times 010 + 10

times 005 + 25 times 030 = 275(13)

In the same ways

A2 (WSM Score) = 30 times 010 + 20

times 005 + 10 times 030 = 7(14)

So the optimal case in the minimization situation is alterna-tiveA1 because it has the lowestWSM scoreWe can write thealternative ranking as follows A1 lt A1 (where ldquoltrdquo denotesldquobetter thanrdquo)

Now we formulate the portfolio revision problem withtransaction costs as a standard mathematical optimizationproblem with the mean-risk framework We will employ thefollowing notation

119873 number of risky assets119890 vector with all entries equal to ones

Consider the optimization problem with the normalizedsingle objective as follows

Maximize 119891 (119909) =119897

sum119896=1

1205961198961198760119896(119909)

Subject to 119909 isin 119883 = 119909 | 119891119894(119909) ge 0 119892

119894(119909)= 0 1 119897

(15)

where the weights are denoted by 120596119894 and

120596119894ge 0

119897

sum119894=1

120596119894= 1 119894 = 1 119897 (16)

And the objective function of 119896th objective function119876119896(119909) after normalization is denoted by 1198760

119896(119909) 119896 = 1 119897

Also we call 119891119894(119909) 119892

119894(119909)inequality and equality constraints

respectively With LWSM approach we have

119876119896(119909) =

119897

sum119894=1

119886119896119894119909119894 119886119896119894isin 119877 (17)

Therefore normalized objective functions have the followingform

1198760119896(119909) =

119876119896(119909)

119878119896

=1198861198961

119878119896

1199091+ sdot sdot sdot +

119886119896119899

119878119896

119909119899 (18)

in which case the floating-point values 119878119896are evaluated in the

following way

119878119896=119899

sum119895=1

1003816100381610038161003816100381611988611989611989510038161003816100381610038161003816 = 0 (19)

Obviously in many practical problems the objectivefunctions are represented by various measure units (eg if

4 Mathematical Problems in Engineering

1198761is measured in kilos 119876

2in seconds etc) For this reason

the objective function normalization is required It is nowobvious that the coefficients have values of the segment [0 1]Denote that we now have the linear programming problem

Maximize 119891 (119909) =119897

sum119896=1

120596119896

119876119896(119909)

119878119896

= 1205961

1198861198961

119878119896

1199091

+ sdot sdot sdot + 120596119899

119886119896119899

119878119896

119909119899

Subject to 119909 isin 119883

(20)

The following theorem gives the practical criteria forthe detection of some Pareto optimal solutions of problem(24) Yu et al [14] presented mean-CVaR model of portfoliooptimization based on LWSM inwhich they assumed that thereturn of the portfolio is based on multi-t-distribution andthey obtained the model for

max (119906 (119908)) = max (1205721119864 (119877) minus 120572

2CVaR) (21)

as follows

max05 (119908119879120583) + 05(120572 + 1

119898 (1 minus 05)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(22)

There are some conditions for coefficients that are usedin WSM For example the sum of them equal 1 and theyare strictly positive In addition to LWSM they must benormalized With this idea the multiportfolio optimizationproblem is as follows

min (119906 (119908)) = min (12057211205902 (119877) minus 120572

2119864 (119877) + 120572

3CVaR)

Subject to 119909 isin 119860(23)

where 1205721 1205722 and 120572

3are strictly positive and 119860 is as the

above assumptions Since all objective functions on MVCmodel are convex we can define the model above to find thesolution as the Pareto optimal set [15] For instance if weconsider 120572

1= 1 120572

2= 0 and 120572

3= 0 the problem turns

to minimize the variance of the portfolio [5]Now according to (P2) as themultiobjective optimization

problem LWSM will be used to solve it as in the followingprocedure

Step 1 Construct the problem based on

min (119906 (119908)) = min (12057211205902 (119877) minus 120572

2119864 (119877) + 120572

3CVaR) (24)

There are several positions of investing for investorwho can manage hisher budget which is related to theamount of 120572

1 1205722 and 120572

3 This note creates several cases

for investors to increase the return or decrease the riskof a portfolio The risk (or return) has an inverse (direct)relation with those coefficientsThe LWSM leads to followingprocedure for MVC model of portfolio

Step 2 Consider

min1205721(119908119879120590119908) minus 120572

2(119908119879120583)

+ 1205723(120572 +

1

119898 (1 minus 120573)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894= 1 0 le 119908

119894le 1

(25)

where 120572 120573 are the belief degree and specific parameterrespectively In this paper it is considered that 120573 = 05 Inaddition according to sum119899

119894=1120572119894= 1 we have 1minus(120572

1+ 1205722) = 1205723

we rewrite problem of (18) as follows

min1205721(119908119879120590119908) minus 120572

2(119908119879120583) + (1 minus (120572

1+ 1205722))

times (120572 +1

119898 (1 minus 05)

119898

sum119896=1

119906119896)

st

119908119879120583 + 120572 + 119906119896ge 0 119906

119896ge 0

119899

sum119894=1

119908119894

0 le 119908119894le 1

(26)

where the belief degree of 120572 set is equal to 095 In additionin CVaR formula after linearization [16 17] we have

119865120573(119908 120572) = 120572 +

1

119898 (1 minus 120573)

119898

sum119896=1

[119891 (119908 119910119896) + 120572]

+

(27)

and 119891(119908 119910119896) is the loss function which can be defined [16]

by 119891(119908 119910119896) = minus119908119879119910