report on the observance of standards and codes …documents.worldbank.org/curated/en/... · the...

TRANSCRIPT

REPORT ON THE OBSERVANCE OF STANDARDS AND CODES (ROSC)

Update by World Bank Staff on ROSC Modules

June 5,2006

36470

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Introduction

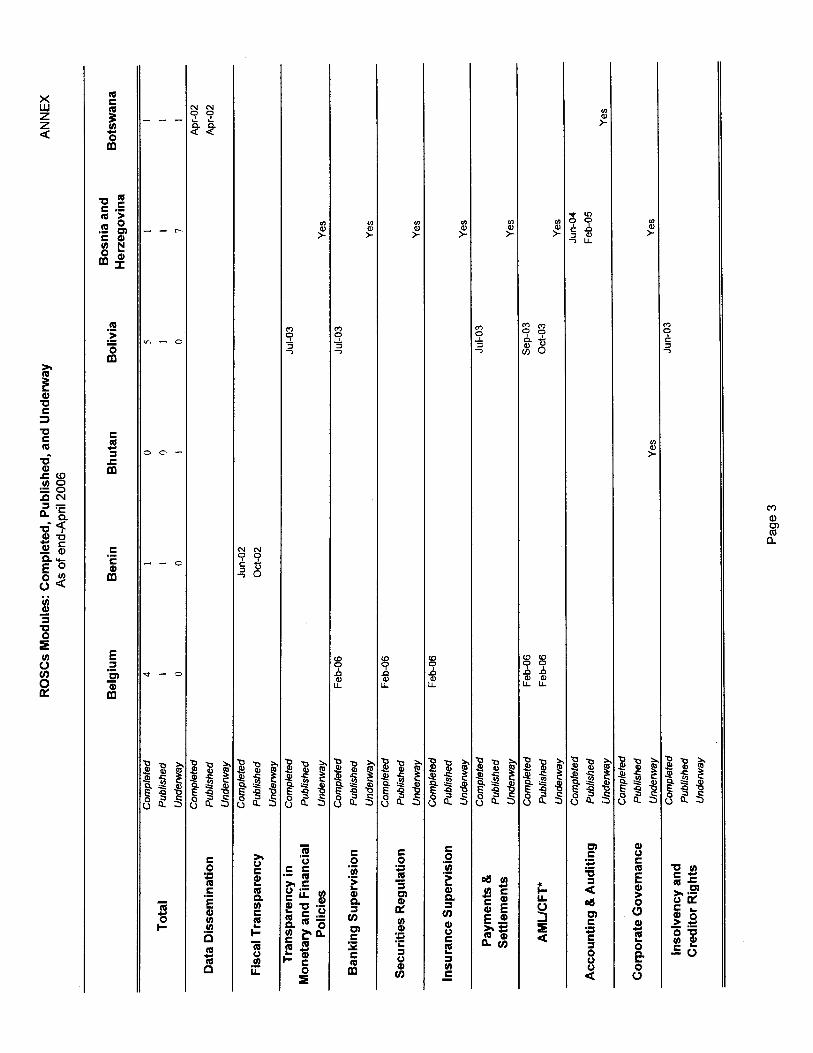

The Report on the Observance of Standards and Codes (ROSC) initiative was launched in 1999 as a prominent component o f efforts to strengthen the international financial architecture. The initiative aims at promoting greater financial stability, both domestically and internationally, through the development, dissemination, adoption, and implementation o f international standards and codes.

The ROSC initiative now covers 12 areas and associated standards, which the Bank and Fund Boards recognized as relevant for their work. These standards relate to policy transparency, financial sector regulation and supervision, and market infrastructure:

two areas are assessed by the Fund (Data Transparency and Fiscal Transparency);

six areas are mainly assessed joint ly by the Bank and the Fund under the FSAP Program (Banking Supervision, Monetary and Financial Policy 'Transparency, Securities, Insurance, Payments and Settlements Systems, and Anti-money Laundering and Combating the Financing o f Terrorism (AMLEFT' ); and

four areas are assessed by the Bank (Corporate Governance, Accounting, Auditing, and Insolvency and Creditor Rights).

Through April 30, 2006, 862 assessments (including updates) had been completed or were underway in 123 countries. As o f end-April, 540 assessments had been published.

__

Most AML/CFT assessments are being conducted by the FATE or FATF-style regional bodies

.. 11

Standards and Codes

Policy Transparency

0 Data Transparency: the Fund’s Special Datu Dissemination Standard and General Data

Fiscal Transparency: the Fund’s Code of Good Practices on Fiscal Transnarenw.

Monetary and Financial Policy Transparency: the Fund’s Code of Good Practices on

Dissemination $vstem (SDDS and GDDS).

0

0

Transnurency in Monetary and Financial Policies (MFPT), (usually assessed under the FSAP).

Financial Sector Regulation and Supervision

0 Banking Supervision: Base1 Committee on Banking Supervision’s (BCBS) Core Principles for

Securities: International Organization of Securities Commission’s (IOSCO) Objectives and

Insurance: International Association of Insurance Supervisors’ (IAIS) lnsurunce Supervisow

Payments Systems: Committee on Payments and Settlements Systems’ (CPSS) Insurance

Effective Banking Supervision (BCP).

Princinles for Securities ReguEation. 0

0

Princirdes (ISP).

Supervisorv Principles, complemented by Recommendations for Securities Settlement ,Yvstems (RSSS) for countries with significant securities trading.

Force (FATF)’s ;i’o+9 Recommendations.

0

0 Anti-money Laundering and Combating the Financing of Terrorism: Financial Action Task

Market Infrastructure

0 Corporate Governance: Organization for Economic Cooperation and Development’s (OECD)

Accounting: International Accounting Standards Board’s International Accounting Standards

Auditing: International Federation of Accountants’ International Standards on Auditing (ISA).

Insolvency and Creditor Rights: A standard based the Bank’s Principles for Effective

Princinles of Corporate Governance.

e

(IASB).

0

e

Insolvency and Creditor Rights Systems and the United Nations Commission on International Trade Law (UNCITRAL) Legislative Guide on Insolvency Law.’

1. Work i s in progress between the Bank and UNCITRAL, in consultation with Fund staff, to finalize such a standard.

... 111

Underway 18 Completed 59

Underway 7 Completed 54

Securities Regulation Published 44

Insurance Supervision Published 41 Underway 6 Completed 76

Payments & Settlements Published 47 Underway 8

AMUCFT Published 33 Completed 40

Underwav 44

IAccounting & Auditing

- ~

Completed 51 Published 40 Underway 13 Completed 48

Underway 8 Corporate Governance Published 39

Completed 27 Insolvency and Creditor Rights Published 6

Underway 7

Completed 725 Total Published 540

Underwav 137

iv

3 a Z z

U E m

.? 0 A 2

,

oll

u)

- ri d

$

m

m m 3

c u) Q U m w E - d

E

c m

.- E m

E m :=. m e w a

m u) 3

.- L CI

a

m C

v) U

i

C E .- m"

E a .- 0) -

m"

IL > $ >

o

Q) L

2

IL >

(u m m a

> f Q 'El E 3 'El E m

0 U

0 5

m m m C

0"

E 0

$ s 0

0 v) m U m E

z

m

w .- s - z

- .- N E m

E 0 v)

Q p. a v)

.- 'E

m E

C 5

d

L :

oll 0) E E a .- .w

8 Y

Q 0 E m

Q E $ c3 d E 0

0 E

P Q)

2 3 U E m 8

>

n u , 3 0 C L

.- := LL

C 0 C 3 C m a, a 3 w

.-

2

- w

U a > m w

s >

r- Q) m m a

II z z a

P m

(3

m .- r d

Q, s t- 6 n E .- d

C 0 Q

d

Q 0 C

U E

U S m C - i i

II >

W a, 0) m a

3 Z z a

)I

Q) U E 3 U E m

p! s s m C

m E 0 I

v)

a U

I

E

s

m E m )I

3

m m Q) m

- E c,

3

a 0 al f!

c3

m E m 5

E 0 v)

Q) Q a v) m C z C

.-

.E

d

E a z Z

P Q)

U E 3 U C m

d v) C

C ¶

.- CI

s Y

(u m m n

m 'z 3

U .- m 5 Y

P 8 s

m E s

m h E

2

ell 0) C E =I 0

U

.- c,

8

5 0 v) m m m

3 tL t: 5

:

m .- '0 Q 0

F

E s a

S 0 P

A

m c m .- a 5 .- J

0

0 u)

5

3

E

m z 3 n

>r 0 E

!i P v) c I- m 0 v)

E - i i

m c Q ._ .- U

z oll m c c .- U

a 8 Y

o m 3 0 & A ? $

X w Z z 4

E Q

U C 3

r -

a, w m a

2 a

n

m s

E

E 0

> I 0 z

0 0 0 0 s i , 2 8

ln al >

m c c 0 0

.- .w

a

Y

v i x

> i

; 6 L h . n e , E v )

N

9 ) P e, v)

P 0 L 8

8 2 d

P

0

.-

3 A L

P 50, ? g ? y -.Z . ^

! e , : v )

I N

bX ! $

P 0 L 8

0 (v a, IJ) m Q

N N 0 9 - a $ 9

m E ._ * s dl 2 E

E a ._ U

8 Y

Q

m z E

m Q

E Q)

0

0

U

g

e, 0) m a

m m 2 % 8 8

m m 0 0 A L 2 8

3 a Z z ? \ D O N

8 - , 8 8 6 L 8 >

G Q D C

Q) U E 3 'CI E m

I N .

N N (I) u) m n

U E m m - .-

m E

E

.- w E

J W N C

..

' * I O

i c ! I

Q 0 E m Q) f

(3

E Q)

0

0

U

g

.- E 'E v)

0 n a tn w S z E m rn

d

c > I >

C 0 u)

Q P a w w C E C

.- 2

i

$ >

m hl al 0 m a

X

$ n

E w m P

m E E N"

C

E p!

5 E Q U

5 t; >

d N