report no. aaa25-cm cameroon agricultural...

TRANSCRIPT

June 30, 2008

Document of the World Bank

Report N

o. AA

A25-C

M

Cam

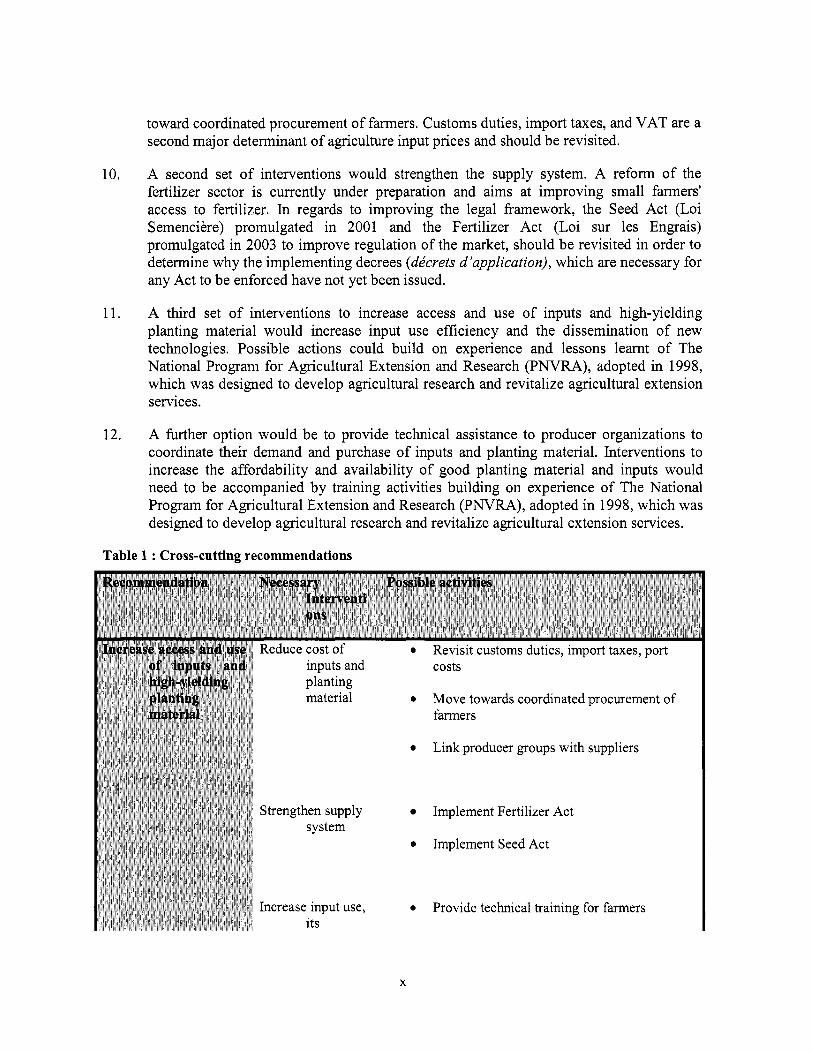

eroon A

gricultural Value C

hain

Report No. AAA25-CM

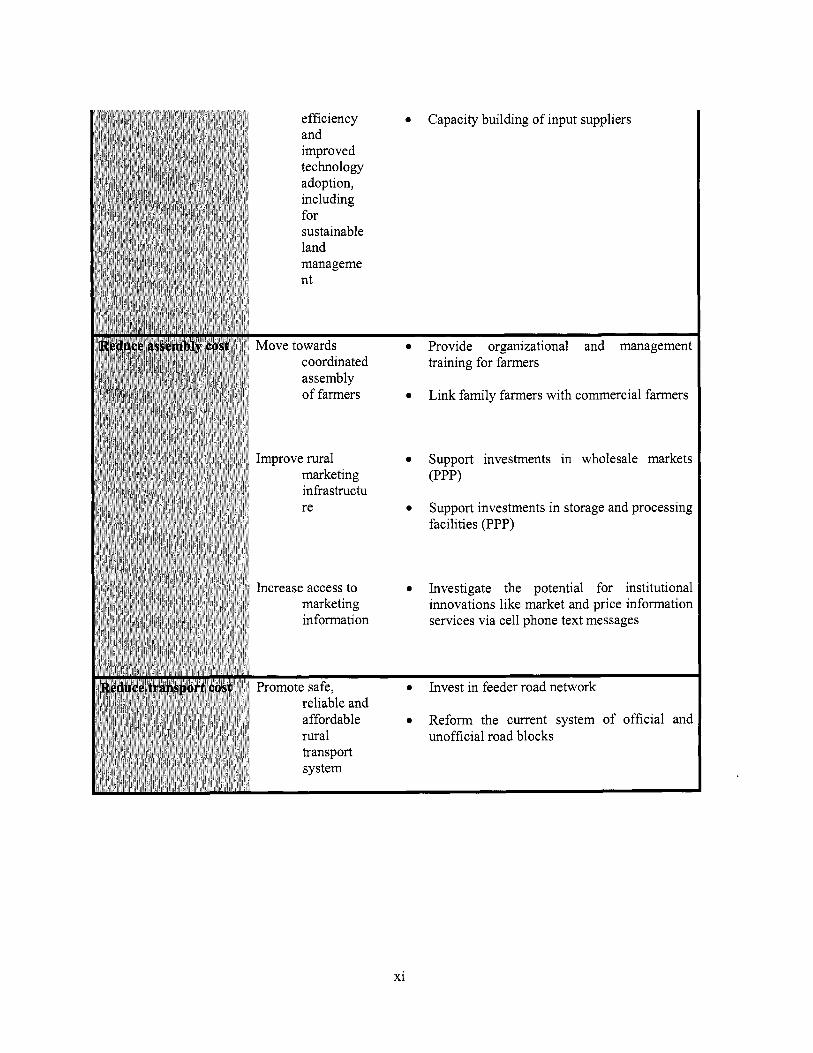

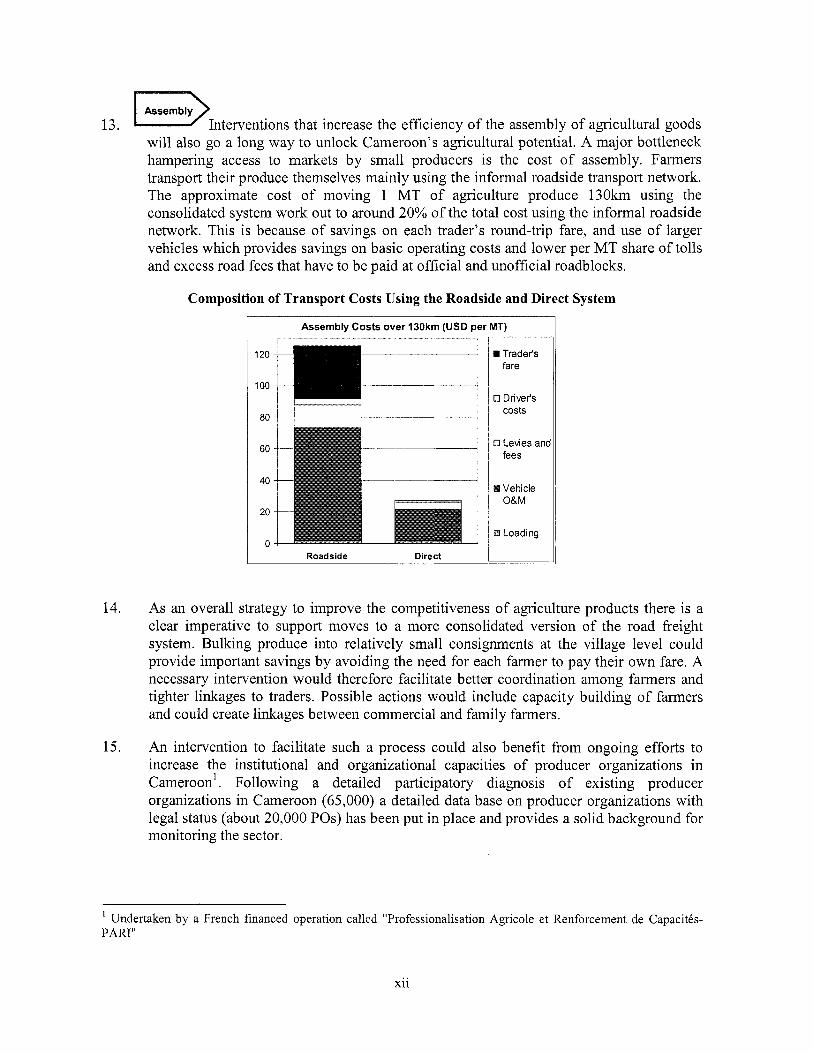

CameroonAgricultural Value Chain

Agricultural and Rural Development UnitSustainable Development DepartmentCountry Department AFCC1Africa Region

Competitiveness StudyPub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

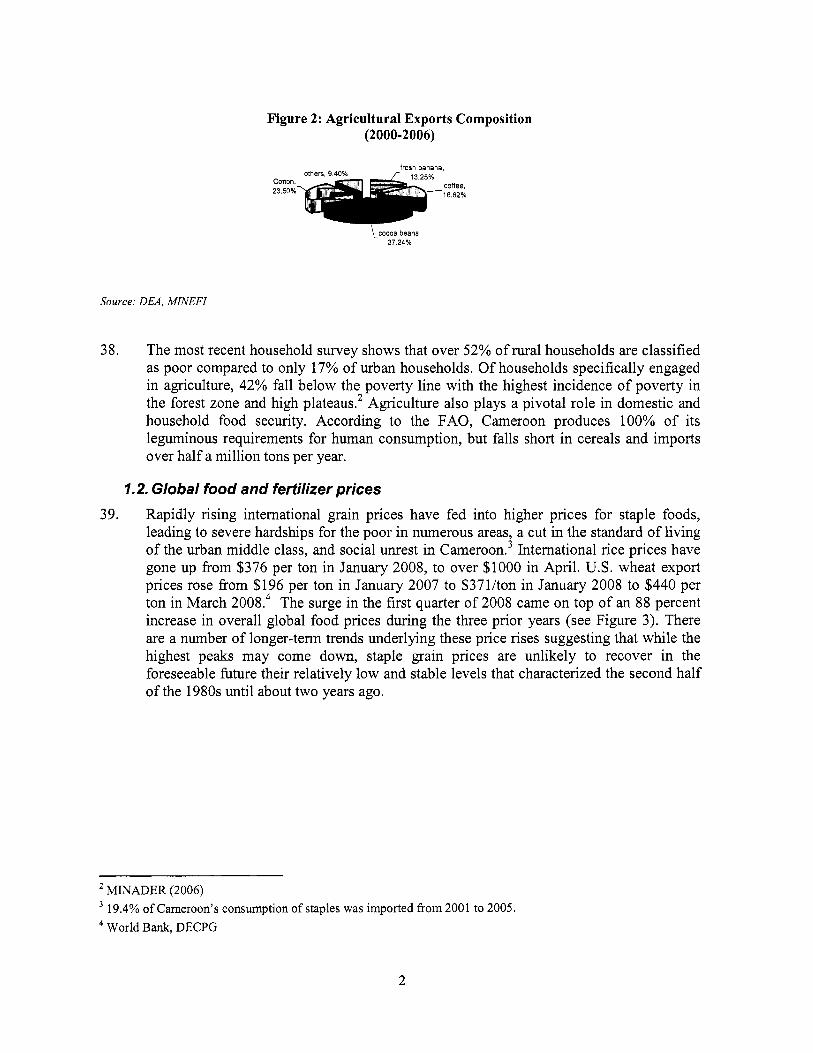

lic D

iscl

osur

e A

utho

rized

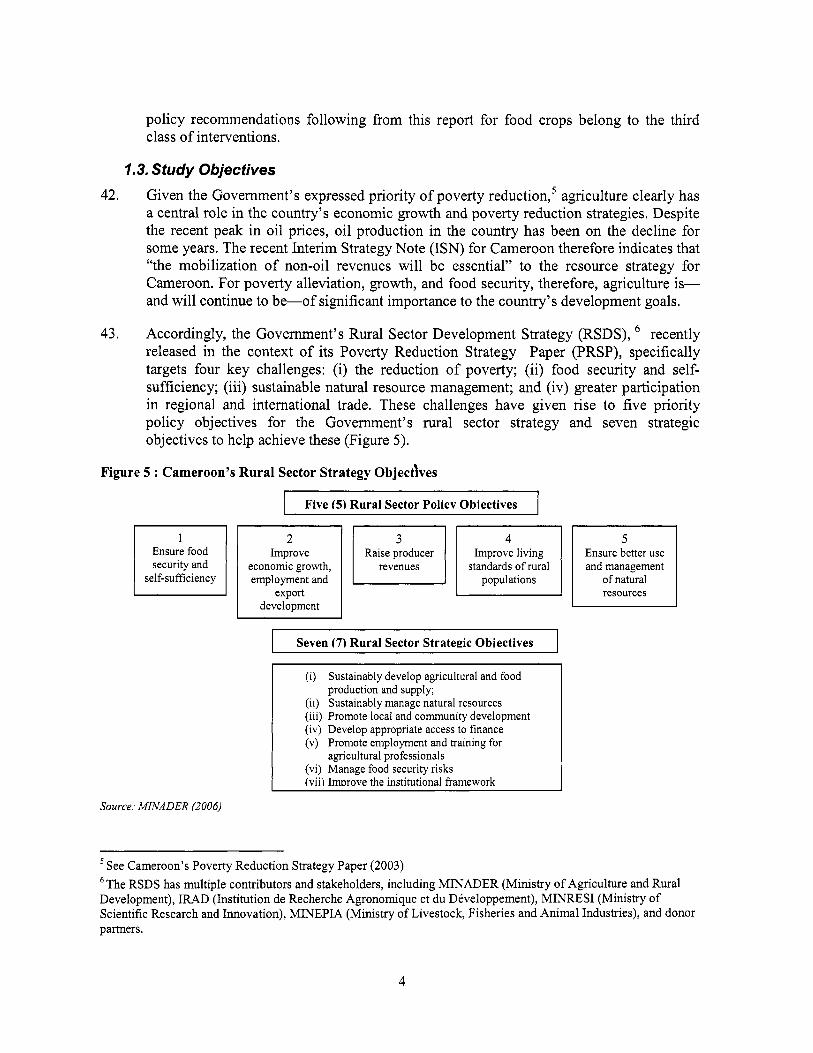

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

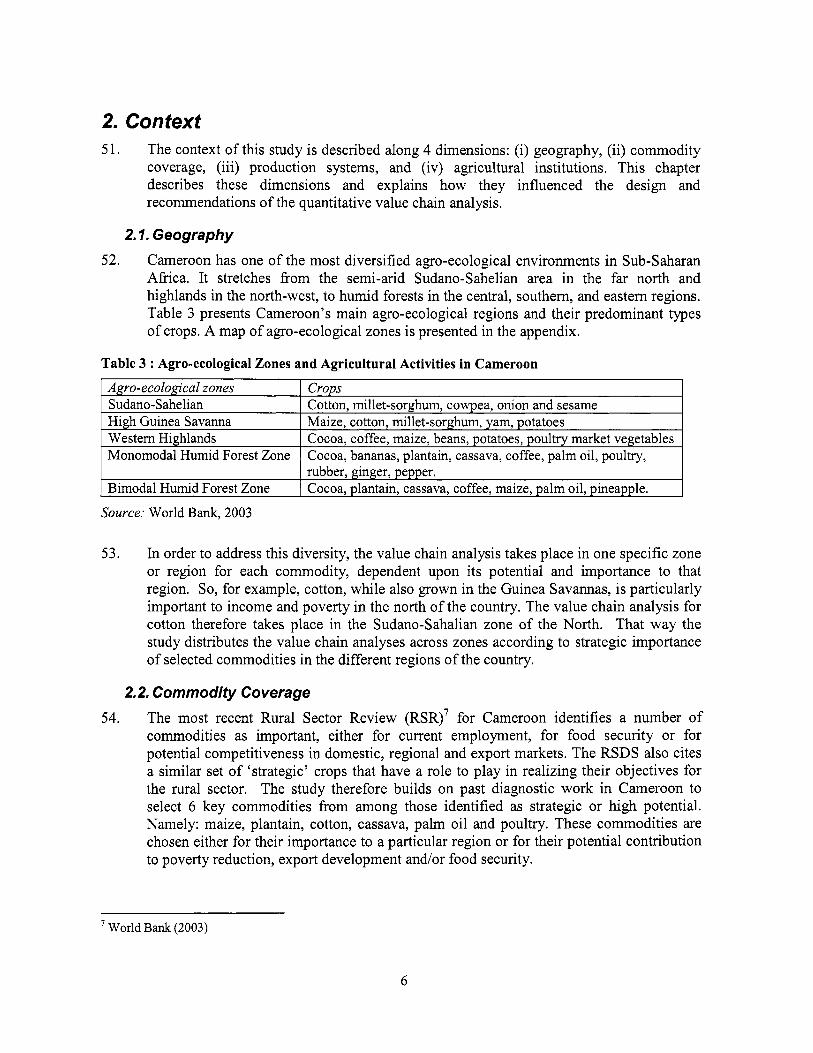

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

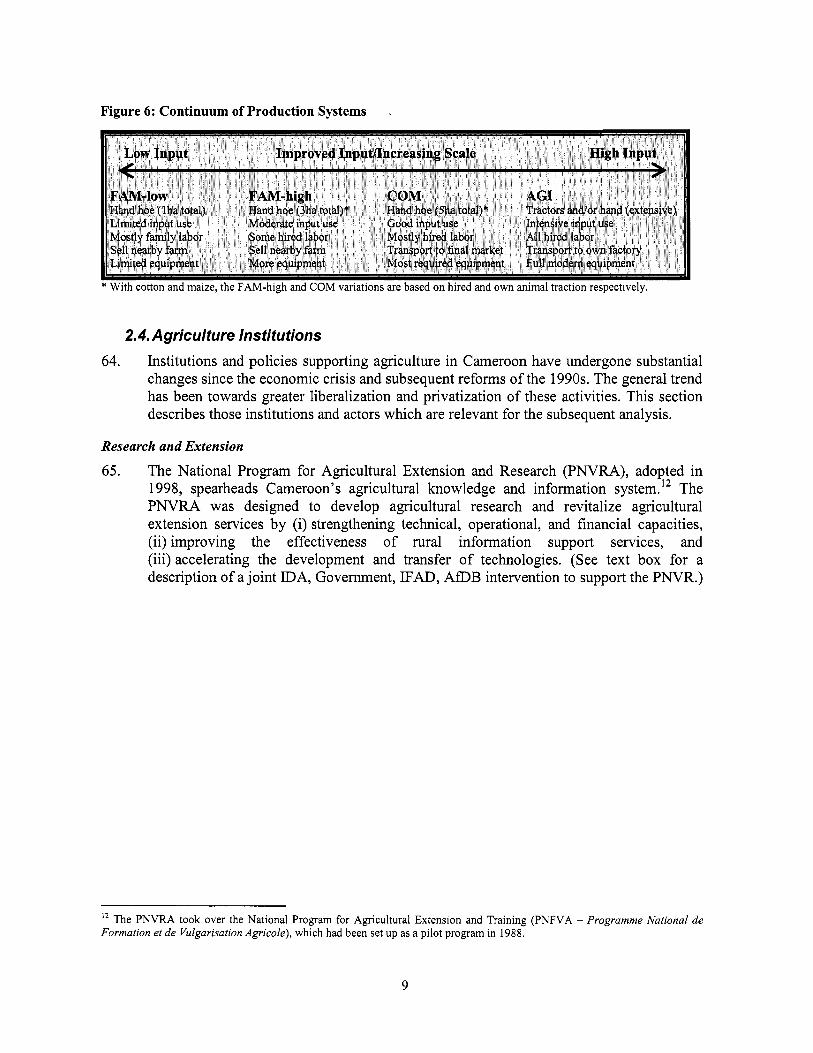

rized

Pub

lic D

iscl

osur

e A

utho

rized

Document of

The World Bank

CAMEROON AGRICULTURAL VALUE CHAIN COMPETITIVENESS STUDY

Final Report June 30,2008

Agriculture and Rural Development (AFTAR)

Sustainable Development Network (SDN)

Africa Region

Vice President: Obiageli Katryn Ezekwesili Country ManagedDirector: Mary A. Barton-Dock Sector Manager: Karen McConnell Brooks Task Team Leader: Ousmane Seck

Acronyms

ACP ADB AGI C A M CCAA C D C D C C E M A C C I C A M CIF C I R A D C N A P A C O M DVA EPA EU FAM FAM high FAM l o w FA0 FFB FOB FONADER GDP ha I C A C IFAD IPM IRAD

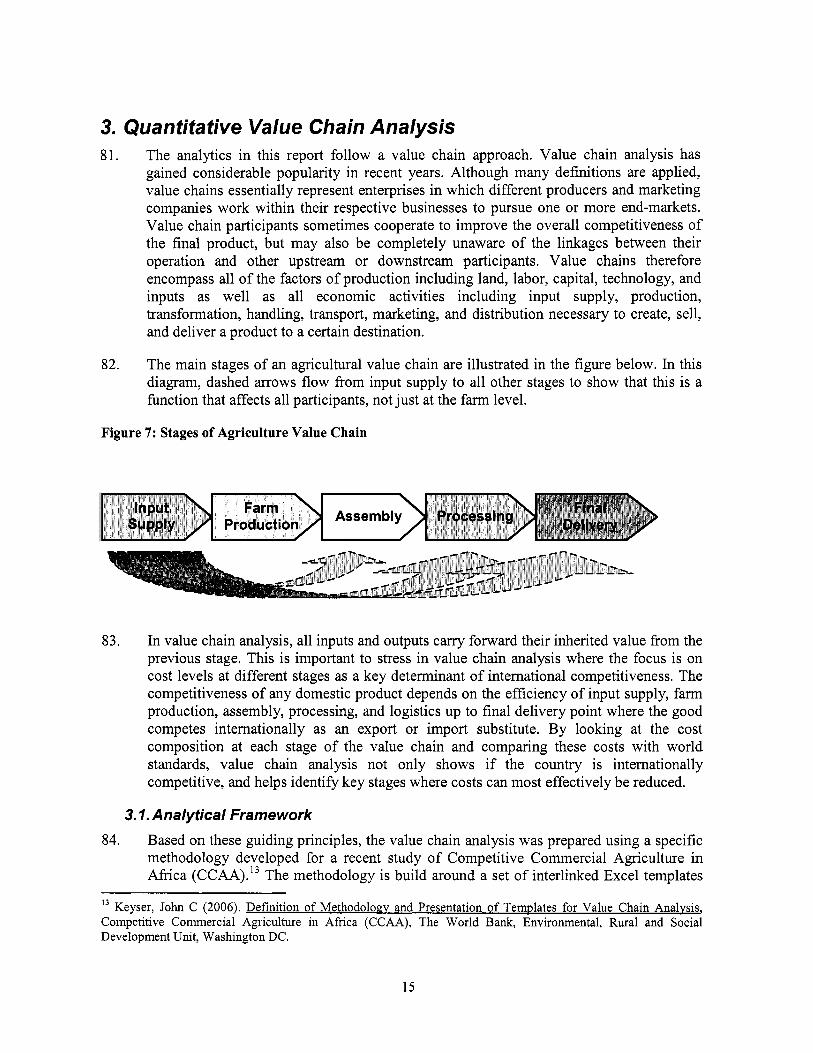

km M A I S C A M MIDENO MIDEVIV MINAGRI MINEPIA MT NGO NPK NPMB PAMOL PNDRT PNEVA P N V R A SABC S A F A C A M SOCAO

kg

African Caribbean and Pacific Asian Development Bank Agribusiness Mvog-Betsi Poultry Farming Compound Competitive Commercial Agriculture in Africa Customs Duty Cameroon Development Corporation Central African Economic and Monetary Community Cameroon Industrial Cotton Corporation Cost, Insurance, and Freight International Cooperation Center for Agricultural Research National Commission for the Certification o f Agricultural Pesticides Commercial Farm Domestic Value Added Economic Partnership Agreement European Union Family Farmer Family Farmer using improved inputs Family Farmer featuring l o w input use Food and Agriculture Organization Fresh Fruit Bunch Free on Board National Rural Development Fund Gross Domestic Product Hectare International Cotton Advisory Committee International Fund for Agricultural Development Integrated Pest Management Institute o f Agricultural Research for Development Ki logram Kilometer Cameroon Maize Corporation North-West Province Development Authority Seedlings and Foodstuff Development Authority Ministry o f Agriculture Ministry o f Livestock and Fishing Metric Ton Non-Governmental Organization Nitrogen Phosphorus and Potassium Fertilizer National Produce Marketing Board Palm Oil Corporation National Program for the Development o f Roots and Tubers National Program for Agricultural Extension and Training National Program for Agricultural Extension and Research Cameroonian Breweries Corporation Ago-industrial Farms o f Cameroon Western Poultry Farmers Cooperative

i

SOCAPALM SODECOTON SOWEDA SPC sv TT UCB USD XAF, BEAC

Cameroon Palm O i l Corporation Cameroon Cotton Development Corporation South-West Development Authority Cameroonian Provenderies Shipment Value Temporary Tax Cameroonian Breweries Union United States Dollar Central Afncan Franc, Bank of the Central African States

11

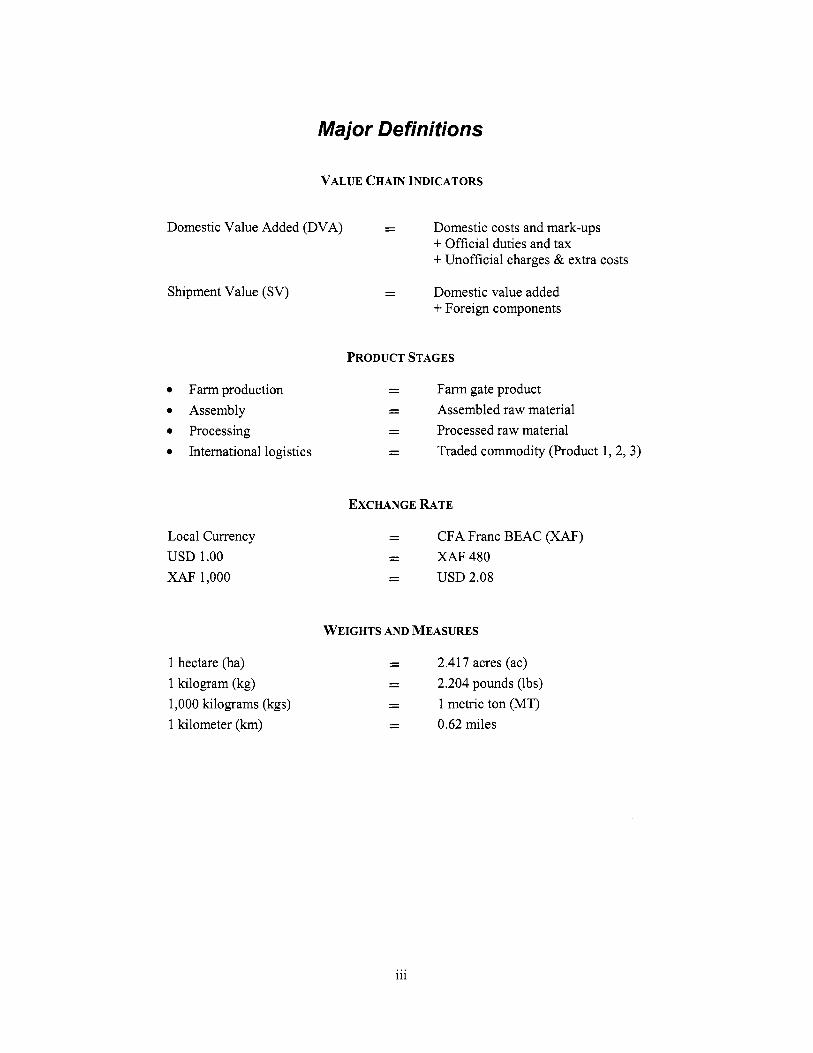

Major De fin itio ns

VALUE CHAIN INDICATORS

Domestic Value Added (DVA) - - Domestic costs and mark-ups + Off ic ia l duties and tax + Unoff ic ia l charges & extra costs

Shipment Value (SV)

0 Farm production 0 Assembly 0 Processing 0 International logistics

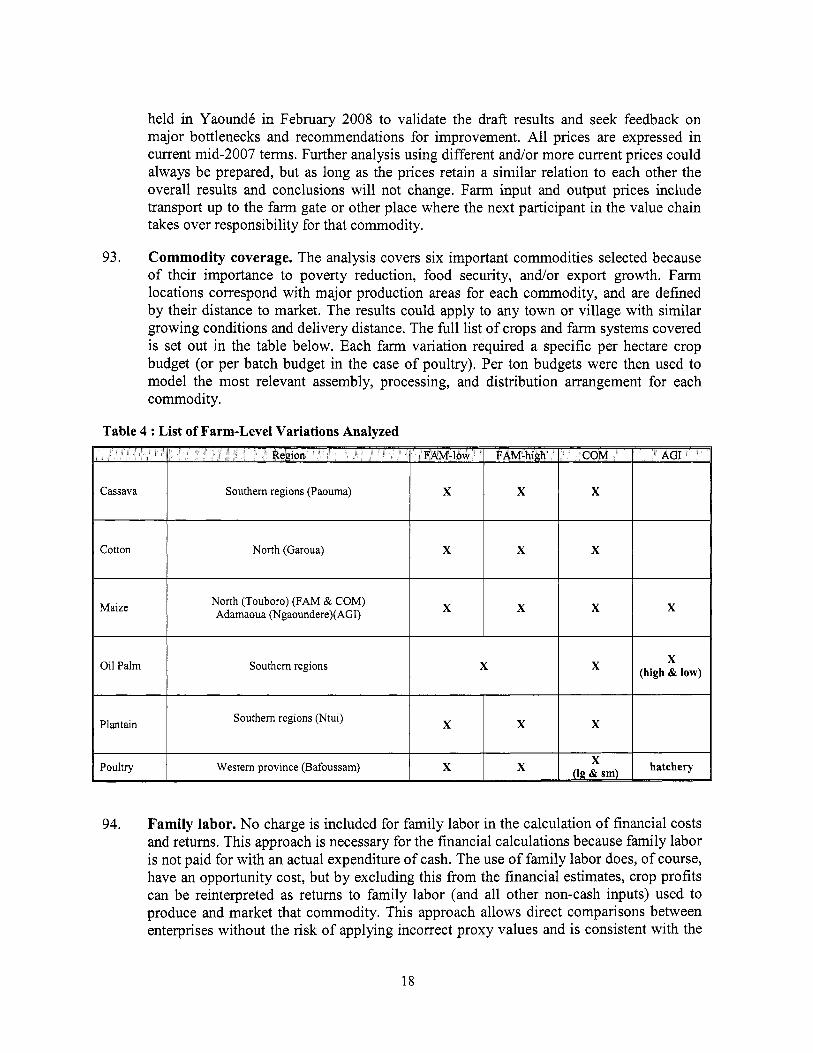

Local Currency U S D 1.00 XAF 1,000

1 hectare (ha) 1 kilogram (kg) 1,000 kilograms (kgs) 1 kilometer (km)

- - Domestic value added + Foreign components

PRODUCT STAGES

- - Farm gate product - - Assembled raw material - - Processed raw material - - Traded commodity (Product 1,2,3)

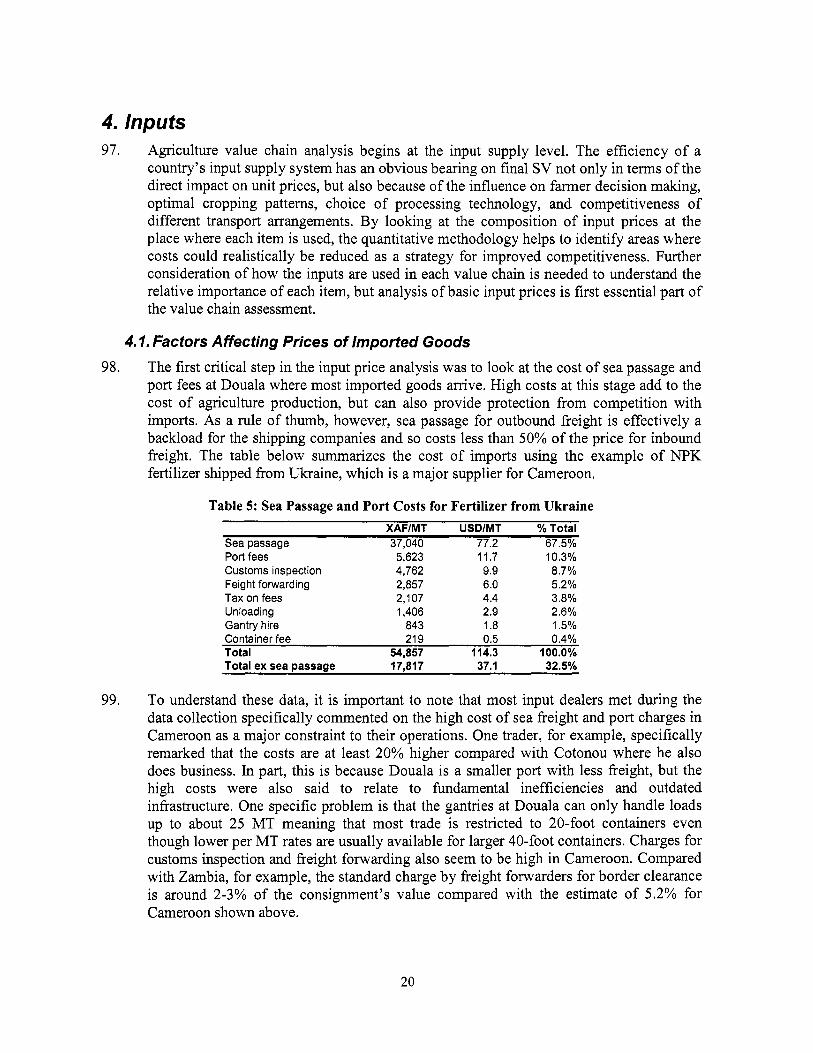

EXCHANGE RATE

- - C F A Franc B E A C (XAF) XAF 480

- - U S D 2.08 - -

WEIGHTS AND MEASURES

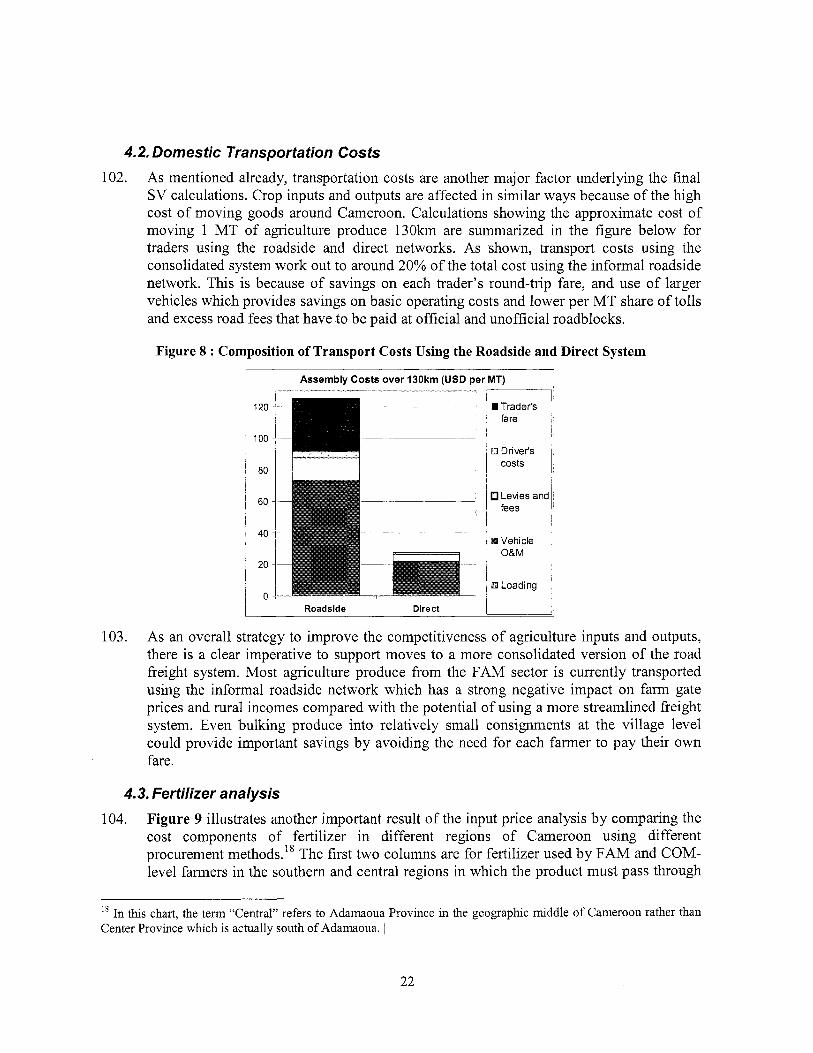

- - 2.417 acres (ac) - - 2.204 pounds (lbs) - - 1 metric ton (MT) - - 0.62 miles

... 111

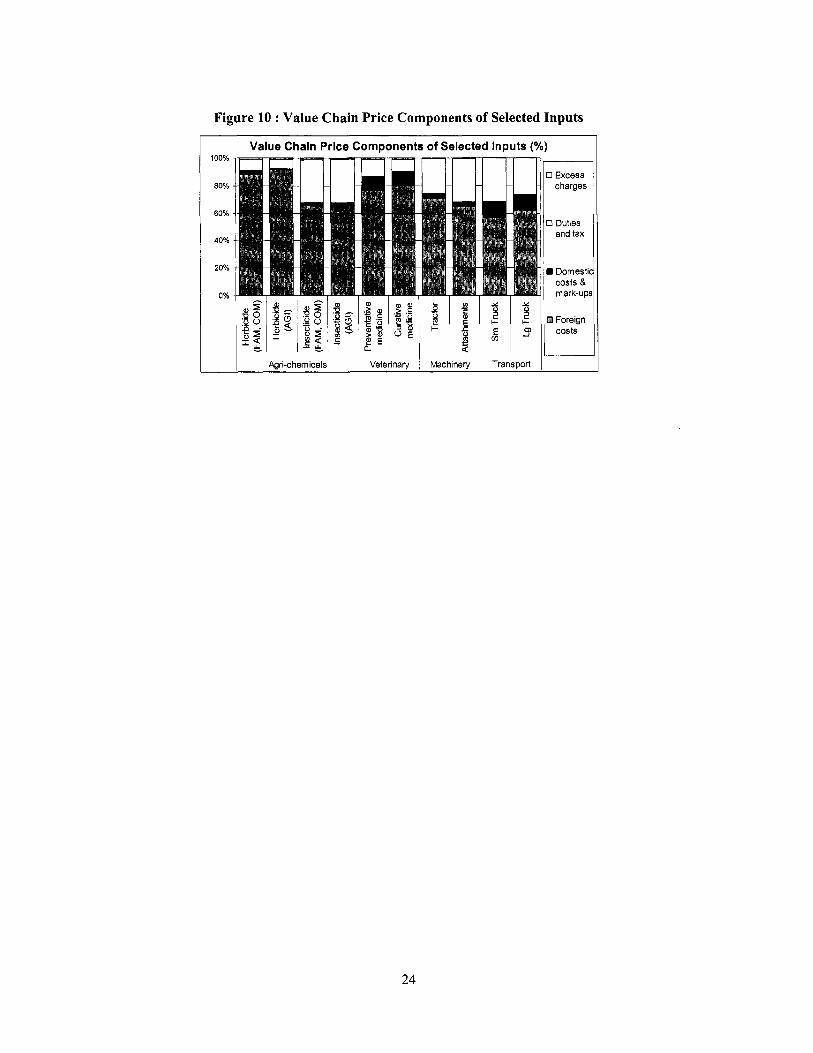

Acknowledgements

This Cameroon Agricultural Value Chain Competitiveness Study was carried out by the Wor ld Bank, the FA0 and a team o f consultants. The Wor ld Bank task team included Ousmane Seck (Task Team Leader and Senior Rural Development Specialist, AFTAR), Loraine Ronchi (Economist, AFTAR), Anke Reichhuber (Economist, AFTAR), Francois Mkouanga (Rural Development Specialist), Germaine Mafougong (Program Assistant, AFTAR), and Irene Marguerite Nnomo Ayinda-Mah (Team Assistant, AFCC1). The Consultant team included John Keyser, Tania Rajadel, Arsene Nkama. Marc Moens (FAO) provided an excellent assessment o f the poultry sector. The Wor ld Bank would l ike to acknowledge the excellent collaboration with Dr. Yankam on the behalf o f the Ministry o f Agriculture and Rural Development (MINADER). The participants o f a stakeholder feedback workshop held in Cameroon in February 2008 are thanked for their substantive comments and feedback. Grahame Beaumont Richard Dixie (Senior Agricultural Specialist, SASDA), Stephen Mink (Lead Economist, AFTSN) and Abdoulaye Seck (Senior Economist, AFTP3) served as Peer Reviewers. Renato Nardello (Senior Operations Officer, AFTAR) provided advice and comments. Mary Barton-Dock (Country Director, AFCCl), Karen McConnell Brooks (Sector Manager, AFTAR), and Francois L e Gall (Program Coordinator, AFTAR) supported the study and ensured that resources were available for i t s implementation. The team would also l ike to acknowledge the financial support provided by the Afr ica Agricultural Markets Trust Fund (DfID).

1v

Table of Contents

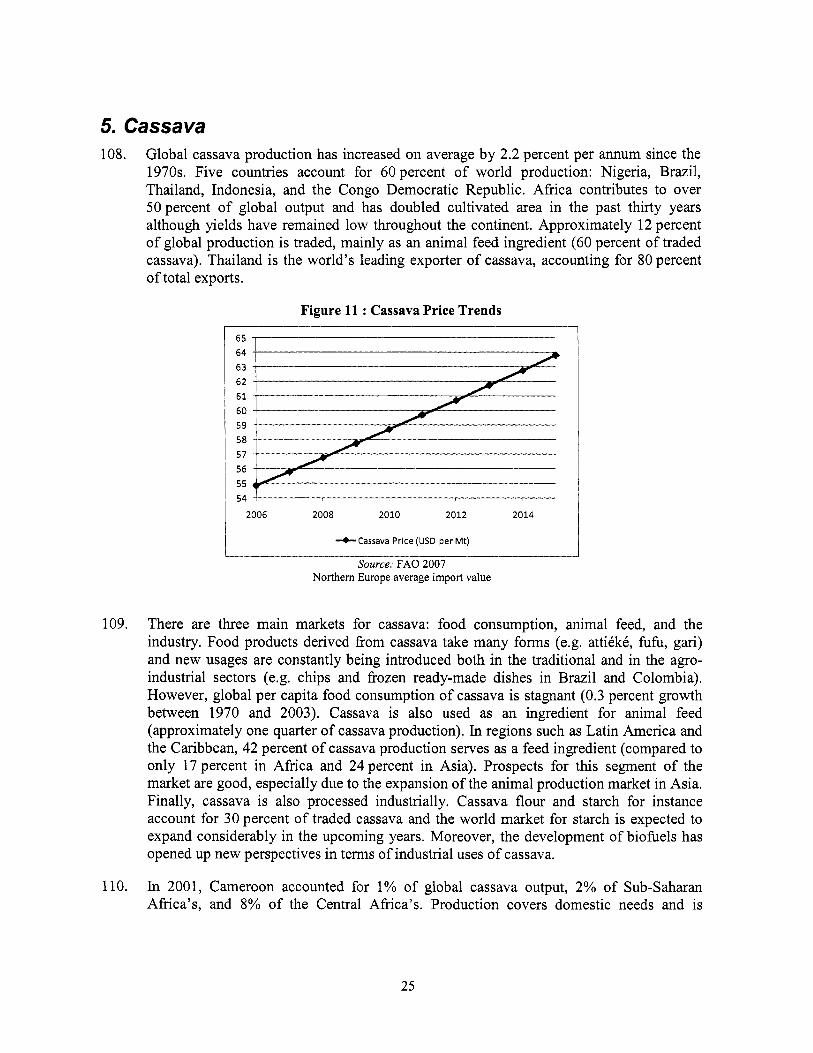

Acronyms ....................................................................................................................................................... i Major Definitions ........................................................................................................................................ 111

Acknowledgements ...................................................................................................................................... iv

. . .

Table of Contents .......................................................................................................................................... v L i s t of Figures ................................................................................................................................................ L i s t o f Tables .............................................................................................................................................. vii Executive Summary .................................................................................................................................. viii 1 . Introduction ........................................................................................................................................... 1 1.1. Role o f Agriculture in Cameroon ...................................................................................................... 1 1.2. Global food and fertilizer prices ........................................................................................................ 2 1.3. Study Objectives ............................................................................................................................... 4 2 . Context .................................................................................................................................................. 6 2.1. Geography ......................................................................................................................................... 6

. . .

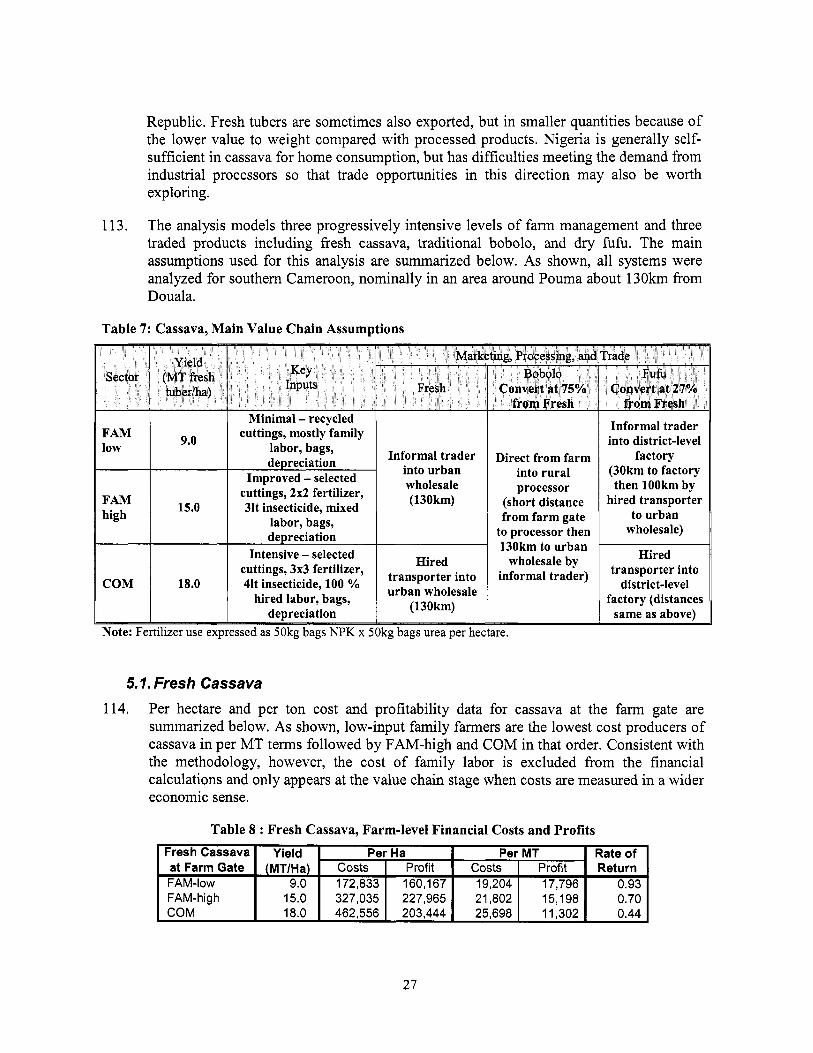

2.2. Commodity Coverage ........................................................................................................................ 6 2.3. Production systems ............................................................................................................................ 8

Quantitative Value Chain Analysis ..................................................................................................... 15

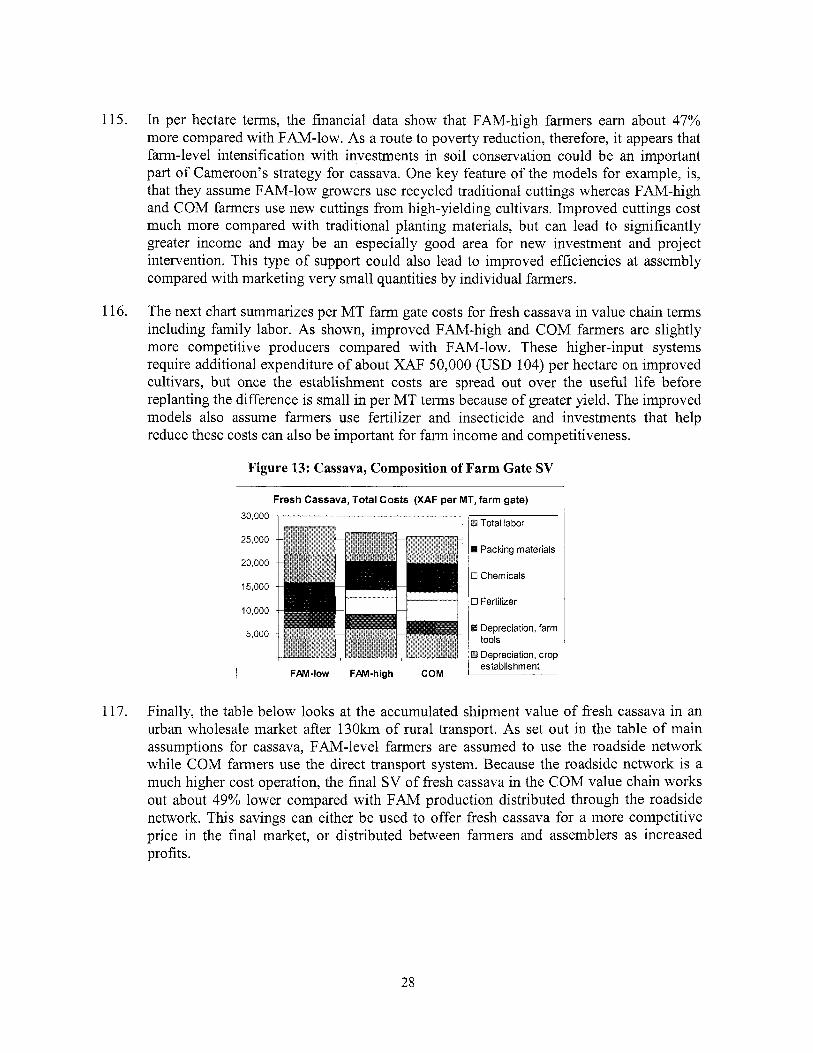

Procedures and Assumptions., ......................................................................................................... 17 4 . Inputs ................................................................................................................................................... 20

Factors Affecting Prices o f Imported Goods ................................................................................... 20 Domestic Transportation Costs ....................................................................................................... 22

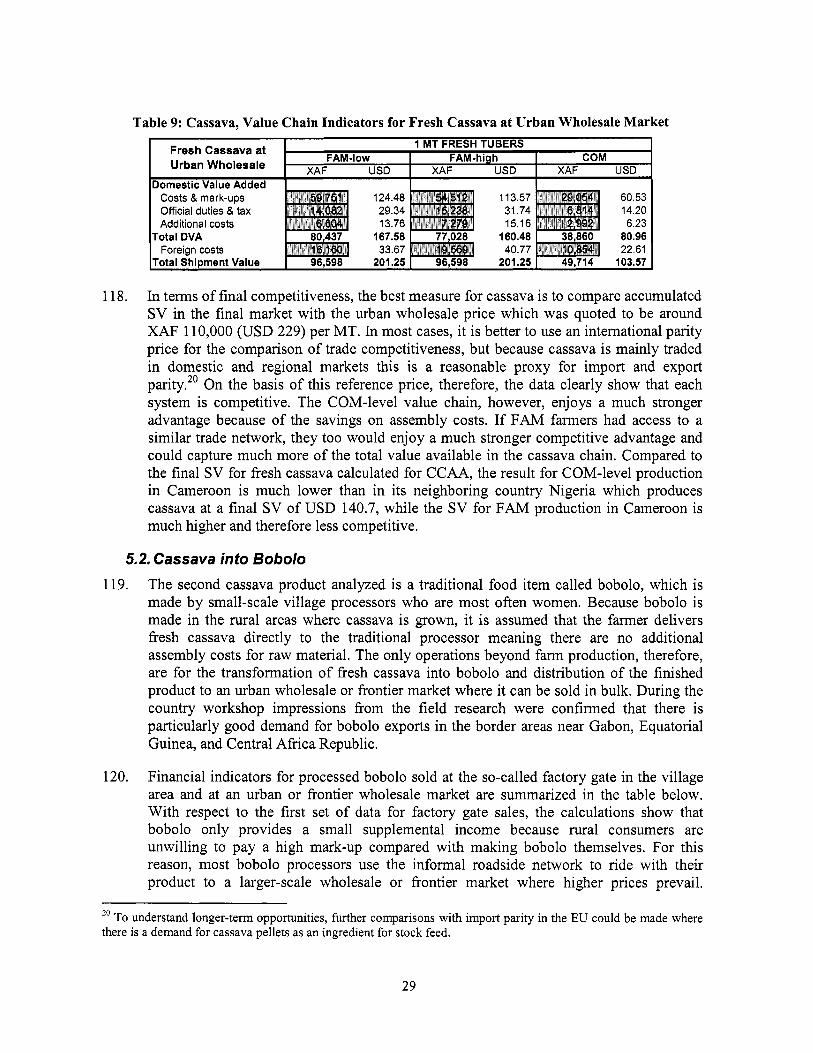

4.3. Fertilizer analysis ............................................................................................................................ 22

2.4. Agriculture Institutions ...................................................................................................................... 9 3 . 3.1. Analytical Framework ..................................................................................................................... 15 3.2.

4.1. 4.2.

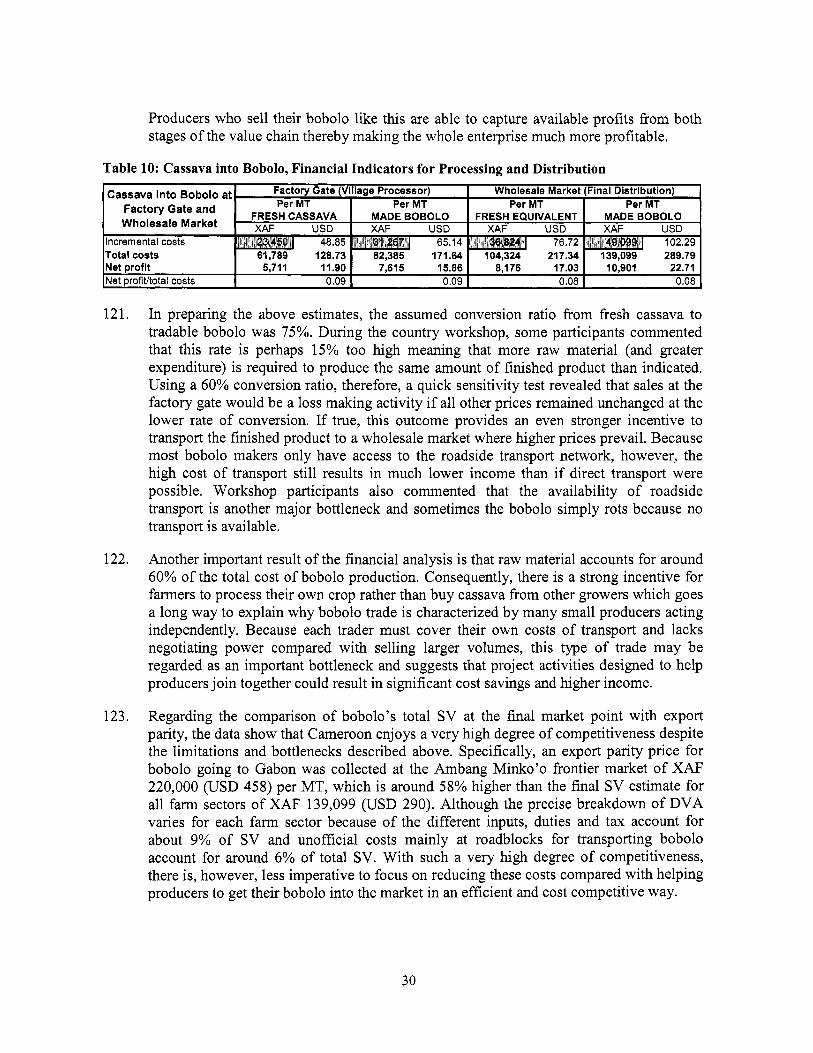

4.4. Cost Composition o f other Inputs ................................................................................................... 23 5 . Cassava ................................................................................................................................................ 25 5.1. Fresh Cassava .................................................................................................................................. 27 5.2. Cassava into Bobolo ........................................................................................................................ 29 5.3. Cassava into Fufu ........................................................................................................................... -31 6 . Cotton .................................................................................................................................................. 33 7 . Maize ................................................................................................................................................... 39 7.1 . Farm Production .............................................................................................................................. 41 7.2. Maize for Grain ............................................................................................................................... 42 7.3. Maize for Brewer’s Grits ................................................................................................................. 44 8 . Palm ..................................................................................................................................................... 46 8.1. Farm Production .............................................................................................................................. 48 8.2. Costs at Assembly, Processing, and Distribution ............................................................................ 50 8.3. Final Competitiveness o f Palm O i l ................................................................................................. 51 9 . Plantain ................................................................................................................................................ 52 9.1 . Farm Production .............................................................................................................................. 54 9.2. Assembly and Marketing ................................................................................................................. 55 10 . Poultry ............................................................................................................................................. 57 10.1. AGIHatchery ............................................................................................................................. 59 10.2. COM Broiler Production 60 10.3. FAM-level Village Chickens -63 1 1 . 11.1. 1 1.2.

............................................................................................................ ....................................................................................................

Conclusions ..................................................................................................................................... 65 Increasing access and use of inputs and high-yielding planting material by family farmers ..... 67 Reducing assembly to market cost for small farmers ................................................................ 68

V

1 1.3. 11 .4 .

Reduce transport cost ................................................................................................................. 7 1

Bibliographie ............................................................................................................................................... 73 Appendix. ............................................................................................................... 74

Issues to be explored .................................................................................................................. 71

List of Figures Figure 1: Growth of Cameroon's Economy ................................................................................................... 1

Figure 4: Global fertilizer prices ................................................................................................................... 3

Figure 7: Stages of Agriculture Value Chain .............................................................................................. 15 Figure 8: Composition o f Transport Costs Using the Roadside and Direct System ................................... 22 Figure 9: Fertilizer Financial and Value Chain Price Build-up ................................................................... 23 Figure 10: Value Chain Price Components o f Selected Inputs ................................................................... 24 Figure 11: Cassava Price Trends ................................................................................................................. 25 Figure 12: Cassava Value Chain Diagram .................................................................................................. 26 Figure 13: Cassava, Composition of Farm Gate SV ................................................................................... 28

Figure 16: Cotton Value Chain Diagram .................................................................................................... 35 Figure 17: Cotton, Composition o f Farm Gate SV (I MT seed cotton before assembly) ........................... -36 Figure 18.Cotton, Total Value Chain Costs by Production Stage and Farm Sector ................................... 38

Figure 20: Maize Value Chain Diagram ..................................................................................................... 40 Figure 2 1 : Maize, Composition o f Farm Gate SV before assembly ........................................................... 42

Figure 2: Agricultural Exports Composition (2000.2006) ............................................................................ 2 Figure 3: Global food prices ......................................................................................................................... - 3

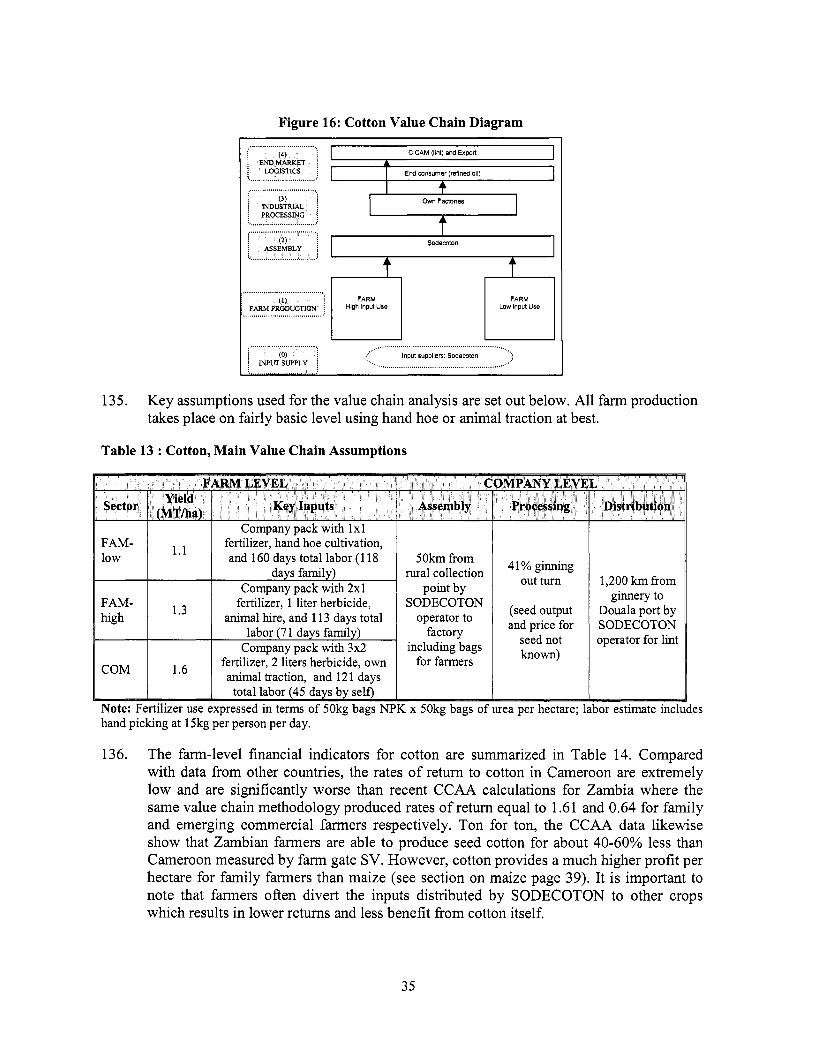

Figure 5: Cameroon's Rural Sector Strategy Objectives .............................................................................. 4

Figure 14: World Cotton Prices in USD/kg ................................................................................................ 33 Figure 15: Evolution of World Prices in USD and FCFA ........................................................................... 33

Figure 19: Maize world market prices in USD/ton ..................................................................................... 39

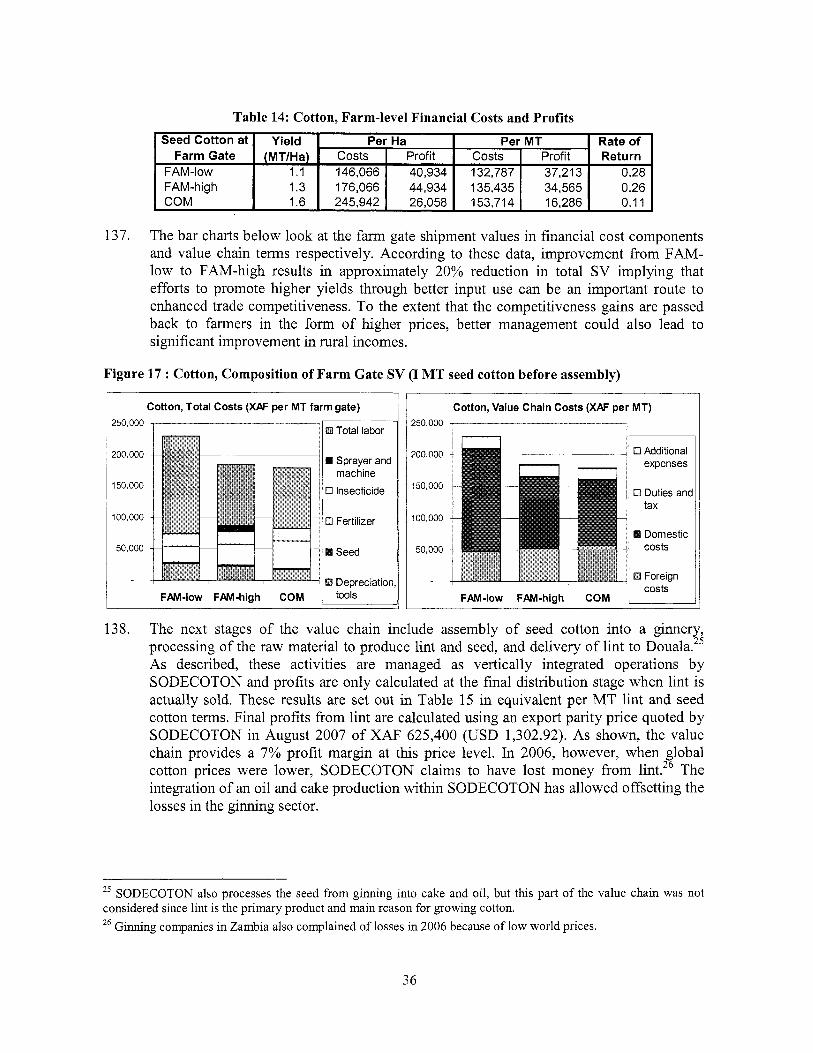

Figure 22: Maize Grain, Composition o f Total Value Chain SV (1 MT grain after assembly) .................. 43 Figure 23: Maize Grits SV by Stage ........................................................................................................... 44 Figure 24: Palm o i l world market prices ..................................................................................................... 46 Figure 25: Palm Oi l Value Chain Diagram ................................................................................................. 47 Figure 26: Palm, Composition o f Farm Gate SV (1 MT FFB before delivery to factory) .......................... 49 Figure 27: Phlm SV by Value Chain Stage ................................................................................................. 50 Figure 28: Palm Total SV at Final Market .................................................................................................. 51 Figure 29: Prices o f Plantain in Selected Urban Centers in Cameroon (XAF per lulogram) ...................... 52 Figure 30: Plantain Value Chain Diagram .................................................................................................. 53 Figure 3 1 : Plantain, Composition o f Farm Gate SV (per Ha and per MT before Assembly) ..................... 55 Figure 32: Plantain, Total SV 1 MT Plantain at Assembly Market ............................................................ 56 Figure 33: Global Poultry Price Trends ...................................................................................................... 57

Figure 35: Poultry, Composition o f Hatchery Gate SV for AGI-level 1-day Chicks (per bird) ................. 60 Figure 36: Poultry, Composition o f Farm Gate SV for COM-level Broiler Chickens (per live bird) ......... 61 Figure 37: Poultry, Composition o f Farm Gate SV for FAM-level Village Chickens (per live bird) ......... 63

Figure 34: Poultry Value Chain Diagram .................................................................................................... 58

vi

List of Tables Table 1 : Cross-cutting recommendations ...................................................................................................... x Table 2: Commodity specific recommendations.. .................................................................................... xvii

Table 4: L i s t o f Farm-Level Variations Analyzed ..................................................................................... -18

Table 6: Selected Import Tariffs and other Tax Rates in Cameroon ........................................................... 21

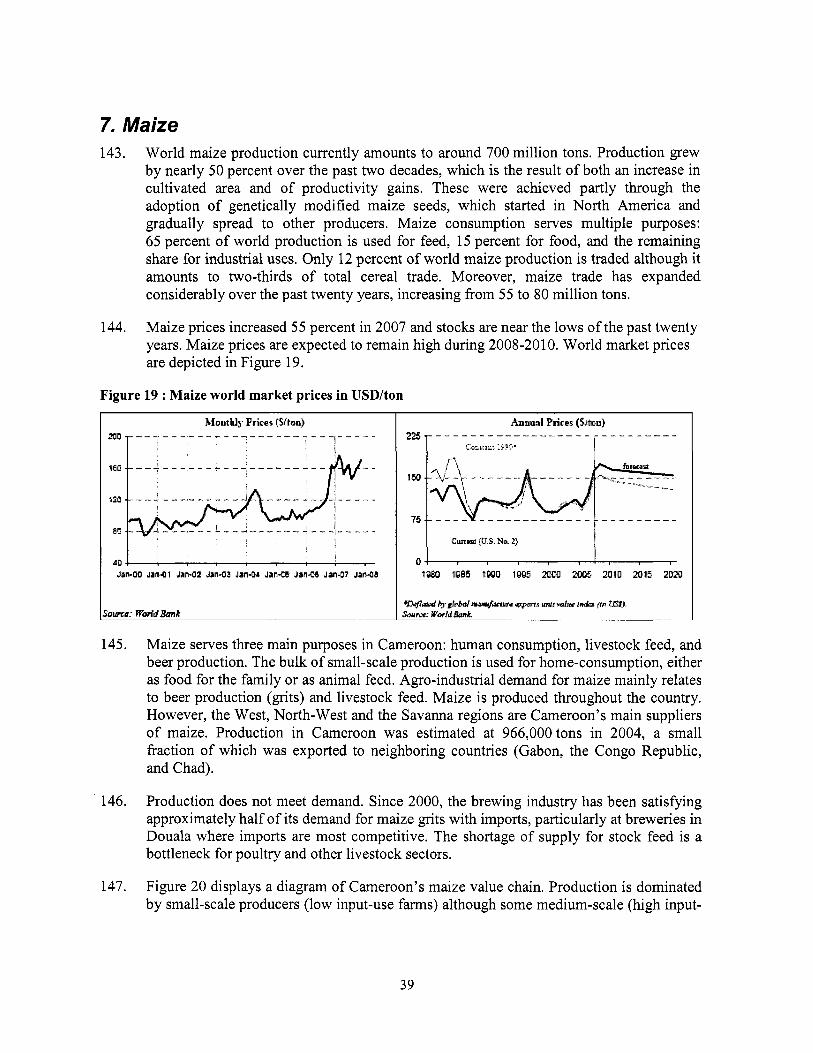

Table 8: Fresh Cassava, Farm-level Financial Costs and Profits ................................................................ 27

Table 3: Ago-ecological Zones and Agricultural Activities in Cameroon ................................................... 6

Table 5: Sea Passage and Port Costs for Fertilizer f rom Ukraine ............................................................... 20

Table 7: Cassava, M a i n Value Chain Assumptions .................................................................................... 27

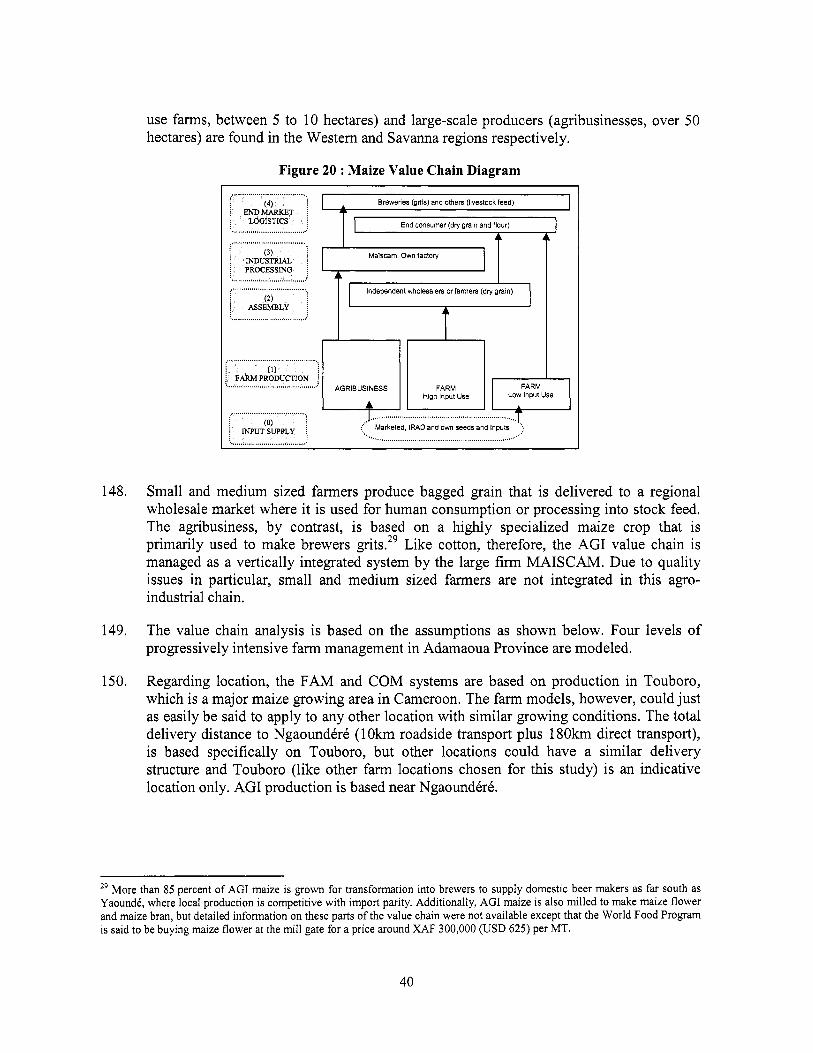

Table 9: Cassava, Value Chain Indicators for Fresh Cassava at Urban Wholesale Market ........................ 29 Table 10: Cassava into Bobolo, Financial Indicators for Processing and Distribution ............................... 30 Table 11: Cassava into Fufu, per MT Assembly Level Costs and Profitability for Roadside and Direct Transport Networks over 30km Delivery Distance ..................................................................................... 31

Table 13: Cotton, M a i n Value Chain Assumptions ..................................................................................... 35 Table 14: Cotton, Farm-level Financial Costs and Profits .......................................................................... 36 Table 15: Cotton, Financial Indicators for Assembly, Processing, and Distribution .................................. 37

Table 12: Cassava into Fufu, Processing-level Financial Indicators ........................................................... 32

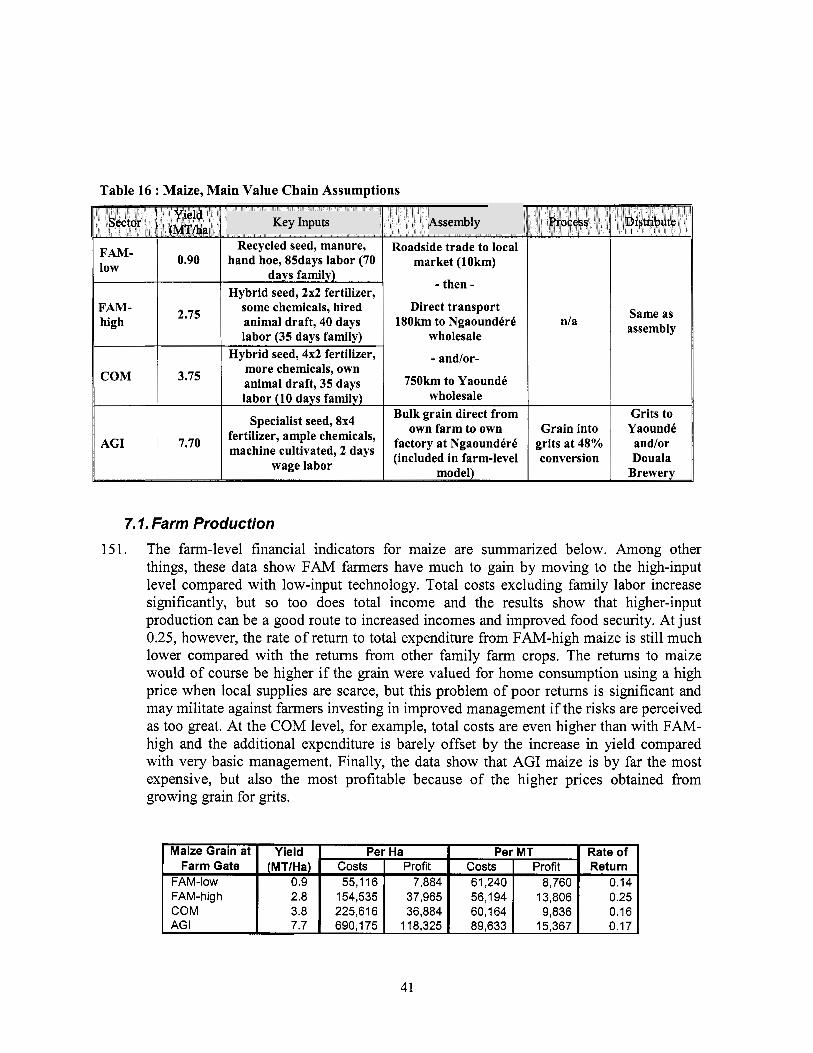

Table 16: Maize, M a i n Value Chain Assumptions ..................................................................................... 41 Table 17: Maize, Farm-level Financial Indicators ...................................................................................... 41 Table 18: Maize, per MT Financial Indicators for AGI Production ............................................................ 44 Table 19: Maize Grits, Competitiveness Gap ............................................................................................. 45 Table 20: Palm, M a i n Value Chain Assumptions ....................................................................................... 48 Table 2 1 : Palm, Farm-level Financial Indicators ........................................................................................ 49 Table 22: Palm AGI Financial Indicators per MT Traded Crude Oil ......................................................... 50 Table 23 : Plantain, M a i n Value Chain Assumptions .................................................................................. 54 Table 24: Plantain, Farm-level Financial Indicators ................................................................................... 54 Table 25 : Poultry, M a i n Value Chain Assumptions .................................................................................... 59 Table 26: Poultry, C O M Financial Indicators at Farm-level ....................................................................... 60 Table 27: Poultry, Summary of Final SV at Distribution after Slaughter per Bird and per MT ................. 61

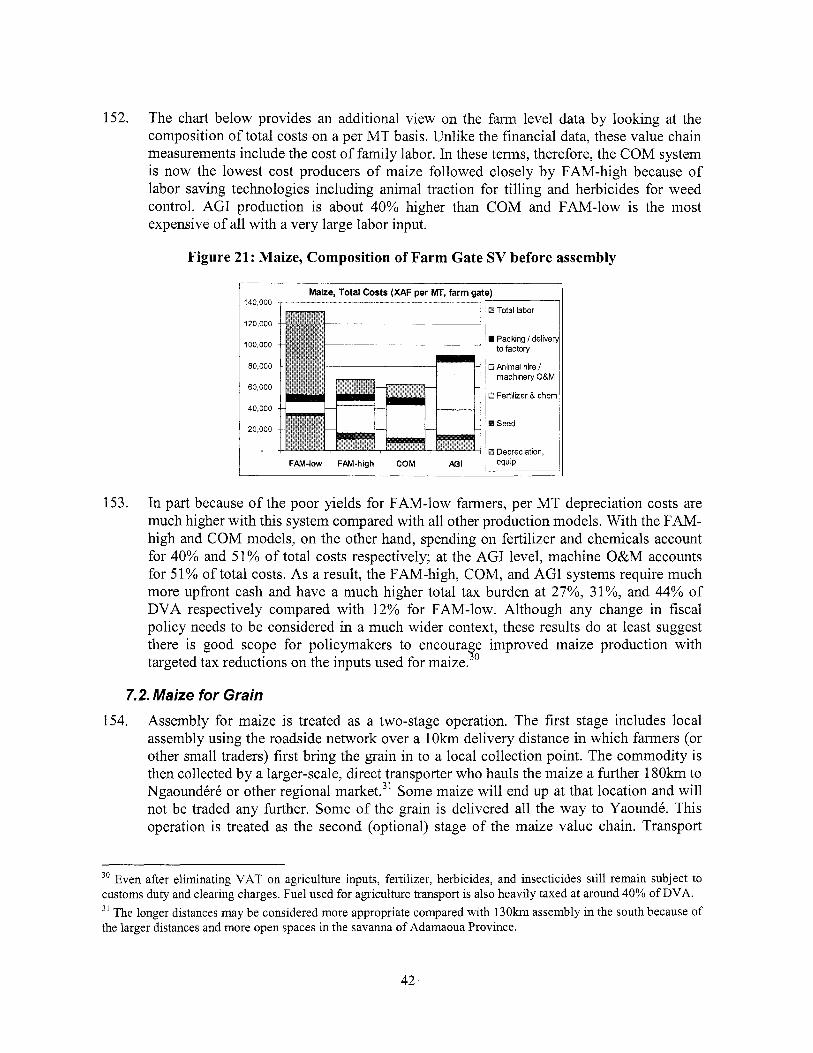

and U S D per MT raw meat) ........................................................................................................................ 62

meat). ............................................................................................................................................ ............. 62 Table 30 .Poultry, FAM Financial Indicators at Farm-level ....................................................................... 63 Table 3 1 : Competitiveness of 6 selected value chains per production system ........................................... -65 Table 32: M a i n bottlenecks of 6 selected value chains per production system ........................................... 66 Table 33 : M a i n cross-cutting recommendations ......................................................................................... 70

Table 28: Poultry, Calculation o f the “Competitiveness Gap” between Total SV and Import Parity (XAF

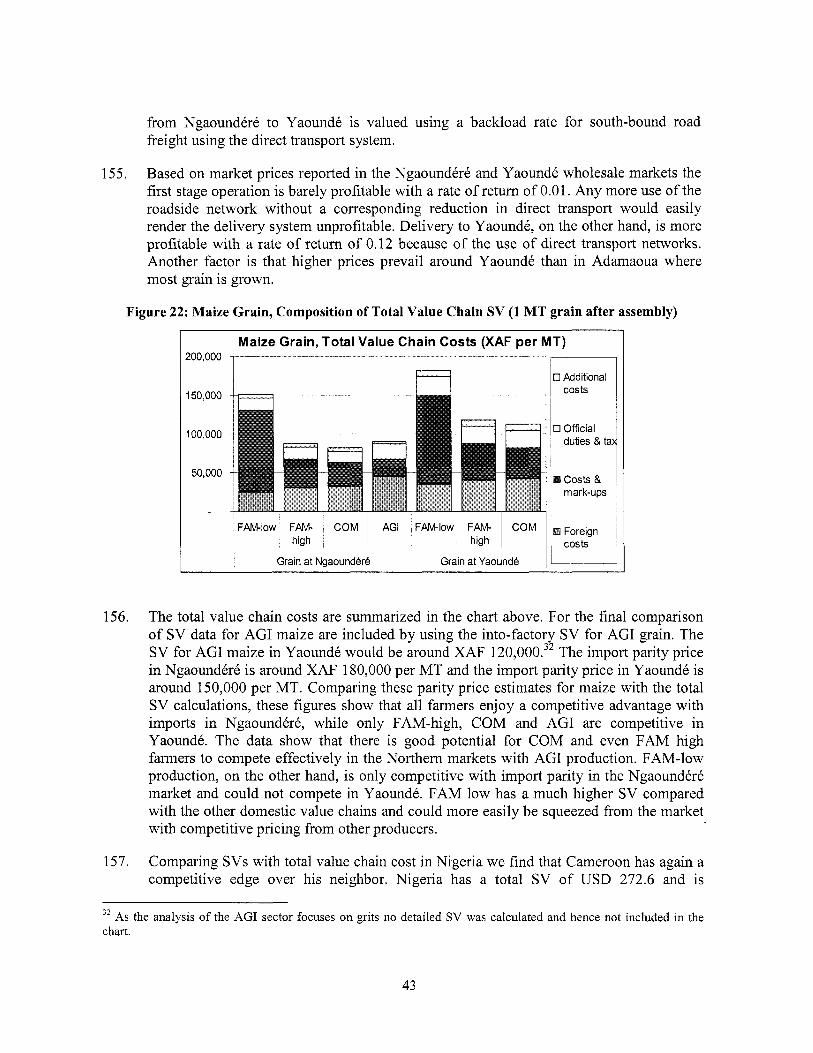

Table 29: Poultry, Detailed Break-down of Value Chain Cost Components (XAF and U S D per MT raw

vii

Executive Summary Objectives and Approach

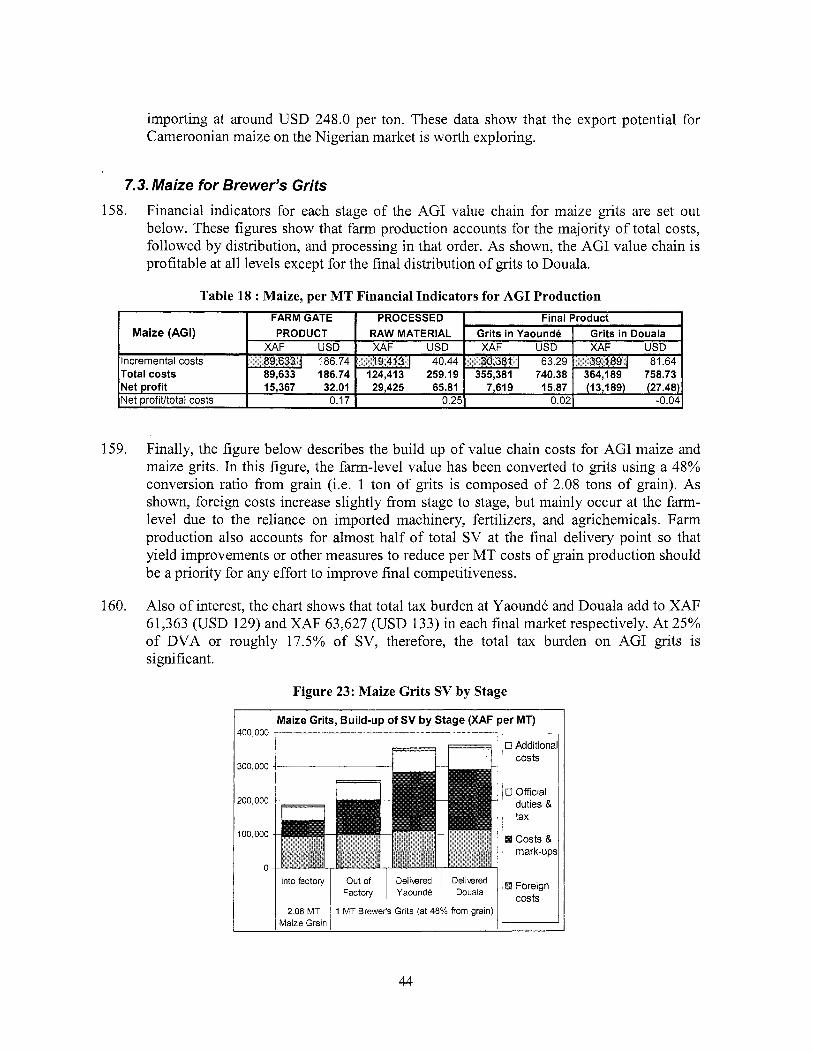

1. This study aims to assist in the realization o f the Government’s rural sector objectives through the specific avenue o f improved commercial agricultural competitiveness. I t explores the concrete constraints and potential for domestic, regional, and/or international competitiveness o f six agricultural value chains that involve family, commercial, and large ago-industrial enterprises in different regions o f Cameroon. The selected chains are cassava, cotton, maize, palm, plantain, and poultry. The immediate objective o f the competitiveness study i s to identify products and farm systems that are currently competitive or have the potential o f becoming competitive in domestic, regional, or global markets. More specifically, the Government has asked the Bank to provide support for i t s growing agricultural program. This Economic and Sector work is expected to inform the preparation o f a new lending operation for the agricultural sector in Cameroon.

2. Rapidly rising international grain prices have fed into higher prices for staple foods, leading to severe hardships for the poor in numerous areas, a cut in the standard o f living o f the urban middle class, and social unrest in Cameroon. There are a number o f longer- term trends underlying these price rises suggesting that while the highest peaks may come down, staple grain prices are unlikely to recover in the foreseeable f i ture their relatively l ow and stable levels that characterized the second hal f o f the 1980s until about two years ago. Governments can respond to the hike in prices through short, medium, and long-term measures. Policy interventions can be divided into three broad classes: (i) interventions to ensure household food security by strengthening targeted safety nets; (ii) interventions to lower domestic food prices through short-run trade pol icy measures or administrative action, and (iii) interventions to enhance longer-term food supply. The investment and pol icy recommendations following from this report for food crops belong to the third class o f interventions.

3. The approach i s based on a quantitative value chain analysis. The main stages o f an agricultural value chain are illustrated in the figure below. By looking at detailed price build-up from stage to stage o f agriculture value chains, the study specifically helps identify key bottlenecks and changes along the chain that need to take place to realize Cameroon’s potential.

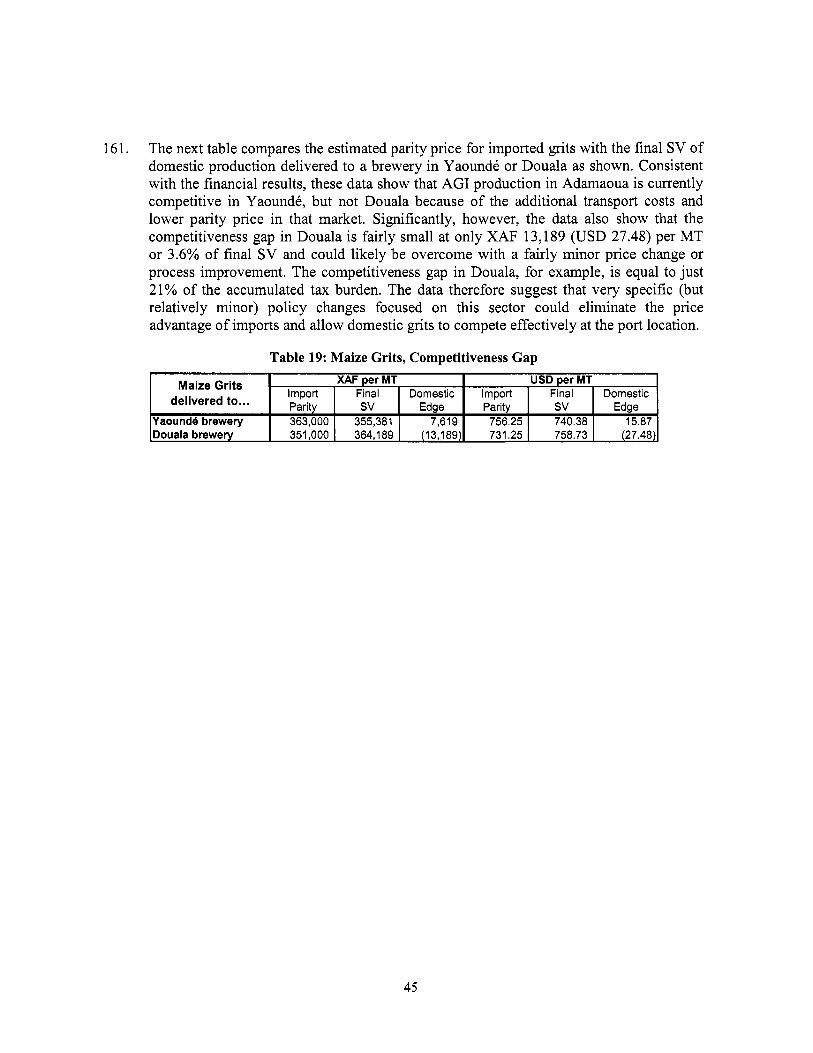

input Farm Supply >’ Productio

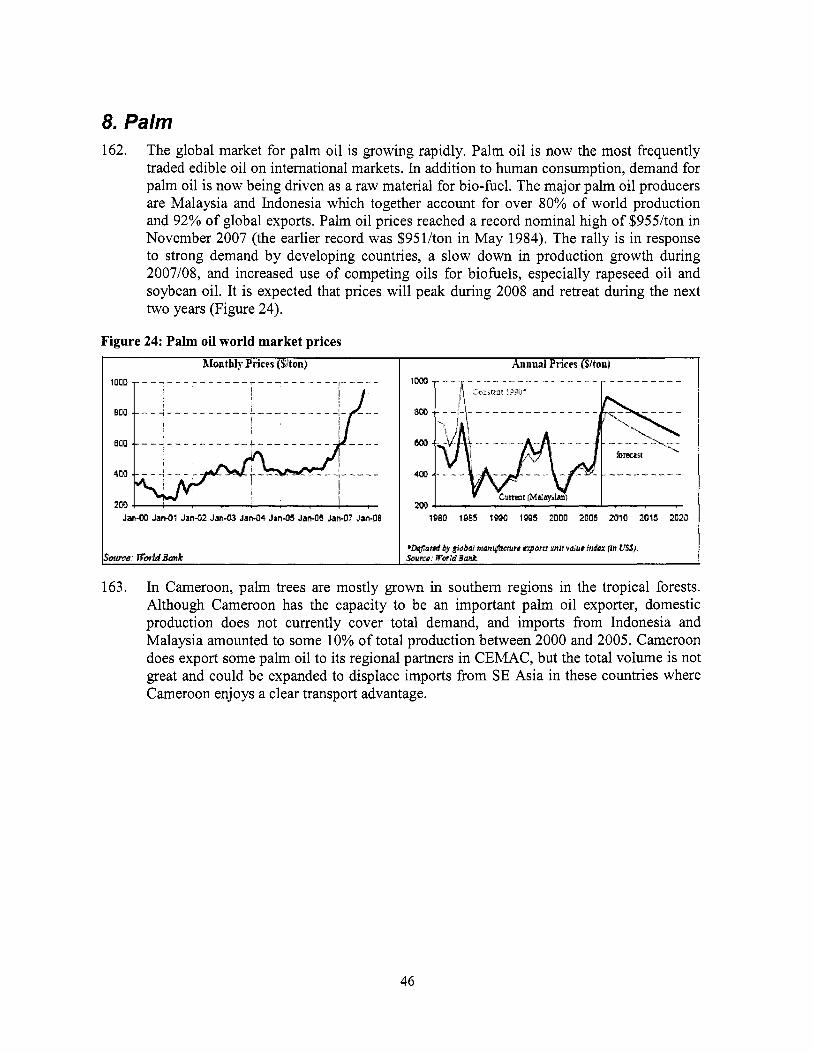

4. As Cameroon mainly has influence over prices within i t s own borders, the methodology i s particularly interested in the composition o f domestic costs. The quantitative value chain analysis i s based on data collected in Cameroon from M a y to August 2007. Subsequent to the data collection and analysis phase, a country workshop was held in

viii

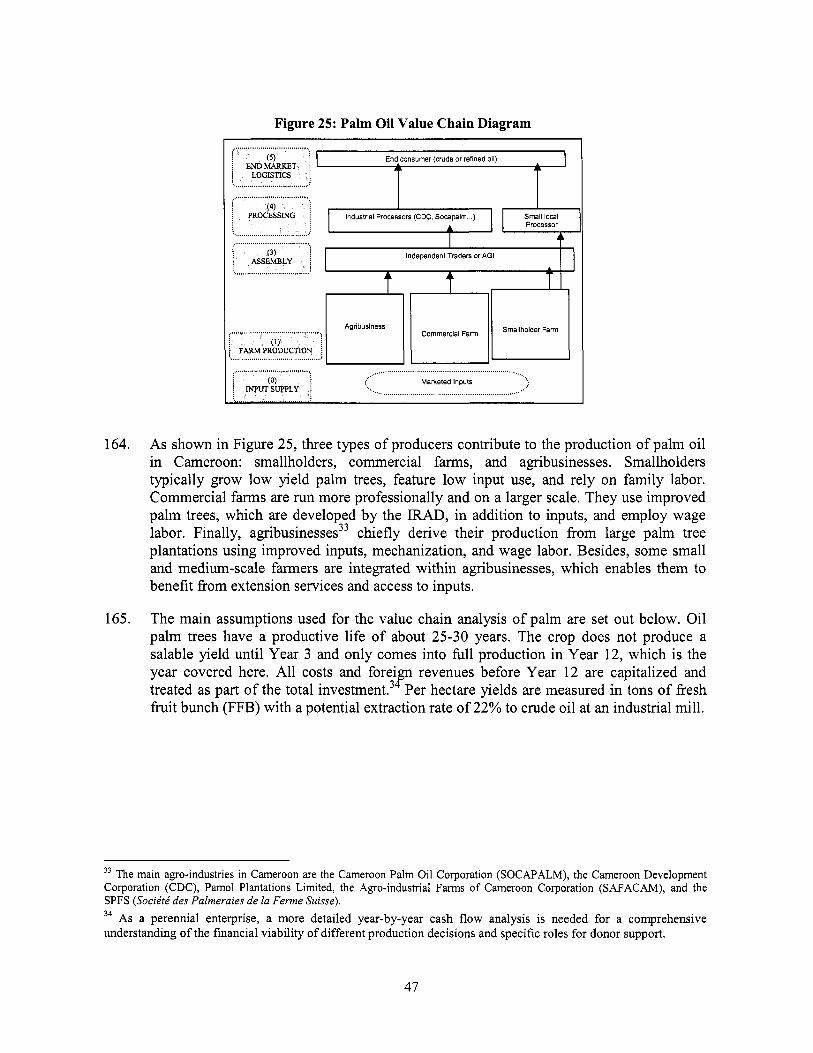

YaoundC in February 2008 to validate the draft results and seek feedback on major bottlenecks and recommendations for improvement.

Cameroon’s potential

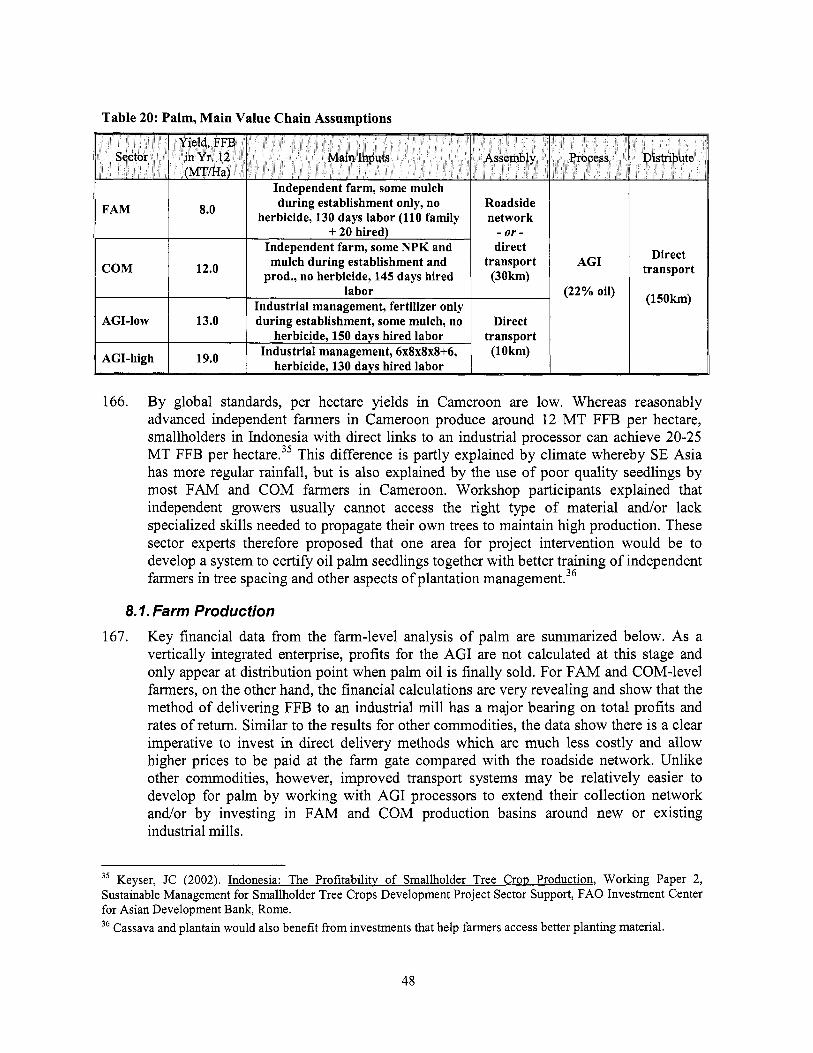

5. The first conclusion to be drawn from the analysis i s that Cameroon has good potential to become a major food supplier to the region because o f i t s competitiveness in cassava, maize, and plantain. Investments in these three sectors would not only improve food security but also lead to higher incomes.

6. This conclusion i s especially relevant in light o f the recent hike in food prices. I t is, however, most l ikely not realistic to expect a significant sustainable supply response from family farms to rising food prices in the short-term. I t wi l l take longer-term efforts to achieve sustainable increases in smallholder agricultural productivity and production levels, al l which require a combination o f services and investments such as extension and technology transfer, access to affordable inputs and credit, access to markets, etc. The short-term sustainable supply response for food crop production could come most realistically from Cameroon’s commercial farming sector which already has the necessary capacity to adapt to market opportunities.

7. Significant growth in income and increased trade competitiveness could also be achieved in the palm o i l sector. For poultry the conclusion i s less straightforward. There i s certainly good reason to expand the production o f village chicken by family farmers with important benefits for food security and poverty reduction in rural areas. The future o f the commercial poultry sector, however, depends on continued trade protection for the medium to long term. Cotton has some potential for competitiveness gains, but l ow global market prices are a major threat to the sustainability o f the sector.

Cross-cutting results

8. Interventions are needed to increase access and use o f inputs and high-yielding planting material by family farmers. The graduation o f family farmers from low-input production to more intensive systems i s important for the competitiveness o f commercial agriculture in Cameroon. In nearly every case, the analysis shows that the increased use o f inputs, high-yielding planting material and better on-farm management including SLM best practices could have a direct positive impact on rural incomes and trade competitiveness. Smallholders rarely have access to inputs and high yielding planting material because they are not affordable or locally not available.

9. Interventions are necessary to reduce the cost o f inputs and planting material. The analysis highlights several options for possible actions. An important result o f the input price analysis highlights the impact o f different procurement methods. Whi le the fertilizer used by FAM and COM-level farmers must pass through the local wholesale and retail network the AGIs import directly. Taken together, the fertilizer price analysis suggests there may be good potential for reducing the cost o f this important input through investments that help streamline the distribution system. One option would be to move

ix

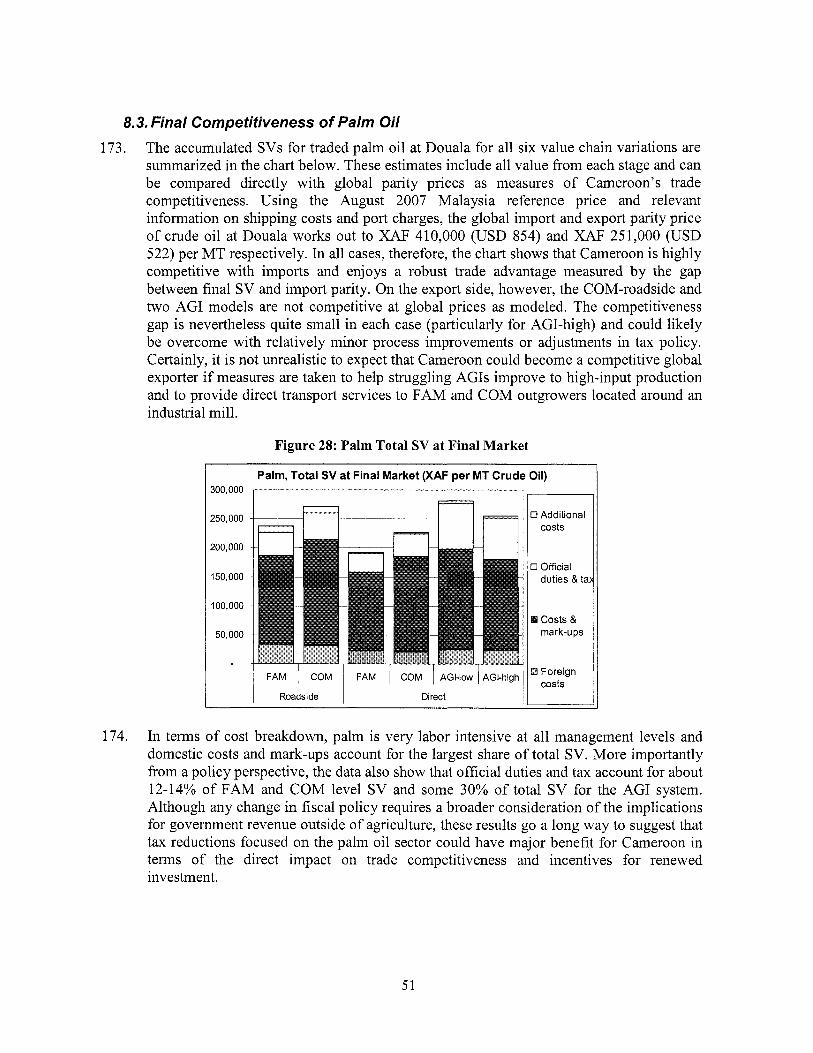

toward coordinated procurement o f farmers. Customs duties, import taxes, and VAT are a second major determinant o f agriculture input prices and should be revisited.

10. A second set o f interventions would strengthen the supply system. A reform o f the fertilizer sector i s currently under preparation and aims at improving small farmers' access to fertilizer. In regards to improving the legal framework, the Seed Act (Loi Semenciere) promulgated in 2001 and the Fertilizer Act (Loi sur les Engrais) promulgated in 2003 to improve regulation o f the market, should be revisited in order to determine why the implementing decrees (de'crets d 'application), which are necessary for any Act to be enforced have not yet been issued.

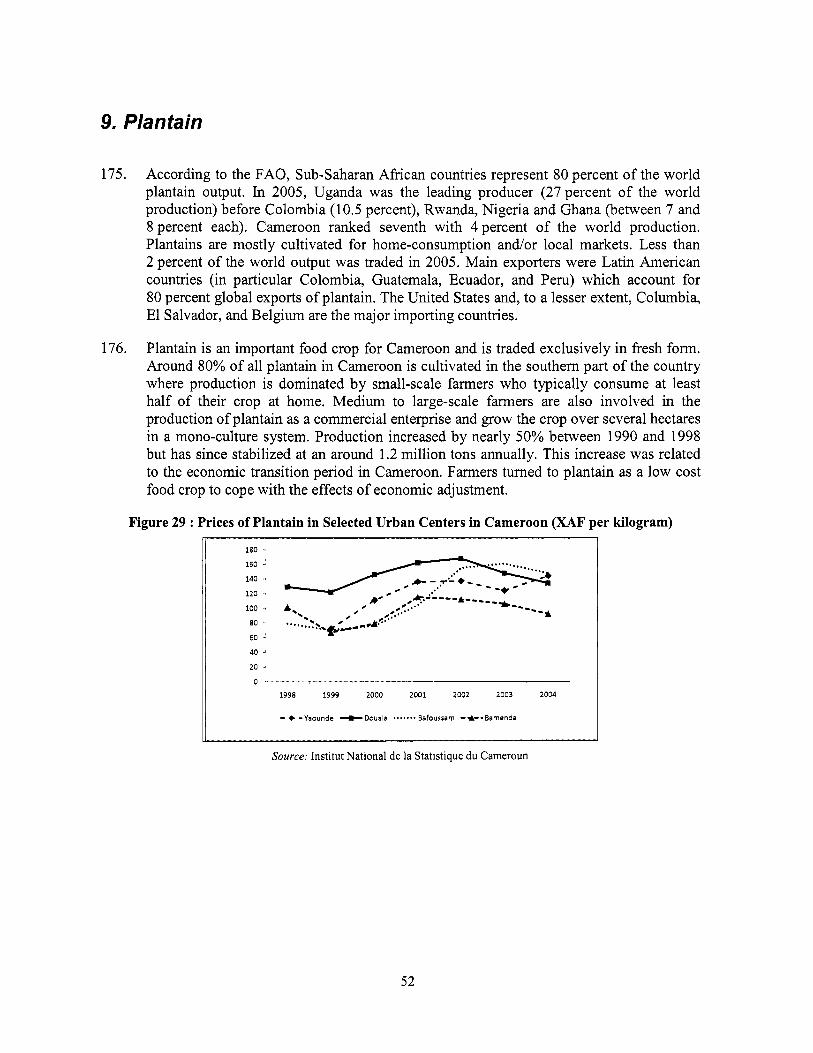

11. A third set o f interventions to increase access and use o f inputs and high-yielding planting material would increase input use efficiency and the dissemination o f new technologies. Possible actions could build on experience and lessons learnt o f The National Program for Agricultural Extension and Research (PNVRA), adopted in 1998, which was designed to develop agricultural research and revitalize agricultural extension services.

12. A hrther option would be to provide technical assistance to producer organizations to coordinate their demand and purchase o f inputs and planting material. Interventions to increase the affordability and availability o f good planting material and inputs would need to be accompanied by training activities building on experience o f The National Program for Agricultural Extension and Research (PNVRA), adopted in 1998, which was designed to develop agricultural research and revitalize agricultural extension services.

Table 1 : Cross-cutting recommendations

0 Move towards coordinated procurement o f farmers

Link producer groups with suppliers 0

Strengthen supply Implement Fertilizer A c t

0 Implement Seed A c t

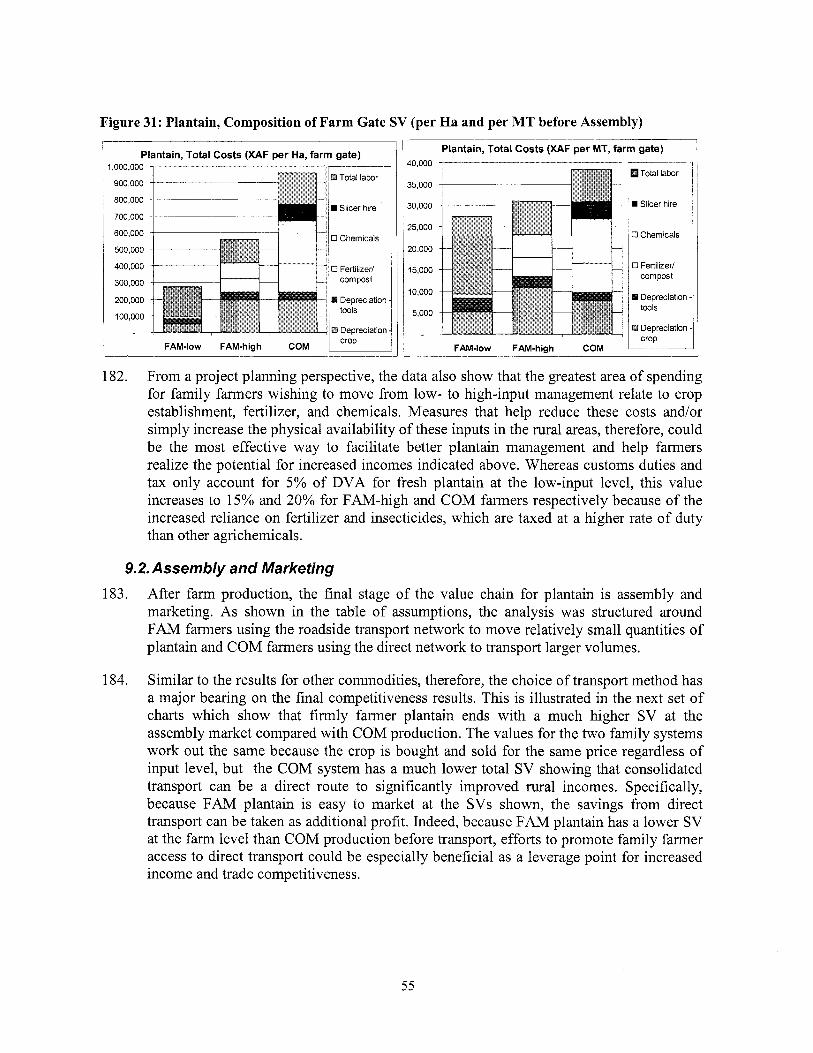

Increase input use, 0 Provide technical training for farmers

X

xi

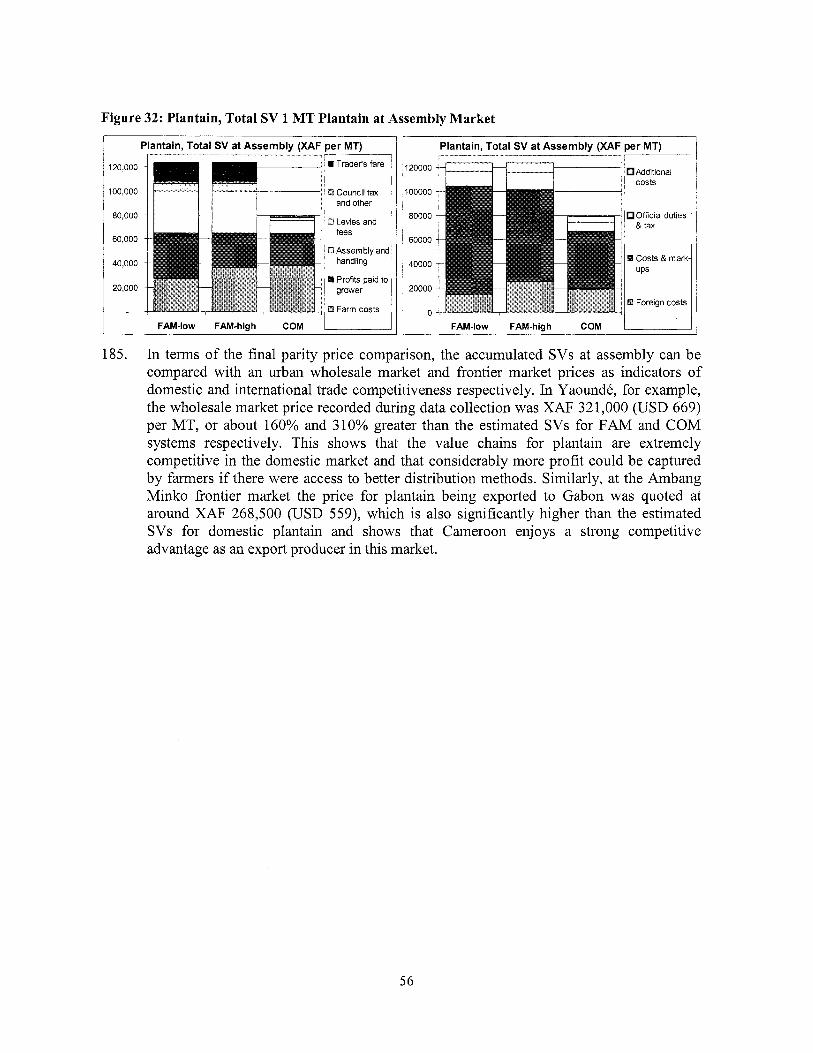

13.

14.

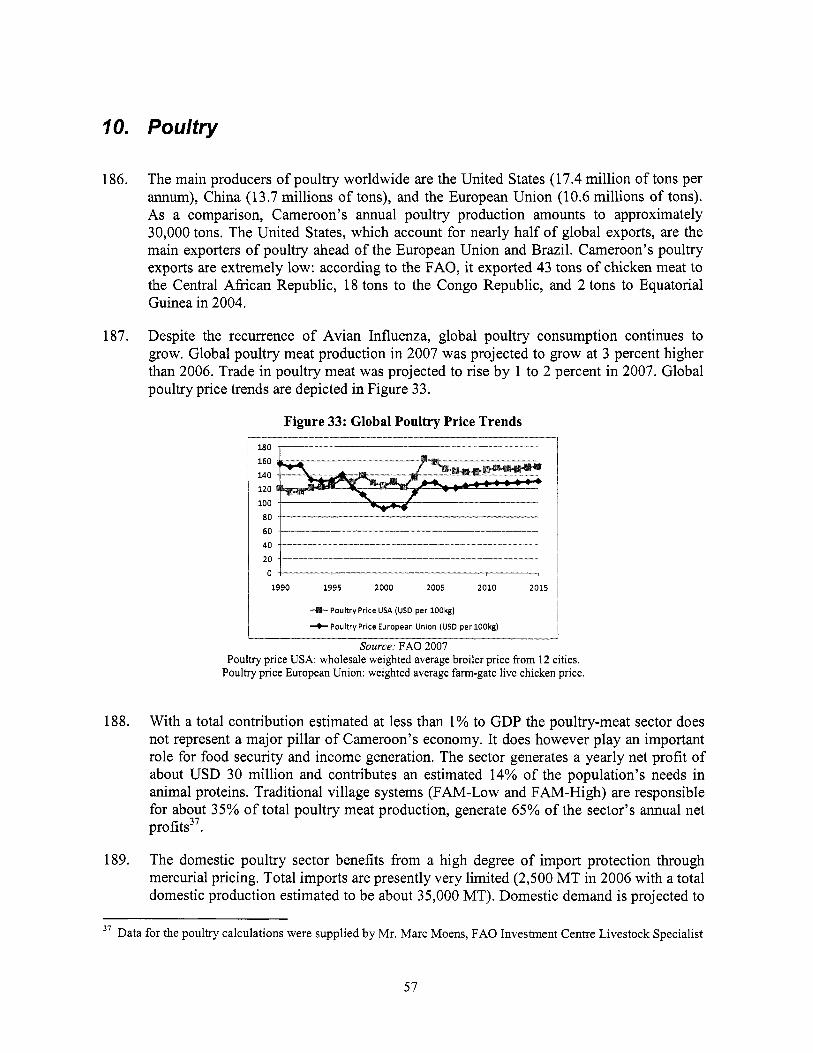

15.

Assembly

will also go a long way to unlock Cameroon's agricultural potential. A major bottleneck hampering access to markets by small producers i s the cost o f assembly. Farmers transport their produce themselves mainly using the informal roadside transport network. The approximate cost o f moving 1 M T o f agriculture produce 130km using the consolidated system work out to around 20% o f the total cost using the informal roadside network. This i s because o f savings o n each trader's round-trip fare, and use o f larger vehicles which provides savings on basic operating costs and lower per MT share o f tolls and excess road fees that have to be paid at official and unofficial roadblocks.

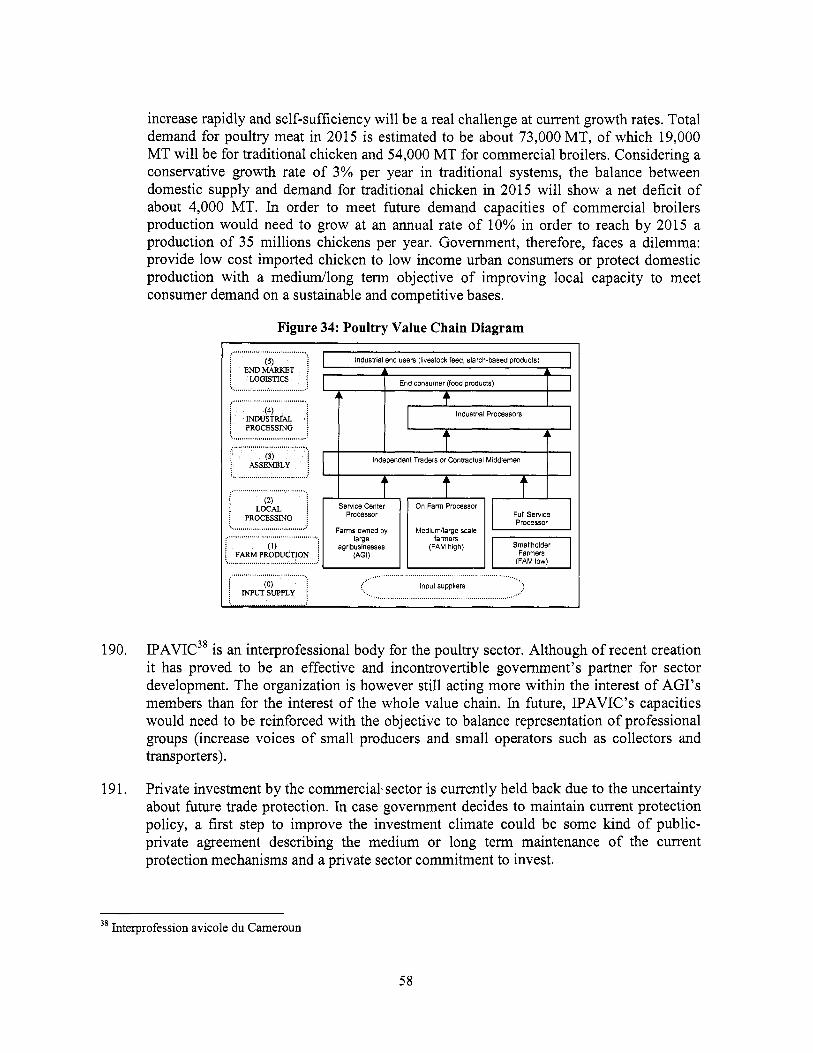

I) Interventions that increase the efficiency o f the assembly o f agricultural goods

Composition of Transport Costs Using the Roadside and Direct System

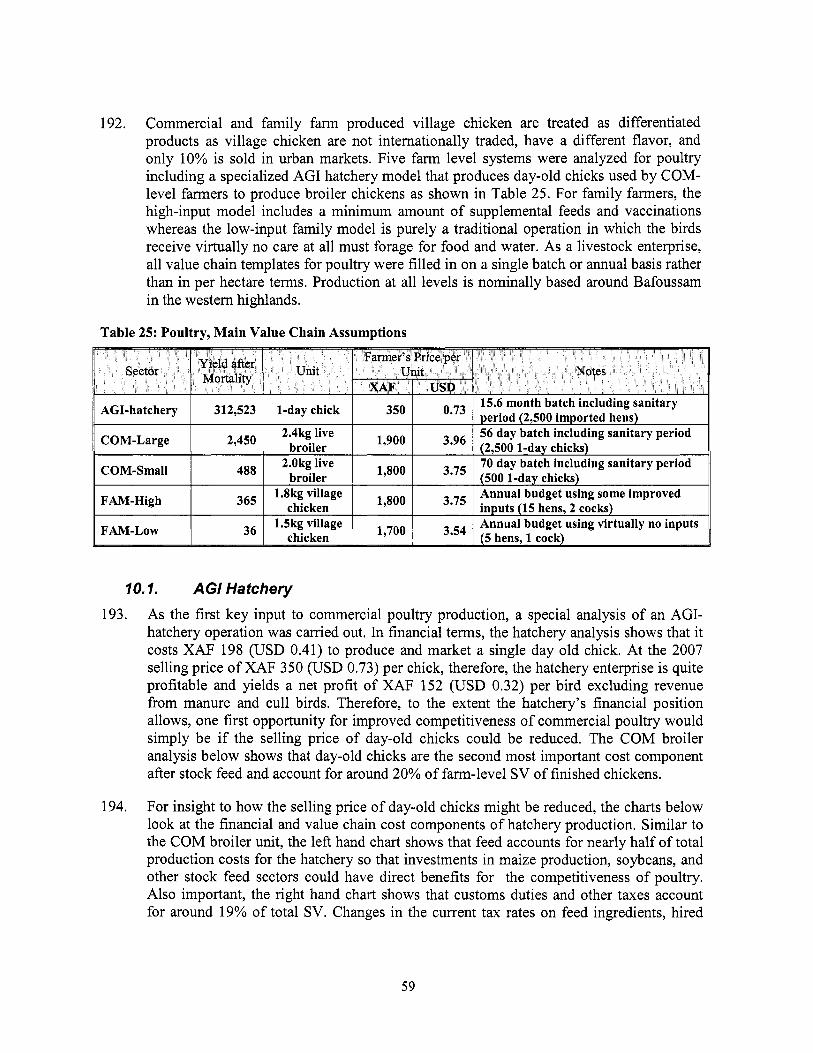

1 Assembly Costs over 130km (USD per MT) I

I Roadside Direct

rn Trader's fare

0 Driver's costs

0 Levies and fees

~

As an overall strategy to improve the competitiveness o f agriculture products there i s a clear imperative to support moves to a more consolidated version o f the road freight system. Bulking produce into relatively small consignments at the village level could provide important savings by avoiding the need for each farmer to pay their own fare. A necessary intervention would therefore facilitate better coordination among farmers and tighter linkages to traders. Possible actions would include capacity building o f farmers and could create linkages between commercial and family farmers.

An intervention to facilitate such a process could also benefit from ongoing efforts to increase the institutional and organizational capacities o f producer organizations in Cameroon'. Following a detailed participatory diagnosis o f existing producer organizations in Cameroon (65,000) a detailed data base on producer organizations with legal status (about 20,000 POs) has been put in place and provides a solid background for monitoring the sector.

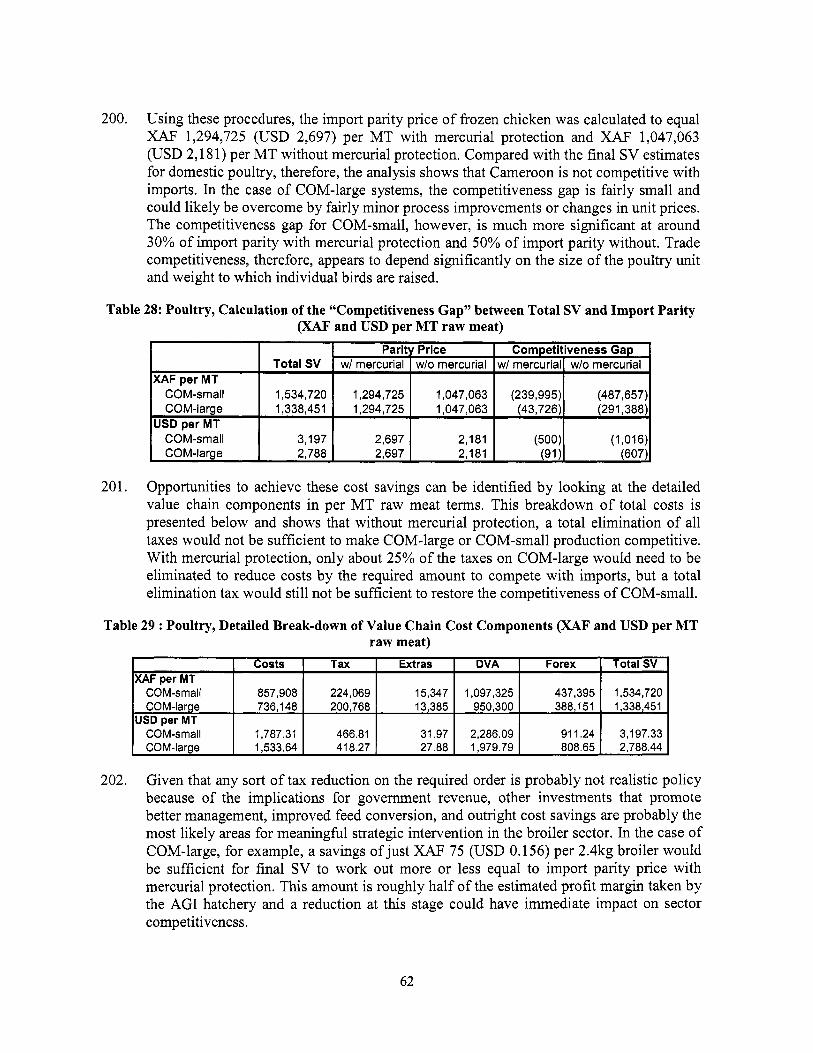

Undertaken by a French financed operation called "Professionalisation Agricole et Renforcement de CapacitCs- 1

P A R I "

xi i

16. The success of tighter horizontal and vertical value chain linkages depends on a transparent and secure trading environment which would allow producers and traders to compare prices and reduce transaction costs o f coordination and negotiation. Participants at the stakeholder feedback workshop specifically mentioned the lack o f trust and information as barriers to coordination. Bringing up to date price information to small farmers i s therefore an imperative for closer market linkages. Hence, a second area o f interventions would aim to increase farmer’s access to market information. For that purpose the potential o f institutional innovations l ike market and price information services via cell phone text messages could be explored. While experience from Ghana and Zambia shows that the private sector tends to be very successful in providing these services initial start-up support from the public sector may be necessary.

17. To firther reduce the cost o f assembly investments would be necessary to improve physical marketing infrastructure. Currently farmers complain about inadequate storage and processing facilities for maize, cassava and other crops. Such investments could therefore be an important area for public-private cooperation. Investments in wholesale markets are a further option to create a more transparent and secure trading environment which would allow producers and traders to compare prices and reduce transaction costs o f coordination and negotiation.

18. Any program to improve the competitiveness o f Cameroon’s agriculture would also need a component focusing o n rural roads linking producers to nearby markets and major transport routes. The poor state o f rural roads leads to high cost o f moving goods around Cameroon and represents a bottleneck to commercialization. I t i s recommended that such a component also reforms the current system o f official and unofficial road blocks and police controls, which pose a heavy burden on agricultural trade in Cameroon.

Commodity specific results

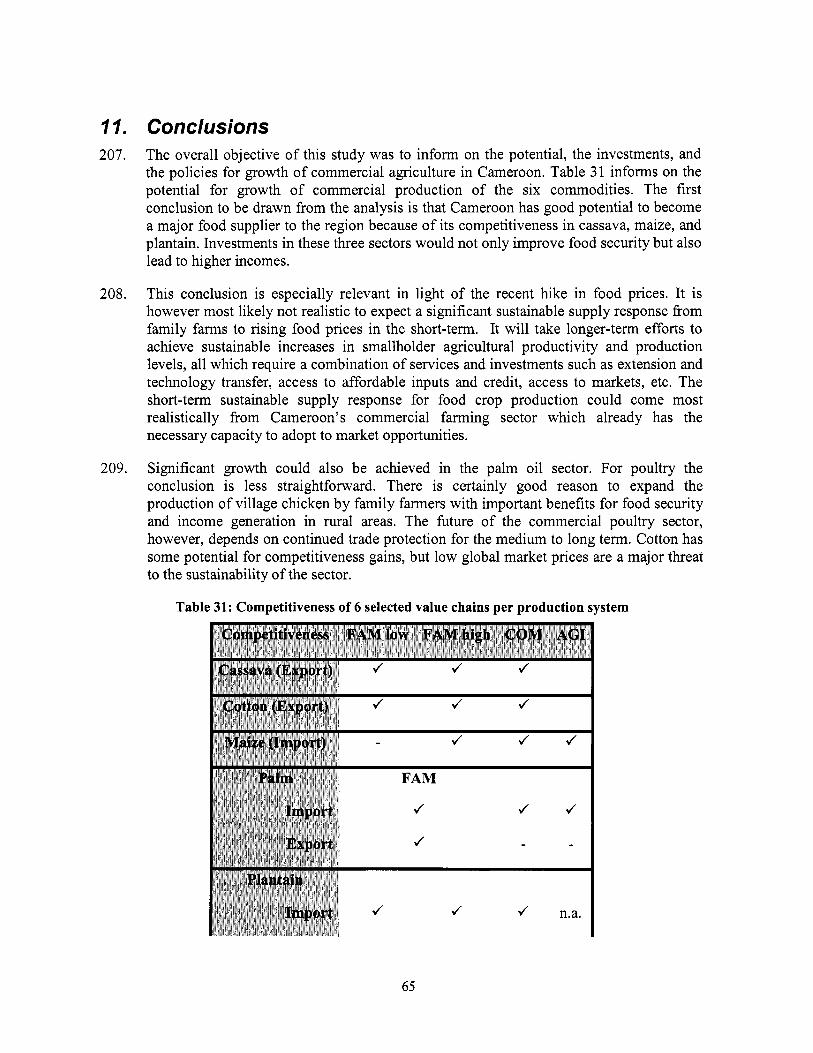

19. Cassava. The results for cassava products (fresh tubers, bobolo, and fufu) are encouraging. They show that Cameroon already enjoys a high degree o f competitiveness and i s well situated to grow in domestic and regional markets. There are opportunities to increase profitability o f family farmers through better soil management and increased use o f improved inputs such as new cultivars and fertilizer. At the higher management levels, per ton cost o f growing cassava decrease showing that farm investments are not only a route to improved incomes, but also enhanced trade competitiveness.

20. Assembly costs are a major bottleneck. Family farms mainly use the informal roadside trade network, whose chaotic nature and high cost o f transporting small quantities o f produce are a significant burden for primary producers. Because the roadside network is a much higher cost operation, the total value chain cost o f fresh cassava in the commercial value chain works out about 49% lower compared with family farm production distributed through the roadside network. If family farmers had access to a similar trade network, they too would enjoy a much stronger competitive advantage and could capture much more o f the total value available in the cassava chain.

... Xll l

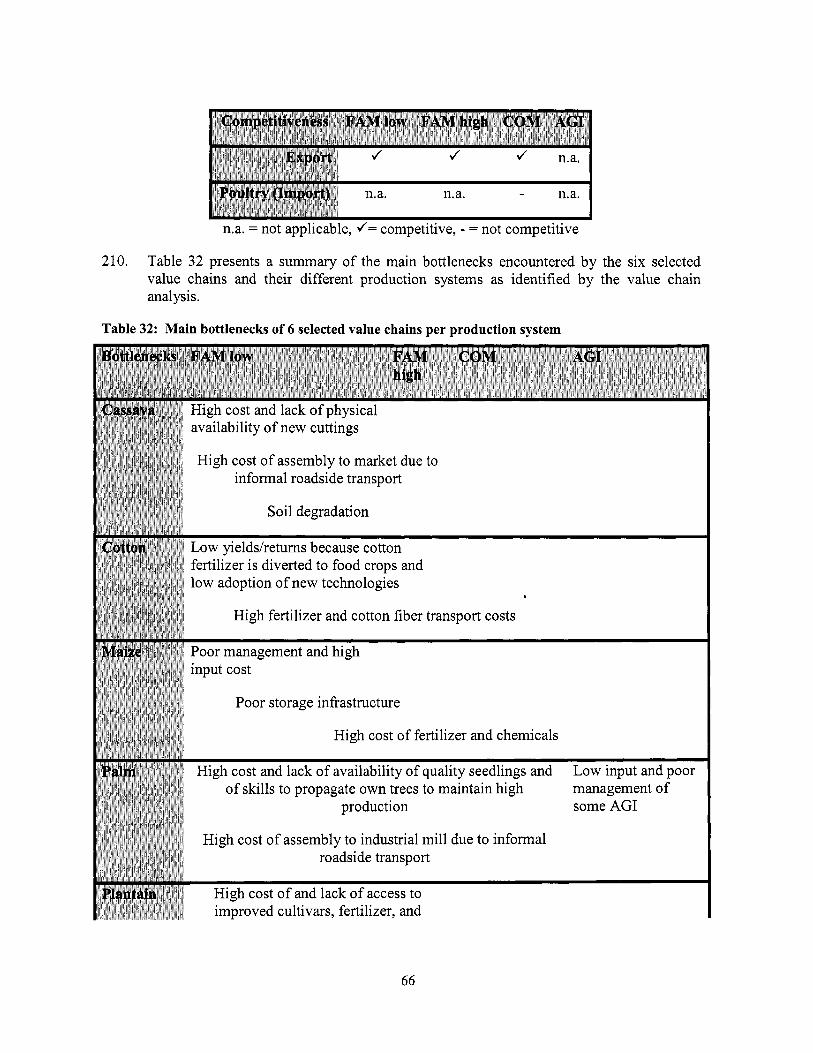

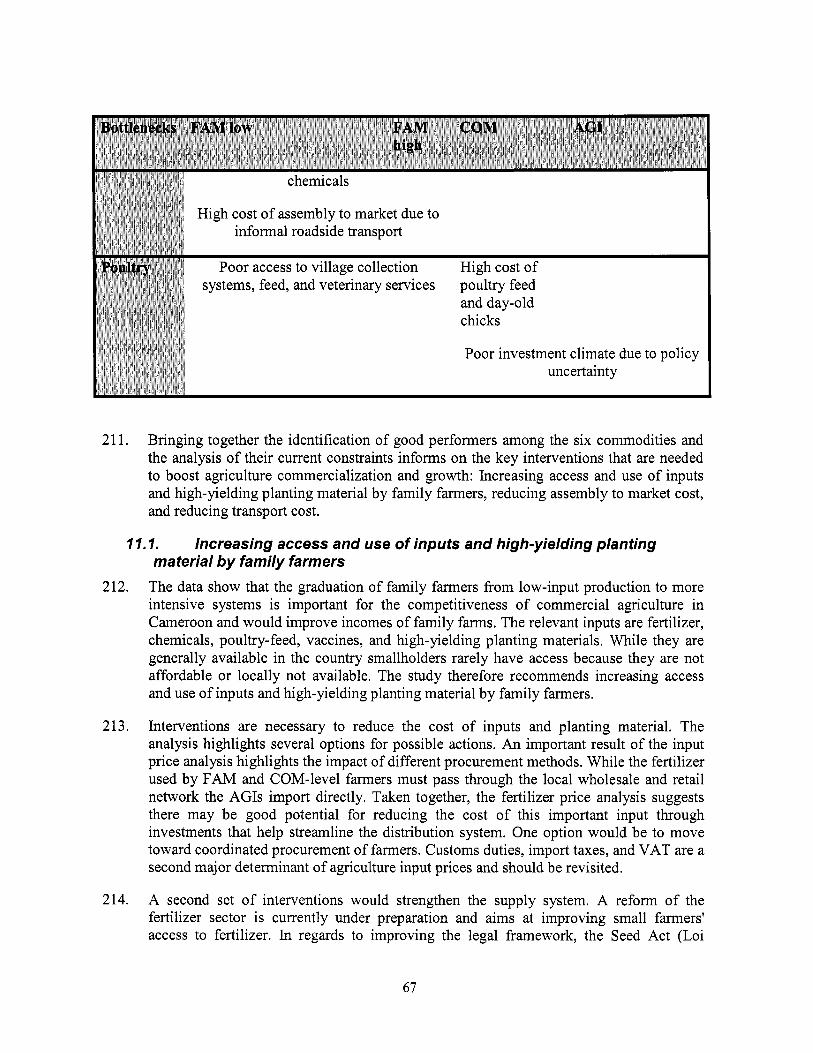

21 Cotton. The cotton sector operates in a very difficult international environment, characterized by decreasing prices and tough competition. The thin margin between total value chain costs and export parity prices i s an important concern for long-term sustainability o f the sector. There i s however some potential for competitiveness gains. I t appears that an important development strategy for Cameroon would be to help low-input farmers adopt improved technologies. In practice, this i s l ikely to come down to investments in farmer extension, input packages and pricing that rewards the use of inputs on cotton compared with diverting inputs to other crops. Beyond farm level improvements significant gains in competitiveness could also be achieved via reduced transport cost.

22. Maize. Family and commercial farmers producing maize at an improved level in Adamaoua and Northern Provinces are competitive with global imports as far south as YaoundC or even Douala. Because Cameroon i s not self-sufficient in grain, therefore, this result shows that investments in improved food production are not only strategically important for food security, but also make good business sense.

23. Similar to Cassava, investments to help family farmers improve from low-input production using recycled seed towards more intensive farming with modern inputs are important. The figure below illustrates the total cost o f maize production before assembly for the different production systems. Measures that would help these low-input farmers improve and achieve lower costs per MT would include improving access to better seed technology, development o f improved input supply systems for compound fertilizers and herbicides, and training in more effective use o f manure fertilizers.

Maize, Composition of total Farm Gate cost before assembly

Make, Total Costs (XAF per MT, farm gate) I 140,000

120.000

100,000

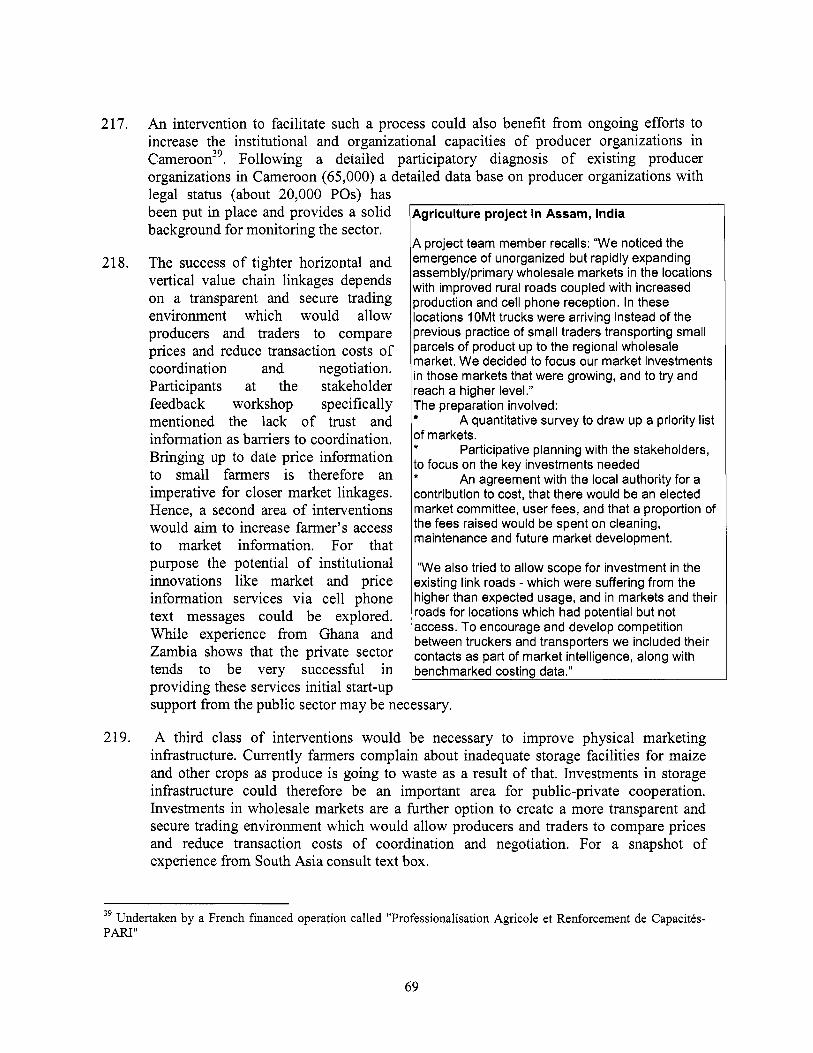

80,000

60,000

40,000

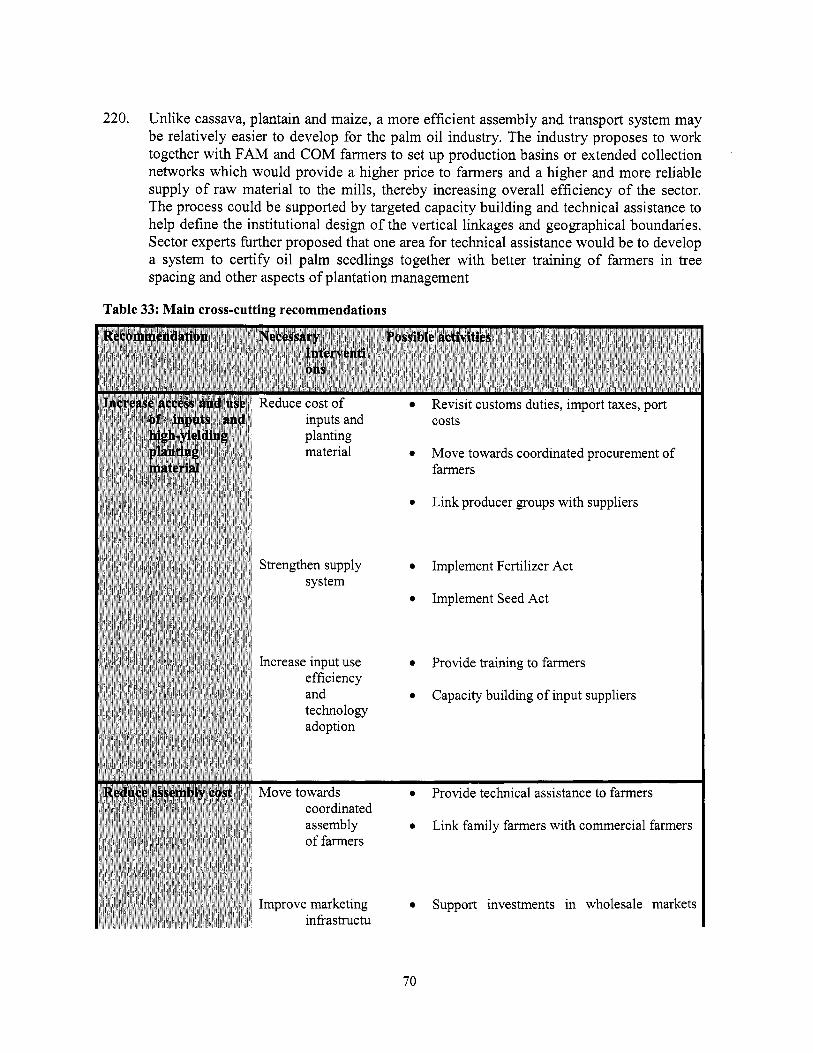

20,000

FAM-IOW FAM-hlgh COM

I.

0 I. I O

Total labor

Packing /delivery to factory

Animal hire / machineryO&M

Fertilizer & chem

Seed

DeDreciation.

24. With respect to the agribusiness sector and i t s production and marketing o f processed maize gr i ts used by the brewing industry, the analysis shows that a relatively minor change in tax or other process improvement could be enough to displace imported gr i ts as far south as Douala.

25. Palm oil. Cameroon i s highly competitive with imports o f palm o i l and enjoys a robust trade advantage measured by the gap between total value chain costs and import parity price. O n the export side, commercial farmers and agribusiness are not competitive at

xiv

global prices but the competitiveness gap i s quite small and could be overcome with the right type o f investment.

Plantain at Yield Per Ha Per MT Farm Gate (MTIHa) Costs Profit costs Profit

FAM-low 10.0 160,864 489,136 16,086 48,914 FAM-high 18.0 569,095 600,905 31,616 33,384 COM 25.0 959.642 665.358 38.386 26.614

26. By global standards, per hectare yields in Cameroon are low. Independent growers usually cannot access the right type o f material and/or lack specialized sk i l ls needed to propagate their own trees to maintain high production. One area for project intervention could be to develop a system to certify o i l palm seedlings together with better training o f independent farmers in tree spacing and other aspects o f plantation management

Rate of Return

3.04 1.06 0.69

27. Family and commercial farmers are much lower cost producers than agribusiness, but the method o f delivering the produce to the industrial mill i s quite often informal roadside transport and has a major bearing on total profits and returns. Unl ike cassava, plantain and maize, a more efficient assembly and transport system may be relatively easier to develop for the palm o i l industry. The industry proposes to work together with FAM and C O M farmers to set up production basins or extended collection networks which would provide a higher price to farmers and a higher and more reliable supply o f raw material to the mills, thereby increasing overall efficiency o f the sector. The process could be supported by targeted capacity building and technical assistance to help define the institutional design o f the vertical linkages and geographical boundaries.

28. Plantain. Cameroon i s highly competitive in plantain. Most marketed plantain i s sold domestically in urban centers. Small quantities are also exported to Gabon and Equatorial Guinea where demand i s high. Looking to the future, the Congo Republic and Chad also have excess demand and represent potential export markets for Cameroon.

29. Per hectare and per ton cost and profitability data for plantain at the farm gate are summarized below. As shown, good potential exists for significant improvement in per hectare profits from better management based on the use o f improved cultivars and fertilizer, but the cost o f achieving these improvements are extremely high. Although the rate o f return for FAM-high management i s s t i l l extremely good, an additional XAF 408,231 (USD 850) total spending i s required per hectare to achieve this level o f profitability.

30. The greatest area o f spending for family farmers wishing to move from low- to high-input management relate to crop establishment, fertilizer, and chemicals. Measures that help reduce these costs and/or simply increase the physical availability o f these inputs in the rural areas, therefore, could be the most effective way to facilitate better plantain management and help farmers realize the potential for increased incomes indicated above.

xv

3 1. Similar to the results for other commodities, the choice o f transport method has a major bearing on the final competitiveness results for plantain. Specifically, because FAM plantain i s easy to market, the savings from direct transport could be taken as additional profit. Indeed, because FAM plantain has a lower SV at the farm level than C O M production before transport, efforts to promote family farmer access to direct transport could be especially beneficial as a leverage point for increased income and trade competitiveness.

32. Poultry. The domestic poultry sector benefits from a high degree o f import protection through mercurial pricing. Domestic demand i s projected to increase rapidly and self- sufficiency wil l be a real challenge at current growth rates. Government, therefore, faces a dilemma: provide l o w cost imported chicken to l ow income urban consumers or protect domestic production with a med iud long term objective o f improving local capacity to meet consumer demand on a sustainable and competitive bases. Private investment by the commercial sector i s currently held back due to the uncertainty about future trade protection. I f government decides to maintain current protection policy, a f i rst step to improve the investment climate could be some kind o f public-private agreement describing the medium or long te rm maintenance o f the current protection mechanisms and a private sector commitment to invest.

33. Commercial and village chicken are treated as differentiated products as village chicken are not internationally traded, have a different flavor, and only 10% i s sold in urban markets. Commercial poultry production does not appear competitive in Cameroon and the thin edge that domestic producers sometimes enjoy depends entirely on trade protection. The competitiveness gap for large commercial producers i s relatively narrow and could be overcome through measures aiming at better management, improved feed conversion, and reduced costs mainly in poultry feed and day-old chicks. Availability o f feed i s a major bottleneck and backward linkages to the maize and soy sectors should be improved to ensure steady supply. Improving competitiveness and help small commercial producers transition to large commercial producers would therefore be among the main priorities.

34. For family farmers the story i s very different as traditional village chickens are very competitive and i t appears that investments in improved production and marketing could offer a good opportunity for increased rural incomes. The challenge in this case would be to develop new collection systems and provide training in the benefits o f routine vaccination, animal shelters, and small amounts o f supplemental feed. N e w distribution systems for feed and veterinary medicines would likely be required for farmers to access the required inputs for improved production.

xvi

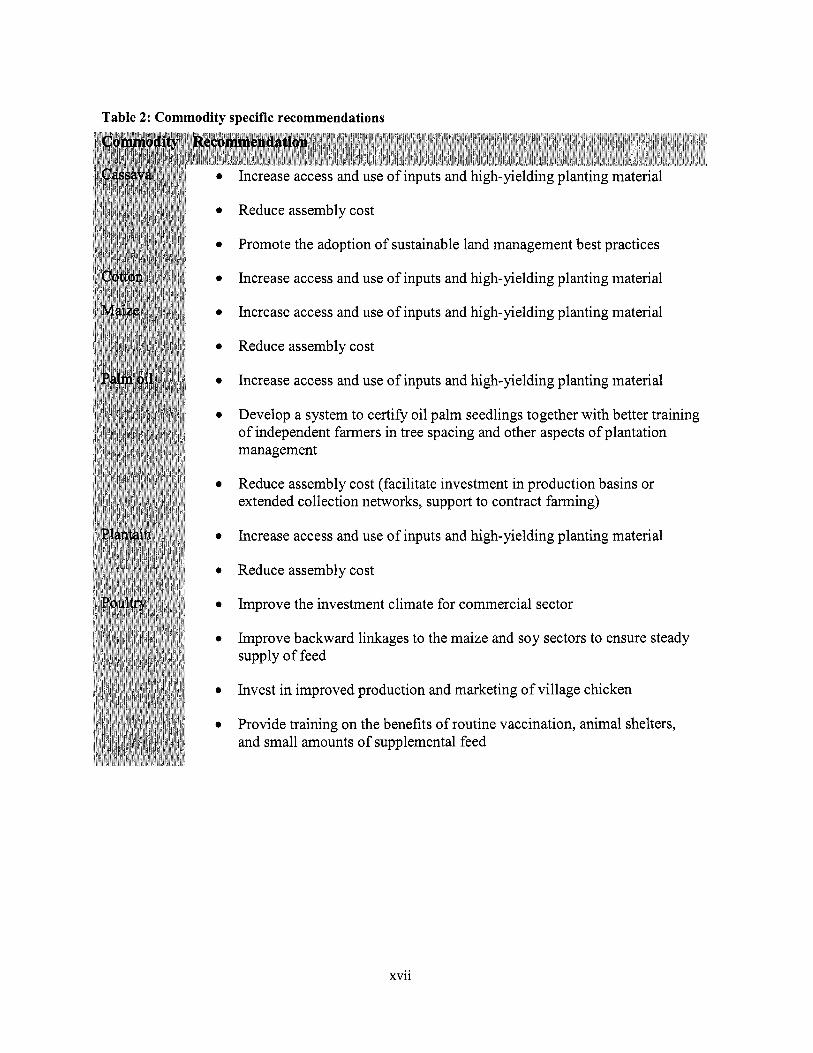

Table 2: Commodity specific recommendations

e

e

e

e

e

e

e

e

e

e

e

e

e

e

e

Increase access and use o f inputs and high-yielding planting material

Reduce assembly cost

Promote the adoption o f sustainable land management best practices

Increase access and use o f inputs and high-yielding planting material

Increase access and use o f inputs and high-yielding planting material

Reduce assembly cost

Increase access and use o f inputs and high-yielding planting material

Develop a system to certify o i l palm seedlings together with better training o f independent farmers in tree spacing and other aspects o f plantation management

Reduce assembly cost (facilitate investment in production basins or extended collection networks, support to contract farming)

Increase access and use o f inputs and high-yielding planting material

Reduce assembly cost

Improve the investment climate for commercial sector

Improve backward linkages to the maize and soy sectors to ensure steady supply o f feed

Invest in improved production and marketing o f village chicken

Provide training on the benefits o f routine vaccination, animal shelters, and small amounts o f supplemental feed

xvii

1. Introduction 1.1. Role of Agriculture in Cameroon

35. Agriculture contributes around 20% to GDP and i t s evolution i s critical for the economy in terms o f j ob creation, diversification, poverty reduction, overall growth and exports. Real GDP growth in Cameroon i s estimated at 2.9% for 2007. Economic growth remained weak because the adverse impact o f high o i l prices on the non-oil sector outweighed the positive impact on the o i l sector. Sti l l , the agriculture sector grew by 3.3% in 2007. The main products with positive volume growth in 2007 are cocoa (4.7

Figure 1 : Growth of Cameroon's Economy

Cameroon's Economy: Annual Growth Rates

percent), coffee (l%), rubber (6.9%), andpalm o i l (8.3%).

Source: World Development Indicators 2007

8

6 * E p n 2

0

Year

-+-Agriculture, mlue added (annual % growth) GDP growth (annua YO)

36. Food crops form the basis o f agricultural production, amounting to over two-thirds o f agricultural GDP. The livestock sub-sector stands at 12 percent o f agricultural GDP. Cash crops contribute to 8 percent o f the agriculture sector's GDP. Finally, the fishing and forestry sub-sectors each account for less than 6 percent o f agricultural GDP. Available statistics for food production, which are based o n broad estimates from field-based staff o f the Ministry o f Agriculture show that food production has increased by approximately 3 percent per year between 2005 and 2007.

37. Agriculture outstrips al l other sectors in Cameroon, including oil, in terms o f export revenues. Cocoa beans, cotton, coffee, and fresh bananas are the main agricultural commodities exported by Cameroon and together they accounted for 90 percent o f agricultural exports between 2000 and 2006 (see Figure 2). Furthermore, almost 60% o f the economically active population in Cameroon is employed by the rural sector and agriculture remains the predominant feature o f rural households: Around 50% o f the population lives in rural areas and fully 90% o f al l rural households are to some degree engaged in agriculture. O f these, approximately one third earn their living from export crops.

1

Figure 2: Agricultural Exports Composition (2000-2006)

[cocoa beans, 37.24%

Source: DEA. MINEFI

38. The most recent household survey shows that over 52% o f rural households are classified as poor compared to only 17% o f urban households. O f households specifically engaged in agriculture, 42% fall below the poverty l ine with the highest incidence o f poverty in the forest zone and high plateaw2 Agriculture also plays a pivotal role in domestic and household food security. According to the FAO, Cameroon produces 100% o f its leguminous requirements for human consumption, but falls short in cereals and imports over hal f a mi l l ion tons per year.

1.2. Global food and fertilizer prices 39. Rapidly rising international grain prices have fed into higher prices for staple foods,

leading to severe hardships for the poor in numerous areas, a cut in the standard o f living o f the urban middle class, and social unrest in C a m e r ~ o n . ~ International rice prices have gone up from $376 per ton in January 2008, to over $1000 in April. U.S. wheat export prices rose from $196 per ton in January 2007 to $371/ton in January 2008 to $440 per ton in March 20OfL4 The surge in the f i rs t quarter o f 2008 came on top o f an 88 percent increase in overall global food prices during the three prior years (see Figure 3). There are a number o f longer-term trends underlying these price rises suggesting that while the highest peaks may come down, staple grain prices are unlikely to recover in the foreseeable future their relatively l ow and stable levels that characterized the second hal f o f the 1980s until about two years ago.

MINADER (2006) 19.4% o f Cameroon’s consumption o f staples was imported from 2001 to 2005. World Bank, DECPG

3

2

Figure 3: Global food prices

Food prices (Nominal 8 Index, Jan 1995=100)

250 I

50 ............................................................. I

40. Increased consumer demand due to rising incomes in many parts o f the developing world has steadily increased demand over the past two or three decades for more convenient and value-added food products, including grain-based livestock products. More recently, increased demand for the raw materials that go into bio-fbels, such as sugarcane, maize, soybean, and palm oil, have led to increased competition for cropland, and have contributed to increased demand for grain. Fuel and fertilizer prices have also risen sharply due to rising o i l prices, which has increased agricultural costs. The surge in fertilizer prices since January 2007, shown in Figure 4, i s o f particular concern with respect to i t s likely discouragement o f smallholder farmers who supply the brunt o f the food in Cameroon.

I

Figure 4: Global fertilizer prices Fertilizer Prices (FOB Bulk), January 2000 - April 2008

1400

1100

1000

1 0

Y 400 1 0 I/; - - ,

AprllwoII -.+

DAP, U.S. 0"lf 3

Source: International Center for Soil Fertility and Agricultural Development (IFDC)

i

41. Governments can respond to the hike in prices through short, medium, and long-term measures. Policy interventions can be divided into three broad classes: (i) interventions to ensure household food security by strengthening targeted safety nets; (ii) interventions to lower domestic food prices through short-run trade policy measures or administrative action, and (iii) interventions to enhance longer-term food supply. The investment and

3

policy recommendations following from this report for food crops belong to the third class o f interventions.

7.3. Study Objectives 42. Given the Government’s expressed priority o f poverty r e d u c t i ~ n , ~ agriculture clearly has

a central role in the country’s economic growth and poverty reduction strategies. Despite the recent peak in o i l prices, o i l production in the country has been on the decline for some years. The recent Interim Strategy Note (ISN) for Cameroon therefore indicates that “the mobilization o f non-oil revenues wil l be essential” to the resource strategy for Cameroon. For poverty alleviation, growth, and food security, therefore, agriculture is- and wil l continue to be-of significant importance to the country’s development goals.

43. Accordingly, the Government’s Rural Sector Development Strategy (RSDS), recently released in the context o f its Poverty Reduction Strategy Paper (PRSP), specifically targets four key challenges: (i) the reduction o f poverty; (ii) food security and self- sufficiency; (iii) sustainable natural resource management; and (iv) greater participation in regional and international trade. These challenges have given rise to five priority pol icy objectives for the Government’s rural sector strategy and seven strategic objectives to help achieve these (Figure 5).

Figure 5 : Cameroon’s Rural Sector Strategy Objecdves

Ensure food security and

self-sufficiency

Source: MINADER (2006)

1 Five (5) Rura l Sector Policv Obiectives I ~ ~~ ~ ~~ ~

economic growth, rev en u e s standards o f rural and management employment and populations o f natural

export resources development

Seven (7) Rura l Sector Strategic Obiectives

(i)

(ii) Sustainably manage natural resources (iii) Promote local and community development (iv) Develop appropriate access to finance (v) Promote employment and training for

agricultural professionals (vi) Manage food security risks (vii’l Immove the institutional framework

Sustainably develop agricultural and food production and supply;

See Cameroon’s Poverty Reduction Strategy Paper (2003) The RSDS has multiple contributors and stakeholders, including MINADER (Ministry o f Agriculture and Rural

Development), IRAD (Institution de Recherche Agronomique et du Dkveloppement), M I N R E S I (Ministry o f Scientific Research and Innovation), M I N E P I A (Ministry o f Livestock, Fisheries and An ima l Industries), and donor partners.

4

44.

45 *

46.

Overall, the agriculture strategy o f Government-and i t s donor par tnersdal ls for a more ‘pragmatic approach’ in achieving the country’s development objectives. This, in turn, demands better information about where interventions can have the most impact and which ones hold the most potential for meeting the ambitious objectives for agriculture development in Cameroon.

This study aims to assist in the realization o f the Government’s rural sector objectives through the specific avenue o f improved commercial agricultural competitiveness. I t explores the concrete constraints and potential for domestic, regional, and/or international competitiveness o f six agricultural value chains that involve family, commercial, and large agro-industrial enterprises in different regions o f Cameroon.

The overall objective o f the study i s to inform on the potential, the investments and the policies for growth o f commercial agriculture in Cameroon in ways that:

(a) achieve broad-based poverty reduction;

(b) increase exports; and

(c) contribute to food security.

47.

48.

49 9

50.

The immediate objective o f the competitiveness study i s to identify products and farm systems that are currently competitive or have the potential o f becoming competitive in domestic, regional, or global markets. More specifically, the Government has asked the Bank to provide support for i t s growing agricultural program. This Economic and Sector Work is therefore expected to inform the preparation o f a new lending operation for the agricultural sector in Cameroon.

By looking at detailed price build-up from stage to stage o f agriculture value chains, the study specifically helps identify key bottlenecks and changes that need to take place to realize competitiveness potential. As Cameroon mainly has influence over prices within i t s own borders, the methodology i s particularly interested in the composition o f domestic costs. If some cost accounts for a large share o f total value, or i s significantly higher than an equivalent international benchmark, then new policies or investments focused on reducing that cost would likely be an effective strategy for enhanced competitiveness.

In addition, the concept note had envisioned to explore possible social and environmental impacts o f any commercialization development. However, due to budget and time constraints it was not possible to analyze these aspects. Similarly, the potential o f niche markets o f the selected commodities had been identified as an important question in the concept note, but due to resource constraints this question could not be pursued further.

This report i s organized into 11 chapters. The next chapter describes the context of Cameroon’s Agricultural Sector. The third chapter gives an introduction to the methodology o f quantitative value chain analysis. Chapters 4 to 10 are dedicated to inputs and the six commodities Cassava, Cotton, Maize, Palm, Plantain, and Poultry. The eleventh chapter concludes offering some reflections on pol icy and investment recommendations. Detailed data tables and price assumptions, maps, and minutes o f the stakeholder feedback workshop are given in appendices 1 , 2, and 3.

5

2. Context

Agro-ecological zones Sudano-Sahelian High Guinea Savanna Western Highlands Monomodal Humid Forest Zone

Bimodal Humid Forest Zone

5 1. The context o f this study i s described along 4 dimensions: (i) geography, (ii) commodity coverage, (iii) production systems, and (iv) agricultural institutions. This chapter describes these dimensions and explains how they influenced the design and recommendations o f the quantitative value chain analysis.

Crops Cotton, millet-sorghum, cowpea, onion and sesame Maize, cotton, millet-sorghum, yam, potatoes Cocoa, coffee, maize, beans, potatoes, poultry market vegetables Cocoa, bananas, plantain, cassava, coffee, pa lm oil, poultry, rubber, ginger, pepper. Cocoa, plantain, cassava, coffee, maize, pa lm oil, pineapple.

2.1. Geography 52. Cameroon has one o f the most diversified agro-ecological environments in Sub-Saharan

Aiiica. It stretches from the semi-arid Sudano-Sahelian area in the far north and highlands in the north-west, to humid forests in the central, southern, and eastern regions. Table 3 presents Cameroon’s main ago-ecological regions and their predominant types o f crops. A map o f agro-ecological zones i s presented in the appendix.

Table 3 : Agro-ecological Zones and Agricultural Activities in Cameroon

Source: World Bank, 2003

53. In order to address this diversity, the value chain analysis takes place in one specific zone or region for each commodity, dependent upon i t s potential and importance to that region. So, for example, cotton, while also grown in the Guinea Savannas, i s particularly important to income and poverty in the north o f the country. The value chain analysis for cotton therefore takes place in the Sudano-Sahalian zone o f the North. That way the study distributes the value chain analyses across zones according to strategic importance o f selected commodities in the different regions o f the country.

2.2. Commodity Coverage 54. The most recent Rural Sector Review (RSR)’ for Cameroon identifies a number o f

commodities as important, either for current employment, for food security or for potential competitiveness in domestic, regional and export markets. The RSDS also cites a similar set o f ‘strategic’ crops that have a role to play in realizing their objectives for the rural sector. The study therefore builds on past diagnostic work in Cameroon to select 6 key commodities from among those identified as strategic or high potential. Namely: maize, plantain, cotton, cassava, palm o i l and poultry. These commodities are chosen either for their importance to a particular region or for their potential contribution to poverty reduction, export development and/or food security.

’ World Bank (2003)

6

55.

56.

57.

58.

59.

Grains, for example, account for h l l y one third o f caloric requirements and are therefore important to food security. In Cameroon, maize single-handedly provides around 20% o f the country’s caloric and protein requirements, Cameroon, however, i s only 70% self- sufficient in grain production and imports are required to cover the gap. In addition to food security objectives, the Government has articulated important export objectives for grains, envisioning a ten-fold increase in export volumes from 2001 to 2015.*

Plantain and Cassava are considered strategic commodities for food security in Cameroon. Together they provide 21% o f the country’s caloric requirements and 27% o f i t s protein. Cameroon is currently self-sufficient in the production o f plantain and cassava, and has strong potential for regional export. Indeed, since the early 1990s’ plantain exports to neighboring Gabon and Equatorial Guinea have grown over 500%.9 Furthermore, plantain and cassava are primarily smallholder crops, important for employment and poverty reduction through, for example, contractual arrangements with larger-scale distributors. Both have important gender elements, given that primary processing and cross-border transport (to Gabon and Equatorial Guinea) i s dominated by women.

Cotton i s one o f six agricultural commodities” that account for the lions’ share o f Cameroon’s export revenues. Produced primarily in the Sudano-Sahalian and High Guinea Savannas o f the northern part o f the country, the production o f cotton i s an important source o f income for the relatively poorer Northern provinces. Together with coffee and cocoa, the production o f cotton provides revenue for over a third o f the agricultural population nationwide due to i t s domination by smallholder production. Cotton therefore represents a value chain wi th important potential impacts on poverty reduction, as well as export development.

As the third biggest producer ofpa lm oil in Africa, Cameroon assigns a strong role to this tree crop in the country’s strategy for achieving economic growth, employment and export development. In addition to its place in the nation’s export and growth strategy, palm o i l i s a basic food commodity in which Cameroon i s not currently self-sufficient. In terms o f poverty reduction and employment, l ike most tree crops, palm o i l holds strong potential for smallholder cultivation. While smallholders already represent some 40% o f plantation acreage (and over a quarter o f national production), the potential for further growth and employment i s strong, given that the capacity for surface extension o f the larger agro-industrial model is limited.

Poultry, for both meat and eggs, has important employment and rural income implications, particularly in the West and the relatively poorer Northern provinces. Traditional smallholder poultry farming makes up 70% o f the nation’s poultry population. Traditional production co-exists with medium scale semi-intensive and larger industrial production, mainly centered on the nation’s cities. In terms o f food, poultry provides over a quarter o f the country’s meat consumption (second to beef, which

* MINADER (2006), p. 14

lo With cocoa, coffee, banana, pa lm oi l and rubber CIRAD (2006)

7

accounts for 50%). Given i t s importance for employment and potential in providing good opportunities for linkages both upstream (e.g. feed) and downstream (e.g. packaging), exploring the competitiveness o f Cameroon’s poultry chain can contribute importantly to the government’s manifold objectives for the rural sector, as well as fostering urban linkages.

2.3. Production systems 60. A variety o f production systems co-exist in Cameroon. Broadly speaking, these can be

classified as smallholder farming, mediudlarge-scale farming and ago-industry. ’’ Smallholder farming covers a broad spectrum o f farm models, including traditional agriculture systems, improved rain-fed cultivation, intensive irrigated agricultural systems, pastoralism, and agro-pastrolism. There are over 1 mi l l ion smallholder production units in Cameroon, producing a wide variety o f grains and other foodstuffs, as wel l as dominating poultry production in Cameroon.

61. Mediudlarge scale farming i s usually mono-cultural and has some degree o f integration with downscale agri-business. They tend to be run as agricultural enterprises, by professional managers or skilled producers, sometimes employing wage labor. They have better access to finance and land than smallholders and may use higher degrees o f mechanization and inputs.

62. The final category o f farm system i s the ago-industrial production system. There are only 20 or so in existence in Cameroon and they represent large, plantation-style production, primarily in export crops and livestock. They use wage labor and depend heavily on agricultural inputs. They are a m i x o f private and public enterprises, with the rate o f privatization accelerating in recent years.

63. Taking into account this diversity the analysis i s based around a continuum o f indicative production possibilities. At the farm level, the spectrum begins with very low-input family farmers (FAM-low) and extends to cover improved smallholder management systems (FAM-high), larger-scale and even more advanced commercial (COM) production systems, and finally very large-scale agri-industrial (AGI) enterprises. In al l cases, i t was decided to cover at least two levels o f FAM management to illustrate potential food security and income benefits Cameroon could receive from investing in improved farm management. Some defining characteristics o f this spectrum are illustrated below.

l1 World Bank (2003)

8

Figure 6: Continuum of Production Systems .

* With cotton and maize, the FAM-high and COM variations are based on hired and own animal traction respectively.

2.4. Agriculture Institutions 64. Institutions and policies supporting agriculture in Cameroon have undergone substantial

changes since the economic crisis and subsequent reforms o f the 1990s. The general trend has been towards greater liberalization and privatization o f these activities. This section describes those institutions and actors which are relevant for the subsequent analysis.

Research and Extension

65. The National Program for Agricultural Extension and Research (PNVRA), adopted in 1998, spearheads Cameroon’s agricultural knowledge and information system. l2 The P N V R A was designed to develop agricultural research and revitalize agricultural extension services by (i) strengthening technical, operational, and financial capacities, (ii) improving the effectiveness o f rural information support services, and (iii) accelerating the development and transfer o f technologies. (See text box for a description o f a joint IDA, Government, IFAD, AfDB intervention to support the PNVR.)

~ ~ _ _ _ _ _

l2 The PNVRA took over the National Program for Agricultural Extension and Training (PNFVA - Programme National de Formation et de Vulgarisation Agricole), which had been set up as a pilot program in 1988.

9

66

As a follow-on intervention to the National Project for Agricultural Extension (PNVA), the National Agricultural Extension and Research Program Support Project (PNVRA) undertook to finance - I D A j o i n t l y with Government, IFAD and ADB- the implementation o f the national agricultural extension policy and agricultural research in the entire country f rom 1999 to 2004. The development objective o f the National Agricultural Extension and Research Program Support Project was to contribute to improving agricultural productivity and incomes in Cameroon in a sustainable way. The outcome o f the overall project towards which the IDA Credit contributed was satisfactory, largely because most o f the expected results at the end were reached or exceeded, in some cases substantially. The components which supported agriculture extension and producer organizations provide interesting lessons learnt:

The original tasks of the Producer Organizations Component were to support the efforts o f the farmer-organization and private sector specialists (SOASPs) to develop formal and informal contacts between producer groups and associations o n the one hand, and private sector suppliers o f agricultural inputs and crop processing equipment, traders, and industrial purchasers o f agricultural products on the other hand. At mid-term, a pi lot activity covering provision o f small equipment and productive infrastructure grants for producer organizations (POs) was introduced. The new approach introduced in 2002 for promoting producer organizations through “micro projects” created a lo t o f enthusiasm among the producers. One reason for this enthusiasm could have been that the approach implied that there would be grant funds available to implement some of the priorities identified by the farmers.

The objectives of the Agricultural Extension Component were to continue supporting a country- wide extension system, to increase the number o f farmers in contact with the extension service f rom 15 percent to 30 percent o f a l l the farm families in Cameroon by the year 2002, to have 1,690 agricultural extension agents (Agent de Vulgarisation de Zone--A VZ) in post, with 200 o f them being women, and to increase the overall adoption rates o f technical messages in contact groups from 40 to 62 percent. At midterm the project activities were reoriented so that the agricultural extension agents became more l ike rural development facilitators in assisting POs in planning and implementation o f their “micro projects”, consisting o f activity plans for productive small infrastructure and equipment, and the delivery o f related agricultural extension advisory services as requested by farmers. The reorientation o f the farmer support f rom a mass-extension system, to a more targeted and comprehensive approach o f advisory assistance to registered producer groups init ially reduced the number o f benefiting families, because the producer groups, with their multitude o f needs, require more o f the support agent’s time. I t also may seem contradictory to the Government’s goal and obligation to look after a l l the rural population. However, under a tight budget constraint the new approach appears to offer a way o f making people and their organizations take over rural development efforts in phases (the groups assisted f irst will “graduate” to develop their members’ economies without the Government’s assistance, at which time the available funds can be transferred to the second set o f producer groups, etc.).

Wor ld Bank (2004)

Relevant ministries such as the Min is t ry o f Agriculture (MINAGRI) or the Ministry o f Livestock, Fisheries, and An imal Industries (MINEPIA) coordinate their actions through the PNVRA. Currently, extension services are also delivered by regional institutions such as the North-West Province Development Author i ty (MIDENO) or the South-West

10

Development Authority (SOWEDA) as wel l as by parastatal enterprises (e.g. S ODECOTON).

67. The Institute o f Agricultural Research for Development (RAD) i s virtually the only organization undertaking varietal selection in Cameroon. I t also produces pre-foundation and foundation seeds for maize, millet, sorghum, rice, cowpeas, groundnuts, tubers, roots, cotton, fruit trees, and palm oil.

Private sector and marketing

68. Following the shutdown in 1990 o f the Seedlings and Foodstuff Development Authority (MIDEVIV) and the National Rural Development Fund (FONADER), which was responsible for the import and distribution o f subsidized fertilizers, the private sector has invested in the marketing o f inputs. I t i s however only partially successful in supplying farmers with affordable quality inputs.

69. Small and medium-scale enterprises have invested in the production and marketing o f improved seed varieties. Farmers, however, complain about the insufficient supply o f seeds as well as about the poor quality o f seeds sold on the market despite high prices, and the misuse o f “Certified Seed” labels. The government hence promulgated a Seed Act (Loi Semenciire) in 2001 to improve regulation o f the market. Implementing decrees (dkcrets d ’application), which are necessary for any Act to be enforced have however not yet been issued.

70. Currently two private importers supply over 90percent o f the fertilizer market. The product must pass through the local wholesale and retail network until it reaches the farmers. Prices o f fertilizer are very high. Quality issues have also arisen. A reform o f the fertilizer sector i s being undertaken since 1994 with USAID support under the so called “Programme de Refonnes du Sous Secteur Engrais-PRSSE” to facilitate importation and marketing o f fertilizers. A follow-up program i s currently under preparation with the South African Merchant Bank and aiming at improving small farmers’ access to fertilizers.

71. Prior to the liberalization o f the agriculture sector, the MIDEVIV was directly involved in the distribution and trade o f foodstuffs on the domestic market, purchasing and collecting agricultural produce from farmers before transporting i t for sale to local markets. The National Produce Marketing Board (NPMB) played a similar role to the MIDEVIV, for agricultural exports. Both organizations were liquidated in the early 1990s and commercialization o f agricultural output was liberalized. Until now the private sector has not been able to fully fill the vacuum lef t by these two institutions and the linkages between producers and output markets are generally weak.

Producer organizations

72. In 1990, government reformed the legal framework o f associations and cooperatives and put in place legal measures including a new law, “the freedom o f association act”. Several institution building measures were also put in place, e.g. the Projet d’appui aux stratkgies paysannes et ri la professionalisation de 1 ’agriculture (ASPPA), and the

11

Cellule de promotion de I 'organisation professionnelle agricole (PROMOPA), an organization with a specific mandate to promote professionalism among smallholder producers. An early outcome o f these measures was the emergence o f large numbers o f grassroots and umbrella organizations, with a wide range o f business activities, and broad geographical coverage at the village, district, department, province or national level. Many POs came from informal ethnic or village-based support systems. Sometimes local leaders seek to position themselves strategically in order to benefit from newly created opportunities in the development assistance business.

73. Most POs are perceived by their members as an instrument to respond to organizational and representational problems. In particular, members see the PO as an interface between them and institutional support arrangements, local governments, private sector, other national organizations (churches, NGOs) and external organizations (donors, NGOs, churches, etc.); they expect PO to act as intermediaries between them and markets; they perceive PO as consensus building structures, relaying requests from producers in the areas o f training, information and technological innovation, organizational support and management. They also expect PO to play important roles in the promotion o f savings, and financing instruments o f micro-projects, for instance as guarantors o f contracted credits, as well as assisting in the recovery o f debt from their members.

Cooperating partners

74. AFD financed an operation called "Professionalisation Agricole et Renforcement de CapacitCs-PARI" which strengthened the institutional and organizational capacities o f producer organizations in Cameroon. The project was launched in 2004 and i s planned to be closed in December 2008. Ma in outputs o f the project include the following: (i) setting up o f a comprehensive institutional and organizational framework for producers at the provincial as well as at the national levels, following a detailed participatory diagnosis o f existing producer organizations al l over the country (65,000), (ii) setting up o f a consultative platform "Cadre Paritaire de Concertation", in each o f the ten provinces, and (iii) putting in place a detailed data base on producer organizations with legal status (about 20,000 POs).

75. Continued support i s expected to be provided under the C2D (Bilateral French HIPC funds) which wil l include three operations: (i) Improving the Competitiveness o f small agropastoral farms; (ii) Reviving the agricultural and livestock professional training centers, and (iii) Strengthening the statistical and Monitoring and Evaluation capacities o f concerned line Ministries (the Ministry o f Agriculture and the Ministry o f Livestock).

76. The EU implemented value chain analyses: (i) Coffee; (ii) Cocoa, and (iii) milk. The analysis for (i) and (ii) i s being completed, while (iii) i s largely initiated. In total, nine commodities are being analyzed. The EU i s also financing the EU-A11 ACP Agricultural Commodities Programme (AAACP). The objective o f this € 45 mi l l ion program i s to strengthen stakeholders' capacities in selected ACP countries to develop and implement sustainable commodity strategies, with a view at improving producers' livelihood and incomes, and to reducing vulnerability at both producer and macro levels. 1/3 o f the

12