renewable energy regulation in spain - … · renewable energy regulation in spain fernando marti...

TRANSCRIPT

RENEWABLE ENERGY REGULATION

IN SPAIN

Fernando Marti Scharfhausen

Vice ChairmanFebruary 2010

1

Vice Chairman

NATIONAL ENERGY COMMISSION

Solar Heat Map

2

Ref.: Plan de Energías Renovables en España 2005-2010. Solar Heat for Industrial Applications, AEE INTEC - Institute for Sustainable Technologies. Junio 2006

Regulation is the key factor

3

Spanish capacit installed

CAPACITY INSTALLED DIC 2008: 95.648 MW =

Spanish capacity installed

CAPACITY INSTALLED DIC 2008: 95.648 MW = 66. 448 MW OS + 29.200 MWSS

Potencia Instalada en España (MW) Diciembre 200824.000

16.658

23.054

15.946

Potencia Instalada en España (MW). Diciembre 2008

7.716

11.869

7.1516.123

0

6.123

1.970

5.161

4Fuente: REE SPECIAL SYSTEMORDINARY SYSTEM

Capacit installed Special S stemCapacity installed: Special System

29.200

35.000

Evolución de la potencia instalada en el régimen especial en España. (Diciembre_2008)

17.48019.248

21.529

24.738

29.200

20.000

25.000

30.000

W

Mini Hydro

PV -CSP

1 407 1 582 2 151 2.606 3.098 3.923 4.5446.271

7.8059.266

11.26613.381

14.980

5 000

10.000

15.000MW

Wind

1.042 1.407 1.582 2.151 606

0

5.000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Cogeneración Eólica Hidráulica Residuos

CHP

Cogeneración Eólica Hidráulica Residuos

Biomasa Trat.Residuos Solar Total

Capacit installed Special S stemCapacity installed: Special System

29 36735.000

Evolución de la potencia instalada en el régimen especial en España. (Junio_2009)

17.48019.248

21.529

24.738

29.200 29.367

20.000

25.000

30.000

W

Mini Hydro

PV -CSP

1 407 1 582 2 151 2.606 3.098 3.923 4.5446.271

7.8059.266

11.26613.381

14.980

5 000

10.000

15.000MW

Wind

1.042 1.407 1.582 2.151

0

5.000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Cogeneración Eólica Hidráulica Residuos

CHP

Cogeneración Eólica Hidráulica Residuos

Biomasa Trat.Residuos "Solar" Total

N mber of installations Special S stemNumber of installations; Special System

53.59360.000

Evolución del numero de instalaciones en régimen especial en España. (Diciembre_2008)

22.69730.000

40.000

50.000

MW

1.342 1.553 1.777 2.079 2.805 3.692 5.492 7.72012.263

22.697

0

10.000

20.000

M

PV

01998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

SOLAR EÓLICA HIDRÁULICA COGENERACIÓN

RESIDUOS TRAT RESIDUOS Total general

7

RESIDUOS TRAT.RESIDUOS Total general

N mber of PV installationsNumber of PV installations

INSTALACIONES FOTOVOLTAICAS

40 000

45.000

50.000

55.000

25.000

30.000

35.000

40.000

5.000

10.000

15.000

20.000

01998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Capacit PV installed

E l ió i t l d l t i i t l d E i

Capacity PV installed

3.4374.000

Evolución e incremento anual de la potencia instalada en Energia Solar. Diciembre_2008

2.500

3.000

3.500

6981.000

1.500

2.000

MW

1 1 1 1 1 2 2 4 8 12 23 48 147

0

500

9SOLAR Incremento sobre el año anterior Total

Share of prod ction of Special S stemShare of production of Special System

28%30%300000

Evolución anual de la demanda bruta y la energía vendida por el régimen especial nacional.

13% 14%16%

18% 19%20% 19%

21%

25%

28%

20%

25%

30%

200000

250000

300000

h

1% 2% 3%4%

6% 6%9%

10%11%

13% 13% %

5%

10%

15%

50000

100000

150000

GW

h

0%0

Demanda b.c. R.Especial % R.Especial/Demanda

10

E d ti f S i l S tEnergy production of Special System

Generated Energy in Spain ( Renewables and CHP)

51.686 51.97257.808

61.441

60.000

70.000

25.131 27.50731.244

36.20042.146

46.909

30.000

40.000

50.000

MW

GW

h

1.630 3.138 4.014 5.697 8.519 10.00614.108 16.499

20.437

0

10.000

20.000

G

01990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

CHP Wind Hydro Waste Biomass waste Treat. Solar PV Total

11

y

Share of green electricity in gross electricity consumption 30% in 2010

Evolución de la participación que representan las energías renovables sobre la demanda en España

Share of green electricity in gross electricity consumption 30% in 2010 Directive

2001/77/CE

26% 26%30%300.000

Evolución de la participación que representan las energías renovables sobre la demanda en España

19%20%

15%

18% 19%

15%

26%

22% 22%

16%

18%

22%23%

20%

16%

19%21% 22%

15%

20%

25%

150 000

200.000

250.000

Wh

16%14%

5%

10%

15%

50.000

100.000

150.000

GW

0%01990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Demanda bruta Hidráulica RO Renovables RE Total Renovables / Demanda bruta

12

CONTENTS

1. Economic regulation:

Ley 54/97, RD 661/2007, RD 1578/2008 and RD-Ley 6/2009

2. Access regulation: 2. Access regulation: RD 1955/2000 and CNE RD Proposal 22April 2009

3. Guarantee of origin:

O d ITC 1522/2007

13

Order ITC 1522/2007

1. Economic regulation: Ley 54/97,RD 661/2007, RD 1578/2008 and RD-Ley 6/2009

14

1. Economic regulation Power Act 1997: Basic purposePower Act 1997: Basic purpose

To establish the Spanish Electricity Regulationith th f ll i th lwith the following three goals:

1 Guaranteeing the supply of electricity power1. Guaranteeing the supply of electricity power

2. Guaranteeing its quality3. Guaranteeing the supply of electricity power

at the lowest possible cost

Environmental protection must be taken into account

15

With a transitional period: warranty by law

1. Economic regulation Power Act 1997: Basic purpose

To establish the Spanish Electricity Regulation with

Power Act 1997: Basic purpose

the following three goals:

Environmental protection must be taken into account onEnvironmental protection must be taken into account onEnvironmental Impact Assessment

I t t d P ll t t P ti d C t lIntegrated Pollutant Prevention and Control

Emission Trading

Special System of Generation (economic incentives)

Demand Side Management Programs (economic incentives)

16

1. Economic regulation

According to Law 54/1997SPECIAL SYSTEM ORDINARY SYSTEM

According to Law 54/1997

Generators ≤ 50MW that use: Conventional generators

The energy produced can be Is obliged to participate in the market

incorporated into grid (priority of dispatching)Payments:

market

Payments: market price

a fixed tariff (guaranteed purchase) a premium in addition to the

17

market price

1. Economic regulation

According to Law 54/1997SPECIAL SYSTEM

According to Law 54/1997

18

1. Economic regulation

According to Law 54/1997SPECIAL SYSTEM

According to Law 54/1997

Bi

19

1. Economic regulation

Methodology CNE

Criteria:

Methodology CNE

1. To reach the targets set in the indicative planning

2 Security and predictability of the economic supports2. Security and predictability of the economic supports

3. Improve the quality of this kind of energy in order to integrate it to the system

4. RES+CHP compatible with Electricity Marketp y

20

1. Economic regulation

Methodology CNECriteria:

Methodology CNE

1. To reach the targets set in the indicative planningEconomic incentives -> Energy and Environmental Policy tool (enough to obtain a reasonable profitability)tool (enough to obtain a reasonable profitability)

21

1. Economic regulation

Methodology CNECriteria:

Methodology CNE

1. To reach the targets set in the indicative planningShare of 12% of primary energy from renewable energyShare of 12% of primary energy from renewable energy

Planning 1998 - 2010Bi d Bi 58 MW i 1998 > 2 300 MW i 2010

Planning 1998 - 2010Bi d Bi 58 MW i 1998 > 2 300 MW i 2010

Share of 30% of electricity from renewable energyShare of 30% of electricity from renewable energy

- Biomass and Biogas: 58 MW in 1998 -> 2.300 MW in 2010- Wind: 837 MW in 1998 -> 20.200 MW in 2010- Solar: photovoltaic 1 MW in 1998 -> 400 MW in 2010

- Biomass and Biogas: 58 MW in 1998 -> 2.300 MW in 2010- Wind: 837 MW in 1998 -> 20.200 MW in 2010- Solar: photovoltaic 1 MW in 1998 -> 400 MW in 2010

CSP 0 MW in 1998 -> 500 MW in 2010- Hydro < 50 MW: 1.190 MW in 1998 -> 2.200 MW en 2010

Urban Waste: 103 en 1998 > 260 MW en 2010

CSP 0 MW in 1998 -> 500 MW in 2010- Hydro < 50 MW: 1.190 MW in 1998 -> 2.200 MW en 2010

Urban Waste: 103 en 1998 > 260 MW en 2010

22

- Urban Waste: 103 en 1998 -> 260 MW en 2010- Cogeneration: 5.000 MW in 1998 -> 8.400 MW in 2012- Urban Waste: 103 en 1998 -> 260 MW en 2010- Cogeneration: 5.000 MW in 1998 -> 8.400 MW in 2012

1. Economic regulation

Methodology CNE cProjection of Capacity forRenewable Energy Sources

Methodology CNE c

Year 2030

Share %

FORESEEN CAPACITY OF RENEWABLES ENERGY SOURCES - 2030

Energy sources Capacity, Mw Share, % Share, % RES / Total Capacity

Share, % RES / Total production

Wind 40.000 48,00 26,5

Solar 15 500 18 60 10 3Solar 15.500 18,60 10,3

Photovoltaic 6.500 7,80 4,3

Thermo - solar 9.000 10,80 6,0

Biomass 4.400 5,28 2,9

Geothermic&Sea waves 800 0,96 0,5

Hydro 22.630 27,16 15,0y , ,

Total RES 83.330 100,00 55,2 40

1. Economic regulation

Methodology CNECriteria:

Methodology CNE

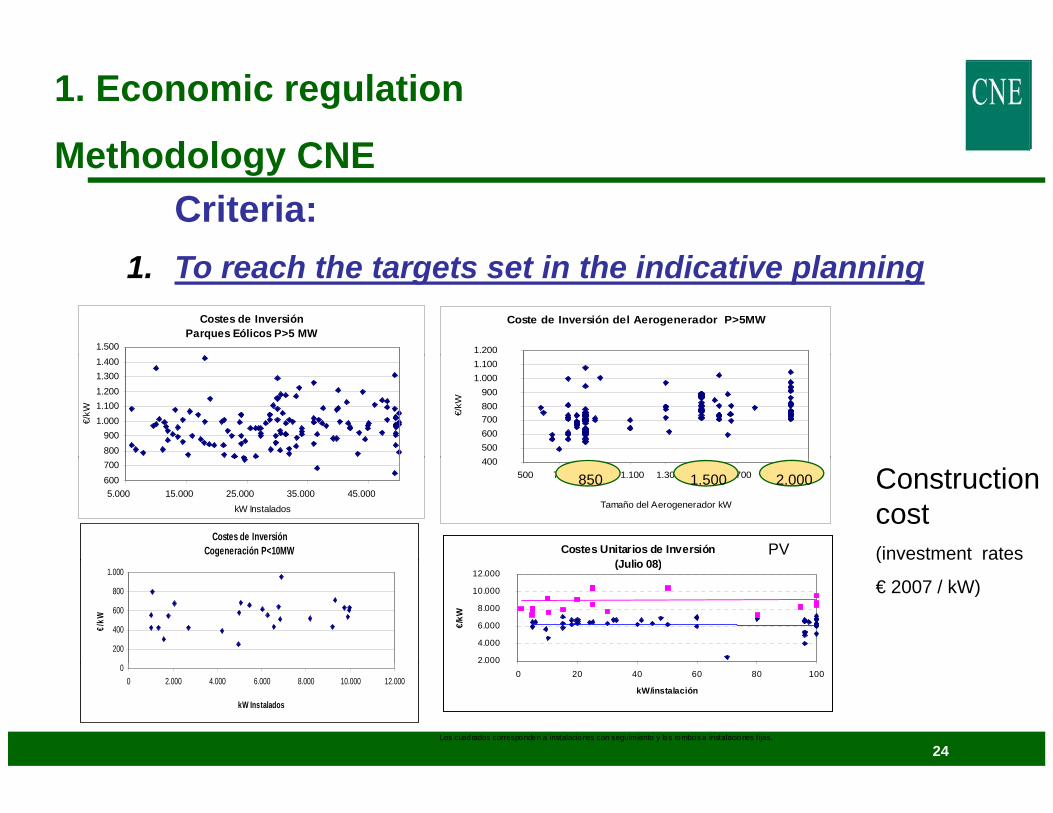

1. To reach the targets set in the indicative planningCostes de Inversión

Parques Eólicos P>5 MW1.500

Coste de Inversión del Aerogenerador P>5MW

1.200

800900

1.0001.1001.2001.3001.400

€/kW

500 600 700 800 900

1.000 1.100

€/kW

Costes de Inversión Cogeneración P<10MW

600700

5.000 15.000 25.000 35.000 45.000 kW Instalados

400 500 700 900 1.100 1.300 1.500 1.700 1.900 2.100

Tamaño del Aerogenerador kW

2.0001.500850 Construction cost (investment ratesCostes Unitarios de Inversión

(J li 08)PV

200

400

600

800

1.000

€/kW

(

€ 2007 / kW)(Julio 08)

2.000

4.000

6.000

8.000

10.000

12.000

€/kW

24

00 2.000 4.000 6.000 8.000 10.000 12.000

kW Instalados

0000 20 40 60 80 100

kW/instalación

Los cuadrados corresponden a instalaciones con seguimiento y los rombos a instalaciones fijas.

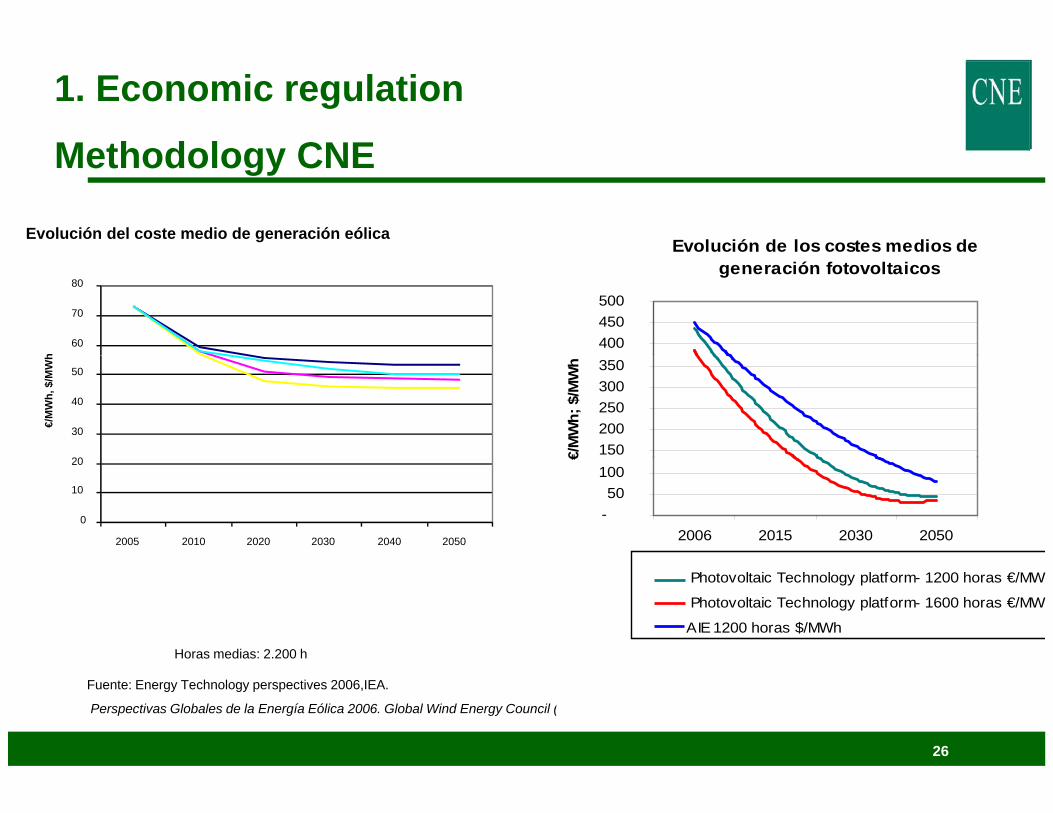

1. Economic regulation

Methodology CNECriteria:

Methodology CNE

1. To reach the targets set in the indicative planning

25IEA

1. Economic regulation

Methodology CNE

Evolución del coste medio de generación eólicaEvolución de los costes medios de

Methodology CNE

60

70

80

h

generación fotovoltaicos

400 450 500

20

30

40

50

€/M

Wh,

$/M

Wh

150 200 250 300 350

€/M

Wh;

$/M

Wh

0

10

20

2005 2010 2020 2030 2040 2050

- 50

100

2006 2015 2030 2050

€

Horas medias: 2.200 h

Photovoltaic Technology platform- 1200 horas €/MW

Photovoltaic Technology platform- 1600 horas €/MW

AIE 1200 horas $/MWh

Polinómica ( Photovoltaic Technology platform- 1600 h

26

Fuente: Energy Technology perspectives 2006,IEA.

Perspectivas Globales de la Energía Eólica 2006. Global Wind Energy Council (GWEC).

Polinómica ( Photovoltaic Technology platform- 1200 h

Polinómica (AIE 1200 horas $/MWh)

1. Economic regulation

Methodology CNE1. To reach the targets set in the indicative planning

Methodology CNE

14,00

15,00

Comparación precios ventas a Tarifa RD 661/07 vs. RD 436/04

RD 436/2004RD 611/2007

10,00

11,00

12,00

13,00

6,00

7,00

8,00

9,00

c€/k

Wh

2 00

3,00

4,00

5,00

6,00

27

1,00

2,00

Cog. g.nat.(10 MW)

Cog. g.nat.(30 MW)

Cog. fuel(10 MW)

Eólica (30MW)

Minih. (5MW)

Minih. (20MW)

Biom. b6.1(3MW)

Biom.b7.1(3 MW)

Biom.b7.2(3 MW)

Biom.b8.3(3 MW)

RSU (40MW)

1. Economic regulation

Methodology CNE1. To reach the targets set in the indicative planning

Methodology CNE

Concentrating Solar Power

45,00

Solar PV

30,00

Fix tariff incentive 2004 vs Incentive 2007 (cent_euro/kWh)

RD 436/2004RD 611/2007

3000

35,00

40,00

10,00

15,00

20,00

25,00

20,00

25,00

30,00

CSP 2009Tariff: 28,7603 c€/kWh

SO 2009 (1S C )

0,00

5,00

10,00

Solar (Thermal) up to 25years

Solar (Thermal) > 25 years

5,00

10,00

15,00SOLAR PV 2009 (1ST. CALL) Roof P <= 20 KW 34,00 c€/kWh

P > 20 kW 32,00 c€/kWhGround 32,00 c€/kWh

28

0,00Fotov. (100 kW)

1. Economic regulation

Methodology CNECriteria:

Methodology CNE

1. To reach the targets set in the indicative planning

2. Security and predictability of the economic supports-> To y yeliminate the regulatory risk (warranty by law ). Non retroactive -> Less uncertainties to investors (and Banks) and less cost to the consumers

- Economic incentives are assured during the life of the installation (existing capacity)

- Every 4 years or when planning is fulfilled, economic incentives are

29

updated (only for new capacity)

1. Economic regulation

Methodology CNECriteria:

Methodology CNE

1. To reach the targets set in the indicative planning

2. Security and predictability of the economic supportsy y

3. Improve the quality of this kind of energy in order to integrate it into the systemintegrate it into the system

30

1. Economic regulation

Methodology CNESpanish power system is practically an isolated system

Methodology CNE

It is necessary to improve the quality of this kind of energy in order to integrate it into the system

..Forecast obligation, and fulfill it (cost of deviations):

RES + CHP with capacity greater than 15 kVAp y g

Supplement for voltage controlWind energy must withstand faulty situations (to improve dynamic stability)

B l t di t hi tBelong to a dispatching center (if their capacity are greater than 10 MW )

If the plant joins the market, ancillary services could be provided

31

..

1. Economic regulation

Methodology CNE3. Improve the quality of this kind of energy in order to

integrate it to the system

Methodology CNE

g yTSO (Tec. System Operator )Control Center for Special System Energy: -Maximum Special System Energy on the gridp y gy g-Maximum Security System

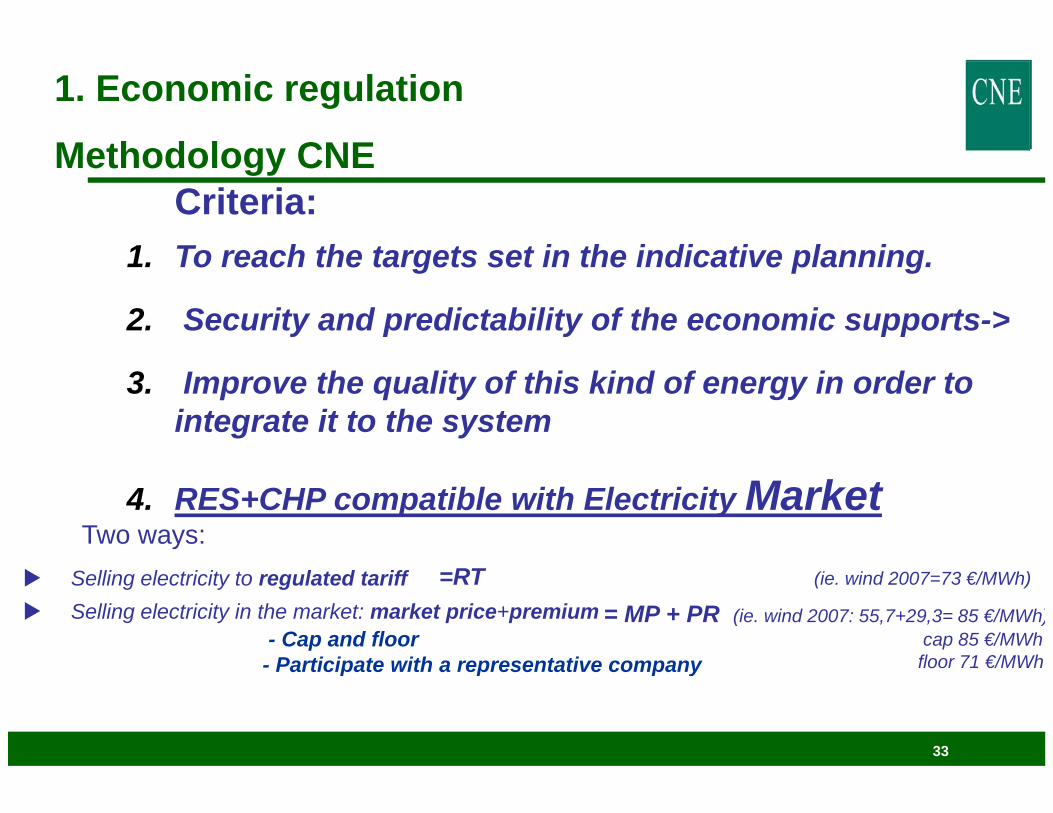

1. Economic regulation

Methodology CNECriteria:

1 To reach the targets set in the indicative planning

Methodology CNE

1. To reach the targets set in the indicative planning.

2. Security and predictability of the economic supports->

3. Improve the quality of this kind of energy in order to integrate it to the system

4. RES+CHP compatible with Electricity MarketTwo ways:

Selling electricity to regulated tariffSelling electricity in the market: market price+premium

- Cap and floor Participate with a representative company

=RT (ie. wind 2007=73 €/MWh)

= MP + PR (ie. wind 2007: 55,7+29,3= 85 €/MWh)cap 85 €/MWhfloor 71 €/MWh

33

- Participate with a representative company floor 71 €/MWh

1. Economic regulation

Methodology CNEMethodology CNE

14,0015,00

Comparación precios ventas a mercado RD 661/07 vs. RD 436/04

RD 436/2004RD 611/2007

9,0010,0011,0012,0013,00

Wh

5,006,007,008,009,00

c€/k

W

1,002,003,004,00

Cog. g.nat.(10 MW)

Cog. g.nat.(30 MW)

Cog. fuel (10MW)

Eólica (30MW)

Minih. (5MW)

Minih. (20MW)

Biom. b6.1(3MW)

Biom.b7.1(3 MW)

Biom.b7.2(3 MW)

Biom.b8.3(3 MW)

RSU (40MW)

34

(10 MW) (30 MW) MW) MW) MW) MW) (3MW) (3 MW) (3 MW) (3 MW) MW)

Reference Market Price=55,7 €/MWh

1. Economic regulation

Methodology CNEMethodology CNEMarket incentive 2004 vs Incentive 2007 (cent_euro/kWh)

35,00

RD 436/2004RD 611/2007

25,00

30,00 Concentrate Solar Power

15,00

20,00 SOLAR THERMAL 2009

Premium : 27,1188 c€/kWhCap: 36,7252 c€/kWhFloor : 27,1228 c€/kWh

5,00

10,00

35

0,00Solar (Thermal)

1. Economic regulation

Market participation

6 000

Market participation

5.000

6.000Ventas a tarifa Ventas a Mercado de ofertas

3.000

4.000

Wh

2.000

GW

0

1.000

2002 2003 2004 2005 2006 2007

H th h i k ?

1. Economic regulation: RD 661/2007

How the mechanism works?

The regional Governments have the competence togauthorize the special system plantsThe plants choose an alternative to sell the electricityTh S i h l t th iThe Spanish regulator pays the premiumTotal yearly amount of regulated tariffs and premiumsare included in the access tariffs paid for byare included in the access tariffs paid for byconsumersThe Spanish regulator makes proposals of regulated

ff ftariffs and premiums for new generators every 4 years

1. Economic regulationCost of Special System 2007 and 2008 for the power consumer

AÑO TECNOLOGIA

Potencia Instalada (MW)

Energía Vendida (GWh) Nº Instalaciones Retribución Total

(Miles €)

Precio Medio Retribución

Total (cent€/kWh)

Prima equivalente *

(miles €)

Prima equivalente * (cent€/kWh)

Sobrecoste (%)

COGENERACIÓN 6 059 17 616 872 1 335 326 7 580 596 712 3 387 2 7%COGENERACIÓN 6.059 17.616 872 1.335.326 7,580 596.712 3,387 2,7%SOLAR 693 495 19.988 214.811 43,384 194.051 39,191 0,9%EÓLICA 14.417 27.474 632 2.146.716 7,814 994.760 3,621 4,4%

HIDRÁULICA 1.909 4.120 928 318.940 7,741 146.190 3,548 0,7%BIOMASA 558 2.173 92 192.155 8,843 101.043 4,650 0,5%

RESIDUOS 569 2.722 33 167.806 6,165 53.674 1,972 0,2%TRAT RESIDUOS 527 3 397 43 316 889 9 328 174 453 5 135 0 8%

2007

TRAT.RESIDUOS 527 3.397 43 316.889 9,328 174.453 5,135 0,8%24.732 57.997 22.586 4.692.644 8,091 2.260.882 3,898 10,1%

COGENERACIÓN 6.157 21.090 884 2.070.197 9,816 716.528 3,398 2,4%SOLAR 3.354 2.492 49.971 1.127.994 45,268 968.055 38,850 3,2%EÓLICA 15.578 31.355 694 3.157.146 10,069 1.144.597 3,650 3,8%

HIDRÁULICA 1.961 4.497 941 432.393 9,615 143.755 3,197 0,5%BIOMASA 580 2 466 98 281 613 11 420 123 326 5 001 0 4%

Total 2007

2008BIOMASA 580 2.466 98 281.613 11,420 123.326 5,001 0,4%

RESIDUOS 579 2.734 34 239.450 8,759 63.970 2,340 0,2%TRAT.RESIDUOS 554 3.088 44 342.385 11,089 144.203 4,670 0,5%

28.763 67.720 52.664 7.651.179 11,298 3.304.434 4,880 10,9%Total 2008

En la tecnología Solar se contemplan 11 MW termosolares

38

1. Economic Regulation: New RD 1578/2008, Concerning solar photovoltaic

PV installations after 30th September 2008

Concerning solar photovoltaic

A pre-assign remuneration register

Four calls per year, to allow a maximum capacity of:Roof : 2/3 * 400 MW/añoGround: 1/3 * 400 MW/año + (extra 100 MW in 2009 y 60 MW in 2010)Ground: 1/3 400 MW/año (extra 100 MW in 2009 y 60 MW in 2010)

Flexible mechanism to transfer capacity between roof and ground installations if the call capacity is not reachedinstallations, if the call capacity is not reached

When the call capacity is reached the tariff for the next call is reduced 2,5% (10% / year )

39

(10% / year )

1. Economic Regulation: New RD 1578/2008, Concerning solar photovoltaic

TARIFF for the first call 2009 :

Concerning solar photovoltaic

Type I: roof P <= 20 KW 34 00 cent€/kWhP <= 20 KW 34,00 cent€/kWhP > 20 kW 32,00 cent€/kWh

T II dType II: groundEvery capacity: 32,00 cent€/kWh

Remark: the updated tariff for existing plants is 45,00 cent€/kWh

40

1. Economic Regulation: New RD-Ley 6-2009, A new pre-assigned remuneration register

A i ti i t

A new pre assigned remuneration register

A pre-assign remuneration register

1. Access and connection point to the power network2. Administrative authorization3. Municipal permit for works4. Guarantee deposit's (20 €/kW)4. Guarantee deposit s (20 €/kW)5. Economic resources or financing > 50%6. Agreement about equipment purchasing > 50%7 Access point to the gas net ork if an7. Access point to the gas network, if any 8. Favorable report using water resources, if any9. Additional guarantee deposit's (20 €/kW, except 100 €/kW for CSP)

41

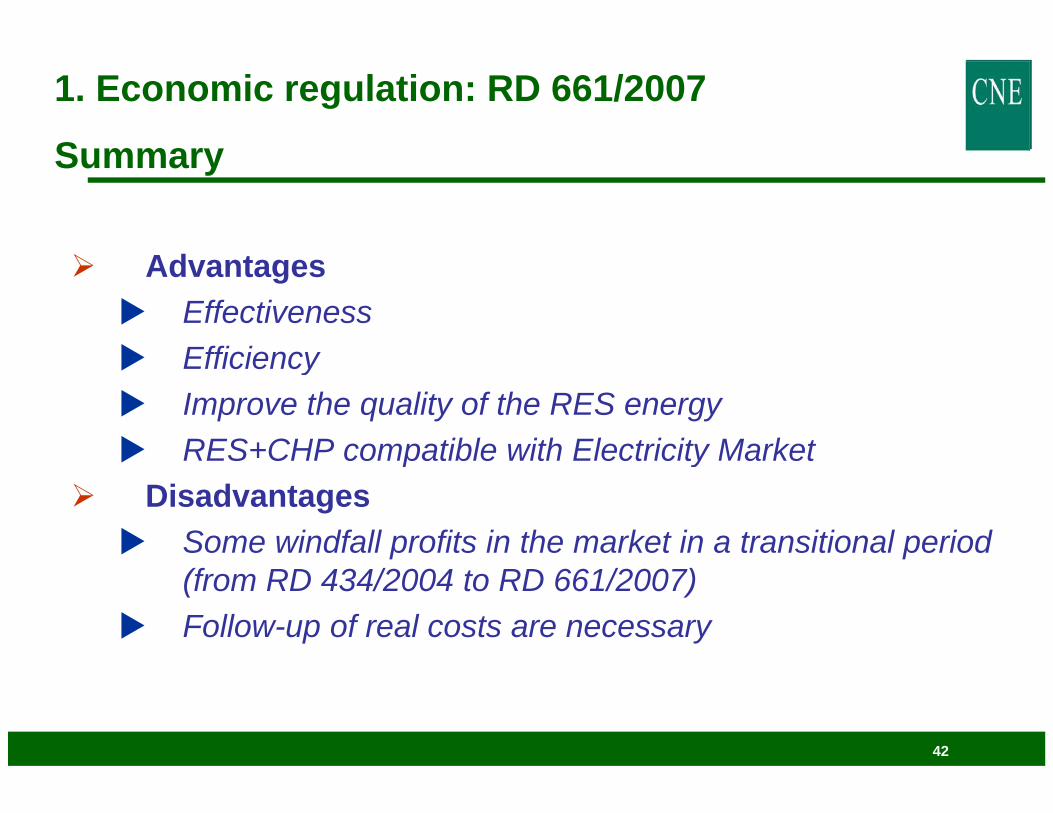

1. Economic regulation: RD 661/2007

SummarySummary

AdvantagesEffectivenessEfficiencyEfficiencyImprove the quality of the RES energyRES+CHP compatible with Electricity MarketRES CHP compatible with Electricity Market

DisadvantagesSome windfall profits in the market in a transitional period (from RD 434/2004 to RD 661/2007)Follow-up of real costs are necessary

42

2 Access regulation: 2. Access regulation: RD 1955/2000 and CNE Proposal 22April

43

2. Access regulation: RD 1955/2000

Try to Eliminate Grid Barriers- Discriminatory access conditions, and non-objective and non-transparent

procedures for grid access

- Insufficient grid capacity available

- Lack of available network capacity

- Lack of transparency on network data

- Low investment levels on expand networksLow investment levels on expand networks

- Long period to obtain authorisation for grid connections

Hi h id ti t

44

- High grid connection costs

2. Access regulation: RD 1955/2000

Resolution of Economy Minister 4th Dec 2000Resolution of Economy Minister 4th Dec 20001. ACCESS (TPA):

Right to transmit energy through the network of another agentg gy g g

There is a relationship with the power market

Controversies are resolved by CNE

2. CONNECTION:

Physical connection

Safety and technical quality

45

Controversies are resolved by Regional Governments

2. Access regulation: RD 1955/2000

Right to the network accessgIt is possible to restrain it only by lack of capacity: to avoid risks inthe safety, regularity and quality of the supplyLimits to access must by solved with the non-existingreserve of capacity principle -> It doesn´t have influence ontemporal preference in the connectiontemporal preference in the connection

Constraints are solved:• Transmission: Belong to a dispatching center and applying grid codes

M d t l i id t t i ( 4 )Mandatory planning avoid permanent constrains (every 4 years)• Distribution: Automatic disconnection equipments and grid codes.

Connection installations and reinforcement of the

46

Connection installations and reinforcement of theexisting grid must be paid for by new plants

2. Access regulation: RD 1955/2000

Access controversial procedure

GENERATORS R tGENERATORS DISTRIBUTORS REGIONS

Report

47

CNE Proposal 22April 2009

2. Access regulation: RD 1955/2000

From 1998 to end 2008 the capacity installed of Special System has increased from 24 200

p p

4.544 MW to 28.763 MW (+24.200 MW)

Energy Planning 2008-2016, included 47.670 MW in 2016 (+ 19.000 MW add)

Economic incentives are the main tool of energy policy to reach planning targetsOther tool is the right of third part access to the network which would be compatible with the security of the power system:y p y

To add a new SO tool: setting area constrains Study of access to the grid of new generator -> to considerate the production of existing generators (to avoid constrains)Mandatory fulfill of the planning develop of the network (transmission and distribution) Publicity of the nodal capacity

Simplified procedure to register small plants

48

Simplified procedure to register small plants

Priority of dispatch for renewables and cogeneration

3. Guarantee of origin: Order ITC 1522/2007

49

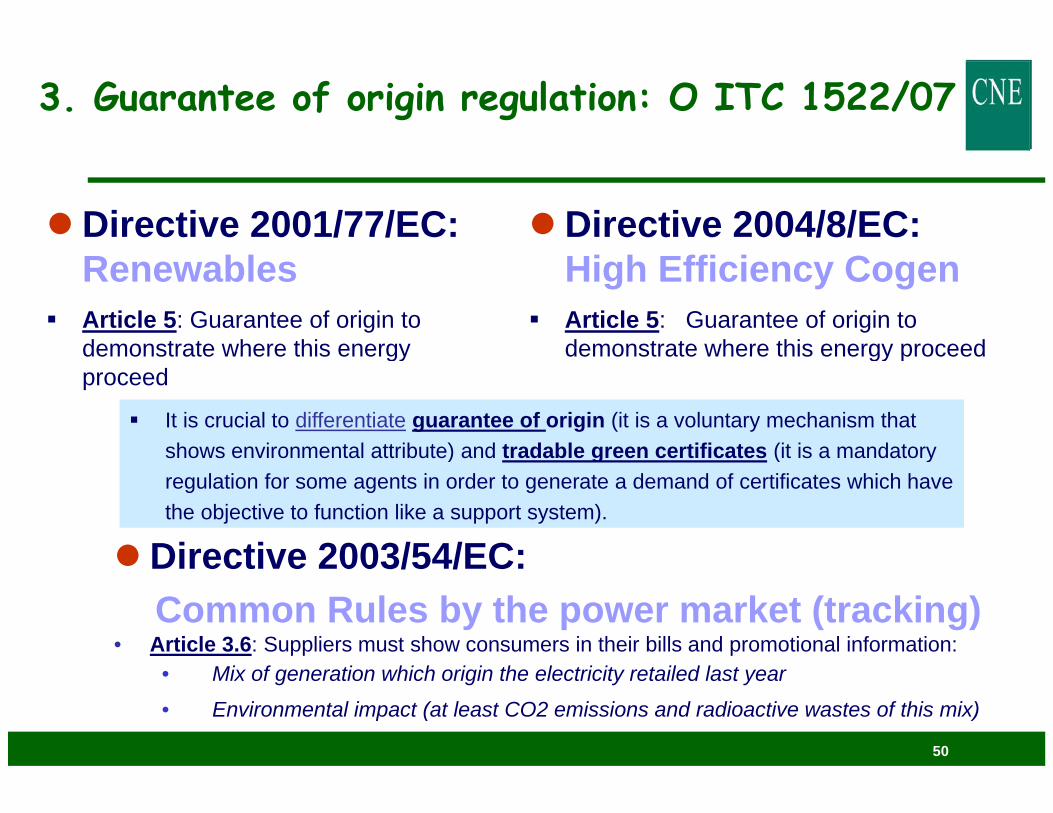

3. Guarantee of origin regulation: O ITC 1522/07

Directive 2001/77/EC: Directive 2004/8/EC: RenewablesArticle 5: Guarantee of origin to demonstrate where this energy

High Efficiency CogenArticle 5: Guarantee of origin to demonstrate where this energy proceeddemonstrate where this energy

proceed demonstrate where this energy proceed

It is crucial to differentiate guarantee of origin (it is a voluntary mechanism that shows environmental attribute) and tradable green certificates (it is a mandatory s o s e o e ta att bute) a d t adab e g ee ce t cates ( t s a a dato yregulation for some agents in order to generate a demand of certificates which have the objective to function like a support system).

Directive 2003/54/EC:Directive 2003/54/EC: Common Rules by the power market (tracking)

• Article 3.6: Suppliers must show consumers in their bills and promotional information:

50

• Mix of generation which origin the electricity retailed last year

• Environmental impact (at least CO2 emissions and radioactive wastes of this mix)

3. Guarantee of origin regulation: O ITC 1522/07Aspects

System Annotations in Count: Web Page CNE

Aspects

GENERATORS SUPPLIERSGoO GoO

CONSUMERS

Sol.CancellationSol. TransferSolicit Expedition

CNE CNECNE

Expedition Transfer Cancellation

51

3. Guarantee of origin regulation: O ITC 1522/07System Annotations in Count: Web Page CNE

52

3. Guarantee of origin regulation: O ITC 1522/07System Annotations in Count: Web Page CNE

53

3. Guarantee of origin regulation: O ITC 1522/07System Annotations in Count: Web Page CNE

54

3. Guarantee of origin regulation: O ITC 1522/07System Annotations in Count: Expeditions 2008

Las garantías expedidas mediante el Sistema de Garantías de Origen representan el 16 % de la producción nacional del 2008 y el 53 %respecto de la producción nacional procedente de fuentes de energía renovables y de cogeneraciónrespecto de la producción nacional procedente de fuentes de energía renovables y de cogeneración

Tipo de Energía Régimen Categoría Nº instalaciones Potencia (MW) Producción Declarada (GWh)

Garantías Solicitadas (GWh)

Garantías Expedidas (GWh)

A Exportar(GWh) (1)

Año 2008Resúmen Garantías de Origen Expedidas

( ) ( ) p ( ) ( ) ( )

Renovables Especial Eólicas 358 10.443 22.438 22.438 21.738 0

Renovables Especial Minihidráulica <10MW 99 314 876 876 840 0

Renovables Especial Fotovoltaicas 79 11 14 14 14 0

Renovables Especial Minihidráulica >10MW 19 414 854 854 853 0

Renovables Especial Biomasa 17 74 394 394 376 0p572 11.256 24.576 24.576 23.821 0

Renovables Ordinario Gran Hidráulica 663 15.884 19.425 20.624 18.488 353663 15.884 19.425 20.624 18.488 353

Total renovables 1.235 27.140 44.001 45.200 42.309 353

Cogeneración AE Especial Gas Natural 9 417 2.741 2.190 2.146 0

Cogeneración AE Especial Fueloil BIA 1 3 85 372 315 275 0

Cogeneración AE Especial Otros 3 216 1.243 1.236 1.235 0

15 718 4.356 3.741 3.656 0

Cogeneración AE Ordinario G. Natural / Ciclo Comb. 3 1.198 5.057 4.199 1.372 03 1.198 5.057 4.199 1.372 0

55

Total Cogeneración AE 18 1.916 9.413 7.940 5.028 0

1.253 29.056 53.414 53.140 47.337 353(1) Las Garantías solicitadas para exportar no están descontadas de las garantías expedidas

TOTAL

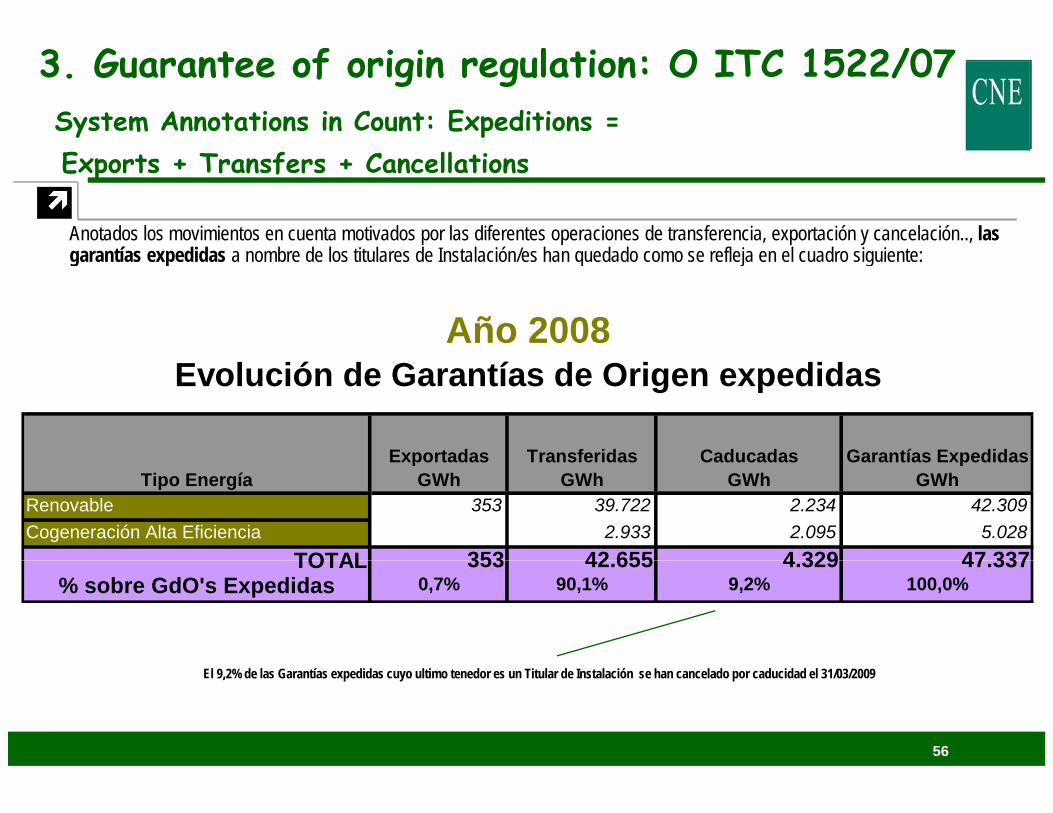

3. Guarantee of origin regulation: O ITC 1522/07System Annotations in Count: Expeditions =

Anotados los movimientos en cuenta motivados por las diferentes operaciones de transferencia, exportación y cancelación.., las garantías expedidas a nombre de los titulares de Instalación/es han quedado como se refleja en el cuadro siguiente:

Exports + Transfers + Cancellations

garantías expedidas a nombre de los titulares de Instalación/es han quedado como se refleja en el cuadro siguiente:

Año 2008Evolución de Garantías de Origen expedidas

Exportadas Transferidas Caducadas Garantías Expedidas

353 39.722 2.234 42.3092.933 2.095 5.028

353 42 655 4 329 47 337

RenovableTipo Energía

Exportadas GWh

TransferidasGWh

Caducadas GWh

TOTALCogeneración Alta Eficiencia

Garantías Expedidas GWh

353 42.655 4.329 47.3370,7% 90,1% 9,2% 100,0%

TOTAL% sobre GdO's Expedidas

56

El 9,2% de las Garantías expedidas cuyo ultimo tenedor es un Titular de Instalación se han cancelado por caducidad el 31/03/2009

3. Guarantee of origin regulation: O ITC 1522/07System Annotations in Count: TRACKING:

MIX PRODUCCIÓN COMERCIALIZADOR

MIX GENERATION AND SUPPLY

Nuclear; 19,3%Renovables; 20,7%

C ió d Alt

Otras; 0,9%

CC Gas Natural;

Carbón; 15,9%

Fuel/Gas; 3,3% Cogeneración de Alta Eficiencia; 1,7%

Cogeneración; 8,1%

30,1%

57

End of presentation

www.cne.eswww.cne.esInformación Estadística sobre las Ventas de Energía del Régimen g g

Especial

58