remember that health care is not like any other consumer good or service. when you shop for a car,...

TRANSCRIPT

• Remember that health care is not like any other consumer good or service.

• When you shop for a car, what should you do?

• You become an informed shopper!

BACKGROUND TO HEALTH CARESOLUTIONS

• But becoming an informed shopper takes a lot of time, energy and patience.

• When do you normally purchase major medical services?

• In an emergency!

• And what happens to smart shopping then?

A. Denial

B. Deregulation/competition

C. Tinker with Medicare/Medicaid

D. Medical savings accounts

E. HMO’S

F. Managed care

G. Canadian system

SOLUTIONS TO THE HEALTH CARE CRISES

Deregulation lower cost Competition lower prices.

• There are numerous regulations for all sectors of the medical industry.

• These regulations are expensive to comply with.

DEREGULATION/COMPETITION

• Deregulation is a plan to eliminate or reduce these regulations.

• By reducing or eliminating these regulations, costs would go down.

• Those medical companies (hospitals, etc.) That lowered their prices would be rewarded by more customers.

• Those medical companies that didn’t lower their prices would be forced to lower prices, or fail.

DEREGULATION - PRO

• This is the perfect competition model

• With competition, everyone is a winner, because competition forces producers to lower costs and prices.

• Medicare = medical care for the elderly.

• Medicaid = medical care for the destitute (the poor) and the disabled.

TINKER WITH MEDICAID AND MEDICARE

MEDICARE/MEDICAID

• Both are federal government programs.

• Both are paid for with federal income and business taxes.

• Both have skyrocketed in cost in the last 20 years.

• There have been a whole series of proposals to deal with MEDICARE and MEDICAID.

• Some proposals have been sensible and have resulted in cost savings without reduction in quality.

• Some proposals have been mean spirited, and have eliminated medical care to people who otherwise qualified for it.

1. If MEDICAID is abolished, who will pay the medical bills for the disabled and the poor?

2. The individuals and then their families.

WHAT HAPPENS IF WE WERE TO ABOLISH MEDICAID

3. But they only get MEDICAID if they are very poor or have severe disabilities.

4. So they won’t be able to pay for their medical bills.

5. Sometimes hospitals write off these bills. But they can’t afford to write them all off.

6. So what happens to the bills that the hospitals don’t write off?

7. They are tacked onto other customers bills!

8. So cutting back or abolishing MEDICAID doesn’t reduce national medical bills, it reshuffles them.

• Basically combines a health insurance policy combined with a tax-advantaged savings account

MEDICAL SAVINGS ACCOUNTS

A. Savings account1.Individuals can place up to $2500 per person,

per year, in a medical savings account.

MEDICAL SAVINGS ACCOUNTS

• This savings account can be in any type of investment vehicle.

• The owner of the account keeps whatever interest, dividends or growth in value this account generates.

3. Since it is pre –tax dollars, this will lowers someone’s taxable income.

4. This in turn lowers a person’s taxes.

5. Any of this money spent on health care is not taxed.

6. If it is withdrawn before retirement, or used for anything other than health care, it becomes taxable.

7. What is not used can be withdrawn after retirement and spent.

B INSURANCE POLICY 1. You have RO purchase an insurance policy

with this, at $100 a month.

2. The insurance policy doesn’t help until you have spent $2000 of your own money. ($2000 deductible)

3. It can then be applied for major catastrophes.

MSA - PRO

A. Increase national savings

B. Increase individual savings

C. Increase competition and reduce costs nationally

A. More people will save1. This allows people to save, which increases

family and then national savings.

C. This will generate competition, which will force down cost nationwide.

1. Consumer smart shopping forces suppliers to respond to consumers by lowering prices.

A. How can people save?1. People already have trouble trying to save,

because wages have fallen. How then can they increase their savings?

MEDICAL SAVINGS ACCOUNTSARGUMENTS AGAINST

B. Who can afford to save?1. Look at the costs of ordinary medical expenses. To

be able to pay them, you need to save a minimum of $500 a year if you are single and healthy.

2. If you have children, plan on $1000 per child, minimum. And that if you have absolutely nothing unusual happening to them.

C. Higher deductibles lead to later problems that a more expensive.

1. Due to the high deductibles, people will forego preventative care and routine checkups.

2. This means that early detection, which leads to early repair, will decrease.

• Instead people will postpone doctor visits until the pain becomes too great.

• And then the problem becomes expensive.

D. Age-health care equation1. Medical bills for most elderly are too high for

most families to realistically save for.

2. What to do we do then?

E. What about those without insurance now?

1. This does nothing for those without health insurance whose numbers continue to increase.

2. How does this help those with in adequate insurance today?

• Have a large number of structures.

• Basically, networks of health service providers: hospitals, clinics and doctors are all linked up.

HMO’S: HEALTH MAINTENANCE ORGANIZATIONS

A Individual Cost Savings1. Members save money compared to being on their

own.

HMO’S:AGRUMENTS IN FAVOR

B. Quality Service1. Most HMO’S have a large network of health

providers, and can provide a variety of specialists to choose from, for each type of illness.

C. National Cost Savings1. Nationally, if people are moved to HMO’S, the

country as a whole can save money, through economies of scale.

A. Not much left in cost savings1. Most of the cost savings from transferring people

to HMO’S has already taken place.

HMO’S:ARGUMENTS AGAINST

B. HMS’S compete for the healthy and the wealthy

1. They actively compete for the healthy and wealthy in the suburbs.

2. They don’t compete for rural patients, city patients or the elderly.

C. They are linked to your job1. Lose your job, you lose your access to an

HMO.

2. Many jobs don’t offer access to HMOS’, especially small and medium sized companies.

• A phrase for any action by any part of the medical industries to control costs.

MANAGED CARE

Examples include:1. Reducing hospital stays as much as possible.

2. Lowering wages.

3. Bypassing unions.

4. Reducing physicians fees.

5. Forcing physicians to reduce required/recommended SURGIES.

6. Financial incentives for physicians to take on more patients.

A. Given all of the padded expenses in our system, there is plenty of room to cut costs without reducing quality or quantity of care.

MANAGED CARE ARUGMENTS FOR

Examples include:1. The pharmaceutical industry is one of the most

profitable in the country, so there is room to cut some of its revenues.

2. For profit hospitals are very profitable, so there is room to cut some of their income as well.

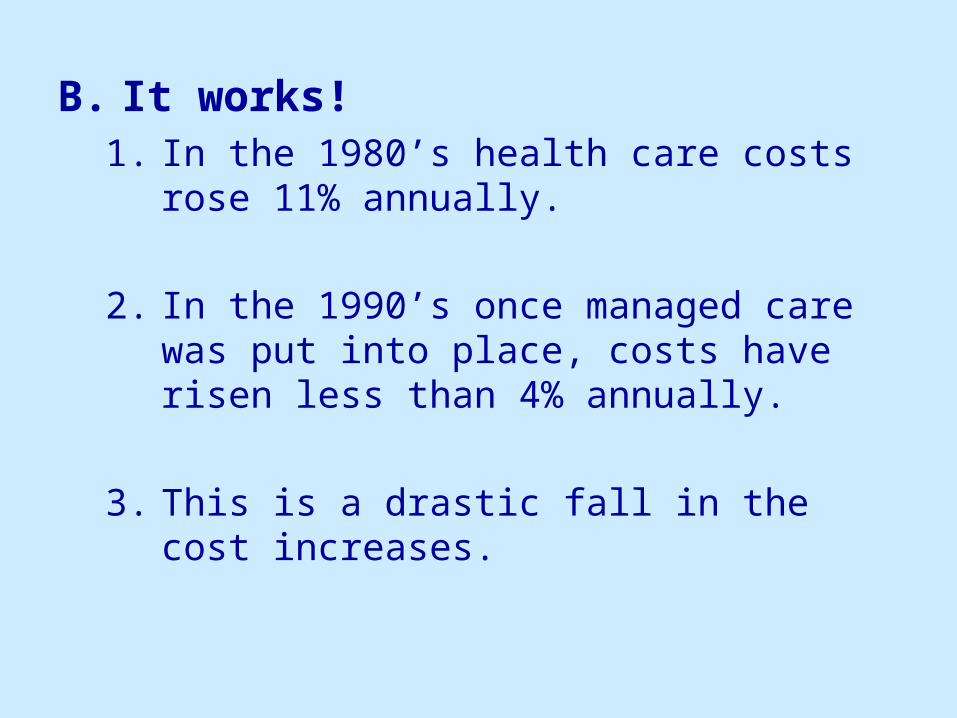

B. It works!1. In the 1980’s health care costs rose 11%

annually.

2. In the 1990’s once managed care was put into place, costs have risen less than 4% annually.

3. This is a drastic fall in the cost increases.

A. It is doing nothing for those without health insurance.

1. Through out the 1990’s even as managed care expanded, the numbers of people without health insurance continued to grow.

MANAGED CARE ARGUMENTS AGAINST

B. It will do little or nothing for those without adequate health insurance.

1. It appears that the number of people with inadequate insurance is also rising.

C. So far, many of these cuts have turned out to affect patients, rather than insurance or pharmaceutical companies or hospitals.

1. Examples include drive-by pregnancies and refusing patients emergency care.

2. Any savings appear to be going to the owners of medical companies, rather than reduced costs to patients.

A. All Canadian citizens are covered.

B. Single payer- the Canadian federal government.

THE CANADIAN SYSTEM: HOW IT WORKS

C. Revenues for health come from progressive income taxes, progressive corporate taxes, and high taxes on alcohol, tobacco products and firearms.

D. Doctors are not government employees.

E. Hospitals are not state owned.

F. Physicians are free to choose their patients.

G. Consumers are free to choose their doctors.

H. Fees are fixed for each service and negotiated between physicians and the government.

I. Nearly all types of medical problems are covered.

A. Universality1. All Canadians have medical coverage,

regardless of income

2. Legal immigrants and students are also covered.

THE CANADIAN SYSTEM:ARGUMENTS FOR

B. It is cheaper.1. Canadians spend only 8% of their GDP on

health care while the us spends 14%

2. One congressional study indicates that adoption of the Canadian system would save the average us family $1000 per year.

C. Improved health.1. More money would be spent on preventative

care, which would save money in the medium and long term.

2. It would also improve health in the short term.

D. Consumer freedom.– Consumers are free to chose their doctor.

E. Physician freedom.

A. Dramatic increase in federal government spending and taxation.

1. One study indicates that federal government spending might increase as much as $500 billion.

2. This would mean dramatic tax hikes as well.

THE CANADIAN SYSTEM:ARGUMENTS AGAINST

B. Increased waiting time and possible rationing of health care.

1. Canadians have longer waiting times for non emergency surgeries and procedures

C. Possible slow down in all types of medical research.

D. Virtual destruction of the health insurance industry.

E. Large number of jobs lost.

THE END