remap 2030 analysis for ukraine - Головна · 2017-08-10 · national renewable energy action...

TRANSCRIPT

REmap 2030 Analysis for Ukraine

Kiev,12 March, 2015

2

• Ukraine is part of the first volume of IRENA’s global renewable

energy roadmap (REmap)

• Ukraine is among the largest 26 energy markets that joined the

REmap initiative

• Focus on the potential, cost and benefits of renewables that can

realistically be deployed beyond Ukraine’s plans to 2020, with focus

on sectors and technologies

• In close collaboration with the SAEE

• Part of the International Climate Initiative (IKI) project, supported

by Germany’s BMUB

• Background paper for the analysis issued

REmap Ukraine background

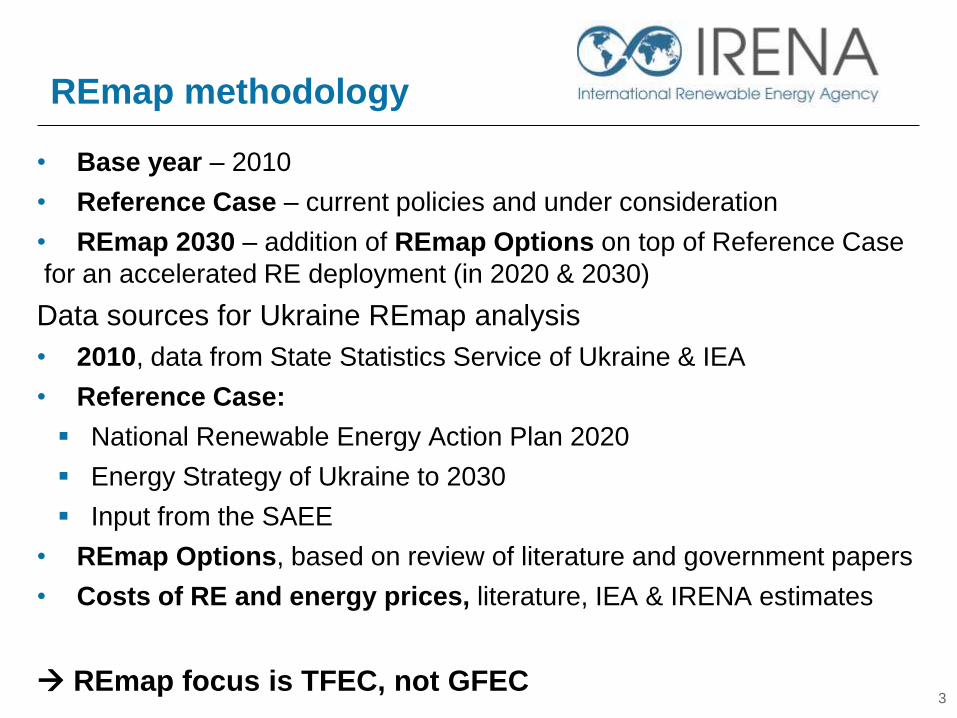

3

• Base year – 2010

• Reference Case – current policies and under consideration

• REmap 2030 – addition of REmap Options on top of Reference Case

for an accelerated RE deployment (in 2020 & 2030)

Data sources for Ukraine REmap analysis

• 2010, data from State Statistics Service of Ukraine & IEA

• Reference Case:

National Renewable Energy Action Plan 2020

Energy Strategy of Ukraine to 2030

Input from the SAEE

• REmap Options, based on review of literature and government papers

• Costs of RE and energy prices, literature, IEA & IRENA estimates

REmap focus is TFEC, not GFEC

REmap methodology

4

IRENA technology

database

IRENA

Costing studies

Learning curves/cost

reduction

assessments

Sectoral/technology

studies

Country Reference

Scenarios

Potentials

Reference FF/Nuclear

technologies

Cost curves

Fuel prices, taxes,

subsidies, capital cost

External

effects

Substitution

cost

REMAP

Options

Methodology at a glance

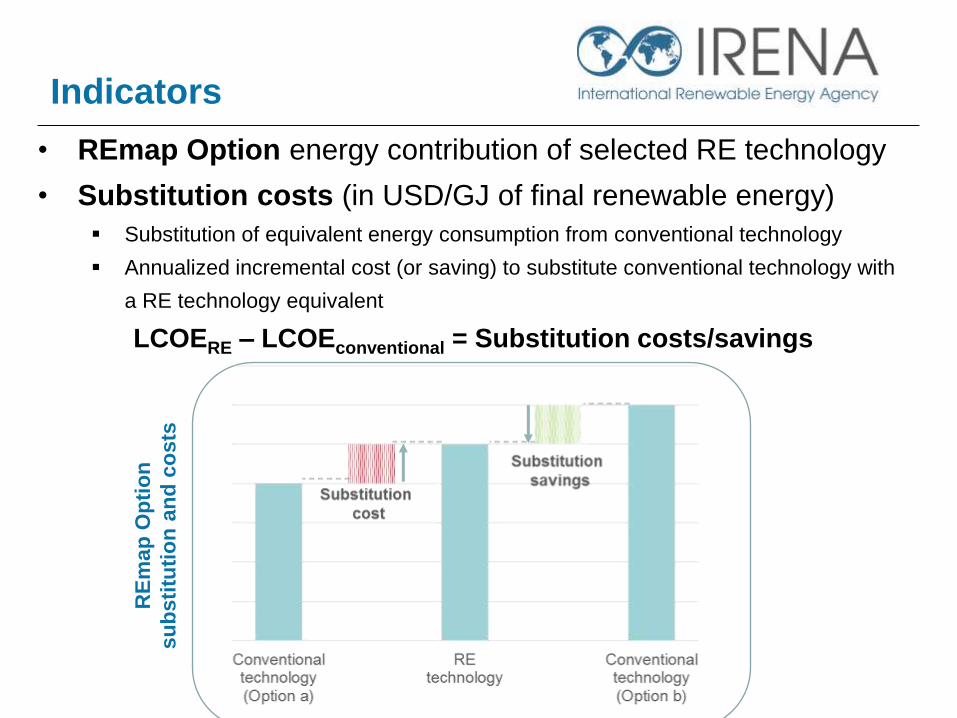

• REmap Option energy contribution of selected RE technology

• Substitution costs (in USD/GJ of final renewable energy)

Substitution of equivalent energy consumption from conventional technology

Annualized incremental cost (or saving) to substitute conventional technology with

a RE technology equivalent

LCOERE – LCOEconventional = Substitution costs/savings

RE

map

Op

tio

n

su

bsti

tuti

on

an

d c

osts

Indicators

REMAP UKRAINE

ANALYSIS

6

• Cost-competitiveness of renewables compared to fossil fuels

• Socio-economic benefits (jobs, energy supply security)

• Short-term and long-term supply security

Natural gas is mainly used for the heating sector (residential, district heat

producers, industry)

65-70% of total consumption is imports (USD 500/tcm, May 2014 import

price)

Storage important for short-term, 32 bcm capacity today, majority in West

Renewables are in particular important for the long-term

Renewables are part of a package of measures, with energy efficiency,

increased own natural gas production, storage, diversification of supply

• There are important questions about:

How to proceed with district heating – upgrade or reduce use

How to deal with energy subsidies and affordability

7

Drivers for renewables

• 2009: 3.3% RE share in TFEC, 67% bioenergy, 32% hydro, 1% others

• 2030 Reference Case: 11.8%; 82% bioenergy, 7% hydro, 4% wind

• REmap 2030: 21.5%

• Total RE use grows ten times from 87 PJ to 870 PJ, substituting natural

gas for heat and coal/NG for power generation, oil in transportation

• Total RE use is about a quarter power, three-quarters end-use

• Biomass key technology for all sectors

• 77% bioenergy, representing 17% of TFEC in 2030

• Between 2010 and 2030, 24.9 GW RE power capacity

Wind and solar PV (+20 GW), biomass (+3.5 GW)

• Total savings in energy system costs of USD 110 million per year

• REmap 2030 reduces Ukraine’s total natural gas demand by 16% in

2030 compared with current policies

8

Key findings

CURRENT SITUATION &

REFERENCE CASE

9

Base year 2009 &

current situation (1/4)

• Ukraine’s TFEC has been decreasing since the early 1990s

• Since 2000 remains flat, around 77 Mtoe/yr in 2012

• Industry: 45%, Buildings: 37%, Transport 15%, Other: 3%

10

Source: IEA (2014)

0

20

40

60

80

100

120

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

TFEC

(M

toe

/yr)

Industry Transport Buildings Other

11

Natural gas 36% of Ukraine’s total primary energy supply,

Consumption is around 40 Mtoe/yr

65-70% of total consumption is imports

Base year 2009 &

current situation (2/4)

Industry29%

Transport16%

Buildings22%

Agriculture / forestry /

fishing2%

Power15%

District heat16%

Source: SSSU & IEA (2012; 2014)

12

Electricity demand has been decreasing, but started to increase slowly since

2001: 145 TWh/yr (1995) to 139 TWh/yr (2012)

Share in end-use sector demand also increasing (2012):

• Industry: 22%, Buildings: 18%, Transport: 7%

Most power plants reached end of life; low capacity factor and efficiencies

Source: IEA (2014)

Base year 2009 &

current situation (3/4)

0

20

40

60

80

100

120

140

160

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Po

we

r co

nsu

mp

tio

n (

TWh

/yr)

Industry Transport Buildings Other Total

13

District heat demand remains important: 12 Mtoe/yr (2012)

Share in end-use sectors: 15% (2012)

Efficiency of DH system is low, up to 60% of total production lost in

production and distribution

Base year 2009 &

current situation (4/4)

0

2000

4000

6000

8000

10000

120001

99

51

99

61

99

71

99

81

99

92

00

02

00

12

00

22

00

32

00

42

00

52

00

62

00

72

00

82

00

92

01

02

01

12

01

2

Dis

tric

t h

eat

co

nsu

mp

tio

n

(kto

e/yr

)

Industry Buildings Source: Radeke and Kosse (2013); IEA (2014)

Reference Case

2010-2030 (1/2)

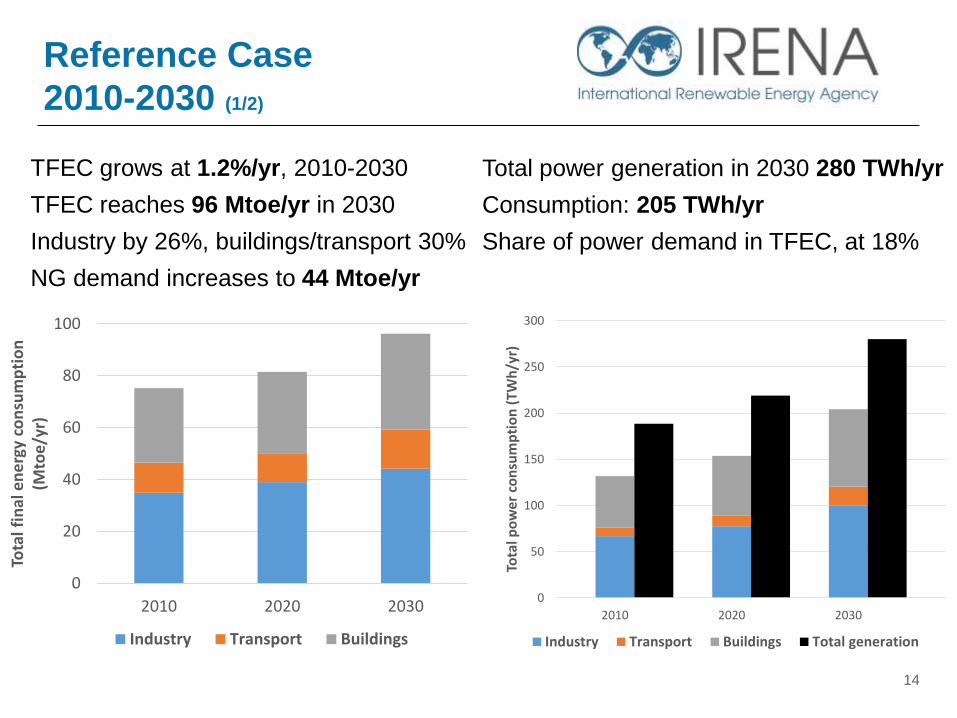

TFEC grows at 1.2%/yr, 2010-2030

TFEC reaches 96 Mtoe/yr in 2030

Industry by 26%, buildings/transport 30%

NG demand increases to 44 Mtoe/yr

Total power generation in 2030 280 TWh/yr

Consumption: 205 TWh/yr

Share of power demand in TFEC, at 18%

14

0

20

40

60

80

100

2010 2020 2030

Tota

l fin

al e

ne

rgy

con

sum

pti

on

(M

toe/

yr)

Industry Transport Buildings

0

50

100

150

200

250

300

2010 2020 2030

Tota

l po

we

r co

nsu

mp

tio

n (

TWh

/yr)

Industry Transport Buildings Total generation

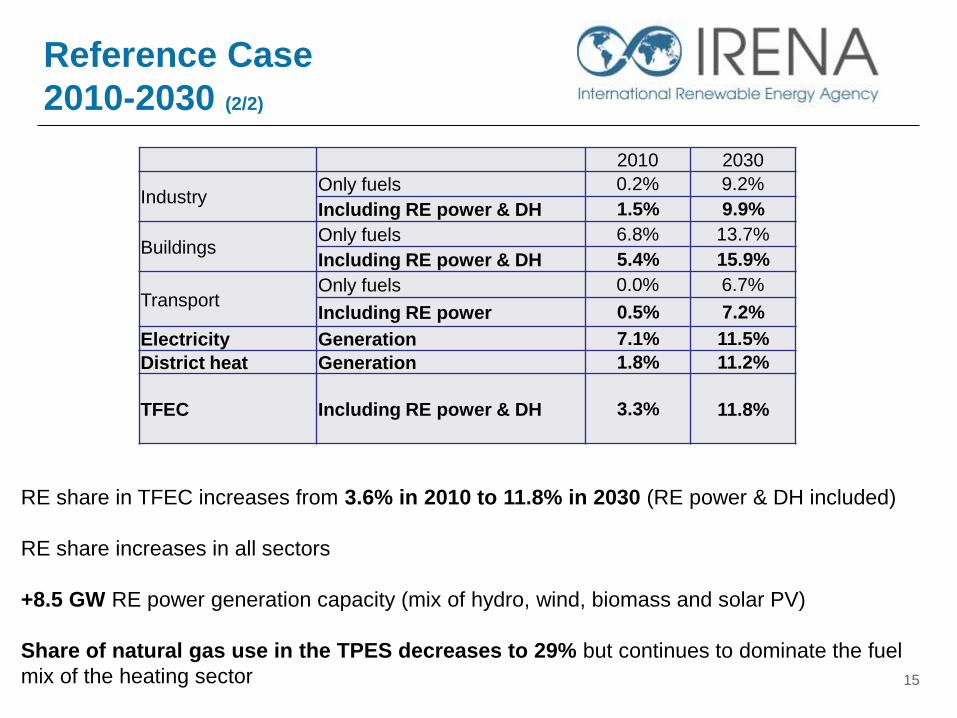

RE share in TFEC increases from 3.6% in 2010 to 11.8% in 2030 (RE power & DH included)

RE share increases in all sectors

+8.5 GW RE power generation capacity (mix of hydro, wind, biomass and solar PV)

Share of natural gas use in the TPES decreases to 29% but continues to dominate the fuel

mix of the heating sector

Reference Case

2010-2030 (2/2)

2010 2030

Industry Only fuels 0.2% 9.2%

Including RE power & DH 1.5% 9.9%

Buildings Only fuels 6.8% 13.7%

Including RE power & DH 5.4% 15.9%

Transport Only fuels 0.0% 6.7%

Including RE power 0.5% 7.2%

Electricity Generation 7.1% 11.5%

District heat Generation 1.8% 11.2%

TFEC Including RE power & DH 3.3% 11.8%

15

REMAP OPTIONS

16

RE consumption, 2009-2030

17

0

200

400

600

800

1000

2009 Reference Case 2030 REmap 2030

Re

new

able

en

erg

y u

se in

TFE

C (

PJ/y

r)

Hydro WindSolar PV Geothermal (electricity)Solid biomass (electricity) BiogasSolar thermal Geothermal (heat)Solid biomass (heat) Heat pumps

Power generation

Heating

Transport 7%

20%

72%

Key developments: - Total RE use grows to 870 PJ (10x)

- RE share reaches 21.5% in TFEC

Total RE use

- Power sector 20%

- Heating sector 72%

(DH large growth)

- Transport sector 7%

- Biomass 77%

- Wind 10%

- Solar 7%

- Others 6%

Power generation capacity

2009-2030

18

0

10

20

30

2009 Reference Case2030

REmap 2030

Inst

alle

d p

ow

er g

ene

rati

on

cap

acit

y (G

W)

Hydropower Wind onshore

Biomass and biogas Solar PV

Geothermal

Key developments: - Total RE capacity 29.6 GW

- RE share in total generation 26.1%

(73.1 TWh/yr, about half is wind)

Mainly non-biomass options

- 6 GW hydro

- Wind growth rate: 570 MW/yr (12 GW)

- Solar PV growth rate: 380 MW/yr (8 GW)

- Continuing increase in biomass-based

power generation, mainly biomass CHP

(3.5 GW)

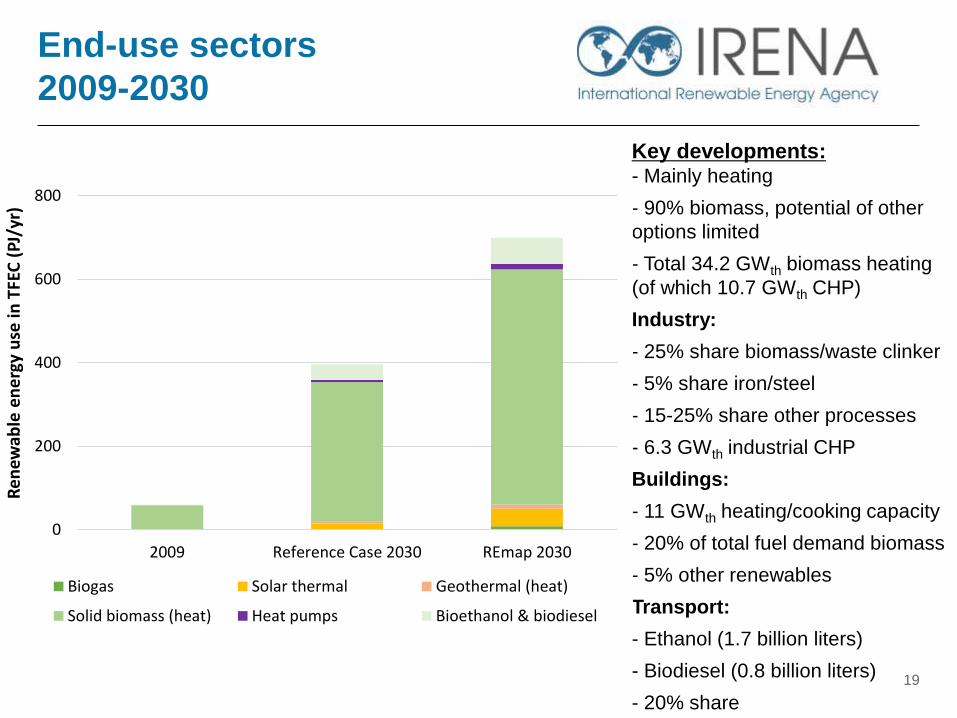

End-use sectors

2009-2030

19

Key developments: - Mainly heating

- 90% biomass, potential of other

options limited

- Total 34.2 GWth biomass heating

(of which 10.7 GWth CHP)

Industry:

- 25% share biomass/waste clinker

- 5% share iron/steel

- 15-25% share other processes

- 6.3 GWth industrial CHP

Buildings:

- 11 GWth heating/cooking capacity

- 20% of total fuel demand biomass

- 5% other renewables

Transport:

- Ethanol (1.7 billion liters)

- Biodiesel (0.8 billion liters)

- 20% share

0

200

400

600

800

2009 Reference Case 2030 REmap 2030

Ren

ewab

le e

ne

rgy

use

in T

FEC

(PJ

/yr)

Biogas Solar thermal Geothermal (heat)

Solid biomass (heat) Heat pumps Bioethanol & biodiesel

Fuel mix for

heat & power generation

20

58% 55% 50%41%

54 Mtoe 60 Mtoe 68 Mtoe 68 Mtoe

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 Reference Case2020

Reference Case2030

REmap 2030

Bre

akd

ow

n o

f fu

el u

se f

or

he

atin

g

NG Biomass Other fuels

8% 7% 6% 4%

189 TWh 219 TWh 280 TWh 280 TWh

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 Reference Case2020

Reference Case2030

REmap 2030

Po

we

r ge

ne

rati

on

by

fue

l typ

e

NG Renewables Other non-renewables

Bioenergy use breakdown

21

Key developments in bioenergy demand :

- Accounts for 77% of total RE use

- 78% for heating

- Its use nearly doubles compared to 2030

Reference Case

- Total demand in REmap 2030: 900 PJ/yr

Bioenergy supply potential in 2030:

IRENA estimates: 1.1 – 1.8 EJ/yr

- Forestry products: 125-485 PJ/yr

- Agr. residues & waste : 645-950 PJ/yr

- Energy crops: 345 PJ/yr

Demand / supply: 50%-80%

Power generation

8%

DH generation,

CHP10%

DH generation, heat only

7%

Residential heating

14%

Industry, commercial

& agriculture heating

47%

Transport14%

Total biomass demandREmap 2030 (900 PJ/yr)

22

Cost-supply curve, 2030

(business perspective)

10. 12. 14. 16. 18. 20.

Average weighted cost of substitution (1.8 USD/GJ)

-10

-5

0

5

10

15

20

-10

-5

0

5

10

15

20

Ave

rag

e s

ub

sti

tuti

on

co

st

(US

D2010/G

J T

FE

C)

Renewable energy share in total final energy consumption (%)

Reference Case developments

3%-12%

3%

Bioethanol (advanced)

Bioethanol (conventional)

Biomass heat (industry)

Biomass power CHP (industry)

Wind onshore

Biogas heat (buildings)

Biodiesel

Geothermal heat (industry)

Biomass district heat

Solar PV (utility)

Biomass heat (buildings)

Solar thermal heat (industry)

Solar thermal heat (buildings)

Biomass heat CHP (industry)

Biomass pellet heat (buildings)

Discount rate: 10%, Coal price in 2030: USD 2.7/GJ, NG price: USD 4.6-13.8/GJ

23

Cost-supply curve, 2030

(government perspective)

Discount rate: 10%, Coal price in 2030: USD 2/GJ, NG price: USD 11-22/GJ

10. 12. 14. 16. 18. 20.

Average weighted cost of substitution (-0.3 USD/GJ)

-12

-7

-2

3

8

-12

-7

-2

3

8

Ave

rag

e s

ub

sti

tuti

on

co

st

(US

D2010/G

J T

FE

C)

Renewable energy share in total final energy consumption (%)

Reference Case developments

3%-13%

3% Bioethanol (advanced)

Bioethanol (conventional)

Biomass heat (industry)

Biomass power CHP (industry)

Biogas heat (buildings)

Biodiesel

Wind onshore

Geothermal heat (industry)

Biomass district heat

Solar PV (utility)

Biomass heat (buildings)

Solar thermal heat (industry)

Solar thermal heat (buildings)

Biomass heat CHP (industry)

Biomass pellet heat (buildings)

Comparison of

costs and benefits, 2030

24

Costs of renewables

Average substitution costs of 2020/2030 options (USD/GJ) -0.3

Total system costs in 2030 (billion USD/yr) -0.1

Total investment needs between 2010-2030 (billion USD/yr) 4.9

Benefits from avoided externalities

CO2 emission reduction potential (Mt CO2/yr) 59

Benefits from human health externality (billion USD/yr) -0.1 - -0.3

Benefits from CO2 emission externality (billion USD/yr) -1.0 - -5.0

Total benefits from externalities in 2030 (billion USD/yr) -1.1 - -5.3

Net system costs in 2030 -1.2 - -5.4

Fossil fuel saving benefits (compared to Reference Case)

Reduction in fossil fuel costs (billion USD/yr) 5.0

Additional costs from biomass use (billion USD/yr) 2.2

Net savings in energy costs (billion USD/yr) 2.8

25

How to accelerate

renewables uptake to 2030

Planning transition pathways

• Develop a national T&D grid plan that considers 15% generation from wind and solar

• Modernise and improve efficiency of existing power & heat generation capacity with

energy efficiency and renewables

• Complement and improve energy efficiency and supply security by diversifying NG imports

and increasing domestic production of natural gas

Creating an enabling business environment

• Utilise local manufacturing capacity to create an affordable market for RE equipment

• Increase in investments in both domestic/foreign in new capacity by easing GT tariffs, and

by developing incentives for small-scale investors

Ensuring smooth integration

• Develop collection systems for agricultural residues, and invest in infrastructure for

sustainable recovery of forestry biomass

Creating and managing knowledge

• Add knowledge on resource potential and cost and benefits of renewables, and develop

norms, rules, standards and definitions