regulation of international business entrepreneurship institute july 22, 2010 prof. gonzalo freixes...

Post on 21-Dec-2015

215 views

TRANSCRIPT

Regulation of International Business

Entrepreneurship Institute

July 22, 2010

Prof. Gonzalo Freixes

A legal and tax perspective

2

The Case of the Bollywood Film Distributors

Bollywood Distributions (BD) wants to set up film distribution operations in the United States.

Prof. Gonzalo Freixes Confidential

Foreign Investment in the U.S.

Prof. Gonzalo Freixes Confidential 3

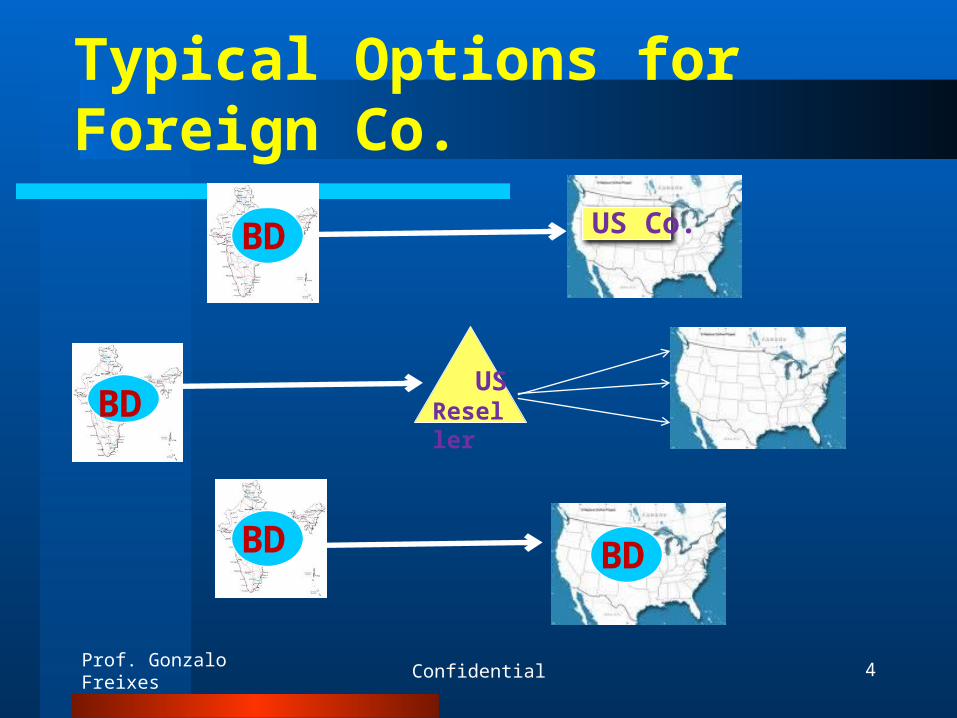

Typical Options for Foreign Co.

4

BD US Co.

BD

US Reseller

BD

BD

Prof. Gonzalo Freixes Confidential

5

Typical Options for Foreign Co.

Form U. S. Domestic Business Entity

Contracting with U. S. Re-seller/Agent

Operating a Branch Office in U. S.

Prof. Gonzalo Freixes Confidential

6

Business Form Considerations

Formalities requiredLiability of ownersManagement structureTransferability (ability to sell)Taxation (separate vs. flow through)

Prof. Gonzalo Freixes Confidential

7

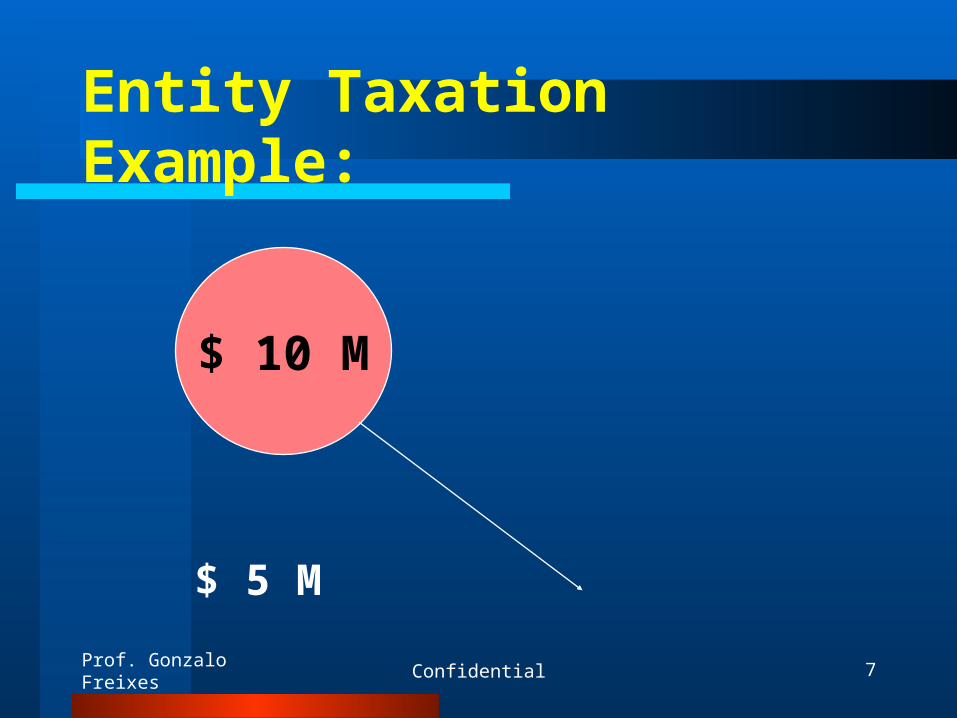

Entity Taxation Example:

$ 5 M

Owners

$ 10 M

Prof. Gonzalo Freixes Confidential

8

Taxes Paid by Corporation

Entity pays $ 3.5 M ($ 10M x .35)

Owners pay $ 750K ($ 5M x .15) 2010

$ 2M ($5M x .40) 2011

TOTAL PAID IRS: $ 4.25 M 2010

$ 5.5 M 2011

Prof. Gonzalo Freixes Confidential

9

Taxes Paid by “Flow Through”

Entity pays $ 0

Owners pay $ 3.5 M*

(Individual Taxes on $ 10 M)

TOTAL PAID IRS: $ 3.5 M*

*3.96M in 2011

Prof. Gonzalo Freixes Confidential

10

Business Form Options

General Partnership/Joint VentureLimited Partnership“C” Corporation“S” CorporationLimited Liability Company

Prof. Gonzalo Freixes Confidential

State Regulation

Corporate Regulation is left to the States

California vs. Delaware

Prof. Gonzalo Freixes Confidential 11

VS

12

Contract with U. S. Re-Seller

Governed by CISG (Convention for the International Sale of Goods) not INDIA

Place of sale – title & risk of loss

Negotiate jurisdiction & conflict of laws

Financing & currency issues

Confidentiality & Non-Competition

Prof. Gonzalo Freixes Confidential

13

Operating a U. S. Branch

• Immigration Issues employees/owners

•Must comply with local business regulations (e.g. Business License)

•Taxation: Subject to U.S. Income Tax + Branch Profits Tax (TBD) + (perhaps) home country taxation

Prof. Gonzalo Freixes Confidential

Focus on U. S. Taxation

Foreign Company invests in U.S.

U. S. Company invests abroad

Prof. Gonzalo Freixes Confidential 14

BD

US Co.

INBOUND TRANSACTIONS

Prof. Gonzalo Freixes 15Confidential

Typical Options for Foreign Co.

Forming a U.S. Business EntityContracting with U. S. Re-seller/AgentOperating a Branch Office in U. S.

Prof. Gonzalo Freixes 16Confidential

U. S. Taxation (Inbound Business)

Passive Investments

Interest, Dividends, Rents, Royalties

Active Business Profits

Selling goods & services in the U.S.

Prof. Gonzalo Freixes 17Confidential

Tax on Passive Investments

Called Tax on “Fixed or Determinable Income” or “Withholding Tax”

Flat 30%

No deductions allowed

Prof. Gonzalo Freixes 18Confidential

Tax on Business Profits

Called Income “effectively connected with a U. S. trade or business”

Includes: Services, sale of inventory, rental real estate, manufacturing, etc.

Taxed at Corporate Rates (15% to 35%) or Individual Rates (10% to 35%)*

*39.6% in 2011Prof. Gonzalo Freixes 19Confidential

Tax Issues – Related Companies

• IndiaCo creates US Subco• IndiaCo sells products to US Subco• Subco sells to U.S. customers• Tax consequences?

1. Will India tax the profits of each? 2. Will US tax the profits of each?

U.S. SubCo

Prof. Gonzalo Freixes 20Confidential

IndiaCo

Source of Income Rules

Income = where service or sale took place.

Shift income to foreign nation by transferring Title & Risk of Loss

IRS allows Parent/Sub to allocate income 50/50 (US & foreign nation).

Prof. Gonzalo Freixes 21Confidential

New Tax Issue – Sub v. Branch

• IndiaCo creates US SubCo (Subsidiary)

• TAX 1: US SubCo pays taxes on US profits

• US SubCo pays dividends to IndiaCo

• TAX 2: IndiaCo pays dividend tax

• IndiaCo operates BRANCH instead

• Does this avoid “double taxation?”

Prof. Gonzalo Freixes 22Confidential

Branch Profits Tax

Foreign Company’s U. S. Branch will pay income tax on U. S. income

+Branch Profits Tax of 30% on income

withdrawn

(Called “dividend equivalent amount”)

Prof. Gonzalo Freixes 23Confidential

Effect of Tax Treaties

Reduces “double taxation” by U. S. and foreign nation

Example: U.S. and India -

Dividends & Interest taxed at 15-20%

Prof. Gonzalo Freixes 24Confidential

New Tax Issue

• IndiaCo manufactures at $ 1 per unit• Assume India has 25% tax rate• India sells to US SubCo at $ 1.95 per unit• US SubCo sells in U.S. for $ 2 per unit• US has 35% tax rate

U.S. SubCo

Prof. Gonzalo Freixes 25Confidential

IndiaCoWho will tax profits?

95¢ 5¢

35%25¢

Transfer Pricing

IRS may re-allocate income between related companies

Will look at “comparable unrelated sales”

Prof. Gonzalo Freixes 26Confidential

Tax on U. S. Subsidiary

U.S. Income subject to U. S. Corporate Tax (35%)

Dividends paid to foreign parent subject to 30% flat tax.

Treaties lower rates (India = 15%)

Watch out for Transfer Pricing

Prof. Gonzalo Freixes 27Confidential

Tax on U. S. Partnership/LLC

Foreign companies taxed on “flow through” basis but subject to Branch Profits Tax!!

Flow through income = “effectively connected with U. S. trade or business”.

Owners will pay at corporate or individual rates on “flow through” income

Prof. Gonzalo Freixes 28Confidential

Tax on U. S. Re-Seller or Agent

Income taxed where “sale” took place

May be U. S. or foreign nation

Focus on contract language

Prof. Gonzalo Freixes 29Confidential

OUTBOUND TRANSACTIONS

Prof. Gonzalo Freixes 30Confidential

Outbound Taxation - Basics

U.S. Taxpayers (including corporations) pay U.S. taxes on all worldwide income.

Foreign Subsidiaries of U.S. Companies do not (unless profits “repatriated”).

Prof. Gonzalo Freixes 31Confidential

Outbound Taxation - Problems

For U.S. Taxpayer:

Double Taxation

For IRS:

Offshore Companies

Prof. Gonzalo Freixes 32Confidential

Outbound Taxation - Solutions

For U.S. Taxpayer:

Foreign Tax Credit

$ 91,500 Exclusion

Tax Treaties

Prof. Gonzalo Freixes 33Confidential

Outbound Taxation - Solutions

For IRS:

Subpart F Income

Controlled Foreign Corporation

(> 50% control or stock value)

Foreign Base Income

(no indigenous economic connection)

Prof. Gonzalo Freixes 34Confidential

Tax Rates: India v. U.S.

TYPE OF TAX U.S. TAX RATEIndia TAX RATE

Corporate Income 35% 35% (domestic)

40% (foreign)

Individual Income 10 – 35% (2010) 0 – 30%

15 – 39.6% (2011) (+10% levy on rich)

Capital Gains 15% (2010) 20%

(Long Term rates) 20% (2011)

Prof. Gonzalo Freixes 35Confidential

Intellectual Property in U.S.

First Use Doctrine (TM & Copyrights)

Copyrights (Federal Regist.) – 95 yrs.

Trademarks (Federal or State Level)

Patents (Federal Regist.) – 17 years

Prof. Gonzalo Freixes Confidential 36

International IP Registration

Paris Convention: National TreatmentPatent Cooperation Treaty: 30 mos. To fileMadrid Protocol: Central filing for TM’sBerne Convention: National Treatment +

Minimum Standards for CopyrightsICANN: Domain Names TRIPS: WTO enforcement of Paris & Berne

Prof. Gonzalo Freixes Confidential 37

Labor & Employment Issues

Employee v. Independent Contractor

At will employment

Discrimination Laws: U.S. & State

Hours, overtime, minimum wage

Payroll Taxes: FICA

Workers CompensationProf. Gonzalo Freixes Confidential 38

39

Securities Regulation

Federal: Securities Act of 1933 Covers sale of any investment to the publicRequires registration unless issuance exempt

States: “Blue Sky” Laws Requires registration in each state California: Requires permit unless exempt

Tax Rates: China v. U.S.

TYPE OF TAX U.S. TAX RATECHINA TAX RATE

Corporate Income 35% 25%

16.5% (HK)

Individual Income 10 – 35% (2010) 5 – 45%

15 – 39.6% (2011) 2 – 17% (HK)

Capital Gains 15% (2010) 20%

20% (2011) 0% (HK)

Prof. Gonzalo Freixes 40Confidential

Prof. Gonzalo Freixes Confidential 41

Choosing Business Entity China, Hong Kong & U.S.

U.S. CHINA HONG KONG

Partnership Cooperative JV Partnership

Limited Partnership None Limited Partnership

L.L.C. Equity JV L.L.C.

Corporation Company Limited Private Limited Company by Shares Public Limited Companyor Equity JV