regulating systemic risk examining the impact of the new financial regulation on institutional...

TRANSCRIPT

Regulating Systemic RiskExamining the Impact of the New Financial Regulation on Institutional Investors

Kenneth Grossberg

What is Systemic Risk?

The risk of collapse of an entire financial system or entire market. As opposed to risk

associated with any one individual entity, group or component of the financial system.

i.e. What is the risk of Mom and Pop Bank defaulting versus the risk to the entire financial system posed by a Goldman default?

Who are the Institutional Investors?What are they Doing?

Pension Funds i.e. CALPERS, Ontario

Teachers Pension Plan Ensuring the provision of

benefits for employees on retirement

Mutual Funds i.e. Vanguard Funds, Jackson

Funds Pooling funds of individual

investors to allow them the benefits of large scale trading

Hedge Funds i.e. Fortress, Citadel Managing the resources of a

few “qualified” investors

A (Brief) Animated Commentary on Institutional Investors

More About Hedge Funds… Who is a “qualified” investor?

Any individual, trust account or institutional fund with at least $5 million in assets to invest with.

More than 8,900 hedge funds, or private investment companies, managed more than $1.43 trillion in assets as of June 2009. (www.hedgefundfacts.org).

The goal of a hedge fund is to make money whether the market rises or falls by engaging in risk management. “Old School” hedge funds actually use hedging to manage risk. “New School” hedge funds seek out greater risk in search of greater returns.

Perverse incentive structure (Risk, Reward, Control, Duration)

Rewarding managers for taking excessive risk at the expense of investors

Hedge funds have historically avoided SEC oversight due to their small size. A typical hedge fund has less than 100 investors, or is comprised of “qualified

purchasers”, exempting it from the registration requirements of the Investment Company Act of 1940, and the Investment Advisers Act of 1940.

The Private Fund Investment Advisers Registration Act of 2009 (www.treas.gov).

Elimination of the Private Adviser Exemption contained in the Investment Advisers Act. A small exception will remain, but it will exclude “an

investment adviser who acts as an investment adviser to any private fund.”

Private fund simply means any “fund available in the private market without government support or guarantee.” (www.businessfinance.com).

Any fund with over $30 million under management would be required to register with the SEC.

Hedge funds with over $10 billion under management would be required to pay a fee for the resolution fund, where other financial institutions trigger fee payment at $50 billion in assets. (www.jimhamiltonblog.blogspot.com).

The Private Fund Investment Advisers Registration Act of 2009.

Collection of Systemic Risk Data; Reports; Examinations; Disclosures Significantly amending the Investment Advisers Act. SEC would be authorized to require any adviser falling under

the act to maintain any and all records regarding private funds advised by the investment adviser necessary or appropriate in the public interest and for the assessment of systemic risk.

Required information would include, but not be limited to: Amount of assets under management Use of leverage (including off-balance sheet leveraging) Counterparty credit risk exposures Trading and investment positions Trading practices Any other information as the SEC, in consultation with the Fed,

determines necessary or appropriate in the public interest and for the protection of investors or for the assessment of systemic risk.

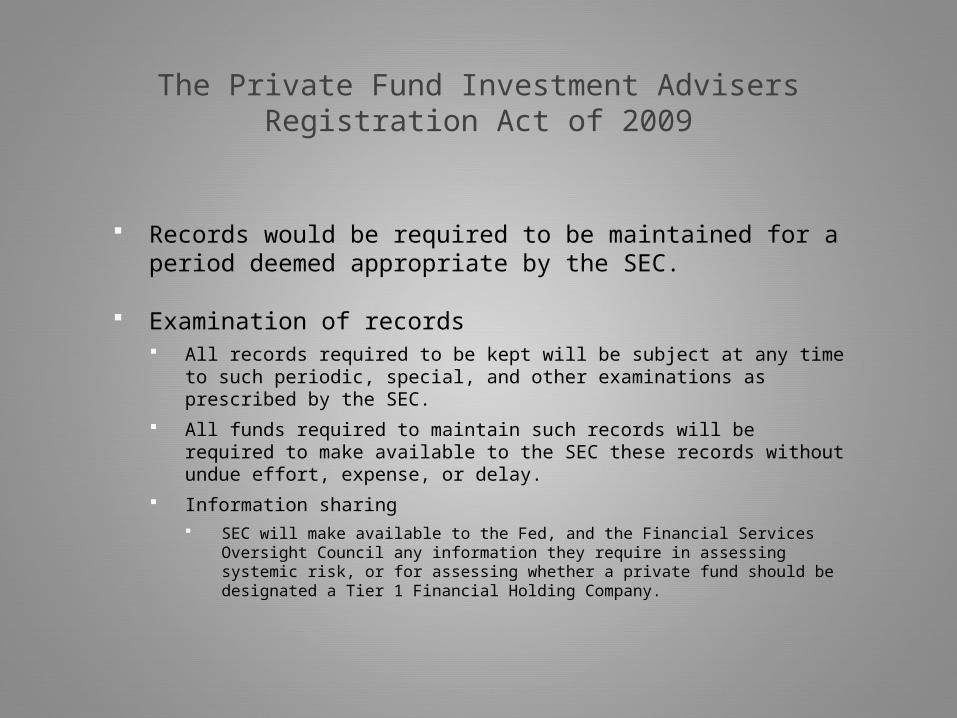

The Private Fund Investment Advisers Registration Act of 2009

Records would be required to be maintained for a period deemed appropriate by the SEC.

Examination of records All records required to be kept will be subject at any time to such

periodic, special, and other examinations as prescribed by the SEC. All funds required to maintain such records will be required to make

available to the SEC these records without undue effort, expense, or delay.

Information sharing SEC will make available to the Fed, and the Financial Services Oversight

Council any information they require in assessing systemic risk, or for assessing whether a private fund should be designated a Tier 1 Financial Holding Company.

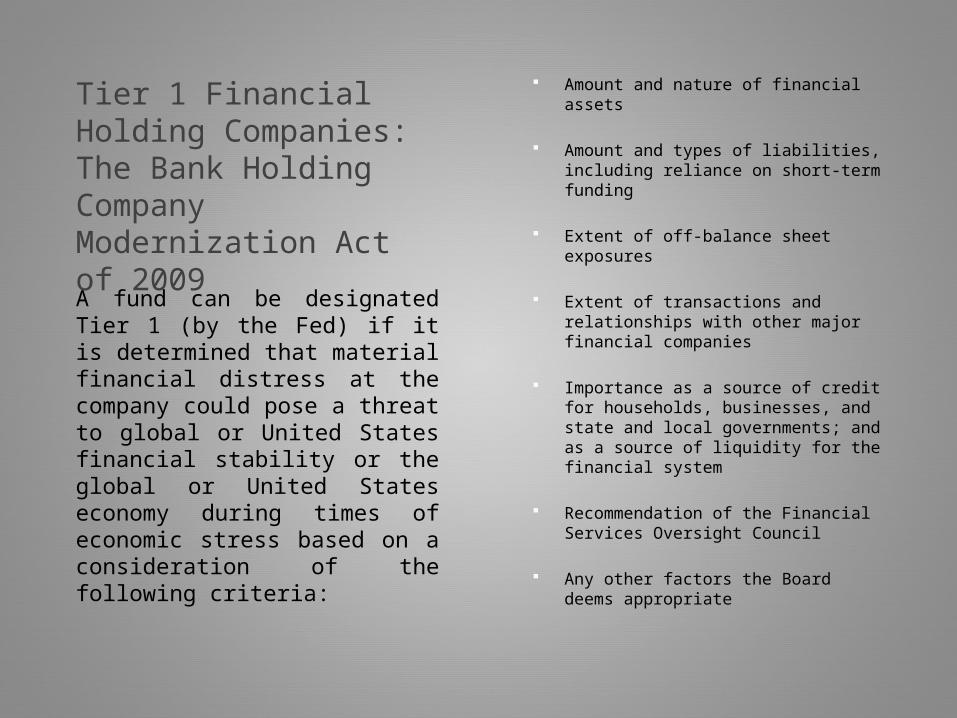

Tier 1 Financial Holding Companies: The Bank Holding Company Modernization Act of 2009

Amount and nature of financial assets

Amount and types of liabilities, including reliance on short-term funding

Extent of off-balance sheet exposures

Extent of transactions and relationships with other major financial companies

Importance as a source of credit for households, businesses, and state and local governments; and as a source of liquidity for the financial system

Recommendation of the Financial Services Oversight Council

Any other factors the Board deems appropriate

A fund can be designated Tier 1 (by the Fed) if it is determined that material financial distress at the company could pose a threat to global or United States financial stability or the global or United States economy during times of economic stress based on a consideration of the following criteria:

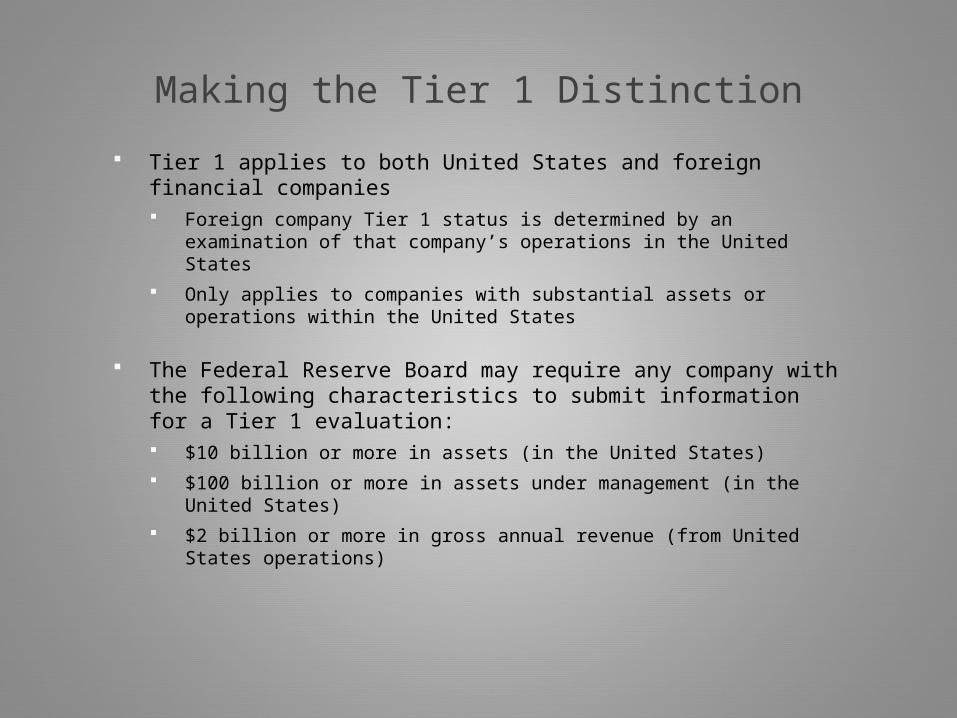

Making the Tier 1 Distinction

Tier 1 applies to both United States and foreign financial companies Foreign company Tier 1 status is determined by an examination of

that company’s operations in the United States Only applies to companies with substantial assets or operations

within the United States

The Federal Reserve Board may require any company with the following characteristics to submit information for a Tier 1 evaluation: $10 billion or more in assets (in the United States) $100 billion or more in assets under management (in the United

States) $2 billion or more in gross annual revenue (from United States

operations)

Prudential Regulation: The Purpose of Making the Tier 1 Distinction

If it is determined that a company qualifies as a Tier 1 Financial Holding Company, it will be subject to prudential regulation including, but not limited to: Risk-based capital requirements Leverage limits (Tangible equity not less than 2% of total

assets, and not more than 65% of the required minimum level of capital)

Liquidity requirements Overall risk management strategies

It is within the discretion of the board to differentiate among Tier 1 Financial Holding Companies based on a consideration of the varying level of risk that each poses to the financial system

Prudential Regulation Continued…

A Tier 1 Financial Holding Company at all times shall be well capitalized and well managed

1. Minimum total risk-based capital ratio of 10 percent2. Minimum tier 1 risk-based capital ratio of 6 percent3. Minimum tier 1 leverage ratio of 5 percent4. Must be under no capital directive

Well managed is undefined

DO NOT CONFUSE TIER 1 CAPITAL with TIER 1 FINANCIAL HOLDING COMPANIES

More requirements for Tier 1 Companies

Periodic reporting under oath Planning for rapid and orderly

dissolution in the event of financial distress

Nature and extent of credit exposure to other Tier 1 companies

Nature and extent of credit exposure of other Tier 1 companies to the institution

Disclosure of systems in place for monitoring and managing risk

Any public disclosure as the board may prescribe

Backup authority granted to the FDIC

Other than enumerated regulations, Tier 1 Financial Holding Companies will be treated as Bank Holding Companies

Even More Requirements… Capital Restoration Planning

Failure to submit an adequate recapitalization plan, or significant undercapitalization could result in: Required sale of enough assets to become well capitalized Requirement that shares sold be voting shares Possible required merger with a well capitalized Tier 1 Financial

Holding Company Requiring implementation of a new management, including a new

board of directors Restrictions on financial activities and total asset growth (requiring

the company to reduce total assets) Restrictions on executive compensation Divestiture Mandatory bankruptcy for critically undercapitalized companies

Even if a company is well capitalized, if the board deems it to be engaged in unsafe or unsound practices, the board has the discretion to treat it as undercapitalized; or if it is undercapitalized, the board has the discretion to treat it as significantly undercapitalized

Concentration Limits for Tier 1 Companies

The Board, by regulation, shall prescribe standards that limit the risks posed by a Tier 1 financial holding company’s exposure to any other company. Prohibition of credit exposure to any unaffiliated company

that exceeds 25% of the Tier 1 company’s capital stock and surplus All extension of credit All repo and reverse repo agreements All securities borrowing and lending transactions All guarantees, acceptances, or letters of credit All purchases of or investments in securities Counterparty exposure in connection with derivative

transactions Any other similar transaction determined by the board

Will the Regulation Work?

For the first time, it appears that the government will possess the information it needs to truly evaluate the systemic risk posed by these institutional investors, BUT… There is little to no mention of what type of metrics will be

used, or how the data will be weighted or analyzed There is still a lot of discretion in the hands of the Federal

Reserve Board to make these determinations These determinations will likely be made without the necessary

level of transparency There is still too much agency overlap with the SEC, FSOC,

Fed, and FDIC all involved in the systemic risk assessment

What impact might the Obama Bank Plan have on this regulation?