regional market focus phillip securities research pte...

TRANSCRIPT

MCI (P) 137/11/2012 Ref No: RM2013_0072 1 of 16

Regional Market Focus

Phillip Securities Research Pte Ltd

16 April 2013

Singapore

Keppel Corporation Ltd - Good news from new customer Recommendation: Accumulate Previous close: S$11.39 Fair value: S$12.38

Falcon Energy awarded Keppel a US$226mn jack-up rig contract

Premium jack-up rigs prices unaffected by strong competition; market share intact

YTD order win to S$2.15bn

Regional Market Focus

16 April 2013

2 of 16

Strategy

- Country Strategy: Thai, 5 Apr / S’pore, 8 Mar / China & HK, 28 Jan - Global Macro, Asset Strategy: 12 Apr, Update / US, 20 Mar / 4 Mar, Update / ASEAN, 5 Dec

Morning Commentary - STI: -0.30% to 3284.37 - SET: +0.69% to 1527.3 - JCI: -0.86% to 4894.6 - KLCI: -0.04% to 1697.8 - HSCEI: -2.02% to 10440.8 - Hang Seng: -1.43% to 21772.7 - Nikkei 225: -1.55% to 13275.7 - ASX200: -0.71% to 3343.6 - India NIFTY: +0.72% to 5568.4 - S&P500: -2.30% to 1552.4 MARKET OUTLOOK: By Ng Weiwen, Macro Analyst Is April the new May? Often we have clients asking us whether they should "Sell in May and go away". Well, our view has been that the risk of profit taking (correction) this 2Q13 for Equities has risen, given softness in US and China macro data. But pull-back in equities offers an attractive opportunity to accumulate our OWs in US, CN & HK (on compelling valuations), ID, PH, TH (resilient domestic demand) and SG (construction boom, attractive dividend yield). In the US, the bears led the charge from the opening till the closing bell as reflected in both S&P 500 and DJIA's price action on Mon on the back of weaker-than-expected Empire State Manufacturing Survey as well as NAHB homebuilder sentiment, along with a subdued global macro backdrop. Is China entering an era of slow growth? Reckon that Chinese policymakers are confronted with a major headache on account of strong credit growth but weak GDP growth (with industrial output and fixed asset investment undershooting) as the recent credit expansion-notwithstanding numerous property curbs- is likely to complicate the context/environment against which policies are set henceforth. Near-term downward bias for the HSI and HSCEI. HSCEI has slipped below its 200dma support level (10.5k level) while the HSI is likely to challenge its key 200dma support at 21.5k level amid a bearish moving average crossover for both indices. The confluence of weaker-than-expected China’s macro data as well as sharp sell-off in gold weighed on the AUD/USD. Already, the Aussie has pierced thru' its lower bollinger band (on a daily time frame) during Tokyo session today. Commodities (gold, silver, oil, copper) all tumbled. Both the Nikkei and USD/JPY likely succumbed to profit taking on Mon. Pullbacks will serve as an opportunity to accumulate long positions in Japan (Nikkei, Topix). Our base case has been that so long as the USDJPY continues to march towards (better if it clears above) the psychological 100 level, the Nikkei will continue to rise higher. Reckon USD/JPY is likely to retest the 99.95 level (11th Apr 2013 high) before challenging the psychological 100 level. STI has remained resilient and continued to consolidate in a tight range, consistent with our earlier guidance. We are cautiously optimistic that the STI will likely challenge the 3320 resistance (followed by the psychological 3400 hurdle) so long as it stays above key support at 3250. Notwithstanding the tight correlation of the SGD and Gold in the ‘safe havens club, reckon that USD/SGD range is likely to hold with strong support at 1.235 (200dma). (All equity indices mentioned in this note are tradeable with Phillip CFDs or ETFs)

Regional Market Focus

16 April 2013

3 of 16

MACRO DATA: In US, homebuilder sentiment continued to disappoint. Specifically, the NAHB housing market index continued to decline for the third consecutive month by 2pts m-m to a reading of 42 in April, on concerns of easing demand as well as tighter credit. Meanwhile, the Empire State manufacturing survey came in weaker than expected, declining 6.1pts m-m to 3.1 in April. These recent data corroborate with our view that the US economy is likely to see a year of 2 halves in 2013 – a soft patch in 1H, followed by a rebound in 2H. (by Ng Weiwen) In Singapore, retail sales gained 3.6% m-m sa in Feb, reversing from a 1.2% contraction in the preceding month. Ex motor vehicles, retail sales surged 7.8%. (by Ng Weiwen) In China, GDP grew by 7.7% y-y in 1q13, trailing the market expected 8.0% y-y growth and the prior 7.9% y-y growth in 4q12. Industrial production grew by 8.9% y-y in Mar, after the 10.1% y-y gain in Feb. FAI rose by 20.9% y-y, slower than the 21.2% y-y pace in Feb, and trailed the market expected 21.3% pace. Retail sales reported a growth of 12.6% y-y in Mar, meeting the market expectation. The unexpected underperforming data reflected a fragile China growth recovery. (by Roy Chen) In Australia, performance services index fell slightly to 55.4 in Mar from 55.5 reading in Feb, indicating a relatively stable expansion in service industry. A separate report shows that home loan rose by 2.0% m-m in Feb, beating the market expected 1.5% m-m gain, after the 1.5% y-y fall in Jan. Investment lending rose by 1.8% m-m, after the 4.4% m-m gain in Jan, indicating a continuous expansion in the nation’s investment. (by Roy Chen)

Regional Market Focus

16 April 2013

4 of 16

Singapore The benchmark STI extended its correction yesterday by -9.82 points to end at

3,284.37 (-0.30%). There were 2.3bn shares traded worth S$1.2bn in value. The top active stocks include SPH (-5.65%), Singtel (+0.28%), DBS (-0.83%),

Ascendasreit (+2.88%), and ISDN (-2.58%). Keppel FELS announced yesterday that it won a contract worth US$226mn

(S$280mn) from a new customer, Falcon Energy Group, to build a KFELS Super B Class jack-up. Our sector analyst continues to like Keppel Corp (TP: S$12.38) as it is well positioned in the O&M sector.

Top picks for the year are Pan United (Buy, TP: S$1.21), SIAEC (Buy, TP: S$6.10) & Boustead Singapore (Buy, TP: S$1.80). Pan United is a dominant supplier to the construction industry in Singapore and we expect the company to perform well given the strong pipeline of infrastructure work over the next few years. SIAEC is a key beneficiary of the aviation growth story in the region and offers excellent dividend yields. There are hidden gems within Boustead Singapore and we believe that the stock would continue to re-rate as the market appreciates the economic moat in its businesses.

Close +/- % +/-FSSTI 3284.37 -9.82 -0.30P/E (x) 13.15P/Bv (x) 1.50

3.00Dividend Yield

STRAITS TIMES INDEX

2500

2700

2900

3100

3300

3500

4/16 7/16 10/16 1/16

Source: Bloomberg

Thailand Thai market is closed on 15 April and 16 April for Songkran Festival holiday

Close +/- % +/-SET INDEX 1527.32 10.51 0.69P/E (x) 17.59P/Bv (x) 2.50

2.81Dividend Yield

STOCK EXCH OF THAI INDEX

900

1000

1100

1200

1300

1400

1500

1600

1700

4/17 7/17 10/17 1/17

Source: Bloomberg

Indonesia

Most stocks listed on the Indonesia Stock Exchange started this week in negative tone, amid declines in Asia stock markets following lower closes on US market Friday, and disappointing China economic growth data. The Jakarta Composite Index (JCI) shed 42.618 points, or 0.86%, at 4,894.592. The decline on Monday included all major sectors. Financial sector fared worst, with 1.16%-plunge, followed by Trade and Services sector that fell 1.09%, and Basic Industry sector dropped 1.05%. The LQ45 index fell 8.526 points, or 1.02%, at 825.598, with 30 of its 45 blue-chip components ended in red. 177 stocks declined, 71 stocks advanced, and 225 stocks stayed unchanged Monday on the Indonesia Stock Exchange, where 2.79 billion shares with total value of IDR 3.4 trillion traded on the regular board. Foreign investors posted net sales of IDR 469.85 billion.

The Jakarta Composite Index (JCI) will likely continue falling on Tuesday (16/04), trailing deep losses on US markets overnight, and as stock markets in Asia started in negative territory this morning on concerns about China’s economic slowdown and rising Yen. We expect the JCI to trade lower today, with support and resistance at 4,870 and 4,937, respectively.

Close +/- % +/-JCI Index 4894.59 -42.62 -0.86P/E (x) 19.06P/Bv (x) 3.10

1.91Dividend Yield

JAKARTA COMPOSITE INDEX

3400

3900

4400

4900

5400

4/16 7/16 10/16 1/16

Source: Bloomberg

Regional Market Focus

16 April 2013

5 of 16

Sri Lanka The Colombo bourse was closed yesterday for Special Bank Holiday

Close +/- % +/-CSEALL Index 5839.88 26.51 0.46P/E (x) 11.61P/Bv (x) 1.72

2.78

Dividend Yield

SRI LANKA COLOMBO ALL SH

4500

4700

4900

5100

5300

5500

5700

5900

6100

4/16 7/16 10/16 1/16

Source: Bloomberg

Australia The Australian share market on Monday moved lower, with the benchmark

S&P/ASX200 index falling 0.91 per cent to 4,967.9 points. Today (16/04/13), the local stock market looks set to open weaker after a

negative finish on overseas markets. The SFE Futures 200 index is pointing downwards 31 points or 0.62 per cent to 4,930.

In economics news on Tuesday, the Reserve Bank of Australia (RBA) will release the minutes of its April board meeting at 1130 AEST.

In equities news, miner Rio Tinto (RIO.AU) will release its first quarter operations review.

Close +/- % +/-S&P/ASX 200 INDEX 4967.91 -45.63 -0.91P/E (x) 20.65P/Bv (x) 1.96

5.74

STANDARD & POORS/ ASX 200 INDEX

Dividend Yield

3800

4000

4200

4400

4600

4800

5000

5200

5400

4/16 7/16 10/16 1/16

Source: Bloomberg

Hong Kong

Local stocks fell. The HSI and HSCEI dropped 316 points and 215 points to 21773 and 10441 respectively.

We believe the market is going to rebound due to China’s CPI in March is lower than market expected and stocks recovered, especially for the Mainland insurance and cement sectors, investors expected the level of tighten monetary policy will not be further enhanced, we believe HSI will start a wave of rebound in short term.

However investors are suggested to maintain attention to the development of two Korea conflicts, which is a major uncertainty to the market recently, we suggest a cautious bullish view in short term.

Technically, the HSI is expected to gain a support from 21500 level, major resistance will be 22300 level.

Close +/- % +/-HSI INDEX 21772.67 -316.38 -1.43P/E (x) 10.35P/Bv (x) 1.39

3.28Dividend Yield

HANG SENG INDEX

17000

18000

19000

20000

21000

22000

23000

24000

25000

4/16 7/16 10/16 1/16

Source: Bloomberg

Regional Market Focus

16 April 2013

6 of 16

Market News

US Gold fell, extending the biggest decline since 1980, stock futures weakened in Australia and oil retreated as concern about economic

growth in China sent the commodity-led global selloff into a third day. Gold retreated 0.7 percent to $1,352.37 an ounce on the Comex as of 8:27 a.m. in Tokyo. The metal plunged 9.3 percent yesterday, the biggest drop since 1980. Australia’s S&P/ASX 200 Index futures retreated 1.3 percent, while contracts on the Standard & Poor’s 500 Index climbed 0.2 percent. Oil fell 1.6 percent to $87.28 a barrel in New York. The yen weakened against all of its major counterparts. The MSCI World Index (MXWO) posted the biggest two-day drop since November and commodities fell to a nine-month low after data showed China’s factory output weakened last month. Manufacturing in the New York region expanded less than projected in April, according to a report from the Federal Reserve Bank of New York. While U.S. stocks extended losses as explosions rocked the finish line area of the Boston Marathon, almost all of the decline came before the incident. (Source: Bloomberg)

Powerful bombs killed two people and injured scores near the finish of the Boston Marathon, turning one of the world’s oldest road races into bloody chaos. The explosions, which investigators were treating as acts of terror, occurred as recreational runners were finishing about 2:50 p.m. local time today, police said. The first, near Copley Square, caused a huge puff of white and orange smoke and was followed by a smaller one. Runners fell to the ground, which was splattered with blood. Two more explosives were found and dismantled, the Associated Press reported, citing an unnamed senior U.S. intelligence official. At least 77 people were hospitalized, with eight in critical condition, including two children, officials said. The president declined to answer a question on whether the attacks were acts of terrorism. The U.S. had no information that any foreign group was planning an attack today, said Senator Dianne Feinstein, a California Democrat who heads the Intelligence Committee. (Source: Bloomberg)

Singapore Most analysts expect developers' sales to moderate over the next few months after they hit a record 2,793 units in March, nearly four

times the 712 units sold in February. The record figure was due to pent-up demand arising from developers holding back launches in February in the aftermath of January's cooling measures and also due to the Chinese New Year festive period. April and May numbers would be "more stabilised", at around 1,500-1,600 units, says PropNex CEO Mohamed Ismail. Jones Lang LaSalle national director (research and consultancy) Ong Teck Hui reckons that developers could sell about 1,500-2,000 units monthly in the next few months. Last month's primary market sales figure of 2,793 private homes (excluding executive condos) is the highest since the Urban Redevelopment Authority began releasing developers' monthly sales data in June 2007. The last time the figure came close to this was in July 2009, when developers moved 2,772 units. (Source: Business Times Online)

RETAIL sales fell 2.7 per cent in February over the corresponding month a year ago, dragged down by motor vehicles. Excluding sales of vehicles, sales were up 10 per cent year-on-year. On a month-on-month basis (seasonally adjusted), retail sales rose 3.6 per cent in February but were up 7.8 per cent excluding receipts from motor vehicles. During the month, retailers of motor vehicles reported sales slumping by as much as 39.7 per cent over February last year, while sales of optical goods & books, furniture & household equipment and petrol service stations registered falls of nine per cent, five per cent and 4.6 per cent respectively. (Source: Business Times Online)

Thailand

The Bank of Thailand sent a letter to foreign securities firms requesting more detailed data on investment inflows into Thailand and reaffirmed that there are remaining tools to monitor the baht and the current baht level remains manageable. (Source: Bisnews)

The Ministry of Finance said Thailand’s public debt stood at Bt5.074trn or 44.05% of GDP at end-Feb 2013, against Bt5.043trn or

44.08% of GDP at end-Jan 2013. (Source: Bisnews) Kasikorn Research Center (KRC) expects the Thai baht will average between 28.05 and 31.00 to US dollar this year, adding that the

currency will gradually appreciate from now on. Every 1% rise in the baht will likely shave 1.1% off exports. KRC also believes the Bank of Thailand would intervene in the market from time to time. (Source: Bisnews)

Hong Kong

Chinese President Xi Jinping’s campaign to rein in lavish spending by officials and state-owned companies is proving so effective that it risks helping end the nation’s economic rebound after one quarter. Bank of America Corp. is among 11 of 40 respondents in a Bloomberg News survey who estimate first-quarter expansion was at or below the previous period’s 7.9 percent pace. The world’s second-largest economy probably grew 8 percent in the January- March period from a year earlier, according to the median forecast ahead of data due April 15 in Beijing, down from an 8.2 percent projection in February. (Source: Bloomberg)

Sands China Ltd. (1928), the Macau casino operator controlled by billionaire Sheldon Adelson, said it expects 2013 gaming revenue for

the Chinese territory to exceed last year, helped by more hotel rooms and rail services. Macau’s casino revenue growth rate should be in the “mid- teens” this year and higher than 2012, Chief Executive Officer Edward Tracy said in an interview in the city yesterday. (Source: Bloomberg)

Indonesia Limitation of subsidized diesel oil consumption will boost inflation in April because transportation and small and medium business sectors

will be affected, an observer said. The inflation will also be boosted with the electricity tariff increase, household consumption, high price of shallots, chili and fuel oil issues. The government in the 2013 state budget allocated IDR 274.7 trillion in subsidy expenditure with a

Regional Market Focus

16 April 2013

7 of 16

subsidy for the electricity sector amounting to IDR 80.9 trillion and for fuels accounting for IDR 193.8 trillion with a total volume of 46 million kiloliters. The volume of fuel quota could reach 53 million kiloliters if no appropriate policy is taken to control fuel consumption which has continued to increase. (Source: Antara News)

South Korean investors are interested in building power plants and infrastructure in Indonesia besides other sectors such as textile, electronic and steel industries in which they have invested. Bilateral trade and investment between South Korea and Indonesia have been expanding due to mutually beneficial and complementary economic structures. Indonesia owns huge amount of natural resources needed by South Korea, while South Korea is very competitive in the area of technology and financing. In 2012, Indonesia exported natural gas, coal, oil and other energy resources worth USD 15.7 billion to South Korea, while it imported petrochemical goods, knitted textiles, synthetic resins, hot rolled and steel sheets worth USD 13.9 billion from the latter. Meanwhile, Indonesia`s Coordinating Minister for Economic Affairs said at the Jeju Initiative meeting held in South Korea last year that South Korean investors have agreed to develop eight infrastructure projects worth USD 50 billion in Indonesia. (Source: Antara News)

Sri Lanka The flag carrier of the United Kingdom, British Airways will resume its services to Sri Lanka from the 14th of April, 2013. After a 15-year

absence, the carrier will start flights from Gatwick airport in London to Sri Lanka's Colombo international Airport in Katunayake via Male in the Maldives. The service will run three times a week on Sunday, Wednesday, and Friday on a Boeing 777-200. it will be offering three classes, flat beds in Club World class, premium economy in World Traveler plus and World Traveler standard economy seats. Sri Lanka offers immense opportunities and scope in tourism and economic growth particularly for the small and medium enterprises segment. Next to India, Britain is the second largest source of tourists for Sri Lanka with 114,218 tourists arriving in the island in 2012. (Source: colombopage.com)

Australia Woodside is facing growing calls to step up distributions to shareholders following the scrapping of plans for a $43 billion-plus liquefied

natural gas plant at James Price Point in Western Australia. Woodside on Friday confirmed that studies had found the development of its Browse gas reserves through an onshore plant at the site, north of Broome in the north of the state, to be uneconomic. (Source: The Australian)

Leighton group has acknowledged for the first time that last year's bribery scandal in Iraq "badly" damaged its reputation and that of its Middle Eastern joint venture in the war-torn country, but claims it is now positioned to win more work there after repairing relations with the Iraqi government. Leighton Holdings remains the subject of an investigation by the Australian Federal Police and was last year questioned by the Iraqi Oil Ministry's petroleum contracts and licensing directorate following claims it paid bribes for information that allowed it to win $US1.3 billion of oil contracts. (Source: The Australian)

The nation's biggest companies say the current $5.52 billion job-matching system is broken and out of touch with what bosses need, calling for major changes including a dramatic increase in work for the dole, and giving agencies "incentive" payments for getting disadvantaged people casual jobs. In a submission to the Gillard government's review of the system, the Australian Chamber of Commerce & Industry says the government must extend incentives across differing modes of employment, including to casual workers. (Source: The Australian)

Regional Market Focus

16 April 2013

8 of 16

14.7 1.50

14.1 2.50

10.4 1.39

15.5 3.10

15.2 1.96

Source: Bloomberg

Jakarta Stock Exchange Composite Index, P/B (X)

Straits Times Index, Forward P/E (X)

Hang Seng Index, Forward P/E (X)

Straits Times Index, P/B (X)

Stock Exchange of Thailand, Forward P/E (X) Stock Exchange of Thailand, P/B (X)

Jakarta Stock Exchange Composite Index,

Hang Seng Index, P/B (X)

S&P/ASX 200 Index, Forward P/E (X) S&P/ASX 200 Index, P/B (X)

10

12

14

16

18

Dec-…

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-…

Oct-1

0

Dec-…

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-…

Oct-1

1

Dec-…

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-…

Oct-1

2

Dec-…

Fe

b-1

3

1.0

1.2

1.4

1.6

1.8

2.0

Dec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

1.0

1.5

2.0

2.5

3.0

Dec-…

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-…

Oct-1

0

Dec-…

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-…

Oct-1

1

Dec-…

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-…

Oct-1

2

De

c-…

Fe

b-1

3

8

10

12

14

16

Dec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

Dec-1

2

Fe

b-1

3

1.01.21.41.61.82.02.2

Dec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

8

10

12

14

16

Dec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

Dec-1

2

Fe

b-1

3

2.22.42.62.83.03.23.43.6

Dec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

10

12

14

16

18

20

Dec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

Dec-1

2

Fe

b-1

3

1.4

1.6

1.8

2.0

2.2

Dec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

8

10

12

14

16

18

Dec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

Dec-1

2

Fe

b-1

3

Regional Market Focus

16 April 2013

9 of 16

Valuations of Major Regional Markets

14.7 1.50

14.1 2.50

10.4 1.39

15.5 3.10

15.2 1.96

Source: Bloomberg

Jakarta Stock Exchange Composite Index, P/B (X)

Straits Times Index, Forward P/E (X)

Hang Seng Index, Forward P/E (X)

Straits Times Index, P/B (X)

Stock Exchange of Thailand, Forward P/E (X) Stock Exchange of Thailand, P/B (X)

Jakarta Stock Exchange Composite Index,

Hang Seng Index, P/B (X)

S&P/ASX 200 Index, Forward P/E (X) S&P/ASX 200 Index, P/B (X)

10

12

14

16

18

De

c-…

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-…

Oct-1

0

De

c-…

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-…

Oct-1

1

De

c-…

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-…

Oct-1

2

De

c-…

Fe

b-1

3

1.0

1.2

1.4

1.6

1.8

2.0

De

c-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

Dec-1

2

Fe

b-1

3

1.0

1.5

2.0

2.5

3.0

De

c-…

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-…

Oct-1

0

De

c-…

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-…

Oct-1

1

De

c-…

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-…

Oct-1

2

Dec-…

Fe

b-1

3

8

10

12

14

16

De

c-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Aug-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

1.01.21.41.61.82.02.2

De

c-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

Dec-1

2

Fe

b-1

3

8

10

12

14

16

De

c-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Aug-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

2.22.42.62.83.03.23.43.6

De

c-0

9

Fe

b-1

0

Apr-1

0

Jun

-10

Au

g-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

Dec-1

2

Fe

b-1

3

10

12

14

16

18

20

De

c-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Aug-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

1.4

1.6

1.8

2.0

2.2

De

c-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Au

g-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

Dec-1

2

Fe

b-1

3

8

10

12

14

16

18D

ec-0

9

Fe

b-1

0

Ap

r-10

Jun

-10

Aug-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

Regional Market Focus

16 April 2013

10 of 16

Source: Bloomberg

World Index

JCI -0.86% 4,894.59

HSI -1.43% 21,772.67

KLCI -0.04% 1,697.77

NIKKEI -1.55% 13,275.66

KOSPI -0.20% 1,920.45

SET 0.69% 1,527.32

SHCOMP -1.12% 2,181.94

SENSEX 0.63% 18,357.80

ASX -0.91% 4,967.91

FTSE 100 -0.64% 6,343.60

DOW -1.79% 14,599.20

S&P 500 -2.30% 1,552.36

NASDAQ -2.38% 3,216.49 COLOMBO 0.46% 5,839.88

STI -0.30% 3,284.37

Regional Market Focus

16 April 2013

11 of 16

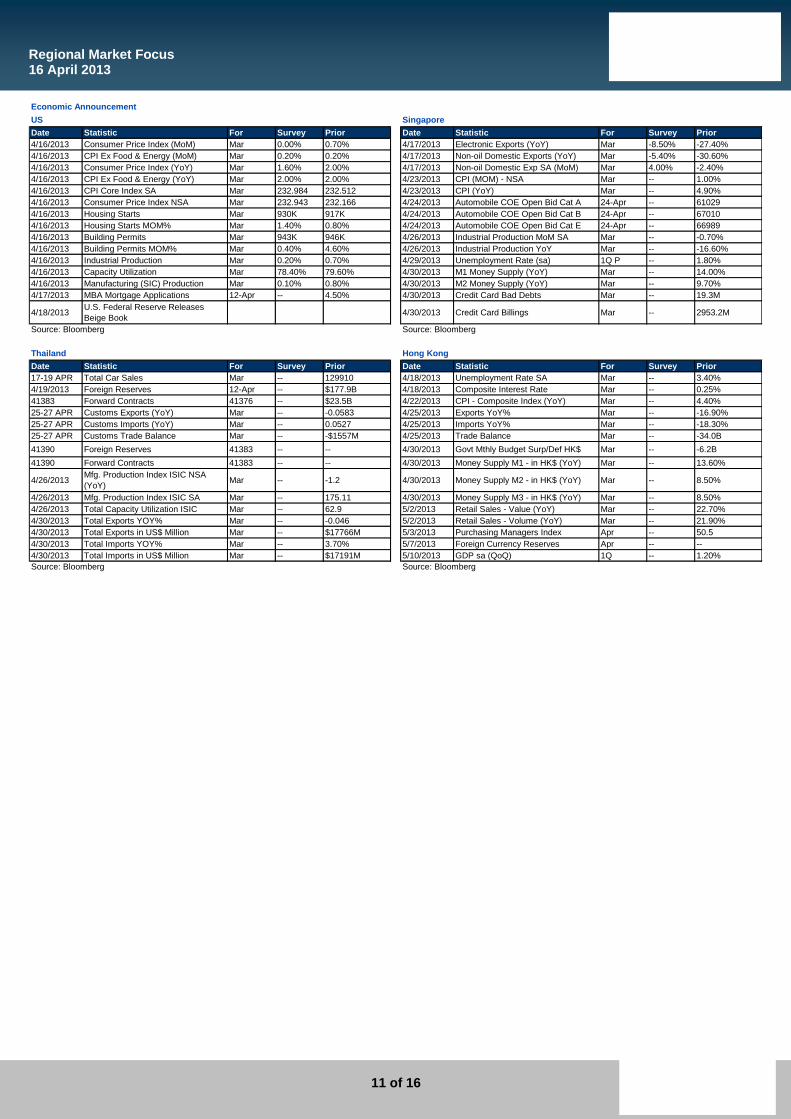

Date Statistic For Survey Prior Date Statistic For Survey Prior

4/16/2013 Consumer Price Index (MoM) Mar 0.00% 0.70% 4/17/2013 Electronic Exports (YoY) Mar -8.50% -27.40%

4/16/2013 CPI Ex Food & Energy (MoM) Mar 0.20% 0.20% 4/17/2013 Non-oil Domestic Exports (YoY) Mar -5.40% -30.60%

4/16/2013 Consumer Price Index (YoY) Mar 1.60% 2.00% 4/17/2013 Non-oil Domestic Exp SA (MoM) Mar 4.00% -2.40%

4/16/2013 CPI Ex Food & Energy (YoY) Mar 2.00% 2.00% 4/23/2013 CPI (MOM) - NSA Mar -- 1.00%

4/16/2013 CPI Core Index SA Mar 232.984 232.512 4/23/2013 CPI (YoY) Mar -- 4.90%

4/16/2013 Consumer Price Index NSA Mar 232.943 232.166 4/24/2013 Automobile COE Open Bid Cat A 24-Apr -- 61029

4/16/2013 Housing Starts Mar 930K 917K 4/24/2013 Automobile COE Open Bid Cat B 24-Apr -- 67010

4/16/2013 Housing Starts MOM% Mar 1.40% 0.80% 4/24/2013 Automobile COE Open Bid Cat E 24-Apr -- 66989

4/16/2013 Building Permits Mar 943K 946K 4/26/2013 Industrial Production MoM SA Mar -- -0.70%

4/16/2013 Building Permits MOM% Mar 0.40% 4.60% 4/26/2013 Industrial Production YoY Mar -- -16.60%

4/16/2013 Industrial Production Mar 0.20% 0.70% 4/29/2013 Unemployment Rate (sa) 1Q P -- 1.80%

4/16/2013 Capacity Utilization Mar 78.40% 79.60% 4/30/2013 M1 Money Supply (YoY) Mar -- 14.00%

4/16/2013 Manufacturing (SIC) Production Mar 0.10% 0.80% 4/30/2013 M2 Money Supply (YoY) Mar -- 9.70%

4/17/2013 MBA Mortgage Applications 12-Apr -- 4.50% 4/30/2013 Credit Card Bad Debts Mar -- 19.3M

4/18/2013U.S. Federal Reserve Releases

Beige Book4/30/2013 Credit Card Billings Mar -- 2953.2M

Date Statistic For Survey Prior Date Statistic For Survey Prior

17-19 APR Total Car Sales Mar -- 129910 4/18/2013 Unemployment Rate SA Mar -- 3.40%

4/19/2013 Foreign Reserves 12-Apr -- $177.9B 4/18/2013 Composite Interest Rate Mar -- 0.25%

41383 Forward Contracts 41376 -- $23.5B 4/22/2013 CPI - Composite Index (YoY) Mar -- 4.40%

25-27 APR Customs Exports (YoY) Mar -- -0.0583 4/25/2013 Exports YoY% Mar -- -16.90%

25-27 APR Customs Imports (YoY) Mar -- 0.0527 4/25/2013 Imports YoY% Mar -- -18.30%

25-27 APR Customs Trade Balance Mar -- -$1557M 4/25/2013 Trade Balance Mar -- -34.0B

41390 Foreign Reserves 41383 -- -- 4/30/2013 Govt Mthly Budget Surp/Def HK$ Mar -- -6.2B

41390 Forward Contracts 41383 -- -- 4/30/2013 Money Supply M1 - in HK$ (YoY) Mar -- 13.60%

4/26/2013Mfg. Production Index ISIC NSA

(YoY)Mar -- -1.2 4/30/2013 Money Supply M2 - in HK$ (YoY) Mar -- 8.50%

4/26/2013 Mfg. Production Index ISIC SA Mar -- 175.11 4/30/2013 Money Supply M3 - in HK$ (YoY) Mar -- 8.50%

4/26/2013 Total Capacity Utilization ISIC Mar -- 62.9 5/2/2013 Retail Sales - Value (YoY) Mar -- 22.70%

4/30/2013 Total Exports YOY% Mar -- -0.046 5/2/2013 Retail Sales - Volume (YoY) Mar -- 21.90%

4/30/2013 Total Exports in US$ Million Mar -- $17766M 5/3/2013 Purchasing Managers Index Apr -- 50.5

4/30/2013 Total Imports YOY% Mar -- 3.70% 5/7/2013 Foreign Currency Reserves Apr -- --

4/30/2013 Total Imports in US$ Million Mar -- $17191M 5/10/2013 GDP sa (QoQ) 1Q -- 1.20%

Source: BloombergSource: Bloomberg

Source: Bloomberg

Thailand Hong Kong

Source: Bloomberg

US Singapore

Economic Announcement

Regional Market Focus

16 April 2013

12 of 16

Date Statistic For Survey Prior Date Statistic For Survey Prior

11-22 APR Total Local Auto Sales Mar -- 103284 15-19 APR Exports YoY% Feb -- -18.20%

11-22 APR Total Motorcycle Sales Mar -- 649434 15-19 APR Imports YoY% Feb -- -21.30%

5/1/2013 HSBC-Markit Manufacturing PMI Apr -- 51.3 4/16/2013 Repurchase Rate 16-Apr 7.50% 7.50%

5/2/2013 Inflation (YoY) Apr -- 5.90% 4/16/2013 Reverse Repo Rate 16-Apr 9.50% 9.50%

5/2/2013 Inflation NSA (MoM) Apr -- 0.63% 4/24/2013Bloomberg April Sri Lanka Economic

Survey

5/2/2013 Core Inflation (YoY) Apr -- 4.21% 4/30/2013 CPI Moving Average (YoY) Apr -- 8.80%

5/2/2013 Exports (YoY) Mar -- -4.50% 4/30/2013 CPI (YoY) Apr -- 7.50%

5/2/2013 Total Imports (YoY) Mar -- 3.00% 06-20 MAY Exports YoY% Mar -- --

5/2/2013 Total Trade Balance Mar -- -$327M 06-20 MAY Imports YoY% Mar -- --

02-06 MAY Danareksa Consumer Confidence Apr -- 93.4 5/7/2013 Repurchase Rate 7-May -- --

02-10 MAY Consumer Confidence Index Apr -- 116.8 5/7/2013 Reverse Repo Rate 7-May -- --

02-10 MAY Money Supply - M1 (YoY) Mar -- 15.10% 5/31/2013 CPI Moving Average (YoY) May -- --

02-10 MAY Money Supply - M2 (YoY) Mar -- 15.00% 5/31/2013 CPI (YoY) May -- --

03-07 MAY Foreign Reserves Apr -- $104.80B 05-20 JUN Exports YoY% Apr -- --

03-07 MAY Net Foreign Assets (IDR Tln) Apr -- 985.39T 05-20 JUN Imports YoY% Apr -- --

Date Statistic For Survey Prior

4/16/2013 New Motor Vehicle Sales MoM Mar -- 0.00%

4/16/2013 New Motor Vehicle Sales YoY Mar -- 9.40%

4/16/2013 RBA Policy Meeting - April Minutes

4/17/2013Bloomberg April Australia Economic

Survey

4/17/2013 Westpac Leading Index (MoM) Feb -- 0.30%

4/18/2013 NAB Business Confidence 1Q -- -5

4/18/2013 RBA FX Transactions Other Mar -- --

4/18/2013 RBA Foreign Exchange Transactn Mar -- 328M

4/18/2013 RBA FX Transactions Govt. Mar -- --

4/23/2013 Conference Board Leading Index Feb -- 0.20%

4/24/2013DEWR Internet Skilled Vacancies

MoMMar -- -1.50%

4/24/2013 Consumer Prices (QoQ) 1Q -- 0.20%

4/24/2013 Consumer Prices (YoY) 1Q -- 2.20%

4/24/2013 CPI - Trimmed Mean (QoQ) 1Q -- 0.60%

4/24/2013 CPI - Trimmed Mean (YoY) 1Q -- 2.30%

Source: Bloomberg

Indonesia

Australia

Sri Lanka

Source: Bloomberg Source: Bloomberg

PHILLIP RESEARCH STOCK SELECTION SYSTEMS

BUY >15% upside from the current price

HOLD Trade within ± 15% from the current price

SELL >15% downside from the current price

We do not base our recommendations entirely on the above quantitative return bands. We consider qualitative factors

like (but not limited to) a stock's risk reward profile, market sentiment, recent rate of share price appreciation, presence or

absence of stock price catalysts, and speculative undertones surrounding the stock, before making our final

recommendation

GENERAL DISCLAIMER

This publication is prepared by Phillip Securities (Hong Kong) Ltd (“Phillip Securities”). By receiving or reading this

publication, you agree to be bound by the terms and limitations set out below.

This publication shall not be reproduced in whole or in part, distributed or published by you for any purpose. Phillip

Securities shall not be liable for any direct or consequential loss arising from any use of material contained in this

publication.

The information contained in this publication has been obtained from public sources which Phillip Securities has no reason

to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”)

contained in this publication are based on such information and are expressions of belief only. Phillip Securities has not

verified this information and no representation or warranty, express or implied, is made that such information or Research

is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in this

publication is subject to change, and Phillip Securities shall not have any responsibility to maintain the information or

Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip

Securities be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of

the information or Research made available, even if it has been advised of the possibility of such damages.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date

indicated and are subject to change at any time without prior notice.

This material is intended for general circulation only and does not take into account the specific investment objectives,

financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable

for all investors and a person receiving or reading this material should seek advice from a financial adviser regarding the

suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of

that person, before making a commitment to invest in any of such products.

This publication should not be relied upon as authoritative without further being subject to the recipient’s own independent

verification and exercise of judgment. The fact that this publication has been made available constitutes neither a

recommendation to enter into a particular transaction nor a representation that any product described in this material is

suitable or appropriate for the recipient. Recipients should be aware that many of the products which may be described in

this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into

transactions involving such products should not be made unless all such risks are understood and an independent

determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein

with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of a security. Any decision to

purchase securities mentioned in this research should take into account existing public information, including any

registered prospectus in respect of such security.

Disclosure of Interest

Analyst Disclosure: Neither the analyst(s) preparing this report nor his associate has any financial interest in or serves as

an officer of the listed corporation covered in this report.

Firm’s Disclosure: Phillip Securities does not have any investment banking relationship with the listed corporation covered

in this report nor any financial interest of 1% or more of the market capitalization in the listed corporation. In addition, no

executive staff of Phillip Securities serves as an officer of the listed corporation.

Phillip Securities (HK)Phillip Securities (HK)Phillip Securities (HK)Phillip Securities (HK) Ltd Ltd Ltd Ltd

2

Availability

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or

entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the

applicable law or regulation or which would subject Phillip Securities to any registration or licensing or other requirement,

or penalty for contravention of such requirements within such jurisdiction.

© 2011 Phillip Securities (Hong Kong) Limited

Phillip Capital – Regional Member Companies

SINGAPORE

Phillip Securities Pte Ltd

Raffles City Tower 250, North Bridge Road #06-00

Singapore 179101 Tel : (65) 6533 6001 Fax : (65) 6535 6631

Website : www.poems.com.sg

MALAYSIA

Phillip Capital Management Sdn Bhd

B-2-6 Megan Avenue II 12 Jln Yap Kwan Seng 50450 Kuala Lumpur Tel : (603) 2166 8099 Fax : (603) 2166 5099

Website : www.poems.com.my

HONG KONG

Phillip Securities (HK) Ltd

11-12/F United Centre 95 Queensway, Hong Kong

Tel : (852) 2277 6600 Fax : (852) 2868 5307

Website : www.poems.com.hk

THAILAND

Phillip Securities (Thailand) Public Co Ltd

15/F, Vorawat Building 849 Silom Road

Bangkok Thailand 10500 Tel : (622) 635 7100 Fax : (622) 635 1616

Website : www.poems.in.th

JAPAN

The Naruse Securities Co Ltd

4-2, Nihonbashi Kabutocho Chuo Ku, Tokyo Japan 103-0026

Tel : (81) 03-3666-2101 Fax : (81) 03-3664-0141

Website : www.naruse-sec.co.jp

UNITED KINGDOM King & Shaxson Ltd

6th Floor, Candlewick House

120 Cannon Street London EC4N 6AS

Tel : (44) 207 426 5950 Fax : (44) 207 626 1757

Website : www.kingandshaxson.com