regional electricity market janez kopaČ,director energy community secretariat conference in...

TRANSCRIPT

1

Regional electricity market

Janez KOPAČ,Director Energy Community Secretariat

Conference in Belgrade, April 25th, 2013

2

AT A GLANCE

1. Geografic scope

2. From theory to praxis The legal parameters – 2nd and 3rd IEM Package

Electricity Target Model for the 8th Region

Reality check – status quo, open challenges, outlook

3. Conclusions

3

EU electricity trading regions

Baltic Central East Central South Central West Northern

South West UK-F-IRL

4

GEOGRAPHIC TARGETEnergy Community vs 8th Region

8TH REGION

5

FROM THEORY TO PRAXISElectricty Wholesale Market Opening in the 8th Region

Legal parametersTheoretical

implementation model

Implementation in praxis

2nd and 3rd IEM package

SEE Target Model on

WMO

Jointly developed by ECRB and

ENTSO-E

Streamlined with EU electricity target model

(different deadlines)

The formal

framework for WMO in the 8th Region exists

already – political committment for real

implementation is lacking

6

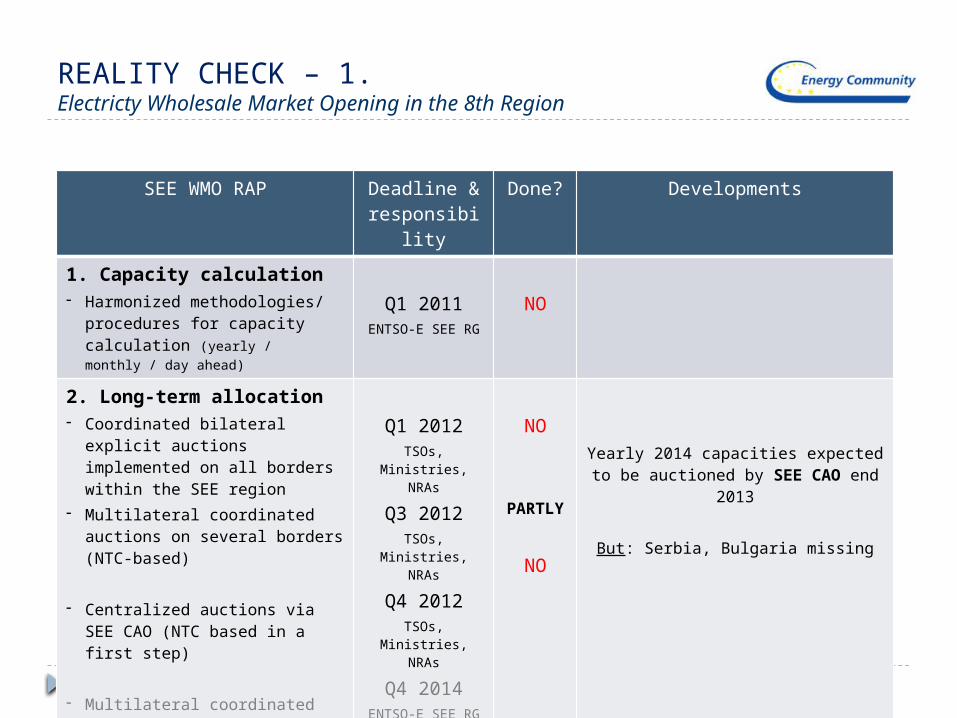

REALITY CHECK – 1.Electricty Wholesale Market Opening in the 8th Region

SEE WMO RAP Deadline & responsibility

Done? Developments

1. Capacity calculation- Harmonized methodologies/

procedures for capacity calculation (yearly / monthly / day ahead)

Q1 2011ENTSO-E SEE RG

NO

2. Long-term allocation- Coordinated bilateral explicit

auctions implemented on all borders within the SEE region

- Multilateral coordinated auctions on several borders (NTC-based)

- Centralized auctions via SEE CAO (NTC based in a first step)

- Multilateral coordinated auctions on all borders (regional one stop shop)

Q1 2012TSOs, Ministries,

NRAs

Q3 2012TSOs, Ministries,

NRAs

Q4 2012TSOs, Ministries,

NRAs

Q4 2014ENTSO-E SEE RG

NO

PARTLY

NO

Yearly 2014 capacities expected to be auctioned by SEE CAO end 2013

But: Serbia, Bulgaria missing

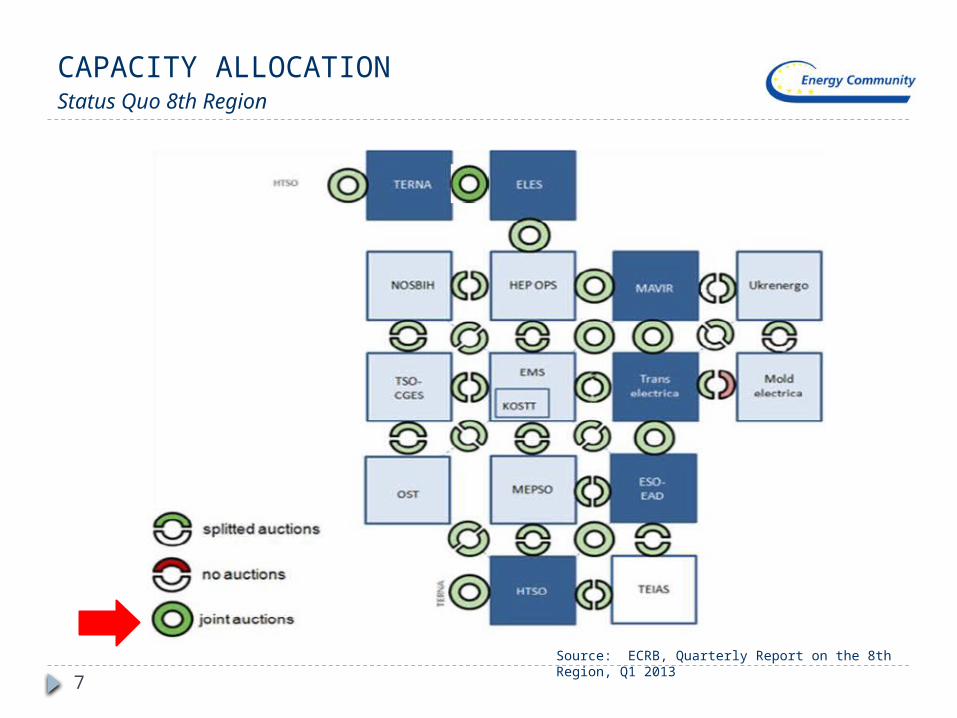

7

CAPACITY ALLOCATIONStatus Quo 8th Region

Source: ECRB, Quarterly Report on the 8th Region, Q1 2013

8

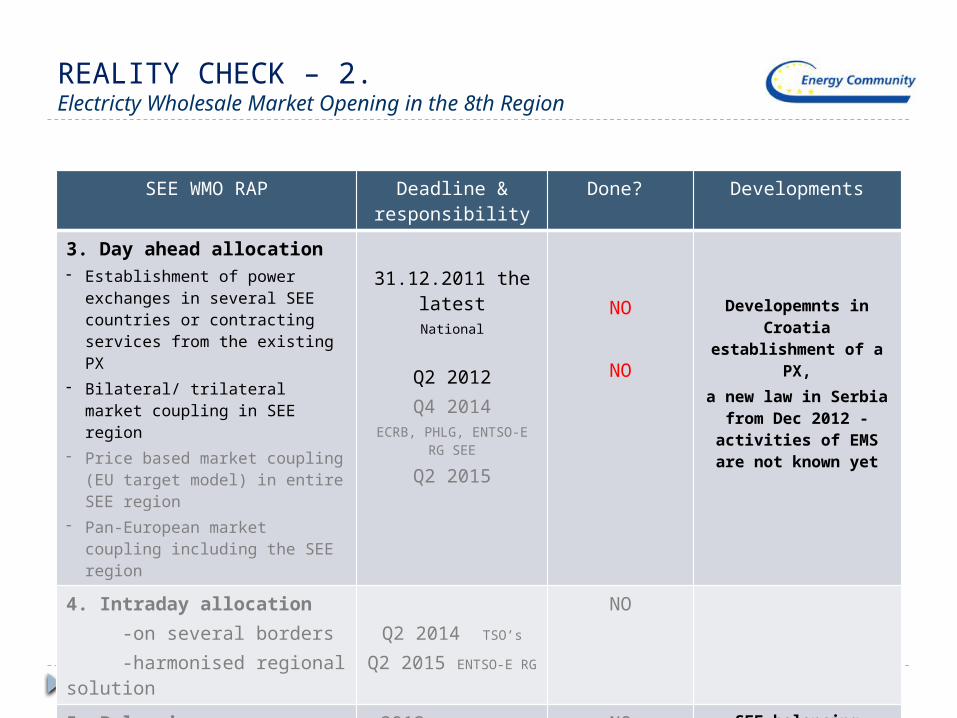

REALITY CHECK – 2.Electricty Wholesale Market Opening in the 8th Region

SEE WMO RAP Deadline & responsibility

Done? Developments

3. Day ahead allocation- Establishment of power exchanges

in several SEE countries or contracting services from the existing PX

- Bilateral/ trilateral market coupling in SEE region

- Price based market coupling (EU target model) in entire SEE region

- Pan-European market coupling including the SEE region

31.12.2011 the latestNational

Q2 2012Q4 2014

ECRB, PHLG, ENTSO-E RG SEE

Q2 2015

NO

NO

Developemnts in Croatia establishment of a PX,

a new law in Serbia from Dec 2012 - activities of EMS are not known yet

4. Intraday allocation -on several borders -harmonised regional solution

Q2 2014 TSO’s

Q2 2015 ENTSO-E RG

NO

5. Balancing 2013 NRA’s, ECRB NO SEE balancing target model

9

TO DO LIST

1. Enforced committed is needed

To abolish barriers for WMO

To complete the missing pre-conditions

2. Swift transposition and implementation of the 3rd package

3. Adoption of EU Network Codes

Active participation of Energy Community NRAs and TSOs in Network Code preparations crucial!

10

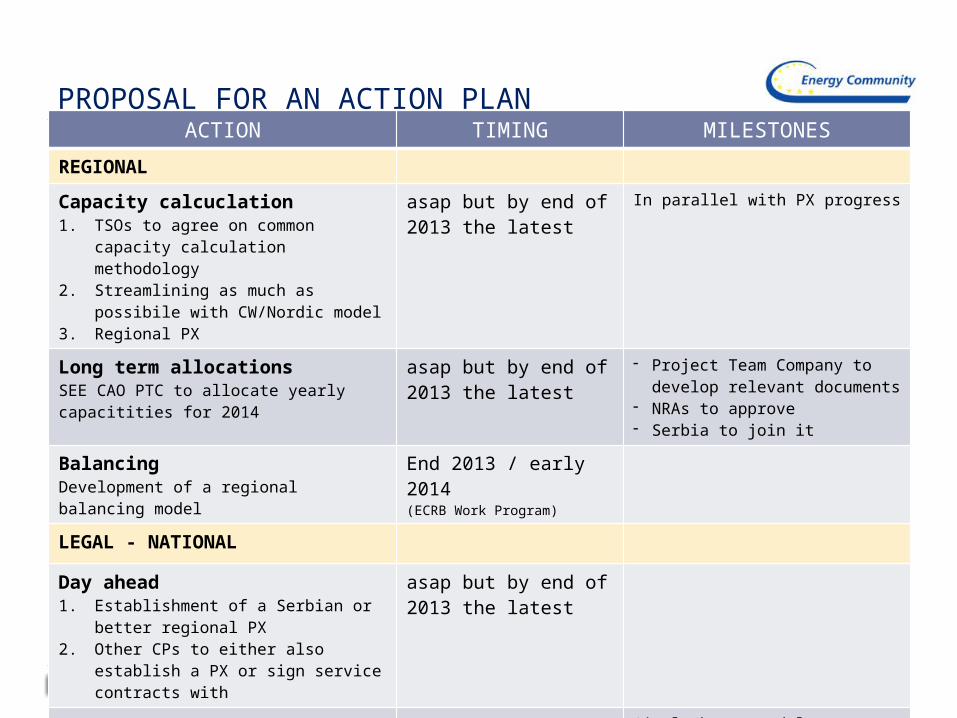

PROPOSAL FOR AN ACTION PLANACTION TIMING MILESTONES

REGIONAL

Capacity calcuclation1. TSOs to agree on common capacity

calculation methodology2. Streamlining as much as possibile with

CW/Nordic model3. Regional PX

asap but by end of 2013 the latest

In parallel with PX progress

Long term allocationsSEE CAO PTC to allocate yearly capacitities for 2014

asap but by end of 2013 the latest

- Project Team Company to develop relevant documents

- NRAs to approve- Serbia to join it

BalancingDevelopment of a regional balancing model

End 2013 / early 2014 (ECRB Work Program)

LEGAL - NATIONAL

Day ahead1. Establishment of a Serbian or better

regional PX2. Other CPs to either also establish a PX

or sign service contracts with

asap but by end of 2013 the latest

Market models1. Phasing out of regulated energy prices- WMO- End-users2. Aboloshment of single buyer models

asap Single buyer models: Albania, Ukraine, Kosovo*, FYR of Macedonia

(* This designation is without prejudice to positions on status, and is in line with UNSCR 1244 and the ICJ Opinion on the Kosovo declaration of independence.)

11

Recommendations of ECS from June 2012 (1) All Contracting Parties to ensure that eligibility is defined in line

with Article 21 of Directive 2003/54/EC, i.e. as the full and unconditional right to choose a supplier for all non-household customers. This requires in particular:

(a) a clear and compliant definition in primary law; (b) the removal of all conditions and requirements other than the status

of being a non-household customer, including references to voltage levels or electricity consumption;

(c) the removal of all administrative obstacles to exercising eligibility such as discretionary or conditional approval by regulatory authorities or market operators, registration requirements, etc.;

(d) ensuring that the right to switch supplier can be exercised continuously (not only by one particular reference date) and swiftly;

(e) the inclusion of resellers in the category of eligible customers, including public suppliers and suppliers of last resort, and the removal of all explicit or structural barriers for them to exercise their eligibility.

12

Recommendations (2)

All Contracting Parties to ensure that the electricity prices for all customers falling within the category defined for the purposes of universal service provision in the first sentence of Article 3(3) of Directive 2003/54/EC (“households and small and medium enterprises”) subject to price regulation are cost-reflective.

All Contracting Parties to ensure the cost-reflectivity of network tariffs.

All Contracting Parties to define clearly and through legislation the public service objectives pursued by price regulation as well as the notions of vulnerable customers subject to special protection or support.

All Contracting Parties to ensure that the electricity prices for all customers not falling within the category defined for the purposes of universal service provision in the first sentence of Article 3(3) of Directive 2003/54/EC (“large customers”) are not subject to price regulation .

All Contracting Parties to ensure that the market design does not impede the goals of market opening and price reforms. To that end, the possibility for public supply must be limited to small customers and may not impede eligibility. Furthermore, there must be no legal obligation for the public supplier to buy exclusively from one single generation company or wholesale supplier.

13

Acronyms CA(M) – Capacity Allocation (Mechanism) CM(P) – Congestion Management (Procedure) IEM – Internal Energy Market PX – power exchange RAP – regional Action Plan SEE – South East Europe WMO – wholesale market opening

14

THANK YOU FOR YOUR ATTENTION!

QUESTIONS?

CONTACT:

Janez Kopač

Director Energy Community Secretariat

15

Influence of coupled markets on prices