regional demand recovery outlook what the data is telling

TRANSCRIPT

1 cirium.com

Regional Demand Recovery Outlook What the data is telling us

ICAO Webinar on Air Transport Data and Analytics

Henk Ombelet– Head of Advisory Operations

D R A F T

29 September 2021

2 cirium.com

Disclaimer of Liability

The material and information contained on this presentation is for general information purposes only.

You should not rely upon the material or information on the presentation as a basis for making any

business, legal or any other decisions.

Whilst we have made every attempt to ensure that the information contained in this presentation has

been obtained from reliable sources, Cirium is not responsible for any errors or omissions, or for the

results obtained from the use of this information.

Whilst we endeavour to keep the information up-to-date or correct, Cirium makes no representation or

warranties of any kind, express or implied about the completeness, accuracy, reliability, suitability or

availability with respect to the information, products or services or related graphics contained within the

presentation for any purpose. Any reliance you place on such material is therefore strictly at your own

risk. Cirium disclaims all warranties, express or implied, including but not limited to warranties of

performance, merchantability or fitness for a particular purpose. In no event will Cirium, its affiliates or

the partners, agents or employees thereof be liable to you, you clients or anyone else for any decision

made or action taken in reliance on the information on the presentation or for any consequential,

special or similar damages, even if advised of the possibility of such damages.

3 cirium.com

Agenda

Cirium Introduction

The state of the market

Recovery and challenges

4cirium.com

Powerful data, advanced analytics and open-system – it’s in our DNA

$10bn revenues

$40bn+ market capitalization.

180+ countries served

75%+ Fortune 500 as clients

30,000+ employees in 40 countries

High growth analytics supported by Big Data

$2.8bn revenues, 8,700 employees

5 petabyte HPCC open-source big data platform

Leading world positions: agriculture, aviation, banking, finance, insurance, law enforcement, national security & petrochemicals

Group Divisions Brands

Legal

Scientific, technical & medical

Exhibitions

Aviation & Travel Sector

Private & Confidential

Risk & data services

A global provider of information-based analytics and decision tools for customers.

5

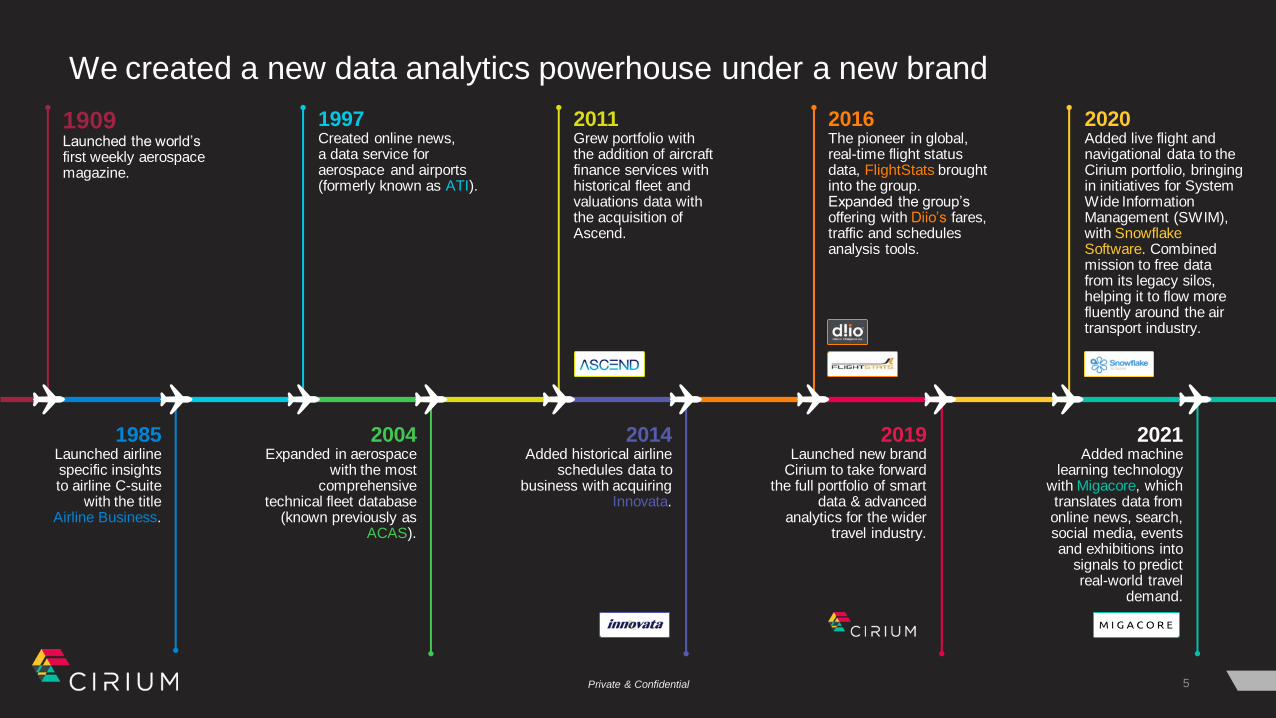

1909Launched the world’s first weekly aerospace magazine.

1997Created online news,a data service for aerospace and airports (formerly known as ATI).

2016The pioneer in global, real-time flight status data, FlightStats brought into the group. Expanded the group’s offering with Diio’s fares, traffic and schedules analysis tools.

2020Added live flight and navigational data to the Cirium portfolio, bringing in initiatives for System Wide Information Management (SWIM), with Snowflake Software. Combined mission to free data from its legacy silos, helping it to flow more fluently around the air transport industry.

1985Launched airline specific insights to airline C-suite

with the title Airline Business.

2004Expanded in aerospace

with the most comprehensive

technical fleet database (known previously as

ACAS).

2014Added historical airline

schedules data to business with acquiring

Innovata.

2019Launched new brand

Cirium to take forward the full portfolio of smart

data & advanced analytics for the wider

travel industry.

2021Added machine

learning technology with Migacore, which translates data from online news, search, social media, events and exhibitions into

signals to predict real-world travel

demand.

Private & Confidential

We created a new data analytics powerhouse under a new brand

2011Grew portfolio with the addition of aircraft finance services with historical fleet and valuations data with the acquisition of Ascend.

6cirium.com

Our mission…

We allow data to flow

fluidly, making it

available how, where

and when it is most

needed, regardless of

the systems and services

where it was created

or will be consumed

“”

Accelerating

Digital Transformation

Private & Confidential

7 cirium.com

The state of the market

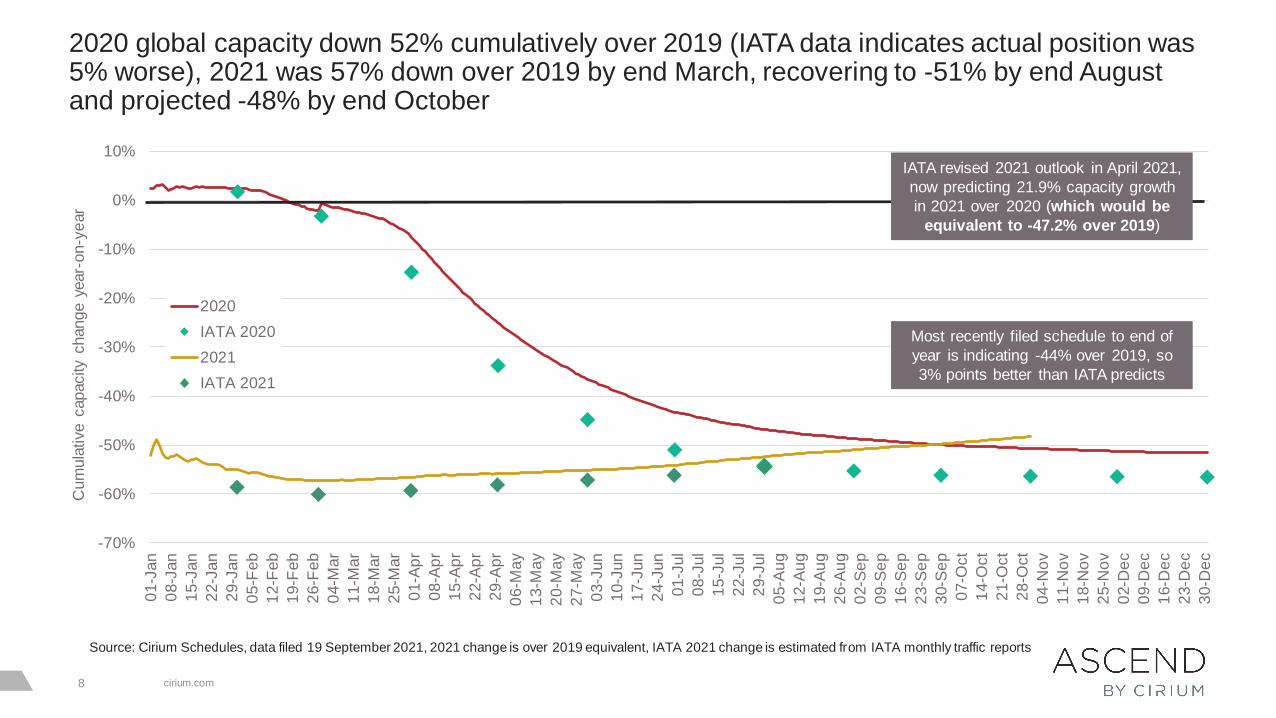

2020 global capacity down 52% cumulatively over 2019 (IATA data indicates actual position was 5% worse), 2021 was 57% down over 2019 by end March, recovering to -51% by end August and projected -48% by end October

cirium.com8

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%0

1-J

an

08-J

an

15-J

an

22-J

an

29-J

an

05-F

eb

12-F

eb

19-F

eb

26-F

eb

04-M

ar

11-M

ar

18-M

ar

25-M

ar

01-A

pr

08-A

pr

15-A

pr

22-A

pr

29-A

pr

06-M

ay

13-M

ay

20-M

ay

27-M

ay

03-J

un

10-J

un

17-J

un

24-J

un

01-J

ul

08-J

ul

15-J

ul

22-J

ul

29-J

ul

05-A

ug

12-A

ug

19-A

ug

26-A

ug

02-S

ep

09-S

ep

16-S

ep

23-S

ep

30-S

ep

07-O

ct

14-O

ct

21-O

ct

28-O

ct

04-N

ov

11-N

ov

18-N

ov

25-N

ov

02-D

ec

09-D

ec

16-D

ec

23-D

ec

30-D

ec

Cum

ula

tive c

apacity

change y

ear-

on-y

ear

2020

IATA 2020

2021

IATA 2021

Most recently filed schedule to end of

year is indicating -44% over 2019, so

3% points better than IATA predicts

IATA revised 2021 outlook in April 2021,

now predicting 21.9% capacity growth

in 2021 over 2020 (which would be

equivalent to -47.2% over 2019)

Source: Cirium Schedules, data filed 19 September 2021, 2021 change is over 2019 equivalent, IATA 2021 change is estimated from IATA monthly traffic reports

China domestic showing recovery following significant decline in August, US domestic market also projecting improvement to only 3% down over 2019 by end October, Europe continues strong summer recovery into October, Intra-Asia remains >65% down through September

cirium.com9

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

Daily

capacity

change y

ear-

on-y

ear

(rolli

ng 7

-day

ave

rag

e)

US Domestic Intra-S America Intra-Europe Intra-Asia China Domestic

Source: Cirium Schedules, data filed 19 September 2021, 2021 change is over 2019 equivalent

Long-haul all remained 60%-70% down over 2019 through end August 2021, Trans-Atlantic showing improvement through September and October, also slow improvement on Europe-Asia but all still down 50-70% by end September

cirium.com10

-100%

-80%

-60%

-40%

-20%

0%

20%

Daily

capacity

change y

ear-

on-y

ear

(rolli

ng 7

-day

ave

rag

e)

Trans-Atlantic Trans-Pacific Europe-Asia

Source: Cirium Schedules, data filed 19 September 2021, 2021 change is over 2019 equivalent

Global completed flights is back where we were a month ago, with no real change at the moment, nor any indication of improvement or otherwise.

cirium.com11

Source: Cirium FlightStats Includes all global scheduled passenger flights

0%

10%

20%

30%

40%

50%

60%

70%

0

20,000

40,000

60,000

80,000

100,000

120,000

Perc

enta

ge c

ancelle

d f

lights

Num

ber

of

flig

hts

Completed Cancelled 7 day mov avg - completed 7 day mov avg - percentage cancelled

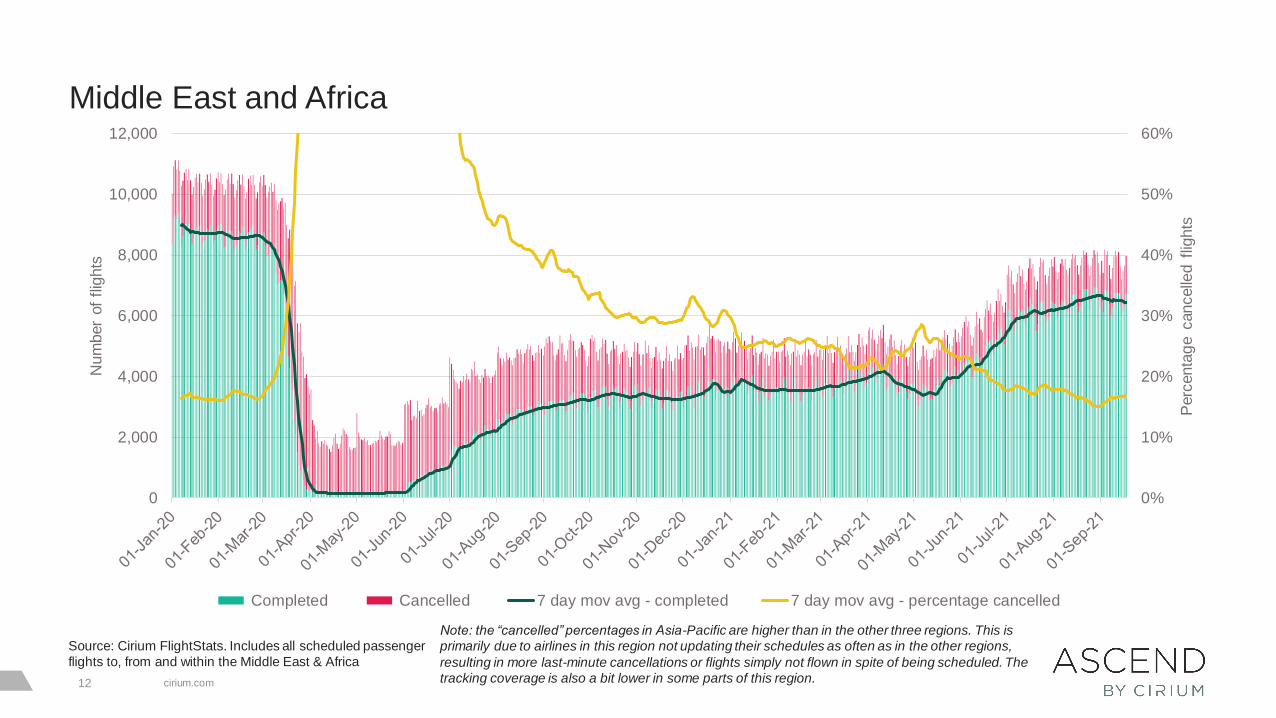

Middle East and Africa

cirium.com12

Source: Cirium FlightStats. Includes all scheduled passenger

flights to, from and within the Middle East & Africa

0%

10%

20%

30%

40%

50%

60%

0

2,000

4,000

6,000

8,000

10,000

12,000

Perc

enta

ge c

ancelle

d f

lights

Num

ber

of

flig

hts

Completed Cancelled 7 day mov avg - completed 7 day mov avg - percentage cancelled

Note: the “cancelled” percentages in Asia-Pacific are higher than in the other three regions. This is

primarily due to airlines in this region not updating their schedules as often as in the other regions,

resulting in more last-minute cancellations or flights simply not flown in spite of being scheduled. The

tracking coverage is also a bit lower in some parts of this region.

Fleet tracking starting to recover back to growth trend as China fleet increases again, marginal growth continues in Asia-Pacific (excluding China) this week, all other regions stable or showing marginal declines over last week

cirium.com13

Source: Cirium utilisation data, commercial passenger jets, utilisation data for aircraft tracked on a daily basis only

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Glo

bal

aircra

ft t

racked d

aily

Single-Aisle

Twin-Aisle

11,908 single-aisle aircraft

tracked on 17 September 2021

vs 14,083 on 3 January 2020

2,518 twin-aisle aircraft tracked

on 17 September 2021 vs

4,089 on 3 January 2020

Average daily utilisation largely stable since early July

cirium.com14

4

5

6

7

8

9

10

11

12

13

14

Fle

et

ave

rag

e d

aily

flig

ht

hours

Single-Aisle

Twin-Aisle

Twin-aisle down on average

16% since start of 2020

Single-aisle down on average

15% since start of 2020

Source: Cirium utilisation data, commercial passenger jets, utilisation data for aircraft tracked on a daily basis only

68 Airline restructurings and bankruptcies

cirium.com15

Source: Cirium Fleets Analyzer

A319, 85

A320, 288

A321, 81

A330, 81

A340, 11A350, 26

A380, 6737 (All),

281

787, 67

767, 41747, 11

777, 49

Turbo props,

86

Embraer E-

Jets, 115

Other, 237

A320neo,

154

A321neo, 39

A350, 4

737 Max,

109

787, 5

777F, 1

ATR72/42, 5

A220, 4

ARJ21, 5

Aircraft in service/storage Aircraft on order

Note: this data only includes airlines

quoted on the previous slide

16 cirium.com

Recovery and challenges

17 cirium.com

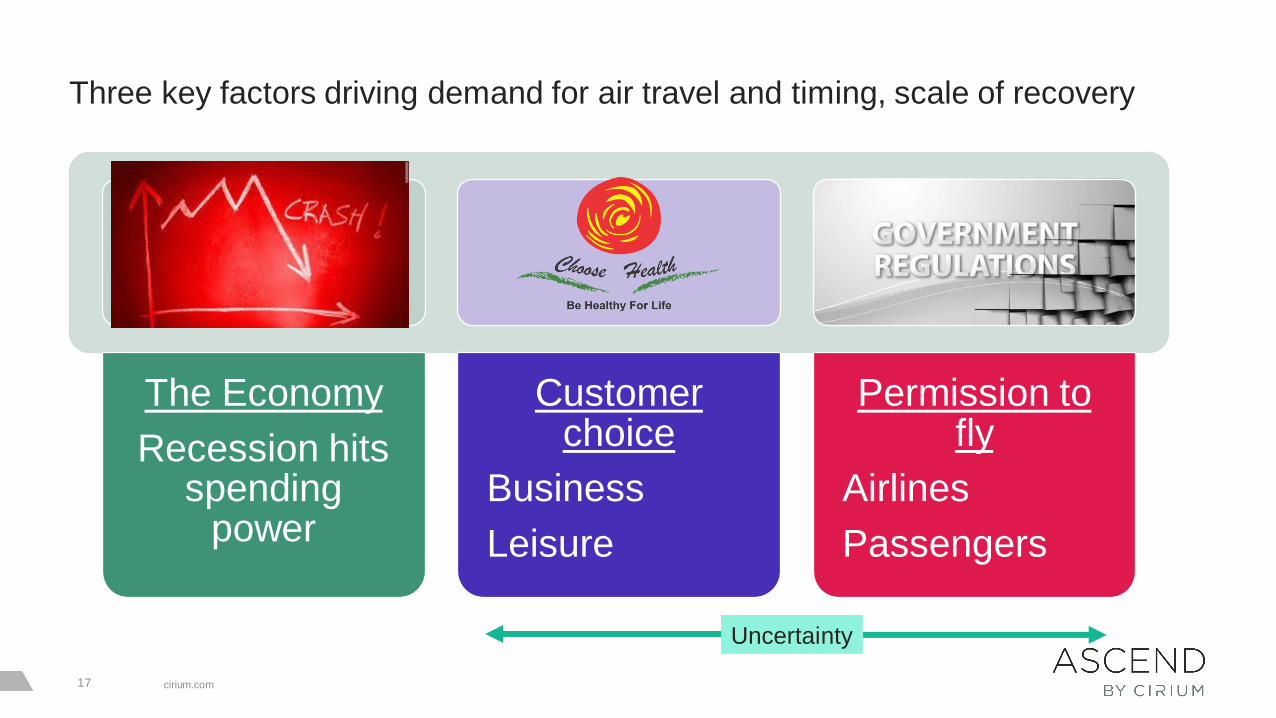

Three key factors driving demand for air travel and timing, scale of recovery

The Economy

Recession hits spending

power

Customer choice

Business

Leisure

Permission to fly

Airlines

Passengers

Uncertainty

18 cirium.com

For GDP, a return to ‘Normal’ growth levels suggested, with Asia leading the way

-8

-6

-4

-2

0

2

4

6

8

% G

DP

gro

wth

Regional GDP Growth Expectations to 2025

Asia and Australasia - [19] Eastern Europe - [13]

Latin America - [20] Middle-East and North Africa - [19]

North America - [2] Sub-Saharan Africa - [17]

Western Europe - [21]

Source: EIU Sep 21

19 cirium.com

Signposts to scenarios

cirium.com19

Issue Signposts – timing/nature varies by scenario

Covid-19 scenario Rate of new cases, Pace of vaccine roll-outs.

Economic forecast GDP forecast levels, direction of change of forecasts, PMIs

Demand recovery IATA traffic releases, Forward schedule, airline ASK announcements, flights flown, level of

cancellations, Travel Agent survey

Travel restrictions Timing of domestic, intra-regional, intercontinental easing. Timing of international travel within EU of

particular note.

Airline environment Airline bankruptcies, lease returns, market values and lease rates

Fleet surplus Fleet in-service, utilisation levels, load factor

OEM production OEMs maintain production at minimum viable rates, before slow recovery in deliveries from 2022

20 cirium.com

‘Opening up’ scenarios based on >70% of adult population vaccinated

Date by when 70% expected to be

fully vaccinatedCountries – ranked by population/ASKs

NowMost of EU, UK, China, Brazil, Canada,

Singapore, Israel, UAE, Chile

Q4 2021

USA, Japan, Mexico, Turkey, South

Korea, Argentina, Morocco, Saudi Arabia,

Malaysia, Australia, Ecuador, Cambodia

Q1 2022Thailand, Colombia, Peru, Taiwan, Kazakhstan,

Tunisia

Q2 2022 India, Indonesia, Russia

H2 2022 Pakistan, Philippines, Vietnam, South Africa,

2023 or later Bangladesh, Ukraine, most of Africa, others

21 cirium.com

Recovery to 2019 demand levels is not synchronous, but in both scenarios long-haul lags domestic and regional, driving at least two more years of sub-2019 demand

cirium.com21

Scenario 4 Scenario 5

Asia Pacific May 2024 March 2023

Europe March 2025 May 2023

North America December 2024 September 2023

China April 2023 September 2022

Latin America October 2024 July 2023

Middle East January 2025 April 2024

Africa June 2025 March 2024

Russia/CIS July 2024 June 2023

World total August 2024 May 2023

Source: Ascend by Cirium Scenario Analysis, total market

July 2021 RPKs down 53.1% vs 2019, a 7% point improvement on June, August expected to be down 52-56%

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

0

100

200

300

400

500

600

700

800

900

1000

Change v

s 2

019

RP

K (

bn)

RPK S3 RPK S4 RPK S5 RPK actual RPK change actual RPK change S4

cirium.com22

Source: Cirium schedules, Ascend by Cirium analysis, IATA (Load Factor)

23 cirium.com

Passenger fleet in service is increasing ahead of more optimistic recovery scenario (S5)

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

22000

Aircra

ft in a

irlin

e p

asseng

er

serv

ice

Actual NB fleet Actual WB fleet Total fleet S1 Total fleet S4 Total fleet S3 Total fleet S5

cirium.com23

Source: Cirium Fleets Analyzer, Ascend by Cirium analysis

24 cirium.com

Aviation Outlook

Conclusions

GDP has been the key driver of long term airline traffic growth

and remains so, but environmental concerns moving up

agenda

Covid-19 dramatically impacted GDP and traffic forecasts. In

addition, consumer health concerns and government

restrictions have reinforced the impact on aviation

The reduction in passenger traffic seen in 2020, around 12

times the level of reduction in GDP, is completely

unprecedented

While GDP growth has turned positive in 2021, traffic

recovery remains stilted

Domestic and regional routes have recovered fastest

Recovery of global traffic could be expected by 2023/4 but

likely many different impacts will be seen on route networks

The continued viability of many elements of the aviation and

travel and tourism supply chain is still uncertain.