recent development in corporate taxation wrt mat, … · recent development in corporate taxation...

TRANSCRIPT

Recent Development in Corporate Taxation wrt MAT, FBT, ESOP & deduction

u/s 10A, 10B and 80IA

June 18, 2008

Rajan R Vora

2008 – Issues in Direct TaxPage 2

Key Amendments2007 & 2008

2008 – Issues in Direct TaxPage 3

Key Amendments in Corporate Tax – Budget 2007► No surcharge if the total taxable income of the company or firm is less

than Rs 1 crore► whether education cess be leviable in such case?

► Dividend distribution tax (‘DDT’) raised from 12.5% to 15% (wef April 1, 2007)

► TDS rates under Section 194-I, 194J and 194H changed as under (wef June 1, 2007)► TDS on rent for use of machinery/ plant equipment reduced to 10%► TDS on professional services, royalty and FTS increased to 10%► TDS on brokerage / commission income increased to 10%

► Profits of 10A and 10B units liable for MAT ► SEZ units and income exempt under Section 10 not liable for MAT (need

not be registered under the SEZ Act)► In case of demerger or amalgamation of undertakings after April 1,

2007 deduction under Section 80-IA not available

2008 – Issues in Direct TaxPage 4

Key Amendments in Corporate Tax – Budget 2007► Payments made after April 1, 2007 otherwise than by account payee

cheque, liable for total disallowance under Section 40A(3)► Employee stock options (‘ESOPs’) made liable for FBT

2008 – Issues in Direct TaxPage 5

Key amendments in Corporate Tax – Budget 2008► Short-term capital gains tax rate on sale of listed securities increased

from 10% to 15%► ‘Book profit’ to be increased by deferred tax and provision thereof for

MAT purposes► Amendments retrospective from April 1, 2001► A few contrary Court rulings impliedly stand overruled

► Banking Cash Transaction Tax (BCTT) withdrawn from April 1, 2009► Aggregate payment made to a person in a day in excess of Rs 20,000

otherwise than by an account payee cheque/ bank draft to be disallowed

► “Book depreciation” (not tax depreciation) to be taken into account for determining the WDV of assets for assessees becoming liable to tax; who were not liable to tax prior years

2008 – Issues in Direct TaxPage 6

Key amendments in Corporate Tax – Budget 2008► Incentives and exemptions

► Extension of tax holiday benefits under Section 10A/10B – now available upto AY 2010-2011 (but subject to MAT)

► 5 year tax holiday currently granted to certain hospitals, extended to hospitals located at other places in India (Some metro cities excluded), subject to conditions

► 5 year tax holiday currently granted to 2 / 3 / 4 star hotels extended to hotels located in specified districts having a World Heritage Site

2008 – Issues in Direct TaxPage 7

Key amendments in Corporate Tax – Budget 2008► Cascading effect of DDT mitigated

► DDT would be payable by a domestic company on dividends, as reduced by dividends received from a subsidiary company, provided,► such dividend received has been subjected to DDT and the domestic

company is not a subsidiary of another company► Indian companies having more than 2-tier structures not benefited► Amendment not to benefit foreign companies having subsidiaries in India

► Due date for filing return of income, FBT return and obtaining tax audit report changed to 30th September of the assessment year (AY 2008-09) for corporate assessees and assessees liable to audit under the Act

2008 – Issues in Direct TaxPage 8

MAT – Recent Developments

2008 – Issues in Direct TaxPage 9

MAT - Amendments

► Finance Act 2007► Profits of units eligible for deduction under Section 10A & 10B are liable

to MAT► SEZ unit entitled to deduction under Section 10AA not liable to MAT► Will units set up in SEZ (not under the SEZ Act) be eligible for MAT?

► Finance Act 2008 (applicable retrospectively from April 1, 2000)► Book profits should be increased by deferred tax and provisions thereof

for computing the MAT liability► Book profits to be increased by income-tax and provision thereof for

computing MAT liability► Clarified that income-tax to include tax on distributed profits/ income,

interest, surcharge and cess

2008 – Issues in Direct TaxPage 10

MAT - issues

► Whether profit on sale of asset directly credited to reserve to be included in book profits

► Decisions in favor of not including such profits

( favourable to assessee)► ITO Vs Frigsales (India) Ltd (4 SOT 376) ► ITO Vs Su-raj Jewellery (India) Ltd (21 SOT 79) ► Oriental Containers Ltd Vs JCIT (19 SOT 30) ► Sutlej Cotton Mills Ltd Vs ACIT ( 45 ITD 22)► Parle International Ltd Vs ITO (ITA No 94/Ahd/04)► CIT Vs Kovai Maruthi Paper & Board (P) Ltd. (168 Taxman 299)► CIT vs Vijayashree Finance and Investment Co. Pvt. Ltd. (2008) 2

DTR 38 (Mad)

2008 – Issues in Direct TaxPage 11

MAT - issues

► Against assessee► RSDV Finance Co. (P) Ltd. Vs ACIT (66 ITD 378)► CIT Vs Veekaylal Investment Co.(P) Ltd. (249 ITR 597) (Bom)

► Whether provision for bad and doubtful debts is an ascertained or unascertained liability and whether the same should be reduced while calculating book profits

► Sums set aside to to meet known liabilities of which amount cannot be accurately estimated does not fall within the definition of provisions and is a accrued or ascertained liabilityFavourable Decisions► JCIT & Ors vs Usha Martin 288 ITR 63 (SB) (Kol)► Peerless Gen. Fin. and Inv Co Vs ACIT 107 TTJ 186 (Kol)

2008 – Issues in Direct TaxPage 12

MAT - issues

► Whether option is available to set off current year’s profit against the loss brought forward or unabsorbed depreciation in a manner different from the manner adopted in Section 115JB?

► Change of method – whether entire depreciation can be written off? ► Whether current years profit can be setoff against brought forward

loss or depreciation in a manner beneficial to assessee?Unfavorable decisions► Rashtriya Ispat Nigam Ltd Vs CIT 285 ITR 1 (AAR)

2008 – Issues in Direct TaxPage 13

FBT – Recent Developments

2008 – Issues in Direct TaxPage 14

FBT – amendments – Budget 2008

► Due date for filing return of FBT for corporate and other specified assesses preponed from 31 October to 30 September

► Scheme for centralised processing of FBT returns introduced► No FBT liable on following

► Non transferable pre-paid electronic meal cards usable at eating joints or outlets

► Expenditure on providing creche facility for employees children,sponsorship of employee sportsperson and organising sports event for employees

► Maintenance of guest house accommodation► Value of fringe benefits on account of festival expenditure reduced from

50% to 20% of total expenditure ► Other amendments

► Certain expenses such as free food and non-alcoholic beverages, gift, token or voucher, etc; on which the employer is not liable to pay FBT would now be taxable in the hands of the employee as perquisites(Valuation rule reintroduced) - implications

2008 – Issues in Direct TaxPage 15

First Decision on FBT-Supreme Court

► Whether levy of FBT in case of transportation of offshore employees from their residence in the home country (overseas) to the place of work in India and back is exempt?► Judgment in the case of R & B Falcon (A) Pty Ltd (Supreme Court) 301

ITR 309

2008 – Issues in Direct TaxPage 16

FBT on ESOPs – concept of ESOPs

Grant Vesting Exercise Sale

► Grant Date► Vesting

Period► Unvested

Option

► Vesting Date

► Exercise Period

► Vested Option

► Exercise Date

► Exercise Price

► Sale after release of lock-in

Stages of a Stock Option Plan

2008 – Issues in Direct TaxPage 17

FBT on ESOPS

► FBT is liable on ESOP from 1st April 2007 ie AY 2008-2009► FBT is payable on the value of fringe benefit to the employee (ie net

of recovery)► Value of fringe benefit shall be the “Fair Market Value” of Shares on

the “date of vesting” of securities reduced by the amount paid by/or recovered from employee

► However, FBT payable by the employer at the “time of exercise” of the options by the employees

► The rate of FBT would be 30% plus applicable surcharge and education cess

► The employer can recover the FBT paid on ESOPs from the employee

► Whether the amount of FBT recovered from employees is considered as a cost of acquisition of shares?

2008 – Issues in Direct TaxPage 18

FBT on ESOPS – contd…

► FBT will now be recognized as tax paid by the employee in connection with a claim of tax credit in a foreign country by the employees

► Will FBT be applicable in case where shares are granted by a foreign holding company to the employees of its subsidiaries

► If yes, whether the FBT would be payable by the foreign company or the Indian subsidiary

► Recovery of FBT from employees to be retained by whom?► Clarification by Circular 9/ 2007► Microsoft decision – 235 ITR 565 (AAR)

2008 – Issues in Direct TaxPage 19

Other IssuesExplanatory Circular 9/2007

2008 – Issues in Direct TaxPage 20

Whether SARs are subject to FBT?

► Stock Appreciation Rights (SARs) are essentially in the nature of cash salary payable to the employee, the actual quantum of which is decided with reference to appreciation in the market price of shares of the employer

2008 – Issues in Direct TaxPage 21

10A/10B - Issues

2008 – Issues in Direct TaxPage 22

10A/10B - Issues

► Wordings of Section 10A different from erstwhile 80I► Whether deduction under section 10A/10B should be computed

before giving effect to unabsorbed business losses and unabsorbed business losses and unabsorbed depreciation ?

► Whether reversal of provisions, write back of expenses, foreign exchange fluctuation gain or income from scrap sales eligible for tax holiday?► Whether the above should be regarded as turnover?► Wipro Limited vs DCIT (96 TTJ 211) (Bang)

► In case of profit “true-ups” by the assessee based on mutually agreed and accounted arm’s length transfer pricing margins, whether the amount of true-up needs to be realized like “export turnover” while determining eligibility to the Tax holiday?► What is the position in case a transfer pricing adjustment is made by the

TPO? – Act► What is the position in case a voluntary transfer pricing adjustment is

made by the assessee himself – I Gate Global Solutions (112 TTJ 1002 Bang)

2008 – Issues in Direct TaxPage 23

10A/10B - Issues

► Whether losses of one STP unit be set off against the business income or income from other sources without harming the deduction/ profits of the other STP unit?► Ms Datamatics Technologies vs Asst CIT (ITA No 78/6/MUM/04)► Mindstree (102 TTJ 691 Bang)► Honeywell International India P Ltd (108 TTJ 924 Del) ► I Gate Global Solutions (112 TTJ 1002 Bang)► Sovika infoteck Ltd (ITA no 8073/M/04) (Mum)

2008 – Issues in Direct TaxPage 24

10A/10B - Issues

► Formula for working of deduction gives absurd results► Export turnover of undertaking/ total turnover of assessee

► Is it necessary that an undertaking is formed with new employees in formation of a new undertaking eligible for tax holiday?► Conversion of DTA into STP/ EOU

► Whether tax holiday would be available in following circumstances► STP units develops software products and physically exports or

electronically transports software outside India to the customer?► STP unit develops software product and physically exports or

electronically transmits outside India to a duplicator on a nominal amount and royalty is received on sales?

2008 – Issues in Direct TaxPage 25

80IA/80IB Issues

2008 – Issues in Direct TaxPage 26

80IA/80IB Issues

Issues for Consideration► Wordings of old Section 80I different from Section 80IA/ 80IB ► Whether brought forward losses and unabsorbed depreciation

pertaining to an undertaking need to be set off against current year’s profit of the relevant undertaking, prior to computing deduction under section 80-IA ?

► Will the answer to the above remain the same in case the assessee has also earned interest income or income from other sources?

2008 – Issues in Direct TaxPage 27

80IA/80IB Issues

legal fictions created under the sections in Chapter VIA

► Section 80-IA(5)/80-IB(13) of the Act► IPCA Laboratory Ltd 266 ITR 521 (SC)► Shirke Construction Equipment Ltd 291 ITR 380 (SC) ► Synco Industries Ltd. Vs. AO (299 ITR 444) (SC)

2008 – Issues in Direct TaxPage 28

Rule 8D -Amendments

2008 – Issues in Direct TaxPage 29

Recent Amendment-Rule 8D

► Section 14A of the Act provides that the expenditure incurred inrelation to income not includible in total income of a tax payer shall not be allowed as a deduction in computing the taxable income

► Section 14A(2) inserted wef 1/4/2007 (AY 2007-2008) bestows powers on the AO to determine the amount of disallowance in accordance with the prescribed method, where:► the AO is not satisfied with the correctness of the claim or► when no expenditure has been incurred in relation to exempt income

2008 – Issues in Direct TaxPage 30

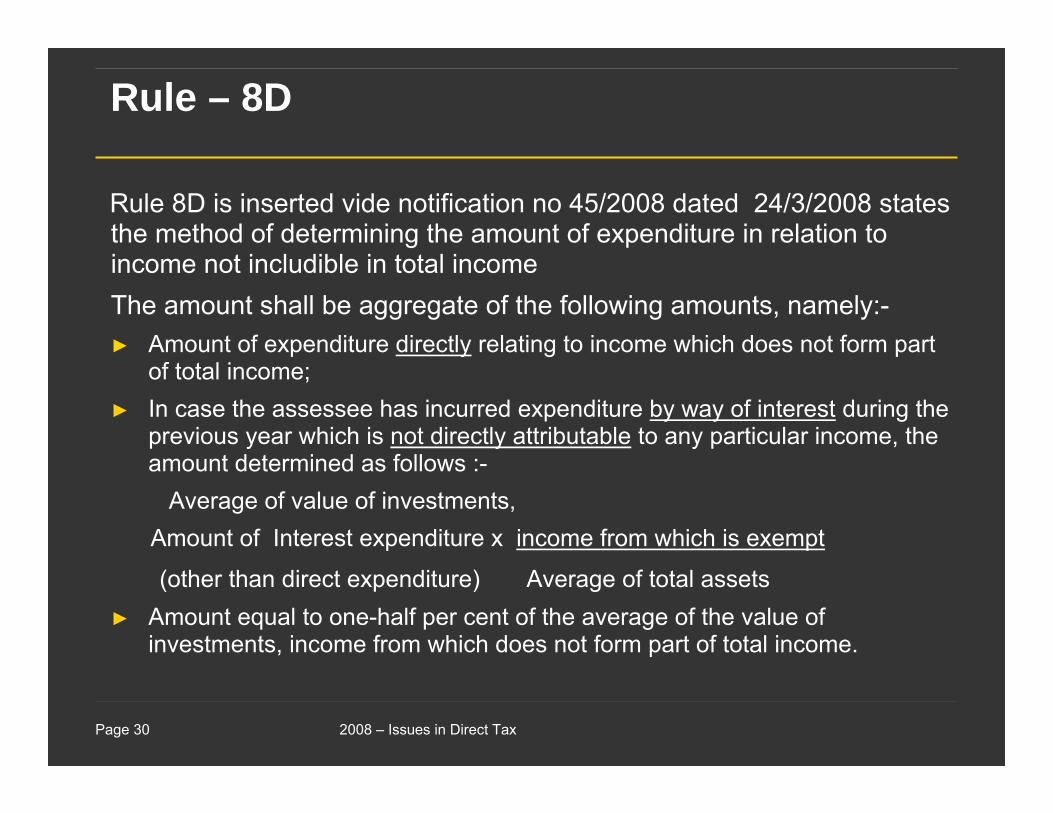

Rule – 8D

Rule 8D is inserted vide notification no 45/2008 dated 24/3/2008 states the method of determining the amount of expenditure in relation to income not includible in total income The amount shall be aggregate of the following amounts, namely:-► Amount of expenditure directly relating to income which does not form part

of total income;► In case the assessee has incurred expenditure by way of interest during the

previous year which is not directly attributable to any particular income, the amount determined as follows :-

Average of value of investments,Amount of Interest expenditure x income from which is exempt

(other than direct expenditure) Average of total assets► Amount equal to one-half per cent of the average of the value of

investments, income from which does not form part of total income.

2008 – Issues in Direct TaxPage 31

Open issues

Open issues:► Whether the methodology as stated in Rule 8D will have

retrospective effect from A.Y 2007-2008 or w.e.f AY 1962-63?► Whether the said rule will apply to all pending tax cases?

2008 – Issues in Direct TaxPage 32

Decisions – stand taken

► Decisions where amendment to Section 14A held to be applicable to all pending assessments.► ACIT vs Citi Corp Finance (India) Ltd 108 ITD 457 (Mum)► Kalpataru Constructions overseas (P) Ltd vs DCIT 13SOT 194 (Mum)► DCIT vs Seksaria Biswar Sugar Factory Ltd 14SOT 66 (Mum)► Prakash Heat Treatment and Industries (P) Ltd vs ITO 14SOT 348

(Mum)► DCIT vs Smita Conductors Ltd 16SOT 251 (Mum)► Narotam Das Bhau vs ACIT 15SOT 629 (Mum)► Conwood Agencies (P) Ltd vs ITO 15SOT 308 (Mum)► Aquarius Travels P Ltd v ITO (114 TTJ 584 DEL) (SB)

► Other issues – adhoc/ proportionate disallowances► Dhanlaxmi Bank v ACIT (12 SOT 625)► ACIT v Citicorp Finance (India) Ltd (12 SOT 248) (MUM)

2008 – Issues in Direct TaxPage 33

Issues

► Whether Section 14A is applicable in the case of investments held as stock-in-trade?► Vidyut Investments Ltd vs ITO 10SOT 284 (Del)► Matter currently before the Special Bench for consideration in the

case of Daga Securities, Mumbai

2008 – Issues in Direct TaxPage 34

Deemed Dividend - Issues

2008 – Issues in Direct TaxPage 35

Issues

► Deemed Dividend – Sec.2(22)► Registered share holder or beneficial owner (Rameshwarlal Sanwarmal

vs CIT (122 ITR 1) SC► Shares held in individual name and on behalf of minor children –

calculation of voting power (CIT vs Sokkalal 236 ITR 981) Madras► Loan deemed as dividend – interest on such loan taxability as perquisite

[CIT v T.P.H.S Selva Saroja (2000) 244 ITR 671, 685,-86 (Mad)]► Loan deemed as dividend – used for business – deductibility of interest

on such loan (Nandlal Kanoria vs CIT (122 ITR 145)► Repayment of loan has no impact on taxability of dividend Sarada v

CIT(1998) 229 ITR 444, 448(SC) & [Tarulata Shyam v CIT (1971) 82 ITR 485, 494 (CAL, affirmed, (1977) 108 ITR 345(SC)]

► Transactions carried on in the normal course of business cannot be treated as loan or advance. Transaction by book entries cannot be equated with granting of loans or advance. (NH Securities Ltd. 11 SOT 302 Mum Trib)

2008 – Issues in Direct TaxPage 36

Issues

► Meaning of term “accumulated profits”► Current profits ► Commercial profits or tax profits [Tea Estates India Private Limited

(1972) 86 ITR 705]► Statutory reserves – investment allowance reserve – 80IB reserve

etc. [P.K.Badiani (1976) 105 ITR 642 (SC)]► Repayment of loan will not replenish accumulated profits

► Book Entries not loan [G.R. Govindarajulu Naidu V CIT (1973)90 ITR 13 (Mad)] & (CIT vs Smt Savithri Sam 236 ITR 1003) Madras

► Accumulated profits not restricted to % of holding of the share holder in the company

Thank you