really final project

TRANSCRIPT

Letter of Transmittal

Date: 29 April, 2012

To Bashir HossainProfessor, Department of BBANorth South University

Subject: Submission of Internship Report.

Dear Sir,

With due respect I am stating that I am Tamanna Sharmin is submitting my Internship

report on “Customer satisfaction with mortgage loan of Standard Chartered Bank ”

for your kind evaluation , as part of my requirement of completing the BBA program.

I acknowledge with thanks for wholehearted support and kind guidance received from

you, I would like to mention that there might be some unintentional error in this

report. I hope that you will consider my shortcomings while you evaluate my paper.

Sincerely Yours

Tamanna SharminID: 072 350 030Department of BBANorth South University

Page 1

Acknowledgement

I would like to begin by thanking the Almighty for giving me physical and mental

strength and blessings to successfully carrying out the Internship Report. In

performing the internship, I was specially exposed to the real life experience. I also

feel it is a unique opportunity for me to learn about the practical work and customer

interaction in a reputed organization. This internship improved my knowledge and

attitude about the field to a large extent.

I am grateful to my respective supervisor Professor Bashir Hossain; Lecturer,

Department of Business Administration for allowing me to do such an interesting and

knowledgeable Internship Report on Standard Chartered Bank Bangladesh and for his

outstanding support and specific direction which made this reports almost a faultless

one. Wonderful ideas and factual path showing are the specialties of those directions.

The report topic is “Customer Satisfaction With Mortgage Loan of Standard

Chartered Bank”. I have done the whole report based on the information from primary

and secondary data.

And my special thanks to my supervisor Abdul Quaium sir, Head of loan operations,

Tareq Hasan, Manager, Loan operations of Standard Chartered Bank, Head office for

their enormous and continual effort and guidance for the successful completion of the

Report. My thanks also goes to Zahid vai, Ashraf vai and Limon vai, Ayesha Nayar,

Ahrar Masud, Officer of SCB for their heartier coordination to understand each and

every task, to work with this product ‘Mortgage Loan’.

And it is my great pleasure to work on this topic as a student of Department of

Business Administration, North South University. For that reason my gratefulness is

always to the Department of Business Administration as a whole.

Page 2

EXECUTIVE SUMMARY

This report is prepared to fulfill the requirement of the course program and it is

concerned about the enlargement of the knowledge regarding the business

environment specially the multinational banks in Bangladesh. As banking is the most

thriving industry in our country, the students of business administration should have a

clear understanding of the procedure through which the private commercial banks and

as well as the multinational banks in our countries operate their business. The

multinational banks in Bangladesh are successfully operating their business and they

are contributing on the country’s economy. They also provide assistance to the local

banks in Bangladesh and help them in expanding their business. Through this report

we have tried to find out the customer satisfaction in terms of mortgage loan of the

renowned multinational bank, Standard Chartered Bank (SCB). In this report one

could find out the different aspect of SCB like history of the bank, their vision and

their overall performance. So here we have shown their performance for the last three

months. Most of the customers are not satisfied with the performance of the loan

sanction. Some of them think that the department is very effective in their work

because they take instant action for the wrong processing and they also inform the

customers about any incomplete instruction. The one disadvantage is they take high

charges for the processing. Overall the whole process of preparing this report was a

stiff learning curve for us.

Standard Chartered Bank is in its 60th year of business in Bangladesh since 1948. It

has built up an enviable goodwill and reputation over the years with sincere and

dedicated service, which saw generations of customers supporting the bank to the top

position where it stands today. Its operation in Bangladesh was further widened and

strengthened by the global acquisition of Grindlays from ANZ Banking Group by the

Standard Chartered for a staggering US$ 1.34 billion in July 2000. This not only

brought in the largest network of a foreign bank in Bangladesh to the disposal of

Page 3

Standard Chartered, but also provided them with a huge customer base. Though

Standard Chartered and Standard Chartered Grindlays were two separate legal

entities, yet in practical terms they have integrated wholly. From January 01, 2003

both of the banks were operating their activities in Bangladesh by renaming them

officially as Standard Chartered Bank and has changed their LOGO.

Standard Chartered Bangladesh today is faced with challenges. Internally, it has

inherited the largest retail customer base of any foreign bank in Bangladesh from

Grindlays. Managing this base along with its existing customers and synchronizing

the operations of the two parts of the bank is a daunting task. Though the Bank is

equipped with modern information technology and a skilled well-trained force

amongst other strengths, yet maintaining the service standards remains a challenge.

Externally, it has to face up to the local commercial banks and foreign banks. The

market scenario in recent years has undergone changes with a number of local private

and foreign banks entering into the market. Besides, the customer today is more

conscious of the quality of service and the benefit offered by various banks and has a

wide array of choices. In the face of such challenges it has become imperative for

Standard Chartered to maintain the level of customer satisfaction and to explore ways

and means to improve it. Therefore, it is crucial for the bank to ascertain the

satisfaction level and reasons for discontent.

The general image of Standard Chartered Bank is that it is “Responsive,

Trustworthy, International, Creative and Courageous.” In Bangladesh Standard

Chartered Bank is primarily consumer finance driven. Standard Chartered services in

Bangladesh, ranges from Personal & Corporate Banking to Institutional Banking,

Treasury and Custodial services The Consumer Banking Service generates more

revenue for its bank. So maintaining the customer satisfaction is the key challenge.

Mortgage loan was launched by SCB in 05August; 2006.SCB launched it with the

lowest interest rate in Bangladesh. And it has cut a very good figure in the total loan

disbursement on the month of January, February and March in Gulshan branch (Head

Office). Because of its competitive interest rate and opportunity for large amount, it

Page 4

has become one of the attractive products to the SCB customers rather than other

banks. I was appointed in the Head Office of Standard Chartered Bank.

The topic of my report is “Customer satisfaction with Mortgage loan of Standard

Chartered Bank” For that reason both Secondary and Primary data collections have

taken place. The analysis is done on the basis of those data. In the secondary data

analysis loan disbursement was shown for the month of January, February and March.

In the primary data analysis, it is found that most of the customers took Mortgage loan

to purchase apartment. There were some factors which motivated customers to take

Mortgage loan but when they applied for it and availed the loan then the real scenario

appeared. Customers thought that there will be low processing fee. But after having

the loan, customers expressed their reaction. SCB should maintain the quality for

which people are satisfied. Such as after analyzing it shows three major source of

satisfaction is interest rate, no hidden charge and opportunity for large amount. The

factors for which they are dissatisfied should be minimized, like high processing fee,

early settlement fee. Customers are more logical and conscious than before. They

must hunt for their benefits. So SCB should make proper decision to capture the best

exposure.

After the analysis and the findings some recommendations are also suggested

regarding service and the loan offer for the next.

Page 5

Me Tamanna Sharmin , student ID: BBA 072 350 030, student of Bachelor of

Business Administration (BBA) major in Marketing from North South University

Bangladesh do hereby declared that this report entitled “Customer Satisfaction in

terms of Mortgage loan” submitted by me to North South University for the

Graduation of B.B.A (Bachelor of Business Administration) degree is of my own and

has not submitted to any other university or institute for the award of any degree as

well as this paper may not use any actual market scenario

Page 6

STUDENT’S DECLARATION

ACKNOWLEDGEMENT

Page 7

Introduction

Page 8

1.Introduction

Standard chartered Bank (SCB) is the most popular bank in the world. It is operating

its business Bangladesh as a multinational bank for more than 100 years. Because of

its wide range of coverage and experience it provides various types of unique

products and service.

Today, Standard Chartered Bank is the largest international bank in Bangladesh with

26 Branches, 57 ATMs and 7 Financial Kiosks; employing over 1,300 people. We are

the only foreign bank in the country with presence in 6 cities – Dhaka, Chittagong,

Khulna, Sylhet, Bogra and Narayanganj; including the country's only offshore

banking units inside Dhaka Export Processing Zone (DEPZ) at Savar and Chittagong

Export Processing Zone (CEPZ). First international bank to extend credit lines to

Bangladesh and open the first external letter of credit (LC) in Bangladesh in 1972 .

Financial Institutions business is the largest contributor to USD Clearing in New York

A leading price player in treasury instruments and foreign currencies Leader and

pioneer in Consumer Banking

The bank increasingly invested in people, technology and premises as its business grew in relation to the country's thriving economy. We currently provide both Consumer Banking and Wholesale Banking Services, ranging from Personal & Corporate Banking to Institutional Banking, Treasury and Custodial services. Extensive knowledge of the market and essential expertise in a wide range of financial services underline our strength to build business opportunities for corporate and institutional clients in Bangladesh. Continuous upgrading of technology and control systems has enabled the bank to offer new and improved services such as Phonebanking, I-banking, e-Lending.

Page 9

Standard Chartered is very much renowned in terms of Loan operations. They have a

range of loans they offer to its consumer in exchange of guaranty and interest. Theses

are Personal Loan, SME, Auto loan, Mortgage loan, Home loan, CIB(Credit

Information Burro), Consumer Credit & Collections (CCU). The first four are known

as the value centers (VC). WM is the liability VC, while the other 3 are the asset VCs.

VCs are the owners of the respective products and sub-products. They are also

responsible for development of new products, promotion & sales of all their products

and maintenance of their portfolio. The last one is the most important part nowadays

in every bank because of the order of Bangladesh Bank`s new regulation.

This VC is the owner of personal loan (PL). The sub products include gift card, travel

cards, unsecured/ partially secured personal loans, Islamic finance etc. Auto VC is the

owner of 2 products - AL & IPF, and all the sub products. They are also responsible

for all the legal matters pertaining to these products. Mortgage VC is the owner of 3

products – ML,SHBL & SHF, and all the sub products. They are also responsible for

all the legal matters pertaining to these products.

Mortgage loan was launched by SCB in 05August; 2006.SCB launched it with the

lowest interest rate in Bangladesh. And it has cut a very good figure in the total loan

disbursement on the month of January, February and March in Gulshan branch (Head

Office). Because of its competitive interest rate and opportunity for large amount, it

has become one of the attractive products to the SCB customers rather than other

banks. I was appointed in the Head Office of Standard Chartered Bank.

.1.1Background

Banks are the most prominent among the financial institutions to create credit and

thus help in different economic activities. All sorts of economic and financial

activities revolve round the axis of the bank. As the industry produces goods and

commodities, so does the bank creates and controls money-market and promotes

formation of capital. From this point of view, banking-a technical profession- can be

termed as industry. Services to its customers are the products of banking industry

besides being a pivotal factor in promoting capital formation in the country.

Commercial banks are the primary contributors to the economy of a country. It helps

Page 10

to flow funds from surplus unit to deficit unit and through this it facilitated the

efficient allocation of the resources as well as accelerated economic growth. This

sector is moving towards new dimension as it is changing fast due to competition,

deregulation and financial reforms. In the modern day banks are playing a significant

role in a country’s economy. As all economic and fiscal activities revolve round this

important 'Industry', the role of banking can hardly be over emphasized. To ascertain

the role of banks and to analyze its operational aspects and its overall impact on our

national economy a thorough study as to its distribution, expansion and contribution is

essential to comprehend its past, present and future bearings for the growth and

development of the banking sector of the country. In the global context, the role of

banks is far - reaching and more penetrating in the economic and fiscal discipline,

trade, commerce, industry, export and import- all carried through the bank. Banks are

the only media through which international trade and commerce emanate and entire

credit transactions, both national and international.

1.2Origin of the report

I have been assigned to do my Internship program in Standard Chartered Bank,

Gulshan Branch; for the academic requirement of Department of Business

Administration. Internal supervisor Professor Bashir Hossain; Lecturer, Department

of Business Administration has assigned to conduct the research study on the topic

“CUSTOMER SATISFACTION WITH MORTGAGE LOAN OF STANDARD CHARTERED

BANK”. After approving the proposal, both the Internal and External supervisor has

assigned this topic to work with Internship program which is a prerequisite for BBA

degree. Actually classroom discussion solely cannot make students to be acquainted

with the real life situation; therefore it is an opportunity for the students to know

about the practical environment of the real business world through this program. It is

a stimulating opportunity and a valuable experience for me to view real business

world. Working in SCB helped me in heartening my theoretical knowledge. And it

will carry greater values for the carrier also.

1 . 3 1 . 3 O b j e c t i v eO b j e c t i v e

The objectives are as follows:

Page 11

Broad objective

To measure the “customer satisfaction with mortgage loan of SCB’

Specific Objective

To identify the overview of mortgage loan procedure.

To discover the total loan disbursement from Gulshan branch and show the

contribution of mortgage loan among the total loan disbursement

Identifying the motivating factors for choosing the mortgage loan of SCB

Analyze the customers satisfaction factors

Analyze the dissatisfaction factors that customers considering

1.4 Significance

This report mainly tends to determine the customer satisfaction of mortgage loan that

Standard Chartered Bank’s CBS (Consumer Banking Service) customers expect and

to what extent Standard Chartered has been able to meet them. The banks and

branches surveyed are all within the geographical location of Dhaka city. The survey

included the customers’ of-SCB only in Gulshan branch. And it opened the door of

being familiarized with the banking environment. The report does not stand as a

universal remedy for the Standard Chartered Bank nor is it the final job regarding the

issue. Further study may take place in the same scope and this can be used as the prior

work in the field.

1.5 Methodology

To meet the objectives of the report, different methodology is used to acquire as well

as to analyze the data. To evaluate the customer selection criteria to provide the

mortgage loan, face to face conversation was conducted with the respective officers of

Gulshan Branch and with Mr. Tareq, manager of mortgage. To identify the

customer’s satisfaction with mortgage loan among various loan products of SCB,

questionnaire survey was conducted. In this research the numbers of respondents were

limited who take Mortgage loan from Gulshan Branch(Head office) of SCB. A

summary of the methodology is provided below:

Page 12

1.4.1 Research Design: Both primary and secondary data were collected. After

collecting the data; the analysis is done mainly with the help of some application

software like MS-Excel. Other methods are also used as per requirement of the report.

Questioner findings are presented in graphical view.

Data Collection Method:

Formal questionnaire for data collection will be use. Sample will be collected from

the general and priority customer of At the same from Standard Chartered Bank.

Information will be collected through informal discussions with Relationship

managers & respective Branch Manager.

Data have been collected from two sources. These are as follows:

A) The Primary Sources of Data:

Face to face conversation with the bank officers and staff.

Direct conversation with the clients.

File study of different section.

Desk work: During my practical orientation I worked according to

the following routine.

B) The Secondary Sources of data:

Annual Report of Standard Chartered Bank.

Different publications of Standard Chartered Bank.

Unpublished data received from the Branch.

Different text books.

Websites

Magazine, Journals, Newspapers.

Bangladesh Bank Database.

Analysis will be done with the help of SPSS software. Statistical tools such as

hypothesis Test, ANOVA, Pearson Chi-square, cross tabulations, Z-test/T-test,

Correlation, Regression, Will coxon, will be also be used in the analysis process.

Page 13

1.4.2 The Sampling Process:

Selection of the population will be defined as----

Elements: All the available customers of Standard Chartered Bank of Gulshan

branch,

Sampling Unit: Direct Customers

Area: Dhaka Metropolitan City

The Sample Size: Since maximum number of customers who have taken mortgage

loan stay in Dhaka, it would give us the mirror image of satisfaction of mortgage

customers of other areas. Considering the time constraint, the sample size had to be

reduced to 56 of the total sample size of 287.

1.6 Source of data

The report is constructed upon both primary and secondary sources of information.

They are:

1.5.1 Primary data collection

Personal interview with the mortgage manager of SCB.

Face to face conversation with the respective officers of the bank.

Questionnaire survey to Mortgage loan borrowers.

1.5.2 Secondary data collection

- SCB’s Annual report of 2011.

- Monthly, quarterly and Half yearly Statements of loan from Gulshan

Branch office.

- The Booklet of Standard Chartered Group.

- Filtered data table of disbursed ‘Mortgage loan’

- Website of SCB www.bd.standardchartered.com

1.7Limitation

Confidentiality of Bank data was another constraint that was faced during

the study. As part of the policy of the Standard Chartered Bank, some data that

could not be used to enhance the parameter of the analysis. Because, maintaining

the secrecy of such data is important to the bank’s interest.

Page 14

Limitation of time was one of the most important factors that shortened the

present study. Due to time constraints, many aspects could not by discuss in

the present study.

Because of time and cost constraint it is not possible to conduct large

number of borrowers for making more productive.

Page 15

COMPANY

OVERVIEW

Page 16

2.STANDARD CHARTERED BANK: AN OVERVIEW

Standard Chartered is the world's leading emerging markets bank headquartered in

London. Its businesses however, have always been overwhelmingly international.

Today Standard Chartered is the world's leading emerging markets bank employing

30,000 people in over 500 offices in more than 50 countries primarily in countries in

the Asia Pacific Region, South Asia, the Middle East, Africa and the Americas.

Standard Chartered is listed on both the London Stock Exchange and the Stock

Exchange of Hong Kong and is in the top 25 FTSE-100 companies, by market

capitalization.

It serves both Consumer and Wholesale Banking customers. Consumer Banking

provides credit cards, personal loans, mortgages, deposit taking and wealth

management services to individuals and small to medium sized enterprises. Wholesale

Banking provides corporate and institutional clients with services in trade finance,

cash management, lending, custody, foreign exchange, debt capital markets and

corporate finance. The Bank combines deep local knowledge with global capability.

The Bank is trusted across its network for its standard of governance and its

commitment to making a difference in the communities in which it operates.

2.1 Motivational factors in Standard Chartered Bank

Standard Chartered supports the rights of the individual as expressed in the 1948

United Nations Universal Declaration of Human Rights (UDHR).

The UDHR contains a number of fundamental rights, which SCB aims to uphold in

all circumstances, including:

The right to life

The right to legal recognition as a person

Freedom of thought, conscience and religion

Freedom of opinion and expression

Freedom from torture

Freedom from cruel, inhumane or degrading treatment

Freedom from slavery and servitude

Page 17

2.2 Vision of SCB

Previously according to “ANZ Grind lays Bank” Nov 1994, its vision statement was

follows:

“We are renowned as the top performing banking group service in Australia, New

Zealand and international market. Provide the greatest return to our shareholders by

achieving some profitable growth. Be perceived by customers and stuff as the best

wherever we operate, have the stuff of the highest caliber. Excel in the way we work

together to make decision and get things done. We will achieve this position by the

end of 1998 and sustain it where after.”

After the acquisition the new vision is one bank one message

“The best of the best-that’s what we’re determined to become! Our aim is for

Standard Chartered to be the worlds leading emerging bank. We will concentrate what

we do best.”

At Standard Chartered our success is built on teamwork, partnership and the diversity of our people.

At the heart of our values lie diversity and inclusion. They are a fundamental part of our culture, and constitute a long-term priority in our aim to become the world's best international bank.

Today we employ 75,000 people, representing 115 nationalities, and you'll find 60 nationalities among our 500 most senior leaders. We believe this diversity helps to fuel creativity and innovation, supporting the development of exciting new products and services for our customers worldwide.

What we stand for

Strategic intent The world's best international bank Leading the way in Asia, Africa and the Middle East

Brand promise

Page 18

2.3 Principles & Values

Leading by Example to be The Right Partner

Values Responsive Trustworthy International Creative Courageous

Approach Participation

Focusing on attractive, growing markets where we can leverage our relationships and expertise

Competitive positioning

Combining global capability, deep local knowledge and creativity to outperform our competitors

Management Discipline

Continuously improving the way we work, balancing the pursuit of growth with firm control of costs and risks

Commitment to stakeholders Customers

Passionate about our customers' success, delighting them with the quality of our service

Our People

Helping our people to grow, enabling individuals to make a difference and teams to win

Communities

Trusted and caring, dedicated to making a difference

Investors

A distinctive investment delivering outstanding performance and superior returns

Regulators

Exemplary governance and ethics wherever we are

Page 19

2.4 Business & Strategy

By combining our global capabilities with deep local knowledge, we develop innovative products and services to meet the diverse and ever-changing needs of individual, corporate and institutional customers in some of the world's most exciting and dynamic markets.

Personal Banking

Through our global network of over 1,750 branches and outlets, we offer personal financial solutions to meet the needs of more than 14 million customers across Asia, Africa and the Middle East.

SME Banking

Our SME Banking division offers a wide range of products and services to help small and medium-sized enterprises manage the demands of a growing business.

Wholesale Banking

Headquartered in Singapore and London, with on-the-ground expertise that spans our global network, our Wholesale Banking division provides corporate and institutional clients with innovative solutions in trade finance, cash management, securities services, foreign exchange and risk management, capital raising, and corporate finance.

Page 20

Islamic Banking

Standard Chartered Saadiq's dedicated Islamic Banking team provides comprehensive international banking services and a wide range of Shariah compliant financial products that are based on Islamic values.

Private Banking

Our Private Bank advisors and investment specialists provide customised solutions to meet the unique needs and aspirations of high net worth clients.

Our people, our values

We are one of the world's most international banks in terms of the diversity of our people. Our 75,000 employees, representing 115 nationalities, are exposed to exciting career opportunities as a result of our unique global footprint.

Our board of directors

Our leaders reflect the diversity that drives Standard Chartered's success and makes us one of the world's most international banks.

Our global team

The Bank offers a well-rounded career that is truly global in scope. Our size and reach facilitate exposure to international banking standards and work experience by

Page 21

2.5People

providing employees with opportunities to travel, interact and learn from other cultures.

Each year as many as 20 per cent of our employees get expanded role opportunities. Over 2,000 of our employees are on cross-border assignments at any one time.

Nearly half of our employees are women, and almost 60 nationalities are represented among the senior management, reflecting the bank's policy towards providing equal opportunity for all employees.

Last year (2007) was the most successful year for Standard Chartered Bank. In the

year of 2007 SCB has got several most important awards which were very significant

for the bank and those awards will certainly help the bank to perform more better way

than the previous years. The awards which the Standard Chartered Bank got are:

Asian Legal Business SouthEast Asia Awards 2007

Global Finance Best Emerging Markets Bank Awards 2007

Global Finance World's Best Internet Banks Awards

Trade Finance Awards for Excellence 2007

Euromoney Awards for Excellence 2007

FinanceAsia Country Awards for Achievement 2007

2.7 HISTORY OF SCB - a year wise progression:

SCB has a history of more than 150 years. The name “Standard” stems from the two

original banks from which it was founded-“Chartered Bank” of India, Australia and

China and “Standard Bank” of British South Africa.

Chartered bank was established in 1853 by a Royal Charter granted by Queen

Victoria of England. The main person behind the Chartered Bank was a Scot, James

Wilson who had also started “The Economist” still one of the most eminent

publications today. He foresaw the advantages of financing the growing trade links

with the areas in the East, where no other financial institution was present that time

widely.

1853

Page 22

2.6Achievement of SCB

Set up by James Wilson in 1853, at the request of Queen Victoria, the Standard

Chartered Bank aimed to finance and manages trade between the British Empire and

its colonies in India, Australia and China. It mainly operates in Asia-Pacific, Latin

America, the Middle East and Africa. In all, it has 500 branches in 56 countries.

1858

The overseas branch of the Chartered Bank opened in Calcutta, Bombay and

Shanghai followed by Hong Kong and Singapore in 1859.

1862

The Standard Bank is incorporated in England and under the new title of The

Standard Bank of British South Africa Limited.

1957

The Chartered Bank and The Standard Bank incorporated as Standard and Chartered

Banking Group Limited.

1969

Merger of The Standard Bank and The Chartered Bank by the incorporation of

Standard and Chartered Banking Group Limited

1973

Standard Chartered acquires the Hodge Group, whose operating company later

becomes Chartered Trust Limited.

1985

Parent company of the group renames Standard Chartered PLC. Standard Chartered

Bank becomes a clearing bank within the UK clearing system.

1993

Receive the very first ‘Best Bank in Asia’ awards from Euromoney magazine.

2000

On 27 April, ANZ announced the sale of its Grindlays businesses in the Middle East

and South Asia, and associated Grindlays Private Banking business, to Standard

Chartered PLC. ANZ announces US$8 million strategic investment in Hong Kong,

online stockbroker, BOOM.com. ANZ announces sales of Grindlays to Standard

chartered for US$1.3 (A$2.2) billion in cash.

2004 and onwards

Number of shares 1,174,520,020. Number of employees (31/12/2003) 30,000. It has

500 branches in 56 countries. At present the bank has 18 offices in Bangladesh. In

Page 23

Bangladesh Standard chartered Bank has more than 620 permanent employees

(31/12/2005)

2.8 Global Market

Expansion in Africa and Asia:

The Standard Bank opened for business in Port Elizabeth, South Africa, in 1863. It

pursued a policy of expansion and soon amalgamated with several other banks

including the Commercial Bank of Port Elizabeth, the Coles berg Bank, the British

Kaffarian Bank and the Fauresmith Bank. The Standard Bank was prominent in the

financing and development of the diamond fields of Kimberly in 1867 and later

extended its network further north to the new town of Johannesburg when gold was

discovered there in 1885. Over time, half the output of the second largest goldfield in

the world passed through the Standard Bank on its way to London.

The Impact of War:

Even the First World War offered opportunities for expansion when the Standard

Bank set up a branch in Tanzania shortly after British troops occupied the formerly

German administered Dares Salaam in September 1916. Both banks survived the

inter-war years but the world trade slump led to the closure of operations in the

Canary Islands, Liberia, the Netherlands, and Equatorial Guinea. Disaster struck the

Chartered Bank's office in Yokohama, Japan, when it was destroyed by an earthquake

in 1923 killing a number of staff. The Chartered Bank was particularly affected by the

Second World War when numerous Asian countries were occupied by Japan.

The Post War Years:

After the Second World War many countries in Asia and Africa gained their

independence. This led to local incorporation in some countries, particularly in Africa.

Other operations such as those in Iraq, Angola, Myanmar and Libya were

nationalized, while in Indonesia the Jakarta office was destroyed in an attempted coup

d'etat. In 1948 the Chartered Bank opened in Bangladesh and during 1957 it acquired

the Eastern Bank. The Eastern Bank gave the Chartered Bank a network of branches

including Aden, Bahrain, Beirut, Cyprus, Lebanon, Qatar and the United Arab

Emirates. The Chartered Bank also entered into a joint venture to form the Irano-

British Bank which opened for business in 1959. The bank grew rapidly and had 24

branches when it was nationalized in 1981. s radically changed and strengthened.

Standard Chartered in the 1990s:

Page 24

Even within this period of apparent retrenchment Standard Chartered expanded its

network, re-opening in Vietnam in 1990, Cambodia and Iran in 1992, Tanzania in

1993 and Myanmar in 1995. With the opening of branches in Macau and Taiwan in

1983 and 1985 plus a representative office in Laos (1996), Standard Chartered now

has an office in every country in the Asia Pacific Region with the exception of North

Korea. In 1998 Standard Chartered concluded the purchase of a controlling interest in

Banco Exterior de Los Andes (Extebandes), an Andean Region bank involved

primarily in trade finance.

Standard Chartered in Middle East & South Asia (MESA):

The MESA region performed well in year 2002. The region accounts for

approximately eleven percent of the group’s revenues. The integration of Grindlays

was successfully completed and the group is now one of the leading international

banks in each of its chosen markets in the region. The contribution of the Group’s

business in the United Arab Emirates reflects the businesses. Standard Chartered now

holds leadership positions in most of its key product segments in the UAE. The

average number of employees in the Middle East and other South Asia region in 2002

was 2995.

Standard Chartered in Hong Kong:

Hong Kong remains the Group’s largest market, generating one third of the Group’s

revenue. They have a network of 74 branches. Standard Chartered has been

transacting business in Hong Kong since 1858 and they issue bank notes there. In

2002, Standard Chartered became the first FTSE 100 Company to launch a new dual

primary listing in Hong Kong. This will make the Group more accessible to Asian

investors and will enhance the Group’s regional profile. The average number of

employees in Hong Kong in 2002 was 4,677.

Standard Chartered in Singapore:

Standard Chartered has been doing business in Singapore for 144 years and has 20

branches and offices, the largest branch network among foreign banks. The business

in Singapore accounts for approximately eleven percent of the Group’s revenues.

Standard Chartered has Qualifying Full Bank Status, which has enabled expansion of

the distribution network. In 2002, Asian banker magazine named Standard Chartered

Page 25

the ‘Best Retail Bank in Singapore’. The average number of employees in Singapore

in 2002 was 2,451.

Standard Chartered in Malaysia:

Standard Chartered is the oldest bank in Malaysia, where there is a network of 29

branches. Malaysia is another of the group’s core markets with broadly based

business as a result of long established franchises. The group continues to expand its

Shared Service Center that was opened in 2001 and carries out operations and

processing activity. The Centre in Kuala Lumpur has contributed significantly to

improvements in the Group’s processing and service efficiency.

Standard Chartered in other Asia Pacific:

The group has more than 80 branches and 14 offices in 14 countries across the region.

In China, Standard Chartered has one of the largest branch networks of any foreign

bank and is well positioned for growth and opportunities. The group is developing its

Consumer Banking business and has opened branches in Shanghai and Shenzhen. In

Thailand, the integration of Nakornthon Bank was successfully completed in

2002.The average number of employees in other Asia Pacific in 2002 is 4851.

Standard Chartered in India Region:

Standard Chartered is the largest international bank in India and, following successful

completion of the integration of Grindlays, have a combined customer base of 2.4

million in Consumer Banking and over 1200 corporate customers in Wholesale

Banking. The group launched its business in Mauritius in 2002 to provide Wholesale

Banking services to corporate client’s .The shared service centre in Chennai continues

to develop rapidly as more services and processes are migrated from other countries.

The average number of employees in the India region in 2002 was 5251.

Standard Chartered in Africa:

Standard Chartered continues to be one of the leading banks in sub Saharan Africa.

The group offers consumer banking and wholesale banking services in 13 African

countries with a network of 149 branches and offices. Standard Chartered recently

launched operations in the Ivory Coast and re-entered Nigeria. Business in East Africa

has performed well. Despite difficulties in Zimbabwe, the group’s business in Africa

has delivered good results. The average number of employees in 2002 was 5009.

Standard Chartered in United Kingdom and the Americas:

Page 26

Businesses in the United Kingdom and the Americas provide services to leading

multinationals and major financial institutions, which trade or invest in Asia, Africa,

the Middle East and Latin America. In 2003, the businesses in the Americans were

extensively restructured to improve efficiency for future growth. The Group also

operates a growing off shore banking business based in Jersey. The average number

of employee in the United Kingdom and Americas in 2002 was 2098.

The Acquisition of ANZ Grindlays by Standard Chartered:

The main idea behind acquisition and merger is making an investment and usually

involves more than mere cash. When two separate legal entities merge every

organization aspect of both companies are expected to change be it internal or

external. Such management decision is taken for a variety of reasons but the ultimate

aim is to add up to shareholder's wealth. For banks operating in the consumer and

wholesale banking sector, earning depends largely on the interest margin as well as

the service charges.

2.9 Standard Chartered Today

Standard Chartered employs 38,000 people in 950 locations in more than 50 countries

in the Asia Pacific Region, South Asia, the Middle East, Africa, the United Kingdom

and the Americas. Standard Chartered is one of the world's most international banks,

with employees representing 80 nationalities.

Standard Chartered PLC is listed on both the London Stock Exchange and the Stock

Exchange of Hong Kong and is in the top 25 FTSE-100 companies, by market

capitalization. It serves both Consumer and Wholesale Banking customers. Consumer

Banking provides credit cards, personal loans, mortgages, deposit taking and wealth

management services to individuals and small to medium sized enterprises. Wholesale

Banking provides corporate and institutional clients with services in trade finance,

cash management, lending, securities services, foreign exchange, debt capital markets

and corporate finance. Standard Chartered is well-established in growth markets and

aims to be the right partner for its customers. The Bank combines deep local

knowledge with global capability. The Bank is trusted across its network for its

standard of governance and its commitment to making a difference in the

communities in which it operates

2.10 Acquisition of ANZ Grindlays Bank by Standard Chartered Bank

Page 27

In August 2000, the US $1.34 billion acquisition of Grindlays Bank was completed.

This made the Standard Chartered Bank the leading international bank in India and

the other countries of South Asia. The acquisition strengthened the Group’s

competitive position in Middle East and brought to the group a respected private

banking business.Standard Chartered Bank has taken the advantage of the expansion

opportunities. Buying Grindlays from ANZ now propel it from number five to

number one among international banks in India, with some choice extra footholds in

the Middle East. At 1.34 billion US dollars, it is hard to complain that Standard

Chartered Bank has overpaid. The financial ease is less compelling for ANZ

shareholders, as there are advantages of getting out of a strategically peripheral

business. This acquisition of Grindlays Bank has added 6000 employees and 4

countries to Standard Chartered Bank’s existing network of 7000 employees and 570

offices in 50 countries. The end result is that Standard Chartered Bank, which went

into the 1997 Asian crisis with strong business in Hong Kong, Singapore and

Malaysia, emerges with additional core markets in India and Thailand.

The deal has made Standard Chartered Bank the largest foreign bank by assets in

India, Pakistan and Bangladesh and the second largest in Sri Lanka and United Arab

Emirates. The bank has been seeking to expand in the region since the end of the

Asian economies crisis, and has finally become successful in its expansion. The

primary goal of the integration is to combine the best of the both the banks, and put

right people in right jobs on the basis of fairness and equitability.

In September 2000, the group agreed to acquire Chase’s Hong Kong consumer

banking business for US$1.32 billion, which makes Standard Chartered Bank the

leader in Hong Kong cards. At that time it was also announced that the chartered

Trust had been sold to Lloyds TSB for 627 million pounds.

Until September 2002, both Standard Chartered and Standard Chartered Grindlays

operated under the same management but as separate entities. With effect from

September 2002, the merger was complete and Standard Chartered Bank started

operating as single entity.

2.11 Acquisition of AMEX in Bangladesh

Standard Chartered Bank has signed an Agreement to acquire the commercial banking

business of American Express Bank Limited in Bangladesh.

Why is SCB acquiring the AMEX business in Bangladesh?

Page 28

Good deposit base

Good corporate clientele

Attractive talent pool

Branch licenses

Defensive strategy

In May, SCB received a NO-OBJECTION-CERTIFICATE to proceed with the BPA

from the Bangladesh Bank and have since signed an Agreement with AMEX. Standard

Chartered Bank plans to migrate AEBL customers to SCB over a three month

Transition Period starting August 01, 2005. From November 01, 2005 all AMEX

customers can visit SCB branches. The acquisition will add 3 branches, and 3 booths

to the existing network.

2.12 Country Classifications

To ensure that key resources (management time, capital, Human resources and

information technology) are correctly allocated and that the exchange of best practice

is accelerated between entities, the group has classified the countries where it operates

into 3 categories: the large, the major and the international. (

Figure: Country classification

2.13 Operation Starting in Bangladesh

Standard Chartered Bank started its business in Bangladesh in 1948, opening its first

branch in the port city of Chittagong. The bank increasingly invested in people,

Page 29

technology and premises as its business grew in relation to the country's thriving

economy. At present the bank has numerous offices in Dhaka Chittagong and Sylhet,

including the country's only offshore banking unit inside the Dhaka Export Processing

Zone at Savar.

Extensive knowledge of the market and essential expertise in a wide range of

financial services underline the strength to build business opportunities for corporate

and institutional clients at home and abroad. Continuous upgrading of technology and

control systems has enabled the bank of offer new services, which include unique

ATMs and Phone-banking.

Standard Chartered's services in Bangladesh, ranges from Personal & Corporate

Banking to Institutional Banking, Treasury and Custodial services. Standard

Chartered is one of the world's most international banks headquartered in London.

This is summary of the main events in the history of Standard Chartered and some of

the organizations with which it merged.

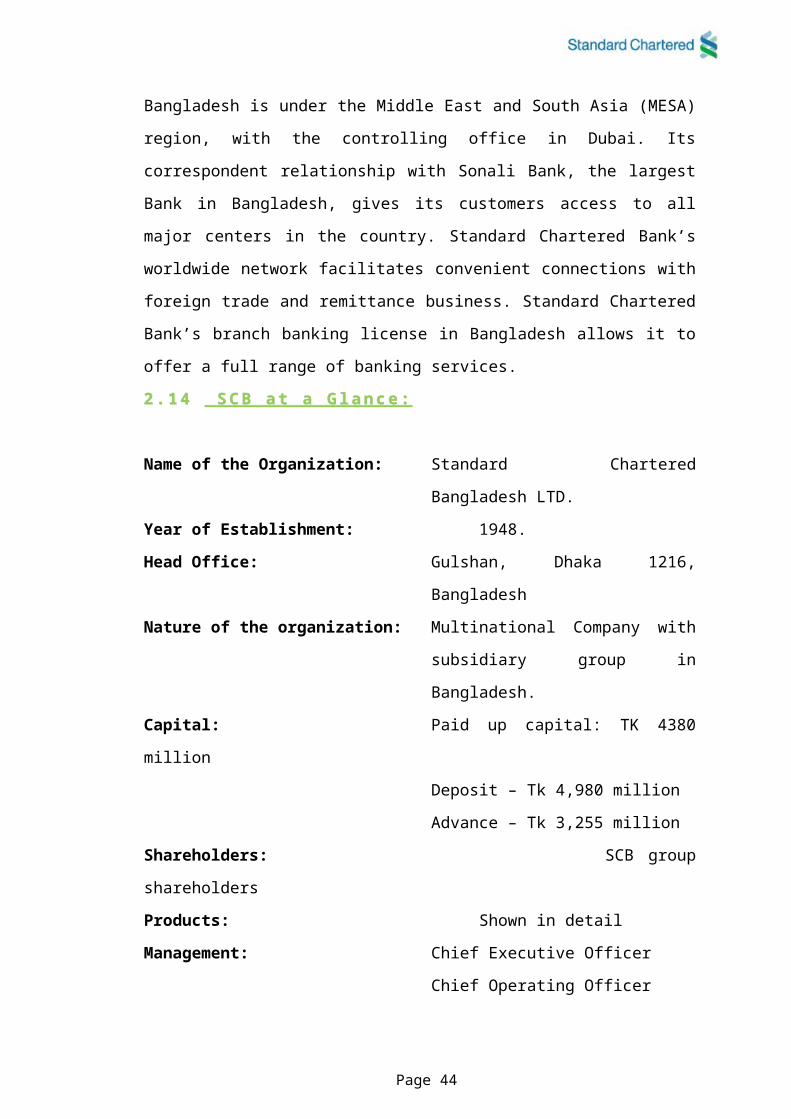

Bangladesh is under the Middle East and South Asia (MESA) region, with the

controlling office in Dubai. Its correspondent relationship with Sonali Bank, the

largest Bank in Bangladesh, gives its customers access to all major centers in the

country. Standard Chartered Bank’s worldwide network facilitates convenient

connections with foreign trade and remittance business. Standard Chartered Bank’s

branch banking license in Bangladesh allows it to offer a full range of banking

services.

2 . 1 4 2 . 1 4 S C B a t a G l a n c e : S C B a t a G l a n c e :

Name of the Organization: Standard Chartered Bangladesh LTD.

Year of Establishment: 1948.

Head Office: Gulshan, Dhaka 1216, Bangladesh

Nature of the organization: Multinational Company with subsidiary

group in Bangladesh.

Capital: Paid up capital: TK 4380 million

Deposit – Tk 4,980 million

Advance – Tk 3,255 million

Shareholders: SCB group shareholders

Products: Shown in detail

Management: Chief Executive Officer

Page 30

Chief Operating Officer

Manager, Personal Financial Services

Head of Corporate Banking

Manager, Human Resources

Manager, Marketing

Number of Branches: 24 (13 in Dhaka, 6 in Chittagong and 1

in each of these places Savar, Sylhet,

Khulna, Bogra and Narayanganj. )

Number of ATM’s: 38

Technology: Offers full online banking from branch to

branch and also from Dhaka to

Chittagong.

Service Coverage &

Customers: Serves individual and corporate

customers within Dhaka & Chittagong.

2.15 2.15 At A Glance Standard Chartered Bank, Gulshan BranchAt A Glance Standard Chartered Bank, Gulshan Branch

To Consistently help the customers construct Intelligent Financial Choices.

By being the preferred provider of the Highest Quality services in the

Chosen business areas, Relevant to all the Constituencies…

Page 31

BSSM

SA CSM STM

CSO1 CSO2 CSO3 CSO4 CSO5 PSO1 PFC1 PFC2

Figure: Organ gram of SCB Gulshan Branch

BRO

Standard Chartered aims to be the right partner for its customers.

Responsive

SCB spend time listening to their customers to understand who they are and how they

operate to anticipate their needs. They empower their employees to deliver great

service, through enabling them to take decisions which positively impact their

customers. How we response to our customer will influence their belief in our

commitment to them.

Trustworthy

Trust is the foundation of every successful relationship. We trust because we believe

in the sincerity of our promise’s peoples set their organization above other

organizations through their unique ability to build trusted relationships with all

stakeholders. Trustworthy is about meaning what they say, being able to explain their

actions, doing what they promise and being consistent in their approach.

Creative

Creativity belongs to those of us who are excited by challenges and engage them in

fresh thinking and an open mind They encourage employees who can see a better way

of doing things to contribute their ideas. The quality of SCB’s people and the

diversity of their backgrounds mean that they have an infinite capacity for fresh ideas

and alternative solutions.

International

As a member of global village we view the world from the widest perspectives. They

believe in working as “one Bank” across all geographies and businesses, providing a

seamless relationship to their customers. They uphold consistent ethical standards

wherever they operate.

Courageous

Being courageous is about confidently doing what’s right. Often the task may seem

Insurmountable but with courage and tenacity, the odds can be overcome. A truly

courageous act both inspires and builds character’s, encourages their people to take

measured risks to deliver improved results for all their stakeholders. The support they

provide to employees gives them the courage to develop their talents and skills so

they can make a difference,

2.16 Organization Structure

Page 32

Divisional Structure

The Standard Chartered Bank in Bangladesh has it’s headquarter Is in Dhaka and It

has branches in Chittagong, Khulna, Bogra and Narayangonj. While the full range of

services is available at the headquarters, other branches offer specific services

appropriate for the location. At the headquarters, the bank mainly consists of two

divisions:

Business Division

Business Support Division

The Business Division has the following departments:

Corporate Banking Group (CBG)

Global Markets (Formerly Treasury)

Financial Institution (Formerly Institutional Banking Group)

Consumer Banking (CB)

Custodial Services (CUS)

The Support division provides assistance to the above business activities and consists

following departments:

Operations

Finance, Administration and Risk Management

Information Technology

Human Resource Department

Legal and Compliance

External Affairs

Credit

Chain of Command and Functions of division Heads

Standard Chartered Bank in Bangladesh follows a hierarchical pattern of command.

The Chief Executive Officer (CEO) reports to the Regional General Manager, MESA

in Dubai. Each of the division’s heads at the headquarters report to the CEO. The

Organogram is shown in the Figure .In Chittagong, managers both report to the

respective line heads and as well as to the Head of Chittagong. The respective branch

managers are responsible for the performance of their unit. The support activities or

functions of the division’s heads are as follows:

Head of Finance and Administration, who looks after the general ledger,

budget, financial scenario of the bank, risk management administration and

audit operation.

Page 33

Head of Consumer Banking, who supervises retail-banking operation like

sales and services, retail lending, product development and product marketing.

Head of Corporate deals with the relationship management, corporate finance

etc.

Head of Human Resources looks after succession planning, training and

industrial matters.

Head of Lending Management who assists the management division of

Corporate, retail and Credit Cards in their lending operations.

Head of Global Markets deals with the foreign exchange, money market and

asset liability operation.

Head of International Services deals with the trade finance, guarantee and

correspondent banking.

Head of Operations who looks after the support services in banking lending,

CBS User, Treasury, SWIFT/TELEX operation etc. Head of Technology is

directly accountable to him.

Figure: Organ gram of Standard Chartered Bank

2.17 Management:

The goal of Standard Chartered Bank is to be the "Bankers of First Choice." Towards that

goal, the overall planning in the Organization is done at the headquarters level in Dhaka by a

Management Committee (MANCO), headed by the CEO and consisting of the business heads

of Corporate Banking, Consumer Banking, Treasury, and from the support divisions the

Page 34

CHIEF EXECUTIVE OFFICER

CHIEF EXECUTIVE OFFICER

Support Manager to CEOSupport Manager to CEO

Head of Corporate and Institutions

Head of Corporate and Institutions

Head of Finance & Admin.

Head of Finance & Admin.

Head of GSAMHead of GSAM

Head of Consumer Banking

Head of Consumer Banking

Head of Human Resource Dept.

Head of Human Resource Dept.

Chief Operating Officer

Chief Operating Officer

Head of Global Markets

Head of Global Markets

Senior Credit Officer

Senior Credit Officer

Head of Information Technology

Head of Information Technology

Head of Financial Institutions

Head of Financial Institutions

Head of Legal & Compliance

Head of Legal & Compliance

Head of External Affairs

Head of External Affairs

heads of Human Resource, Operations and Finance Departments. They meet once a month,

or when a special situation arises, to plan the strategic decisions. The decision making,

although apparently based on a top-down approach, leaves room for participation down to the

level of department heads, which are responsible for carrying out the planning of their

department within the broad guidelines set by MANCOM.

Among the broad strategic objectives are:

1Creating a congenial work environment

2Modernization of the Management Information System to achieve full automation by

drastically cutting down paper work in the long run.

3Focusing on service quality and consumer needs.

4Recruiting and maintaining top-grade, efficient employees.

5To invest in those technological systems which will upgrade and enhance financial

services, and

6 Creating an excellent brand image of the Bank.

2.18 Banking services

Standard Chartered Bank is providing two types of services.

1) Retail or Consumer Financial Services

2) Business or Corporate Financial Services

Structure of Consumer Banking

In the following figure, the reporting line and the responsibilities of the top

management of consumer banking division of the standard chartered bank is

presented.

Figure: Consumer Banking Division of SCB Source: SCB’s Official

Document

Page 35

Head of Consumer Banking

Head of Consumer Banking

Manager SQ and MISManager SQ and MIS

Support ServiceSupport Service

Manager BFSManager BFS

Control and MIS ManagerControl and MIS Manager

Head of Product Marketing Service

Head of Product Marketing Service

Head of Banking Products

Head of Banking Products Heads of CardsHeads of CardsHead of

Distribution and Priority Banking

Head of Distribution and

Priority Banking

Head Credit and Collections

Head Credit and Collections

Business Banking of SCB

It is very true that major contribution to the bank’s equity has been from business

banking sector. It provides several types of services under business banking

(Figure1.4 below).

Figure: Business Banking of SCB Source: Business Banking,

SCB

Corporate Banking

SCB is recognized as the leading financial institution in corporate finance services in

Bangladesh. A professional management team caters to the needs of its clients and

provides them with a wide range of financial services some of which are project

financing and investment constancy, syndicated debt and equity, bond and guaranties,

local and international treasury products.

Institutional Banking

This service of SCB is designed for different fund based organizations like donor

agencies, NGOs, voluntary organizations, foreign missions, airlines, shipping lines

and their personnel with the facilities like convertible and non-convertible current

accounts, convertible Taka accounts, which are freely convertible to major

international currencies, local and foreign currency remittances through a large

network of branches and correspondence.

Commercial Banking

SCB offers different commercial banking facilities to all commercial concerns

specially those with particular involvement with import and export finance. It also

provides bonds and guarantees, investment advice, leasing facilities, project finance

opportunities.

Quasi Governmental Banking

The Quasi Government Service of SCB helps the government by providing different

financial service like efficient and knowledgeable management of trade business

Page 36

(import and export), skills in barter, swaps and counter trade deals. In addition, the

opportunity of debenture finance for new projects, possibilities of hard currency loans

and lease deals, the opportunity of syndicated hard currency, financing of loans and

import L/C, highly efficient account management and remittance handling within the

country or aboard.

Treasury Banking

The treasury of SCB is one of the leading treasuries that offers foreign exchange

requirements, provides market commentaries, economic forecasts and advisory to its

major corporate clients. To keep its customers’ up to date with what is happening in

the money markets, SCB has “Weekly Treasury Updates”.

Consumer Banking Services

The service of PFS and Credit Card Services are known as Retail Banking or

Consumer Banking. Retail banking deals with the providing the bank services to

individuals on a one-to-one basis.

Personal Banking Services

SCB started its personal banking services in March 1992. Besides usual deposit

services, consumer finance services of SCB have been most popular. This section of

report discussed all these personal banking services; consumer finance services of

SCB have been most popular. This section of report discusses all these personal

banking services provided by SCB.

a) Deposit Services

SCB has the deposit services for its customers. SCB’s deposit services are shown in

the figure below:

Figure: Deposit service Source: SCB’s Official Document

b) Locker Facilities

Page 37

SCB’s locker service allows the customers to keep their valuable in a safe and secure

place and access the same at convenient times.

c) Government Bonds

Like other banks, SCB provides its customers with bond services. Three types of

government bonds are available with the bank. These bonds are sold and related

accounts are maintained according to the already established procedures.

d) Consumer Finance

SCB first introduced consumer finance in Bangladesh and until today they are the

market leaders. It has varieties in financing its retail customers with innovative

products. These nclude different types of credit and saving schemes shown in the

figure in the following figure:

Figure: Scheme offered under consumer finance of SCB

Source: External Affairs division, SCB

e) Chequebook

The customer service department helps the customers to collect new chequebook. The

Chequebook is sought due mainly to two reasons: If the customer has lost it or if it is

stolen. In addition to these services, officers also take order for new chequebook for

the customers. Usually it takes two workings days to collect a new chequebook.

f) ATM Services

There are various services provided to ATM card users like they can apply for new

ATM card. The customer can apply to halt the lost ATM card. The bank for free of

charge provides an ATM if it’s normally being expired. If the customer damages the

card then there’s a replacement fee of BDT 300tk to collect a new ATM card. Also

customer can collect the card after 24 hours from customer service department

without any fees.

g) Accounts Statement and Certificate

Page 38

Usually every account holder gets statement through mail as per their requirements

when they open the account. There is an option in the account opening form about

statement frequency and the customer can mention the period to send statement

through mail. Except this, most of the time customer came to collect statement or

certificate from the bank for many purposes like visa purpose, tax payment purpose

etc. As the detail information is up to date time to time through online services and

software’s, the customer service officer normally can provide one year statement for

the customer on the spot.

h) Closing an account

An account holder is required to bring all the materials that have been provided by the

bank during opening the account if the customer wants to close an account. Basically

an ATM card, a chequebook is provided by the bank for an account holder. Whenever

an account holder comes to close the account the customer service officer tale backs

those materials from the customers and destroyed it in front of the customer. A bank

account closing charge and government excise fee being taken from the customers to

close an account. This is the formality to close an account.

i) Purchase of Sanchaya Patra on Behalf of a customer

SCB is providing free service for the account holder by purchasing Sanchaya Patra

on behalf of the customer. If an account holder wants to purchase Sanchaya Patra

than he or she can apply directly from any branch of Standard Chartered Bank. The

fund is transfer from the account as much as the customer wants to purchase based on

the government rules and regulation. The customer can encash this security to refund

purpose. The customer also can deposit coupon interest into their account very easily.

j) Different types of queries

Many customer come to various branches of SCB with different types of queries.

Most common queries are given bellow:

To know the account opening process.

To know about loan facilities.

To know about the account position.

To know the account balance.

To know about any fund transfer.

Enquiry about lost Cheque, and ATM card.

To know about any returned Cheque information.

Different charges for different activities regarding account/ card services.

Page 39

These are the most common queries of the customers. Queries vary according to

situations and instances of emergency.

k) Credit Card Services

SCB provide credit card services in an exclusive manner with different offerings for

the customers. To be a card holder the applicant must have to provide TIN number,

trade license, voter id with attested photo/passport/driving license, minimum six year

bank statement or source of income to get a credit card. The authority decides the

credit limit by analyzing the statement of the applicant. There are four types of credit

card offered by SCB.

l) SMS (Short Message Service) Banking Services

SCB has introduced SMS Banking Service in Bangladesh with Grameen Phone and

City Cell the two biggest mobile companies in the country. SMS banking is the

simplest way of finding out Accounts daily/monthly balance or credit cards daily

outstanding balance and available limit; statement balance, minimum due amount and

payment due date. With SMS banking all this information will be available in users’

cell phone.

With SMS banking service, customers do not have to wait to statements to arrive

through mail or call up at cards call center/phone banking. Once a customer become a

member of SMS banking, will have 24 hours access to the key financial information

of his/her credit card/account.

m) E-Statement Service

This is secure and reliable way to receive Credit Card/Account Statement’s anywhere

in the world. An account holder of SCB can receive e-Statements with the help of the

Internet. It is a fast, reliable and efficient service of Standard Chartered to minimize

customer’s convenience.

n) Auto Bills Pay Service

It is the simplest way and most convenient way of paying Monthly Bills of mobile

phone, electricity, internet, cable TV, etc. Paying any bills has never been so easier.

With the help of Account/Credit Card, a holder can put an end to the hassle and

frustration involved in paying bills as the traditional way.

2.19 Competitive market analysis

Page 40

Threat of New Entrant

The flexible governmental policy regarding the financial sector development has

made it difficult more for entering Private local and foreign banks into the industry. .

So, considering the situation, the threat of new entrants is very high in the banking

industry. Standard Chartered’s brand loyalty, product innovation, high service quality

will make it difficult for new entrants to take market share

Bargaining Power of Customers and Suppliers

In consumer banking the bargaining power is different from the other banking

services. Here the individual customers are directly interacting with the bankers and

here is a opportunity for the customers to say more. Diversifying into personal baking

can be a good alternative to sustain the increasing bargaining power of the clients

Threats of Substitute Products

Leasing companies, NBFIs (Non-Banking Financial Institutions), DFIs (Development

Financial Institutions); etc are coming up with the alternative financial solutions in

relation to traditional solutions provided by banking sector Efforts should be made

find new avenues of business like leasing, insurance service to sustain the threat of

substitute products. Efforts have already been taken such “Islamic Banking” division

at Gulshan which tries to capture the Islamic minded people

Rivalry among Existing Banks

The level of competition among the players in the banking sector is very high. The

technological integration, better managerial and human resources have resulted in the

tremendous competition for the market share. Historically, Grindlays had the largest

market share among the foreign banks. But after the acquisition of Grindlays,

Standard Chartered became the giant with around 70% market share of the total

foreign banks. Major strategies followed by these competing banks to ensure more

value are as follows:

Constant review of client needs and deposit trends.

Maintain good relations with the corporate clients.

ATM service should be up to the the marks so that people can withdraw and

deposit money at any time (24 hours)

They waive certain banking charges like ledger fee, minimum balance fee, etc.

for certain large corporate clients.

the baking sector should be specialize in specific service areas, minimize cost,

through efficient management

Page 41

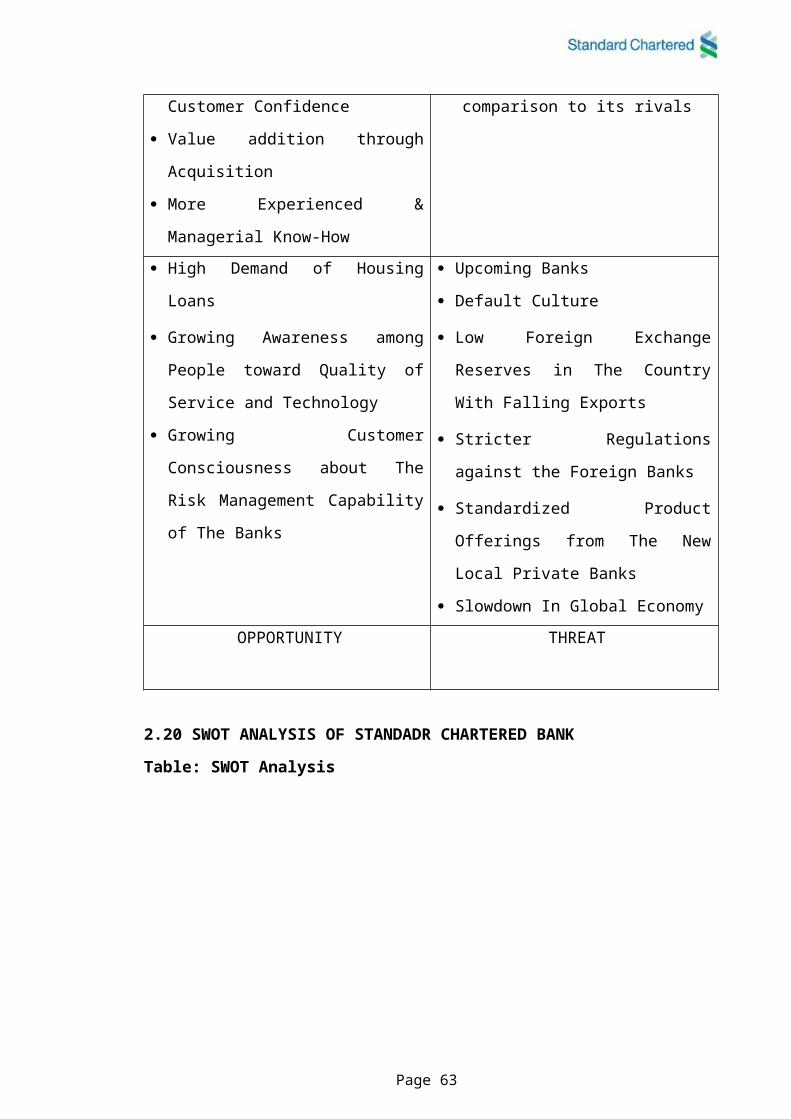

2.20:Swot Analysis

STRENGTH WEAKNESS

Strong corporate Identity

Wide range of Financial Product

Offerings

Local Knowledge with Global

Capability

Strong employee bonding and

belongingness

Young Enthusiastic Workforce

Free Exchange of Communication

MBO

Strong Operating and Branding

Activities

Achievement of High Customer

Confidence

Value addition through Acquisition

More Experienced & Managerial

Too Many Contract Workers

Low Remuneration Package for Entry

Level Officers

Concentration on Varied Financial

Products

Very Little Active Account Being

Maintained Till the End

No Transparency Regarding the

Decisions Taken By Upper

Management

Loss of Valuable Market Information

due to Top-Down Communication

Method

Charges high fees in comparison to its

rivals

Page 42

Know-How

High Demand of Housing Loans

Growing Awareness among People

toward Quality of Service and

Technology

Growing Customer Consciousness

about The Risk Management Capability

of The Banks

Upcoming Banks

Default Culture

Low Foreign Exchange Reserves in

The Country With Falling Exports

Stricter Regulations against the Foreign

Banks

Standardized Product Offerings from

The New Local Private Banks

Slowdown In Global Economy

OPPORTUNITY THREAT

2.20 SWOT ANALYSIS OF STANDADR CHARTERED BANK

Table: SWOT Analysis

Page 43

PROJECT

PART

Page 44

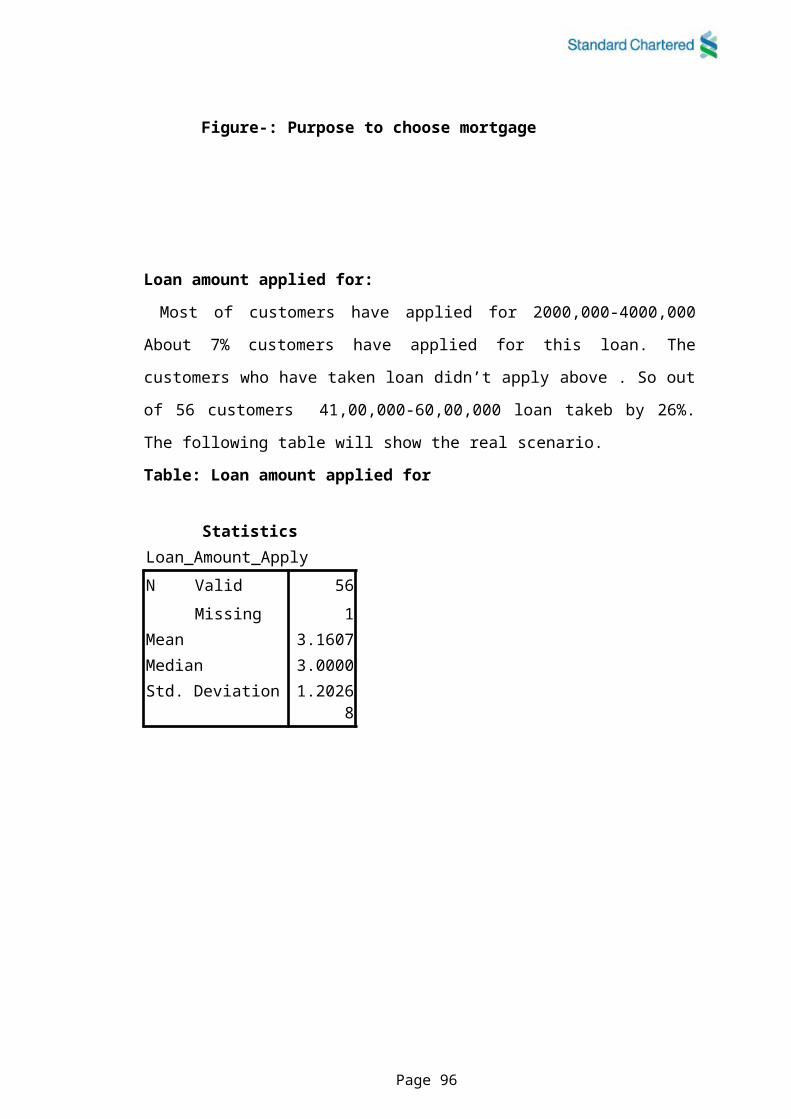

3At a glance ‘MORTGAGE LOAN’

3.1 Standard Chartered Home loan:

Every body dreams to have a home of their own. To make your dream true Standard

chartered bank bought a new home loan scheme with exciting features. To build a

new home or apartment, to restructure, to expansion or to transfer other financial

institution’s to SCB you can take Standard chartered home loan scheme.

The Mortgage loan offers following benefits:

Attractive interest rate

No hidden cost

No fixed deposit or personal guarantee is needed *

No need to hold a account with Standard chartered bank

Loan can be received on installment

Facility of only interest payment during structuring of building

Loan is granted on shortest possible time

Facility of repayment of loan fully or partial before maturity

Loan can be granted by mortgaging land

Easy and simple documentation

Special characteristics of home loan:

Loan disbursement on installment: There is facility to take home loan on

installment. This will depend how much amount the client will handle through down

payment.

Financial during structuring: Loan is available only after completion of foundation

and structuring

Matters that need to consider

Page 45

Clients who are at least three years in their profession are targeted for this loan

scheme. Following things are considered during processing of loan application form.

1.Loan is granted on the basis of applicant’s professional experiences, condition

of the business, position of the real estate, past financial transactions, current debt

etc.

2. Loan will depend on CIB report on applicant’s debts

Amount of home loan:

Minimum Amount: Minimum Loan amount: BDT 500k.

Maximum Amount:

1. Loan is granted on highest 80% of current value of asset in case of buying new

home or apartment. In this case maximum loan amount will be 1 crore taka.

2. Loan is granted on highest 75% of current value of asset in case of

restructuring, extension, and furnishing. In this case maximum loan amount is

1crore taka.

3. Home loans from other financial institutions are transferable to standard

chartered home loan scheme. In this case maximum loan amount is 75 lac taka.

Time frame of home loan:

Maturity of loan repayment is depending on original borrower’s age and profession.

Maximum maturity of home loan is 20 years.

Home loan disbursement:

Borrower can take the whole loan amount at a time or in partial disbursement

according his needs. There is facility of paying interest only on disbursed loan

amount.

Home loan payment process:

Equal monthly installment: Loan can repay by monthly installment combining

the principle amount and interest. In this case monthly installment will be charged

based on maturity and interest of the loan. So there can be difference in monthly

installment due to different maturity with same interest.

Interest only: In this case you can only repay the interest before the hand over of

home or apartment. After the hand over you have to repay the loan by monthly

installment.

Collateral of home loan:

Page 46

Home loan is provided by mortgaging any kind of real estate.

Fee and charges of home loan:

Processing and documentation fee of new loan: 1.5 % of granted loan. No

processing fee is required in case of transferring other loans to standard chartered

bank.

Settlement fee: There is option to repay the whole loan before maturity. In this case

fee on depend on current status of the loan. Beside all the insurance fee of real estate

are on the applicant side. There will be 15% vat on all the fee and charges of home

loan.

3.2 Documents required for home loan:

1. 2 copies passport size photo of applicant

2. Photocopy of passport of the applicant.

3. Bank statement of last 12 months

4. Pay slip in case of job holder and a certificate from the employer

5. In case of professionals, photocopy of professionals certificate.

6. In case of businessman, photocopy of trade license, in case of partnership deed

is required

7. Tin certificate photocopy

8. In case of restructuring, furnishing, extension Cost list provided by developer.

Mortgage in detail:

3.3 Product Range:

Home Loan: For purchasing residence for dwelling purpose

Home Credit: Extending loan facilities for different purposes

House extension: Loan facility for extension of house on freehold or

leasehold land by mortgaging the property before disbursement. LTV

to be calculated on current status only

Renovation work / face uplifting: Loan facility for renovation or face

uplifting work of apartment or house by mortgaging the property

before disbursement. Property valuation to be done based on current

value of property. Registered mortgage required.

Finishing work for almost completed property: Loan facility for

finishing work of almost completed property (50% work done).

Page 47

Take-over loan: Transfer of existing housing / house renovation loan

from other bank or FI.

3.4 Customer Segments:

Segment 1: Salaried Professionals

Employees of MNCs

Employees of Supranational Organizations

Employees of middle to large-corporates

Employees of government offices

Employees of private organizations having salary with SCB or other

banks

Segment 2: Self Employed professionals / Businessmen

Businesspersons or self employed professionals having at least 06-

month /12-month account relationship with SCB or other bank

Segment 3: Landlord / Landlady

People having a stable source of income from rented premises

Segment 4: Wage Earners (100% Secured loan only)

Wage earners or NRBs having A/C with SCB or any other bank

Exclusion segments: Customers with business in manpower, Tour

operators, stock brokers, & Land developers. Only applicable for NTB

customers. For existing customers, financing allowed under L2.

Restricted segments: Film actor / actress, freelancers, PEP, transport

business, Lawyers, Journalists, Police. For L2 same as above rule is

applicable. Lawyers, journalists and security forces will fall under L-3

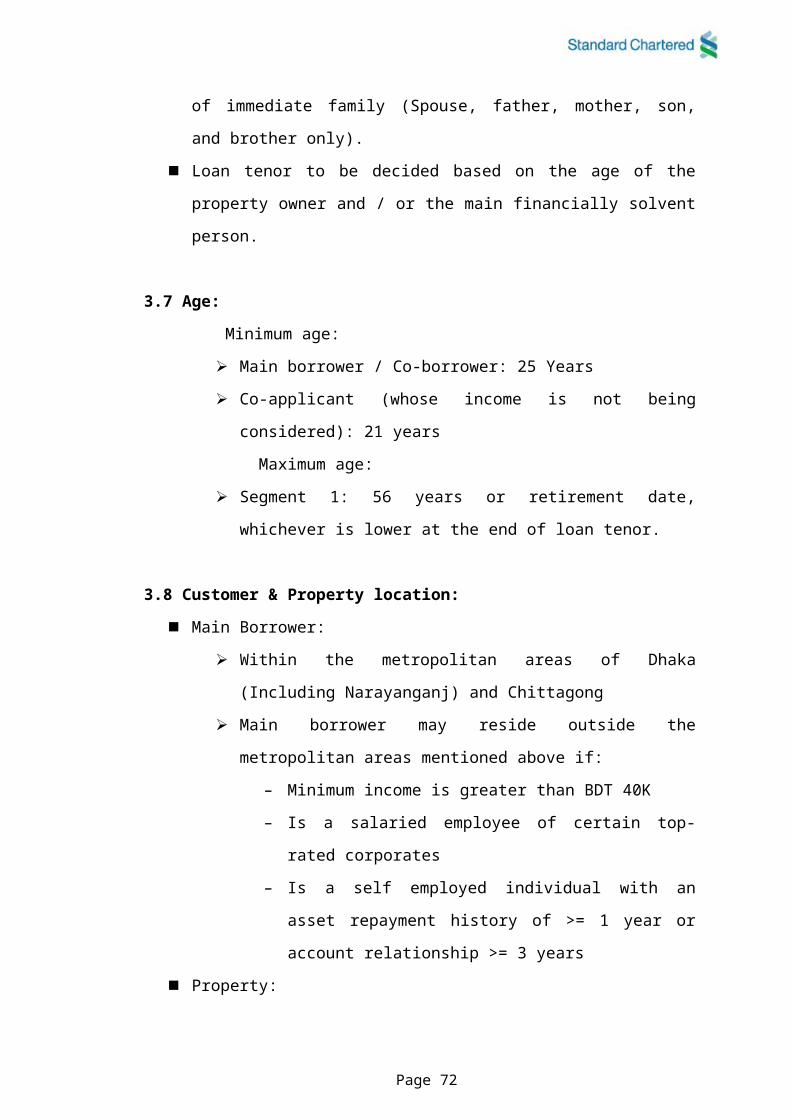

3.5 Primary borrower:

Must be the owner of the property if the property owner and the main

financially eligible person are different persons

Loan tenor to be decided based on the age of the property owner and / or the

main financially solvent person, whichever is lower.

3.6 Secondary applicant:

Co-applicant

Page 48

Co-applicant is generally mandatory for all proposals except for cases where

the primary owner is both the property owner and the financially eligible

person and assigns his/her Life Insurance Policy in favor of the bank.

For co-applicants, flexibility in some areas of eligibility is allowed.

Relationship and no. of co applicants may vary depending on the title

ownership of the property to be mortgaged.

Co-borrower