real estate joint ventures: waterfall structures, developer promote...

TRANSCRIPT

Real Estate Joint Ventures:

Waterfall Structures, Developer Promote,

IRR Lookback, Clawback and CatchupCalculating and Structuring Promote, Planning for Phantom Income, and Taxation of Carried Interest

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

THURSDAY, JANUARY 31, 2019

Presenting a 90-minute encore presentation with interactive Q&A

Seth R. Hoffman, Chief Operating Officer and General Counsel,

HighBrook Investors, New York

Benjamin R. Weber, Partner, Sullivan & Cromwell, New York

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

5Copyright ©2018 Sullivan & Cromwell LLP

Real Estate Joint Ventures

Benjamin Weber Sullivan & Cromwell LLP

Seth Hoffman HighBrook Investors

6Copyright ©2018 Sullivan & Cromwell LLP

Introduction

7Copyright ©2018 Sullivan & Cromwell LLP

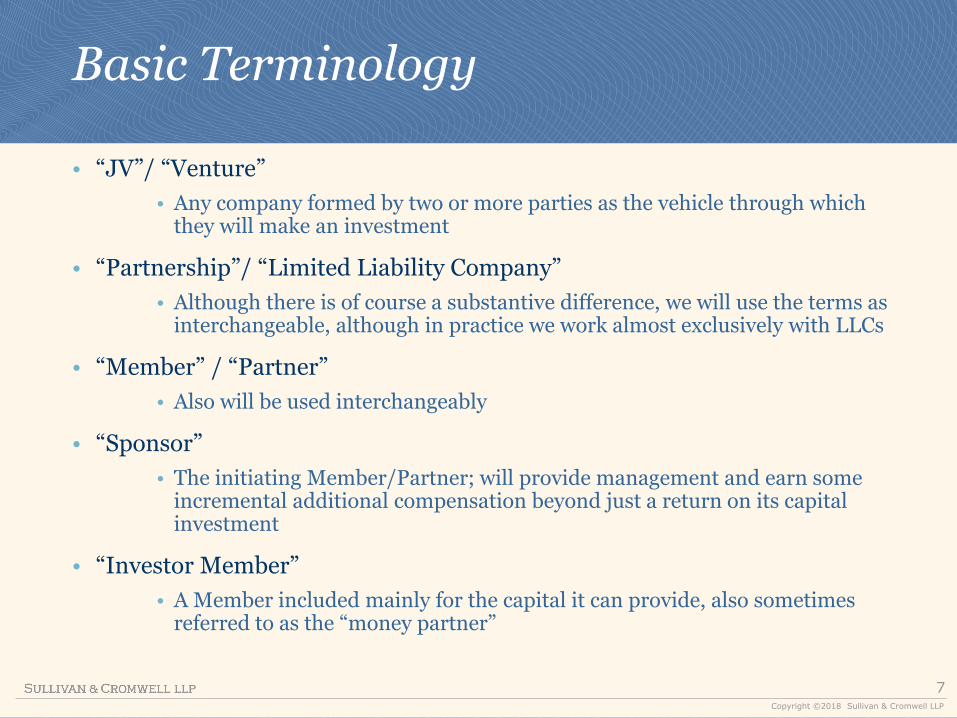

Basic Terminology

• “JV”/ “Venture”

• Any company formed by two or more parties as the vehicle through which they will make an investment

• “Partnership”/ “Limited Liability Company”

• Although there is of course a substantive difference, we will use the terms as interchangeable, although in practice we work almost exclusively with LLCs

• “Member” / “Partner”

• Also will be used interchangeably

• “Sponsor”

• The initiating Member/Partner; will provide management and earn some incremental additional compensation beyond just a return on its capital investment

• “Investor Member”

• A Member included mainly for the capital it can provide, also sometimes referred to as the “money partner”

8Copyright ©2018 Sullivan & Cromwell LLP

PlatformSingle Property Fund

Range of Structures

Managing Member

Investor Member(s)

JV

Properties within an asset

class

Managing Member

Investor Member

JV

Property

Sponsor/

Managing Member

JV

Assets within scope of stated

investment strategy

Limited partners

9Copyright ©2018 Sullivan & Cromwell LLP

Major Topics:

1. Purpose – Why is the venture being formed; what is the expected investment timeframe and will there be any limits on the scope of the venture’s business? How many partners and who will they be?

2. Management – Who will control the venture and how? If the Sponsor will manage, will the other partner(s) have approval rights or any other ability to assert control? Can the Managing Member be removed as manager and, if so, when and how will the replacement be determined and what other consequences will be suffered by the Sponsor and its affiliates? How will the partners develop (and update) the venture’s business plan and budget?

3. Capital Contributions – Who can call for additional capital and when? What level of commitment is being given by each partner; will capital be funded pro rata or on some other basis; is the funding obligation mandatory or voluntary; and what will the consequences be if a partner fails to fund when capital is called?

4. Distributions – How and when will revenues be shared among partners?

5. Transfer Rights – What approval will a partner need in order to be able to transfer its interest; and how will that rule apply to indirect transfers?

6. Exit Mechanism; Dispute Resolution – How and when will the venture end? What options will exist if the partners cannot agree on a major decision or if one partner wants or needs to exit and the other is not ready to sell?

10Copyright ©2018 Sullivan & Cromwell LLP

Secondary Topics

• Will the JV depend on third-party services (property management; leasing; general contracting; accounting and/or tax preparation)?

• Will the JV pay fees to any partner or any affiliate of a partner?

• What will the JV agreement say about the partners’ respective duties (silence vs. disclaimers; operating standard)?

• Will there be any affiliate guarantees – to support partner funding obligations or to backstop JV obligations?

• How will “cash available for distribution” be determined and by whom (it’s all about reserves)?

• Tax matters (allocations, partnership representative, recent changes in law – no more TMP and no more tax termination on majority transfer)

• Indemnification of Members

11Copyright ©2018 Sullivan & Cromwell LLP

Purpose

• A JV agreement normally includes an express statement of the purpose for which the company was formed

• The purpose can be very broad

• e.g., “any purpose for which an LLC can be formed under DE law”

• But the Investor Member and/or a mortgage lender generally will require that the purpose be limited to the intended scope

• e.g., “buying, owning, managing, leasing, renovating and selling the commercial building located at [address] and activities incidental thereto”

• Should “exchange” be included in the litany?

• Changing the “purpose” will usually require special approval

12Copyright ©2018 Sullivan & Cromwell LLP

Purpose

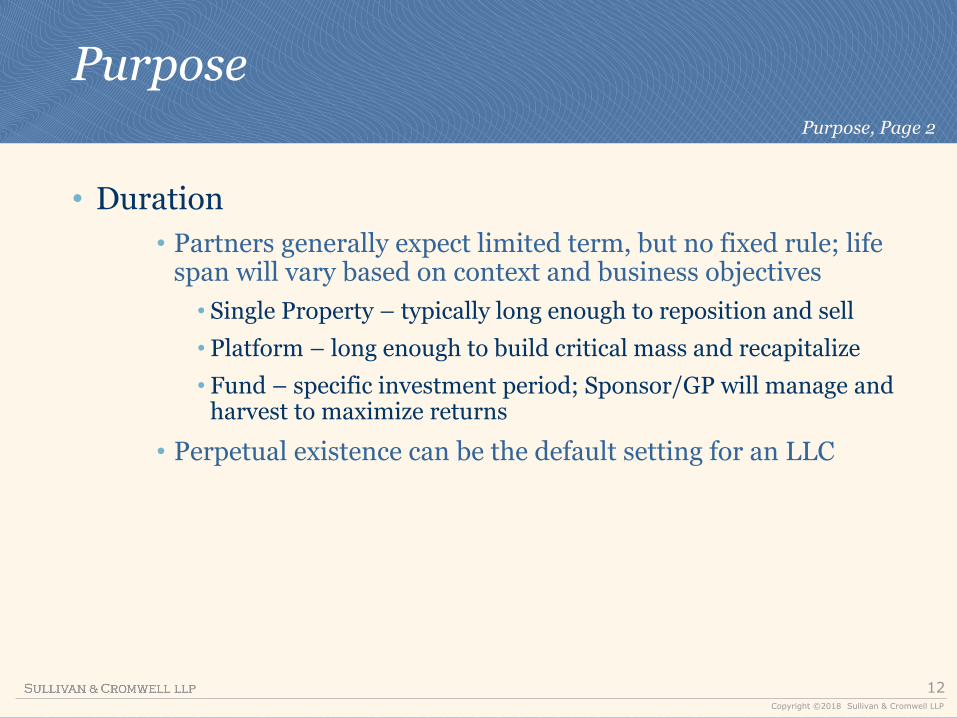

• Duration

• Partners generally expect limited term, but no fixed rule; life span will vary based on context and business objectives

• Single Property – typically long enough to reposition and sell

• Platform – long enough to build critical mass and recapitalize

• Fund – specific investment period; Sponsor/GP will manage and harvest to maximize returns

• Perpetual existence can be the default setting for an LLC

Purpose, Page 2

13Copyright ©2018 Sullivan & Cromwell LLP

Management

• Fiduciary Duties of Members

• General Rule: Partners owe each other the fiduciary duties of loyalty and care; Managing Member bears this in particular

• Often the Investor Member will disclaim any duties, fiduciary or otherwise, to the fullest extent permitted by law

• Permitted in DE; but no Member can avoid the implied covenant of good faith and fair dealing (must act with honesty and not contrary to the spirit of the agreement in the performance and enforcement of a contract)

• Disclaimer should not override Managing Member’s responsibility to meet the agreed operating standard

• Consider whether the disclaimer should apply to the non-managing Member if it has replaced the Sponsor as Managing Member (for cause?)

Fiduciary Duty is “something stricter than the morals of the market place. Not honesty alone, but the punctilio of an honor the most

sensitive, is then the standard of behavior.”1

Fiduciary Duty is “something stricter than the morals of the market place. Not honesty alone, but the punctilio of an honor the most

sensitive, is then the standard of behavior.”1

1Meinhard v. Salmon, 164 N.E. 545 (N.Y. 1928) (Justice Cardozo).

14Copyright ©2018 Sullivan & Cromwell LLP

Management

Management Structures

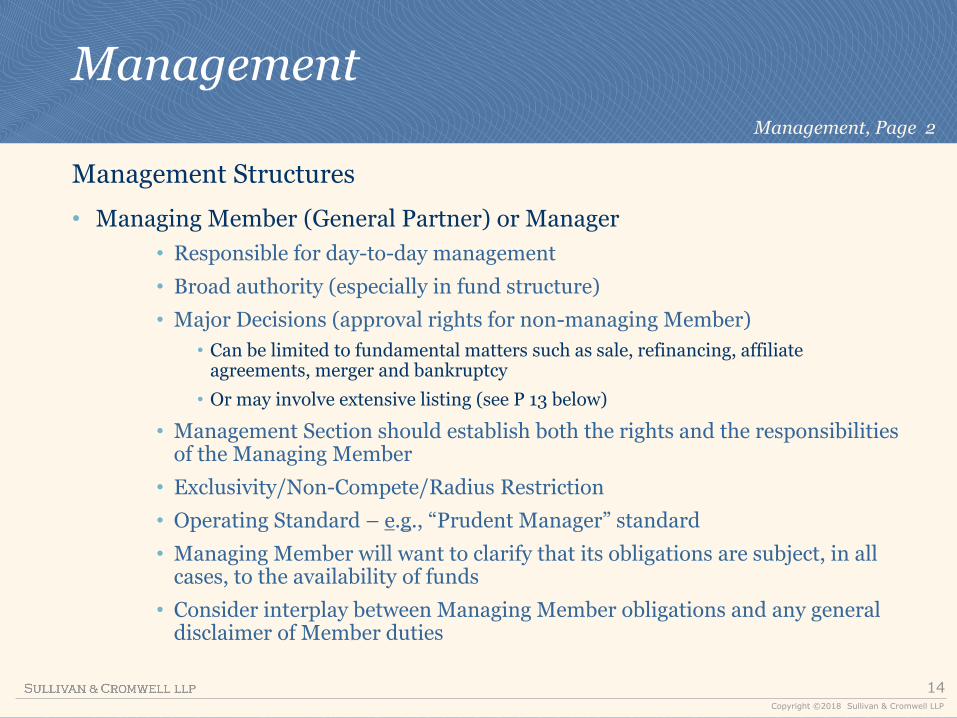

• Managing Member (General Partner) or Manager

• Responsible for day-to-day management

• Broad authority (especially in fund structure)

• Major Decisions (approval rights for non-managing Member)

• Can be limited to fundamental matters such as sale, refinancing, affiliate agreements, merger and bankruptcy

• Or may involve extensive listing (see P 13 below)

• Management Section should establish both the rights and the responsibilities of the Managing Member

• Exclusivity/Non-Compete/Radius Restriction

• Operating Standard – e.g., “Prudent Manager” standard

• Managing Member will want to clarify that its obligations are subject, in all cases, to the availability of funds

• Consider interplay between Managing Member obligations and any general disclaimer of Member duties

Management, Page 2

15Copyright ©2018 Sullivan & Cromwell LLP

Management

• The Managing Member/Sponsor may have one or more affiliates that can provide services the JV would otherwise have to hire from a 3rd party

• Examples include:

• Acquisition Fee / Finder’s fee

• Asset Management Fee

• Property Management Fee

• Leasing Agency Fee

• Construction Management Fee

• Financial Advisory Fee

• Disposition Fee

• Guaranty Fee

• Fees to affiliates are generally paid before distributions (although they could be layered into the distribution waterfall) and should be taken into account when assessing overall economics to the Sponsor

• Sponsor affiliates may be able to provide services at a discount to market rate

• Sponsor affiliate may be willing to defer fees during cash flow shortage, something a 3rd party provider would be less likely to accept

• Mortgage lender will expect subordination from affiliate service providers

Management, Page 3

16Copyright ©2018 Sullivan & Cromwell LLP

Management

• Committee of Member Representatives (if so, what vote required?)

• Administrative Member (implies more limited authority)

• Both Members (all actions require joint approval)

• Will Investor Member have any authority to act alone?

• Should represent JV in matters involving possible conflict with the Sponsor (e.g., matters arising pursuant to an agreement between the JV and the Sponsor or an affiliate of the Sponsor)

• Giving notices, calling default, enforcing remedies, granting waivers and negotiating amendments

• May reserve a right to act when Sponsor has failed (after notice)

• May retain the right to take any and all Major Decisions unilaterally (particularly if 80% or more of equity)

• Consider what this really means (e.g., can Investor Member amend the LLC agreement, cause breach of loan documents or act in violation of the LLC agreement. . .?)

Management, Page 4

17Copyright ©2018 Sullivan & Cromwell LLP

Management Management, Page 5

Investor Member Approval Rights • Major Decisions

• Who can propose a Major Decision for consideration, and who must approve (Investor Member vs. Investor Member and Sponsor)?

• Drafting Note: Choice between “Sponsor” and “Managing Member” could make a difference following removal

• Significant Decisions vs. Fundamental Decisions

• Spending outside approved budget

• Incurring debt

• Acquiring additional property

• Sale or other disposition of property

• Affiliate agreement

• Material contract

• Commencing or settling litigation

• Admitting additional Members

• Bankruptcy *

• Merger or other restructuring

• Forming a subsidiary

• Becoming an employer

• Any action that would result in a loan default

• Amending JV agreement

18Copyright ©2018 Sullivan & Cromwell LLP

Management

Removal

• Can Managing Member be Removed?

• Without cause – i.e., at election of Investor Member?

• For cause – e.g., fraud, misappropriation, willful breach (e.g., taking major decision without requisite approval), criminal indictment/conviction

• Upon an agreed trigger

• Failure to satisfy a “key man” requirement

• Failure to meet an agreed performance measure

• Tied to business plan

• Tied to a schedule

• Tied to results (occupancy/revenues)

Management, Page 6

19Copyright ©2018 Sullivan & Cromwell LLP

Management

• Consequences of removal

• Loss of management function

• loss of approval rights, not just role reversal

• Loss of promote or fees – is that fair? Should promote at least be available if needed by the JV to properly reward a replacement manager?

• Termination of affiliate agreements

• Loss of other rights (e.g., to initiate buy/sell or forced sale)

• Buyout of interest

• At FMV

• Discount to FMV

• Invested capital

Management, Page 7

20Copyright ©2018 Sullivan & Cromwell LLP

Management

Budget

• Members should have clear understanding of how and when JV funds will be spent

• Budget is the main tool for Investor Member to control expenditures

• Can give Sponsor/Managing Member broad authority

• Investor Member should pay careful attention to scope and format of proposed budget

Management, Page 8

21Copyright ©2018 Sullivan & Cromwell LLP

Management

• Consider appropriate mechanisms to give Managing Member appropriate breathing room to do its job

• Reserves

• Permitted variations (e.g., 5% of any line item, but not more than 3% in the aggregate)

• Ability to re-allocate cost savings from one line item to another

• Exception for emergency expenditures

• Exception for non-discretionary items

• RE taxes, insurance, utilities

• Loan payments (scheduled vs. all)

• Amounts due under approved contracts

Management, Page 9

22Copyright ©2018 Sullivan & Cromwell LLP

Management

• Consider timing, to assure resolution of any disputes (keeping in mind that mortgage lender may have separate approval rights)

• Approval process

• Managing Member produces or commissions initial draft for review (60-90 days before year-end)

• Investor Member reviews and approves or objects within a reasonable time (e.g., 2 weeks)

• Deemed approval (may only apply after second notice, with legend in all caps and “BOLD”, “warning, failure to act will. . .”, etc.)

• Managing Member must have obligation to revise and re-submit on shorter timeframe

Management, Page 10

23Copyright ©2018 Sullivan & Cromwell LLP

Management

• What happens if Members cannot agree on proposed budget?

• Majority owner may have final say

• Deadlock – not great for project, may appear to give leverage, but exercise of power may not be practical (cutting off nose to spite face)

• Require objection by line-item (line-items that did not draw an objection considered approved for new year)

• Use prior year’s budget until the parties can agree

• Possibly with a % increase (e.g. 3% for inflation)

• Limit to non-discretionary items

• Prior year might not have been a good reference year

• May not always be appropriate (e.g., development project)

• Avoids complete shutdown, but may encourage a Member to hold out

• Consider a sunset after 3-6 months to ensure further negotiation

Management, Page 11

24Copyright ©2018 Sullivan & Cromwell LLP

Management

• Managing Member should be required to propose an update to the budget to address a mid-year change in circumstances

• In some cases, Investor Member can unilaterally adjust the budget during the year (prospective only)

• Budget controls are only as good as the form of budget

• If possible, attach agreed form to establish required detail

• Investor Member must be diligent in annual review

Management, Page 12

25Copyright ©2018 Sullivan & Cromwell LLP

Management

Guaranty Obligations• JV may need external guaranty to support a financing, lease or other

obligation (common for commercial mortgage debt)

• If a partner provides credit support, directly or through a credit worthy affiliate, the partner or its affiliate may require compensation (e.g., a guaranty fee or incremental additional share of distributions)

• JV agreement should address reimbursement of guaranty payments• Deemed capital contribution by guarantor

• Special capital call to restore balance

• Repayment before distributions

• Special management rights (e.g., right to initiate forced sale)

• Some Major Decisions warrant special consideration (e.g., bankruptcy or other willful breach of loan terms)

• Treatment may be different depending on basis for guaranty claim• Environmental vs. voluntary bankruptcy, transfer in breach or other “bad boy” act)

• May address in JV agreement or in a separate agreement between principals

• Failure to address could result in unintended windfall to unaffiliated partners

• Consider treatment upon transfer by or removal of guarantor/affiliate• Condition buyout (or removal?) upon obtaining release (prospective only)

• Remaining Member to provide credit backstop

Management, Page 13

26Copyright ©2018 Sullivan & Cromwell LLP

Capital Contributions

• Capital normally is called only when $ is needed (timing will impact annualized returns)

• Will partners fund pro rata or on some other basis?

• Pro rata is the norm

• One partner may fund disproportionately initially or until a target is reached

• Preferred equity may defer funding until common equity has achieved minimum target

• Sponsor may have a right to bring in additional partners if initial partners reach a funding limit or otherwise decline further investment

• Will the Sponsor be responsible for cost overruns (e.g., in development project)? Will the Sponsor receive credit for $ contributed to cover overruns and, if so, how and when?

27Copyright ©2018 Sullivan & Cromwell LLP

Capital Contributions

• Who can call capital?

• Managing Member – when needed or when approved by Investor Member (specifically or by virtue of the approved budget)

• Investor Member (when Managing Member is failing to act)

• Is funding voluntary or mandatory? Is there an upper limit?

• What are the remedies/consequences for failure to fund (hard to draft well)

• Return funded capital to the Members pending agreement

• Allow funding Member to cover shortfall as:

• A loan to the Company, to be repaid before distributions to Members;

• A loan to the non-funding Member (to be repaid from distributions otherwise payable to the non-funding Member; any recourse?); or

• Additional capital that dilutes the non-funding Member’s interest

• Funding Member may have the right to convert a Member loan to equity at will or after an agreed delay (to allow non-funding Member to raise funds to repay)

Capital Contributions, Page 2

28Copyright ©2018 Sullivan & Cromwell LLP

Capital Contributions

• Penalties for failure to fund capital when called; options include:

• No penalty if funding is not mandatory (but % will be diluted)

• Punitive dilution if funded as equity (e.g., 2:1 credit, with corresponding adjustment to invested capital and % interests)

• Partner loan to non-funding partner or to JV, in either case with interest at a default rate

• Action to compel funding by defaulting partner (or guarantor thereof – not common, but important to consider if an investor funded through a special purpose entity)

• Admit a new investor to fund the shortfall (terms?)

• Buy out defaulting partner • Based on invested capital, FMV or discount to FMV (may be delayed

until a threshold is reached, e.g., dilution below X% or representing more than Y% of initial investment)

• Elimination of rights (vote or other rights; entire interest)

• Loss of capital credit (e.g., 50% reduction in capital contribution credit)

Capital Contributions, Page 3

29Copyright ©2018 Sullivan & Cromwell LLP

Capital Contributions

• Special Considerations re Penalty for Failure to Fund

• If non-funding Member is diluted, will there be any change in percentage interest used for subsequent capital calls?

• A Member loan at default interest may be more tax-efficient for the funding Member than imposing punitive dilution due to timing of income recognition

• A REIT may not want to own unsecured debt (bad REIT asset); some REITs propose a special preferred equity interest in lieu of debt (should be available to all Members on same basis)

Capital Contributions, Page 4

30Copyright ©2018 Sullivan & Cromwell LLP

Distributions

• Partner Loans (debt always paid before equity)

• Return of Capital • Return of invested funds

• Often pro rata, but can be with priority

• Based on character of funds, e.g., return “of” is only paid from capital event proceeds

• Return on Investment• Pro rata until each partner (or a benchmark partner) has received

an agreed annualized return

• IRR – Internal Rate of Return (excludes external factors)

• Excel’s XIRR function compounds annually

• Unlimited Variations• Can introduce additional layers/priorities

• Cash from operations vs. capital event proceeds

31Copyright ©2018 Sullivan & Cromwell LLP

Distributions

• Basic Distribution Waterfalls

• Straight up: all distributions paid pro rata in accordance with invested capital

• Priority: to Investor Member until “X”, and then to Sponsor Member as catch-up and thereafter pro rata

• Based on character of funds: e.g., operating revenues per one provision and capital event proceeds per another

• Promote: to all partners pro rata untila certain IRR and thereafter a special allocation to one partner (the “promote” interest) and the balance to all partnerspro rata

Distributions, Page 2

Return of CapitalReturn of Capital

Return on Capital(e.g., to a __% IRR)

Return on Capital(e.g., to a __% IRR)

Promote (level 1)e.g., 10% to Sponsor, balance to

partners pro rata

Promote (level 1)e.g., 10% to Sponsor, balance to

partners pro rata

Promote (level 2)e.g., 20% to Sponsor,

balance to partners pro rata

Promote (level 2)e.g., 20% to Sponsor,

balance to partners pro rata

32Copyright ©2018 Sullivan & Cromwell LLP

Distributions

• Promote

• Disproportionate distribution to the Sponsor, usually only after all Members have achieved an agreed minimum return

• Simple example on prior slide

• Terminology: “twenty percent over a five”, which means a special allocation to the Sponsor of 20% of all cash available for distribution after all Members have achieved a 5% IRR

• Consider how the IRR hurdle is drafted (e.g., after a named partner has achieved an agreed IRR vs. after all partners have achieved an agreed IRR)

• Can be portfolio-based or asset-by-asset

• Clawback

• Provision that addresses a situation in which, with the benefit of hindsight, early installments of promote are later determined to have been unwarranted

• Can arise in multi-asset portfolios, if promote is paid on a by-asset basis, and also if additional capital is required after the Sponsor has earned promote

• Can address by return of promote (for reallocation among Members) and/or by adjusting subsequent capital funding to reverse prior promote

Distributions, Page 3

33Copyright ©2018 Sullivan & Cromwell LLP

Distributions

• Clawback Guaranty

• Because Managing Member is often a single purpose entity with no other assets, consider whether a credit parent should guaranty the obligation to fund clawback payments (recognizing that final determination would be made at end of investment, when Managing Member may not be receiving sufficient further distributions to fund the clawback payment)

• Escrow – alternatively, the Managing Member could be required to leave promote payments in escrow (e.g., with the JV) pending confirmation that promote will not be subject to clawback

• Clawback is not always required,particularly if no expectation ofpromote payments before sale

Distributions, Page 4

34Copyright ©2018 Sullivan & Cromwell LLP

Distributions

Tax considerations

• JVs do not pay entity-level income tax; income, loss and other tax attributes are allocated to Members per JV agreement

• JV gives each partner a report of annual income (Form K-1)

• Income is allocated to the Members in the year realized, regardless of whether the JV actually distributes any cash

• If distributions are not paid on a strictly pro-rata basis, the allocations of tax items (income, loss, deduction) must be made in a manner that corresponds with economic reality

• The tax rules permit more than one method of allocating tax items, and the differences can have a significant impact on the tax treatment of a Member’s investment

• Important to include tax counsel early and throughout the preparation and negotiation of any JV agreement

Distributions, Page 5

35Copyright ©2018 Sullivan & Cromwell LLP

Distributions

• Tax Distributions

• JV partners sometimes agree in advance that, if it has the cash available at the end of the year, the JV will make a special distribution to help the partners pay the taxes due as a result of their having been JV partners during that year

• Distributions of this type are referred to as “tax distributions”

• In general, the partners agree that if aggregate distributions to a partner in a particular tax year did not at least match the federal, state and city income tax owed by the partner on income allocated to it for that year (assuming highest marginal tax rates), the JV will make a special distribution to the partner as necessary to cover the shortfall

• Tax distributions, if any, are then taken into account when computing subsequent distributions, and adjustments are made, as necessary to bring the partners back into conformity with the general distribution regime

Distributions, Page 6

36Copyright ©2018 Sullivan & Cromwell LLP

Transfer Rights

• JV agreements often prohibit all transfers, unless approved by the Managing Member or pre-approved in the transfer section

• Approving a proposed transfer is often a Major Decision• Does this mean the Managing Member can approve its own

transfers?

• Members sometimes negotiate for pre-approval of:• Transfers to affiliates

• Transfers among existing Members

• Transfers for estate planning

• A transfer if the interest is first offered to existing Member(s)

• Approved transfers are often more accommodating to the Investor Member than the Sponsor/Managing Member

• Consider whether the prohibition should also apply to transfers of interests in a Member (indirect transfers) and, if so, how far up and what exceptions are needed (e.g., for transfers of LP interests in a fund or of publicly traded shares)

37Copyright ©2018 Sullivan & Cromwell LLP

Transfer Rights

• Special Provisions:

• No transfer that will raise PTP risk or require registration under securities laws

• No transfer to a “prohibited person”

• No transfer in violation of law

• No transfer without corresponding assumption

• [No transfer that will result in tax termination (no longer a problem)]

• Any transfer to a third party is subject to ROFO or ROFR

• Drag-along and tag-along rights

Transfer Rights, Page 2

38Copyright ©2018 Sullivan & Cromwell LLP

Exit Mechanism; Dispute Resolution

Members are reluctant to be trapped in a JV; here are some options if the JV relationship starts to break down:

• If Investor Member owns substantial majority, it may have final say on any disagreement

• Allow transfer of interest – subject to agreed limitations

• Allow transfer after a right of first offer (ROFO)

• Grant the other Member a right of first refusal (ROFR) – right to match

• Buy/sell

• Initiating Member offers to buy the other; recipient must choose either to sell or to reverse the transaction and buy the initiating Member’s interest at the valuation implied by the initial offer

• Can work against a Member with limited access to capital

• Financing and/or credit support arrangements (i.e., a guaranty) may have an impact on decision whether to initiate or how to respond

39Copyright ©2018 Sullivan & Cromwell LLP

Exit Mechanism; Dispute Resolution

• Forced sale – the dissatisfied Member can require that the JV market and sell the property and dissolve the JV

• Solves for lack of capital

• Consider who will run the sale process and how

• Non-initiating Member should have option to buy out the initiating Member at implied valuation to avoid sale

• Purchase price is based on hypothetical sale/liquidation

• Should address transfer tax and other costs (actual vs. deemed)

• Arbitration may be good for legitimate dispute re value or another factual matter, but is less useful for mere disagreement about a business decision

• Business teams may be inclined to say “we’ll just have to work it out”, but is bad planning to allow true deadlock

Exit Mechanism; Dispute Resolution, Page 2

Benjamin WeberPartnerSullivan & Cromwell [email protected](212) 558-3159

Seth HoffmanChief Operating Officer and

General Counsel HighBrook [email protected](212) 906-4317

Any questions?