real estate cairo - commercial property and investment ...€¦ · february with the participation...

TRANSCRIPT

Real Estate Market Overview Q1 2012

Cairo Cairo

Cairo – Regaining Stability • The Cairo real estate market remains characterised by

uncertainty. The upcoming Presidential Elections should provide greater direction and usher in a period of greater certainty over the second half of 2012.

• However more clarity is returning to the market as the dust continues to settle following the revolution in 2011. This is resulting in increased levels of confidence and activity. Evidence of this includes:- - The first Cityscape Egypt finally took place at the end of

February with the participation of most of the major real estate developers and the announcement of several new projects by developers such as Amer Group.

- While many development projects have been delayed, some major projects continue towards completion. Cairo Festival City will deliver its first office phase in mid-2012 and Damac is looking to open its retail and office project opposite Dandy Mall in 2013.

- Construction has recommenced on a number of projects that had previously been suspended (eg: Qatari Diar’s major mixed use development on the Nile Corniche).

- The residential sector has seen returning confidence and increased sales activity. SODIC has recently announced that several future stages of their West Town project have now been ‘Sold Out’ off plan.

- Tourist visitors to Egypt have increased by 40% in the first quarter (compared to Q1 2011), providing a major boost to the Cairo hospitality sector.

- There remains active demand for up to 10,000 sq m of office space from international occupiers, although many of these groups have scaled back their requirements in light of portfolio optimisation strategies and have postponed decisions until after the results of the presidential elections are known.

- Retailers continue to open new stores with recent examples including Go Sport which signed a contract for their first store in Egypt at Dandy Mall. First IMAX cinemas has also signed a contract to open in the Sheikh Zayed neighbourhood on 6th October.

- Many local retailers have continued to take new units in street front locations.

• The prospects for the Cairo real estate market for the remainder of 2012 and beyond will be largely dependent upon the ability of the new President to work with the government to address many of the challenges that have been left largely unresolved over the past year.

2

Talking Points • Whilst clarity maybe returning to the market, the Egyptian

economy has not yet recovered from the impact of the 2011 revolution. Real GDP grew by just 1.8% in 2011 and is forecast to grow by even less in 2012, with IHS Global Insights revising its 2012 forecast down to just 0.8%. However stronger growth of 4.8% is forecast for 2013.

• Despite further meetings between the government and the IMF, final approval for the proposed USD 3.2 Billion loan to Egypt has yet to be received.

• The Central Bank of Egypt has announced that for the first time since the revolution foreign reserves increased by USD 100 million in April to reach USD 15.2 Billion.

• Tourist numbers increased by 40% over Q1. While tourist arrivals to Egypt decreased in January, February recorded an increase of 257% compared to February 2011 with the number of tourists exceeding 750,000. This trend continued in March with tourist numbers up 73% on the corresponding month last year.

• After several delays, Cityscape Egypt, a major real estate exhibition, finally took place on the 20th of February. Most of the large developers participated in the exhibition offering new products and more flexible payment terms.

• Property tax could be introduced in July. The Ministry of Finance announced that the property tax law had been revised and sent to the parliament for approval.

• As part of its effort to attract capital repatriation from Egyptians living abroad, the National Bank of Egypt announced US Dollar savings certificates with attractive interest rates. The accounts are now available for countries in the Gulf area and are likely to be extended to other countries later in the year.

• There has been positive feedback on the land sales programme

to overseas Egyptians. In March, the Ministry of Housing announced the release of 8,000 land plots in new cities around Cairo for Egyptian citizens living abroad. 350 reservations were received with some down payments having already been transferred.

3

Cairo Rental Clock - Q1 2012

*Hotel clock reflects the movement of RevPAR. Source: Jones Lang LaSalle Note: This diagram illustrates where Jones Lang LaSalle estimate each prime market is within its individual rental cycle as at end of relevant quarter.

4

Q1 2012

Rental Growth Slowing

Rents Falling

Rental Growth Accelerating

Rents Bottoming Out

Office

Retail

Hotel*

Residential

Cairo Market Overview

Office

• Grade A vacancies have increased to approximately 38% following recent completions of Grade B and C buildings in New Cairo and elsewhere. The vacancy rate is expected to increase further as additional new supply is delivered in 2012.

Office Supply • There was just one new building completed in Q1 2012. This as

the Summit 44 building on 90 Road in New Cairo with a GLA of 17,500 sq m. The major tenant in this building is Nestle who are occupying approximately 7,500 sq m.

• This completion brings the current Grade A office stock to approximately 729,000 sq m across the Cairo metro area. The vast majority of this space is in the new urban cities (New Cairo & 6th of October), with just one building, Nile City Tower (108,000 sq m), providing Grade A quality space in Central Cairo.

• A further 61,000 sq m is expected to complete over the rest of 2012 with major projects including Cairo Festival City (20,000 sq m) and Mivida by Emaar Misr.

• Recent completions of Grade B space and the upcoming supply of Grade A space are providing tenants with an improving standard and range of options. This is resulting in more tenant favourable market conditions in the office sector.

• A potential 260,000 sq m of new space that could be completed before the end of 2014, increasing the current Grade A stock to around 1 million sq m. However, much of this space is only likely to be constructed once tenant commitments have been secured. This is proving difficult as many occupiers are currently adopting a ‘wait and see’ approach and placing their expansion plans on hold. Actual completion levels are therefore likely to be more limited.

Source: Jones Lang LaSalle, Q1 2012 Note: GLA of Grade A Office Space

6

711 711 729 790940

61150 50

0

200

400

600

800

1,000

1,200

2010 2011 2012 2013 2014

Total

Stoc

k (`0

00 sq

m)

Office Supply (2010 – 2014)

Future Supply Completed Stock

Major Existing & Future Office Projects in Greater Cairo

Downtown

Helwan

Smart Village

6 Oct City & Sheikh Zayed

New Cairo

CityStars

Nile City Towers

Maadi

Citadel Plaza

Mivida

Existing

Future Supply

Cairo Festival City

7

Office Rental Performance • Peaking at USD 55 per sq m per month in 2010, the effective

rent for Prime office space in Central Cairo declined by around 20% during 2011.

• There has been no change in Prime office rents in Q1 2012, with rents in the only Grade A building in Central Cairo (Nile City Towers) remaining at USD 45 per sq m per month.

• The major reason for this decline in rentals during 2011 was the release of Grade B space into the market during a period of limited new tenant demand. Grade A rents are likely to decline further in 2012 in line with upcoming supply.

• Asking rents for Grade B space in Central Cairo currently range from USD 20 –36 per sq m per month, which are more in line with Grade A space in New Cairo.

• Asking rentals for Grade A space in New Cairo and West Cairo are currently around USD 25 and USD 20 per sq m per month respectively.

• Leasing incentives such as rent free periods, landlord contributions to fit out and the provision of additional parking slots, are expected to increase across all building grades, causing net effective rentals to decline. It is anticipated that secondary / lower quality buildings will be hardest hit when forced to compete with new better quality product as it is introduced into the market.

• Other means by which landlords are becoming more accommodating include more flexible lease terms, providing tenants with rolling break options and the right of first refusal.

Source: Jones Lang LaSalle * Prime office rents in Central Cairo

Prime Office Rents* (Q4 2010 – Q1 2012)

8

Indicator Level Comment / Outlook

Current Grade A Office Stock 729,000 sq m Most Grade A supply outside of Central Cairo (eg: City Stars) with Grade A supply in CBD limited to one building – Nile City Tower.

Future Grade A Supply (2012) 60,000 sq m Further construction delays and cancellations could reduce this supply pipeline.

Greater Cairo Grade A Vacancy 38%

Grade A rents in Central Cairo New Cairo West Cairo

USD 45 / sq m / month USD 25 / sq m / month USD 20 / sq m / month

Office Market Summary

9

Cairo Market Overview

Residential

• Many of the larger developers like Emaar & Amer Group have extended their payment plans to offer 7 to 10 year programs and this has stimulated further demand.

• Reflecting the increased confidence in this market, Amer Group has launched 6 new projects across Egypt of which 3 are in Greater Cairo (Porto New Cairo, Porto October and Porto Pyramids).

• While not covered in our supply data, the government is going forward with providing low income housing under the Youth housing program launched in 2007. This is in addition to the new plan to build 1 million affordable housing units announced in 2011.

Residential Supply & Demand • New large developments within central Cairo are almost non-

existent with the exception of the Uptown Cairo project by Emaar Misr.

• Our coverage of the residential sector focuses on gated compounds offering high quality villas and apartments in the new urban cities.

• There has been a major shift from high end luxury villas to apartments aimed at middle income earners within gated compounds over the past two years, as this sector was previously under supplied. Major developers such as Palm Hills Development (PHD) and 6th of October Development and Investment Company (SODIC) have led this shift towards mid-priced upscale apartments.

• Developers such as Orascom Housing Development (OHD) have invested in more affordable housing projects

• The residential market has witnessed an improvement in performance and sentiment during Q1 2012, following the High Court ruling in favour of TMG in the highly publicised Madinaty project.

• This increased activity is reflected by strong sales in Westown by SODIC where the first 3 phases (approximately 300 units) have been sold ‘off plan’.

11

53 69 73 78105

5

27

24

020406080

100120140

2010 2011 2012 2013 2014

Numb

er o

f Unit

s (in

000's

)

Future Supply Completed Stock

Source: Jones Lang LaSalle, Q1 2012

Residential Supply (2010 - 2014)

Major Existing & Future Residential Projects in Greater Cairo

12

Helwan

New Cairo Palm Hills October

Westown Mivida

Existing

Future Supply

Cairo Festival City

New Giza Katameya Heights

DreamLand

kenana

Residential Performance Demand Drivers • An increase in the number of marriages per annum is the major

driver of demand for residential units in Cairo. There were over 860,000 marriages in Egypt in 2011.

• Most of the end user demand is targeting the two new urban cities. This is likely to continue as more companies decentralise and employees seek residences closer to their workplace.

• Demand for residential units in downtown Cairo is driven by investors and a small portion of the population who are looking to upgrade their area of residence.

• Efforts by the government to grow the mortgage sector in Egypt could potentially push demand further.

Performance • The average price per sq m in New Cairo is estimated at around

USD 1,780 for villas and USD 1,040 per sq m for apartments. • Within 6th of October, the average price for villas is currently

USD 1,246 and USD 916 per sq m for apartments. • The average rent for a three bedroom villa in New Cairo is

currently USD 3,100 per month while two bedroom apartment rentals average almost USD 1,000 per month.

• For 6th of October, the average rental for three bedroom villa is around USD 2,800 per month while two bedroom apartments rent for around USD 850 per month.

13

0200400600800

1,0001,2001,4001,6001,8002,000

Apartment Villa Apartment Villa

6th of October New Cairo

USD

per s

q m

Sale Price (Q1 2012)

- 500

1,000 1,500 2,000 2,500 3,000 3,500

Apartment Villa Apartment Villa

6th of October New Cairo

USD

per m

onth

Rental Rates (Q1 2012)

Source: Jones Lang LaSalle* * Rentals relate to a basket of two bedroom apartment and three bedroom villas in each location.

Source: Jones Lang LaSalle* * Sale prices USD per sq m

Indicator Level Comment / Outlook

Current Stock 72,000 units Based on a sample of 100 gated compound projects in New Cairo and 6th of October

Future Supply (2013) 27,000 Units Further construction delays and cancellations could reduce this supply pipeline.

Sales Performance (USD / SQ M) New Cairo Villa Apartment 6th of October Villa Apartment

1,780 1,050

1,250 920

Rental Performance (USD/ Month) New Cairo 3 bedrooms Villa 2 bedrooms Apartment 6th of October 3 bedrooms Villa 2 bedrooms Apartment

3,100 970

2,800 850

Residential Market Summary

14

Retail Cairo Market Overview

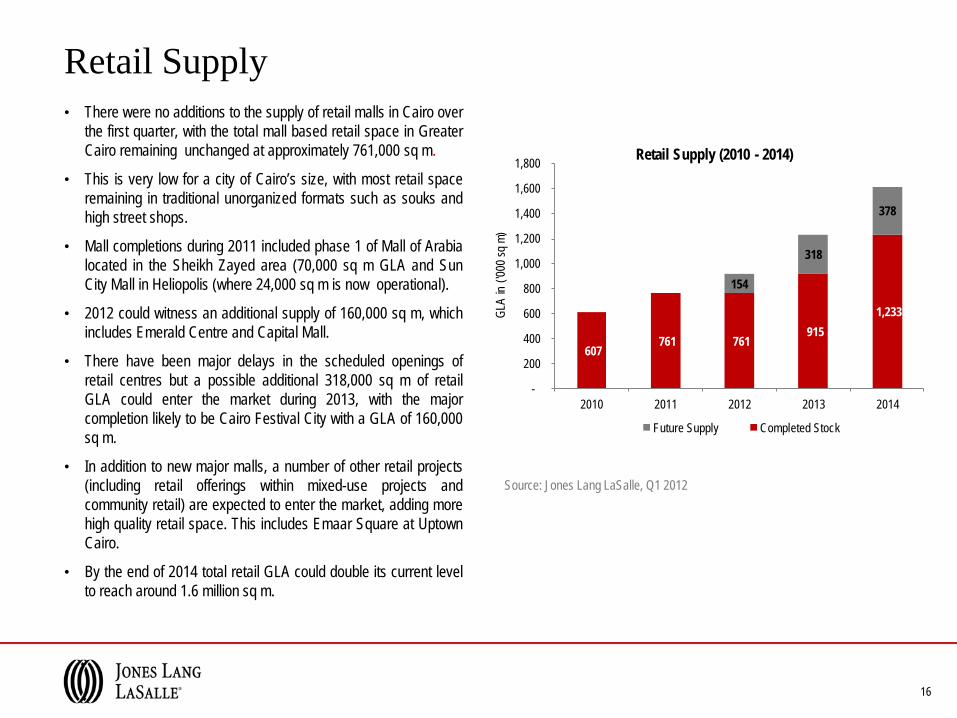

Retail Supply • There were no additions to the supply of retail malls in Cairo over

the first quarter, with the total mall based retail space in Greater Cairo remaining unchanged at approximately 761,000 sq m.

• This is very low for a city of Cairo’s size, with most retail space remaining in traditional unorganized formats such as souks and high street shops.

• Mall completions during 2011 included phase 1 of Mall of Arabia located in the Sheikh Zayed area (70,000 sq m GLA and Sun City Mall in Heliopolis (where 24,000 sq m is now operational).

• 2012 could witness an additional supply of 160,000 sq m, which includes Emerald Centre and Capital Mall.

• There have been major delays in the scheduled openings of retail centres but a possible additional 318,000 sq m of retail GLA could enter the market during 2013, with the major completion likely to be Cairo Festival City with a GLA of 160,000 sq m.

• In addition to new major malls, a number of other retail projects (including retail offerings within mixed-use projects and community retail) are expected to enter the market, adding more high quality retail space. This includes Emaar Square at Uptown Cairo.

• By the end of 2014 total retail GLA could double its current level to reach around 1.6 million sq m.

Source: Jones Lang LaSalle, Q1 2012

16

607 761 761

915 1,233

154

318

378

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2010 2011 2012 2013 2014

GLA

in ('0

00 sq

m)

Retail Supply (2010 - 2014)

Future Supply Completed Stock

Major Existing & Future Malls in Greater Cairo

Mall of Arabia

Dandy Mall

Cairo Festival City

Sun City Mall

CityStars

Maadi City Centre

Existing

Future Supply

17

Composition of Retail Supply • Cairo is currently under provided with retail malls. The proportion

of total retail space in malls will increase in the future as multiple community and regional malls are delivered.

• Super Regional and Regional Malls will account for 29% of total mall based retail stock in Cairo by 2015.

Name Type of Retail Centre GLA (sq m)

CityStars Super Regional 150,000

Mall of Arabia Super Regional 180,000

Maadi City Center Regional 33,500

Dandy Mall Regional 65,000

Golf City Mall Regional 40,000

Sun City Mall Regional 60,000

Katameya Downtown Community 30,000

Source: Urban Land Institute (ULI)

Type of Centre Range of GLA (sq m)

Convenience Less than 3,000

Neighbourhood 3,000-10,000

Community 10,000-30,000

Regional 30,000-90,000

Super Regional 90,000-150,000

Source: Jones Lang LaSalle

Major Retail Centres in Greater Cairo

Retail Supply (by type in 2015)

Source: Jones Lang LaSalle

28%

20%

13%

11%

9%

9%

9%

1%

Community Super RegionalNeighborhood Specialty Lifestyle CentreConvenience RegionalBoutique Power Centre / Factory Outlet

18

Retail Rentals • Average quoting rents for prime line stores in Regional & Super

Regional malls in Greater Cairo have remained unchanged over the past quarter and currently range from USD 920 to USD 1,410 per sq m per annum. In certain circumstances, retailers may however achieve lower rates.

• Although the limited supply of good quality retail space in Greater Cairo should have resulted in strong competition and rental growth, the economic and security concerns stemming from the recent instability have had a negative impact on retail spending and have resulted in average asking rents for Regional and Super Regional malls declining by 20% - 30% over the past year.

• Average rental rates are expected to remain stable in the short term before possibly softening again in 2013 in the face of additional levels of new supply.

• While base rentals are lower than pre-revolution levels, some centres have been able to achieve turnover rentals over and above base rental levels.

• Retailers are asking to set rents in EGP rather than dollars, as they believe that the EGP will weaken over the next few years.

• Some retailers have been successful in negotiating tenant only break clauses, to manage their exit strategies if committing in an unstable or untested market.

• Most key retailers have scaled back or delayed their expansion plans, awaiting the outcome of the upcoming presidential elections. The most active current players include Carrefour, Al Shaya, Al Hokkair and Ra Sport.

• The number of new to market entrants has also reduced.

Source: Jones Lang LaSalle

Average Quoting Rental Rates: Regional / Super Regional Centres in Greater Cairo

Line Shops (USD / sq m / per annum) USD 920 – USD 1,410

19

Retail Sector Summary

Indicator Level Comment / Outlook

Current Retail Space (GLA) 761,000 sq m The GLA of good quality retail malls remains low but is increasing as a percentage of total GLA.

Future Supply (by end 2014) 1.6 million sq m There is a substantial supply which could potentially be added to the retail sector by the end of 2014.

Current Vacancy Level

29% The vacancy rates represent the operational Super Regional malls in Cairo.

Average quoting rents (line stores in regional / sub regional malls)

USD 920 - USD 1,410 sq m per annum

Rents are expected to remain stable in short term before declining in longer term due to increased competition.

20

Cairo Market Overview

Hotel

Hotel Demand & Supply

• The tourism sector has been one of the fastest growing areas of GDP over the past five years but due to the instability the country went through in 2011, the tourism sector experienced a 33% decline in tourist arrivals to Egypt.

• The tourism losses in 2011 are estimated to be worth in the order of USD 3.8 Billion. Tourist nights decreased by 22% to 114 million nights in 2011 after reaching 141 million nights in 2010.

• Average tourist expenditure per day has also declined from USD 80 in 2010 to USD 72 in 2011.

• The greatest decline was among Americans, where tourist arrivals declined 49% in 2011, with European tourist numbers decreasing by 35% to 7.2 million in 2010 from 11.1 million in 2010

• Tourist arrivals have however recovered somewhat in Q1 2012 with a 40% increase recorded over 2011 levels. This increase was particularly marked in February (up 257% compared to Feb 2011 and March (up 73% )

22

Total Visitors in Egypt 2009 2010 2011

No of Tourists (Millions) 12.5 14.7 9.8 No of Nights (Millions) 126 141 114

Revenue (USD Billions) 10.7 12.5 8.8

Demand • There were no new hotel rooms introduced into the market in

Q1/2012 with the existing supply of quality rooms in Cairo remaining unchanged at 27,000 rooms in 159 properties.

• According to the Egyptian Hotel Association, there are a further

28 hotels offering 8,920 rooms currently under construction in Cairo.

05101520253035404550

02000400060008000

10000120001400016000

Hotel

s

Room

s

Current Hotel Supply

Rooms Hotels

Source: Egyptian Hotel Association 2011

Source: Ministry of Tourism 2011

Supply

Major Existing & Future Hotels in Greater Cairo

23

Existing

Future Supply

InterContinental City Stars

Marriott

Four Seasons

Dusit Thani

Hilton Dreams

St. Regis Cairo

Nile Ritz Carlton

Existing

Future Supply

Hotel Performance • The average daily rate (ADRs) has remained relatively stable at USD 54 in the year to March 2012. While this is largely in line with

levels recorded in 2011, it remains 60% below the level of USD 132 recorded in the same period of 2010.

• Average occupancy rates have however increased from their nadir of 35% in the first three months of 2011 to their current level of 45% (year to March 2012) on the back of the 40% increase in the number of tourist arrivals.

Source: STR Global

0102030405060708090

0

20

40

60

80

100

120

140

2007 YTD 2008 YTD 2009 YTD 2010 YTD 2011 YTD 2012 YTD

Occu

panc

y (%

)

ADR

(USD

)

Hotel Performance (YT March 2007 - 2012)

ADR Occupancy

24

Indicator Level Comment / Outlook

Total number of Hotels 159 Includes all Hotels ( 5,4,3,2,1 Stars and Unclassified)

Total number of rooms 26,800 Includes all Hotels ( 5,4,3,2,1 Stars and Unclassified)

Occupancy (Year to March 2012)

45%

Average Daily Rate (ADR) (Year to March 2012)

USD 51

RevPar (1st Quarter 2012 )

USD 23

Hotel Market Summary

25

Definitions and Methodology Residential: • The supply data is based on our quarterly survey of 100 projects

located in New Cairo and 6th of October, starting from 2011.

• Completed building refers to a building that is handed over for immediate occupation.

• Residential performance data is based on two separate baskets one for rental basket for Villas and apartments and another basket for sales performance for both villas and apartments.

• The two baskets covers projects in both New Cairo and 6th of

October.

Retail:

• Classification of Retail Centres is based upon the ULI definition as published in Retail Development, 4th Edition published by ULI.

• Prime Rent represents the quoted average rent for the top 5 shopping malls in greater Cairo.

• Retail supply relates to the Gross Lettable Area (GLA) within retail malls.

Office: • The supply data is based on our quarterly survey of the Grade A

office space located in Downtown, New Cairo and West Cairo.

• Completed building refers to a building that is handed over for immediate occupation.

• Prime Office Rent represents the top open-market rent that could be expected for a notional office unit of the highest quality and specification in the best location in a market, as at the survey date (normally at the end of each quarter period). The Prime Rent reflects an occupational lease that is standard for the local market. It is a face rent that does not reflect the financial impact of tenant incentives, and excludes service charges and local taxes.

Hotels: • Hotel room supply is based on existing supply figures provided by

Egyptian Hotel Association as well as future hotel development data tracked by Jones Lang LaSalle Hotels. Room supply includes all graded supply and excludes serviced apartments.

• STR performance data is based on monthly survey conducted by STR Global.

26

www.joneslanglasalle-mena.com COPYRIGHT © JONES LANG LASALLE IP, INC. 2012 This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Ayman Sami Head Egypt [email protected]

Robin Pugh Head of Agency MENA [email protected]

David Macadam Head of Retail MENA [email protected]

Chiheb Ben-Mahmoud Executive Vice President Jones Lang LaSalle Hotels [email protected]

Marwan Sery Research Manager Egypt [email protected]

Craig Plumb Head of Research MENA [email protected]

Contacts:

Follow us on: