real estate 2010 edition

DESCRIPTION

A prime European investment marketTRANSCRIPT

I N V EST I N SW EDEN

Real EstateA prime European investment market – 2010 edition

Official name The Kingdom of Sweden

Political system Constitutional Monarchy

Head of State King Carl XVI Gustaf

Central government Center-right majority government, ruling since the election in 2006. General elections are held every four years.

Prime Minister Fredrik Reinfeldt

Population 9.3 million

Population density 22 per sq. km

Area 450,000 sq. km (174,000 sq. mi)

Time zone GMT + 1 hour (end October–end March)GMT + 2 hour (end March–end October)

GDP per capita $ 51,804 (SEK 398,490/€ 35,864)Source: IMD 2009

Exchange rates SEK 1 = € 0.09 SEK 1 = $ 0.13 (Average 2009)

Currency 1 krona = 100 öre

Largest cities (population*) Stockholm (1,958,884) Göteborg (915,062) Malmö (584,734)

* Greater metropolitan area

key facts sweden

Sweden

StockholmKarlstad

Gävle

Uppsala

Västerås

ÖrebroEskilstuna

Norrköping

Umeå

Luleå

Göteborg Jönköping

LinköpingBorås

Växjö

LundKristianstad

Karlskrona

Malmö

HelsingborgHalmstad

Kiruna

Sundsvall

Östersund

Europe

1

contents

2 Summary

4 Investment market

5 Investment market overview 6 Selected cross-border transactions 2009 7 Investment aspects 8 Case: KLP Eiendom

9 The Swedish economy

11 Key economic indicators

13 Fiscal aspects

16 Case: Green buildings and sustainable cities

18 Legal aspects

22 Cities & regions for investment

25 Case: Hospitality and leisure property

27 Contacts

Welcome to Sweden!

summary

Stable outlook, recovery underway

Sweden remains one of Europe’s most favored markets for cross-border investments, showing resilience throughout one of the most challenging periods in recent history. Attractive historical returns, an investor-friendly business environment and a diversi-fied and stable economy characterize the market.

A mature and liquid property market

Sweden has been a long time favorite for cross-border investment. An investor-friendly and efficient business environment, with profes-sional participants in all steps of the investment process, has contrib-uted to making Sweden one of Europe’s largest markets for cross-border property investment. National institutional investors and private investors ensure high liquidity in the major markets even in difficult times of the cycle. Many of the largest commercial property owners are international investors with a multi-year investment his-tory in Sweden.

One of the world’s most competitive countries

The Swedish economy boasts large numbers of global brand names across a wide range of industry sectors, including information tech-nology, energy and life science. Productivity improvements, low wage and price inflation and Sweden’s niche in high technology fields have benefited Sweden’s competitiveness. Sweden offers a stable and transparent business environment, great people skills and a high capacity for innovation. Sweden is also noted for high levels of inter-national trade; exports account for nearly 40 percent of GDP.

Sweden’s major export sectors Distribution of exports by industry sector, Jan–Nov 2009

Machinery, 16%

Electrical products & telecom, 14%

Chemicals & pharmaceuticals, 14%

Forest products, 13%

Minerals, 9%

Automotive products, 8%

Energy products, 7%

Other mechanical, 7%

Other, 12%

Source: Statistics Sweden

2

0

50

100

150

200

250

20092008200720062005200420032002

Foreign ownership of Swedish real estateSEK billion, by acquisition value

Source: Cushman Wakefield

Strong public finances, sound banking sector

The Swedish public finances are strong. The level of public debt in relation to GDP is far below many western peers. Having for many years emphasized the need for strong public finances, Sweden has had the means to introduce measures to counter the effects of the global economic slowdown. For example, strong injections are being made into the local government sector in 2010. Swedish banks are well capitalized and in good shape to support a recovering economy. The GDP outlook foresees a return to solid growth in 2010 and beyond.

–8–6–4–202468

Eurozone

Sweden

Interest rates, 10-year

Budget balance

Current account balance

Strong public financesCurrent account and budget balance, % of GDP

Sweden Eurozone

Source: Economist, February 2010

summary

Easy to do business

Skilled professionals, smooth business procedures and receptivity to international ownership make Sweden an easy country to operate in. Advisors have substantial experience in cross-border transactions and the legal system responds well to investor demands for security and cost-efficiency. Most documentation is in English. A strong presence of multi-national companies, many with regional headquarters for northern Europe located here, contributes to Sweden’s international business environment.

Investment opportunities

There is ample argument to support the view that Swedish property prices have now bottomed out, following a 2009 that saw both prices and invest-ment volumes fall. Yields have stabilized across all asset classes. Against the background of economic recovery prospects and the scope for sustain-able long-term growth, the Swedish property market now offers a range of investment opportunities. Among contributing factors are the positive yield gap, opportunities for discount on portfolios and larger investment volumes and still relatively high risk premiums.

International investor presenceA selection of foreign owners with property holdings in Sweden

Abu Dhabi Investment Authority (UAE)

AXA Real Estate Investment Managers (France)

Bank of Ireland Private Banking (Ireland)

Boultbee (UK)

Citycon (Finland)

Commerz Real (Germany)

Credit Suisse (Germany)

Deka (Germany)

Deutsche Bank/RREEF (Germany)

DnB Nor (Norway)

Ejendomsinvest (Denmark)

Eurocommercial (Netherlands)

GE Real Estate (US)

GIC Real Estate (Singapore)

HSH Real Estate (Germany)

ING Real Estate (Netherlands)

Invesco (UK/Germany)

Investea (Denmark)

IVG (Germany)

KLP Eiendom (Norway)

Klépierre (France)

MEAG (Germany)

Orion Capital Managers (UK)

Pembroke Real Estate (US)

Property Group (Denmark)

SveaReal (Norway)

Unibail-Rodamco (France)

Vital (Norway)

3

Gateway to the Nordic property markets

Sweden, Denmark, Finland and Norway are all mature property markets that offer high liquidity and transparency. As stable and diversified econ-omies with strong public finances they have all managed to mitigate the aftermath of the financial crisis better than most other nations. Sweden is the largest country, has the largest property investment market and is the natural base for property investment in the region. To date, Sweden has received the majority of investments into the region.

4

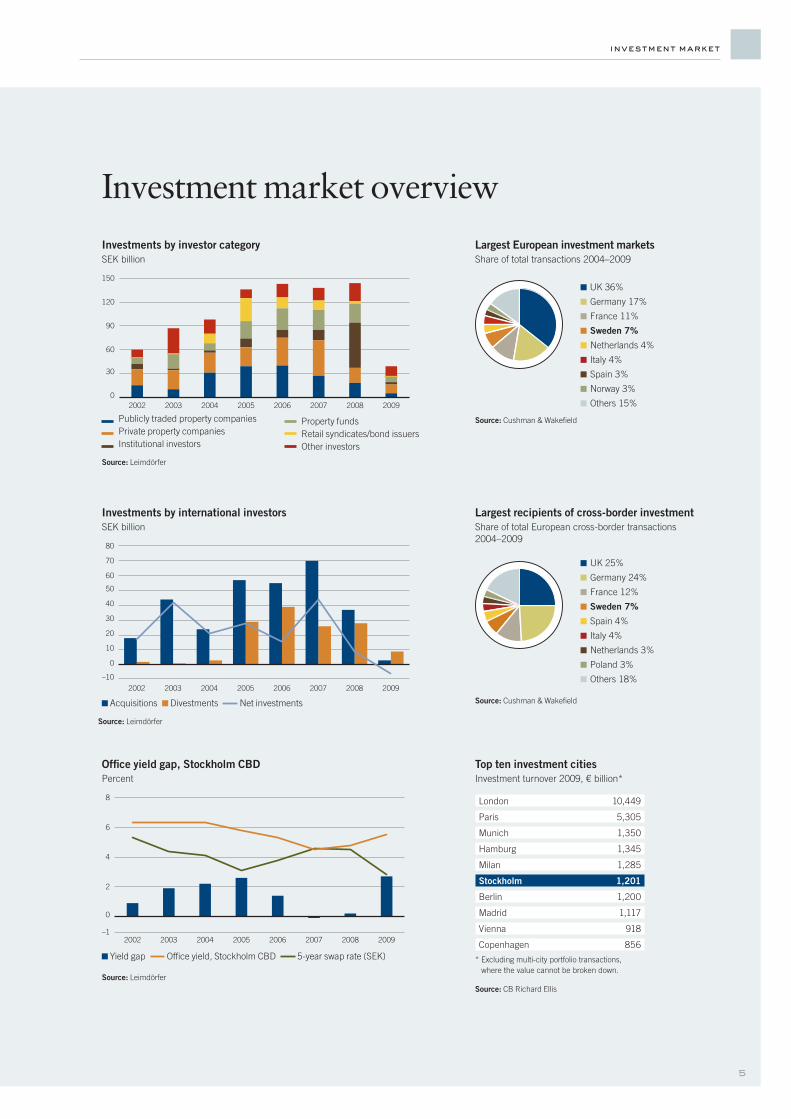

Subdued investment volumes and falling property prices during 2009 lead many to believe that the Swedish property investment market has reached the bottom. In the five-year period to 2009, Sweden was Europe’s fourth-largest investment market.

Stable investment market

Total real estate transactions amounted to some SEK 40 billion (€ 4 billion/$ 5.5 billion) in 2009, down by some 70 percent compared with 2008. Investments by international investors fell to its lowest level in more than a decade. Cross-border transactions, involving a foreign buyer or seller, amounted to 26 percent of total transaction volume compared with 36 percent in 2008. As the year progressed transaction activity picked up; transaction volumes more than doubled between the third and the fourth quarter. In spite of the reduced investment activity, Sweden remained one of Europe’s largest investment markets.

The challenging financing environment put a dampering effect on the size of transactions. However, there was still substantial transaction activity. In all, the total number of transactions valued at SEK 100 million (€ 10 million/ $ 14 million) or more were down by a relatively modest 25 percent compared with 2008.

Low-risk assets in favor

The year was marked by an absence of large portfolio transactions, with the exception of the SEK 1.7 billion (€ 170 million/$ 235 million) deal in the university city of Umeå, involving local real estate investors. The largest single asset transaction was the sale of the Royal Viking Hotel in Stockholm to the Norwegian institutional inves-tor KLP. The sale by Atrium Ljungberg of seven retail properties in southern Sweden to the Swedish-based prop-erty investor NIAM for SEK 1.0 billion (€ 100 million/ $ 142 million) was the largest retail transaction. The larg-est cross-border transactions are presented on page 6.

More than 30 percent of the total transaction volume was directed at residential property, compared with 15 per-cent in 2008. A large share of residential property is sold to housing cooperatives, particularly in the largest cities. Given the challenging market situation and the low risk

appetite, this is not surprising. The share of office property fell to 39 percent from 60 percent in 2008. The full break-down is presented on page 6.

Foreign investors that were active buyers during 2009 included Norwegian KLP mentioned above, German CommerzReal, Deka and IVG, as well as Pembroke Real Estate, the real estate arm of Fidelity Investments.

Substantial ownership by active investors

By year-end 2009, international investors owned Swedish real estate assets amounting to more than SEK 200 billion (€ 20 billion/$ 28 billion) by acquisition value. Among the major international owners are GE Real Estate, ING Real Estate, Klépierre, Unibail-Rodamco, Valad Property Group and London and Regional.

There is great diversity among investors, including property companies, institutional investors and property funds. As a large share of property assets are owned by active institutional investors and real estate companies there is generally good supply of investment product.

investment market

• Europe’s fourth-largest real estate investment market.• Europe’s fourth-largest cross-border investment location.• Substantial ownership by active investors.

key features

Europe’s fourth-largest investment market

5

investment market

Office yield gap, Stockholm CBDPercent

Yield gap Office yield, Stockholm CBD 5-year swap rate (SEK)

Acquisitions Divestments Net investments

0

10

20

30

40

50

60

70

80

–10

Divestments

Acquisitions

20092008200720062005200420032002

Net investments

0

2

4

6

8

–1

Yield gap

20092008200720062005200420032002

5-year swap rate (SEK)

O�ce yield, Stockholm CBD

0

30

60

90

120

150Other investors

Property funds

Institutional investors

Private property companies

Private property companies

Publicly traded property companies

20092008200720062005200420032002

Investments by investor categorySEK billion

Investments by international investorsSEK billion

Publicly traded property companies Private property companies Institutional investors

Property funds Retail syndicates/bond issuers Other investors

Source: Leimdörfer

Source: Cushman & Wakefield

Source: Leimdörfer

Source: Leimdörfer

Source: CB Richard Ellis

Largest European investment marketsShare of total transactions 2004–2009

UK 36%

Germany 17%

France 11%

Sweden 7%

Netherlands 4%

Italy 4%

Spain 3%

Norway 3%

Others 15%

Largest recipients of cross-border investmentShare of total European cross-border transactions 2004–2009

UK 25%

Germany 24%

France 12%

Sweden 7%

Spain 4%

Italy 4%

Netherlands 3%

Poland 3%

Others 18%

Source: Cushman & Wakefield

London 10,449

Paris 5,305

Munich 1,350

Hamburg 1,345

Milan 1,285

Stockholm 1,201

Berlin 1,200

Madrid 1,117

Vienna 918

Copenhagen 856

* Excluding multi-city portfolio transactions, where the value cannot be broken down.

Top ten investment citiesInvestment turnover 2009, € billion*

Investment market overview

investment market

Selected cross-border transactions 2009

Source: Cushman Wakefield

Source: Leimdörfer

Source: Leimdörfer Source: Leimdörfer

Type of premises by main use 2009Share of total transaction volume

Office 39%

Residential 31%

Hotel 8%

Industrial 7%

Retail 5%

Other 10%

International investor origin 2009Share of cross-border acquisitions

Germany 46%

Norway 43%

US 5%

Other 6%

Type of investors 2009Share of total investment market

Private property companies 28%

Property funds 18%

Publicly traded property companies 12%

Institutional investors 8%

Other investors 34%

Buyer Seller Property unit Price, MSEK Area, m²

Kungsleden, Sweden NLP, Norway Logistics property portfolio across Sweden 525 109,000

Deka, Germany Host Hoteleiendom, Norway Hotel property in Göteborg CBD 440 n/a

Catella Real Estate AG, Germany DB Real Estate, Germany Office property in Malmö CBD 405 11,000

IVG, Germany Skanska, Sweden Office property in Stockholm 400 12,000

Lundbergs, Sweden Boultbee, UK Retail property in Linköping 372 14,000

Svenska Bostadsfonden, Sweden Heimstaden, Norway Residential portfolio in Kalmar and Borgholm 300 31,000

Commerz Real, Germany TK Development, Denmark Retail property in Stockholm 280 14,300

Tegeltornet, Sweden Citycon, Finland Residential property portfolio in Stockholm 181 12,050

Heba, Sweden Citycon, Finland Residential property portfolio in Stockholm 176 6,100

Pembroke Real Estate, US Vasakronan, Sweden Office property in Stockholm CBD 160 3,150

Jernhusen, Sweden iii, Germany Office property in Göteborg CBD n/a 8,500

Ikano Bostad, Sweden Acta, Norway Residential property portfolio in Malmö n/a 28,500

Hemfosa, Sweden GPT Halverton, Australia Commercial property portfolio across Sweden n/a 63,000

Aberdeen Property Investors, UK Skanska, Sweden Office property in Malmö CBD n/a 14,200

KLP, Norway RBS Nordisk Renting, UK Hotel property in Stockholm CBD n/a 26,400

Börjesson family, Sweden Valad Property Group, Australia Office property in Malmö CBD n/a 10,500

AMF Pension, Sweden DB Real Estate, Germany Office property in Stockholm CBD n/a 25,600

KLP, Norway Diligentia, Sweden Hotel property in Malmö CBD n/a 13,600

6

Ownership Swedish commercial propertiesEstimated market value 2009, SEK 725 billion

Institutions and foreign owners 49%

Listed companies 15% Private owners 15% Municipal housing & public companies 13%

Housing co-ops 6% Owner occupier 2%

Source: Newsec

“ Sweden is a very accessible market for international investors and most properties are sold in an open process. For years, the economy has outperformed the majority of eurozone countries. I have few doubts about Sweden’s ability to maintain its leading compet-itive and innovative position.”

Steinar Manengen, CEO, KLP Eiendom

Finland

SwedenNorway

Estonia

Latvia

Lithuania

PolandGermany

Denmark

investment market

7

Investment aspects

Source: Newsec

Aberdeen Property Investors, UK

Acta, Norway

AFA Fastigheter, Sweden

Alecta, Sweden

Akademiska Hus, Sweden

Akelius Fastigheter, Sweden

AMF Pension, Sweden

Atrium Ljungberg, Sweden

Balder, Sweden

Boultbee, UK

Brinova, Sweden

CA Fastigheter, Sweden

Castellum, Sweden

Dagon, Sweden

Diligentia, Sweden

Diös, Sweden

DnB Nor/Vital, Norway

Fabege, Sweden

GE Real Estate, US

Heimstaden, Norway

Hufvudstaden, Sweden

Humlegården, Sweden

ING Real Estate, Netherlands

Kilenkrysset, Sweden

Klépierre, France

Kungsleden, Sweden

London and Regional, UK

Lundbergs, Sweden

Niam, Sweden

Nordisk Renting, UK

Norrporten, Sweden

Northern European Properties, UK

Property Group, Denmark

SEB Trygg Liv, Sweden

Skanska, Sweden

Stena Fastigheter, Sweden

SveaReal, Norway

Unibail-Rodamco, France

Vasakronan, Sweden

Valad Property Group, Australia

Wallenstam, Sweden

Wihlborgs, Sweden

The largest property owners in Sweden

Strong correlation to UK property market

Historically, the UK property market, e.g. London, has been a leading indicator for the Swedish property market, e.g. Stockholm. Looking at total returns for prime proper-ties in these two markets over the course of more than two decades, Stockholm typically lags developments in London with one year.

Positive yield gap

As a result of the record-low interest rates, the yield gap between five-year borrowing rates and office property yields currently amounts to 2.5–3 percent. This is expected to con-tract somewhat during 2010, as interest rates start to move upwards. Even so, the yield gap is expected to remain at historically high levels.

High transparency, low costs for transferring assets

The Swedish property market offers outstanding transpar-ency, due to openness in public property records, a highly-evolved legal system and an abundance of market infor-mation. Investment performance indices are also in place.

Market transparency, the reliability of the legal system and common use of standardized documentation concur to reducing transactions costs.

Stable domestic banking system

The Swedish property financing market is dominated by a handful of domestic banks and complemented by a number of international banks. Data from Statistics Sweden, which assembles statistics on Swedish-based financial institutions, show that Swedish financial institutions accounted for 88 percent of commercial property financing by year-end 2009, while foreign-owned financial institutions accounted for 12 percent.

The stability of the Swedish banking sector, aided by considerable government intervention during 2009, is a com-fort to the property investment market. Following capital raisings and other capital measures during 2009, the Swed-ish banks are now among Europe’s best-capitalized banks. SEB, for example, had a total capitalization of 14.7 percent at year-end 2009.

The Nordic property market comprises markets in Sweden, Denmark, Finland and Norway – stable countries with sizeable investment markets, high liquidity and transparency. Sweden, the largest country, is the natural base for property investment in the region and has seen the largest inflow of capital.

Gateway to investments in northern Europe

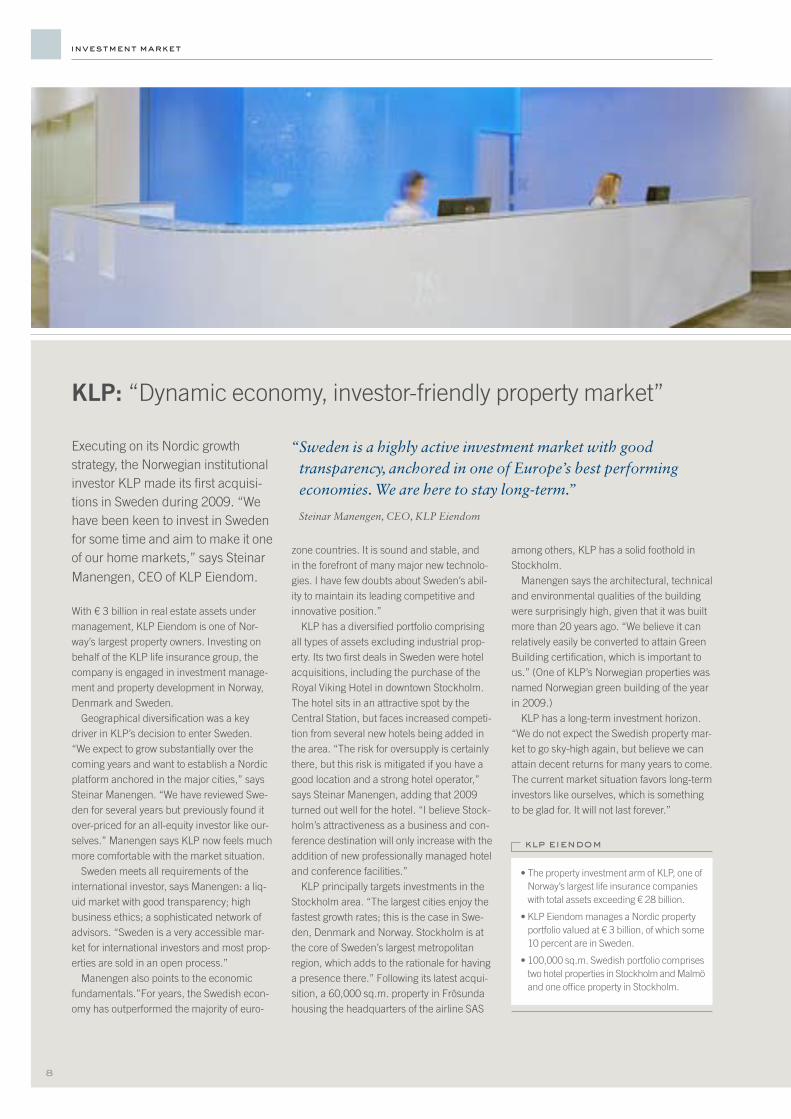

investment market

Executing on its Nordic growth strategy, the Norwegian institutional investor KLP made its first acquisi-tions in Sweden during 2009. “We have been keen to invest in Sweden for some time and aim to make it one of our home markets,” says Steinar Manengen, CEO of KLP Eiendom.

With € 3 billion in real estate assets under management, KLP Eiendom is one of Nor-way’s largest property owners. Investing on behalf of the KLP life insurance group, the company is engaged in investment manage-ment and property development in Norway, Denmark and Sweden.

Geographical diversification was a key driver in KLP’s decision to enter Sweden. “We expect to grow substantially over the coming years and want to establish a Nordic platform anchored in the major cities,” says Steinar Manengen. “We have reviewed Swe-den for several years but previously found it over-priced for an all-equity investor like our-selves.” Manengen says KLP now feels much more comfortable with the market situation.

Sweden meets all requirements of the international investor, says Manengen: a liq-uid market with good transparency; high business ethics; a sophisticated network of advisors. “Sweden is a very accessible mar-ket for international investors and most prop-erties are sold in an open process.”

Manengen also points to the economic fundamentals.”For years, the Swedish econ-omy has outperformed the majority of euro-

zone countries. It is sound and stable, and in the forefront of many major new technolo-gies. I have few doubts about Sweden’s abil-ity to maintain its leading competitive and innovative position.”

KLP has a diversified portfolio comprising all types of assets excluding industrial prop-erty. Its two first deals in Sweden were hotel acquisitions, including the purchase of the Royal Viking Hotel in downtown Stockholm. The hotel sits in an attractive spot by the Central Station, but faces increased competi-tion from several new hotels being added in the area. “The risk for oversupply is certainly there, but this risk is mitigated if you have a good location and a strong hotel operator,” says Steinar Manengen, adding that 2009 turned out well for the hotel. “I believe Stock-holm’s attractiveness as a business and con-ference destination will only increase with the addition of new professionally managed hotel and conference facilities.”

KLP principally targets investments in the Stockholm area. “The largest cities enjoy the fastest growth rates; this is the case in Swe-den, Denmark and Norway. Stockholm is at the core of Sweden’s largest metropolitan region, which adds to the rationale for having a presence there.” Following its latest acqui-sition, a 60,000 sq.m. property in Frösunda housing the headquarters of the airline SAS

among others, KLP has a solid foothold in Stockholm.

Manengen says the architectural, technical and environmental qualities of the building were surprisingly high, given that it was built more than 20 years ago. “We believe it can relatively easily be converted to attain Green Building certification, which is important to us.” (One of KLP’s Norwegian properties was named Norwegian green building of the year in 2009.)

KLP has a long-term investment horizon. “We do not expect the Swedish property mar-ket to go sky-high again, but believe we can attain decent returns for many years to come. The current market situation favors long-term investors like ourselves, which is something to be glad for. It will not last forever.”

KLP: “Dynamic economy, investor-friendly property market”

“ Sweden is a highly active investment market with good transparency, anchored in one of Europe’s best performing economies. We are here to stay long-term.”

Steinar Manengen, CEO, KLP Eiendom

• The property investment arm of KLP, one of Norway’s largest life insurance companies with total assets exceeding € 28 billion.

• KLP Eiendom manages a Nordic property portfolio valued at € 3 billion, of which some 10 percent are in Sweden.

• 100,000 sq.m. Swedish portfolio comprises two hotel properties in Stockholm and Malmö and one office property in Stockholm.

klp eiendom

8

9

the swedish economy

Sweden’s export-oriented economy has been heavily affected by the fall in global demand instigated by the financial crisis. However, a vigorous business community, strong institu-tions and public finance fundamentals pro-vide the basis for a solid recovery.

As the recession has spread around the world, both con-sumer and industrial demand has decreased significantly. Hit by this fall in demand, the Swedish export sector has been forced to decrease industrial production and staff.

Since the export industries generate more than half of Sweden’s GDP, the global downturn has had a major impact on Sweden’s industrial production. Telecommuni-cations manufacturers, the pharmaceutical industry and producers of investment goods for the energy sector have managed rather well, but steel producers and car manu-facturers have experienced sharply declining demand. Exports bottomed out during the second half of 2009 due to the levelling out of the current global inventory adjustments.

Competitive now and in the future

Looking beyond the current crisis, fundamentals suggest that Sweden will remain an innovative, well-performing economy with high capacity to adjust to changing condi-tions. Sweden’s core industries drive demand for sophisti-cated services and advanced technologies. Historically, the manufacturing industry has posted some of the fastest productivity growth rates in the world.

A strong presence of multinational companies is both the result and the driving force of Sweden’s international business environment. Companies of Swedish origin in-clude AstraZeneca, Ericsson, H&M, Ikea, SCA, Scania, Securitas and Volvo. A quarter of the private sector work-force is employed by foreign-owned companies.

Scope for solid rebound

There are good prospects that Sweden’s economic recovery will be somewhat stronger than the OECD average. Senti-ment indicators continued to climb during late 2009 and both consumer and business confidence levels are among the highest in the world. Because of the weak krona and

a business structure that lies early in the economic cycle, the Swedish industry is well positioned to take advantage of an increase in international demand. Expansive fiscal policies, a strong transmission mechanism that makes interest rate policy powerful and strong balance sheets benefit household consumption.

Unemployment is expected to level off at around 10 per-cent in mid-2010, but the jobless rate is still expected to be significantly higher than before the economic crisis began, reflecting a persistent widening of the output gap.

Meanwhile the number of company bankruptcies has been surprisingly small, a major difference compared to the 1990s and also well below the level during the recession fol-lowing the dotcom crisis. In a number of respects, the econ-omy looks set to emerge from the crisis with limited struc-tural damage, which will strengthen its ability to recover.

Strong public finances

Despite the deep recession and discretionary fiscal policy, public finances have weakened less than expected. Deficits

• Strong public finances.• Innovative, well-performing economy.• Highly international business environment.

key features

Solid recovery in sight

the swedish economy

10

in general government sector net lending are expected to level off at 2.5 percent of GDP 2010 and 2011. Public fi-nances are thus significantly stronger in Sweden than in most other developed countries, which gives fiscal policy larger room for manoeuvre. The budget bill for 2010 in-cludes income tax cuts and supplementary grants to local governments, making fiscal policy as expansive in 2010 as in 2009 (stimulus effect of 1–1.5 percent of GDP).

Expected rises in disposable income

The real disposable incomes of Swedish households are ex-pected to increase during 2009–2010 despite the sluggish economy. The reason is a combination of higher transfer payments, low interest rates and low inflation rates. Growth in private consumption is expected to stay above the zero mark in 2009–2010 despite a rising saving ratio. The mood of households is forecast to improve in 2010, resulting in a lower saving ratio and faster growth in private consump-tion; the bottoming out of the recession in combination with increasing asset prices will have a positive effect on consumer confidence, outweighing the negative effects of increasing unemployment.

Solid platform for growth

Sweden’s fiscal and monetary policies have contributed to maintaining a macroeconomic environment conducive to growth. Government spending limits are set and agreed with Parliament. The independent Riksbank has main-tained price stability with an inflation target set at 2 percent over the economic cycle. A number of structural reforms, deregulations and privatizations have been un-dertaken. The national pension system was reformed already in the mid 1990s. The government debt level is among the lowest in Europe. With an average annual growth rate of 3 percent in the last decade, before the on-set of the global economic crisis, Sweden outperformed the Euro zone by almost 1 percentage point per year.

Sweden’s economy is deeply integrated into the Europe-an economy, which accounts for 70 percent of exports and 80 percent of imports. Major trading partners are Germany, the US, the UK and the neighboring Scandinavi-an countries. Moreover, Swedish companies have substan-tial interests in Central and Eastern Europe and in Asia, notably China, where some 500 Swedish companies are established.

Global competitiveness surveys regularly give Sweden top rankings, with high marks for R&D, innovation, the cor-porate taxation regime, infrastructure and public sector efficiency. The latest Global Competitiveness Report, pub-lished by the World Economic Forum, ranked Sweden as the world’s fourth most competitive country. The annual 4 percent of GDP expenditures on R&D contribute to Sweden’s position as the number one in innovation per-formance among European countries.

of swedish origin

Sweden’s largest companiesSales 2008, SEK billion

Volvo Group, automotive 303.7

Ericsson, mobile systems 208.9

Vattenfall, energy 164.5

Skanska, construction 143.7

Sony Ericsson, mobile communications 123.0

SCA, pulp & paper 110.4

Electrolux, household appliances 104.8

TeliaSonera, telecommunications 103.6

Scania, automotive 93.7

Sandvik, metals technology 92.7

ICA, retail 91.0

Nordea, banking 89.7

Source: Invest in Sweden Agency

11

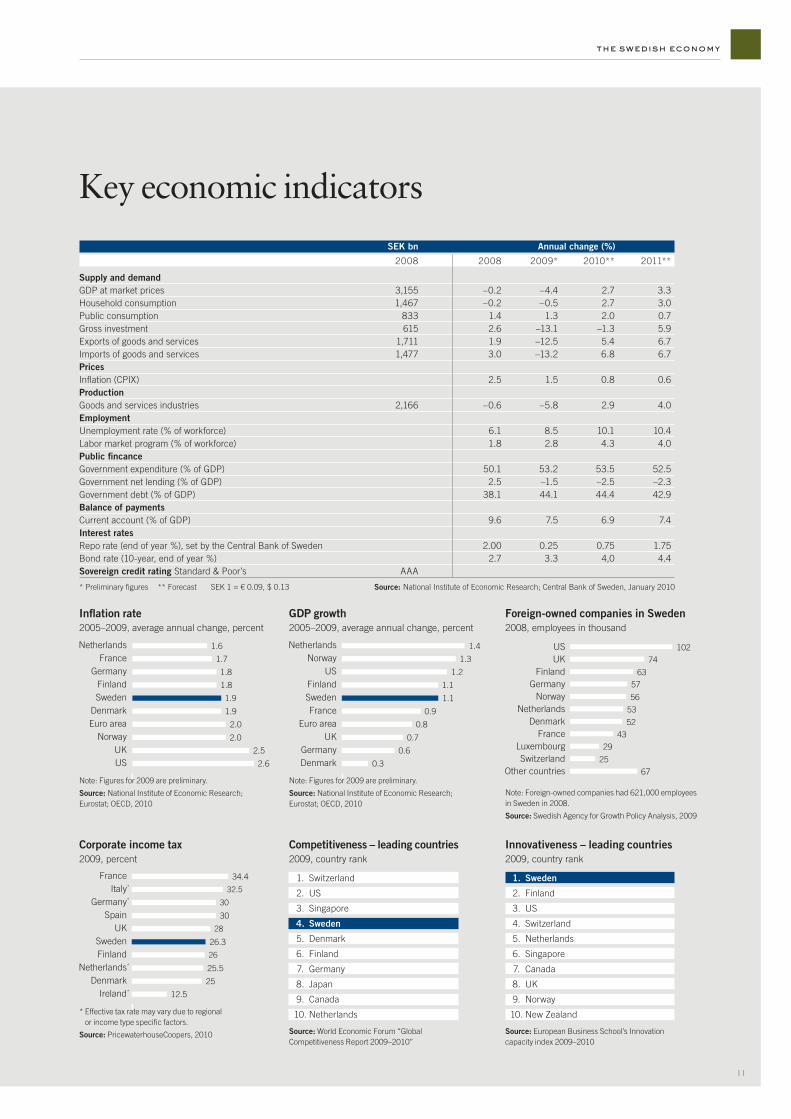

the swedish economy

SEK bn Annual change (%)

2008 2008 2009* 2010** 2011**

Supply and demandGDP at market prices 3,155 –0.2 –4.4 2.7 3.3Household consumption 1,467 –0.2 –0.5 2.7 3.0Public consumption 833 1.4 1.3 2.0 0.7Gross investment 615 2.6 –13.1 –1.3 5.9Exports of goods and services 1,711 1.9 –12.5 5.4 6.7Imports of goods and services 1,477 3.0 –13.2 6.8 6.7PricesInflation (CPIX) 2.5 1.5 0.8 0.6ProductionGoods and services industries 2,166 –0.6 –5.8 2.9 4.0EmploymentUnemployment rate (% of workforce) 6.1 8.5 10.1 10.4Labor market program (% of workforce) 1.8 2.8 4.3 4.0Public fincanceGovernment expenditure (% of GDP) 50.1 53.2 53.5 52.5Government net lending (% of GDP) 2.5 –1.5 –2.5 –2.3Government debt (% of GDP) 38.1 44.1 44.4 42.9Balance of paymentsCurrent account (% of GDP) 9.6 7.5 6.9 7.4Interest ratesRepo rate (end of year %), set by the Central Bank of Sweden 2.00 0.25 0.75 1.75Bond rate (10-year, end of year %) 2.7 3.3 4,0 4.4Sovereign credit rating Standard & Poor’s AAA

* Preliminary figures ** Forecast SEK 1 = € 0.09, $ 0.13 Source: National Institute of Economic Research; Central Bank of Sweden, January 2010

USUK

NorwayEuro areaDenmarkSwedenFinland

GermanyFrance

Netherlands 1.6

1.7

1.8

1.8

1.9

1.9

2.0

2.0

2.5

2.6

Note: Figures for 2009 are preliminary.

Source: National Institute of Economic Research; Eurostat; OECD, 2010

Inflation rate2005–2009, average annual change, percent

DenmarkGermany

UKEuro area

FranceSwedenFinland

USNorway

Netherlands 1.4

1.3

1.2

1.1

1.1

0.9

0.8

0.7

0.6

0.3

Note: Figures for 2009 are preliminary.

Source: National Institute of Economic Research; Eurostat; OECD, 2010

GDP growth 2005–2009, average annual change, percent

Other countriesSwitzerland

LuxembourgFrance

DenmarkNetherlands

NorwayGermany

FinlandUKUS 102

74

63

57

56

53

52

43

29

25

67

Foreign-owned companies in Sweden2008, employees in thousand

Note: Foreign-owned companies had 621,000 employees in Sweden in 2008.

Source: Swedish Agency for Growth Policy Analysis, 2009

Competitiveness – leading countries2009, country rank

1. Switzerland

2. US

3. Singapore

4. Sweden

5. Denmark

6. Finland

7. Germany

8. Japan

9. Canada

10. Netherlands

Source: World Economic Forum “Global Competitiveness Report 2009–2010”

Innovativeness – leading countries2009, country rank

1. Sweden

2. Finland

3. US

4. Switzerland

5. Netherlands

6. Singapore

7. Canada

8. UK

9. Norway

10. New Zealand

Source: European Business School’s Innovation capacity index 2009–2010

Ireland*

DenmarkNetherlands*

FinlandSweden

UKSpain

Germany*

Italy*

France 34.4

32.5

30

30

28

26.3

26

25.5

25

12.5

* Effective tax rate may vary due to regional or income type specific factors.

Source: PricewaterhouseCoopers, 2010

Corporate income tax2009, percent

Key economic indicators

11

fiscal aspects

12

fiscal aspects

13

Fiscal system suited for property investment

Sweden has an uncomplicated taxation struc-ture and competitive corporate taxes. Sweden applies participation exemption, has no thin capitalization rules and allows full deduction for interest in most cases.

Investments normally through holding company

Investments in Swedish property can be made through a limited liability company (“AB”), a non-resident company, or a partnership. Investors normally adopt either a resi-dent or a non-resident holding company structure, for example a holding company owning stock in one or more subsidiary companies. Creating presence through acquir-ing an off the shelf company takes one to two days, estab-lishing a limited liability company takes a little longer.

Mostly indirect transactions

Capital gains tax exemption normally applies for Swedish corporate entities for gains related to the disposal of shares. These rules, in combination with the fact that real estate transfer tax is not levied on indirect transfers of real estate, have resulted in transfers of real estate properties being made mostly through indirect transactions. A potential investor is therefore likely to be offered to acquire shares in a Swed-ish company holding the target property.

Use of special purpose companies

Even if an investor is offered to acquire a property in a direct transaction, the investment would more likely be effected through a Swedish special purpose company. This simplifies holding and increases flexibility in a later disposal. The owner of Swedish property may use an intercompany reor-ganization by partial division to transfer the property to the special purpose company. No transfer tax is levied on a property transfer through partial demerger. Should the property be transferred to the special purpose company through a direct asset transfer, transfer tax would be levied.

Competitive corporate taxes

Sweden’s corporate income tax rate is 26.3 percent, but the effective tax rate is lower due to the possibility of deferring taxation of profit. Computation of taxable income is based on statutory accounts, to which certain adjustments are

made for tax purposes. Interest expenses on externally borrowed funds, as well as property-related expenses, are tax-deductible for resident and non-resident companies and partnerships owning Swedish property.

Tax depreciation and actual latent capital gains tax

Property should be carried at its initial purchase price. An annual depreciation rate for tax purposes of between 2 and 5 percent of the acquisition cost is allowed with re-spect to buildings. Parts of the building may be classified as building equipment and may be depreciated according to the same rules as machinery and equipment.

Depreciation is not allowed for land. The tax basis on a property will remain unchanged in case of an indirect ac-quisition. Thus, no “step-up” in tax basis will be achieved for depreciation or capital gain tax purposes.

An investor should be aware that there is a “latent capital gain” related to the property. The seller most often makes an intra-group transfer of the property into the special purpose vehicle below market value which results in a latent

• Competitive levels of corporate income tax.• Tax exemption on gains related to the disposal of shares.• No transfer tax on sale of real estate holding company.

key features

14

fiscal aspects

tax issue in the special purpose vehicle. There are transac-tion examples where the buyer has been able to negotiate a price reduction for the latent tax, but far from in all trans-actions as a number of investors can manage the latent tax issue in their own structure.

Tax allocation reserve to smooth profit variations

Swedish tax legislation offers a general option to set up a reserve, which can best be described as a “tax allocation reserve”, in addition to an excess depreciation reserve. This option allows companies to carry back losses to off-set previous years’ profits. The reserve is based on a com-pany’s annual taxable income. One-fourth of the taxable income may be appropriated to this reserve. A particular year’s allocation to the reserve can be released at the dis-cretion of the company. The reserve must be released to taxable income at the latest in the sixth year after the year when it was added to the reserve. A taxable interest income is calculated on the total amount of reserves allocated by the beginning of the financial year. For the financial year 2009 the interest rate amounts to 2.08 percent.

Profit transfer possibility for group companies

Each company within a group constitutes a separate taxa-ble entity. The group, as such, is not taxed. However, the group relationship is taken into account by means of “group contributions”. These entail a straight transfer of profits between two group companies; a transfer that is deductible for the transferring company and taxable for the receiving company. An important requirement to qual-ify for group tax relief is that more than 90 percent of the common ownership has existed for the entire fiscal year, or, if the subsidiary was incorporated or acquired as an off the shelf company during that year, since the date when the subsidiary started to carry out business activities.

Dividends often exempt from withholding tax

Dividends distributed by a non-listed resident company to a foreign company are exempt from withholding tax, pro-vided that the recipient would be exempt from taxation had the company been resident in Sweden.

For listed shares, the ownership must be at least 10 per-cent of the voting power and shares must be held for at least twelve consecutive months in order for the dividends to be tax exempt. Note that this requirement does not have to be

fulfilled at the time of the dividends distribution, only before the shares are ultimately disposed of. In cases where with-holding tax will be levied, the ordinary tax rate is 30 per-cent, but it is often reduced by provisions in a double tax treaty. No withholding tax or branch profits tax is appli-cable to permanent establishments operating in Sweden, to which the shares in question pertain.

Tax exemption for capital gains

Non-listed shares are exempt from capital gains taxation. For listed shares, exemption requires at least a 10 percent ownership of the voting rights and a minimum one year own-ership period or, alternatively, that the shares are held for business reasons. Shares held in foreign companies will nor-mally qualify for tax exemption. Capital losses on shares that fulfill the tax exemption requirements are not deductible.

As of January 1, 2010, tax exemption applies also for capital gains on disposal of participations in partnerships, and on disposal of shares held by partnerships respectively.

No thin capitalization rules

There are no thin capitalization rules in Sweden – interest paid is a tax-deductible cost. However, interest paid on a

• Sweden is among Europe’s most favorable jurisdictions for holding

companies, a result of participation exemption rules in combination

with other tax rules and case law.

• Capital gains and dividends from business related shares are exempt

from tax. The definition of business related shares is generous

compared to other countries.

• Applies to shares held in, or dividends received from, companies in

Sweden and abroad.

Qualification for tax exemptionUnlisted shares Always tax exempt – ie. no qualification time or

minimum holding of votes or capital.

Listed shares Must hold at least 10 percent of the voting rights or

must be held in the course of the holder’s business.

Must be held at least one year.

Other competitive tax rules• Low effective corporate tax rate

• Interests fully deductible for tax purposes

• No thin capitalization rules

• No withholding taxes on interests

• No stamp tax or capital duties on share capital

• Extensive double tax treaty network

sweden’s holding company regime

15

fiscal aspects

loan at a rate that is above the market interest rate may be treated as a dividend distribution with regard to the excess portion (“hidden dividend distribution”). The added fact that withholding tax is not levied on interest makes it favo-rable to create structures where the return on investment is distributed as interest. As mentioned above, an investor is often offered to acquire shares in a Swedish company. Spe-cific features of Sweden’s fiscal system make it possible to debt finance a stock acquisition in a real estate company and offset profits from current business against interest on loans related to the share acquisition.

Interest deduction limitation

New anti-debt push down rules are in effect from January 1, 2009. The new rules affect interest costs related to loans raised from affiliated companies in connection with intra-group acquisition of shares. The rules also cover loans from affiliated companies that replace loans raised by third par-ties for such purposes. However, deduction for interest is still allowed if the interest income is ultimately picked up at a tax rate of at least 10 percent or, alternatively, the intra-group acquisition and the intra-group loans are deemed to be ‘commercially justified’.

The rules do not affect loans given by third parties, to the extent that such loans are not met by a receivable on the external lender by an affiliated company (back-to-back loans). Most importantly, the new rules do not affect loans raised for acquisitions made from third parties.

No transfer tax for deals within company structure

The acquisition or disposal of stock in a company holding real estate may be performed without paying transfer taxes. The direct acquisition of legal title to Swedish property is for legal entities subject to 3 percent transfer tax.

Loss carryforward possibilities

Losses may be carried forward without a time limit. Special rules apply when the ownership of a corporation changes.

Tax treatment on direct sale of real estate

Both resident and non-resident companies that own Swedish property are subject to Swedish corporate income tax at the ordinary rate of 26.3 percent, on capital gains realized at the sale of real estate. Capital losses on sale of real estate can be offset only against capital gains on such assets, realized by

the company or another company within the group. Losses on real estate may be carried forward without time limit.

VAT issues to consider

Sales and permanent letting of properties and premises are generally not subject to VAT. However, it is possible to opt for voluntary registration for VAT purposes regarding let-ting of business premises, provided that the business con-ducted on the premises are subject to VAT.

According to a government inquiry from 2009, the above exemption regarding letting of properties could be abolished as from January 1, 2011. Hence, if implemented, the letting of properties, except residential premises, would be subject to 25 percent VAT irrespective of the nature of the business conducted on the premises. This could affect lease agreements that are currently not subject to VAT.

Input VAT on transaction costs could under certain con-ditions be recovered. Assuming that the company bearing the costs conducts business activities subject to VAT and that the costs are related to a transaction subject to VAT or to the VATable business in general, input VAT could be recovered.

Corporate income tax 26.3 percent (as of 2009). The effective tax rate

is lower due to the possibility of deferring taxation of profit.

Property transfer tax Direct acquisition of the legal title to Swedish

property is subject to 3 percent transfer tax (for legal entities). Property

transfer tax is levied on the higher of the acquisition price and the tax

assessment value of the property.

Value added tax (VAT) standard rate 25 percent. Sales and permanent

letting of properties and premises are generally not subject to VAT.

However, it is possible to opt for voluntary registration for VAT purposes

regarding letting of business premises, provided that the business

conducted on the premises are subject to VAT.

Annual property taxResidential property SEK 1,200/apartment or 0.4%*

Commercial office space 1.0%**

Industrial property 0.5%**

Stamp duty on mortgages 2 percent. Payable solely upon the first

registration of a mortgage. Existing mortgages are transferred to the

buyer upon acquisition.

Note: Tax rates applicable in January, 2010.

* SEK 1,200/apartment but not higher than 0.4% of the tax assessment value of the apartment.

** Tax is based on an assessment value set by the Swedish Tax Agency. This value is supposed to correspond to 75 percent of the estimated market value of the property.

relevant swedish taxes

16

fiscal aspects

Green buildings and sustainable cities: Sweden in the lead

Sweden is recognized for its strong environmental awareness and lead-ing position in developing sustaina-ble cities. Property owners, develop-ers, architects and property lenders are now making collective efforts to advance green property construction.

As the result of environmentally conscious policymaking and a comprehensive approach Sweden has become a hot-spot for develop-ment of energy efficient buildings and sustain-able city districts. Sweden is the European leader in energy use from renewable sources, partly thanks to pioneering waste-to-energy developments and extensive build-up of district heating/cooling systems in Swedish municipalities. In 2010, one of Europe’s most energy-efficient buildings, Kungsbrohuset in Stockholm, was completed.

The European Union’s Green Building Pro-gram, set up in 2004 to improve the energy efficiency of non-residential buildings in Europe has been rapidly implemented in Sweden.

The property developer NCC is behind several Green Buildings sold to international

real estate investors. According to Jonny Hell-man, environmental director at NCC Property Development, Swedish property developers have come a long way in holistic property construction. “Stringent environmental poli-cies have long since been in place. Aspects such as waste handling, soil contamination and the use of environmentally certified buil-ding materials are taken very seriously.”

More importantly, the Swedish real estate industry is now making a collective effort to advance environmentally-friendly building practices. During 2009, twelve companies and organizations including NCC, SEB, Vasakro-nan, the Swedish Property Federation and the cities of Stockholm and Malmö co-founded the Sweden Green Building Council (SGBC).

SGBC aims to support the transformation to greener property construction and real estate management by influencing decision-makers, disseminating knowledge and developing various supportive tools. One important task is to champion the development of a limited number of commonly accepted and locally adapted green building standards. In Sweden, the industry has in principle agreed on three standards going forward: the UK and US standards BREEAM and LEED, and the Swedish standard ‘Miljöklassad Byggnad’.

According to Jonny Hellman, the establish-ment of SGBC marks important progress. “Fewer standards and more widespread use of them will increase transparency and highlight the sustainability commitment of the industry to a larger audience, including tenants, lenders and media. I am confident that the increased attention will only serve to speed up sustaina-bility developments within the industry.”

Anna Denell, head of environmental devel-opment at Sweden’s largest property company Vasakronan, says she has been surprised to see how fast environmentally-friendly building has taken a foothold in the industry. “Nowa-days, all new real estate projects are marketed with some degree of green ambition statement attached,” she says. “We have also seen a tremendous change in customer interest – today, customers actively inquire about the energy performance of buildings and are keen to make an environmental contribution through their choice of premises.”

These developments are also affecting existing stock, through upgrading projects and on-going property management. Vasa-kronan recently completed its most compre-hensive renovation project to date, the upgrading of an office property at Vasagatan in central Stockholm. Here, the company has applied a number of features to improve the buildings sustainability performance, includ-ing solar heating, sedum roofing and modern ventilation, climate and lighting systems. Similar upgrades are being made or planned by other property owners.

A company that has shown how much can be achieved in older buildings is Brostaden, a part of Castellum. Brostaden was the first

“ All new Swedish real estate projects are marketed with some degree of green ambition statement attached. Customers are keen to make an environmental contribution through their choice of premises.”

Anna Denell, Manager Development and Environment, Vasakronan

17

fiscal aspects

corporate partner of the EU Green Building program, meeting the requirement that 30 percent of the portfolio qualifies as Green Buildings. For the past ten years, Brostaden has worked to improve energy efficiency in its 90 properties, principally built in the 1970s and 1980s. The energy use in Brostaden’s properties is some 30 percent below the Swedish average for commercial properties. During 2009, the company was invited to present its experiences to the European Commission.

The ambitious plans by Swedish munici-palities support the industry’s activities. The capital of Stockholm is the first city to be awarded the European Green Capital title, in recognition of its efforts to reduce green-

house gas emissions and to let the city grow in a sustainable way. By 2050, Stockholm aims to be wholly independent of fossil fuels.

A new city district, Stockholm Royal Sea-port, is intended to be Stockholm’s next inter-national showcase for sustainable urban construction. The holistic focus relies as much on sustainable mobility (biking, public transport run on renewable fuels, plug-in hybrid cars) as on energy-efficiency in build-ings. On completion, Stockholm Royal Sea-port will be home to some new 10,000 apart-ments and 30,000 work places.

Anna Denell says the development of city districts like Royal Seaport showcases Swed-ish know-how in sustainable urban planning, adding that they also show that city planners

understand that the greatest benefit to the environment is to undertake such projects in the existing city spaces.

“ The establishment of Sweden Green Building Council marks important progress. The indus-try’s sustainability commitment will be highlighted to a larger audience, including tenants, lenders and media.”

Jonny Hellman, Environmental Director, NCC Property Development

Swedish cities have integrated the planning of transport and traffic, water and sewage treatment, waste collection, employment and housing to create increasingly sustainable cities with low carbon footprints. Examples are found in all of Sweden’s largest cities. The city districts of Hammarby Sjöstad in Stockholm and Western Harbor in Malmö, both constructed in former industrial areas, are

some of the world’s foremost sustainable city concepts. One of Sweden’s major urban planning projects, Royal Seaport in the north-eastern part of the inner city, promises to take the next step in sustainable city planning.

www.alvstranden.com www.hammarbysjostad.sewww.malmo.se/sustainablecity www.stockholmroyalseaport.com

Eco-cities: the Swedish model

Hammarby Sjöstad, StockholmStockholm Royal Seaport Western Harbor, MalmöNorra Älvstranden, Göteborg

18

legal aspects

Secure, reliable and cost-efficient

The legal system strikes a good balance be-tween demands for security, reliability, trans-parency and cost-efficiency. It is well-suited for cross-border property investments.

Highly developed system

A well-functioning property legal system must protect the interests of all parties involved – investors, creditors, ten-ants and the public. This means guaranteed predictability, reliability and security. Such a system should also be easy to operate in, with structural mechanisms to ensure low transaction costs. The Swedish property legal system re-sponds well to each of these demands.

The regulation of property

The Swedish Land Code (Jordabalken) regulates all essen-tial aspects of private real estate law, such as property fixtures, formal requirements, mortgages, usufructs (the right to use and enjoy a property), easements, leases and the registration of property rights. All Swedish land is di-vided into property units which are individually identified by a name and a code. A property unit may be demarcated horizontally as well as vertically, thus creating a three- dimensional property unit. An important feature is that ownership is not only restricted to the land. The property unit also consists of accessories such as buildings or other facilities built above or below ground by the owner for permanent use. Furthermore, fixtures that have been in-stalled in buildings by the property owner and that are in-tended for permanent use in the building are considered part of the property unit.

The Swedish Land Register

The boundaries of all property units and their ownership are registered in the Swedish Land Register (Fastighets-registret). The Register contains information regarding the location of the property unit, the title holder, plans and regulations, mortgages, easements, tax assessment values and the purchase price for the last transfer. A buyer is obli-gated to register for title within three months of completing the transfer of property. Failure to register within the stip-ulated time will not, however, make the transfer invalid. Although most legal protection for a buyer derives from the

agreement, the registration in the Register is important for many reasons. For example, title registration is necessary for the buyer when applying for mortgages on the property and gives the buyer – in good faith – priority to title from the day of application for registration. Parties can depend on the information in the Register. If, for example, a registered title holder is proven not to be entitled to ownership of the prop-erty and has been granted new mortgages, the Swedish gov-ernment guarantees compensation for any losses incurred by a creditor who, in good faith, has relied upon the infor-mation in the Register. Therefore, there is no need for title insurance and consequently it does not exist in Sweden.

Cross-border transactions

It is generally considered easy to do business in Sweden. Almost everyone speaks English and agreements and doc-umentation in English are commonly used. Advisors have substantial experience in cross-border transactions. Share

• Ownership includes buildings and other facilities.• Property may be demarcated horizontally and vertically.• No notary procedure required to transfer property.• No need for title insurance.• No restrictions on foreign ownership of property.

key features

19

legal aspects

purchase agreements, real estate sale and purchase agree-ments, and lease agreements are generally less comprehen-sive than Anglo-American agreements, which is estab-lished market practice. Further, there are no restrictions on foreign ownership of property.

The use of special purpose vehicles

The Swedish Land Code stipulates certain formal require-ments for a transfer of a property to be valid. Although direct sales of property has become more common in the aftermath of the global credit crunch, transactions where property is sold indirectly through legal entities still domi-nate the market. There are a number of reasons for this. It reduces transaction costs, as a sale of a company does not incur stamp duty. Sellers are also normally exempt from capital gains tax on the sale of shares in Swedish limited liability companies. In addition, an option to buy or sell shares in a company is legally binding whereas options on property are not. Commonly, the property-owning compa-ny is a newly established special purpose vehicle whose sole purpose is to own and operate the specific property. This ensures that the company’s contingent liabilities are limited.

Sales processes

Most investment property is sold through dedicated real estate consultants, although sales directly by the owner do occur. Negotiations are often made directly with the pro-spective buyer or through its legal adviser. The sale may also be performed through a controlled auction, i.e. the buyer is selected at the seller’s own discretion following a due diligence process in which a number of interested buy-ers have participated. However, controlled auctions have become less common due to reduced market activities.

Due diligence

In Sweden, due diligence work is often coordinated by the legal consultants or directly by the investor. As the liabili-ty of the sellers, especially in controlled auctions, is gener-ally limited to the warranties given in the transfer agree-ment, the due diligence process is important. The process normally involves legal consultants, financial and tax con-sultants as well as technical and environmental consultants. As regards environmental issues, the Swedish Environ-mental Code (Miljöbalken) is primarily based upon the “polluter pays principle”. However, it also contains provi-

sions which may lead to a subsidiary liability for the prop-erty owner, as is the case in many jurisdictions.

Property development projects

The Swedish legal system places no restrictions on the ac-quisition of property development projects and agreements can be entered into during any phase of the project. The investor generally enters into a conditional sale and purchase agreement with a property developer. At the completion date, the developer is to deliver to the investor a fully de-veloped property, including buildings and tenants. Incen-tive schemes are often built into the agreement, whereby the purchase price is a factor of the property’s rental value. The parties can also agree on a model lease agreement and a model construction agreement that shall be used for the development and letting of premises within the property.

Few restrictions on transfer of property

In Sweden there are few restrictions with regard to the transfer of property. However, the Pre-emption Act (Förköps lagen) allows Swedish municipalities pre-emption rights under certain circumstances when a property situated within their boundaries is subject to a purchase. A legisla-tive proposal has been presented proposing that the Pre-emption Act shall cease from May 1, 2010.

Creating and pledging mortgage security

The holder of the legal title to a property is entitled to take out a mortgage (Inteckning) in the property. A mortgage of any amount can be made, even an amount much higher than the actual market value of the property, but as there is a two percent stamp duty on the face value of the mort-gage, the owner and its lender generally limit the mort gages to the lower end of the amount of the loan and the market value of the property. The mortgages are given chronological priority in the Swedish Land Register and information de-scribing the amount of each mortgage, which is a fixed sum, is also shown in the Register. A mortgage can be made either in Swedish kronor or in euro. Each mortgage is evidenced by a mortgage certificate (Pantbrev) which can either be in physical form or in electronic form. In order to create a val-id mortgage pledge in a property, the owner of the property must enter into a pledge agreement whereby the mortgage certificates are pledged as security for a claim from a credi-tor and the mortgage certificates must be delivered to such

20

legal aspects

creditor. A mortgage certificate is perpetual and can be used and reused without incurring any stamp duty or transaction costs other than the initial stamp duty of two percent when applying for the mortgage.

Mortgage financing provides strong security

The security interest of a creditor holding valid security in a property cannot be extinguished upon a sale of such property. In the case of a bankruptcy proceeding, the cred-itor has priority and is entitled to an amount up to the face value of the mortgage certificates pledged to the creditor, plus an additional 15 percent out of the sales proceeds from the executive sale of the property.

Financial assistance restrictions

There are no thin capitalization rules in Sweden but there are legal restrictions as regards financial assistance. A Swed-ish limited liability company may not lend funds or provide security to its shareholders or sister companies. Nor may it give upstream or cross-stream guarantees. There are certain exemptions available, inter alia if it is made to shareholders or sister companies within the same group (Koncern). An-other important restriction in relation to acquisitions is the

so called loan prohibition (Förvärvslåneförbudet). A Swed-ish limited liability company may not lend funds, provide security or give guarantees to be used for the actual acquisi-tion of the company itself. Given the common use of special purpose vehicles, this often means the target property can-not be used as security for the acquisition financing of the special purpose vehicle. The drawback of this restriction is often mitigated by the lender trying to create a ring fenced security, especially in special purpose vehicle structures. Furthermore, it is still possible for the special purpose vehi-cle to pledge mortgages in the property for its own business financing or refinancing.

Flexible security structures

In an attempt to keep transaction costs as low as possible (but also due to financial assistance problems) lenders have, for the last couple of years, accepted alternative security structures instead of maximizing the mortgage security. Such alternatives often include combinations whereby already existing mortgage certificates are pledged (but no new applications for mortgages are made) together with a ring fenced security structure, comprising pledges over the shares, bank accounts in and receivables of the property-

21

legal aspects

owning entity, as well as sometimes so-called springing mortgages. The frequent use of special purpose vehicle structures facilitates such ring fenced security structures.

Publicly owned property may be let as a site-leasehold

A property unit owned by a municipality or another public entity may be let as a site-leasehold (Tomträtt). A site-leasehold is very similar to ownership. The site-leaseholder may transfer, mortgage, let and, in all material respects, use the site-leasehold in the same way as the owner of a property unit may use its property. In return for the site-leasehold, the site-leaseholder pays a rent, based on the value of the property. The rent is reviewed every ten years, unless a longer period is agreed upon. In the absence of a mutual agreement on the new rent under revision either party can submit the matter to the court for final decision. The rent is determined by the market value of the property (taking into account the current use of the property) at the time for review. The site-leasehold may be terminated by the property owner only at the end of certain periods of time. The periods are at least 20 years. The site-leaseholder is normally entitled to compensation for the value of build-ings and other accessories to the site-leasehold if it is termi-nated. Deviations from the rules that normally apply to site-leaseholds may, in some cases, be made in the agree-ment, which should therefore be reviewed prior to purchase of a site-leasehold.

Commercial lease regulations tied to the Land Code

Generally, commercial leases are entered into for a term of three to five years, with rents linked to changes in the Swedish CPI (Consumer Price Index). Further, the Swedish Land Code stipulates mandatory regulations in favor of the tenant. Most parties in Sweden therefore use standard agreements for commercial leases. A normal agreement consists of a four-page document and an appendix with special provisions. Since parties are generally familiar with these agreements, the result is often shorter times for negotiating or analyzing lease agreements and thus lower legal fees. Rent levels must be set at a reasonable rental market value. If the parties cannot agree on the rent level, the regional rental tribunal may determine what consti-tutes a reasonable rental market value for the premises in question, by comparing similar premises at similar loca-tions. However, the tribunal may only determine the mar-

ket rent in connection with the extension of a lease. As re-gards the initial lease period, it is up to the landlord and the tenant to agree on the rent.

Energy performance of buildings

Sweden has implemented the EC directive 2002/91/EC on the energy performance of buildings. The act has been in force since 2006 and essentially means that buildings need to be declared for their energy performance. The declara-tion needs to be carried out by certified experts.

Regulated rental market for residential leases

Residential leases are generally entered into for an indefinite term with a three-month period of notice. With regard to residential leases the Swedish Land Code stipulates man-datory regulations in favor of the tenant. As a rule, the rents for residential leases shall not substantially exceed the rents set by the municipality housing companies. Thus, there is no free rental market for residential leases in Sweden. Standard form agreements are often used and the typical agreement is a two-page document.

Payment terms Rents for premises are generally quoted in SEK,

Swedish krona, as a total sum for the agreed space. Rental statistics

and comparisons are quoted in SEK per square meter and year. The

standard agreement anticipates advance quarterly or monthly rental

payments. Rent adjustments during the term of the lease are based

on changes in the Swedish CPI (Consumer Price Index).

Items included in the rent Office space is normally provided fitted to

the needs of the tenant (within reason). Retail and industrial spaces

are often provided without fittings. In general, rent includes heating

and water but not electricity. Further, the rent includes cleaning of

common areas and snow removal. Property tax and VAT are charged

on top of the rent.

Day-to-day management and maintenance The landlord bears the

costs of day-to-day management and exterior maintenance.

Key money and deposits Key money is rarely charged in the office

sector, but is common in the retail sector. A security deposit or bank

guarantee equivalent is common.

Improvements Construction work in the rented unit may only be un-

dertaken subject to the express approval of the landlord. Such work is

generally executed at the expense of the tenant and includes an obli-

gation to rebuild to the original state when the agreement expires un-

less otherwise agreed.

guide to commercial rents

22

cities & regions for investment

Innovative and industrious regions

Sweden’s metropolitan areas and regional anchor cities have all been the target for cross-border property investment. The city-regions are well equipped for stable long-term growth; four of Europe’s ten most innovative regions are Swedish.

Solid foundation in innovative industry base

Sweden is home to a number of successful innovative envi-ronments and industry clusters, including aerospace, auto-motive, energy, engineering, financial services, informa-tion technology and life sciences. Importantly, industry activity is complemented by strong applied and basic re-search activity at universities. A survey by the European Commission, measuring innovation performance in 203 European regions, placed four Swedish regions among the top ten.

Good prerequisites for growth

The specific characteristics of Sweden’s industrial and scientific asset base means Sweden is a particularly good setting for multi-disciplinary innovation – few places of a similar size offer such breadth of research expertise and know-how in complementary knowledge fields. There is strong public support to reinforce the most attractive in-novative environments, to promote company growth and R&D, but also to stimulate inflow of investments, quali-fied staff and new companies.

International presence throughout the country

The majority of cross-border property investments have been made in Stockholm, Göteborg and Malmö, the three largest cities and nodes of the suburban regions Mälardalen, West Sweden and Skåne/Öresund Region. Stockholm is Europe’s 10th largest office market, while Göteborg is placed 31st and Malmö 44th.

However, international investments have been recorded all over the country. These have predominantly been made in one of Sweden’s anchor cities – a region’s administrative capital, the largest city, a university city or, normally, a combination of the three. From north to south, they include Luleå, Umeå, Sundsvall, Uppsala, Karlstad, Västerås,

Örebro, Norrköping, Linköping, Jönköping, Växjö, Karls-krona, Kristianstad and Helsingborg.

Stockholm – European Green Capital 2010

Stockholm has been among Europe’s most important in-vestment markets for real estate for a number of years, and has remained so in spite of the financial crisis. The city was Europe’s sixth largest investment market in 2009.

Stockholm, labelled the Capital of Scandinavia, is regarded as Northern Europe’s commercial and financial hub. It is the preferred location for multinational compa-nies and financial institutions that set up regional head-quarters in Scandinavia or the Baltic Sea region. Stockholm drives economic growth in the Mälardalen region, which encompasses cities like Eskilstuna, Uppsala, Västerås and Örebro.

Stockholm has a stronger focus on private services than any other Swedish region. Industrial activity is concentrated in the information and communication technologies (ICT), financial services and life science sectors. Stockholm hosts

• Stockholm is Europe’s 10th largest office market.• Population growth in virtually all major cities.• International ownership in most of Sweden’s major cities.

key features

23

cities & regions for investment

one of the world’s most prominent ICT clusters, one of Europe’s largest life science clusters and the largest finan-cial center in northern Europe. Karolinska Institutet, the renowned biomedical university is located here. Stockholm is recognized as an environmental leader – the city was named European Green Capital 2010 and aims to be whol-ly independent on fossil fuels by 2050.

By 2030, the Stockholm region is estimated to have some 4 million inhabitants. In order to meet this growth, some € 30 billion ($ 40 billion) is being invested in strategic city development and infrastructure projects in the region. These projects cover everything from road, railway, harbor and airport expansion to investments in office, retail, resi-dential and hotel property.

Göteborg – the Gateway to Scandinavia

Göteborg, Sweden’s second largest city, is renowned for its strong sense of community and pragmatic approach to collaboration between public and private entities. The city has the largest port in northern Europe and is the focal point for much of Scandinavia’s industrial capacity.

The city’s industrial base is in advanced manufacturing, logistics and high-tech R&D, with headquarters or head-quarters functions of companies such as Volvo Group, Volvo Cars, SKF, Ericsson, AstraZeneca, Stena and ESAB, among others. Some 50 percent of Scandinavia’s total in-dustrial capacity is located within a 300 kilometer radius of the city.

Göteborg also has significant activity in international trade and freight and is Scandinavia’s leading export region. There is suitable infrastructure for transport via road, rail and sea – the Göteborg Region has on numerous occasions been ranked the best Swedish location for logistics centers.

The Göteborg Region hosts over 2,000 foreign-owned companies, of which more than two-thirds have placed their headquarters in the region. The region is knowledge- intensive with more than 60,000 students and well-known higher education institutions including the Chalmers Uni-versity of Technology and Göteborg University.

The strategy for sustainable growth of the Göteborg Region is based on a comprehensive extension of regional infrastructrure and public transport as well as large-scale development of the Göteborg city center, creating homes for 30,000 new inhabitants and commercial space for 40,000 new jobs.

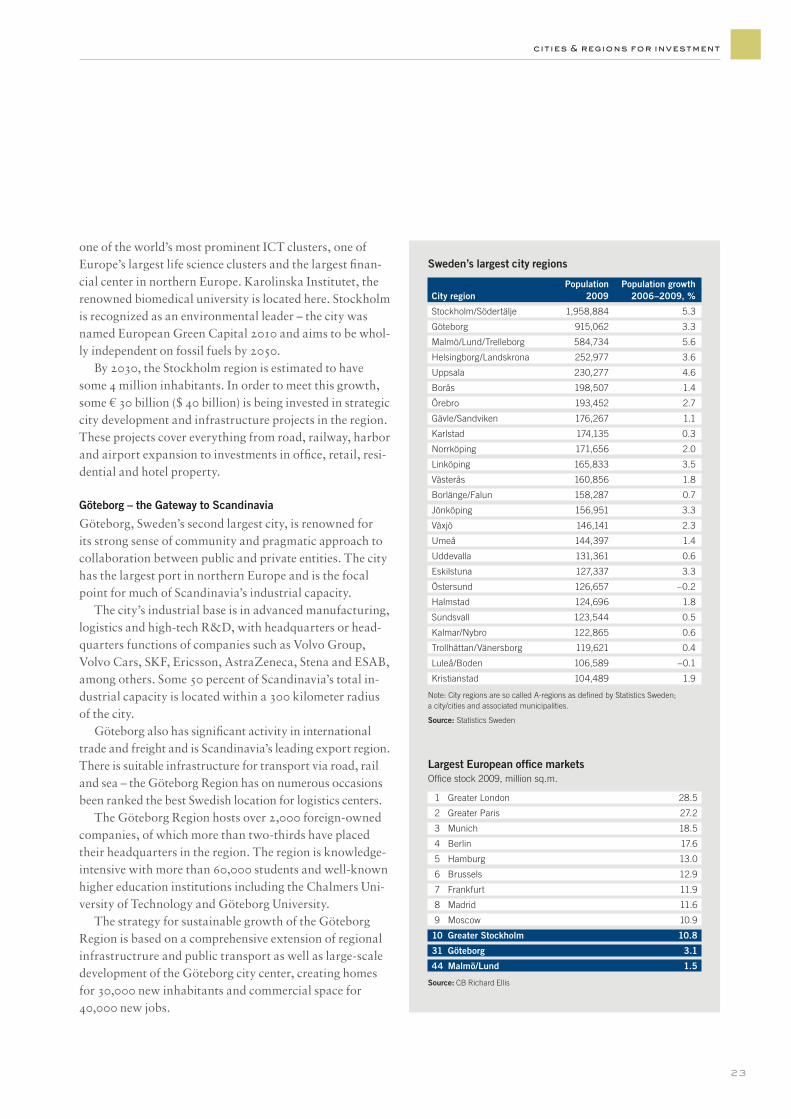

Sweden’s largest city regions

Population Population growth City region 2009 2006–2009, %

Stockholm/Södertälje 1,958,884 5.3

Göteborg 915,062 3.3

Malmö/Lund/Trelleborg 584,734 5.6

Helsingborg/Landskrona 252,977 3.6

Uppsala 230,277 4.6

Borås 198,507 1.4

Örebro 193,452 2.7

Gävle/Sandviken 176,267 1.1

Karlstad 174,135 0.3

Norrköping 171,656 2.0

Linköping 165,833 3.5

Västerås 160,856 1.8

Borlänge/Falun 158,287 0.7

Jönköping 156,951 3.3

Växjö 146,141 2.3

Umeå 144,397 1.4

Uddevalla 131,361 0.6

Eskilstuna 127,337 3.3

Östersund 126,657 –0.2

Halmstad 124,696 1.8

Sundsvall 123,544 0.5

Kalmar/Nybro 122,865 0.6

Trollhättan/Vänersborg 119,621 0.4

Luleå/Boden 106,589 –0.1

Kristianstad 104,489 1.9

Note: City regions are so called A-regions as defined by Statistics Sweden; a city/cities and associated municipalities.

Source: Statistics Sweden

Largest European office marketsOffice stock 2009, million sq.m.

1 Greater London 28.5

2 Greater Paris 27.2

3 Munich 18.5

4 Berlin 17.6

5 Hamburg 13.0

6 Brussels 12.9

7 Frankfurt 11.9

8 Madrid 11.6

9 Moscow 10.9

10 Greater Stockholm 10.8

31 Göteborg 3.1

44 Malmö/Lund 1.5

Source: CB Richard Ellis

cities & regions for investment

0

2

4

6

8

10

12B-locations in suburbs

A-locations in suburbs

CBD

0908060402009896949290

Office yields Stockholm1990–2009, percent

CBD A-locations in suburbs B-locations in suburbs

Source: Newsec

0

2

4

6

8

10

12B-locations in suburbs

A-locations in suburbs

CBD

0908060402009896949290

Office yields Göteborg1990–2009, percent

CBD A-locations in suburbs B-locations in suburbs

Source: Newsec

0

2

4

6

8

10

12A-locations in suburbs

Rest of inner city

CBD, Western Harbour

0908060402009896949290

Office yields Malmö1990–2009, percent

City, Western Harbor Rest of inner city A-locations in suburbs

Source: Newsec

24

E18 E4

E4

E20

AdjacentSuburbs

Solna/Sundbyberg

Kista

Rest of Inner City

CBD

Bromma

Frösunda

Alvik

Nacka

University

Marievik

Globen

Solna Centrum

Nacka Strand

KTH

SundbybergsCentrum

25 km25 km25 km25 km25 km25 km25 km25 km25 km

E22

CBD

Old Town

Bulltofta

Malmö Stadium

Rest of

Rosen-gård

Limhamn

Möllevången

Harbor

Hyllie

Inre Ringvägen

Inner City

WesternHarbor

Eastern Göteborg

20 km

Rest of Inner City

Mölndal

Norra Älvstranden

Hisingen

WesternGöteborg

E20

Gårda

LindholmenScience Park

Majorna

Kålltorp

Annedal

Chalmers University of Technology

CBD

Gullbergsvass

Stockholm Göteborg Malmö

Office stock, million square meters 10.8

Population (greater Stockholm) 1,958,884

Population growth, 2006–2009 (%) 5.3

Office stock, million square meters 3.1

Population (greater Göteborg) 915,062

Population growth, 2006–2009 (%) 3.3

Office stock, million square meters 1.5

Population (greater Malmö) 584,734

Population growth, 2006–2009 (%) 5.6

Malmö – At the heart of the Öresund Region

The Öresund Region is one of Europe’s most dynamic re-gions, with a strong industrial and scientific asset base and focus on growth and innovation. Over 3.6 million inhabit-ants live on the Swedish and Danish sides of the Öresund Strait, in an increasingly integrated region served by two in-ternational airports. The largest, Copenhagen/Kastrup, is accessed from Sweden in 20 minutes via the Öresund Bridge.