rea group annual report 2009

TRANSCRIPT

realestate.com.au Ltd

REA

Gro

up

An

nu

al Rep

ort 2009

ORGANICALLY GR WNREA GROUP ANNUAL REPORT 2009

Des

igne

d an

d pr

oduc

ed b

y H

aym

an D

esig

n

NOTES

Cert no. XXX-XXX-XXXX

Chairman’s letter 1CEO & MD’s letter 2Highlights 5Revenue & Operations 6

Australian Business Summary 9Overseas Business Summary 10REA People 15Financial Statements 16Corporate Information 80

CONTENTS

www.rea-group.com 1

CHAIRMAN’S LETTER

REA GROUP DELIVERS STRONG ORGANIC GROWTH IN FY09

Our strong balance sheet and operating cash fl ow have enabled the Company to pay shareholders a dividend of 10 cents per share on 16 October 2009 out of retained profi ts, as previously announced.

The dividend will be combined with a Dividend Reinvestment Plan (DRP), giving you the option to reinvest the dividend in return for new shares. These new REA shares will be issued at a 2.5% discount to the relevant volume weighted average market price to provide additional value to those shareholders who elect to participate.

In his fi rst year as REA Group CEO, Greg Ellis has built an experienced and world class executive team with a clear strategy for business growth and innovation which is fully supported by the Board.

On behalf of the Board I would like to thank Greg and the executive team at REA Group for their dedication and passion during the past year. The results of their exceptional work are detailed in this Annual Report.

Finally, I thank you for your ongoing support and commitment to the success of REA Group. We look forward to building on this success in 2010.

Richard J FreudensteinChairman

Dear shareholders,

This year has seen REA Group continue its great tradition of delivering strong fi nancial and operating results. Despite being a tumultuous economic period across the globe, REA Group has achieved very good growth in revenue, EBITDA and operating cash fl ow.

With challenges come opportunities and REA Group has seized upon the economic environment to increase its leadership in Australia and in key markets overseas where online property advertising is capturing a growing share of real estate marketing spend.

In 2009, core priorities for the Board and executive team were maintaining market leadership and growing and protecting shareholder value.

In line with this prudent approach to REA Group’s operations and growth, we have taken steps to exit unprofi table and non-core businesses. While the associated impairment costs signifi cantly impacted 2009 NPAT, these are one-off costs which will help drive long-term shareholder value by focusing the Company on core businesses.

On behalf of the Board of Directors, Executive and the REA Group team, I am proud to share with you our key achievements:

Revenue from continuing operations up 26% to $167.8 million•

EBITDA increased by 34% to $62.3 million•

Cash from operations increased by 100% to $31.8 million.•

2 REA Group Annual Report 2009

CEO & MANAGING DIRECTOR’S LETTER

Dear shareholders,

I am pleased to share with you the fi rst Annual Report during my tenure as CEO and Managing Director of REA Group.

Since joining the company in September 2008 I have undertaken a strategic review of the business and made extensive structural changes to help us realise our goal of profi table growth in markets where our position is strong and the market size and market dynamics are attractive.

This has resulted in greater focus on organic growth in our core Australian market and the highly attractive Italian market. It has also meant taking decisive action to divest under performing businesses in Australia and overseas.

Our 2009 results have seen very strong growth in Australia and Italy despite a turbulent economy and property industry. Today an estimated 95% of Australian real estate agents subscribe to our sites and our Italian business, casa.it, now outranks realestate.com.au in both the total number of real estate agent subscribers and the number of active listings.

The continued and increasing patronage of our sites by real estate agents and advertisers, as well as the millions of consumers around the world who visit our sites every month to fulfi ll their property needs, is testimony to the value we deliver.

While the online environment is a highly competitive one, REA Group has a clear innovation and growth strategy to ensure we continue to raise the bar and deliver valuable services to our target markets.

Our business is now focused on the future of online property advertising and I am confi dent we have the right team and the right strategy in place to continue our market leadership and growth.

I would like to thank our customers for the opportunity to work to enhance the value of both our businesses and our users for their continued support of our sites globally.

Finally my sincere thanks to the entire team at REA Group for their hard work, pride and enthusiasm for what we can achieve in the years ahead.

Greg EllisCEO & Managing Director

STRONG STRUCTURESUPPORTSSTRONG GROWTH

www.rea-group.com 3

4 REA Group Annual Report 2009

www.rea-group.com 5

Revenue from continuing operations up 26% to $167.8 million.•

EBITDA increased by 34% to $62.3 million.•

Cash from operations increased by 100% to $31.8 million.•

Company’s fi rst dividend of 10 cents per share to be paid on • 16 October 2009.

Commercial property business revenue in Australia grew • by 58% to $15.0 million.

Traffi c (unique browsers) to realestate.com.au increased • to 4.5 million (Nielsen) – more than double the traffi c of its nearest competitor.

Approximately 95% of Australian real estate agents now • subscribe to REA Group sites.

Italian site casa.it now has over 8,000 paying agents and • another 2,600 on trial subscriptions.

Businesses in the United Kingdom and United Arab Emirates were • divested during FY09 in order to focus on the Australian market and international markets where our market position is strong and the market size and market dynamics are attractive.

REA GROUP DEMONSTRATES THE POWER OF ORGANIC GROWTH IN CORE MARKETS.

HIGHLIGHTS

$167.8

REVENUE ($millions)

FY 05 06 07 08 09

33.4

54.9

89.4

133.6

$62.3

6.5

FY 05 06 07 08 09

EBITDA ($millions)

16

30.3

46.6

OPERATING CASH FLOW ($millions)

FY 05 06 07 08 09

$31.8

6.8

10.8

21.1

15.9

6 REA Group Annual Report 2009

REVENUE & OPERATIONS

FY2005 FY2006 FY2007 FY2008 FY2009 Growth

Revenues from Services * 33,416 54,921 89,402 133,562 167,795 26%

Operating Expenses (26,951) (38,910) (59,081) (86,929) (105,495) 21%

EBITDA 6,465 16,011 30,321 46,633 62,300 34%

EBITDA Margin 19% 29% 34% 35% 37%

Depreciation and Amortisation (1,051) (1,766) (4,230) (6,404) (7,348) 15%

Impairment of goodwill – – – – (6,141)

Impairment of intangibles – – – – (1,854)

EBIT 5,414 14,245 26,091 40,229 46,957 17%

Net Interest (Expense) / Income 206 (403) 461 (21) 344

Earnings Before Tax 5,620 13,842 26,552 40,208 47,301 18%

Income Tax (Expense) 2,472 (4,039) (7,535) (14,720) (18,598) 26%

Loss of discontinuing operations – (3,162) (8,028) (9,725) (63,341) 551%

Minority Interest (net of taxes) – 1,581 4,076 6,581 35,584 441%

Profi t attributed to members of parent 8,092 8,222 15,065 22,344 946 (96)%

Employees (FTE) excluding UK 159 238 409 537 526 (2)%

Employees (FTE) in UK – 56 70 130 79 (39)%

Subscribing Paying Agents excluding UK 6,414 7,806 12,961 16,341 18,879 16%

Subscribing Paying Agents in UK – 2,907 4,050 6,137 5,519 (10)%

* Excludes Interest Income

FIVE YEAR OVERVIEWFINANCIAL COMPARATIVE DATA IN $’000

WHO IS REA GROUP?REA Group owns and operates the leading real estate and commercial property advertising sites in Australia, including its fl agship site realestate.com.au, as well as international real estate property advertising sites such as the market-leading Italian site, casa.it.

Headquartered in Melbourne, Australia, REA Group aims to deliver effective online advertising solutions through its stable of sites to help real estate agents sell or rent properties and win new listings.

REA Group’s Australian businesses represent 90% of total Company revenue. These businesses continue to experience strong growth, despite economic and property sector volatility.

REA Group’s Italian business, casa.it, offers substantial growth potential as the Italian market for internet advertising is still at a relatively early stage.

REA Group’s business goal is profi table growth in markets where its position is strong and the market size and market dynamics are attractive. Continuous innovation and the delivery of a great user experience – for real estate agents, commercial clients, and house hunters alike – are the keys to achieving this goal.

www.rea-group.com 7

8 REA Group Annual Report 2009

www.rea-group.com 9

REA Group’s core business is in Australia where it operates the leading residential and commercial property advertising sites.

realestate.com.au continues its leadership in the Australian market with traffi c (unique browsers) to realestate.com.au increasing to 4.7 million (Nielsen) in June 2009, up from 4.1 million unique browsers in June 2008. The gap between realestate.com.au and its nearest competitor domain.com.au (#2 residential site in Australia) widened to 2.4 million, positioning realestate.com.au with more than twice the volume of traffi c to domain.com.au.

During FY09 realestate.com.au launched a mobile version of the site. By June 2009 the mobile version had over 163,000 unique browsers (Omniture), a 23% increase in traffi c since going live in April 2009. realestate.com.au also introduced new research features for consumers including comprehensive sale and auction data and online selling guides.

Developer advertising (home and land packages) on realestate.com.au increased by 43% or $6.0 million in 2009, due primarily to the popular First Home Owners Grant.

In recognition of the diffi cult economic times and subsequent impact on real estate agents REA Group froze residential subscriptions for 12 months from February 2009. This represented a signifi cant investment by the Company to assist the industry during diffi cult economic times.

realcommercial.com.au is Australia’s leading commercial property advertising site, with just under 300,000 unique browsers (Nielsen) and over 300,000 property listings in June 2009. Revenue grew by a record 58% to $15.0 million in FY09.

realholidays.com.au is REA Group’s holiday rental site which welcomed over 175,000 unique browsers (Nielsen) in June 2009. Aimed at the domestic short term holiday market, realholidays.com.au leverages the high volume of traffi c that passes through the realestate.com.au and realcommercial.com.au sites.

Media advertisingIncreased usage of our sites by consumers delivers greater reach and an enhanced value proposition for advertisers such as media companies or developers. In the 2009 fi nancial year, total media advertising revenue in Australia grew 16% to $36.2 million.

This year also saw the launch of reagroupmedia.com.au, a media centre site which has proven to be an insightful and valuable tool for those working in the media buying industry.

AUSTRALIAN BUSINESS SUMMARY

FROM STRENGTH TO STRENGTH

PAYING AGENTS IN AUSTRALIA

1m

2m

3m

4m

5m

6m

JUN 04 JUN 05 JUN 06 JUN 07 JUN 08 JUN 09

5.23m

JUN 04 JUN 05 JUN 06 JUN 07 JUN 08 JUN 09

$

200

400

600

800

1,000

1,200

$1,040

JUN 04 JUN 05 JUN 06 JUN 07 JUN 08 JUN 094,000

6,000

8,000

10,000

9,000

7,000

5,000

9,332

JUN 04 JUN 05 JUN 06 JUN 07 JUN 08 JUN 09

000s

300

400

500

600572,000

UNIQUE BROWSERS IN AUSTRALIA

AVERAGE MONTHLY REVENUE PER AGENT FOR AUSTRALIA LISTINGS IN AUSTRALIA

10 REA Group Annual Report 2009

OVERSEAS BUSINESS SUMMARY

ITALY RECORD RESULTSIN 2009

With a potential market of around 32,000 real estate agents in Italy, casa.it has succeeded in signing up 25% of agents to date.

In light of its focus on high potential international markets, casa.it has become the centerpiece of REA Group’s profi table growth strategy overseas and will benefi t from signifi cant enhancements including:

improved consumer experience and site features•

improved product offers for customers such as two classes of • subscriptions (standard and platinum) and three price points (small, regular, and unlimited listings); plus

automated monthly billing for customers.•

In July 2009, casa.it signed a strategic partnership with the Italian Real Estate Federation (FIAIP).

FIAIP is the leading real estate federation in Italy with more than 12,000 associated members. The partnership between casa.it and FIAIP has been developed to increase internet usage and awareness among associated real estate agents. The partnership will include training for real estate agents conducted by casa.it, workshops, and casa.it branding on all internet and web-marketing material associated with FIAIP.

casa.it set a new REA Group record with its 2009 growth results. It continued to lead the market in number of unique browsers and increased paying agents by 46% to 8,053, with an additional 2,682 agents on trial subscriptions. Historically, agents convert to paid subscriptions after a three month trial.

UNIQUE BROWSERS (millions)

JUN JUN JUN 07 08 09

JUN JUN JUN 07 08 09

1.4

0.80.7

JUN JUN JUN 07 08 09

8,053

3,511

5,514

PAYING AGENTS (number)

530

213

299

ACTIVE LISTINGS (000’s)

www.rea-group.com 11

12 REA Group Annual Report 2009

OVERSEAS BUSINESS SUMMARY (CONTINUED)

LUXEMBOURG AND OTHER COUNTRIES – CONTINUING TO BUILD SUCCESS

The Luxembourg business is profi table, with EBITDA margin increasing from 30% to 33% in FY09. REA Group site athome.lu continues to be the market leader in Luxembourg.

Elsewhere across Europe and Australasia REA Group continues to invest for growth.

From its base in Luxembourg, the atHome team also operates atHomeLorraine.fr and atHomeAlsace.fr in France, both strong players in their regions, and atHome.de in the Moselle region of Germany.

In Hong Kong, REA Group publishes the squarefoot.com.hk and Inside Discovery Bay magazines, leaders in their market niche, as well as a residential website targeting English speaking users which continues to attract increasing numbers of customers and consumers.

In New Zealand, REA Group operates the largest commercial property advertising site, realcommercial.co.nz.

REVIEW OF INTERNATIONAL PORTFOLIOFollowing a strategic review of its international portfolio of businesses, REA Group has divested a number of under performing businesses in order to focus on its market-leading businesses in Australia and Italy.

In the UK, three print publications were closed in May 2009, and in August 2009 REA Group successfully completed a share sale of the UK online business it jointly owned with News International Ltd.

In July 2009 REA Group entered an agreement to sell its 51% stake in its UAE business, propertyfi nder.ae. The sale was approved by local UAE regulatory authorities in September 2009.

Other smaller businesses that were sold or exited during this period are the Altowin business and Belgium presence, the residential business in New Zealand, and the Clarke Computers business (Trust accounting).

NURTURING OUR OTHEROVERSEAS BUSINESSES

www.rea-group.com 13

14 REA Group Annual Report 2009

www.rea-group.com 15

REA TEAM – RECOGNISED INDUSTRY EXPERTSREA staff are highly sought after as conference speakers and lecturers across Australia. In the past year, members of the team have spoken at many events including:

IT and Online MediaDubai Cityscape Conference presentation ‘Online Advertising – • The Power of the Internet to Reach Global Buyers’ (Scott Holmes, Group Display Advertising Manager)

Australian Direct Marketing Association • Search Marketing Seminar(Max Sim, Senior SEO Advisor)

Small Business Conference on “Use of the internet to Promote • your Business”(Henry Ruiz, GM Consumer Marketing)

Swinburne University Masters of IT, ‘Careers in IT’• (Daniel Oertli, CIO)

Swinburne University Masters of IT, hosted site visit to REA Group• (Andy Kelk, Lead Software Developer)

Real EstateCentury 21 Conference; and•

Adelaide Advertiser Real Estate Seminar• (Greg Ellis, CEO)

Laing and Simmons National Conference;•

L.J.Hooker Admirals National Conference;•

Northern England Agents Real Estate Seminar UK;•

Century 21 Account Managers Conference; and•

Young Agents Association NSW Seminar• (Bill Russell, Manager Industry Development)

Investor and FinanceCFO Magazine Master Class on Procurement• (Chris Dau, Financial Controller)

Macquarie Bank Investor Conference;•

Lodge Partners Growth Company conference; and•

ABN Morgan Conference• (Georg Chmiel, CFO)

Melbourne Business School, Executive MBA Class • on Mergers and Acquisitions(Andy Sheats, GM Strategy & Corporate Development

VOLUNTEERING AND CHARITABLE DONATIONSREA Group supports the involvement of staff in community work and offers all staff one volunteer day per year.

REA Group staff actively support the REACH Foundation, with 30 staff around Australia taking part in the REACH Heroes days and Leadership days. These days are part of REACH Foundation’s secondary school program which aims to make a positive difference in the lives of young people in our community. Team members have also provided professional assistance to REACH via event management, public relations, and program development support.

In 2009 REA Group staff also raised funds for the Cancer Council and the Red Cross, with donations matched dollar for dollar by the Company.

REA PEOPLE

GREAT RESULTS DON’T HAPPEN ALL BY THEMSELVES – IT TAKES A TEAM OF GREAT PEOPLE!

REA Group actively recruits smart, innovative and high performing people who have the passion to build and support its market leading products and sites.

16 REA Group Annual Report 2009

CONTENTS

Directors’ report 17

Auditor’s Independence Declaration 29

Corporate governance statement 30

Financial report

Income statements 36

Balance sheets 37

Statements of changes in equity 38

Cash fl ow statements 39

Notes to the fi nancial statements 40

Directors’ declaration 76

Independent auditor’s report 77

Shareholder information 79

Corporate information 80

FINANCIAL STATEMENTSFor the year ended 30 June 2009

www.rea-group.com 17

DIRECTORS’ REPORT

Your directors present their report on the consolidated entity (referred to hereafter as the Group) consisting of REA Group Limited and the entities it controlled at the end of, or during, the year ended 30 June 2009.

DirectorsThe following persons were directors of REA Group Limited during the fi nancial year and up to the date of this report:

Mr Richard J FreudensteinMr Roger AmosMs Kathleen ConlonMr Greg Ellis (appointed 23 September 2008)Mr John D McGrathMr Alasdair MacLeodMr Jeremy Philips (appointed 4 March 2009)Mr Stephen P RueMr Sam R WhiteMr Simon T Baker (Managing Director/CEO until 4 August 2008)

Principal activitiesThe Group’s principal activity during the year was the provision of online advertising services, which include:

(a) Online advertising of residential properties for sale and rent in multiple countries

(b) Online advertising of commercial properties for sale and lease in multiple countries

(c) Provision of online display advertising space for advertisers in various industries

(d) Provision of website development services to the real estate industry

(e) Software licensing of estate agent back offi ce solutions(f) Print publications to advertise properties for sale and rent(g) Other services

Dividends – REA Group LimitedSince the end of the fi nancial year the directors have recommended the payment of a fi nal ordinary dividend of $12.7 million (10 cents per fully paid share) to be paid on 16 October 2009 out of retained profi ts at 30 June 2009. The directors have also introduced a Dividend Reinvestment Plan which will allow shareholders to elect to re invest the dividend and receive fully paid ordinary REA shares at a 2.5% discount to the weighted average market price calculated over a nominated period.

Review of operationsDuring the year the Group successfully continued its organic growth in online real estate advertising. As at 30 June 2009, the Group operated 21 websites in ten countries, with most of the sites being ranked either fi rst or second in their respective markets.

The key priorities for the Group are:

(a) Execution of a clear strategy which centers around the focus on being the number 1 or number 2 player in every area of operations. As a result some businesses were closed or sold during FY09

(b) Increase in product and innovation rate across the businesses(c) Continued uplift of the skill base of staff(d) Investment in new information technology to further improve

user experience and agent satisfaction(e) Profi table growth

Performance IndicatorsManagement and the Board monitor the Group’s overall performance, from the implementation of its mission statement and strategic plan through to the performance of the company against operating plans and fi nancial budgets and forecasts. The Board, together with management, have identifi ed key performance indicators (KPI’s) that are used regularly to monitor performance.

Dynamics of the BusinessREA Group Limited primarily operates in the online real estate classifi ed advertising market for residential and commercial property.

The three key drivers of advertising revenue for the Group are:

The number of real estate offi ces within any particular market, • which determines the number of subscriptions purchased

The number of listings within any particular market, which • primarily determines the take up of additional advertising products

The number of visitors to the site, which determines the • effectiveness of the classifi ed advertising and determines the take up of display advertising revenue by developer and third party advertisers.

The underlying housing market is infl uenced by certain macro economic factors such as population growth, the unemployment rate, interest rates, international migration, regional population growth, GDP growth, annual house sales growth, and other factors.

Discontinued Operations – United KingdomIn November 2005, REA acquired a 50% stake in propertyfi nder.com, the then number four site in the United Kingdom. Since its acquisition, the combination of propertyfi nder and subsequently acquired sites have evolved to be in equal number two or three market position depending on the metrics used. Facing adverse market conditions, the group closed its print operations in April 2009. In May 2009, the Group commenced a review its UK operations which lead to the sale of the online operations on 7 August 2009. The UK operations are disclosed as discontinued operations in these accounts. Refer to note 9 for detailed disclosure.

www.rea-group.com 17

18 REA Group Annual Report 2009

DIRECTORS’ REPORT CONTINUED

Financial PerformanceOverall, FY09 was the best year in the history of the Group on a Revenue, EBITDA, and EBITDA margin basis. While in the past, growth was based on a combination of organic and acquisition, FY09 was based on organic growth only.

The Group’s core business of online advertising has shown strong resilience to the current global economic crisis. The relative robustness of the online business is a result of the product structure

(subscriptions with additional upgrade products) and the price and convenience of online advertising over print advertising.

During FY09, a number of businesses were reviewed and exited, such as the New Zealand residential business, the Belgium operations, and Clarke Computers (trust accounting software). The decision to review and exit the UK market has resulted in a separate disclosure of the UK business in the fi nancials for FY09 and the previous years.

Financial Comparative Datain $’000 FY 2005 FY 2006 FY 2007 FY 2008 FY 2009

Growth FY08

to FY09

Revenues from Services* 33,416 54,921 89,402 133,562) 167,795 26%

Operating Expenses (26,951) (38,910) (59,081) (86,929) (105,495) 21%

EBITDA 6,465 16,011 30,321 46,633 62,300 34%

EBITDA Margin 19% 29% 34% 35% 37%

Depreciation and Amortisation (1,051) (1,766) (4,230) (6,404) (7,348) 15%

Impairment of goodwil – – – – (6,141)

Impairment of intangibles – – – – (1,854)

EBIT 5,414 14,245 26,091 40,229 46,957 17%

Net Interest (Expense) / Income 206 (403) 461 (21) 344

Earnings Before Tax 5,620 13,842 26,552 40,208 47,301 18%

Income Tax benefi t / (Expense) 2,472 (4,039) (7,535) (14,720) (18,598) 26%

Loss from discontinuing operations – (3,162) (8,028) (9,725) (63,341) 551%

Minority Interest (net of taxes) – 1,581 4,076 6,581 35,584 441%

Profi t attrib. to members of parent 8,092 8,222 15,065 22,344 946 (96)%

Employees (FTE) excluding UK 159 238 409 537 526 (2)%

Employees (FTE) in UK – 56 70 130 79 (39)%

Subscribing Paying Agents excluding UK 6,414 7,806 12,961 16,341 18,879 16%

Subscribing Paying Agents in UK – 2,907 4,050 6,137 5,519 (10)%

*Excludes Interest Income

Key Financial HighlightsThe key fi nancial highlights for FY09 included:

Revenue from continuing operations of $167.8 million, up by 26 • per cent over the last fi nancial year.

Operating expenses from continuing operations of $105.5 million, • up by 21 per cent over the last fi nancial year. The key drivers of the increase in operating expenses are employee costs, consultants, technology costs and bad debt provisions. Due to the current economic climate, a review was undertaken to assess current and future business strategies. As a result of this review, staff numbers decreased from 667 as at June 2008 to 605 as at June 2009.

EBITDA from continuing operations of $62.3 million, up by 34 per •

cent over the last fi nancial year. The Group has increased its EBITDA margin from 35 per cent to 37 per cent. The Group’s cost base does not grow linearly during the year due to ‘one off’ transactions, the impact of changes to foreign exchange rates, and seasonality. This usually leads to a lower profi tability in the fi rst half year compared to the preceding second half year of the previous fi nancial year.

Property Listings across all sites increased to 1,609,573 listings as • at June 2009, up by 151,520 listings compared to June 2008.

Subscribing Paying Agents increased from 22,478 as at 30 June • 2008 to 24,398 as at 30 June 2009 mainly due to a strong increase in agent numbers in Italy.

www.rea-group.com 19

AustraliaThe Australian business is the key driver of value creation within the Group. It consists of 3 major business units. The leading residential advertising business (realestate.com.au), the leading commercial advertising business (realcommercial.com.au) and a strong display advertising business focusing on developers and third parties. The Australian business also encompasses a holiday rentals site (realholidays.com.au), a backoffi ce software business for realestate agents (HubOnline), a web design services business, and a majority share in the lead generation business (homeguru.com.au and ozhomevalue.com.au).

Australia

Online Advertising

Residential properties

realestate.com.auproperty.com.aurealholidays.com.auhomeguru.com.auozhomevalue.com.au

Commercial properties

realcommercial.com.au

Agent Solutions

Real estate agents

Hub OnlineWeb Design Services

The key highlights of the Australian business are:

The number of paying subscribing agents across all portals • increased to 9,332 as at 30 June 2009, up from 9,190 as at 30 June 2008 resulting in an estimated market penetration of approximately 95 percent of all agents. The agent numbers refl ect subscriptions of agents to one or more of the three portals within the Australian business (realestate.com.au, realcommercial.com.au, or realholidays.com.au).

Over FY09, all three portals experienced strong growth. The • commercial segment in particular saw revenues increase by 58% to $15,056k (2008: increase by 52% to $9,519k).

Additional advertising revenue represents 37 percent (compared • with 38 percent in FY08) of the overall revenue from residential agents. Additional advertising revenues represent mainly the sale of Agent banners, Feature properties, Guaranteed Top Spot (GTS), and eBrochures. These sales have increased by approximately 24 percent compared to the previous year. Subscription revenues have grown even faster by 25 percent, which marginally increased their share of the overall revenues from 62 percent to 63 percent. While a price freeze for residential subscriptions was announced during FY09, revenues grew through an increase in market penetration.

The competitive environment remains dynamic. The Group’s • strategy will continue to evolve to meet any challenges.

The Group operates across a number of countries. Key operational highlights on a country basis are as follows:

Country Revenue EBITDA Marginin $’000

FY 2009

Australia 149,651 83,484 56%

Italy 8,540 (3,691) (43)%

Luxembourg 4,304 1,441 33%

Other countries 5,300 (6,905) (130)%

Unallocated overhead – (12,029) -%

Total continued operations 167,795 62,300 37%

FY 2008

Australia 120,719 61,946 51%

Italy 5,401 (2,819) (52)%

Luxembourg 3,532 1,054 30%

Other countries 3,910 (3,601) (92)%

Loss of associate (homeguru.com.au) – (185) -%

Unallocated overhead – (9,762) -%

Total continued operations 133,562 46,633 35%

20 REA Group Annual Report 2009

DIRECTORS’ REPORT CONTINUED

Overseas Businesses

Overseas

Italy Online Advertising Residential Properties casa.it

Luxembourg Online Advertising Residential PropertiesCommercial Properties

athome.luatoffi ce.lu

Print Advertising Residential Properties athome magazineathome new homes

Other countries Online Advertising Residential Properties athomeAlsace.fr (France)athomeLorraine.fr (France)athome.be (Belgium)athome.de (Germany)squarefoot.com.hk (Hong Kong)propertyfi nder.ae (UAE)allglobalproperties.com

Commercial Properties realcommercial.co.nz

Print Advertising Residential Properties Squarefoot (Hong Kong) Inside Discovery Bay (Hong Kong)

Discontinued Operations United Kingdom

Online Advertising Residential Properties propertyfi nder.comhotproperty.co.ukukpropertyshop.co.uk

Print Advertising (until April 2009)

ItalySince February 2007, REA has acquired approximately 69 percent of casa.it with the remaining 31 percent owned by SKY Italia. casa.it is the leading residential real estate site in the Italian market. During the last year, REA has consolidated casa.it’s strong market position by further investing in sales and marketing.

casa.it has seen a signifi cant increase in agent numbers and now has the second highest number of subscribing agents in the group up from 5,514 paying agents in June 2008 to 8,053 in June 2009. In addition, 2,682 trial agents are now also using the site. In total, 10,735 agents were using the site in June 2009. Together with private listers, the agents have uploaded more active listings than are to be found on realestate.com.au. In June 2009, casa.it attracted 1.4 million unique visitors to the site (June 2008: 0.7 million), the highest traffi c number in the history of casa.it (Source: Omniture).

LuxembourgIn February 2007, REA acquired the atHome Group. The atHome Group comprised the number one sites in Luxembourg, athome.lu and atoffi ce.lu. The Luxembourg business has improved its EBITDA margins from 30 percent to 33 percent while further strengthening its dominant market position.

All other countriesIn addition to Luxembourg, the atHome Group has operations in the neighbouring countries and a strong position in North Eastern France (Alsace and Lorraine Region). Overall, the number of paying agents in the atHome Group increased from 957 (June 2008) to 1,230 (June 2009).

The Hong Kong business also grew its revenues in the online and print advertising space. Given the uncertainty of the economic environment, the Group has reviewed the ongoing business plan for

the business and as a result has recorded an impairment charge against its acquired intangibles during FY09.

The current economic climate in UAE has lead to a worsening of the real estate market in the UAE for the foreseeable future. As a result, the Group’s share in the business was sold for US$310k (AUD$380k) on 31 July 2009 and an appropriate impairment and write off of its intangible assets was taken at 30 June 2009. The sale is subject to approval by UAE authorities.

Unallocated OverheadThe Group allocates costs related to its back offi ce functions consisting of the IT development activities for the online portals and agent solutions business, delivering online advertising and agent solution products, as well as certain central head offi ce functions. Unallocated costs include one off costs for corporate affairs, the group fi nance function, the corporate development function, certain IT development costs, and costs of the Board and the Company Secretarial function.

Traffi c on WebsitesMany of the 21 websites of the Group continue to be leaders in online real estate advertising in their regions / countries. According to independent rating auditors Nielsen/NetRatings and Omniture (UK), the monthly readership (measured in Unique Visitors) of all websites increased by 22 per cent from 8.2 million in June 2008 to 10.0 million in June 2009.

The Australian residential website realestate.com.au had 4.5 million Unique Visitors and the gap to the second placed website domain.com.au increased to a record 2.4 million visitors. Also according to Nielsen/NetRating and Omniture, the overall number of pages of information (page impressions) viewed by readers of the Group’s websites increased by 4 per cent from 592 million in June 2008 to 615 million in June 2009.

www.rea-group.com 21

Cash FlowOperating cash fl ow has increased from $15.9m in FY08 to $31.8m in FY09.

Investment for Future PerformanceThe company will continue to strengthen and grow its businesses in both online advertising and in other related sectors of the real estate industry.

Signifi cant changes in the state of affairsSignifi cant changes in the state of affairs of the Group during the fi nancial year were as follows:

Review of UK business leading to closure of print and sale of • online interest in the business.

Sale or closure of smaller non market leading investments.•

The company changed its name from realestate.com.au Limited • to REA Group Limited.

Matters subsequent to the end of the fi nancial yearAs at the date of this report, other than as disclosed in note 35, the directors are not aware of any circumstance that have arisen since 30 June 2009 that has signifi cantly affected, or may signifi cantly affect:

(a) the Group’s operations in future fi nancial years, or(b) the results of those operations in future fi nancial years, or(c) the Group’s state of affairs in future fi nancial years.

Environmental regulationThe company is complying with all environmental regulations and is not subject to any particular environmental requirements.

Information on Directors

Mr Richard J Freudenstein BEc, LLB (Hons). Non executive chairman. Age 44.

Experience and expertiseMr Freudenstein is the Chief Executive Offi cer of News Digital Media (the digital division of News Limited), which includes digital properties, news.com.au, truelocal.com.au, CARSguide.com.au and moshtix.com.au and related activities involving News Limited newspaper and magazine websites, including vogue.com.au and taste.com.au. Mr Freudenstein is non executive Chairman of CareerOne.com.au and sits on the board of News Limited, FOXTEL and The Bell Shakespeare Company. Mr Freudenstein returned to Australia in August 2006 after seven years at British Sky Broadcasting, the last six as Chief Operating Offi cer. Mr Freudenstein has worked for News Corporation and related companies since 1994.

Special responsibilitiesChair of the Board.Member of remuneration and nomination committee.

Mr Roger Amos FCA, MAICD. Non executive Director. Age 61.

Experience and expertiseMr Amos is an independent Director of Austar United Communications Limited, where he is Chair of the Audit Committee and a member of the Remuneration Committee. He is Chairman of Tyrian Diganostics Limited. He also has a non executive

role as Chairman for Ineum Consulting Group Plc and is a member of both the Audit Committee and the Remuneration Committee. Mr Amos had a long and distinguished career with international accounting fi rm KPMG, retiring in June 2006 after 25 years as a partner in the Assurance and Risk Advisory Services Division. In addition to his portfolio of clients, focused on the Information, Communications and Entertainment Industry (ICE), Mr Amos held various roles in the KPMG Global ICE industry groups, including Global Chairman of the Communications Industry Group. Mr Amos also serves as a Director of the Opera Foundation of Australia which supports the development of emerging opera talent through awards and scholarships.

Special responsibilitiesChair of audit risk and compliance committee.Member of remuneration and nomination committee.Interests in shares and options2,363 ordinary shares in REA Group Ltd.

Ms Kathleen Conlon BA(ECON)(DIST), MBA, MAICD. Non executive Director. Age 45.

Experience and expertiseMs Conlon is a professional non executive Director. She is a non executive Director of CSR Limited (since 2004), where she serves on the Safety Health and Environment and Audit committees. She is also a non executive director of DLA Phillips Fox and a member of Chief Executive Women. She is also a NSW Council Member of the Australian Institute of Company Directors. Ms Conlon brings over 20 years of professional consulting experience to her boards. She is a recognised thought leader in strategy and business improvement, and has advised leading companies across a range of industries and countries. In her seven years as a partner and director of the Boston Consulting Group (BCG), Ms Conlon led BCG’s Asia Pacifi c Operations Practice Area and, previously, the Sydney Offi ce. In 2003, Ms Conlon was awarded a Centenary Medal for service to business.

Special responsibilitiesMember of audit risk and compliance committee.Chair of remuneration and nomination committee.

Mr Greg Ellis BBus. Managing Director/CEO. Age 47.

Experience and expertiseMr Ellis has over 20 years business experience, 14 of which have been in senior line management positions. He has worked in Australia, Asia and Europe. Prior to joining the REA Group he was Marketing Director Asia Online Services for Microsoft. He has been Managing Director of Online and Search at World Directories in the Netherlands. Mr Ellis also spent fi ve years at Sensis and 11 years at Telstra. At Sensis, he was most recently General Manager of Sensis Interactive. At Telstra, his most recent role was National General Manager, Marketing Strategy & Planning. He was appointed Managing Director on 23 September 2008.

22 REA Group Annual Report 2009

DIRECTORS’ REPORT CONTINUED

Mr John D McGrath Qualifi cations. Non executive Director. Age 45.

Experience and expertiseMr McGrath founded McGrath Estate Agents in 1988. He has grown the company to be one of Australia’s most successful property services groups, selling over $3.25 billion in residential property in Sydney in FY09. The company became the fi rst real estate company to be ranked on BRW’s Australia’s Fastest Growing Private Companies List and is a 3 time recipient of BRW’s Fast 100. McGrath Estate Agents also owns Oxygen Home Loans, its mortgage broking business, as well as Total Real Estate Training that provides training programs and seminars for the real estate industry. Mr McGrath is a Director of McGrath Group of Companies and the Rawson Group. In 2003, he was awarded a Centenary Medal for service to business. In 2008, he was honoured by the Real Estate Institute of NSW with the Woodrow Weight OBE Award, a lifetime achievement award for his outstanding contribution to the real estate industry.

Special responsibilitiesMember of remuneration and nomination committee.2,139,086 ordinary shares in REA Group Ltd.

Mr Alasdair MacLeod Qualifi cations. Non executive Director. Age 48.

Experience and expertiseMr MacLeod is the Managing Director of News Limited’s NSW publishing company, Nationwide News, and sits on the Board of News Limited. Nationwide News publishes The Daily Telegraph, Sunday Telegraph, The Australian, Weekend Australian, mX and Sportsman. Mr MacLeod joined News Limited in 2002 as Managing Director of the company’s community newspapers division which publishes over 120 titles throughout Australia. He relocated to Australia after thirteen years with News International in the UK where he held a number of senior positions including Managing Director of online division News Network and General Manager of Times Newspapers, the publisher of The Times and The Sunday Times. Prior to joining the News Group, Mr MacLeod worked with Citibank Limited in Sydney and in Hong Kong.

Interests in shares and options18,880 options over Class A News Corporation Limited shares4,000 Class A News Corporation shares

Mr Jeremy Philips BA, LLB, MPA. Non executive Director. Age 37.

Experience and expertiseMr Philips is Executive Vice President, Offi ce of the Chairman, at News Corporation. He is a member of News Corp’s Executive Management Committee, and is based in New York. He focuses on strategy and digital acquisitions across the company. He was Vice Chairman and co founder of ecorp Limited, a holding company for leading Internet businesses in Australia, including ebay Australia, ninemsn and Ticketek. Prior to that, he was a consultant at McKinsey & Company. Jeremy is a graduate of the University of New South Wales (Arts and Law) and the Harvard Kennedy School of Government. He is a member of the board of One Laptop Per Child. Mr Philips was appointed a director on 4 March 2009.

Interests in shares and options24,318 Class A News Corporation shares

Mr Stephen P Rue CA, BBS, DPA. Non executive Director. Age 43.

Experience and expertiseMr Rue is the Chief Financial Offi cer of News Limited, the Australian arm of News Corporation. He was appointed to his current role in May 2003, and previously was the company’s Group Finance Manager. Mr Rue fi rst joined News Limited in 1996 and moved into the role of Treasurer and Special Projects Manager prior to being appointed Group Finance Manager. Mr Rue’s experience includes 8 years at Arthur Andersen where he held the position of Senior Manager in their Audit and Business Advisory division. Mr Rue is Chairman of Community Newspaper Group Limited and a Director of News Limited and Australian Associated Press Pty Limited. Mr Rue is a Chartered Accountant and holds a Bachelor of Business Studies and a Diploma in Professional Accounting.

Special responsibilitiesMember of audit risk and compliance committee.Interests in shares and options49,000 options over Class A News Corporation Limited shares

Mr Sam R White B.Com, LLB. Non executive Director. Age 38.

Experience and expertiseMr White joined Ray White Real Estate in 1991 and was appointed to its Board in 1998. Mr White is also Chairman of the Loan Market Group, a leading mortgage and insurance broking group. Mr White has a Bachelor of Commerce and a Bachelor of Law from the University of Queensland.

Special responsibilitiesMember of remuneration and nomination committee.

Interests in shares and options564,211 ordinary shares in REA Group Ltd.

Mr Simon T Baker BSc, MBA Managing Director/CEO. Age 42.

Experience and expertiseMr Baker was the Managing Director and Chief Executive Offi cer of REA Group until 4 August 2008.

Company Secretary

Ms Moana Weir BA, LLB(Hons), MAICDMs Weir has 8 years senior management experience in public companies with international operations in the online IT and advertising industries. Prior to this she worked as an in house lawyer at Coles Myer Ltd, and practised as an IP/IT lawyer at leading Australian law fi rms, most recently Allens Arthur Robinson. She holds a BA and Bachelor of Laws Degree (Honours), and is admitted to practice as a barrister and solicitor in the Supreme Court of Victoria, Australia. She is a member of the Australian Institute of Company Directors. Ms Weir was appointed company secretary on 15 December 2008.

www.rea-group.com 23

Meetings of directorsThe numbers of meetings of the company’s board of directors and of each board committee held during the year ended 30 June 2009, and the numbers of meetings attended by each director were:

Meetings of committees

Full meetings of directorsAudit Risk and

Compliance MeetingsRemuneration and

Nomination Committee Meetings

A B A B A B

Mr Richard J Freudenstein 7 7 – – 2 2

Mr Roger Amos 7 7 5 5 2 2

Ms Kathleen Conlon 7 6 5 5 2 2

Mr Greg Ellis (appointed 23 September 2008) 5 5 – – – –

Mr John D McGrath 7 7 – – 2 1

Mr Alasdair MacLeod 7 7 – – – –

Mr Jeremy Philips (appointed 4 March 2009) 2 2 – – – –

Mr Stephen P Rue 7 6 5 5 – –

Mr Sam R White 7 6 – – 2 2

Mr Simon T Baker (until 4 August 2008) – – – – – –

A Number of meetings held during the time the director held offi ce or was a member of the committee during the yearB Number of meetings attended

REMUNERATION REPORT (AUDITED)This report outlines the remuneration arrangements in place for directors and executives of REA Group Limited ‘the company’ and the Group is in accordance with the requirements of the Corporations Act 2001 and its regulations.

Remuneration philosophyThe performance of the company depends upon the quality of its directors and executives. To prosper, the company must attract, motivate and retain highly skilled directors and executives. To this end, the company embodies the following principles in its remuneration framework:

Provide competitive rewards to attract high calibre executives•

Signifi cant portion of executive remuneration ‘at risk’, dependent • upon meeting pre determined performance benchmarks

Establish appropriate, demanding performance hurdles in relation • to variable executive remuneration

Remuneration and Nomination CommitteeThe Remuneration and Nomination Committee of the Board of Directors of the company is responsible for determining and reviewing compensation arrangements for the directors, the Chief Executive Offi cer (CEO) and the senior management team. The committee assesses the appropriateness of the nature and amount of remuneration of directors and senior managers on a periodic basis by reference to relevant employment market conditions with the overall objective of ensuring maximum shareholder benefi t from the retention of a high quality board and executive team.

Remuneration structureIn accordance with best practice corporate governance, the structure of non executive director and senior manager remuneration is separate and distinct.

Non executive director remunerationObjectiveThe Board seeks to set aggregate remuneration at a level which provides the company with the ability to attract and retain directors of the highest calibre, whilst incurring a cost which is acceptable to shareholders.

StructureThe Constitution and the ASX Listing Rules specify that the aggregate remuneration of non executive directors shall be determined from time to time by a general meeting. An amount not exceeding the amount determined is then divided between the directors as agreed. The latest determination was at the Annual General Meeting held in November 2006 when shareholders approved an aggregate remuneration of $350,000 per year. The amount of the aggregate remuneration sought to be approved by shareholders and the manner in which it is apportioned amongst directors is reviewed annually. The remuneration of non executive directors for the period ending 30 June 2009 is detailed in the table on page 25 of this report.

Senior manager and executive director remunerationObjectiveThe company aims to reward executives with a level/mix of remuneration commensurate with their position and responsibilities within the company and so as to:

Reward executives for performance against targets set by • reference to appropriate benchmarks;

Align the interests of executives with those of shareholders;•

Link reward with the strategic goals and performance of the • company; and

Ensure total remuneration is competitive by market standards.•

24 REA Group Annual Report 2009

DIRECTORS’ REPORT CONTINUED

StructureRemuneration costs consist of the following key elements:

Fixed remuneration•

Variable remuneration•

The table on page 26 of this report gives details the variable component of the fi ve most highly remunerated senior managers.

Fixed RemunerationObjectiveThe level of fi xed remuneration is set so as to provide a base level of remuneration which is both appropriate to the position and is competitive in the market. Fixed remuneration is reviewed annually. All contracts for new senior management have to be approved by the Remuneration and Nomination Committee. In addition, deviations from the budgeted salary increases also require approval.

StructureSenior managers are given the opportunity to receive part of their fi xed (primary) remuneration in fringe benefi ts such as motor vehicles and education expense payment plans. It is intended that the manner of payment chosen will be optimal for the recipient without creating undue cost for the company. This fi xed remuneration component of the fi ve most highly remunerated senior managers is detailed in the table on page 26 of this report.

Variable Remuneration – Short Term Incentives = STIObjectiveThe objective of the STI program is to link the achievement of the company’s operational targets with the remuneration received by the executives charged with meeting those targets. The total potential STI available is set at a level so as to provide suffi cient incentive to the senior manager to achieve the operational targets and such that the cost to the company is reasonable in the circumstances.

StructureActual STI payments granted to each senior manager depends on the extent to which specifi c operating targets set at the beginning of the fi nancial year are met. The operational targets consist of a number of Key Performance Indicators (KPI’s) covering both fi nancial and non fi nancial measures of performance. Typically included are measures such as contribution to revenues, profi tability, customer service, risk management, product management, and leadership/team contribution. The company has approved predetermined benchmarks which must be met in order to trigger payments under the short term incentive scheme. Payments made are usually delivered as a cash bonus.

STI bonus for FY08 and FY09For FY08, STI cash bonuses of $372,786 as previously accrued in that period vested to executives and were paid in the 2008 fi nancial year. There were no forfeitures. The maximum STI cash bonus for the 2009 fi nancial year of $502,749 has been accrued on the basis that it is probable that all executives will meet their respective KPI’s for the period. Any adjustments between the actual amounts and the amounts accrued will be adjusted in FY10. The minimum amount of the STI cash bonus assuming that no executives meet their respective KPIs for the 2009 fi nancial year is nil.

Variable Remuneration – Long Term Incentives = LTIObjectiveThe objective of the LTI plan is to link the achievement of the company’s long term targets with the remuneration received by the executives charged with meeting those targets. The total potential LTI available is set at a level so as to provide suffi cient incentive to the senior manager to achieve the long term targets and such that the cost to the company is reasonable in the circumstances.

StructurePlanned LTI payments granted to each senior manager depends on the extent to which specifi c targets set at the beginning of plan are met. The targets are revenue and profi tability related targets in the third year after the initiation of the plan. Payments made are usually delivered as rights to company shares. The company does not encourage entering into arrangements to protect the value of unvested LTI awards. This includes entering into contracts to hedge the exposure to options of shares granted as part of their remuneration package.

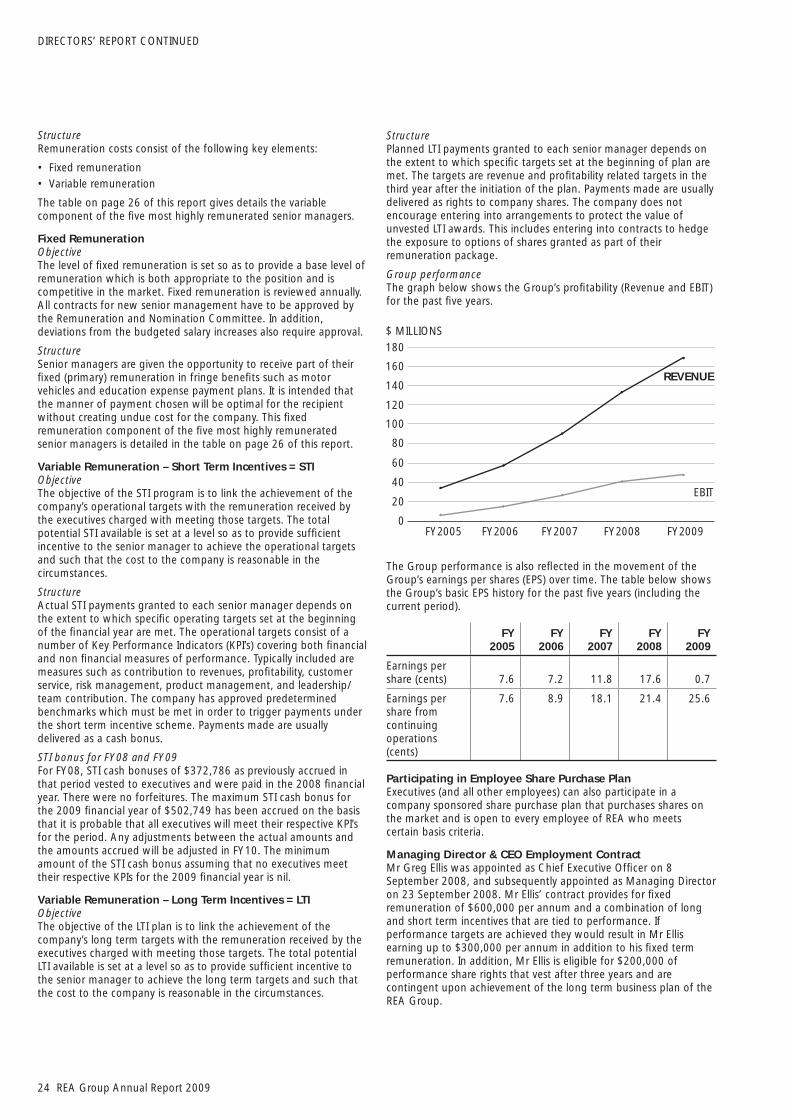

Group performanceThe graph below shows the Group’s profi tability (Revenue and EBIT) for the past fi ve years.

The Group performance is also refl ected in the movement of the Group’s earnings per shares (EPS) over time. The table below shows the Group’s basic EPS history for the past fi ve years (including the current period).

FY2005

FY2006

FY2007

FY2008

FY2009

Earnings per share (cents) 7.6 7.2 11.8 17.6 0.7

Earnings per share from continuing operations (cents)

7.6 8.9 18.1 21.4 25.6

Participating in Employee Share Purchase PlanExecutives (and all other employees) can also participate in a company sponsored share purchase plan that purchases shares on the market and is open to every employee of REA who meets certain basis criteria.

Managing Director & CEO Employment ContractMr Greg Ellis was appointed as Chief Executive Offi cer on 8 September 2008, and subsequently appointed as Managing Director on 23 September 2008. Mr Ellis’ contract provides for fi xed remuneration of $600,000 per annum and a combination of long and short term incentives that are tied to performance. If performance targets are achieved they would result in Mr Ellis earning up to $300,000 per annum in addition to his fi xed term remuneration. In addition, Mr Ellis is eligible for $200,000 of performance share rights that vest after three years and are contingent upon achievement of the long term business plan of the REA Group.

180

160

140

120

100

$ MILLIONS

REVENUE

EBIT

80

60

40

20

0FY2005 FY2006 FY2007 FY2008 FY2009

www.rea-group.com 25

DirectorsWith the exception of the changes noted below, the following persons held offi ce as directors of REA Group Limited during the whole of the fi nancial year and up to the date of this report.

Mr Richard J Freudenstein (Chairman)Mr Roger Amos (Non executive Director)Ms Kathleen Conlon (Non executive Director)Mr Greg Ellis (Managing Director/CEO appointed 23 September 2008)Mr John D McGrath (Non executive Director)Mr Alasdair MacLeod (Non executive Director)Mr Jeremy Philips (Non executive Director appointed 4 March 2009)Mr Stephen P Rue (Non executive Director)Mr Sam R White (Non executive Director)Mr Simon T Baker (Managing Director and Chief Executive Offi cer until 4 August 2008)

Director remuneration

DirectorsShort term

employee benefi tsShare based

payments Total

(% of total

performance related)

Salary & Fees

Cash Bonus

Super-annuation

Long Service Leave LTIP*

Roger Amos

2009 76,453 – 6,873 – – 83,326 0%

2008 77,982 – 7,018 – – 85,000 0%

Kathleen Conlon

2009 67,278 – 6,070 – – 73,348 0%

2008 64,220 – 5,780 – – 70,000 0%

John McGrath

2009 64,220 – 5,780 – – 70,000 0%

2008 94,037 – 8,463 – – 102,500 0%

Greg Ellis

2009 448,836 239,808 40,395 – 66,667 795,706 39%

2008 – – – – – –

Simon Baker

2009 775,009 70,459 103,092 (42,689) 84,929 990,800 16%

2008 530,001 300,000 47,700 42,689 15,071 935,461 34%

*Long Term Incentive Plan.Directors’ fees are paid only to independent or executive directors. All other directors, not being independent, did not receive any directors’ fees during the fi nancial period.

ExecutivesThe key management personnel and the names of the 5 executives who receive the highest remuneration for the year ended 30 June 2009 were:

Mr Georg Chmiel Chief Financial Offi cerMr Daniel Oertli Chief Information Offi cer (since 17 February 2009)Mr Daniele Mancini Country Manager Italy (since 1 April 2009)Mr Jamie Pride General Manager Australia (until 2 March 2009)Ms Gillian Kent General Manager United Kingdom Mr Shaun Di Gregorio General Manager International

26 REA Group Annual Report 2009

DIRECTORS’ REPORT CONTINUED

Executives remuneration

Executives Short termShare based

payments Total

(% of total performance

related)

Salary & Fees

Cash Bonus Other

Super-annuation

Long Service Leave LTIP*

Georg Chmiel

2009 330,000 59,000 – 36,000 6,595 153,145 584,740 36%

2008 310,000 55,000 – 30,401 5,583 11,304 412,288 16%

Shaun Di Gregorio

2009 320,000 78,666 – 36,900 12,419 122,516 570,501 35%

2008 263,333 80,000 – 30,308 21,930 9,043 404,614 22%

Daniele Mancini

2009 168,455 22,818 – 3,251 – – 194,524 12%

2008 – – – – – – – –

Daniel Oertli

2009 121,218 29,278 – 10,910 – – 161,406 18%

2008 – – – – – – – –

Jamie Pride

2009 212,209 53,333 12,000 16,154 – (3,090) 290,606 17%

2008 70,770 36,889 – 6,369 – 3,090 117,118 34%

Gillian Kent

2009 325,239 73,179 – 53,008 – 72,484 523,910 28%

2008 154,399 49,669 – 39,597 – 4,291 247,956 22%

*Long Term Incentive Plan (see note 38).

Rights granted and vested during the year

Terms and Conditions for each right Vested

30 June 2009Granted Number Grant date

Fair value per right at grant date

Exercise price per

rightExpiry

dateFirst

exercise dateLast

exercise date No. %

Mr Greg Ellis 42,009 1 July 2008 4.40 0 n/a 1 July 201130 September

2011 – 0.0

Mr Georg Chmiel 34,091 1 July 2008 4.40 0 n/a 1 July 201130 September

2011 – 0.0

Mr Shaun Di Gregorio 27,273 1 July 2008 4.40 0 n/a 1 July 2011

30 September 2011 – 0.0

TOTAL 103, 373 –

The terms ‘director’ and ‘offi cer’ have been treated as mutually exclusive for the purposes of this disclosure. The elements of emoluments have been determined on the basis of the cost to the company and the consolidated entity.

Options granted as part of remunerationOther than as part of the Long Term Incentive Plan, there were no other options granted as part of remuneration for the year ended 30 June 2009.

www.rea-group.com 27

INDEMNIFICATION AND INSURANCE OF DIRECTORS AND OFFICERSFor FY09, the company paid premiums totalling $1,609 in respect of contracts insuring all the directors of REA Group Limited against costs incurred in defending proceedings for conduct involving:

1. a wilful breach of duty; or

2. a contravention of Sections 182 or 183 of the Corporations Act (2001), as permitted by section 199B of that Act.

REA Group Limited has entered into a standard form deed of indemnity, insurance and access with the independent directors against liabilities they may incur in the performance of their duties as directors of REA Group Limited, except liabilities to REA Group Limited or a related body corporate, liability for a pecuniary penalty or compensation order under the Corporations Act, and liabilities arising from conduct involving a lack of good faith. REA Group Limited is obliged to maintain an insurance policy in favour of independent directors for liabilities they incur as directors of REA Group Limited and to grant them a right of access to certain company records. In addition, each Director is indemnifi ed, as authorised by the Constitution, on a full indemnity basis and to the full extent permitted by law, for all losses or liabilities incurred by the Director as a director of a member of the Group. The indemnity operates only to the extent that the loss or liability is not covered by insurance.

Up to 11 November 2005 (when News Limited increased its share in REA Group Limited to a controlling shareholding) the company held a Directors’ and Offi cer’s Liability Insurance Policy on behalf of current directors and offi cers of REA Group Limited and its controlled entities. On 11 November 2005, this policy was converted into a seven year run off cover. REA Group Limited is now covered by a D&O insurance for the News Corporation Group of companies. This cover excludes claims brought by major shareholders (News Limited).

Non audit servicesThe company may decide to employ the auditor on assignments additional to their statutory audit duties where the auditor’s expertise and experience with the company and/or the Group are important.

Details of the amounts paid or payable to the auditor (Ernst & Young) for audit and non audit services provided during the year are set out below.

The Board of directors has considered the position and, in accordance with advice received from the audit committee, is satisfi ed that the provision of the non audit services is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001. The directors are satisfi ed that the provision of non audit services by the auditor, as set out below, did not compromise the auditor independence requirements of the Corporations Act 2001 for the following reasons:

all non audit services have been reviewed by the audit committee • to ensure they do not impact the impartiality and objectivity of the auditor

none of the services undermine the general principles relating to • auditor independence as set out in APES 110 Code of Ethics for Professional Accountants.

During the year the following fees were paid or payable for audit and non audit services provided by the a uditor of the parent entity, its related practices and non related audit fi rms:

Consolidated

2009$

2008$

Audit and review of fi nancial reports 484,000 492,000

Assurance related services 46,370 36,000

Total remuneration for audit services 530,370 528,000

Due diligence services 21,683 198,000

Total remuneration for other assurance services 21,683 198,000

28 REA Group Annual Report 2009

DIRECTORS’ REPORT CONTINUED

Review of Financial Condition

Capital structureAt the end of the year, 127,255,057 (2008: 127,255,057) ordinary shares were outstanding. The Group is equity fi nanced as at the date of this report with an undrawn credit line of $14 million for short term fi nancing needs, which will expire in September 2009 ($4 million) and October 2010 ($10 million).

Treasury policyExcess funds are currently invested in an overnight professional funds account.

Cash from OperationsDuring the fi nancial year, the Group delivered $31.8 million (2008: $15.9 million) in operating cash fl ows.

Liquidity and FundingThe company has suffi cient funds to fi nance its operations.

Risk ManagementThe Group takes a proactive approach to risk management. The Board is responsible for ensuring that risk and opportunities are identifi ed on a timely basis and that the Group’s objectives and activities are aligned with the risks and opportunities identifi ed by the Board. The mechanisms for risk management include approval of a strategic plan by the Board, the approval of operating budgets and their regular review against actual fi nancial data. (Refer also note 3.)

Auditor’s independence declarationA copy of the auditor’s independence declaration as required under section 307C of the Corporations Act 2001 is set out on page 29.

Rounding of amountsThe company is of a kind referred to in Class Order 98/100, issued by the Australian Securities and Investments Commission, relating to the ‘’rounding off’’ of amounts in the directors’ report. Amounts in the directors’ report have been rounded off in accordance with that Class Order to the nearest thousand dollars, or in certain cases, to the nearest dollar.

AuditorErnst & Young continues in offi ce in accordance with section 327 of the Corporations Act 2001.

This report is made in accordance with a resolution of directors.

Mr Richard J FreudensteinDirectorMelbourne, 20 August 2009

www.rea-group.com 29

Auditor’s Independence Declaration to the Directors of REA Group LimitedIn relation to our audit of the fi nancial report of REA Group Limited for the fi nancial year ended 30 June 2009, to the best of my knowledge and belief, there have been no contraventions of the auditor independence requirements of the Corporations Act 2001 or any applicable code of professional conduct.

Ernst & Young

David McGregorPartner

20 August 2009Melbourne, Australia

Ernst & Young Building8 Exhibition StreetMelbourne VIC 300 AustraliaGPO Box 67 Melbourne VIC 3001

Tel: +61 3 9288 8000Fax: +61 3 8650 7777www.ey.com/au

AUDITOR’S INDEPENDENCE DECLARATION

Liability limited by a scheme approved under Professional Standards Legislation

30 REA Group Annual Report 2009

CORPORATE GOVERNANCE STATEMENT

The Corporate Governance arrangements for the Group (REA) are set by the Board having regard to the particular circumstances of the Group and the best interests of shareholders. REA is committed to best practice in corporate governance where these practices are appropriate and add value to REA. The Board and management of REA maintain a constant interest in governance, including assessing the guidelines of regulatory and investor bodies and considering other national and international practices. This leads to the governance arrangements being reviewed regularly to ensure compliance with legal requirements, to meet the expectations of shareholders and to best address the circumstances of REA. During 2009, all existing Board and Committee Charters were reviewed and revised by the Board as deemed necessary.

The information on the following pages shows compliance by REA Group Limited against the revised Corporate Governance Principles and Recommendations of the ASX Corporate Governance Council in accordance with Listing Rule 4.10.

This statement also provides information on other governance practices adopted by REA Group Limited. This statement is current as at the date of the 2009 Directors’ Report and, unless otherwise indicated, the information was true for the whole of the fi nancial year commencing on 1 July 2008. The information provided below contains references to the REA web site (www.investor.rea-group.com). This statement should be read in conjunction with this web site and with the Directors’ Report.

Recommendation Compliance

Section 1

1.1 Companies should establish the functions reserved to the board and those delegated to senior executives and disclose those functions.

The Board has adopted a Charter that details the functions and responsibilities of the Board, which is available on the REA Group web site. Management of REA’s day-to-day operations is undertaken by the Managing Director and Chief Executive Offi cer, subject to specifi ed delegations of authority approved by the Board.

The Board has also adopted the practice of formal letters of appointment for all new directors. The letter sets out the key terms and conditions of the director’s appointment.

✔

1.2 Companies should disclose the process for evaluating the performance of senior executives

The Remuneration Committee oversees the performance and determines performance assessment of senior executives. For all line managers and staff, a formal performance review framework is in place to monitor outcomes, set KPI’s and review achievements against set goals.

✔

Section 2

2.1 A majority of the Board should be independent directors.

A majority of the Board are not independent directors. Due to the size of the company, and the strategic relationships, the directors have determined that it is inappropriate to increase the number of directors to a size where there can be a majority of independent directors. This decision does not however limit the size of the Board, nor preclude the appointment of additional directors.

The matters and thresholds considered by the Board in assessing the independence of directors are set out in the Board’s Charter, which is available on REA’s web site. The defi nition of independent director does not depart from that recommended by the ASX Corporate Governance Council. Materiality thresholds have been determined by the Board.

The Board makes an assessment of the independence of each director upon appointment and in August of each year. Directors are required on an ongoing basis to disclose to the Board relevant personal interests and confl icts of interest. Upon any such disclosure, a director’s independence is reassessed.

✕

2.2 The Chairperson should be an independent director.

The current chairperson, Richard J Freudenstein, is not assessed as independent. His appointment is seen as a refl ection of his signifi cant experience and industry knowledge.

✕

2.3 The roles of the Chairperson and Chief Executive Offi cer should not be exercised by the same individual ✔

2.4 The Board should establish a nomination committee.

The Board has a Remuneration and Nomination Committee.

The Nomination Committee should be structured so that it:

Consists of a majority of independent directors•

Is chaired by an independent director•

Has at least 3 members•

The Board has adopted a Charter for the Committee, a copy of which is available on REA’s website. •

✔(from 30 June

2009)

2.5 Companies should disclose the process for evaluating the performance of the Board, its committees and individual directors.

The Board of Directors initiated a formal review of the individual Director’s and the performance of the Board and its committees during 2009.

✔

www.rea-group.com 31

Recommendation Compliance

Section 3

3.1 Companies should establish a code of conduct and disclose the code or a summary of the code.

REA has adopted a Code of Conduct to guide the standards of ethical behaviour expected of REA directors and employees in the performance of their work. A copy of the REA Code of Conduct is available on REA’s website.

✔

3.2 Companies should establish a policy concerning trading in company securities by directors, senior executives and employees and disclose the policy or a summary of that policy.

The REA Share Trading Policy is available on the REA website.

✔

Section 4

4.1 The Board should establish an audit committee.

The Board has established an Audit Risk and Compliance Committee that operates under a charter approved by the Board.

✔

4.2 The audit committee should be structured so that it:

Consists of only non-executive directors•

Consists of a majority of independent directors•

Is chaired by an independent chair, who is not chair of the Board•

Has at least three members•

✔

4.3 The Audit Committee should have a formal charter.

A copy of the Charter of the Audit Committee is available on the REA website.

✔

Section 5

5.1 Establish written policies and procedures designed to ensure compliance with ASX Listing Rule disclosure requirements and to ensure accountability at a senior management level for that compliance and disclose those policies or a summary of those policies.

The Board has adopted the REA Market Disclosure Policy, which sets out the key obligations of the Board and senior management to ensure that REA complies with its disclosure obligations under the ASX Listing Rules and the Corporations Act 2001 (Cth). A copy of the REA Market Disclosure Policy is available on the REA website.

✔

Section 6

6.1 Companies should design a communications policy for promoting effective communication with shareholders and encouraging participation at general meetings and disclose their policy or a summary of that policy.

The Board has adopted a REA Shareholder Communications Policy, a copy of which is posted on the REA website.

✔

Section 7

7.1 Companies should establish policies for oversight and management of material business risks and disclose a summary of those policies.

The Audit Risk and Compliance Committee has included within its terms of reference, a section dealing with the monitoring and establishment of policies regarding risk management and overseeing.

✔

7.2 The Board should require management to design and implement the risk management and internal control system to manage the company’s material business risks and report to it on whether those risks are being managed effectively. The Board should disclose that management has reported to it as to the effectiveness of the company’s management of its material business risks.

REA has adopted a risk management framework throughout its operations to proactively and systematically identify, assess and address events that could potentially impact upon business objectives. Under the Risk Management Policy, which supports the risk management framework, there is regular reporting to the Board and the Audit Risk and Compliance Committee. REA has an internal audit function which reports to the Audit Risk and Compliance Committee and the Managing Director and Chief Executive Offi cer. The Audit Risk and Compliance Committee oversees the internal audit function and the appointment of the Internal Audit Manager. The Internal Audit Manager meets with both the Chairman of the Audit Committee and the Audit Committee as a whole in the absence of management. This function has full access to personnel and information and is independent of the external auditor.

✔

7.3 The Board should disclose whether it has received assurance from the chief executive offi cer (or equivalent) and the chief fi nancial offi cer (or equivalent) that the declaration provided in accordance with section 295A of the Corporations Act is founded on a sound system of risk management and internal control and that the system is operating effectively in all material respects in relation to fi nancial reporting risks.

The Board receives a written declaration prior to the acceptance of the annual fi nancial statements.

✔

32 REA Group Annual Report 2009

CORPORATE GOVERNANCE STATEMENT CONTINUED

Recommendation Compliance

Section 8

8.1 The Board should establish a remuneration committee.

The Board has a Remuneration and Nomination Committee.

The Nomination Committee should be structured so that it:

Consists of a majority of independent directors•

Is chaired by an independent director•

Has at least 3 members•

The Board has adopted a Charter for the Committee, a copy of which is available on REA’s website.

✔(from 30 June

2009)

8.2 Companies should clearly distinguish the structure of the non-executive directors’ remuneration from that of executive directors and senior executives.

As discussed in the Remuneration Report contained in the Directors’ Report, 100% of the remuneration of non-executive directors is fi xed and non-executive directors do not participate in any incentive plan.

Remuneration paid to executives in 2009 included fi xed and variable components, as detailed in the Remuneration Report.

✔

Structure of the Board

The directors in offi ce are:

Name Position Period in offi ce at 30 June 2009

Mr John D McGrath Non-executive director 8 years, 9 months

Mr Sam R White Non-executive director 6 years, 10 months

Mr Alasdair MacLeod Non-executive director 6 years, 4 months

Mr Stephen P Rue Non-executive director 5 years, 10 months

Mr Roger Amos Non-executive director 3 years

Mr Richard J Freudenstein Chairman, Non-executive director 2 years, 7 months

Ms Kathleen Conlon Non-executive director 2 years

Mr Greg Ellis Managing Director/CEO 9 months

Mr Jeremy Philips Non-executive director 4 months

The skills, experience and expertise relevant to the position of director held by each director in offi ce at the date of the annual report is included in the Directors’ Report. Directors of REA Group Limited are considered to be independent when they are independent of management and free from any business or other relationship that could materially interfere with – or could reasonably be perceived to materially interfere with – the exercise of their unfettered and independent judgement.

In the context of director independence, “materiality” is considered from both the company and individual director perspective. The determination of materiality requires consideration of both quantitative and qualitative elements. An item is presumed to be quantitatively immaterial if it is equal or less than 5% of the appropriate base amount. It is presumed to be material (unless there is qualitative evidence to the contrary) if it is equal to or greater than 10% of the appropriate base amount. Qualitative factors considered include whether a relationship is strategically important, the competitive landscape, the nature of the relationship and the contractual or other arrangements governing it and other factors which point to the actual ability of the director in question to shape the direction of the company’s strategy. In accordance with the defi nition of independence above, and the materiality thresholds set, the following directors of REA Group Limited are considered to be independent:

Mr Roger Amos•

Ms Kathleen Conlon•

Mr John D McGrath•