raymond james 36 th annual institutional investors conference bill rutherfordcfo and executive vice...

TRANSCRIPT

Raymond James36th Annual Institutional Investors ConferenceBill Rutherford CFO and Executive Vice PresidentDr. Ravi Chari Senior Vice President, Clinical ExcellenceMark Kimbrough Vice President, Investor Relations

March 3, 2015, Orlando, FL

22

2

FORWARD-LOOKING STATEMENTS AND NON-GAAP FINANCIAL MEASURES

This presentation may contain certain forward-looking statements provided by Company management. These statements are intended to be covered by the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts, including statements regarding future operations, financial results, cash flows, costs and cost management initiatives, capital structure management, growth rates, and operational and strategic initiatives, and can also be identified by the use of words like “may,” “believe,” “will,” “expect,” “project,” “estimate,” “anticipate,” “intend,” “plan,” “initiative,” “continue” or words or phrases of similar meaning. These forward-looking statements speak only as of the date hereof and are based on our current plans and expectations and are subject to a number of known and unknown uncertainties and risks, many of which are beyond our control. These risks and uncertainties are described in headings such as “Risk Factors” in our annual report on Form 10-K for the year ended December 31, 2014 and other reports to be filed with the Securities and Exchange Commission. As a consequence, current plans, anticipated actions and future financial position and results of operations may differ significantly from those expressed in any forward-looking statements in today’s presentation. You are cautioned not to unduly rely on such forward-looking statements when evaluating the information presented and we do not intend to update any of these forward-looking statements.

The presentation may contain certain non-GAAP measures, including Adjusted EBITDA. The Company’s earnings release for the year ended December 31, 2014, located on the Company’s investor relations page at www.hcahealthcare.com, includes reconciliations of the difference between certain non-GAAP financial measures with the most directly comparable financial measure calculated in accordance with GAAP. These non-GAAP financial measures should not be considered alternatives to the GAAP financial measures.

References to “Company” used herein refer to HCA Holdings, Inc. and its affiliates, unless otherwise stated or indicated by context.

33

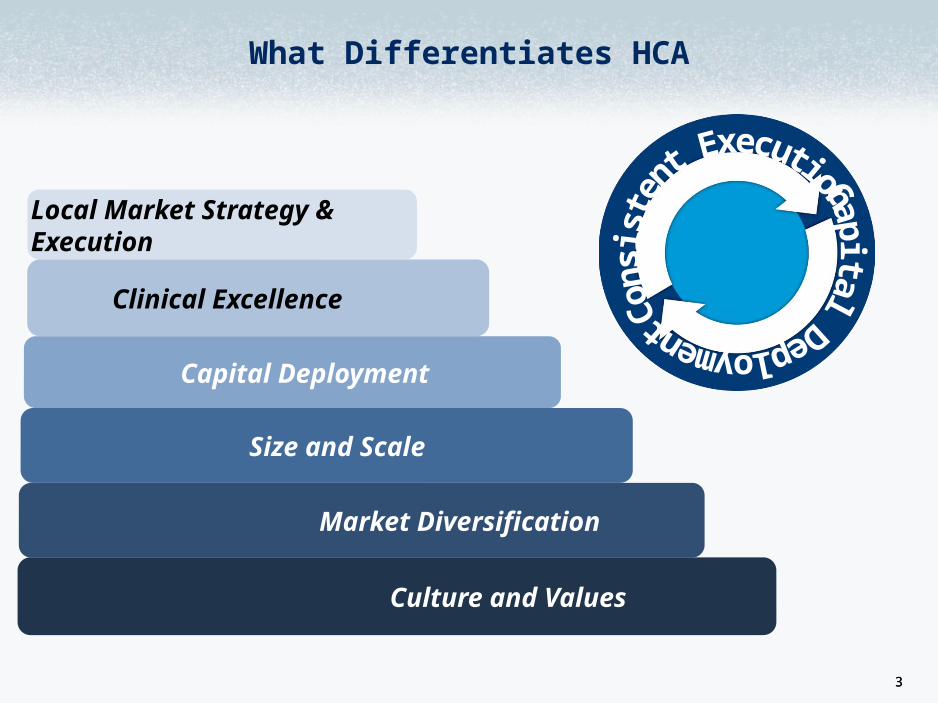

What Differentiates HCA

Local Market Strategy & Execution

Culture and Values

Clinical Excellence

Market Diversification

Capital Deployment

Size and Scale

44

What Differentiates HCA

$1.56B of Adjusted EBITDA Growth from 2010 – 2014

2010 2011 2012 2013 2014 $5.0

$5.5

$6.0

$6.5

$7.0

$7.5

$8.0

$5.87$6.06

$6.53 $6.57

$7.43Adjusted EBITDA (in Billions)

Adjusted EBITDA (in Billions)

55

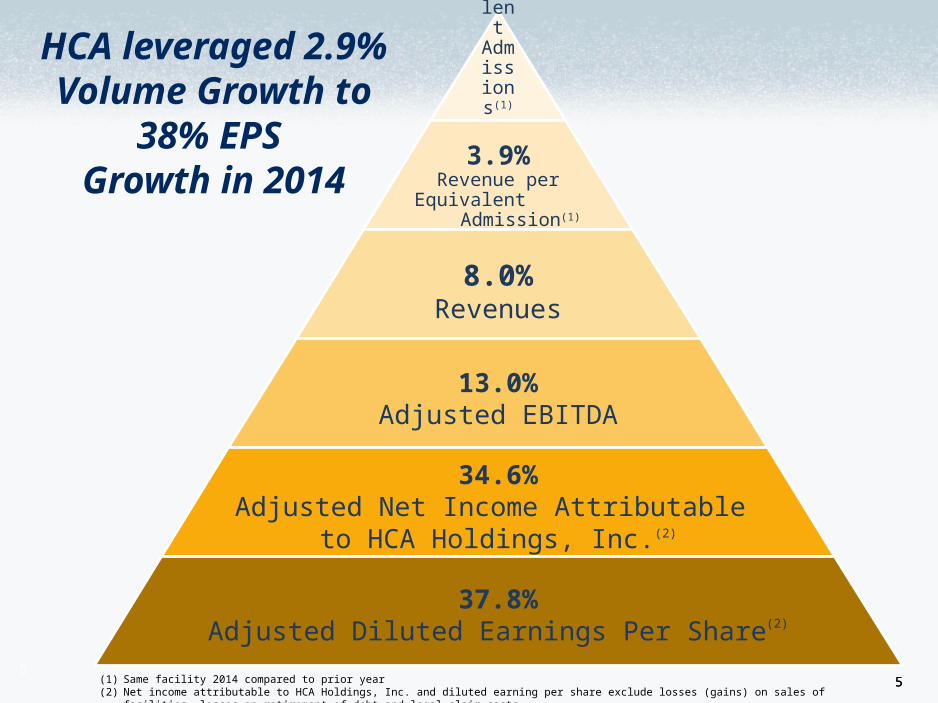

5

2.9%Equivalent

Admissions(1)

3.9%Revenue per

Equivalent Admission(1)

8.0%Revenues

13.0%Adjusted EBITDA

34.6%Adjusted Net Income Attributable

to HCA Holdings, Inc.(2)

37.8%Adjusted Diluted Earnings Per Share(2)

(1) Same facility 2014 compared to prior year(2) Net income attributable to HCA Holdings, Inc. and diluted earning per share exclude losses (gains) on sales of facilities, losses on retirement of debt and legal claim costs.

HCA leveraged 2.9% Volume Growth to

38% EPS Growth in 2014

66

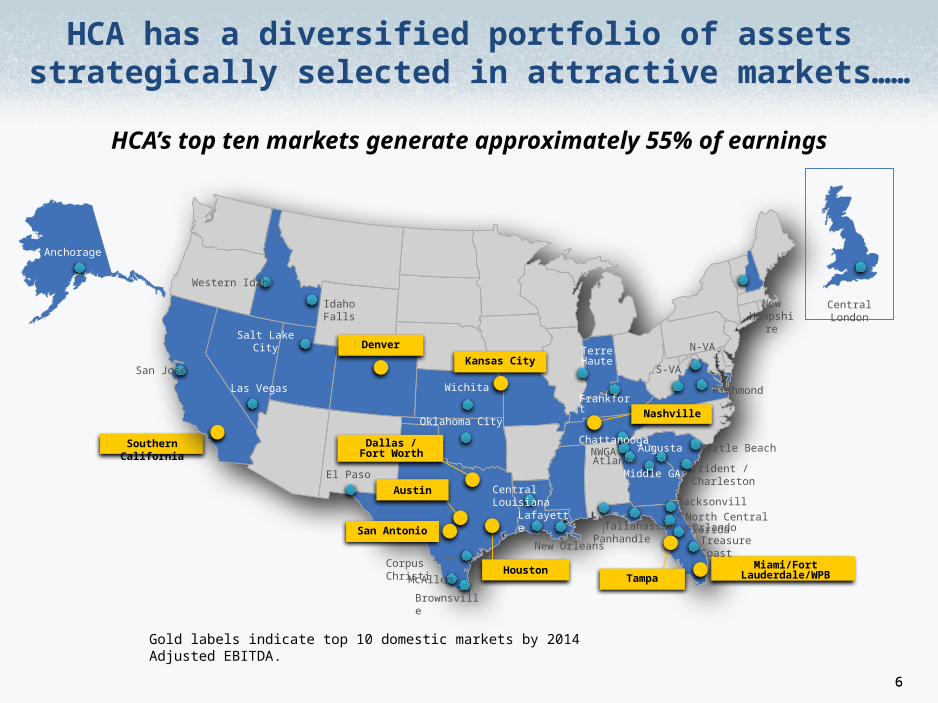

HCA has a diversified portfolio of assets strategically selected in attractive markets……

Salt Lake City Denver

Kansas City

Miami/Fort Lauderdale/WPB

Dallas /Fort Worth

San Antonio

New Hampshire

Western Idaho

San Jose

Southern California

Las Vegas

Idaho Falls

Myrtle Beach

Trident / Charleston

JacksonvilleNorth Central Florida

OrlandoTreasure Coast

N-VA

Richmond

S-VA

Augusta

Tallahassee

Wichita

Oklahoma City

Central Louisiana

Lafayette

New OrleansPanhandle

El Paso

Corpus Christi

McAllen

Brownsville

TerreHaute

Frankfort

ChattanoogaNWGAAtlanta

Middle GA

Anchorage

Nashville

HoustonTampa

Austin

Central London

Gold labels indicate top 10 domestic markets by 2014 Adjusted EBITDA.

HCA’s top ten markets generate approximately 55% of earnings

77

7

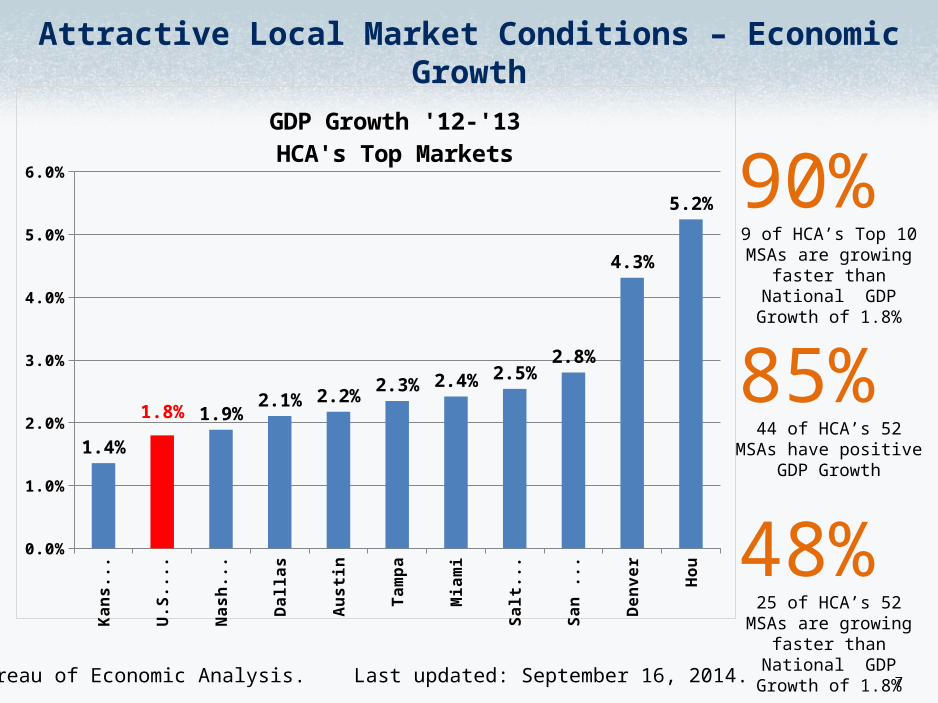

Attractive Local Market Conditions – Economic Growth

Source: Bureau of Economic Analysis. Last updated: September 16, 2014.

90% 9 of HCA’s Top 10 MSAs are

growing faster than National GDP Growth of

1.8%

85% 44 of HCA’s 52 MSAs have

positive GDP Growth

48% 25 of HCA’s 52 MSAs are

growing faster than National GDP Growth of

1.8%Kans

as ..

.

U.S

. GD

P

Nas

hvill

e

Dal

las

Aus

tin

Tam

pa

Mia

mi

Salt

Lak

e

San

An.

..

Den

ver

Hou

ston

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1.4%

1.8% 1.9%2.1% 2.2% 2.3% 2.4% 2.5%

2.8%

4.3%

5.2%

GDP Growth '12-'13HCA's Top Markets

88

Salt Lake City Denver

Kansas City

Miami/Fort Lauderdale/WPB

Dallas /Fort Worth

San Antonio

New Hampshire

Western Idaho

San Jose

Southern California

Las Vegas

Idaho Falls

Myrtle Beach

Trident / Charleston

JacksonvilleNorth Central Florida

OrlandoTreasure Coast

N-VA

Richmond

S-VA

Augusta

Tallahassee

Wichita

Oklahoma City

Central Louisiana

Lafayette

New OrleansPanhandle

El Paso

Corpus Christi

McAllen

Brownsville

TerreHaute

Frankfort

ChattanoogaNWGAAtlanta

Middle GA

Anchorage

Nashville

HoustonTampa

Austin

Central London

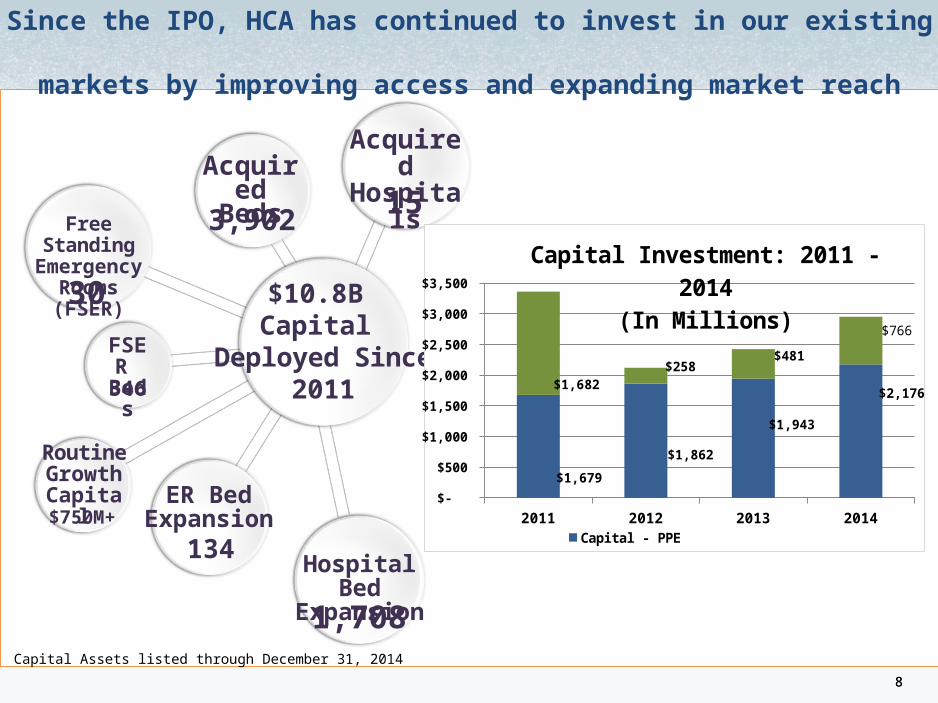

Since the IPO, HCA has continued to invest in our existing markets by improving access and expanding market reach

Acquired Hospitals

Free Standing Emergency

Rooms (FSER)

15

$10.8B Capital

Deployed Since2011

30

AcquiredBeds3,902

FSER Beds346

ER Bed Expansion

134

Routine Growth Capital$750M+

Hospital Bed Expansion1,708

2011 2012 2013 2014 $-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$1,679

$1,862

$1,943

$2,176 $1,682

$258 $481

$766

Capital Investment: 2011 - 2014(In Millions)

Capital - PPE Capital - Acquisitions

Capital Assets listed through December 31, 2014

99

HCA’s Sustainable Growth Agenda

“Be the Preferred Provider System in the Market”

Industry leading quality and service

Profitable growth through distinctive MD and patient relationships and value

Efficiency levels that continue to lead the industry

A well-informed response to evolving market environment

Unparalleled development of future leaders

1010

10

Industry leading quality and service

Setting the Standard for Clinical Excellence in Support of HCA’s Strategic Agenda

o Create Patient-Centered Care Models

o Reduce Variation in Care Delivery

o Deliver Industry-Leading Outcomes

o Set Industry Standards for Care Delivery

o Support and Engage Clinicians

o Deploy Best-in-Class IT Tools

o Gain External Affirmation

Generating Value for:

Informed consumers with high deductible health plans

Physicians seeking high quality, efficient places to practice

Payers desiring innovative collaboration

Employers managing benefit costs

1111

11

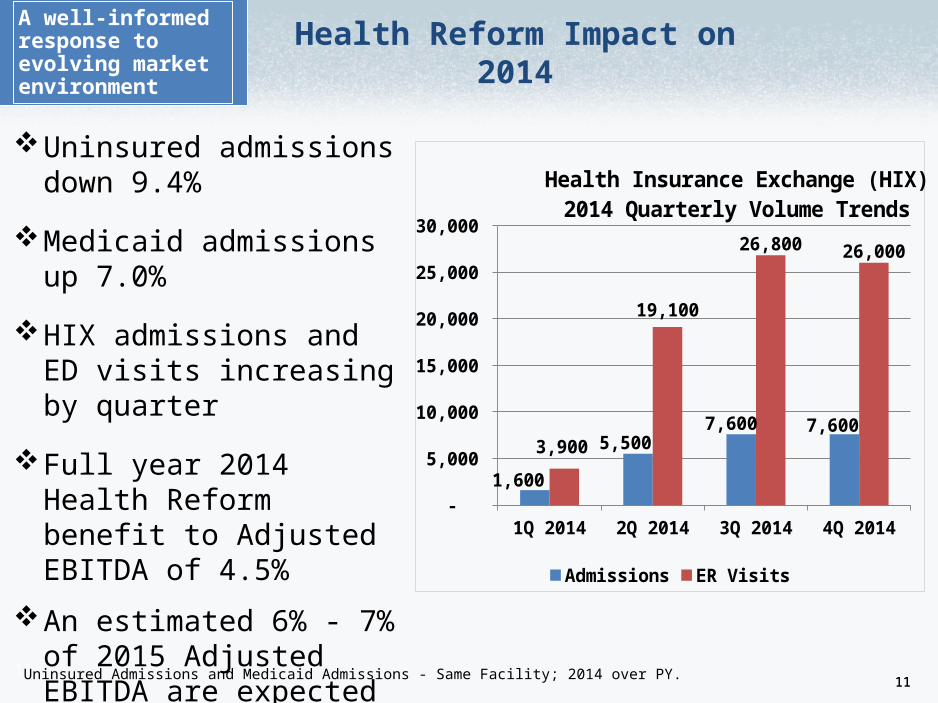

Health Reform Impact on 2014

Uninsured admissions down 9.4%

Medicaid admissions up 7.0%

HIX admissions and ED visits increasing by quarter

Full year 2014 Health Reform benefit to Adjusted EBITDA of 4.5%

An estimated 6% - 7% of 2015 Adjusted EBITDA are expected to be related to the benefits of health reform

A well-informed response to evolving market environment

Uninsured Admissions and Medicaid Admissions - Same Facility; 2014 over PY.

1Q 2014 2Q 2014 3Q 2014 4Q 2014 -

5,000

10,000

15,000

20,000

25,000

30,000

1,600

5,500 7,600 7,600

3,900

19,100

26,800 26,000

Health Insurance Exchange (HIX)2014 Quarterly Volume Trends

Admissions ER Visits

1212

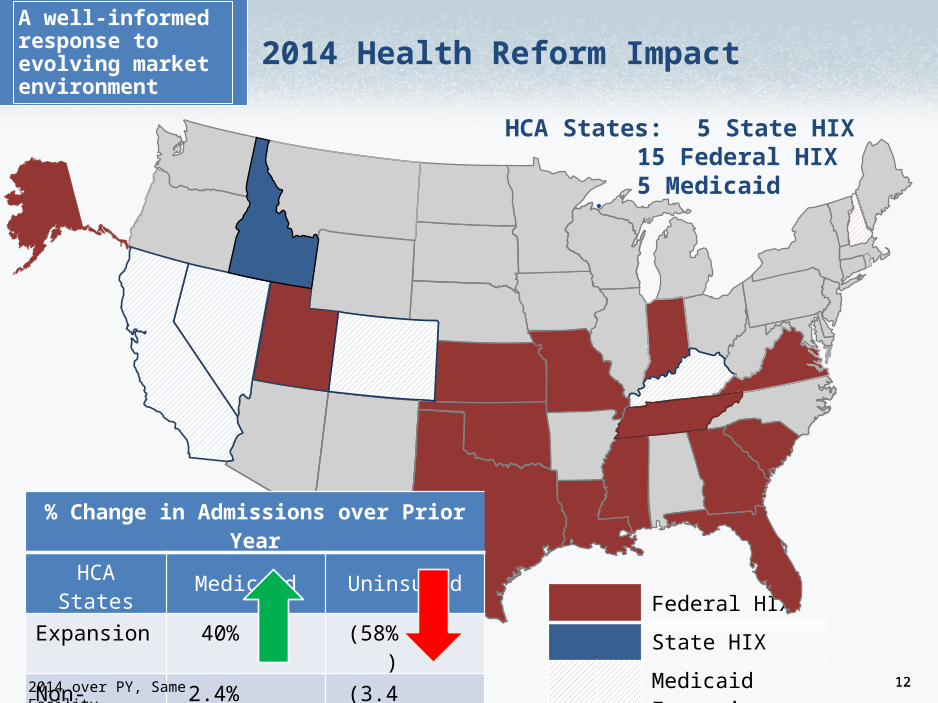

HCA States: 5 State HIX 15 Federal HIX

5 Medicaid Expansion

Federal HIX

State HIX

Medicaid Expansion

A well-informed response to evolving market environment

2014 Health Reform Impact

% Change in Admissions over Prior Year

HCA States Medicaid Uninsured

Expansion 40% (58%)

Non-Expansion 2.4% (3.4%)

All 7.0% (9.4%)

2014 over PY, Same Facility

1313

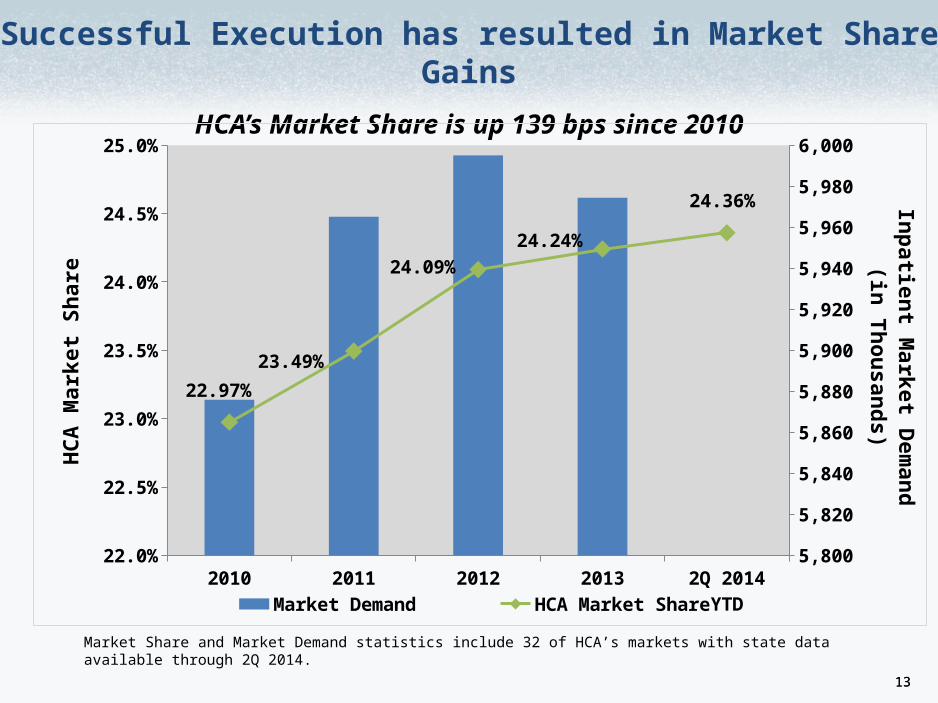

Successful Execution has resulted in Market Share Gains

HCA’s Market Share is up 139 bps since 2010

Market Share and Market Demand statistics include 32 of HCA’s markets with state data available through 2Q 2014.

2010 2011 2012 2013 2Q 2014 YTD5,800

5,820

5,840

5,860

5,880

5,900

5,920

5,940

5,960

5,980

6,000

22.0%

22.5%

23.0%

23.5%

24.0%

24.5%

25.0%

22.97%

23.49%

24.09%24.24%

24.36%

Market Demand HCA Market Share

Inpatient Market Dem

and(in Thousands)

HCA

Mar

ket S

hare

1414

Equivalent Admissions and Emergency Room Visits

Consistent Volume Growth2014 % Change

Equivalent Admits: 4.0%ER Visits: 6.9%

2010 2011 2012 2013 20140

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

2,468,400 2,595,900 2,832,100 2,844,700 2,958,700

5,706,200 6,143

6,912,000 6,968,100 7,450,700

Equivalent Admissions ER Visits

1515

Acquisitions

Cash Flow from Operations

Capital Expenditures

Special Dividends

Share Repurchases1

$15.3 B

$7.3 B

$3.2 B

$3.2B

$3.8B

Cash Flow Trends from March 2011 IPO through 2014

1 Share repurchases does not include newly announced $1B share repurchase in February 2015

1616

What Differentiates HCA

Local Market Strategy & Execution

Culture and Values

Clinical Excellence

Market Diversification

Capital Deployment

Size and Scale

Raymond James36th Annual Institutional Investors ConferenceBill Rutherford CFO and Executive Vice PresidentDr. Ravi Chari Senior Vice President, Clinical ExcellenceMark Kimbrough Vice President, Investor Relations

March 3, 2015, Orlando, FL