raising your first $1mm to $5mm a view from both sides of the table

TRANSCRIPT

What You’re Really Asking When You Raise Your Seed

> Knowledge = Better decisions to finance your startup

Why We’re Here

My Path

Badge #244 for 7 years, 1st Ex Pat in Europe

Mentor was Vin Prothro - 31%, 30%, 15%….

Rod Canion advice on first 10 employees + conflict

Early Angie’s List - Funded by Austin Ventures, Fremont Ventures & Silicon Valley Bank. Sold to NYSE:OC

Private Client Investment Advisor with > $500mm AUM Mostly Alternative Assets like Venture, Hedge Funds

Makes business networking easier, raised $6.5mm fromView Capital, Kayne Anderson, Romano, Gore, Forehand…

Founder

Typical Entrepreneur Before Fund Raising Starts

After 6+ Months Of Rejection

Entrepreneurship Is A Lot More This

=

Than This!

The undertaking of a business enterprise with a complete, total,

utter lack of respect of the resources you currently control!

My Definition Of Entrepreneurship

Entrepreneurship is not easy

You Must Be Passionate, Very Passionate

Alternative Investment Industry @ 30,000 feet

Understanding The Fundraising Landscape - Let’s Start With The Money Sources

Asset Allocation - Drives 94% of returns

Alternative asset class - Venture is a very small subset

PE / Hedge Fund / Collectables

Fund of Funds (FoF)

Non Correlation

Yield

Investment Consultants / Cambridge Associates

David Swenson “Yale Model” Pioneering Portfolio Management

Pensions / Endowments / Sovereign Funds

Banker / iBanker

Denominator problem - post 2008

.5-5% Fee & 0-44% Carry (2&20 is common but still rich)

A Few Allocator Terms

More Terms

So, a GP takes OPM from LPs and charges a Management Fee to allocate to PCs after Calling funds for Seed/A/B/C+

rounds so they can generate an IPO or M&A Exit to take their Carry….then raise their next fund…

More Terms

So, a GP, takes OPM from LPs and charges a Management Fee to allocate to PCs after Calling funds for Seed/A/B/C+

rounds so they can generate an IPO or M&A Exit to take their Carry….then raise their next fund…

all so they can buy their 3rd vineyard!

Investors Play in Specific Stages

B C D E

Venture StageBurning cash

Hit or Miss (VC)

Growth StageReinvesting cash

Premium value (IPO)

MatureExcess cash flow

Not growth or value

Fading WinnerCareful with cashValue play (LBOs)

Forced ChangeInsufficient cash

Deep discount (Vulture)

Cost of Capital

Retu

rn o

n In

vest

men

t

“Left-Side” “Right-Side”

An Investor’s Perspective of Company Life Cycles

A

B C D E

Venture StageBurning cash

Hit or Miss (VC)

Growth StageReinvesting cash

Premium value (IPO)

MatureExcess cash flow

Not growth or value

Fading WinnerCareful with cashValue play (LBOs)

Forced ChangeInsufficient cash

Deep discount (Vulture)

Cost of Capital

Retu

rn o

n In

vest

men

t Microsoft

Intel

Dell

Yahoo

Salesforce

“Left-Side” “Right-Side”

RadioShack

An Investor’s Perspective of Company Life Cycles

A

B C D E

Venture StageBurning cash

Hit or Miss (VC)

Growth StageReinvesting cash

Premium value (IPO)

MatureExcess cash flow

Not growth or value

Fading WinnerCareful with cashValue play (LBOs)

Forced ChangeInsufficient cash

Deep discount (Vulture)

Cost of Capital

Retu

rn o

n In

vest

men

t Microsoft

Intel

Dell

Yahoo

Salesforce

Equity market system set up to unlock the

value of Stage B growth stories

VCs exist to feed left-side demand

Market tends to be critical, even hostile to companies outside its Stage B sweet

spot

PEs exist to exploit right-side discounts and cash

flows

“Left-Side” “Right-Side”

RadioShack

An Investor’s Perspective of Company Life Cycles

A

Venture Capital Firm

(General Partner)

Limited Partners (Investors) (public pension funds, corporate pension funds, insurance companies, high net-worth individuals, family offices, endowments, foundations,

fund-of-funds, sovereign wealth funds, etc)

Ownership of the Fund

Fund / Investment Management

Investment Investment Investment

Venture Capital Fund (Limited Partnership)

The Fund’s ownership of the portfolio investments

Generic Venture Capital / PE Firm Structure

Venture Capital Is A Stressed Industry

Barbell Market Forming

A Shrinking Market in the Middle

Large VCs Getting Larger

More Angels and Micro Funds

Record Size Fund From NEA

Rise In Earliest Stage Investors

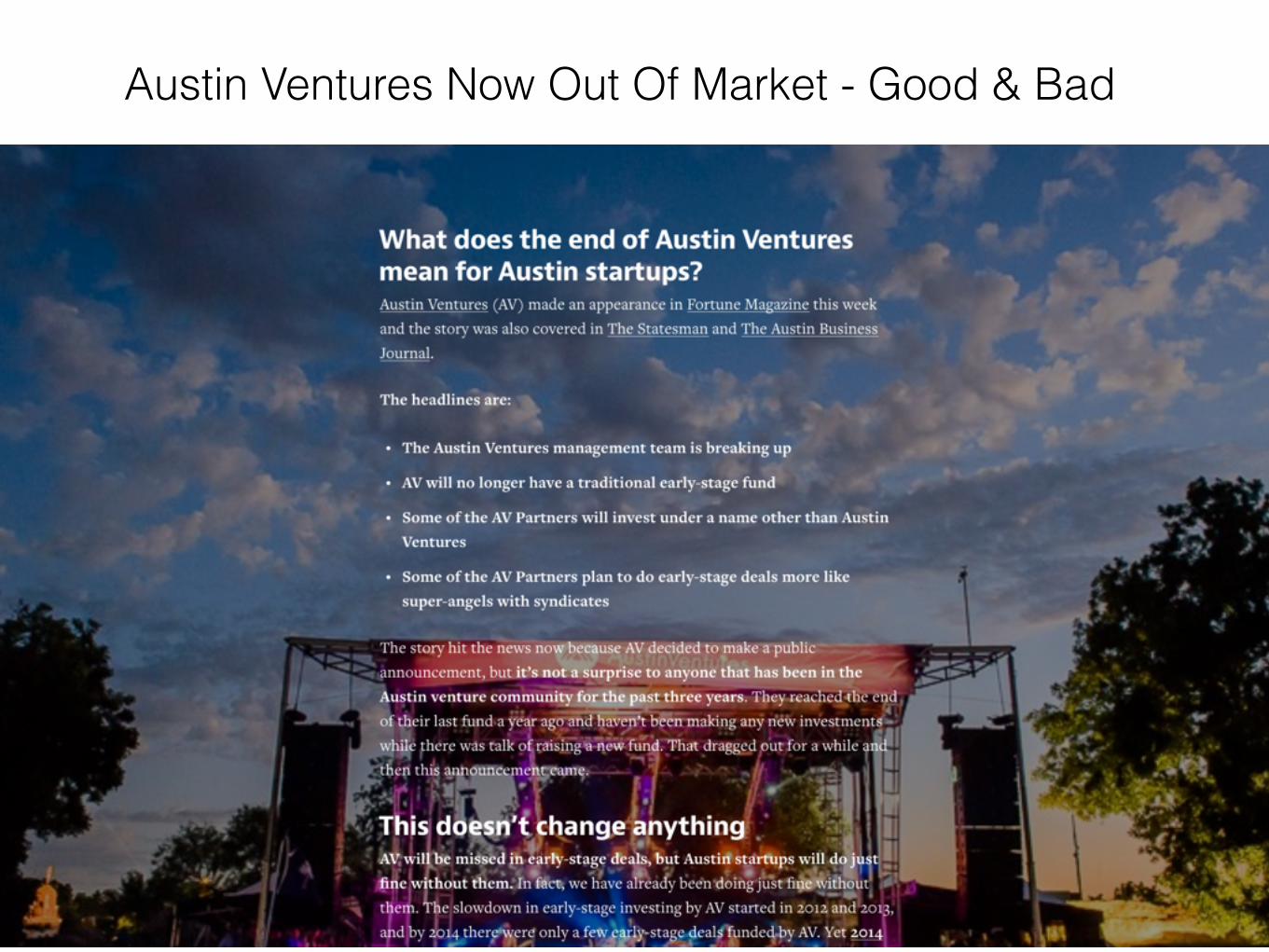

Austin Ventures Now Out Of Market - Good & Bad

Raising Early Stage Funds @ 30,000 feet

Understanding The Fundraising Landscape - Now Let’s Spend Time On Entrepreneurs

Fiduciary ~Ship Captain

Traction - Speaks louder than words, it yells in fact Term sheet

Details are another presentation

Debt Secured debt Convertible debt

Equity Preferred Equity Common Equity

Founders Shares

Warrants

Option Pool / Vesting / Cliff

Sample Entrepreneur Terms

Fiduciary ~Ship Captain

Traction - Speaks louder than words, it yells in fact Term sheet

Not going to discuss term sheets in detail as that is another detailed presentation

Debt Secured debt Convertible debt

Equity Preferred Equity Common Equity

Founders Shares

Warrants

Option Pool / Vesting / Cliff

Sample Entrepreneur Terms

Capital Stack

Capitalization Table (Cap Table)

Accredited Investor $1mm, $200k / $300k (J.O.B.S Act will help here)

Due Diligence (DD)

LTV / CaC

Burn Rate

Fume Date

Sample Entrepreneur Terms

A Superior Plan Of Attack Increases Odds for Success

1) Vision of how the future > today

2) State a significant problem Pain killer > vitamin

3) How you solve that problem

4) How you will generate an unfair competitive advantage

5) Market opportunity Remember my Vin Prothro comment on 31%, 30%, 15%?

6) Qualifications of the team

7) Money needed & milestones to achieve

Use the “west coast fund raising offense” and focus your efforts on the

highest % investors. The others are typically a waste of time.

7 Things Before You Pitch

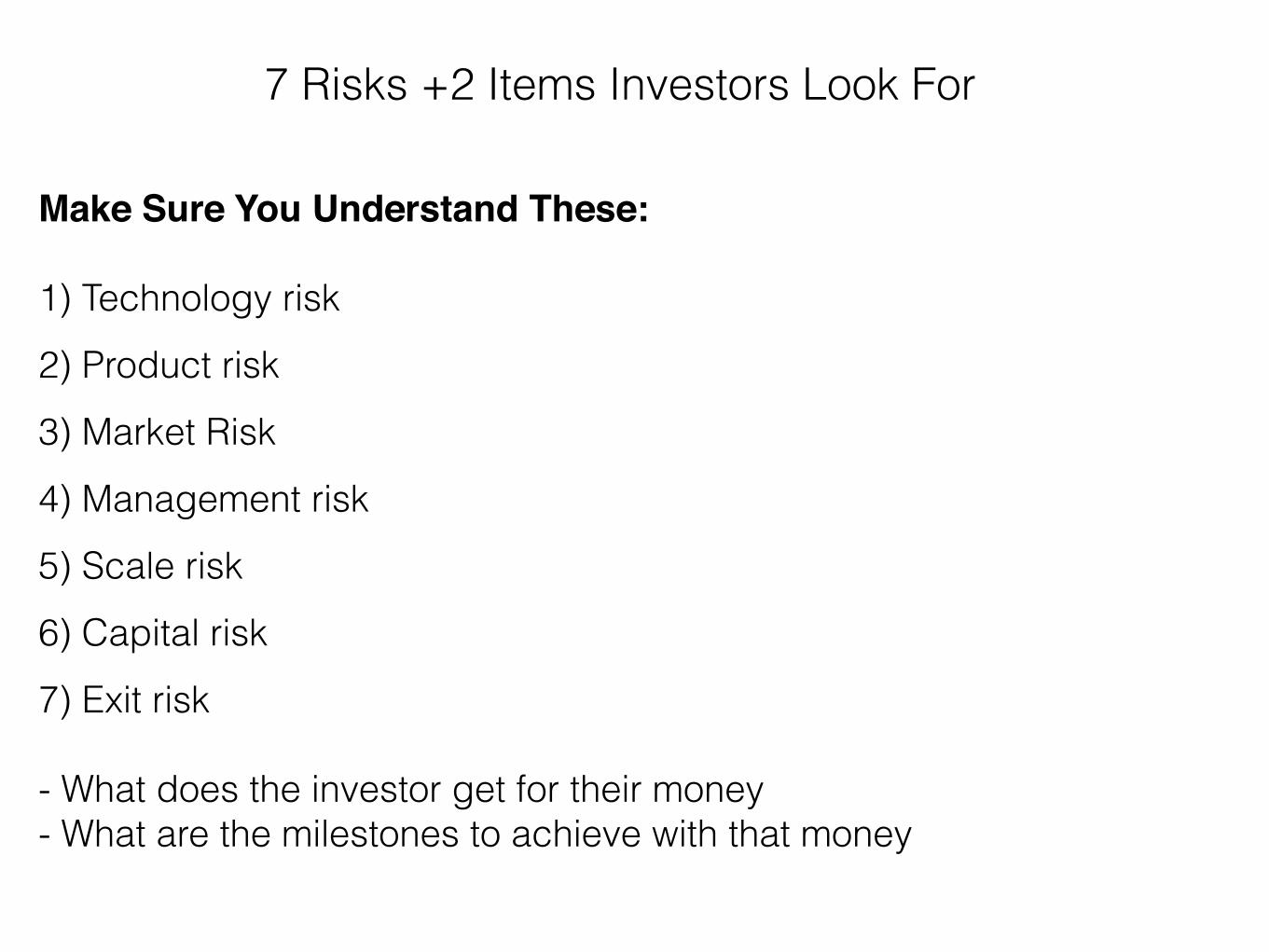

Make Sure You Understand These: 1) Technology risk

2) Product risk

3) Market Risk

4) Management risk

5) Scale risk

6) Capital risk

7) Exit risk

- What does the investor get for their money - What are the milestones to achieve with that money

7 Risks +2 Items Investors Look For

SEED STAGE:

Your own money (keep your burn low, consulting)

“ MCI Round”

Angels

MicroVC

FO = Family Office

MFO = Multi Family Office

Venture Fund (Be wary of Seed spread allocations)

Equity and Debt Crowdfunding (J.O.B.S Act)

Product based Crowdfunding (e.g. Kickstarter)

Gov programs, SBIC, SBA loans/grants DBE (disadvantaged business enterprise) Minority Owned, Veteran Owned, Service Disabled Veteran Owned

Options To Finance Your Business

“Venture capital is not the most risk-taking part of the equation. We VCs wait until things are more developed” says Wilson. “I trust angels I know and the early legwork and diligence they do. I don’t know where ‘lazy’ comes from. They’re probably the most important part of the capital stack because they believe in entrepreneurs before VCs do.”

– Fred Wilson

Importance Of Respected Angels

LATER STAGE = New Options

Later stage venture

PE / Growth equity firm

Hedge funds (relatively new and not always good for venture)

Investment banks (esp if they see a public exit)

Mutual funds (only for mega hits)

Royalty funds

Options To Finance Your Business

Worry Less About Valuation And More About Investor Fit

Business Goal = Sustainable Business Model + Exit

Business Goal = Sustainable Business Model + Exit

But Only Fools Focus On The Exit

Business Goal = Sustainable Business Model + Exit

But Only Fools Focus On The Exit

Superior Execution = More Liquidity Options

.000006 chance to build a $1b in revenue business

Business Goal = Sustainable Business Model + Exit

But Only Fools Focus On The Exit

Superior Execution = More Liquidity Options

Self Harvest - What Great Family Dynasties Are Built On

Mergers & Acquisition “M&A”

Initial Public Offering “IPO”

SecondMarkets / SharesPost (now NASDAQ Private Market)

ESO Funds

“ReCap” (e.g. SurveyMonkey exit)

“Acquihire” = no bueno, but last alternative before wind down or “BK”

Right Exit Is What YOU Want For Your Business

When Raising Funds CEOs Balance A Lot

StartUps Can Be Controlled Chaos

Tips For Finding the Right Investor Marriage

Don’t ask for money until you’ve left your job Unless from mom and dad

Don’t get excited about a VC taking a meeting - it is their job Qualify them and don’t waste YOUR time

Introductions are critical, esp the right one Portfolio company CEOs make great introductions

Check your emotion when you see the Caller ID My approach to mentors vs. advisors

Hints, Not Rules

$500k is the old $5mm - part of MicroVC rise, AWS

NDAs - no real investor will sign one except for some corporates

Pro forma P&Ls

People who say they can help you raise money are generally WOTs

Hints, Not Rules

A Taxi Driver Can Have a Great Idea It Is Mostly About The Team, Market & Idea Execution

This team did pretty well

An MVP, Especially with Traction, Helps Tremendously

The Best Businesses Build Unfair Competitive Advantages

Don’t Go Down Alley Of Unimportant Things

Successful Businesses Can Start Anywhere

First Office in Menlo Park, CA

Questions to Ask Angels, FOs, MFOs

How many deals have you done in the last year? Market, stage, geography

3 Reasons why investing in highest risk stage Generally less for returns than other reasons

Call CEOs of 3 deals that went south on them Did they flee the foxhole or keep fighting

How involved or uninvolved do you want to be?

How can you help me the most?

Sample Qualification Questions to Avoid Dr No

Questions to Ask Funds

How many deals have you done in the last year? Market, stage, geography

How do you pitch your LPs on your unique value? Why will you add more value to my business than the other funds? What vintage fund is it + how much is left for new investments? How carry is allocated? Equal % among GPs or Not?

Helps you understand who’s really on your team Call CEOs of 3 deals that went south on them

Did they flee the foxhole or keep reasonably fighting

Sample Qualification Questions to Avoid Dr No

1. A Great One-LinerThink of it as your elevator pitch… in one sentence.It’s a hybrid of:

- Your product / vision - Your company purpose- A starting point for the pitch

Common framework: “We are X for Y”* *assuming X is attractive and Y is a big enough opportunity!

2. Know Your Audience

Before crafting a pitch deck, understand:- Who you are meeting with?- What is the investor’s and the firm’s focus?- Are there related investments?- How much time do you have?

These influence your deck, the discussion and likely questions you’ll be asked.

3. 10-15 Slides

The deck is important... But the conversation is more important.Budget your time accordingly. Allow for discussion alongside each slide.

10-15 slides. Max. Will provide suggested structure later in deck

4. Beware the Demo

For early stage companies, it’s all about product.And the best mark of product is market validation.Demos are great… but remember these four rules:

1. Be careful of time.2. Don’t get lost in product.3. Have backup if (when!) something goes wrong.4. Give even weight to product & traction / data.

5. Expect the Deck to be Shared

Whether you like it or not (!),your deck will be shared (i.e. among partnership).Goal: be equally compelling with/without voiceover.

How?- deck should tell its own story.- do *not* rely on builds, intricate slides.- make the file size manageable for email.- PDF or secure URL are great alternatives to PPT.

Go Ugly Early And Ask The Hard Questions - A Delicate Balance, But Respect Their Time & YOURS!

When raising private equity (VC), always remember a VC is a political animal trapped inside a limited partnership.

- On a hot streak or a cold streak - Always wanting to be the one to find the next big deal - Always worried they’ll be embarrassed in partner meeting

Mitigate that risk for them and they will work on being your sponsor

It takes an average of 21 months for established entrepreneurs to secure VC funding compared to 37 months for first-timers

Always Remember The Politics

Some Investors Can Be a Boil On The Ass of Progress

Introductions From Trusted Associates?

A True Fund Raising Story

David

David

Can I Trust a Social Media Footprint?

Fake David

Fake David Never Worked For Soros Or Samsung Family Office

Fake David

But Did Make An Interesting Introduction

Fake David

Family is now a Who@ Investor

=

Transparency + Trust Helped Turn a Lemmon Into Lemonade

Fred Wilson of Union Square Ventures http://avc.com/

Mark Suster http://www.bothsidesofthetable.com/

Brad Feld http://www.feld.com/

Bill Gurley http://abovethecrowd.com/

Ben Horowitz http://www.bhorowitz.com/ (The Hard Thing about Hard Things)

First Round Review http://firstround.com/review/

Naval & Babak from AngelList http://venturehacks.com/

Steve Blank, Lean StartUp http://steveblank.com/

Eric Reis, Lean StartUp http://www.startuplessonslearned.com/

Blogs to Read and Learn Much More

Lastly, Entrepreneurship Explained In A 3 Minute Dance Video

Want This Deck Or Access To My Evernote Advice Folder?

follow me on Twitter@leeblaylock

& email me at [email protected]