rabodirect financial health barometer

TRANSCRIPT

RaboDirect Financial Health Barometer A Five-Year Review

1

About the white paper

RaboDirect Financial Health Barometer – A Five-Year Review

RaboDirect’s annual Financial Health Barometer delivers a comprehensive overview of Aussies’ attitudes towards their financial health.

Each year the survey records the attitudes of more than 2,000 financial decision makers aged between 18 and 65. Results are weighted by gender, age and location, according to statistics from the Australian Bureau of Statistics. The survey is conducted in order to empower Aussies to better understand and improve their financial situation.

This white paper is a longitudinal report into the key insights from RaboDirect’s Financial Health Barometer over five years, covering results from 2011 – 2015. This is the first time that a retrospective look at the findings has been undertaken since the survey started in 2010.

financial decisions makers over 5 years

10,000Aged between 18 and 65

While Aussies know that they have to save for a comfortable retirement or a rainy day, their attitudes towards saving and financial wellbeing are changing. Sentiment is driven by a range of factors including the perceived health of the national and global economy, wage growth and fluctuations in the local cash rate. Also, how financially literate a person is affects the way they think and feel about their financial health. Frankly, there’s much to weigh up and balance out.

At RaboDirect we’ve documented the changing attitudes of Aussies to their financial health, through our annual Financial Health Barometer survey. The RaboDirect Financial Health Barometer – A Five-Year Review, is the first retrospective look at findings providing fascinating insight into the financial behaviour of Australian consumers over the last five years.

The white paper uncovers how people’s confidence in their savings and their financial settings can shift in response to changing economic conditions. It explores the use of financial advice, consumers’ opinions of the advice industry, their expectations of retirement savings, and their confidence – or lack thereof – in money matters.

The research shows that as a whole, Aussies have become less confident and less engaged with their finances.

The results profile Baby Boomers as the least financially confident and engaged generation, while on a gender basis, women continue to have less than men in retirement savings and aren’t as confident when it comes to their overall finances.

Concerningly, expectations about how much people plan to have in their super accounts when they retire has fallen over time. The research found that in 2014 Baby Boomers said they expected to have $452,310 falling to $309,077 in 2015.

Confidence in the financial advice process is also slipping. In 2015, 29 per cent of respondents agreed or strongly agreed that they trusted financial advice down from 40 per cent in 2014. The average score across the five years was 31 per cent.

What’s more, almost twice the number of people now think that advice is “only for the wealthy,” compared to when the survey was done in 2012 (28 per cent versus 17 per cent).

Introduction RaboDirect Financial Health Barometer – A Five-Year Review

So are Aussies really losing interest in their finances and applying less sense to their dollars and cents? If so, the implications could go far beyond having a smaller savings balance. A growing disinterest with finance could lead to falling levels of prosperity, potentially impacting Australians’ health and wellbeing, their quality of life in retirement and overall happiness. And that can’t be a good thing.

Through laying out these trends, this white paper highlights a growing need to reinvigorate Aussies’ confidence in and energy around their finances to help make the most out of every dollar they have, so they can make the most out of life.

The following section provides the evidence; the ‘meat’ that substantiates our insights and conclusions. It’s a comparative and detailed analysis of RaboDirect’s Financial Health Barometer over the past five years, covering:

• Superannuation and retirement expectations• Attitudes towards financial advice• Consumer confidence

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015

4%

13%

29%

39%

15%

3%

14%

24%

40%

18%

4%

15%

29%

37%

15%

5%

18%

27%

37%

12%

8%

20%

35%

27%

10%

Please indicate the extent to which you agree or disagree with each of the following statements

“Financial planning is only important for those who have a lot of money”

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

2

Behind the family home, superannuation remains Australians’ most valuable asset. Often the reality of how much people have in their super, versus the perception of how much they think they’ll need, is an indicator of how financially informed they are. The research shows that over the five years, expectations about how much is needed to retire has tumbled, with fewer Australians going above and beyond to grow their super nest egg.

On average, the number of people making voluntary superannuation contributions fell between 2013 and 2015, particularly among the Gen X and Baby Boomer groups. In 2014, 33 per cent of Gen X and 27 per cent of Baby Boomers had made voluntary contributions: in 2015 these figures fell to 24 per cent and 21 per cent respectively.

The survey continues to show a major difference between male and female super balances in Australia, highlighting the need for women to make additional contributions. However, the research shows that men have consistently contributed more to their super than women. Only one in five (21 per cent) women made voluntary super contributions in 2014 and 2015, compared to more than 30 per cent of men in the same period (37 per cent in 2014 and 31 per cent in 2015).

Superannuation

0%

5%

10%

15%

20%

25%

30%

35%

40%

Male Female Total

37%

32% 31%

21%

26%

21%

29%29%26%

In the last 12 months have you made any voluntary contributions to your superannuation fund(s)?

Yes. By gender

2013 2014 2015

1 An update on the level and distribution of retirement savings, Association of Superannuation Funds, March 20142 ASFA Retirement Standard, June Quarter 2015

(https://www.moneysmart.gov.au/superannuation-and-retirement/how-super-works/super-contributions/how-much-is-enough)

ON THE FLIP SIDE, MORE AND MORE GEN Ys ARE MAKING CONTRIBUTIONS INTO THEIR SUPER, WITH 32 PER CENT MAKING VOLUNTARY CONTRIBUTIONS IN 2015, UP FROM 29 PER CENT IN 2014

What’s worrying, the research shows that the amount Aussies think they’ll have to retire on is below average industry estimates and is declining. ASFA estimates the lump sum needed to support a comfortable lifestyle for a couple is $640,000 (or $545,000 for a single person) assuming a partial Age Pension2.

In 2012, Gen Y expected to retire on $514,798, Gen X expected to retire on $462,444 and Boomers expected to retire on $404,865; by 2015 these figures had fallen by 13 per cent, 8 per cent and 23.5 per cent respectively.

RaboDirect Financial Health Barometer – A Five-Year Review

3

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

Gen Y Gen X TotalBaby Boomers

$486,442

$514,798

$447,776

$569,872

$463,221

$462,444

$423,706

$499,518

$404,865

$309,077

$452,310

$460,759

$470,485

$398,707

$516,658

$436,274

How much do you expect to have in superannuation when you retire?

Average. By generations

2012 2013 2014 2015

In 2015, respondents felt they needed less money to retire on than was the case in previous surveys. We also found that a growing number of Gen Ys believe that employer-funded superannuation will be enough to cover their retirement needs: this proportion increased more than twofold, from 12 per cent in 2011 to 28 per cent in 2015.

Our research shows that in 2012 Gen Y said they’d need $784,421 to retire on, but this figure fell 14 per cent in 2015. Gen X said they’d need $875,253 to retire on in 2012, but only $844,396 in 2015 – a drop of four per cent. In 2015, Boomers indicated they’d need $785,769 to retire on, down 13 per cent from 2012.

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

$1,200,000

Gen Y Gen X TotalBaby Boomers

$1,100,000

$886,286$697,353

$749,291

$784,421

$675,685

$875,253

$844,396

$909,441

$785,768

$907,838

$849,395

$761,481

$829,087

$1,000,184

$932,110

$906,838

How much in total in superannuation would you estimate an average retiree at the age of 65 would need for their retirement until they are 85 years

(for 20 years)?

Average. By generations

2012 2013 2014 2015

The declining perception of how much super is needed to support a comfortable lifestyle in retirement is concerning because the cost of living in Australia is rising, with the country topping Deutsche Bank’s list of the most expensive countries since 20123. As well, investor returns from cash and fixed interest remain subdued, considering the Reserve Bank of Australia’s cash rate has remained at record lows of two per cent since May 2015 after fluctuating between 4 – 2.5 per cent since 2010.

3 Deutsche Bank, 2015, The Random Walk: Mapping the World’s Prices

RaboDirect Financial Health Barometer – A Five-Year Review

4

Financial advice has been in the hot seat in Australia over the period of the white paper review. We’ve seen a string of scandals involving financial advice and the federal government’s Financial System Inquiry (FSI), which proposed the biggest overhaul in the history of the Australian financial system. The FSI and a flurry of related regulatory reviews revealed deep problems with some aspects of our financial system in Australia, and as a result the advice sector had to lift its game and increase its educational and behavioural standards. The results of our five-year review show that these events have coloured the way Aussies view financial advice – and the industry has some way to go to fully retain consumers’ trust.

Advice

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015

6%

29%

32%

26%

7%

10%

33%

30%

23%

5%

10%

36%

30%

19%

3

5%

9%

37%

28%

20%

4

5%

10%

31%

31%

18%

10%

Please indicate the extent to which you agree with the following statements

“I have a long term financial plan”

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

THE GOOD NEWS FROM THE SURVEY IS THAT SINCE 2011, MORE PEOPLE ARE PLANNING FOR THEIR LONG-TERM FINANCIAL FUTURE

But this is not uniform across the generations: while more Gen Y say they have a long term financial plan, the Baby Boomers are increasingly less likely to say the same.

In 2011, 35 per cent of Aussies were planning for their long-term future, with the figure increasing six per cent in 2015 to 41 per cent. However, in recent years this trend has slipped back: in 2014, 46 per cent of people said they had a long-term financial plan.

By generation, less Baby Boomers are planning for their long-term future. In 2014, 51 per cent of Boomers reported that they had a long-term financial plan, but this proportion fell to 37 per cent in 2015. For Gen X in 2014 the number of people with a financial plan was 43 per cent, falling to 38 per cent in 2015; while for Gen Y, 45 per cent of people said they had a financial plan in 2014, which actually increased in 2015, to 48 per cent.

RaboDirect Financial Health Barometer – A Five-Year Review

5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%11%

34%

28%

21%

5%

12%

36%

27%

18%

7%

8%

35%

30%

21%

5%

10%

28%

33%

18%

11%

9 %

28%

33%

18%

11%

2014 2015 2014 2015

8%

43%

27%

18%

4%2014 2015

Gen Y Gen X Baby Boomers

Please indicate the extent to which you agree with the following statements

“I have a long term financial plan” By generations

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

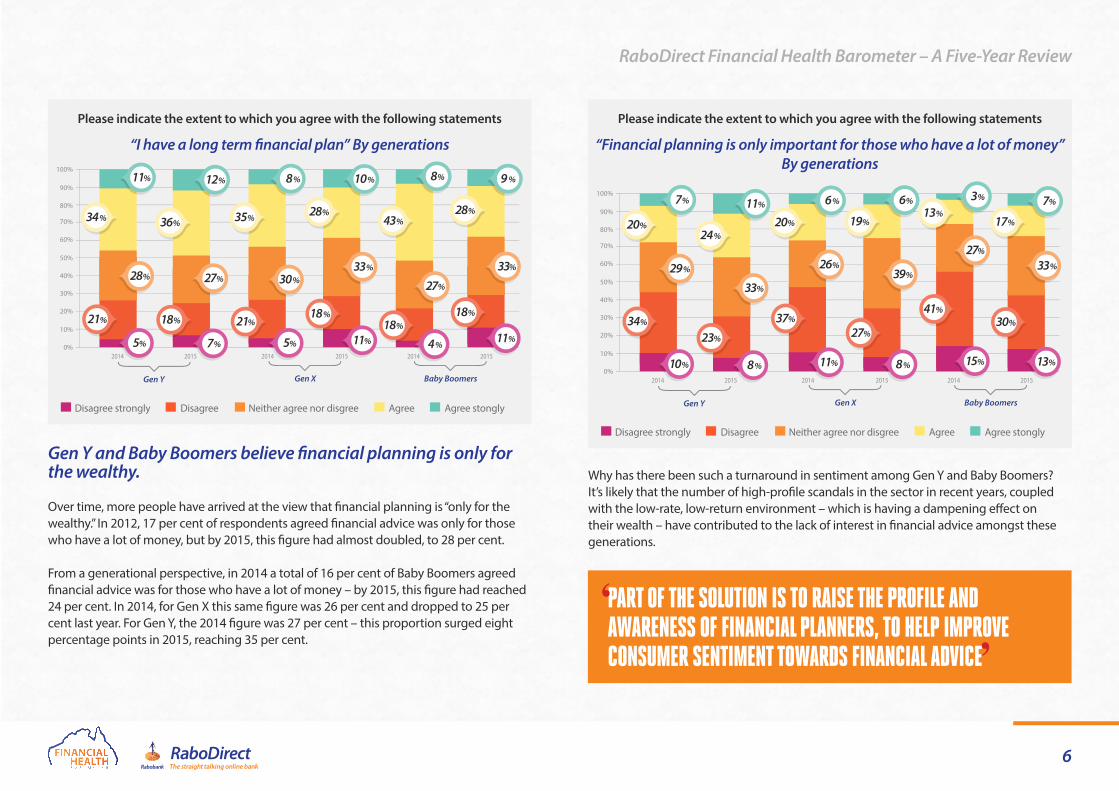

Gen Y and Baby Boomers believe financial planning is only for the wealthy.

Over time, more people have arrived at the view that financial planning is “only for the wealthy.” In 2012, 17 per cent of respondents agreed financial advice was only for those who have a lot of money, but by 2015, this figure had almost doubled, to 28 per cent.

From a generational perspective, in 2014 a total of 16 per cent of Baby Boomers agreed financial advice was for those who have a lot of money – by 2015, this figure had reached 24 per cent. In 2014, for Gen X this same figure was 26 per cent and dropped to 25 per cent last year. For Gen Y, the 2014 figure was 27 per cent – this proportion surged eight percentage points in 2015, reaching 35 per cent.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100% 7%

20%

29%

34%

10%

11%

24%

33%

23%

8%

6%

20%

26%

37%

11%

6%

19%

39%

27%

8%

7%

17%

33%

30%

13%

2014 2015 2014 2015

3%

13%

27%

41%

15%

2014 2015

Gen Y Gen X Baby Boomers

Please indicate the extent to which you agree with the following statements

“Financial planning is only important for those who have a lot of money” By generations

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

Why has there been such a turnaround in sentiment among Gen Y and Baby Boomers? It’s likely that the number of high-profile scandals in the sector in recent years, coupled with the low-rate, low-return environment – which is having a dampening effect on their wealth – have contributed to the lack of interest in financial advice amongst these generations.

PART OF THE SOLUTION IS TO RAISE THE PROFILE AND AWARENESS OF FINANCIAL PLANNERS, TO HELP IMPROVE CONSUMER SENTIMENT TOWARDS FINANCIAL ADVICE

RaboDirect Financial Health Barometer – A Five-Year Review

6

All generations are becoming less trusting of financial advice.

Over the life of the survey there has only been a slight shift in the number of people who distrust financial advice. Yet when looking at yearly comparisons, there was a substantial shift between 2014 and 2015. In 2014, 40 per cent of people said that they trusted financial advice, but in 2015, this figure fell to 29 per cent.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100% 5%

44%

41%

9%2%

8%

31%

48%

10%3%

6%

35%

42%

12%

5%

4%

22%

51%

14%

9%

3%

20%

41%

19%

17%

2014 2015 2014 2015

2%

29%

42%

19%

8%

2014 2015

Gen Y Gen X Baby Boomers

Please indicate the extent to which you agree with the following statements

“I trust the advice from financial advisors and financial planners” By generations

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100% 5%

44%

41%

9%2%

8%

31%

48%

10%3%

6%

35%

42%

12%

5%

4%

22%

51%

14%

9%

3%

20%

41%

19%

17%

2014 2015 2014 2015

2%

29%

42%

19%

8%

2014 2015

Gen Y Gen X Baby Boomers

Please indicate the extent to which you agree with the following statements

“I trust the advice from financial advisors and financial planners” By generations

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

When comparing different generations, although more Gen Ys trust financial advice, there has been a bigger downward trend year-on-year in this group compared to other generations. In 2014, 49 per cent of Gen Y agreed that they trusted advice provided by planners or advisers. In 2015, this figure had dropped ten percentage points to 39 per cent. For Gen X in 2014 this figure was 41 per cent, dropping to 26 per cent in 2015, a change of fifteen percentage points. For Baby Boomers in 2014, the number was 31 per cent, falling to 23 per cent in 2015, a difference of eight percentage points.

40%in 2014

People’s trust of financial services

29%in 2015

falling to

RaboDirect Financial Health Barometer – A Five-Year Review

7

Consumer confidence is fragile at present. The ABS 2015 December quarter figures show the household savings ratio fell to 7.6% from 8.7% in the September 2015 quarter, to levels not seen since before the global financial crisis. Dwelling approvals also fell by 7.5 per cent in January, driven by a 9.1 per cent fall in apartment approvals. On the other hand, spending lifted over the tail end of 2015, providing a boost to December quarter economic growth4.

This patchy outlook is also evident in consumers’ confidence about their finances.

Consumers are becoming less confident about their finances

In general, consumer confidence in their finances is dropping. In 2013, 52 per cent of consumers said they agreed or strongly agreed they were confident with their finances, but by 2015 this figure had fallen to 45 per cent.

In 2013, half Gen Y and Gen X respondents agreed they were confident with their finances, with 59 per cent of Baby Boomers feeling the same.

In 2015, those figures dropped to 46 per cent for Gen Y and Baby Boomers, and 45 per cent for Gen X.

Consumer Confidence

52%in 2013

Consumer confidence in their finances

falling to

had confidence

45%in 2015had confidence

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%9%

41%

27%

19%

4%

9%

37%

33%

16%

6%

7%

43%

29%

17%

4%

8%

37%

36%

14%

5%

9%

37%

34%

14%

6%

2013 2015 2013 2015

12%

47%

25%

12%4%

2013 2015

Gen Y Gen X Baby Boomers

Please indicate the extent to which you agree with the following statements

“I am confident with my finances” By generations

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

4 Australian Bureau of Statistics (ABS) January 2016, Retail Trade and Buildings Figures (http://www.abs.gov.au/AUSSTATS/[email protected]/DetailsPage/5206.0Dec%202015?OpenDocument)

It is likely that Baby Boomers are less confident because of their experience of the financial crisis of 2007/2008, which had a disproportionate impact on their wealth. In keeping with this, Generations Y and X aren’t as pessimistic because retirement is further off, giving them longer to accumulate wealth.

RaboDirect Financial Health Barometer – A Five-Year Review

8

Consumers are less informed about their finances.

The results show that consumers feel increasingly less informed about their finances. In 2011, 55 per cent of people agreed or strongly agreed that they were informed about financial matters, whereas in 2014 this figure was 57 per cent, and by 2015 it was down to 49 per cent.

Surprisingly – given their age and arguably greater experience – Baby Boomers feel they’re the least informed of all generations. In 2014, 61 per cent of Baby Boomers agreed or strongly agreed that they were informed about their finances, but this number fell to 50 per cent last year. In 2014 this figure was 53 per cent for Gen X, decreasing to 45 per cent last year. In 2014, 55 per cent of Gen Y respondents felt well-informed, a proportion that dropped marginally to 52 per cent last year.

This trend can also be seen across the genders, with women feeling increasingly less informed about financial matters compared to men over time. In 2014, 58 per cent of men said they agreed or strongly agreed that they tried to stay informed about financial matters, a number that dropped to 54 per cent last year. For women this figure was 55 per cent in 2014, and 44 per cent in 2015.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%10%

45%

29%

13%2%

10%

42%

33%

10%5%

11%

42%

33%

12%2%

8%

37%

34%

16%

6%

8%

42%

30%

14%

7%

2014 2015 2014 2015

11%

50%

28%

10%1%

2014 2015

Gen Y Gen X Baby Boomers

Please indicate the extent to which you agree with the following statements

“I try to stay informed about money matters and finances” By generations

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

13%

45%

29%

10%2%

11%

43%

31%

10%5%

8%

47%

30%

12%2%

6%

38%

33%

16%

7%

9%

40%

32%

13%

6%2014 2015 2014 2015

11%

46%

30%

11%2%

2014 2015

Male Female Total

Please indicate the extent to which you agree with the following statements

“I try to stay informed about money matters and finances” By gender

Disagree strongly Disagree Neither agree nor disgree Agree Agree stongly

RaboDirect Financial Health Barometer – A Five-Year Review

9

There appears to be a correlation between consumer confidence and the amount consumers regularly save: as consumers’ level of savings have come down, so too have consumers’ confidence. For instance, in 2014 respondents’ average savings in a typical month was $908, a figure that fell to $705 in the 2015 survey. At the same time, in 2014 a total of 49 per cent of consumers agreed or strongly agreed that they were confident with their finances, a number that dropped to 45 per cent in the current survey. The more confident people are about their finances, the more likely they are to actively grow their wealth.

SO THERE IS OPPORTUNITY FOR ALL AUSSIES TO BECOME MORE INFORMED ABOUT THEIR FINANCES TO HELP BOOST THEIR SAVINGS

RaboDirect Financial Health Barometer – A Five-Year Review

10

With research showing that Aussies are becoming increasingly disengaged towards their finances, now is the time to act, to make a real difference not only to savings balances, but also to mindsets. It’s about getting financially fit.

There are important steps consumers can take to change their financial position today:

• #FinancialGoals. A long-term financial plan is about visualising what finances will look like at various intervals of time: five, ten and 25 years from now. This involves deciding where you want to live, how much you’re prepared to live on each year, and the types of debts and assets you would realistically expect to have. A thorough review of your current financial position will help to provide a realistic direction on what is achievable. Assess information such as how much you already have in the retirement kitty, your existing salary, how much you can save each month and your risk appetite. This will help you to develop a tailored financial plan, which should be reviewed regularly to ensure you’re still on track to meeting your long-term goals.

• Pay down debt first. The 2015 Financial Health Barometer discovered that Gen X has the highest level of average debt at $172, 015 above Gen Y ($114, 155) and Baby Boomers ($100, 234), and over half (55%) of us have debts tied up on credit cards. Paying off your debts fast, particularly credit card debit which usually carries a high interest rate, before saving reaps more financial reward.

• Get interested in interest rates. The 2015 Financial Health Barometer research found that 40 per cent of Australians are saving into a transactional account as the main place for their savings – a decision that means that collectively, they’re missing out on $2.3 billion* in potential interest. Making sure you’re getting the best rates available across all of your accounts, and that you’re not paying excessive account-keeping fees, will ensure that your savings plan is packing punch.

• Put a regular savings plan in place. Set up direct debit into a true high interest savings account for a specific amount each payday. Putting any extra cash you have into your savings account rather than leaving it idle in your everyday transaction account will mean you’re earning the best possible interest rate on unused money.

• Make voluntary contributions to super. The amount you decide to contribute will depend on how much disposable income you have. Do a budget and work out how much you can afford to contribute each month. Due to the wonders of compound interest, even a small amount, such as the price of an extra coffee a week, can lead to thousands of dollars in return once you retire. A financial planner or tax consultant can help you understand the tax benefits additional contributions can have.

• Seek independent advice. We wouldn’t expect the Aussie cricket team to embark on its next campaign without reviewing previous performance and asking the coach for advice. Likewise, finding a trusted adviser to offer independent advice can be a crucial element in setting yourself up for financial success. Consider reaching out to an industry body such as the Financial Planning Association, where you can find registered financial planners. Then, book an appointment and arm yourself with details of your financial position, such as your recent tax return and bank statements, and an idea of what you want your financial future to look like. Financial advisers can help with a wide range of tasks, from putting effective savings plans in place to more complex investment strategies.

A healthy financial future is about being passionate about your pennies, no matter what the headlines are saying or how the market is tracking; it’s about being forever committed to achieving your best financial position. While getting ahead financially can feel daunting, you can remain engaged and enthusiastic about your financial goals because the results clearly show the more engaged you are, the better your financial future.

Conclusion

NOW IS THE TIME TO ACT, TO MAKE A REAL DIFFERENCE NOT ONLY TO SAVINGS BALANCES, BUT ALSO TO MINDSETS. IT’S ABOUT GETTING FINANCIALLY FIT

RaboDirect Financial Health Barometer – A Five-Year Review

Read more Financial Health Barometer results and handy tips to get you financially fit VISIT OUR BLOG

* Roy Morgan Single Source, 12 months to April 2015 (n=33,630) Australians aged 14+ years who hold a transaction account

11RaboDirect is a division of Rabobank Australia Limited ABN 50 001 621 129 AFSL no.234700.