question no.1 is compulsory. answer any five...

TRANSCRIPT

1 ME29 / Prime / Final

FLRG Number of Pages : 6 Total Marks: 100 Number of questions: 7 Time Allowed: 3 Hrs

Question No.1 is compulsory. Answer any five out of the remaining questions. Working notes should form part of the answer.

Wherever necessary, suitable assumptions may be made by the candidates.

1. Answer any four of the following:

(a) On 1st December, 2008, Ceebee Construction Co. Ltd. undertook a contract to construct a building for Rs.85 lakhs. On 31st March, 2009 the company found that it had already spent Rs.64, 99,000 on the construction. Prudent estimate of additional cost for completion was Rs.32, 01,000. What amount should be charged to revenue in the final accounts for the year ended 31st

March, 2009 as per provisions of Accounting Standard 7 (Revised)?

(b) While executing a new project, the company had to pay Rs.50 lakhs to the State Government as part of the cost of roads built by the State Government in the vicinity of the project for the purpose of carrying machinery and materials to the project site. The road so built is the property of the State Government. Advise the company on the following item while from the view point of finalization of accounts.

(c) The following details are available in the books of Sun Ltd.,

Particulars

Rs. in lakhs

(a) Provision for tax:

For 2005-2006 200 For 2006-2007 300 For 2007-2008 250

Advance tax paid:

For 2005-2006 175 For 2006-2007 350 For 2007-2008 270

Sun Ltd. estimates its Deferred Tax Liabilities to be Rs.100 lakhs and its Deferred. Tax Assets to be Rs.20 lakhs. How will the above be disclosed?

(d) Global Ltd. is showing an intangible asset at Rs.72 lakhs as on 01.04.2007 and that item

was required for Rs.96 lakhs on 01.04.2004 and that item was available for use from that date. Global Ltd. has been following the policy of amortization of the intangible asset over a period of 12 years on straight line basis. Comment on the accounting treatment of the above with reference to relevant accounting standard.

2 ME29 / Prime / Final

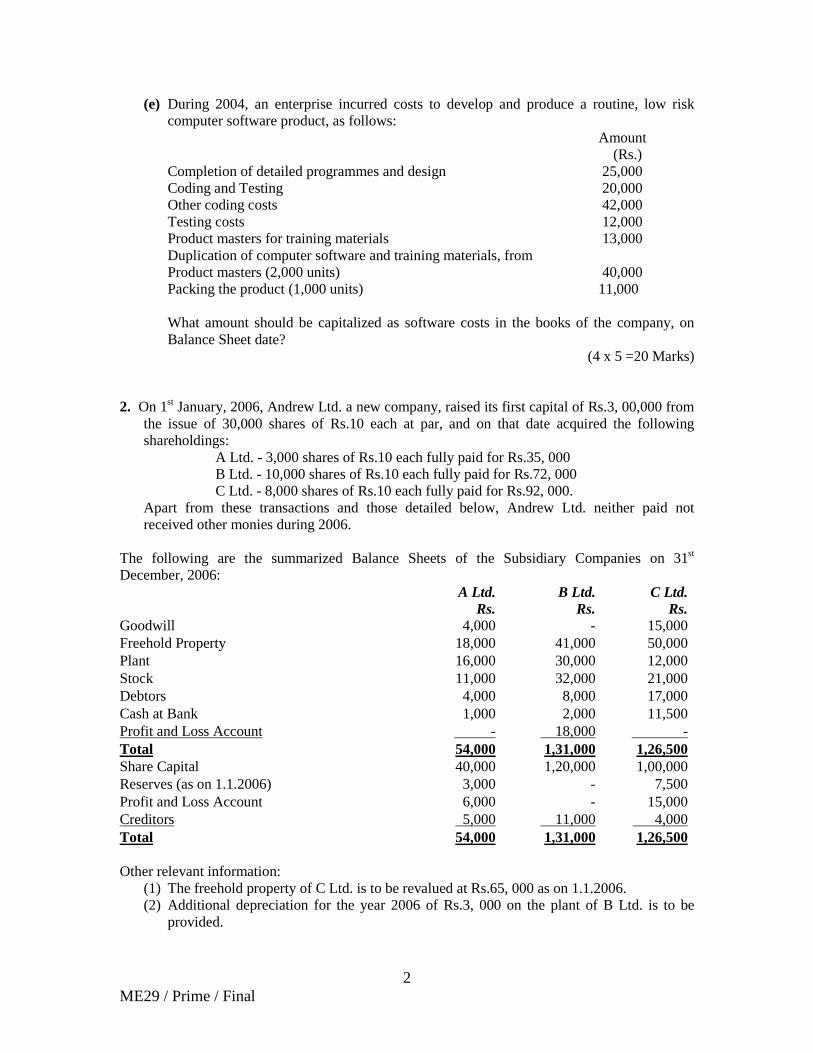

(e) During 2004, an enterprise incurred costs to develop and produce a routine, low risk computer software product, as follows:

Amount (Rs.)

Completion of detailed programmes and design 25,000 Coding and Testing 20,000 Other coding costs 42,000 Testing costs 12,000 Product masters for training materials 13,000 Duplication of computer software and training materials, from Product masters (2,000 units) 40,000 Packing the product (1,000 units) 11,000

What amount should be capitalized as software costs in the books of the company, on Balance Sheet date?

(4 x 5 =20 Marks) 2. On 1st

A Ltd. - 3,000 shares of Rs.10 each fully paid for Rs.35, 000

January, 2006, Andrew Ltd. a new company, raised its first capital of Rs.3, 00,000 from the issue of 30,000 shares of Rs.10 each at par, and on that date acquired the following shareholdings:

B Ltd. - 10,000 shares of Rs.10 each fully paid for Rs.72, 000 C Ltd. - 8,000 shares of Rs.10 each fully paid for Rs.92, 000.

Apart from these transactions and those detailed below, Andrew Ltd. neither paid not received other monies during 2006.

The following are the summarized Balance Sheets of the Subsidiary Companies on 31st

December, 2006:

A Ltd. Rs.

B Ltd. Rs.

C Ltd. Rs.

Goodwill 4,000 - 15,000 Freehold Property 18,000 41,000 50,000 Plant 16,000 30,000 12,000 Stock 11,000 32,000 21,000 Debtors 4,000 8,000 17,000 Cash at Bank 1,000 2,000 11,500 Profit and Loss Account - 18,000 - Total 54,000 1,31,000 Share Capital

1,26,500 40,000 1,20,000 1,00,000

Reserves (as on 1.1.2006) 3,000 - 7,500 Profit and Loss Account 6,000 - 15,000 Creditors 5,000 11,000 4,000 Total 54,000 1,31,000

1,26,500

Other relevant information: (1) The freehold property of C Ltd. is to be revalued at Rs.65, 000 as on 1.1.2006. (2) Additional depreciation for the year 2006 of Rs.3, 000 on the plant of B Ltd. is to be

provided.

3 ME29 / Prime / Final

(3) The stock of A Ltd. as on 31st

(4) As on 31

December, 2006 has been undervalued by Rs.2, 000 and is to be adjusted.

st

(5) The balances on Profit and Loss Accounts as on 31

December, 2006 Andrew Ltd. owed A Ltd. Rs.3, 500 and is owed Rs.6, 000 by B Ltd. C Ltd is owed Rs.1,000 by A Ltd., and Rs.2,000 by B Ltd.,

st

(6) During 2006, A Ltd. and C Ltd. declared and paid interim dividends of 8% and 10% respectively.

December, 2005 were: A Ltd. Rs.2, 000 (credit); B Ltd. Rs.12, 000 (debit); and C Ltd. Rs.4, 000 (credit).

You are required to prepare the Consolidated Balance Sheet of Andrew Ltd. and its subsidiary companies as on 31st

(16 Marks) December, 2006, ignore taxation.

3. The following is the Balance Sheet of Narmada Ltd. as on 31st

March, 2009:

Balance Sheet Liabilities Rs. Assets Rs.

4,00,000 Equity shares of Rs.10 each fully paid

40,00,000 Goodwill 4,00,000

13.5% Redeemable preference shares of Rs.100 each fully paid

20,00,000 Building 24,00,000

General Reserve 16,00,000 Machinery 22,00,000 Profit and Loss Account 3,20,000 Furniture 10,00,000 Bank Loan (Secured against fixed assets)

12,00,000 Vehicles 18,00,000

Bills Payable 6,00,000 Investments 16,00,000 Creditors 31,00,000 Stock 11,00,000 Debtors 18,00,000 Bank Balance 3,20,000 _____ __________ Preliminary Expenses 2,00,000 Total 1,28,20,000 Total

1,28,20,000

Further information: (i) Return on capital employed is 20% in similar businesses. (ii) Fixed assets are worth 30% more than book value. Stock is overvalued by rs.1,

00,000. Debtors are to be reduced by Rs.20, 000. Trade investments, which constitute 10% of the total investments, are to be valued at 10% below cost.

(iii) Trade investments were purchased on 1.4.2008. 50% of Non-Trade Investments were purchased on 1.4.2007 and the rest on 1.4.2006. Non-Trade Investments yielded 15% return on cost.

(iv) In 2006-2007 new machinery costing Rs.2, 00,000 was purchased, but wrongly charged to revenue. This amount should be adjusted taking depreciation at 10% on reducing value method.

(v) In 2007-2008 furniture with a book value of Rs.1, 00,000 was sold for Rs.60, 000. (vi) For calculating Goodwill two years purchase of super profits based on simple

average profits of last four years are to be considered. Profits of last four years are as under:

4 ME29 / Prime / Final

Year Rs. 2005-2006 16,00,000 2006-2007 18,00,000 2007-2008 21,00,000 2008-2009 22,00,000

(vii) Additional depreciation provision at the rate of 10% on the additional value of Plant and Machinery alone may be considered for arriving at average profit. Find out the intrinsic value of the equity share. Income-tax and Dividend tax are not to be considered.

(16 Marks)

4. (a) The following information is available of a concern: Calculate E.V.A.:

Debt capital 12% Rs.2,000 crores Equity capital Rs.500 crores Reserve and surplus Rs. 7,500 crores Capital employed Rs.10,000 crores Risk-free rate 9% Beta factor 1.05 Market rate of return 19% Equity (market) risk premium 10% Operating profit after tax Rs.2,100 crores Tax rate 30%

(b) Popular Ltd. started its business on 01.04.2007. It issued one lac Equity Shares of Rs.10 each at par and 30,000. 9% Debentures of Rs.50 each, both were fully subscribed. It purchased Plant and Machinery for worth Rs. 15 Lac and goods for trading worth Rs.12 lac @ Rs.100 per unit. Estimated life of plant and machinery was 10 years with no scrap value. Goods were sold at Profit of 40% on selling price. Collection from Debtors outstanding as on 31.3.2008 amounted to Rs.5 lac. Goods sold were replaced at a cost of Rs.120 per unit, the number of units being the same. Trade Creditors outstanding as on 31.3.2008 were Rs.3 lac. The replaced goods were entirely in stock on 31.3.2008; replacement cost of goods was considered to be Rs.140 per unit. Replacement cost of machine was Rs.20 lac as on 31.3.2008. Draft Profit and Loss Account and Replacement reserve on replacement cost basis.

(2 x 8 = 16 Marks) 5 Given below Balance Sheets of Bat Ltd. and Ball Ltd. as on 31.12.2006. Ball Ltd. was merged

with Bat Ltd. with effect from 1.1.2007 and the merger was in the nature of purchase.

Balance Sheets as on 31.12.2006

Liabilities Rs. Bat Ltd.

Rs. Ball Ltd. Assets

Rs. Bat Ltd.

Rs. Ball Ltd.

Share Capital: Equity Shares of Rs.10 each

7,00,000 2,50,000 Sundry Fixed Assets

9,50,000 4,00,000

5 ME29 / Prime / Final

General Reserve 3,50,000 1,20,000 Investments (Non-trade)

2,00,000 50,000

P & L A/c 2,10,000 65,000 Stock 1,20,000 50,000 Export Profit Reserve

70,000 40,000 Debtors 75,000 80,000

12% Debentures 1,00,000 1,00,000 Advance Tax 80,000 20,000 Sundry Creditors 40,000 45,000 Cash & Bank

Balances

2,75,000

1,30,000 Provisionfor Taxation

1,00,000

60,000

Preliminary Expenses

10,000

-

Proposed Dividend

1,40,000

50,000 _____

________

_______

Total 17,10,000 7,30,000 Total 17,10,000

7,30,000

Bat Ltd. would issue 12% Debentures to discharge the claims of the debenture holders of Ball Ltd. at par. Non-trade investments of Bat Ltd. fetched @ 25% while those of Ball Ltd. fetched @ 18% Profit (pre-tax) by Bat Ltd. and Ball Ltd. during 2004, 2005 and 2006 were as follows:

Year Bat Ltd.

Rs. Ball Ltd.

Rs. 2004 5,00,000 1,50,000 2005 6,50,000 2,10,000 2006 5,75,000 1,80,000

Goodwill may be calculated on the basis of capitalization method taking 20% as the pre-tax normal rate of return. Purchase consideration is discharged by Bat Ltd. on the basis of intrinsic value per share. The company decided to cancel the proposed dividend. Prepare Balance Sheet of Bat Ltd. after merger.

(16 Marks) 6 (a) Alpha Ltd. commenced its business on 1st

April, 2006, 2,00,000 equity shares of Rs.10 each at par and 12.5% debentures of the aggregate value of Rs.2,00,000 were issued and fully taken up. The proceeds were utilized as under:

Rs. Fixtures and Equipments (Estimated life 10 years, no scrap value)

16,00,000

Goods purchased for resale at Rs.200 per unit 6,00,000

The goods were entirely sold by 31st

January, 2006 at a profit of 40% on selling price.

Collections from debtors outstanding on 31st March, 2006 amounted to Rs.60,000, goods sold were replaced at a cost of Rs.7,20,000, the number of units purchased being the same as before. A payment of Rs.40,000 to a supplier was outstanding as on 31st

The replaced goods remained entirely in stock on 31 March, 2006.

st

March, 2006.

Replacement cost as at 31st

March, 2006 was considered to be Rs.280 per unit.

6 ME29 / Prime / Final

Replacement cost of fixtures and equipments (depreciation on straight line basis) was Rs.20,00,000 as at 31st

March, 2006.

Draft the Profit and Loss Account and the Balance Sheet on replacement cost (entry value) basis and on historical cost basis.

(b) The Balance Sheet of War Ltd. as on 31.3.2008 is given: (Rs. in ‘000)

Liabilities Rs.

Amount Assets Rs.

Amount

Share Capital: Equity shares of Rs.10 each

800 Fixed Assets 2,700

Securities Premium 100 Non-trade Investments 300 General Reserve 780 Stock 600 Profit and Loss A/c 120 Sundry Debtors 360 10% Debenture 2,000 Cash and Bank 160 Creditors 320 _____ _____ Total 4,120 Total

4,120

War Ltd. buy back 16,000 shares of Rs.20 per share. For this purpose, the Company sold its all non-trade investments for Rs.3, 20,000. Give Journal Entries with full narrations effecting the buy back.

(2 x 8 = 16 Marks) 7. Write short notes on any four from the following: (a) Explain significant differences and similarities between Indian Accounting Standards,

IAS/IFRS and US GAAPs on the issues of

(i) Changes in accounting policies. (ii) Inventories.

(b) Distinguish between Integral Foreign Operation and Non-integral Foreign Operation. (c) Difficulties in accounting Brands (d) Embedded derivatives (e) Asset Management Company in the context of Mutual Fund.

(4 x 4 = 16 Marks)

ME29 / Prime / Final 1

PRIME ACADEMY 29TH

SESSION MODEL EXAM FINANCIAL REPORTING- NEW SYLLABUS

SUGGESTED ANSWERS

1 (a) Rs.

Cost incurred till 31st 64,99,000 March, 2009 Prudent estimate of additional cost for completion 32.01,000 Total cost of construction 97,00,000 Less: Contract price 85,00,000 Total foreseeable loss 12,00,000

According to para 35 of AS 7 (Revised 2002), the amount of Rs.12, 00,000 is required to be recognized as an expense. Contract work in progress = Rs.64, 99,000 x 100

(c) Disclosure of Current and Deferred Tax balances will be on the basis of principles laid down in AS-22. These are:

= 67% 97, 00,000 Proportion of total contract value recognized as turnover as per para 21 of AS 7 (Revised) on Construction Contracts = 67% of Rs.85, 00,000 = Rs.56, 95,000.

(b) In this case, the capital expenditure incurred by the company would not be represented by any actual assets, since the roads would remain the property of the relevant State authorities even though a part of their cost has been defrayed by the company in order to facilitate its business. Having regard to the nature of the expenditure and the purpose for which it is incurred, it is suggested in para 10 of Guidance Note on Treatment of Expenditure. During Construction Period that it would be more appropriate and realistic to classify such expenditure in the balance sheet under the heading of “Capital Expenditure” rather than either, write-off the expenditure to revenue or classify the expenditure under the heading of “Miscellaneous Expenditure” or “Deferred Revenue Expenditure” subject to two conditions. In the first place, the description of the specific item on the balance sheet should be such as to indicate quite clearly that the capital expenditure is not represented by any assets owned by the company. In the second place, the capital expenditure should be written off over the approximate period of its utility or over a relatively brief period not exceeding five years, whichever is less.

(a) Current tax assets and liabilities can be set off, if the enterprise has a legally enforceable right to

set off the recognized amounts and intends to settle them on a net basis. (b) Deferred tax assets and liabilities can be set off, if the items relate to taxes on income levied by

the same governing taxation laws. Applying these principles, the required disclosures will be as follows:

Liabilities Rs. Rs. Assets Rs. Rs. Deferred tax liabilities Less: Deferred tax assets

100 20

80

Current assets, loans and advances Advance tax paid Less: Provisions

795 750

45

ME29 / Prime / Final 2

(d) As per Para 63 of As 26 “Intangible Assets”, the depreciable amount of an intangible asset should be allocated on a systematic basis over the best estimate of its useful life. There is a resuttable presumption that the useful life of an intangible asset will not exceed ten years from the date when the asset is available for use. Amortisaton should commence when the asset is available for use. Global Ltd. has been following the policy of amortization of the intangible asset over a period of 12 years on straight line basis. The period of 12 years is more than the maximum period of 10 years specified under As 26. Accordingly, Global Ltd. would be required to restate the carrying amount of intangible asset as on 1.4.2007 at Rs.96 lakhs less Rs.28.8 lakhs (Rs.9.6 lakhs x 3 years) = Rs.67.2 lakhs. If amortization had been as per As 26, the carrying amount would have been Rs.67.2 lakhs. The difference of Rs.4.8 lakhs i.e. (Rs.72 lakhs-67.2 lakhs) would be required to be adjusted against the opening balance of revenue reserves. The carrying amount of Rs.67.2 lakhs would be amortised over 7 ( 10 less 3 ) years in future.

(e) As per para 44 of AS-26, costs incurred in creating a computer software product should be charged to research and development expense when incurred until technological feasibility/ asset recognition criteria has been established for the product. Technological feasibility/asset recognition criteria has been established upon completion of detailed programme design or working model. In this case, Rs.45,000 would be recorded as an expense (Rs.25,000 for completion of detailed program design and Rs.20,000 for coding and testing to establish technological feasibility/ asset recognition criteria). Cost incurred from the point of technological feasibility/asset recognition criteria until the time when products costs are incurred are capitalized as software cost (Rs.42,000 + Rs.12,000 + Rs.13,000) Rs.67,000.

2. Consolidated Balance Sheet of Andrew Ltd. and its subsidiaries A Ltd. B Ltd. and C Ltd. as on 31st

Liabilities

December, 2006

Rs. Rs. Assets Rs. Rs.

Share Capital Fixed Assests Issued & Subscribed 30,000 shares of Rs 10 each fully paid

3,00,000

Goodwill Freehold Property Plant

19,000 1,24,000

55,000

Reserve & Surplus Investments - Reserve on Consolidation 25,950 Current Assets Profits & Loss A/c 20,900* Loans & Advances Secured Loans - Stock in trade 66,000 Unsecured Loans - Sundry Debtors 35,000 Current Liabilities & Provisions

Less: Inter Co. Debts

12,500

22,500

Sundry Creditors 23,500 Cash at Bank 1,28,100 Less: Inter Co. 12,500 11,000 Minority Interest 56,750 Total 4,14,600 Total 4,14,600 Analysis of Profits:

Capital Profit Rs.

Revenue Profit Rs.

(i) C Ltd. Profit & Loss Account on 1.1.2006 less Div (4000-4000)

-

Reserve on 1st 7,500 Jan 2006 Appreciation in the value of Freehold Property 15,000 Profit for the year after interim dividend 15,000 22,500 15,000 Minotiry interest 20% 4,500 3,000

ME29 / Prime / Final 3

Share of Andrew Ltd. 18,000 12,000 (ii) B Ltd. Loss on the date of acquisition -12,000 Loss suffered during the year (21,000 – 12,000)

-9,000

-12,000 -9,000 Minority Interest (1/6) 2,000 1,500 Share of Andrew Ltd. -10,000 -7,500 *Revenue Profit of C Ltd. Rs.12,000 Revenue Profit of B Ltd. -Rs.7,500 Revenue Profit of A Ltd. Rs.6,000 Rs.10,500 Add: Interim dividend received Rs.10,400 Rs.20,900 (iii) A Ltd. Reserve on 1.1.2006 3,000 Profit on 1.1.2006 less Dividend (2,000-2,000) - - Profit earned during the year (after interim dividend Rs.3,200)

8,000

3,000 8,000 Minority Interest (1/4) 750 2,000 2,250 6,000

(iv) Cost of Control / Capital Reserve

Cost of Investments in A Ltd. less Dividend (35,000-1,500)

33,500

Cost of Investments in B Ltd. 72,000 Cost of Investments in C Ltd. less Dividend (92,000-3,200)

88,800

1,94,300 Paid up value of shares held in A Ltd. 30,000 Paid up value of shares held in B Ltd. 1,00,000 Paid up value of shares held in C Ltd. 80,000 Capital Profits in A Ltd. 2,250 Capital Profits in B Ltd. -10,000 Capital Profits in C Ltd. 18,000 2,20,250 Capital Reserve 25,950

(v) Minority Interest

A Ltd.

Rs. B Ltd.

Rs. C Ltd.

Rs. Share Capital 10,000 20,000 20,000 Capital Profits 750 -2,000 4,500 Revenue Profits 2,000 -1,500 3,000 12,750 16,500 27,500

56,750

ME29 / Prime / Final 4

(vi) Bank A/c – Andrew Ltd.

Dr. Cr. Rs. Rs. To Share Capital 3,00,000 By Investments in A Ltd. 35,000 To Investments in A Ltd. 1,500 By Investments in B Ltd. 72,000 To Investments in C Ltd. 3,200 By Investments in C Ltd. 92,000 To Dividends- A Ltd. 2,400 By B Ltd. (indebtedness) 6,000 C Ltd. 8,000 By Balance c/d 1,13,600 To A Ltd. 3,500 3,18,600 3,18,600

(vii) Sundry Assets

Freehold Property

Rs.

Plant

Rs.

Stock

Rs.

Debtors

Rs.

Cash at Bank

Rs. (a) Andrew Ltd. - - - 6,000 1,13,600 (b) A Ltd. 18.000 16,000 13,000 4,000 1,000 (c) B Ltd. 41,000 27,000 32,000 8,000 2,000 (d) C Ltd. 65,000 12,000 21,000 17,000 11,500 1,24,000 55,000 66,000 35,000 1,28,100 Less: Inter Co. debts 12,500 22,500

3. Calculation of intrinsic value of equity shares of Narmada Ltd.

(a) Calculation of Goodwill:

1) Capital employed Rs. Rs. Fixed Assets Building 24,00,000 Machinery (Rs.22,00,000 + Rs.1,45,800) 23,45,800 Furniture 10,00,000 Vehicles 18,00,000 75,45,800 Add: 30% increase 22,63,740 98,09,540 Trade investments (Rs.16,00,000 x 10% x 90%) 1,44,000 Debtors (Rs.18,00,000- Rs.20,000) 17,80,000 Stock (Rs.11,00,000-Rs.1,00,000) 10,00,000 Bank balance 3,20,000 1,30,53,540 Less: Outside liabilities Bank Loan 12,00,000 Bills Payable 6,00,000 Creditors 31,00,000 49,00,000 Capital employed 81,53,540

ME29 / Prime / Final 5

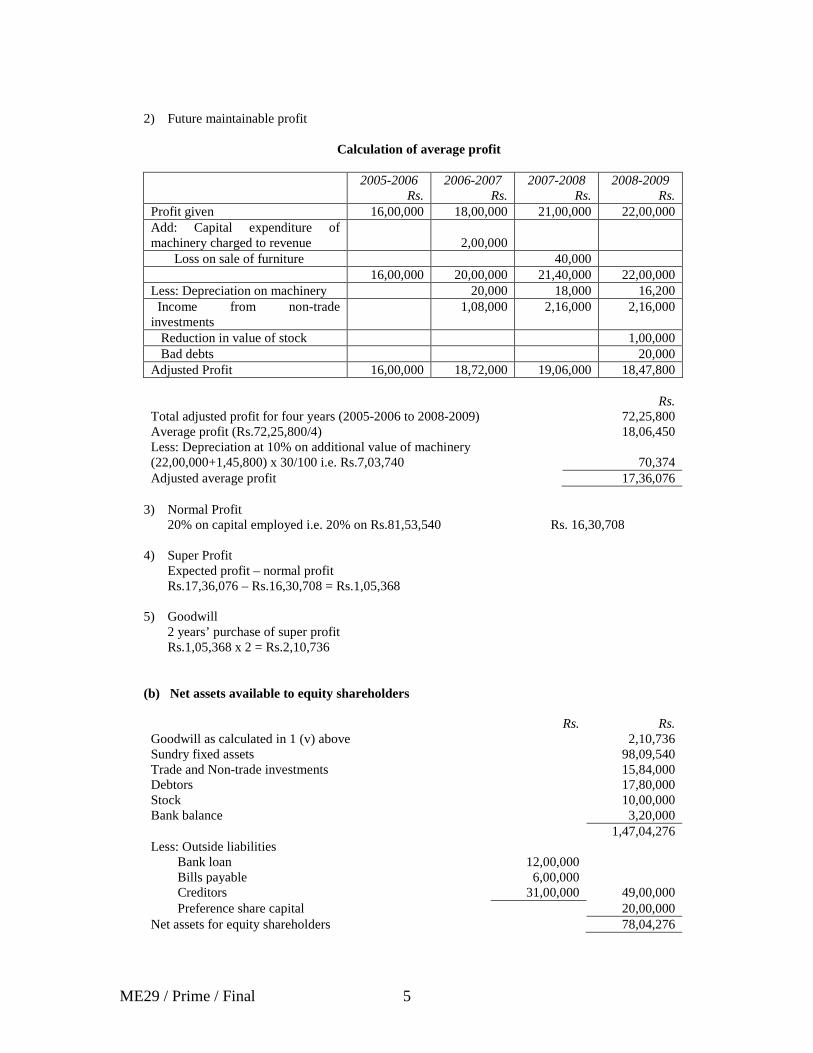

2) Future maintainable profit

Calculation of average profit

2005-2006 Rs.

2006-2007 Rs.

2007-2008 Rs.

2008-2009 Rs.

Profit given 16,00,000 18,00,000 21,00,000 22,00,000 Add: Capital expenditure of machinery charged to revenue

2,00,000

Loss on sale of furniture 40,000 16,00,000 20,00,000 21,40,000 22,00,000 Less: Depreciation on machinery 20,000 18,000 16,200 Income from non-trade investments

1,08,000 2,16,000 2,16,000

Reduction in value of stock 1,00,000 Bad debts 20,000 Adjusted Profit 16,00,000 18,72,000 19,06,000 18,47,800

Rs. Total adjusted profit for four years (2005-2006 to 2008-2009) 72,25,800 Average profit (Rs.72,25,800/4) 18,06,450 Less: Depreciation at 10% on additional value of machinery (22,00,000+1,45,800) x 30/100 i.e. Rs.7,03,740

70,374

Adjusted average profit 17,36,076 3) Normal Profit

20% on capital employed i.e. 20% on Rs.81,53,540 Rs. 16,30,708

4) Super Profit Expected profit – normal profit Rs.17,36,076 – Rs.16,30,708 = Rs.1,05,368

5) Goodwill

2 years’ purchase of super profit Rs.1,05,368 x 2 = Rs.2,10,736

(b) Net assets available to equity shareholders

Rs. Rs. Goodwill as calculated in 1 (v) above 2,10,736 Sundry fixed assets 98,09,540 Trade and Non-trade investments 15,84,000 Debtors 17,80,000 Stock 10,00,000 Bank balance 3,20,000 1,47,04,276 Less: Outside liabilities Bank loan 12,00,000 Bills payable 6,00,000 Creditors 31,00,000 49,00,000 Preference share capital 20,00,000 Net assets for equity shareholders 78,04,276

ME29 / Prime / Final 6

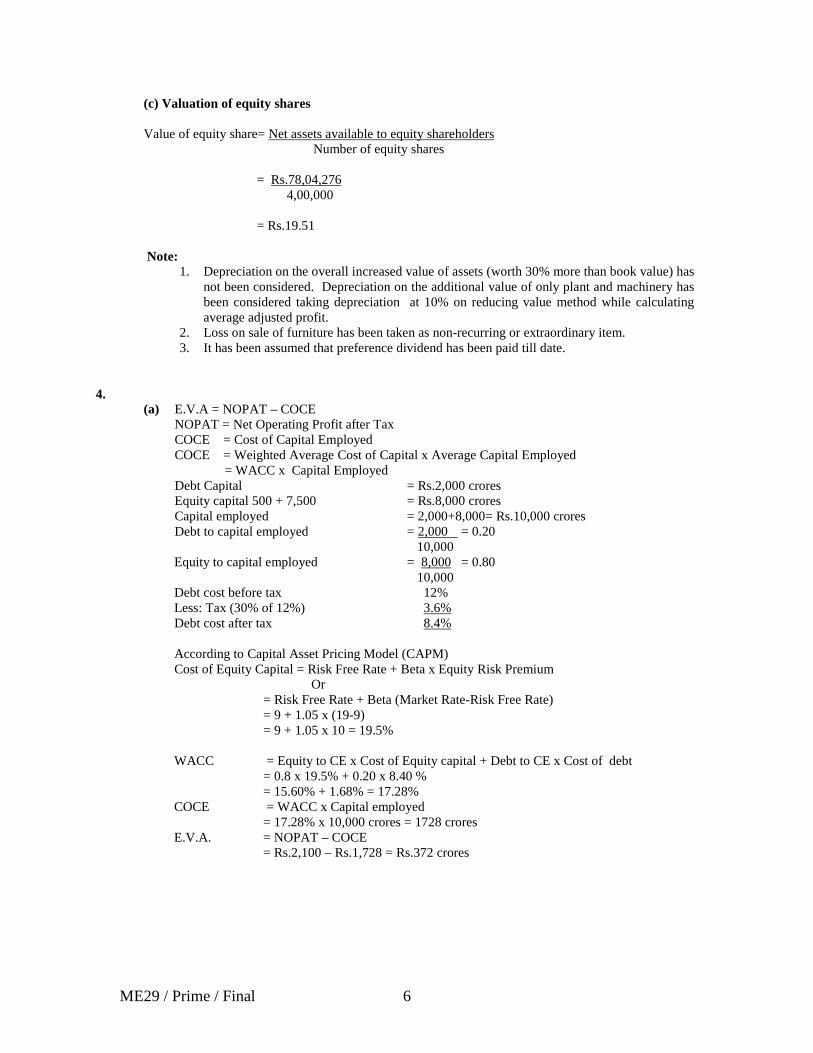

(c) Valuation of equity shares Value of equity share= Net assets available to equity shareholders Number of equity shares =

1. Depreciation on the overall increased value of assets (worth 30% more than book value) has not been considered. Depreciation on the additional value of only plant and machinery has been considered taking depreciation at 10% on reducing value method while calculating average adjusted profit.

Rs.78,04,276 4,00,000 = Rs.19.51 Note:

2. Loss on sale of furniture has been taken as non-recurring or extraordinary item. 3. It has been assumed that preference dividend has been paid till date.

4. (a) E.V.A = NOPAT – COCE

NOPAT = Net Operating Profit after Tax COCE = Cost of Capital Employed COCE = Weighted Average Cost of Capital x Average Capital Employed = WACC x Capital Employed Debt Capital = Rs.2,000 crores Equity capital 500 + 7,500 = Rs.8,000 crores Capital employed = 2,000+8,000= Rs.10,000 crores Debt to capital employed = 2,000 = 0.20

10,000 Equity to capital employed = 8,000 = 0.80 10,000 Debt cost before tax 12% Less: Tax (30% of 12%) 3.6% Debt cost after tax 8.4% According to Capital Asset Pricing Model (CAPM) Cost of Equity Capital = Risk Free Rate + Beta x Equity Risk Premium Or = Risk Free Rate + Beta (Market Rate-Risk Free Rate) = 9 + 1.05 x (19-9) = 9 + 1.05 x 10 = 19.5% WACC = Equity to CE x Cost of Equity capital + Debt to CE x Cost of debt = 0.8 x 19.5% + 0.20 x 8.40 % = 15.60% + 1.68% = 17.28% COCE = WACC x Capital employed = 17.28% x 10,000 crores = 1728 crores E.V.A. = NOPAT – COCE = Rs.2,100 – Rs.1,728 = Rs.372 crores

ME29 / Prime / Final 7

(b) M/s Popular Ltd. Profit & Loss Account as on 31.03.2008

Rs. Sales 20,00,000 Less: Cost of sales (Refer W.N.1) 14,40,000 Gross Profit 5,60,000 Less: Depreciation (Refer W.N.2) 1,75,000 Profit before interest 3,85,000 Less: Debenture interest (Refer W.N.3) 1,35,000 Profit after charging depreciation and interest 2,50,000

Replacement Reserve

Realised Gain Rs.

Unrealised Gain

Rs. Stock: Sold (Rs.14,40,000-Rs.12,00,000) 2,40,000 Unsold goods 12,000 x (Rs.140-Rs.120) 2,40,000 Plant & Machinery Depreciation (Rs. 1,75,000-Rs.1,50,000) 25,000 Book value of asset [(Rs.20,00,000- Rs.2,00,000) less (Rs.15,00,000-Rs.1,50,000)]

4,50,000 2,65,000 6,90,000

Replacement Reserve= Rs.2,65,000 + Rs.6,90,000 = Rs.9,55,000 Working Notes:

1. Sales and Cost of sales Sale Price @ 40% profit on Selling Price = Rs.12,00,000 x (100/60) = Rs.20,00,000 Cost of Sales =12,000 x Rs.120 = Rs.14,40,000

2. Depreciation under replacement cost basis

Under replacement cost basis, depreciation is calculated (on average basis) which can be shown as follows: 15,00,000 + 20,00,000

3. Debenture Interest

=10% of Rs.17,50,000 = Rs.1,75,000 2

30,000 x Rs.50 x 9% = Rs.1,35,000

5. (1) Valuation of Goodwill

(i) Capital Employed Bat Ltd. Ball Ltd. Rs. Rs. Rs. Rs. Sundry-Assets as per Balance Sheet 17,10,000 7,30,000 Less: Preliminary Expenses 10,000 - Non-trade Investment 2,00,000 2,10,000 50,000 50,000 15,00,000 6,80,000 Less: Sundry Liabilities 12% Debentures 1,00,000 1,00,000 Sundry Creditors 40,000 45,000 Provision for Taxation 1,00,000 2,40,000 60,000 2,05,000 12,60,000 4,75,000

ME29 / Prime / Final 8

(ii) Average Pre-Tax Profit Bat Ltd.

Rs. Ball Ltd.

Rs. 2004 5,00,000 1,50,000 2005 6,50,000 2,10,000 2006 5,75,000 1,80,000 17,25,000 5,40,000 Simple Average 5,75,000 1,80,000 Less: Non-trading income 50,000 9,000 5,25,000 1,71,000 (iii) Goodwill Capitalisation Value of average profit 5,25,000 26,25,000 x 100

20 1,71,000 8,55,000 x 100 20

Less: Capital Employed 12,60,000 4,75,000 13,65,000 3,80,000 (2) Intrinsic Value per Share Bat Ltd. Ball Ltd. Rs. Rs. Rs. Rs. Goodwill 13,65,000 3,80,000 Sundry Other Assets less preliminary expenses

17,00,000

7,30,000

30,65,000 11,10,000 Less: Liabilities 12% Debentures 1,00,000 1,00,000 Sundry Creditors 40,000 45,000 Provision for Tax 1,00,000 2,40,000 60,000 2,05,000 28,25,000 9,05,000 Intrinsic value per share 28,25,000

70,000 =Rs.40.40

9,05,000 25,000 = Rs.36.20

(3) Purchase Consideration 25,000 Shares @ Rs.36.20

Liabilities

Rs. 9,04,960 To be discharged by 22,400 [25,000 x 36.20/40.40] Shares @ Rs.40.40 Rs. 9,04,960 Cash for fraction Rs.40

Balance Sheet of Bat Ltd. (after merger with Ball Ltd.)

Rs. Rs. Assets Rs. Rs.

Share Capital Goodwill 3,80,000* 92,400 Equity Shares of Rs.10 each

9,24,000 Sundry Fixed Assets Balance

9,50,000

(of which 22,400 shares were issued to the vendors

Add: Assets takenover

4,00,000

13,50,000

otherwise than cash) Investments General Reserve 3,50,000 Balance 2,00,000 P & L A/c 2,10,000 Add: Investments Add: Proposed taken over 50,000 2,50,000 Dividend written off 1,40,000 3,50,000 Stock Balance 1,20,000 Share Premium 6,80,960 Add: Stock taken over 50,000 1,70,000 Export Profit Reserve Debtors : Balance 75,000

ME29 / Prime / Final 9

Balance 70,000 Add: Taken over 80,000 1,55,000 Add: Balance of Ball Ltd. 40,000 1,10,000 Advance Tax Bal. 80,000 12% Debenture Balance 1,00,000 Add: Bal of Ball Ltd. 20,000 1,00,000 Add: 12% Debentures issued at par other than cash

1,00,000

2,00,000

Cash & Bank Balance Add: Balance of Ball Ltd. taken over

2,75,000

1,30,000

Sundry creditors Balance 40,000 4,05,000 Add: Liabilities taken over

45,000

85,000

Less: Purchase consideration discharged

40

4,04,960

Provision for Taxation 1,00,000 Preliminary expenses 10,000 Add: Prov.for Taxation of Ball Ltd.

60,000

1,60,000

Amalgamation Adjustment A/c

40,000

28,59,960 28,59,960 * Goodwill= Purchase consideration – Net Assets acquired Rs. 9,05,000-Rs. 5,25,000 = Rs. 3,80,000

6. (a)

Profit and Loss Account for the year ended 31st

March, 2006

Historical Cost Basis

Rs.

Replacement Cost Basis

Rs. Sales 10,00,000 10,00,000 Less: Cost of Sales 6,00,000 7,20,000 Gross Profit 4,00,000 2,80,000 Less: Depreciation 1,60,000 1,80,000 Profit before interest 2,40,000 1,00,000 Less: Debenture interest 25,000 25,000 Net Profit 2,15,000 75,000 Balance Sheet of Alpha Ltd. as at 31st

March, 2006

Historical Cost Basis

Rs.

Replacement Cost Basis

Rs. Liabilities Equity Share Capital 20,00,000 20,00,000 Profit and Loss Account 2,15,000 75,000 Replacement Reserve - 6,20,000 12.5% Debentures 2,00,000 2,00,000 Creditors 40,000 40,000 24,55,000 29,35,000 Assets Fixtures and Equipment 14,40,000 18,00,000 Stock 7,20,000 8,40,000 Debtors 60,000 60,000 Cash and Bank 2,35,000 2,35,000 24,55,000 29,35,000 Working Notes: (i) Replacement cost of sales on the basis of replacement cost on the date of sale = Rs.240 x

3,000=Rs.7,20,000

ME29 / Prime / Final 10

(ii) Under replacement cost basis, depreciation, calculated on the average basis = 10% of Rs.16,00,000 + Rs.20,000

= Rs.1,80,000 2 (iii) Fixtures and equipments at net current replacement cost.

Rs. Gross replacement cost 20,00,000 Less: Depreciation, 10% of Rs.20,00,000 2,00,000 18,00,000

(iv) Replacement Reserve+ Realised holding gains + Unrealised holding gains Realised holding

gains Rs.

Unrealised holding gains

Rs. Stocks: Sold (replacement cost at the date of sale- historical cost) Rs. (7,20,000 – 6,00,000)

1,20,000

Unsold [closing stock x (closing rate – rate at the date of purchase)] = 3,000 x Rs.280 – 240

1,20,000

Fixtures and Equipments: Depreciation Rs. (1,80,000 – 1,60,000) 20,000 Net book value at year end, (Rs.18,00,000- Rs.14,40,000) 3,60,000 1,40,000 4,80,000 Replacement + Reserve = Rs.1,40,000 + Rs. 4,80,000 = Rs.6,20,000.

(b) Journal Entries for Buy-back of shares of War Ltd.

Debit Rs.

Credit Rs.

(i) Bank A/c Dr. To Non-trade Investments To Profit & Loss A/c (Being the entry for sale of Non-trade Investments)

3,20,000 3,00,000

20,000

(ii) Shares Buy back A/c (16,000 x Rs.20) Dr. To Bank A/c (Being purchase of 16,000 shares @ Rs.20 per share)

3,20,000 3,20,000

(iii) Equity Share Capital A/c (16,000 x Rs.10) Dr. Buy-back Premium (16,000 x Rs.10) Dr. To Shares Buy-back A/c (Being cancellation of shares bought back)

1,60,000 1,60,00

3,20,000

(iv) Securities Premium A/c Dr. General Reserve Dr. To Buy-back Premium (Being adjustment of buy-back premium)

1,00,000 60,000

1,60,000

(v) General Reserve Dr. To Capital Redemption Reserve (Being the entry for transfer of General Reserve to Capital Redemption Reserve to the extent of face value of equity shares bought back)

1,60,000 1,60,000

ME29 / Prime / Final 11

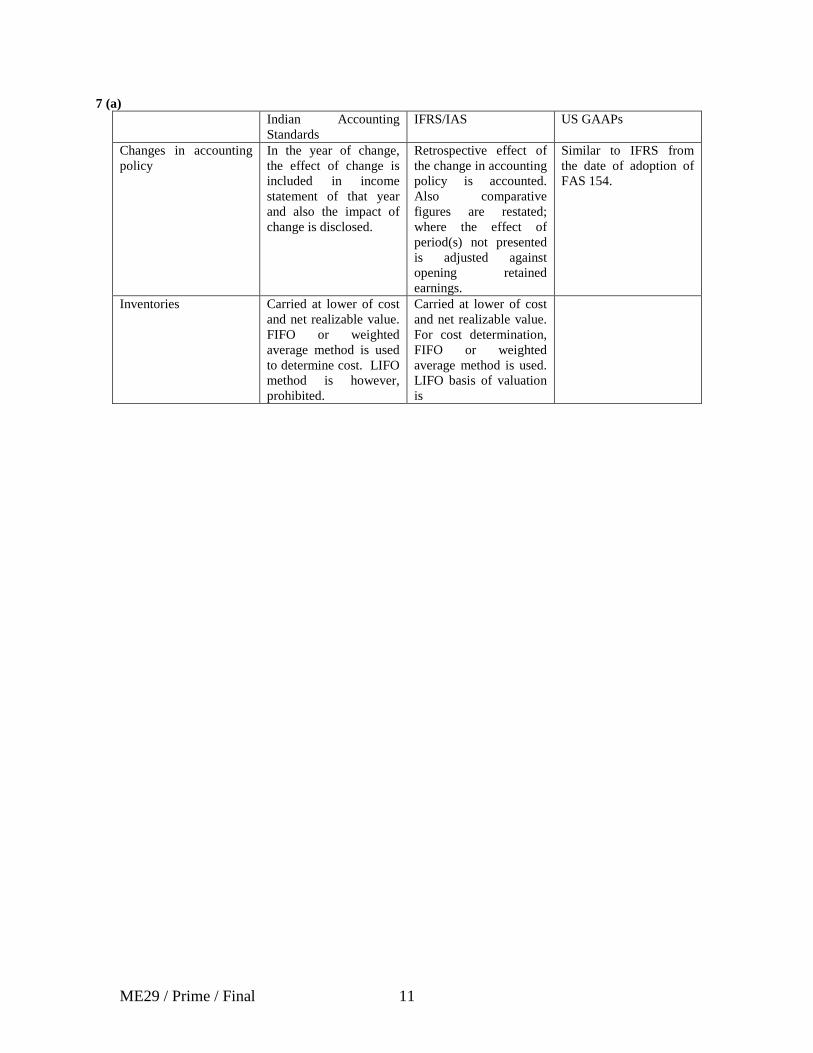

7 (a) Indian Accounting

Standards IFRS/IAS US GAAPs

Changes in accounting policy

In the year of change, the effect of change is included in income statement of that year and also the impact of change is disclosed.

Retrospective effect of the change in accounting policy is accounted. Also comparative figures are restated; where the effect of period(s) not presented is adjusted against opening retained earnings.

Similar to IFRS from the date of adoption of FAS 154.

Inventories Carried at lower of cost and net realizable value. FIFO or weighted average method is used to determine cost. LIFO method is however, prohibited.

Carried at lower of cost and net realizable value. For cost determination, FIFO or weighted average method is used. LIFO basis of valuation is

1

ME29 / Prime / Final

SCFM

Number of Pages : 5 Total Marks: 100 Number of questions: 6 Time Allowed: 3 Hrs

Question 1 is compulsory. Answer any 4 from the rest

1a. Television Ltd. has a proposal for manufacturing car televisions. The project would involve cost of plant Rs.500 lacs, installation cost of Rs.100 lacs and working capital of Rs.125 lacs. The annual capacity of the plant is to manufacture 20,000 sets. Price per set is Rs.20, 000/-, with a variable cost ratio of 65%. Cash-fixed costs in the first year, including promotion expenditure of Rs. 120 lacs, is Rs. 420 lacs and is thereafter Rs. 300 lacs each year. Depreciation at is at 25% WDV. Working capital requirements is 25% of sales. The company expects that the plant’s capacity utilization over its estimated useful life of seven years is as under:

Year 1 2 3 4 5 6 7

Capacity utilization % 25 40 50 75 100 100 100

Terminal value of the project is 20% at invoice price. If the hurdle rate is 12%, and tax rate is 35% plus 5% surcharge, can the project be accepted? While evaluating, you have to keep in mind that the Company has other sources of income against which the losses if any from this project, can be set off. Also assume that the terminal value would include release of founds blocked in working capital.

(14 Marks)

b. An initial outlay of Rs. 12 lacs is contemplated in a project, for which the following cash flow estimates have been prepared:

2

ME29 / Prime / Final

Net CFAT (Rs.) Probability

Year 1

Year 2

Year 3

4,00,000

3,50,000

2,50,000

3,50,000

4,50,000

5,00,000

2,60,000

3,20,000

4,10,000

0.30

0.40

0.30

0.25

0.35

0.40

0.45

0.25

0.30

Advise whether the project is worthwhile, if RADR is 17%? What should be the maximum project cost, if it were to be taken up.

(6 Marks)

2.a Basic information: (i) Asset related: cost Rs.120 lace; tax depreciation 40%; Useful life 4 years; RV after three years

Rs.25.92 lacs (ii) Leasing: Full pay out: three years lease: lease Quote Rs.434 per 1000: payment annually in

arrears (iii) Borrow and buy three-years loan; interest rate 15%; Quantum to be determined, such that annual

repayment of principals will be equal to annual lease rental payment (iv) Others: tax rate is 40%, and opportunity cost of capital is 11%.

Based on information given above, determine the preferred option as between leasing and buying.

(12 Marks)

b. Write Short notes on Venture Capital.

(4 Marks)

3

ME29 / Prime / Final

c. You have a housing loan with one of India’s top housing finance companies. The amount outstanding is Rs.1, 89,540. You have just now paid an instilment. You next instilment falls due a year later. There are five more installments to go, each being Rs.50, 000. Another housing-finance company has offered to take over this loan on a seven year repayment basis. You will be required to pay Rs.36, 408 per annum, with the first instilment falling a year later. The processing fee is 3% of amount taken over. For swapping you will have to pay Rs.12, 000 to the first company .should you swap the loan?

(4 Marks)

3.a Imperial Ltd. Is evaluating the feasibility of acquiring control of Hospital surgical (HS), an unlisted, private company.

Turn over Rs.2400 lacs

Earnings Rs.30 lacs

Number of share 60,000

Share held by Small group of family members

% of Debt in total debt and equity 25%

Dividend pay out 50%

Estimated Growth in dividend 5% constant

Imperial expect to offer a price which would be at least 15% less than what would the price, if the share were to be listed. RBI Bond rate is presently ruling at 6% and market beta of 1.44, with debt level which is one –eighth of equity level. What price should Imperial pay for the share of HS? Assume that there is no taxation.

(16 Marks)

b Write Short notes on Net Asset Value.

(4 Marks)

4.a Consider the following data relating to KM stock. KM has a beta of 0.7 with NIFTY. Each Nifty contract is equal to 200 units. KM now quotes at Rs 150 and the Nifty future is 1400 Index points. You are long on 1200 shares of KM in the spot market.

(i) How many futures contracts will you have to take?

(ii) Suppose the price in the spot market spot market drops by 10%, how are you protected?

(iii) Suppose the price in the spot market jumps up by 5%, what happens?

(4 Marks)

4

ME29 / Prime / Final

b. you have invested in four securities (A,B,C and D),the following sums:

A: Rs.10,000; B: Rs20,000; C: Rs. 16,000; D: Rs.14,000

The β values of the securities are 0.80, 1.20, 1.40 and 1.75 respectively. (i) If the risk free return is 4.25%, and the market return is 11%, what is the expected return on the portfolio? (ii) If you encash your investment in security β and reinvest the funds in RBI Bonds yielding a return of 4.25%, what is the β value of the portfolio and its expected return?

(8 Marks)

c. Mr. A can earn a return of 16 per cent by investing in equity share his own. Now he is considering a recently announced equity based mutual fund scheme in which the initial expenses are 5.5 per cent and annual recurring expenses are 1.5 per cent. How much should the mutual fund earn to provide Mr. A a return of 16 per cent?

(4 Marks)

d. What do you mean by the term ‘spread’? What are the factors determining it?

(4 Marks)

5.a The balance sheet of K Ltd shows that its share have a par value of Rs.8 The paid up capital is Rs. 20 lacs. The share premium show Rs. 6 lacs and the retained earning are Rs. 84 lacs. The current market price is Rs. 60. What will happen to the equity account and to the number of share outstanding and to the market price in each of the following situation? Consider each situation independently and discuss

(i) If there is a 1:5 bonus issue (ii) If there is a 2:1 stock split (iii) If there is a 1:2 reverse slit

(8 Marks)

b. Write Short notes on constant dividend plus

(8 Marks)

c. Write short notes on Straddle

(4 Marks)

5

ME29 / Prime / Final

6 Write short notes on any four:

(i) Diversifiable risk or Non-Diversifiable risk

(ii) Options contract

(iii) Short selling

(iv) Global Depository Receipts (GDR)

(v) Zero coupons

(vi) Interest Rate Futures

(4 x 5 = 20 Marks)

ME29 / Prime / Final 1

PRIME ACADEMY 29TH SESSION MODEL EXAM

STRATEGIC FINANCIAL MANAGEMENT NEW SYLLABUS - SUGGESTED ANSWERS

1 (a) Step:1 Initial Outflow (Rs. lacs)

Capital Expenditure 600 Working Capital 125 Total 725 Step:2 In between cash flow

YR

WN 1 Depreciation

Opening WDV

Depreciation @ 25%

Closing WDV

600 150 450 2 450 113 337 3 337 84 253 4 253 63 190 5 190 48 142 6 142 36 106 7 106 27 79

W N 2 Tax 35+5% = 36.75% It is assumed that loss of first year can be adjusted in the first year itself Tax saved = 81 (220 X 36.75%) Step:3

Details

, Statement showing computation of CFAT during project life

Note 1 2 3 4 5 6 7 Volume % 25 40 50 75 100 100 100 Volume Units 5000 8000 10000 15000 20000 20000 20000 Sales (In lacs) 1000 1600 2000 3000 4000 4000 4000 Contribution @35% 350 560 700 1050 1400 1400 1400 Less: Cash Fixed Costs (420) (300) (300) (300) (300) (300) (300)

Less: Depreciation 1 (150) (113) (84) (63) (48) (36) (27) PBT (220) 147 316 687 1052 1064 1073 Less: Tax @ 36.75% 2 81 (54) (116) (252) (387) (391) (394)

PAT (139) 93 200 435 665 673 679 Add: Depreciation 150 113 84 63 48 36 27 Less: Change in Working Capital 3 (125) (150) (100) (250) (250) - -

Net CFAT (114) 56 184 248 463 709 706

ME29 / Prime / Final 2

Details

W N 3

Note 1 2 3 4 5 6 7 Working Capital ( 25% of Sales) 250 400 500 750 1000 1000 1000

Increase in working Capital 125 150 100 250 250 0 0

Step:4 Terminal Value: Invoice Price x 20% = 100 (-) WDV = (79) Excess of sales Proce over WDV = 21 Tax @ 36.75% = (8) Net Sale value = 92 Recapture of working Capital = 1000_____ Total = 1092 Lacs Step:5

Yr

, Capital Budgeting Analysis statement

CF (Rs) DF(12%) DCF(Rs) 0 (725) 1.000 (725) 1 (114) 0.893 (102) 2 56 0.797 45 3 184 0.712 131 4 248 0.636 158 5 463 0.567 263 6 709 0.507 359 7 (706+1092) 0.452 813 NPV 942

Conclusion: Since NPV of the project is positive, project may be accepted

1 (b) Step I: Compute Expected cash flow Year's Net CFAT ( Rs. Probability Amount Rs. Rs. Year 1 400,000 0.30 120,000

350,000 0.40 140,000

250,000 0.30 75,000 335,000

Year 2 350,000 0.25 87,500 450,000 0.35 157,500

500,000 0.40 200,000 445,000

Year 3 to 5 260,000 0.45 117,000

320,000 0.25 80,000

410,000 0.30 123,000 320,000

ME29 / Prime / Final 3

Step II : Compute RADR. This is given as 17% Step III : Compute NPV using a RADR of 17%

Year Cash Flow Discount Factor PV / Rs. (Rs) @ 17%

0 (12,00,000) 1.000 (12,00,000) 1 3,35,000 0.855 2,86,425 2 4,45,000 0.731 3,25,295 3 3,20,000 0.624 1,99,680 4 3,20,000 0.534 1,70,880 5 3,20,000 0.456 1,45,920

NPV (71,800)

Step IV:

Decision - The NPV of the project , at a RADR of 17% is negative , Hence the project should be rejected

Maximum Project cost. For Acceptance, the project cost, should be curtailed and Step V: revised downwards t Rs11,28,200

( Rs.12.00 Lacs, Less Rs.71,800).

2 (a) Step 1.

Lease quote Rs.434/1000

Compute annual lease rentals

Cost: Rs.120 lacs Rentals = Rs.52,08,000 Note: Rentals = 120 lacs x 434/1000 = Rs.52,08,000 Step 2.

• Discount the lease rentals at borrowing rate, and derive its PV.

Determine loan equivalent Loan amount bearing an interest of 15%, repayment in which equals lease rentals. Can be computed as under.

• Establish a link between the derived PV, with the PV of asset. • Determine PV per thousand of the value of asset. In the instant case, if lease rental of Rs.52,08,000 is an annuity. PVAF for 15% for three years 2.283. The PV of lease rentals is 11,891 (thousands), against current value of asset at Rs.120 lacs. This works out to 991 per thousand; hence, loan amount will be 0.991 x 12000 = Rs.11892. Amount / Rs.000

Commencement Interest at 15% Principal Repayment 11,892.00 1783.80 3434.20 5208 8467.80 1270.17 3937.83 5208 4529.97 679.50 4528.50 R/off dif. 1.47

ME29 / Prime / Final 4

Step 3.

Annual lease rentals

PV of tax shield on lease rentals (discounted at COC 11%) Amount/Rs.000

5208.00 Tax rate 0.40 Tax shield 2083.20 3 year PVAF at 11% 2.4437 PV of tax shield 5090.87

Step 4:

Depreciation on 120,00 @ 40%

PV of tax shield on depreciation (discounted at COC 11%) Tax Shield @ 0.40 Dis. Factor At 11% PV Rs.000

4800 1920 0.901 1729.92 2880 1152 0.812 935.42 1728 691 0.731 505.12

PV of tax shield 3170.46 Step 5:

Interest on loan At 11%

PV of Tax shield on interest on loan (Discount at COC 11%) Tax shield at 40%

PV Rs.000 Disc. Factor

1783.80 713.52 0.901 642.89 1270.17 508.07 0.812 412.56 679.50 271.80 0.731 198.69

PV of tax shield 1254.14 Step 6:Salvage: Rs.25.92 lacs

PV of Salvage value: (COC 11%) 0.731 Rs.18.95 lacs

Step 7:

Net Advantage to Lease = Difference between A and B Evaluation

A B (1) Initial Investment Rs.12000.00 (3) PV of Lease rentals Rs.11892.00 (2) PV of Tax Rs.5090.87 Shield on lease rentals

(4) PV of tax shield on depreciation

Rs.3170.46

(5) PV of tax shield on interest on loan

Rs.1254.14

(6) PV of net salvage value

Rs.1895.00

Rs.17090.87 Rs.18211.60 Decision: Since value of B > A, decision is in favour of borrowing and buying

2 (b) 1. Venture Capital

The phrase Venture Capital4 was first coined at the Harvard Business School in the early 1950s to define a century old activity!

ME29 / Prime / Final 5

What it means Venture Capital5

• Finance new and rapidly growing companies

is money provided by professionals who invest alongside management, in young, rapidly growing companies that have the potential to develop into economic powerhouses. A firm engaged in providing venture capital and related services is referred to as a venture capitalist. Venture Capital (VC) firms are generally private partnerships, or closely held private companies, funded by private and public pension funds. Venture Capital is also referred to as Risk Capital. What do they do? Venture capitalists:

• Purchase equity shares • Assist in the development of new products or services • Add value to the enterprise through active participation in management Where do they invest? Venture capitalists invest in: • First generation businesses promoted by first generation entrepreneurs. • Untried products and untested products and technology. • High risk projects that have high risk of failures but where the rewards, if successful, are

enormous. • Businesses that represent long-term investments ranging between 3 and 7 years. In short, Venture Capital is capital available for investment in the equity of an enterprise. The venturer may also park some money in debt but the distinguishing feature is that he retains some shares in the equity of the venture. But, as we will see in the later part of the Chapter, a venture capitalist is not a mere passive investor. His role is much wider.

2 (c) Step I: Present Interest rate On a loan amount of Rs.1, 89,540, annuity being Rs.50, 000, PVAF works out to 3.791 (1, 89,540/50,000). From the PVAF table for 5 years, we find that this corresponds to 10%. Step II: New rate On an identical loan amount, annuity of Rs. 36,408 for seven years results in a PV AF of 5.206, (1, and 89,540/36,408). From PVAF table for 5 years, we find that this corresponds to 8%. Step III: Base case decision Interest rate is prima facie beneficial. Step IV: Additional charges to be incurred are (a) Swap charges Rs.12, 000 (b) Processing fee 3% on loan amount Rs. 5,686 If we reckon these two factors, the IRR works out to 10.947% Step V: Evaluation & Decision Implicit interest rate on existing loan is 10%, while proposed loan is at 10.947%. Proposed loan is more expensive. Do not swap.

ME29 / Prime / Final 6

3 (a) An analysis We have to first determine the equity Beta of HS (using geared-ungeared Beta model). Estimated Beta value of HS will lead us assess the expected return on equity (Ke) of HS, from which, market price can be estimated by applying dividend growth model. Bid price will be at a 15% discount on the estimated listing price. Step 1:

(a) Unlevered Beta value β

Determination of Beta for HS

u = β

−+ )1( tDebtEquity

Equityg

If Equity = 1, then, Debt = 1 x (1/8) = 0.125

βu

125.1100= 1.44

βu

(b) Beta value for the leverage of HS (β

= 1.28

g

Β

assumed as X)

g = β 71.1)1(=

−+Equity

tDebtEquityu

Βg

75.01 = 1.28

Βg = 1.71

Expected Beta value of HS = 1.71 Step 2: E(r) of HS using CAPM [E(RHS) = Rf + βA (Rm – Rf)] = 6 + 1.71 (14 – 6) = 19.68% Step 3: Market price using dividend growth model Current year earnings Rs.50 per share (30 lacs/60,000) DPS0 Rs.25 per share DPS1 (25 x 1.05) Rs.26.25 Capitalisation rate Rs. (Ke – g) = 19.68 – 5 = 14.68% Market price 178.81 Step 4: Assessing price payable (estimated market price less 15% discount) = 178.81 x 85% = 151.9925 (or say Rs.152) Step 5: Value of the firm Estimate of price payable Rs.152 per share Number of shares 60,000 Price payable (60,000 x 152) = Rs.91,20,000 Or say Rs.91.20 lacs Recommendation: Maximum price payable by Imperial for acquisition of HS is Rs.91.20 lacs

ME29 / Prime / Final 7

3 (b) Net Asset Value (NAV): Each day, the mutual fund computes the net asset value of the unit. The NAV of a mutual fund is the amount which a unit holder would receive if the mutual fund were wound up that day. This value is obtained by deducting the total liabilities of the fund from the closing market value of the holdings and dividing it by the number of units outstanding. The NAV is the fund’s single most important number. If the value of the investment in the fund’s portfolio goes up, other things remaining equal, the value of the fund, and hence the net asset value of the unit, increases. Similarly if the value of the investment holdings in the fund’s portfolio comes down, the value of the fund and hence the net asset value of the fund, will come down. Thus, the net asset value per unit fluctuates every time any asset experiences a change in its market price.

4 (a) Part (i)

• Futures to be sold = Hedge ratio x [ Units of spot position requiring hedging / No of units underlying one futures contract]

since you are long on the spot market, you have to go short in the futures market. Hence you have to sell NIFTY.

= 0.7 x 1200 / 200 = 4.2

Part (ii)

• If the price of KM falls by 10%, it means it has fallen from Rs 150 to Rs 135 ie by Rs 15. Consequently the index will fall by 15/0.7 ie 21.429. It will fall to 1378.571 index points.

Price falls

• Since your stock fell by Rs 15, on your 1200 shares you have lost 1200 x 15 = Rs 18000.

• You have sold 4.2 contracts in index futures. You have gained 21.429 points. You have gained 4.2 x 200 x 21.429 = Rs 18000.

• Your gain is offset by your loss.

Part (iii)

• If the price of KM goes up by 5%, it means an increase of Rs 150 x 0.05 = Rs 7.5.

Price Increase

Consequently the index will rise by 7.5/0.7 ie 10.714 and will touch 1410.714 • Since your stock rose by 5% or Rs. 7.50, on your 1200 shares you gained 1200

x 7.5 = Rs 9000. • You have bought 4.2 contracts in index futures. You lost 10.714 points. Your total

loss on the futures is 4.2 x 200 x 10.714 = Rs 9000 • Your gain is offset by your loss.

4 (b) Part (i) Computation of expected return of a portfolio

Computation of β of portfolio, based on value-weightage. Value weight proportions are 10:20:16:14 Value weighted Beta would therefore be 1.3125 (shown below)

ME29 / Prime / Final 8

Security Amount

Invested Weighted Investment

β Wt * β

A 10000 0.17 0.80 0.1360 B 20000 0.33 1.20 0.3960 C 16000 0.27 1.40 0.3780 D 14000 0.23 1.75 0.4025 60000 1.00 Σ Wt. β = 1.3125

Applying CAPM. Expected return can be ascertained as follows: Rj = Rf + β x (Rm – Rf) = 4.25 + 1.3125 (11-4.25) = 4.25 + 1.3125 (6.75) Rj = 13.11% Part (ii)

Security

Re-computation of Beta of security B is substituted by a risk free investment. Beta for a risk free investment is zero, (RBI Bonds)

Amount invested

Weighted investment

β Wt x β

A 10000 0.17 0.80 0.1360 RBI Bonds 20000 0.33 0 0 C 16000 0.27 1.40 0.3780 D 14000 0.23 1.75 0.4025 60000 1.00 Σ Wt. β - 0.9165

Beta of new portfolio, in which RBI bond has been included is: 0.9165 Applying CAPM. Expected return can be ascertained as follows: Rj = Rf + β x (Rm – Rf

100%15%16055.01(

1×

+×−

) = 4.25 + 0.9165 (11-4.25) Expected Return on revised Portfolio = 10.44%

4 (c) Return required =

(i.e.) 18.43%.

4 (d) Spread: You will not be able to buy foreign currency from a bank at the same rate at which you can sell the same currency to it. This is because the bank whose business it is to buy and sell will have to make a margin to cover costs and make a small profit. For that matter, this is normal of any business. This difference between the banks’s buying rate (bit rate) and the bank’s selling rate (ask rate) is called the “spread”. If the bid rate for ∈ is Rs.50 and the ask rate is 52, the spread will be Rs2. The following two factors determine the size of the spread.

• Stability of the exchange rate:

•

If the exchange rate is expected to be stable, the spread will be narrow. If the exchange rate is volatile, the spread will be wider. Depth of the market:”Depth” refers to the volume of transactions in the market. A “deep” market has a high volume of transactions with several dealers simultaneously engaged in transacting business. In this case, the spread will be

ME29 / Prime / Final 9

narrower than for a “thin” market where there is a low volume of transactions and a few dealers.

5 (a) Part (i):

000,50,28

000,00,20==

Bonus issue W.N: 1 Current number of shares

shares.

W. N: 2 Bonus issue = 1:5 Therefore, number of shares to be issued = 50,000 shares. W.N: 3 Equity account A sum of Rs.4,00,000 (50,000 x 8) will be transferred from Retained Earnings to equity share capital. W.N: 4 No of shares outstanding = Current no of shares + Bonus shares = 2,50,000 + 50,000 = 3,00,000. W.N: 5 New P

share.per 50.000,00,3

60000,50,2S N

P S 0 Rs=×

=+×

=

0

Part (ii):

000,00,54

8000,50,2Value Face

Value Face Old shares of nos. =

×=

×=

NewOld

Stock split A 2:1 stock split means 2 shares will be issued for every one share held. W.N: 1 New nos. of shares

W.N: 2 Equity account

There will be no change in the equity account. Face value will drop to Rs. 4.218 Rs=×

W.N: 3 New P

share.per 30.000,00,5

60000,50,2shares ofnumber New

P Old shares ofnumber 0 RsOld

=×

=×

=

0

Part (iii):

shares. 000,25,116

8000,50,2=

×=

Reverse split A 1:2 reverse split means one share will be issued for every two shares held. W.N: 1 Number of Shares

Shares outstanding = 1, 25,000.

ME29 / Prime / Final 10

W.N: 2 Equity account There will be no change in the equity account. Face value will rise to 8 x 2 = Rs. 16 per share. W.N: 3

New share.per 120.000,25,1000,50,2

0 RsP ==

Summary: Particulars Shares (Nos) Equity A/c impact Market Price

Rs. (a) Existing 2,50,000 Not Applicable 60 (b) Bonus issue 3,00,000 24,00,000 50 (c) Stock split 5,00,000 FV at Rs.4 30 (d) Reverse split 1,25,000 FV at Rs.16 120

5 (b) The constant dividend model had its fair share of advantages and disadvantages. It was okay a company with stable earning. But not all companies can enjoy that advantage of stable earning. At the same time companies would like to offer a promised minimum dividend. The constant dividend plus approach does just this. Under this approach a fixed low dividend per share is always payable. An additional dividend per share in the form of either interim dividend or special dividend is than paid in years of good profits. In years of not so good profits the extra or special dividend is not paid. Advantages . A minimum return is guaranteed in line with the constant dividend plan. . Dividends are linked to profits in line with the constant payout plan. In a sense, one

enjoys the best of both the plans!

5 (c) Straddle 1. Straddles involve simultaneous purchase or sales of options with the same strike price and

same expiry date. 2. There are two types of straddles – Long and Short

a. In a long straddle you buy a call and buy a put (same number of calls and same number of puts) at the same exercise price and same expiry date.

b. In a short straddle you write a call and write a put (same number of calls and same number of puts) at the same exercise price and same expiry date. This is also called straddle write.

3. The implications are as follows: a. A long straddle will produce a limited loss zone in the middle ground; an increasing

profit zone in the upper ground and an increasing profit zone in the lower ground. In other words, if the market price moves away from the exercise price by an amount which is greater than the cost of the initial position, unlimited profits will be made. If it falls within the range, limited losses will be incurred. This strategy will be profitable if the

ME29 / Prime / Final 11

stock’s price moves above or below the strike price to a degree greater than the total cost of buying options.

b. A short straddle (aka straddle write) creates an opening credit position because it involves writing options. If the market price moves away from the exercise price by an amount which is greater than the initial credit, unlimited losses will be made. In the middle ground profits will be made. This strategy will be profitable if the stock’s price does not move above or below the striking price to a degree greater than the total proceeds received by the investor.

What should you do? You should do long straddle if you believe that the stock will either jump steeply or fall steeply. You should do short straddle if you believe that the stock will move within a narrow range. You should however remember that if the stocks move out of this narrow range you would lose heavily in a straddle write. Gross Payoff on Straddle

S ≤ E S > E Long Straddle E – S S – E Short Straddle S - E E - S

Note: Gross payoff adjusted for net premium received or paid gives net payoff. Where: S = Spot price; E = Exercise price

6 (i) Diversifiable risk or Unsystematic risk:

This risk affects only the particular security and is hence specific to the security. It is therefore also called Specific risk. For instance, an increase in the price of bamboo (Which is the raw material for making paper) will affect the fortune of a paper manufacturing company but will have no effect on the fortunes of a cement manufacturing company. This is a risk specific to the paper industry. Specific risk is the “contribution” per se of one security to the risk of a portfolio of securities and is therefore distinct for each individual investment. Such a risk can, by careful efforts at diversification, be reduced. Math Formula: Since there are only two types of risks, the value for under systematic risk is “total risk” less “systematic risk”. Non-diversifiable or systematic risk: This risk cuts across industries and affects all companies operating in the market. It is therefore also called portfolio risk or market risk. It is the risk that an entity’s cash flows may be affected by factors that are beyond the control of the management of entity. For example, changes in interest rate, inflation, taxation etc. affect all companies. Non-diversifiable risk reflects the sensitivity of an entity’s revenue to changes in macro-economic factors and depends on the degree of sensitivity of costs to total revenue. An entity with low revenue- sensitivity, i.e., where the revenues are relatively stable, will carry a low- risk relative to another with high revenue sensitivity.

ME29 / Prime / Final 12

Math Formula: The value of systematic risk is the product of two elements. One is the correlation between the stock and the Market.(Corrjm ).The other is the relationship between risk element in stock and risk element in stock market. (σj) This can be expressed as σj x Corrjm. . σm (σm

•

)

6 (ii) “An option is a contract between two parties under which the buyer of the option buys the right and not the obligation to buy or sell, a standardized quantity (contract size) of a financial instrument (underlying asset) at or before a pre determined date (expiry date) at a price, which is decided in advance (exercise price or strike price).” When the option gives the buyer of the option the right to buy it is called a call option. When the option gives the buyer of the option the right to sell it is called a put option. For providing the option the writer charges a price. We now proceed to break this definition down threadbare.

Right:•

An option is a derivative instrument involving a “right”. Holder and Writer:

•

One party “buys” the right and the other party “Sells” the right. The one who buys the right is called the “buyer” or the “holder” of the option. The one who sells the right is called the “Seller” or the “Writer” of the option. Call and put option:

•

The right can be the “right to buy” an underlying asset. Such a right is called a “Call option”. The right can be the “right to sell” an underlying asset. Such a right is called a “Put option”. Obligation:

•

The holder can demand performance; he is not obliged to perform. In contrast, the writer is obliged to perform; he cannot demand performance. Exercise price:

•

The price at which the underlying asset can be bought or sold, as the case may be, is called the exercise price. The exercise price is also referred to as the strike price. Expiry date:

•

The date by which the right should be exercised is called the expiry date. Option premium: When the buyer buys a right (either the right to buy or the right to sell) he has to pay the writer a price. this is called the option premium or option price.

The Right Example: The rights offer by a company is a typical example of an option. The rights offer gives the shareholder the right to subscribe. It does not compel him to subscribe. The shareholder buys the right to buy i.e. the right to subscribe. He is therefore the holder of the option. The company sells the option. It is therefore the writer of the option. This is a call option because the shareholder buys the right to buy shares. The rights price is the exercise price. The rights closure date is the expiry date. There is no option premium involved. Features:

a. Standardization: Like futures, the contract is standardized as to quantity, date and month of delivery, price, minimum amount by which price would move.

The features of an option contract are very similar to that of a futures contract except that only one of the two parties is obliged to perform.

ME29 / Prime / Final 13

b. Deal with the clearinghouse: The clearinghouse guarantees performance. Consequently there is no risk of default.

c. Mark to market margin: Since the clearinghouse acts as a guarantor, it would require the parties to maintain a deposit (margin) with it.

6 (iii) Short selling: Short selling involves selling a stock which you don’t own and buying it back later to square the position. A short seller resorts to this strategy because he expects prices to fall and wants to benefit from the fall. In a falling market this is a good way to make money. Consider this example. WIPRO is quoting at Rs 2400. You feel that the stock is overpriced and expect it to fall to Rs 2100 in a month’s time. The only way to gain in a falling market is to make sale. But you do not have WIPRO shares. You therefore elect to sell now and buy it back a month later and thereby profit Rs 300 per share. Since you don’t have shares and delivery has to be made within 2 days of the transaction, your broker borrows shares on your behalf and delivers them. This is called stock lending. You are required to pay stock lending charges. The concept of short selling is central to a number of futures and options strategies which we will outline later.

6 (iv) Global Depository Receipts (‘GDRs)

(a) The shares underlying the depository receipts do not carry voting rights.

: Many large Indian corporate entities have been able to tab global equity market to raise foreign currency funds by way of equity, through this route of issuing GDRs. An Indian company issues ordinary equity shares. These shares are “deposited” with custodian banks (mostly domestic banks). Custodian Banks establish a link with a Depository bank overseas. Depository bank, in turn issues Depository Receipts in US dollars. Funds are raised when overseas entities purchase these depository receipts, at a agreed price. The important characteristics are:

(b) The instruments are freely traded (listed in Luxemburg or other permitted Exchanges).

(c) They are marketed globally, without being confined to borders of any market or country (it can be traded in more than one currency).

(d) Investors (mostly institutional investors) earn fixed income by way of dividends (dividends are paid in issuer- currency, converted into dollars by depository and paid to investors, and hence exchange risk is with investor).

(e) The GDRs can be converted into underlying shares, by Depository/ Custodian banks redeeming the issue, with reference to price prevailing in NSE or BSE. At times, reverse- conversion (conversion of underlying shares into GDRs) is also permitted, though this area is not yet open to Indian companies.

ME29 / Prime / Final 14

6 (v) Zero-Coupons

1. Zero Coupon Bonds are debt instruments (in the nature of secured or unsecured debentures) evidencing loans borrowed for a given period.

:

2. The special feature of such bonds is that the borrower does not pay any interest during the “tenor” of the loan.

3. The bonds are issued at fore value and redeemed at a premium on face value. The premium represents the compensation the investor receives over tenor of the bond by way of compounded interest.

4. From the borrower’s point of view there is no cash outflow to cover interest, while from the investor’s point of view, the instrument provides little or no liquidity unless traded in the market.

5. In a scenario of reducing interest rates, the yield on Zero coupon bonds would be higher than what the market would otherwise offer, and the converse applies when interest rates begin to rise after the issue of Zero Coupon Bonds.

6 (vi) INTEREST RATE FUTURES (IRF)

1.

: Meaning: A Futures contract is, by definition, a forward contract, which trades on the exchange. IRF involves a national purchase and sale of a bond at the traded price and a notional delivery of the underlying asset on the specified expiry date. IR Futures are available in major currencies (US $, Sterling, Yen, Euros, Sw. Franc etc). These contracts can be used in both lending and borrowing situations. Why IRF: A CFO is generally faced with two different situations. Having tied his company to fixed interest rate, he might now expect interest rates to fall. Alternatively having tied the company to floating rates, he might now expect interest rates to rise. Both these will put him in difficulty. To overcome them he might trade in IRF. Central to understanding this is the principle of interest rate risk. When interest rates fall, instruments that offer higher coupon rates rise in value. When interest rates rise, instruments that offer lower coupon rates will fall in value. A couple of examples will help understand this.

Have a view that interest rates will fall:

2.

Suppose the current implied interest rate is 6%. He expects the interest rate to fall to say 5%. Suppose 1 contract = 2000 units. He buys one futures contract at say Rs 55.5. Suppose a few days later the implied interest rate falls to 5%. The IRF quotes Rs 60.8 in the market. He sells and gains Rs 60.8-55.5=5.3 per unit. On 2000 units he scores 2000 x 5.3 = Rs 10,600/- Have a view that interest rates will rise:

This derivative instrument comes as a useful means of hedging risk against the risk of the interest rate movements.

Suppose the current implied interest rate is 5%. The CFO expects the interest rate to climb. Suppose the current market price of a IRF is Rs 61. He sell one futures contract at Rs 61. Suppose a few days later the implied interest rate raises to 5.3% and the IRF quotes Rs 59. He buys one IRF and pockets the difference of Rs 2 per unit or Rs 4000 in all.

ME29 / Prime / Final 15

It must be noted that when you contract for 3-month interest rate futures for Euro 1 million, You are merely laying out an interest rate at which you will either borrow or lend Euro 1 million, beginning March. Commencement of the period of notional landing or borrowing is synchronized with the maturity of IRF. To understand that we should take a look at the following features which are relevant?

1. Period:

2.

IRF is standardized with reference to period. There are two types of IRF – short term and long term. The former runs for a three-month cycle, the latter for one year. Contract Size:

3.

The Contract Size standardized and depends on the currency. For example, for a short-term 3-month contract, sizes for USD, Euros and sterling is 1 million each. For Swiss Franc the size is 500,000. /-. For the INR it is Rs 200,000 irrespective of whether it is short term or long term. Rate of interest:

4.

The rate of interest is in built into the price of the futures contract. The price of IR- Futures is “100 minus interest rate”. If you buy an IRF quoted at 93.25, you would be dealing in an interest rate of 6.75% p.a. (100.00-93.25) Profit or loss:

5.

The profit or loss in a futures contract is represented by a TICK. A tick means a 0.01% “interest” on the amount represented by the contract size. This is also the minimum movement in price. If the contract size is 500,000, the value of a tick for a three month contract will be 12.50.[500,000 x 0.01 % x 3/12] Obligations:

6.

When you buy an IRF, You will be contracting to buy an “entitlement” to receive interest payment on a notional amount in a given currency Conversely, when you sell an IRF, you are making a promise to undertake an interest-payment obligation on a notional amount in a given currency Buying could be considered the equivalent of investing and selling the equivalent of borrowing. On maturity:

IRFs are closed out by the contracting party, by taking an opposite position. This part can be closed out with the following principles

• If you have an asset portfolio and expect interest rates to fall, you will buy IRF • If you have an asset portfolio and expect interest rates to rise, you will sell IRF • If you have a liability portfolio and expect interest rates to fall, you will sell IRF • If you have a liability portfolio and expect interest rates to rise, you will buy IRF

Interest Rate Expectation Asset Liability Down Up

Buy Sell

Sell Buy

1 ME29 / Prime / Final

AAPC

Number of Pages : 3 Total Marks: 100 Number of questions: 7 Time Allowed: 3 Hrs

Answer Question Nos. 1 and 2 and four from the rest.

1. As a statutory auditor, how would you deal with the following:

(a) Vishwak Ltd. has announced a voluntary retirement plan for its employees on January 1,

2008. The scheme is scheduled to close on June 30, 2008. The scheme envisaged an initial lump sum payment of maximum of Rs.2 lakhs and monthly payments over the balance period of service of employees coming under the plan. 200 employees opted for the scheme as on March 31, 2008. The total lump sum payment for these employees would be Rs.250 lakhs and the aggregate of future payments to them would amount to Rs.1,500 lakhs. However, no payment had been made to the employees under the scheme up to March 31, 2008, nor the company made any provision in its accounts towards any liability under the scheme.

(b) War Ltd. has borrowed Rs.25 crores from financial institutions during the financial year 2007/08. These borrowings are used to invest in shares of Peace Ltd. a subsidiary company which is implementing a new project estimated to cost Rs.50 crores. As on 31st March, 2008, since the said project was not yet complete, the directors of War Ltd. resolved to capitalize the interest on the borrowings amounting to Rs.3 Crores and add it to the cost of investments. As a statutory auditor for the year ended 31st

March 2008, how would you deal with this matter?

(c) Mr. Vijay is appointed as the auditor of KINGS Travels Ltd. with audit fees of Rs. 35,000. He purchased air ticket from Delhi to Kolkata and back for Rs.18, 000 from the client for his personal work and the amount remains unpaid at the end of the year as it is a general practice of the client to give credit to all. Mr. Vijay claims that he does not incur any disqualification as contained in Section 226(3)(d) of the Companies Act. How would you deal with the following, as a statutory auditor?

(d) Mr. Anand, who conducts the tax audit u/s 44AB of the Income-Tax Act, 1961 of M/s

ABC, a partnership firm has received the entire audit fees of Rs.25,000 in April 2008 in respect of the tax audit for the year ended 31.3.2008. The audit report was however signed in September, 2008.

(4 x5 = 20 Marks)

2 ME29 / Prime / Final

2. Comment on the following with reference to the Chartered Accountants Act, 1949 and schedules there to:

(a) Mr.Rajesh, a Chartered Accountant in practice has been elected as the treasurer of a Regional Council of the Institute. The Regional Council had organized an international tour through a tour operator during the year for its members. During the audit of the Regional Council, it was found that Mr. Rajesh had received a personal benefit of Rs.50,000 from the tour operator.

(b) CA Damodaran, a Chartered Accountant prepared a project report for one of its clients

to obtain bank finance (long-term) of Rs.50 lakhs from a Commercial Bank. Consequent to the sanction of the loan by the bank CA Damodaran raised a bill for his services @ 2% of the loan sanctioned.

(c) P, a Chartered Accountant had accepted appointed as an auditor of QRS Company

Limited without ascertaining from the Company whether the requirement of Sections 224 and 225 of the Companies Act had been complied with. However, he realized this defect only after acceptance.

(d) M/s. ABC, a firm of Chartered Accountants has taken a loan for acquiring computers,

from a company whose Managing Directors’ son is an Articled Trainee with A, a partner of M/s ABC.

( 4 x 4 = 16 Marks)

3 (a) AS a branch auditor of a nationalized bank, how would you verify the following?

1) Advances to DOT COM Companies. 2) Balances in account of a bank situated in a foreign country.

(b) Explain the Auditor’s liability in case of unlawful acts or defaults by clients. ( 4 + 4 + 8 = 16 Marks)

4 (a) Enumerate the ‘ Basic Elements of Audit Report’ as enshrined in AAS-28.

(b) Briefly discuss the compliance procedures and their use in evaluation of internal controls. ( 2 x 8 = 16 Marks)

5. Answer the following:

(a) Mention the difference between ‘report’ and ‘certificate’. (b) What are the contents of reports and certificates for special purposes? (c) For what purposes the Cost Auditor refers to financial records while conducting Cost

Audit of an entity? ( 4 + 6 + 6 = 16 Marks)

3 ME29 / Prime / Final

6. (a) Answer in brief : Sampling Risk (b) Explain what is meant by “Representations by Management” and indicate to what extent an

auditor can place reliance on such representations. (c) State the reporting responsibility of an auditor in the context of non-compliance of Law and

Regulation in a audit of Financial Statement. ( 4 + 6 + 6 = 16 Marks)

7. Write short notes on the following:

(a) Rolling Settlement

(b) Preliminary Report under Peer Review

(c) Human Resource Accounting

(d) Probable format of environmental statement.

( 4 x 4 = 16 Marks)

1 ME29 / PRIME / FINAL

PRIME ACADEMY

29TH

a. Those which provide further evidence of conditions that existed at the balance sheet date; and

SESSION – MODEL EXAM

ADVANCED AUDITING AND PROFESSIONAL ETHICS – NEW SYLLABUS

SUGGESTED ANSWERS

1 (a) Accounting Standard (AS) -4 (Revised) on ‘Contingencies and Events Occurring After the Balance Sheet Date’ states that events occurring after the ‘balance sheet date are those significant events, both favourable and unfavourable, that occur between the balance sheet date and the date on which the financial statements are approved by the Board of Directors in the case of a company, and, by the corresponding approving authority in the case of any other entity.

Two types of events can be identified as:

b. Those which are indicative (of conditions that arose subsequent to the balance sheet date).

It further states that assets and liabilities should be adjusted for events occurring after the balance sheet date that provide additional evidence to assist the estimation of amounts relating to conditions existing at the balance sheet date or that indicate that the fundamental accounting assumption of going concern (i.e., the continuance of existence or substratum of the enterprise) is not appropriate.

As per facts of the case, a condition existed on the balance sheet date (31st

As per Accounting Standard 13 on “Accounting for Investments”, the cost of investment includes acquisition charges such as brokerage, fees and duties. In the instant case, War Ltd. has used borrowed funds for making investment in shares of a subsidiary company. For acquiring shares of a subsidiary company, apart from any fees, duties etc. there are no cost incurred for investing in shares. Hence, any borrowing costs incurred cannot be treated as part of cost of investments and cannot be added to the cost of investments. The Accounting Standard 16 on “Borrowing Costs” also does not consider investment in

March, 2008) regarding the liability towards the Voluntary Retirement Plan (VRP) since the management started the VRP in the month of January, 2008 and 200 employees opted for the VRP as on March 31, 2008. Since it was probable that future events will confirm that a liability has been incurred on the balance sheet and that the amount could be estimated on reasonable basis, a provision for payments under the VRP would be required to be made for an appropriate amount for the aforesaid number of employees.

(b) Capitalisation of interest on Borrowings in respect of Investments:

2 ME29 / PRIME / FINAL

shares as qualifying assets that can enable a company to add the borrowing costs to investments. In the instant case therefore, the statutory auditor would qualify his report by stating that the borrowing costs have been wrongly added to the cost of investments rather than charging them to the profit and loss account. The effect of the same on the profit for the year would also have to be mentioned in the audit report.

(c) Disqualification of auditors: