quantity theory of money - randycragun.comrandycragun.com/courses/3150lectures/lecture8.pdf ·...

TRANSCRIPT

Quantity Theory of Money

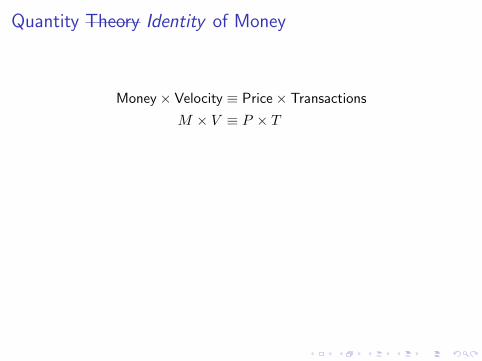

Quantity Theory Identity of Money

Money× Velocity ≡ Price× Transactions

M × V ≡ P × T

How many dollars we need for our purchases depends on howquickly dollars move around

Example

I Buy 10 hats

I at $2 each

I Have $5 of money in the economy

I What is V ?

Quantity Theory Identity of Money

Money× Velocity ≡ Price× Transactions

M × V ≡ P × T

How many dollars we need for our purchases depends on howquickly dollars move around

Example

I Buy 10 hats

I at $2 each

I Have $5 of money in the economy

I What is V ?

Quantity Theory Identity of Money

Money× Velocity ≡ Price× Transactions

M × V ≡ P × T

How many dollars we need for our purchases depends on howquickly dollars move around

Example

I Buy 10 hats

I at $2 each

I Have $5 of money in the economy

I What is V ?

Quantity Theory of Money

Transactions are hard to measure

Output is similar but includes used goods

Money× Velocity = Price× Output (1)

M × V = P × Y (2)

This V : “income velocity of money”

Quantity Theory of Money

Transactions are hard to measure

Output is similar but includes used goods

Money× Velocity = Price× Output (1)

M × V = P × Y (2)

This V : “income velocity of money”

Quantity Theory of Money

Transactions are hard to measure

Output is similar but includes used goods

Money× Velocity = Price× Output (1)

M × V = P × Y (2)

This V : “income velocity of money”

Quantity Theory of Money

Transactions are hard to measure

Output is similar but includes used goods

Money× Velocity = Price× Output (1)

M × V = P × Y (2)

This V : “income velocity of money”

Quantity Theory of Money

Real money balances: MP :

how much stuff the money can buy

Money demand: function that tells us how much real moneypeople want to hold. For instance:(

M

P

)d

= kY (3)

Money demand consists of a theory about V(M

P

)d

= kY ⇐⇒M1

k= PY ⇐⇒ V =

1

k(4)

High k =⇒

{High demand for money

Low velocity

Quantity Theory of Money

Real money balances: MP : how much stuff the money can buy

Money demand: function that tells us how much real moneypeople want to hold. For instance:(

M

P

)d

= kY (3)

Money demand consists of a theory about V(M

P

)d

= kY ⇐⇒M1

k= PY ⇐⇒ V =

1

k(4)

High k =⇒

{High demand for money

Low velocity

Quantity Theory of Money

Real money balances: MP : how much stuff the money can buy

Money demand: function that tells us how much real moneypeople want to hold. For instance:(

M

P

)d

= kY (3)

Money demand consists of a theory about V(M

P

)d

= kY ⇐⇒M1

k= PY ⇐⇒ V =

1

k(4)

High k =⇒

{High demand for money

Low velocity

Quantity Theory of Money

Real money balances: MP : how much stuff the money can buy

Money demand: function that tells us how much real moneypeople want to hold. For instance:(

M

P

)d

= kY (3)

Money demand consists of a theory about V

(M

P

)d

= kY ⇐⇒M1

k= PY ⇐⇒ V =

1

k(4)

High k =⇒

{High demand for money

Low velocity

Quantity Theory of Money

Real money balances: MP : how much stuff the money can buy

Money demand: function that tells us how much real moneypeople want to hold. For instance:(

M

P

)d

= kY (3)

Money demand consists of a theory about V(M

P

)d

= kY ⇐⇒M1

k= PY ⇐⇒ V =

1

k(4)

High k =⇒

{High demand for money

Low velocity

Quantity Theory of Money

Real money balances: MP : how much stuff the money can buy

Money demand: function that tells us how much real moneypeople want to hold. For instance:(

M

P

)d

= kY (3)

Money demand consists of a theory about V(M

P

)d

= kY ⇐⇒M1

k= PY ⇐⇒ V =

1

k(4)

High k =⇒

{High demand for money

Low velocity

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory?

To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

Quantity Theory of Money

Constant V is a simplifying theory

We know of many things that will change V

I ATMs

I Credit cards

I Other changes in payment technologies

But what is the purpose of the theory? To answer questions like

I What will happen if the CB increases the money supply?

I What will happen to prices if incomes increase and the CBdoes not change the money supply?

I What are the sources of long-run inflation?

Valid theory as long as V does not change in response to Y , P , orM in the times we are studying

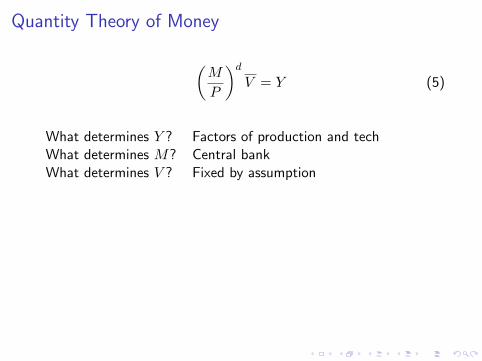

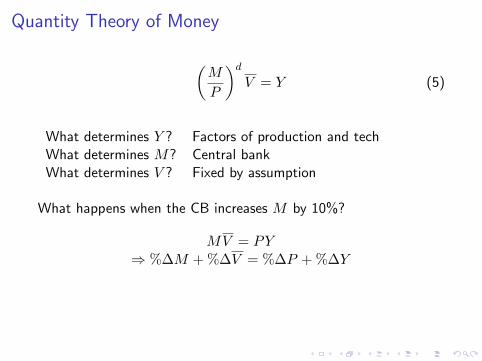

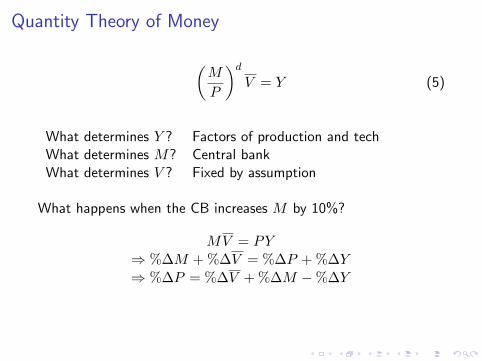

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ?

Factors of production and techWhat determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and tech

What determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

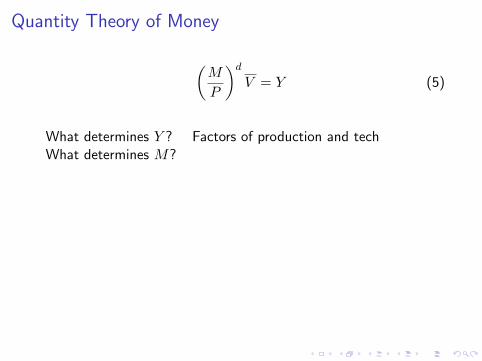

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M?

Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bank

What determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bankWhat determines V ?

Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

Quantity Theory of Money

(M

P

)d

V = Y (5)

What determines Y ? Factors of production and techWhat determines M? Central bankWhat determines V ? Fixed by assumption

What happens when the CB increases M by 10%?

MV = PY

⇒ %∆M + %∆V = %∆P + %∆Y

⇒ %∆P = %∆V + %∆M −%∆Y

⇒ π = %∆V + %∆M − g (6)

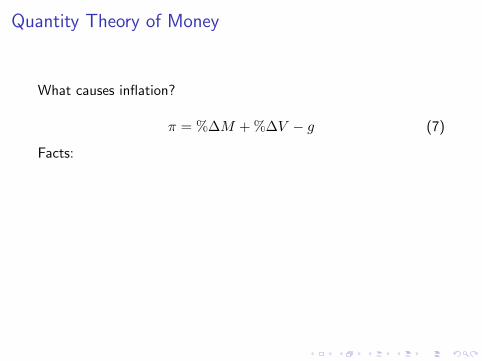

Quantity Theory of Money

What causes inflation?

π = %∆M + %∆V − g (7)

Facts:

I π ranges from -10% to trillions of percent per year

I g is usually between -2% and 10%

I V is fairly constant over time (%∆V ≈ 0)

Conclusion: “Inflation [in the long-run] is always and everywhere amonetary phenomenon” –Milton Friedman

Quantity Theory of Money

What causes inflation?

π = %∆M + %∆V − g (7)

Facts:

I π ranges from -10% to trillions of percent per year

I g is usually between -2% and 10%

I V is fairly constant over time (%∆V ≈ 0)

Conclusion: “Inflation [in the long-run] is always and everywhere amonetary phenomenon” –Milton Friedman

Quantity Theory of Money

What causes inflation?

π = %∆M + %∆V − g (7)

Facts:

I π ranges from -10% to trillions of percent per year

I g is usually between -2% and 10%

I V is fairly constant over time (%∆V ≈ 0)

Conclusion: “Inflation [in the long-run] is always and everywhere amonetary phenomenon” –Milton Friedman

Quantity Theory of Money

What causes inflation?

π = %∆M + %∆V − g (7)

Facts:

I π ranges from -10% to trillions of percent per year

I g is usually between -2% and 10%

I V is fairly constant over time (%∆V ≈ 0)

Conclusion: “Inflation [in the long-run] is always and everywhere amonetary phenomenon” –Milton Friedman

Quantity Theory of Money

What causes inflation?

π = %∆M + %∆V − g (7)

Facts:

I π ranges from -10% to trillions of percent per year

I g is usually between -2% and 10%

I V is fairly constant over time (%∆V ≈ 0)

Conclusion: “Inflation [in the long-run] is always and everywhere amonetary phenomenon” –Milton Friedman

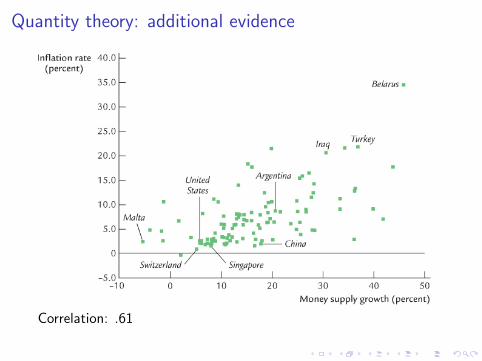

Quantity theory: additional evidence

Correlation: .79

Quantity theory: additional evidence

Correlation: .61

Quantity theory: additional evidence

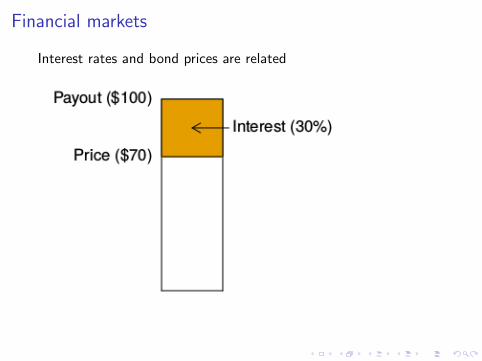

Financial markets

Interest rates and bond prices are related

If the Fed buys more bonds, what happens to interest rates?

Financial markets

Interest rates and bond prices are related

If the Fed buys more bonds, what happens to interest rates?

Financial markets

Interest rates and bond prices are related

If the Fed buys more bonds, what happens to interest rates?

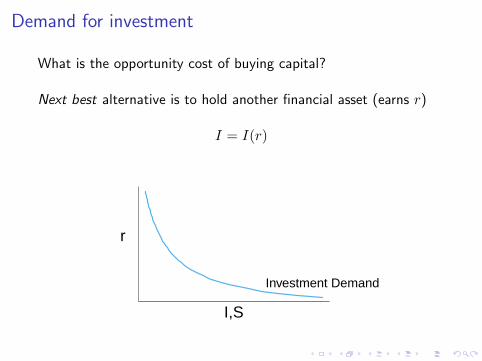

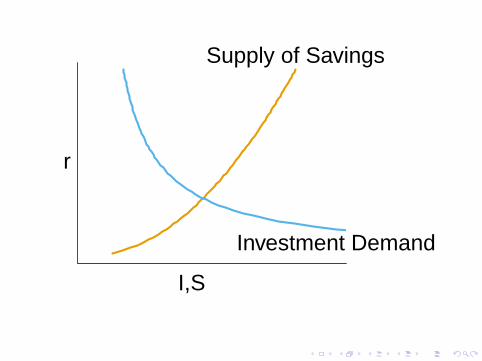

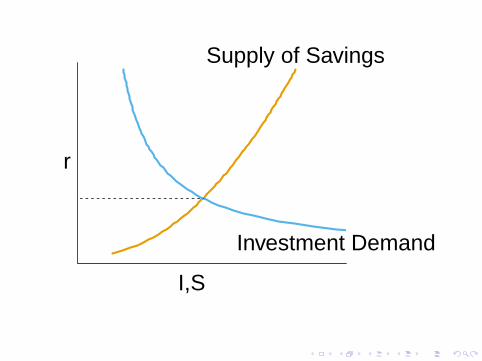

Demand for investment

What is the opportunity cost of buying capital?

Next best alternative is to hold another financial asset (earns r)

I = I(r)

Investment Demand

I,S

r

Demand for investment

What is the opportunity cost of buying capital?

Next best alternative is to hold another financial asset (earns r)

I = I(r)

Investment Demand

I,S

r

Demand for investment

What is the opportunity cost of buying capital?

Next best alternative is to hold another financial asset (earns r)

I = I(r)

Investment Demand

I,S

r

Demand for investment

What is the opportunity cost of buying capital?

Next best alternative is to hold another financial asset (earns r)

I = I(r)

Investment Demand

I,S

r

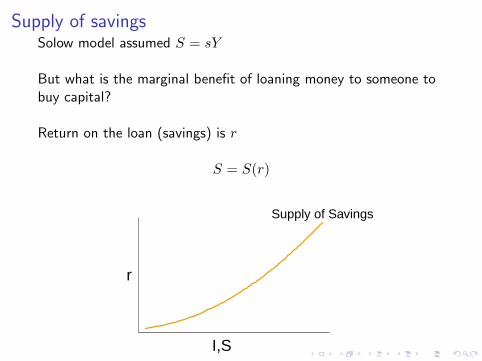

Supply of savingsSolow model assumed S = sY

But what is the marginal benefit of loaning money to someone tobuy capital?

Return on the loan (savings) is r

S = S(r)

Supply of Savings

I,S

r

Supply of savingsSolow model assumed S = sY

But what is the marginal benefit of loaning money to someone tobuy capital?

Return on the loan (savings) is r

S = S(r)

Supply of Savings

I,S

r

Supply of savingsSolow model assumed S = sY

But what is the marginal benefit of loaning money to someone tobuy capital?

Return on the loan (savings) is r

S = S(r)

Supply of Savings

I,S

r

Supply of savingsSolow model assumed S = sY

But what is the marginal benefit of loaning money to someone tobuy capital?

Return on the loan (savings) is r

S = S(r)

Supply of Savings

I,S

r

Supply of savingsSolow model assumed S = sY

But what is the marginal benefit of loaning money to someone tobuy capital?

Return on the loan (savings) is r

S = S(r)

Supply of Savings

I,S

r

Supply of Savings

Investment Demand

I,S

r

Supply of Savings

Investment Demand

I,S

r

Interest rates

You buy a bond for $100

It pays out $110 in a month

The interest rate was 10% per month

i =Pricef − Pricei

Pricei(8)

This is a nominal interest rate

A real interest rate corrects for inflation

Interest rates

You buy a bond for $100

It pays out $110 in a month

The interest rate was 10% per month

i =Pricef − Pricei

Pricei(8)

This is a nominal interest rate

A real interest rate corrects for inflation

Interest rates

You buy a bond for $100

It pays out $110 in a month

The interest rate was

10% per month

i =Pricef − Pricei

Pricei(8)

This is a nominal interest rate

A real interest rate corrects for inflation

Interest rates

You buy a bond for $100

It pays out $110 in a month

The interest rate was 10% per month

i =Pricef − Pricei

Pricei(8)

This is a nominal interest rate

A real interest rate corrects for inflation

Interest rates

You buy a bond for $100

It pays out $110 in a month

The interest rate was 10% per month

i =Pricef − Pricei

Pricei(8)

This is a nominal interest rate

A real interest rate corrects for inflation

Interest rates

You buy a bond for $100

It pays out $110 in a month

The interest rate was 10% per month

i =Pricef − Pricei

Pricei(8)

This is a nominal interest rate

A real interest rate corrects for inflation

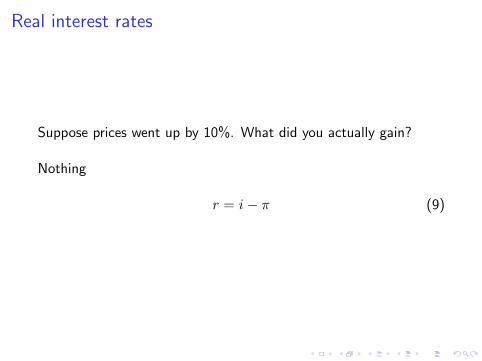

Real interest rates

Suppose prices went up by 10%. What did you actually gain?

Nothing

r = i− π (9)

Real interest rates

Suppose prices went up by 10%. What did you actually gain?

Nothing

r = i− π (9)

Real interest rates

Suppose prices went up by 10%. What did you actually gain?

Nothing

r = i− π (9)

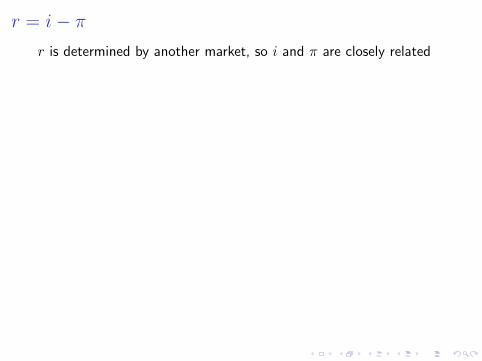

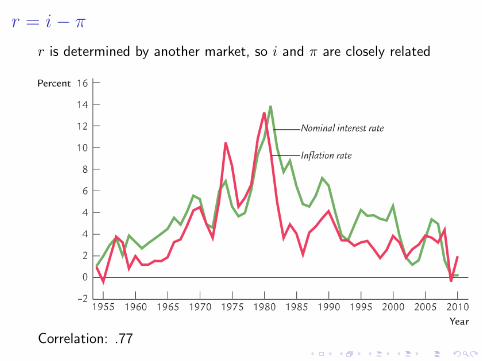

r = i− πr is determined by another market, so i and π are closely related

Correlation: .77

r = i− πr is determined by another market, so i and π are closely related

Correlation: .77

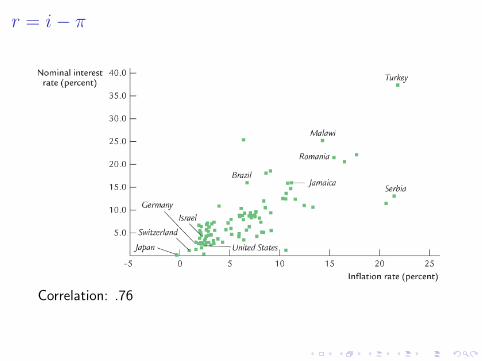

r = i− π

Correlation: .76

Ex ante (before) and ex post (after)

i = r + π (10)

Investors and lenders know what r they want

They try to choose i to get that r

But do you know what π will be this year?

Ex ante (before) and ex post (after)

i = r + π (10)

Investors and lenders know what r they want

They try to choose i to get that r

But do you know what π will be this year?

Ex ante (before) and ex post (after)

i = r + π (10)

Investors and lenders know what r they want

They try to choose i to get that r

But do you know what π will be this year?

Ex ante (before) and ex post (after)

i = r + π (10)

Investors and lenders know what r they want

They try to choose i to get that r

But do you know what π will be this year?

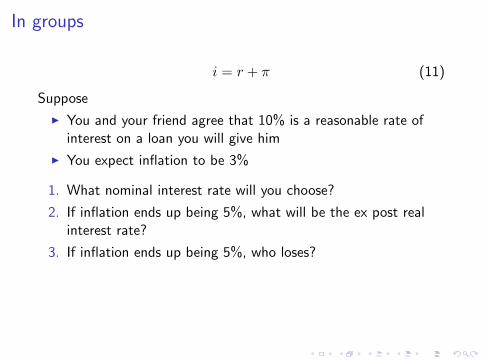

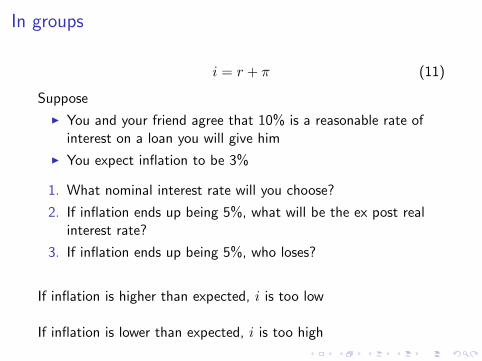

In groups

i = r + π (11)

Suppose

I You and your friend agree that 10% is a reasonable rate ofinterest on a loan you will give him

I You expect inflation to be 3%

1. What nominal interest rate will you choose?

2. If inflation ends up being 5%, what will be the ex post realinterest rate?

3. If inflation ends up being 5%, who loses?

If inflation is higher than expected, i is too low

If inflation is lower than expected, i is too high

In groups

i = r + π (11)

Suppose

I You and your friend agree that 10% is a reasonable rate ofinterest on a loan you will give him

I You expect inflation to be 3%

1. What nominal interest rate will you choose?

2. If inflation ends up being 5%, what will be the ex post realinterest rate?

3. If inflation ends up being 5%, who loses?

If inflation is higher than expected, i is too low

If inflation is lower than expected, i is too high

In groups

i = r + π (11)

Suppose

I You and your friend agree that 10% is a reasonable rate ofinterest on a loan you will give him

I You expect inflation to be 3%

1. What nominal interest rate will you choose?

2. If inflation ends up being 5%, what will be the ex post realinterest rate?

3. If inflation ends up being 5%, who loses?

If inflation is higher than expected, i is too low

If inflation is lower than expected, i is too high

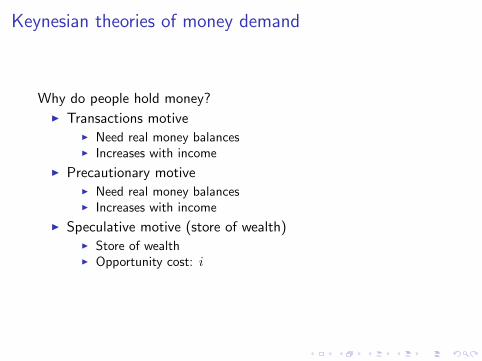

Keynesian theories of money demand

Why do people hold money?

I Transactions motive

I Need real money balancesI Increases with income

I Precautionary motive

I Need real money balancesI Increases with income

I Speculative motive (store of wealth)

I Store of wealthI Opportunity cost: i

Keynesian theories of money demand

Why do people hold money?I Transactions motive

I Need real money balancesI Increases with income

I Precautionary motiveI Need real money balancesI Increases with income

I Speculative motive (store of wealth)

I Store of wealthI Opportunity cost: i

Keynesian theories of money demand

Why do people hold money?I Transactions motive

I Need real money balancesI Increases with income

I Precautionary motiveI Need real money balancesI Increases with income

I Speculative motive (store of wealth)

I Store of wealthI Opportunity cost: i

Keynesian theories of money demand

Why do people hold money?I Transactions motive

I Need real money balancesI Increases with income

I Precautionary motiveI Need real money balancesI Increases with income

I Speculative motive (store of wealth)I Store of wealthI Opportunity cost: i

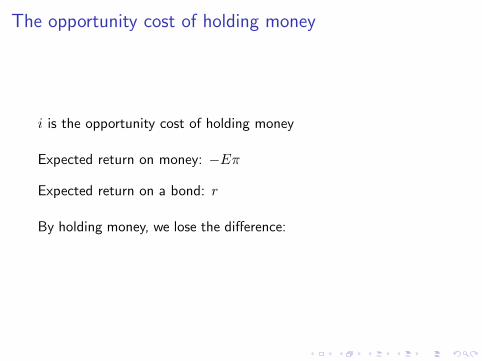

The opportunity cost of holding money

i is the opportunity cost of holding money

Expected return on money: −Eπ

Expected return on a bond: r

By holding money, we lose the difference: r− (−Eπ) = r+Eπ = i

The opportunity cost of holding money

i is the opportunity cost of holding money

Expected return on money:

−Eπ

Expected return on a bond: r

By holding money, we lose the difference: r− (−Eπ) = r+Eπ = i

The opportunity cost of holding money

i is the opportunity cost of holding money

Expected return on money: −Eπ

Expected return on a bond: r

By holding money, we lose the difference: r− (−Eπ) = r+Eπ = i

The opportunity cost of holding money

i is the opportunity cost of holding money

Expected return on money: −Eπ

Expected return on a bond:

r

By holding money, we lose the difference: r− (−Eπ) = r+Eπ = i

The opportunity cost of holding money

i is the opportunity cost of holding money

Expected return on money: −Eπ

Expected return on a bond: r

By holding money, we lose the difference: r− (−Eπ) = r+Eπ = i

The opportunity cost of holding money

i is the opportunity cost of holding money

Expected return on money: −Eπ

Expected return on a bond: r

By holding money, we lose the difference:

r− (−Eπ) = r+Eπ = i

The opportunity cost of holding money

i is the opportunity cost of holding money

Expected return on money: −Eπ

Expected return on a bond: r

By holding money, we lose the difference: r− (−Eπ) = r+Eπ = i

Money demand

(M

P

)d

= L (i, Y ) (12)

L is for “liquid”

Velocity is not constant

Money demand

(M

P

)d

= L (i, Y ) (12)

L is for “liquid”

Velocity is not constant

Money demand

(M

P

)d

= L (i, Y ) (12)

L is for “liquid”

Velocity is not constant

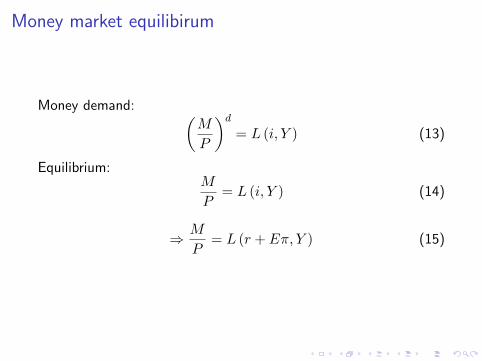

Money market equilibirum

Money demand: (M

P

)d

= L (i, Y ) (13)

Equilibrium:M

P= L (i, Y ) (14)

⇒ M

P= L (r + Eπ, Y ) (15)

Money market equilibirum

Money demand: (M

P

)d

= L (i, Y ) (13)

Equilibrium:M

P= L (i, Y ) (14)

⇒ M

P= L (r + Eπ, Y ) (15)

Money market equilibirum

Money demand: (M

P

)d

= L (i, Y ) (13)

Equilibrium:M

P= L (i, Y ) (14)

⇒ M

P= L (r + Eπ, Y ) (15)

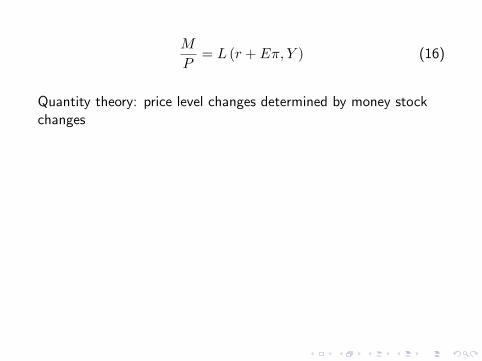

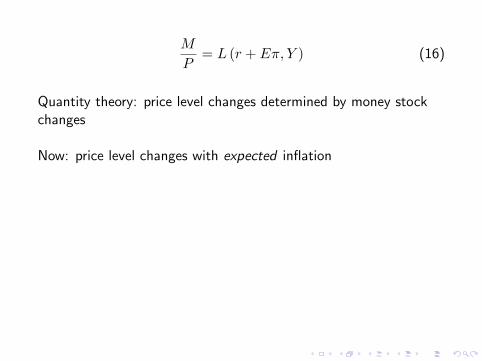

M

P= L (r + Eπ, Y ) (16)

Quantity theory: price level changes determined by money stockchanges

Now: price level changes with expected inflation

If the Fed tells us that there will be more inflation

I Demand for real money balances will fall

(opp. cost of money, i, increased)

I Supply of real money balances must fall in equil.

I The price level will rise

One way to fight inflation: convince people it is not happening

M

P= L (r + Eπ, Y ) (16)

Quantity theory: price level changes determined by money stockchanges

Now: price level changes with expected inflation

If the Fed tells us that there will be more inflation

I Demand for real money balances will fall

(opp. cost of money, i, increased)

I Supply of real money balances must fall in equil.

I The price level will rise

One way to fight inflation: convince people it is not happening

M

P= L (r + Eπ, Y ) (16)

Quantity theory: price level changes determined by money stockchanges

Now: price level changes with expected inflation

If the Fed tells us that there will be more inflation

I Demand for real money balances will fall

(opp. cost of money, i, increased)

I Supply of real money balances must fall in equil.

I The price level will rise

One way to fight inflation: convince people it is not happening

M

P= L (r + Eπ, Y ) (16)

Quantity theory: price level changes determined by money stockchanges

Now: price level changes with expected inflation

If the Fed tells us that there will be more inflation

I Demand for real money balances will fall

(opp. cost of money, i, increased)

I Supply of real money balances must fall in equil.

I The price level will rise

One way to fight inflation: convince people it is not happening

M

P= L (r + Eπ, Y ) (16)

Quantity theory: price level changes determined by money stockchanges

Now: price level changes with expected inflation

If the Fed tells us that there will be more inflation

I Demand for real money balances will fall

(opp. cost of money, i, increased)

I Supply of real money balances must fall in equil.

I The price level will rise

One way to fight inflation: convince people it is not happening

M

P= L (r + Eπ, Y ) (16)

Quantity theory: price level changes determined by money stockchanges

Now: price level changes with expected inflation

If the Fed tells us that there will be more inflation

I Demand for real money balances will fall

(opp. cost of money, i, increased)

I Supply of real money balances must fall in equil.

I The price level will rise

One way to fight inflation: convince people it is not happening

M

P= L (r + Eπ, Y ) (16)

Quantity theory: price level changes determined by money stockchanges

Now: price level changes with expected inflation

If the Fed tells us that there will be more inflation

I Demand for real money balances will fall

(opp. cost of money, i, increased)

I Supply of real money balances must fall in equil.

I The price level will rise

One way to fight inflation: convince people it is not happening

M

P= L (r + Eπ, Y ) (16)

Quantity theory: price level changes determined by money stockchanges

Now: price level changes with expected inflation

If the Fed tells us that there will be more inflation

I Demand for real money balances will fall

(opp. cost of money, i, increased)

I Supply of real money balances must fall in equil.

I The price level will rise

One way to fight inflation: convince people it is not happening

Portfolio theory of money demand

(M

P

)d

= L (i, Y ) (17)

This is missing some pieces

I Wealth

I Wealth 6= incomeI Mishkin claims that increase in wealth has a smaller impact in

money demand than increase in income

I Risk

I How safe is money?I ↑Risk ⇐= ↓money demandI ↑Riskiness of other assets ⇐= ↑money demand

I Relative liquidity

Portfolio theory of money demand

(M

P

)d

= L (i, Y ) (17)

This is missing some piecesI Wealth

I Wealth 6= incomeI Mishkin claims that increase in wealth has a smaller impact in

money demand than increase in income

I Risk

I How safe is money?I ↑Risk ⇐= ↓money demandI ↑Riskiness of other assets ⇐= ↑money demand

I Relative liquidity

Portfolio theory of money demand

(M

P

)d

= L (i, Y ) (17)

This is missing some piecesI Wealth

I Wealth 6= incomeI Mishkin claims that increase in wealth has a smaller impact in

money demand than increase in income

I RiskI How safe is money?

I ↑Risk ⇐= ↓money demandI ↑Riskiness of other assets ⇐= ↑money demand

I Relative liquidity

Portfolio theory of money demand

(M

P

)d

= L (i, Y ) (17)

This is missing some piecesI Wealth

I Wealth 6= incomeI Mishkin claims that increase in wealth has a smaller impact in

money demand than increase in income

I RiskI How safe is money?I ↑Risk ⇐= ↓money demandI ↑Riskiness of other assets ⇐= ↑money demand

I Relative liquidity

Portfolio theory of money demand

(M

P

)d

= L (i, Y ) (17)

This is missing some piecesI Wealth

I Wealth 6= incomeI Mishkin claims that increase in wealth has a smaller impact in

money demand than increase in income

I RiskI How safe is money?I ↑Risk ⇐= ↓money demandI ↑Riskiness of other assets ⇐= ↑money demand

I Relative liquidity

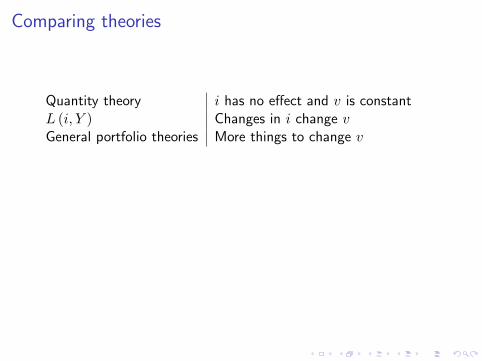

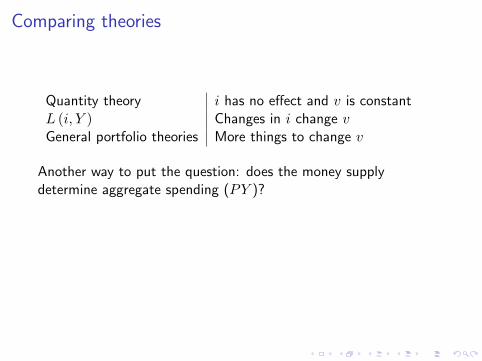

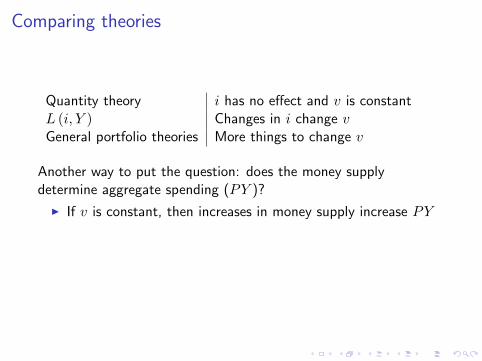

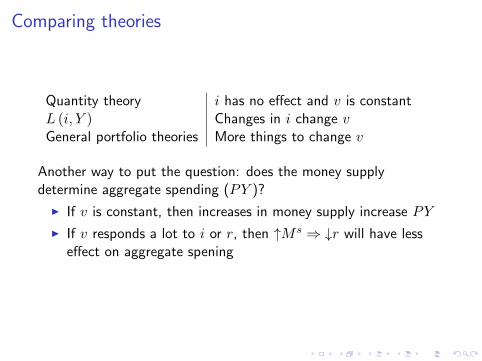

Comparing theories

Quantity theory

i has no effect and v is constant

L (i, Y )

Changes in i change v

General portfolio theories

More things to change v

Another way to put the question: does the money supplydetermine aggregate spending (PY )?

I If v is constant, then increases in money supply increase PY

I If v responds a lot to i or r, then ↑M s ⇒ ↓r will have lesseffect on aggregate spening

Comparing theories

Quantity theory i has no effect and v is constantL (i, Y )

Changes in i change v

General portfolio theories

More things to change v

Another way to put the question: does the money supplydetermine aggregate spending (PY )?

I If v is constant, then increases in money supply increase PY

I If v responds a lot to i or r, then ↑M s ⇒ ↓r will have lesseffect on aggregate spening

Comparing theories

Quantity theory i has no effect and v is constantL (i, Y ) Changes in i change vGeneral portfolio theories

More things to change v

Another way to put the question: does the money supplydetermine aggregate spending (PY )?

I If v is constant, then increases in money supply increase PY

I If v responds a lot to i or r, then ↑M s ⇒ ↓r will have lesseffect on aggregate spening

Comparing theories

Quantity theory i has no effect and v is constantL (i, Y ) Changes in i change vGeneral portfolio theories More things to change v

Another way to put the question: does the money supplydetermine aggregate spending (PY )?

I If v is constant, then increases in money supply increase PY

I If v responds a lot to i or r, then ↑M s ⇒ ↓r will have lesseffect on aggregate spening

Comparing theories

Quantity theory i has no effect and v is constantL (i, Y ) Changes in i change vGeneral portfolio theories More things to change v

Another way to put the question: does the money supplydetermine aggregate spending (PY )?

I If v is constant, then increases in money supply increase PY

I If v responds a lot to i or r, then ↑M s ⇒ ↓r will have lesseffect on aggregate spening

Comparing theories

Quantity theory i has no effect and v is constantL (i, Y ) Changes in i change vGeneral portfolio theories More things to change v

Another way to put the question: does the money supplydetermine aggregate spending (PY )?

I If v is constant, then increases in money supply increase PY

I If v responds a lot to i or r, then ↑M s ⇒ ↓r will have lesseffect on aggregate spening

Comparing theories

Quantity theory i has no effect and v is constantL (i, Y ) Changes in i change vGeneral portfolio theories More things to change v

Another way to put the question: does the money supplydetermine aggregate spending (PY )?

I If v is constant, then increases in money supply increase PY

I If v responds a lot to i or r, then ↑M s ⇒ ↓r will have lesseffect on aggregate spening

Practice questions

In groups:

I Graph L (i, Y ) w.r.t. i and Y

I What happens to velocity of money when i increases?

I What would happen to money demand and velocity of moneyif grocery stores started accepting treasury bills as payment?How would this change the definition of money?

I True, false, or uncertain: having more buyers and sellers in themarket for commercial paper would make commercial paperless liquid because sellers would have to compete more.

I Debit card fees get lowered because of better technologies forprocessing the transactions

I Bankers become worried about potential bank runs

I The ECB buys more bonds