quantitative easing vs federal reserve pam gundlatch and our views

TRANSCRIPT

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 1/45

“To QE3 or not to Q E3That is the Question”

DoubleLine Multi ‐Asset Growth Fund

Jeffrey Gundlach Chief Executive Officer

Jeff ShermanPortfolio Manager,Commodities

pr ,

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 2/45

Disclosures

Multi ‐Asset Growth FundInvestments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer ‐term debt securities. Investments in Asset ‐Backed and Mortgage ‐Backed Securities include risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. The Fund invests in foreign securities which typically involve greater volatility and political, economic and currency risks then do investments in domestic securities and the issuers of which are typically subject to different accounting standards. These risks are greater for investments in emerging markets. Investments in lower ‐rated and non ‐rated securities present a greater risk of loss to principal and interest than higher ‐rated securities. The Fund may invest in securities related to real estate, which may decline in value as a result of

. , , , , management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Commodity ‐linked derivative instruments may involve additional costs and risks such as changes in commodity index volatility or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes,

tariffs and international economic, political and regulatory developments. Investing in derivatives could lose more than the amount invested. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. The Fund is non ‐diversified, which means that it may concentrate its assets in a smaller number of issuers than a diversified fund.

1

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 3/45

Risk Disclosures

Total Return Bond FundInvestments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer ‐term debt securities. Investments in Asset ‐Backed and Mortgage ‐Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Investments in lower ‐rated and non ‐rated securities present a greater risk of loss to principal and interest than higher ‐rated securities.

ou e ne ota eturn on un nten s to nvest more t an o ts net assets n mortgage ‐ ac e secur t es o any matur ty or type. The Fund therefore potentially is more likely to react to any volatility or changes in the mortgage ‐backed securities marketplace.

Core Fixed Income FundInvestments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer ‐term debt

‐ ‐. as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. The Fund invests in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging markets. Investments in lower ‐rated and non ‐rated securities

present a greater risk of loss to principal and interest than higher ‐rated securities.

While the Fund is no ‐load, management fees and other expenses still apply. DoubleLine Funds are distributed by Quasar Distributors, LLC.

2

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 4/45

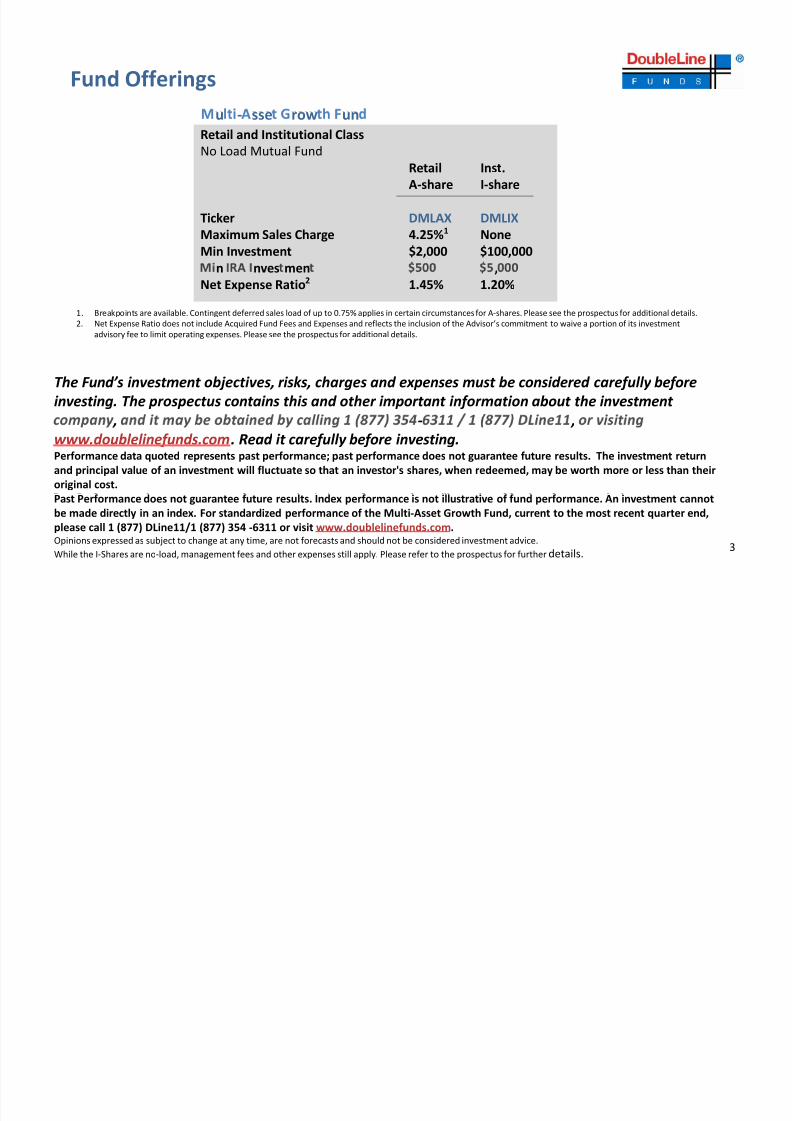

Fund Offerings

Retail and Institutional ClassNo Load Mutual Fund

Retail Inst.A‐share I ‐share

u ‐ sse row un

Ticker DMLAX DMLIXMaximum Sales Charge 4.25% 1 NoneMin Investment $2,000 $100,000

n nves men ,Net Expense Ratio 2 1.45% 1.20%

1. Breakpoints are available. Contingent deferred sales load of up to 0.75% applies in certain circumstances for A‐shares. Please see the prospectus for additional details.2. Net Expense Ratio does not include Acquired Fund Fees and Expenses and reflects the inclusion of the Advisor’s commitment to waive a portion of its investment

advisory fee to limit operating expenses. Please see the prospectus for additional details.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment

,‐

,

www.doublelinefunds.com . Read it carefully before investing. Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Past Performance does not guarantee future results. Index performance is not illustrative of fund performance. An investment cannot be made directly in an index. For standardized performance of the Multi ‐Asset Growth Fund, current to the most recent quarter end, please call 1 (877) DLine11/1 (877) 354 ‐6311 or visit www.doublelinefunds.com .Opinions expressed as subject to change at any time, are not forecasts and should not be considered investment advice.While the I‐Shares are no ‐load, management fees and other expenses still apply. Please refer to the prospectus for further details. 3

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 5/45

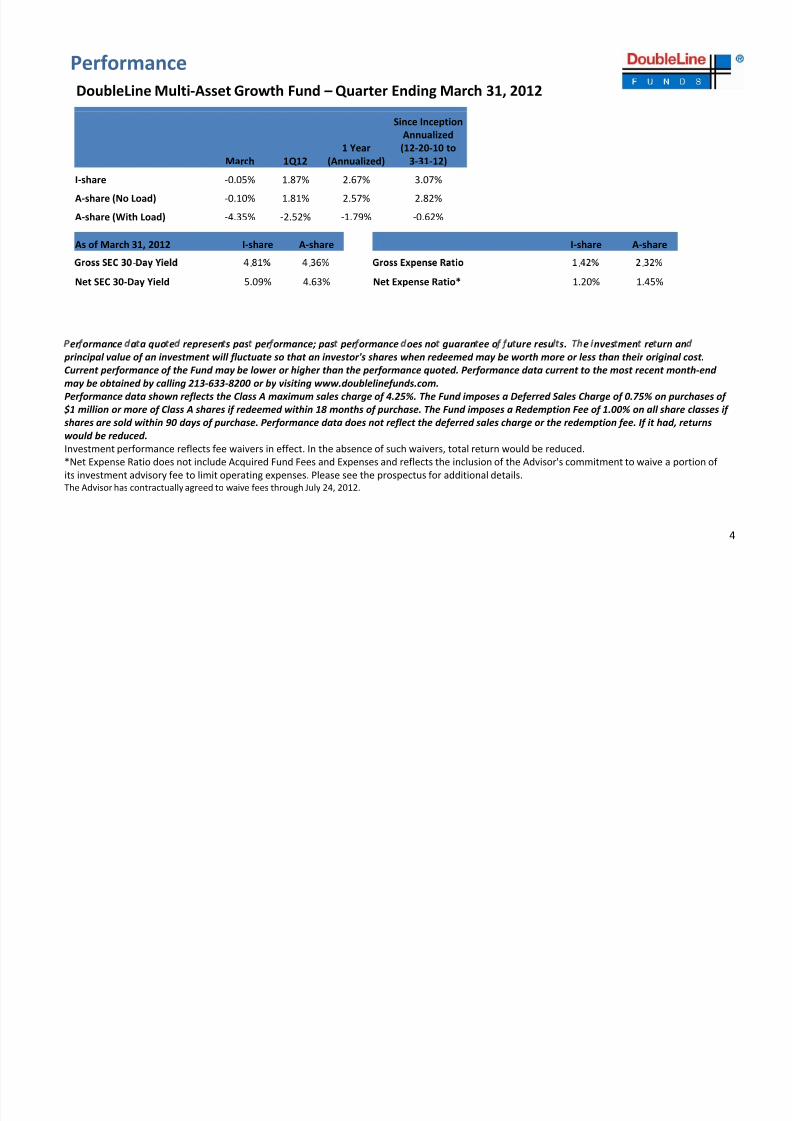

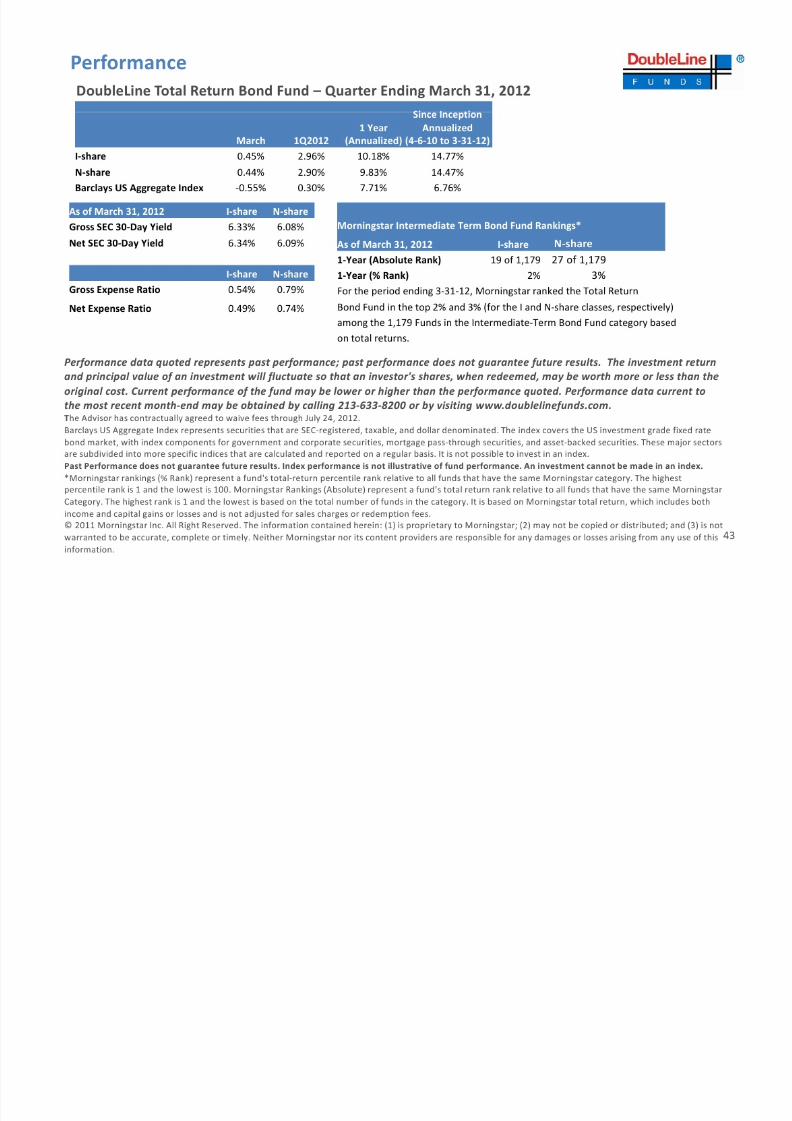

PerformanceDoubleLine Multi ‐Asset Growth Fund – Quarter Ending March 31, 2012

March 1Q121 Year

(Annualized)

Since Inception Annualized(12‐20‐10 to

3‐31‐12)

I‐share ‐0.05% 1.87% 2.67% 3.07%

I‐share A ‐share

A‐share (No Load) ‐0.10% 1.81% 2.57% 2.82%

A‐share (With Load) ‐4.35% ‐2.52% ‐1.79% ‐0.62%

As of March 31, 2012 I‐share A ‐share

‐ . .

Net Expense Ratio* 1.20% 1.45%

. .

Net SEC 30‐Day Yield 5.09% 4.63%

er ormance a a quo e represen s pas per ormance; pas per ormance oes no guaran ee o u ure resu s. e nves men re urn an principal value of an investment will fluctuate so that an investor's shares when redeemed may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month ‐end may be obtained by calling 213 ‐633 ‐8200 or by visiting www.doublelinefunds.com. Performance data shown reflects the Class A maximum sales charge of 4.25%. The Fund imposes a Deferred Sales Charge of 0.75% on purchases of $1 million or more of Class A shares if redeemed within 18 months of purchase. The Fund imposes a Redemption Fee of 1.00% on all share classes if

shares are

sold

within

90

days

of

purchase.

Performance

data

does

not

reflect

the

deferred

sales

charge

or

the

redemption

fee.

If

it

had,

returns

would be reduced. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.*Net Expense Ratio does not include Acquired Fund Fees and Expenses and reflects the inclusion of the Advisor's commitment to waive a portion of its investment advisory fee to limit operating expenses. Please see the prospectus for additional details.The Advisor has contractually agreed to waive fees through July 24, 2012.

4

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 6/45

Announcements

Webcast News –Jeffrey Gundlach – April 19, 2012Litman Gregory Masters Alternative Strategies Fund 1

April 19, 2012 1:15 pm PT

Please visit www.mastersfund.com

Jeffrey Gundlach – May 8, 2012DoubleLine Total Return & Core Fixed Income Bond FundsMay 8, 2012 1:15 pm PDT/4:15 pm EDT

Luz Padilla – June 12, 2012ou e ne merg ng ar ets xe ncome un

June 12, 2012 1:15 pm PDT/4:15 pm EDTPlease visit www.astonfunds.com

o ece ve resen a on es:You can email [email protected]

1. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing.

5

The prospectus contains this and other important information about the investment company, and it may be obtained by calling 1‐800 ‐960 ‐0188. Read it carefully before investing.References to other mutual funds should not be interpreted as an offer of these securities. Jeffrey Gundlach is a sub ‐advisor to the Litman Gregory Masters Fund, which is also distributed by Quasar Distributors, LLC.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 7/45

“To QE3 or not to QE3That is the Question”

DoubleLine Multi ‐Asset Growth Fund

Jeffrey Gundlach Chief Executive Officer

Global Theater

Cast:Ben

BernankeAngela

April 17, 2012

Central Banks

Mario Draghi

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 8/45

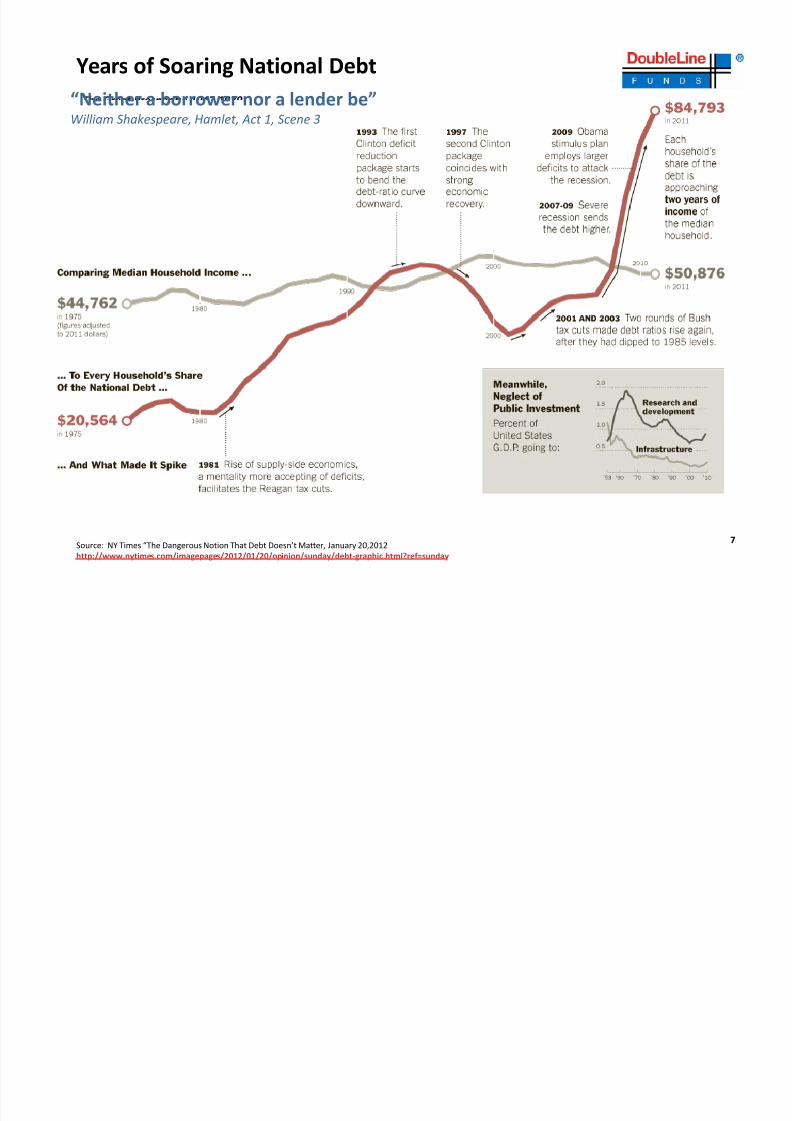

Years of Soaring National DebtThe Great Prosperity: 1947 ‐1979

“Neither a borrower

nor

a lender

be”William Shakespeare, Hamlet, Act 1, Scene 3

Source: NY Times “The Dangerous Notion That Debt Doesn’t Matter, January 20,2012 http://www.nytimes.com/imagepages/2012/01/20/opinion/sunday/debt ‐graphic.html?ref=sunday

7

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 9/45

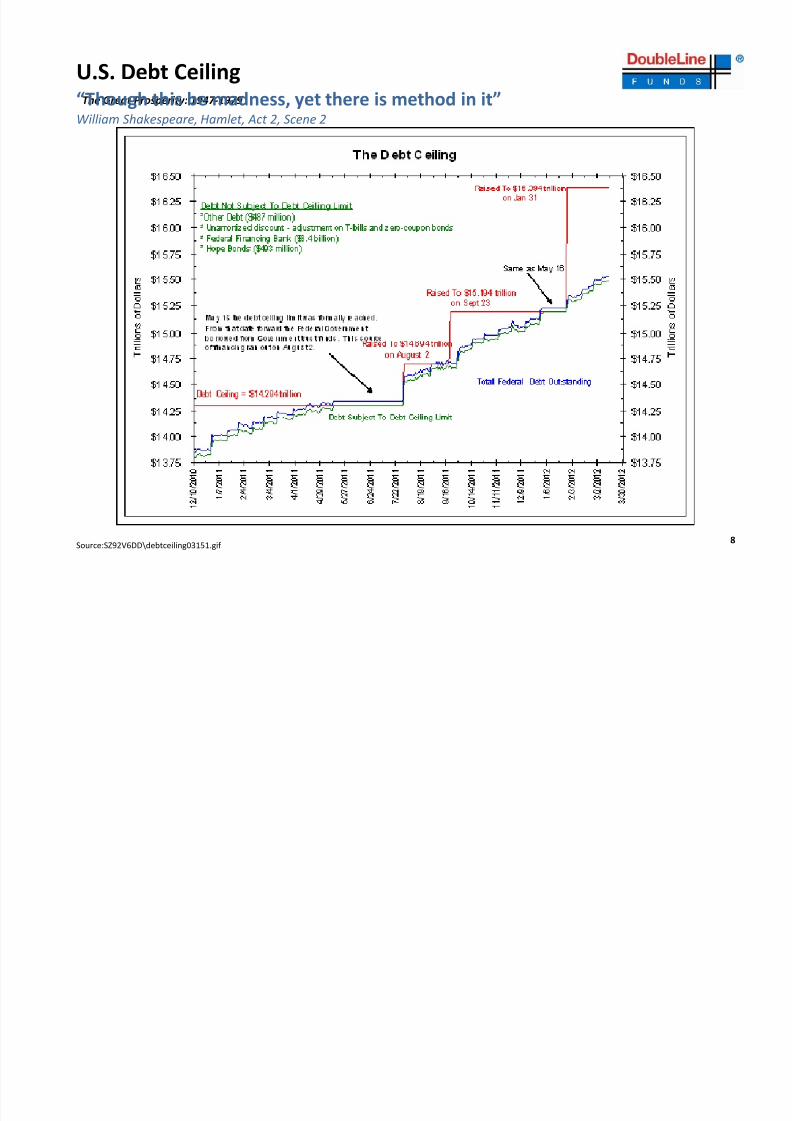

U.S. Debt CeilingThe Great Prosperity: 1947 ‐1979

“Though this

be

madness,

yet

there

is

method

in

it”William Shakespeare, Hamlet, Act 2, Scene 2

Source:SZ92V6DD\debtceiling03151.gif 8

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 10/45

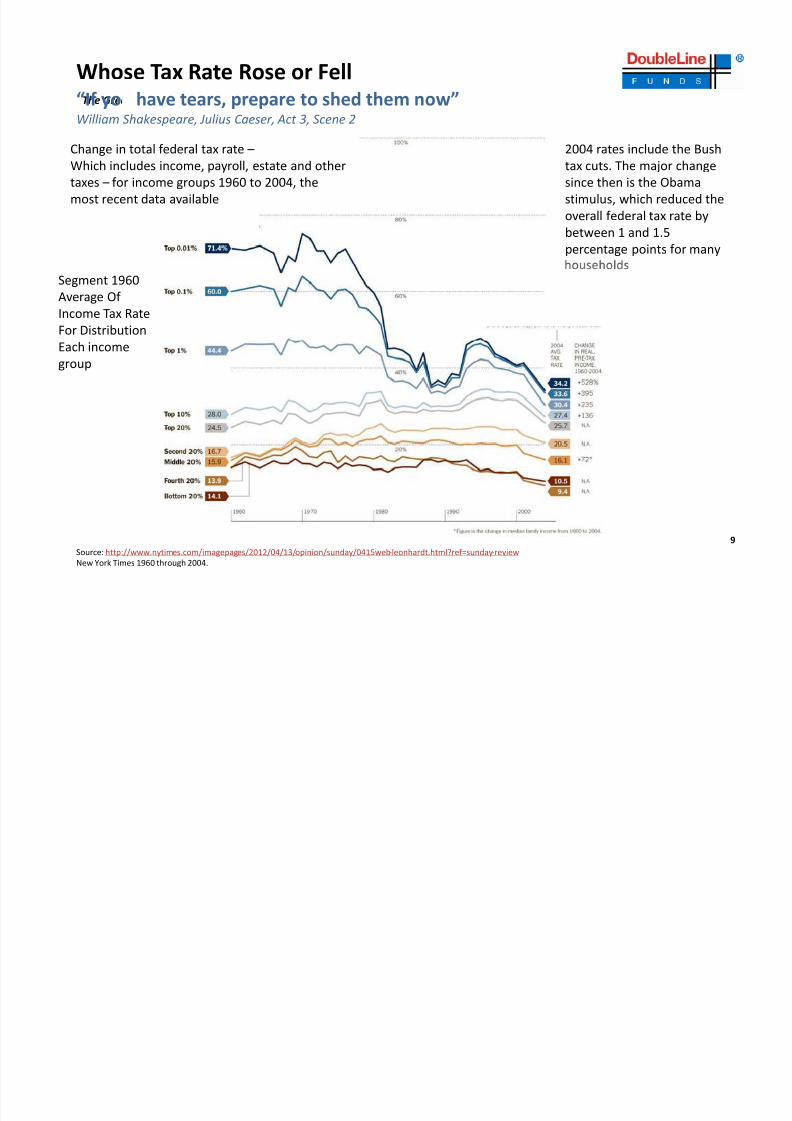

Whose Tax Rate Rose or FellThe Great Prosperity: 1947 ‐1979

“If you

have

tears,

prepare

to

shed

them

now”William Shakespeare, Julius Caeser, Act 3, Scene 2

Change in total federal tax rate –Which includes income, payroll, estate and other taxes – for income groups 1960 to 2004, the

2004 rates include the Bush tax cuts. The major change since then is the Obama

most recent data available stimulus, which reduced the

overall federal tax rate by between 1 and 1.5 percentage points for many

Segment 1960 Average Of Income Tax Rate For Distribution Each income group

Source: http://www.nytimes.com/imagepages/2012/04/13/opinion/sunday/0415web ‐leonhardt.html?ref=sunday ‐reviewNew York Times 1960 through 2004.

9

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 11/45

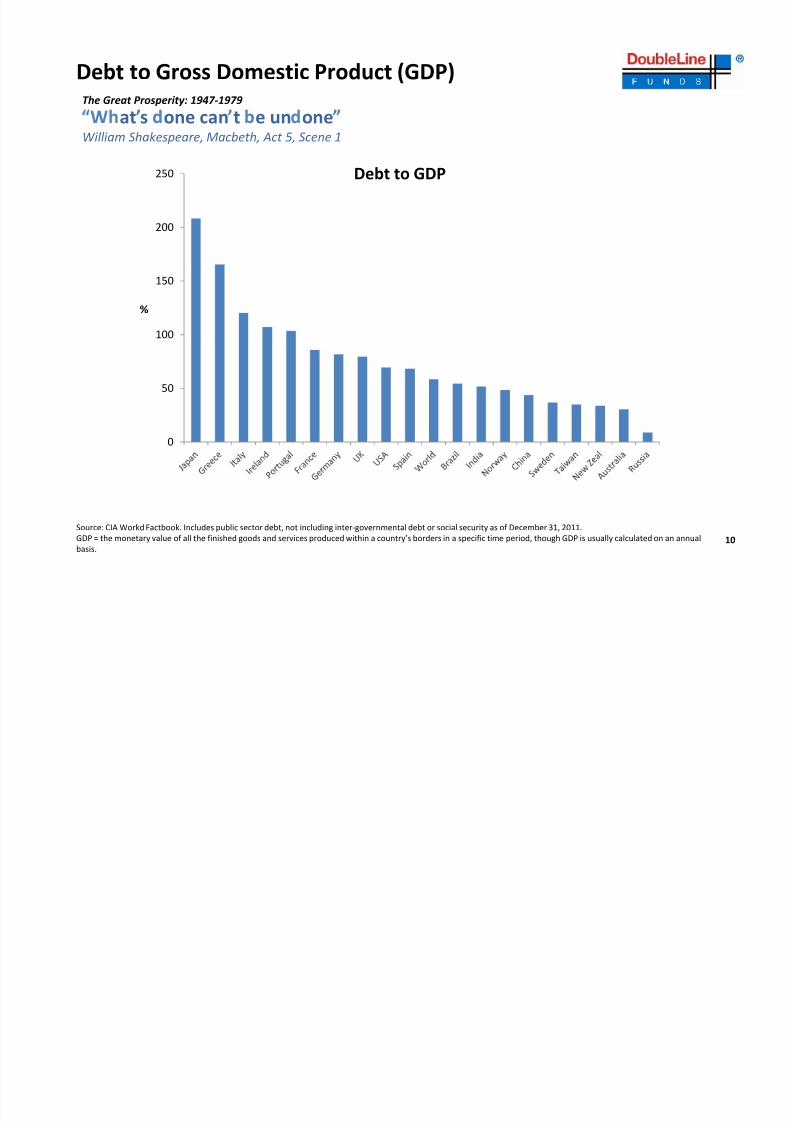

Debt to Gross Domestic Product (GDP)The Great Prosperity: 1947 ‐1979

250 Debt to GDP

at s one can t e un oneWilliam Shakespeare, Macbeth, Act 5, Scene 1

200

100

150

%

50

0

Source: CIA Workd Factbook. Includes public sector debt, not including inter ‐governmental debt or social security as of December 31, 2011.GDP = the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis.

10

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 12/45

The Great Prosperity: 1947 ‐1979

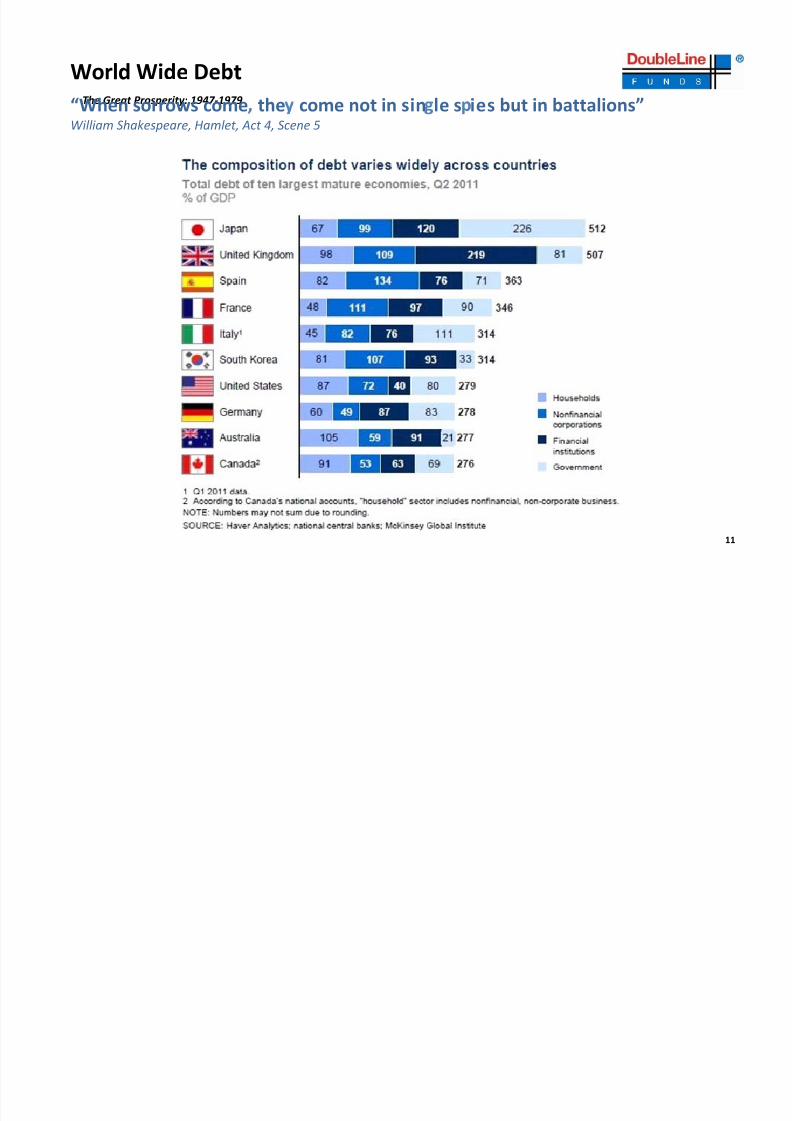

World Wide Debt

“When sorrows come the come not in sin le s ies but in battalions”William Shakespeare, Hamlet, Act 4, Scene 5

11

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 13/45

The Great Prosperity: 1947 ‐1979

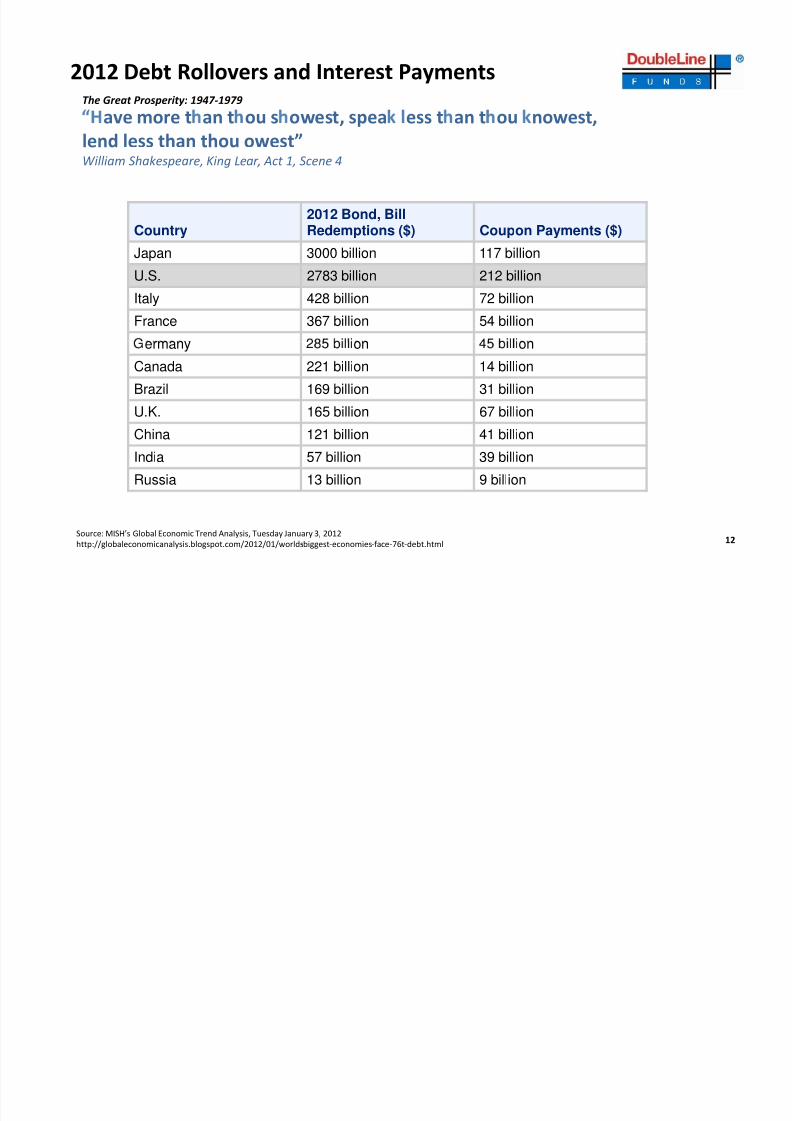

2012 Debt Rollovers and Interest Payments

ave more t an t ou s owest, spea ess t an t ou nowest, lend less than thou owest”William Shakespeare, King Lear, Act 1, Scene 4

Country 2012 Bond, BillRedemptions ($) Coupon Payments ($)

Japan 3000 billion 117 billion

U.S. 2783 billion 212 billion

Italy 428 billion 72 billion

France 367 billion 54 billionermany on on

Canada 221 billion 14 billion

Brazil 169 billion 31 billion

U.K. 165 billion 67 billion

China 121 billion 41 billionIndia 57 billion 39 billion

Russia 13 billion 9 billion

12Source: MISH’s

Global

Economic

Trend

Analysis,

Tuesday

January

3,

2012http://globaleconomicanalysis.blogspot.com/2012/01/worlds ‐biggest ‐economies ‐face ‐76t ‐debt.html

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 14/45

The Great Prosperity: 1947 ‐1979

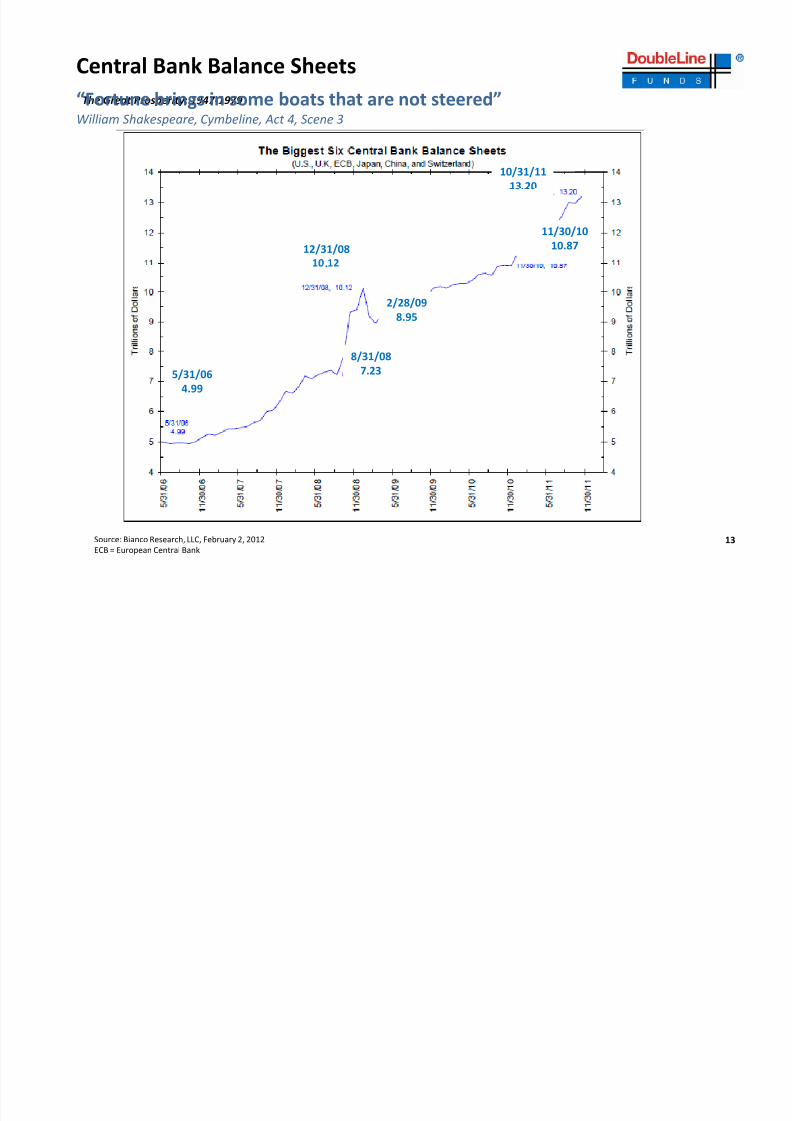

Central Bank Balance Sheets“Fortune brings in some boats that are not steered”

10/31/1113.20

William Shakespeare, Cymbeline, Act 4, Scene 3

12/31/08

11/30/1010.87

.

2/28/098.95

5/31/064.99

8/31/087.23

13Source: Bianco Research, LLC, February 2, 2012ECB = European Central Bank

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 15/45

The Great Prosperity: 1947 ‐1979

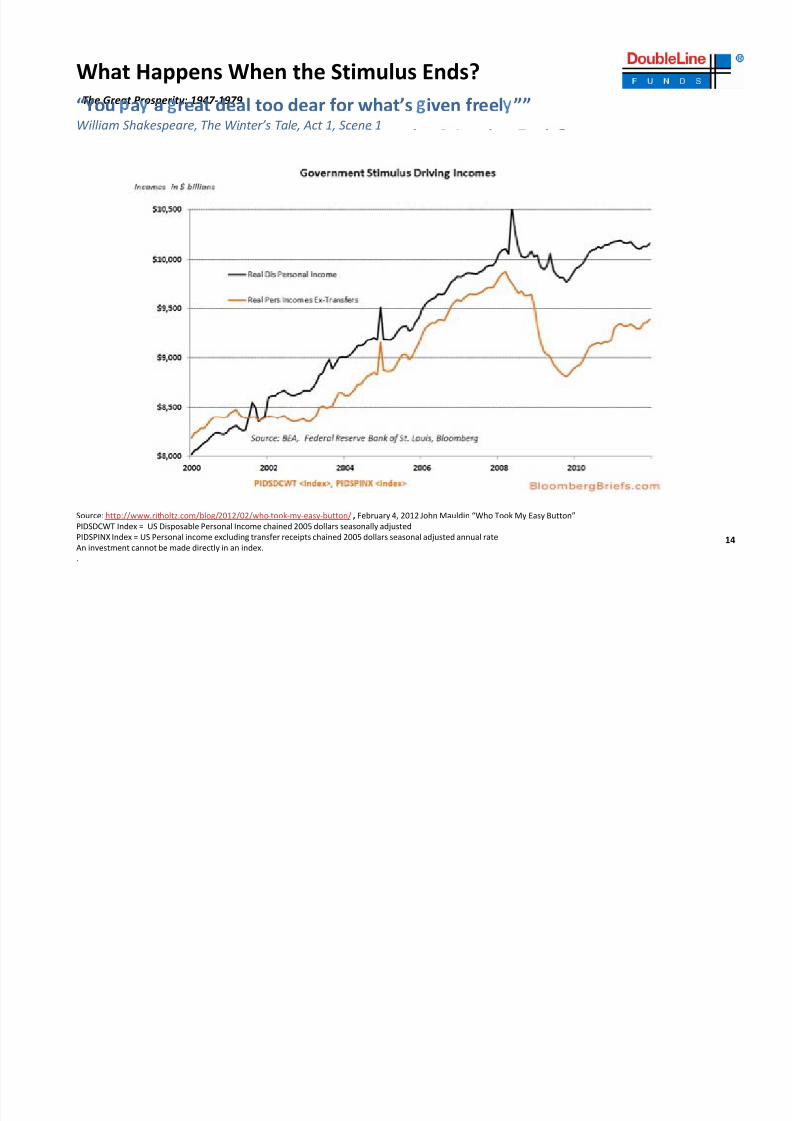

What Happens When the Stimulus Ends?

“You a a reat deal too dear for what’s iven freel ””William Shakespeare, The Winter’s Tale, Act 1, Scene 1

14

Source: http://www.ritholtz.com/blog/2012/02/who ‐took ‐my‐easy ‐button/ , February 4, 2012 John Mauldin “Who Took My Easy Button”PIDSDCWT Index = US Disposable Personal Income chained 2005 dollars seasonally adjusted

PIDSPINX Index = US Personal income excluding transfer receipts chained 2005 dollars seasonal adjusted annual rateAn investment cannot be made directly in an index..

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 16/45

The Great Prosperity: 1947 ‐1979

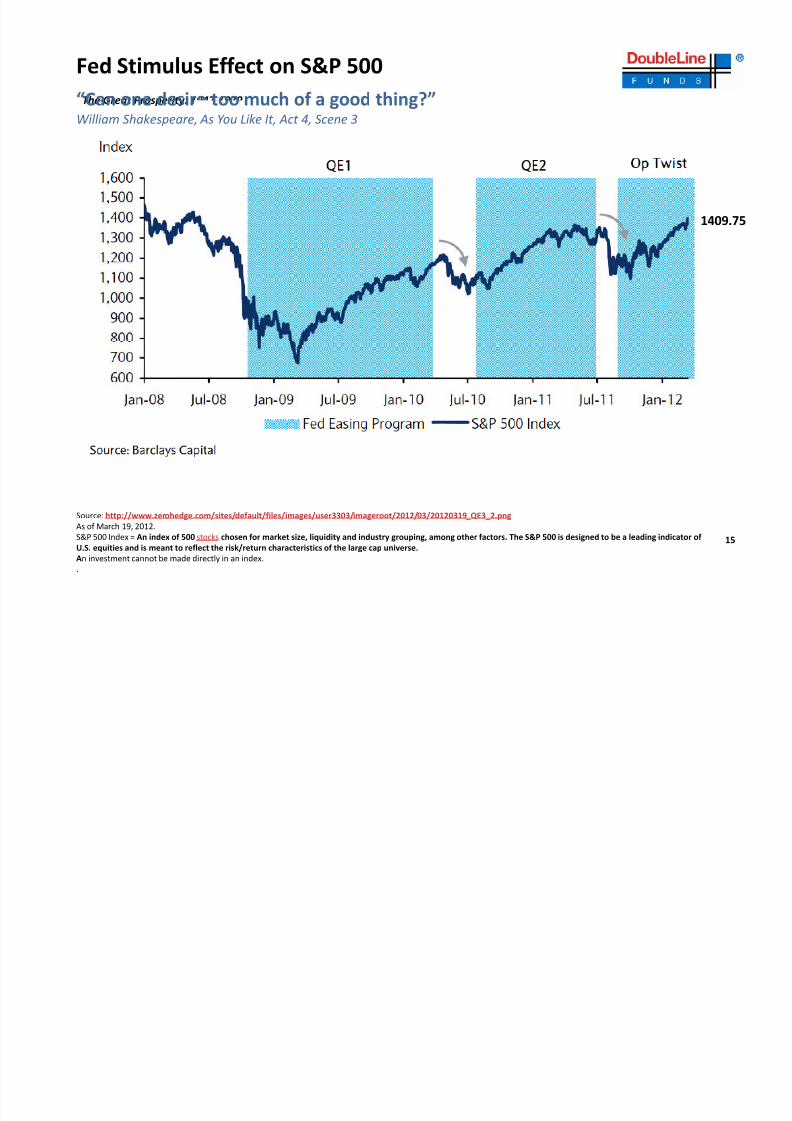

Fed Stimulus Effect on S&P 500“Can one desire too much of a good thing?”William Shakespeare, As You Like It, Act 4, Scene 3

1409.75

15

Source: http://www.zerohedge.com/sites/default/files/images/user3303/imageroot/2012/03/20120319_QE3_2.pngAs of March 19, 2012.

S&P 500 Index = An index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. An investment cannot be made directly in an index..

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 17/45

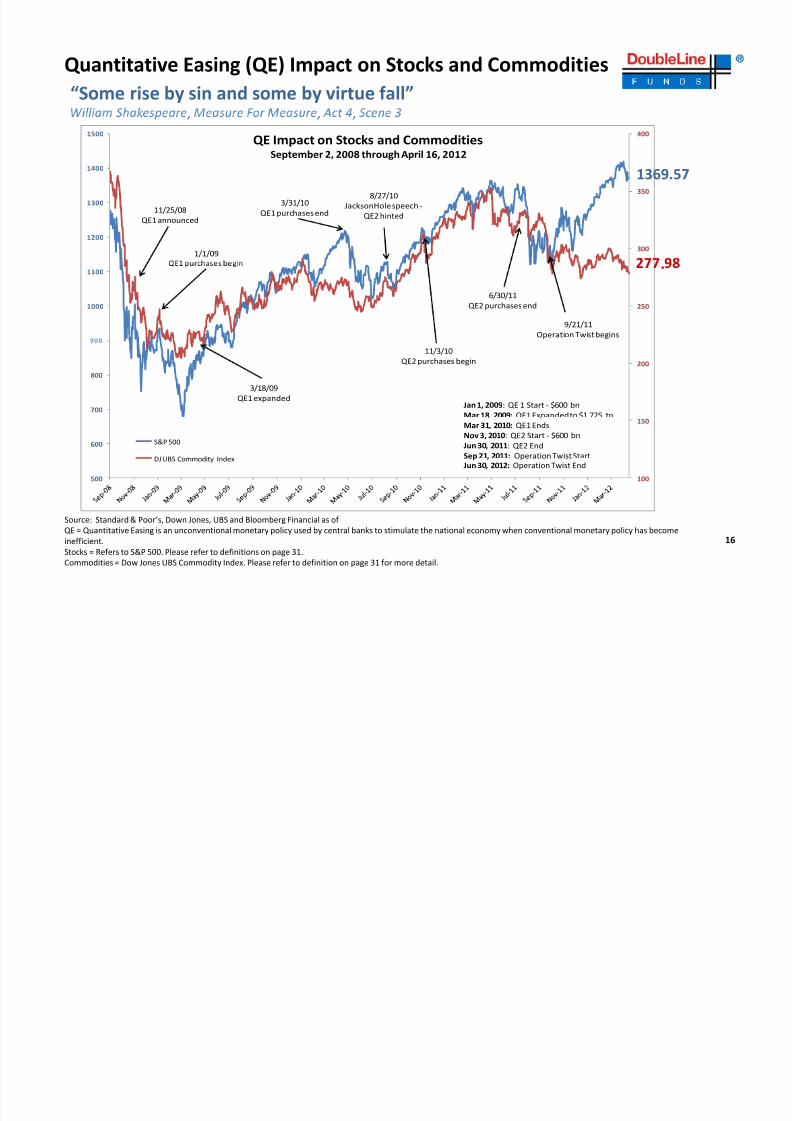

Quantitative Easing (QE) Impact on Stocks and Commodities“Some rise by sin and some by virtue fall”

400

1400

1500QE Impact on Stocks and Commodities

September 2, 2008 through April 16, 2012

1369.57

, , ,

300

350

1200

130011/25/08

QE1 announced

1/1/09

3/31/10QE1purchases end

8/27/10JacksonHole speech ‐

QE2 hinted

2501000

1100

6/30/11QE2 purchases end

9/21/11Operation Twist begins

.

200

700

800

Jan 1, 2009 : QE 1 Start ‐ $600 bnMar 18, 2009: QE1 Expanded to $1.725 tn

3/18/09QE1 expanded

11/3/10QE2 purchases begin

100

150

500

600 S&P 500

DJ UBS Commodity Index

Mar 31, 2010: QE1 EndsNov 3, 2010 : QE2 Start ‐ $600 bnJun 30, 2011 : QE2 EndSep 21, 2011: Operation Twist StartJun 30, 2012: Operation Twist End

16

Source: Standard & Poor’s, Down Jones, UBS and Bloomberg Financial as of QE = Quantitative Easing is an unconventional monetary policy used by central banks to stimulate the national economy when conventional monetary policy has become inefficient.Stocks = Refers to S&P 500. Please refer to definitions on page 31.Commodities = Dow Jones UBS Commodity Index. Please refer to definition on page 31 for more detail.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 18/45

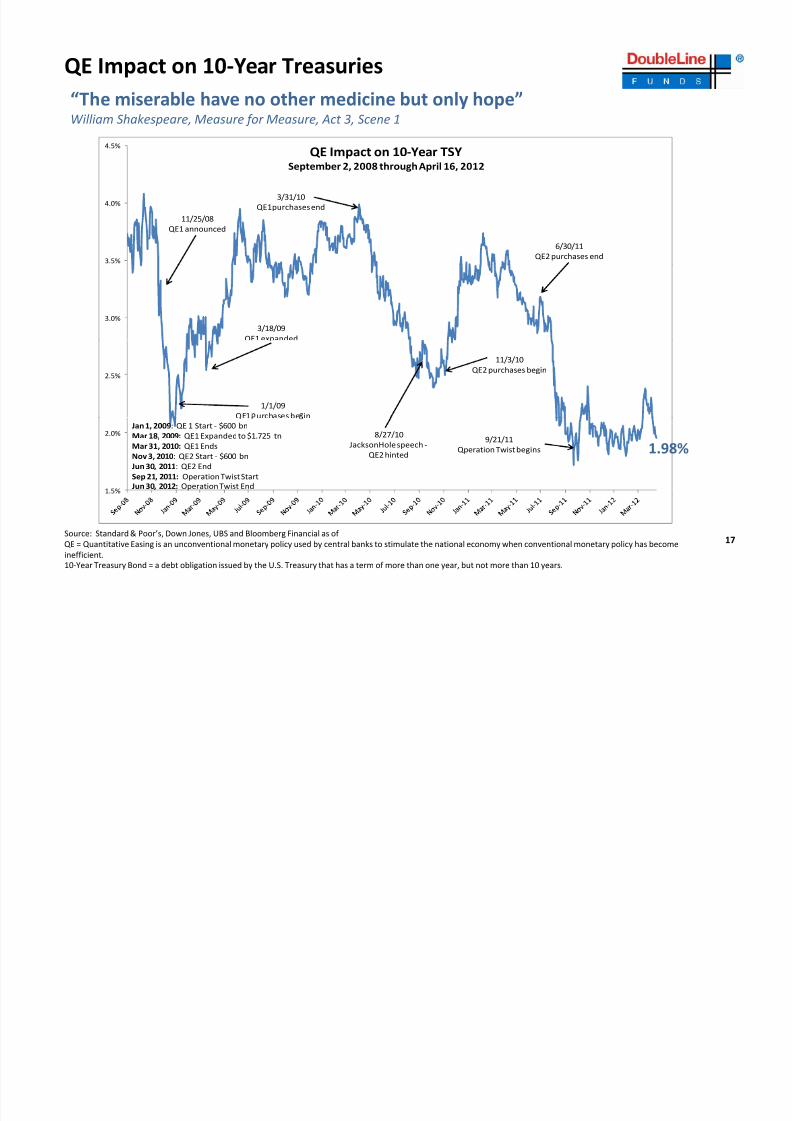

QE Impact on 10‐Year Treasuries“The miserable have no other medicine but only hope”

4.5%QE Impact on 10 ‐Year TSY

September 2, 2008 through April 16, 2012

William Shakespeare, Measure for Measure, Act 3, Scene 1

3.5%

4.0%

11/25/08QE1 announced

3/31/10QE1purchases end

6/30/11QE2 purchases end

3.0%3/18/09

QE1 expanded

2.5%

1/1/09QE1 urchases be in

11/3/10QE2 purchases begin

1.5%

2.0%

8/27/10JacksonHole speech ‐

QE2 hinted

Jan 1, 2009 : QE 1 Start ‐ $600 bnMar 18, 2009: QE1 Expanded to $1.725 tnMar 31, 2010: QE1 EndsNov 3, 2010 : QE2 Start ‐ $600 bnJun 30, 2011 : QE2 EndSep 21, 2011: Operation Twist StartJun 30, 2012: Operation Twist End

9/21/11Qperation Twist begins 1.98%

17Source: Standard & Poor’s, Down Jones, UBS and Bloomberg Financial as of QE = Quantitative Easing is an unconventional monetary policy used by central banks to stimulate the national economy when conventional monetary policy has become inefficient.10‐Year Treasury Bond = a debt obligation issued by the U.S. Treasury that has a term of more than one year, but not more than 10 years.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 19/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 20/45

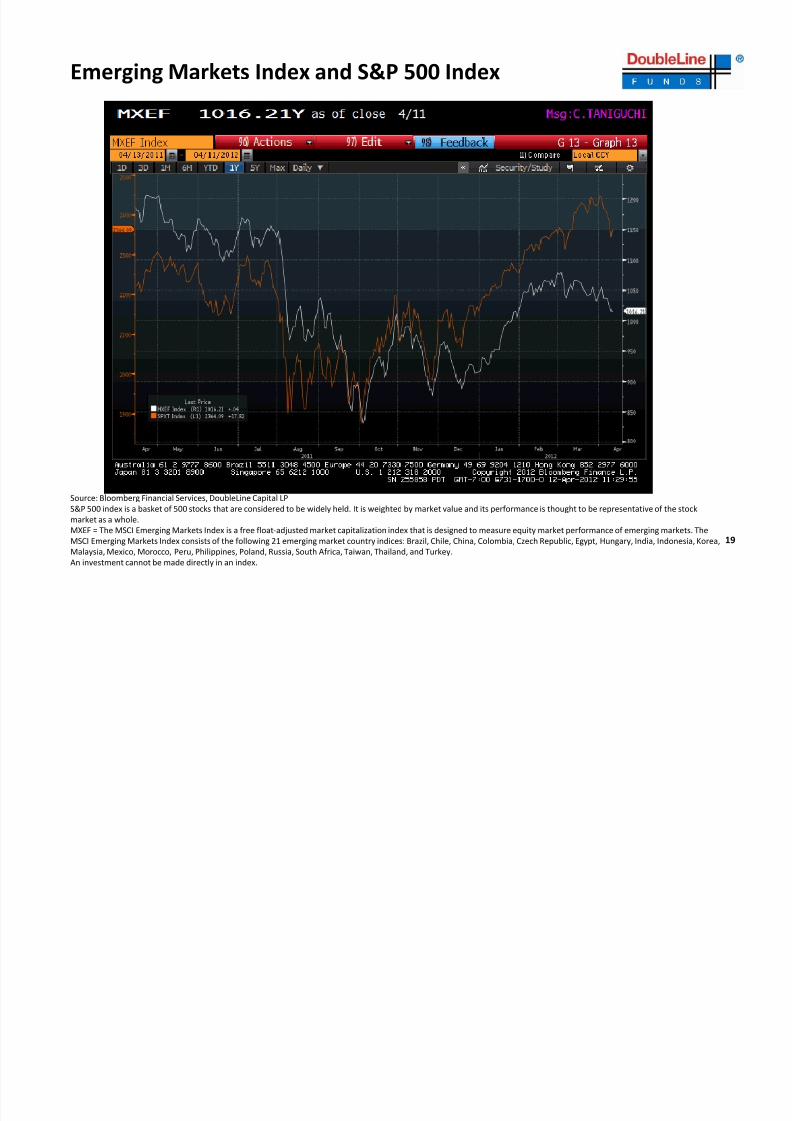

Emerging Markets Index and S&P 500 Index

Source: Bloomberg Financial Services, DoubleLine Capital LPS&P 500 index is a basket of 500 stocks that are considered to be widely held. It is weighted by market value and its performance is thought to be representative of the stock market as a whole.MXEF = The MSCI Emerging Markets Index is a free float ‐adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.An investment cannot be made directly in an index.

19

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 21/45

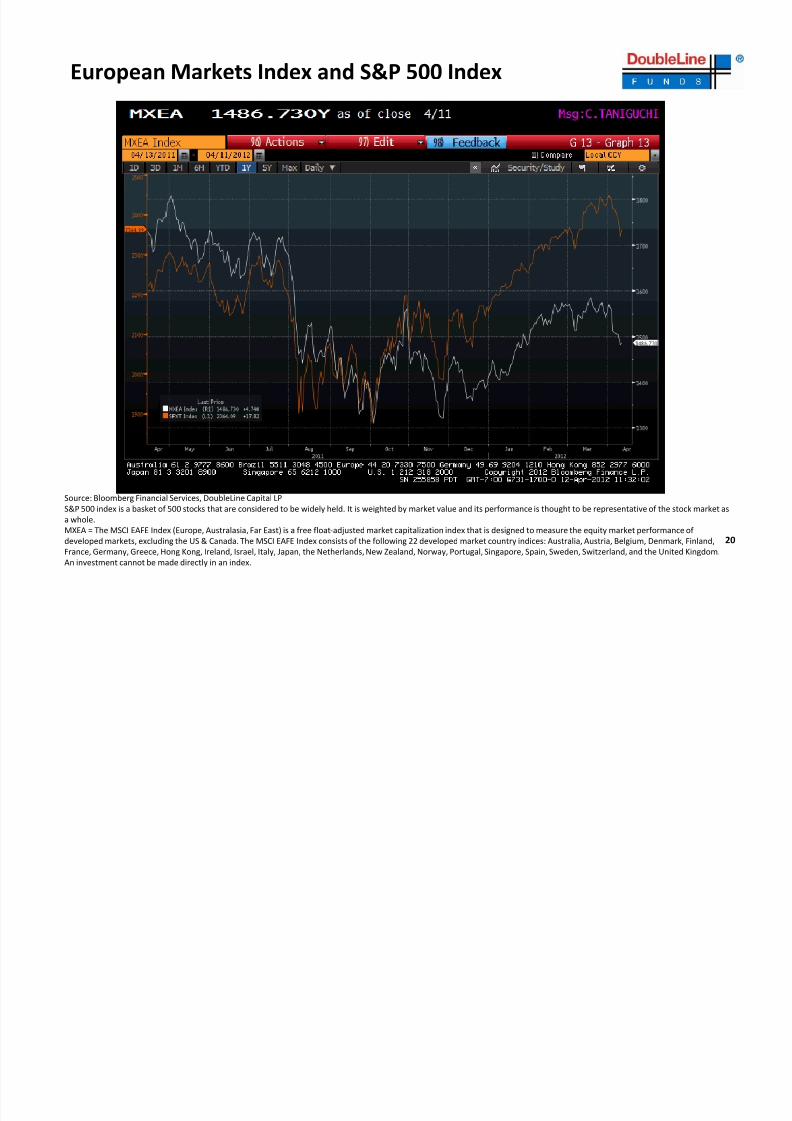

European Markets Index and S&P 500 Index

Source: Bloomberg Financial Services, DoubleLine Capital LPS&P 500 index is a basket of 500 stocks that are considered to be widely held. It is weighted by market value and its performance is thought to be representative of the stock market as a whole.MXEA = The MSCI EAFE Index (Europe, Australasia, Far East) is a free float ‐adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.An investment cannot be made directly in an index.

20

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 22/45

“To QE3 or not to QE3That is the Question”

DoubleLine Multi ‐Asset Growth Fund

Jeff ShermanPortfolio Manager,Commodities

April 17, 2012

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 23/45

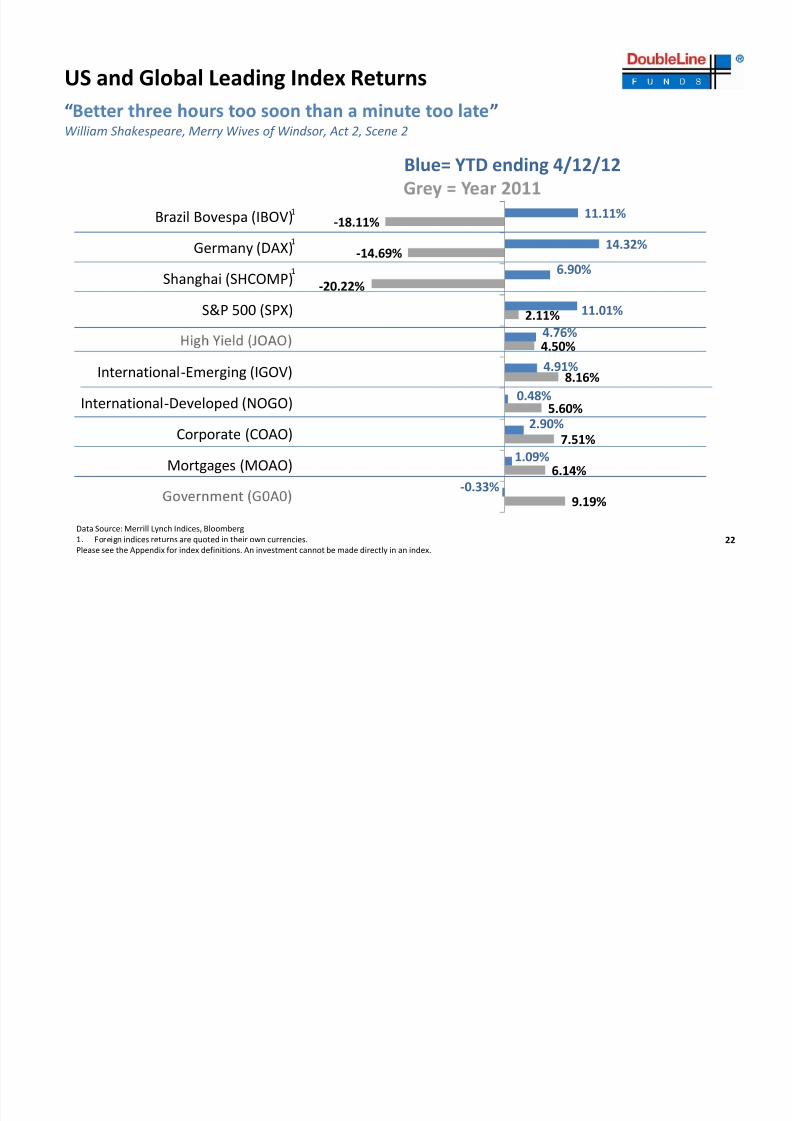

US and Global Leading Index Returns

“ ”

Blue= YTD ending 4/12/12

William Shakespeare, Merry Wives of Windsor, Act 2, Scene 2

‐14.69%

‐18.11%14.32%

11.11%

Germany (DAX)Brazil Bovespa (IBOV)

1

1

2.11%

‐20.22%

4.76%

11.01%

6.90%

S&P 500 (SPX)

Shanghai (SHCOMP)1

5.60%

8.16%

4.50%

0.48%

4.91%

International ‐Developed (NOGO)

International ‐Emerging (IGOV)

6.14%

7.51%

‐0.33%

1.09%

2.90%

Mortgages (MOAO)

Corporate (COAO)

9.19%

Data Source: Merrill Lynch Indices, Bloomberg

1. Foreign indices returns are quoted in their own currencies.Please see the Appendix for index definitions. An investment cannot be made directly in an index.

22

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 24/45

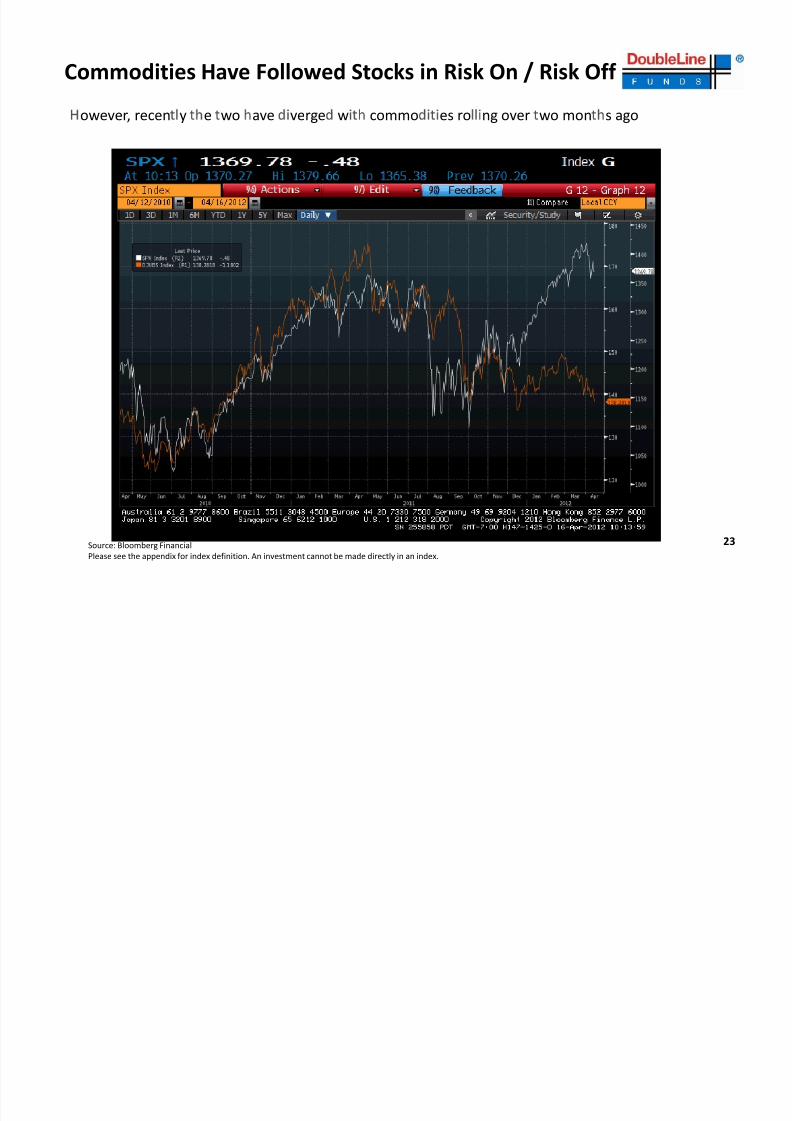

Commodities Have Followed Stocks in Risk On / Risk Off

owever, recen y e wo ave verge w commo es ro ng over wo mon s ago

23Source: Bloomberg FinancialPlease see the appendix for index definition. An investment cannot be made directly in an index.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 25/45

Copper Spot Prices – Looking Weak Once Again

24Source: Bloomberg FinancialPlease see the appendix for index definition. An investment cannot be made directly in an index.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 26/45

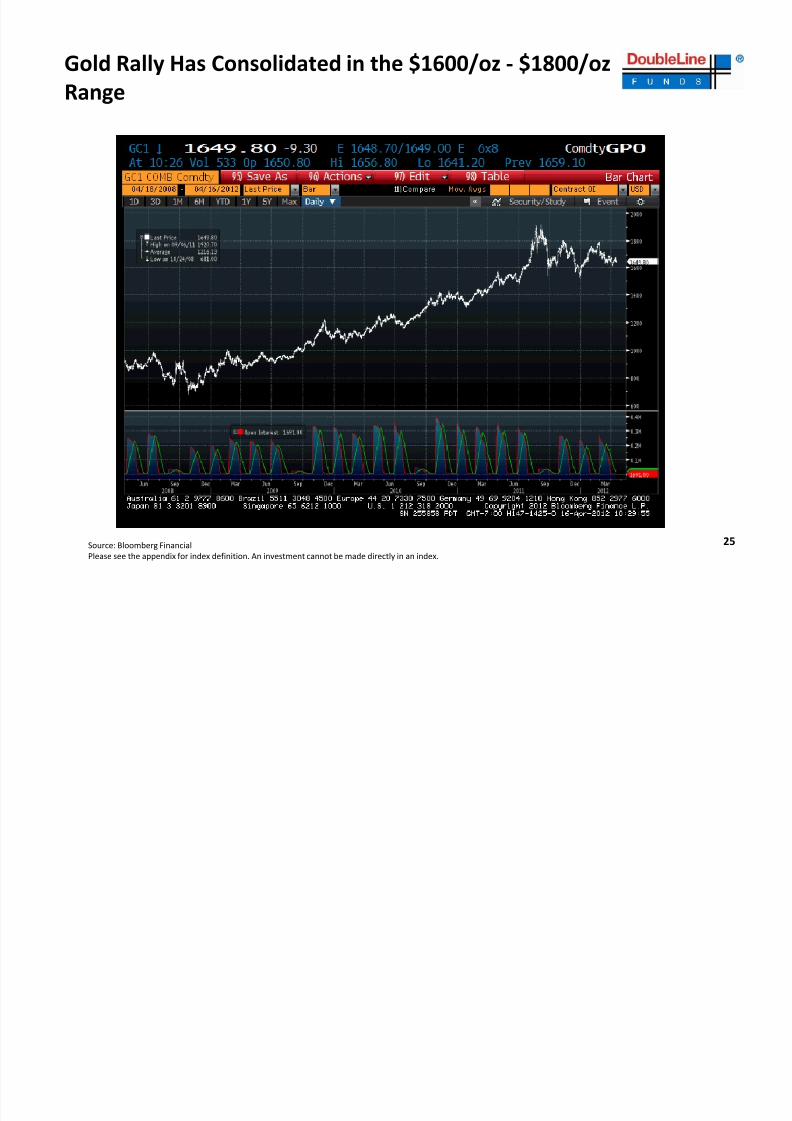

Gold Rally Has Consolidated in the $1600/oz ‐ $1800/ozRange

25Source: Bloomberg FinancialPlease see the appendix for index definition. An investment cannot be made directly in an index.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 27/45

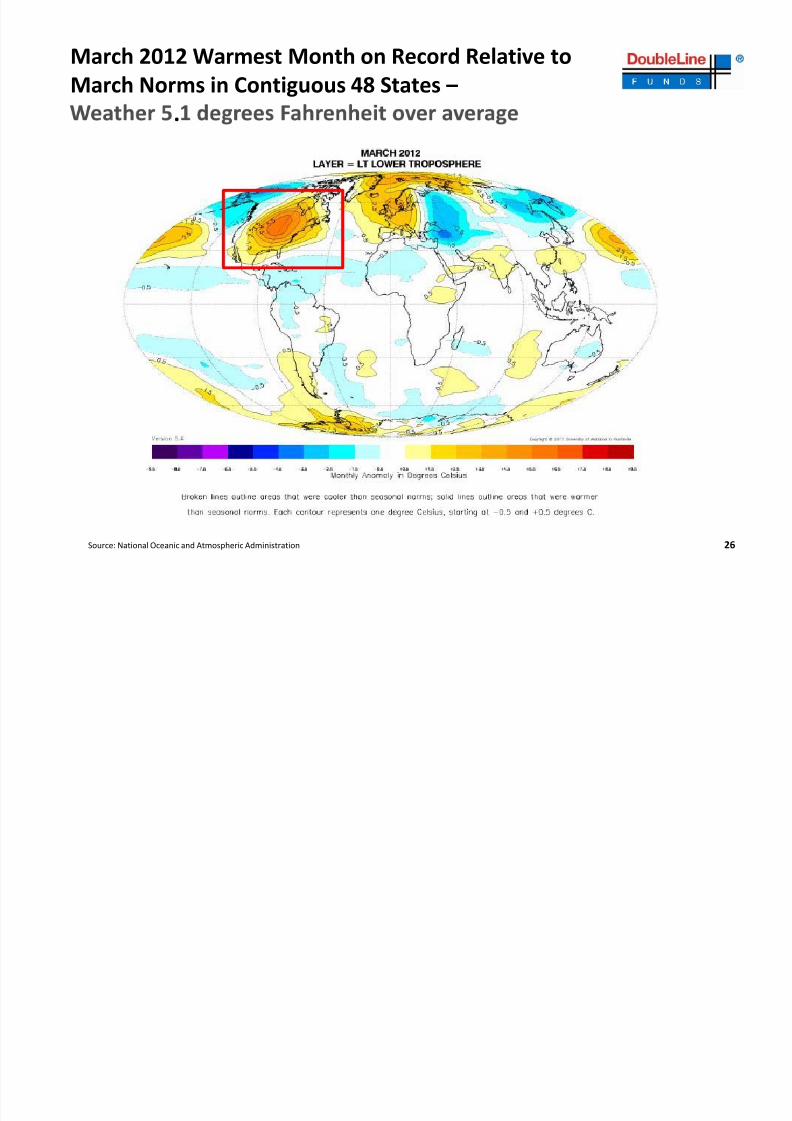

March 2012 Warmest Month on Record Relative to March Norms in Contiguous 48 States –

.

26Source: National Oceanic and Atmospheric Administration

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 28/45

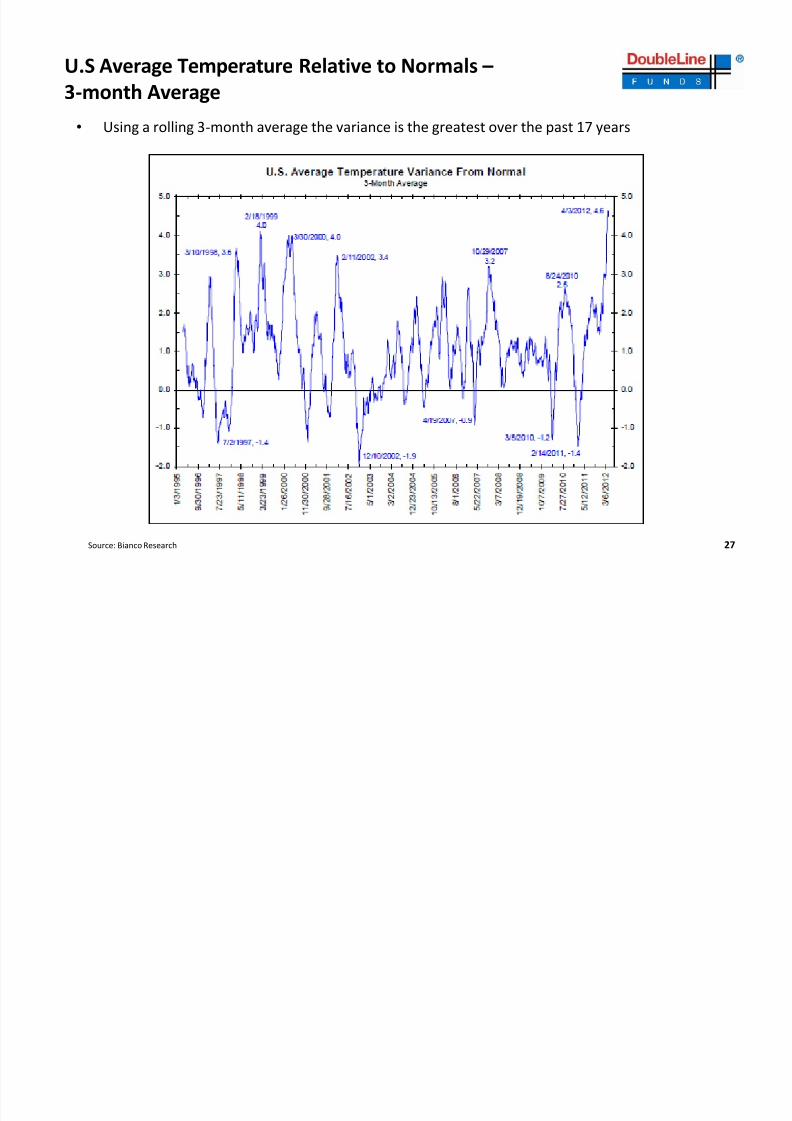

U.S Average Temperature Relative to Normals –3‐month Average

• Using a rolling 3 ‐month average the variance is the greatest over the past 17 years

27Source: Bianco Research

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 29/45

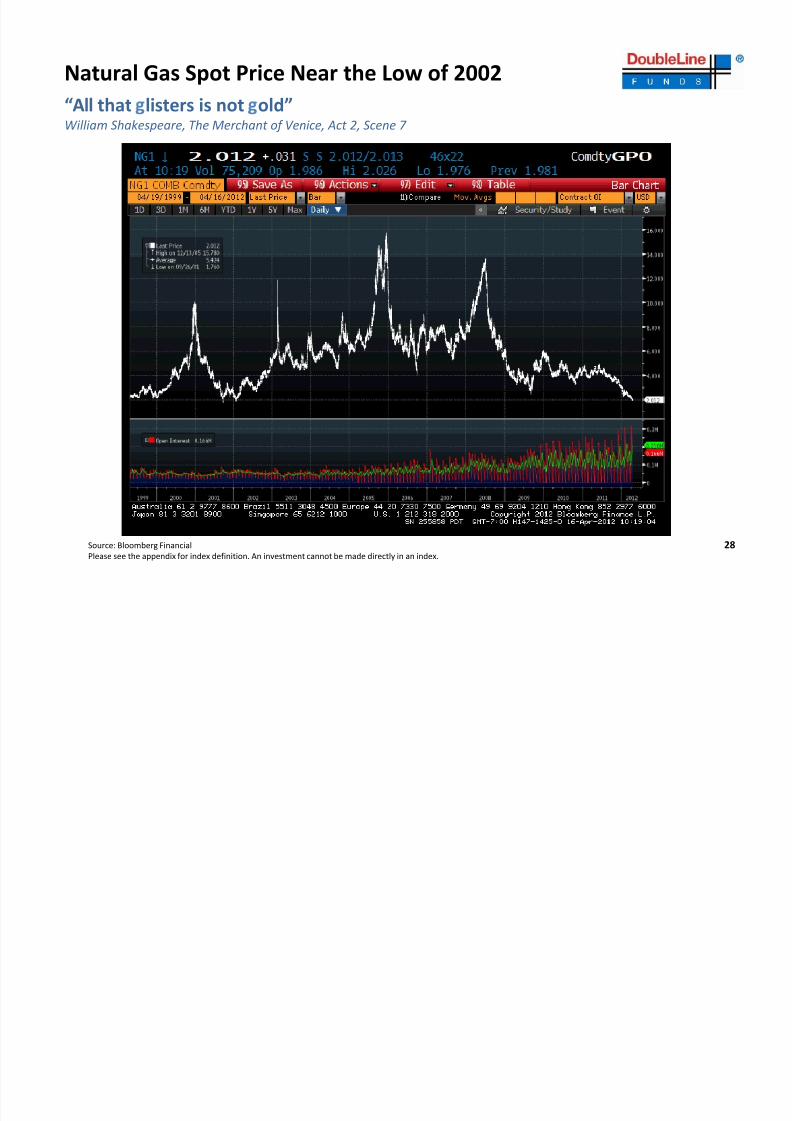

Natural Gas Spot Price Near the Low of 2002

“All that

listers

is

not

old”William Shakespeare, The Merchant of Venice, Act 2, Scene 7

28Source: Bloomberg FinancialPlease see the appendix for index definition. An investment cannot be made directly in an index.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 30/45

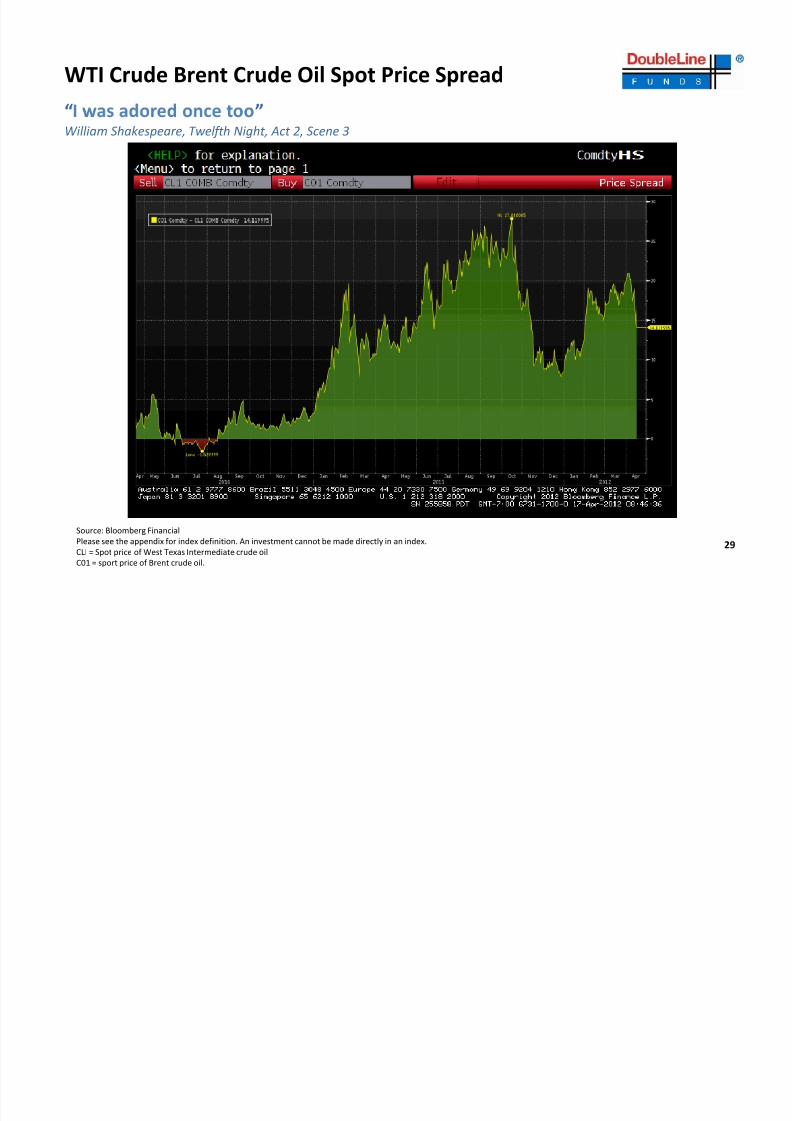

WTI Crude Brent Crude Oil Spot Price Spread

“ ” William Shakespeare, Twelfth Night, Act 2, Scene 3

29Source: Bloomberg Financial

Please see the appendix for index definition. An investment cannot be made directly in an index.CLI = Spot price of West Texas Intermediate crude oilC01 = sport price of Brent crude oil.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 31/45

Multi ‐Asset Growth Fund Philosophy

The DoubleLine Multi ‐Asset Growth Fund provides a flexible global asset allocation framework that

‐ “ ”

volatility and avoid catastrophic principal losses.

30

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 32/45

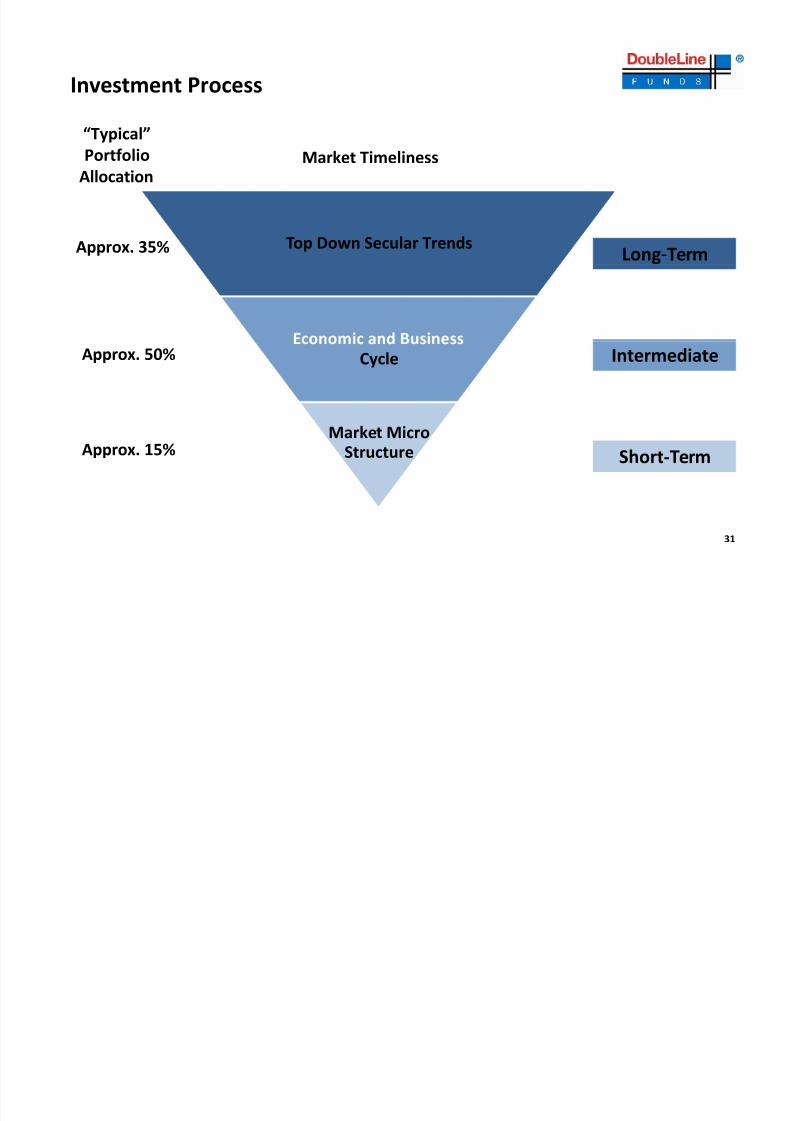

Investment Process

Market Timeliness“Typical”Portfolio

Allocation

Top Down Secular TrendsLong‐TermApprox. 35%

Cycle IntermediateApprox. 50%

Market Micro Structure Short ‐TermApprox. 15%

31

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 33/45

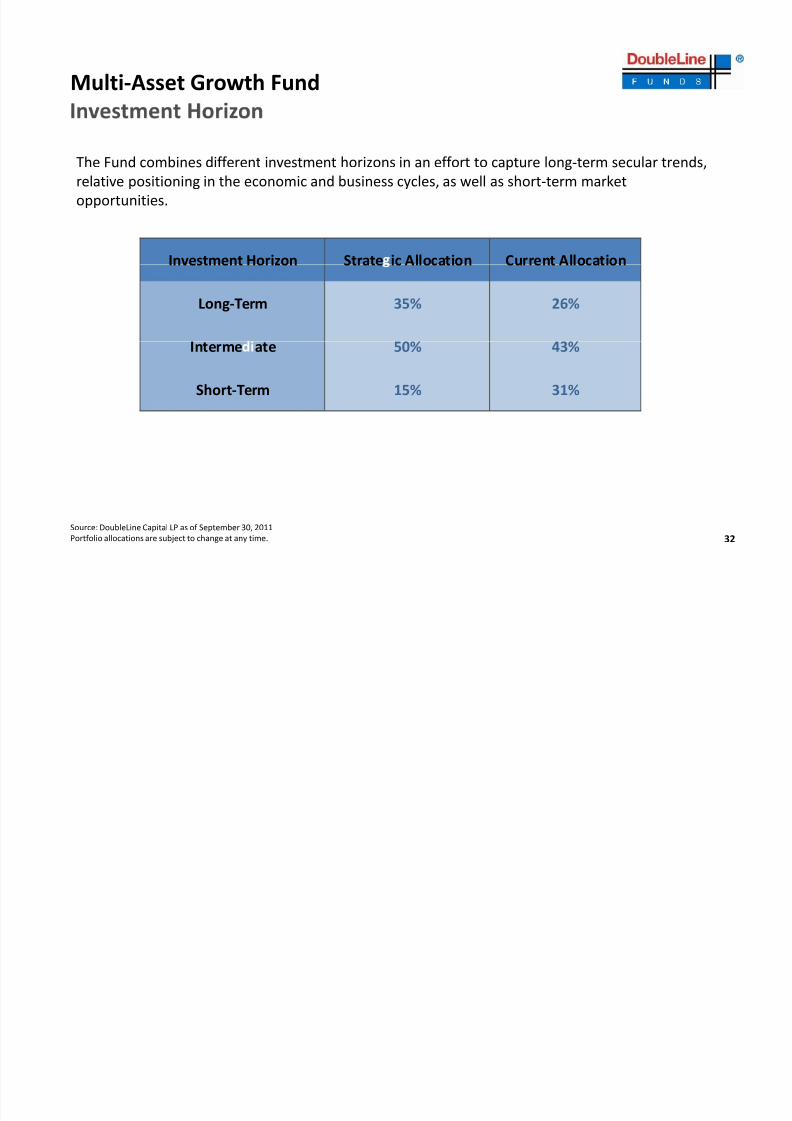

Multi ‐Asset Growth Fund

The Fund combines different investment horizons in an effort to capture long ‐term secular trends, relative positioning in the economic and business cycles, as well as short ‐term market opportunities.

Investment Horizon Strate ic Allocation Current Allocation

Long‐Term 35% 26%

Interme ate 50% 43%

Short ‐Term 15% 31%

32

Source: DoubleLine Capital LP as of September 30, 2011

Portfolio allocations

are

subject

to

change

at

any

time.

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

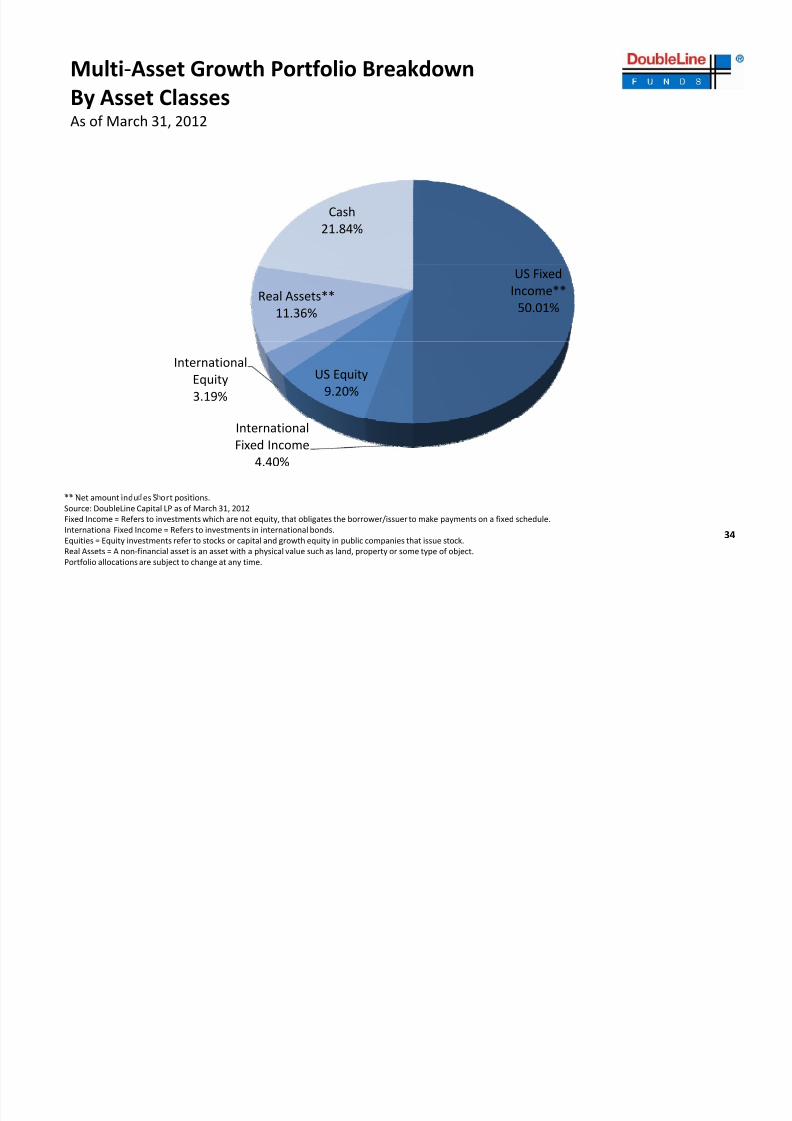

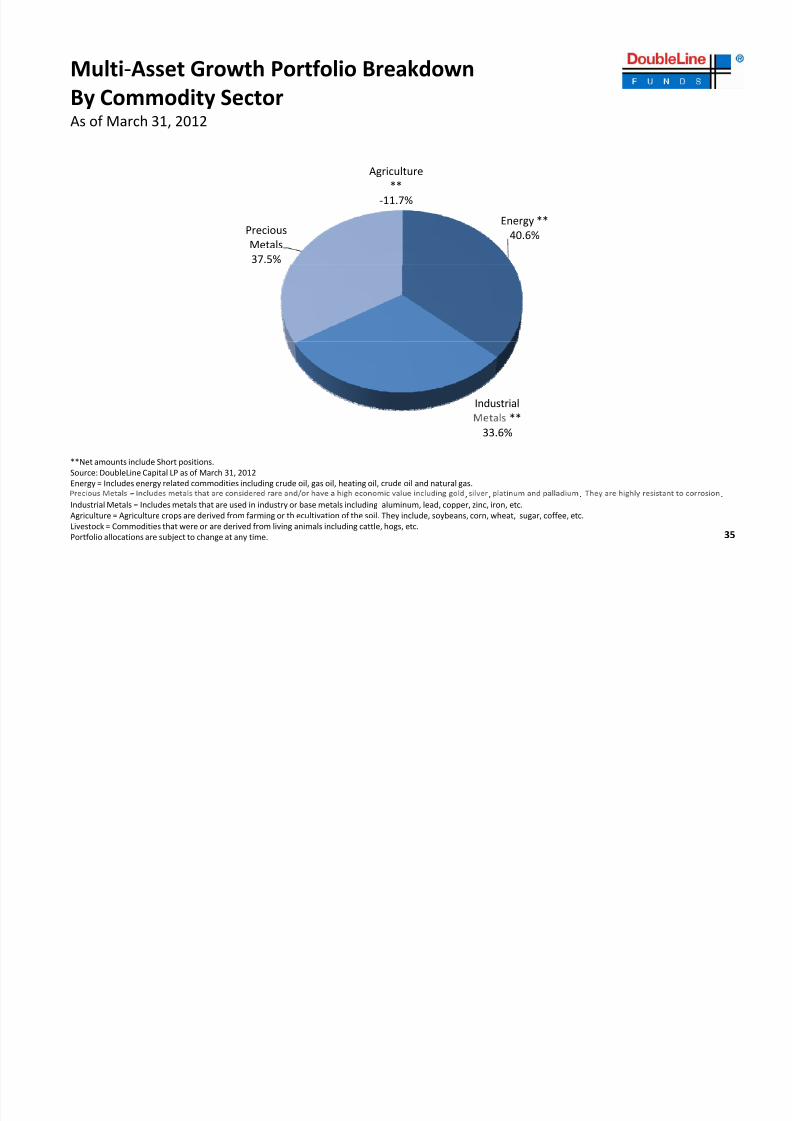

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 34/45

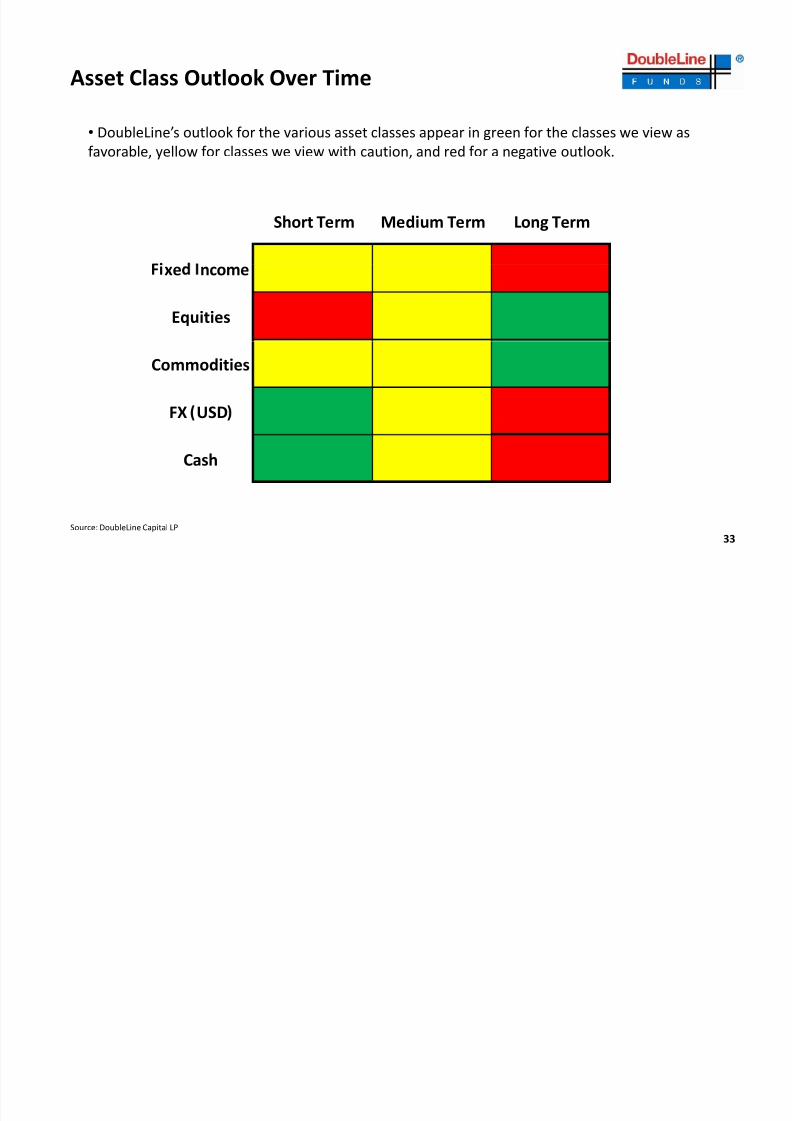

Asset Class Outlook Over Time

• DoubleLine’s outlook for the various asset classes appear in green for the classes we view as favorable, yellow for classes we view with caution, and red for a negative outlook.

Short Term Medium Term Long Term

xe ncome

Equities

Commodities

FX USD

Cash

33

Source: DoubleLine Capital LP

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 35/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 36/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 37/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 38/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 39/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 40/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 41/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 42/45

Disclaimer

Important Information Regarding This ReportThis report was prepared as a private communication and was not intended for public circulation. Clients or prospects may authorize distribution to their consultants or other agents.

Issue selection processes and tools illustrated throughout this presentation are samples and may be modified periodically. Such charts are not the only tools used y e nves men eams, are ex reme y sop s ca e , may no a ways pro uce e n en e resu s an are no n en e or use y non ‐pro ess ona s.

DoubleLine has no obligation to provide revised assessments in the event of changed circumstances. While we have gathered this information from sources believed to be reliable, DoubleLine cannot guarantee the accuracy of the information provided. Securities discussed are not recommendations and are presented as examples of issue selection or portfolio management processes. They have been picked for comparison or illustration purposes only. No security presented within is either offered for sale or purchase. DoubleLine reserves the right to change its investment perspective and outlook without notice as market conditions dictate or as additional information becomes available.

Important Information Regarding Risk FactorsInvestment strategies may not achieve the desired results due to implementation lag, other timing factors, portfolio management decision ‐making, economic or market conditions or other unanticipated factors. The views and forecasts expressed in this material are as of the date indicated, are subject to change without notice, may not come to pass and do not represent a recommendation or offer of any particular security, strategy, or investment. Past performance is no guarantee of future results.

Important Information Regarding DoubleLineIn preparing the client reports (and in managing the portfolios), DoubleLine and its vendors price separate account portfolio securities using various sources, including independent pricing services and fair value processes such as benchmarking.

To receive a complimentary copy of DoubleLine’s current Form ADV Part II (which contains important additional disclosure information), a copy of the DoubleLine’s proxy voting policies and procedures, or to obtain additional information on DoubleLine’s proxy voting decisions, please contact DoubleLine’s Client

Services.

41

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 43/45

Disclaimer

Important Information Regarding DoubleLine’s Investment StyleDoubleLine seeks to maximize investment results consistent with our interpretation of client guidelines and investment mandate. While DoubleLine seeks to maximize returns for our clients consistent with guidelines, DoubleLine cannot guarantee that DoubleLine will outperform a client's specified benchmark or the market. Additionally, the nature of portfolio diversification implies that certain holdings and sectors in a client's portfolio may be rising in price while others are falling; or, that some issues and sectors are outperforming while others are underperforming. Such out or underperformance can be the result of many factors, such as but not limited to duration/interest rate exposure, yield curve exposure, bond sector exposure, or news or rumors specific to a single name.DoubleLine is an active manager and will adjust the composition of client’s portfolios consistent with our investment team’s judgment concerning market conditions and any particular sector or security. The construction of DoubleLine portfolios may differ substantially from the construction of any of a variety of bond market indices. As such, a DoubleLine portfolio has the potential to underperform or outperform a bond market index. Since markets can remain inefficiently priced for long periods, DoubleLine’s performance is properly assessed over a full multi ‐year market cycle.

Clients are requested to carefully review all portfolio holdings and strategies, including by comparing the custodial statement to any statements received from DoubleLine. Clients should promptly inform DoubleLine of any potential or perceived policy or guideline inconsistencies. In particular, DoubleLine understands that guideline enabling language is subject to interpretation and DoubleLine strongly encourages clients to express any contrasting interpretation as soon as practical. Clients are also requested to notify DoubleLine of any updates to Client’s organization, such as (but not limited to) adding affiliates (including broker

dealer affiliates),

issuing

additional

securities,

name

changes,

mergers

or

other

alterations

to

Client’s

legal

structure.

DoubleLine® is a registered trademark of DoubleLine Capital LP.

© 2011 DoubleLine Ca ital LP

42

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 44/45

8/2/2019 Quantitative Easing vs Federal Reserve PAM Gundlatch and Our Views

http://slidepdf.com/reader/full/quantitative-easing-vs-federal-reserve-pam-gundlatch-and-our-views 45/45